Dynamic Equilibrium with Insider Information and General Uninformed Agent Utility

Abstract.

We study a continuous time economy where agents have asymmetric information. The informed agent (“”), at time zero, receives a private signal about the risky assets’ terminal payoff , while the uninformed agent (“”) has no private signal. is an arbitrary payoff function, and follows a time-homogeneous diffusion. Crucially, we allow to have von Neumann-Morgenstern preferences with a general utility function on satisfying the standard conditions. We prove existence of a partial communication equilibrium (PCE), where at time , receives a less-informative signal than . In the single asset case, this signal is recoverable by viewing the equilibrium price process over an arbitrarily short period of time, and hence the PCE is a dynamic noisy rational expectations equilibrium. Lastly, when has power (constant relative risk aversion) utility, we identify the equilibrium price in the small and large risk aversion limit.

1. Introduction

The study of economies with asymmetric information has historically focused on the static Exponential-Gaussian framework with exogenous noise trading. In this model uninformed agents () and informed agents () have exponential (constant absolute risk aversion or “CARA”) utility, and the private signal, asset terminal payoff and noise trader demand are jointly normally distributed. Recent advances extend results beyond Gaussian terminal payoffs ([4]) and to dynamic, diffusion-based models where noise traders display endogenous behavior ([7]). However, the CARA utility structure is retained. In this paper, we generalize [7] to allow the uninformed agent to have von Neumann-Morgenstern (vNM) preferences with a general utility function on satisfying standard conditions. In this setting, we examine the existence and properties of equilibria.

The information conveyed by prices plays a fundamental role in economics. It determines the investment opportunities of agents in markets and informs managerial decision-making within firms. The degree of informational efficiency of prices, i.e., the extent to which prices reveal information disseminated in the economy, is widely thought to be a critical ingredient for smooth market and economic operations. Yet, studies of economies with asymmetric information, even those providing recent advances, remain limited to the CARA utility model, thus raising questions about the broad applicability of conclusions. Generalizations along the preference dimension are therefore desirable in order to assess the robustness and limits of prior results. This paper takes a step in this direction. While it maintains the CARA behavior of informed agents and noise traders , it allows for uninformed agents with vNM preferences where the utility function satisfies standard monotonicity, concavity, Inada and asymptotic elasticity conditions.

The paper contributes on three fronts. First, we prove the existence of a partial communication equilibrium (PCE) in which a noisy version of the informed agent’s signal is released at the outset. The PCE (as opposed to an equilibrium where all agents have identical information), is of interest as it preserves the informed agent’s informational advantage. This result is valid under mild conditions upon the underlying diffusion , terminal payoff function and uninformed agent utility function, see Assumptions 2.1, 2.3 and 2.6 below. An important feature of this equilibrium, and one that does not hold under CARA utility, is that when the uninformed agent has a general utility function, his policy depends on his initial wealth, and hence on the initial price vector, as agents are endowed with exogenous initial share endowments, rather than exogenous initial wealth. It follows that the equilibrium price, as well as its volatility and the market price of risk, at any date, depend on the initial endowment as well. Therefore, our results enable the study of endowment effects on equilibrium quantities, something that is not possible in the CARA setting.

Second, focusing on the single asset case, we show the PCE is in fact a dynamic noisy rational expectations equilibrium (DNREE). What this means is that the filtration used by (the market filtration) coincides with that generated by the underlying economic factor process (diffusion ) and the equilibrium price process. This in turn, provides a mechanism for information communication through the endogenously determined equilibrium price. That the endogenous price reveals the public signal holds because the price path over any arbitrarily small interval cannot be the same for different realizations of the signal. Revelation of the public signal ensures that equilibrium filtrations for the informed and uninformed agents correspond to those in the PCE, implying the two equilibria coincide.

Third, we derive a quasi-explicit (in terms of the Lambert function) solution when has constant relative risk aversion (CRRA), i.e., when the economy is comprised of a mixture of CRRA and CARA agents. In this context, we identify the equilibrium price in the limit as relative risk aversion either explodes or vanishes. When ’s risk aversion goes to infinity, the agent seeks certainty, implying equilibrium is driven by the behavior of the two CARA agents. The limit equilibrium price is then the same as in an economy with just the two CARA agents. When ’s risk aversion vanishes, the limit equilibrium price does not correspond to the risk neutral price, as might have been intuitively expected. The reason it departs from it is because CRRA utility enforces a non-negative wealth constraint, which does not vanish in the small risk aversion limit.

Methodologically, we contribute by relating an equilibrium where agents have differing information sets, to one where agents have identical information but differ in their beliefs and/or random endowments. Heuristically, this is because for two random variables such that almost surely with density , then on the set , one has . This enables us to first establish the existence of a “signal-realization” equilibrium where agents have common information, using classical results on optimal investments in complete markets. We then lift the signal realization equilibrium to the signal level, by using delicate measurability arguments for parameter driven stochastic integrals, as can be found in [24, 1, 8, 7]. In particular, our method essentially imposes no integrability restrictions on the insider and market signals, a desirable outcome as equilibrium is established conditioned on these signals. The only cost to this is that we use generalized conditional expectations when defining the sets of acceptable trading strategies. However, as discussed in Remark 3.1, the use of generalized conditional expectations is natural to the problem. We hope this methodology can be used in the future to extend beyond the CARA insider case.

The paper relates to three branches of the asset pricing theory literature. First, it connects directly with [7], which proves existence and properties of equilibria in dynamic CARA-diffusion models with bounded rational noise trading. That paper shows in particular existence of a DNREE if the (vector) payoff function is linear in the underlying (vector) factor, or in the one asset case if it is monotonic with respect to the single underlying factor. Here, we extend the analysis by allowing for uninformed agents with general utility functions satisfying standard Inada and elasticity conditions and arbitrary payoff function satisfying the Jacobian condition. We also show that a DNREE exists in the single asset case, and prove that a vehicle for revelation is the asset price. Equilibria display the same informational content as in the pure CARA model, establishing robustness along the uninformed agent’s preferences dimension.

Second, it relates more generally to the broad literature on asymmetric information. Pioneering contributions by [9] and [11] respectively show the existence of a fully revealing and a noisy rational expectations equilibrium in the static CARA-Gaussian setting. An early departure from that classic setting can be found in [22], a paper that introduces the notion of full communication equilibrium (FCE) and establishes its relation to the concept of rational expectations equilibrium. Our notion of PCE is a direct extension of FCE. Recent contributions, while maintaining the CARA setting, provide extensions to non-Gaussian distributions. Notable studies along these lines include [4] and [5]. Our analysis differs in terms of generality pertaining to the uncertainty structure, the uninformed agent’s preferences with non-CARA utility, and the temporal setting. The second aspect implies price dynamics that depend on initial prices, a significant complication. The third element mandates that markets be proven to be endogenous complete. Our proof of existence overcomes these two hurdles

Finally, it also relates to the general literature on existence and uniqueness of Arrow-Debreu equilibria in the standard model with homogeneous information, notably [12], [15] and [16] for dynamic models. Original contributions in that area focused on static economies and can be found in [3] and [20].

The paper is organized as follows. Section 2 presents the model, main assumptions and equilibrium definitions. Section 3 precisely states the optimal investment problems. Section 4 states the main result, and derives the equilibrium clearing condition central to the analysis. Section 5 constructs solutions to the market clearing condition at the signal realization level. Section 6 establishes the existence of a PCE and Section 7 shows the PCE is a DNREE. Section 8 identifies prices when has CRRA utility as the risk aversion tends to zero and infinity. Section 9 contains an example when the terminal payoff is that of a Geometric Brownian motion. Short proofs are in the main text, while longer proofs are in Appendices A-D.

2. Setup

The factor process and terminal payoff

Fix an integer . The underlying probability space supports a -dimensional Brownian motion , and we denote by the -augmentation of ’s natural filtration. The underlying factor process is a time homogeneous diffusion taking values in , and satisfying the SDE

where we assume

Assumption 2.1.

The drift function is bounded and uniformly Lipschitz. The volatility function is bounded, uniformly Lipschitz, and invertible for each . Furthermore, the map is bounded.

Remark 2.2.

Our requirements ensure a unique strong solution taking values in for any starting point . Also, the conditions on (as well the requirements in Assumption 2.3 below) are primarily enforced to invoke the non-degeneracy results of [16, 26]. Beyond smoothness, well posed-ness and local ellipticity, our requirements may be relaxed to the same extent as they could to use the conclusions of [16, 26].

The investment horizon is for fixed. The risky assets have outstanding supply and terminal payoff for a given function . In addition to the risky assets, the agents may also invest in a money market account with exogenous interest rate . Regarding the payoff function we assume

Assumption 2.3.

is and such that . Additionally, the Jacobian of is of full rank for Lebesgue almost every and there is such that both and , where .

Remark 2.4.

We require because the uninformed agent has preferences defined only for positive wealth.

Remark 2.5.

Though not apparent at first, our assumptions cover when is an OU process. Indeed, in terms of model primitives, is only used through its terminal value , which appears both in the terminal payoff and the insider signal . Thus, we can switch from to where , and calculation shows that if then . Though has time dependent volatility, the volatility function satisfies the analyticity assumptions in [16] and regularity assumptions in [26], and hence results go through using instead of .

Continuing, we may also handle when the terminal payoff is that of a geometric Brownian motion. Indeed, this corresponds to for a certain vector and matrix ,111In other words, the insider’s signal is multiplicative, rather than additive, in the terminal stock price. and . Clearly satisfies Assumption 2.1 and satisfies Assumption 2.3. This specification is considered in Section 9 below.

Agents and signals

At time , there is an insider, or informed agent “” who observes the private signal

There is also a uninformed agent “” who possesses no private signal. Lastly, there is a misinformed agent, or noise trader “” who thinks he receives at , but in actuality receives

Above, and the set of strictly positive definite symmetric matrices. While we allow for general , our noise trader specification is primarily made to incorporate two cases of interest. First, when . This corresponds to the noise trader mis-perceiving his signal precision. Second, when . This corresponds to when the noise trader receives a truly independent signal, but one with the same first two moments as .

and have CARA, or exponential, utilities with respective risk aversions .222Exponential utility corresponds to the utility function so that the absolute risk aversion is the constant . As is standard in the literature, to justify the price taking assumption that agents do not internalize their impact on prices, we assume agents are representative of a group of identical, “small” agents and that collectively, the insider and noise traders have respective weights in the economy of . The uninformed agent has weight in the economy of and preferences dictated by a utility function, which we also label . Regarding , we make the standard assumptions, as in [17].

Assumption 2.6.

is , strictly increasing, strictly concave, satisfies the Inada conditions , as well as the asymptotic elasticity condition .

Remark 2.7.

Our results easily extend to when the domain of is for . We take for notational ease. While our assumptions do not cover CARA preferences for , this case was extensively studied in [7].

Agent is endowed at time with a constant shares in the risky asset, and no position in the money market. The positions are consistent with market clearing in that

Agents maximize utility from terminal wealth given their information, and other than the share position, have no endowments.

Remark 2.8.

Similarly to Remark 2.4, we require . This allows the uninformed agent to not trade if he wishes.

Equilibrium definition

We now define the partial communication equilibrium (PCE) and dynamic noisy rational expectations equilibrium (DNREE), starting with the PCE. To avoid technicalities, at this point we take the information sets, price process, as well as the sets of acceptable trading strategies as given. In the next section, each will be precisely defined.

In the PCE, there is a (to-be-determined) market filtration enlarging and satisfying the usual conditions. This is the filtration used by . The insider uses the filtration , the initial enlargement of with respect to the private signal . The idea behind enlarging is that a portion of the insider’s private information is communicated at the outset to the uninformed agent. The (to-be-determined) price process is a continuous semi-martingale. and identify their respective trading strategies by maximizing expected utility from terminal wealth, given their respective initial information sets .

As for , a consequence of our noise trader convention (see [7, Remark 2.2] for additional discussion) is that if has optimal strategy where is measurable333 is the predictable sigma field and are the Borel sets., then . In words, the noise trader (modulo risk aversion) uses the same “signal to strategy” function as the insider. However, he plugs an incorrect signal into the function. This means he acts like an informed agent with characteristics , processing as if it were the true signal .

With this notation, we define

Definition 2.9.

is a Partial Communication Equilibrium (PCE) if

| (2.1) |

and if .

The idea behind the strict informational set inclusions is that, in a PCE, the market is provided information in addition to that given by the factor process, but the insider still has the finest information set. This rules out the unrealistic (though possible - see [7, Section 3]) case when the insider’s signal is completely passed to the market so . We next turn to the DNREE

Definition 2.10.

is a Dynamic Noisy Rational Expectations Equilibrium (DNREE) if (2.1) holds and if , where is the right-continuous enlargement of the filtration generated by and .

We see that a DNREE prevails if the market signal is recoverable at time (i.e. for any time ) based upon market observable quantities. This provides a mechanism for transmission of the market signal. Note also that by right-continuity of we know that automatically. Thus, under a DNREE we have . Lastly, we must use the right-continuous enlargement of because it might not be true that either is right continuous or (more importantly) that the incremental informational content of relative to is measurable.

3. The Optimal Investment Problems

Price process and martingale measures

Before defining the optimal investment problems, we must first derive the candidate PCE market filtration and price process . To this end, assume there is a signal ( is explicitly defined in (4.2) below) communicated to the market at time , and which satisfies the Jacod condition almost surely on (c.f. [13]), with density

| (3.1) |

This defines the market filtration . The insider has filtration , where we assume is also such that the Jacod condition holds almost surely on ,444Both and satisfy the usual conditions, see [1, Proposition 3.3] and [8, Lemma 4.2]). writing

Next, let the candidate equilibrium price process be a continuous semi-martingale taking the form

| (3.2) |

where is a to-be-determined measure equivalent to on . This will determine the equilibrium dynamics

| (3.3) |

where is a Brownian motion and are predicable processes. This implies is the volatility and the market price of risk. Our goal is to obtain enforcing the PCE. To do so, a key role is played by the to martingale preserving measure (see [21, 2, 1]) , defined through

Motivated by the Markovian environment, we assume takes the form

| (3.4) |

where is a to-be-determined function such that . We define in this manner because direct calculations show for all test functions and

| (3.5) |

which enables us to go back and forth between conditioning on (i.e. knowing ) and conditioning on (i.e. not knowing ) but fixing a realization of . By taking we obtain

| (3.6) |

which shows the conditional law of and conditional law of coincide. With so defined, we may define the price process as in (3.2) and is a martingale measure.

has filtration , and for any martingale measure as in (3.4) one may construct an associated martingale measure with terminal density

| (3.7) |

This is because, for such , one has for and measurable, integrable that (see [7, Lemma S4.8])

| (3.8) |

In particular, this implies that if is a local martingale, then it is also a local martingale, as the two measures agree on conditional expectations (with their own information sets) of market measurable quantities.

Optimal investment problems

Having defined the price process and candidate martingale measures, we may now define the optimal investment problems. To motivate our definition, note that at time , agents have already received their signals. Therefore, expectations are conditional expectations with respect to time 0 information sets, and as the wealth processes depend on the random variables we do not want want to require integrability conditions that treat as random variables.

Let us introduce some notation, valid on a general probability space with sub-sigma algebra . First, recall that conditional expectations of non-negative random variables are always well defined. Next, for define the set

and the class of functions

For the conditional expectation of given is well defined setting , and .

With this notation, let us start with . Because has CARA preferences, her initial share endowment plays no role in her optimal investment problem, and she solves

| (3.9) |

where

and where the admissible class of trading strategies is555All inequalities between random variables are assumed to hold almost surely.

| (3.10) |

We next consider , for whom the initial share endowment does not factor out of the objective function. Here, his allowable trading strategies are

then has the optimal investment problem

| (3.11) |

Remark 3.1.

It is possible to provide a concrete description of when a given measurable (respectively measurable) random variable lies in (resp. ). Consider a measurable random variable which takes the form for a measurable function . Using (3.6) we conclude

In particular, using (3.5) we find

Similarly, from (3.8) we obtain for measurable random variables

Therefore, we require the appropriate martingale measure integrability, once we have passed to the signal realization level, for each possible signal realization. This is intuitive as the agents have already seen the signals prior to solving their optimal investment problems.

4. The Main Result

Our main result is the following theorem. To state it, define the insider and noise trader weighted risk tolerances

| (4.1) |

Theorem 4.1.

The proof of Theorem 4.1 is carried out in the sections below. In the remainder of this section, we formally derive a clearing condition which, provided markets are complete, yields the function which determines in (3.4). In the later sections we will rigorously establish the result.

The clearing condition

Note that of (4.2) is of the same form as , just with lower precision

Next, define

as the pdf of a random vector. Direct calculations show satisfies the Jacod condition almost surely on , with conditional pdf where

so that in (3.1), . Lastly,

| (4.3) |

This implies from (3.4) has density . Next, define as the conditional density of , and note that where

where above (and for later use)

This implies

With this notation, direct computations show (see [7, S1]) that

| (4.4) |

and hence from (3.7) we find that . With all this notation, the first order optimality condition for is

| (4.5) |

where the second equality follows by plugging in for and using (3.8). Therefore, by our noise trader convention

| (4.6) |

Using (4.1) this gives the population weighted terminal gains

Remark 4.2.

We pause briefly to discuss why the market signal takes the form in (4.2). Namely, consider when for a function invertible in . Invertibility implies that (in words, knowing then is the same as knowing , as is invertible in and ) and hence the first order conditions in (4.5), (4.6) are unchanged. Then, in the population weighted gains, the only component dependent on private information is

We need this quantity to be measurable. Clearly this can be achieved by taking the market signal to be , and this is what was done in [7]. Presently we take as in (4.2). As the equilibrium is unchanged choosing or . We choose as it is of the same form as and hence yields the interpretation that the market gets a signal of the same form as the insider, just of a lower precision. Note also that the form of is independent of ’s preferences, which is understandable as only and have private signals to communicate.

We lastly consider , who using (4.3) has first order optimality condition

where is measurable. We can write this as (abusing notation by writing inverse marginal utility as , according to convention)

| (4.7) |

provided enforces the static budget constraint

| (4.8) |

In equilibrium, according to (2.1), we must have

Plugging in for the optimal wealth processes, we need to enforce

To simplify this equation, define the function

Using this and we obtain the clearing condition

| (4.9) |

If we can find functions solving (4.8), (4.9) then, provided the resultant markets are complete and certain integrability conditions hold, the above wealth processes will be optimal and hence a PCE will hold.

5. Solving the clearing condition

We now identify solutions to (4.8), (4.9). Using (3.5), we see that on and provided (4.8) holds, (4.9) becomes

| (5.1) |

As is now fixed, let be a given constant and assume take the form

| (5.2) |

for a to-be-determined function such that expectation above is finite for each fixed. This enforces , as (3.6) yields the stronger

Applying (3.5) again, the budget constraint (4.8) will hold provided

| (5.3) |

Lastly, plugging in for and and absorbing all constants into in (5.1), we seek solutions to

| (5.4) |

where

Remark 5.1.

Our first lemma concerns solutions to (5.4) for fixed. To state it, define the absolute risk aversion and weighted risk tolerance functions

Lemma 5.2.

Proof of Lemma 5.2.

By the Inada conditions, is strictly decreasing with and . This implies is strictly decreasing in , taking the value and and at . Therefore, there is a unique solving (5.4). That (5.8) holds is clear and the derivative is negative because . The upper bound in (5.10) is clear from (5.7) as is decreasing. The lower bound in (5.10) follows because is decreasing and so that

Similarly, (5.11) holds because

∎

Having obtained solutions to (5.4), let us now consider (5.1) and (5.3). Using Assumption 2.3, (4.3), (3.5) as well as Lemma 5.2 it is clear that for all

and hence all the expectations in (5.1) and (5.3) are well defined. The next lemma shows that provided there is enforcing (5.3), then (5.1) holds.

Lemma 5.3.

Proof of Lemma 5.3.

From Remark 5.1 we know that if solves (5.4) then it also solves each equality in (5.5). Next, using (3.5) on the budget constraint (5.3) is (here we omit function arguments for the sake of brevity)

where we have used (4.3). This implies in (5.1)

Above, we used (5.5) in the second and fourth equality, and the budget constraint in the third equality. This gives (5.1), finishing the result.

∎

In light of Lemma 5.3, our goal is to identify a map which enforces (5.3). This is achieved in the following theorem, whose proof is in Appendix A, which shows that solutions exist for each and may be chosen in an Borel measurable manner. Furthermore, solutions are unique provided the map is non-decreasing.

Theorem 5.4.

Remark 5.5.

CRRA utility

Assume CRRA utility with relative risk aversion . Here, (5.4) specifies to

which has “explicit” solution

| (5.12) |

where (“Product-Log” or “Lambert” function) is the inverse of on .

6. Existence of a PCE

According to Theorem 5.4, there is a Borel mesaurable map such that if we set (see (4.3) and (5.2))

| (6.1) |

then in (3.5) is well defined and the clearing and budget conditions , (5.1), (5.3) hold. However, this does not yet establish a PCE, because the above analysis occurred at the signal realization, not signal, level and we have not identified the trading strategies. In this section we use Theorem 5.4 to rigorously prove Theorem 4.1 in three steps.

First, we will establish a “signal realization level” PCE where all agents have the same information but where the signal realizations yield differing endowments. Here, we a-priori assume market completeness, and we use classical results on equilibrium in complete markets, in conjunction with the analysis in Section 5. Second, we will lift up from the signal realization level to the signal level, using the stochastic integration identities from [7, Appendix AS.4], as well as delicate arguments concerning generalized conditional expectations (to avoid imposing unverifiable integrability assumptions on the model inputs). Lastly, we will verify our assumption of market completeness. Throughout, Assumptions 2.1, 2.3 and 2.6 are in force.

Signal realization level PCE

Based upon Theorem 5.4 the clearing condition (5.1) holds, and using (3.5) at the realization level the price process of (3.2) is where . Assumption 2.3 and Lemma 5.2 show is well defined, and it is clear that in our Markovian environment (see [10]) has volatility for a given function . For the time being let us assume

Temporary Assumption 6.1.

For each , is of full rank for Lebesgue almost every .

Later, we will verify temporary Assumption 6.1 using [16] in conjunction with Assumptions 2.1, 2.3 and 2.6, but for now, we take it as given. Next, as discussed in Remark 3.1 (see also (3.8) and (4.4)), direct calculation shows for all non-negative measurable random variables that

Motivated by this identity, at the realization level where is fixed, we consider the following optimization problem for , where “” means that is measurable.

| (6.2) |

where in the optimization. Lemma 5.2 and (6.1) imply both and , and hence there exists a unique optimizer which satisfies the first order conditions

yielding . Therefore, by our noise trader convention

where is the realization of , which in view of (4.2) is recoverable given realizations of . As for , we have for measurable random variables , provided the conditional expectation is well defined, that

This motivates us to consider, for the initial wealth

the optimal investment problem

Here, we follow convention, and set if . To invoke the standard complete market optimization results we need the following lemma, whose proof is given in Appendix B.

Lemma 6.2.

Define for . Then, for all we have

| (6.3) |

In view of Lemma 6.2 we may invoke [18, Theorems 1,2] to conclude that an optimal exists and satisfies

Writing this out in terms of and adjusting we have

Lastly, in view of Theorem 5.4 we recall that therein is found precisely to ensure . Therefore, we have

Having identified the optimal terminal wealth for each agent, we invoke temporary Assumption 6.1 to obtain the optimal policies. This gives

At this point, we must briefly discuss the optimal policies for , , and how they use their respective “private” information. To this end, note that and hence there is a (matrix-valued) trading strategy such that (see [23, Chapter 4]). It is clear by uniqueness666Strict concavity of the utility functions gives almost sure uniqueness of the optimal terminal wealth, see [17]. In a diffusive setting, this implies uniqueness of the trading strategy up to negligible sets ([14]) which, in general, is as precisely as we can enforce the equilibrium clearing condition in (2.1). However, in our Markovian setting, there is sufficient regularity to deduce uniqueness of the trading strategy functions. that

where

Now, define the (market measurable) strategy

The associated gains process is a martingale with terminal value

Above, the second equality follows from (6.1) and the is everything within the parentheses. The third equality follows from (5.4) as the factors out. By the martingale property we know and hence . But this implies that almost surely we have

Temporary Assumption 6.1 ensures almost surely and hence the realization level PCE holds. To conclude, we have just proved

Signal level PCE

We now establish the PCE at the signal, not signal realization level. From the previous section we have constructed strategies at the realization level which clear the market and by plugging in for 777Lemma 6.5 below shows signal-realization level strategies are appropriately measurable. it still holds that almost surely

However, we must verify the above strategies are optimal at the signal level. To this end, we start with the insider . First, to connect from (3.10) with from (6.2), let us write, for a given , to stress the dependence on . We then have the following lemma

Lemma 6.4.

If then there is a set of full Lebesgue measure such that for .

Proof of Lemma 6.4.

Next, we would like to know if as constructed above is such that and if . To answer this question, we use the following lemma, taken directly from [7, Online Appendix, Proposition S4.6].888This proposition collects results on initial enlargements found in [24, 1, 8] To state the lemma, let be a random variable satisfying the Jacod condition almost surely on and define .

Lemma 6.5.

Let be jointly measurable such that for each . Then

-

(1)

For each there is a measurable such that with .

-

(2)

The function is measurable and is well defined.

-

(3)

The processes and are indistinguishable.

Proposition 6.6.

is optimal for (3.9).

Proof of Proposition 6.6.

As it suffices to show it minimizes the conditional expectation in (3.9). To this end, let , recall the set from Lemma 6.4, and to stress the dependence write . We then have

∎

Having shown is optimal for , it immediately follows by our convention that the noise trader uses the strategy . Thus, it remains to consider . Copying Lemma 6.4, for each if we write to stress the dependence, we know there is a set of full Lebesgue measure such that for we have both and where . Additionally, using Lemma 6.5 we conclude . Therefore,

Proposition 6.7.

solves (3.11).

Proof of Proposition 6.7.

As it suffices to show it maximizes the conditional expectation in (3.11). To this end, let , and to stress the dependence write . We then have

∎

Putting all these results together, we have proved

Verifying market completeness

The last thing to do is verify temporary Assumption 6.1, which is done in the following proposition.

Proof of Proposition 6.9.

The result will follow provided we verify the assumptions in [16, Theorem 2.3] for each fixed signal realization . To connect to the notation in [16], we have (the symbol on the left side of the equation is the associated one in [16])

[16, Assumptions (A1),(A3)] clearly hold and [16, Assumption (A2)] will hold provided we may find such that

| (6.5) |

where, as in Assumption 2.3, superscript denotes the component of a vector and subscript is the derivative relative to the component of the argument. By Assumption 2.3 this clearly holds for . As for , calculations similar to those in Lemma 5.2 show that

As , by Assumption 2.3 the magnitude of the right side above is bounded by for some (which might change from line to line below). (6.5) readily follows from Lemma 5.2 as

Here, the last inequality holds because the map

is bounded from above on by constant depending only on . ∎

Putting everything together yields Theorem 4.1, except for DNREE statement, which is addressed in the next section.

7. Existence of a DNREE

We have shown existence of a PCE under Assumptions 2.1, 2.3 and 2.6. We obtain the existence of a DNREE, according to Definition 2.10, if the signal is instantaneously recoverable using the information in , the right-continuous enlargement of ’s natural filtration. In [7], we showed that if has CARA preferences and (or in the one dimensional case, if is monotonic), then the PCE was a DNREE because the time price was invertible in the signal. This was a very special outcome of CARA preferences, and while numerical computations suggest the time price is invertible in , a formal proof of this fact has been elusive. However, this does not rule out the signal being recoverable at any time , and hence existence of a DNREE, as we now show in the univariate case. Results are valid assuming

Assumption 7.1.

The dimension is .

Recall the pricing function . We first state the following result, whose proof is given in Appendix C.

Proposition 7.2.

Using this result we finish the proof of Theorem 4.1 by proving

Proposition 7.3.

Proof of Theorem 7.3.

Let be the (potentially unknown) signal realization and . By the support theorem [25] and continuity of , the information in allows us to see the collection of numbers . By Proposition 7.2 there is only one compatible with the collection and hence we can back out . As this works for any realization we see that , for any and hence by right-continuity of both and we see that and the DNREE follows. ∎

8. Relative Risk Aversion Asymptotics

While Theorem 4.1 establishes existence of a PCE and DNREE, as ’s preferences are general, explicit formulas for equilibrium quantities are difficult to obtain. This fact remains true even when has CRRA preferences. To obtain more concrete expressions, in this section we specify to when has CRRA utility and consider the risk aversion limits and . Proofs of the propositions below are given in Appendix D.

We first let . To gain intuition for the result, consider (5.4) when . Formally, if then and by absorbing into we expect that

In view of (6.1), (3.2) and (3.5) one expects the limiting price function to be

| (8.1) |

This argument in fact leads to the correct price, as the following proposition shows.

Proposition 8.1.

We next consider , obtaining an a priori surprising result. To state it, we first fix and consider solutions to

| (8.2) |

As Assumption 2.3 implies, for fixed , that is bounded from below, it is clear there exists a unique solving the above. With this notation we have

Proposition 8.2.

Remark 8.3.

Vanishing risk aversion, , intuitively suggests approaches risk neutrality. But if were truly risk neutral, this agent’s behavior would be expected to drive the equilibrium price to the risk neutral price (i.e. the risk neutral agent would be expected to dominate in the price formation process) given by

Now, as is bounded from below in for fixed, it is natural to wonder if is such that . Indeed, if this were the case then . However, if this were true, then in view of (8.2) one would have

Therefore, it is natural to define by the right side above, and then check if . If so, then the limiting price is the risk neutral price. However, as can be seen when is Gaussian, typically, one does not have for all signal realizations , and hence even as the uninformed agent’s relative risk aversion vanishes, the limit price is not the risk neutral price. The explanation for this counter-intuitive phenomenon is that, unlike a truly risk neutral agent, power utility enforces a non-negativity constraint, even in the limiting case.

9. Example

We consider and , i.e., the terminal payoff is a geometric Brownian motion and the signal is on the log-payoff, or alternatively the signal is multiplicative, rather than additive, on the terminal payoff. Lastly, we consider with CRRA utility. Therefore, Assumptions 2.1, 2.3 and 2.6 are all satisfied.

With all the assumptions met, we obtain a PCE and DNREE from Theorem 4.1. Next, we examine the impact of coefficients on the price, volatility and market price of risk (MPR), in the context of this example. For numerical computations, we use the baseline set of parameters

| (9.1) |

Note in particular that we are assuming the noise trader is a mis-perceiving insider.

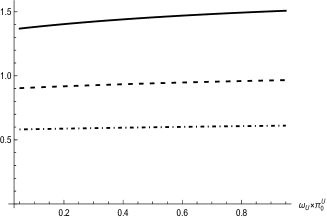

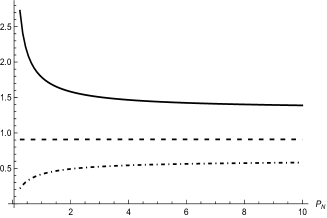

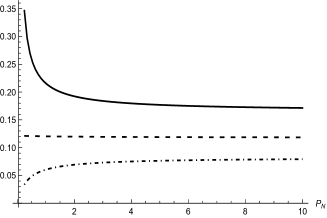

9.1. Sensitivity with respect to uninformed initial endowment

Figure 1 plots the time 0 price, volatility and market price of risk versus the weighted uninformed initial share endowment, for various values of the signal . Here, we see that price and volatility increase slightly with the endowment, while the MPR decreases significantly. An increase in ’s endowment increases his initial wealth. This raises ’s demand for the risky asset, leading to an excess aggregate demand for the asset. Adjustment to equilibrium is then consistent with a simultaneous increase in the volatility and decrease in the MPR. The latter effect increases the stock price.

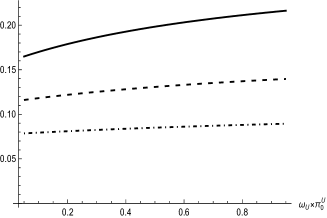

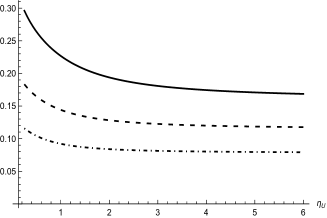

9.2. Sensitivity with respect to uninformed relative risk aversion

Figure 2 plots the time 0 price, volatility and MPR versus the relative risk aversion of for various values of . Here, we see a decrease in the price and volatility coefficient as risk aversion increases, and an increase in the MPR. In essence, the more risk averse requires greater compensation for a given level of risk, leading to an increase in the MPR and a reduction in the asset price. These adjustments are consistent with a simultaneous decrease in the equilibrium volatility. The limit prices in Figure 2 correspond to those in Propositions 8.1 and 8.2.

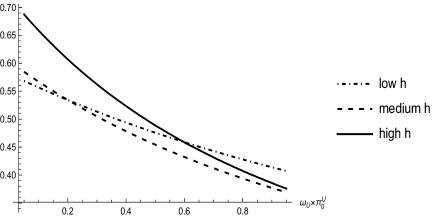

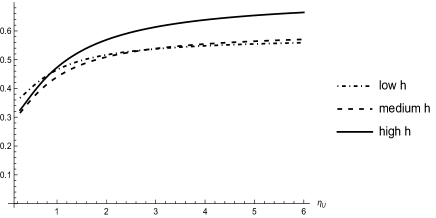

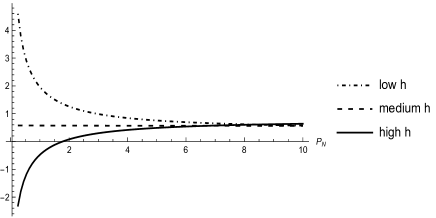

9.3. Sensitivity with respect to noise trader precision

Figure 3 plots the time 0 price, volatility and MPR versus the noise trader precision , for various values of .999The computation of accounts for the fact that the distribution of depends on . When the noise trader becomes an insider, when the market signal becomes pure noise. The plots show the reaction depends on the signal realization. For high (low) the price and volatility decrease (increase) and the MPR increases (decreases). An increase in the noise trader precision implies the market signal is more reliable and the informational advantage of the informed shrinks. The demand for the asset then decreases (increases) if the signal is sufficiently high (low), leading to the effects described. In the limit, as , effectively becomes an insider and the price and MPR both become insensitive to . At the opposite extreme, as , is unable to extract any useful information from and information disparity is greatest. Any small change in the neighborhood of then has a large impact on heterogeneity and leads to a strong response of equilibrium quantities.

Appendix A Proofs from Section 5

Proof of Theorem 5.4.

Omitting all function arguments, we seek solving (5.3), which is equivalent to

| (A.1) |

where the second equality holds because solves (5.5). To prove existence of such we will show that is continuous in with and . We will also show that provided is non-deceasing then is strictly decreasing in and solutions are unique. Lastly, we will prove the measurability results.

We start with the limiting statements. Let , which in view of Lemma 5.2 implies the almost sure limits . This means that for we have almost surely that (here, we omit the function arguments for brevity, and note in (5.5) that )

By (5.11) we know the right-most quantity above is integrable, and hence by dominated convergence the denominator in (A.1) goes to . As for the numerator, recall from Remark 2.8 that . Thus, by Fatou’s lemma, the numerator exceeds (in the limit)

so that . Recalling from (5.6) we have by (5.10), (5.11) and because is decreasing

The expectations on the right side no longer depend on and each are finite. Thus, , because .

We next prove continuity by showing the numerator and denominator in (A.1) are each continuous. For the numerator, note that does not depend on , and from Lemma 5.2 we have for

This implies

Therefore, by Assumption 2.3 and (4.3) we see that the numerator is not only continuous, but differentiable in . Turning to the denominator, using (5.11) we obtain for (as is increasing)

and

Again, using from (4.3) we find that the denominator is also differentiable, hence continuous in . Therefore, by continuity there exists a solution to . As for the uniqueness statement, clearly is strictly decreasing. Additionally,

Thus, if is non-decreasing then is non-increasing in and hence non-increasing (almost surely) in . Therefore, is strictly decreasing and hence uniqueness follows.

The last thing to discuss is measurability of in , which follows from the Kuratowski-Ryll-Nardzewski measurable selection theorem. Indeed, for define

Assuming is jointly continuous in (which can be shown using Lemma 5.2) it is easy to see that is closed (hence Borel) for each closed . Now, let for some and (for large enough so that it is not empty) set . Straightforward computations show that

and hence is Borel for each . But this implies that is Borel for each open and hence the Kuratowski-Ryll-Nardzewski measurable selection theorem implies that we may select measurably in .

∎

Appendix B Proofs from Section 6

Proof of Lemma 6.2.

From (6.1) we see that

We first claim that (6.3) holds when . Indeed, as , is decreasing and convex. Therefore,

Next, for any

Using (5.11) in Lemma 5.2 we deduce

for some constant . Therefore, for

The result follows from Assumption 2.3 and the construction of . When we have

As satisfies the reasonable asymptotic elasticity condition in Assumption 2.6, we deduce from [18, Corollary 6.1 (iii’)] the existence of and a constant such that when . Using again that is decreasing, this implies

By definition of we know so that

Therefore,

(6.3) holds because we already showed and by Lemma 5.2 we know for some constant . ∎

Appendix C Proofs from Section 7

Proof of Proposition 7.2.

Define

From [10] we know is smooth enough in to use Ito’s formula. Therefore, from (3.2), (3.5), (5.2) we see that

so that has market price of risk . Next, write as the second order operator associated to , so that for smooth functions

Again using [10], we know that solves the PDE

Therefore, if the statement is true (which implies coincide for ) then it follows that on we have

As we know from Proposition 6.9 that for each , and (Lebesgue almost every) that . Thus, as is non-degenerate as well, we have Lebesgue almost surely on that

| (C.1) |

By continuity the above holds for all . Thus, as solves the PDE

we see that satisfies, on

Again, using (C.1) we know by Ito’s formula that almost surely

which by the support theorem for diffusion processes (see [25]) implies for Lebesgue almost every (hence all by continuity) that

But, this implies

satisfies the PDE

and is such that almost surely on . We now apply [26, Theorem 1.2] to . To match their notation define the operator . We then have

so that for a constant . As Lemma 5.2 implies for some , the assumptions of [26, Theorem 1.2] are met with therein and we may conclude that if there exists any such that is identically zero, then it must be that is identically constant as well. But, this is an obvious contradiction if . ∎

Appendix D Proofs from Section 8

Proof of Proposition 8.1.

Throughout, is fixed. Let us first assume there is a sequence and a number such that

| (D.1) |

Given this, we claim

| (D.2) |

First, (5.12) implies

| (D.3) |

Next, for any , and hence

| (D.4) |

Using we obtain for any

| (D.5) |

Using this, and the assumption that we verify (D.2). We now turn to identifying . To this end, re-writing (5.3), using (4.3), and setting , we have for each

| (D.6) |

From (D.3) we find

From (5.7) we know (as is fixed) that is bounded from below by some constant . As is increasing this implies

where the last equality hold as . and (D.5) then imply that for large enough

| (D.7) |

and hence is almost surely bounded from above. We may express (D.6) as

| (D.8) |

The bounded convergence theorem and (D.2) yield

and hence for any such that from (D.1) converges, the limit is uniquely identified. Lastly, note that

Using the exact same arguments as above for fixed (i.e. multiplying the numerator and denominator by and using the bounded convergence theorem), we may pass the limit through the expectation operator to obtain (8.1).

The final item to prove is that implies from (D.1) converges to a finite (unique) limit, for whatever we choose that satisfies (5.3). As we have already shown that every sub-sequence which converges to a finite limit, has the same limit point, it suffices to show cannot happen.

Assume . From (D.4) and (D.6) we obtain

Using that is increasing, (D.5) and Fatou’s lemma, we deduce

As for the denominator, let be fixed and take large enough so that for large enough. As is increasing and is large we have

Above, the second equality follows from (D.4) and the inequality from (D.7), which was valid for general constants and does not require (D.6). As such

As such, contradicts (D.6) in the limit . Lastly, assume . Here, we will use a slightly different argument to reach a contradiction. First, using that is increasing and (D.5), if then for any constants

| (D.9) |

Next, from (5.10), (D.8), and using the notation of (5.6) we deduce that

Above, we have written for the quantity in (5.10), and used Assumption 2.3 which implies that is non-negative. Therefore, there is a quantity depending only on (and not ) such that

From (5.9), and using we have (see (5.12))

where . Therefore,

But, as this violates (D.9), showing that and finishing the proof. ∎

Proof of Proposition 8.2.

Throughout, is fixed. Also, we may assume , and hence from Theorem 5.4 is the unique enforcing (5.3). Let us first assume there is a sequence and a number such that

Given this, we first claim

| (D.10) |

Indeed, (5.12) gives

where

Next, for any , and hence

By assumption . As l’Hopital’s rule shows

we verify (D.10) for . Next, the above identities also imply

| (D.11) |

which in turn yields (D.10) as

Having obtained the limiting values in (D.10) we now identify . To this end, re-writing (5.3) and using (4.3) we have for each

| (D.12) |

Using the explicit formula for in (4.3), the upper bound for in Lemma 5.2 and Assumption 2.3, it is clear that

where the inequality follows because, for fixed, is bounded from below in (see (5.7)). As for the denominator we first note from (D.11) that

Using that is increasing, for and , we obtain

so that for

Assumption 2.3, the definition of in (4.3) and the upper bound for in Lemma 5.2 allow us to invoke the dominated convergence theorem to obtain

But, this implies

which is exactly (8.2) at . However, as the right side in (8.2) is strictly decreasing in the argument , we see that . Therefore, we have shown that for any such that converges to some , it must be that . Lastly, note that

Using the exact same arguments as above for fixed, we may pass the limit through the expectation operator to obtain (8.3).

The final item to prove is that implies . Now, we have already shown that every sub-sequence which converges to a finite limit, has the same limit point . It thus suffices show cannot happen. To do this, we recall from the proof of Theorem 5.4, that for the right hand side of (D.12) is strictly decreasing in . Given this, assume that , and for a given assume is large enough so that . By monotonicity

With fixed, we repeat the above analysis taking to obtain

As this holds for any we take and use monotone convergence to obtain , a contradiction. Therefore, . Similarly, if , fix and take large enough so that . By monotonicity

Taking gives

Taking and use monotone convergence to obtain , a contradiction. Therefore, and the proof is complete. ∎

References

- [1] J. Amendinger, Martingale representation theorems for initially enlarged filtrations, Stochastic Process. Appl., 89 (2000), pp. 101–116.

- [2] J. Amendinger, P. Imkeller, and M. Schweizer, Additional logarithmic utility of an insider, Stochastic Process. Appl., 75 (1998), pp. 263–286.

- [3] K. J. Arrow and G. Debreu, Existence of an equilibrium for a competitive economy, Econometrica, 22 (1954), pp. 265–290.

- [4] B. Breon-Drish, On existence and uniqueness of equilibrium in a class of noisy rational expectations models, The Review of Economic Studies, 82 (2015), pp. 868–921.

- [5] G. Chabakauri, K. Yuan, and K. E. Zachariadis, Multi-asset noisy rational expectations equilibrium with contingent claims, Review of Economic Studies, forthcoming (2021).

- [6] R.-A. Dana and M. Jeanblanc, Financial markets in continuous time, Springer Finance, Springer-Verlag, Berlin, 2003. Translated from the 1998 French original by Anna Kennedy.

- [7] J. Detemple, M. Rindisbacher, and S. Robertson, Dynamic noisy rational expectations equilibrium with insider information, Econometrica, 88 (2020), pp. 2697–2737.

- [8] C. Fontana, The strong predictable representation property in initially enlarged filtrations under the density hypothesis, Stochastic Process. Appl., 128 (2018), pp. 1007–1033.

- [9] S. Grossman, On the efficiency of competitive stock markets where trades have diverse information, Journal of Finance, 31 (1976), pp. 573–585.

- [10] D. Heath and M. Schweizer, Martingales versus PDEs in finance: an equivalence result with examples, Journal of Applied Probability, 37 (2000), pp. 947–957.

- [11] M. F. Hellwig, On the aggregation of information in competitive markets, Journal of Economic Theory, 22 (1980), pp. 477–498.

- [12] J. Hugonnier, S. Malamud, and E. Trubowitz, Endogenous completeness of diffusion driven equilibrium markets, Econometrica, 80 (2012), pp. 1249–1270.

- [13] J. Jacod, Grossissement initial, hypothese (H’) et theoreme de Girsanov, Springer Berlin Heidelberg, Berlin, Heidelberg, 1985, pp. 15–35.

- [14] I. Karatzas and S. E. Shreve, Methods of mathematical finance, vol. 39 of Applications of Mathematics (New York), Springer-Verlag, New York, 1998.

- [15] D. Kramkov, Existence and uniqueness of Arrow–Debreu equilibria with consumptions in , Theory of Probability & Its Applications, 60 (2016), pp. 688–695.

- [16] D. Kramkov and S. Predoiu, Integral representation of martingales motivated by the problem of endogenous completeness in financial economics, Stochastic Process. Appl., 124 (2014), pp. 81–100.

- [17] D. Kramkov and W. Schachermayer, The asymptotic elasticity of utility functions and optimal investment in incomplete markets, Ann. Appl. Probab., 9 (1999), pp. 904–950.

- [18] , Necessary and sufficient conditions in the problem of optimal investment in incomplete markets, Ann. Appl. Probab., 13 (2003), pp. 1504–1516.

- [19] A. Mas-Colell, M. D. Whinston, J. R. Green, et al., Microeconomic theory, vol. 1, Oxford university press New York, 1995.

- [20] L. W. McKenzie, On the existence of general equilibrium for a competitive economy, Econometrica, 27 (1959), pp. 54–71.

- [21] I. Pikovsky and I. Karatzas, Anticipative portfolio optimization, Adv. in Appl. Probab., 28 (1996), pp. 1095–1122.

- [22] R. Radner, Rational expectations equilibrium: Generic existence and the information revealed by prices, Econometrica, 47 (1979), pp. 655–678.

- [23] S. E. Shreve, Stochastic calculus for finance. II, Springer Finance, Springer-Verlag, New York, 2004. Continuous-time models.

- [24] C. Stricker and M. Yor, Calcul stochastique dépendant d’un paramètre, Z. Wahrsch. Verw. Gebiete, 45 (1978), pp. 109–133.

- [25] D. W. Stroock and S. R. S. Varadhan, On the support of diffusion processes with applications to the strong maximum principle, in Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and Probability (Univ. California, Berkeley, Calif., 1970/1971), Vol. III: Probability theory, 1972, pp. 333–359.

- [26] J. Wu and L. Zhang, Backward uniqueness for general parabolic operators in the whole space, Calc. Var. Partial Differential Equations, 58 (2019), pp. Paper No. 155, 19.