Distribution-Free Joint Independence Testing and Robust Independent Component Analysis Using Optimal Transport

Abstract.

In this paper, we study the problem of measuring and testing joint independence for a collection of multivariate random variables. Using the emerging theory of optimal transport (OT)-based multivariate ranks, we propose a distribution-free test for multivariate joint independence. Towards this we introduce the notion of rank joint distance covariance , the higher-order rank analogue of the celebrated distance covariance measure, which can capture the dependencies among all the subsets of the variables. The can be easily estimated from the data without any moment assumptions and the associated test for joint independence is universally consistent. We derive the asymptotic null distribution of the estimate, using which we can readily calibrate the test without any knowledge of the (unknown) marginal distributions (due to the distribution-free property). We also provide an efficient data-agnostic resampling-based implementation of the test which controls Type-I error in finite samples and is consistent with only a fixed number of resamples. In addition to being distribution-free and universally consistent, the proposed test is also statistically efficient, that is, it has non-trivial asymptotic (Pitman) efficiency (power against alternatives). We demonstrate this by computing the limiting local power of the test for both mixture alternatives and joint Konijn alternatives. We then use the measure to develop a new method for independent component analysis (ICA) that is easy to implement and robust to outliers and contamination. Extensive simulations are performed to illustrate the efficacy of the proposed test in comparison to other existing methods. Finally, we apply the proposed method to learn the higher-order dependence structure among different US industries based on stock prices. As a byproduct of our theoretical analysis, we develop a version of Hoeffding’s classical combinatorial central theorem for mutiple independent permutations and a multivariate Hájek representation result for joint rank statistics, which might be of independent interest.

Key words and phrases:

Asymptotic efficiency, combinatorial central limit theorem, distance correlation, joint dependence measures, multivariate ranks, optimal transport, Stein’s method.1. Introduction

Given probability distributions on with marginal laws , respectively, and joint law on , where , the mutual independence testing problem is given by

| (1.1) |

where is the product of the marginal distributions . This has been extensively studied in the case , which is the classical pairwise independence testing problem for a collection of random variables. For univariate distributions, that is, , nonparametric tests for pairwise independence begin with the celebrated results of Hoeffding [37] and Blum et al. [7]. These tests are distribution-free, that is, the distributions of the test statistics under do not depend on the (unknown) marginal distributions, and consistent against a general class of alternatives. Since then a slew of methods for measuring and testing univariate pairwise independence have been proposed. These include, among several others, results of Yanagimoto [75], Feuerverger [21], Bergsma and Dassios [5], Nandy et al. [56], Heller et al. [36] and the recent breakthrough of Chatterjee [14, 15].

Pairwise independence testing is more challenging for dimensions greater than 1, that is, either or , because of the lack of a natural ordering in multivariate data. One of the most popular methods for pairwise multivariate independence testing is the celebrated distance covariance () of Székely et al. [70] and Székely and Rizzo [69], which measures dependence between 2 random vectors based on the difference of their joint and marginal characteristic functions and can be estimated using the correlation among the pairwise distances. The distance covariance is zero if and only if the null hypothesis of independence holds, provided and have finite first moments. Another approach is based on the Hilbert-Schmidt independence criterion (HSIC), which also provides a consistent kernel-based test for pairwise independence (see Gretton et al. [28, 27, 29]). Sejdinovic et al. [65] showed that distance covariance and the kernel-based independence criterion are, in fact, equivalent if the kernel is chosen based on the relevant distance function. Other popular methods include mutual information-based tests [2, 6, 43, 74], graph-based methods [19, 34, 22], the maximal information coefficient [61], ranking of interpoint distances [35, 55], ball covariance [58], and binning approaches based on partitions of the sample space [35, 50, 77] (see [41, 49] for reviews of the various methods). However, none of the aforementioned multivariate tests simultaneously inherit the distribution-free and universal consistency properties of the rank-based univariate tests. A breakthrough in this direction was made recently by Deb and Sen [18] and Shi et al. [67] using optimal transport (OT) based multivariate ranks [16, 31, 30]. The OT-based tests for pairwise independence are distribution-free in finite samples, computationally feasible, universally consistent (that is, the power of the tests converge to 1 as the sample size increases), and enjoy attractive efficiency properties [68] (see also [20, 50]).

In this paper we consider the mutual independence testing problem (1.1) for more than 2 variables. Measuring and testing higher-order dependence111We say a collection of random variables has higher-order dependency if they are pairwise independent but not jointly independent. and understanding the dependence structure between the variables are much more involved tasks than detecting pairwise dependence. Examples of such higher-order dependencies abound in the literature. This includes, among others, applications in diagnostic checking for directed acyclic graphs (DAGs), where the noise variables are assumed to be jointly independent, hence inferring pairwise independence is not enough, and independent component analysis (ICA), which entails finding a suitable transformation of multivariate data with mutually independent components (see Section 5 for details). In fact, Böttcher [8] collects over 350 datasets featuring statistically significant higher-order dependencies. While there are a few results for mutual independence testing in the univariate case, where (see [4, 17, 23, 42, 60] and the references therein), in higher dimensions the problem is much more challenging. Towards this, Pfister et al. [59] generalized the HSIC to multiple variables and obtained kernel-based tests joint independence (see also Sejdinovic et al. [64] for a kernel-based 3-variable interaction test). Recently, Böttcher et al. [9] and Chakraborty and Zhang [12] proposed higher-order generalizations of the distance covariance, which provide consistent tests for multivariate joint independence. This is referred to as the total distance multivariance by Böttcher et al. [9] or the joint distance covariance () by Chakraborty and Zhang [12]. One of the attractive properties of the distance multivariance/ is that it has a hierarchical structure that can capture the dependence among any subset of the variables. Recently, Roy et al. [63] proposed tests for joint independence based on pairwise distances and linear projections (see also Banerjee and Ghosh [3] for generalizations to functional data). However, none of the aforementioned methods possesses the distribution-free property of the univariate methods. In fact, these tests usually have intractable (non-Gaussian) asymptotic distributions under that depend on the (unknown) marginal distributions and are generally calibrated using permutation methods.

In this paper we propose a distribution-free test for joint independence using the framework of OT-based multivariate ranks. Towards this, we introduce the notion of rank joint distance covariance , the rank analogue of the , which is obtained by aggregating the (higher-order) rank distance covariances () over all the subsets of variables (Section 2.4). The higher-order characterizes the mutual independence of a subset of variables given their lower-order independence and the characterizes the total mutual independence of all the variables (Proposition 2.10). The and, hence, the can be consistently estimated from data without any moment assumptions (Theorem 2.12). Consequently, since OT-based multivariate ranks are themselves distribution-free (see Section 2.3), we can construct a distribution-free test for multivariate joint independence based on the estimated . The proposed test has the following properties:

-

•

Distribution-free, universally consistent tests: Since is well-defined whenever the marginal distributions are absolutely continuous and is zero if and only if the null hypothesis of joint independence holds, our proposed test is consistent whenever the joint distribution has absolutely continuous marginals (Proposition 3.2). Moreover, we can use the estimates to obtain distribution-free, universally consistent tests for higher-order independence of a subset of variables given their lower-independence. For example, if a collection variables are pairwise independent, the measure can be used to construct distribution-free, consistent tests for 3-way or higher-order dependence (see Remark 3.3 for a discussion and Section 7 for an application in real data).

-

•

Asymptotic null distribution: In Section 3.1 we derive the limiting distribution of the proposed test under the null hypothesis of joint independence. In fact, we derive the limiting joint distribution of the estimates for all the subsets of variables, which can be expressed as a squared integral of a certain Gaussian process or, equivalently, as an infinite weighted sum of independent chi-squared distributions (Theorem 3.7). One remarkable property of the limiting distribution is that the distributions of the estimates across the various subsets are asymptotically independent, thereby facilitating the hierarchical testing for higher-order dependence mentioned above. Since the OT-based multivariate ranks are distributed as uniform random permutations, the estimates can be expressed as a combinatorial sum indexed by multiple (more than 1) independent permutations. For this we use Stein’s method based on exchangeable pairs to develop a version of Hoeffiding’s classical combinatorial central limit theorem for multi-dimensional arrays (tensors) indexed by independent permutations (see Theorem A.1 in Appendix A), a result which might be of independent interest. The distribution-free property implies that the asymptotic null distribution of the test statistic does not depend on the distribution of the data generating mechanism, hence, can be readily used to calibrate the test statistic.

-

•

Finite sample properties: The distribution-free property also allows us to approximate the quantiles of the null distribution in finite samples using a data-agnostic resampling technique. Consequently, we can calibrate the test statistic to have finite sample level (Section 3.2). Interestingly, this finite sample implementation is consistent with only a finite number of resamples (Theorem 3.11). Hence, we can implement the proposed test both asymptotically and in finite samples efficiently, without having to estimate any nuisance parameters of the marginal distributions or use computationally intensive data-dependent permutation techniques to approximate the rejection thresholds.

-

•

Asymptotic efficiency: In Section 4 we establish the asymptotic (Pitman) efficiency of the proposed test by computing its limiting power for local contiguous alternatives (alternatives shrinking towards at rate ) [71]. Specifically, we derive the asymptotic distribution of the proposed test for two kinds of local alternatives: mixture alternatives (Theorem 4.1) and joint Konijn alternatives (Theorem 4.4). To the best of our knowledge, these are the first results on the efficiency properties of nonparametric joint independence tests. This implies that the proposed test, in addition to being distribution-free, universally consistent, and computationally feasible, is also statistically efficient, making it particularly attractive for modern data applications. The proof of the local power analysis is based on a Hajék representation result for the estimates (Proposition 4.5), which allows us to replace the empirical rank maps with their population counterparts without altering the limiting distribution of the test statistic under .

Going beyond hypothesis testing, the can be used more generally to quantify deviations from joint independence. Specifically, in Section 5 using the measure as an objective function we develop a new method for the independent component analysis (ICA) problem that is robust to outliers and contamination. ICA is a method for extracting independent components from multivariate data that emerged from research in artificial neural networks and has found applications in blind source separation, feature extraction, computational biology, and time series analysis (see [39] for a review). Our estimator, which is obtained by minimizing the measure, can be computed efficiently and is consistent for the independent components (Theorem 5.2). We illustrate the effectiveness of the proposed ICA estimator with the approach of Matteson and Tsay [52] based on the in various simulation settings (Section 6.4).

In Section 6 we compare the performance of the proposed test with other popular tests for joint independence, such the dHSIC [59], [12], and the based measure in [52]. Our test performs well across a variety of data distributions and is especially powerful compared to the existing tests in contamination models and heavy-tailed distributions.

Finally, in Section 7 we apply our method to a dataset consisting of stock prices of different companies in USA. Our approach sheds more insights into the structure of the higher-order dependencies in this data, producing results that are more interpretable than existing methods. All the implementation of tests can be found in GitHub.

2. Rank-Based Joint Independence Measures

In this section, we define a rank-based measure of joint independence by combining higher-order distance covariances with optimal transportation of measures. We review the relevant concepts regarding higher-order distance covariance and joint dependence measures in Section 2.2 and OT-based multivariate ranks in Section 2.3. The rank-based joint dependence measures are introduced in Section 2.4 and their estimation is discussed in Section 2.5. We begin by introducing some notations.

2.1. Notations

Fix and suppose is a random vector, where each is a random variable taking values in , for and . The characteristic function of will be denoted by

for .

Definition 2.1.

The random vector is said to be -independent (for some ) if for any sub-family the random variables are mutually independent.

Throughout we will denote

for . Moreover, for define

| (2.1) |

Finally, for , let and denote the collection of all probability distributions and Lebesgue absolutely continuous probability distributions on , respectively.

2.2. Higher-Order Distance Covariance and Joint Dependence Measures

The celebrated distance covariance of Székely and Rizzo [70] is a powerful measure for independence between two random vectors. It has been widely used for testing of independence [70, 66], feature screening [48] and general association analysis, including canonical component analysis [79] and independent component analysis [52]. Recently, there has been efforts to generalize the notion of beyond pairwise independence to joint independence of a collection of random vectors. Towards this, independently and concurrently, Böttcher et al. [9] and Chakraborty and Zhang [12] proposed the following higher-order generalization of . This is referred to as the distance multivariance (by Böttcher et al. [9]) or the -th order (by Chakraborty and Zhang [12]).

Definition 2.2 ([9, Definition 2.1] and [12, Definition 1]).

The -th order of is defined as the positive square root of

| (2.2) |

where for , and is as defined in (2.1).

Clearly, whenever the collection are mutually independent. However, the converse is only true for , in which case (2.2) reduces to the classical between two random vectors and [70]. In other words, when the joint independence of is not a necessary condition for to be zero. (For example, whenever .) One can conclude are jointly independent when under the additional assumption that are -independent (see Definition 2.1 and [9, Theorem 3.4]), but not in general. To characterize joint independence one has to consider all possible interactions between the variables . This leads to the notion of the total distance multivariance [9] or the joint distance correlation () [12]. Towards this, we need the following notation: For with denote by and

| (2.3) |

where . In other words, is the -th order for the variables in .

Definition 2.3 ([12, Definition 2]).

Given a vector non-negative weights , the joint distance covariance of the random vector is defined as:

| (2.4) |

completely characterizes the joint independence of , that is,

| (2.5) |

(see [12, Proposition 3]). Moreover, by choosing all the weights to be equal, that is, , for , one gets the total distance multivariance as in [9, Definition 2.1]. Chakraborty and Zhang [12] suggests choosing , for some constant , which allows the following simplier expression that does not require evaluating all the dCov terms in (2.4).

Lemma 2.4 (Proposition 4 in [12]).

For any ,

where be an independent copy of and, for ,

Depending on whether or , puts more or less weights on the lower-order dependence terms, respectively. For example, if the joint distribution of is known to be Gaussian, where mutual independence is equivalent to pairwise independence, larger values of should be considered. Otherwise, a smaller makes more sense.

2.3. Multivariate Ranks Based on Optimal Transport

To motivate the notion of multivariate ranks based on optimal transport, let us recall some fundamental facts about univariate ranks. Suppose that is a random variable with distribution function . Here, the distribution function itself serves as the one-dimensional population rank function, which has the property that , that is, transports to , the uniform distribution on . In fact, when has finite second moment, it can be shown that is the almost everywhere unique map that transports to and minimizes the expected squared-error cost, that is,

where the minimization is over all functions that transport the distribution of to the uniform distribution on . This shows that in dimension 1, ranks can be thought of as the univariate analogue of the celebrated Monge transportation problem [54, 73]. Hallin et al. [31, 30] used this interpretation of ranks and proposed the following multivariate generalization.

Definition 2.5 ([18, 31, 30]).

Given a random variable and a pre-specified reference distribution , with , the multivariate population rank map is defined as:

| (2.6) |

where the minimum is over all functions that transports the distribution of to and denotes the usual Euclidean norm in .222Note that, even though the definition in (2.6) is not meaningful when does not have finite second moment, OT-based multivariate ranks can still be defined using the Brenier-McCann theorem [53, 10], which says that there exists an almost everywhere unique map , which is the gradient of a convex function and satisfies . This notion coincides with that in Definition 2.5, whenever and have finite second moment.

To define the empirical analogue of the population multivariate rank we begin with a ‘natural’ discretization of the pre-specified reference distribution , that is, the empirical measure converges converges weakly to . The natural choice for is , whose empirical distribution converges to . For higher dimensions one can choose as i.i.d. points from or, more commonly, a deterministic quasi-Monte Carlo sequence such as the Halton sequence [18, 38]. Then, given i.i.d. samples from a distribution , the multivariate empirical rank map is the optimal transport map from the empirical distribution of the data to . In other words,

| (2.7) |

where

and denotes the set of all permutations of . This is a minimum bipartite matching problem (also known as the assignment problem), which is a fundamental problem in combinatorial optimization that can be solved exactly time [40] and approximately in near-linear time (see [1] and the references therein).

A remarkable feature of the optimal transport based multivariate empirical ranks defined in (2.7) is that they mimic the distribution-free property of univariate ranks [18, 31].

Proposition 2.6 ([31, Proposition 1.6.1] and [18, Proposition 2.2]).

Suppose that are i.i.d. samples from a distribution . Then the vector of empirical ranks

is uniformly distributed over the permutations of the fixed grid .

The result above suggests a general strategy for constructing non-parametric distribution-free tests, by replacing the data points with their empirical ranks (appropriately defined depending on the testing problem). This strategy was recently adopted in [18, 67] to construct distribution-free, computationally efficient, and universally consistent multivariate two-sample and independence tests. For other interesting properties and applications of optimal transport based ranks see [16, 24, 33, 32] and the references therein.

Remark 2.7.

Common choices of the reference distribution are , the uniform distribution on the -dimensional cube [18], the spherical uniform distribution , which is the product of the uniform distribution on and the uniform distribution on the unit sphere [30, 67], and , the -dimensional standard Gaussian [20]. Hereafter, for concreteness we will choose and will denote the Halton sequence corresponding to this distribution. However, our results continue to hold for any reference distribution with finite moments, which, in particular, includes the spherical uniform and the standard multivariate Gaussian.

2.4. Rank-Based Joint Dependence Measures

We are now ready to define the rank-based counterparts of the -th order and . Towards this, suppose, as before, is a -dimensional random vector, where each is a random variable taking in with distribution , for and . Throughout we will assume and denote the population rank map of by (recall Definition 2.5), for .

Definition 2.8.

The -th order rank of is defined as the positive square root of

| (2.8) |

where , for , and is as defined in (2.1).

Note that the -th order is obtained from the -th order by replacing with their population rank maps . For , (2.8) reduces to the rank distance covariance of defined in [18, 67], which, like the classical , is zero if and only if . For the , as in , we need to consider all the interactions between the variables to characterize the joint indepedence. This leads to our the notion of rank joint distance covariance ():

Definition 2.9.

Given a vector non-negative weights , the rank joint distance covariance of the random vector is defined as:

| (2.9) |

where

| (2.10) |

Moreover, for any ,

| (2.11) |

Note that .

As in Lemma 2.4, has the following compact representation:

| (2.12) |

where be an independent copy of and, for ,

| (2.13) |

Note that are i.i.d. when the variables are mutually independent (by the definition of the optimal transport maps). Therefore, the distribution of does not depend on the marginal distributions of under mutual independence. Moreover, characterizes the joint independence of .

Proposition 2.10.

Proof.

Note that are independent when are mutually independent, which implies , by definition. For the converse, note that and are independent implies are mutually independent by [9, Theorem 3.4]. Then, since , by McCann’s theorem [53] (see also [18, Proposition 2.1]) there exists a measurable function such that almost everywhere , for . This implies, are mutually independent. This completes the proof of (1).

For (2) note that if and only if for all with . The result then follows from (1). ∎

2.5. Consistent Estimation of

In this section we discuss how and can be consistently estimated given samples i.i.d. , with , from a distribution . The natural plug-in estimator of , for with , is:

| (2.14) |

where is the empirical rank map for the -th marginal distribution, that is, the optimal transport map from to , with the Halton sequence in , for . Using the representation in (2.12) and (2.13) the estimate in (2.14) can be written as:

| (2.15) |

where

| (2.16) |

for . Consequently, the natural plug-in estimate of (2.9) is

| (2.17) |

and that of (2.11) (using the representation in (2.12) is

Remark 2.11.

For with , consider the function

| (2.18) |

where , for and, hence, , for . Evaluating at the data points gives us the natural plug-in estimate of (recall (2.3)) which is denoted by:

where , for . On the other hand, evaluating on the the rank transformed data gives us the estimate of in (2.14). Specifically, recalling (2.14) note that

| (2.19) |

where , for . The function will play an important role in the calibration of the independence tests on discussed in Section 3.

To establish the consistency of we will assume the following:

Assumption 1.

For every , the empirical distribution of converges weakly to .

As mentioned before, Assumption 1 holds whenever is the Halton sequence in (which is our default choice), for a random sample i.i.d. points, or other quasi-Monte Carlo sequences as well (see [18, Appendix D] for a discussion on the various of choices ). Under this assumption we have the following result:

Theorem 2.12.

The proof of Theorem 2.12 is given in Appendix B. One of the highlights of the above result is that it holds without any moment assumptions on the data generating distribution. This is in contrast to consistency results for which require the distribution to satisfy certain moment conditions. Consequently, the rank-based joint dependence measures are more robust to heavy-tail distributions, as will been seen from the simulations in Section 6.

3. Distribution-Free Joint Independence Testing

In section we discuss new distribution-free tests for the multivariate joint independence testing. Given i.i.d.samples , with , from a distribution with marginal distributions such that , for , consider the joint independence testing problem:

| (3.1) |

Our test for (3.1) will be based on rejecting for ‘large’ values of , for a given choice non-negative weights . Note that the vector of ranks are distributed uniformly over the permutations of , for (by Proposition 2.6) and under independent over . Hence, the distribution of under does not depend on the marginal distributions .

Proposition 3.1 (Distribution-freeness under ).

Under , the distribution of is universal, that is, it is free of .

The above result automatically gives a finite sample distribution-free independence test that uniformly controls the Type-I error for (3.1). To this end, fix a level and let denote the upper quantile of the universal distribution in Proposition 3.1. Consider the test function:

| (3.2) |

This test is exactly distribution-free for all and uniformly of level under ,333Strictly speaking, to guarantee exact level , we have to randomize , as the exact distribution of is discrete. However, this makes no practical difference unless is very small. that is,

| (3.3) |

Moreover, since is a consistent estimate of , which characterizes joint independence, the test is consistent against all fixed alternatives. This is summarized in the following proposition (see Appendix B for the proof).

Proposition 3.2 (Universal consistency).

Suppose Assumption 1 holds. Then the test is universally consistent, that is, for any ,

| (3.4) |

Remark 3.3.

Note that, while provides a distribution-free, universally consistent test for joint independence, the individual can be used for testing the joint independence of the subset of variables given that they are independent. This is because if and if only if the variables are mutually independent, provided they are independent. For example, if we are interested in testing pairwise independence:

then the test which rejects for ‘large’ values of

will be distribution-free and consistent. This is, in fact, the rank-analogue of the test based on pairwise distance covariances studied in [76]. Similarly, if we know that 3 variables are pairwise independent, then can be used to obtain a distribution-free, consistent test for the mutual independence of . Another attractive property of is that the collection is asymptotically independent over under the null hypothesis of joint independence (see Theorem 3.7), which can be leveraged to learn the higher-order dependencies among the variables .

Remark 3.4.

As mentioned in the Introduction, another related measure for joint independence based on the second-order was proposed by Matteson and Tsay [52], and its rank version was discussed in [18]. Although these measures characteristic joint independence, unlike it is unable to capture the dependence structure among the variables. In Section 6 we compare our method with test proposed in [52] in simulations.

3.1. Asymptotic Null Distribution

In this section we will derive the asymptotic null distribution of the collection of random variables:

| (3.5) |

where , and consequently that of . To describe the limit we need the following definition:

Definition 3.5.

Denote by a collection of mutually independent complex-valued Gaussian processes such that, for each ,

| (3.6) |

a complex-valued Gaussian process indexed by (recall ) with zero mean and covariance function:

| (3.7) |

where

-

•

and , with , for , and

-

•

are independent with , for .

Remark 3.6.

The covariance function (3.7) can be expressed in closed form using the fact,

for and . Hence,

where and .

With the above definition we can now describe the asymptotic distribution of the collection (3.5) under the null hypothesis of joint independence.

Theorem 3.7.

The proof of Theorem 3.7 is given in Appendix C. One of the challenges in dealing with and is that they are functions of dependent multivariate ranks. To solve the problem, we develop a version of the classical Hoeffiding’s combinatorial central limit theorem for -tensors indexed by multiple independent permutations (see Theorem A.1 in Appendix A), a result which might be more broadly useful in the analysis of other nonparametric tests. Our proof of the combinatorial CLT uses Stein’s method based on exchangeable pairs, combined with techniques from empirical process theory gives us the result in Theorem 3.7.

Remark 3.8.

(Equivalent representation of the limiting distribution) By considering the process as a random element in and an eigen-expansion of the integral operator on associated with the covariance kernel (3.7) the limit in (3.8) can be expressed as:

where are positive constants and are i.i.d. (see [46, Chapter 1, Section 2]). Hence, by the independence of the processes , the limit in (3.9) can be represented as an infinite sum weighted chi-squares:

for a sequence of positive constants and are i.i.d. .

Remark 3.9.

Another interesting consequence of Theorem 3.7 is that collection is asymptotically independent. This can be attributed to the representation of as a product of zero mean (under ) random variables (recall (2.14)). This property is shared by the (equivalently, the distance multivariance) which has a similar product structure (see [9, Theorem 4.10]).

3.2. Approximating the Cut-off and Finite Sample Properties

Note that the limit in (3.8), as expected, does not depend on the distribution of the data or the specific choices of . This is a manifestation of the distribution-free property of the multivariate ranks. Hence, if denotes the -th quantile of the distribution in the RHS of (3.9), the test which rejects when

| (3.10) |

will have asymptotic level and universally consistent for the hypothesis (3.1). Although this test is asymptotically valid, there is, in general, no tractable form of the quantile for the distribution (3.9). Nevertheless, using the distribution-free property of the multivariate ranks we can still approximate the quantiles of (3.8) (and consequently (3.9)) in a data-agnostic manner. This is because is a function of the multivariate ranks (recall (2.14) and (2.19)), and the ranks are independent and the uniformly distributed over the permutations of , for (by Proposition 2.6). Therefore, we can compute an approximate quantiles of as follows: For repeat the following two steps:

-

Generate i.i.d. uniform random permutations from .

-

Compute the value of the statistic on the permuted Halton sequences , where

for . More precisely, we evaluate

(3.11) where is the function in (2.18) and , for .

Then the permutation -th quantile of is obtained as:

| (3.12) |

To compute the permutation -value, let be the rank of (the original value computed from the data) in the sequence

by breaking ties at random and where denotes the rank of the largest element. Then the permutation -value as . Note that if is true, . In other words,

| (3.13) |

is a finite sample level test.

Remark 3.10.

Note that the resampling method described above is different from the (data-dependent) bootstrap/permutation method used to calibrate , or other independence tests which are not distribution-free), where the asymptotic distribution depends on the (unknown) marginal distributions of (see [12, Proposition 9]). On the other hand, our method can be used to compute the cut-offs by only permuting the Halton sequences, without any knowledge of the data, and hence is much more efficient when one has to do multiple tests.

Although (3.13) produces a test which has level in finite samples, its power properties with a finite number of permutations is a-priori unclear. This is due to fact that for any collection of random permutations , the RHS of (3.11) tends to zero with high probability (see Proposition D.1 in Appendix D). This combined with Theorem 2.12 leads to the following result:

Theorem 3.11 (Consistency with finite number of resamples).

Suppose Assumption 1 holds. Fix and suppose . Then, for any fixed ,

4. Local Power Analysis

In this section, we derive the asymptotic local power of the statistic under the contiguous alternatives. In the context of testing pairwise independence two types of local alternatives have been considered in the literature: (1) mixture alternatives [20, 68] and (2) Konijn alternatives which was originally proposed in [44] and has been later investigated in [26] and used more recently in [20, 68]. To the best of our knowledge, local power analysis has not been carried out for joint independence testing of more than 2 variables. The first step towards this is to define contiguous versions of the mixture and Konijn alternatives for multiple random vectors. For this suppose the joint distribution has density with respect to the Lebesgue measure in and the marginal distributions have densities with respect to the Lebesgue measures in , respectively.

4.1. Mixture Alternatives

The mixture alternatives constructed as follows: Given a consider the following mixture density in :

where for , , and is a probability density function with respect to the Lebsegue measure in such that the following holds:

Assumption 2.

The support of is contained in that of and

where the expectation is taken under , that is, .

Under this assumption contiguous local alternatives are obtained by considering local perturbations of the mixing proportion as follows:

| (4.1) |

for some . This type of alternative captures all local additive perturbations from by compressing potential lower-order dependence among the variables in the functions . The following theorem derives the distribution of under as in (4.1).

Theorem 4.1.

The proof of this theorem is given in Appendix E. Using this result we can derive the limiting local power of the test based on . Specifically, if denotes the CDF of the limiting distribution in (4.4) then local asymptotic power of the test (recall (3.10)) is given by

This implies, (and similarly and in (3.2) and (3.13), respectively) have non-trivial Pitman efficiency and is rate-optimal, in the sense that,

4.2. Konijn Alternative

The Konijn family of alternatives [44] for 2 random vectors can be defined as follows: Given two independent random vectors , , and , consider the law of

| (4.5) |

where and are and dimensional deterministic matrices, respectively. Note that when , the random vectors are independent and as increases introduces dependence/correlation through the matrix . Gieser [25] showed that if one choses , for some , then the distributions of and are contiguous when and are elliptically symmetric distributions centered at and with covariance matrices and , respectively. Here, we extend the Konijn family to multiple random vectors as follows:

Definition 4.2.

Given independent random vectors , where , for , and , consider the law of

| (4.6) |

where , for , is a a dimensional deterministic matrix.

Note that the matrix in (4.6) is a times block matrix with in the -th diagonal block for and in the -th block for . When , the matrix is identity and, hence, by continuity there exists a neighborhood of zero such that is invertible for . Therefore, by a change of variable formula, for , the density of can be written as:

| (4.7) |

where is the density of . Hereafter, we will denote and assume the following:

Assumption 3.

The family of distributions satisfies the following:

-

•

The support of does not depend on . In other words, the set does not depend on .

-

•

The map is continuously differentiable.

-

•

The Fisher information

is well-define, finite, strictly positive, and continuous at .

Under the above assumption, we consider the following sequence of local hypotheses:

| (4.8) |

for some . We show in Lemma E.1 that and as in (4.8) are contiguous under Assumption 3. This assumption also ensures that the family is quadratic mean-differentiable (QMD) (see [47, Definition 12.2.1]) and, hence, Le Cam’s theory of contiguity applies (see [47, Chapter 12] and [71, Chapter 6] ) .

Remark 4.3.

To describe the limiting distribution of under , denote the likelihood ratio and its derivative as:

where .

4.3. Hájek Representation and Proof Outline

The proofs of Theorems 4.1 and 4.4 are given in Appendix E. One of the main ingredients of the proof is a Hájek representation for the empirical process associated with , which shows that we can replace the empirical rank maps in the definition of with their population counterparts without altering its limiting distribution under . Since this result could be of independent interest we summarized this as a proposition below. To describe the result, consider the following empirical process:

| (4.12) |

where , and , for . Recalling (2.14), note that

| (4.13) |

One of the challenges of dealing with the process is the dependence across the indices arising from the empirical rank maps . The Hájek representation result shows that this dependence is asymptotically negligible under . Towards this, define the oracle version of the empirical process where the empirical rank maps in replaced with their population analogues empirical rank maps

| (4.14) |

for as in (3.6). We are now ready the state the Hájek representation result which shows that the difference between and its oracle version is under .

Proposition 4.5.

Once the Hájek representation is established the limiting distribution of under contiguous local alternatives can be obtained as follows:

-

•

The first step is to show the alternatives considered in (4.1) and (4.8) are mutually contiguous with . While this is well-known for the case of 2 variables and relatively straightforward to extend to multiple variables for the mixture alternative (4.1), for the Konjin alternative (4.8) establishing contiguity is much more involved. Invoking Le Cam’s second lemma [71], we show in Lemma E.1 that Konjin alternatives as in (4.6) are contiguous under Assumption 3.

-

•

Next, we derive the joint distribution of the collection of empirical processes and the log-likelihood under . Proposition 4.5 together with contiguity and Le Cam’s third lemma [71] gives the joint distribution of under as in (4.1) and (4.8). The results in (4.2) and (4.9) then follow by the representation in (4.13) and the continuous mapping theorem.

Remark 4.6.

Note that, as expected, one obtains the limiting null distribution of by substituting in Theorems 4.1 and 4.4. In fact the Hájek representation result provides an alternative strategy to proving of the asymptotic null distribution, which does require the combinatorial CLT for multiple permutations. Nevertheless, we present both approaches because the technical by-products emerging from them, namely the Hájek representation and the combinatorial CLT, are results of independent interest. In particular, the scope of the combinatorial CLT with multiple permutations goes beyond rank-based methods to other nonparametric independence tests, such as methods based on geometric graphs [22].

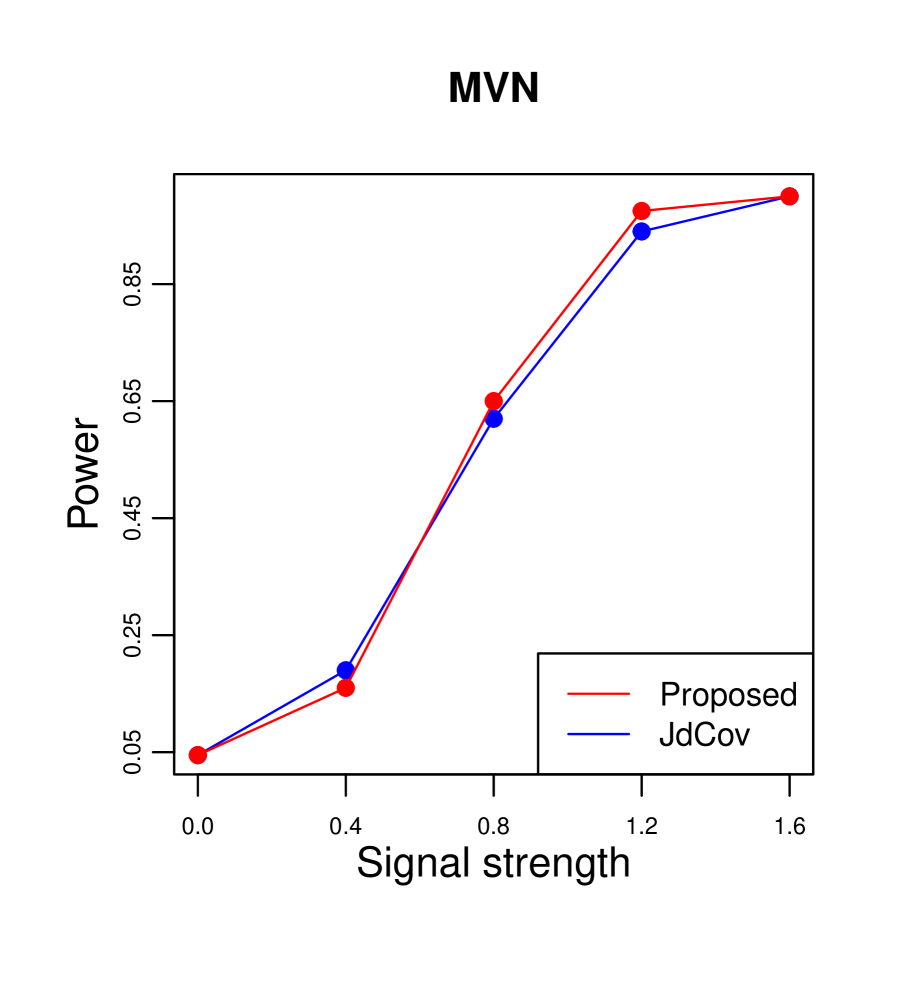

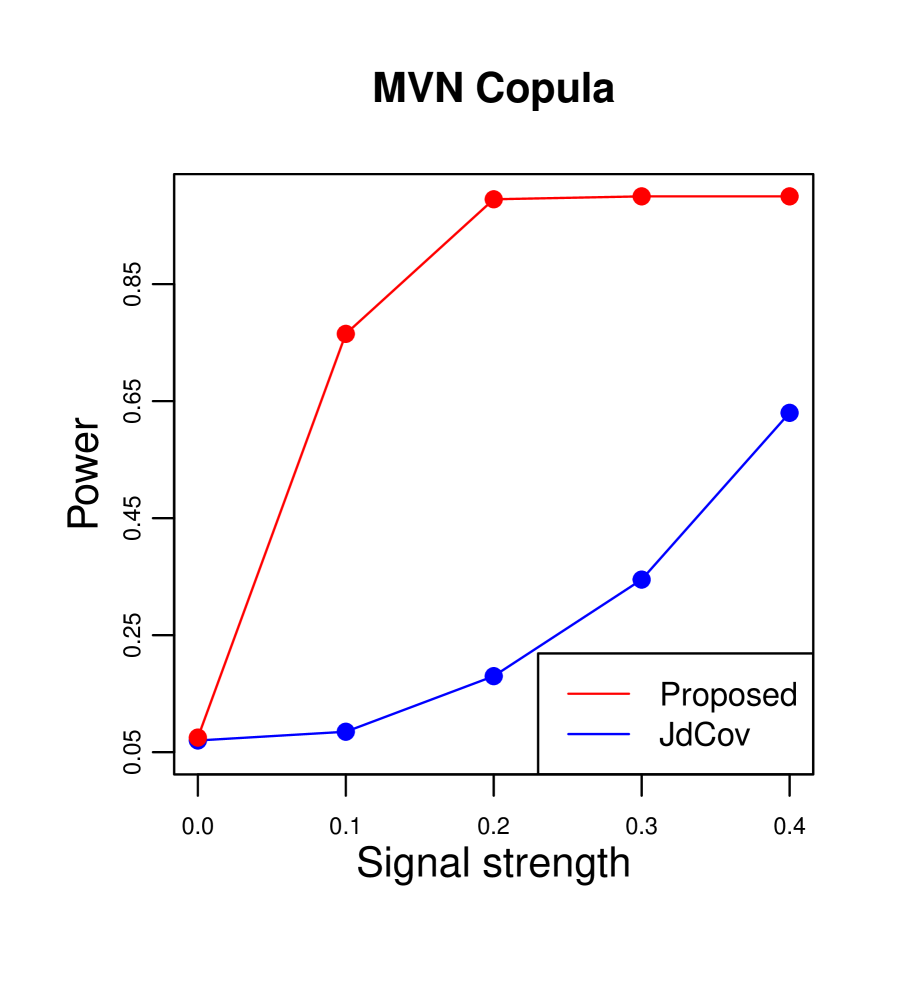

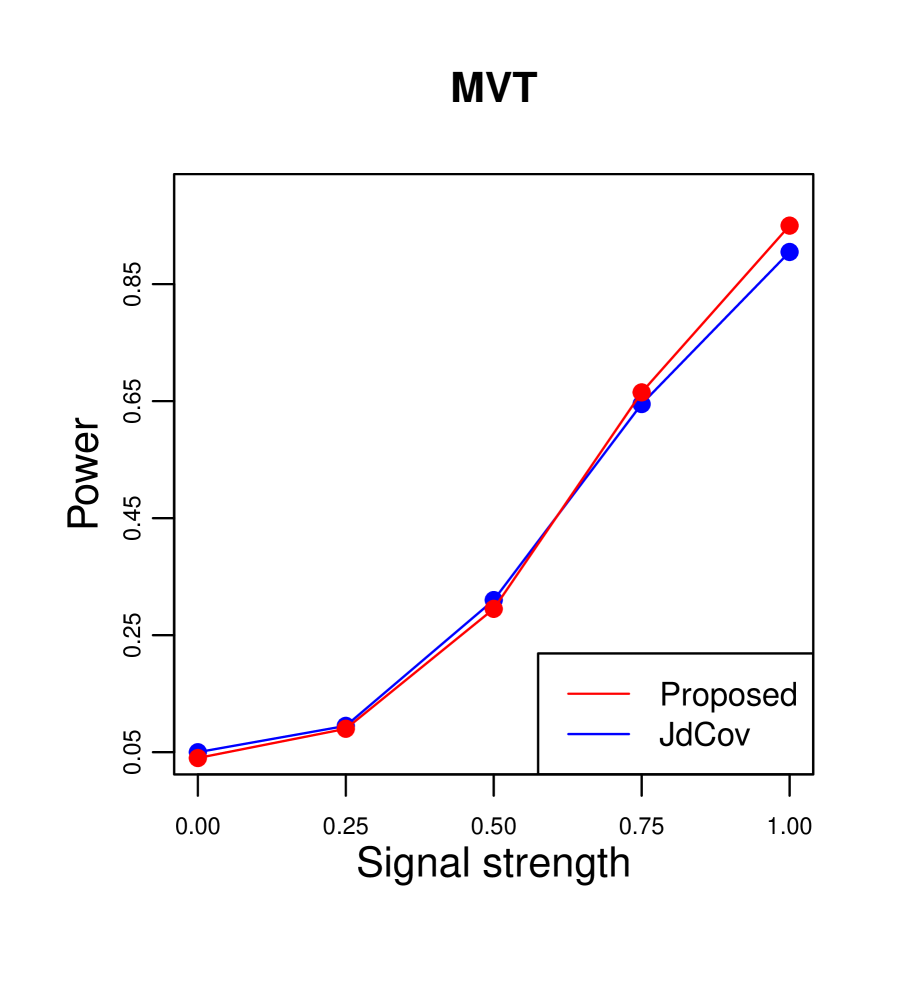

To validate the asymptotic results discussed above we present a finite sample simulation comparing the empirical power of the based test with test based on studied in [12]. Towards this we consider the following 3 distributions: (1) the multivariate normal (MVN), (2) the third-order multivariate normal copula (MVN copula),444A random variable is said to follow a -dimensional -th order, for , multivariate normal copula if , where as in [12, Example 1], and (3) the multivariate student distribution (MVT) with 5 degrees of freedom, with dimensions . In all the 3 cases the mean vectors are set to zero and the covariance matrix is and . We set the number of variables , the matrices , for and compute the matrix as in (4.6) by varying as follows: for the Gaussian case, for the Gaussian copula case, and for the multivariate -distribution. Table 1 shows the empirical power (over 200 repetitions) with sample size as a function of the signal strength ( varying as above), for tests based on the and the . The plots show that our method has comparable power with for the Gaussian and -distributions, while it is significantly better than the in the more heavy-tailed Gaussian copula model, illustrating the attractive efficiency properties of rank-based distribution-free methods.

(a)

(b)

(c)

5. Robust Independent Component Analysis

In this section, we apply the measure to develop a robust method for independent component analysis (ICA). Towards this, suppose be a random vector satisfying the following the moment conditions:

Assumption 4.

The random vector has a continuous distribution with and .

The ICA model assume that there is a random vector with jointly independent coordinates such that , where is a nonsingular mixing matrix. Without loss of generality, we assume is standardized such that and . Then by the spectral decomposition:

where and are the matrix of eigenvectors and the diagonal matrix of the corresponding eigenvalues of , respectively. Define and . Note that and . Therefore, when the ICA model holds we can write

| (5.1) |

where . This implies, , that is, is an orthogonal matrix.

Following Matteson and Tsay [52] we restrict , where denotes the set orthogonal matrices with determinant 1 (the rotation group) and parameterize by a vector , where is a vectorized triangular array of rotation angles of length indexed by , as follows:

| (5.2) |

where is the identity matrix with the and elements replaced by , the element replaced by and the element replaced by . To ensure the existence and uniqueness of the representation (5.2) define

| (5.3) |

Then by [51, Theorem 2.3.2] there exists a unique inverse map of into such that the mapping is assured to be continuous if either all elements on the main-diagonal of are positive, or all elements of are nonzero (see [52, 51] for more details on such decompositions).

Another identification issue with the ICA model is the sign and order of the independent components. Suppose is a signed permutation matrix and then note that in which case are the new independent components and is the new mixing matrix. This necessitates considering metrics that are invariant to the scale, sign, and order of the independent components, when comparing different estimates (see Section 6.4 for details).

In general the ICA model (5.1) is misspecified, in which case is chosen such that the components of are as close to mutually independent as possible. To this end, the provides a robust measure for quantifying deviations from joint independence. Hence, one choose by minimizing the following objective function:

| (5.4) |

Recall that the (population) rank map in the 1-dimensional case is the distribution function, hence, can be computed by replacing in (2.8) with , the distribution function of , for , where denotes the transpose of -th row of .

5.1. -Based ICA Estimator

We now discuss how one can estimate based on samples by minimizing the empirical version of (5.4). Towards this, suppose be i.i.d. samples distributed as satisfying Assumption 4. We define approximately uncorrelated observations , where is the sample covariance matrix of . Assumption 4 implies that . To simplify notation, we omit the above steps described and assume are i.i.d. samples distributed as , which has zero mean vector and identity covariance matrix. Also, we arrange such that the -th row of is , that is, has dimension .

To estimate from we replace in (5.4) with its empirical version

| (5.5) |

Note that for any value of the objective function can be computed easily, since in dimension 1 the empirical rank map is the empirical distribution function. Specifically, the empirical rank map for the -th component is . To establish the consistency of we need the following definition:

Definition 5.1.

We say is consistent for over if the function is continuous in and , as , for any metric on satisfying if and only if there exists a signed permutation matrix such that .

With this definition we can now state the consistency result of . Towards this, recall the definition of from (5.3) and let denote a sufficiently large compact subset of the space .

Theorem 5.2.

The proof of Theorem 5.2 is given in Appendix F.2. This shows that the proposed estimator is consistent for for metrics which are invariant to the non-identifiability issues of the ICA problem. The assumption of uniform boundedness is required to guarantee the distribution function is Lipschitz, which ensures the equicontinuity of the objective function.

5.2. Practical Implementation

One of the challenges in directly implementing gradient based methods to minimize the objective in (5.5) is that, the empirical distribution functions are not differentiable with respect to . Matteson and Tsay [52] suggested a practical way to circumvent this issue by estimating the univariate distribution functions , for , using kernel-based methods. Specifically, we consider the following problem:

| (5.6) |

with and

| (5.7) |

where is the integral of a density kernel and is a data dependent bandwidth for the -th component, for (see Section 2 in [52] for practical choices of ). The optimization problem (5.6) can now be solved using a gradient-based method (see Section F.1 for the computation of the gradient).

The advantages of using kernel-based estimates is that they have nice theoretical properties, which can be used to establish the consistency of the estimate . In particular, if we assume that is a positive measurable function of the -th coordinates of such that as , then

as , for (see Corollary 1 in [11]). Then whenever is Lipschitz and Assumption 4 and the conditions in Theorem 5.2 holds, similar to the proof Theorem 2.1 in [52], by replacing their objective function with , it can be shown that is consistent for over .

6. Simulation Study

In this section, we showcase the efficacy of the proposed test, both in terms of Type-I error control and power, across a range of simulation settings. For our test we implement the finite sample version discussed in Section 3.2 with cut-off chosen as in (3.12) and all the weights set to 1. We compare our method (hereafter referred to as ) with the JdCov based test in [12], the dCov based test studied by Matteson and Tsay [52] (hereafter denoted as MT), and the dHSIC based test [59]. The section is organized as follows: In Section 6.1 we present the results on Type-I error control. The empirical power for testing joint independence is given in Section 6.2 and results for detecting higher-order dependence are in Section 6.3. The performance of the ICA estimator is studied in Section 6.4.

6.1. Type-I Error Control

To illustrate the finite sample Type-I error control of the proposed test we consider in the following three settings:

-

Multivariate Gaussian: are i.i.d. .

-

Third-order Gaussian copula: are independent random vectors in with i.i.d. coordinates distributed as .

-

Cauchy: are independent random vectors in with i.i.d. coordinates distributed as , the Cauchy distribution with location parameter 0 and scale to parameter 1.

Table 1 shows the empirical Type-I error probability (over 500 repetitions) with sample size for the different tests in the above 3 situations. Our test satisfactorily controls Type-I error in finite samples, validating the theoretical results. The other tests also have good Type-I error control.

| Distribution | Multivariate Gaussian | Gaussian Copula | Cauchy |

|---|---|---|---|

| Proposed | 0.038 | 0.042 | 0.042 |

| JdCov | 0.036 | 0.030 | 0.046 |

| Matteson-Tsay (MT) | 0.056 | 0.046 | 0.056 |

| dHSIC | 0.032 | 0.074 | 0.050 |

6.2. Power Results

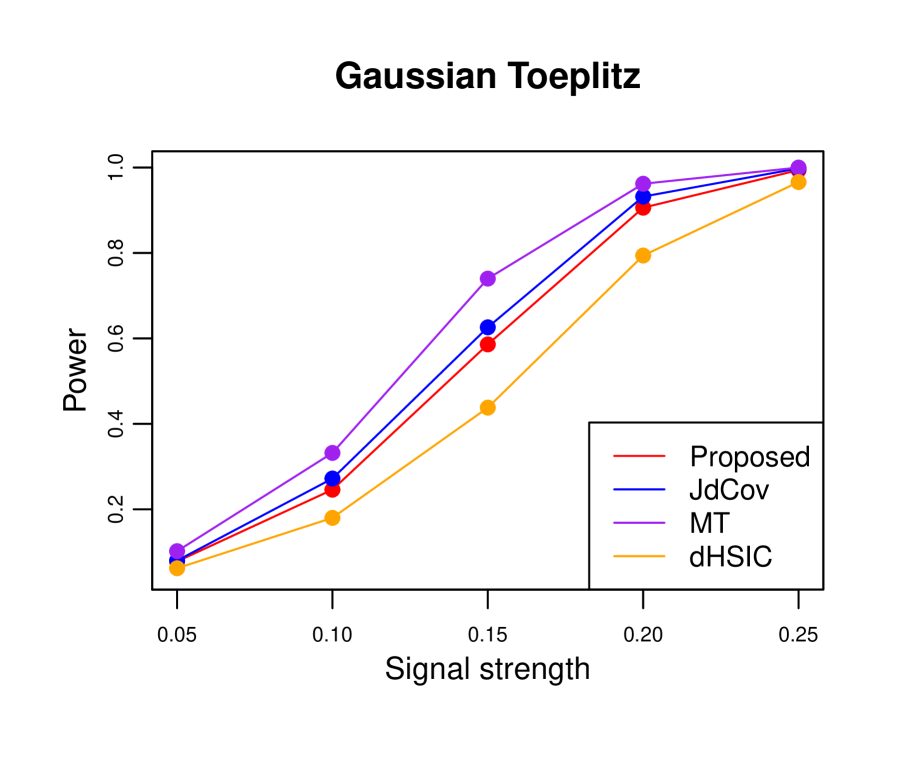

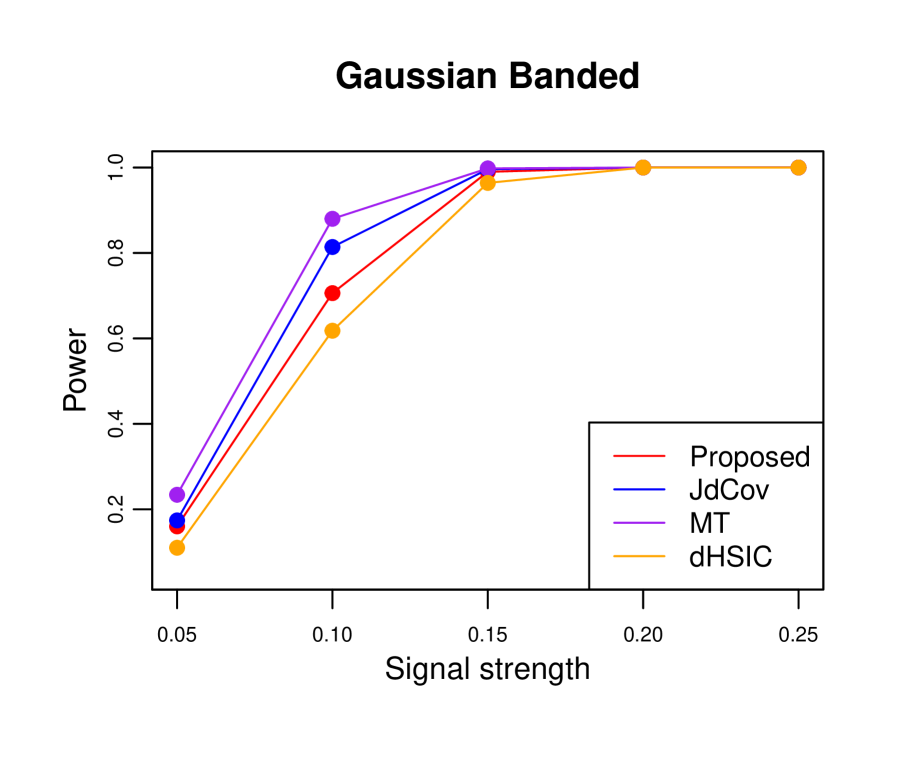

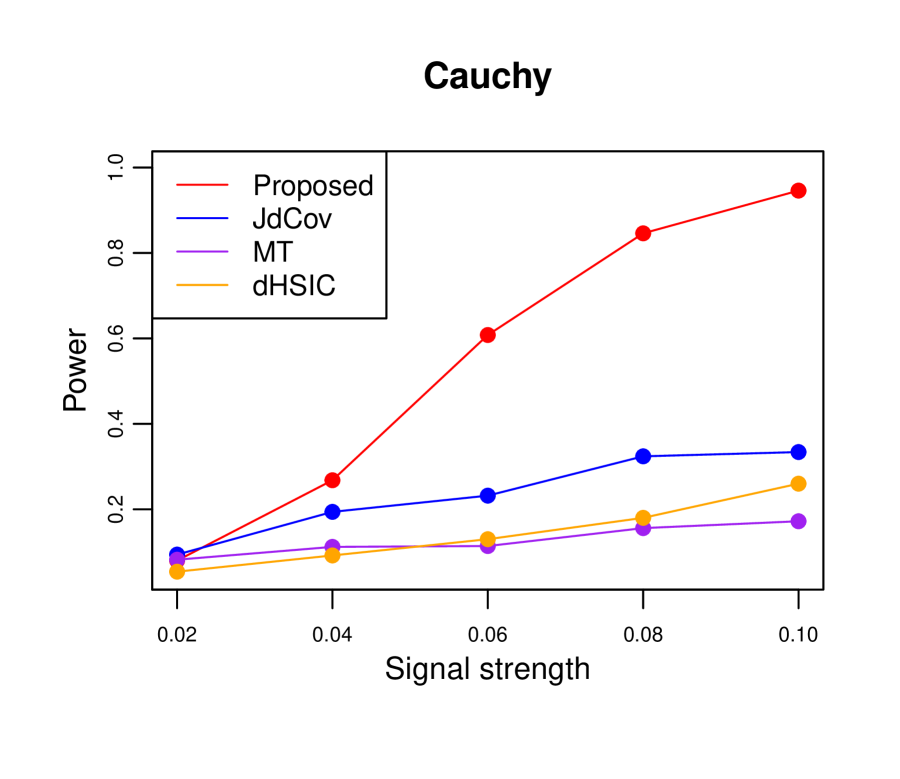

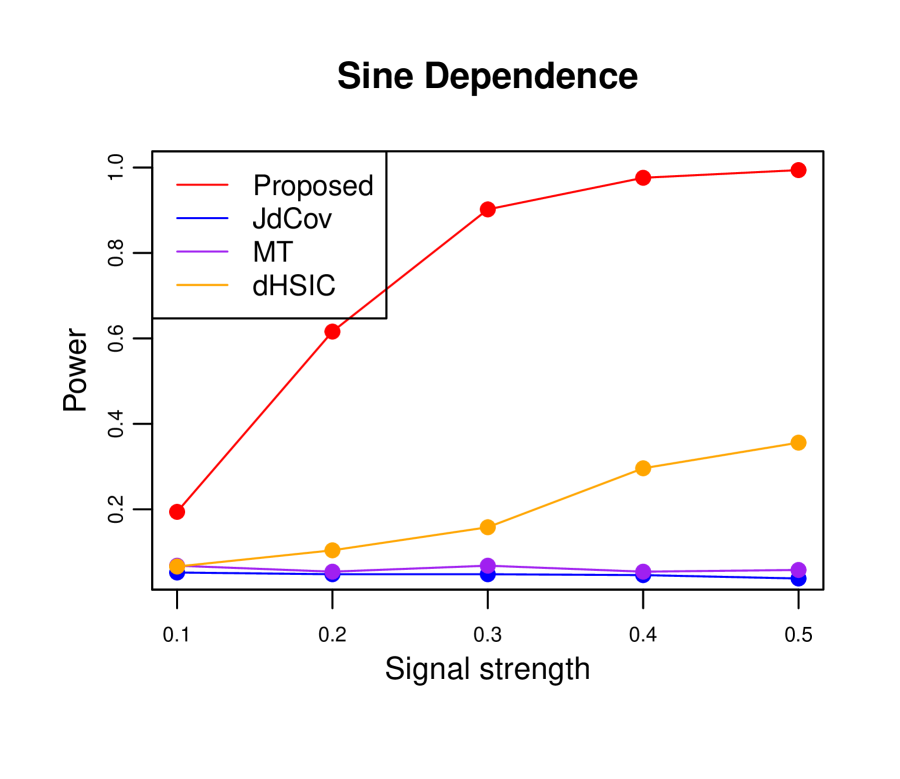

In this section we compare the empirical power of with the existing methods in the 4 settings described below. In the first 2 cases we have (light-tailed) multivariate Gaussian distributions with covariance structure as in [12, Example 2], the third setting is a (heavy-tailed) Cauchy regression model, and the fourth is a Cauchy sine dependence model (similar to [78]). Throughout we set the sample size and compute the empirical power over 500 repititions.

(a)

(b)

-

Multivariate Gaussian with autoregressive covariance structure: In this case the data is generated as follows: where has an autocorrelation structure, that is, . Then the first 3 coordinates of are set as , second 3 coordinates as , and the last 3 coordinates as . Figure 2 (a) shows the empirical power of the different tests as varies between to over a grid of 5 equally spaced values.

-

Multivariate Gaussian with banded covariance matrix: Here, where has a banded structure, that is, for , for , and otherwise. As before, the first 3 coordinates of are set as , second 3 coordinates as , and the last 3 coordinates as . Figure 2 (b) shows the empirical power of the different tests as varies between to over a grid of 5 equally spaced values.

-

Cauchy regression: In this case is generated as follows:

(6.1) for , where have i.i.d. coordinates distributed according to , and with . Note that the variables are mutually dependent because of the shared noise vector. Figure 3 (a) shows the empirical power of the different tests as varies between to 1 over a grid of 5 equally spaced values.

-

Sine dependence: In this case is generated as in (6.1), but with a different noise distribution. Specifically, we fix , generate with i.i.d. coordinates distributed according to as before, but change as where . Figure 3 (b) shows the empirical power of the different tests as varies between to over a grid of 5 equally spaced values.

We observe from the plots in Figure 2 that the along with the other methods have very similar performance in the Gaussian settings. On the other hand, Figure 3 shows in the heavy-tailed Cauchy and sine dependence settings the significantly outperforms the other tests. Overall the emerges as the preferred method by exhibiting good power over a range of data distributions.

(a)

(b)

6.3. Higher-Order Dependence

In this section we consider situations where the variables are pairwise independent but jointly dependent. Specifically, generate as follows:

-

•

Suppose , and are independent random vectors with i.i.d. coordinates distributed according to , where is a distribution in that is symmetric around .

-

•

For , set and set if is positive, otherwise set .

It can easily be checked that are pairwise independent. However, they are mutually dependent, since, for example, is always non-negative. In the simulations we choose to the following 4 distributions: (1) , (2) the -distribution with 2 degrees of freedom , (3) the -distribution with 3 degrees of freedom , and (4) the Cauchy distribution , equivalently, the the -distribution with 1 degree of freedom.

In Table 2 we show the empirical power (over 500 iterations) with sample size of the following 3 tests (and their corresponding versions based on /):

-

•

The test for pairwise independence that rejects for large values of

-

•

The test for higher-order independence that rejects for large values of .

-

•

The test for joint independence based on .

The results in Table 2 show that for all the 4 distributions considered both the and based tests successfully detect the null hypothesis of pairwise independence (probability of Type-I error). However, the based test fails to detect higher-order dependence for the Cauchy distribution and joint dependence for the and the Cauchy distribution. This is not unexpected because the consistency of the based rely on certain moment assumptions which are not satisfied by heavy-tailed distributions like the and the Cauchy (recall that does not have finite variance and does not have finite mean). On the other hand, the based tests easily detects both the higher-order and joint dependences in the all 4 cases, which once again highlights the robustness and broad application of the proposed method.

| Dependence | Pariwise | Higher-Order | Joint | |||

| Tests | JdCov | Proposed | JdCov | Proposed | JdCov | Proposed |

| Gaussian | 0.058 | 0.054 | 1 | 1 | 1.000 | 0.942 |

| 0.052 | 0.064 | 1 | 1 | 0.868 | 0.904 | |

| 0.056 | 0.040 | 1 | 1 | 0.098 | 0.888 | |

| Cauchy | 0.064 | 0.044 | 0.04 | 1 | 0.050 | 0.788 |

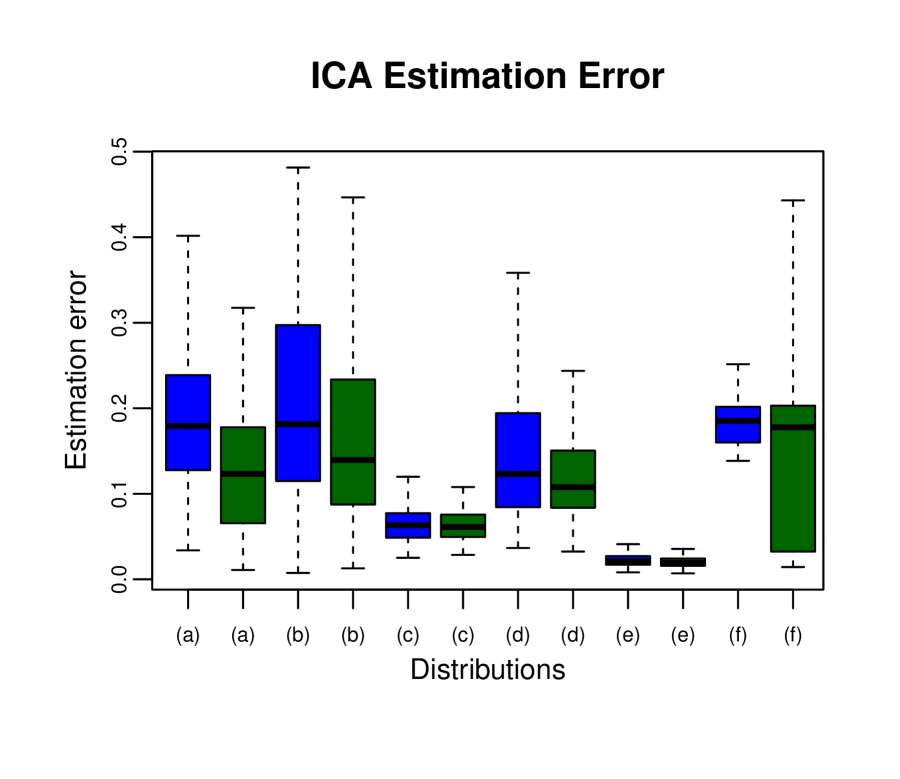

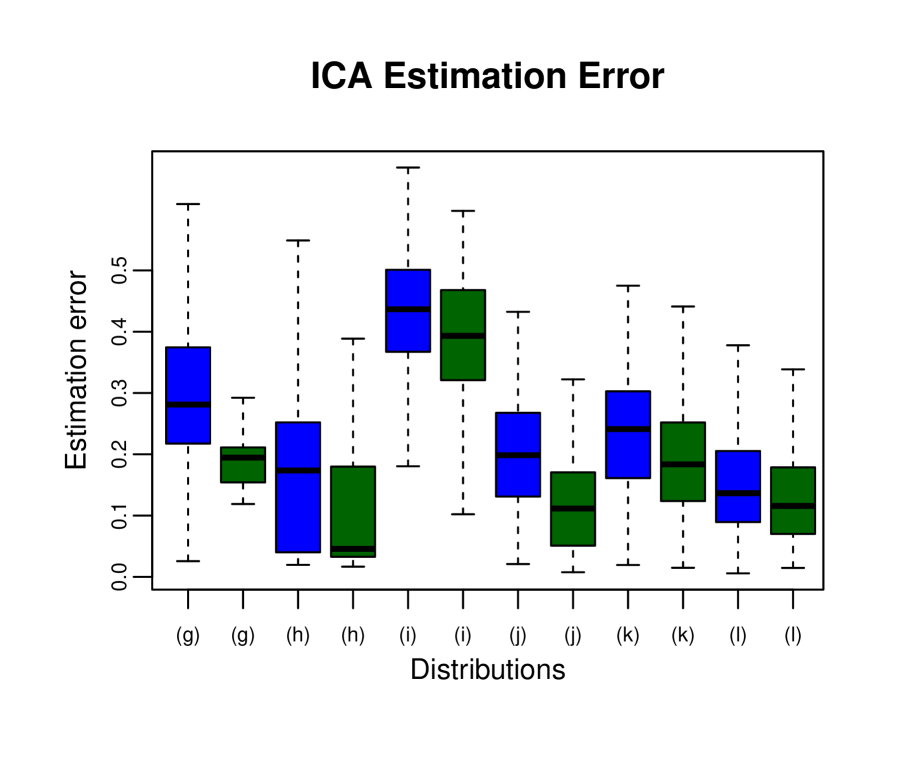

6.4. Performance of the ICA Estimator

To evaluate the performance of the distribution-free ICA estimator proposed in Section 5, we consider the following model:

where , i.i.d. for some distribution , and is a random mixing matrix with condition number between 1 and 2, using the R package ProDenICA.555https://cran.r-project.org/web/packages/ProDenICA/index.html We consider 12 candidate distributions for as described Table 3. For each candidate distribution we apply the gradient descent algorithm to solve the optimization program (5.6) (where the gradient is derived in Section 5.2). We compare our results with the method proposed in Matteson and Tsay [52]. As in [52] the estimation error is measured in the following metric, which is designed to resolve the non-identifiability issues:

where

-

•

is the estimated mixing matrix,

-

•

denotes the Frobenius norm,

-

•

, where is the the set of nonsingular matrices, is a signed permutation matrix, and is a diagonal matrix with positive diagonal elements.

The computation for metric is available in the R package JADE [57]. We set dimension and the sample size and present the results in 4, where the indices in -axis denote different distributions as described in Table 3. The results in Table 3 show that our estimator have smaller estimation error and variance except for distribution (f).

| Estimation Error (Standard Deviation) | |||

|---|---|---|---|

| Index | Distribution | Proposed | MT |

| 0.129 (0.077) | 0.192 (0.094) | ||

| 0.170 (0.109) | 0.209 (0.120) | ||

| 0.067 (0.028) | 0.073 (0.049) | ||

| 0.127 (0.069) | 0.148 (0.088) | ||

| 0.034 (0.046) | 0.038 (0.055) | ||

| 0.157 (0.121) | 0.181 (0.120) | ||

| 0.189 (0.110) | 0.310 (0.132) | ||

| 0.115 (0.117) | 0.174 (0.134) | ||

| 0.390 (0.105) | 0.435 (0.104) | ||

| 0.121 (0.085) | 0.205 (0.093) | ||

| 0.191 (0.097) | 0.236 (0.107) | ||

| 0.131 (0.084) | 0.157 (0.101) | ||

7. Real data application

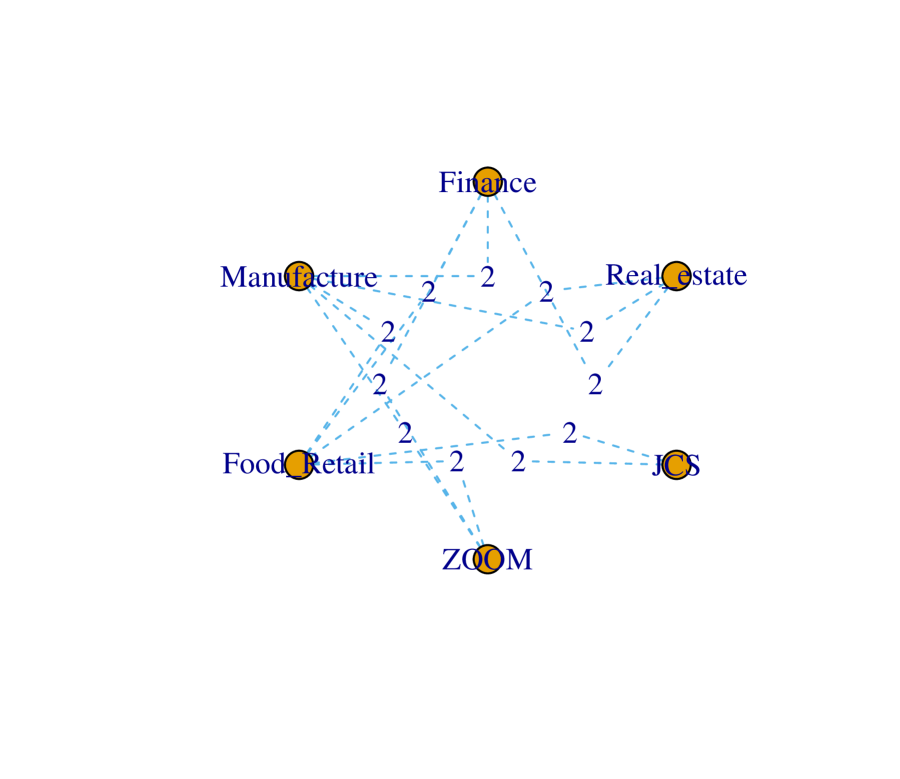

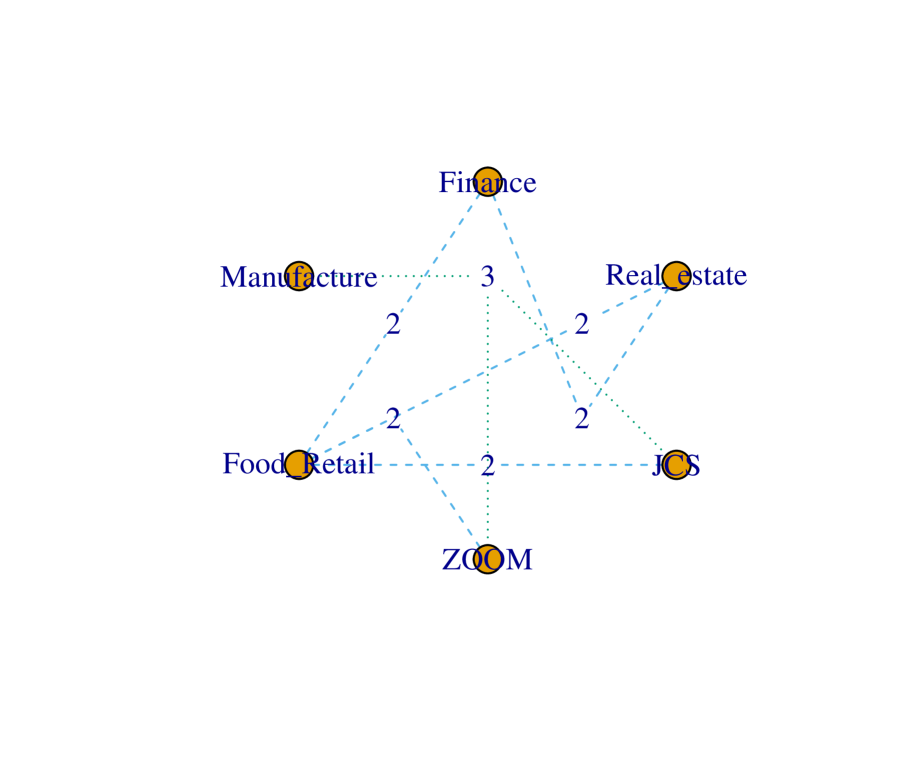

In this section, we apply our method to the stock price data available in R package gmm. The data can be accessed using the command data(finance). The dataset has prices for 24 stocks corresponding to 20 companies in US starting from January 5th, 1993 to January 30th, 2009. Since the dataset has several missing entries before 2003, we use data from the 2003-2009 period for 9 of these companies (described below) for our analysis. To account for the temporal dependence, we average the stock prices over the week, after which we obtain data points. We categorize the different companies into 6 different industries according to North American Industry Classification System (NAICS) as follows: (1) Real Estate (RE) category which contains the company NHP, (2) the Food and Retail (FR) category which includes the companies WMK and GCO; (3) Manufacture (M) category including ROG, MAT, and VOXX; (4) the Finance (F) category with the company FNM; (5) Communications Systems (JCS); and (6) Zoom Technologies (ZOOM). We created 2 separate categories for the companies JCS and ZOOM because their stock prices seem to vary independently of the other companies, possibly due to their relatively small scales, even though they both belong to the information industry.

7.1. Results and Analysis

To understand the dependency structure between the 6 categories (industries) described above, we first test the pairwise dependence of the stock prices between different industries. Then we test for higher-order dependencies between triples of categories for which the null hypothesis of pairwise independence is accepted. We report the results for the tests based on and for comparison. Throughout we set the significance level to .

The -values for the pairwise independence tests are summarized in Table 4. Note that this entails performing , so the -values are adjusted using the BH-procedure. To better visualize the results, we plot the dependency graph between 6 categories using function dependence.structure in R package multivariance [8] and the results are shown in Figure 5. From these we can see that hypothesis of pairwise independence is accepted by for the following 3 triples: (I) Real Estate-JCS-ZOOM, (II) Finance-JCS-ZOOM, and (III) Manufacture-JCS-ZOOM. On the other hand, only accepts the pairwise independence hypothesis for the triple: Real Estate-JCS-ZOOM when using . This might be due to the small scale of companies JCS and ZOOM, which tends to make them independent of each other and among others. Moreover, observe that the Manufacture and Food and Retail categories are prone to be dependent with all the others, which is also reasonable because their services are essential to the other industries.

| -values | ||

|---|---|---|

| Industry-Industry | JdCov | Proposed |

| RE-JCS | 0.096 | 0.136 |

| RE-ZOOM | 0.188 | 0.107 |

| RE-FR | 0.002 | 0.000 |

| RE-M | 0.002 | 0.000 |

| RE-F | 0.002 | 0.000 |

| JCS-ZOOM | 0.152 | 0.136 |

| JCS-FR | 0.002 | 0.004 |

| JCS-M | 0.002 | 0.258 |

| JCS-F | 0.102 | 0.408 |

| ZOOM-FR | 0.008 | 0.010 |

| ZOOM-M | 0.012 | 0.058 |

| ZOOM-F | 0.032 | 0.968 |

| FR-M | 0.002 | 0.000 |

| FR-F | 0.002 | 0.000 |

| M-F | 0.002 | 0.000 |

The -values for testing third-order independence for the 3 triples for which the hypothesis of pairwise independence are accepted are given in Table 5. We observe from Table 5 that the third-order based -value, which tests for the null hypothesis of joint independence of RE, JCS, and ZOOM given their pairwise independence, accepts the null hypothesis at level . However, the based -value, which tests for the null hypothesis of joint independence of RE, JCS, and ZOOM (without any assumptions on pairwise independence), rejects the null hypothesis of joint independence at . Given that the pairwise independence hypothesis has been accepted, for consistent hierarchical interpretability one would have ideally expected the third-order and the to have the same conclusions. On the other hand, the conclusions from the and -values are hierarchically consistent. Moreover, Figure 5(b) shows that there is higher-order dependence between JCS, ZOOM, and Manufacture industries when using and . This may be because JCS and ZOOM, and Manufacturing will typically serve as downstream industries but direct links between them are not obvious due to the scales of the companies.

(a)

(b)

.

| Real estate-JCS- ZOOM | 0.101 | 0.020 | 0.187 | 0.063 |

|---|---|---|---|---|

| Finance-JCS-ZOOM | 0.274 | 0.425 | ||

| Manufacture-JCS-ZOOM | 0.003 | 0.006 |

Acknowledgment

The authors are grateful to Björn Böttcher and David Matteson for sharing their codes and datasets. BBB was partly supported by NSF CAREER Grant DMS-2046393 and a Sloan research fellowship.

References

- Agarwal and Sharathkumar [2014] P. K. Agarwal and R. Sharathkumar. Approximation algorithms for bipartite matching with metric and geometric costs. In STOC’14—Proceedings of the 2014 ACM Symposium on Theory of Computing, pages 555–564. ACM, New York, 2014.

- Ai et al. [2022] C. Ai, L.-H. Sun, Z. Zhang, and L. Zhu. Testing unconditional and conditional independence via mutual information. Journal of Econometrics, 2022.

- Banerjee and Ghosh [2022] B. Banerjee and A. K. Ghosh. Test of independence for hilbertian random variables. Stat, 11(1):e474, 2022.

- Beran et al. [2007] R. Beran, M. Bilodeau, and P. L. de Micheaux. Nonparametric tests of independence between random vectors. Journal of Multivariate Analysis, 98(9):1805–1824, 2007.

- Bergsma and Dassios [2014] W. Bergsma and A. Dassios. A consistent test of independence based on a sign covariance related to kendall’s tau. Bernoulli, 20(2):1006–1028, 2014.

- Berrett and Samworth [2019] T. B. Berrett and R. J. Samworth. Nonparametric independence testing via mutual information. Biometrika, 106(3):547–566, 2019.

- Blum et al. [1961] J. R. Blum, J. Kiefer, and M. Rosenblatt. Distribution free tests of independence based on the sample distribution function. Ann. Math. Statist., 32:485–498, 1961.

- Böttcher [2020] B. Böttcher. Dependence and dependence structures: estimation and visualization using the unifying concept of distance multivariance. Open Statistics, 1(1):1–48, 2020.

- Böttcher et al. [2019] B. Böttcher, M. Keller-Ressel, and R. L. Schilling. Distance multivariance: New dependence measures for random vectors. The Annals of Statistics, 47(5):2757–2789, 2019.

- Brenier [1991] Y. Brenier. Polar factorization and monotone rearrangement of vector-valued functions. Communications on pure and applied mathematics, 44(4):375–417, 1991.

- Chacon and Rodriguez-Casal [2010] J. E. Chacon and A. Rodriguez-Casal. A note on the universal consistency of the kernel distribution function estimator. Statistics & Probability Letters, 80(17-18):1414–1419, 2010.

- Chakraborty and Zhang [2019] S. Chakraborty and X. Zhang. Distance metrics for measuring joint dependence with application to causal inference. Journal of the American Statistical Association, 2019.

- Chatterjee [2007] S. Chatterjee. Stein’s method, 2007. URL https://souravchatterjee.su.domains/AllLectures.pdf.

- Chatterjee [2021] S. Chatterjee. A new coefficient of correlation. Journal of the American Statistical Association, 116(536):2009–2022, 2021.

- Chatterjee [2022] S. Chatterjee. A survey of some recent developments in measures of association. arXiv preprint arXiv:2211.04702, 2022.

- Chernozhukov et al. [2017] V. Chernozhukov, A. Galichon, M. Hallin, and M. Henry. Monge–kantorovich depth, quantiles, ranks and signs. The Annals of Statistics, 45(1):223–256, 2017.

- Csörgő [1985] S. Csörgő. Testing for independence by the empirical characteristic function. Journal of Multivariate Analysis, 16(3):290–299, 1985.

- Deb and Sen [2021] N. Deb and B. Sen. Multivariate rank-based distribution-free nonparametric testing using measure transportation. Journal of the American Statistical Association, pages 1–16, 2021.

- Deb et al. [2020] N. Deb, P. Ghosal, and B. Sen. Measuring association on topological spaces using kernels and geometric graphs. arXiv preprint arXiv:2010.01768, 2020.

- Deb et al. [2021] N. Deb, B. B. Bhattacharya, and B. Sen. Efficiency lower bounds for distribution-free hotelling-type two-sample tests based on optimal transport. arXiv preprint arXiv:2104.01986, 2021.

- Feuerverger [1993] A. Feuerverger. A consistent test for bivariate dependence. International Statistical Review/Revue Internationale de Statistique, pages 419–433, 1993.

- Friedman and Rafsky [1983] J. H. Friedman and L. C. Rafsky. Graph-theoretic measures of multivariate association and prediction. The Annals of Statistics, pages 377–391, 1983.

- Gaißer et al. [2010] S. Gaißer, M. Ruppert, and F. Schmid. A multivariate version of Hoeffding’s phi-square. Journal of Multivariate Analysis, 101(10):2571–2586, 2010.

- Ghosal and Sen [2022] P. Ghosal and B. Sen. Multivariate ranks and quantiles using optimal transport: Consistency, rates and nonparametric testing. The Annals of Statistics, 50(2):1012–1037, 2022.

- Gieser [1993] P. W. Gieser. A new nonparametric test for independence between two sets of variates. PhD thesis, University of Florida, 1993.

- Gieser and Randles [1997] P. W. Gieser and R. H. Randles. A nonparametric test of independence between two vectors. Journal of the American Statistical Association, 92(438):561–567, 1997.

- Gretton et al. [2005a] A. Gretton, O. Bousquet, A. Smola, and B. Schölkopf. Measuring statistical dependence with hilbert-schmidt norms. In International conference on algorithmic learning theory, pages 63–77. Springer, 2005a.

- Gretton et al. [2005b] A. Gretton, R. Herbrich, A. Smola, O. Bousquet, B. Schölkopf, et al. Kernel methods for measuring independence. 2005b.

- Gretton et al. [2007] A. Gretton, K. Fukumizu, C. Teo, L. Song, B. Schölkopf, and A. Smola. A kernel statistical test of independence. Advances in neural information processing systems, 20, 2007.

- Hallin [2017] M. Hallin. On distribution and quantile functions, ranks and signs in . ECARES Working Papers, 2017.

- Hallin et al. [2020a] M. Hallin, E. del Barrio, J. A. Cuesta-Albertos, and C. Matrán. On distribution and quantile functions, ranks, and signs in : a measure transportation approach. Ann.Stat. (to appear), 2020a.

- Hallin et al. [2020b] M. Hallin, D. La Vecchia, and H. Liu. Center-outward R-estimation for semiparametric VARMA models. Journal of the American Statistical Association, pages 1–14, 2020b.

- Hallin et al. [2022] M. Hallin, D. Hlubinka, and Š. Hudecová. Efficient fully distribution-free center-outward rank tests for multiple-output regression and manova. Journal of the American Statistical Association, pages 1–17, 2022.

- Heller et al. [2012] R. Heller, M. Gorfine, and Y. Heller. A class of multivariate distribution-free tests of independence based on graphs. Journal of Statistical Planning and Inference, 142(12):3097–3106, 2012.

- Heller et al. [2013] R. Heller, Y. Heller, and M. Gorfine. A consistent multivariate test of association based on ranks of distances. Biometrika, 100(2):503–510, 2013.

- Heller et al. [2016] R. Heller, Y. Heller, S. Kaufman, B. Brill, and M. Gorfine. Consistent distribution-free -sample and independence tests for univariate random variables. The Journal of Machine Learning Research, 17(1):978–1031, 2016.

- Hoeffding [1948] W. Hoeffding. A Non-Parametric Test of Independence. The Annals of Mathematical Statistics, 19(4):546 – 557, 1948.

- Hofer [2009] R. Hofer. On the distribution properties of Niederreiter-Halton sequences. J. Number Theory, 129(2):451–463, 2009. ISSN 0022-314X.

- Hyvärinen and Oja [2000] A. Hyvärinen and E. Oja. Independent component analysis: algorithms and applications. Neural networks, 13(4-5):411–430, 2000.

- Jonker and Volgenant [1987] R. Jonker and A. Volgenant. A shortest augmenting path algorithm for dense and sparse linear assignment problems. Computing, 38(4):325–340, 1987.

- Josse and Holmes [2016] J. Josse and S. Holmes. Measuring multivariate association and beyond. Stat. Surv., 10:132–167, 2016.

- Kankainen [1995] A. Kankainen. Consistent testing of total independence based on the empirical characteristic function. University of Jyväskylä, 1995.

- Kinney and Atwal [2014] J. B. Kinney and G. S. Atwal. Equitability, mutual information, and the maximal information coefficient. Proceedings of the National Academy of Sciences, 111(9):3354–3359, 2014.

- Konijn [1956] H. Konijn. On the power of certain tests for independence in bivariate populations. The Annals of Mathematical Statistics, 27(2):300–323, 1956.

- Kosorok [2008] M. R. Kosorok. Introduction to empirical processes and semiparametric inference. Springer, 2008.

- Kuo [1975] H.-H. Kuo. Gaussian measures in banach spaces. Gaussian Measures in Banach Spaces, pages 1–109, 1975.

- Lehmann and Romano [2005] E. L. Lehmann and J. P. Romano. Testing Statistical Hypotheses. Springer Texts in Statistics. Springer, New York, third edition, 2005. ISBN 0-387-98864-5.

- Li et al. [2012] R. Li, W. Zhong, and L. Zhu. Feature screening via distance correlation learning. Journal of the American Statistical Association, 107(499):1129–1139, 2012.

- Ma [2022] J. Ma. Evaluating independence and conditional independence measures. arXiv preprint arXiv:2205.07253, 2022.

- Ma and Mao [2019] L. Ma and J. Mao. Fisher exact scanning for dependency. Journal of the American Statistical Association, 114(525):245–258, 2019.

- Matteson [2008] D. S. Matteson. Statistical inference for multivariate nonlinear time series. The University of Chicago, 2008.

- Matteson and Tsay [2017] D. S. Matteson and R. S. Tsay. Independent component analysis via distance covariance. Journal of the American Statistical Association, 112(518):623–637, 2017.

- McCann [1995] R. J. McCann. Existence and uniqueness of monotone measure-preserving maps. Duke Mathematical Journal, 80(2):309–323, 1995.

- Monge [1781] G. Monge. Mémoire sur la théorie des déblais et des remblais. Histoire de l’Académie Royale des Sciences de Paris, 1781.

- Moon and Chen [2022] H. Moon and K. Chen. Interpoint-ranking sign covariance for the test of independence. Biometrika, 109(1):165–179, 2022.

- Nandy et al. [2016] P. Nandy, L. Weihs, and M. Drton. Large-sample theory for the bergsma-dassios sign covariance. Electronic Journal of Statistics, 10(2):2287–2311, 2016.

- Nordhausen et al. [2014] K. Nordhausen, J. Cardoso, J. Miettinen, H. Oja, E. Ollila, and S. Taskinen. Jade: Jade and other bss methods as well as some bss performance criteria. R package version, pages 1–9, 2014.

- Pan et al. [2019] W. Pan, X. Wang, H. Zhang, H. Zhu, and J. Zhu. Ball covariance: A generic measure of dependence in banach space. Journal of the American Statistical Association, 2019.

- Pfister et al. [2018] N. Pfister, P. Bühlmann, B. Schölkopf, and J. Peters. Kernel-based tests for joint independence. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(1):5–31, 2018.

- Póczos et al. [2012] B. Póczos, Z. Ghahramani, and J. Schneider. Copula-based kernel dependency measures. arXiv preprint arXiv:1206.4682, 2012.

- Reshef et al. [2011] D. N. Reshef, Y. A. Reshef, H. K. Finucane, S. R. Grossman, G. McVean, P. J. Turnbaugh, E. S. Lander, M. Mitzenmacher, and P. C. Sabeti. Detecting novel associations in large data sets. science, 334(6062):1518–1524, 2011.

- Resnick [2013] S. I. Resnick. A Probability Path. Springer Science & Business Media, 2013.

- Roy et al. [2020] A. Roy, S. Sarkar, A. K. Ghosh, and A. Goswami. On some consistent tests of mutual independence among several random vectors of arbitrary dimensions. Statistics and Computing, 30(6):1707–1723, 2020.

- Sejdinovic et al. [2013a] D. Sejdinovic, A. Gretton, and W. Bergsma. A kernel test for three-variable interactions. Advances in Neural Information Processing Systems, 26, 2013a.

- Sejdinovic et al. [2013b] D. Sejdinovic, B. Sriperumbudur, A. Gretton, and K. Fukumizu. Equivalence of distance-based and RKHS-based statistics in hypothesis testing. Ann. Statist., 41(5):2263–2291, 2013b.

- Sejdinovic et al. [2013c] D. Sejdinovic, B. Sriperumbudur, A. Gretton, and K. Fukumizu. Equivalence of distance-based and rkhs-based statistics in hypothesis testing. The annals of statistics, pages 2263–2291, 2013c.

- Shi et al. [2020a] H. Shi, M. Drton, and F. Han. Distribution-free consistent independence tests via center-outward ranks and signs. Journal of the American Statistical Association, pages 1–16, 2020a.

- Shi et al. [2020b] H. Shi, M. Hallin, M. Drton, and F. Han. On universally consistent and fully distribution-free rank tests of vector independence. arXiv preprint arXiv:2007.02186, 2020b.

- Székely and Rizzo [2009] G. J. Székely and M. L. Rizzo. Brownian distance covariance. The annals of applied statistics, 3(4):1236–1265, 2009.

- Székely et al. [2007] G. J. Székely, M. L. Rizzo, and N. K. Bakirov. Measuring and testing dependence by correlation of distances. The annals of statistics, 35(6):2769–2794, 2007.

- Van der Vaart [2000] A. W. Van der Vaart. Asymptotic statistics, volume 3. Cambridge university press, 2000.

- Van Der Vaart and Wellner [1996] A. W. Van Der Vaart and J. Wellner. Weak convergence and empirical processes: with applications to statistics. Springer Science & Business Media, 1996.

- Villani [2003] C. Villani. Topics in optimal transportation, volume 58 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, 2003. ISBN 0-8218-3312-X.

- Wu et al. [2009] E. H. Wu, L. Philip, and W. K. Li. A smoothed bootstrap test for independence based on mutual information. Computational statistics & data analysis, 53(7):2524–2536, 2009.

- Yanagimoto [1970] T. Yanagimoto. On measures of association and a related problem. Annals of the Institute of Statistical Mathematics, 22(1):57–63, 1970.

- Yao et al. [2018] S. Yao, X. Zhang, and X. Shao. Testing mutual independence in high dimension via distance covariance. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(3):455–480, 2018.

- Zhang [2019] K. Zhang. Bet on independence. Journal of the American Statistical Association, 114(528):1620–1637, 2019.

- Zhang et al. [2018] Q. Zhang, S. Filippi, A. Gretton, and D. Sejdinovic. Large-scale kernel methods for independence testing. Statistics and Computing, 28(1):113–130, 2018.

- Zhu et al. [2020] H. Zhu, R. Li, R. Zhang, and H. Lian. Nonlinear functional canonical correlation analysis via distance covariance. Journal of Multivariate Analysis, 180:104662, 2020.

Appendix A Combinatorial CLT with multiple permutations

In this section we derive an analogue of Hoeffding’s combinatorial CLT [37] for tensors with multiple random permutations. We begin with the following assumption:

Assumption 5.

Fix and suppose is a sequence of -tensors satisfying the following conditions:

-

For all and ,

(A.1) -

There is a universal constants such that , for all , and .

Under this assumption we have the following theorem:

Theorem A.1.

Fix and suppose is a sequence of -tensors satisfying Assumption 5. Consider independent random permutations of the set and define

Then, as ,

The proof of Theorem A.1 is given in Section A.1. We first show that by centering , condition (1) in Assumption 5 holds without loss of generality.

Remark A.2.

A.1. Proof of Theorem A.1

For notational convenience we will present the proof of Theorem A.1 for . The proof can be easily extended to general by following the arguments. Hereafter, we will assume is a sequence of -tensors satisfying Assumption 5. We begin by computing .

Lemma A.3.

Suppose Assumption 5 holds. Then

Proof.

Since by Assumption 5, we can always normalize the elements of such that . Hereafter, we will assume is normalized such that . To prove the CLT in Theorem A.1 will use Stein’s method based on exchangeable pairs [13]. The first step towards this is to construct an exchangeable pair for the random permutations . This is done as follows:

-

•

We define . Choose a transposition uniformly at random from the set of transpositions on and define , that is, , , and for .

-

•

Similarly, choose an independent transposition uniformly at random from the set of transpositions on and define .

Lemma A.4.

is an exchangeable pair.

Proof.

Denote by the collection of all permutations of and suppose . Then by the independence between and ,

where the second inequality uses the fact that and are marginally two exchangeable pairs. ∎

Recall that and define

| (A.5) |