Expected Value of Matrix Quadratic Forms

with Wishart distributed Random Matrices

All data generated or analysed in this article are available in [5]. )

Abstract

To explore the limits of a stochastic gradient method, it may be useful to consider an example consisting of an infinite number of quadratic functions. In this context, it is appropriate to determine the expected value and the covariance matrix of the stochastic noise, i.e. the difference of the true gradient and the approximated gradient generated from a finite sample. When specifying the covariance matrix, the expected value of a quadratic form is needed, where is a Wishart distributed random matrix and is an arbitrary fixed symmetric matrix. After deriving an expression for and considering some special cases, a numerical example is used to show how these results can support the comparison of two stochastic methods.

Key words: Wishart distribution, quadratic form, expected value, second momentum, stochastic gradient method, averaging

1. Outline

The Wishart distribution is a generalization of the distribution. According to [7] and [8] the Wishart distribution plays a prominent role in estimating the covariance matrix in context of multivariate statistics. Therefore, it is not surprising that this important distribution is subject of current research. For instance, [11] considers quadratic forms with non-negative definite matrix and normally distributed random matrix and investigates what are the necessary and sufficient conditions for to be Wishart distributed. Based on this, [10] examines in the special case of with expected value zero under which conditions is central Wishart distributed. Furthermore, in [12] the dispersion matrix of is derived, where is an arbitrary nonrandom matrix.

In this paper we are interested in a different kind of quadratic form: For a Wishart distributed and a symmetric matrix we derive an expression for the expected value of . For this is the second momentum of the Wishart distribution and thus part of the examination of the momenta of the Wishart distribution in [2].

In [9] a different and more general formula for the expected value of was already derived, where with symmetric positive definite matrices and . While the formulation in [9] is mathematically equivalent to the one derived in this paper for the special case considered here, the actual computation of the expected value is quite different - using a linear system based on Kronecker products in [9] and a lower dimensional variant below.

This paper is structured as follows. First, in chapter 3., we motivate in the context of the stochastic gradient method why an expression for the expected value is needed. In the 4. chapter we recall two important, well-known properties of Wishart distributed random matrices. With this preparation, we are then able to present a theorem with a general expression for in the 5. chapter, prove the assertion, and derive more compact expressions under stronger assumptions. Also the connection to the result of [9] is worked out in more detail. Finally, we show in chapter 6. that the approximated value for increasing sample size approaches the theoretical value from the previous chapter, which illustrates the statement of the theorem, and use the theorem to compare the ordinary stochastic gradient method with a variant that uses averaging.

An application of the expected value derived here is the minimization of a random convex quadratic function. While convex quadratic problems in some form are the simplest nontrivial problems, they are complex enough to reproduce local dynamics of more difficult smooth problems. They arise in practical applications in the form of large scale systems of linear equations and least squares problems. Studying the performance of a method on convex quadratic problems is a fundamental preparation to extend the method to more general problems (see [4] and [3]).

2. Notation

In this paper the all-one and the all-zero vectors and matrices are denoted by

and the identity matrix by with dimension . The Hadamard product of two matrices and of the same dimension is defined componentwise as . Let be the Kronecker product of two arbitrary matrices and . A matrix has rank , determinant and trace . If a matrix is positive definite, we write . The vector with the diagonal elements of a quadratic matrix is denoted by and for a vector the expression symbolizes the diagonal matrix with the entries of on its diagonal. The vector is obtained by stacking the columns of on top of one another. The inverse function of vec is . Furthermore, denotes the set of all symmetric, positive definite matrices, i. e.

| (1) |

The expected value and the covariance matrix of a random vector are denoted by and whenever they exist.

3. Motivation

3.1 Stochastic Gradient Method

In order to find the minimum of a function , i. e. the root of , the gradient descent can be used whose iterates are generated with step length starting at a point . If is very large, the calculation of the exact gradient is computationally expensive. To avoid computing the full gradient at each iteration, it can be approximated. Assuming an i. i. d. chosen batch from the uniform distribution of , the expected value of is

This is the motivation for using the approximation instead of , i. e. the stochastic gradient (descent) method (SGD) is given by the iterates

| (2) |

There exist numerous modifications of the stochastic gradient method. The following example can be useful to examine the limits of a SGD method or to compare two variants of SGD.

3.2 Random quadratic functions

As in [6], we assume a fixed matrix with and . At each iteration we draw random vectors and independently from the -variate normal distribution with expected value and covariance matrix . Briefly, this can be written as . With we are able to define the functions

| (3) |

Since has the expected value and the covariance matrix , it holds and the second momentum is given by . Because are quadratic functions of and with expected value

and due to the existence of the fourth momenta of and , for a given the variances of are bounded and almost surely it exists

| (4) |

The stochastic gradient method uses the approximation instead of the full gradient . Therefore it is reasonable to examine the noise defined by

| (5) |

with expected value

Using the independence of and and defining , the covariance matrix of can be written as

| (6) |

This motivates us to determine expected values of the form with random vectors and a symmetric matrix .

4. Introduction

In the context of multivariate statistics, the following definition is of great importance:

Definition 1

For independent and identically distributed (i. i. d.) random vectors with covariance matrix the random matrix is called -variate Wishart distributed with scale matrix and degrees of freedom. We write .

Remark 1

Alternatively can be defined by , where is a random matrix, which columns are independent and identically distributed. This coincides exactly with Definition 1.

The following result is well known:

Lemma 1

The expected value of is

In the proof of the main result, the following important property of Wishart distributed random matrices will also be needed. For the sake of completeness it is proved here.

Lemma 2

Consider with , and . Then

-

Proof.

Since we assume , there exist independent and identically distributed so that . Consider with the expected value and positive definite due to the full rank of , thus . Then we are able to conclude that .

5. Determination of

The following theorem is the main result of this paper:

Theorem 1

For we consider the -variate Wishart distributed random matrix with the symmetric, positive definite scale matrix and degrees of freedom, i. e. . Furthermore, we deal with a fixed matrix . The expected value of the quadratic form is

-

Proof.

Let the matrix be factorized as with diagonal matrix and orthogonal matrix , i. e. . Since , there exist i. i. d. random vectors so that with . We note that Lemma 1 gives us . Now we define the unitary transformations

Since , its components have the momenta , and , and due to Lemma 2 we find

The expected value of is componentwise given by

All in all, we obtain

With as defined above one gets

which corresponds exactly to the assertion.

In practice, the following special cases might be of interest. Additionally to the assumptions of Theorem 1 we demand . Then the result of the theorem simplifies to

| (7) |

If we assume in addition that , we get

| (8) |

Finally, the assumption leads to the special case analyzed in paper [6]. With it follows immediately from Theorem 1:

Corollary 1

The second momentum of a distributed random matrix with scale matrix is given by

Now we are able to present an expression for the covariance matrix of the noise (6) in which the random variables have been eliminated. Since we can define the random matrix and using (7) we conclude

where and satisfy and .

In case of this expression can be simplified to

As mentioned before, an alternative expression for can be derived. If one chooses , , and in Theorem 2.2.9 (ii) from [9], one obtains for

| (9) |

where is the commutation matrix consisting of blocks with entries each. In the ()-th block the only non-zero element is a “1” in position (). It is a permutation matrix that can be used to describe the relationship between the vectorized forms of a square matrix and its transpose, since . Using the calculation rule for Kronecker products we get

where denotes the sum over all entries of a matrix . Thus, we get the same expression as in Theorem 1.

6. Numerical examples

6.1 Illustrative example

For dimension we generate randomly the matrices and with i. i. d. standard normally distributed entries and ensure, that is symmetric and . Let and . The aim is to determine . With the diagonal matrix and the orthogonal matrix from an eigendecomposition and with Theorem 1 we get on the one hand

On the other Hand, the expected value can be approximated with realizations as

| (10) |

because the law of large numbers provides

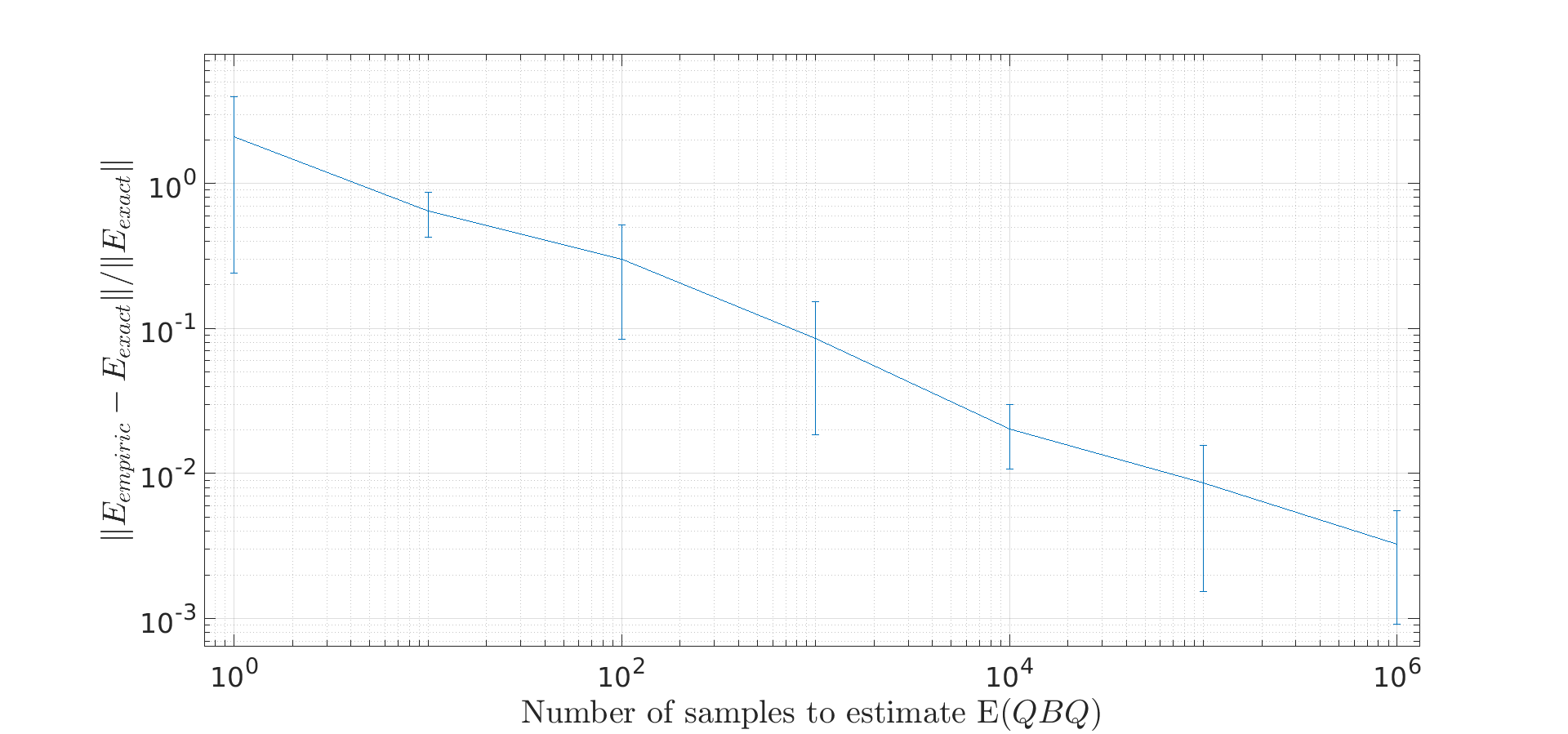

To get an impression of how fast approaches the theoretical value for increasing sample size , we plot the relative error against . Due to the randomness during the generation of and and in the realizations of , ten independent runs are made. At each run the relative error is calculated for . Thus, to be more precise, the logarithmic plot in figure 1 shows the arithmetic means of the relative errors in dependence of .

The standard deviation is represented by error bars:

to the number of samples used for the approximation .

For the mean distance between and is about which leads to a relative error of 2. Using samples this distance reduces to approximately 90 and the relative error to . The curve in the logarithmic plot is roughly linear decreasing. Two interesting observations arise: For large the approximation tends to the result of Theorem 1 and in order to approximate adequately by (10) many samples and a lot of time is needed. Thus, the main result is not only theoretically fascinating but also of practical relevance.

6.2 Comparison of two SGD methods

Our actual goal, as mentioned before, is to compare two algorithms that approximate solutions for the problem with from (4). For dimensions we randomly generate the entries of the matrices and i. i. d. from the distribution and ensure that is positive definite and that is positive semidefinite with norm and condition number .

As initial value we choose the entries randomly from and normalize the vector. Set the number of iterations to and let the step length be given by . Let be the iterates generated by the SGD method (2). A variation of the SGD method described above is the averaged SGD as analyzed in [13]. Starting with the iterates of the ASGD can be defined as

| (11) |

where are the iterates of the ordinary SGD method and . In each iteration we randomly draw and from , calculate , the gradient of defined in (3), the iterates and and the noise from (5). The necessary condition for a minimum of at is that the gradient has to vanish, i. e. . By construction the global optimal solution is . Below the two algorithms are compared by creating graphs of and in dependence of the number of iterations , respectively.

Additionally, we are interested in using our insights about the noise for this comparison. Since is valid independently of , the approximation should tend to . This motivates plotting with respect to the number of samples to estimate .

On the other hand, depends on . At the optimal solution the covariance matrix of the noise is just the scale matrix . We can use this to investigate, how the covariance matrices of the iterates, that can be calculated exactly using Theorem 1, approach to with increasing number of iterations. Thus we plot in dependence of the number of iterations .

This way we obtain the following four graphs:

is compared to the iterates of the ASGD method (red, dashed line).

On the left hand side the norm of the gradient and the distance to the optimal solution are shown with respect to the number of iterations . The ASGD method reaches lower values in both cases. In addition to that statistical fluctuations are much smaller.

At the top on the right hand side there is a plot of the distance of the empiric estimate of the expected value of the noise to the exact expected value in dependence of the number of samples. Both algorithms perform comparably well. Bottom right we have a plot of the distance of the covariance matrix of the noise in the iteration to the covariance matrix at the optimal solution with respect to . Again, the ASGD method performs better in both counts: by reaching lower values and by fluctuating less.

The advantages of the ASGD are not surprising and consistent with the results of [13]. This serves as a simple example of how two algorithms can be compared using Theorem 1.

7. Conclusion

In Theorem 1 it was proven that the expected value of the quadratic form with and can be expressed using , , and an eigendecomposition . Moreover, special cases for certain , and were derived from this general formula, for instance the second momentum of a Wishart distributed random matrix , i. e. . A first example demonstrates the validity of the theorem. Beyond that the result is used to compare two stochastic methods.

Acknowledgment

I would like to express my sincere thanks to Florian Jarre, Holger Schwender and Dietrich von Rosen for their support and valuable comments.

References

- [1]

- Bishop u. a. [2018] \NAT@biblabelnumBishop u. a. 2018 Bishop, Adrian N. ; Del Moral, Pierre ; Niclas, Angèle u. a.: An introduction to Wishart matrix moments. In: Foundations and Trends® in Machine Learning 11 (2018), Nr. 2, S. 97–218

- Goh [2017] \NAT@biblabelnumGoh 2017 Goh, Gabriel: Why Momentum Really Works. In: Distill (2017). http://dx.doi.org/10.23915/distill.00006. – DOI 10.23915/distill.00006

- Gonzaga u. Schneider [2016] \NAT@biblabelnumGonzaga u. Schneider 2016 Gonzaga, Clóvis C ; Schneider, Ruana M.: On the steepest descent algorithm for quadratic functions. In: Computational Optimization and Applications 63 (2016), Nr. 2, S. 523–542

- Hagedorn [2022] \NAT@biblabelnumHagedorn 2022 Hagedorn, Melinda: GitHub repository. In: https://github.com/MHagedorn/wishart (2022)

-

Hagedorn u. Jarre [2022]

\NAT@biblabelnumHagedorn u. Jarre 2022 Hagedorn, Melinda ;

Jarre, Florian:

Optimized convergence of stochastic gradient

descent by weighted averaging. In: Preprint, https://optimization-online.org/2022/09

/optimized-convergence-of-stochastic-gradient-descent-by-weighted-averaging/ (2022) - Härdle u. Hlávka [2015] \NAT@biblabelnumHärdle u. Hlávka 2015 Härdle, Wolfgang K. ; Hlávka, Zdeněk: Multivariate statistics: exercises and solutions. Springer, 2015

- Kanti u. a. [1979] \NAT@biblabelnumKanti u. a. 1979 Kanti, Mardia ; Kent, JT ; Bibby, John: Multivariate analysis. 1979

- Kollo u. Von Rosen [2005] \NAT@biblabelnumKollo u. Von Rosen 2005 Kollo, Tonu ; Von Rosen, Dietrich: Advanced multivariate statistics with matrices. Springer, 2005

- Masaro u. Wong [2003] \NAT@biblabelnumMasaro u. Wong 2003 Masaro, Joe ; Wong, Chi S.: Wishart distributions associated with matrix quadratic forms. In: Journal of multivariate analysis 85 (2003), Nr. 1, S. 1–9

- Mathew u. Nordström [1997] \NAT@biblabelnumMathew u. Nordström 1997 Mathew, Thomas ; Nordström, Kenneth: Wishart and chi-square distributions associated with matrix quadratic forms. In: journal of multivariate analysis 61 (1997), Nr. 1, S. 129–143

- Neudecker [1985] \NAT@biblabelnumNeudecker 1985 Neudecker, H: On the dispersion matrix of a matrix quadratic form connected with the noncentral Wishart distribution. In: Linear algebra and its applications 70 (1985), S. 257–261

- Polyak u. Juditsky [1992] \NAT@biblabelnumPolyak u. Juditsky 1992 Polyak, Boris T. ; Juditsky, Anatoli B.: Acceleration of stochastic approximation by averaging. In: SIAM journal on control and optimization 30 (1992), Nr. 4, S. 838–855