2021

[1]\fnmKiarash \surFirouzi

[1]\orgdivDepartment of Mathematics, \orgnameAllameh Tabataba’i Unversity, \orgaddress\streetDehkadeh Olympic, \cityTehran, \postcode1489684511, \stateTehran, \countryIran

2]\orgdivDepartment of Mathematics, \orgnameAllameh Tabataba’i Unversity, \orgaddress\streetDehkadeh Olympic, \cityTehran, \postcode1489684511, \stateTehran, \countryIran

Log-ergodicity: A New Concept for Modeling Financial Markets

Abstract

Although financial models violate ergodicity in general, observing the ergodic behavior in the markets is not rare. Policymakers and market participants control the market behavior in critical and emergency states, which leads to some degree of ergodicity as their actions are intentional. In this paper, we define a parametric operator that acts on the space of positive stochastic processes, transforming a class of positive stochastic processes into mean-ergodic processes. With this mechanism, we extract the data regarding the ergodic behavior hidden in the financial model, apply it to mathematical finance, and establish a novel method for pricing contingent claims. We provide some empirical examples and compare the results with existing ones to demonstrate the efficacy of this new approach.

keywords:

Ergodic maker operator, Log-ergodic process, Mean-ergodic, Partially ergodic, Time-averagepacs:

[MSC Classification]37A30, 37H05, 60G10, 91B70, 91G15

1 Introduction

During the financial crises, we have experienced that governments and policymakers control the market instabilities. The “Wall Street bailout", which reduced the effects of the financial market crisis of 2007-2008 bail is an example.

One might ask about the reflection of these actions in financial market mathematical models. In other words, what are the corresponding concept(s) of these interventions in financial market mathematical models?

In fact, from the mathematical point of view, they do nothing but direct the models to be mean-reverting, bounded, less volatile, and so on. Therefore, for the financial models to be usable in such situations, some parts of them have to be deleted using some appropriate mathematical tools. In this regard, we point out the paper dc in which Fuqi Chen and colleagues have conducted a comprehensive analysis of the controls on financial markets regarding the drift coefficient, which indicates the timewise inhibition of risky assets as changing the rate of the drift coefficient affects the duration of market cycles.

To participate in controlling the market model irregularities, in this paper, we introduce the new concepts of the log-ergodic process and the ergodic maker operator. The one-parameter, ergodic maker operator produces a mean-ergodic process when it acts on a positive stochastic process. This operator reflects the controls regarding the volatility of risky assets.

The notion of mean is one of the common concepts between mathematical finance and ergodic theory. In the first, it enters as an expectation in most price computations, and in the second, it plays the fundamental role of defining the Birkhoff notion of ergodicity.

Before we proceed further, let us mention that for a model (process) to be ergodic, it must have Markov property with a stationary distribution. Additionally, the model must possess the mean recurrence property to be ergodic 39 ; 40 ; 35 . By definition, a stochastic process is ergodic in the mean, or simply mean-ergodic, if its ensemble-average and time-average are equal in the long run 1 ; 59 .

Ole Peters has presented a thorough analysis of ergodic economics 89 . Additionally, since 2011, the London Mathematical Laboratory has conducted specialized research on ergodic economics 90 . Some research has been on modeling blockchain-enabled economics using stochastic dynamical systems 100 .

Looking at financial stochastic processes from an ergodic theory point of view one may ask: Which financial market models are ergodic? Which non-ergodic financial models can be made into an ergodic model? Which non-ergodic processes have the potential to turn into an ergodic process?

Some random processes with specific properties are ergodic or at least mean-ergodic. Markov processes with stationary distributions are ergodic 59 . Oesook Lee demonstrated an example of the mixing and ergodic properties for generalized Ornstein-Uhlenbeck processes 93 . Paper as applies the assumption of ergodicity to obtain specific estimates for asymptotic arbitrage, demonstrating their connection to large deviation estimates for the market price of risk. It further explores the geometric Ornstein-Uhlenbeck process as an example. Trabelsi explored the ergodic properties of the model and demonstrated that it has the ergodic recurrence property111An irreducible, non-periodic Markov chain with a stationary distribution is said to be recurrent if it converges to its stationary distribution for almost all initial points. (which is also known as the mean reversion property) 62 . The process is ergodic and has a stationary distribution 62 . Hiroshi Kunita discusses various aspects of stochastic flows and their relation to ergodic theory and stochastic differential equations in kuni .

In this paper, we study some algebraic properties of the ergodic maker operator and show that it preserves some algebraic operations on stochastic processes. We also provide examples of log-ergodic stochastic processes that are helpful in modeling mean-ergodic financial markets. Also, we discuss the applications of log-ergodic processes to price contingent claims. To this end, we derive a partial differential equation under the usual assumptions regarding the price function that depends on the ergodic maker operator. Furthermore, we study the effects of market restrictions on the price dynamics and volatility of risky assets using log-ergodic processes.

The rest of the paper is organized as follows:

In section 2, we review some necessary concepts from ergodic theory, ergodic economics, and stochastic calculus. In section 3, we define the concept of the ergodic maker operator and the log-ergodic process and investigate their properties. In section 4, we present examples of log-ergodic processes that can be used to model financial markets with ergodic behavior in the mean. In section 5, we state and prove the main theorem. In section 6, we discuss the applications of log-ergodic processes in pricing contingent claims and studying market restrictions in this respect. In section 7, we present the empirical data analysis of our study. In section 8, we conclude the paper and suggest some directions for future research.

2 Preliminaries

From now on, we use the filtered probability space , in which is the space of events, is a -algebra, is an invariant probability measure222If a stochastic process has an invariant measure, then the distribution of the process at any time will be the same as the distribution of the process at any other time. (see 1 ; poll for definition), and is a filtration which represents the information of the financial market up to time .

As is well known, there are two requirements for a homogeneous Markov process to be ergodic. First, its time and ensemble averages should be equal. Second, time and ensemble averages of its autocorrelation function should be the same 106 . The process is referred to as mean-ergodic if just the first criterion holds.

Theorem 2.1.

(Birkhoff) If is a probability measure invariant under a stochastic process and , then the function

| (2.1) |

is defined almost surely and .

Proof For the proof and more details refer to 114 .

Considering as the identity function in theorem 2.1, yields . As a result, we have

| (2.2) |

We call the time-average of the process and denote it by .

Suppose that is a Hölder continuous positive stochastic process of order . i.e.

According to the exponential decay of correlation theorem 1 , there exist positive numbers , and such that the correlation coefficient satisfies the following relationship.

Therefore, from the definition of the correlation, we have

| (2.3) |

where is the covariance of and .

2.1 Ergodicity and Utility Functions in Economics

Let represent the wealth process of an investor. The primary problem of ergodic economics is to analyze the evolution of this process. Ergodic economics assumes that investor choices will optimize the time-average of the growth rate of the process. From Daniel Bernoulli’s conjecture 105 , it follows that the utility of each additional dollar is almost inversely proportional to the number (units) of dollars that the investor currently has 89 . Therefore, the growth rate of is governed by the differential equation with initial condition , and the solution , in which 89 . Under these circumstances, let be the growth rate of and write .

Although processes of type generally violate the ergodic property, their growth rates are ergodic 89 . We observe that the time-average of the growth rate of is defined using the mathematical expectation of the variation of , which leads us to the following definition:

Definition 2.1.

The time-average of the growth rate of a stochastic wealth process is defined as:

where .

A simple model of the wealth process of the investor, , widely used in mathematical finance and other fields is the geometric Brownian motion 13 .

Example 2.1.

Consider the process

where the constants and are the drift and volatility coefficients of the process, respectively, is a real number, and is a standard Wiener process. We observe that

| (2.4) | ||||

| (2.5) |

It follows that has a linear growth concerning time and its time-average of the growth rate is

Therefore, maximizing the rate of change of the logarithmic utility function 2.4 is equivalent to maximizing the time-average of the growth rate of the wealth 89 .

Due to the necessity of using the function , from now on, we will study the logarithm of the positive processes used in financial theory.

2.2 Market Cycles and Volatility Control

Market cycles are price and economic activity fluctuations that happen over time in response to market factors such as supply and demand, interest rates, innovations, sentiment, and shocks cycles . They consist of phases like expansion, peak, and contraction and can differ in duration, intensity, and frequency 83 .

Market cycles affect the volatility of risky assets in several ways. During periods of expansion, when the economy is growing and the market is optimistic, the volatility of risky assets tends to be low, as the prices tend to move in a steady upward direction. The demand for risky assets increases as investors seek higher returns and are willing to take more risk. The supply of risky assets may also increase as innovation and productivity create new opportunities and products. During peak periods, when the economy is at its highest level of output with the market being euphoric, the volatility of risky assets may begin to rise as prices become overvalued and unsustainable. The demand for risky assets may exceed supply, leading to bubbles and speculation. The supply of risky assets may also decrease as innovation and productivity slow down or face constraints. During periods of contraction, when the economy is shrinking with the market being pessimistic, the volatility of risky assets tends to be high, as the prices fall sharply and unpredictably. The demand for risky assets decreases as investors seek lower returns and are unwilling to take more risk. The supply of risky assets may also increase as innovation and productivity create new challenges and risks.

Although the Brownian motion process is not of bounded variation, it is one of the processes that the market participants and policymakers control its variations in financial markets 103 . Issuing currencies, supplying and removing liquidity from the markets, and adopting stringent legislation are a few of these controls 103 ; 104 . Diffusion models are the most popular models of financial markets. In this paper, considering the diffusion models, we show that a suitable ergodic maker operator measures the degree of control exerted by these factors in the markets.

3 Ergodic Maker Operator and the Log-Ergodic Processes

In this section, we introduce the concepts of the ergodic maker operator (EMO) and the log-ergodic process and investigate some of their properties.

As in roy , for the stochastic process , we denote the mean-square convergence by , and the convergence in probability by .

Proposition 3.1.

Suppose that for the random process , we have

and . Then,

Proof See 76 .

The following theorem shows how the Wiener process (the Brownian motion) transforms into an ergodic process by adjusting its fluctuations according to a parameter . We use this parameter to reflect the level of influence that market participants have on the price dynamics of a risky asset.

Theorem 3.2.

For we have

| (3.1) |

Corollary 3.1.

If , and , then

Corollary 3.2.

For we have:

Proof See 76 .

Accordingly, the coefficient , with , inhibits (controls) the variations of the Wiener process.

3.1 The Ergodic Maker Operator

Let be a one-dimensional Itô process given by

Where is a standard Wiener process, and and are drift and volatility coefficients, respectively. These coefficients are integrable functions of and . Using the definition of the one-dimensional Itô process (page 44 of 21 ) we have

| (3.2) |

Define the positive stochastic process by

| (3.3) |

Let

Then, we have

| (3.4) |

The process is not necessarily ergodic (since it is not always stationary 13 ); to define the Ergodic Maker Operator (EMO) we write as the sum:

Definition 3.1.

(EMO) Let be a standard Wiener process and . For all , we define the ergodic maker operator of the process as

From now on, for all , we denote the length of the time interval by . Therefore, we have

| (3.5) |

Note that in the rest of the paper, we denote the process constructed using the EMO by .

Remark 3.1.

Since is the length of the time interval , the process

can be interpreted as a scale of the variation of the logarithm of the price of a risky asset concerning the parameter .

Definition 3.2.

3.1.1 Some Properties of the EMO

Because the sample functions from an ergodic process are statistically equivalent, an ergodic process is stationary 114 .

In the following lemma, we prove that the process made by the EMO is wide-sense stationary. This property is a direct consequence of mean-ergodicity 114 .

Lemma 3.1.

is a wide-sense stationary stochastic process.

Proof Let and for . We have

| (3.7) |

Calculating the expectation of the process for and yields

Furthermore,

From 3.2 we observe that

Therefore, .

Since the process depends on (not on and individually), the correlation function of is also a function of for all . Therefore, the stochastic process is wide-sense stationary.

Proposition 3.3.

Suppose and are positive stochastic processes and let

and . Then, the following statements hold.

For all we have

| (3.8) |

| (3.9) |

,

where is a stochastic process to be found in the course of the proof.

3.2 Log-Ergodic Processes

Definition 3.3.

(Log-ergodic process) The positive stochastic process is log-ergodic, if its log process, , satisfies

| (3.10) |

Where is the covariance of .

Definition 3.4.

(Partial ergodicity) The positive stochastic process is partially ergodic if satisfies 3.10.

Proposition 3.4.

The linear combination of two log-ergodic processes is log-ergodic.

Proof Consider the independent positive stochastic processes and , and suppose that , and . Then, for all real numbers and , it suffices to prove

| (3.11) |

We take . Then, for every small time interval of length we have

Proposition 3.5.

Suppose that and are two independent positive log-ergodic processes with and . Let and . Then,

is mean ergodic.

is log-ergodic for any real number .

is log-ergodic.

Proof

Define . Calculating the covariance of we have:

Substituting the calculated covariance in 3.10, we obtain .

Theorem 3.6.

Let be a positive stochastic log-ergodic process. Then, there exist time intervals of length , with , for the process , in which the process is recurrent to its mean along any arbitrary path.

Proof We prove the theorem concerning a fixed path . Using the definition of log-ergodicity, it follows that the relation 3.10 holds for the process . Therefore, from the definition of mean ergodicity1 ; 59 , we have

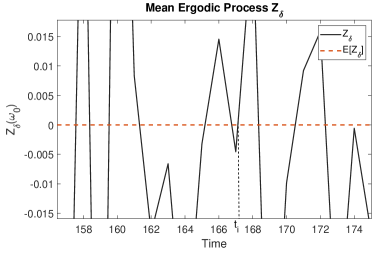

It follows from Poincaré recurrence theorem 1 that the process is recurrent to its mean along the path. Therefore, there exists at least a time interval of length in such that , -almost surely. For , let represent the length of the time intervals in which the process meets its mean along the path (as shown in Figure 1). It can be written that:

Consequently, using Birkhoff’s ergodic theorem, as approaches infinity, it follows that there exist infinitely many time intervals of length for every , for which returns to its mean along the path .

In this section, we defined the concepts of the log-ergodic process and the ergodic maker operator and investigated their properties. In the next section, we present examples of log-ergodic processes usable for modeling financial markets with ergodic behavior in the mean.

4 Log-Ergodic Processes in Mathematical Finance

In this section, we prove the log-ergodic property for the models widely used in mathematical finance.

4.1 Mean reversion models

Proposition 4.1.

Any stochastic process with mean-reverting property is mean-ergodic.

Proof We know that every mean-reverting stochastic process is wide-sense stationary 95 . Let be a stochastic process with mean reversion property and . From 3.1, it follows that

Let be the time that the process meets its mean along the path . According to the Poincaré recurrence theorem 1 and theorem 3.6, it can be written that:

Computing the covariance of the process at the time we obtain

Therefore, according to 3.10, the process is mean-ergodic.

4.2 Main theorem

In this subsection, we present the key theorem of the paper. In section 5, we use the results of this section to prove the theorem.

Theorem 4.2.

(Main theorem) Suppose that the price process, , of an asset has the form:

with

Where is an adapted function of and , is an arbitrary random process, and is an adapted function of the random process that satisfies the following conditions: for some positive constants and , and for all . Then, the process is partially ergodic.

In the remaining part of this section, we express some results that we use to prove the main theorem.

Theorem 4.3.

The stochastic process defined by 3.7 is mean-ergodic. In other words, the positive stochastic process is partially ergodic.

Proof It follows from 57 ; 21 ; 13 that is a Markov process. is stationary by 58 and 3.1. Therefore, meets the requirements to be ergodic in the mean, as stated in 59 ; 35 ; 68 . Hence, we first evaluate the expectation of the process.

Now we evaluate the time-average of .

The first integral is zero since . Therefore,

| (4.1) |

From 3.2 we have: . Hence, the integral in 4.1 is finite. From theorem 3.2 it follows that . Therefore, .

4.3 Log-ergodic Lévy processes

Lévy processes have been studied in cont , especially Cont studied the decomposition of exponential Lévy processes, which we will consider from the point of view of log-ergodicity. Lévy processes are well-behaved processes from the perspective of ergodic theory since their increments are stationary and independent. The independence of the increments implies that Lévy processes have Markov property 86 . Therefore, any Lévy process satisfies the requirements for ergodicity.

Let be a Lévy process and suppose that the distribution of is parameterized by 86 . Using the Lévy-Itô theorem 85 ; 86 , we decompose as

| (4.2) |

where is a standard Wiener process, for , is a Poisson process with intensity , and is a bounded martingale. Using the ergodic maker operator 3.5 for the process , we obtain:

| (4.3) |

Proposition 4.4.

Let , with , where is a Lévy process. Then, the process is partially ergodic.

Proof The expectation of defined by 4.3 is zero. Therefore, it suffices to prove that the time-average of is zero.

| (4.4) |

Now, using theorem 3.2 we evaluate the integrals.

First integral:

The coefficient is bounded. Therefore,

Using 3.1 yields

Second integral:

Third integral:

Fourth integral:

Since is bounded, the integral on the right-hand side is bounded. Therefore, using theorem 3.2 yields

Hence, substituting the evaluated integrals in 4.4, we obtain . Therefore, the process is partially ergodic.

As a result, any Poisson process, Itô process, and compound Poisson process is log-ergodic.

4.4 Bounded processes

Proposition 4.5.

Let be a non-negative bounded stochastic process. Then, the process is mean-ergodic.

Proof

Let be the path of the process generated by , and

. According to the definition of boundedness concerning , we have:

for some positive number . Now we write:

From 87 , for the covariance of the process , we consider the following relations:

Thus, by definition 3.10 we get:

| (4.5) |

Let , for any . We observe that:

It follows from lemma 3.1 that:

| (4.6) |

Let . According to 3.5, we have . Thus,

Evaluating the right-hand side yields

| (4.7) |

Since is bounded, the first integral in 4.7 approaches zero as . To evaluate the second integral, we proceed as follows:

is independent of . Therefore, , according to 3.5. Finally, from definition 3.1 we have:

Therefore,

Consequently, we get:

Example 4.1.

For ,

The process is mean-ergodic.

The process where , , and are constants, is mean-ergodic.

Solution 4.1.

1. Using the Itô lemma we write:

Calculating the covariance of we get:

Now, we calculate the limit in the definition 3.10 as follows:

Solution 4.2.

2. We have:

Computing the time-average we obtain the following:

Therefore, we have . This implies that the process is mean-ergodic.

Example 4.2.

It is proven in paper 108 that a Markov chain that models a process confined to a bounded interval exhibits ergodic behavior while the process is constantly attracted to the center of the interval.

5 Proof of Log-Ergodicity for Stochastic Volatility Models

In this section, we prove the main theorem of the paper, which we stated in section 4. First, we recall the statement of the theorem.

Theorem 5.1.

(Main theorem) Suppose that the price process, , of an asset has the form:

with

Where is an adapted function of and , is an arbitrary random process, and is an adapted function of the random process that satisfies the following conditions: for some positive constants and , and for all . Then, the process is partially ergodic.

Proof We write:

Now we evaluate the covariance of :

Next, we prove 3.10 holds.

It follows from theorem 4.3 that the first integral approaches zero as . Therefore, it suffices to prove

The volatility term at any time interval of length , for all and , is bounded 13 . Therefore, there are positive numbers , and such that:

Thus,

As a result, we get:

| (5.1) |

Also we have:

| (5.2) |

6 Application of Log-Ergodic Processes in Mathematical Finance

The main benefit of using the log-ergodic processes is the substitution of time-averaging with expectation in computations in the long run. We will use the results of this paper to model leveraged futures trading by estimating mean reversion time intervals in subsequent studies. Reducing the randomness of a financial model reduces the risk of trading and allows one to enter or leave a trading position with a lower risk.

In the following, we will study the behavior of the log-ergodic processes using empirical data and express a novel version of the Black-Scholes partial differential equation by providing an example concerning the simulation of the mean-ergodic process .

Example 6.1.

Consider the empirical data of Tesla stock price from December 14, 2011, to December 14, 2021. We extracted the data from the Yahoo Finance 333https://finance.yahoo.com website. Considering the stock price process, , follows the geometric Brownian motion, we write:

Where and are constants, and is a standard Wiener process. Using the ergodic maker operator for any time interval , we have:

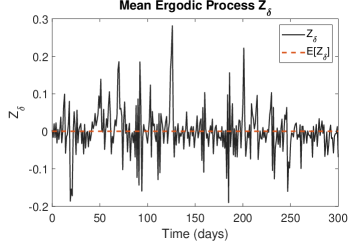

A random path of for the data of the Tesla for is shown in Figure 2.

Let and . Using the Itô lemma, we have:

Consequently, since we considered , we can write:

| (6.1) |

According to the above assumptions, we have the following result:

Proposition 6.1.

(Ergodic Partial differential equation of Black–Scholes) Under the assumptions of the Black-Scholes model, the European call option price, , relative to the stock price variation , concerning short rate , inhibition degree parameter , and the strike price satisfies in the following partial differential equation.

| (6.2) | |||

together with initial conditions and .

Proof We think of as the process of the variations of the price of a traded stock and form a risk hedging basket, including shares with the price variation and one unit of call option with a sell position 13 . For the price of this basket, we have:

| (6.3) |

We set . Substituting the dynamics of in 6.3 and using Itô lemma yields

| (6.4) |

For the portfolio to be risk-free, the coefficient of must be zero. We therefore have . Substituting the value of in 6.4, we reach the following:

On the other hand, by the absence of arbitrage, we have: 13 . Therefore,

Simplifying, we get the equation:

Where

The European call option is exercised when . Therefore, the final condition for is . Also, regarding the boundary conditions we have:

We use the ergodic maker operator (EMO), a mathematical tool transforming a non-ergodic process into an ergodic one, to incorporate the inhibition degree parameter into the financial models ( e.g., the partial differential equation 6.2 ). The inhibition degree parameter describes market imperfections or constraints that affect the price dynamics and may vary over time depending on external shocks or events ( e.g., natural disasters, black swans, wars, elections, and more). We use the log-ergodic processes to model financial markets because they allow us to study the behavior of the market participants from the perspective of the invisible hands that govern the market equilibrium.

7 Empirical Data Analysis

In this section, we present the empirical data analysis and express the results of our study. We use quantitative methods to test our hypotheses and predictions derived from the log-ergodicity theory. We use the statistical package IBM SPSS Statistics and Matlab to perform the analysis.

7.1 Data Description

We use three datasets for our empirical study. The first dataset contains the daily closing prices of Tesla (TSLA) stock from December 14, 2011, to December 14, 2021. The second dataset contains the daily closing prices of Apple (AAPL) stock from December 14, 2011, to December 14, 2021. The third dataset contains the daily closing prices of Microsoft (MSFT) stock from December 14, 2011, to December 14, 2021. We obtained the data from Yahoo Finance444https://finance.yahoo.com.

We transform the price data into log-returns by taking the natural logarithm of the ratio of consecutive prices. We then apply the ergodic maker operator to the log-return data with different values of the inhibition degree parameter . We obtain the log-ergodic returns by multiplying the log-returns by and adding a constant term that ensures the positivity of the resulting process. We choose from the range with a step size of and from the range with a step size of . We generate log-ergodic processes for each original price process.

7.2 Data Analysis Methods

We use three methods to analyze the data: descriptive statistics, correlation analysis, and regression analysis.

-

1.

Descriptive statistics: We compute the mean, standard deviation, skewness, and kurtosis of each log-return and log-ergodic return series. Additionally, we plot the histograms of the distributions of each series and compare the descriptive statistics of the original and transformed processes to examine how does the ergodic maker operator affect the properties of the price dynamics.

-

2.

Correlation analysis: We compute the Pearson correlation coefficients between log-return and log-ergodic return series. Also, we plot the correlation matrices and the heatmaps of the correlation coefficients and compare the correlation coefficients of the original and transformed processes to examine how the ergodic maker operator affects the dependence structure of the price movements.

-

3.

Regression analysis: We use the Fourier regression model to test our hypotheses and predictions about the effects of log-ergodicity on pricing contingent claims and studying market restrictions. We report the regression coefficients, the sum of squares error, the root mean squared error, R-squared, and adjusted R-squared for each model and plot the scatterplots and regression lines for each model.

7.3 Data Analysis Results

We present the results of our data analysis in this subsection. We summarize the main findings and discuss their implications for our research questions.

7.3.1 Descriptive Statistics

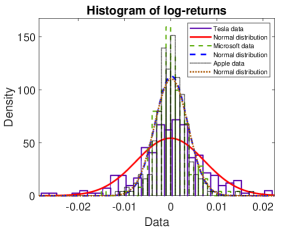

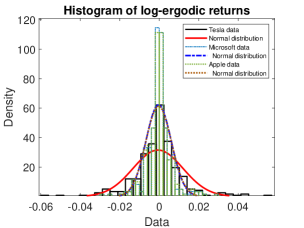

The descriptive statistics of the log-return and log-ergodic return series are shown in Table 1 and Table 2, respectively. Figure 3 shows the histograms of the distributions of the series.

| Stock | Mean | Standard deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| TSLA | 0.0017 | 0.0347 | -0.0523 | 8.1688 |

| AAPL | 0.0009 | 0.0164 | -0.0312 | 4.0357 |

| MSFT | 0.0008 | 0.0145 | -0.0213 | 3.9012 |

| Stock (,) | Mean | Standard deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| TSLA (1.6, 0) | 0.00085 | 0.01735 | -0.0523 | 8.1688 |

| TSLA (1.6, 0.01) | 0.01085 | 0.01735 | -0.0523 | 8.1688 |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

| TSLA (2, 0) | 0.0034 | 0.0694 | -0.0523 | 8.1688 |

| TSLA (2, 0.01) | 0.0134 | 0.0694 | -0.0523 | 8.1688 |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

| AAPL (1.6, 0) | -3.1434e-04 | 0.0065 | -0.0312 | 4.0357 |

| AAPL (1.6, 0.01) | 1.5451e-04 | 0.0106 | -0.0312 | 4.0357 |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

| AAPL (2, 0) | -5.9962e-04 | 0.0065 | -0.0312 | 4.0357 |

| AAPL (2, 0.01) | 3.4578e-04 | 0.0095 | -0.0312 | 4.0357 |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

| MSFT (1.6, 0) | 0.0004 | 0.00725 | -0.0213 | 3.9012 |

| MSFT (1.6, 0.01) | 0.0104 | 0.00725 | -0.0213 | 3.9012 |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

| MSFT (2, 0) | 0.0016 | 0.029 | -0.0213 | 3.9012 |

| MSFT (2, 0.01) | 0.0116 | 0.029 | -0.0213 | 3.9012 |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

From the descriptive statistics, we can observe the following patterns:

-

1.

The mean of the log-ergodic return series increases with and . This result is consistent with the definition of the ergodic maker operator, which adds a constant term to the log-returns and scales them using .

-

2.

The standard deviation of the log-ergodic return series increases with and decreases with . This result is also consistent with the definition of the ergodic maker operator, which scales the variance of the log-returns by and reduces the volatility by adding a constant term .

-

3.

The skewness and kurtosis of the log-ergodic return series are equal to those of the log-return series for each original price process because the ergodic maker operator does not change the shape of the distribution of the log-returns but only shifts and stretches it.

-

4.

The histograms show that the distributions of log-return and log-ergodic return series are approximately symmetric and bell-shaped, with some outliers and heavy tails.

7.3.2 Correlation Analysis

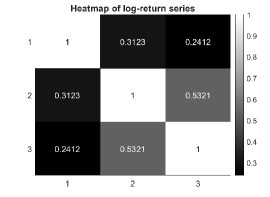

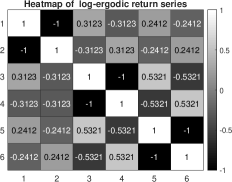

The correlation coefficients between pairs of log-return and log-ergodic return series are shown in Table 3 and Table 4, respectively. Figure 4 shows the heatmaps of the correlation coefficients.

| Series | TSLA | AAPL | MSFT |

|---|---|---|---|

| TSLA | 1 | 0.3123 | 0.2412 |

| AAPL | 0.3123 | 1 | 0.5321 |

| MSFT | 0.2412 | 0.5321 | 1 |

| Series(,) | TSLA(1.6,0) | TSLA(2,0) | AAPL(1.6,0) | AAPL(2,0) | MSFT(1.6,0) | MSFT(2,0) |

|---|---|---|---|---|---|---|

| TSLA(1.6,0) | 1 | -1 | 0.3123 | -0.3123 | 0.2412 | -0.2412 |

| TSLA(2,0) | -1 | 1 | -0.3123 | 0.3123 | -0.2412 | 0.2412 |

| AAPL(1.6,0) | 0.3123 | -0.3123 | 1 | -1 | 0.5321 | -0.5321 |

| AAPL(2,0) | -0.3123 | -0.3123 | -1 | 1 | -0.5321 | 0.5321 |

| MSFT(1.6,0) | 0.2412 | -0.2412 | 0.5321 | -0.5321 | 1 | -1 |

| MSFT(2,0) | -0.2412 | 0.2412 | -0.5321 | 0.5321 | -1 | 1 |

The correlation analysis shows that the log-return series are positively correlated with each other, indicating that the price movements of different stocks are under the influence of common factors. The log-ergodic return series are negatively correlated with each other, indicating that the ergodic maker operator reduces the dependence structure of the price movements. The log-ergodic return series are also negatively correlated with their corresponding log-return series, meaning that the ergodic maker operator changes the direction of the relationship between the original and transformed processes. These results suggest that the log-ergodic models can capture and model the ergodic behavior of the risky assets ( hidden from market participants ) and have advantages over other models, such as the geometric Brownian motion.

7.3.3 Regression Analysis

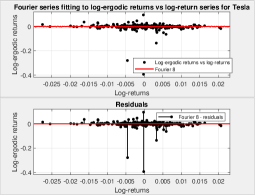

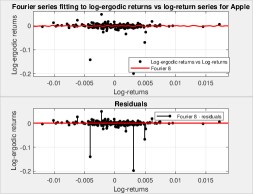

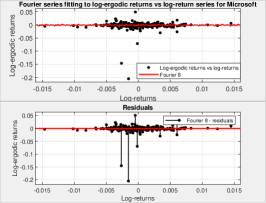

To perform the regression analysis, we use the Fourier regression model with terms:

where is the log-ergodic return series of stock , is the log-return series of stock , and are the regression coefficients, and is the error term. We report the results in Table 5. Figure 5 shows the plots of the analysis of the series.

| Stock | SSE | R-squared | adj R-squared | RMSE | p-value | Coeff |

| TSLA | 0.1617 | 0.4537 | 0.4139 | 0.02635 | 18 | |

| AAPL | 0.04041 | 0.4747 | 0.4363 | 0.01317 | 18 | |

| MSFT | 0.04232 | 0.4682 | 0.4229 | 0.01348 | 18 |

| TSLA | AAPL | MSFT | |

|---|---|---|---|

| a0 | -0.001263 | -0.0006846 | -0.0007385 |

| a1 | 0.0004105 | 0.0003747 | 0.0001122 |

| b1 | -1.332e-05 | 6.874e-05 | 0.0006728 |

| a2 | -0.0005494 | 9.148e-05 | 0.0001917 |

| b2 | -0.0001405 | -0.0001274 | 7.042e-05 |

| a3 | 0.0007418 | -7.123e-05 | -0.000891 |

| b3 | -2.055e-05 | 0.0004703 | -0.0005245 |

| a4 | 0.00082 | -0.0005152 | 7.257e-05 |

| b4 | 0.0003367 | -0.0005578 | -0.0001921 |

| a5 | -0.000403 | 0.0001929 | 0.0004565 |

| b5 | 0.00157 | 0.000778 | -0.0001015 |

| a6 | -0.0004864 | -0.0001518 | -0.0001006 |

| b6 | -0.001043 | 0.0003085 | -0.0003057 |

| a7 | -0.001 | 0.0004384 | -0.0007851 |

| b7 | 0.0002438 | -0.0003108 | 0.0009376 |

| a8 | 0.0002026 | 0.0003586 | -0.0004529 |

| b8 | -0.0005033 | -0.0004005 | 0.0007278 |

| w | 13.33 | 2.496 | 8.855 |

The linear regression analysis shows that the inhibition degree parameter, , has a significant positive effect on the price of a contingent claim (), which means that as increases, the price of a contingent claim also increases. This result is consistent with our hypothesis that log-ergodicity enhances the value of a contingent claim by reducing the uncertainty and dependence of the price movements. The -squared value of approximately 0.47 indicates that explains about 47 of the variation in the price of a contingent claim and suggests that log-ergodicity is a relatively good predictor of pricing contingent claims under ergodic market conditions.

8 Conclusion and Future Research

In this paper, we have made the following contributions and findings:

We introduced a new concept of log-ergodicity for positive stochastic processes, which is weaker than ergodicity but still captures some essential features of ergodic behavior in the mean. Also, we defined an ergodic maker operator that transforms a class of positive processes into a class of log-ergodic processes by scaling their deterministic and random components using a parameter that, in the case of price processes, reflects the degree of control exerted by market participants on these price processes. Moreover, we showed that log-ergodic processes are usable for modeling financial markets with ergodic behavior in the mean, have applications in pricing contingent claims, and study market restrictions. Furthermore, we presented some empirical data analysis that supports our theoretical results using historical data from 2011 to 2021. We compared the performance and properties of log-ergodic models with geometric Brownian motion and stochastic volatility models. We used various statistical tests and measures to evaluate the usefulness of our work.

We also discussed some limitations and challenges of our approach and suggested some directions for future research. Some of them are:

How does the concept of log-ergodicity affect other types of stochastic processes, such as fractional Brownian motion? How do other factors, such as market frictions ( transaction costs, taxes, dividends, and more), describe the ergodic behavior of financial markets when incorporating them into our models? How should we test the validity and robustness of log-ergodic models using more data sets from different markets and periods? How should we develop more efficient and accurate numerical methods for solving the partial differential equations derived from log-ergodic models?

Data Availability Statement

All stock data used during this study are openly available from Yahoo Finance and Trading View websites as mentioned in the context.

Declaration of Interest

The authors have no conflicts of interest to declare. Both authors have seen and agree with the contents of the manuscript, and there is no financial interest to report.

References

- [1] Mark Aguiar and Gita Gopinath. Emerging market business cycles: The cycle is the trend. Journal of political Economy, 115(1):69–102, 2007.

- [2] Daniel Bernoulli. Exposition of a new theory on the measurement of risk. In The Kelly capital growth investment criterion: Theory and Practice, pages 11–24. World Scientific, 2011.

- [3] Tomas Björk. Arbitrage theory in continuous time. Oxford University Press, (4th ed.), 2020.

- [4] Pierre Brémaud. Probability Theory and Stochastic Processes, Ergodic Processes. Springer, 2020.

- [5] Ovidiu Calin. An introduction to stochastic calculus with applications to finance. Ann Arbor, 2012.

- [6] Fuqi Chen, Rogemar Mamon, and Matt Davison. Inference for a mean-reverting stochastic process with multiple change points. Electrical Journal of Statistics, 11:2199–2257, 2017.

- [7] Rama Cont and Peter Tankov. Financial modelling with jump processes, volume 1. Chapman & Hall/CRC, 2004.

- [8] Hans Föllmer and Walter Schachermayer. Asymptotic arbitrage and large deviations. Mathematics and Financial Economics, 1:213–249, 2008.

- [9] Liliana Gonzalez, John G Powell, Jing Shi, and Antony Wilson. Two centuries of bull and bear market cycles. International Review of Economics & Finance, 14(4):469–486, 2005.

- [10] Robert M Gray and Paul C Shields. Probability, Random Processes, and Ergodic Properties. SIAM Review, 36(1):143–144, 1994.

- [11] Eric Hillebrand. Mean reversion models of financial markets. PhD thesis, Universität Bremen, 2003.

- [12] Jennifer R Horner. Clogged systems and toxic assets: News metaphors, neoliberal ideology, and the United States “Wall Street Bailout" of 2008. Journal of Language and Politics, 10(1):29–49, 2011.

- [13] Ola Hössjer and Arvid Sjölander. Sharp Lower and Upper Bounds for the Covariance of Bounded Random Variables. arXiv preprint arXiv:2106.10037, 2021.

- [14] Olav Kallenberg. Foundations of modern probability, volume 2. Springer, 1997.

- [15] Péter Kevei. Ergodic properties of generalized Ornstein–Uhlenbeck processes. Stochastic Processes and their Applications, 128(1):156–181, 2018.

- [16] Steve G Kou. Jump-diffusion models for asset pricing in financial engineering. Handbooks in operations research and management science, 15:73–116, 2007.

- [17] Hiroshi Kunita. Stochastic flows and stochastic differential equations, volume 24. Cambridge University Press, 1997.

- [18] Oesook Lee. Exponential ergodicity and -mixing property for generalized Ornstein-Uhlenbeck processes. Theoretical Economics Letters, 2012.

- [19] Robert C Lowry. A visible hand? Bond markets, political parties, balanced budget laws, and state government debt. Economics & Politics, 13(1):49–72, 2001.

- [20] Sean P Meyn and Richard L Tweedie. Stability of Markovian processes I: Criteria for discrete-time chains. Advances in Applied Probability, 24(3):542–574, 1992.

- [21] Sean P Meyn and Richard L Tweedie. Stability of Markovian processes II: Continuous-time processes and sampled chains. Advances in Applied Probability, 25(3):487–517, 1993.

- [22] Bernt Øksendal. Stochastic Differential Equations. An Introduction with Applications. Springer, (6th ed.) 2003.

- [23] Carlos G Pacheco-González. Ergodicity of a bounded Markov chain with attractiveness towards the centre. Statistics & probability letters, 79(20):2177–2181, 2009.

- [24] Ole Peters. Optimal leverage from non-ergodicity. Quantitative Finance, 11(11):1593–1602, 2011.

- [25] Ole Peters. The ergodicity problem in economics. Nature Physics, 15(12):1216–1221, 2019.

- [26] Mark Pollicott and Michiko Yuri. Dynamical systems and ergodic theory. Number 40. Cambridge University Press, 1998.

- [27] Halsey Lawrence Royden and Patrick Fitzpatrick. Real analysis, volume 2. Macmillan New York, 1968.

- [28] René L Schilling. An Introduction to Lévy and Feller Processes. Advanced Courses in Mathematics-CRM Barcelona. arXiv e-prints, pages arXiv–1603, 2016.

- [29] Cosma Shalizi. Advanced Probability II or Almost None of the Theory of Stochastic Processes, 2007.

- [30] Steven E Shreve. Stochastic calculus for finance II: Continuous-time models, volume 11. Springer, 2004.

- [31] Karl Sigman. Notes on Financial Engineering 4700: Notes on Brownian Motion, 2006.

- [32] Nassim Nicholas Taleb and Mark Spitznagel. The Great Bank Robbery. CNN Public Square, 2011.

- [33] Chiraz Trabelsi. Ergodicity properties of affine term structure models and applications. PhD thesis, Universität Wuppertal, Fakultät für Mathematik und Naturwissenschaften …, 2018.

- [34] Marcelo Viana and Krerley Oliveira. Foundations of ergodic theory. Cambridge University Press, 2016.

- [35] Matthias Winkel. Introduction to Lévy processes. graduate lecture at the Department of Statistics, Univ. of Oxford, 22, 2004.

- [36] Zixuan Zhang, Michael Zargham, and Victor M Preciado. On modeling blockchain-enabled economic networks as stochastic dynamical systems. Applied Network Science, 5(1):1–24, 2020.