Uncovering the Dynamics

of the Wealth Distribution

)

Abstract

I introduce a new way of decomposing the evolution of the wealth distribution using a simple continuous time stochastic model, which separates the effects of mobility, savings, labor income, rates of return, demography, inheritance, and assortative mating. Based on two results from stochastic calculus, I show that this decomposition is nonparametrically identified and can be estimated based solely on repeated cross-sections of the data. I estimate it in the United States since 1962 using historical data on income, wealth, and demography. I find that the main drivers of the rise of the top 1% wealth share since the 1980s have been, in decreasing level of importance, higher savings at the top, higher rates of return on wealth (essentially in the form of capital gains), and higher labor income inequality. I then use the model to study the effects of wealth taxation. I derive simple formulas for how the tax base reacts to the net-of-tax rate in the long run, which nest insights from several existing models, and can be calibrated using estimable elasticities. In the benchmark calibration, the revenue-maximizing wealth tax rate at the top is high (around 12%), but the revenue collected from the tax is much lower than in the static case.

1 Introduction

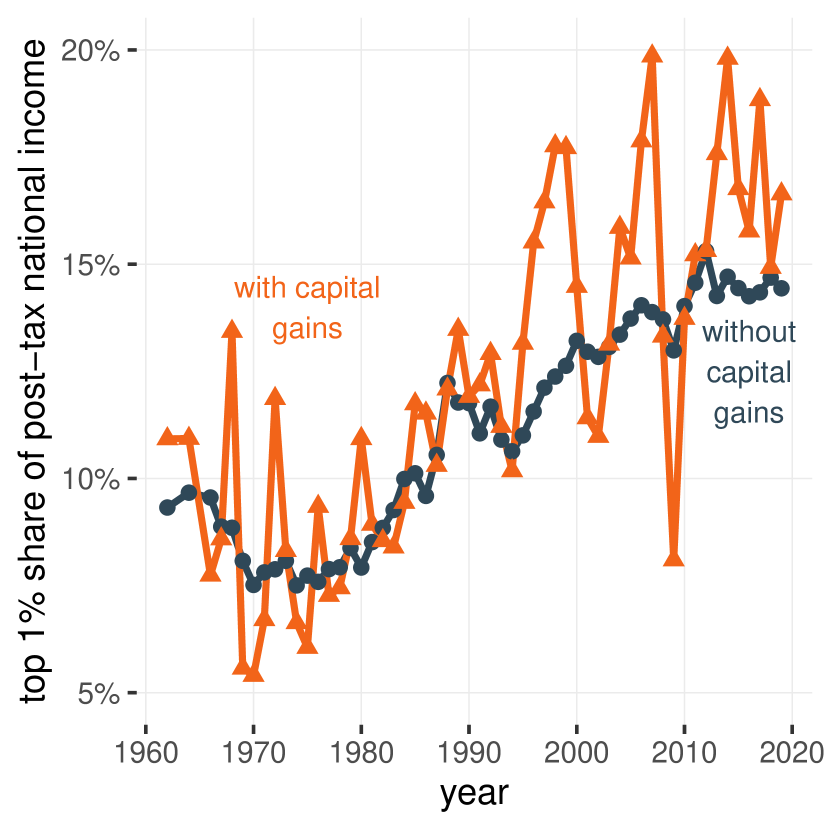

Wealth inequality has sharply increased in the United States. By combining income tax returns with macroeconomic balance sheets, [90] find that the share of wealth owned by the top 1% has increased by more than 10 pp. since the late 1970s.111[90] is a revision of [89], which accounts for heterogeneous returns, as well as the more important role of private business wealth at the top found by [67]. See also [91]. [46] find a similar trend using survey data (Figure 1).222Other estimates, notably [67], also find a similar increase of the top 1% share, although they also find a somewhat more muted increase than [90] for the top and narrower top groups.

But despite this growing amount of data documenting the historical evolution of the distribution of wealth, our understanding of the drivers of this trend remains elusive. Is it solely a consequence of the rise of labor income inequality? Or is it also the result of higher rates of return? What about capital gains? Does it have anything to do with the decline of the estate tax? Does it reflect changes to the distribution of saving rates? These are basic questions, and if we had long-run longitudinal data on income and wealth, they would be fairly easy to answer. After all, they simply ask how observable phenomena affect the process of wealth accumulation in direct, mechanical ways. But because longitudinal wealth data is scarce and limited, in practice, answering them has remained a challenge. That we don’t have a straightforward understanding of such proximate causes of wealth inequality is a problem in and of itself, but it also impedes our ability to answer several related questions. It makes it more difficult to adequately calibrate economic models of the wealth distribution, which are used to investigate the deeper, underlying causes of rising inequality. It limits our understanding of the effect of widely discussed policies, such as wealth and inheritance taxation.

Contribution

This paper addresses this issue by introducing a new way to decompose the evolution of wealth inequality in terms of individual-level factors, and in spite of the lack of panel data. The decomposition accounts for demography, inheritance, assortative mating, labor income, rates of return, consumption, and, importantly, mobility. It does so in a way that only requires repeated cross-sections, and therefore can be applied to historical data. The approach is tractable and allows for a transparent, visual identification of the key parameters.

I estimate this decomposition in the United States since the 1960s, and in doing so, I establish the main direct drivers of the rise of wealth inequality over that period. To that end, I use historical microdata on the distribution of income and wealth [90], which I combine with a large set of data from censuses, surveys, demographic tables, and macroeconomic accounts. For example, I construct measures of assortative mating as well as age-specific marriage and divorce rates since the 1960s to estimate their effect on the wealth distribution. I also microsimulate the entire demographic history of the United States since the mid-19th century to statistically reconstruct intergenerational linkages, and combine them with distributional parameters for intergenerational wealth transmission as a way to measure the effect of inheritance and of the estate tax.

Finally, I develop a way to incorporate wealth taxation within the framework of this paper, derive a simple formula for how the wealth distribution would react to any wealth tax in the long run, and use my empirical estimates to calibrate it for the United States. The framework of the paper presents several advantages here as well. A typical difficulty when analyzing wealth or capital taxation is that the standard models lead to a menagerie of “corner solutions,” and the associated policy recommendations are often extreme, fragile, and hard to interpret. Small changes in parameters (e.g., an intertemporal elasticity of substitution just above or below one) lead to diametrically opposite results (e.g., an optimal tax of 0% or 100%) [68].333This is for example the case in the reanalysis of the model of [42] by [68] in the case with no government spending. In light of this situation, [60] have argued for a simpler framework — one that centers the same equity-efficiency trade-off that governs the theory of optimal labor income taxation [51] and, in practice, dominates policy considerations. In this framework, the elasticity of capital supply with respect to the net-of-tax rate directly dictates the optimal level of capital taxation.444As long as this elasticity is finite, positive capital taxes are desirable. We can interpret earlier arguments that capital should never be taxed [15, 42] as the consequence of assuming an infinite elasticity [50, 60]. But finding a way to model this elasticity in a realistic yet tractable way, without facing the same degeneracy issues as earlier models, remains difficult. Here, because the model is stochastic and features mobility, it organically leads to well-behaved steady-states and finite elasticities of wealth with respect to the net-of-tax rate, under a wide range of economic behaviors, and without the need to resort to ad hoc modeling devices such as wealth in the utility function [60, e.g.,]. Because the continuous-time formalism is highly tractable, I can obtain simple formulas that combine and extend insights from earlier studies of progressive wealth taxation [41, 62, e.g.].

Overview of the Methodology

This paper uses a stochastic, continuous-time framework, and its methodology rests on two results from stochastic calculus. First, I use [78]’s (\citeyeargyongy_mimicking_1986) theorem to prove that two factors drive the dynamics of the wealth distribution: the mean and the variance of savings, conditional on wealth. This remains true even in models that feature heterogeneous agents and complex shocks: [78]’s (\citeyeargyongy_mimicking_1986) theorem shows that this complexity can be marginalized out, and therefore that the evolution of the wealth distribution can, under very general conditions, be summarized by a single stochastic differential equation (SDE). This SDE captures the two forces that shape the distribution of wealth: the average savings of the different parts of the distribution (a.k.a. the drift), and the mobility across the distribution (a.k.a. the diffusion).

Having reduced the dynamic of wealth to this simple model, I apply the [44] forward equation, a standard result of stochastic calculus, which is known to be extremely useful in understanding how wealth distributions get their power-law shape [25]. This equation relates how wealth evolves stochastically at the individual level with how the distribution of wealth evolves deterministically in the aggregate. Traditionally, this equation is used deductively: starting from a set of parameters for how individual wealth evolves, we apply it to determine how the distribution changes. This paper argues that it is possible to use that equation inductively. That is, looking at how the distribution changes, we can infer the parameters (the mean and the variance of savings) that govern the underlying individual wealth accumulation process.

That we can infer the individual wealth accumulation process — including a mobility parameter — from cross-sectional data may prima facie be counterintuitive. This paper provides a simple explanation for that fact. Basically, mobility is a force that spreads out observations and, therefore, flattens the wealth density locally. Consequently, the changes it exerts on the distribution depend on how flat it is to begin with. In contrast, the local effect exerted by the drift (i.e., how much wealth grows at a given point on average) is akin to a local translation and is independent of the shape of the density. This distinction is not a mere technicality: it is the central piece of the mechanism that allows steady-state distributions to emerge in the first place, and it has empirically measurable consequences. By looking at how the local evolution of the wealth density relates to its current shape, I can therefore estimate both parameters.

I estimate the full model, while also accounting for income and the role played by demography, assortative mating, and inheritance. I show that the model correctly reproduces the past evolution of wealth inequality. When I compare my findings to the (albeit scarce and limited) longitudinal survey data on wealth that exists in the United States, I find that my results are consistent. I use the model to decompose the evolution of wealth inequality and to generate simple counterfactuals showing how wealth inequality would have evolved if certain factors (e.g., labor income inequality, capital gains) had stayed at their 1980 levels.

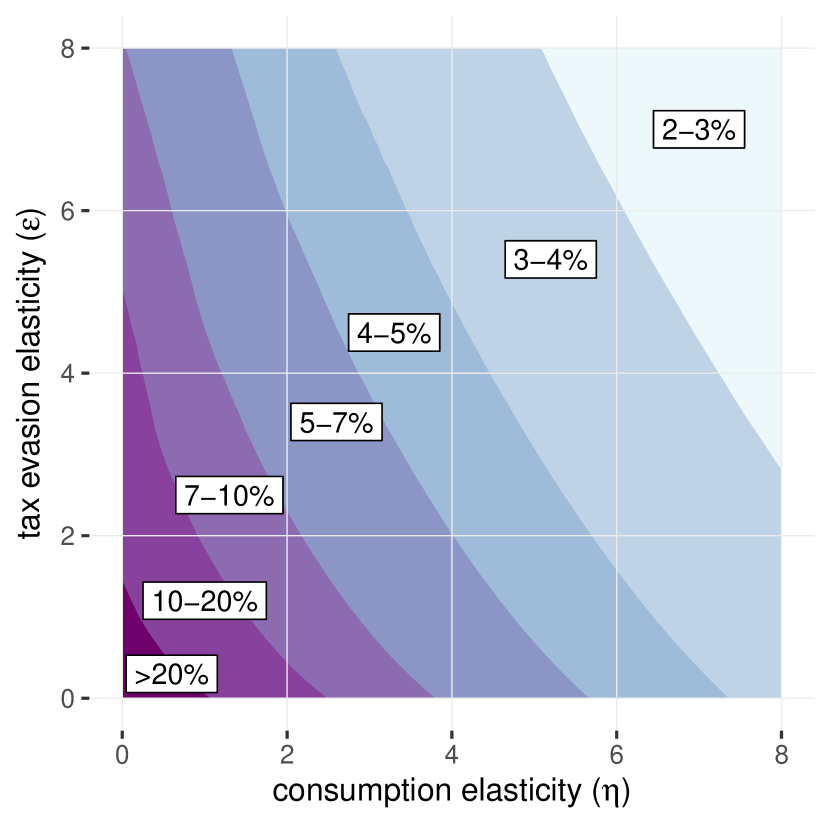

Finally, I include wealth taxation into the model, and derive a simple formula for how the wealth distribution would react to an arbitrary wealth tax in the long run, which connects the field of capital taxation to the theories of the wealth distribution. This formula depends on three factors: mobility across the wealth distribution, tax avoidance, and savings responses. Mobility is built into the framework and calibrated using this paper’s estimate. For tax avoidance and savings responses, I rely on reduced-form expressions that depend on simple, estimable behavioral elasticities, which I calibrate using quasi-experimental evidence from the literature [10, 66, 41, 72, 54, 47]. A comprehensive tool to simulate the effect of arbitrary wealth taxes in the United States, using this paper’s formulas, is available online at https://thomasblanchet.github.io/wealth-tax/.

Findings

After applying the decomposition to the United States since 1962, I find that the main drivers of the rise of the top 1% wealth share since the 1980s have been, in decreasing level of importance, higher savings at the top, higher rates of return on wealth (essentially in the form of capital gains), and higher labor income inequality. Other factors have played a minor role.

Notably, the wealth accumulation process that I estimate features a rather large heterogeneity of savings for a given level of wealth and, therefore, a large degree of mobility across the distribution. That amount of mobility is comparable to what I independently find in longitudinal survey data from the Survey of Consumer Finances (SCF) and the Panel Study of Income Dynamics (PSID), and in a panel of the 400 richest Americans from Forbes. This finding cuts against the “dynastic view” of wealth accumulation, and suggests that existing models of the wealth distribution underestimate the extent of wealth mobility. This has several implications.

First, the large heterogeneity of savings implies that high levels of wealth inequality can be sustained even if the wealthy consume, on average, a sizeable fraction of their wealth every year. Second, high mobility offers a straightforward answer to a puzzle pointed out by [26]: that the usual stochastic models that can explain steady-state levels of inequality are unable to account for the speed at which inequality has increased in the United States.555[26] primarily focus on income inequality, but their formal findings apply to wealth as well. But high mobility leads to faster dynamics and, therefore, can account for the dynamic of wealth we observe in practice.666This solution differs from the solutions proposed by [26], which involve introducing temporary changes to the drift to accelerate dynamics at the beginning of a transition.

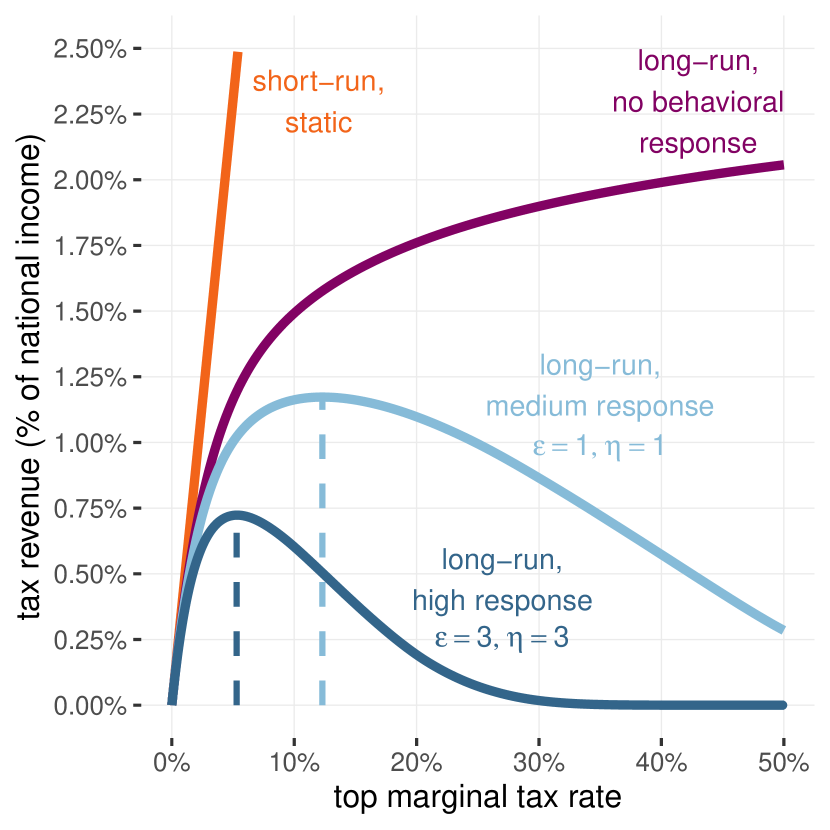

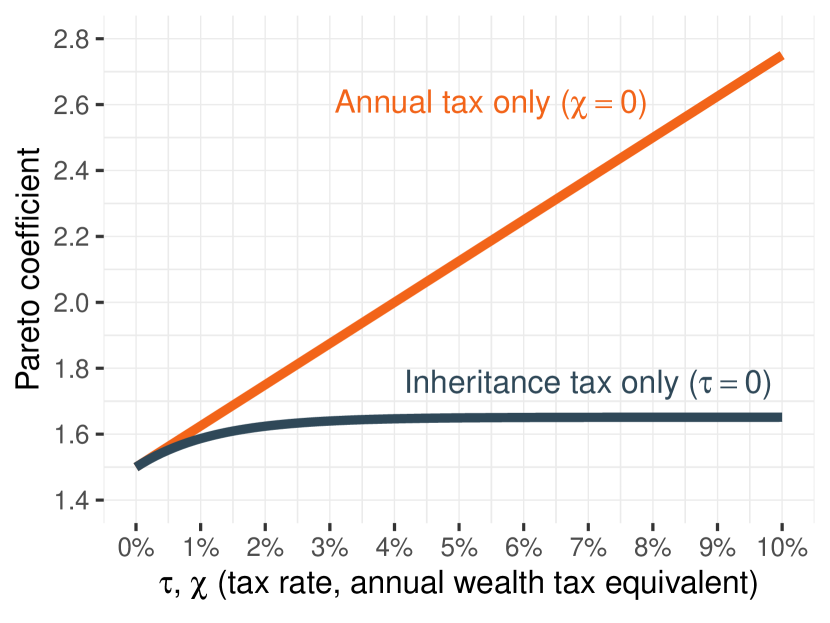

The study of wealth taxation also yields new insights. First, the degree of mobility across the wealth distribution — which explicitly appears in the formula I derive — generates a mechanical effect that fixes many degeneracy issues from deterministic models. And it is a crucial determinant of the response of the wealth stock to a tax. Indeed, without mobility, an annual wealth tax would affect the same people repeatedly, and absent behavioral responses, the tax base would eventually go to zero. With mobility, new, previously untaxed wealth continuously enters the tax base, which avoids that phenomenon. [62] study this effect, but within a very restrictive setting — my formula extends and operationalizes their idea to more complex and realistic cases, and this affects some of the conclusions.777[62] consider a wealth tax at a constant average rate above a threshold. My formulas apply to arbitrary wealth taxes, including the more common case of a constant marginal rate within a bracket. In light of this result, the significant mobility that I find suggests that a wealth tax could raise more revenue, all other things being equal. Second, even in the simplest model, the reduced-form elasticity of wealth with respect to the net-of-tax rate is nonconstant — much higher for low rates than higher ones. (This directly results from the fact that the complete formula depends on both the average and the marginal tax rate.) As a consequence, the revenue-maximizing rate for a linear wealth tax above $50m is high (12% in my benchmark calibration), yet the revenue raised from said tax in the long run is quite low, only about a quarter of what the tax would raise in the absence of response.888If the elasticity were constant, a 12% revenue-maximizing rate would be associated with a revenue reduction of 60% compared to the inelastic case, as opposed to 75% here. Third, my simulations suggest that the effects of an annual wealth tax differ in fundamental ways from those of an inheritance tax of seemingly comparable magnitude. I show in a simple model that this distinction is driven by the lifetime of generations: the longer people live, the less potent the estate tax compared to a wealth tax.

2 Literature Review

2.1 Models of the Wealth Distribution

The conventional way of studying the determinants of wealth inequality is to construct a model of an economy where people face various individual shocks. The prototypical model for this line of work comes from [1] and [36], who study the distribution of wealth in [8] type models in which people face idiosyncratic uninsurable labor income shocks. In these models, people accumulate wealth for precautionary or consumption smoothing purposes. But these motives quickly vanish as wealth increases, so they cannot rationalize large wealth holdings. As a result, these models notoriously underestimate the real extent of wealth inequality.

The literature, then, has searched for ways to extend these models and match the data. One possibility involves additional saving motives for the rich, such as a taste for wealth [12] or bequests [17]. Another solution is to introduce idiosyncratic stochastic rates of returns in the form of entrepreneurial risk [53, 11, 7]. Yet another option introduces heterogeneous shocks to the discount rate [45].

Recent contributions have zoomed in on specific features and issues. Following the finding from [4] (in Sweden) and [20] (in Norway) that the wealthy enjoy higher returns, several papers have examined this mechanism in the United States. [71] finds that heterogeneous returns play a critical role in explaining the current levels of wealth inequality. [16] embeds a portfolio choice model in a wealth accumulation model. In this paper, because of heterogeneous portfolio composition, households have different exposures to aggregate risks. The wealthy invest more in high-risk, high-return assets like equity. As a result, [16] finds that abnormally high stock market returns have been a critical driver of the rise in wealth inequality in the United States. [35], on the other hand, use a different model and conclude that changes in tax progressivity, rather than changes in rates of return, explain the rise in wealth inequality.

In general, models of the wealth distribution seek to explain two facts: that wealth inequality is high (that is, higher than income inequality) and that its top tail is shaped like a power law. Existing models differ across many dimensions, but when it comes to explaining these facts, they usually share a common mechanism: namely, that wealth accumulates through a series of individual multiplicative random shocks, with frictions at the bottom. Assuming that the shocks have adequate properties, such models can generate both high wealth inequality and power-law tails. In discrete time, we can formulate this idea using the theory of [43] processes. Assume that the wealth of person evolves according to a linear recurrence equation with random coefficients: , where is a multiplicative shock (typically reflecting stochastic returns or preference shocks) and is a friction term (typically reflecting labor income). Then, under very general conditions, wealth admits a steady-state distribution with a power-law tail, whose fatness is determined by the properties of the multiplicative shock [43, 32, 70, 29, 31]. We can formulate a continuous-time version of this mechanism using stochastic calculus [25].999[65] rigorously study the the continuous time version of [43] processes. In this paper I consider simpler — and less literal — continuous time analogs to [43] processes. This formalism presents major advantages in terms of flexibility and tractability, notably because of the [44] equation, which establishes a straightforward relationship between the distribution of the individual random shocks and the evolution of the wealth distribution in the aggregate.

We can understand the relation of the current paper to this literature with the help of Figure 2. The “standard approach,” represented by the blue arrow at the bottom, takes a deductive path. Starting from a set of microfoundations, it solves and simulates the model to arrive at a wealth distribution. Assuming the model matches the data, we can use it to study policies and generate counterfactuals. Implicitly or explicitly, that approach can be broken down into several steps. First, microfoundations lead to a wealth transition equation that effectively determines the dynamics of the wealth distribution. For every level of wealth, two parameters characterize this equation: the average, and the variance of wealth growth (i.e., mobility). That these two parameters are sufficient to characterize the dynamics of the distribution can be rigorously proven using [78]’s (\citeyeargyongy_mimicking_1986) theorem. Then, I can feed these parameters into the [44] equation, which describes how the wealth density evolves.

This paper takes the reverse path, as characterized by the two red arrows in Figure 2. I start from the data on the evolution of the wealth distribution and then use the [44] equation to infer the parameters of the wealth transition equation. Many different microfoundations can lead to the same wealth transition equation; therefore, in my approach, the complete model of the economy remains unknown. Yet knowing just the wealth transition equation already opens many possibilities. It is sufficient to study many mechanisms, counterfactuals, and policies. And when more complete models remain necessary, the approach makes it easier to discriminate between them.

We can, in particular, compare this paper to two recent studies that also use a primarily empirical approach within the framework of stochastic wealth accumulation models. [6] fit a model of stochastic wealth accumulation to data for the United States. They start from an explicitly microfounded model of consumption and use the method of simulated moments to identify the parameters that best replicate observed data. These parameters determine the shape of the utility function and the process for the rate of return. There are four main differences between their approach and mine. First, they estimate consumption by estimating a two-parameter utility function, while I estimate a nonparametric profile of saving rates by wealth. Their approach is more structural and tightly parameterized; my approach is more flexible and reduced form. Second, they use direct information on wealth mobility in a given year, from the 2007–2009 panel of the SCF, to estimate their model; I validate my estimate of mobility against the SCF, but I do not use it directly. Third, their model is nonlinear and estimated using the method of moments; my approach works by fitting a univariate linear equation for each level of wealth, making the source of identification highly explicit and easy to check graphically. Fourth, their primary goal is to replicate the levels rather than the trends in wealth inequality, so their main model assumes that the economy is at its steady state. In a separate exercise, they additionally replicate trends. My approach directly reproduces both levels and trends by construction — and in fact, I use the trends as an essential source of identification.

[30] decomposes the evolution of top wealth shares in the United States while accounting for the role of demography and mobility. Like this paper, [30] decomposes changes in the wealth distribution that are caused by the first moment of wealth growth rates (average savings) and by the second moment (mobility).101010The decomposition in [30] also accounts for higher moments of the distribution of wealth growth rates (i.e., skewness, kurtosis, etc.), but he finds that these have a negligible impact on the wealth distribution. Like this paper, [30] finds an important role for mobility. His methodology, however, requires longitudinal data, for which he uses the Forbes 400 ranking of the wealthiest Americans.111111[30] also applies his methodology without direct panel data but with a separate estimate of the variance of wealth growth. However, estimating this variance still requires some form of longitudinal data. In contrast, I use historical data on income and wealth to directly infer this parameter, allowing me to analyze the rise of wealth inequality since 1962. In contrast, the Forbes 400 rankings started in 1982. My analysis uses the entire wealth distribution, not only the top of the tail. Finally, I also account for labor income, inheritance taxation, and assortative mating. [30] and this paper provide complementary evidence of the dynamics of wealth accumulation and find a similar result: that mobility across the wealth distribution is sizeable and plays a crucial role in shaping the wealth distribution.

2.2 Synthetic Saving Rates

Another way of using wealth distribution data to study the drivers of wealth inequality is to construct synthetic saving rates for the different parts of the wealth distribution [89, 46, 28, e.g.,]. Synthetic savings are constructed as if each bracket of the wealth distribution was a single infinitely lived individual: for example, if the average wealth of the top 1% is $10m at the start of the year and $11m at the end, then the top 1% had $1m in synthetic savings. As such, synthetic savings are a composite measure that combines the effects of average wealth growth with the effect of mobility. They do not distinguish between them.

Since my approach explicitly accounts for mobility, it lets me disentangle the two effects. In the spirit of [30], I show that synthetic savings are the sum of several terms: one that depends on average wealth growth, one that depends on mobility, and additional terms that account for other factors, such as demography. This decomposition makes it possible to model synthetic savings more realistically.

Notably, I find that the way synthetic saving rates combine the effect of mobility with other factors is endogenous to the wealth distribution itself. That is, synthetic savings will differ depending on whether inequality is high or low, even if people’s actual behavior is the same. To eliminate this endogeneity, we would have to assume zero mobility in the wealth distribution.

2.3 Wealth and Capital Taxation

A well-known, early result in the theory of optimal taxation is that, in a standard neoclassical model, the optimal linear tax rate on capital is zero, even from the perspective of workers who own no capital [15, 42].121212Another famous rationale for not taxing capital comes from [2]. In their model, there is no heterogeneity of wealth conditional on income. Therefore, assuming income can be taxed, taxing wealth provides no additional equity gains while also distorting intertemporal choices. This justification for not taxing capital would not apply to my model since wealth is heterogeneous conditional on income. This result has been overturned in more sophisticated models which introduce, for example, uncertainty [1], incomplete markets [21], heterogeneous altruism [22], tax progressivity [58] or capital accumulation by workers [5]. More recently, [68] have reanalyzed the models of [15] and [42], and have overturned many of their conclusion: they show that significant capital taxes are in fact often desirable within these two models.

Overall, the main issue with the theory of capital taxation is that its models tend to behave erratically. Many of its results focus on edge cases and corner solutions, which are highly dependent on the specific primitives of the economy, can be hard to interpret, and imply unrealistic behavior. As a result, the theory has remained of limited use for guiding policy. For example, a common interpretation of the zero-tax result of [15, 42] is that their model implicitly assumes the capital stock to be infinitely elastic.131313See [3, 50, 60], although this interpretation is not universally accepted, see [68]. This assumption makes capital taxation infinitely costly, so the equity gain from taxation is never worth the efficiency cost. Such a setting arguably constitutes an extreme edge case. In more realistic models featuring a finite elasticity, the usual equity-efficiency trade-off would determine the desirability of capital taxation [50, 60]. In line with this view, [60] ultimately argued that the long-run elasticity of the capital stock to the net-of-tax rate is a sufficient statistic for the optimal design of capital taxation and developed formulas for optimal tax rates, similar to those that exist for labor income [57, 51].

However, the value of that elasticity remains elusive. In the short run, several empirical papers have used quasi-experimental settings to estimate it: [66] in Sweden, [47] in Colombia, [10] in Switzerland, [72] in the Netherlands and [41] in Denmark. With some exceptions, these elasticities tend to be small. This is consistent with the view that a government trying to raise revenue with a one-off, unexpected wealth tax could choose a very high marginal rate. But the policy-relevant parameter is the long-run elasticity, which is far more uncertain and likely larger. Indeed, the short-run elasticity only captures tax avoidance or short-run saving responses. But over time, wealth taxes also keep people from accumulating wealth, either through mechanical (lower post-tax rates of return) or behavioral effects (lower savings). This process slowly erodes the tax base. But because it takes a long time to materialize, it is hard to cleanly identify it in the data.

This paper provides a useful framework for addressing this issue. We can start from the empirically estimated wealth transition equation, which reproduces the true evolution of the wealth distribution. Then we can modify that equation to incorporate a wealth tax, as well as an arbitrary set of behavioral responses. For this paper, I focus on two effects (tax avoidance and a decrease in savings), but the framework is flexible enough to accommodate many other extensions. Using the modified equation for the evolution of wealth, we can simulate counterfactual evolutions of the wealth distribution and therefore estimate how the tax base would react to any wealth tax. We can fully simulate the model to observe transitory dynamics. However, if we focus on the long run, we can obtain simple analytical formulas that characterize the alternative steady-state. In my model, the long-run elasticity of capital supply remains finite in all cases because of mobility, but setting the mobility parameter to zero recovers the infinite elasticity as in [15] and [42].

We can connect the approach in this paper to two recent papers that try to assess the long-run effects of wealth taxes. [41] use their short-run elasticity estimates to calibrate a structural model of savings at the top. They indeed find a higher elasticity in the long run. [62] consider the problem of taxing the very top of the wealth distribution (billionaires) using data from the Forbes rankings. These two papers provide models that shed different lights on the problem. [41] model wealth accumulation using a deterministic model of intertemporal choice. This model features standard preferences over a consumption path and a taste for end-of-life wealth (i.e., bequests). They use it to derive analytical expressions linking the long-run elasticity of wealth to the short-run elasticity and preference parameters. This model emphasizes the role of behavioral savings responses, but as it is deterministic, it does not account for the role of mobility. In contrast, [62] only focus on mobility. Because they look at billionaire wealth, they assume that the role of consumption is negligible. In that model, mobility is the sole determinant of wealth elasticity in the long run. If it is low, then a wealth tax ends up taxing the same people again and again: as their wealth mechanically goes down, so does the tax base. Therefore, the elasticity of taxable wealth is high, and the ability to tax wealth is limited in the long run. However, if mobility is high, the tax base often gets renewed. Individuals are subjected to the tax for shorter periods, with new, previously untaxed wealth entering the tax base regularly: as a result, the elasticity is lower.

My model combines the mechanisms from both papers and accounts for tax avoidance. Combining the mechanisms as such substantively alters some of the conclusions. In [41], there is a mechanical effect of wealth taxes, and because the model is deterministic, this mechanical effect becomes infinite in the long run. Their model can generate a finite elasticity of capital supply overall, because an infinite behavioral effect compensates for the infinite mechanical effect in the opposite direction. However, looking at these effects separately in the long run still runs into degeneracy problems.141414[41] circumvent the issue by looking at a long but finite horizon (30 years). In comparison, because I introduce mobility, my model remains well-behaved at the steady state even if I shut down behavioral responses. In [62], the wealth tax can only consist of a constant average tax rate over a threshold. In comparison, my model allows for arbitrary tax schedules, including the more standard case of a constant marginal rate above a threshold. Far above the tax threshold, the marginal and the average tax rate are similar, so their model behaves similarly to the mechanical component of my mine. Close to the threshold, however, the distinction between them matters. In particular, I find that under a purely mechanical model, even confiscatory wealth tax rates would raise a non-negligible revenue from people just above the tax threshold who recently entered the tax base. And so the Laffer curve never goes to zero. As a result, unlike [62], I conclude that the mechanical model remains insufficient to characterize revenue-maximizing tax rates: doing so requires a behavioral response.

3 Theory

Time is continuous, indexed by . Individuals are indexed by . Individual wealth evolves stochastically. I model this evolution using an Itô process, which can flexibly model most continuous-time stochastic processes. Such a process is locally characterized by two parameters: the drift , and the diffusion . Over a small period of time , the change in the value of the wealth of individual at time has mean and variance . This process is represented in the form of a SDE and commonly written as follows:

This section will explain how the parameters for drift and diffusion at the individual level can be connected to the aggregate evolution of the wealth distribution (while accounting for heterogeneity, demography, etc.), and therefore how they can be inferred from changes in the shape of the wealth distribution.

3.1 Income and Consumption

3.1.1 Evolution of Individual Wealth

Individual has idiosyncratic consumption, labor income, and rate of return on their wealth. Similarly to [13]’s (\citeyearcarroll_buffer-stock_1997) interpretation of [24]’s (\citeyearfriedman_theory_1957) permanent income hypothesis, labor income is the sum of a permanent (i.e., slow-moving) component , and of transitory shocks with variance — with and both being arbitrary bounded stochastic processes. Consumption and rates of return follow a similar model, with slow-moving components and , and transitory shocks with variances and . I express all monetary quantities as a fraction of average national income, which grows at rate . As a result, wealth evolves according to the SDE:151515This formulation assumes that the transitory shocks are uncorrelated. We could account for correlated shocks by including additional covariance terms, as in Bienaymé’s identity. To simplify the exposition, I focus on the uncorrelated case.

| (1) |

That is, individual wealth is a stochastic process with a drift equal to and a diffusion equal to . Note that the economy’s growth rate appears in the drift term due to the normalization of all the quantities by the economy’s average income.

3.1.2 Evolution of the Distribution of Wealth

We can directly relate the evolution of individual wealth described by equation (1) to the overall distribution of wealth. A standard result of stochastic calculus states that, if a large number of stochastic processes follow the same SDE, then the probability density function (PDF) that describes the distribution of their value at a given time follows a partial differential equation (PDE) known as the [44] forward equation [25]. This result provides a direct way to connect the evolution of individual wealth (as in equation (1)) with the aggregate distribution of wealth (as is observed in historical data). However, I need to account for the possibility that the drift and the diffusion vary across individuals . To that end, I will apply a result from [78], which states that it is possible to average out the heterogeneity of individual wealth processes and still retrieve the same wealth distribution in the aggregate. After applying that result, I use the [44] forward equation to connect equation (1) to the evolution of the wealth distribution.

Reduction to a Single Equation using [78]’s (\citeyeargyongy_mimicking_1986) Theorem

In simple terms, [78]’s (\citeyeargyongy_mimicking_1986) theorem states the following. Consider a large number of stochastic processes , each following a SDE with their own drift and diffusion . Then the PDF describing the distribution of the value of these processes will behave exactly as if their drift and their diffusion were replaced by the conditional expectations and . This result, plus some basic rules of stochastic calculus, makes it possible to reduce the arbitrarily complex nature of individual wealth accumulation into a single SDE that characterizes the entire wealth distribution. I can state the following result.

Proposition 1.

Let , and be the average labor income, rate of return and consumption, conditional on wealth at time . Similarly, let , and be the variance of labor income, rates of return and consumption, conditional on wealth at time . Then, the stochastic process governed by the SDE with deterministic coefficients:

has the same marginal distribution as the process described by equation (1).

Proof.

See Appendix A.1. ∎

Proposition 1 reduces the dynamics of the wealth distribution to a single SDE, in which everyone with the same wealth faces the same drift and the same diffusion . In that equation, the diffusion becomes easily interpretable as a mobility parameter. If it were equal to zero, everyone with the same wealth would face the same wealth growth, so there would be no movement across the distribution. But when that parameter is not zero, the approach can account for the mobility across the wealth distribution, which is a sizeable phenomenon [30]. From now on, I will therefore refer to as a mobility parameter.

The Kolmogorov Forward Equation

Using the reduced SDE of Proposition 1, I can now apply the Kolmogorov forward equation. The density which describes the distribution of wealth at time obeys the PDE:

| (2) |

This equation describes the evolution of a quantity that is observable in the historical data (the density of wealth ) while connecting it to parameters that characterize wealth accumulation at the individual level: the drift , and the diffusion . Thus, it directly connects individual economic behavior with the distribution of wealth.

3.1.3 Interpretation of the Different Effects

The previous section derived equation (2) using results from stochastic calculus. This section provides a more direct and intuitive understanding of the equation. The purpose is twofold. First, it provides an understanding of the central equation that does not require familiarity with stochastic calculus. Second, it gives a more transparent basis for how and why the decomposition introduced in this paper works.

Integration of the Kolmogorov Forward Equation

For empirical purposes, it is useful to rewrite equation (2) in its integrated version, which involves the cumulative distribution function (CDF) of wealth, . After re-arranging terms, we get:

| (3) |

Each of these terms captures a different mechanism. I discuss them in turn below. To fix ideas, let us consider and that the population is normalized to one, so that is the number of billionaires, and is the change in the number of billionaires.

Local Effect of Average Change in Wealth

Assume that wealth growth is a deterministic function of wealth: everyone with the same wealth experiences the same wealth change, so there is no mobility (). Consider the case where wealth growth is positive at the top, so that the number of billionaires increases.

Over a short period, the number of people crossing the $1bn threshold will be proportional to (i) , the number of people that were initially at the threshold, and (ii) , the pace at which their wealth increases. Therefore, we get , which corresponds to equation (3) when .

This formula is known as a transport equation. If wealth growth is uniform (), then it translates the entire wealth distribution by a factor over a period . The general formulation makes it possible to consider non-uniform wealth growth.161616Note that with the change of variable , we get . Hence, is the growth of the th quantile.

Local Effect of Mobility

Now, consider the opposite thought experiment. Everyone, even if they have the same wealth, experiences a different wealth growth. But they are as likely to go up or down, so, on average, wealth growth is zero (). Furthermore, assume that the amplitude of wealth variations is uniform (). Under these conditions, the number of billionaires will still change.

Indeed, some people just below $1bn will see their wealth increase and become billionaires. This flow is proportional to (i) , the number of people right below $1bn, and (ii) the amplitude by which their wealth varies. Conversely, some people just above $1bn will see their wealth decrease and drop out of the list of billionaires. This flow is proportional to (i) , the number of people right above $1bn and (ii) the amplitude by which their wealth varies.

In general, these two flows will not cancel out because there are not as many people right below and right above $1bn. This difference between the population on each side of the threshold is effectively captured by the derivative of the density . Mathematically, this derivative appears from writing the difference between the two flows, and then taking the limit as and . After applying the correct proportionality factor, we get , which corresponds to equation (3) when and . Unlike the equation modeling the effect of average wealth growth, in this equation, the effect on the number of billionaires depends not on the value of the density but on its gradient. This formula is known as a diffusion equation and is best understood as a transformation that flattens wealth density.

To make sense of this effect, consider two extremes. First, if the wealth density is flat at the top, then the number of people who cross the $1bn threshold from both sides will cancel out. Hence, even though wealth changes at the individual level, the overall effect on the distribution is nil. Now, assume that, on the contrary, the wealth density is infinitely steep, so that there are no billionaires but many people just below $1bn. Some people will see their wealth increase and become billionaires. But since there is initially no one above $1bn, there can be no countervailing flow of people leaving the group. And therefore, the number of billionaires will increase very fast.

Local Effect of the Mobility Gradient

If the amplitude of wealth mobility is not uniform, there is a third effect on the wealth distribution. Indeed, assume that there is more variation in wealth growth above $1bn than below: then, downward mobility will exceed upward mobility. Thus, even with no average growth and a flat density, people who drop out of the billionaire group will outnumber those who enter it. This phenomenon creates an additional effect on , which depends on how mobility varies throughout the distribution. Hence, it is a function of the mobility gradient , and is equal to .

3.1.4 Phase Portrait and The Dynamics of Wealth Inequality

Consider the case where the drift and mobility parameters are constant over time: and . Equation (3) is best represented as a curve that relates the current level to the current evolution of inequality, as in Figure 3. This curve — a phase portrait — lets us picture the dynamics of wealth inequality in a simple way.

Note: This diagram is a phase portrait of the dynamics of inequality for a given wealth level located towards the top of the wealth distribution. These dynamics can be pictured in a two-dimensional space where each axis represents a quantity associated to the wealth distribution, whose PDF is and whose CDF is . The -axis is equal to and is a proxy for inequality levels (high values mean high inequality). The -axis is equal to and is a proxy for inequality changes (high values mean increasing inequality). The diagram represents the transition from a low inequality level () to a high inequality level (), with constant and . During this transition, the system moves alongside the orange line with slope and intercept . When the system reaches the -axis, where , it is a its steady-state.

The term on the right-hand side of equation (3) measures the relative slope of the density. In the upper tail of the wealth distribution, the density is sloping downward, so . This value is a good proxy for top wealth inequality. If it is high, then the density decreases at a slow rate: i.e., the tail is fat, and inequality is high. Conversely, if its value is low, then inequality is low as well.171717If wealth follows a Pareto distribution with coefficient , then . So, as , inequality goes to infinity and increases to zero. We can analogously interpret the term on the left-hand side of equation (3) as a change in the fatness of the top tail of the distribution. When it exceeds zero, the tail becomes fatter, and inequality increases.181818If wealth follows a Pareto distribution with coefficient , then . Therefore, is associated with a decrease in , which corresponds to an increase in inequality.

In Figure 3, the first quantity (inequality level, in blue) is on the -axis and the second quantity (inequality change, in green) is on the -axis. Equation (3) states that, with stable parameters, the data points representing the current state of inequality must lie alongside a straight line (in orange), with intercept and slope . Where this line crosses the -axis, inequality is neither increasing nor decreasing: this is the distribution’s steady state.

Dynamics of Wealth Inequality and Convergence to a Steady State

Consider the transition to a high inequality steady state. On Figure 3, start from the inequality level . This level is below the steady-state level , so inequality will change. We can decompose this change into (i) the effect of average wealth growth and of the mobility gradient, which the intercept captures, and (ii) the effect of mobility, which the slope captures. As we can see on the graph, (i) decreases inequality, whereas (ii) increases it. At first, the effect of (ii) is stronger, so inequality increases overall by . In the next period, inequality is higher, equal to . A higher inequality means a fatter tail, hence a flatter density. Having a flatter density weakens the effect of (ii). The effect of (i), on the other hand, remains unchanged. Overall, inequality still increases, but by a lower amount, . The process repeats. Inequality keeps increasing, which flattens the density, weakens the effect of (ii) but leaves the effect of (i) unchanged. Asymptotically, we reach . At this point, the effect of (ii) has been weakened to the point that it perfectly counterbalances (i). We have reached the steady state.

Rationale for the Steady State

This framework provides a robust justification for the emergence of a steady state — one that doesn’t preclude but also doesn’t require behavioral responses. Without mobility, the only way to get a steady-state distribution of wealth is for behavioral responses (and general equilibrium effects) to lead to a point where saving rates as a proportion of wealth become identical throughout the distribution. Any deviation from this situation leads to a degenerate steady state in the long run. In contrast, here, the distribution eventually stabilizes because of the mechanical interaction between mobility and drift, so the model remains well-behaved for a wider range of economic behaviors.

Distinction Between Drift and Mobility

This framework shows how drift and mobility have different impacts on the distribution and why that distinction matters. In a model without mobility, the red line in Figure 3 would be flat. The only way to account for inequalities of wealth that are neither increasing nor decreasing at a constant rate is to assume that the intercept changes with each period (which usually implies some form of behavioral change). In contrast, once we introduce mobility, it becomes possible to account for any linear downward-slopping evolution of inequality in the phase portrait of Figure 3 with a much more parsimonious model that only involves two time-invariant parameters: one for drift and one for mobility.

3.2 Other Processes Affecting the Wealth Distribution

I account for other phenomena impacting wealth distribution besides drift and diffusion (which capture individual income and consumption). The three phenomena that I consider in this paper are birth and death, inheritance, and assortative mating. I first introduce these effects in equation (2) and then gives a version of equation (3) that include them as well.

Births and Deaths

At any time , a fraction of people die. Let be the density of their wealth. Simultaneously, a fraction of people appears with a random initial endowment drawn from a distribution with density . The total population grows at a rate . This process impacts , i.e., the change in the wealth density at wealth and time , by:

and the equation (2) becomes:

Inheritance

I model inheritance as a jump process. With a probability , people see their wealth jump from to where is the amount of inheritance received, net of taxes. Let be the density of the value of the inheritance, conditional on the value of wealth, and conditional on receiving an inheritance. We can model the jump process as a death with rate and as an injection with rate . So, the effect of inheritance on , i.e., the change in the wealth density at wealth and time , is:

and the equation (2) with both demography and inheritance is:

Marriages, Divorces and Assortative Mating

Finally, I account for the effect of marriages and divorces. I adopt the convention that wealth is split equally among spouses. At any time , a fraction of people get married. Let be the density of their wealth as individuals, and be the density of their wealth as couples. The strength of assortative mating is captured by the relationship between and : at the limit, if people always choose a spouse with identical wealth, then . The effect of marriages on the wealth distribution is therefore . We can construct an opposite process for divorces. Let be combined effect of marriages and divorces on . Then the equation (2) with the effect of demography, inheritance, marriages, and divorces becomes:

| (4) |

Integrated Version

Rewrite equation (4) in an integrated form, similar to (3). Define , , and . After integrating equation (4) and re-arranging terms, we get:

| (5) |

This equation is similar to (3), with additional correction terms on the left-hand side to account for demography, inheritance, and assortative mating. The fundamental dynamics of wealth inequality remain similar to those pictured in the phase portrait in Figure 3, except that the -axis needs to be adapted to include the correction terms. This equation will serve as the basis for the decomposition introduced in this paper.

3.3 Decomposition of the Different Effects

I will use equation (5) to decompose the various factors affecting the distribution of wealth. All the terms in the equation can be directly observed or separately estimated, except those related to consumption. Therefore, these unobserved parameters have to be estimated as a type of “residual.” This section explains how.

Estimating Equation for the Complete Model

Let us go back to the equation (5). Separate the drift and the diffusion into their observed component (income) and their unobserved component (consumption):

Move the observed components of drift and mobility to the left-hand side of equation (5). The complete equation for the left-hand side becomes:

All the components of are either directly observable or separately estimable. We can therefore rewrite (5) in its final form:

| (6) |

Identification

Equation (6) provides the basis for estimating the parameters. It shows a relationship similar to that shown in Figure 3. We require three assumptions to get point estimates of the mean and the variance of consumption conditional on wealth over a period .

Assumption 1.

For all , we can observe (or separately estimate) and at distinct times with .

Assumption 2.

For all , the parameters and are constant over time, i.e., and for .

Assumption 3.

The wealth distribution is changing over time, in the sense that, for all , we observe the distribution for at least to periods such that .

These three assumptions ensure we can meaningfully fit a line through the different points as in Figure 3. Assumption 1 states that we need to observe the wealth distribution and its evolution during two different periods, a consequence of the fact that we need at least two points to be able to fit a line. In practice, and in the presence of statistical noise, more than two points are preferable to get robust estimates. Assumption 2 ensures that the parameters that govern the relationship (6) remain stable over the period of time under consideration. Finally, Assumption 3 states that the distribution of wealth must change over the period where we observe it. This assumption comes from the fact that we are using local variations in the flatness of the density to disentangle the drift from mobility. This strategy only works if the flatness does, in fact, vary. If these three assumptions are satisfied, then we can proceed with the estimation in two steps:

- Step 1

-

Estimate and for every using a line-fitting method.

- Step 2

-

Using the estimate for , estimate the mobility gradient , and use it to get the estimate of .

Ex-ante Estimate of the Effect’s Magnitude

I use variations in the flatness of the density over time to disentangle the effect of drift from that of mobility. But are these variations large enough to provide reliable empirical estimates? Some rough but simple calculations can give a general idea of the magnitude of the effects at play. Between its high point in the 1970s and today, the Pareto coefficient of wealth in the upper tail went from to . Assume a mobility parameter at the top, which matches the estimates in this paper (and separate estimates from the SCF and the PSID). The effect of mobility under these conditions is equal to . A useful way to interpret this number is to say that mobility has the same effect on the distribution as an average wealth growth of , which went from to of wealth — a 4% change. The change in the effect of mobility that is attributable to the flattening of the wealth density at the top is, therefore, sizable — equivalent to the mechanical effect that a permanent 4% wealth tax would have.

Potential Limitations

The main limitation of the method is that it requires the parameters for the drift and the mobility induced by consumption to be constant (or at least not to have a downward or upward trend) over sufficiently long periods. Estimates may be biased if this is not the case. For example, assume that the drift decreases over time. On the phase portrait in Figure 3, the linear relationship (in orange) moves down over time. As a result, the observed data points on the phase portrait will lie on a curve that could take many different shapes, but, in general, will appear more downward-sloping than the true relationship. If we were to estimate the decomposition in that context, we would therefore overestimate the diffusion parameter.

In practice, there are two ways to address this issue. The first one is to check that the empirical phase portrait to which we fit the line remains relatively close to linearity. While this does not guarantee that the assumption of a constant and is verified, it can identify some problematic cases. The second one is to verify that the parameters estimated from the decomposition are consistent with external estimates of savings and mobility. I perform both checks in this paper’s empirical section, suggesting that the simple model with a constant and since the 1980s works well.

4 Estimation for the United States

4.1 Data

I estimate the parameters in decomposition (6) for the United States. I start in 1962, when sufficiently detailed microdata on the distribution of income and wealth in the United States becomes available. I primarily rely on the tax-based microdata from [90], which I complement in a number of ways. Using the data collected, I perform microsimulations of mortality, birth, inheritance, marriage, and divorce, which I use to estimate the impact of the corresponding phenomenons on the wealth distribution. I briefly review the data and methodology below and provide more details in Appendix B.

Income and Wealth

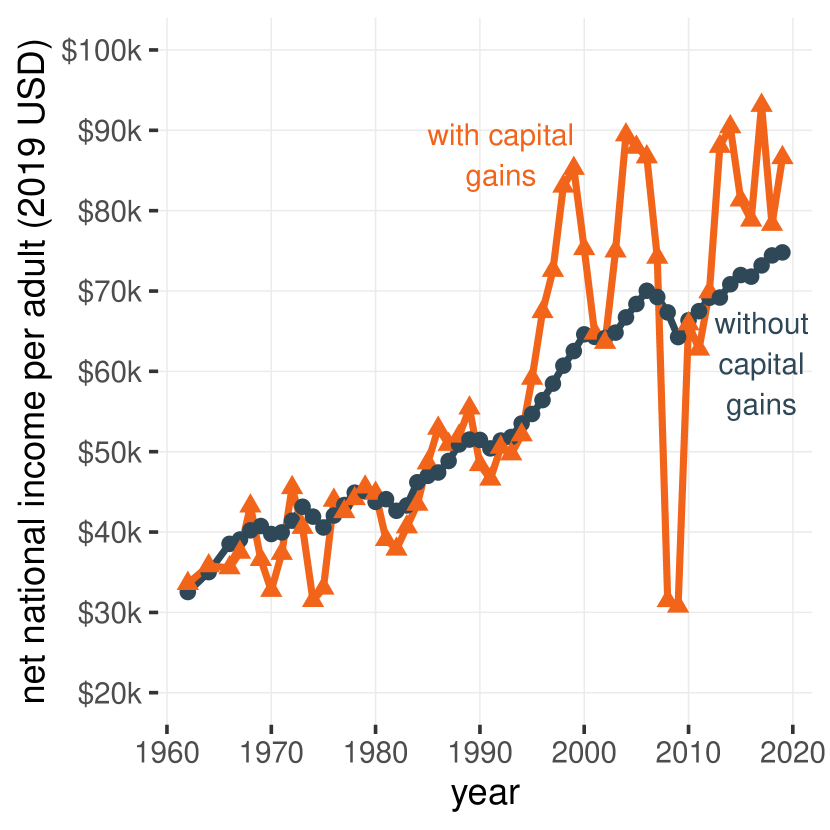

For income and wealth, I rely on the Distributional National Accounts (DINA) tax-based microdata from [90]. These data distribute the entirety of national income and wealth, as measured by the national accounts, every year since 1962, to adult individuals (20 and older). They infer the distribution of wealth from capital income flows, following the capitalization method of [89].191919Their latest revision [90] accounts for heterogeneous returns. This data does not distribute capital gains since they are not part of national income. I incorporate them in the data by assuming a constant capital gains rate by asset class, as in [87]. The information on age in the DINA microdata is also limited, so I replace it with information from the Survey of Consumer Finances (SCF). I match DINA and SCF observations one-to-one based on their rank in the wealth distribution. I use this to estimate a rank in the age distribution by sex for each observation and attribute to them the age that matches this rank according to official demographic data.

Demography and Intergenerational Linkages

I estimate the entire demographic history of the United States since 1850 by year, age, and sex, including population counts, mortality rates, female and male fertility rates by birth order. I start the estimation in 1850, long before the income and wealth data starts (in 1962), because I use the demographic data to simulate intergenerational linkages between parents and children. So if a centenarian dies in 1962, I must be able to retrace that person’s entire fertility history since their birth and retrace the mortality history of that person’s children.

I construct this data by collecting and harmonizing data from official sources (United States Census Bureau), historical databases (Human Mortality Database, Human Life Table Database, Human Fertility Database, Human Fertility Collection) and academic publications [79]. To make projections for the future, I rely on the forecast (medium variant) of the World Population Prospects [93]. For male fertility rates, which are not a standard demographic parameter, I combine the female fertility rates with the joint age distribution of mixed-sex couples in the IPUMS census microdata [88].

First, I use this data to simulate deaths, assuming that people die at random according to their age and sex-specific mortality rate. I also account for births by assuming that people enter the population at age 20 with a constant exogenous wealth distribution estimated from the data.202020People aged 20 have very low levels of wealth, so in practice, this is close to assuming that people start with zero wealth.,212121The birth rate is estimated here as a residual between population growth and the crude death rate, so in effect, it also incorporates the effect of immigration. Second, I simulate intergenerational linkages. For every person in the data, I assume this person had children according to their sex, age, year, and birth-order-specific fertility rates. Then I assume these children experience mortality in line with their sex, year, and age-specific mortality rates. This methodology generates a distribution for the age and sex of the direct descendants of every person in the sample, which I use to distribute inheritances.

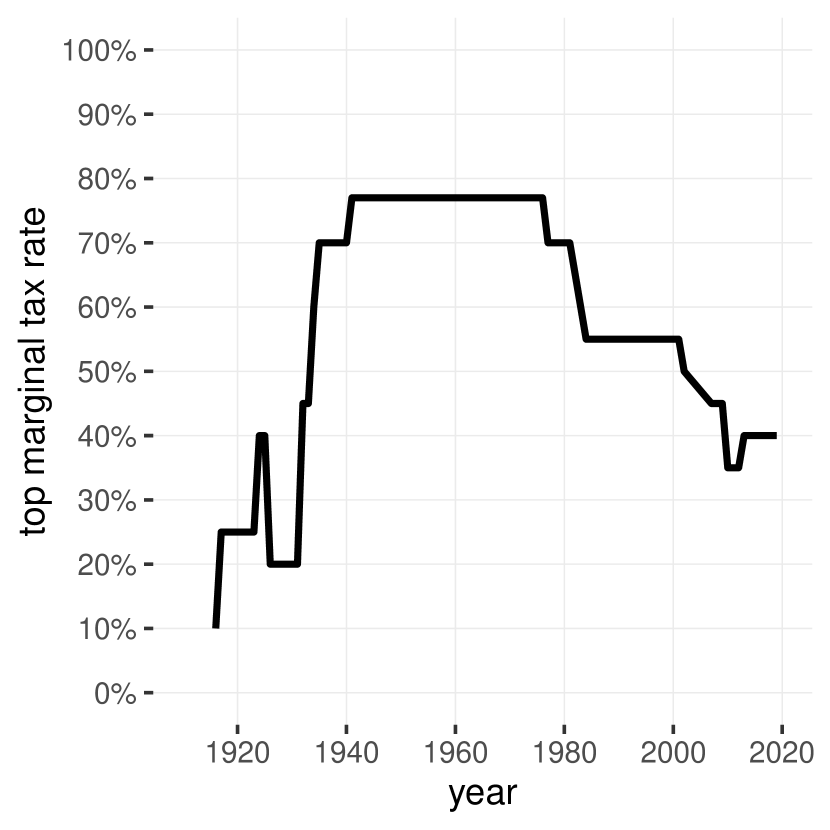

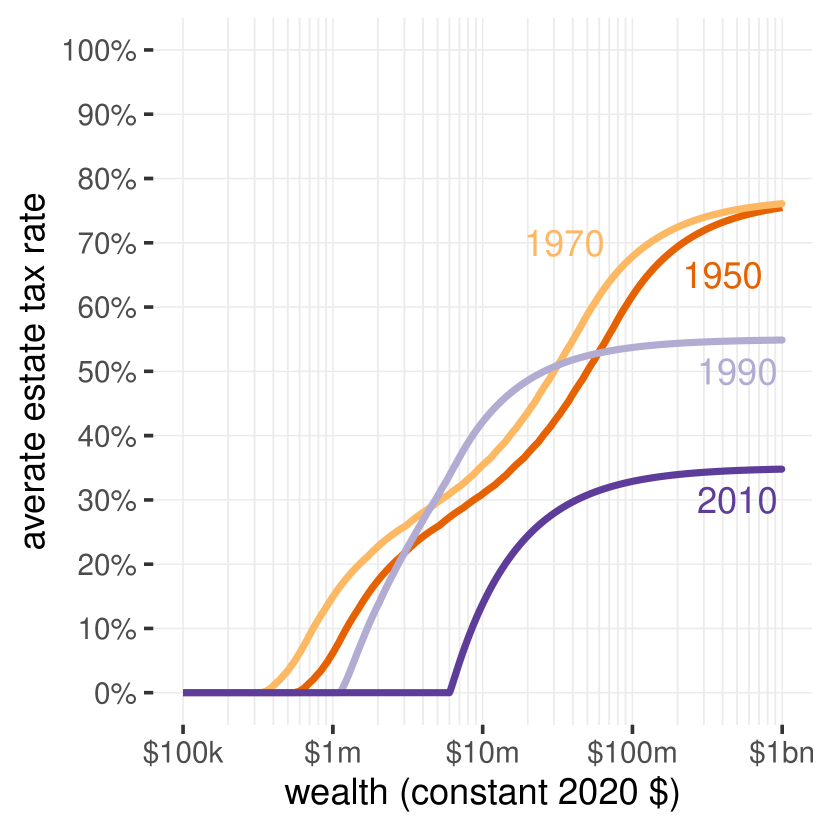

Inheritance and Estate Taxation

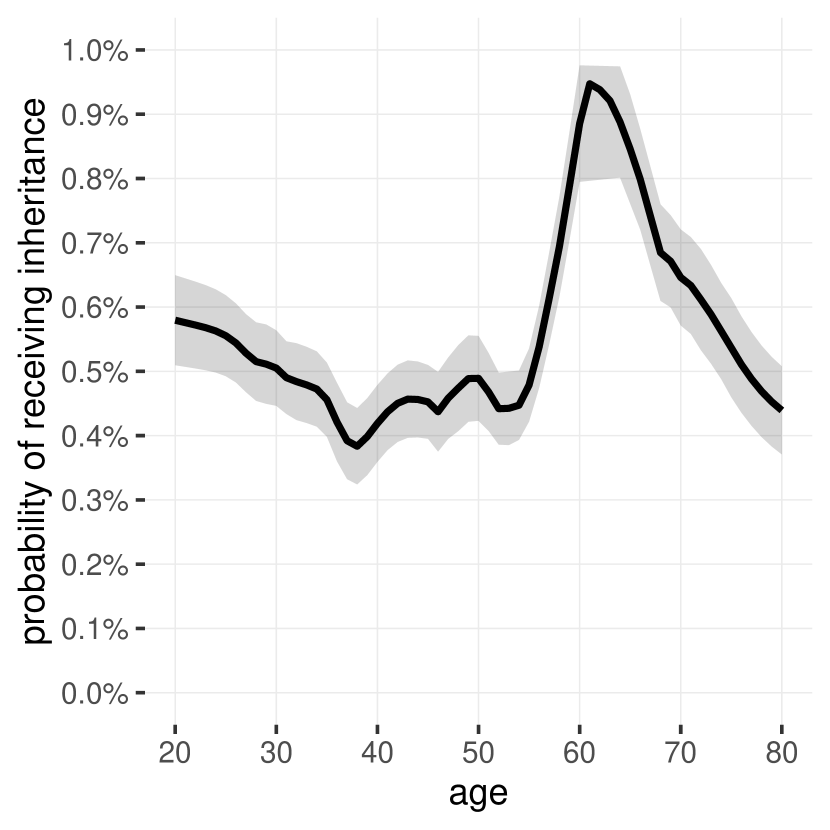

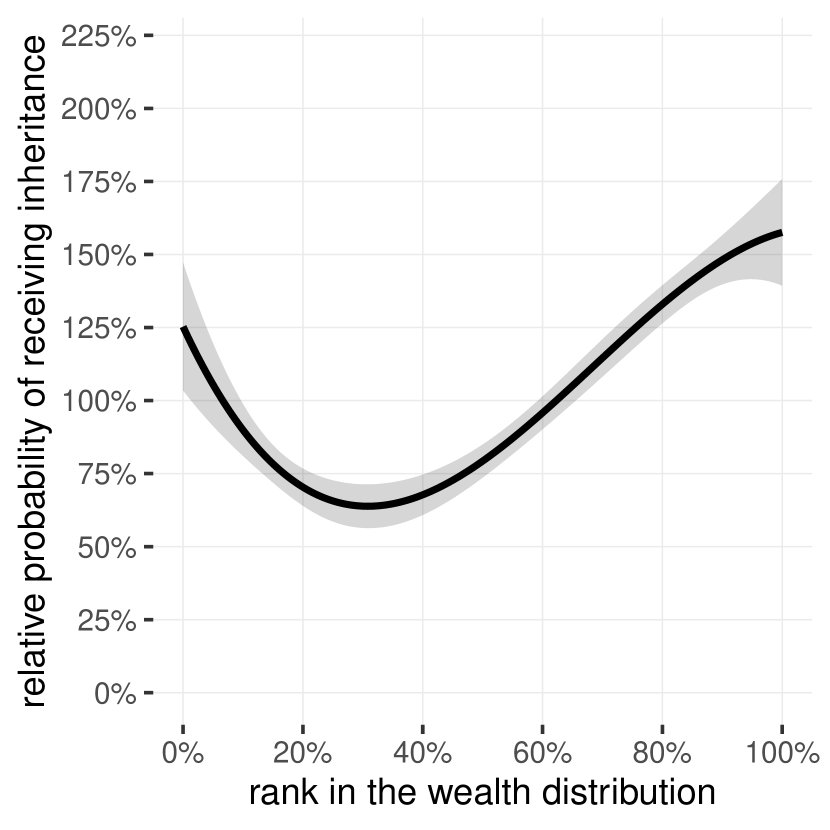

When someone dies, I assume that their wealth is transmitted to their spouse (if any), without estate tax, or to their children, after payment of the estate tax. To calculate the estate tax, I collect complete statutory schedules of the federal estate tax over the second half of the 20th century. I assume that wealth is split equally among descendants, as is the norm in the United States [85]. I account for the possibility that wealthier people are more likely to inherit and receive larger inheritances. I use the SCF to estimate the relative probability of receiving an inheritance, as well as the rank in the inheritance distribution, as a function of the rank in the wealth distribution, conditional on age. Within a given age group, I simulate international wealth transmission according to these parameters.

Marriages, Divorces and Assortative Mating

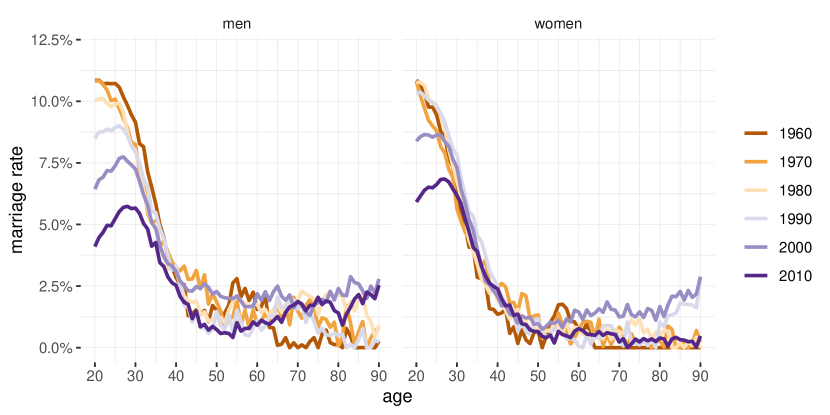

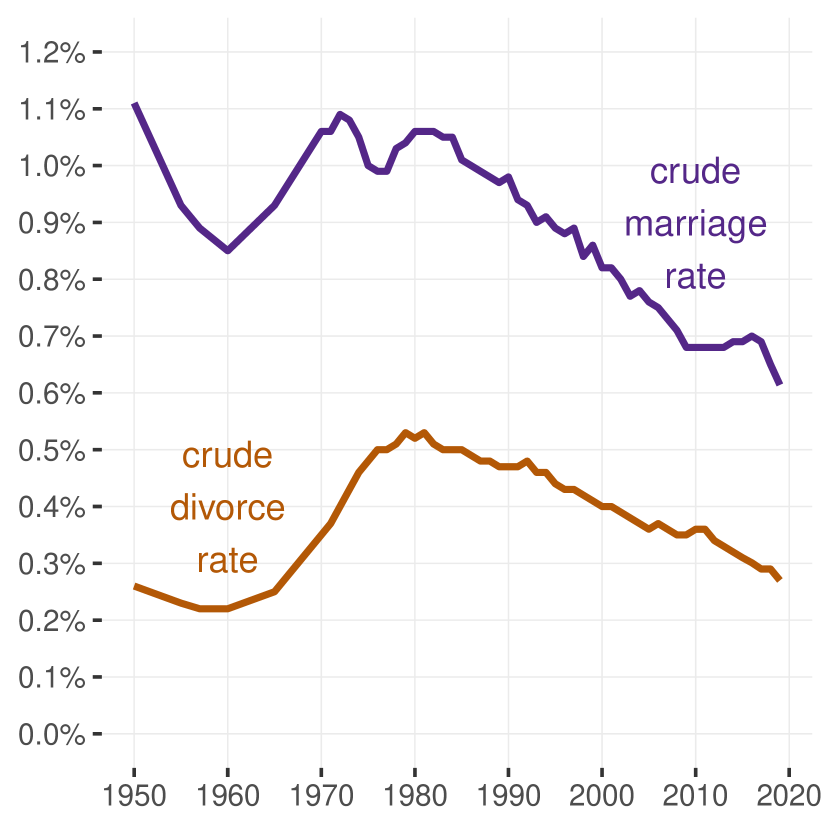

I collect data on the aggregate rate of divorce and marriage from the National Vital Statistics System (NVSS) [74]. In addition, I reconstruct age and sex-specific rates using population data disaggregated by marital status from IPUMS census microdata [88].

I determine the extent of assortative mating by estimating the joint distribution of the ranks in the wealth distribution at the time of marriage using the Survey of Income and Program Participation (SIPP) panel (2013–2016). I also consider the impact of assortative mating on divorce by estimating the distribution of the share of wealth owned by each couple member before they get divorced using the same data.

Then, I simulate the process of marriage and divorce by randomly selecting people to get wedded in a given year according to age and sex-specific marriage rates, and then marry them to one another to reproduce the joint distribution of wealth ranks at marriage in the SIPP. Similarly, I simulate the effect of divorce by randomly selecting people to get separated according to their age and sex-specific divorce rates, and split the couple’s wealth among both spouses according to the SIPP data.

4.2 Estimation

Wealth Distribution

First, I normalize the distribution of wealth by the average national income per adult. Then, I transform it using the inverse hyperbolic sine function ().222222I.e., . This transformation makes the distribution of wealth easier to manipulate empirically. And because we operate in a continuous time framework, it creates no practical difficulty: Itô’s lemma establishes a direct correspondence between the parameters of the process for and for .232323Itô’s lemma states that, if a process follows the SDE , then follows the SDE . See Appendix Section C.3 for details.

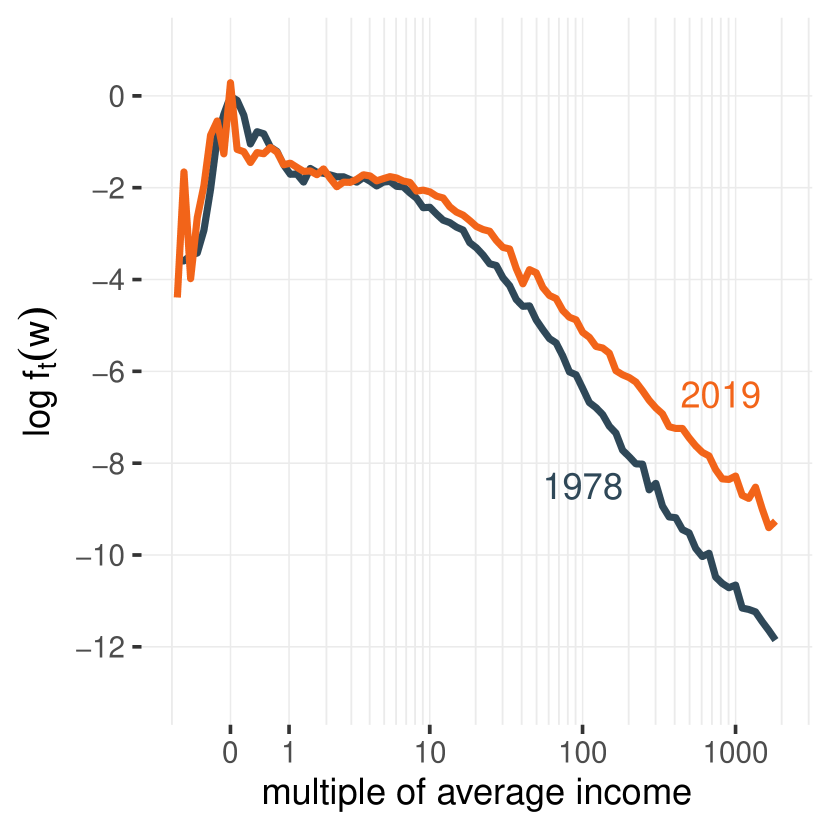

Source: Own computation using the Distributional National Accounts (DINA) microdata from [90]. Note: Wealth is always expressed as a multiple of national income. Densities in Figure 4(a) are estimated as histograms with 91 bins of size on the scale, ranging from to times average income ( to on the scale).

I select a range of values (from to times average income) which the wealth microdata consistently covers over the entire period.242424The range goes from to on the scale. I divide this range into bins of equal size, each representing units of .252525This represents 91 bins. Figure 4(a) plots the density of wealth, as estimated by the frequency of these bins. I display two years: 1978, which has the lowest inequality, and 2019, which has the highest inequality and is also the most recent data available. I use the logarithm of the density, so changes in the top tail of the wealth distribution are more clearly visible. It appears linear in the top tail, which follows from the fact large wealth holdings follow a power law.262626At the top, the wealth distribution is approximately Pareto, and the inverse hyperbolic sine is approximately logarithmic, so the distribution of transformed wealth in approximately exponential. Note that , i.e., the derivative of the logarithm of the density is equal to the quantity of interest on the right-hand side of equation (6). Hence, our interest lies in the slopes of the lines, which I estimate by running locally weighted linear regressions through the values of Figure 4(a).272727In the benchmark specification, I use a rectangular kernel and a bandwidth of . See Appendix C.4 for robustness checks. The top tail has driven most of the changes in the wealth distribution, and indeed this is where we observe most of the variation. In 1978, when inequality was at its lowest, the density at the top was quite steep, with a slope around . By 2019, inequality had increased dramatically, leading to a fatter tail and a flatter density, with a slope around .

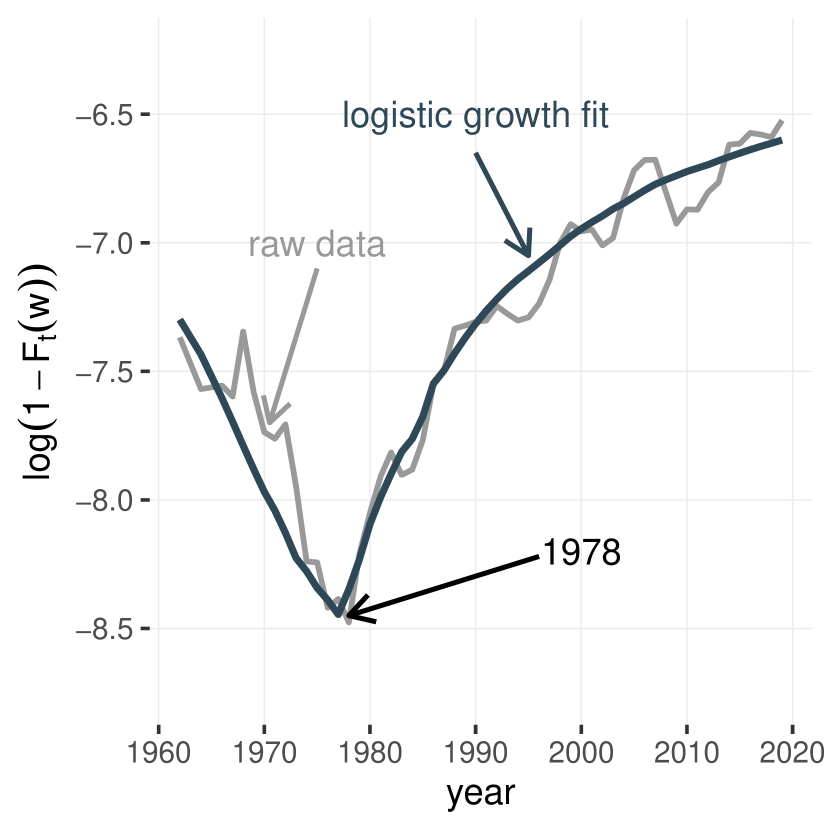

Changes in the Distribution of Wealth Over Time

For each wealth bin, I estimate , which is the relevant measure for the evolution of the wealth distribution as it appears on the left-hand side of equation (6). Let us begin with , the logarithm of the numerator (see Figure 4(b) for the bin corresponding to 500 times the average income). The raw data shows two clear trends, one on each side of the year 1978, which correspond to the decreasing part and the increasing part of the U-shaped evolution of wealth inequality. I use a parametric approximation to filter out the short-run variations around these trends (which are not my focus here). Using nonlinear least squares, I fit a logistic growth model for each bin, separately on each side of the year 1978.282828The logistic curve can be written as where are the three parameters which capture, respectively, the initial value, the asymptotic value, and the rate of convergence.,292929This model is attractive for three reasons: (i) empirically, it fits the data well, (ii) it captures the features that we expect, i.e., that of a process that grows at first, and then settles to a steady state, and (iii) if we locally approximate the distribution with an exponential distribution with rate parameter , then equation (3) collapses to a logistic differential equation for , whose solution is the logistic curve function. Note that this approximation can only be valid locally and does not provide a global solution to the partial differential equation (3). From this parametric approximation, I estimate the time derivative of . Finally, I retrieve the quantity of interest using the fact that .

Other Processes

I separately estimate the effects of income, demography, inheritance, marriage, and divorce, using the microdata and, when needed, microsimulations based on the microdata. For income, I directly calculate the mean and the variance within each wealth bin and use this to estimate the drift and the mobility induced by income. For demography, inheritance, marriage, and divorce, I simulate the processes in the microdata and use the difference between the CDFs before and after simulation to estimate the effects.

Estimation of Drift and Mobility

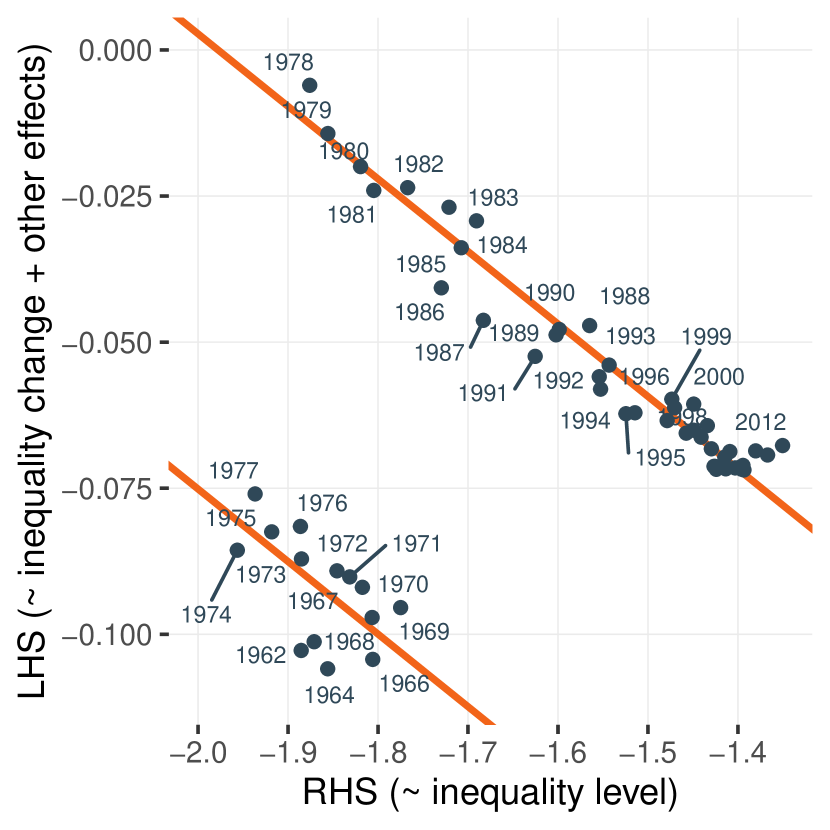

Having estimated all the observable components of equation (6), we can plot the empirical counterpart to the phase portrait in Figure 3, for every wealth bin. The result, for each year and for the bin corresponding to a wealth level of 500 times the average income, is shown in Figure 5(a). Due to the inverse hyperbolic sine transform of wealth and to the inclusion of effects besides drift and mobility, the interpretation of the parameters is not as straightforward as in Figure 3. But the fundamental linear relationship should hold.

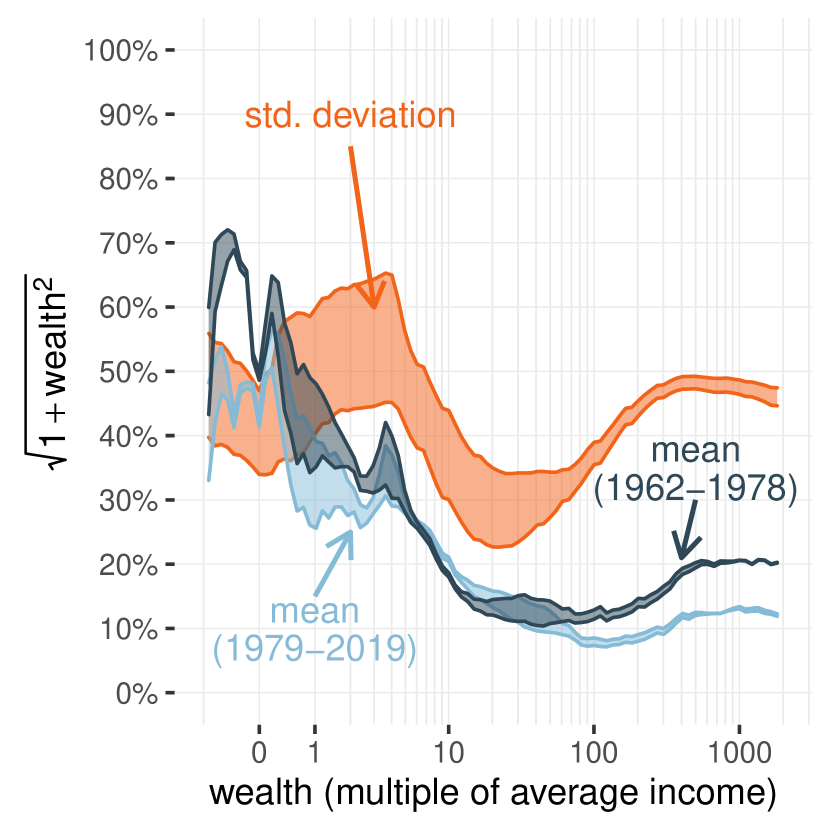

Source: Author’s estimations. Note: This scatter plot shows the empirical counterpart to the phase portrait described by equation (6), for a level of wealth that correspond to 500 times the average national income (around $40m in 2022). The two linear lines, fitted for 1962–1977 and 1978–2019, correspond to the relationship defined by equation (6). See main text and Appendix C for details on the estimation procedure.

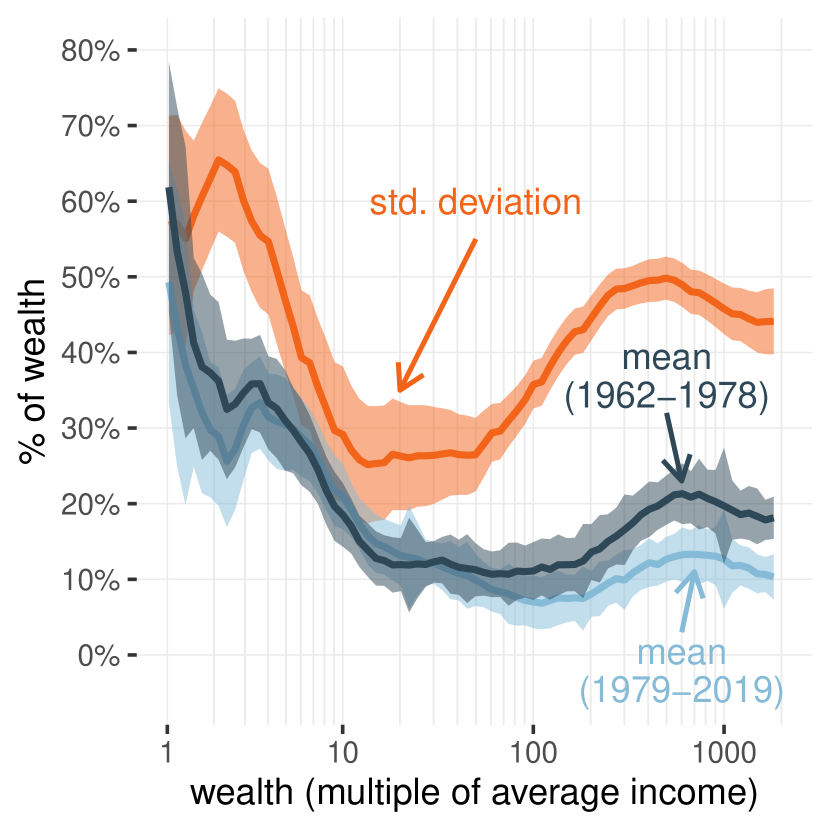

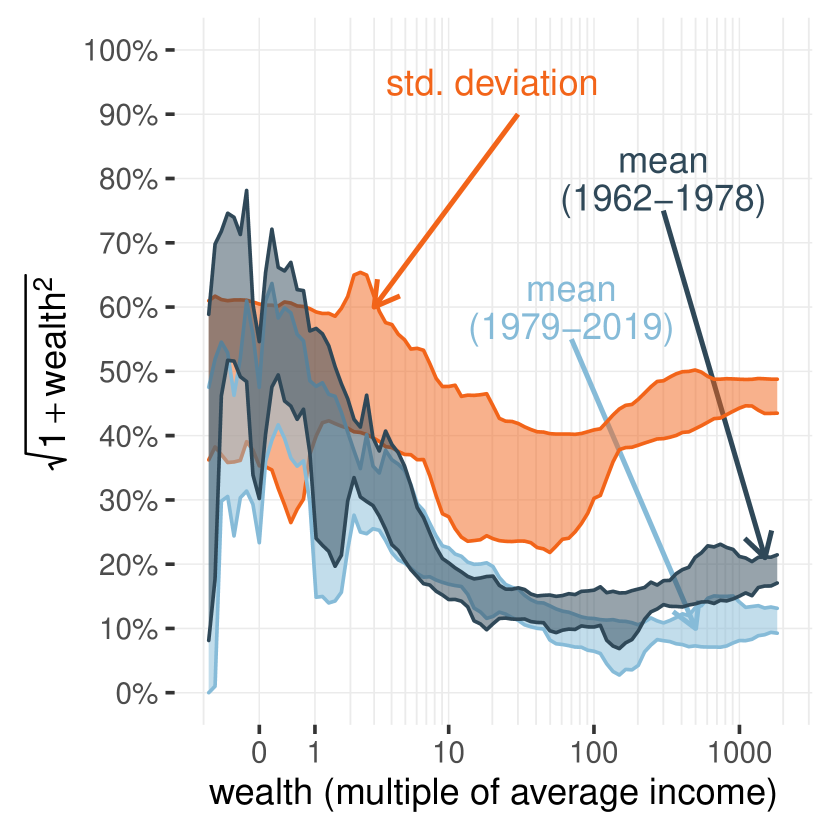

Source: Author’s estimations. Note: This graph shows the average and the standard deviation of consumption by wealth, as estimated from the slope and the intercept of the linear relationships in the left panel, for every wealth bin. Parameters have been adjusted to account for the data transformations, as explained in Appendix C.3. Areas around the lines indicate 95% confidence intervals, estimated using a bootstrap procedure described in Appendix C.2.

Two facts stand out. First, there has been a structural break between 1962–1977 and 1978–2019. Indeed, it is impossible to account for wealth’s evolution during both periods by assuming the same linear relationship on the phase portrait: the underlying accumulation process (i.e., the parameters of the propensity to consume) must have changed. Second, within each of these periods, the relationship between the left-hand side and the right-hand side of equation (6) is indeed linear. Therefore, a parsimonious model, with a constant mean and variance of consumption by wealth, can account for the trajectory of wealth since 1978, and, separately, for the trajectory between 1962 and 1977. If we focus, for example, on the post-1978 period, we can see the dynamics described in Figure 3 at play. We start in 1978, with a low but rapidly increasing inequality level. But as inequality goes up, the pace at which it increases slows down progressively.

Note that, while there is unmistakable evidence that the intercept of the linear relationship (which captures drift) has changed between periods, there is no clear sign that the slope (which captures mobility) is different.303030This is partly the result of a smaller sample size over 1962–1977. In light of this, and to get more robust estimates, I assume the same mobility parameter over both periods and only let the drift vary. I apply the same model within all wealth bins: for each of them, I fit two linear relationships with the same slope. I use [75] regressions to account the presence of error terms on both sides of equation (6). Appendix C.1 provides details of the procedure, alongside robustness checks. I extract the coefficients from these regressions and transform them so that they can be interpreted in terms of the mean and variance of consumption (see Step 2 in Section 3.3, as well as Appendix C.3 for additional adjustments to account for the inverse hyperbolic sine transform of wealth). This finally allows me to plot Figure 5(b), the profile of the mean and the variance of consumption by wealth. This figure also displays 95% confidence intervals, calculated using a bootstrap procedure, which accounts for the presence of error terms on both sides of equation (6), as well as autocorrelations across years and wealth bins, described in Appendix C.2.

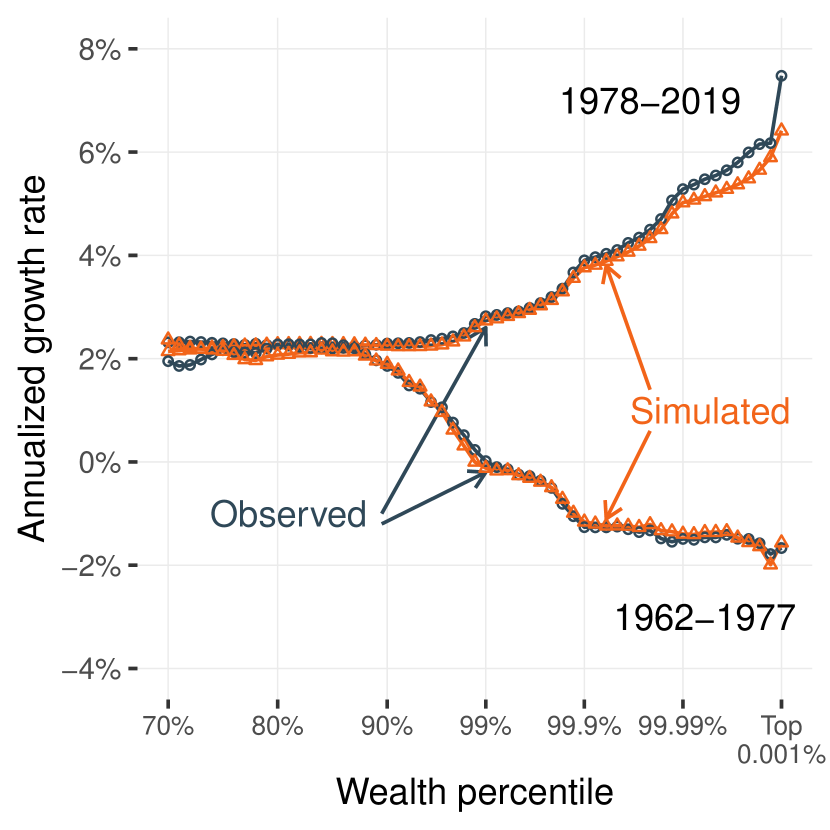

Several findings emerge from Figure 5(b). First, the variance of consumption is large, which implies a significant role for mobility in the wealth distribution. Second, on average, people consume a significant fraction of their wealth, even at the top, and even in periods of increasing wealth inequality. This matters, in particular, for our understanding of the wealth distribution in the steady state. Significant consumption levels at the top — in general exceeding income — create a tendency for large wealth holdings to reverse toward the mean. In the long run, the reversion towards the mean counterbalances mobility’s effect, making it possible for a steady-state distribution to emerge.313131The presence of demographic effects also contributes to the existence of a nondegenerate steady-state. If consumption at the top were too low, then wealth at the top would grow without bounds, and so would inequality. Note that at no point did I restrict the parameter values to force the existence of a steady state: a nondegenerate steady state arises naturally from the data in a model with constant drift and constant mobility. Finally, we see that changes in the average consumption between 1962–1978 and 1979–2019 are most significant at the top of the distribution (i.e., wealth above 50 times the average income), which aligns with the view that top wealth holders have been the primary drivers of rising wealth inequality.

Relation to the Rest of the Literature

How do these estimates relate to the rest of the literature, and what can we learn from them? We can simplify the situation by focusing solely on the top of the distribution and on the two key parameters (the drift and the mobility) while ignoring the other, less important phenomenons (mobility gradient, demography, etc.) Figure 6 summarizes the situation. The various models of the literature can be schematically represented on a two-dimensional plane, where the -axis corresponds to the amount of drift (), and the -axis corresponds to the amount of mobility (). In this representation, all models with a nondegenerate steady-state lie on the top left quadrant, pictured in Figure 6. The bottom half is not meaningful because it implies negative mobility; the top right quadrant implies an infinite steady-state inequality because there is no reversion towards the mean at the top.323232The drift term is normalized by the economy’s growth rate, so it is still possible to have a nondegenerate steady-state if people at the top experience positive wealth growth on average as long as that growth remains below the economy’s growth rate. Demography and the mobility gradient are other phenomenons that make it possible to sustain a steady state with positive drift at the top. In any case, it remains true that the emergence of a steady-state requires limited wealth growth at the top.

What wealth distribution is implied by the different points? At the steady-state, the derivative of the wealth distribution with respect to time is zero, and therefore equation (3) becomes:

| (7) |

This equation characterizes a set of straight diagonal lines for every distribution of wealth, passing through the origin of the plane. Each of them is an “isoinequality” line, defining the set of parameter values that lead to the same steady-state distribution of wealth. These isoinequality lines indicate that models can attain any long-run inequality level, either using a high-savings/low mobility regime (points close to the origin) or using a low-savings/high mobility regime (points far away from the origin).

The set of lines that roughly match the inequality levels typically seen in the United States is colored in orange in Figure 6. Combinations of parameters above this line correspond to higher inequality; combinations that lie below, to lower inequality. Importantly, models on the same isoinequality line still differ when it comes to dynamics. High-savings/low-mobility regimes feature slow transitions between steady-states, while the opposite holds for low-savings/high-mobility regimes.333333Figure 3 can demonstrate this. Increasing the slope of the line while keeping the same point of intersection with the -axis leads to the same steady-state but with higher derivatives of the distribution with respect to time (on the -axis), and therefore faster transitions.

We can now study where the different models in the literature stand and compare them to this paper’s estimate. Start the from [1] and similar [8] models (item 1, Figure 6). These models notoriously underestimate inequality for two reasons. First, people in these models accumulate wealth only for precautionary or consumption smoothing motives, so they have no reasons to accumulate the type of large wealth holdings we observe in practice. Second, because everyone earns the same rate of return, mobility at the top is only the result of labor income shocks. Since labor income is small compared to wealth at the top of the distribution, there is limited mobility as well. These facts put these models squarely in the bottom left corner of Figure 6. To fix this problem, a second set of models (item 2, Figure 6) introduced additional saving motives [12, 17] such as a taste for wealth, or for bequests. These models manage to match observed inequality levels by increasing savings at the top but do not fundamentally change the extent of wealth mobility. This puts them within the area of realistic steady-state inequality levels (orange diagonal) by moving them to the right of [1] models in the bottom right corner. A third set of models (item 3, Figure 6) also introduces idiosyncratic stochastic returns [53, 11, 7]. This increases mobility at the top because people with the same initial wealth may now move up or down the distribution depending on whether they get high or low returns. That being said, mobility remains quite limited because it is only the result of heterogeneous labor and capital income. Conditional on wealth, however, consumption remains essentially homogeneous because of consumption smoothing. This limited amount of mobility implies slow dynamics, as was identified by [26] for income inequality. This paper (item 4, Figure 6) finds that to match the dynamics of inequality that we observe, we need even higher mobility (and consequently lower savings).343434This is a parsimonious alternative to the solutions suggested by [26], which involve the introduction of additional short-run dynamics at the beginning of transition periods.

We can also the synthetic savings method [89, 46, 28] to this paper. In equation (3), define the synthetic saving as , and then apply the change of variable , where is a fractile and is the quantile function. We get:

which indeed corresponds to the traditional definition of synthetic savings. Note, however, that the definition of depends on the distribution of wealth, so a more accurate formula would be . Synthetic saving rates methods can either choose to ignore the dependency on , or explicitly eliminate it by setting .

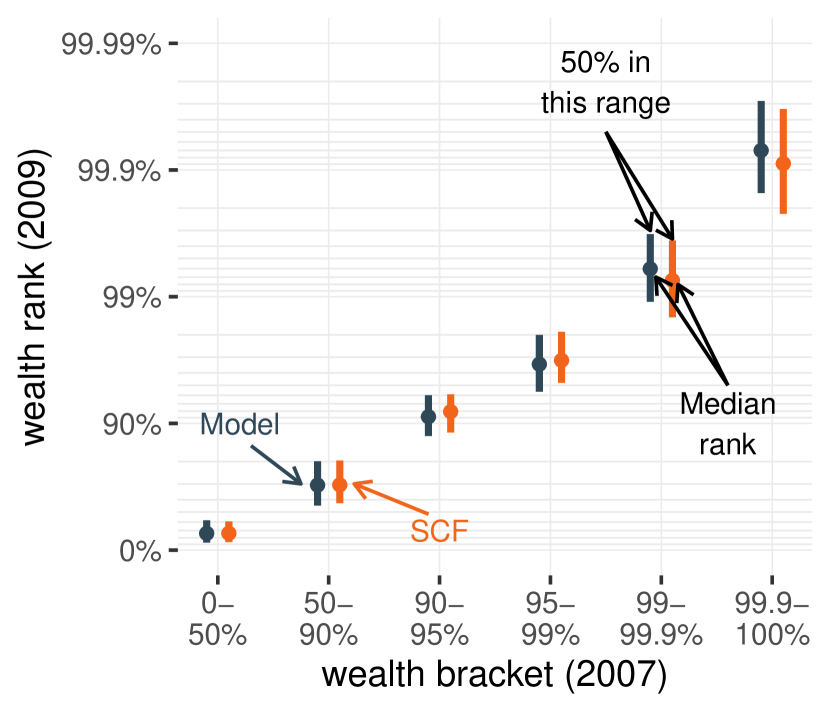

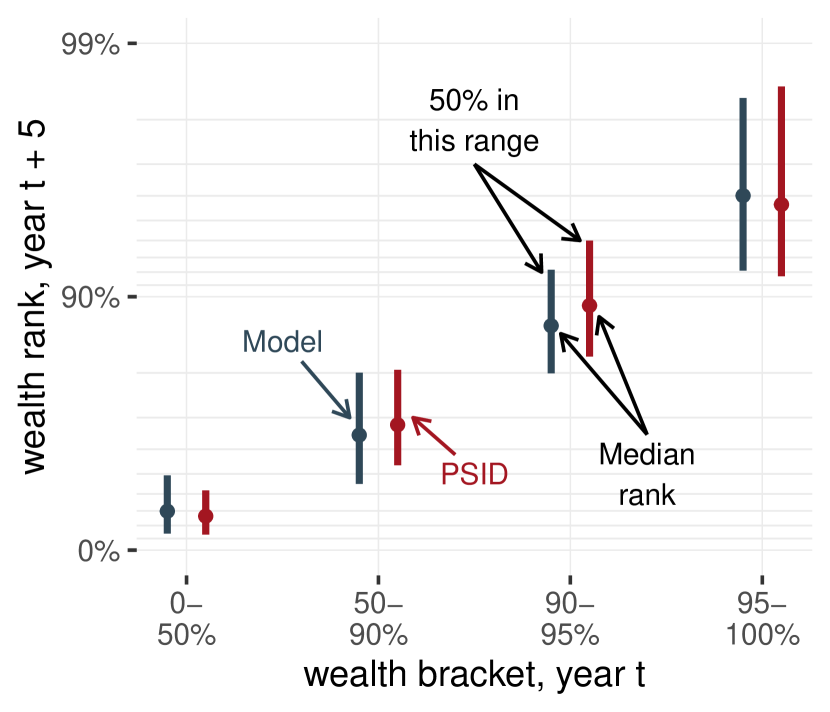

4.3 Validation

We can assess the validity and consistency of the model in two different ways. First, we can look at its internal consistency. (If we simulate the evolution of the wealth distribution using the estimated parameters, do we reproduce the observed data?) Second, we can look its external consistency. (Are the estimated parameters consistent with external observations?) In this section, I address both questions.

Replication of Observed Wealth Inequality Dynamics

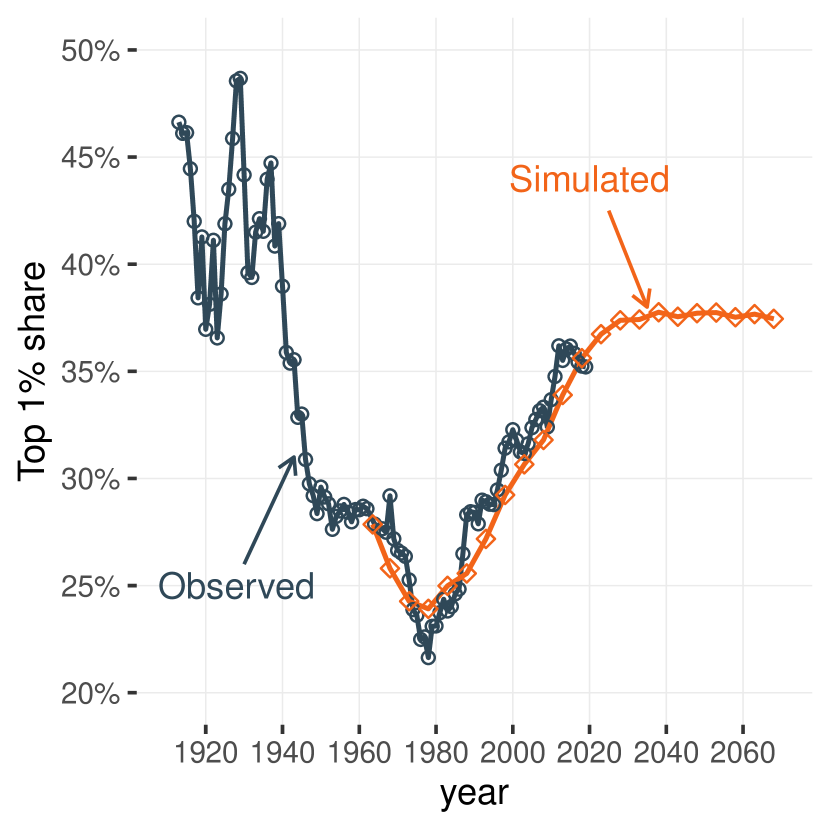

Starting from the distribution of wealth in 1962, and assuming that all the factors which affect the wealth distribution remain at their observed value, I can use the mean and variance of the propensity to consume estimated from the model to simulate the evolution of the wealth distribution. An elementary requirement for the general validity of the approach is that the evolution of the simulated wealth distribution matches the one observed in reality.

Note: The simulation of the model involves randomly simulated values: to filter out the resulting statistical noise, I simulate the model five times and take the median of the simulations. See main text for details. After 2019, the simulation use the demographic projection (medium variant) from the World Population Prospects [93] and otherwise assumes that economic parameters remain fixed at their latest observed values.