Contract-Backed Digital Cash

Summary

We present a series of essays on digital money combined with secure transactional execution of digital contracts.

In Chapters 1 to 3, based on an exchange theory of money Henglein decomposes money into orthogonal aspects and identifies digital cash as the digital equivalent of physical cash: secure, fungible, decentralized, directly controlled, private; but enhanced with qualitatively new functionality: being extremely efficiently transferable and storable and, most importantly, contract-backed. This facilitates fully digitalized, inexpensive, guaranteed transactional execution such as atomic resource exchanges, without a multitude of intermediaries and expensive or slow semi-manual processes. A didactic objective is decomposing properties of money and blockchain/DLT into independent functional aspects to illustrate the enormous unexplored design space, both for concrete digital money designs and not yet explored or under-utilized distributed systems techniques for implementing them. This is aimed at disentangling discussions of digital money design (policy and governance) from potentially misleading and unnecessary preconceptions about particular database, distributed computing, cryptography or data structure techniques, such as Byzantine consensus, cryptographic hashing, Merkle trees, UTxOs, blind signatures, zero-knowledge proofs, etc.

In Chapter 4, Henglein and Olesen review the contemporary banking system and take a critical look at its insistence on relegating individuals and non-bank businesses to private money, which is not secure since it is subject to default risk. Is it really meaningful that ordinary individuals’ and businesses’ digital money is exposed to credit default risk whereas banks, the specialists in assessing credit default risk, have access to guaranteed default-free digital money?

In Chapter 5, Henglein presents a general functionality-oriented framework for blockchain and distributed ledger technology, understood as peer-to-peer platforms for securely managing ownership and exchanges of money and other resources. Their key property is decentralized governance: operating without pre-appointed parties that have privileged access to or control of the system. Decentralization is arguably essential for a free economy with fair competition and thus for digital money. In a centralized digital money system, third parties such as IT companies and banks operating it, gain an inherent competitive advantage since money is involved in all economic transactions.

The final chapters discuss and illustrate the power and role of programmable (contract-backed) digital money in case studies.

For the private sector, in Chapter 6, Sylvest describes effective tokenization of invoice debt using smart contracts on Ethereum, with stablecoins as digital money pegged to US dollars. This corresponds to debt securitization—packaging commercial zero-coupon bonds into tradable securities111Without calling them securities—but effectively available at much lower cost to small and medium-size enterprises.

For the public sector, in Chapter 7, Debois argues the benefits of smart contracts for disbursing payments transparently and reliably in accordance with social legislation.

Finally, in Chapter 8, Nielsen and Olesen propose the establishment of a Danish E-krone with limited usage or limited size, describe a use case and argue its political and economic benefits.

Collectively, the essays illustrate the existing and, in particular, future potential of digital money when powered by smart digital contracts that effectively eliminate both counterparty risk (somebody doesn’t pay or doesn’t deliver) and settlement risk (a trade fails and needs to be aborted) by orders-of-magnitude faster settlement than current practice.

The essays should be of interest to public and private actors (re)considering the role of digital money with secure end-to-end digitalization in a modern society such as Denmark, which provides an efficient digital infrastructure that has an authoritative legal entity register, digital signatures, land registry, energy production data, public data hubs and more that are ready to be integrated into fully automated digital contracts that incorporate transactional digital money for secure economic exchanges. This includes central banks who are competing with both Big Tech and people in hoodies to control the kind of digital cash that will be provided to ordinary citizens and businesses, whether they know it or like it; banks that know that money is about economic exchanges, not individual electronic transfers (which has been a solved problem since the 1960s), and that climate change/green transition, sustainability, funding of SMEs and efficient trade finance require novel, securely and transparently automated forms, analysis, monitoring and enforcement of financial contracts; regulators who may be tempted to enshrine proven—and outdated—practices and technology into conservative regulation without eying the new opportunities of incorporating high-performance privacy-preserving technology for reducing systemic risk and enforcing anti money laundering and counter terrorism funding laws made possible by contract-backed digital cash; politicians and administrators committed to efficiently, fairly and transparently providing legally compliant services to their citizens; and fintech companies ready to pounce on the possibilities of building on top of user-definable smart contracts with bonafide quasi-central-bank issued digital currency by unleashing the computational power of what would have been classified as supercomputers twenty years ago: smartphones.

Authorship and working group on digital cash

The chapters have been authored separately. The authors (only) are responsible for their contents; see the chapter author(s) at the beginning of each chapter. The chapters have been lightly copy-edited for inter-chapter cohesion. The report has been delayed by more than two years due to adversarial circumstances encountered by the editor in the first half of 2019.

The working group on digital cash, which operated in 2018, provided valuable discussions and direction. Its meetings were open and attended by members affiliated with the project partners and other organizations, including Michel Avital (CBS), Søren Debois (ITU), Boris Düdder (DIKU), Jonas Hedman (CBS), Fritz Henglein (DIKU and Deon Digital), Kim Peiter Jørgensen (ITU), Morten Nielsen (Aryze), Christian Olesen (DIKU), Omri Ross (DIKU), Peter Sestoft (ITU), Gert Sylvest (TradeShift Frontiers).

Acknowledgements

The project contract-backed digital cash has been made possible by a grant by the Danish Innovation Network for Finance IT to Copenhagen Business School (CBS), the IT University of Copenhagen (ITU) and the Department of Computer Science at the University of Copenhagen (DIKU). It has been supported in kind by Tradeshift Frontiers, MakerDao, Aryze, and Deon Digital. It has benefited from the invaluable practical help by Copenhagen FinTech and encouragement by the Copenhagen FinTech Lab community.

Chapter 1 An exchange theory of money

Fritz Henglein

We develop a theory of money based on bilateral resource exchange as the basic economic primitive, where one economic agent gives something to another only in exchange for receiving something from that agent in return. The challenge is how to compose such exchanges into achieving a multi-lateral exchange that optimizes resource distribution to achieve a fabled Arrow-Debreu equilibrium (Glicksberg, 1952; Arrow and Debreu, 1954). This is analogous to figuring out how to implement multi-party consensus using pairwise message passing in distributed computing (Axtell, 2003). While taking distributed consensus as a magical primitive with instantaneous effect (as in blockchain systems and much of rational agent economics) is a wonderful and powerful primitive both in computer programming and in economic theory, implementing it using pairwise exchange between unreliable and self-interested agents, respectively network nodes, turns out to be almost arbitrarily hard to achieve. The notion of money as a real thing pops prominently up in this implementation struggle, that is in the machine room of economics, not so much in macroeconomics.

The present account of money is completely ahistorical. Is is an entirely made-up and simplified rationalization, but it should be familiar, if not entirely covered, by traditional tit-for-tat accounts based on coincidence of wants (Kiyotaki and Moore, 2002; Kiyotaki et al., 2001), payments (Kahn and Roberds, 2009) or duality of economic events (McCarthy, 1982). Alexander Del Mar complained that “[a]s a rule political economists […] do not take the trouble to study the history of money; it is much easier to imagine it and to deduce the principles of this imaginary knowledge.” (Del Mar, 1895) Our account would only aggravate his complaint since it is not even given by an economist, but comes from a computer science perspective where synthesizing models at will is the rule of the day.

Nonetheless, we hope it can serve as a coherent story of money as a real thing, even and especially when entirely manufactured ex nihilo, and as being inextricably connected to contracts: goods now for money now, goods now for money later, money now for money later. In general, a contract is a prescriptive multi-party protocol for transferring resources and transmitting information, where a single transfer of money in isolation is almost never the full story. The single act of handing over physical cash or digitally transferring bank money is a solved problem; ensuring that all transfers required by a contract happen is unfortunately not solved by that.

1.1 Resource permutations by exchanges

Let us assume we have a set of agents, where each agent has an economic resource to offer and is in need of a potentially different resource for consumption or to produce something. For simplicity we will also assume that each agent has a single resource to offer and a single resource she needs and that the agents collectively have enough resources to satisfy all needs. This can be generalized mathematically to weighted resource baskets without changing the conceptual fundamentals (Rambaud et al., 2010; Torres Garcia, 2020).

If we number the agents , we can describe the resources they own at the beginning by a vector . The desired end state is a permutation of , that is one-to-one function that moves resource originally owned by agent to agent . E.g. if the agents own , after an exchange between and they own , respectively:

A single pairwise exchange corresponds to a transposition in terms of permutation theory. If an agent exchanges her resource only for a resource she ultimately needs she can only exchange with another agent who happens to need exactly what she has. There is no way of achieving arbitrary permutations by only executing such coincidence-of-wants fulfilling exchanges. Every permutation is accomplishable by a sequence of exchanges, though: It necessarily requires (some) agents to be willing to accept a resource in an exchange even though it is not what they actually need, but is used in a future exchange for their actually needed resource. For example, if represent the needs of our three agents initially owning , there are no immediate-wants exchanges reaching the final state, but if agent is willing to accept in the first exchange, the following exchanges reach the desired end state:

Note that agent transitions through ownership of on her way from initially owning to eventually owning .

1.2 Commodity money: Resources for exchange

Accepting a resource for the sole purpose of trading it away again is a delicate mind game: It is based on the agents’ mutually reinforcing belief that accepting it is okay because somebody else will accept it down the line. Such a resource serves as a medium of exchange. Intuitively, that belief is bootstrapped from the knowledge that somebody can actually use the resource (for consumption or for production of something), and it is reinforced if the resource is observably and effectively used in exchanges by others; is fungible and countable (a commodity); retains its value over time and space; and is easy to transport and store. Such a resource constitutes commodity money.

Historically, several different resources have served as commodity money more or less well, including gold, silver, barley and cows (Zarlenga, 2004). Its perceived preservation of value derives from the commodity having intrinsic value: it can be consumed, or something useful can be produced from it. The primary use of a commodity serving as money is for being traded multiple times, by multiple agents, rather than being consumed. It is accepted in a trade for the express purpose of being traded away again rather than consumed or used for production. As we have seen, the need for one or few types of physical resources serving as money in exchanges can be derived from the decomposition of macroeconomically beneficial multilateral resource exchanges into a set of bilateral resource exchanges. It requires that an agent accepts at least one more resource type in exchange for the products she produces than the ones she is interested in consuming. The macroeconomic benefit of accepting (commodity) money, something agents accept in exchange for their products even though they cannot directly make use of the money received, does not in itself provide an incentive to a self-interested agent to accept it. Translating the benefit into self-interest can be explained in multiple ways: by a Peter Pan theory (self-reinforcing belief that it’s okay to accept it because others believe the same) or Mahagonny theory (the requirement to pay taxes using it guarantees demand for it), FOMO (other agents having more trades by accepting money), mechanism enforcement (an authority requiring accepting money as legal tender to assure macroeconomic—or just their own—benefits), etc.

As for FOMO, agents not accepting commodity money avoid the risk of being stuck with something they do not need themselves, but cannot efficiently participate in multilateral economic exchanges that effectively transport resources through time and space to where they are most useful. This is a competitive disadvantage compared to agents participating in multilateral exchanges by accepting commodity money, which in turn increases the competitive pressure on agents to accept commodity money.

An attractive feature of commodity money is that it not only serves as a medium of exchange, but serves as a store of value that frees the exchange from having to take place at the same time and place: What is needed can be gotten at a later time (by storing the commodity money) and at a different place (by transporting the commodity money there). This provides an effective way of delaying to committing to a particular need and its time and location of delivery: an agent can opportunistically trade away her resource right away and at any opportune location, without having to commit to a particular need of her own at the same time or place.

1.3 Outside money

Commodity money such as gold derives its value from being an effective medium of exchange. But what if interacting agents don’t have any commodity money on hand? Consider our scenario

of three agents interested in a permutation of their bespoke resources , none of which is trusted to be commodity money. Since the permutation is not a coincidence-of-needs permutation111A permutation with maximal cycle length 2. they are stuck.

One solution is bringing in a fourth agent who owns commodity money ; see state 1 of Figure 1.1. By exchanging for with agent (state 2) she injects commodity money into the system, whereupon can pay for receiving from (state 3), then can pay to for (state 4), and eventually can pay to for (state 5).

Agent starts and ends with owning and is the only agent who accepts a resource (in the first exchange) that is neither commodity money nor what she eventually wants, which, to top the peculiarity off, is just what she already has to start with. Why would Agent 0 participate at all if she already has what she needs? She provides outside money, commodity money that she injects from the outside into the system of trading agents ; it unlocks their stalemate, which is due to their lack of coincidence of wants. After receiving back in the final step, Agent can engage with another set of agents using the same commodity money .

Note that none of the agents own at the beginning or at the end of the interaction, and agent owns the same at the beginning and at the end, but, magically, the of agent provided the lubricant for facilitating the multiway exchange between and .

In this fashion a single “special” agent owning commodity money can facilitate arbitrary multiway permutations where (ordinary) agents only accept the resource they need for consumption or production or commodity money.

There are still some problems:

-

1.

There might be too little money. The permutation is made possible by a single , but this is extremely slow: Only one exchange is facilitated at a time. For agents we need rounds of exchanges, where only one exchange is performed during each round. The average production activity, measured in units of , per agent per round is since only one agent receives the resource they need for production, even though there is production capacity in a round. If had units of , all exchanges could be completed in rounds instead of rounds: First, in parallel, each agent sells their resource for to agent ; then, also in parallel, each agent buys the resource they need for from .

As more agents with production capacity arrive, standing in line for a fixed number of increases their demand and thus the value of (in terms of the amount of resources bid for it)—we get deflation.

-

2.

Conversely, there might be too much money. If production capacity decreases and/or more become available, the value of the is depressed—we get inflation.

-

3.

The commodity money brought in by designated agent might be used up by some agent and not returned to Agent 0, preventing further exchanges. In other words, the uses as a commodity and as money compete with each other.

-

4.

The same commodity is used as money in multiple exchanges, which may take place at different locations and at different times. This requires the commodity to be securely storable and efficiently transportable. A resource suitable for consumption is prone to be perishable, however; and a production resource is likely to be bulky and expensive to transport.

The problem with deflation is that it has a self-reinforcing depressing effect on the economic activity it is supposed to make possible. An owner of deflationary commodity money is incentivized to hold on to it since, at any given point in time, it is likely to be worth even more (in terms of other resources) in the future, leading her to ultimately never actually trade it for anything, which negates its economic function as medium of exchange.

The problem with inflation is that the decline in value (in terms of other resources) limits the time the money retains its exchange value, thus also limiting its transportation to other places. It incentivizes its holder to immediately exchange it for a consumption or production resource. This limits its economic function as mediator that breaks the coincidence-of-wants conundrum: ultimately one might as well engage in a barter without the money as an intermediary, and we are back at the problem of gridlocking the economy by limiting it to coincidence-of-wants exchanges.

The problem with commodity money being both commodity and money is that it may have an incidental inflationary or deflationary effect. Considering gold as commodity money, if there is a sudden fad to wear expensive watches or buy new electronic devices or get gold crowns, this may suddenly reduce the amount of gold available as medium of exchange and lead to deflationary economic depression; once the fad is over and replaced by wearing charms made from biodegradable materials, the sudden availability of recycled gold may lead to inflationary anxiety over losing its value. Paradoxically, while the trust in commodity money derives from its usability as commodity its predictable value to the economy as a facilitator of arbitrary resource permutations derives from it actually not being used in production or consumption.

1.4 Representative money

The problem with commodity money being bulky or perishable can be addressed by replacing the commodity proper by a transferable promise to deliver it upon request; this is representative money. A prominent form of representative money is the US Dollar between 1900 and 1971, which represented an IOU of a certain amount of gold.

The basic idea is transferring a bearer certificate of ownership instead of transferring the actual commodity in an exchange. The commodity can be kept at a safe storage place under the guard of a designated administrator who issues such bearer certificates of ownership. The certificates express ownership of a commodity by an agent and its separate possession by the administrator. They serve as proxies for the commodity in exchanges.

Let us write for a transferable promissory note (“IOU”) issued by agent , in which promises to turn over to any agent who owns the note in exchange for the note itself. The note itself is now a resource that can be transferred. If the resource is commodity money and the issuer is widely trusted to satisfy its obligation, the note constitutes representative money. We write for ’s obligation to deliver on the promise. This is a liability, a negative resource. Not “owning” it is preferable to owning it.

The magic of promises as resources is that we can generate them out of nothing. An agent can split (nothing) into a transferable, positive promise to turn something over and the complementary negative obligation of turning it over on demand:

or simply . For now, we don’t allow negative resources to be transferable: It is a liability that an agent “owns” and that can only be canceled if she delivers on it by turning over the actual resource in exchange for the note—or by receiving the note back in exchange for something else.

Recall the exchanges in Figure 1.1, where Agent injects liquidity in the form of to facilitate the exchanges by the other agents . Since is not consumed, but used for exchanges only, she can replace commodity money by representative money and keep the in storage instead; see Figure 1.2.

Note that at any given point Agent has enough in storage to instantaneously redeem the IOUs she has issued and are circulating amongst other agents; that is, the total number of is always at least as great as the number of on her books. As long as that is the case every outstanding IOU can effectively be treated as a certificate of ownership of the corresponding amount of ; Agent only possesses (stores) the , but does not own it.

1.5 Loans

In Figure 1.2 Agent interacts with 2 other agents: Agent whom she initially transfers to in exchange for physical resource and Agent whom she eventually exchanges and with. In other words, Agent needs to handle physical resources and engage in trades with multiple agents even though her net interest and function is to provide liquidity only. We can remove the first need by Agent accepting an IOU from Agent instead; see Figure 1.3.

At every point in time all outstanding IOUs by all agents are covered by actual resources and still work as certificates of ownership. At the end, Agent is involved in what is effectively a three-way exchange: Agent is interested in , which is in possession of Agent , and has money for it; , however, is pledged away to Agent . So Agent acquires the right to from Agent and eventually insists on getting it delivered. This requires a tricky three-way consensus.

One way of breaking this three-way exchange into independent two-way exchanges is by Agent and Agent entering into a loan agreement and, separately and independently, Agent and Agent into an ordinary goods-for-money exchange. At its core, a loan consists of (a contract to perform) two exchanges: for and then for , money now for money later. In Figure 1.4, Agent exchanges for with Agent , and they eventually perform the reverse exchange.

Instead of exchanging commodity money , representative money can be used, if the issuer of the promissory note is generally trusted to deliver upon demand to anybody holding ; see Figure 1.5.

This means a loan consists of Agents and exchanging IOUs with each other twice, with some time in between so that and others can engage in useful exchanges in that time. The point of the IOU exchanges is to inject liquidity into a system of trading agents by temporarily replacing a low-quality IOU by a high-quality IOU with medium-of-exchange status.

Between the two exchanges Agent holds an without actually owning and thus risks getting neither nor back. The value and business of Agent is thus performing the interconnected tasks of providing sufficient liquidity for others to effect useful trades and taking on, aggregating and managing the risk of not getting its money back. In this fashion she isolates other agents from having to perform their own creditworthiness checks on agents issuing IOUs. She charges a fee (interest) for the value of that, of course, which in our examples is left out for simplicity. And she may require a collateral, an IOU by the borrower of a rarely traded resource , as security.222Additionally or alternatively, may also require getting whatever buys with the borrowed money as collateral. For example, in Figure 1.6 Agent gives as collateral to Agent during the loan.

If Agent fails to repay , Agent can insist on exchanging for and canceling (exchanging) the mutual IOUs for ; see Figure 1.7.

1.6 Inside money

Note that is never transferred in Figures 1.5, 1.6 and 1.7. If another agent ever wanted to redeem , Agent could say: “Why do so? You are not really interested in itself for consumption or production, but just in its medium-of-exchange value. You may as well use instead and keep safely stored with me.” In general, if Agent owns initially and finally, every sequence of exchanges involving can be simulated by a sequence using instead of . In particular, the is never exchanged.

This gives rise to a Jedi trick idea: does not even need to exist for the purposes of exchange, only the belief in its existence! To wit, Figure 1.8 shows Agent issuing without actually owning . The exchanges work as before, if the other agents trust the exchange value of as much as and never ask for delivery of .

Observe that is not traded at all, only IOUs involving . The promissory note created by the issuer before she actually has the , if ever, is inside money.333The classical distinction between outside and inside money is a question of which subset of agents is considered. The same money that is outside money in the system without Agent 0 is inside money in the same system with Agent 0.

1.7 Fractional reserve banking

Issuing representative money that must be fully backed by the underlying resource at all times, as in Figure 1.5, is essentially full reserve banking: all issued IOUs can instantaneously be redeemed by Agent . In particular, the underlying resources must have been produced. The IOU issued by Agent as part of her loan to Agent in Figure 1.5 is an example of a transfer that is fully covered by Agent ’s reserves. If we think of Agent as a bank, it corresponds to the bank lending some of its equity to Agent . The volume of loans it can make in this fashion is limited by its equity.

The diametric opposite to full reserve banking is if none of the IOUs are backed and thus none of them can be redeemed, as in Figure 1.8; this is the essence of fiat money, which we will get to later. In Figure 1.8 Agent simply “prints” representative money out of thin air with no reserves, loans it to Agent and gets away with it since nobody ever redeems it. If the volume of IOUs issued is not bounded in any fashion, that is there is a reserve, capital and balance sheet requirement the bank could, in principle, print as much money as its printers will allow.

In between full-reserve and no-reserve banking is fractional reserve banking. The basic idea is to have enough reserves on hand to satisfy actual redemption requests and thus bluff all IOU holders into believing that one could satisfy any incoming redemption requests, but then count on the IOUs being mostly used as media of exchange that are eventually traded back to the issuer without ever being redeemed, thus making the sufficiency of the fractional reserves self-fulfilling.

1.7.1 Current promises backed by future promises

A closer look at these examples reveals that the bank, Agent , is not simply printing money without backing in any resources, but it has other resources than . In Figure 1.8, she owns , the repayment promise by Agent , instead of a to cover the outstanding IOU .

There are three fundamental differences and attendant potential problems with having instead of as a reserve for an outstanding .

-

•

The resource is simply something else than what a holder of expects upon redemption, namely the resource itself. The holder of a promise to get a specific refrigerator delivered on demand may not accept getting offered a freezer instead.

-

•

The resource is a future payment by Agent ; the promise exists now, but the actual loan repayment is at some time in the future. This form of “reserve” does not have to exist yet as a physical resource, but can be something that (presumably) only exists in the future.

-

•

The value of is uncertain; Agent may go bankrupt and default on her loan. The future resource may never materialize.

Fractional reserve banking can be thought of as a form of full reserve banking with uncertainties, where the reserves are, for the most part, different resources than what the issued IOUs actually promise; the resources may exist physically only at some point in the future, if ever, and there is a risk they never will.

Relaxing full to partial reserve requirements alleviates the need for having extraordinary amounts of commodity money to realize the full potential of economic exchanges. A reserve requirement reduces the requirements on how many units of need to exist and be stored at any given time by a factor of .

1.7.2 Seigniorage

Fractional reserve banking gives rise to a lucrative business: Seigniorage, the issuance (printing) of multiple IOUs for a single actual resource in reserve, where each IOU is traded at the same value as the resource itself. With a reserve requirement, IOU production has a whopping 90% lower cost than producing the underlying resource.

1.7.3 Fractional reserve banking risks

Fractional reserve banking carries a number of risks.

-

•

Lack of stability: A multiplicative increase of IOUs due to increased production of may devalue both and IOUs in a multiplicative fashion. IOUs may rapidly lose value due to a bank run (see below). A bank can go bankrupt at any point in time, making IOUs issued by that bank suddenly worthless.

-

•

Distortion of economic activity: The immense profitability of seignorage favors banking over other economic sectors, especially if seignorage profits are privatized, as they are in modern fractional reserve banking.

-

•

Bank runs: If there is a rumor, whether true or not, that a bank may not honor all IOUs it has issued, the optimal strategy for an IOU holder is to redeem their IOUs as quickly as possible, which necessarily leads to a bank run where all IOU holders seek to redeem their IOUs. This is, by definition of fractional reserve banking, not possible. In this case some IOU holders will get their redemption request satisfied, some not. In particular, IOUs are not arbitrarily interchangeable, not living up to the fungibility requirement of money. It depends on how fast their owners are at redeeming them. If, at some point, it is decided to reduce the value of an IOU to the fraction actually covered by existing reserves, as in a bank default, the IOUs issued by that bank lose exchange value, which negates their presumed stability-of-value property. Such reduction indirectly converts seigniorage profits made earlier and transferred (as dividends) to the owners to losses for those holding the IOUs at the time of the bank run.444In practice a bank experiencing a run has other assets, as we noted, which affects the effective value of an IOU after a bank’s bankruptcy. Furthermore, as the IOUs issued by the particular bank suddenly become worthless and IOUs issued by other banks retain their exchange value, this negates the value of bank-issued IOUs as single unit of account that is independent of their issuer.

These are not just hypothetical risks. The world-wide depression of 1929 started with a bank run in the US where depositors demanded their deposits paid out in US Federal Reserve issued cash. The banks employed fractional reserve banking, so they did not have enough cash reserves covering the customer deposits. They tried to borrow cash from The Federal Reserve, which issues the cash. Since cash had a full reserve requirement in terms of gold, the Federal Reserve did not have nor procure enough gold to print enough cash to make the loans to the banks. The banks defaulted; other banks who had given credit to them (had IOUs from them), saw those IOUs become worthless, defaulted themselves and so on.

1.8 Fiat money

An agent can create (and its dual ) out of thin air instantaneously, in the desired amounts and on demand. In both full reserve and fractional reserve banking redemption of an IOU , that is exchanging it for the resource , requires that has such on hand. What if we simply remove the redemption part of an IOU? Then nobody can show up, in hand, and demand delivery of ; the IOU can only be used as medium of exchange, not for redeeming it (exchanging it for delivery of ). As we have seen in Figure 1.8 the IOUs are sufficient for facilitating multiway exchanges, without being on hand or even existing. could be Rai stones, unicorns, dilithium on Planet Remus or anything else that is entirely made up. What makes an unredeemable IOU be perceived as money is the collective trust in —and thus Agent as its issuer—having and retaining a stable exchange value over time and across space when trading it against ordinary economic resources such as in Figure 1.8 that are used for consumption and production. If and only if this succeeds, this is fiat money555From “fiat”, Latin, for “Let it be done.”: it is made up and it has store-of-value, stable-value and unit-of-account properties of money. The key question, of course, is: how can a non-redeemable IOU, essentially a piece of paper that says “Worth 5 unicorns. Signed, Alice”, be trusted to be a store of value and serve as a medium of exchange?

1.9 Central bank money

A central bank is a designated agent that is exclusively able and empowered by a sovereign state to produce nonredeemable IOUs of some made-up resource , called a currency, out of thin air; that is, it can split into any number of units of and its dual liability at any time and subsequently transfer (but not ) to any other agent.

An example of Agent is Nationalbanken, the central bank of Denmark, where is . Let us call the Fabled Danish Krone; it is entirely made up. The central bank can instantaneously print a promissory note saying “The bearer of this note can redeem it at any time for 1 Fabled Danish Krone at Platform , Kings Cross Station. Signed, Nationalbanken.” and simultaneously print a note “Nationalbanken owes 1 Fabled Danish Krone to whoever redeems such note” and put it in its own ledger. It can then give or loan the promissory note to another agent , who in turn can use it as medium of exchange to pay other agents for resources she needs. In case of a loan, eventually needs to trade resources she has produced to get back a note issued by the central bank and return it at the end of the loan. Importantly, such note need not be the same note; any note (or notes) with the same (aggregate) amount can be substituted for the original note; that is, notes are fungible: any set of notes can be replaced by any other set of notes with the same aggregate amount of Fabled Danish Kroner. Otherwise, each note would ultimately constitute its own currency with potentially different value to different agents, diminishing its role as liquid medium of exchange.

Mathematically, starting with , the sum total of the values of IOUs in existence at any given point in time, including the liabilities of the form , remains . This is because both transforming into and transferring from one agent to another keeps their sum total across all agents invariant, and IOUs can be neither lost nor duplicated.666We can model lost money as being owned by a hypothetical “sink” agent that only receives money without ever paying anybody, and successful forging as unauthorized issuance in the central bank’s name. Since only the central bank can own liabilities , this means that it is the only agent with a negative balance, which necessarily equals the sum total of IOUs held by all other agents combined. The key job of the central bank is to observe prices, the amount of paid in exchanges with goods and services and, in some fashion, add or extract amounts of circulating amongst the other agents to keep those prices stable over time. (The “in some fashion” is the tricky part, of course.)

To position as a dominant medium of exchange, an important agent, the government, can force other agents to make payments (think taxes) in as well as insisting on making payments itself in . This creates an immediate demand for and self-reinforcing trust in its function as a canonical medium of exchange. Additionally, legislation may be put in place that forces all agents in a country to accept payment in , ensuring that an agent can pay with down the line when accepting in a trade. Additionally, disallowing payment in competing money-like resources eliminates potential competitors that could fragment liquidity and undermine a government’s and central bank’s fiscal and monetary policy power.

1.10 Private bank money

Any agent can in principle issue transferable promissory notes and thus produce a personal currency. For example, Bob can issue a note that says that the bearer can redeem it for a central bank note like the above; that is, the note represents .777“The bearer of this note can redeem it at any time at my office for a note issued by Nationalbanken that says that its bearer can redeem it for 1 Fabled Danish Krone at Platform , Kings Cross Station. Signed, Bob.” The typical form is a check to “Bearer” (or “Cash”) to be paid in cash (central bank money). Such a promissory note is not fiat money; indeed its prime purpose is being redeemed for the central bank note, which does constitute fiat money as it cannot be redeemed. Being transferable, Bob’s note may serve as medium of exchange – it is Bob’s Danish Krone (BDKK) – but it carries a serious risk of redemption failure since Bob may issue many more such notes than he can assuredly redeem for central bank money. For example, Bob can issue new BDKK, transfer them to his friends in exchange for promises to get them back later (loans), have his friends redeem BDKK for all the central bank DKK Bob actually has, and then declare bankruptcy, leaving the remaining holders of BDKK without possibility of redeeming them for central bank DKK, especially if Bob’s friends in the mean time have lost the central bank DKK they got in a casino (they say).

Private bank money in the form of bank deposits is like Bob money: promissory notes by a regulated agent that are redeemable for central bank money (cash) upon demand. Regulation and oversight of a bank are there to avoid that a bank’s owners run from their obligations by declaring bankruptcy or print too many IOUs that they cannot redeem.

1.11 Central bank money versus private bank money versus private IOUs

The differences between , , and where is the central bank, is a bank, and is neither central bank nor ordinary bank are subtle, but important:

-

•

is fiat currency, a mythical resource that can only be manufactured by the central bank ; it can do so near-instantaneously, at near-zero cost and in arbitrary amounts.

-

•

is fungible central bank currency; an unnumbered IOU in some amount issued by the central bank to deliver to its holder on demand, but with the extra clause that it cannot be redeemed. An amount of corresponds to any set of unnumbered bills or coins whose sum adds to the given amount. Since cannot be redeemed it is indistinguishable in function from . Indeed, we will identify and :

Mathematically, we can think of one as the infinite IOU sequence . It is an IOU that, when presented to the central bank for redemption, is simply returned: “Here is what you are owed.” This model explains why is simultaneously a claim against the central bank and an asset: it can be redeemed, but only for itself.888Calling it a claim is somewhat misleading, almost facetious since one cannot really get anything else but the claim back. Redeeming a claim against a shoemaker to get a pair shoes results in a pair of shoes being delivered. The shoes can then be used for walking, which the claim itself is not suitable for. The claim and the shoes are observably different. Trying to redeeming a 100 DKK note at Nationalbanken is a different matter. At best it may result in being exchanged for two 50 DKK notes. Whatever is possible with those can also be done with the 100 DKK note; they are observably equivalent. Instances are account balances, whether held in a centralized or decentralized database such as the currency reserve balances in a central bank database system or the Ether balances associated with each address in Ethereum, where “Ethereum” is the (decentralized implementation of the) non-sovereign “central bank” issuing the magical currency Ether and “Bitcoin” is the (decentralized implementation of the) non-sovereign central bank issuing the magical currency Bitcoin.

-

•

is a currency note, a numbered (serialized) central bank note in some particular amount. The serial number can be used to track its use; in particular, it is distinguishable from other notes with the same amount, but different number. Examples are numbered (physical) cash notes issued by a central bank, (digital) unspent transaction outputs (UTxO) in Bitcoin-style blockchain and distributed ledger systems, and nonfungible tokens in Ethereum-like blockchain systems.

-

•

is bank money, an IOU issued by bank that can be redeemed for . It is a legal requirement that must fully honor the IOU: it must deliver in exchange for receiving at a 1:1 bank money for central bank currency exchange rate. Note, though, that may fail to honor the redemption request; it may simply default on it. Furthermore, and for banks are required to be exchanged at a 1:1 exchange rate, which, modulo default by or , is a corollary of and being one-to-one exchangeable.999Bank may, however, want to refuse to enter into a contract with a customer where it issues an in exchange for , that is let customers deposit physical cash. This might be the case where, as is currently the case, banks receive less interest from the central bank than it gives its customers.

-

•

is a promise by to redeem it for . Depending on who is it may be worth anything between and nothing.

These are all transferable bearer instruments.

Note that an ordinary private bank account is not a specific amount of central bank currency owned by its account owner and merely stored in the bank. The account owner owns an IOU issued by the bank, not the central bank, in the amount of its current balance. The difference is that the account owner does not own the central bank currency itself, but only the promise to get the central bank currency from the bank on demand – the bank may not (and typically will not) actually have enough central bank currency on hand to redeem the IOU on demand.

It is instructive to illustrate the difference between bank money and (central bank issued) physical cash. The cash in a bank box is central bank currency owned by the customer who put it in the bank box; the cash is not owned by the bank. The bank merely provides the storage facility. If the cash disappears from the bank box without permission by the customer, somebody has stolen it, which is a criminal act. A standard bank account, on the other hand, is a call loan made to the bank: The customer transfers ownership of the central bank currency to the bank in exchange for a promise to get it returned on demand. If the customer makes such a demand and the bank does not comply with it, this is “only” breach of contract, not a criminal act. If a bank goes bankrupt and it is found that the cash contents of its bank boxes have disappeared because the bank used it for other purposes, then this constitutes theft. A bank account balance that cannot be honored, on the other hand, is failure to satisfy a contract, which is not theft. Account owners provide loans to the bank; thus, in principle, they should conduct a thorough creditworthiness involving everything the bank engages in to assess their chances of getting their loans back.

Banks offer bank boxes in their vaults for securely storing valuables, including physical cash. A natural question is: Why not offer secure storage of central bank digital currency?

Chapter 2 Keeping track of money

Fritz Henglein

In Chapter 1 we started out with a conceptual ownership state: agents own resources , respectively, and engage in exchanges eventually resulting in them owning , respectively. But how is this ownership state implemented in practice? Most importantly, how is it ensured that transfers of resources are really transfers: that the resource is subsequently not only owned or possessed by the recipient, but is also no longer owned or possessed by the sender?

This is a particularly touchy issue for fiat money: Fiat money is entirely made up. Its greatest achievement, being extremely cheap to produce is also its greatest achilles heel: how to prevent it from being duplicated (sending the money, but keeping a copy – that is forging it) or, maybe of slightly lesser concern, being lost?

More drastically, with entirely digital fiat money, there is not even a basement to store physical bills and coins in to cross-check how much money there really is. Where is it then? In a spreadsheet, database, blockchain system, smart card chip? How can one be sure that somebody updating a number in a spreadsheet in some bank doesn’t create money that didn’t exist before and just gives it to a good friend?

In this chapter we discuss a conceptual framework for representing an ownership state and how money transfers are made in it. It unifies the notions of token-based and account-based money, which are often considered distinct, and suggests that a key distinction is whether transfers are more or less confidential (privacy-preserving), which is a property of the transfers, not of the money being transferred.

2.1 Ownership states and transfers

A resource exchange, the fundamental transaction in the exchange theory of Chapter 1, consists of two resource transfers: one from A to B, the other from B to A. A resource ownership state is represented by a map from agents to resources. This map is conceptual in nature; it represents a mathematical function that is not necessarily known (observable) in its entirety by any single agent. Each agent has a view—partial information—of this map; the stipulated mathematical existence of the map expresses that the views are consistent with each other, not that there is any agent who knows the entire function. In our explanations the reader has been put into the role of an almighty Olympic observer who can “see” the entire ownership state; this must not be confused with any real agent being able to do the same. In particular, this does not even imply that the map necessarily exists as a table, database or other data structure in any one computer or network of computers.

2.2 Ownership: Control and balance

It is useful to introduce an intermediate layer between agents and the resources they own: agents control resource identifiers, unique identifiers that are mapped to a balance of the (economic) resources they represent at a particular point in time. If, at a particular point in time, agent controls resource identifier and points to resource we say that owns at that time, and the set of all ownership relations of this kind constitutes the (global) ownership state at that time. In this fashion the functional composition of control and balance maps defines the resource ownership state. This provides a useful conceptual as well as mathematical and computer systems-oriented framework for both physical and digital as well as token-based and account-based forms of money.

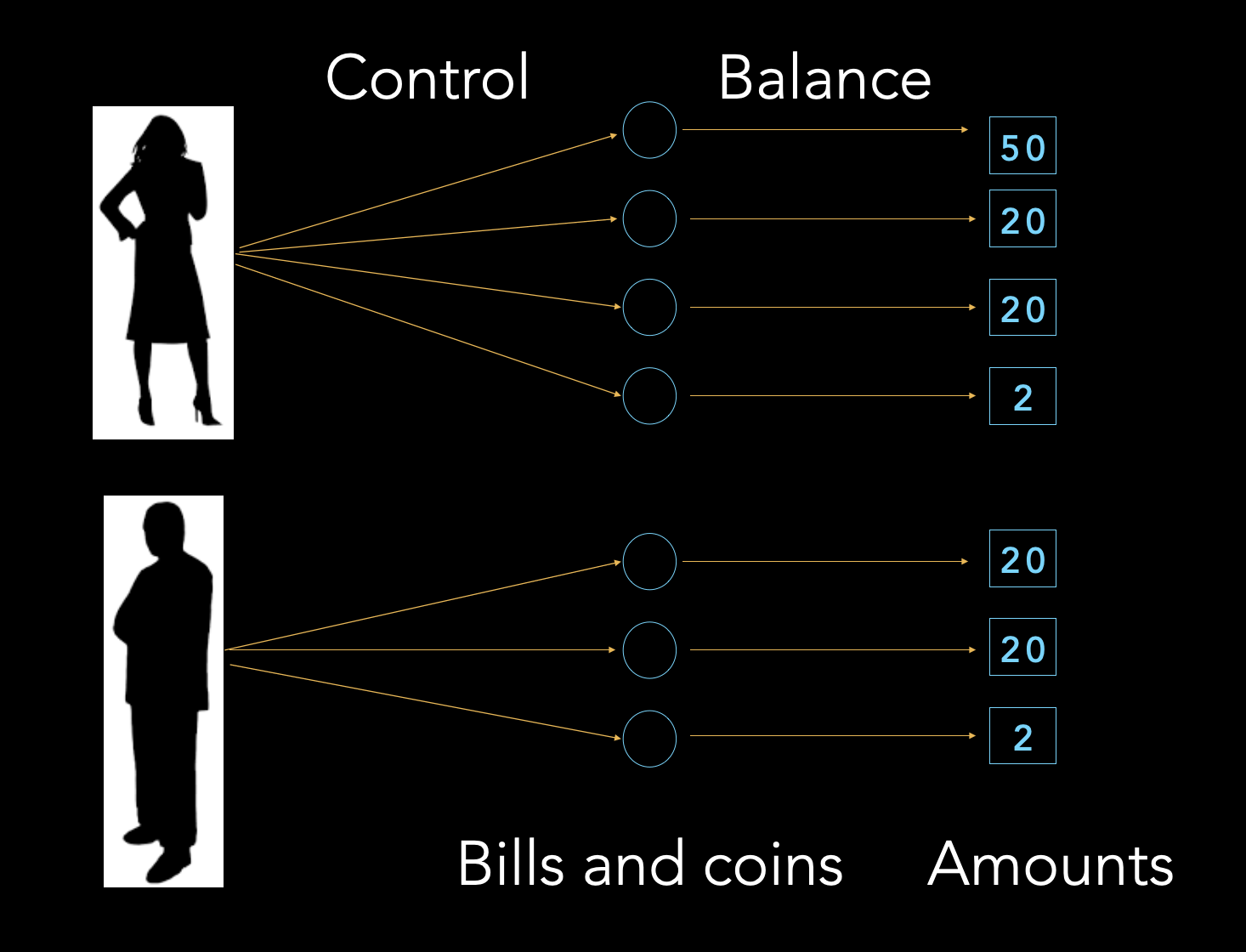

Physical cash

For physical cash, the resource identifiers are physical coins and bills, which are mapped to their money value, which is what is written on them. Agents exercise control over the resource identifiers by controlling access to their location in the real world. For example, in Figure 2.1, Alice controls 4 distinct bills and coins by knowing where they are and being able to effectively handing them over to anybody else she and only she decides to give them to. They have balances of DKK 50, 20, 20 and 2, respectively. The control map is completely decentralized and private; it is not stored in any single place or system: there is no single agent who knows which agent controls which resource pointers. The balance map is also quite private: the central bank (only) knows which resource identifiers are circulating and how much each is worth; other agents don’t know that beyond possibly remembering/storing which notes they happen to have owned themselves at some of time, for example by storing the serial numbers of each banknote that passes through their hands. Note that the control and balance maps exist conceptually, but are not stored in any one place or computer system.

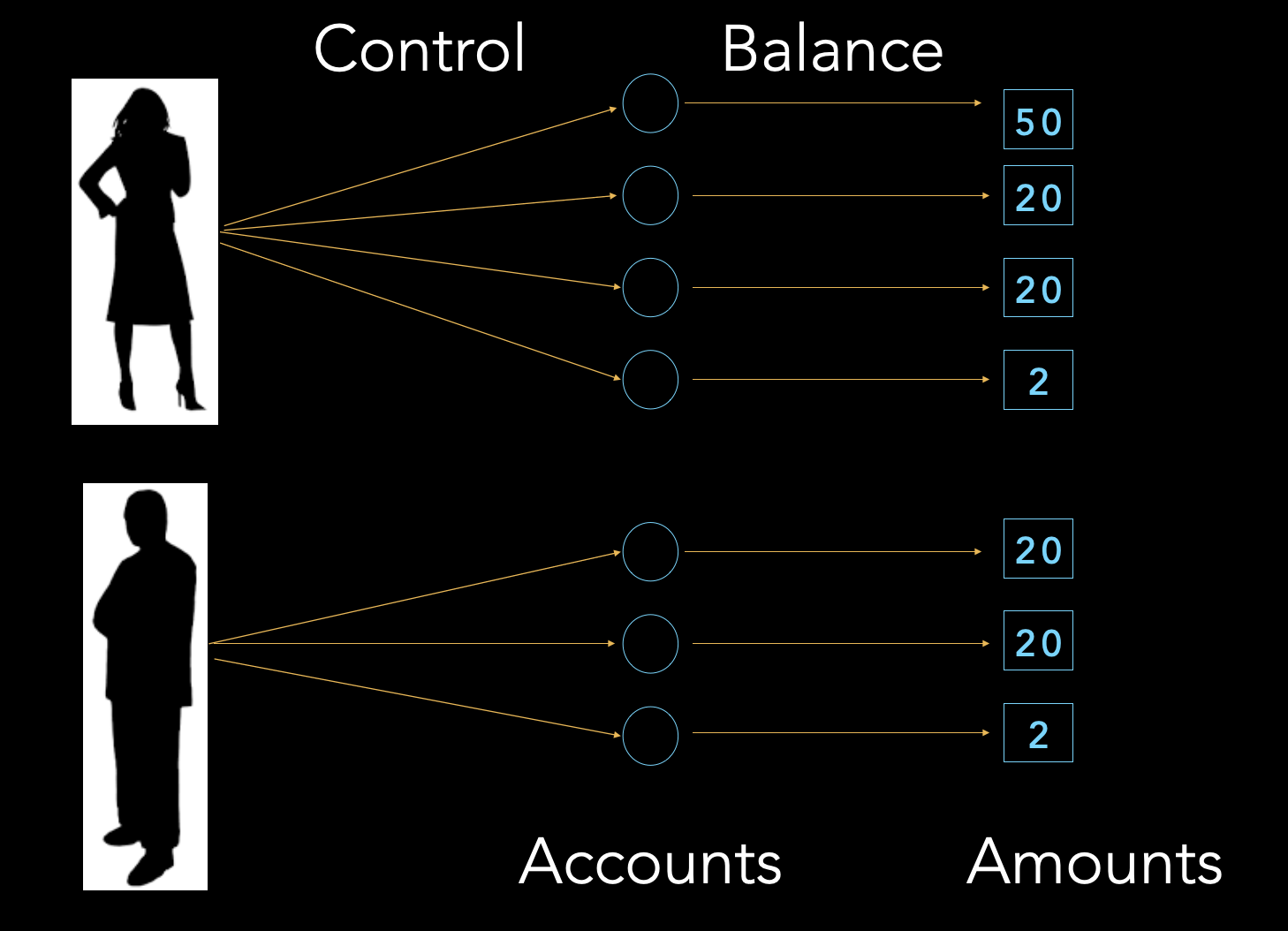

Bank money

For bank money, the resource identifiers are account numbers, which are mapped to their balances. The account numbers are partitioned into subsets, where each is stored and managed by a separate bank. Agents exercise control over the accounts by authorizing the bank managing them to transfer an amount to another account. For example, in Figure 2.2, Alice controls (has) 4 bank accounts (they could be in different banks or in the same bank), with account balances of DKK 50, 20, 20 and 2, respectively. The control map is not particularly private. Nowadays, a bank is required to know which accounts are controlled by which person or company, and it can be compelled to disclose this information to others, notably law enforcement. A bank does not nor need not know who controls the bank accounts in other banks.

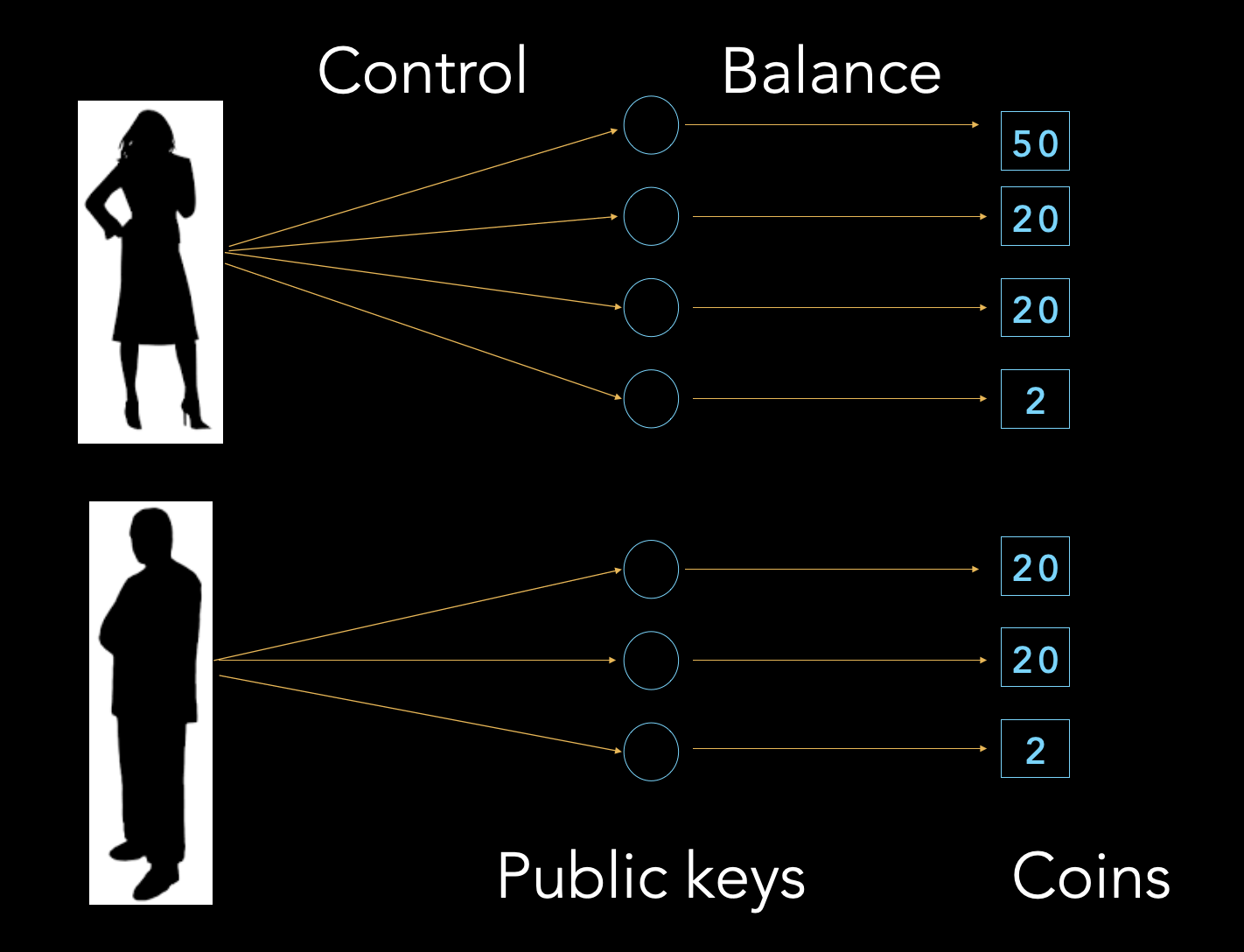

Cryptocurrency

For cryptocurrency (blockchain-hosted currency), the resource identifiers are addresses corresponding to public keys, which are mapped to their balances (Ethereum) or sets of UTxOs, where each UTxO has a fixed balance (Bitcoin). Addresses are equivalent to account numbers in a bank. Agents exercise control over addresses by a digital signature: providing proof of knowledge of a secret private key corresponding to the public key, without effectively revealing the private key itself or anything else about it. The control map is private, as for physical cash. The balance map is completely public, however: every agent anywhere has access to it in its entirety at any time. For example, in Figure 2.3, Alice has 4 private keys, each corresponding to a separate public key and thus to a unique address. The balances of the 4 addresses are 50, 20, 20 and 2 Ether, respectively (Ethereum); or one UTxO each that asserts ownership (“pay to pub key hash”) of 50, 20, 20 and 2 BTC, respectively (Bitcoin).

Functionally, Bitcoin and Ethereum can each be thought of as a bank that offers numbered accounts, where nobody at the bank conducts a KYC check and no documentation as to the origin of the funds is required, but all account transfers, that is updates to the balance map, are posted publicly, in contrast to banks, which are expected to do the opposite: keep transfers and balances private, with the notable exception that bank employees and systems have access to them.

In contrast to Bitcoin, Ether and similar blockchain-based cryptocurrencies with public transaction ledgers, some blockchain systems additionally seek to achieve complete transaction privacy of cryptocurrency transactions. This corresponds to a virtual bank that offers numbered accounts, has no idea about who controls them, and validates and performs encrypted money transfers in a secure enclave of its computer system such that nobody, not even at the bank, knows or can deduce which accounts and how much money is involved in a transaction or even what the balances of its accounts are. The aforementioned computer system is virtual in blockchain systems: it is a decentralized peer-to-peer network implementing a replicated state machine that collectively acts as if it where a 1960s mainframe computer that executes single-threaded programs only, in batch mode, additionally employing various cryptographic techniques such as zero-knowledge proofs to keep information private even inside the network.111A zero-knowledge proof of a statement such as “No money has been duplicated or lost in the transactions so far” is a proof that is convincing to a rational – and mathematically inclined – observer without disclosing any additional, effectively usable information to the observer but the veracity of the statement.

If a bank with no knowledge about their account owners’ identities, performing transfers blindly and retaining no information about them sounds outrageously in conflict with banks collecting and storing extraordinary amounts of private and confidential information about individuals and companies to satisfy KYC, AML, CTF and other legislation, it is worth pointing out that Physical Cash, the (real-world) locations of physical cash around wherever it is, can be considered to be such a zero-knowledge bank. And it is – still – legal in all known jurisdictions. With physical cash there is no real-world bank, a private company with employees and computer systems under its direction, that is required and entitled to get detailed information from the account owners (cash owners), it is the account owners themselves who are responsible for providing information about their identity, storing relevant transactions and providing additional documentation in evidence of origin of funds and compliance with legislation to surrender it directly, without detour through a private third party, to law enforcement agencies on a concrete need-to-know basis.

2.3 Transfers

The effect of a resource transfer is to update the resource ownership state such that the ownership has changed, but the sum total of resources remains the same.

Having decomposed ownership into control and balance, there are two fundamental ways of achieving a transfer.

-

•

Control-based: transfer of control.

-

•

Balance-based: transfer of balance.

In Figure 2.4, Bob transfers 20 units of a currency to Alice in one of two ways. In the account-based transfer, only the balance map is updated: balance of one of the resource identifiers he controls is decreased by 20 and the balance of one of Alice’s resource identifiers is increased by 20. In the control-based transfer, only the control map is updated: Bob transfers control of one of his resource identifiers, which has a balance of 20, to Alice.

If only control transfers are possible, then the balance of a resource pointer is fixed. Such a resource identifier can only be created with a fixed balance and eventually retired in its entirety; it is a token.

2.4 Token-based versus account-based money

Money and other resource (asset) transfers can happen control-based or balance-based; be maximally public (all agents can see them), maximally private (only the transfer agents can see them) or 3d-party-visible (a designated agent such as the bank maintaining an account system can see them); and occur in a system with centralized or decentralized governance.

Specific combinations are often taken as the point of departure in discussions on currency: token-based money (physical cash) and account-based money (bank money stored in a database system); see Table 2.1. They can be freely combined, however: Asset transfer granularity/fungibility, privacy level and governance/distribution can in principle be designed and implemented and thus tuned to whichever requirements one has in mind. Discussions on central bank digital currency (CBDC) need not and should not be limited by restricting assumptions about CBDC hosted on a decentralized system necessarily requiring a UTxO-model, by an account-based system necessarily having centralized governance, awarding helicopter money or paying interest requiring a database system, etc.

For example, popular cryptocurrencies have already added some additional combinations: Unspent transaction outputs (UTxO); accounts with public balance-based transfers; fungible (balance-based) and nonfungible (control-based) publicly transferable tokens. See Table 2.1 with examples.

The relation between account-based and token-based money can be made precise by algebraic resource accounting (Torres Garcia, 2020).

| Asset transfer type | Transfer | Privacy | Governance | ||||

| control | balance | publ. | 3d party | priv. | centr. | decentr. | |

| Account-based | ✓ | ✓ | ✓ | ||||

| Token-based | ✓ | ✓ | ✓ | ||||

| UTxO (Bitcoin) | ✓ | ✓ | ✓ | ||||

| Account balance (Ether) | ✓ | ✓ | ✓ | ||||

| Fungible tokens (ERC-20) | ✓ | ✓ | ✓ | ||||

| Nonfung. tokens (ERC-721) | ✓ | ✓ | ✓ | ||||

| Digital cash | ✓ | ✓ | ✓ | ||||

Chapter 3 Digital cash

Fritz Henglein

In Section 2.4 we discussed the most common forms of combining control and balance as a framework for describing how money is stored and transferred: token-based and account-based money.

Intuitively, account-based money is more fungible. It is like token-based money with the resource identifier removed. It is analogous to removing the serial numbers from banknotes and going one step further: treating any set of banknotes as completely indistinguishable from a single unnumbered banknote that carries the sum of their values. It is only the sum that can be observed. There is no way of distinguishing a “collection” of money from any other collection with the same amount: the collection immediately melts into its sum, the balance. This maximal level of fungibility—complete indistinguishability—is the essence of account-based money, money per se: money is money, $50 is $50, no matter what the history of money transactions is or into how many units (bills, coins, tokens) the amount is partitioned. In particular, money should not come with a history of transactions that is inextricably attached to it. Such histories make differences between money with the same face value observable and thus may give them different exchange value. A bitcoin used in a ransomware attack is not worth as much as a newly minted bitcoin, compromising its unit-of-account and medium-of-exchange properties.111A bitcoin is effectively a nonfungible token. There are multiple reasons why Bitcoin can be considered money-like, but not money: it is expensive and slow to produce due to mining costs and timing (it is essentially a non-consumable commodity with high production costs), in contrast to cheaply produced fiat money; it is not a stable store of value since it has a built-in deflationary issuance policy, which is furthermore not tied to economic production for stability; it is not a unit of account and is not one-for-one interchangeable, since bitcoins have observable histories, which impacts their exchange value.

Account-based money has practical advantages over token-based money. Changing a set of tokens (or UTxOs) into another one with the same total amount is automatic and built-in in account-based money; it does not require a transaction, as in token-based money. A large set of transfers can be replaced by another set with the same effect, as in netting when a set of transfers amongst two or more parties are consolidated into net flows between them. Nobody can complain about doing that with fungible money since all sets of transfers with the same net effect are in principle identical: there are no tokens with observable and trackable identities.222Access to a transaction history still reveals a lot, of course, even if the money per se is fully fungible. This is analogous to a cash coin, by itself, being indistinguishable from other cash coins and providing no information where it came from. A transaction history contains the fungible money involved, but fungible money by itself does not point back to transactions. In particular, fungible money exists by itself, without any transactions attached to or accessible from it. In contrast, netting UTxO- or NFT-based payments may lead to complaints: Receiving a bitcoin that has previously been involved in a ransomware attack instead of a “clean” one with the same amount may have different value (and consequences) for its recipient.

3.1 Digital cash criteria

We stipulate that ideal digital cash should be

-

•

sovereign fiat money (not private bank money), that is not an IOU that can become worthless because the issuer refuses to or cannot redeem it;

-

•

maximally fungible, that is account-based money;

-

•

transferred with maximal privacy, without transaction histories attached;

-

•

be under its owner’s direct control, without requiring cooperation by a designated third party (bank or e-money account provider); and

-

•

have decentralized governance, without a priori designated agents that have privileged access to balances and control of transfers.

See the bottom line of Table 2.1.

Ideal digital cash emulates physical cash, with two notable differences: It is account-based (not partitioned into tokens, like coins and bills), and it is in principle transferable in arbitrary amounts near-instantaneously and over arbitrary long distances. Does this mean that a particular digital cash design must admit these properties? Of course not. Being freed from the inherent limitations of physical cash is to make different designs of digital cash with particular restrictions possible. Different designs may be mutually exclusive and may have different objectives, depending on the jurisdiction333or anarcho-libertarian community.

For example, in one digital cash design all transactions might be public (as in most blockchain systems); in another transfers up to some small amount could be completely private, large transfers disclosed or disclosable to a regulatory body, and transfer settlement time could depend on the size of the transfers (the bigger the amount, the slower settlement); in yet another, transfers could be restricted to legal entities registered in a certain jurisdiction; etc.

These are (money) policy and (system) governance questions that should ideally be kept separate from (technical) distributed systems design and implementation to ensure that existing systems and their proponents do not unduly influence policy and governance desiderata. Which kinds of digital cash do we, say in Denmark, want, is likely quite different from, say, Ukraine. How private, how limited, which amounts, how much slowed down, monitored by whom under which legal authority and under which circumstances, with or without support for helicopter money, with or without support for dynamic amount adjustments (interest)? How are they governed – who decides what about the properties of the particular digital cash design, and who has access to which information under which circumstances? And only then: How do you build a (distributed) system that delivers this within the limits of what is theoretically and practically possible in distributed computing, cryptography, hardware design, verified programming?

Depending on particular desiderata, the digital cash could be hosted on and operated by a secure distributed system with privileged/centralized IT-governance, e.g. by a trusted cloud system provider; a decentralized system whose nodes are operated by an open or closed association (DLT, permissioned blockchain); a decentralized system with no authentication (permissionless blockchain); or combinations of those.

Ideally, distributed systems design and implementation should depend on and be driven by policy and governance desiderata, not conversely. The design space of distributed systems is far from exhausted by existing centralized RDBMS- and decentralized peer-to-peer, blockchain- or DLT-based systems.

3.2 Digital cash and banks

We have already noted that private banks are put into the somewhat peculiar—privileged and precarious—position of requiring their customers to provide confidential information that is relevant for investigating, ensuring and enforcing that the customers abide by legislation: paying their taxes, not laundering money, not funding criminal or terrorist operations. These are the customers’ obligations vis a vis government institutions put in charge of law enforcement. Why are banks, as private enterprises that are primarily responsible to their shareholders, in the middle of this?

The disassociation of digital cash from bank money and bank transactions makes it possible to deconstruct bank services. A bank can still act as appointed custodian for customers to provide a trustworthy transaction record and support a customer in providing evidence of source of funds, recipients of funds, etc., to law enforcement agencies. After all, banks enjoy much higher trustworthiness for carefully recording and not tampering with customer transactions than the average customer herself. But trustworthy, tamper-proof recording that holds up to the scrutiny of law enforcement agencies is no longer out of reach for common customers: Cryptographically secured immutable document structures (Haber and Stornetta, 1990) have been popularized and made publicly available by blockchain and peer-to-peer systems (Benet, 2014). Distilling money into digital cash rather than taking bank money and its stored bank ledgers as the given, the customer who is ultimately responsible for abiding by the law can delegate secure and tamper-proof recording to any trustworthy party or system, without necessarily giving the bank that performs the transfers access to that information and thus without making the bank co-culpable in case the customer does something fishy.

Banks are likely to remain the go-to agents as custodians of digital cash and/or tamper-proof record keeping for their customers, since they can provide multiple economic benefits for the customer, even without having to rely on the de-facto legal monopoly to access private and confidential customer information they have been given by KYC, AML and CTF legislation. In particular, they can still borrow from their customers by offering them deposit accounts, in addition to digital cash storage accounts that are fully backed by central bank reserves. And they can continue issuing their own bank money, providing their signature expertise of creditworthiness assessment and aggregated credit risk management, and fullfilling their core economic role: Providing inside money (credit money) for facilitating productive economic activities—bank loans.

Digital cash is about providing direct, equitable, private access to secure (default-free, for any amount) fiat money, in analogy to physical cash. These supplement loans to a bank in the form of deposit accounts, not replace them.

3.3 Digital cash in the real world

Does digital cash exist? Not in its ideal form, where it corresponds to physical cash “on speed”: secure (no counterparty risk), fully fungible (not discernible from other people’s money), directly controlled (no requirement of intermediary), transferred privately (no built-in disclosure to a third party), very fast over any (geographic or jurisdictional) distance (unless explicitly limited according to a specific policy).

Arguably the most important aspect of digital cash is its security, its owner being protected against selective default by a counterparty. Modern bank money provides speed and low transaction costs, but is typically not secure since a private bank may default without the entire banking system defaulting. Thus there is a risk that somebody’s money can suddenly be worth a lot less than somebody else’s, even if they had the same amount beforehand.444This is in contrast to severe inflation or the collapse of a central bank, where the value of everybody’s money is devalued equally, rather than selectively.

This is not a theoretical risk. As we have noted previously, fractional reserve banking has essentially two equilibria. Most of the time it works as desired, but occasionally it goes into a bank run phase where customers run to try to extract as much of their deposits before they are depleted and the bank defaults. Such defaults have been frequent prior to the advent of central-bank fiat money; they are still quite common, most recently in connection with the global financial crisis of 2008, in the aftermath of which a number of banks, including Danish ones, defaulted.

Some countries offer de facto secure bank money to individuals and companies. For example, the Postal Bank of Japan is majority-owned by the State of Japan, which essentially extends the State’s non-default guarantee to the Postal Bank and thus to its depositors, for any amount of money deposited. PostFinance in Switzerland does not issue credit money; it is required to have full reserves for its deposits in the form of cash reservers at the Swiss National Bank and extremely high quality Swiss government bonds, which guarantees that deposits are fully backed by central bank money and the full faith and trust in the Swiss government and its ability to collect taxes.

These de facto full-reserve banks safely store money for their customers rather than borrow it since they don’t create credit money that gets the same status as the money in their customers’ deposit accounts. There is little historical evidence to suggest that access by individuals and businesses to secure (fully backed) digital money carries the risk of outcompeting private banks and causing a sudden outflow of deposits. To the contrary, private banks have proven to do quite well in competition with secure state banks. For example, Denmark does no longer have a bank that provides secure storage of digital money to individuals and non-bank businesses for nontrivial amounts of money. Only the Danish banks themselves have that access.

3.4 The need for transactional money

Many discussions of digital forms of money focus on transfers, that is reliably getting money from A to B. Secure, reliable and efficient transfers are key for the fundamental functionality of money: if you cannot transfer it, it cannot serve as a medium of exchange. Despite vast numbers of people still being without any access to digital money or only to semi-automated (and thus costly) ways of effecting transfers, this is arguably a largely solved problem with bank money. In many parts of the world, it can be done conveniently by credit card, debit card, app-based (mobile pay), account-to-account bank transfers (via SEPA, SWIFT, Fedwire messaging combined with interbank credits, clearing houses and central bank settlement), or non-bank account transfers (in centralized database systems managed by e-money account providers such as WeChat, Alipay, Revolut); ever more, faster and cheaper transfer solutions are arriving. So, is “digital money” a solved problem?

Providing secure execution of individual transfers in isolation of each other misses the key challenge. Money transfers occur invariably in connection with other events; they are payments for something. Any theory of money is based on economic resource exchanges: money is not a medium of transfer, but a medium of exchange.

In Section 1 the primitive operation is a two-party exchange of (economic) resources, upon which everything else is built. Such an exchange comprises two transfers, one from A to B and the other from B to A. Such an exchange must be an atomic transaction: One transfer happens if and only if the other transfer happens. Putting this contrapositively, if A doesn’t transfer her resource to B, then B does not transfer his resource to A either; or he assuredly gets it back if he has already done so.

Efficiently transferrable digital money is not enough; digital money needs to be efficiently transactional since its very purpose is facilitating exchanges, atomic transactions comprising multiple transfers where at least one of them is a money transfer and the other ones will typically be transfers of other economic resources, typically physical goods and services. The fact that there are still vast amounts of losses due to one party delivering something and the other one not paying for it or the other way round suggests that this is not a solved problem.

3.5 Digital contracts

A contract is an agreement between at least two distinct agents that commits them to a course of action involving multiple events such as transfers of money and other resources.555We refrain from a legal or historical analysis of the concept of contract since we only want to highlight the importance of treating a set of events collectively, not only each event in isolation. A digital contract is a formally specified contract where both data and logic are rigorously specified with mathematical or programmatic precision.666Not to be confused with natural language document templates where only the data and/or the revision and signature process is digitalized.

An exchange contract is a simple kind of bilateral contract requiring two transfers of resources, where one agent gives something to another in return for receiving something of comparable value from the other. In Section 1 we have seen a number of more complex contracts arise, in particular financial contracts (money-now for money-later) such as loans, with and without collateralization. In general, a contract can involve a considerable number of resources, events and agents with obligations, permissions and prohibitions whose conditions stretch over a long period of time. Examples are bonds, insurance and pension contracts, or complex commercial contracts such as the staged delivery of a cement factory involving production, transportation, trading, inspection of goods and processes, etc, with multiple options, penalties, etc. In general, a contract may specify many alternative acceptable executions (sequences of events) of varying lengths.

3.5.1 Managing contracts

A contract is a passive object, analogous to a rule book or protocol. A contract executes itself as much as the paper it is written on: Not at all. Apart from the contract parties the execution of a contract draws on additional agents.

-

•

Contract managers: virtual or real third parties the contract parties have agreed on that inform the contract parties of contract events and determine whether actions are in accordance with the contract or not. These often take the form of a virtual (conceptual) third party consisting of the contract parties themselves communicating with each other, plus a contractually specified court to resolve disagreements.

-

•

Transaction managers: real or virtual third parties that guarantee that resource exchanges happen atomically, as in payment-versus-delivery in financial instrument trading. Typically this is done by banks, notaries, central counterparties, security depositories or similar that collectively serve as escrow agents and guarantors of atomic exchange execution.

-

•

Resource managers: real or virtual third parties that are used to determine legal ownership of certain resources and authoritatively perform transfers of these resources. Examples are banks for (bank) money, public authorities for land registries, central security depositories for securities.

A digital contract is a formal specification of a contract as rule book or protocol, analogous to a (behavioral) type or an interface specification in a programming language; in particular, it does not execute itself.

A contract manager for a digital contract is a mechanism777hardware/software system that monitors and validates that a contract action such as a transfer is in accordance with what the contract allows or stipulates. It signals when a contract is successfully completed, manifestly breached (cannot be completed to a successful sequence of events) or is still live (neither terminated nor manifestly breached) and in which state it is.

A transaction manager for a (sub)contract (including but not limited to exchange contracts such as payment-versus-delivery) is a mechanism that guarantees that

-

•

either an acceptable path in accordance with the mathematical semantics of the digital contract is executed to completion (commit);

-

•

or, if it does not complete, all resource transfers already performed are effectively undone or compensated for such that the net effect of the failed contract execution is equivalent to no resource transfers having occurred (abort).

A transaction manager for an exchange contract thus guarantees that the two transfers either happen and are finalized (committed) or that none of them have effect (aborted). This ensures a modicum of fairness: something-for-something or nothing-for-nothing, preventing something-for-nothing breaches. A stronger requirement would be that the contract succeeds for the agent(s) who correctly perform(s) their part of the contract even if some counterparty fails to do so. This is what a central counterparty typically provides in an exchange contract by interposing itself as benevolent man in the middle between the two exchange agents.