A Comprehensive Survey on Enterprise Financial Risk Analysis from Big Data Perspective

Abstract

Enterprise financial risk analysis aims at predicting the future financial risk of enterprises. Due to its wide and significant application, enterprise financial risk analysis has always been the core research topic in the fields of Finance and Management. Based on advanced computer science and artificial intelligence technologies, enterprise risk analysis research is experiencing rapid developments and making significant progress. Therefore, it is both necessary and challenging to comprehensively review the relevant studies. Although there are already some valuable and impressive surveys on enterprise risk analysis from the perspective of Finance and Management, these surveys introduce approaches in a relatively isolated way and lack recent advances in enterprise financial risk analysis. In contrast, this paper attempts to provide a systematic literature survey of enterprise risk analysis approaches from Big Data perspective, which reviews more than 250 representative articles in the past almost 50 years (from 1968 to 2023). To the best of our knowledge, this is the first and only survey work on enterprise financial risk from Big Data perspective. Specifically, this survey connects and systematizes the existing enterprise financial risk studies, i.e. to summarize and interpret the problems, methods, and spotlights in a comprehensive way. In particular, we first introduce the issues of enterprise financial risks in terms of their types, granularity, intelligence, and evaluation metrics, and summarize the corresponding representative works. Then, we compare the analysis methods used to learn enterprise financial risk, and finally summarize the spotlights of the most representative works. Our goal is to clarify current cutting-edge research and its possible future directions to model enterprise risk, aiming to fully understand the mechanisms of enterprise risk generation and contagion.

Index Terms:

Fintech, Enterprise Financial Risk, Small and Medium-sized Enterprises, Big Data.1 Introduction

Enterprise financial risk analysis has long been a focus of scholarly research in the fields of Finance and Management [1]. Whether young start-ups, small and medium-sized enterprises (SMEs) or famous Fortune 500 enterprises, to some extent they all inevitably face one or multiple financial risks, such as credit risk, guarantee risk, supply chain risk, bankruptcy risk, etc [2]. In particular, enterprises face big risk challenges when an economic crisis or a gray rhino incident happened, such as the financial crisis in 2008 [1] and COVID-19 epidemic in 2020 [3]. In the modern economic system, as the global financial system becomes more deeply interconnected, enterprises face both the intra-risk and contagion risk [4, 5]. Therefore, predicting the financial risk of enterprises is of great importance for both government policymakers and financial institutions.

Studies on enterprise financial risk analysis, which originated in the fields of Finance and Management, have gradually attracted increasing numbers of researchers from Computer Science (CS). The earliest research mainly focused on the three most commonly used statistical econometric methods, e.g. multivariate discriminant analysis, linear probability model, and logistic regression, and studied their application in enterprise risk prediction [6].

With technological advancements in natural language processing (NLP) and artificial intelligence (AI), researchers have begun to evaluate enterprise financial risk from a Big Data perspective. Besides traditional enterprise financial index, more enterprise risk intelligence is taken into consideration, such as non-financial textual information and relational data [7]. Specifically, to deal with textual risk information, NLP techniques, including sentiment analysis and event extraction are used to dig enterprise risk signals from non-financial textual data. To model the risk momentum spillover on enterprise relational data, AI techniques, including deep learning and Graph Neural Networks (GNN), are utilized to evaluate the enterprise contagion risk. This series of studies has opened up new avenues for analyzing the generation and contagion mechanisms of enterprise financial risk from a Big Data perspective.

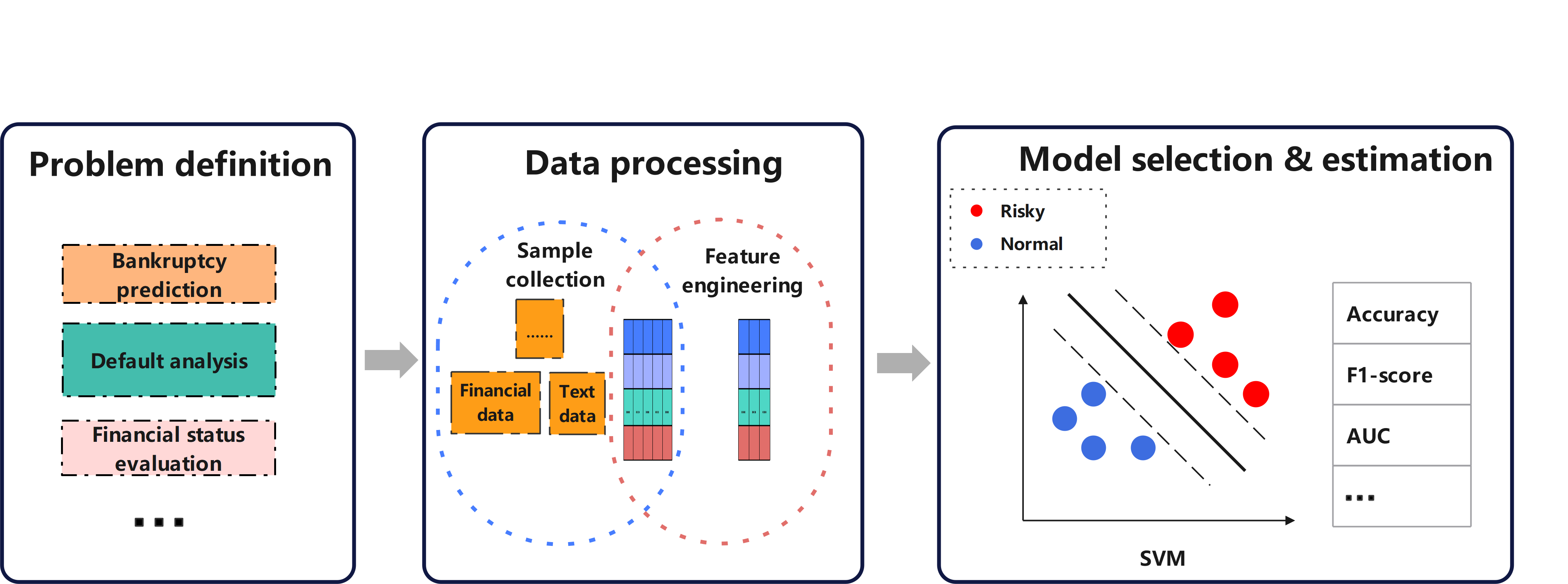

Figure 2 and Figure 2 show the number of relevant publications in the past thirteen years and their distribution in terms of different research directions. Due to the rapid expansion of the enterprise risk research based on the CS and AI technologies, it is both necessary and challenging to comprehensively review the relevant studies. In this work, we systematically review nearly 260 representative articles111In this work, we have collected nearly 2,000 publications about enterprise financial risk and have selected 256 of the best and most recent publications on enterprise risk.. We endeavor to summarize the problems, methodologies and spotlights of enterprise financial risk analysis in a comprehensive way, which may help readers to have a better understanding of the current research status and ideas. Figure 3 shows the framework of this survey.

The contributions of this work are threefold:

-

•

This survey provides a systematic and comprehensive review of existing research for enterprise financial risk. To the best of our knowledge, this is the first and only survey work on enterprise financial risk from the Big Data perspective.

-

•

We propose a novel holistic taxonomy of existing enterprise financial risk analysis. For each specific part, the contemporary landscape is summarized and insightful analysis is provided.

-

•

We discuss the limitations of current research and propose five potential research directions for enterprise financial risk analysis.

The remainder of this article is organized as follows. Section 2 formalizes the problems of enterprise risk analysis from four different directions, including the risk types, analysis granularity, risk intelligence and evaluation metrics. In Section 3, we will systematically introduce the approaches used more frequently. Section 4 summarizes the spotlights of the most representative studies. Section 5 provides guidance for future research directions. Finally, we conclude the survey in Section 6.

2 Problem Formalization

2.1 Financial Risk Types

In this section, we review the previous research on enterprise risk analysis in terms of risk types, i.e., credit risk, bankruptcy risk, guarantee risk, and financial risk, which are summarized in Table I.

| Enterprise Risk Types | Literature | Focus | Experiment | Method | ||||

| Industry | Country | Period | Size | Metric | Category | Methodology | ||

| Credit Risk | [8] | All industries | China | 1999-2004 | 120 | AC | ML | IBDR |

| [9] | Manufacturing | China | 2015-2017 | 1,091 | AUC,KS | SEM | MLR | |

| [10] | Manufacturing | China | 2011-2019 | 924 | AC,Type I, II error | DL | M-GL | |

| [11] | All industries | Italy | 2014 | 2.4M | GC,SCC | Hybrid Model | MLR, CT, NN | |

| [12] | All industries | China | 2012-2013 | 48 | AC, Type I, II error | ML | RSRAB | |

| [13] | Automotive | China | 2019 | 192 | AC | Hybrid Model | GA, SVM and NN | |

| Bankruptcy Risk | [14] | All industries | China | 2016-2018 | 3.5M | AUC | ML | TSMOFS |

| [15] | All industries | Belgian,UK | 2011-2014 | 2.4M | AUC | ML | SVM | |

| [16] | All industries | Japan | 2002-2016 | 2,062 | AC | DL | CNN | |

| [17] | All industries | Korea | 1995-1998 | 168 | AC, Type I, II error | ML | BPN, KN | |

| [18] | All industries | US | 1994-2014 | 11,827 | AUC | DL | Word Embedding, CNN, LR, RF, SVM | |

| [19] | Industry | US | 1981-1995 | 5,999 | P-value | SEM | Z-score, O-score | |

| Guarantee Risk | [20] | Banking | German | 1996-2006 | 452 | P-value | SEM | Z-score |

| [21] | All industries | China | 1997-2005 | 9,060 | CC | SEM | Regression | |

| [22] | All industries | China | 1999 | 875 | P-value | SEM | Descriptive statistics | |

| [23] | Banking | Japan | 1996-2002 | 100 | P-value | SEM | Regression | |

| [24] | All industries | Asia | 2013-2016 | 0.11M | AUC | DL | DGANN | |

| [25] | All industries | Asia | 2013-2016 | 0.11M | Macro-F1 score | DL | DNN | |

| Financial Risk | [26] | All industries | Slovak | 2015 | 62,533 | P-value | ML | MRA |

| [27] | All industries | Worldwide | 1992-2009 | 9,000 | CC | SEM | PDA | |

| [28] | All industries | Worldwide | 2008-2013 | 539 | P-value | ML | Panel regression | |

| [29] | High-tech industries | Worldwide | 2016-2020 | 600 | AC | ML | PSO-BP | |

| [30] | E-commerce | China | - | 3,617 | AC | DL | DL, DFT | |

| [31] | All industries | Worldwide | 1996-2013 | 17,057 | P-value | SEM | OLS and FFE regressions | |

-

•

ML: The machine learning methods. SEM: Statistical econometric measurement. DL: The deep learning methods. AC: Average accuracy. IBDR: Integrated binary discriminant rule. AUC: Area under curve. NN: neural networks. CNN: Convolutional neural networks. BPN: The BP network. KN: The Kohonen network. RF: Random forest. CC: Correlation coefficient. DGANN: The dynamic graph attention neural network. DNN: The deep neural network. MLR: Multiple Linear regression. PDA: Panel data regression. DFT: Data fusion technology. OPM: Option pricing model. LR: Logistic regression (this only refers to machine learning). MNL: Multinomial Logit. CT: Classification tree. RSRAB: Random Subspace-Real AdaBoost. GA: The genetic algorithm. M-GL: The multiview graph-based learning. TSMOFS: Two-stage multiobjective feature-selection. OLS: Ordinary least squares. FFE: Firm fixed effects.

2.1.1 Credit Risk

The enterprise credit risk refers to the possibility of loss due to the default of one party or the change of credit quality or morality in the transaction. The attributes of enterprise credit risk are characterized by comprehensiveness, bidirectionality, transitivity, diffusivity, cumulativeness, hiddenness, suddenness, and uncertainty. Credit risks mainly exist in various credit transactions among financial institutions and enterprises, enterprises and enterprises, governments and enterprises [32, 33].

Credit risk arises from a number of reasons, either as a result of defaulted payments by customers or as a result of internal mismanagement of the business. In addition, credit risk can also arise from external macro causes and from the financing firm’s own problems. Duffie et al. [34] find that the level and shape of the maturity structure of a firm’s default probability depends on the firm’s default distance. Belas et al. [35] explore the impact of the determinants of SME credit risk, paying particular attention to the role of social and economic factors. Tang et al. [36] focus on the impact of the interaction between market conditions and default risk on firms’ credit spreads.

2.1.2 Bankruptcy Risk

Corporate bankruptcy risk refers to the possibility that a company may not be able to repay its debts or maintain the necessary funds to sustain its operations, potentially leading to bankruptcy. This can have negative implications on the company’s operations, financial stability, and stakeholders. Factors that may contribute to corporate bankruptcy include financial structure [37], governance structure [38], directors’ characteristics [39], corporate social responsibility [40], macroeconomic environment [41], global shock events [42], etc. Companies facing bankruptcy risk may need to take steps such as reducing expenses, increasing revenue, and developing financial plans to mitigate their risk.

2.1.3 Guarantee Risk

Guarantee risk refers to the risk caused by the inability of the lender to recover the principal and interest of the loan through the collateral or guarantor when the borrower fails to repay the loan on time or defaults.

At the enterprise level, Cowan et al. [43] find that partial credit guarantees severely affect the default rate of insured loans, which suggests that guarantees affect firms’ incentives to repay loans. Jian et al. [21] analyze the determinants of Chinese firms’ participation in the guarantee ring from the perspectives of macroeconomics and microeconomics. At the financial institution level, GROPP et al. [20] empirically analyze the impact of public guarantees on banks’ risk-taking through natural experiments. Additionally, in the study on the feasibility of bond securitization, Wu et al.[44] propose an expression of rate of return of securities based on guarantee letters and introduce two key indicators to build a return model for bond securities.

2.1.4 Financial Risk

Financial risk refers to the possibility of losses that an enterprise may suffer due to unpredictable or uncontrollable factors that cause actual income and expected income to deviate in various financial activities. Financial risks can be divided into liquidity risk, financing risk, investment risk, etc., based on the source of risk. Moreover, the existence of financial risks may cause fluctuations in the value of enterprise assets, reduced income, or deterioration of financial conditions.

The financial risks of enterprises are affected by many factors, which can be analyzed from two aspects: internal and external factors. Internal factors include management decisions [45], internal control, financial management level, corporate culture and other factors [46, 47]. External factors include economic environment [48], market competition, laws and regulations, industry risks, financial market fluctuations, etc. Enterprises can prevent financial risks via establishing a financial risk warning system and analyzing internal and external environments [49, 50, 51].

2.2 Risk Analysis Granularity

In this section, we review the previous research on risk analysis in terms of different granularity, i.e., individual enterprise risk, enterprise chain risk, and system risk, which are summarized in Table II.

| Risk Analysis Aspect | Literature | Focus | Experiment | Methodology | ||||

| Industry | Country | Period | Size | Metric | Category | Methodology | ||

| Individual Enterprise | [34] | Industry | US | 1971-2001 | 28,000 | AUC | SEM | Maximum likelihood estimation |

| [52] | Industry | US | 1995-2003 | 4,000 | AIC, BIC | SEM | The Percentage Zeros, LOT | |

| [53] | Manufacturing | China | 1990-1999 | 88 | AC, Type I, II error | ML | GA-SVM | |

| [54] | Banking | Australian, German China | 2000-2010 | 2,818 | AC, Type I error | SEM | LDA, t-test, LR | |

| [55] | Manufacturing | India | 2011-2012 | 205 | CFA | SEM | Structural equation | |

| Enterprise Chain | [56] | Banking | Greek | 2004-2007 | 1,000 | AC, AUC | ML | ELECTRE |

| [57] | All industries | French | 1997-2015 | 10,000 | AC, F-measure | ML | Self-organizing neural network | |

| [58] | All industries | Poland | 2008-2016 | 10,000 | AC, AUC,Recall | ML | XGBoost, NN | |

| [59] | Financial | Australia | 1994 | 690 | AC, Recall, F-measure, AUC | ML | NN | |

| Systemic | [60] | Tourism | US | 2018-2020 | 95 | TRSI, SII | SEM | TALIS |

| [61] | Commerce | China | 2007-2016 | 86 | Z-score | SEM | Difference estimation method | |

| [62] | Financial markets | US | 1998-2010 | 116 | P-value | SEM | PCA | |

| [63] | Banking | US | 1976-2001 | 0.4M | P-value | SEM | Simple panel data models | |

| [64] | Financial | US, UK, Canadian | 1996-2005 | 2,171 | P-value | SEM | MRA | |

| [65] | All industries | European, US | 1999-2018 | 1,770 | CARs, CAARs, ARV | SEM | CAPM | |

2.2.1 Individual Enterprise Risk

Individual enterprises face many risks when operating and are also affected by various pressures during management activities. In the process of trade, multiple enterprises usually cooperate to achieve the best benefits. In this section, we will analyze individual enterprise risk based on industry type and find that current research mainly focuses on industry and manufacturing.

For industry, barrier selection frameworks exhibit better calibration and discrimination capabilities than other market-based models such as Merton (1974) or Black and Cox (1976) [66]. Other studies have focused on the comparative analysis of traditional statistical methods for distress classification and prediction, namely LDA and NN. In the manufacturing and construction industries, new methods are proposed to improve the predictability of corporate bankruptcy and insolvency risks, such as Self-Organized Maps (SOM) [67] and Z-score models [68]. In the retail industry, a multi-industry survey of the bankruptcy of some Korean companies can be used to construct an industry-specific insolvency prediction model [69]. As for the financial industry, previous research focus on the banks [70], and analyzing the risk propagation process between banks is crucial [71, 72].

2.2.2 Enterprise Chain Risk

Enterprise chain is a macro concept that essentially refers to a group of companies with some intrinsic connections, including structural and value dimensions. Enterprise chains can be further divided into supply chains, guarantee chains, transaction chains, and credit chains. This section introduces risk analysis for different enterprise chains.

In research on supply chains. Heckmann et al. [73] identify core characteristics used to define, quantify, and model supply chain risks through a literature review. However, Babich et al. [74] discover that competition among suppliers in a supply chain affects the equilibrium wholesale price. Blome et al. [75] present propositions on how firms manage supply risk during a financial crisis. In the context of guarantee chains, Cheng et al.[76] investigate the prediction of successive default events for network-guaranteed loans. Similarly, regarding transaction chains, using transaction data and payment network-based variables rather than the financial accounting data, Kou et al. [14] propose a model for predicting SME bankruptcy. Moreover, as for credit chains, Battiston et al.[77] propose a simple production network model by applying the supplier-customer relationships involving trade credit extensions.

2.2.3 Systemic Risk

Systemic risk refers to the risk inherent to the entire market or market segment, caused by factors beyond the control of a specific company or individual. We present an overview of systemic risk based on its sources.

As exemplified by recent studies [78, 79, 80, 81], systemic events, including epidemics, as well as terror attacks [82], possess the potential to exert a substantial influence on the global economy. As an illustration, during the COVID-19 pandemic, healthcare and technology sectors have experienced increased activity and revenue, while tourism-linked industries have suffered due to global movement restrictions[60]. Furthermore, the formulation and implementation of national policies hold a pivotal position in shaping the trajectory of a country’s economy[61, 83]. For instance, intrastate bank deregulation boosts the local market power of banks, but decreases innovation and risk for young private firms [84, 63]. Additionally, a disruption to the financial network has the capacity to spark a domino effect that may lead to widespread systemic failures. [85, 86, 87]. In order to fully understand this problem, Petrone et al.[88] and Tafakor et al.[89] are dedicated to developing financial network models that can expose contagion mechanisms and identify potential patterns of systemic threats among nodes.

2.3 Enterprise Risk Intelligence

Table III presents previous studies on risk analysis in terms of enterprise risk intelligence, i.e., financial index, non-financial textual information, relational data, and intelligence integration. And Figure 4 shows the publication treads of enterprise risk intelligence over the years.

| Enterprise Risk Intelligence | Literature | Experiment | Methodology | |||

| Period | Size | Metric | Category | Methodology | ||

| Financial Index | [90] | 1995-2001 | 592 | AC | ML | LR |

| [91] | 2004-2015 | 0.83 M | AC | DL | GNN | |

| [92] | 1998-2018 | 651 | AC, AUC, ROC | Hybrid Model | NIM, CNN-DL, SVM | |

| [93] | - | 1,000 | Recall, AC | DL | ANN | |

| [94] | 2007 | 250 | AUC | DL | Graph Pattern Mining | |

| Non-financial Textual Information | [95] | 2014-2018 | 83 | AUC, Recall, F1-score | DL | DeepRisk approach |

| [96] | 1980-2009 | 16,966 | P-value | SEM | Discrete hazard model | |

| [97] | - | 1.5 M | KS, AUC | DL | AMG-DP model | |

| [98] | 2015-2018 | 6,494 | MAE | DL | MR-QA | |

| Relational Data | [99] | 2019-2020 | 4,040 | AUC | DL | TH-GNN |

| [100] | 2011-2018 | 0.43 M | - | SEM | Three-factor model | |

| [101] | 2014 | 47 M | AC, Recall | DL | NN | |

| [4] | 2000-2021 | 0.11 M | AC, Recall, F1-score | DL | GNN | |

| [102] | - | 1 M | AUC | DL | ST-GNN | |

| Intelligence Integration | [103] | 1989-1997 | 300 | P-value | SEM | The logical model |

| [104] | 2001-2018 | 0.64 M | AC | ML | BPN | |

| [105] | 2011-2019 | 924 | AC | DL | M-GL | |

| [78] | 2020 | 1,584 | P-value | SEM | DCC-GARCH model | |

2.3.1 Financial Index

Financial indicators refer to relative indicators for enterprises to summarize and evaluate their financial status and operating results, including indicators of solvency, operating capacity, and profitability. In this section, we comprehensively review the impact of financial indicators on corporate risk.

Solvency refers to the company’s ability to pay current liabilities with current assets, mainly depending on whether the company’s capital structure and long-term profitability are sound. Among them, the asset-liability ratio [103, 106], quick ratio [92], working capital, etc., are all excellent corporate indicators that are employed to study the determinants of bankruptcy and analyze risk characteristics. Credit default swap (CDS) data and bond data are also commonly used to study their relationship with corporate risk [107, 108, 109]. The relevant indicators of enterprise operating ability include inventory turnover rate, accounts receivable turnover rate, current asset turnover rate, and total asset turnover rate, etc. The risks resulting from insufficient liquidity of funds are often worthy of attention [110]. Among them, Takahashi et al. [111] find that the capital flow of some bankrupt companies decreased significantly with the research on the typical financial characteristics of bankrupt companies in Japan. Profitability refers to the ability of an enterprise to earn profits, including gross sales rate, net sales rate, net asset rate, and return on equity. These indicators are often used to calculate the company’s profit margin and the stability of supply and demand, thereby helping banks predict enterprise credit and alleviate financial difficulties and liquidity shortages in the interbank market [112, 113].

2.3.2 Non-financial Information

Non-financial variables: Non-financial variables gauge the success of a business in domains such as operations, customers, and employees. Undoubtedly, non-financial variables related to customers include customer churn rate and personal rating, etc [114, 115]. Zhang et al.[115] explore the impact of interest rates and customer churn rates on bank profitability and customer retention. When it comes to employee-related non-financial variables, board structure has emerged as a commonly studied factor [116, 117]. Existing approaches [118, 119, 120] have explored the impact of data characteristics such as director turnover rate, board size, and CEO duality on corporate credit risk. Correspondingly, non-financial variables related to company operation typically include business cycle and macroeconomic variables [121, 57, 122]. Kang et al. [123] and Giesecke et al. [124] analyze the influence of price-related indices (energy price risk, resource risk, inflation risk) and national development-related indices (GDP) on corporate default risk.

Textual Information: Companies can leverage the power of news reports and sentiment analysis to assess risk by analyzing textual information found in news reports and qualitative risk disclosures in corporate filings. Tsai et al.[125] and Nyman et al.[126] utilize news sentiment analysis on a large volume of news reports to predict credit risk and volatility indicators for companies. Furthermore, legal documents can provide valuable information to assess risk too. Yin et al.[9] and Altman et al.[127] combine information related to legal actions taken by creditors to recover outstanding debts, company filing history, consolidated audit report/opinion data, firm-specific characteristics and legal judgments to build models to predict the enterprises default risk. In addition, conference calls [128, 129] and interview text [130, 131] also can be used to analyse corporate risk.

2.3.3 Relational Data

Relational data defines relationships between entities and is widely used in the study of the relationship between individual enterprises or enterprises, such as equity relationship, cooperation relationship, supply chain relationship, management relationship, etc [15]. It can be used to study the network of relationships between SMEs and the cooperative relationships of firms [101]. And a well-constructed corporate relationship network can be processed with the utilization of HGNN, which captures information at different levels. Furthermore, this approach effectively combines the financial and relationship data of a company, allowing for a more accurate assessment of corporate financial risk and the study of corporate relationship networks [99]. For example, Tobback et al. [15] use relationship data to construct a network of corporate relationships and make enterprise risk predictions. Relational data is also applied to the study of supply chain relationships. By collecting supply chain relationship data between enterprises (including direct suppliers, sub-tier suppliers and interactions between suppliers), a supply chain network containing multiple tiers of suppliers can be constructed. For instance, Wang et al. [100] use social network analysis methods to analyze the structural characteristics of the supply chain network, identify key enterprises and potential risk points. Relational data can also be used to mine supply linkages between SMEs and construct relevant topologies. Yang el al. [102] effectively analyze financial risk by constructing a supply chain graph.

2.3.4 Intelligence Integration

In the assessment of corporate risk, different kinds of information are captured. Generally, financial data is integrated with non-financial data to obtain comprehensive information. Non-financial information, like firm size, corporate governance indexes [132], and audit opinions [133], has already been demonstrated to be practical in risk prediction. Due to varied research goals, the specific types of non-financial information utilized in risk assessment may vary. Furthermore, there is a growing trend in risk management towards uniting relational data with financial data. Cleofas [134] combines accounting statements with business information, bank customer data, and credit applicant records to predict bankruptcy. Such data depicts the relationship between a company and linked enterprises [135], or the relationship between a company and banks [136]. Integration also happens among the three types of data mentioned above. For instance, Zhao et al. [137] utilize transaction data, web news as well as company relations and executives’ information to predict the stock movement.

2.4 Enterprise Risk Evaluation

2.4.1 Datasets

| Datasets | Tasks | Descriptions | Period | Size | ||||||

| SMEsD [4] | Bankruptcy Risk Prediction |

|

2014-2020 | 4,229 | ||||||

|

|

|

1996-2012 | 761 | ||||||

| Listed SMEs data[139] |

|

|

2014-2015 | 53 | ||||||

| Interview data[75] | Supply Chain Risk Management |

|

2009-2010 | - | ||||||

|

|

|

2010-2017 | 1,902 | ||||||

| Bank loan portfolio[141] |

|

|

1994-1997 | 1,411 | ||||||

| Bankruptcy financial data[142] |

|

|

1995-1999 | - |

We present the various datasets used for enterprise risk analysis in Table IV. These datasets cover different types and domains of information, providing scholars with rich materials to analyze and evaluate enterprises financial risks. The most widely used datasets in previous research mainly include SME datasets, financial datasets, stock datasets, rating datasets, credit guarantee datasets, etc. Previously, most traditional statistical econometric models substantially rely on financial data and text data to assess enterprise risk. However, with the advancement of machine learning and deep learning approaches, a wider range of datasets is now utilized. For instance, bank loan and credit guarantee data provide insights into financing and credit risks.

2.4.2 Evaluation Metrics

Evaluation metrics are crucial in the modeling process. Appropriate indices should be chosen for different tasks and models. In this section, four evaluation indicators are discussed in detail and Table V presents the main formulae for calculating these indicators.

Kolmogorov-Smirnov statistic (KS): The K-S test examines the distribution of continuous random variables and evaluates model’s discrimination performance. Using KS, Chang et al. [9] conduct 10 independent 10-fold cross-validations, predicting model recognition performance and obtaining 100 performance estimates.

AUC: The AUC curve, under the ROC curve and enclosed by axes, measures separability and learner quality. It is an important measure for financial risk prediction [143], where a larger AUC indicates a better classifier. AUC compares prediction effectiveness for hard, soft, and integrated features with various approaches. For default risk prediction, which is an unbalanced classification problem, AUC reflects the classifier’s learning effect more fully [144, 145].

F-measure: The F-Measure, which is a weighted harmonic average of precision and recall, is a good choice for evaluating unbalanced classification models [145]. Higher F-measures indicate better handling of unbalanced data [133]. Zhu et al. [146] assess IEML methods (i.e., multi-boosting and RS–boosting) on 377 datasets using F-measure as the evaluation metric.

Kappa measure: Using confusion matrices, the Kappa coefficient measures classification accuracy, considers chance agreement, and offers a better performance reflection than accuracy or precision and recall. It is a decent option for assessing unbalanced data classification, with higher coefficients indicating better prediction [133].

| Metric | Formula | Parameter and Explanation | Reference | ||||

| KS | : True positive rate; : True negative rate. | [9, 97] | |||||

| AUC |

|

[9, 143, 144] | |||||

| F-measure |

|

[145, 146, 133] | |||||

| Accuracy | TN: True Negative; FP: False Positive. | [146, 147, 148] | |||||

| Recall Rate | TP: True Positive; FN: False Negative. | [144, 149] | |||||

| Kappa measure | : The proportion of correct predictions made by the model; : The proportion of correct predictions made by the random classifier. | [133] |

3 Methodologies

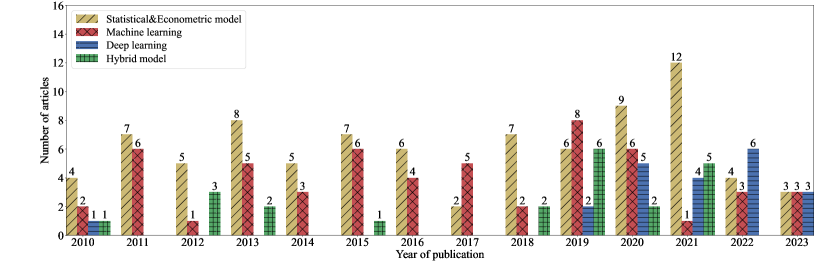

Table VI presents the previous studies on risk analysis in terms of analysis models, i.e., statistical model, machine learning model, deep learning model and hybrid model. Figure 5 exhibits a chronological overview of influential enterprise risk analysis method. And Figure 9 shows the publication trends of analysis models over the years.

| Category | Literature | Focus | Experiment | Methodology | ||||

| Intelligence | Country | Industry | Period | Size | Metric | |||

| Statistical Econometric Methods | [20] | Financial statements | Germany | Banking | 1995-2006 | 1,329 | P-value | Z-Score |

| [172] | Stock market data financial statements | China | - | 2004-2006 | 80 | Expected default | KMV | |

| [173] | CDS Spreads | US | - | 2006-2012 | 100 | Risk probability | Copula | |

| [78] | Financial data | Worldwide | Banking | During the COVID-19 | 1,584 | P-value | CoVaR | |

| [103] | Balance sheet questionnaire | Italian | - | 1989-1997 | - | P-value | Logit model | |

| [174] | Financial data stock market data | China | - | From 2007 | - | P-value | Logit Regression | |

| Machine Learning Methods | [15] | Financial ratios Executive information | Belgian, UK | - | 2011-2014 | 400,000 | AUC | SVM |

| [175] | Financial statements | - | - | 1975-1982 | 129 | Accuracy | NN | |

| [62] | Stock market data | US | All industries | 1998-2010 | - | Absorption Ratio | PCA | |

| [176] | Financial statements | - | All industries | - | 66,000 | Accuracy | RF | |

| [177] | Financial ratios | Turkish | - | 2005-2011 | 2,722 | Accuracy, F-Measure | DT | |

| [178] | Financial ratios | Polish | - | - | 240 | Accuracy, AUC | PTVPSO-FKNN | |

| Deep Learning Methods | [16] | Financial statements | Japan | - | 2002-2016 | 2,164 | AUC | CNN |

| [91] | Loan data | China | - | - | - | AUC | GNN | |

| [150] | Financial ratios | Polish | - | 2002-2013 | - | AUC | BSM-SAES | |

| [179] | Financing behavior data static enterprise demographic data | China | - | 2014-2018 | 83 | F1, AUC | DNN | |

| [102] | Corporate relations, lending data | China | - | - | 280M | AUC, KS | ST-GNN | |

| Hybrid approach | [180] | Financial data, default distance | China | - | 2003-2008 | 2,470 | Significance | KMV, RF, RST |

| [181] | Financial data, stock data | China | IT | 1999-2006 | 321 | Accuracy | CART–CBR, RST–GRA–CBR, RST–CBR | |

| [171] | Interview information | - | - | - | 1 | Expected utility | BBN, EUT | |

3.1 Statistical Econometric Methods

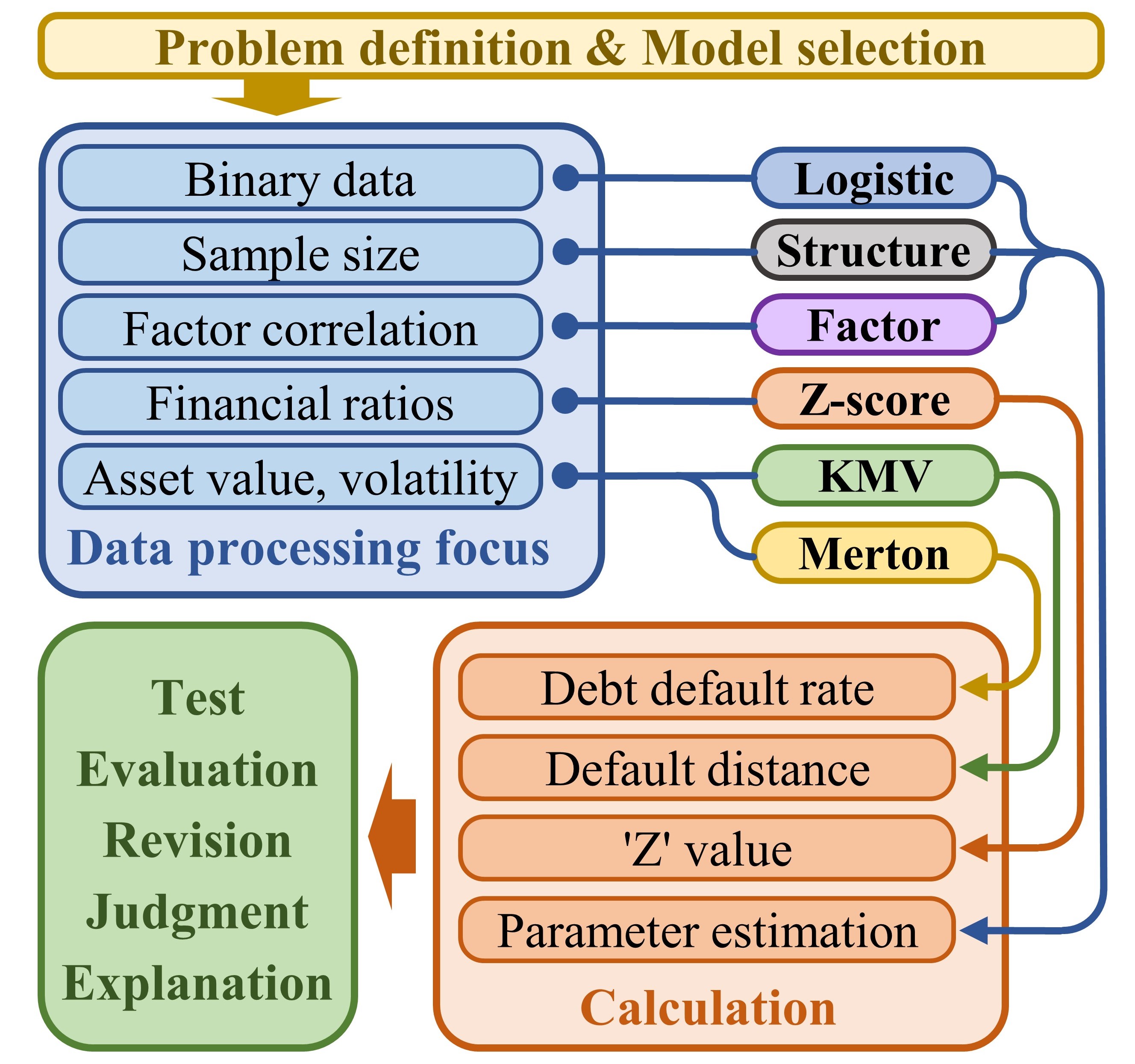

The study of enterprise risk originated from traditional economic disciplines. In this section, we will briefly introduce the following main statistical models: Regression Model, Z-score Model, Merton Model, KMV Model, Complex Network, Structural Equation Model, and Factor Model. Figure 6 illustrates the pipeline of several general traditional models. Table VII presents the core formulas of the main statistical models discussed in this section.

| Model | Main Formular | Parameter and Explanation |

| Logistic Regression | : Probability of ; : The intercept term of the regression function; : Row vectors of regression coefficients; : Column vectors of explanatory variables. | |

| Z-score Model | : Working capital/Total assets ratio; : Retained earnings/Total assets ratio; : Earnings before interest and tax/Total assets ratio; : Market value of equity/Total liabilities ratio; : Total sales/Total assets ratio. | |

| Merton Model | : Cumulative probability distribution function of the standard normal distribution; : European call Option price; : Stock price at time 0; : Executive price; : Continuously compounded risk-free rate; : Duration of options; : Stock price volatility. | |

| KMV Model | : Distance to Default; : The risk–free rate of the return of the asset of the company; : The current value of the asset of the company; : The face value of the debt; : The annualized company value volatility; : Long-term debt; : Short-term debt. | |

| Structural Equation Model | : Number of endogenous variables; : Number of exogenous variables; : vector of observed endogenous variables; : matrix of regression slopes; : vector of observed exogenous variables; : vector of regression intercepts; : matrix of regression slopes; : vector of disturbances; : covariance matrix of disturbances. | |

| Factor Model | : Asset or portfolio return ; : Risk-free rate; : Market revenue; : Factor exposure; : Simulated portfolio returns for size factor at time (small minus big); : Simulated portfolio return of book-to-market factor at time (high minus low). |

3.1.1 Regression Model

The regression model plays a crucial role in economic research, as it helps verify the relationship between explanatory variables and the response variable. Many classic risk-related studies utilize regression model[38, 9, 106, 182]. More specifically, Beasley et al.[155] adopt an ordinal logistic regression model to demonstrate that the implementation of enterprise risk management requires leadership. Eckles et al.[183] use probit regression to calculate the likelihood of enterprises adopting ERM. Habermann et al.[182] employ panel regression to investigate the relationship between CSR and bankruptcy.

3.1.2 Z-score Model

The Z-score model employs a set of financial ratios to evaluate a company’s financial distress. It takes the following factors into account, such as asset size, liquidity, profitability, financial structure, debt servicing capacity, and asset utilization for making predictions. Therefore, it is widely applied in bankruptcy forecasting [184, 19]. A company with a Z-score lower than 1.8 is considered to have a high risk of bankruptcy [2]. In particular, Xu et al.[185] utilize the model to predict the bankruptcy risk of Japanese listed companies, and Gropp et al.[186] use it to measure the bank’s risk under public guarantees.

3.1.3 Merton Model

The Merton model, proposed by Merton in 1974 [187], is a renowned credit risk measurement model that primarily assesses corporate default risk from the perspective of option pricing[188, 189]. Vassalou et al.[154] adopt the Merton model to gauge the default risk of individual companies and analyze the effect of default risk on stock returns. However, its application is not limited to assessing default risk alone. Xu et al.[185] also use the Merton model to detect signs of corporate bankruptcy from option price information, while Hilscher et al.[190] conduct a study on the relationship between the Merton model’s failure beta, CDS spreads, and credit ratings.

3.1.4 KMV Model

The KMV model, deriving from Merton’s option pricing theory, estimates default probabilities. It primarily utilizes stock market data to evaluate a company’s ability to repay loans and determine its actual default probability. Despite having strict assumptions, the model proves effective in certain aspects. For instance, Reisz et al.[66] apply the KMV model to estimate the bankruptcy probability of companies. Chen et al. [156] enhance the predictive validity of the KMV model for credit defaults of listed SMEs in China by adjusting its parameters. For studying the relationship between technological competition and enterprise bankruptcy, Eisdorfer et al.[191] use three bankruptcy risk measurement models, including the KMV model, as control variables.

3.1.5 Complex Network

A complex network comprises a large number of nodes and intricate relationships between them. Many researchers utilize this structure to analyze financial and systemic risk[192, 193, 85]. To be specific, Zhu et al.[192] apply the complex network method to study the contagion of international financial risks. Wu et al.[193] propose a SICM model based on complex networks to examine the contagion mechanism of financial risk. Chen et al.[3] adopt scale-free networks as the foundation for analyzing corporate credit risk on supply chain networks.

3.1.6 Structural Equation Model

The structural equation model (SE) is a statistical method for evaluating relationships between variables. SE is often employed to analyze questionnaires and variables that are difficult to measure accurately, and it has found widespread use in supply chain studies[55, 194, 195, 196]. Specifically, Imbierowicz et al.[197] utilize SE to analyze the correlation between liquidity and credit risk. Jajja et al.[196] apply SE to investigate the relationship between supply chain risk of manufacturing firms and firm agility performance. Munir et al.[195] employ SEM to examine the connection between supply chain integration and supply chain risk management.

3.1.7 Factor Model

Factor models resemble regression models in that they both study the influencing factors of dependent variables. However, the factors in factor models are not directly observable. Commonly used models include the single-factor model[198, 199], three-factor model[200], and multi-factor model[108, 201]. For instance, Wang et al.[200] employ a three-factor model to study the risk of quarterly heterogeneity in supply chains. Brusset et al.[198] utilize a single-factor model to investigate the factors related to supply chain elasticity. Ang et al.[108] apply CDS spread data and a multi-factor model to examine financial market systemic risk in sovereign countries.

3.1.8 Other Statistical Models

There are numerous common statistical models in traditional economic or management fields for studying enterprise risk. For instance, Duffie et al.[34] employ maximum likelihood estimation to investigate the term structure of the conditional probability of enterprise bankruptcy. Angilella et al.[157] develop a credit risk model based on a multi-criteria model to assess innovative SMEs. Cachon et al.[153] utilize the Nash equilibrium in game theory to analyze competition and cooperation between suppliers and retailers. Considering international oil prices, Maghyereh et al.[158] implement the Delta CoVaR method to measure the systemic risk of banking systems in GCC countries. Due to space constraints, many statistical models have not been mentioned, but these methods also contribute to the study of corporate risk.

3.2 Machine Learning Methods

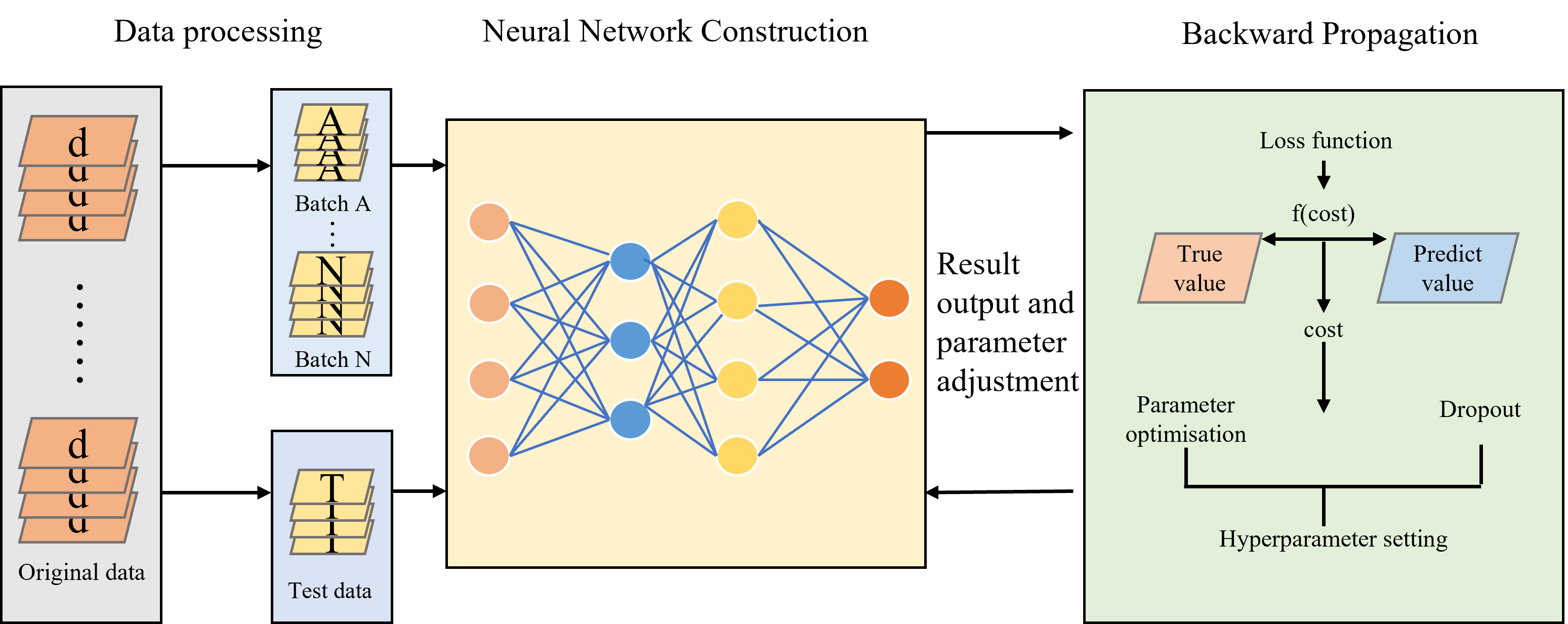

Machine learning methods have gained popularity in enterprise risk prediction and analysis. Compared with traditional statistical methods, machine learning has several advantages. Specifically, it exhibits stronger adaptability, allowing it to more effectively handle non-linear relationships and high-dimensional data. Furthermore, machine learning models have stronger scalability and model generalization capabilities. Table VIII shows the core formulas of the main machine learning models and the meaning of the parameters of these models in this section. Figure 7 shows the general pipeline of machine learning models in enterprise risk analysis.

3.2.1 Logistic Regression

Although supported by linear regression theory, Logistic Regression (LR) introduces nonlinear factors via sigmoid function, thus being capable of dealing with classification problems. LR is often used to analyze a company’s external environment and internal operations. For instance, Everett et al. [41] make a special study of the relationship between macroeconomics and small-firm failure through LR. It finds that a better economic environment can lead some firms to fail due to their propensity to exit after realizing profits. Utilizing a LR model, Zorn et al. [163] analyze the problem of corporate bankruptcy from the perspective of layoffs , finding that downsizing firms are twice as likely to get bankruptcy as non-downsizing firms.

3.2.2 Neural Networks

Neural network (NN) is a machine learning algorithm that emulates the behavioral characteristics of animal neural networks, and is capable of end-to-end data processing.

Boasting for being capable of handling non-linear relationships and high-dimensional data, NN has been extensively applied in enterprise risk prediction. For instance, Coats et al. [202] use a NN to analyze a company’s future financial position. Iturriaga et al. [203] combine multilayer perceptrons and SOM for the financial domain. Not only can the probability of bankruptcy be predicted, but it can also visualize the probability of bankruptcy three years before the bankruptcy occurs. Improvements in performance of the NN can be achieved through better training methods, better architecture, or better input data. In [204], the author analyzes the NN model in three aspects: data span, NN architecture and iteration times. It is found that rich data can improve the performance of the model, and the latter two need to be properly valued to avoid overfitting. Additionally, many studies have optimized input data from different perspectives, all of which have resulted in improved performance of the model [205, 57, 69].

3.2.3 Support Vector Machine

Support vector machine (SVM) is a type of generalized linear classifier that performs binary classification through supervised learning. The decision boundary of SVM is determined by the maximum margin hyperplane, which is calculated based on the sample data.

SVM is widely utilized for bankruptcy prediction, and it is a good choice to apply SVM model when the sample size is small [206]. Also, choosing different kernels for different prediction scenarios may be a good way to improve model performance [207]. Some methods such as feature selection and parameter tuning are used to improve the performance of SVM in enterprise risk analysis. Specifically, many researchers have done a lot of work on feature selection so that SVM can obtain better prediction performance [162, 208]. Other scholars are devoted to the optimization of feature selection and parameter selection [209].

3.2.4 Decision Tree

Decision Tree (DT) is a classical classification and regression algorithm in machine learning. DT is a straightforward and interpretable method that is commonly employed for simple prediction tasks, or as a component of more complex prediction models. As an illustration, Delen et al. [177] employ a two-stage analytical approach to investigate firm risk. The first stage involved the use of exploratory factor analysis to verify the underlying dimensions of financial ratios. In the second stage, four commonly-used decision tree models were utilized to explore potential relationships between firm risk and financial ratios. Sung et al. [210] adopt DT as the bankruptcy prediction model because of its great interpretability. When dealing with excessive variables, DT can also be used for variable selection[211]. To achieve better performance, various optimization methods of DT have been proposed by many scholars. These methods include ensemble methods and other statistical methods [145, 164, 212].

3.2.5 Random Forest

The Random Forest (RF) algorithm is a popular ensemble classifier that utilizes multiple decision trees for training and predicting samples. It is widely acknowledged for its robustness and accuracy in handling complex classification problems.

Although RF demonstrates impressive accuracy, it often requires more time to process large-scale datasets. Therefore, it is recommended to use RF if high prediction accuracy is critical and the dataset is small.

RF can also be used to output intermediate results. Combining evidence theory and RF, Zhu et al. [213] find that

the RF classification result is used as the fundamental probability distribution for evaluating financial risk characteristics, and the evidence synthesis rule of evidence theory is used for multi-source information fusion to determine the financial risk level and corresponding probability distribution.

| Model | Main Formular | Parameter and Explanation |

| Logistic Regression | :Probability of ; : The intercept term of the regression function; | |

| : Row vectors of regression coefficients; : Column vectors of explanatory variables | ||

| Neural Networks | : The activated neuron in layer ; : The activated neuron in layer ; | |

| : Weight from the neuron in layer to the neuron in layer ; | ||

| : The offset of the neuron in layer | ||

| Support Vector Machine | : Parameter vector; : Offset term; | |

| : Label ; : The sample | ||

| Genetic Algorithm | :Probability of individual being selected; | |

| : Population size; : Fitness of individual | ||

| Decision Tree | : Information entropy; : Sample set; | |

| : Number of sample categories; : Proportion of the class sample |

3.2.6 Genetic Algorithm

The Genetic Algorithm (GA) is a biologically-inspired optimization technique that simulates the mechanisms of natural selection and inheritance presented in living systems. GA is typically employed for multi-objective optimization or black-box optimization problems. Current research tends to utilize GA as a tool for rule exploration or as a component of enterprise risk analysis model [214]. For instance, in [160], bankruptcy rules are extracted through GA and applied to bankruptcy prediction. In [215], a robust bankruptcy prediction model is constructed by combining genetic programming algorithm with rough set theory.

3.2.7 Others Methods

Previous studyies often attempt to improve machine learning models by combining theories from different fields or integrating multiple models to enhance performance. Yeh et al. [216] combine DEA, rough sets, and SVM to improve the ability of SVM to predict company bankruptcy. Tsakonas et al. [217] propose the application of genetic programming-based neural logic networks, which can explain the network structure through a set of expert rules. Most models that are using ensemble-based techniques attempt to evaluate all bankruptcy scenarios, either using the same set of variables or the same set of samples. In many cases, these two assumptions do not hold. Jardin et al. [218] use biclustering and neural network-based ensembles to predict bankruptcy. Biclustering methods can estimate subgroups of data while considering possible relationships between samples and variables. Chen et al. [178] propose a bankruptcy prediction model based on the adaptive FKNN method, and the continuous PSO method is used to determine the neighborhood size and fuzzy parameters of the model.

3.3 Deep Learning Methods

Deep learning, a subfield of machine learning, which harnesses the power of artificial neural networks, has a sophisticated architecture consisting of multiple layers for processing. Through back propagation, the model parameters are continuously updated, enabling autonomous data exploration and the generation of informative features. Thus, deep learning methods overcome the limitations of manually designed features and pave the way for more effective financial risk analysis. In this section, we discuss various applications of deep learning methods in risk analysis based on their structural characteristics.

3.3.1 Convolutional Neural Networks

CNNs are advanced deep learning models that leverage unique features such as local connectivity and weight sharing. These unique features make CNNs highly effective in extracting significant features from complex financial data, revealing obscured patterns and trends that can facilitate precise predictions and informed decisions regarding future market [219]. Based on this feature, Wei et al. [49] extract structured data and unstructured text from corporate annual reports and construct a financial risk prediction system using CNN and LSTM methods. Hosaka et al. [16] convert the financial scale data into grayscale images and then apply CNN in bankruptcy prediction.

3.3.2 Autoencoder

Autoencoder is an unsupervised neural network model that aims to compress the input data into a low-dimensional feature space and then reconstruct the original input data from this feature space. Therefore, Autoencoder can also be used for enterprise financial risk analysis. For instance, Soui et al. [151] utilize SAE to extract the best features and also use softmax classifiers to predict bankruptcy. Smiti et al. [150] propose a novel approach called BSM-SAES. This approach combines a boundary synthesis minority oversampling technique and a stacked autoencoder based on the softmax classifier.

3.3.3 Graph Neural Networks

GNN is a deep learning method based on graph structure that transforms nodes and edges into a dense vector form and employs the topological information of the graph for computation and inference. And GNN is commonly used for node classification in enterprise risk analysis. For instance, Yang et al. [102] put forward an innovative framework for financial risk analysis based on supply chain graph mining. Meanwhile, Bi et al. [99] propose TH-GNN, which is applied to tribe-style graphs, with the first level encoding the structural patterns of tribes through contrastive learning and the second level diffusing information based on inter-tribal relationships. Then Bi et al. [152] present KT-GNN, which simulates the transfer of knowledge from vocal nodes to silent nodes by transferring the distribution during message passing and representation learning. It is also used in the financial risk assessment scenario.

3.4 Hybrid Models

In the field of enterprise risk research, a single model may have poor performance in prediction or evaluation. Therefore, some studies combine several models to complement each other’s strengths, hoping to avoid some limitations and improve the overall performance of model evaluation.

3.4.1 Homogeneous Hybrid Model

Some hybrid models are of the same category, which signifies they either combine SEMs or various ML and DL methods. For instance, Giesecke et al. [166] and Pra et al.[220] both employ contagion models with Bernoulli mixture models to investigate different aspects of credit risk for large financial institutions and enterprise borrowing-lending network. Voda et al.[68] utilize the canonical discriminant analysis, sensitivity analysis and stepwise least squares estimation to examine bankruptcy risk.

It can be founded that some previous studies have leveraged multiple ML and DL algorithms. For example, Chen et al.[221] devise a hybrid model combining NN and K-means algorithm to forecast financial distress. Ahn et al.[168] combine GA with the case-based reasoning (CBR) method to improve bankruptcy prediction performance. To better predict the credit risk, You et al.[139] propose a RS-MultiBoosting model, which combines random subspace and MultiBoosting.

In pursuit of further improved prediction performance, some works attempt to merge at least three ML algorithms.

Sun et al.[167] suggest a data mining method that combines attribute-oriented induction, information gain, and DT to predict financial distress problems.

They later improve this method based on multiple classifier serial combinations involving SVM, multiple discriminant analysis (MDA) and CBR [222].

Hung et al.[223] propose a model that combines DT, BPN and SVM to better forecast bankruptcy.

3.4.2 Cross-hybrid Model

Cross-hybrid models combine different types of models, such as statistical and ML models. These models effectively represent the integration of economics and computer science and may achieve a good balance between prediction accuracy and interpretability.

Since the advent of ML techniques, some works have been endeavoring to amalgamate them with SEM, and this approach remains a productive area of research and development even today. For instance, Cheng et al.[224] combine NN and logit analysis to build a hybrid model named RBFN to forecast financial distress. Fernando et al.[67] propose a method for corporate bankruptcy prediction that combines SOM and Multivariate Adaptive Regression Splines. Tarei et al.[225] combine multiple criteria decision making, integrated decision-making trial and evaluation laboratory analytical network process to develop a framework for quantifying supply chain risk.

Some scholars endeavor to integrate three distinct approaches. For example, Xu et al.[92] propose an integrated model called NIM to predict bankruptcy, which combines CNN-oriented DL, SVM and soft set theory. Gao et al.[226] utilize BPNN, analytic hierarchy processes, and data mining algorithm HIUA to forecast the financial risk of listed companies. In order to measure systemic financial risks, Huang et al.[227] employ logistic regression, NN and time-varying parameter vector autoregressive model to process multiple data.

Many studies combining the strengths of more models are widely conducted. For instance, Yildirim et al.[228] contend big data analysis is suitable for corporate credit default prediction, so they introduce two hybrid models based on logistic regression, DT, RF, gradient boosting and graph theory. Sun et al.[229] propose a multi-classifier hybrid model to forecast financial distress, which combines MDA, Logit, NN, DT, SVM, CBR. Jardin et al.[170] construct two models for bankruptcy prediction, which are based on discriminant analysis, logistic regression, FNN, Cox’s model, SOM and NN.

4 Spotlights of Representative Works

In this section, we first make a brief introduction to the rep- representative works and then present their unique contributions.

| Reference | Title | Journal | Year | Citations | ||

| [2] | Financial ratios, discriminant analysis and the prediction of corporate bankruptcy | J FINANC | 1968 | 23685 | ||

| [230] |

|

J FINANC | 1995 | 3069 | ||

| [231] |

|

Journal of management | 2006 | 2781 | ||

| [232] |

|

J FINANC | 2008 | 2754 | ||

| [233] |

|

Journal of Business Venturing | 2011 | 2486 | ||

| [1] |

|

J FINANC ECON | 2012 | 2468 | ||

| [234] |

|

The review of financial studies | 1997 | 2368 | ||

| [72] | Systemic risk and stability in financial networks | American Economic Review | 2015 | 2119 | ||

| [235] |

|

Decision sciences | 2007 | 1891 | ||

| [236] | A neural network model for bankruptcy prediction | IJCNN | 1990 | 1465 | ||

| [237] |

|

Journal of Business Ethics | 2006 | 1384 | ||

| [238] | Benchmarking state-of-the-art classification algorithms for credit scoring | JORS | 2003 | 1192 | ||

| [239] |

|

IJPE | 2008 | 1160 | ||

| [209] | Bankruptcy prediction using support vector machine with optimal choice of kernel function parameters | EXPERT SYST APPL | 2005 | 1154 | ||

| [240] |

|

ABACUS | 2007 | 1086 | ||

| [241] |

|

INFORMS | 2019 | 1086 | ||

| [242] |

|

Information Sciences | 2014 | 753 | ||

| [243] |

|

J FINANC | 2012 | 675 | ||

| [147] |

|

EXPERT SYST APPL | 2017 | 656 | ||

| [244] |

|

J BANK & FINANC | 2011 | 586 | ||

| [245] |

|

Production Economics | 2015 | 506 | ||

| [22] |

|

J BANK & FINANC | 2009 | 473 | ||

| [197] |

|

J BANK & FINANC | 2014 | 466 | ||

| [20] |

|

REV FINANC | 2014 | 348 | ||

| [18] |

|

EJOR | 2019 | 232 | ||

| [16] |

|

EXPERT SYST APPL | 2019 | 209 | ||

| [102] |

|

IJCAI | 2021 | 45 |

We select the representative works based on citations and methodological progress. The citation for each reference is based on the citation statistics from Google Scholar as of April 23, 2023. Table IX presents the most representative studies during the period from 1968 to 2023 in terms of citations. The highly cited studies can be broadly divided into two groups according to their focus: existence and methods. Table X summarizes the findings of these representative works for easy review.

The first category is the existence category, which focuses on demonstrating the comovements between enterprise financial risk and various types of data including financial index, textual information, relational data and intelligence integration. For instance, Belas et al. [38] conduct a study that revealed that there was a direct connection between the corporate governance structure and enterprise bankruptcy. Imbierowicz et al. [197] examine the relationship between liquidity risk and credit risk in the banking industry from different perspectives. Chae [245] analyze supply chain tweets and gain insight into the potential role of Twitter in supply chain practice and research.

The second category focuses on utilizing various techniques, particularly the latest advances in NLP and ML, to extract valuable information from textual media and relation data. This helps establish connections between enterprise multi-source heterogeneous data and financial risk. Barboza et al. [147] employ four machine learning models to predict the probability of enterprise bankruptcy, and discovery that RF is the best. Campbell et al. [232] leverage a reduced-form econometric model to predict short- and long-term corporate bankruptcies and failures, while showing that stocks with a high risk of failure tend to deliver lower average returns.

| Group | Reference | Contribution | ||

| Existence | [197] |

|

||

| [241] |

|

|||

| [240] |

|

|||

| [246] |

|

|||

| [245] |

|

|||

| [243] |

|

|||

| [239] |

|

|||

| [235] |

|

|||

| Methods | [1] |

|

||

| [147] |

|

|||

| [237] |

|

|||

| [242] |

|

|||

| [244] |

|

|||

| [234] |

|

|||

| [232] |

|

|||

| [230] |

|

5 Directions For Future Work

5.1 Enterprise Intelligence

We anticipate that enterprise risk prediction will increasingly rely on the integration and analysis of diverse data sources. Such sources may include information from customers, industries, affiliated companies, and governments, with seemingly insignificant data such as business utility bills also potentially providing effective supplements to traditional data. And, it is also crucial to note that data availability can be a significant challenge for enterprise risk prediction. Thus, it is imperative to prioritize the construction of open databases that can serve as a platform for sharing. By doing so, we can unlock the full potential of the data and gain a more comprehensive understanding of risk profiles.

5.2 Analysis Model

With the advancement of deep learning, there has been rapid progress in the development of models that can capture more intricate information and effectively process unstructured data. GNN and time series information extraction based on deep learning are two promising technologies with great potential. In recent years, graph neural networks have emerged as a novel neural network paradigm specifically tailored to learn from and reason about graph-structured data, which is known to contain rich relational information. It combines the advantages of graph and deep learning to achieve deeper information correlation. Currently, there are some studies on enterprise risk analysis based on graph attention [247, 149]. And the growth of enterprises is a dynamic and continuous evolving process. To better understand the enterprises risks from a temporal perspective, it is essential to incorporate time-series information into the analytical framework. While traditional measurement methods have been employed for time-series analysis [248, 133], there is growing interest in leveraging deep learning techniques, including LSTM [249] and transformer [250], to more accurately model and analyze enterprise risks over time. In addition, heterogeneous convergence is a promising way to model the multidimensional nature of enterprise risk. By integrating different models, we can comprehensively present and analyze risks from multiple perspectives, achieving a significant improvement in analytical performance.

5.3 Contagion Mechanism

Current research is examining the potential risks that financial networks pose to companies. However, to fully comprehend these risks, it is essential to gain a deeper understanding of the specific pathways through which they are transmitted. This involves identifying the impact of risk on individual companies, as well as the extent to which these risks spread. Additionally, it is crucial to investigate the temporal aspects of risk transmission, such as the length of time it takes for risks to spread to related companies. Furthermore, whether the risks types of related companies are the same as those of the original company is also significant. Unfortunately, technological limitations have prevented a systemic study of these questions. Given the progress of globalization, it is critical to gain a comprehensive understanding of risk transmission mechanisms. Therefore, further exploration into this research direction is highly recommended.

5.4 Risk Interpretability

Despite existing deep learning models have achieved success in enterprise risk analysis, these methods are often treated as black-boxes and cannot explain “Why the model makes certain predictions?”. This limitation hinders their application in critical areas such as finance and security. To address this issue, several techniques are proposed to explain the deep models for image and text data [251, 252]. And the explanation techniques for GNNs are categorized into two main classes: instance-level methods [253] and model-level methods [254, 255, 256]. Therefore, exploring a risk detector that can provide high-quality predictions and explanations simultaneously is a promising approach for future research on enterprise financial risk.

5.5 LLMs for Enterprise Financial Risk

LLMs can be applied in various scenarios, such as intelligent customer service, investment advisory, marketing, risk manage- ment, operations, investment research, investment banking, quan- titative trading. In the financial industry, LLMs have already been deployed, with examples including Morgan Stanley, Stripe, and Bloomberg GPT. In the area of enterprise financial risks, LLMs can be utilized for public opinion analysis and regulation extraction from texts. Furthermore, LLMs can also be employed to improve existing financial NLP tasks, such as relation extraction and named entity recognition, so as to construct enterprise knowledge graphs. Then, the inference capability of LLMs on graph-structured data can be leveraged to analyze financial risks of enterprises.

6 Conclusion

In this survey, we attempt to cascade and systematize existing research on enterprise financial risk, providing a comprehensive review of enterprise risk analysis. This is the first survey for enterprise financial risk from the Big Data perspective. In particular, we first begin with an introduction to the types, granularity, intelligence and evaluation metrics of enterprise financial risk. Then we classify models of enterprise financial risk, show the basic implementation framework for each type of model, and summarise representative approaches in enterprise risk analysis. Finally, we elaborate on current cutting-edge research and its possible future directions. We believe that this survey will provide researchers in the field with the fundamental knowledge and a clear framework for research.

Acknowledgments

The research is supported by the National Natural Science Foundation of China under Grant Nos. U1811462, 71725001, 71910107002, 61906159, 62176014, 71873108, 62072379, and Sichuan Science and Technology Program under Grant No. 2023NSFSC0032, 2023NSFSC0114, and Guanghua Talent Project of Southwestern University of Finance and Economics, and “Double-First Class” International Innovation Project (SYL22GJCX07).

References

- [1] M. Billio, M. Getmansky, A. W. Lo, and L. Pelizzon, “Econometric measures of connectedness and systemic risk in the finance and insurance sectors,” Journal of financial economics, vol. 104, no. 3, pp. 535–559, 2012.

- [2] E. I. Altman, “Financial ratios, discriminant analysis and the prediction of corporate bankruptcy,” The Journal of Finance, vol. 23, no. 4, pp. 589–609, 1968.

- [3] W. Chen, Z. Li, and Z. Xiao, “On credit risk contagion of supply chain finance under covid-19,” Journal of Mathematics, 2021.

- [4] Y. Zhao, S. Wei, Y. Guo, Q. Yang, Q. Li, F. Zhuang, J. Liu, and G. Kou, “Combining intra-risk and contagion risk for enterprise bankruptcy prediction using graph neural networks,” arXiv preprint arXiv:2202.03874, 2022.

- [5] K. Abduraimova, “Contagion and tail risk in complex financial networks,” Journal of Banking & Finance, p. 106560, 2022.

- [6] R. A. Collins and R. D. Green, “Statistical methods for bankruptcy forecasting,” Journal of Economics and Business, vol. 34, no. 4, pp. 349–354, 1982.

- [7] W. Xu, W. Liu, C. Xu, J. Bian, J. Yin, and T.-Y. Liu, “Rest: Relational event-driven stock trend forecasting,” in Proceedings of the Web Conference 2021, 2021, pp. 1–10.

- [8] Z. Hua, Y. Wang, X. Xu, B. Zhang, and L. Liang, “Predicting corporate financial distress based on integration of support vector machine and logistic regression,” Expert Systems with Applications, vol. 33, no. 2, pp. 434–440, 8 2007.

- [9] C. Yin, C. Jiang, H. K. Jain, and Z. Wang, “Evaluating the credit risk of smes using legal judgments,” Decision Support Systems, vol. 136, p. 113364, 2020.

- [10] C. Wang, F. Yu, Z. Zhang, and J. Zhang, “Multiview graph learning for small-and medium-sized enterprises’ credit risk assessment in supply chain finance,” Complexity, vol. 2021, 2021.

- [11] E. Letizia and F. Lillo, “Corporate payments networks and credit risk rating,” EPJ Data Science, vol. 8, no. 1, p. 21, 2019.

- [12] Z. You, X. Chi, W. Gang-Jin, and Y. Xin-Guo, “Predicting china’s sme credit risk in supply chain finance based on machine learning methods,” Entropy, vol. 18, no. 5, p. 195, 2016.

- [13] B. Sang, “Application of genetic algorithm and bp neural network in supply chain finance under information sharing,” Journal of Computational and Applied Mathematics, vol. 384, p. 113170, 3 2021.

- [14] G. Kou, Y. Xu, Y. Peng, F. Shen, Y. Chen, K. Chang, and S. Kou, “Bankruptcy prediction for smes using transactional data and two-stage multiobjective feature selection,” Decision Support Systems, vol. 140, p. 113429, 2021.

- [15] E. Tobback, T. Bellotti, J. Moeyersoms, M. Stankova, and D. Martens, “Bankruptcy prediction for smes using relational data,” Decision Support Systems, vol. 102, pp. 69–81, 2017.

- [16] T. Hosaka, “Bankruptcy prediction using imaged financial ratios and convolutional neural networks,” Expert systems with applications, vol. 117, pp. 287–299, 2019.

- [17] K. Lee, D. Booth, and P. Alam, “A comparison of supervised and unsupervised neural networks in predicting bankruptcy of korean firms,” Expert Systems with Applications, vol. 29, no. 1, pp. 1–16, 2005.

- [18] F. Mai, S. Tian, C. Lee, and L. Ma., “Deep learning models for bankruptcy prediction using textual disclosures,” European journal of operational research, vol. 274, no. 2, pp. 743–758, 2019.

- [19] I. D. Dichev, “Is the risk of bankruptcy a systematic risk?” the Journal of Finance, vol. 53, no. 3, pp. 1131–1147, 1998.

- [20] R. Gropp, C. Gruendl, and A. Guettler, “The impact of public guarantees on bank risk-taking: Evidence from a natural experiment,” Review of Finance, vol. 18, no. 2, pp. 457–488, 2014.

- [21] J. Ming and X. Ming, “Determinants of the guarantee circles: The case of chinese listed firms,” Pacific-Basin Finance Journal, vol. 20, no. 1, pp. 78–100, 2012.

- [22] B. Henk, C. Rebel A, and F. Lawrence J, “Expropriation through loan guarantees to related parties: Evidence from china,” Journal of Banking & Finance, vol. 33, no. 1, pp. 141–156, 2009.

- [23] J. A. Wilcox and Y. Yasuda, “Government guarantees of loans to small businesses: Effects on banks’ risk-taking and non-guaranteed lending,” Journal of Financial Intermediation, vol. 37, pp. 45–57, 2019.

- [24] D. Cheng, X. Wang, Y. Zhang, and L. Zhang, “Risk guarantee prediction in networked-loans,” in Proceedings of the Twenty-Ninth International Conference on International Joint Conferences on Artificial Intelligence, 2021, pp. 4483–4489.

- [25] C. Dawei, N. Zhibin, and Z. Yiyi, “Contagious chain risk rating for networked-guarantee loans,” in Proceedings of SIGKDD, 2020, pp. 2715–2723.

- [26] K. Valaskova, T. Kliestik, and M. Kovacova, “Management of financial risks in slovak enterprises using regression analysis,” Oeconomia Copernicana, vol. 9, no. 1, pp. 105–121, 2018.

- [27] I. Oikonomou, C. Brooks, and S. Pavelin, “The impact of corporate social performance on financial risk and utility: A longitudinal analysis,” Financial Management, vol. 41, no. 2, pp. 483–515, 2012.

- [28] J. F. Kölbel, T. Busch, and L. M. Jancso, “How media coverage of corporate social irresponsibility increases financial risk,” Strategic Management Journal, vol. 38, no. 11, pp. 2266–2284, 2017.

- [29] M. Zhai, “Risk prediction and response strategies in corporate financial management based on optimized bp neural network,” Complexity, vol. 2021, 2021.

- [30] Y. Cao, Y. Shao, and H. Zhang, “Study on early warning of e-commerce enterprise financial risk based on deep learning algorithm,” Electronic Commerce Research, vol. 22, no. 1, pp. 21–36, 2022.

- [31] J.-B. Kim, L. Li, L. Y. Lu, and Y. Yu, “Financial statement comparability and expected crash risk,” Journal of Accounting and Economics, vol. 61, no. 2-3, pp. 294–312, 2016.

- [32] D. McKillop, D. French, B. Quinn, A. L. Sobiech, and J. O. Wilson, “Cooperative financial institutions: A review of the literature,” International Review of Financial Analysis, vol. 71, p. 101520, 2020.

- [33] K. Xing, D. Luo, and L. Liu, “Macroeconomic conditions, corporate default, and default clustering,” Economic Modelling, vol. 118, p. 106079, 2023.

- [34] D. Duffie, L. Saita, and W. Ke, “Multi-period corporate default prediction with stochastic covariates,” Journal of financial economics, vol. 83, no. 3, pp. 635–665, 3 2007.

- [35] J. Belas, L. Smrcka, B. Gavurova, and J. Dvorsky, “The impact of social and economic factors in the credit risk management of sme,” Technological and Economic Development of Economy, vol. 24, no. 3, pp. 1215–1230, 2018.

- [36] D. Y. Tang and Y. Hong, “Market conditions, default risk and credit spreads,” Journal of Banking & Finance, vol. 34, no. 4, pp. 743–753, 4 2010.

- [37] J. A. Ohlson, “Financial ratios and the probabilistic prediction of bankruptcy,” Journal of accounting research, pp. 109–131, 1980.

- [38] C. M. Daily and D. R. Dalton, “Bankruptcy and corporate governance: The impact of board composition and structure,” Academy of Management journal, vol. 37, no. 6, pp. 1603–1617, 1994.

- [39] P. Arora, “Financially linked independent directors and bankruptcy reemergence: The role of director effort,” Journal of Management, vol. 44, no. 7, pp. 2665–2689, 2018.

- [40] H. Kamalirezaei, A. A. Anvary Rostamy, A. Saeedi, and M. Khodaei Valeh Zaghard, “Corporate social responsibility and bankruptcy probability: Exploring the role of market competition, intellectual capital, and equity cost,” Journal of Corporate Accounting & Finance, vol. 31, no. 1, pp. 53–63, 2020.

- [41] J. Everett and J. Watson, “Small business failure and external risk factors,” Small business economics, vol. 11, no. 4, pp. 371–390, 1998.

- [42] M. Cowling, R. Brown, and A. Rocha, “¡? covid19?¿ did you save some cash for a rainy covid-19 day? the crisis and smes,” International Small Business Journal, vol. 38, no. 7, pp. 593–604, 2020.

- [43] K. Cowan, A. Drexler, and Á. Yañez, “The effect of credit guarantees on credit availability and delinquency rates,” Journal of Banking & Finance, vol. 59, pp. 98–110, 2015.

- [44] W. Binghui, “Asset securitization and rate of return: A study on letters of guarantee,” Physica A: Statistical Mechanics and its Applications, vol. 490, pp. 1551–1554, 2018.

- [45] T. McNulty, C. Florackis, and P. Ormrod, “Boards of directors and financial risk during the credit crisis,” Corporate Governance: An International Review, vol. 21, no. 1, pp. 58–78, 2013.

- [46] B. Sabri, C. Alexis, M. Riadh, and S. Asif, “Does corporate social responsibility reduce financial distress risk?” Economic Modelling, vol. 91, pp. 835–851, 2020.

- [47] G. C. Landi, F. Iandolo, A. Renzi, and A. Rey, “Embedding sustainability in risk management: The impact of environmental, social, and governance ratings on corporate financial risk,” Corporate Social Responsibility and Environmental Management, 2022.

- [48] X. Li, J. Wang, and C. Yang, “Risk prediction in financial management of listed companies based on optimized bp neural network under digital economy,” Neural Computing and Applications, pp. 1–14, 2022.

- [49] W. Wei and B. Li, “Analysis and risk assessment of corporate financial leverage using mobile payment in the era of digital technology in a complex environment,” Journal of Mathematics, vol. 2022, 2022.

- [50] L. Zhu, M. Li, and N. Metawa, “Financial risk evaluation z-score model for intelligent iot-based enterprises,” Information Processing & Management, vol. 58, no. 6, p. 102692, 2021.

- [51] G. Qiao, L. Du et al., “Enterprise financial risk early warning method based on hybrid pso-svm model,” Journal of Applied Science and Engineering, vol. 22, no. 1, pp. 171–178, 2019.

- [52] K. Carling, T. Jacobson, J. Lindé, and K. Roszbach, “Corporate credit risk modeling and the macroeconomy,” Journal of banking & finance, vol. 31, no. 3, pp. 845–868, 3 2007.

- [53] C.-H. Wu, G.-H. Tzeng, Y.-J. Goo, and W.-C. Fang, “A real-valued genetic algorithm to optimize the parameters of support vector machine for predicting bankruptcy,” Expert systems with applications, vol. 32, no. 2, pp. 397–408, 2007.

- [54] D. Liang, C.-F. Tsai, and H.-T. Wu, “The effect of feature selection on financial distress prediction,” Knowledge-Based Systems, vol. 73, pp. 289–297, 2015.

- [55] S. Ambulkar, J. Blackhurst, and S. J. Grawe, “Firm’s resilience to supply chain disruptions: Scale development and empirical examination,” Journal of Operations Management, vol. 33, pp. 111–122, 2015.

- [56] M. Doumpos and C. Zopounidis, “A multicriteria outranking modeling approach for credit rating,” Decision Sciences, vol. 42, no. 3, pp. 721–742, 7 2011.

- [57] P. du Jardin, “Dynamic self-organizing feature map-based models applied to bankruptcy prediction,” Decision Support Systems, vol. 147, p. 113576, 2021.

- [58] S. Hwijae, H. C, P. Du, and H. Hyung Ju, “Data analytic approach for bankruptcy prediction,” Expert Systems with Applications, vol. 138, p. 112816, 2019.

- [59] A. Khashman, “A neural network model for credit risk evaluation,” International Journal of Neural Systems, vol. 19, no. 04, pp. 285–294, 2009.

- [60] S. J. H. Shahzad, T. H. V. Hoang, and E. Bouri, “From pandemic to systemic risk: contagion in the us tourism sector,” Current Issues in Tourism, vol. 25, no. 1, pp. 34–40, 2022.