Fully Data-driven Normalized and Exponentiated Kernel Density Estimator

with Hyvärinen Score

Abstract

Recently, Jewson and Rossell, (2022) proposed a new approach for kernel density estimation using an exponentiated form of kernel density estimators. The density estimator contained two hyperparameters that flexibly controls the smoothness of the resulting density. We tune them in a data-driven manner by minimizing an objective function based on the Hyvärinen score to avoid the optimization involving the intractable normalizing constant caused by the exponentiation. We show the asymptotic properties of the proposed estimator and emphasize the importance of including the two hyperparameters for flexible density estimation. Our simulation studies and application to income data show that the proposed density estimator is promising when the underlying density is multi-modal or when observations contain outliers.

Keywords: kernel smoothing, density estimation, bandwidth selection, unnormalized model, Fisher divergence

1 Introduction

Nonparametric density estimation, particularly kernel density estimation (KDE), is routinely used in a variety of fields, including economics (e.g. DiNardo et al.,, 1996). For independent observations, , the KDE at a given value is defined as

| (1) |

where is a kernel function and is the bandwidth parameter. To apply the KDE (1), one needs to specify the kernel function as well as the bandwidth parameter controlling the smoothness of . The selection of is known to be more significantly related to the accuracy of the density estimation than that of kernel function (e.g. Fan and Gijbels,, 1996; Wasserman,, 2006). If is smaller than necessary, the estimated density will be more serrated than required; moreover, if is larger than necessary, the estimated density will be over-smoothed such that it fails to capture the essential features of the true density. Hence, many studies have attempted to develop appropriate selection methods for . Popular techniques include several types of cross validation (CV) (Rudemo,, 1982; Scott and Terrell,, 1987; Hall et al.,, 1992) and plug-in methods (Sheather and Jones,, 1991; Hall et al.,, 1991); these methods have been reviewed in Jones et al., (1996), and Sheather, (2004).

However, the performance of the KDE (1) with the single tuning parameter selected by the existing methods may not be satisfactory in some cases. This may be because the KDE includes only a single tuning parameter to control the smoothness. For example, when observations contain a small number of outliers, the resulting value of tends to be smaller than necessary, leading to serrated estimation results.

Recently, in the framework of general Bayesian inference (Bissiri et al.,, 2016), Jewson and Rossell, (2022) consider the exponential of a weighted log-likelihood for KDE, , as an unnormalized model, where denotes another tuning parameter (learning rate). Consequently, they propose an extended KDE by using the normalized version of the unnormalized density estimation, defined as the power of (1), which is given by:

| (2) |

Parameter can provide additional flexibility to the KDE. In particular, a representative role of is to adjust the smoothness of the KDE, i.e., when is smaller than necessary, can be too small to smooth the density estimator. In other words, acts on the kernel for each observations so provides local smoothness, and acts on the combination of all the kernels so provides global smoothness of the density. To optimize the two parameters , Jewson and Rossell, (2022) employ techniques of fitting feasible unnormalized model with the Fisher divergence (Hyvärinen,, 2005), such that the estimator of can be defined as the minimizer of the Hyvärinen score. In this study, we then theoretically and numerically investigate the new fully data-driven tuning method and the final density estimator. Our main contributions can be summarized as follows:

-

1.

We theoretically characterize asymptotically optimal and in terms of the Fisher divergence (defined in Section 3.2 as and , respectively). In particular, our results show that optimal is not necessarily 1, which suggests the theoretical relevance of using in the context of KDE. In addition, the results of numerical experiments also suggest cases in which is more effective in comparison to other methods.

-

2.

We also demonstrate sharp asymptotic results including consistency of the estimated tuning parameters. Notably, our results do not assume the independence of each term in the Hyvärinen Score, unlike previous study (Jewson and Rossell,, 2022). The assumption of independence is not valid because KDE refers to all observations. To the best of our knowledge, this is the first time that such statements have been proven without assuming independence.

In a closely related study, Jewson and Rossell, (2022) also conduct a theoretical analysis of their method within a general framework. However, it differs from our work in several respects. First, their work is limited to Gaussian kernels, whereas we analyze general symmetric kernels. In addition, as we shall point out later, their theoretical work assumes that the generalized likelihood is an additive form of each observation; however, this assumption does not hold true for KDE. Our theoretical study does not rely on this assumption. Finally, and most importantly, we provide theoretical characterizations of the parameters and give an empirical explanation of their roles. We believe that this study goes beyond the case of KDE and serves as the first step in guaranteeing the validity of Jewson and Rossell, (2022)’s methodology for many subjects that were not fully addressed by Jewson and Rossell, (2022), and in revealing its unknown properties.

The remainder of this paper is organized as follows. In Section 2, we describe the background of the method and propose the estimator of the two tuning parameters in the unnormalized KDE (2) with the Hyvärinen score. Section 3 presents the primary theoretical results. We use the proposed method in Section 4 to present the numerical results and comparisons, and conclude the paper in Section 5. The supplementary material contains additional technical results and proofs.

2 Methodology

2.1 Settings and Fisher divergence

Let be a data domain. Suppose that we are given independent and identically distributed samples defined on with an unknown distribution and density function . Then, is said to be an -th order kernel, for positive integer if

see Wasserman, (2006, pp.55) or Tsybakov, (2009, pp.3) for typical second-order kernels and Wand and Jones, (1995, pp.32-35) for higher-order kernels.

Under the model (2), the joint (unnormalized) density for the observed sample is given by

| (3) |

where and are the same as (1) and (2), respectively, but the dependence on the entire sample is addressed in these notations. The proper likelihood of can be obtained by appropriately normalizing the joint density (3). However, as noted in Jewson and Rossell, (2022), is bounded below by a positive constant as

such that the joint model (3) has an infinite normalizing constant. Models with diverging normalizing constants cannot be interpreted directly in terms of probability; however, the model can be interpreted as describing relative probabilities (Jewson and Rossell,, 2022).

As an alternative construction of the joint probability model for , we consider the leave-one-out (LOO) form

and define an alternative joint model as follows:

| (4) |

Although the normalizing constant of the joint model (4) may not diverge unlike that in (3), it requires -dimensional intractable integration.

Jewson and Rossell, (2022) considered the joint model of as a generalized statistical model with diverging normalizing constant and employed the Hyvärinen score (hereafter referred to as the “H-score") to the joint model to obtain a proper objective function for . Note that the parameter estimation using the H-score is called as score matching (Hyvärinen,, 2005), and the H-score is an empirical version of the Fisher divergence between the joint model and true density , which is defined as

| (5) |

where denotes the -dimensional gradient vector (see Hyvärinen,, 2005, pp.697). This divergence is suitable for the inference of unnormalized models because the gradient of the logarithm does not depend on the normalizing constants.

Although is normalizable, it involves an unrealistic -dimensional integral, as mentioned earlier. Jewson and Rossell, (2022) considered the Fisher-divergence for non-normalizable models, but Hyvärinen, (2005) is designed for cases where the normalizing constants are difficult to compute and is suitable for coping with our problem.

Remark 1.

In the following section, we consider two types of Fisher divergences. The first version is the Fisher-divergence between the joint unnormalized model or , which are defined as (3) or (4), respectively, and true density . We denote them as and , respectively. This type of Fisher-divergence was first introduced by Jewson and Rossell, (2022). In their concept, the exponential of a loss function is considered as an unnormalized probability model. In the context of bandwidth selection for KDE, the feasible loss function based on the negative log-likelihood is given by or and then the resulting unnormalized model is or .

The second version represents the Fisher divergence between the estimator for future observations and true density (denoted as ). Because the estimator to be used is , the tuning parameter should be selected such that is minimized. In Section 3.3, we confirm the asymptotic equivalence between the H-score based on or and Fisher divergence .

From a frequentist standpoint, it is standard to start from and make its empirical counterpart with leave-one-out technique (LHS defined later); however in the generalized Bayesian method, it is standard to consider . Although we consider as a starting point for constructing the H-score, which is applicable to both frequentistic and generalized Bayesian methods, the theorems we present bellow are equally valid, even if we start from .

2.2 Estimation of parameters in the exponentiated KDE

We introduce two objective functions to estimate using the H-scores of the in-sample joint density (3) (denoted by IHS) and the LOO-based joint density (4) (denoted by LHS). Note that IHS has already been adopted in Jewson and Rossell, (2022); however, LHS is an alternative that follows the standard approach to model evaluation in the context of kernel smoothing. As discussed latter (Remark 3), IHS and LHS are asymptotically equivalent. From the Fisher divergence , the -th component of IHS is given by:

| (6) |

where , and . Similarly, LHS is derived from the unnormalized model , given by:

Now, we have the objective functions:

| (7) | |||

| (8) |

We then estimate and as follows:

| (9) |

or setting to be some constant (e.g., ),

| (10) |

Because the objective functions in (9) and (10) are smooth functions of and , the optimization problems can be solved easily using iteration algorithms.

Given the values of , the unnormalized density estimator can be obtained from (2). Thus, the normalized version is given by:

such that .

Remark 2.

As we mentioned previously, Jewson and Rossell, (2022) also consider a similar estimator for the density estimation problem. However, unlike our study, they restrict the problem to the Gaussian kernel case only. Furthermore, although they treated (6) as an independent term and performed theoretical analysis, their argument was not rigorous in this sense, evident from the form of the H-score during KDE, which depends on all observations. Therefore, contrary to their claims, their theoretical considerations would not provide any guarantee that (7) and (8) converge to the Fisher divergence.

3 Theoretical Results

Here, we present the asymptotic properties of the proposed exponentiated KDE. In particular, we derive the following four properties under suitable regularity conditions, as stated later:

-

1.

Decomposition of the expected Fisher divergence into two terms (bias and variance terms), given in Section 3.1.

-

2.

Characterization of the theoretically optimal and , given in Section 3.2.

-

3.

Consistency of the parameters estimated by the Hyvärinen score, given in Section 3.3.

-

4.

Properties of the expected Fisher divergence and Hyvärinen score when is fixed, given in Section 3.4.

First, we state the regularity conditions to establish the theoretical properties.

Assumption (D) (Data Generating Process).

-

D(a):

are random samples with an absolutely continuous distribution with Lebesgue density .

-

D(b):

is an interior point in the support of .

-

D(c):

In a neighborhood of , is -times continuously differentiable and its first -derivatives are bounded.

-

D(d):

The following conditions hold:

-

D(e):

For the density function , there are no constant (independent of ) such that the following equality holds: .

Assumption (K) (Class of kernel functions).

-

K(a):

Kernel function is bounded, even function, of order , and twice continuously differentiable almost everywhere on the support of .

-

K(b):

and

-

K(c):

, , and are Hölder continuous.

In the following, we assume that the bandwidth and the learning rate depend on the sample size , denoted by and respectively. In addition, following the standard asymptotic framework in the literature on kernel smoothing, we assume that the sequence tends toward as (for example Wand and Jones, 1995, pp.20, Wasserman, 2006, pp.73 or Tsybakov, 2009, pp.3). As an analogy of this assumption on the bandwidth, we impose the assumption on the learning rate. In addition, we perform the theoretical analysis without this assumption for in Section 3.4.

Assumption (M) (Asymptotic framework).

-

M(a):

The parameter space of the bandwidth is defined as and limited as for arbitrarily small and some constant .

-

M(b):

The parameter space of the learning rate is defined as and limited as for arbitrarily small and and some constant .

Assumption D(b) excludes the theoretical analysis at the boundary of the support of . It is well known that simple kernel-based estimators, such as KDE and Nadaraya-Watson estimator suffer from a bias at the boundary of the support of the observations without an ingenuity (Fan and Gijbels,, 1996) (see Cattaneo et al., (2020) and references therein for details and the recent progress on this problem in density estimation). We use Assumption D(c) for the expansions in Lemma S1-S10. We need Assumption D(d) to show the equivalency of the expected Hyvärinen score to the expected Fisher divergence, as shown in Theorem 3 using integration by parts. Our operation can be understood as the inverse of the transformation of Fisher divergence into an empirically estimable form proposed by Hyvärinen, (2005). Assumption D(e) is a high-level condition that guarantees the existence of a theoretically optimal bandwidth defined as Corollary 2. Even if this assumption does not hold true, we can derive theoretically optimal bandwidth that differs from Corollary 2; see Remark 6 for further details.

Assumption K(a) is a standard one in the context of KDE. We use Assumption K(b) for the integration by parts in the proof of lemmas. This assumption is not restrictive and the Gaussian Kernel and many other kernels satisfy this condition. Finally, Assumption K(c) is required for Theorem 4. Assumption K(c) is not essential because that Theorem 4 could be proved without it if one adopt the other strategies for the proof.

Under Assumption M(a) or both M(a) and M(b), the Fisher-divergence and Hyvärinen Score are expanded. Note that Assumption (M) limits the parameter space of the bandwidth sequence such that and as holds true, and that of the learning rate such that as and hold true.

Remark 3.

Jewson and Rossell, (2022) constructed the H-score without the LOO technique. According to Jewson and Rossell, (2022)’s and our numerical studies, it is evident that estimator with parameters selected based on such HyvÀrinen score does not overfit (overfitting indicates that the estimated bandwidth is significantly close to ).

This is theoretically explained below. The definition of the Fisher-divergence contains the ratio of the first-order density derivative estimator to density estimator . The order of the variance of is , which dominates that of (See Jones,, 1994). However, when deriving the H-score, the term with the order, which occurs because of not performing LOO and can cause overfitting, is eliminated by the derivative at the evaluation point . It can be observed that and do not appear in the numerator of (6). To rephrase, a part of the density derivative is substantially estimated in the LOO manner. Although the term remains without performing LOO, its influence is asymptotically negligible, because the density derivative estimator, whose variance rate is , is dominant as explained. Therefore, parameter selection based on the IHS (6) does not result in overfitting. In addition, our theoretical results are asymptotically invariant irrespective of H-score being constructed in LOO manner.

3.1 Decomposition of expected Fisher divergence

We first consider the decomposition of the expected Fisher divergence into two terms. These terms can be regarded as bias and variance like terms, similar to the decomposition of Mean Integrated Squared Erorr (MISE) in the standard nonparametric estimation. The results are presented in the following proposition.

Proposition 1 (Decomposition of the expected Fisher divergence).

For a given density estimator for density , possibly different from and , it holds that

provided that and exist, where is the expectation operator over the whole observation . The definitions of and are given below.

Proof.

See Section S5.1 in Supplementary Material. ∎

This decomposition provides us clear insights into the expected Fisher divergence. Specifically, we understand that the expected Fisher divergence is the weighted MISE of the estimator of and balances its squared bias and the variance.

3.2 Characterization of theoretically optimal parameters

Here, we provide the asymptotic results for characterizing theoretically optimal and . Accordingly, we provide a fundamental result showing the asymptotic representation of the expected Fisher divergence as follows:

Theorem 1 (Asymptotic representation of the expected Fisher divergence).

Among the leading terms of the expected Fisher-divergence, the first three terms represent the asymptotic bias of the score function of KDE and the last term represent the asymptotic variance of it. So, asymptotically, the minimization of the Fisher-divergence can be interpreted as selecting the that balances these bias and variance terms.

Remark 4.

When the support of the underlying density is non-compact, moment does not exist. It is well known that a similar phenomenon occurs in the least-squares CV method for regression estimators such as the Nadaraya-Watson estimator, where the inverse of density emerges in the variance term; thus, trimming significantly improves the accuracy (see Racine and Li,, 2004; Hall et al.,, 2007). Because the data must lie within a finite range, trimming procedures will not be necessary in our case. Although the DGPs in our numerical studies have non-compact support, the selected bandwidths and learning rates do not behave in a problematic manner.

Based on Theorem 1, we define the asymptotically optimal bandwidth and the asymptotically optimal learning rate .

Definition 1 (Asymptotically Optimal Parameters).

Asymptotically optimal parameters are defined as the minimizer of the leading terms of the expected Fisher divergence.

Remark 5.

In Definition 1, the parameter space is limited to . This implies that the asymptotically optimal bandwidth is optimal in bandwidths that satisfy the conditions and . This kind of definition is standard in the literature on kernel smoothing. For example, the MISE optimal bandwidth is defined in the same manner, i.e., its leading terms are minimized under ; see Wand and Jones, (1995, equation 2.13), Wasserman, (2006, equation 6.30), and Tsybakov, (2009, pp.15).

The optimal learning rate is explicitly given by the following corollary:

Corollary 1 (Theoretically optimal ).

Under the same assumptions as those in Theorem 1 and Assumption D(e), theoretically optimal can be given by:

The defintion of is given below. In particular, the optimal is larger than 1 if .

Proof.

The first claim follows immediately from Theorem 1 and the first-order condition for minimization. Note that integration by parts yields

Hence, when , . Because and are always strictly positive, is always negative when . This proves the second claim. ∎

Although we show that only when , this will be adequate for the following reasons; is the most common case, is unsuitable for the proposed method because a higher-order kernel makes negative at some points and thus, does not take any value in .

We can also characterize the theoretically optimal and as -dependent sequences. The following two corollaries state that converges to at the rate of and converges to at the rate of .

Corollary 2 (Theoretically optimal bandwidth).

Proof.

See Section S4.2 of Supplementary Materials. ∎

Remark 6.

For to exist, must be strictly positive. The non-negativity is proven in Section S4.2 by the Cauchy-Schwarz inequality. Also, the equality does not hold true for many densities. For example, has the form of Corollary 2 for all DGPs in our numerical studies. In addition, even when the equality is valid, higher-order expansion of the expected Fisher-divergence yields a theoretically optimal bandwidth. This expansion can be obtained by using Assumption M(b) and rearranging Theorem 5 with respect to .

By inserting the explicit form of in Proposition 2 into in Proposition 1, we can characterize the optimal as -dependent sequence. Specifically, the following corollary explicitly states that converges to at the rate of .

Corollary 3 (Theoretically optimal as -dependent sequence).

Finally, the following theorem guarantees, at least asymptotically, that the Fisher divergence is convex and the vector of such theoretically optimal parameters satisfies the second-order condition for minimization; that is, we can select the parameters empirically if the sample size is large.

Theorem 2.

Under the same assumptions as those in Theorem 1, the expected Fisher divergence is asymptotically a convex function with respect to ; and thus, satisfies the sufficient condition for minimizing of the expected Fisher divergence.

Proof.

See Section S4.3 of Supplementary Material. ∎

Remark 7.

In the Supplementary Material, we derive the asymptotic expansion of MISE as Theorem S1: , where and are some constants. In view of this expansion and Corollary 2 and 3, the proposed KDE with Fisher-divergence optimal parameters, , does not achieve the optimal convergence rate (for example, for twice continuously differentiable densities).

3.3 Consistency

In this section, we provide propositions for the consistency of with . Accordingly, we first provide an asymptotic representation of the expected H-score.

Theorem 3.

The above theorem gives asymptotic equivalency of the expected Hyvärinen score to expected Fisher divergence and thus their minimizers.

Corollary 4.

Under the same assumptions as those in Theorem 3, the minimizer of the expected H-score (both IHS and LHS) and that of the expected Fisher divergence is equivalent.

Proof.

This can be immediately deduced from Theorem 3. ∎

The following theorem states that the components that depend on and in the stochastic process converges (at the rate required for consistency of tuning parameters) to 0 uniformly in and on the given parameter space.

Theorem 4.

Under Assumptions D(a) - D(c), (K) and (M), the process is given by:

where is defined as:

and does not depend on or . is the expectation operator over -th observation. Additionally, is a stochastic process which satisfies

In addition, this statement holds true for the case of LHS.

Proof.

See Section S4.5 of Supplementary Material for an outline of the proof. ∎

Corollary 4 states that the minimizer of the expected Fisher-divergence and the expected H-score is equivalent, and Theorem 4 guarantees that we can get the minimizer of the expected H-score by minimizing the empirical H-score. Consequently, Theorem 4 and Corollary 4 imply the consistency of with in probability.

Corollary 5.

Under the same assumptions as those in Theorem 4, we obtain

Proof.

See Section S4.6 in Supplementary Material for the proof. ∎

Note that we need the rescaling factors and in the denominators because these parameters converge to as . Therefore, we must consider this property to guarantee the consistency of the parameters.

3.4 Properties under fixed

In this section, we provide the asymptotic representation of the expected Fisher divergence and expected H-score with fixed . It should be noted that does not depend on ; therefore, we drop the subscript in this section. First, for the higher-order expansion of the expected Fisher divergence and the expected H-score, we strengthen the assumptions on the data generating process.

Assumption (D’) (Data generating process).

-

D’(a):

In a neighborhood of , is -times continuously differentiable and its first -derivatives are bounded.

-

D’(b):

For any integer , the following holds true:

Note that we need, among Assumption (M), only Assumption M(a) and not M(b) for the following two theorems. The main result is the following theorem.

Theorem 5.

If is fixed as , does not converge to as because .

Furthermore, we can establish asymptotic equivalency of the expected Hyvärinen score to the expected Fisher divergence when is fixed.

Theorem 6.

Even when is fixed, the expected H-score is asymptotically equivalent to the expected Fisher divergence. Combined with Theorem 5, we can see that the Hyvärinen Score selects the bandwidth that minimizes an unreasonable criterion when is fixed to some value that is not , so one should learn and simultaneously as long as consistency is one’s concern.

4 Numerical Examples

4.1 Simulation studies

We compare the numerical performance of the proposed exponentiated KDE with the standard KDE methods through simulation studies. Following the work by Marron and Wand, (1992); Jewson and Rossell, (2022), we generated the synthetic data from the following Gaussian mixtures: , where and are the mean and variance of the normal distribution, respectively, and is the mixing proportions that satisfies . Specifically, we considered the following five scenarios:

-

1.

Bimodal: and, .

-

2.

Trimodal: , and

-

3.

Claw: , and then for .

-

4.

Skewed: , and for .

-

5.

Outlier: , and .

For the simulated dataset, we applied the exponentiated KDE with and estimated using the LOO H-score (LHS) and in-sample H-score (IHS). We also applied the standard KDE using the bandwidth selected by the following two methods:

-

-

Unbiased cross-validation (CV): Bandwidth is determined by minimizing Note that is an unbiased estimator of MISE.

-

-

MISE optimal plug-in (PI): Bandwidth is set to the asymptotic mean integrated squared error (AMISE) optimal bandwidth given by:

where and . For , we adopt the following estimator given in Hall and Marron, 1987a : where the kernel function and bandwidth may be different from and , respectively.

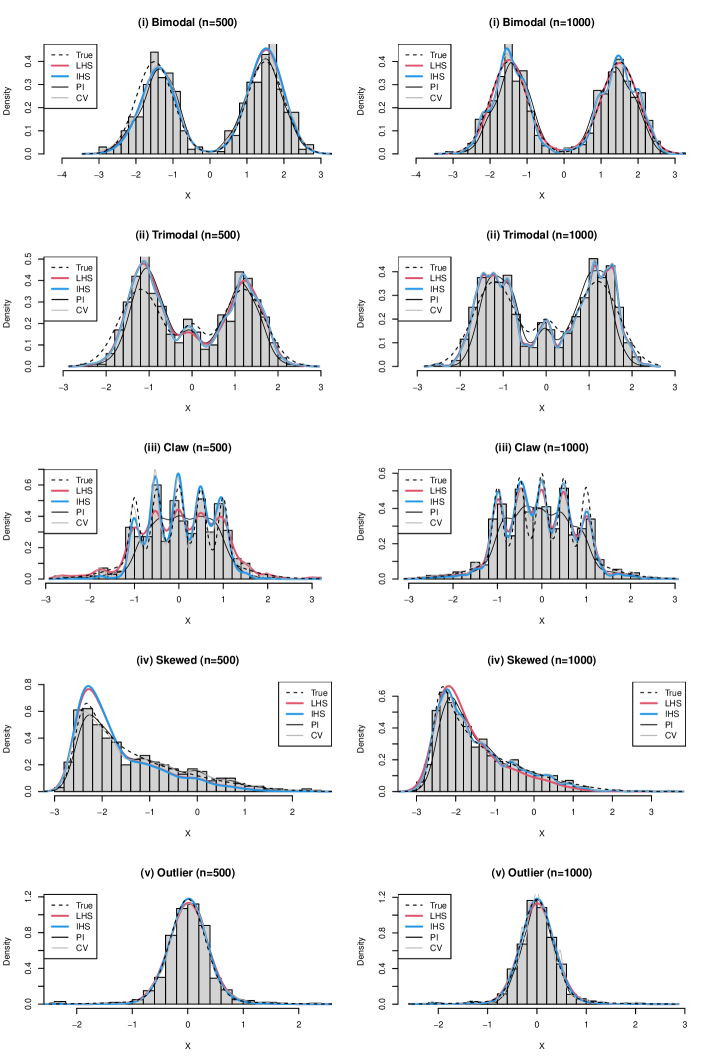

Throughout the experiment, we adopted a Gaussian kernel for all the methods. Furthermore, we set the minimum values of for LHS and IHS to to avoid numerical instability. Under the same five scenarios of the true density forms, we generated and samples and estimated the density functions based on the generated data. In Figure 1, we first present the density functions estimated using the IHS, LHS, CV, and PI methods with the true density under a single simulated dataset.

To quantitatively compare the performances of the four density estimations, we computed the integrated squared error (ISE) and Kullback-Leibler divergence (KL), defined as follows: Furthermore, to measure the estimation accuracy of the smoothness of the true density, we also computed the ISE of the curvature, defined as: Note that the above values were approximated by a set of grid points, , in our study. Based on 1000 Monte Carlo replications, we computed 1000 values of ISEf, KL, and ISEC, and we obtained , , and quantiles of 1000 replications. The results of ISEf are summarized in Table 1. It is reasonable that PI exhibits the best performance in most scenarios since the bandwidth of PI is selected to minimize AMISE. However, it is interesting that the proposed HS methods provide better results in some scenarios. Since IHS and LHS are not ISE-oriented objective functions, we suspect that this improvement in ISE is caused by the introduction of . To examine these conjectures, we theoretically derive the asymptotic MISE of and MISE optimal parameters in Sections S2.1 and S2.2 of Supplementary Material. Based on the theoretical results, we compare the asymptotic MISE of and , and provide an additional discussion on the numerical results of ISE in Section S2.3. Further, the results of KL and ISEC are presented in Table 2 and Table 3, respectively. It is observed that the results of KL are similar to those of MISE in Table 1. Regarding the estimation accuracy of the curvature, we can see that either IHS or LHS attains the minimum values among the four methods, showing a benefit of introducing an additional smoothness parameter . The performance differences can be observed between IHS and LHS in the finite sample, but the differences are smaller when compared to the case since these two methods are asymptotically equivalent.

| Scenario | Quantiles | LHS | IHS | CV | PI | LHS | IHS | CV | PI | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.16 | 0.16 | 0.30 | 0.26 | 0.07 | 0.07 | 0.17 | 0.15 | ||||

| (i) Bimodal | 0.28 | 0.29 | 0.43 | 0.37 | 0.13 | 0.13 | 0.24 | 0.21 | |||

| 0.49 | 0.51 | 0.66 | 0.50 | 0.23 | 0.24 | 0.35 | 0.28 | ||||

| 0.87 | 1.17 | 0.62 | 0.60 | 0.94 | 1.10 | 0.66 | 0.65 | ||||

| (ii) Trimodal | 1.24 | 1.53 | 0.89 | 0.86 | 1.17 | 1.36 | 0.85 | 0.83 | |||

| 1.62 | 1.95 | 1.26 | 1.21 | 1.45 | 1.64 | 1.06 | 1.04 | ||||

| 1.70 | 1.28 | 5.41 | 0.94 | 1.15 | 0.80 | 4.42 | 0.55 | ||||

| (iii) Claw | 2.27 | 1.64 | 5.66 | 1.17 | 1.45 | 1.03 | 4.70 | 0.69 | |||

| 3.20 | 2.11 | 6.02 | 1.44 | 1.88 | 1.33 | 4.98 | 0.84 | ||||

| 0.80 | 0.84 | 0.72 | 0.39 | 0.62 | 0.59 | 0.41 | 0.23 | ||||

| (iv) Skewed | 1.18 | 1.23 | 1.10 | 0.54 | 0.94 | 0.90 | 0.64 | 0.30 | |||

| 1.61 | 1.74 | 1.82 | 0.71 | 1.30 | 1.32 | 1.06 | 0.41 | ||||

| 0.27 | 0.18 | 0.38 | 0.35 | 0.16 | 0.12 | 0.22 | 0.21 | ||||

| (v) Outlier | 0.48 | 0.32 | 0.57 | 0.59 | 0.27 | 0.19 | 0.33 | 0.33 | |||

| 0.82 | 0.63 | 0.87 | 0.91 | 0.43 | 0.33 | 0.48 | 0.49 | ||||

| Scenario | Quantiles | LHS | IHS | CV | PI | LHS | IHS | CV | PI | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.52 | 0.53 | 1.61 | 0.97 | 0.26 | 0.26 | 0.82 | 0.58 | ||||

| (i) Bimodal | 0.81 | 0.83 | 2.99 | 1.29 | 0.39 | 0.39 | 1.89 | 0.75 | |||

| 1.31 | 1.34 | 5.80 | 1.65 | 0.61 | 0.62 | 3.92 | 0.96 | ||||

| 3.31 | 4.34 | 5.99 | 2.39 | 3.51 | 4.19 | 5.23 | 2.62 | ||||

| (ii) Trimodal | 4.38 | 5.55 | 8.73 | 3.26 | 4.30 | 4.98 | 7.20 | 3.22 | |||

| 5.67 | 6.96 | 13.42 | 4.39 | 5.26 | 6.01 | 10.06 | 3.93 | ||||

| 3.54 | 4.78 | 25.53 | 2.96 | 3.00 | 3.68 | 19.22 | 1.93 | ||||

| (iii) Claw | 4.72 | 6.44 | 27.89 | 4.00 | 3.78 | 5.17 | 20.82 | 2.68 | |||

| 7.08 | 8.65 | 30.52 | 7.32 | 4.78 | 6.61 | 22.57 | 4.46 | ||||

| 2.85 | 3.12 | 3.94 | 1.39 | 2.26 | 2.08 | 2.68 | 0.84 | ||||

| (iv) Skewed | 4.11 | 4.33 | 5.98 | 1.73 | 3.25 | 3.08 | 3.91 | 1.03 | |||

| 5.64 | 5.96 | 9.29 | 2.19 | 4.39 | 4.25 | 6.08 | 1.29 | ||||

| 1.39 | 1.34 | 0.66 | 1.24 | 1.11 | 0.98 | 0.48 | 0.82 | ||||

| (v) Outlier | 2.12 | 1.90 | 1.50 | 1.76 | 1.69 | 1.36 | 1.03 | 1.11 | |||

| 3.11 | 2.85 | 4.27 | 3.12 | 2.34 | 1.94 | 2.65 | 2.07 | ||||

| Scenario | Quantiles | LHS | IHS | CV | PI | LHS | IHS | CV | PI | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.09 | 0.09 | 0.34 | 0.38 | 0.05 | 0.04 | 0.25 | 0.27 | ||||

| (i) Bimodal | 0.16 | 0.17 | 0.47 | 0.55 | 0.08 | 0.08 | 0.35 | 0.40 | |||

| 0.30 | 0.32 | 0.67 | 0.89 | 0.14 | 0.14 | 0.47 | 0.64 | ||||

| 1.25 | 1.56 | 0.81 | 1.01 | 1.33 | 1.59 | 0.99 | 1.18 | ||||

| (ii) Trimodal | 1.80 | 2.24 | 1.19 | 1.64 | 1.78 | 2.09 | 1.29 | 1.64 | |||

| 2.63 | 3.58 | 1.79 | 2.80 | 2.33 | 2.81 | 1.67 | 2.30 | ||||

| 2.00 | 1.13 | 6.52 | 1.49 | 1.14 | 0.66 | 5.65 | 1.10 | ||||

| (iii) Claw | 2.95 | 1.61 | 6.65 | 1.90 | 1.75 | 0.91 | 5.93 | 1.37 | |||

| 4.22 | 2.45 | 6.75 | 2.47 | 2.57 | 1.28 | 6.14 | 1.70 | ||||

| 0.14 | 0.14 | 0.21 | 0.15 | 0.10 | 0.10 | 0.14 | 0.11 | ||||

| (iv) Skewed | 0.20 | 0.21 | 0.28 | 0.21 | 0.15 | 0.15 | 0.19 | 0.15 | |||

| 0.28 | 0.30 | 0.40 | 0.29 | 0.20 | 0.20 | 0.27 | 0.21 | ||||

| 0.07 | 0.04 | 0.20 | 0.17 | 0.04 | 0.03 | 0.15 | 0.12 | ||||

| (v) Outlier | 0.13 | 0.09 | 0.31 | 0.30 | 0.07 | 0.06 | 0.21 | 0.20 | |||

| 0.21 | 0.22 | 0.45 | 0.60 | 0.12 | 0.12 | 0.29 | 0.38 | ||||

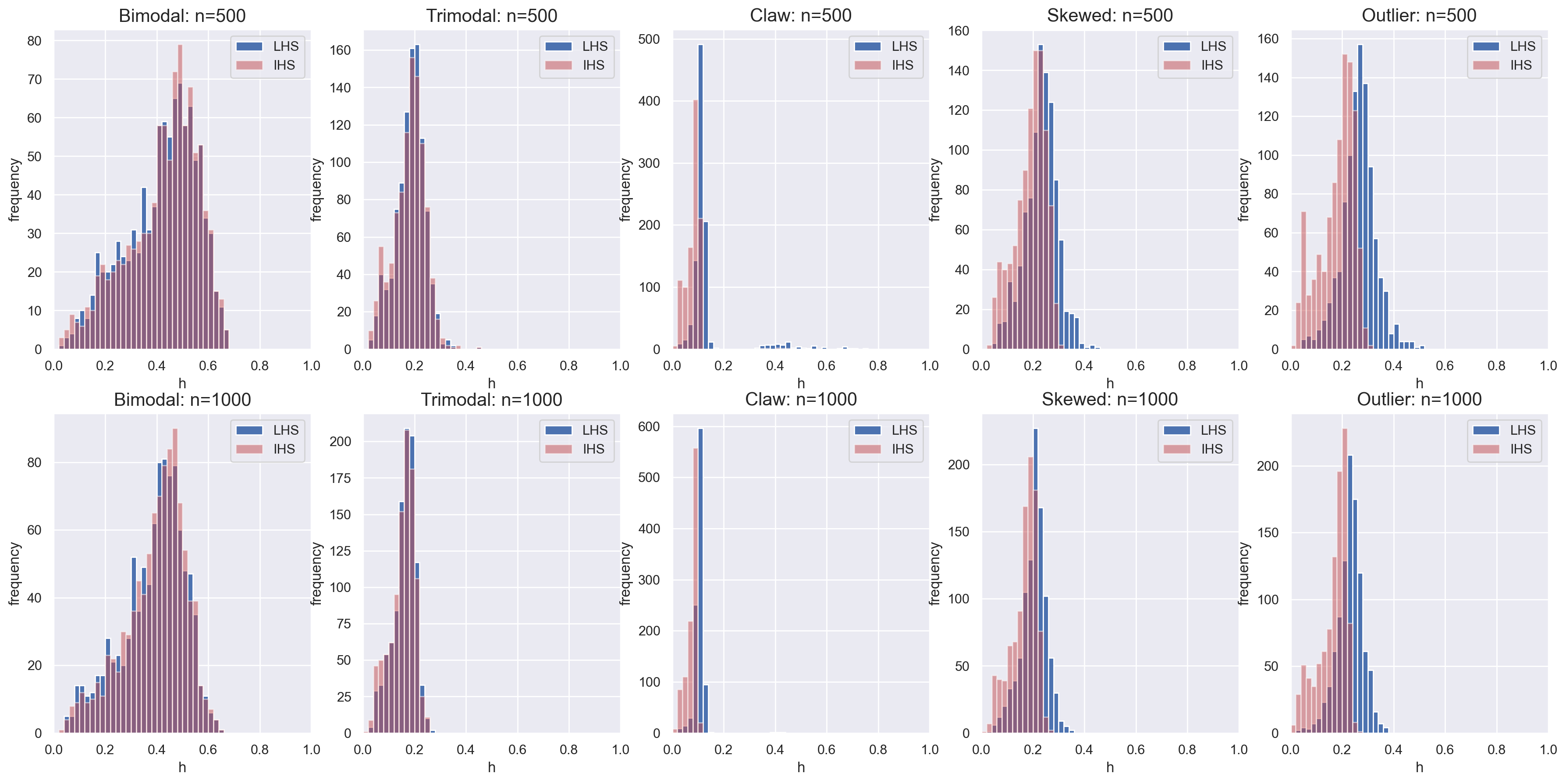

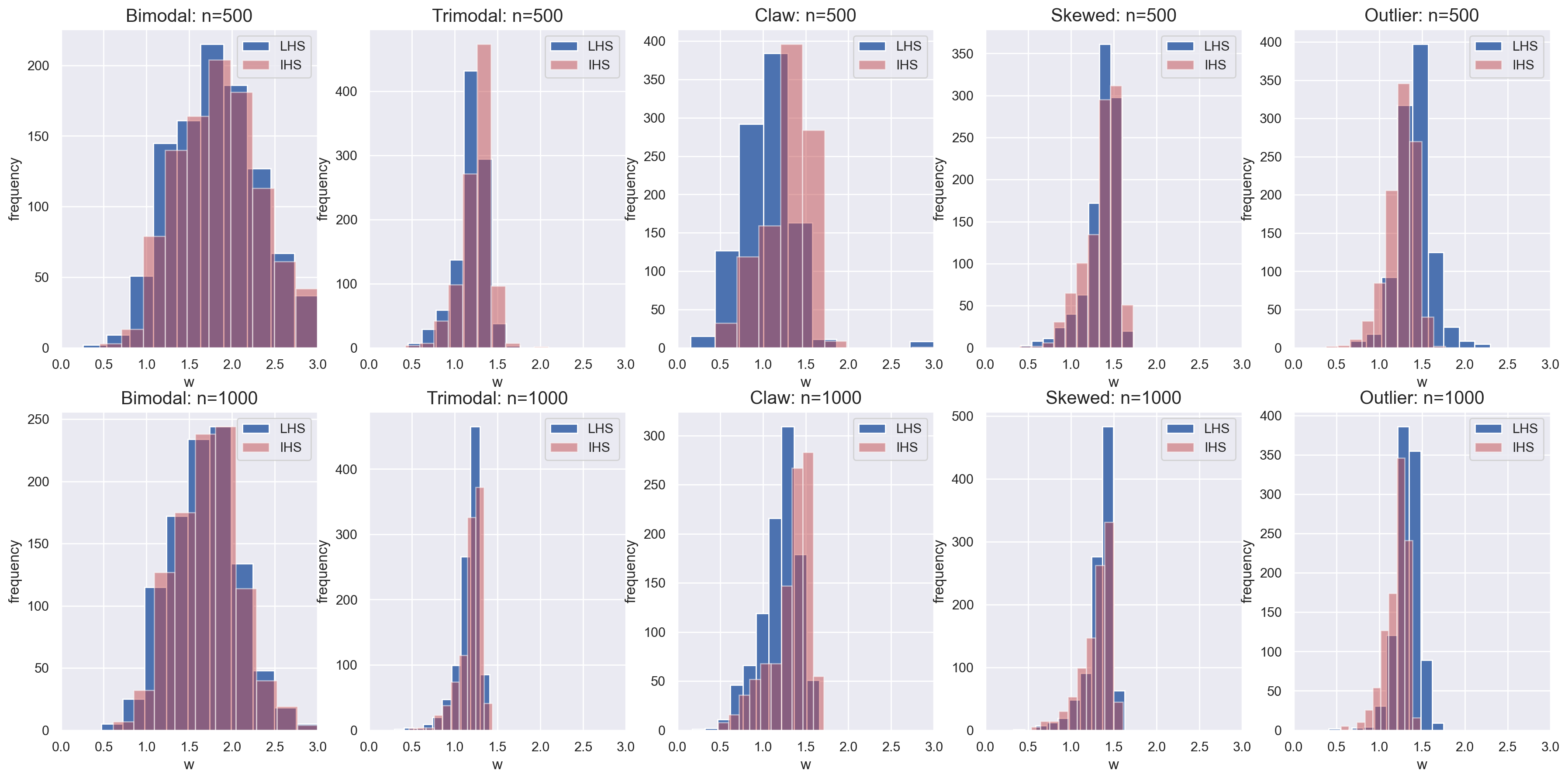

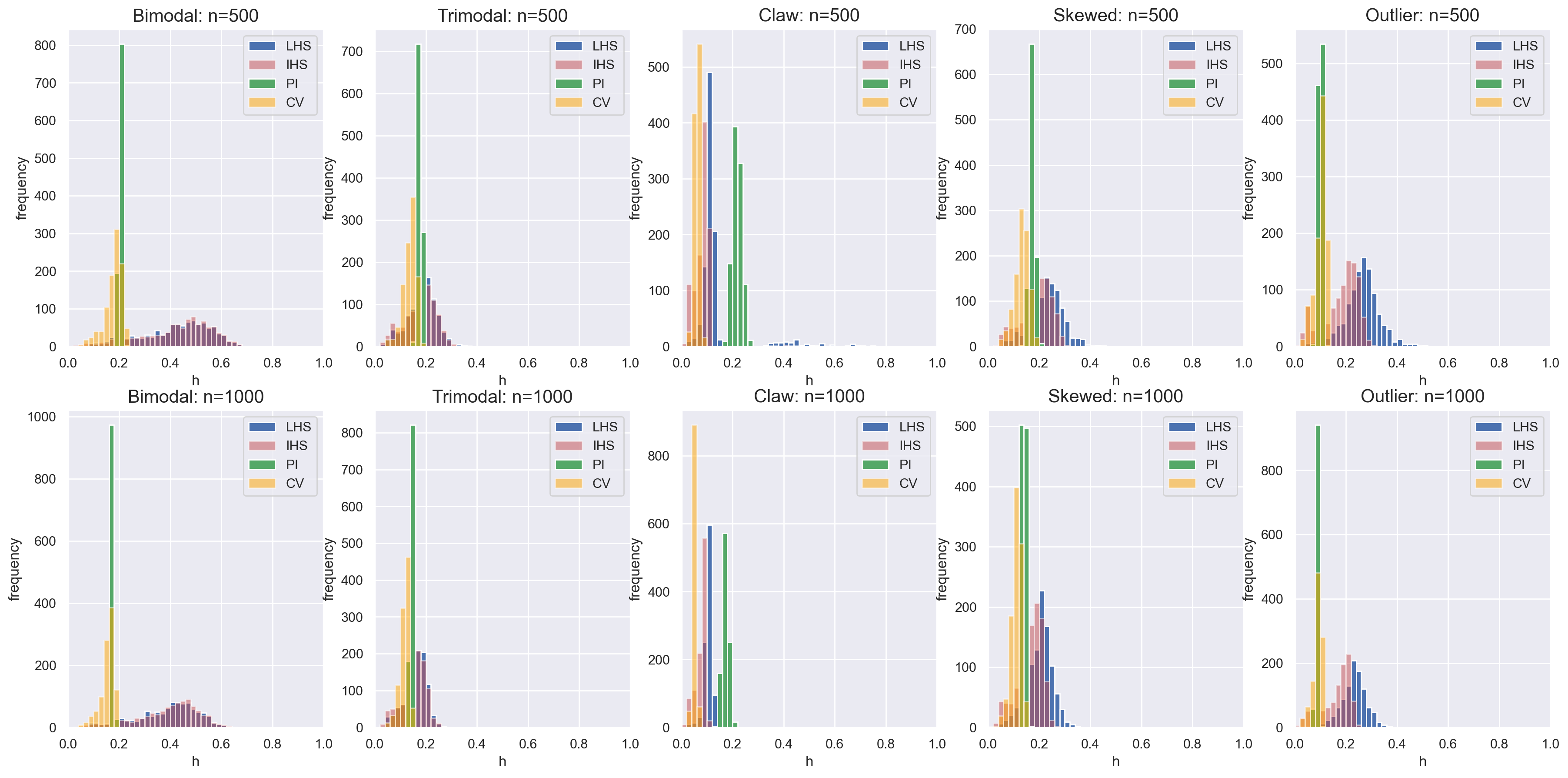

To investigate the roles of the two hyperparameters in the exponentiated KDE (2), we present the two-dimensional histograms of the Monte Carlo replications of the estimated by LHS in Figure 2. First, the variability between Monte Carlo replications under is found to be smaller than that under , which is consistent with the convergence of the H-score. In addition, the optimal is significantly different for the five scenarios, indicating the flexibility of the proposed exponentiated KDE. In scenarios (iii) and (iv), the variability of the estimated is considerably small, and the form of the final density estimate is dictated only by the additional parameter . Furthermore, when a sample contains outliers in scenario (v), the optimal bandwidth in standard KDE tends to be unnecessarily small for capturing local fluctuations near outliers; this difficulty can be addressed by incorporating . Moreover, the histogram of under scenario (v) shows that the optimal value of in scenario (v) is smaller than those in other scenarios, leading to a smoother density estimate. A detailed comparison of optimal values is presented in Section S3 and explained in Section S2.3 of Supplementary Material. According to Figures S1 and S2, LHS and IHS tend to provide similar optimal values for . In addition, Figure S3 shows that the uncertainties of parameters estimated by IHS and LHS are significantly larger than those estimated by PI and CV, whereas the numerical ISE of IHS and LHS is smaller than those of PI and CV in some cases (Table 1) . This suggests the significant benefit of introducing .

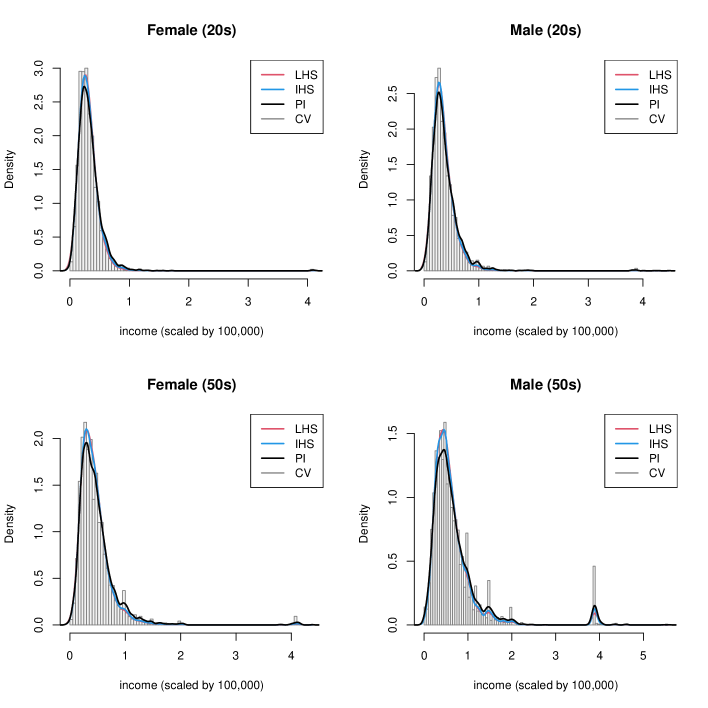

4.2 Real data application

The estimation of income distributions is particularly popular in labor market analysis (see DiNardo et al.,, 1996; Hajargasht et al.,, 2012; Kobayashi et al.,, 2022 for instance).

We apply the proposed methodology to the Current Population Survey (CPS) to estimate income distributions.

The CPS is a monthly survey of approximately households in the United States, carried out by the Bureau of Labor Statistics.

We used a dataset created by B. Hansen, named cps09mar, which used certain variables from the CPS for March 2009.

The dataset and its detailed description can be downloaded from https://www.ssc.wisc.edu/~bhansen/econometrics/.

We applied the proposed method to sub-samples of females and males aged in their 20s or 50s.

The sample sizes of the four sub-samples are 3,426 for females (20s), 4,764 for females (50s), 4,540 for males (20s), and 6,079 for males (50s).

To avoid the same observed values, we added a small noise following , which will be used in the subsequent analysis.

For each sub-sample, we applied the proposed H-score-based KDE along with the standard KDE method used in Section 4.1, where the minimum bandwidth of LHS and IHS is set in the same way as in Section 4.1. The estimated tuning parameters are listed in Table 4, and the estimated densities are presented in Figure 3. The bandwidth selected by PI and CV are similar, leading to almost the same density estimates. On the other hand, the estimated bandwidth in LHS and IHS are larger than those of PI and CV, and the power parameter is larger than . Comparing the resulting density estimates, HS methods can capture the main body of the histogram while PI and CV methods underestimate the density around the mode, which can be attributed to outlying households with significantly high income. Hence, we can conclude that the proposed HS methods can flexibly capture the underlying density without being affected by outlying households owing to the additional flexibility of in the exponentiated KDE (2).

| LHS | IHS | PI | CV | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Female (20s) | ||||||||||

| Female (50s) | ||||||||||

| Male (20s) | ||||||||||

| Male (50s) | ||||||||||

5 Concluding Remarks

In this study, we investigated a new framework for data-driven density estimation with an intractable normalizing constant. We estimated the tuning parameters by minimizing the Hyvärinen score, an empirical version of the Fisher divergence. We then scrutinized the theoretical properties of the proposed estimator, including the asymptotic role of tuning parameters and consistency of the proposed estimator. The main contribution of this study to the literature on kernel-smoothing-based density estimators is the characterization of the additional tuning parameter . Moreover, we interestingly discovered that the theoretically optimal is not , implying that the accuracy of KDE can be improved by allowing .

Nevertheless, some remaining theoretical issues must be addressed. First, although we demonstrated the consistency of selected parameters with the asymptotic Fisher divergence, the uncertainty of has not been fully discussed. Likewise Hall and Marron, 1987b , it would be meaningful to evaluate the closeness between minimizers of the Hyvärinen score and exact Fisher divergence. Second, the extension to multivariate cases, and the investigation of the properties of at the boundary point are valuable. In addition, consideration of conditional densities may lead to the discovery of properties that differ from the mere analogy of those of density estimation. Specifically, Hall et al., (2004, 2007) reported that the unbiased least-squares CV smoothes out irrelevant regressors. We suspect that the procedure of Jewson and Rossell, (2022) does too.

Numerous studies have been conducted on the effect of bandwidth on the performance of kernel-smoothing-based estimators. However, several issues cannot be solved by tuning only a single bandwidth parameter. A notable example is the estimation of contaminated density, as illustrated by the income distribution in Section 4.2, where the additional tuning parameter makes KDE robust against contamination. Hence, the proposed approach could also be useful for other kernel-smoothing methods.

Finally, while two methods (IHS and LHS) are asymptotically equivalent, the finite sample performance is not necessarily similar, as confirmed in our numerical studies. Some theoretical investigation regarding this issue is left to a future study.

Funding

This study was supported by JSPS KAKENHI (grant no. 21H00699 and 23H00805).

References

- Bissiri et al., (2016) Bissiri, P. G., Holmes, C. C., and Walker, S. G. (2016). A general framework for updating belief distributions. Journal of the Royal Statistical Society. Series B, 78(5):1103.

- Cattaneo et al., (2020) Cattaneo, M. D., Jansson, M., and Ma, X. (2020). Simple local polynomial density estimators. Journal of the American Statistical Association, 115(531):1449–1455.

- DiNardo et al., (1996) DiNardo, J., Fortin, N., and Lemieux, T. (1996). Labor market institutions and the distribution of wages, 1973-1992: A semiparametric approach. Econometrica, 64(5):1001–1044.

- Fan and Gijbels, (1996) Fan, J. and Gijbels, I. (1996). Local Polynomial Modelling and Its Applications: Monographs on Statistics and Applied Probability 66, volume 66. CRC Press.

- Hajargasht et al., (2012) Hajargasht, G., Griffiths, W. E., Brice, J., Rao, D. P., and Chotikapanich, D. (2012). Inference for income distributions using grouped data. Journal of Business & Economic Statistics, 30(4):563–575.

- Hall, (1987) Hall, P. (1987). On kullback-leibler loss and density estimation. The Annals of Statistics, 15(4):1491–1519.

- Hall et al., (2007) Hall, P., Li, Q., and Racine, J. S. (2007). Nonparametric estimation of regression functions in the presence of irrelevant regressors. The Review of Economics and Statistics, 89(4):784–789.

- (8) Hall, P. and Marron, J. S. (1987a). Estimation of integrated squared density derivatives. Statistics and Probability Letters, 6(2):109–115.

- (9) Hall, P. and Marron, J. S. (1987b). Extent to which least-square cross-validation minimises integrated squared error in nonparametric density estimation. Probability Theory and Related Fields, 74:567–581.

- Hall et al., (1992) Hall, P., Marron, J. S., and Park, B. (1992). Smoothedcross-validation. Probability Theory and Related Field, 92:1–20.

- Hall et al., (2004) Hall, P., Racine, J., and Li, Q. (2004). Cross-validation and the estimation of conditional probability densities. Journal of the American Statistical Association, 99(468):1015–1026.

- Hall et al., (1991) Hall, P., Sheather, S. J., Jones, M. C., and Marron, J. (1991). On optimal data-based bandwidth selection in kernel density estimation. Biometrika, 78(2):263–270.

- Hyvärinen, (2005) Hyvärinen, A. (2005). Estimation of non-normalized statistical models by score matching. Journal of Machine Learning Research, 6(4).

- Jewson and Rossell, (2022) Jewson, J. and Rossell, D. (2022). General bayesian loss function selection and the use of improper models. Journal of the Royal Statistical Society Series B, 84(5):1640–1665.

- Jones, (1994) Jones, M. (1994). On kernel density derivative estimation. Communications in Statistics-Theory and Methods, 23(8):2133–2139.

- Jones et al., (1996) Jones, M. C., Marron, J. S., and Sheather, S. J. (1996). A brief survey of bandwidth selection for density estimation. Journal of the American statistical association, 91(433):401–407.

- Kobayashi et al., (2022) Kobayashi, G., Yamauchi, Y., Kakamu, K., Kawakubo, Y., and Sugasawa, S. (2022). Bayesian approach to lorenz curve using time series grouped data. Journal of Business & Economic Statistics, 40(2):897–912.

- Marron and Wand, (1992) Marron, J. S. and Wand, M. P. (1992). Exact mean integrated squared error. The Annals of Statistics, 20(2):712–736.

- Racine and Li, (2004) Racine, J. and Li, Q. (2004). Nonparametric estimation of regression functions with both categorical and continuous data. Journal of Econometrics, 119(1):99–130.

- Rudemo, (1982) Rudemo, M. (1982). Empirical choice of histograms and kernel density estimators. Scandinavian Journal of Statistics, 9(2):65–78.

- Scott and Terrell, (1987) Scott, D. W. and Terrell, G. R. (1987). Biased and unbiased cross-validation in density estimation. Journal of the American Statistical Association, 82(400):1131–1146.

- Sheather, (2004) Sheather, S. J. (2004). Density estimation. Statistical science, pages 588–597.

- Sheather and Jones, (1991) Sheather, S. J. and Jones, M. C. (1991). A reliable data-based bandwidth selection method for kernel density estimation. Journal of the Royal Statistical Society: Series B, 53(3):683–690.

- Tsybakov, (2009) Tsybakov, A. (2009). Introduction to Nonparametric Estimation. Springer Science & Business Media.

- Wand and Jones, (1995) Wand, M. P. and Jones, M. (1995). Kernel smoothing. Springer Science & Business Media.

- Wasserman, (2006) Wasserman, L. (2006). All of nonparametric statistics. Springer Science & Business Media.

Supplemental Materials for “Fully Data-driven Normalized and Exponentiated Kernel Density Estimator with Hyvärinen Score"

Appendix S1 Notations

In this section, we provide the list and notes of the notations used in the proof.

-

•

Expectation operator

-

–

: the expectation operator over the whole observation.

-

–

: the expectation operator over only -th observation.

-

–

-

–

-

•

To simplify notation, we write

-

•

Constants associated with the kernel function

-

•

Constants in the leading terms of Expected Fisher-divergence

-

•

: individual Hyvärinen Score for -th observation, which is explicitly defined in Section S6.1.

About the dependence of parameters on : If and depend on , we write them as and respectively to clarify the dependence. When we suppose both the cases where the parameters depend on and the cases where they do not in general, we do not give the subscript .

Appendix S2 Additional Theoretical Results (MISE)

In this section, we investigate the asymptotic MISE (Mean Integrated Squared Error) of .

S2.1 MISE

Theorem S1.

| DGP | ||||

|---|---|---|---|---|

| Bimodal | -0.563 | -1.415 | 0.373 | |

| Trimodal | -0.931 | -1.321 | 0.481 | |

| Claw | -6.929 | -1.193 | 0.107 | |

| Skewed | -1.038 | -1.260 | 0.120 | |

| Outline | -3.677 | -0.487 | -1.641 |

S2.2 MISE Optimal Parameters

We denote the MISE optimal parameters as and . Minimizing the leading terms in Theorem S1 with respect to gives the MISE optimal .

Using this results, we have the MISE optimal parameters as -dependent sequences.

Remark S1.

Since from the Cauchy-Schwarz inequality, by definition, and for the DGPs in our numerical studies. These imply that MISE optimal is larger than for the five DGPs.

Remark S2.

The MISE optimal bandwidth converges to at the rate of , so the estimated bandwidth via H-score leads to oversmoothing for MISE. However, MISE optimal approaches to at the rate of and is faster than that of Fisher-divergence optimal (), so Fisher-divergence optimal in turn leads to undersmoothing for MISE. Combining these results on and , although certainly leads to oversmoothing, compensate the lack of smoothness.

S2.3 Relative asymptotic MISE between with and without

In this section, we consider the benefit from introducing based on the asymptotic MISE. Table S2 and S3 describe the asymptotic bias, asymptotic variance, asymptotic MISE and asymptotic relative MISE of and for each DGP in Section 4. These quantities of are calculated with the MISE optimal bandwidth for the standard KDE (See e.g. Wand and Jones,, 1995, pp.22, Wasserman,, 2006, pp.134, Tsybakov,, 2009, pp.8) and those of are with .

In view of Table S2 and S3, consistently with the intuition, the asymptotic bias is reduced by introducing . Because of this asymptotic bias reduction and the fact that has no influence on the asymptotic variance as shown in Theorem S1, the bandwidth is larger than that without , so the asymptotic variance is also smaller. As a result, the allowing improves the asymptotic MISE for all DGPs.

S2.3.1 Additional Discussion on the Simulation Results

Based on Table S2 and S3, we provide additional explanation on the numerical studies. We also refer Figure S1 and S2 to compare the parameters selected by IHS and those by LHS and Figure S3 to compare the estimated bandwidth by IHS, LHS, CV and PI.

Numerical performance of would depend on (1) how much benefit there is in introducing , (2) whether the Fisher-divergence optimal parameters are close to the MISE optimal parameters , and (3) how much do the estimated parameters vary. Relative MISE in Table S2 and S3 reveals the first element. The second and third factors are not theoretically clarified in this paper but Figure S3 numerically compares the third factor with that of PI and CV for the standard KDE. With this in mind, we offer some discussion on the results for each DGP.

In scenario (i) Bimodal, Figure S1 and S2 show that there is no significant difference in the distributions of both estimated bandwidth and learning rate between IHS and LHS. Accordingly, the are almost identical between IHS and LHS. On the other hand, according to Table 1, IHS and LHS performs better than the ISE-oriented fully data-driven method (CV) in the ISE. Not only that, H-score based also outperforms PI. More notably, Figure S3 shows that the parameters selected by IHS and LHS are considerably more varied than those by PI and CV. Nevertheless, the ISE of by HS-based method listed in Table 1 is smaller than those of by PI and CV. These would be because, in view of Table S2 and S3, the benefit of introducing is large. For the same reason, IHS and LHS perform better than CV and PI in scenario (v).

In other scenario, tuned by IHS and LHS are inferior to tuned by PI or to by both PI and CV. The reason would be that (1) the advantage of introducing is not that great for these DGPs in view of Table S2 and S3, and that (2) CV and PI are designed to minimize MISE, while LHS and IHS are not as well as (3) the variability of estimated parameters (Figure S3). Among them, scenario (iii) Claw is the remarkable case where IHS and LHS differ in MISE The LHS estimates smaller than the IHS. To compensate for the lack of smoothness, is also estimated to be smaller in LHS, but the frequency of is quite high especially when . Considering that the asymptotic MISE optimal is greater than 1, it is consistent with the theory that LHS perform worse than IHS.

| DGP | Estimator | Bias | Variance | MISE | Relative MISE |

|---|---|---|---|---|---|

| (i) Bimodal | |||||

| (ii) Trimodal | |||||

| (iii) Claw | |||||

| (iv) Skewed | |||||

| (v) Outlier | |||||

| DGP | Estimator | Bias | Variance | MISE | Relative MISE |

|---|---|---|---|---|---|

| (i) Bimodal | |||||

| (ii) Trimodal | |||||

| (iii) Claw | |||||

| (iv) Skewed | |||||

| (v) Outlier | |||||

Appendix S3 Additional Figures of Simulation Results

Appendix S4 Outline of the Proofs

We provide the outline of the proofs in this section and technical details in separated sections, because the proofs are long and tedious rather than difficult.

S4.1 Outline of the Proofs of Theorem 1 and 5

In this subsection, we provide the outline of the proofs for Theorem 1 and 5. We expand the expected Fisher divergence up to higher-order than necessary to prove Theorem 1, because Theorem 5 needs the expansion.

S4.2 Proof of Corollary 2

Proof.

Since optimal is , the leading terms of the expectation of turns out to be

Since and (as shown later) the quantity in the bracket is positive, we can immediately deduce the explicit form of optimal bandwidth.

Next, we show that is non-negative. Recalling the definition of and , and letting

then we can see that

| (S5) |

so

from Cauchy-Schwarz inequality. Assumption D(e) exclude the cases where the equality holds. ∎

S4.3 Proof of Theorem 2

Proof.

The Hesse matrix of expected Fisher divergence is given by

Then, the Hessian is

| (S6) |

Since is positive from its definition and is non-negative as shown in Section S4.2, the first term in (S6) is non-negative. Also, from Assumption K(a) and the domain of is , which imply that . Therefore, combined with the fact that is positive and is non-negative, the second term in (S6) is non-negative. Finally, since and are strictly positive, the last term in (S6) is strictly positive. Written in inequalities,

Then, in view of (S6), the Hessian is always strictly positive.

Since, moreover, is always strictly positive, determinants of all leading principle sub-matrices are strictly positive. This implies that the Hesse matrix is strictly positive definite. ∎

S4.4 Outline of the proof of Theorem 3 and 6

In this subsection, we provide the outline of the proofs for Theorem 3 and 6. Similarly to the proof for the expansion of expected Fisher divergence, we expand the expected Hyvärinen score up to higher-order than necessary to prove Theorem 3, becasuse 5 needs the expansion.

In view of Section S6.1, empirical Hyvärinen score, under fixed , has two terms and , then, from the tower propety, the expected Hyvärinen score is given by as follows.

From the result of computation in Section S6.2.1 and S6.2.2,

and

then we have the asymptotic representation of the expected Hyvärinen score.

Next, we transform coefficients in order to prove the asymptotic equivalency of the expected Hyvärinen score to the expected Fisher divergence. One can show that, under Assumption D’(b), integration by parts yields

| (S7) | |||

| (S8) | |||

| (S9) | |||

| (S10) | |||

| (S11) |

These imply that

Then, from Assumption M(b),

Now, we have the asymptotic representation of expected Hyvärinen score with the same shape as the expected Fisher divergence.

S4.5 Outline of the Proof of Theorem 4

Proof.

See Section S6.3, for the derivation of .

Next, we will show that , with the discretization technique of parameter space likewise (Hall,, 1987, pp.1509-1510). Details of descretization are too lengthy in our case and the process is almost identical with Hall, (1987), so we will omit it. Under K(c), there exist lattice points and close enough to each other so that, for some constant

and, for some ,

holds. Then

so, from Chebyshev’s inequality, we have

In Section S6.3, we have derived the bound on as

Recalling the parameter space is limited so that and as , since,

we have a required bound to prove the theorem.

Remark S3.

Although it is natural doubt that, for example, does not converge even if , one can show that it is sufficient by deviding the cases, in order to prove the Theorem, to guarantee that the product of one of the terms in and converges. In the following, we provide one of the cases for illustration. We do not provide the proof of all cases to avoid tediousness.

Let take the case where dominants the other terms as example. For arbitrarily small , it holds that

In this case, since is dominated by as

so, implies . ∎

S4.6 Proof of Corollary 5

Proof.

First we define as

Using this notation, from Theorem 4, we have

Also, since and minimize the empirical Hyvärinen Score, it holds that

These imply that

| (S12) |

Then, from the uniqueness of the optimal parameters (Theorem 2), we can confirm that for any , there exists such that is satisfied for all and such that and . Thus

where the convergence is shown as (S12). Now, we confirm that the Theorem 4 implies

∎

Appendix S5 Properties of Expected Fisher divergence

In this section, we provide the detail computation for expected Fisher divergence. We need the result in this section to prove Theorem 1 and 5. Section S5.1 is bias and variance like decomposition of the expected Fisher divergence. Sections S5.2 and S5.3 are detail computation of bias and variance like terms of expected Fisher divergence. In this section, all expansion is conducted under Assumption M(a) and with fixed .

S5.1 Bias and Variance Decomposition

Since we can consider Fisher divergence of as Weighted MISE of , we can decompose into the squared bias and variance terms as follows.

S5.2 Bias

In order to get the asymptotic representation of the bias term, we compute at first.

where the third equality expands the denominator of the right-hand side of the second equality around . Since from a straightforward computation,

combined with Lemma S1, which states that

These imply that is expanded as follows.

then we have the asymptotic representation of the bias term.

S5.3 Variance

In order to get the asymptotic representation of the variance term, we expand

at first.

where the bound on the remainder term follows from Lemma S11 and Cauchy-Schwarz inequality. Since Lemma S2, S3 and S4 state that

These imply that is expanded as follows.

Since from the result of the computation in S5.2, the asymptotic representation of is given by

then we have the asymptotic representation of .

Appendix S6 Properties of Hyvärinen score

In this section, we provide the detail computation to investigate the properties of empirical Hyvärinen score. We need the result in this section to prove Theorem 3, 4 and 6. S6.1 is the derivation process of empirical Hyvärinen score and the generalisation of Section A.2.2 of Jewson and Rossell, (2022). Section S6.2 is detail computation of the expected Hyvärinen Score. Section S6.3 scrutinise the empirical Hyvärinen score in order to prove Theorem 4.

S6.1 Derivation of empirical Hyvärinen score

As Section A.2.2 of Jewson and Rossell, (2022), kernel density loss function to be the log-density

| (S13) |

The Hyvärinen score is then composed of the first and second derivatives of the log-density, given by

then, the Hyvärinen score of the kernel density estimate is

We introduce abbreviations for these two terms.

Then, we call the following statistics as ’empirical Hyvärinen score’.

S6.2 Expected Hyvärinen score

In this subsection, we derive the asymptotic representation of expected Hyvärinen score. In view of the definition of empirical Hyvärinen score derived in Section S6.1,

We compute these two term separately.

S6.2.1

First, in order to derive , we transform into a tractable form.

where the third equality multiplies the right hand side by

and the final equlity expands

around . Conditional on , because is a KDE from a sample with size of , converges. From this transformation, we have the conditional expectation of given as follows.

where the second equality multiplies the right-hand side by , the third equality expands the denominator. Because , this expansion is convergent.

S6.2.2

S6.3 Empirical Hyvärinen score

In order to get the asymptotic representation of the process , in other words, to derive and to bound , we expand the empirical Hyvärinen score . Recall that is given by as follows.

Then, expanding around yields

Next, we expand the denominator in the bracket around

. From Lemma S11,

so the expansion is valid. In addition, we have straightforwardly the bound of

then Cauchy-Schwarz’s inequality guarantees

This implies that it is sufficient to consider the expansion up to the second term. Then, we have

In the following, we transform and into a tractable form. First, we deal with .

| (S14) |

Letting the summand in the right hand side of (S14) be and its symmetrised version be , then we have U-statistics representation of the leading term of as

Since the leading term of has third-order U-statistics form, Hoeffding-decomposition yields

In the same process as , we have U-statistic representation of and its Hoeffding-decomposition.

| (S15) |

Letting the summand in the right hand side of (S15) be and its symmetrised version be , then we have U-statistics representation of the leading term of as

Hoeffding-decomposition yields

Remark S4.

The bound on the cubic term follows from Lemma S17. This bound is not sharp but sufficient for our aim, because obviously .

Since and , in order to bound , we compute the convergence rate of the variance of and and their covariance.

The constant terms , and are cancelled out by the corresponding term of , we only consider the other terms. Define . In addition, letting and be some functions of , then from Lemma S12 and S13,

these imply that

| (S16) |

| (S17) |

First, we compute the variace of . As a standard property of Hoefdding-decomposition, the covariance of the terms in the decomposition are all . Obviously, the variance of the first term is . In addition, Lemma S14 states that , combined with Lemma S16, the variance of is

| (S18) |

Similarly, since Lemma S15 state that , combined with Lemma S17, the variance of is

| (S19) |

From Cauchy-Schwarz inequality,

| (S20) |

Then, is bounded as

| (S21) |

Therefore in view of (S16) and (S17), we have

| (S22) |

and is bounded as .

Appendix S7 Proof of Theorem S1 (MISE)

In this section, we expand the MISE of .

S7.1 Preliminary Expansion

S7.2 Bias

From (S23), the expectation of is

Since

and Lemma S18 states that

it follows that

where the final equality follows from the fact that since and its derivatives are bounded (Assumption D(c)). This implies that the squared bias is

Integration of these term with respect to over gives the bias term in Theorem S1.

S7.3 Variance

Appendix S8 Lemmas

S8.1 Lemmas for the Computation of Expected Fisher divergence

S8.1.1 Lemmas for Computation of the Bias Term

Lemma S1.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a), it holds that

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

where the second equality follows from the assumption that is i.i.d. sample (Assumption D(a)). The third equality follows from the change of variables , the fourth equality follows from integration by parts combined with Assumption K(b), and the fifth equality expand and around combined with the assumption of -th order kernel (Assumption K(a)) and the smoothness assumption (Assumption D’(a)). ∎

S8.1.2 Lemmas for Computation of the Variance Term

Lemma S2.

Under Assumption D(a), D(c), D(b) , K(a), K(b) and M(a), it holds that

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

Lemma S3.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a), it holds that

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

Lemma S4.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a),

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

S8.2 Lemmas for the Computation of Expected Hyvärinen score

Lemma S5.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a), it holds that

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

Lemma S6.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a), it holds that

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

Lemma S7.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a), it holds that

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

Lemma S8.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a), it holds that

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

Lemma S9.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a), it holds that

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

Lemma S10.

Under Assumption D(a), D(c), D(b), K(a), K(b) and M(a),

and strengthening Assumption D(c) to D’(a), it holds that

Proof.

We prove only the second claim. One can prove the first claim in the same way and the proof is easier.

Since the process of the expansion is similar to of Lemma S1, we omit the detail explanation. ∎

S8.3 Lemmas for the Uniform Convergence of Empirical Hyvärinen score

S8.3.1 Lemmas for the expansion of Empirical Hyvärinen score

For notational simplicity, we rewrite as .

S8.3.2 Lemmas for the Hajék Projection Terms of Empirical Hyvärinen score

Lemma S12.

Proof.

From the following computations of , for some function of , we have

then, rearranging the right hand side for yields

In the following, we compute for each permutation separately, for some function and of .

-

•

-

•

-

•

∎

Lemma S13.

Proof.

From the following computation of , we have,

then, rearranging the right hand side for ,

In the following, we provide the result of computation of for each permutation separately. The computation process of them is same as of and straightforward but much longer and more tedious, so we provide only the results, for each permutation separately, for some function and of .

-

•

-

•

-

•

-

•

and

∎

S8.3.3 Lemmas for the Quadratic Projection Terms of Empirical Hyvärinen Socre

Lemma S14.

Proof.

The proof is straightforward but too lengthy, so we will omit it. ∎

S8.3.4 Lemmas for Bounding the Remainder Terms of Empirical Hyvärinen Socre

Lemma S16.

Letting be a summand of a third order U-statistics, under the assumption that , at least, the first projection term converges at the rate of , the quadratic term and the cubic term .

Proof.

Define as follows,

then the first projection term of a third order U-statistics and its squared moment are

Since for , from the standard property of U-statistics,

From the assumption, this implies

The proof for the quadratic term and for cubic term are similar. ∎

Lemma S17.

Letting be a summand of a fifth order U-statistics, under the assumption that , at least, the projection term converges at the rate of , the quadratic term and the cubic term .

Proof.

The proof is similar to Lemma S16. ∎

S8.4 Lemmas for MISE

Proof.

where the first equality expands the left hand side around , and the remainder of the second equality follows from the next Lemma. ∎

Lemma S19.

Proof.

Since the expansion of around yields

it holds that

This result and Markov’s inequality imply the lemma. ∎

Lemma S20.

Proof.

where the first term in the fifth equality follows form the change of variables of . ∎