Functional estimation and change detection for nonstationary time series111This is an Accepted Manuscript of an article published by Taylor & Francis in the Journal of the American Statistical Association on September 27, 2021, available at: https://www.tandfonline.com/10.1080/01621459.2021.1969239.

Abstract

Tests for structural breaks in time series should ideally be sensitive to breaks in the parameter of interest, while being robust to nuisance changes. Statistical analysis thus needs to allow for some form of nonstationarity under the null hypothesis of no change. In this paper, estimators for integrated parameters of locally stationary time series are constructed and a corresponding functional central limit theorem is established, enabling change-point inference for a broad class of parameters under mild assumptions. The proposed framework covers all parameters which may be expressed as nonlinear functions of moments, for example kurtosis, autocorrelation, and coefficients in a linear regression model. To perform feasible inference based on the derived limit distribution, a bootstrap variant is proposed and its consistency is established. The methodology is illustrated by means of a simulation study and by an application to high-frequency asset prices.

Keywords: gradual change; locally stationary process; -variation; bootstrap inference

1 Introduction

While statistical theory has historically been concerned with the study of data which is identically distributed, or at least stationary, this temporal homogeneity is often violated in practice. For example, economic time series are typically heteroscedastic, which is especially prominent for returns of financial assets. Statistical inference which does not account for nonstationarity may thus lead to wrong conclusions. However, the treatment of nonstationary models poses methodological challenges. Specifying the temporal variation nonparametrically, inference is often based on asymptotic methods, and it is in general not clear how to define a suitable limit in a nonstationary setting. As a remedy, Dahlhaus, (1997) suggested to regard the time index as a fraction of the sample size, which allows for infill asymptotics. This perspective leads to the concept of locally stationary time series, which has since been extended and generalized, see e.g. Wu and Zhou, (2011); Dahlhaus et al., (2019); Truquet, (2019).

In this paper, we study a multivariate, locally stationary time series model given by the causal representation

| (1) |

where for iid random variables . For each fixed and , the sequence is stationary. By letting the kernel depend on the fraction , the model explicitly accounts for nonstationarity. We assume that the kernel converges to a limiting kernel as in , and that admits some form of regularity. The nonlinear model (1) has been introduced by Zhou and Wu, (2009), and later been refined by Zhou, (2013). In contrast to the existing studies, the regularity assumptions imposed on the mapping in this paper are much less restrictive, as we only require finiteness of some -variation instead of Hölder continuity; see the detailed discussion in Section 2.

A statistician might be interested in various properties of the time series . We denote the quantity of interest by a local parameter , or , which is a functional of the law of , resp. . The estimator proposed in this paper is applicable for any parameter of the form , where , and is a sufficiently smooth function. Upon replacing by for a function , we may also study parameters , i.e. any parameter which may be expressed as a function of moments of . This framework is rather general, and contains for example the variance, kurtosis, and autocorrelations at fixed lag.

Depending on the application, different functionals of the temporal variation might be of interest, e.g. its temporal average as studied by Potiron and Mykland, (2020), its maximum value , or its value at some . For instance, estimation of is studied by Cui et al., (2020), who estimate the autocovariance function of a locally stationary time series via polynomial smoothing, and by Dahlhaus and Richter, (2019). The latter example is a nonparametric problem, and thus in general suffers from slow rates of convergence, depending on the regularity of . In this paper, we tackle the temporal variation by studying the integrated parameter

and we propose a corresponding estimator of . The function contains all information about the local parameter and is thus a nonparametric object as well. However, from a statistical perspective, it is attractive to formulate hypotheses in terms of since the latter may be estimated at a parametric rate , as demonstrated by our functional central limit theorem presented in Section 3. We note that the idea of recovering a rate of convergence via integration has also been employed in other areas of nonparametric estimation, e.g. when performing inference for integrated squared density derivatives in an iid setting (Hall and Marron,, 1987; Bickel and Ritov,, 1988), for convolutions of nonparametrically specified densities (Schick and Wefelmeyer,, 2004), and for quadratic integrals of derivatives of a regression function (Huang and Jianqing,, 1999). The previous references consider estimation of a single integrated quantity, but the functional estimation of a local parameter via its integral function is also common practice in high-frequency econometrics, when estimating integrated volatility or integrated nonlinear functionals of volatility; see Jacod and Rosenbaum, (2013), Aït-Sahalia and Jacod, (2014), and the references therein. In the context of nonstationary time series, this is applied, e.g., by Dahlhaus, (2009), who considers linear functionals of the time-varying spectral density.

A general method to estimate integrated parameters has been suggested by Potiron and Mykland, (2020). They construct block-wise estimators and average them to obtain an estimator of . While this approach could be adapted to the functional estimation of , the verification of their assumptions for the estimators entails additional analytical effort for each special case. In particular, they require strong conditions on the bias of , and present explicit debiasing procedures for specific examples. In contrast, our proposed estimator is based on a linearization procedure around a nonparametric pilot estimator , and may be regarded as a generic approach for removing leading bias terms. We suggest a pilot estimator based on local smoothing, but our results are deliberately formulated under much weaker conditions, requiring only assumptions on the rate of convergence of . Many modern approaches to filtering and regression are based on statistical learning theory, which typically yields satisfactory rates of convergence, but does not lend itself to statistical inference. Our linearized estimator thus enables rigorous asymptotic inference based on these pilot estimates. Details are presented in Section 3.

Our estimator is particularly useful to test for change-points in the local parameter. Here, the null hypothesis is that the parameter is the same for all , which may be formulated equivalently as

| (2) |

Analysis of this hypothesis of structural stability has a long history in statistics, see Aue and Horváth, (2013) for a recent review. Early studies were concerned with the stability of the mean (Page,, 1954, 1955). The methodology has since been extended, and there exist procedures to test for, e.g., the stability of variances (Gao et al.,, 2019), regression coefficients (Horváth,, 1995), or autocovariances (Berkes et al.,, 2009; Killick et al.,, 2013; Preuss et al.,, 2015). Our approach provides a unifying framework to study these problems for parameters which may be written as a function of nonlinear moments. Besides the mentioned examples, this also includes novel change-point tests which have not been studied previously, e.g. a test for the temporal stability of kurtosis. The proposed change-point tests are robust against various model misspecifications, e.g. nonstationarity and nuisance changes under the null hypothesis. In particular, our test only monitors changes in the parameter , but not in the parameter itself. For example, our statistic is sensitive to changes in the variance, but robust to changes in the unknown and time-varying mean value. The change-point tests based on our estimator are discussed in greater detail in Section 4 below.

There are parameters of interest which may not be expressed as a function of finitely many moments, for example quantiles of the marginal distribution, or functionals of the local spectral measure as considered by Dahlhaus, (2009). A very general framework is presented by Shao and Zhang, (2010), where an arbitrary functional of the time series’ distribution is studied. The assumptions therein are formulated in terms of the influence function corresponding to the statistical functional of interest. Their verification is far from simple and basically amounts to proving claims very similar to the steps we take in this article. In contrast, we believe that the conditions imposed in the present paper are conveniently verified for a broad range of practical problems. The framework of Shao and Zhang, (2010) is also adopted by Dette and Gösmann, (2020) and applied to the monitoring of quantiles, as well as by Gösmann et al., (2021). Note that these authors study the stationary case only, while we allow for nonstationarity. It might be of interest to extend the methodology introduced in the present paper to more general functionals. We leave this question for future work.

The outline of this paper is as follows. After defining the model in Section 2, we describe the functional estimator in Section 3 and present our asymptotic results., we give the rigorous definition of our model and present the technical assumptions. The application of our results to change-point problems is discussed in Section 4, and the finite sample properties of our proposed procedure are assessed via simulations study in Section 5. Our methodology is illustrated by an application to financial data in Section 6. Appendix A in the supplement contains additional remarks, and Appendix B contains further examples and simulation results for change point testing. All technical proofs are deferred to Appendix C.

Notation

For a function , we denote the first order differential, and by the Hessian matrix. For two sequences , we write if as . For , we denote . Weak convergence of probability measures and random elements is denoted by . For a vector , the Euclidean norm is denoted by , and for a matrix , we denote by the operator norm, i.e. . The spectral radius of a matrix is denoted as , where the are the complex eigenvalues of . The transpose of a matrix is denoted by . For a random vector , we denote by the norm, for . The notation is introduced in Section 2.

2 Model

Let be a triangular array of random variables which is causal in the sense that for a sequence of functions . Here, we denote

where the are iid random variables. The functions are assumed to be measurable, where we endow the sequence space with the projection -Algebra, see (Billingsley,, 1999, Example 1.2).

By using a sequence of functions , we will be able to apply our results to investigate the power of the proposed tests against local alternatives. Furthermore, letting the kernel depend on allows us to account for potential discretization errors, see Example 1 below. We assume that the kernel tends towards a limiting kernel , in the sense that

| (A.1) |

for some . Note that we do not require a rate of convergence in (A.1). Furthermore, we require the function to satisfy some regularity conditions. A very mild condition can be formulated in terms of -variation for some , defined as

The latter definition is independent of the chosen , since . The -variation of the limiting kernel is denoted analogously as . We assume that

| (A.2) |

and will be further specified if necessary. Note that for , hence assumption (A.2) is stronger for smaller .

The assumption of finite -variation is less restrictive than the piecewise-locally-stationary (PLS) framework suggested by Zhou, (2013), which amounts to requiring piecewise Lipschitz continuity with finitely many breakpoints. The PLS framework has been applied for change-point analysis by Dette and Wu, (2019), Dette et al., (2019), among others. In contrast, finite -variation still allows for infinitely many discontinuities of the mapping . On the other hand, if the latter mapping is Hölder continuous with exponent , then for . Thus, assumption (A.2) is more general than requiring Hölder continuity, and it combines classical smoothness conditions as well as discontinuities in a single framework. The special case of bounded -variation has been considered by Dahlhaus and Polonik, (2009) for linear processes. Our framework also contains the model of Dahlhaus et al., (2019) as a special case, see Section A.1 in the supplement.

The third and last assumption imposed on the causal kernel is uniform ergodicity. We employ the physical dependence measure introduced by Wu, (2005). To define the dependence measure, we introduce an iid copy of the Denote for ,

We assume that there exists a value such that, for all

| (A.3) |

This implies that

see Proposition C.1 in the appendix.

This set of assumptions suffices to establish a functional central limit theorem for the partial sums of the . An analogous limit theorem has been proven by Zhou, (2013) under the more restrictive PLS assumption.

Theorem 2.1.

By virtue of the Cramer-Wold device, Theorem 2.1 can be extended to the multivariate case to yield weak convergence in the space endowed with the product topology. Note that this topology is different from the Skorokhod topology on the space of cadlag functions , see (Jacod and Shiryaev,, 2003, VI.1.23).

We conclude this section by giving an example of a process which satisfies assumptions (A.1)-(A.3), highlighting that the imposed conditions are rather weak.

Example 1.

Consider the time-varying vector autoregressive (tvVAR) process in dimensions which satisfies

where is a sequence of iid, -dimensional random vectors with finite moments of all orders, , and are matrix valued functions. Note that higher-order autoregressive processes may also be studied in this framework by stacking the lagged values of the process, effectively increasing the dimension . For example, an autoregression of order two may be described in terms of the state vector , taking values in . Time-varying autoregressive models are classical examples of locally-stationary time series. Early investigations of these models include Subba Rao, (1970) and Grenier, (1983), and more recent contributions are due to Moulines et al., (2005), Dahlhaus and Polonik, (2009), and Giraud et al., (2015), among others.

We extend to the domain by setting and for . The autoregressive process may be cast into our framework as

This infinite sum is well-defined if we suppose that , that the spectral radius of , is at most , and that the function admits some minimal regularity. In particular, if the function has bounded -variation for some , then for any , see Lemma C.8 in the appendix. Hence, assumption (A.3) is satisfied. Furthermore, if the functions , , and are left-continuous, we have by dominated convergence for any , with limiting kernel

In particular, condition (A.1) holds. Finally, Proposition C.9 in the appendix shows that assumption (A.2) holds if . Moreover, in the more regular case that , , and are -Hölder continuous, the kernel is also -Hölder continuous in , uniformly in , and thus the same holds for . The latter property is required to apply Proposition 3.1 discussed in the following section.

3 Estimating integrated parameters

For the locally stationary model introduced in Section 2, we denote the local moments by

Inference for the function resp. can be performed in various ways. For example, one might assume a parametric form for the mapping . Here, we are interested in testing nonparametric hypotheses imposed on the function . To this end, instead of treating the moment function directly, we suggest to consider its integral. In particular, for a nonlinear function , we study the integrated quantity

Note that most hypotheses on may be reformulated in terms of . In Section 4, we will study change-point detection, where the null hypothesis for is equivalent to the hypothesis . It is also possible to study the hypothesis , which is equivalent to . Another appealing aspect of studying the integrated quantity instead of is that the former may be estimated at a parametric rate , even in a nonparametric framework, see our results below. Though this might be surprising at first sight, note that a similar phenomenon occurs in the classical statistical setting of iid observations, where the empirical distribution function is consistent, while nonparametric density estimation only allows for slower, nonparametric rates of convergences.

A straightforward way to estimate is to consider the partial sum process

| (3) |

where is a nonparametric estimator of , and may be introduced to alleviate boundary issues. This approach has two shortcomings. First, its distributional properties strongly depend on the specific estimator . Thus, additional theoretical effort is required when adapting corresponding inferential procedures to new situations. Second, for nonlinear , the estimator may be bias-dominated, impeding statistical inference.

In particular, a Taylor expansion yields

| (4) |

For most estimators , the bias of this expression is not smaller than . If one considers, for example, a local average with bandwidth , and assumes to be Lipschitz continuous, then the bias of is of order , which is at best . In a related situation, Jacod and Rosenbaum, (2013) suggest to solve this problem by undersmoothing, i.e. choosing , and correcting the quadratic bias term in (4) explicitly; see also (Potiron and Mykland,, 2020, Section 4.2). However, the latter quadratic bias term strongly depends on the specific estimator , so that the approach of Jacod and Rosenbaum, (2013) may not be easily transfered to different problems.

As a generic approach for asymptotically unbiased estimation of integrated functionals, we propose the linearized partial sum estimator

| (5) |

for some initial offset , lag , , to be specified later, and assuming to be sufficiently smooth. The pilot estimator needs to satisfy minimal high-level assumptions formulated below. Then, a Taylor expansion of readily yields, for some between and ,

It can be shown that converges to zero sufficiently fast. Moreover, if is sufficiently regular, and the estimator is good enough, then , whereas is asymptotically unbiased and tends towards a Gaussian process.

We require the function to have bounded first and second derivatives in a neighborhood of the path of . Formally, introduce the convex set , and its -neighborhood . We require that there exists a and a such that

| (A.4) |

By restricting the boundedness assumption to the set , we may also consider functions of the form , if on the set . Without localization, (A.4) would not hold for this choice of .

Regarding the pilot estimator, we require that is measurable w.r.t. the past innovations , i.e. is a (potentially nonlinear) filter. By additionally introducing the lag , the measurability condition on serves to de-bias the term . In particular, as , the random vectors and decouple by virtue of (A.3). Furthermore, we require the estimator to be consistent in the sense that

| (A.5) | ||||

| (A.6) |

The initial offset allows to circumvent boundary issues of the estimator . The assumptions (A.5) and (A.6) are rather mild. Property (A.6) requires some weak form of uniform consistency of the estimator. If is globally smooth, i.e. , then (A.6) is vacuous, and is a valid choice. Property (A.5) is a requirement on the rate of convergence of , in a form routinely studied in nonparametric statistics. The latter assumption is discussed in detail in Section A.2 of the supplement. If we are willing to impose some additional smoothness conditions, a suitable nonparametric estimator may be obtained by local averaging. In particular, we define

for a sequence . Note that can be interpreted as a one-sided kernel smoother of Nadaraya-Watson type.

Proposition 3.1.

By allowing the vanishing discontinuous part in Proposition 3.1, we may account for potential discretization errors.

For the local smoother , as well as for any other estimator satisfying our assumptions (A.5) and (A.6), the functional estimator admits a central limit theorem with parametric rate . Our main result may be formulated as follows.

Theorem 3.2.

Just as in Theorem 2.1, the Cramer-Wold device may be used to extend Theorem 3.2 to the multivariate setting where takes values in . The functional weak convergence then holds in the product space . If and , we may alternatively choose as centering term, such that has the asymptotic distribution given in Theorem 3.2.

Remark 1.

The suitable choice of the lag parameter depends on the strength of the dependency of the time series. On the one hand, the bias term grows polynomially with , i.e. , see Lemma C.5 in the supplement. This suggests to choose the lag as small as possible. On the other hand, needs to be large enough such that and decouple, in order for to be asymptotically unbiased. In particular, in view of assumption A.3, we need to ensure that . To ensure that both, and the bias of , are negligible, a conservative choice is for some factor . The sensitivity of our methodology with respect to is assessed by simulations in Section 5.

Remark 2.

In contrast to Theorem 2.1, the central limit theorem of the linearized estimator requires , i.e. the kernel needs to be more regular. This restriction is due to the bias incurred by the lag . In particular, we can only ensure that if , see Lemma C.5 in the supplement. On the other hand, the criticality of occurs because , see Lemma C.4 in the supplement. Note that both issues are not present in the linear case of Theorem 2.1.

The integrand of the asymptotic variance of the limit process corresponds to the long-run variance under the local, stationary model . In particular, a direct application of the delta method shows that

| (6) |

If our model is indeed stationary, Theorem 3.2 shows that has the same asymptotic distribution as (6). In this sense, accounting for the nonstationarity does not increase the asymptotic variance.

To perform feasible inference based on Theorem 3.2, we need to handle the unknown asymptotic variance process. A consistent estimator may be constructed via blocked subsampling, similar to the suggestion of Carlstein, (1986).

Theorem 3.3.

Let the conditions of Theorem 3.2 hold for some , and . Choose some such that , . Then, as ,

The convergence holds uniformly in since is monotone.

Theorem 3.3 is a special case of the slightly more general Theorem C.7 in the appendix. Note that the upper bound on reduces to if .

The estimator may be used to perform inference based on via the following multiplier bootstrap scheme, similar to Zhou, (2013).

Theorem 3.4.

It can also be shown that the bootstrap consistency of Theorem 3.4 holds under weaker rate constraints on , replacing the rate by for some . However, a smaller value of requires stronger conditions on , see Theorem C.7 in the appendix. The local smoother is still consistent in the non-smooth case, where only , although at a slower rate. Hence, the latter estimator may still be utilized for consistent variance estimation. This is of particular interest for applications to change-point tests, as described in the following section, where the bootstrap procedure is still consistent under various alternative hypotheses.

4 Change-point detection

A major motivation to perform inference for the integrated parameter resp. is that the estimator may be used to test for change-points. Our framework lends itself to test the hypothesis

| (7) |

To perform a test for this problem, a common approach is to formulate the CUSUM statistic, which in our case reads as

| (8) | ||||

The main result Theorem 3.2 yields that as , which is identically zero if the null hypothesis holds. In this case, Theorem 3.2 yields that

where is the Gaussian limit process. The limit distribution may be approximated via the bootstrap procedure outlined in Theorem 3.4, i.e. by sampling the random variable , so that by virtue of Theorem 3.4. In particular, denote by the quantile of , and by the quantile of . In practice, the quantile may be approximated up to arbitrary precision by sampling from the conditional distribution . The corresponding test procedure may then be formulated as follows.

Proposition 4.1.

Although we focus on the uniform CUSUM test statistic, the functional central limit theorem for the process also enables the consideration of alternative statistics, e.g. the MOSUM statistic introduced by Bauer and Hackl, (1978), see also Chu et al., (1995), or the Cramér-von Mises statistic .

A desirable property of change-point tests is robustness against nuisance changes. For the quantity to be non-constant, it is necessary that the local moment changes. It is thus tempting to instead test the null hypothesis , which is methodologically simpler to achieve. For example, the methods of Zhou, (2013) and Vogt and Dette, (2015) are applicable to test for . However, this approach bears the risk to falsely detect a change although remains constant. For example, it might happen that the variance of a time series is non-constant, while the autocorrelation structure remains constant, as studied by Dette et al., (2019). Furthermore, Schmidt et al., (2020) tests for homoscedasticity with a non-constant mean function. A related approach is presented by Demetrescu and Wied, (2018). By design, our test is only sensitive to changes in the quantity .

Another type of nuisance change might occur in the parameters which are not explicitly described by the local moment function . For example, when testing for changes in the mean of a heteroscedastic time series, the variance is a nuisance parameter not contained in the vector , but relevant for statistical inference, see Górecki et al., (2018) and Pešta and Wendler, (2020). We account for this type of nonstationarity by working in a locally stationary framework which allows not only for heteroscedasticity, but also for a varying dependency structure. This has also been suggested by Zhou, (2013), who designs a corresponding test for changes in the mean. The recent articles Vogt and Dette, (2015), Dette et al., (2019), and Cui et al., (2020), also employ a locally stationary model.

Test statistics for the change point problem usually need to be standardized by an estimator of their asymptotic variance. However, variance estimators designed for the stationary case might be inconsistent under the alternative, resulting in a loss of power, see (Juhl and Xiao,, 2009; Shao and Zhang,, 2010) and the discussion therein. In contrast, our bootstrap procedure is consistent under the alternative where is not constant and potentially discontinuous, see Theorem 3.4 and the discussion thereafter. Moreover, we may investigate the behavior of our test statistic under local alternatives at rate .

Proposition 4.2.

Note that under the local alternative of Proposition 4.2, the simple estimator still satisfies (A.5) and (A.6) if is smooth, see Proposition 3.1. Hence, Theorem 3.4 is still applicable so that the bootstrap is consistent, and the CUSUM test with bootstrapped critical values has non-trivial power against local alternatives in direction , given that . We also point out that the test has power not only against abrupt changes, but also against changes which occur gradually in time.

The proposed procedure allows for a unified treatment of change-point tests for a wide range of parameters of interest, as demonstrated by the examples below. Previously, suitable test statistics have been constructed individually for these problems, while our results show that they may be treated in a rather generic way.

4.1 Changes in autocorrelation

The dependency structure of time series is commonly described in terms of their autocovariance function. It is thus natural to test the latter for structural stability, as suggested by Berkes et al., (2009). They construct a CUSUM test based on the partial sums which form the empirical autocovariance estimator at fixed lag, and derive limit theorems under the assumption of stationarity. A method to detect changes without fixing the lag is mentioned by (Steland,, 2020, Example 3). The case of a nonparametric mean function is investigated by Li and Zhao, (2013), and multiple change-points are studied by Preuss et al., (2015). The non-stationary case is investigated by Killick et al., (2013), although without a rigorous analysis of the type I error.

Alternatively, in the same univariate setting, Dette et al., (2019) test whether the autocorrelation remains constant, for some fixed . This problem is more involved, since it requires standardization by the marginal variances, which are an additional nuisance quantity. They allow the marginal variance to be non-constant and estimate it non-parametrically, in order to standardize the observations. Furthermore, Dette et al., (2019) study a nonlinear, locally stationary specification of the underlying time series. Hence, they account for potential nonstationarity under the null hypothesis.

We may formulate the problem to test for constant autocorrelations in our general framework. To this end, we set for , assuming for simplicity that for . Now set , so that . Again, assumptions (A.1)-(A.3) are a direct consequence of the corresponding properties of . The function is bounded on any compact set . Thus, if , then (A.4) holds for as well. We may thus construct based on this time series and function to obtain an estimator for the integrated autocorrelation . The corresponding CUSUM statistic satisfies (8).

4.2 Further examples

The kurtosis of a random variable is defined as . For a univariate time series , let . Then can be written as a function of . In particular,

If , then satisfies (A.4) so that our results are applicable, and the CUSUM statistic (8) in combination with the bootstrap procedure yields a feasible change-point test. To the best of our knowledge, the proposed method is the first test for structural stability of the marginal kurtosis.

In a similar way, we may consider the skewness of a random variable provided that the variance of is bounded away from zero, or the coefficient of variation if the expectation of is bounded away from zero. A further example which may be cast in our framework are time-varying autoregressive models, as presented in example 1, where the coefficients may be identified in terms of finitely many autocovariances by means of the Yule-Walker equations. Our methodology could thus be used to test for changes in the second autoregressive component of a univariate tvAR model.

5 Finite sample performance

To assess the finite sample performance of our proposed change-point test, we evaluate its size and power properties via simulations. We consider the locally stationary autoregressive process given by

| (9) |

The innovations are chosen as independent, zero-mean random variables having a symmetrized Gamma distribution with shape parameter , standardized to unit variance. We use

and for , either of the three functions

We want to test for stability of the lag-1 autocorrelation, which is equivalent to the stability of the autoregressive coefficient . To this end, we apply the change-point test presented in Section 4.1 , in combination with the local estimator .

As described in Remark 2, the lag parameter should be chosen just big enough such that the functional dependence measure at lag is negligible. We choose and analyze the effect of the factor below. Once is specified, the smoothing bandwidth may be determined via cross-validation, by minimizing the prediction error

where denotes the local average with bandwidth . In our simulations, we consider bandwidths from the interval . Then, a natural choice for the offset is . Finally, we choose the window size for the bootstrap procedure as . Thus, is the only parameter to be chosen manually. While a data-driven choice of the lag parameter is desirable, deriving a corresponding method is out of scope of this article.

To find the critical value of the CUSUM test, for each individual sample, we resample independent realizations based on the bootstrap approximation of Theorem 3.4. Equivalently, we may use the bootstrap samples to compute an approximate p-value for the CUSUM test statistic. When assessing the size of the CUSUM test, we set , and for the power analysis, we set respectively .

| DWZ | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.26 | 0.19 | 0.28 | 0.04 | 0.03 | 0.05 | 0.04 | 0.03 | 0.04 | 0.05 | 0.04 | 0.04 | 0.50 | 0.54 | 0.49 | |

| 500 | 0.02 | 0.03 | 0.02 | 0.02 | 0.13 | 0.03 | 0.04 | 0.37 | 0.05 | 0.05 | 0.49 | 0.07 | 0.18 | 0.67 | 0.22 |

| 1000 | 0.01 | 0.18 | 0.01 | 0.02 | 0.55 | 0.04 | 0.04 | 0.81 | 0.09 | 0.06 | 0.89 | 0.11 | 0.13 | 0.91 | 0.21 |

| 5000 | 0.02 | 1.00 | 0.20 | 0.04 | 1.00 | 0.33 | 0.07 | 1.00 | 0.42 | 0.08 | 1.00 | 0.46 | 0.07 | 1.00 | 0.47 |

| 10000 | 0.03 | 1.00 | 0.56 | 0.06 | 1.00 | 0.68 | 0.08 | 1.00 | 0.74 | 0.09 | 1.00 | 0.76 | 0.07 | 1.00 | 0.78 |

Table 1 presents the size and power of the proposed test in the presented example, for various values of and different choices . The power values correspond to the alternatives based on , and based on . We find that our test is rather conservative, i.e. the type-I error is actually smaller than the nominal level, and this conservativeness vanishes asymptotically as increases. In particular, our test does not falsely detect a structural break even though the nuisance parameter is non-constant. On the other hand, the method consistently detects deviations from the null hypothesis, as demonstrated by the increasing power against the alternative. Moreover, it is found that the smallest lag value yields the best size approximation. Note that the differences in power for various choices of may be partially explained by the different test sizes. For the latter choice of , we also depict the distribution of the simulated p-values in Figure 1. The p-values should ideally be uniformly distributed. Indeed, for large sample size , the accuracy of the p-values increases, in line with our theoretical results.

For comparison, we also implement the change point test for constant lag-1 autocorrelation proposed by Dette, Wu, and Zhou (Dette et al.,, 2019). The corresponding size and power are also presented in Table 1, labeled as DWZ. In small samples, the latter test achieves a higher power, which may be explained by a correspondingly higher rate of false positives. For large sample sizes, the power is similar to our proposed test, showing that our broadly applicable method is competitive against the specialized test of Dette et al., (2019).

| error | 0.172 | 0.120 | 0.053 | 0.058 | 0.031 | 0.039 | 0.012 | 0.018 | 0.008 | 0.013 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| bias | 0.071 | -0.114 | 0.022 | -0.054 | 0.011 | -0.036 | -0.001 | -0.016 | -0.002 | -0.012 | |

| error | 0.242 | 0.197 | 0.061 | 0.093 | 0.035 | 0.066 | 0.011 | 0.031 | 0.008 | 0.023 | |

| bias | 0.163 | -0.197 | 0.039 | -0.093 | 0.020 | -0.066 | 0.002 | -0.031 | -0.001 | -0.023 | |

| error | 0.180 | 0.134 | 0.053 | 0.062 | 0.032 | 0.044 | 0.012 | 0.020 | 0.008 | 0.014 | |

| bias | 0.084 | -0.131 | 0.025 | -0.060 | 0.012 | -0.043 | -0.000 | -0.019 | -0.002 | -0.014 | |

We also assess the quality of as an estimator of , , in comparison to the plug-in estimator . Table 2 presents the mean absolute errors of both estimators, as well as their corresponding bias. Except for the smallest sample size , the proposed linearized estimator performs better than the simple plug-in estimator. In particular, the linearization greatly decreases the bias of the estimator.

We also assess the finite sample performance of a change point test for the coefficients of a linear regression model. The simulation results are presented in Section B.3 of the supplement.

6 Empirical illustration

To demonstrate the use of our results in practice, we study an application to high-frequency financial data. In particular, we study the price of the german mid-cap stock-index MDAX on April 4, 2016, from 9:00-15:30, at a sampling frequency of second. The data is available as a free sample from the data shop of Deutsche Börse, and part of the supplementary material of this article. We study the log-returns , , with sample size .

While many models for asset prices imply uncorrelated returns, empirical research suggests that autocorrelation may be non-zero, especially at high sampling frequencies (Hansen and Lunde,, 2006). This dependence structure is typically attributed to the microstructure of the market, e.g. rounding effects or bid-ask rebounds. Recently, Andersen et al., (2019) studied the intraday returns of the NASDAQ100 stocks and found evidence for autocorrelation which is not only non-zero, but also non-constant.

Using the framework laid out in Section 4.1 above, we may rigorously perform asymptotic inference for the local autocorrelation . To this end, we use the local estimator and choose its bandwidth via cross-validation as in Section 5, with .

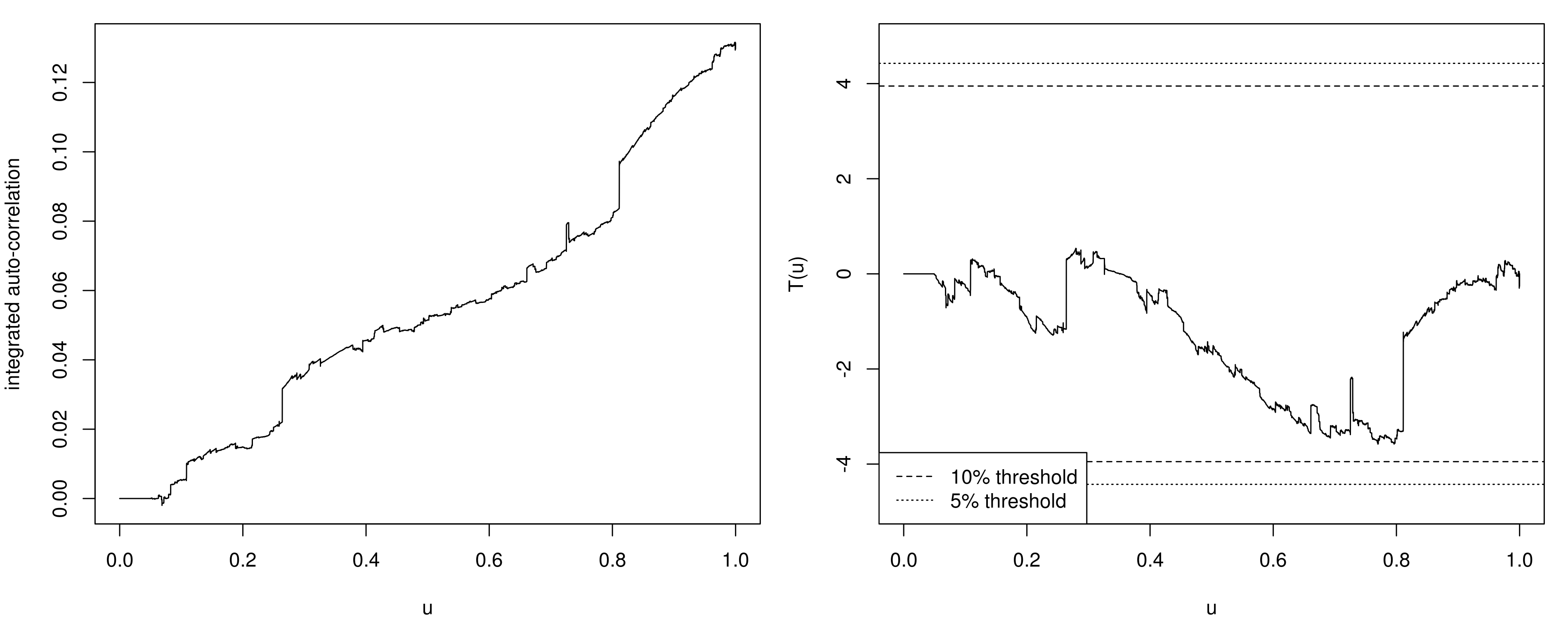

The functional estimator of the lag-1 autocorrelation is depicted in Figure 2 (left). First, we observe that is roughly increasing, which indicates that the lag-1 autocorrelation is positive on average. Indeed, the average lag-1 autocorrelation is estimated as , with asymptotic standard deviation . Moreover, visual inspection of suggests that the slope is varying, which corresponds to a non-constant autocorrelation. To test this hypothesis rigorously, we perform the CUSUM test suggested in Section 4. The right panel of Figure 2 shows the CUSUM process , and the critical thresholds for a significance level of and , respectively. The critical values are obtained using the bootstrap approximation of Theorem 3.4, with bootstrap samples. The bootstrap-based p-value of the CUSUM test statistic is , based on bootstrap samples. Note that the sample size is rather large, and the simulation results of Section 5 suggest that the bootstrap approximation is satisfactory for this regime. Hence, we find that the variation of the lag-1 autocorrelation is not significant. That is, based on the bootstrapped CUSUM test, we may not reject the null hypothesis of constant lag-1 autocorrelations for this particular dataset at a significance level of .

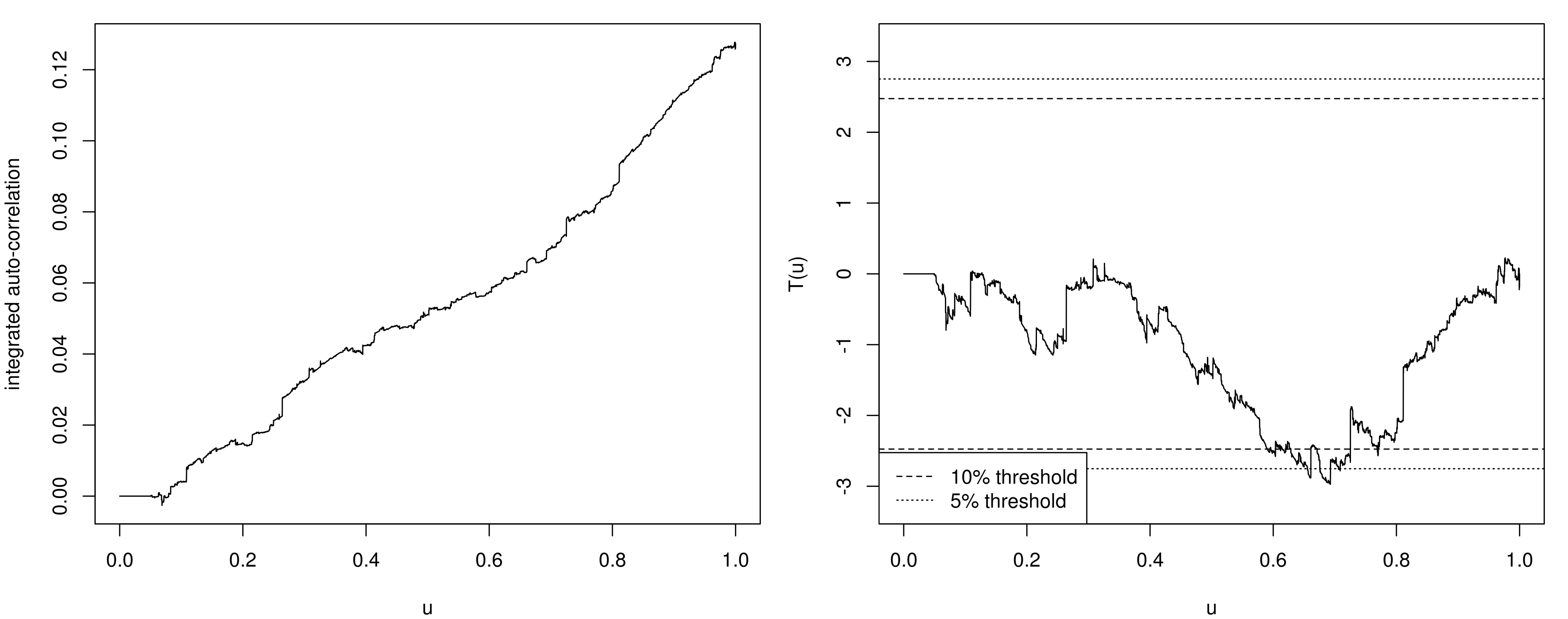

The visible discontinuities of the path of in Figure 2, suggest that the estimator is influenced by few very large price changes . While our bootstrap procedure automatically accounts for this, the resulting large variance decreases the power of the change point test. To reduce the effect of the heavy tails of the log returns, we repeat our analysis for the transformed increments . We choose , which corresponds to the average size of and leads to a unimodal distribution of transformed returns (not depicted). The estimator of the lag-1 autocorrelation of the transformed returns is depicted in Figure 3, as well as the corresponding CUSUM process. The p-value of the CUSUM test is , hence the hypothesis of constant lag-1 autocorrelation is rejected for the series at a significance level of . Although the autocorrelations of and are not the same parameters, both may be interpreted similarly in the present application. In particular, our findings support the claim of Andersen et al., (2019) that the serial correlation of intraday log returns is non-constant for the present data set. In contrast to Andersen et al., (2019), our change point test does not assess whether the autocorrelation changes its sign.

We also analyze the variance, mean, and kurtosis of and as outlined in Sections B.1 and 4.2. For , the CUSUM tests for constant variance, mean, and kurtosis yield the p-values , , and , respectively. For , the respective p-values are , , and , respectively. In combination with our statistical results on the autocorrelation, this provides strong evidence for nonstationarity of and .

Many models for asset returns at very high frequencies describe the observed price as the sum of two latent components: the fundamental price , and the so-called microstructure noise , such that . The fundamental price is typically modeled as a semimartingale, and inference for this component needs to account for the microstructure effects, see e.g. Jacod et al., (2009). The microstructure noise is typically assumed to be independent, or dependent but stationary (Hansen and Lunde,, 2006; Aït-Sahalia et al.,, 2011). Nonstationary dependent noise is considered by Jacod et al., (2017), but such that the autocorrelation of the microstructure is constant. The approach we pursue in the present paper does not distinguish between the fundamental price and the microstructure effects. Nevertheless, our empirical findings may motivate the investigation of microstructure models which allow for a nonstationary dependence structure.

Appendix A Further remarks

A.1 Alternative definition of local stationarity

The model described in Section 2 may also be compared to the definition of locally-stationary processes introduced by Dahlhaus et al., (2019). They require that for each , there exists a stationary process such that

-

(i)

, and

-

(ii)

, for some and .

If the time series and , , are -measurable, we may represent them as , and , for kernels and which are measurable w.r.t. . Without loss of generality, we may suppose that is a left-continuous, piecewise constant mapping with finitely many break points at , for . Then

Conditions (i) and (ii) imply that is bounded for any . Hence, provided that the time series is measurable, our framework contains the model of Dahlhaus et al., (2019) as a special case. For instance, we may describe temporally varying auto-regressive processes, as described in Example 1.

A.2 Rates of convergence of the pilot estimator

Property (A.5) is a requirement on the rate of convergence of , in a form routinely studied in nonparametric statistics, see e.g. (van de Geer,, 2010, Ch. 9). The achievable rate of convergence in nonparametric regression depends in particular on the smoothness of the function . In our model, the only regularity assumption on is (A.2), which implies that . Thus, empirical process theory suggests an achievable rate of convergence of for . This rate can be derived by combining general results for least squares regression with subgaussian errors (van de Geer,, 2010, Thm. 9.1) with entropy bounds for the class of functions of bounded p-variation (Giné and Nickl,, 2016, Cor. 3.7.50). Note that this rate is in line with the requirement (A.5) if . Furthermore, we point out that this rate of convergence matches the rate under the assumption of Hölder continuity with exponent . While the Hölder-continuous case may be treated via local smoothing, the generic approach to achieve this rate of convergence under the assumption of finite -variation is via empirical risk minimization, which in particular uses the whole sample. However, we additionally require that is -measurable, rendering this approach infeasible. While it might be possible to construct a suitable online estimator which achieves the desired rate of convergence for functions of bounded p-variation, this is out of the scope of this article. See for example Baby and Wang, (2019) and Raj et al., (2020) for the case based on iid observations.

Another alternative is to formulate a parametric estimator of , which will typically satisfy (A.5) with the stronger rate . For example, this approach is feasible if is piecewise constant with a single breakpoint. However, in order to apply a parametric estimator, additional assumptions need to be imposed on the underlying time series. If these parametric assumptions do not hold, any inference based on the corresponding asymptotic results will be flawed. This encourages the use of nonparametric estimators for the local moment function .

Appendix B More examples of change point problems

B.1 Changes in variance

For a univariate time series , various researches have designed tests for constancy of the variances , starting with the investigation of asset returns by Hsu et al., (1974) and the corresponding methodology of Wichern et al., (1976). A test based on cumulative sums of squared observations has been suggested by Inclán and Tiao, (1994), and Chen and Gupta, (1997) suggest an alternative procedure based on the Schwarz information criterion. The approach of Inclán and Tiao, (1994) has been generalized by Lee and Park, (2001) to dependent processes, and by Aue et al., (2009) to the multivariate case. A common shortfall of many procedures is that they require constancy of the mean , which is a nuisance parameter in the present situation. More recent work studies the case of non-constant mean by using a suitable nonparametric estimator thereof, see Gao et al., (2019) and Schmidt et al., (2020). Note that the latter references still require stationarity of all remaining nuisance quantities, such as autocorrelations and higher order moments.

An alternative test for homoscedasticity can be formulated using our results. Based on the univariate time series , we define the vector valued time series with mean . Then , for . It is straight-forward to check that if satisfies assumptions (A.1)-(A.3) for , then satisfies the assumptions for . Moreover, and all its derivatives are bounded on compacts, such that (A.4) holds if is bounded. Thus, the asymptotic result (8) holds and yields a test for the hypothesis , allowing for non-stationary mean under very mild regularity conditions on dependency structure of .

B.2 Changes in regression coefficients

Suppose we observe a univariate time series and a -dimensional vector time series , such that . The noise values satisfy and . We want to test whether is constant, or varies with . This problem has been studied, among others, by Horváth, (1995), Horváth et al., (2004), and Aue et al., (2008) for uncorrelated innovations . Correlated regression errors are treated, for example, by Robbins et al., (2016). In this setting, the hypothesis may be formulated in the form (7), since

where and . Thus, , for

where the matrix is interpreted as a -dimensional vector. Assumptions (A.1)-(A.3) are a direct consequence of the corresponding properties of and . Moreover, satisfies (A.4) if we ensure that the smallest eigenvalue of admits a uniform lower bound.

Note that is a -dimensional parameter. It is straight-forward to extend the CUSUM statistic to the multivariate setting, e.g. by replacing the absolute value by an arbitrary vector norm. Alternatively, one might test for changes in a single coordinate of .

B.3 Further simulation results

To further assess the finite sample performance of our proposed procedure, we study the regression model

for regression coefficients , and noise process as in equation (9) of the article, using and as specified, and autoregression coefficient . The cofactors are independent, bivariate normal random vectors, independent of , with covariance matrix

Here, we want to test for structural stability of the first regression coefficient , and we apply the CUSUM test as outlined in Section B.2. For our simulations, we employ the model with regression coefficients as null hypothesis, and , as alternatives, i.e. a gradual change.

| 0.16 | 0.14 | 0.15 | 0.08 | 0.06 | 0.08 | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | |

| 500 | 0.01 | 0.02 | 0.01 | 0.01 | 0.06 | 0.01 | 0.02 | 0.16 | 0.03 | 0.04 | 0.21 | 0.04 |

| 1000 | 0.01 | 0.10 | 0.01 | 0.02 | 0.28 | 0.04 | 0.04 | 0.41 | 0.07 | 0.04 | 0.45 | 0.09 |

| 5000 | 0.03 | 0.96 | 0.20 | 0.05 | 0.99 | 0.28 | 0.06 | 0.99 | 0.33 | 0.07 | 0.99 | 0.35 |

| 10000 | 0.05 | 1.00 | 0.46 | 0.06 | 1.00 | 0.53 | 0.07 | 1.00 | 0.58 | 0.08 | 1.00 | 0.58 |

The distribution of the bootstrap-based p-values under null hypothesis is depicted in Figure 4. Values of the test’s size and power are presented in Table 3, for different choices of the lag parameter . Just as for the autocorrelation, we find that our proposed test for the regression coefficient is conservative, and that the size approximation is better for smaller . As the sample size increases, the distribution of the p-values approaches the desired uniform distribution, and the size of the test tends towards the nominal level. This demonstrates the robustness of our test against non-stationary nuisance parameters. Furthermore, the CUSUM test consistently detects the nonstationarity of the regression coefficient as the sample size increases.

Appendix C Technical proofs

C.1 Equivalence of the physical dependence measure

Proposition C.1.

Let , be as in Section 2. Let be a measurable function, where we endow with the -Algebra generated by all finite projections. If for some , then

Proof of Proposition C.1.

Consider the martingale . Since , the martingale convergence theorem guarantees that that as . Now note that , such that we also obtain as and thus as . Hence, for any , and any ,

But . Thus, letting , we find that

∎

C.2 Asymptotics of partial sums

Proof of Theorem 2.1.

We exploit the geometric decay of the dependence measure (A.3) to employ a coupling construction. To this end, we split the observations into blocks of length and let . Furthermore, let with be a smaller block length. It turns out that the rates are appropriate, for some . We decompose

| (10) |

Consider the remainder term . By assumptions (A.1) and (A.2), we have for all . The union bound and Markov’s inequality yield, for any ,

Since , this term tends to zero for our choice of , since for .

In (10), the random variables , , may be replaced by independent copies as follows. For each , let be an independent copy of the . Then

for a random variable with , by virtue of (A.3). Note that the are independent and satisfy , for . Analogously, we may construct independent copies of , , such that . Hence,

The remainder term satisfies

which is asymptotically negligible since and , and .

We now establish a central limit theorem for the term . This result will also apply to the term with a different rate of convergence, and we will be able to conclude that the latter is negligible. To this end, consider

for some , using the boundedness of . Furthermore, condition (A.3) implies that . Hence, it can be checked that

for some , and . Thus, for any ,

| (11) |

The term tends to zero uniformly in because the are bounded, and . The third term may be bounded as

which tends to zero since by assumption, and .

To treat the term , we show that . First, we find that for and any ,

Both summands may be treated identically using (A.3). In particular, assuming w.l.o.g. ,

Hence,

| (12) |

which implies that . Moreover, we have that , because the same argument as above yields

| (13) |

Hence, we find that is bounded and of bounded -variation, uniformly in . The same holds for . This suffices to establish convergence of the Riemann sum in (11), since

By our choice of and , in particular , the latter term tends to zero. Moreover, uniformly in by the dominated convergence theorem. We have thus shown that

uniformly in . On the other hand, following the same steps, we can show that

which tends to zero by our choice of . Doob’s inequality thus yields that

in probability, as . Hence, , uniformly in .

To establish a central limit theorem, we verify Lyapunov’s condition. By our assumptions on , in particular convergence and bounded -variation in , we know that for some constant , uniformly in and . Hence,

| (14) |

since . This term tends to zero since by our choice of . Thus, the functional central limit theorem is applicable, see e.g. (Jacod and Shiryaev,, 2003, Thm. VIII.3.33). We obtain

∎

C.3 Properties of the local smoother

Proposition 3.1 is a consequence of the following two Lemmas.

Lemma C.2.

Let (A.3) hold for some . Let and choose such that . Then, as ,

Proof of Lemma C.2.

The union bound and Markov’s inequality yield, for any ,

| (15) |

To bound the latter norm, we apply Theorem 1 of Liu et al., (2013). The latter result is formulated for stationary time series of the type . However, the stationarity is only strictly required for the last equation of the proof therein, where we may replace by , which is bounded by virtue of (A.3) for . At all other occasions in the proof of Liu et al., (2013), only the quantity is relevant, which may be replaced in our nonstationary setting by

By assumption (A.3), we have . Hence, for our case, the bound of Liu et al., (2013) reads as follows: For all and all such that ,

for a factor which does not depend on nor . For the latter two inequalities, we used that and for , and the geometric decay of . Thus,

This term tends to zero if . We hence obtain the uniform convergence via the union bound (15). ∎

Lemma C.3.

Let (A.3) hold for some . Suppose that is -Hölder continuous with Hölder constant independent of . Then

If, instead of Hölder continuity, we assume that for some , then

Furthermore, if such that is -Hölder continuous with Hölder constant independent of , and , then

Proof of Lemma C.3.

Assume without loss of generality that the are scalar, i.e. . Otherwise, we may treat each component individually. We have

| (16) | ||||

The Hölder continuity of yields

Alternatively, if we only assume ,

Note that , which is bounded. The third case is obtained by a combination of the two previous bounds.

C.4 Functional central limit theorem for

Recall the decomposition , where

The first term is a discretized version of the integral , and its convergence depends on the regularity of the function . Assumption (A.2) implies , which may be used to treat the term as follows.

Lemma C.4.

For any function , it holds that

Proof of Lemma C.4.

It holds that

Regarding the term , note that for all , and large enough. Then the mean value theorem and the boundedness of on yield for any , such that . Thus, for large enough and for any such that ,

Moreover, since is bounded,

completing the proof. ∎

In particular, for and , we find that

The term may be treated directly by our assumptions on the nonparametric estimator , and using additionally the regularity of .

Lemma C.5.

Proof of Lemma C.5.

Assumption (A.1) implies that for sufficiently large, for all . Moreover, for all , with probability tending to one. Since is convex, we find that for all , with probability tending to one. On this event, it holds that

Moreover, if , boundedness of yields

If , we may apply Hölder’s inequality to obtain

This yields the claimed upper bound. ∎

The last term admits a functional central limit theorem with scaling factor , as shown in the following Lemma. Its proof follows the same ideas as the proof of Theorem 2.1, but additional care is needed when treating the random but consistent factor .

Lemma C.6.

Proof of Lemma C.6.

As in the proof of Theorem 2.1, we split the sum into blocks of size , and , for some arbitrarily small to be chosen in the sequel. We assume to be sufficiently large such that . Denote by the number of blocks.

Step (i): As a first step, we match the upper and lower limits of the sum with the block size . Define

By virtue of Lemma C.2 and (A.4), for all , with probability tending to one, such that

Since , the union bound and Markov’s inequality yield the upper bound . Using , we obtain

Since , we may choose sufficiently small such that the latter term is of order .

Step (ii): Next, we introduce , and

By virtue of assumption (A.6), we have in probability. Now, for each , let be an independent copy of the , and define

This construction yields that the and the are martingale differences, since is measurable w.r.t. , and since . It also holds that . Moreover, by virtue of (A.3), it holds that and . Now define the martingales

and note that

since , and , upon choosing sufficiently small.

Step (iii): Define the two sequences of filtrations , and . Then is an martingale, and is a martingale. The predictable quadratic variation of is given by

We observe that

where the last inequalities are a consequence of (A.3), and the boundedness of and on . Moreover,

| (19) |

In the proof of Lemma C.5, we have shown that , which tends to zero because by assumption. Hence, (19) tends to zero as , and we thus obtain

| (20) |

where the term vanishes uniformly in . Note that we may omit the indicators asymptotically by virtue of assumption (A.6). Analogously, we obtain

Step (iv): We further simplify the asymptotic expression for . In (20), we want to replace by . Observe that

By (A.2), and since the latter term is of order if is small enough. Hence,

| (21) |

The covariance term may be simplified as follows. Define

Note that (A.3) implies that for some constant , where denotes an arbitrary matrix norm. In particular, is well defined since the series is finite.

Now, for any , let . Since , we find that for ,

Therefore,

The latter term tends to zero upon choosing small enough, since . Note also that . Finally, since , we have shown that

| (22) |

where the last step holds because and due to the boundedness of and , which is in turn implied by (A.3) and (A.2) for . Note also that the term in (22) vanishes uniformly in .

Analogously, we may show that

using again the boundedness, and the fact that such that the number of summands is asymptotically negligible. This implies that by the Burkholder-Davis-Gundy inequality for martingales.

Observe that the function has bounded -variation, see (12). Moreover, has bounded -variation by assumptions (A.2) and (A.4). Since both and are bounded, we find that has bounded -variation. Thus, as in Lemma C.4,

Assumption (A.1) implies that and uniformly in . The latter uniform convergence holds because uniformly in , and by virtue of (A.3). Hence,

Step (v): Having at hand the limit of , a functional central limit theorem for holds if we can verify Lyapunov’s condition. We have, for any ,

where we used that is uniformly bounded. By choosing sufficiently small, and using , the latter term tends to zero. Hence, the functional central limit theorem for martingales, e.g. (Jacod and Shiryaev,, 2003, Thm. VIII.3.33), yields

In the previous steps, we have established that , which yields the desired result. ∎

C.5 Bootstrap inference

Theorem 3.3 is a special case of the following more general theorem about consistent estimation of the limiting variance. In contrast to the central limit theorem for , here, we only require the weaker assumption

| (C.5*) |

for some .

Theorem C.7.

Proof of Theorem C.7.

Step (i): As a first step, we are concerned with the estimators . We decompose

With probability tending to one, it holds that for all by virtue of (A.6). On this event, we may exploit the regularity and boundedness of such that

for . Now, via the inequality , we obtain

It thus suffices to show that

| (23) |

and

| (24) |

Step (ii): Regarding the term (23), we find that

| (25) | ||||

The second term may be bounded by noting that, for ,

In the second inequality, we used that , , and that is uniformly bounded due to (A.2). If , we find that

such that the second term in (25) is of order .

Concerning the first term in (25), we note that

Since , this yields

for some finite . An alternative upper bound, which is sharper for , is given by

such that

Thus, the union bound and Markov’s inequality yield that

Furthermore, as in the proof of Lemma C.5,

Plugging this into (25), we have thus shown that

For , this bound reduces to

which tends to zero by the assumptions , , and . For , we find that

which also tends to zero as .

Step (iii): It remains to study the term (24). Introduce the random variables

such that we are led to study the term . To bound the covariances of the , we write , such that (A.3) may be exploited. Let be an integer, and recall that

where the are an independent copy of the . Then

| via the inequality , | ||||

| by Hölder’s inequality, | ||||

In the last step, we used , the boundedness of due to (A.2), and the ergodicity (A.3).

Now consider such that . If , then is independent of , such that

These findings may be summarized as

| (26) |

In particular,

which tends to zero by assumption. Thus, as .

Step (iv): The expected value of may be computed as

using the geometric ergodicity (A.3) in the second step. Note that the remainder term is of order , uniformly in and , because for all , and large enough.

Just as in the proof of Lemma C.6, step (iv) therein, we find that

as . Moreover, since as , uniformly in , the dominated convergence theorem yields that

uniformly in . Furthermore, uniformly in , such that

Together with the variance bound derived in step (iii), this establishes (24) and thus completes the proof. ∎

Theorem 3.3 is a consequence of Theorem C.7 for . Regarding the bootstrap consistency, Theorem 3.4, note that is precisely the variance process of .

Proof of Theorem 3.4.

Conditionally on , is a zero mean Gaussian process with independent increments, and variance function for as in Theorem C.7. It may hence be represented as for a standard Brownian motion which is independent of . The uniform convergence of thus yields . This yields weak convergence of in probability. That is, for any probability metric which metricizes weak convergence on the Skorokhod space, we have , where denotes the measure induced by the random element . ∎

C.6 Properties of the tvVAR example

To show existence of the tvVAR process of Example 1, we want to show that , where denotes the Euclidean operator norm. If for all , this conclusion is obvious. However, the latter condition is too restrictive for many applications. For example, consider the univariate autoregressive process of order given by . This process may be represented as a tvVAR process with state vector , and autoregressive matrix

| (27) |

A typical condition for the stability of is that the autoregressive polynomial has no (complex) roots of absolute value smaller than , see e.g. (Giraud et al.,, 2015, Sec. 3.1.3). Equivalently, the spectral radius of is bounded by . On the other hand, we have for all , irrespective of the coefficients .

In view of the previous example, we do not restrict the Euclidean operator norm to be smaller than one. Instead, we impose an upper bound on the spectral radius of the matrices , i.e. . This comes at the price of requiring additional regularity of the mapping .

Lemma C.8.

Let , , be a sequence of matrices such that , and . Assume furthermore that for some ,

Then for any , there exists a such that

Proof of Lemma C.8.

We proceed as in the proof of (Giraud et al.,, 2015, Lemma 8). For any , we have

| (28) |

Here, we employ the convention if , i.e. the empty product is the identity matrix.

In the literature, results similar to Lemma C.8 have been established to show existence of the tvVAR model. The existing results are formulated for matrices for some function . In particular, (Moulines et al.,, 2005, Proposition 13) requires to be Hölder continuous, and Lemma 8 of Giraud et al., (2015) replaces Hölder continuity by some arbitrarily weak uniform continuity. Proposition 2.4 of Dahlhaus and Polonik, (2009) requires to be of bounded variation. The bounded -variation imposed in Lemma C.8 is weaker than the assumptions of Moulines et al., (2005) and Dahlhaus and Polonik, (2009). Compared to Giraud et al., (2015), we allow for discontinuities. On the other hand, Giraud et al. only require uniform continuity, without further restrictions on the modulus of continuity, which also includes some irregular continuous cases where for all .

Proposition C.9.

Let as in Example 1, with and , and suppose that the matrices have spectral radius for all .

-

1.

If , , and for some , then there exists some such that for all .

-

2.

If , , and are -Hölder continuous in the Euclidean operator norm , then there exists such that for all , the mapping is -Hölder continuous in with Hölder constant .

Proof of Proposition C.9.

Note that by assumption. In the sequel, the factor may vary from line to line. For any , we have

In the last step, we used Lemma C.8 for some . In the Hölder continuous case, Lemma C.8 is applicable because -Hölder continuity implies finite -variation. In the case of finite -variation, Lemma C.8 is directly applicable.

We now consider the regularity of . For any , we have

| (29) |

Now if , , and are -Hölder continuous with Hölder constants , , and , we find that

and the latter series are finite since .

Alternatively, we may treat the case of finite -variation. Let . Applying the Minkowski inequality to (29), we find obtain

Since , this completes the proof. ∎

C.7 Properties of the CUSUM test

Proof of Proposition 4.1.

By virtue of a result of Lifshits, (1983), see the Corollary on p. 606 therein, we find that the distribution of is absolutely continuous, apart from a potential atom at . Since for some , the variance structure of the process yields that . Due to the Gaussianity of , it holds that , such that . Hence, the cumulative distribution function is continuous. Denote furthermore by the (random) distribution function of the bootstrap approximation. We have to show that as , where denotes the quantile function corresponding to a cumulative distribution function .

Suppose to the contrary that , then for some , there exists a subsequence as such that . Since in probability, there exists a further subsequence, also denoted by , such that almost surely as . This implies that , for all where is continuous (Van der Vaart,, 1998, Lemma 21.2). Since is left-continuous and has at most countably many discontinuities, we find that

where denotes the right-hand limit. Since is continuous, we have , such that almost surely. Via the dominated convergence theorem, we obtain , completing the proof by contradiction. ∎

Proof of Proposition 4.2.

It holds that

By virtue of Theorem 3.2, . Moreover,

Now use that , uniformly in by virtue of the boundedness of . Since for all , we obtain

In the last step, we use Lemma C.4 and the fact that . Moreover, the convergence holds uniformly in . This establishes the convergence of .

∎

References

- Aït-Sahalia and Jacod, (2014) Aït-Sahalia, Y. and Jacod, J. (2014). High-Frequency Financial Econometrics. Princeton University Press, Princeton.

- Aït-Sahalia et al., (2011) Aït-Sahalia, Y., Mykland, P. A., and Zhang, L. (2011). Ultra high frequency volatility estimation with dependent microstructure noise. Journal of Econometrics, 160(1):160–175.

- Andersen et al., (2019) Andersen, T. G., Archakov, I., Cebiroglu, G., and Hautsch, N. (2019). Local Mispricing and Microstructural Noise: A Parametric Perspective. Technical report.

- Aue et al., (2009) Aue, A., Hörmann, S., Horváth, L., and Reimherr, M. (2009). Break detection in the covariance structure of multivariate time series models. The Annals of Statistics, 37(6B):4046–4087.

- Aue and Horváth, (2013) Aue, A. and Horváth, L. (2013). Structural breaks in time series. Journal of Time Series Analysis, 34(1):1–16.

- Aue et al., (2008) Aue, A., Horváth, L., Hušková, M., and Kokoszka, P. (2008). Testing for changes in polynomial regression. Bernoulli, 14(3):637–660.

- Baby and Wang, (2019) Baby, D. and Wang, Y.-X. (2019). Online forecasting of total-variation-bounded sequences. Advances in Neural Information Processing Systems, 32:11071–11081.

- Bauer and Hackl, (1978) Bauer, P. and Hackl, P. (1978). The Use of MOSUMS for Quality Control. Technometrics, 20(4):431.

- Berkes et al., (2009) Berkes, I., Gombay, E., and Horváth, L. (2009). Testing for changes in the covariance structure of linear processes. Journal of Statistical Planning and Inference, 139(6):2044–2063.

- Bickel and Ritov, (1988) Bickel, P. J. and Ritov, Y. (1988). Estimating Integrated Squared Density Derivatives: Sharp Best Order of Convergence Estimates. Sankhya: The Indian Journal of Statistics, Series A, 50(3):381–393.

- Billingsley, (1999) Billingsley, P. (1999). Convergence of probability measures. John Wiley & Sons.

- Carlstein, (1986) Carlstein, E. (1986). The Use of Subseries Values for Estimating the Variance of a General Statistic from a Stationary Sequence. The Annals of Statistics, 14(3):1171–1179.

- Chen and Gupta, (1997) Chen, J. and Gupta, A. K. (1997). Testing and Locating Variance Changepoints with Application to Stock Prices. Journal of the American Statistical Association, 92(438):739–747.

- Chu et al., (1995) Chu, C.-S. J., Hornik, K., and Kuan, C.-M. (1995). MOSUM Tests for Parameter Constancy. Biometrika, 82(3):603.

- Cui et al., (2020) Cui, Y., Levine, M., and Zhou, Z. (2020). Estimation and Inference of Time-Varying Auto-Covariance under Complex Trend: A Difference-based Approach. arXiv preprint 2003.05006.

- Dahlhaus, (1997) Dahlhaus, R. (1997). Fitting time series models to nonstationary processes. Annals of Statistics, 25(1):1–37.

- Dahlhaus, (2009) Dahlhaus, R. (2009). Local inference for locally stationary time series based on the empirical spectral measure. Journal of Econometrics, 151(2):101–112.

- Dahlhaus and Polonik, (2009) Dahlhaus, R. and Polonik, W. (2009). Empirical spectral processes for locally stationary time series. Bernoulli, 15(1):1–39.

- Dahlhaus and Richter, (2019) Dahlhaus, R. and Richter, S. (2019). Adaptation for nonparametric estimators of locally stationary processes. arXiv preprint 1902.10381.

- Dahlhaus et al., (2019) Dahlhaus, R., Richter, S., and Wu, W. B. (2019). Towards a general theory for nonlinear locally stationary processes. Bernoulli, 25(2):1013–1044.

- Demetrescu and Wied, (2018) Demetrescu, M. and Wied, D. (2018). Testing for constant correlation of filtered series under structural change. Econometrics Journal, 22:10–33.

- Dette and Gösmann, (2020) Dette, H. and Gösmann, J. (2020). A Likelihood Ratio Approach to Sequential Change Point Detection for a General Class of Parameters. Journal of the American Statistical Association, 115(531):1361–1377.

- Dette and Wu, (2019) Dette, H. and Wu, W. (2019). Detecting relevant changes in the mean of nonstationary processes—A mass excess approach. The Annals of Statistics, 47(6):3578–3608.

- Dette et al., (2019) Dette, H., Wu, W., and Zhou, Z. (2019). Change Point Analysis of Correlation in Non-stationary Time Series. Statistica Sinica, 29:611–643.

- Gao et al., (2019) Gao, Z., Shang, Z., Du, P., and Robertson, J. L. (2019). Variance Change Point Detection Under a Smoothly-Changing Mean Trend with Application to Liver Procurement. Journal of the American Statistical Association, 114(526):773–781.

- Giné and Nickl, (2016) Giné, E. and Nickl, R. (2016). Mathematical Foundations of Infinite-Dimensional Statistical Models. Cambridge University Press.

- Giraud et al., (2015) Giraud, C., Roueff, F., and Sanchez-Perez, A. (2015). Aggregation of predictors for nonstationary sub-linear processes and online adaptive forecasting of time varying autoregressive processes. The Annals of Statistics, 43(6):2412–2450.

- Górecki et al., (2018) Górecki, T., Horváth, L., and Kokoszka, P. (2018). Change point detection in heteroscedastic time series. Econometrics and Statistics, 7:63–88.

- Gösmann et al., (2021) Gösmann, J., Kley, T., and Dette, H. (2021). A new approach for open‐end sequential change point monitoring. Journal of Time Series Analysis, 42:63–84.

- Grenier, (1983) Grenier, Y. (1983). Time-dependent arma modeling of nonstationary signals. IEEE Transactions on Acoustics, Speech, and Signal Processing, 31(4):899–911.

- Hall and Marron, (1987) Hall, P. and Marron, J. S. (1987). Estimation of integrated squared density derivatives. Statistics and Probability Letters, 6(2):109–115.

- Hansen and Lunde, (2006) Hansen, P. R. and Lunde, A. (2006). Realized Variance and Market Microstructure Noise. Journal of Business & Economic Statistics, 24(2):127–161.

- Horváth, (1995) Horváth, L. (1995). Detecting changes in linear regressions. Statistics, 26(3):189–208.

- Horváth et al., (2004) Horváth, L., Hušková, M., Kokoszka, P., and Steinebach, J. (2004). Monitoring changes in linear models. Journal of Statistical Planning and Inference, 126(1):225–251.

- Hsu et al., (1974) Hsu, D.-A., Miller, R. B., and Wichern, D. W. (1974). On the stable paretian behavior of stock-market prices. Journal of the American Statistical Association, 69(345):108–113.

- Huang and Jianqing, (1999) Huang, L. S. and Jianqing, F. A. (1999). Nonparametric estimation of quadratic regression functionals. Bernoulli, 5(5):927–949.

- Inclán and Tiao, (1994) Inclán, C. and Tiao, G. C. (1994). Use of Cumulative Sums of Squares for Retrospective Detection of Changes of Variance. Journal of the American Statistical Association, 89(427):913–923.

- Jacod et al., (2009) Jacod, J., Li, Y., Mykland, P. A., Podolskij, M., and Vetter, M. (2009). Microstructure noise in the continuous case: The pre-averaging approach. Stochastic Processes and their Applications, 119(7):2249 – 2276.

- Jacod et al., (2017) Jacod, J., Li, Y., and Zheng, X. (2017). Statistical properties of microstructure noise. Econometrica, 85(4):1133–1174.

- Jacod and Rosenbaum, (2013) Jacod, J. and Rosenbaum, M. (2013). Quarticity and other functionals of volatility: Efficient estimation. The Annals of Statistics, 41(3):1462–1484.

- Jacod and Shiryaev, (2003) Jacod, J. and Shiryaev, A. N. (2003). Limit Theorems for Stochastic Processes, volume 288 of Grundlehren der mathematischen Wissenschaften. Springer, Berlin, Heidelberg.

- Juhl and Xiao, (2009) Juhl, T. and Xiao, Z. (2009). Tests for changing mean with monotonic power. Journal of Econometrics, 148(1):14–24.

- Killick et al., (2013) Killick, R., Eckley, I. A., and Jonathan, P. (2013). A wavelet-based approach for detecting changes in second order structure within nonstationary time series. Electronic Journal of Statistics, 7(1):1167–1183.

- Lee and Park, (2001) Lee, S. and Park, S. (2001). The Cusum of Squares Test for Scale Changes in Infinite Order Moving Average Processes. Scandinavian Journal of Statistics, 28(4):625–644.

- Li and Zhao, (2013) Li, X. and Zhao, Z. (2013). Testing for changes in autocovariances of nonparametric time series models. Journal of Statistical Planning and Inference, 143(2):237–250.

- Lifshits, (1983) Lifshits, M. A. (1983). On the absolute continuity of distributions of functionals of random processes. Theory of Probability & Its Applications, 27(3):600–607.

- Liu et al., (2013) Liu, W., Xiao, H., and Wu, W. B. (2013). Probability and moment inequalities under dependence. Statistica Sinica, 23:1257–1272.

- Moulines et al., (2005) Moulines, E., Priouret, P., and Roueff, F. (2005). On recursive estimation for time varying autoregressive processes. The Annals of Statistics, 33(6):2610 – 2654.

- Page, (1954) Page, E. (1954). Continuous Inspection Schemes. Biometrika, 41(1/2):100–115.

- Page, (1955) Page, E. (1955). A Test for a Change in a Parameter Occurring at an Unknown Point. Biometrika, 42(3/4):523–527.

- Pešta and Wendler, (2020) Pešta, M. and Wendler, M. (2020). Nuisance-parameter-free changepoint detection in non-stationary series. TEST, 29:379–408.

- Potiron and Mykland, (2020) Potiron, Y. and Mykland, P. (2020). Local Parametric Estimation in High Frequency Data. Journal of Business & Economic Statistics, 38(3):679–692.

- Preuss et al., (2015) Preuss, P., Puchstein, R., and Dette, H. (2015). Detection of Multiple Structural Breaks in Multivariate Time Series. Journal of the American Statistical Association, 110(510):654–668.

- Raj et al., (2020) Raj, A., Gaillard, P., and Saad, C. (2020). Non-stationary online regression. arXiv preprint 2011.06957.

- Robbins et al., (2016) Robbins, M. W., Gallagher, C. M., and Lund, R. B. (2016). A General Regression Changepoint Test for Time Series Data. Journal of the American Statistical Association, 111(514):670–683.

- Schick and Wefelmeyer, (2004) Schick, A. and Wefelmeyer, W. (2004). Root n consistent density estimators for sums of independent random variables. Journal of Nonparametric Statistics, 16(6):925–935.

- Schmidt et al., (2020) Schmidt, S., Wornowizki, M., Fried, R., and Dehling, H. (2020). An Asymptotic Test for Constancy of the Variance under Short-Range Dependence. arXiv preprint 2002.10178.

- Shao and Zhang, (2010) Shao, X. and Zhang, X. (2010). Testing for change points in time series. Journal of the American Statistical Association, 105(491):1228–1240.

- Steland, (2020) Steland, A. (2020). Testing and estimating change-points in the covariance matrix of a high-dimensional time series. Journal of Multivariate Analysis, 177:104582.

- Subba Rao, (1970) Subba Rao, T. (1970). The fitting of non-stationary time-series models with time-dependent parameters. Journal of the Royal Statistical Society. Series B (Methodological), 32(2):312–322.

- Truquet, (2019) Truquet, L. (2019). Local stationarity and time-inhomogeneous Markov chains. The Annals of Statistics, 47(4):2023–2050.

- van de Geer, (2010) van de Geer, S. (2010). Empirical Processes in M-Estimation. Cambridge University Press.

- Van der Vaart, (1998) Van der Vaart, A. W. (1998). Asymptotic statistics. Cambridge University Press.