Combinatorial Civic Crowdfunding with Budgeted Agents: Welfare Optimality at Equilibrium and Optimal Deviation ††thanks: To appear in the Proceedings of the Thirty-Seventh AAAI Conference on Artificial Intelligence (AAAI ’23). A preliminary version of this paper titled “Welfare Optimal Combinatorial Civic Crowdfunding with Budgeted Agents” also appeared at GAIW@AAMAS ’22.

Abstract

Civic Crowdfunding (CC) uses the “power of the crowd” to garner contributions towards public projects. As these projects are non-excludable, agents may prefer to “free-ride,” resulting in the project not being funded. For single project CC, researchers propose to provide refunds to incentivize agents to contribute, thereby guaranteeing the project’s funding. These funding guarantees are applicable only when agents have an unlimited budget. This work focuses on a combinatorial setting, where multiple projects are available for CC and agents have a limited budget. We study certain specific conditions where funding can be guaranteed. Further, funding the optimal social welfare subset of projects is desirable when every available project cannot be funded due to budget restrictions. We prove the impossibility of achieving optimal welfare at equilibrium for any monotone refund scheme. We then study different heuristics that the agents can use to contribute to the projects in practice. Through simulations, we demonstrate the heuristics’ performance as the average-case trade-off between welfare obtained and agent utility.

Keywords Civic Crowdfunding Nash Equilibrium Social Welfare

1 Introduction

Local communities often find it beneficial to elicit contributions from their members for public good projects. E.g., the construction of markets, playgrounds, and libraries, among others [1]. These goods provide the local community with social amenities, generating social welfare. This process of generating funds from members towards community services is referred to as Civic Crowdfunding (CC). CC is instrumental in changing the interaction between local governments and communities. It empowers citizens by allowing participation in the design and planning of public good projects [2]. Such democratization of public projects has led CC to become an active area of research [3, 4, 5, 6, 7, 8]. Moreover, introduction of web-based CC platforms [9, 10] has added to its popularity.

As depicted in Figure 1, typically, multiple projects are simultaneously available for CC. We refer to CC for multiple projects as combinatorial CC. Formally, CC comprises strategic agents who observe their valuations for the available public projects. Each project has a known target cost and deadline. Each agent contributes to the available projects as per its valuations and within its budget. The agent valuations are such that the overall sum is greater than the project’s target cost, i.e., there is enough valuation (interest) for the project’s funding. A project is funded when the agents’ total contribution meets the target cost within the deadline. When funded, each agent obtains a quasi-linear utility equivalent to its valuation for the project minus its contribution. In turn, the community generates social welfare – the difference in the project’s total valuation and cost.

Free-riding.

The primary challenge in CC is due to the non-excludability of the public projects. That is, the citizens can avail a project’s benefit without contributing to its funding. Consequently, strategic agents may free-ride and merely wait for others to fund the project. When the majority decides to free-ride, the project remains unfunded despite sufficient interest in its funding [11]. To persuade strategic agents to contribute, researchers propose to provide additional incentives to them in the form of refunds.

Refunds.

Zubrickas [12] presents PPR, Provision Point Mechanism with Refunds, which employs the first such refund scheme. PPR assumes that a central planner keeps some refund budget aside. If the project is not funded, the planner returns the agent’s contribution and an additional refund proportional to the agent’s contribution. The refund scheme incentivizes the agents to increase their contribution to obtain a greater refund. The characteristic of the resulting game is that the public project is funded at equilibrium. However, PPR and subsequent works ([13] and references cited therein) assume that agents have an unlimited individual budget; in reality, the agents may have a limited budget. To this end, we aim to determine the funding guarantees for a subset of public projects that maximize social welfare within the available budget.

Our Approach and Contributions

This paper lays the theoretical foundation for combinatorial CC with budgeted agents. Table 1 presents the overview of our results, described in detail next.

Budget Surplus (BS). We first study the seemingly straightforward case of Budget Surplus, i.e., the overall budget across the agents is more than the projects’ total cost. For this, it is welfare optimal to fund all the projects. Despite the surplus budget, we show that the projects’ funding cannot be guaranteed at equilibrium (Theorem 2 and Corollary 1).

Subset Feasibility (SF). We observe that the budget distribution among the agents plays a significant role in deciding the funding status of the projects. Conditioning on the budget distribution, we introduce Subset Feasibility of a given subset of projects. We prove that Subset Feasibility coupled with Budget Surplus guarantees funding of every available project at equilibrium (Theorem 3), thereby generating the maximum possible social welfare.

Budget Deficit (BD). Trivially, in the case of Budget Deficit – when there is no Budget Surplus – one can only fund a subset of projects. It may be desirable that such a subset is welfare-maximizing within the budget. We refer to the funding of the socially welfare optimal subset at equilibrium as socially efficient equilibrium. For this case, we present the following results.

First, we show that, in general, achieving socially efficient equilibrium is impossible for any refund scheme (Example 1). Next, we prove that even with the stronger assumption of Subset Feasibility, it is still impossible to achieve socially efficient equilibrium (Theorem 4). Specifically, we prove that strategic deviations may exist for agents such that the optimal welfare subset remains unfunded. We then show that it is NP-Hard for an agent to find its optimal deviation, given the contributions of all the other agents (Theorem 6 and Corollary 2). Due to Theorem 4 and hardness of optimal deviation (Theorem 6), we construct five heuristics for the agent’s contributions and empirically study their social welfare and agent utility through simulations (Section 6).

Property Socially Efficient Equilibrium Budget Surplus ✗ (Corollary 1) Budget Surplus + Subset Feasibility ✓ (Theorem 3) Budget Deficit + Subset Feasibility ✗ (Theorem 4)

2 Related Work

Several works study the effect of agents’ contribution to public projects [6, 14, 15, 16]. One way of modelling agent contribution is using Cost Sharing Mechanisms (CSMs) in CC [17]. More concretely, CSMs focus on sharing the cost among the strategic agents to ensure that an efficient set of projects are funded [17, 18, 19, 20, 21]. The authors in [6, 22] model CSMs for non-excludable public projects and provide agent contributions that ensure specific desirable properties, e.g., individual rationality and strategy-proofness. However, these works do not guarantee funding at equilibrium since agents are strategic and CSMs do not offer refunds.

In another line of work, funding of public projects is modeled as Participatory Budgeting (PB) [23]. Brandl et al. [16] study a model without targets costs and without quasi-linear utilities, applicable for making donations to long-term projects. Generally, in the PB literature, the utility of an agent is determined by the number of projects funded or the costs of the projects (e.g., [24, 25]), whereas in CC, it is the difference between the agent’s valuation and contribution. Aziz et al. [26] consider a PB model with budget constraints and quasi-linear utilities when the project is funded. The authors prove the impossibility of finding an approximation to welfare optimal funded subset of projects which also ensure weak participation, i.e., positive utility to all agents. However, they do not assume strategic agents.

For excludable public projects, Soundy et al. [15] focus on effort allocation by strategic agents towards the project’s completion. Contrarily, we focus on funding guarantees of non-excludable public projects with strategic agents.

CC with Refunds.

In the seminal work, Bagnoli and Lipman [27] present Provision Point Mechanism (PPM) for single project CC, without refunds. Consequently, PPM consists of several inefficient equilibria [27, 28]. Agents may also free-ride since the projects are non-excludable [11]. To overcome such limitations, Zubrickas [12] presents PPR, a novel mechanism that offers refunds proportional to contributions. Based on the attractive properties of PPR, other works propose different refund schemes for different agent models and strategy space [13, 29, 30, 31]. However, these works only focus on a single project with agents having unlimited budgets.

Among recent works, Padala et al. [32] attempt to learn equilibrium contributions when agents have a limited budget in combinatorial CC using Reinforcement Learning. However, the work does not provide any funding guarantees – welfare or otherwise – for the projects.

Chen et al. [14] analyze the existence of cooperative Nash Equilibrium for funding a single public project using ‘external investments.’ Their work considers agents to have binary contributions, unlike our setting, where agent contributions are in . Moreover, in their utility structure, agents receive a fixed fraction of the total contribution when the project is funded; otherwise, their contribution is returned. That is, they do not model agent valuations.

We remark that while our work is motivated by the existing CC literature, it remains fundamentally different. To the best of our knowledge, we are the first to study the funding guarantees for combinatorial CC with budgeted agents. We also focus on an agent’s equilibrium behavior and study the hardness of the optimal strategy for the agents.

3 Preliminaries

This section presents our CC model and important definitions. We also summarize PPR for the single project case.

3.1 Combinatorial CC Model

Let be the set of projects to be crowdfunded with target costs . Let denote the set of agents interested in contributing to all projects. We consider a limited budget for each agent . Each agent has a private valuation for the project , denoted by . We consider additive valuations, i.e., an agent has a value of for a funded subset . Let denote the total valuation in the system for the project . An agent contributes to project , s.t., . The total contribution towards a project is denoted by . The project is funded if by the deadline, and each agent gets the funded utility of . If the project is unfunded , the agents are returned their contributions and in some mechanisms, additional refunds, as defined later.

Welfare Optimal.

Ideally, when there is limited budget, it may be desirable to fund welfare optimal subset defined as follows. Note that, the welfare obtained from project if funded is and zero otherwise [33, 34]111All the results presented in this paper also hold if .

Definition 1 (Welfare Optimal).

A set of projects is welfare optimal if it maximizes social welfare under the available budget, i.e.,

| (1) |

We make the following observations based on Definition 1.

-

•

Finding requires public knowledge of s, s and the value . Contrary to the PB or CSM literature, the aggregate valuation is assumed to be public knowledge in the CC literature [12, 29]. Similarly, we also assume that the overall budget in the system is public knowledge. This may be done by deriving the overall budget by aggregating citizen interest [35, 36].

-

•

Computing is NP-Hard as it can be trivially reduced from the KNAPSACK problem. However, note that our primary results focus on ’s funding guarantees at equilibrium (and not actually computing it). Moreover, computing may also not be a deal breaker as the number of simultaneous projects available will not be arbitrarily large. One may also employ FPTAS [37].

Refund Scheme.

We define the refund scheme for each project as s.t. is agent ’s refund share for contributing to project . The overall budget for the refund bonus is public knowledge. Typically, if a project is unfunded, the agents receive , and zero refund otherwise. The total refunds distributed for project can be such that (e.g., [12]) or (e.g., [29, 13]). Throughout the paper, we assume that .

The CC literature also assumes that is anonymous, i.e., refund share is independent of agent identity. Further, consider the following condition for a refund scheme, assuming is differentiable w.r.t. .

Condition 1 (Contribution Monotonicity (CM) [13]).

A refund scheme satisfies Contribution Monotonicity (CM) if it is strictly monotonically increasing with respect to the contribution , i.e.,

3.2 Agent Utilities and Important Definitions

Let define a general combinatorial CC game. In this, the overall agent utility can be defined as.

Definition 2 (Agent Utility).

Given an instance of , with agents having valuations and contributions , the utility of an agent for each project is given by

where is an indicator variable, such that if is true and zero otherwise.

An agent ’s utility for project is either when is funded, and otherwise. Let denote the total utility an agent derives, i.e., . This incentive structure induces a game among the agents. As the agents are strategic, each agent aims to provide contributions that maximizes its utility. As such, we focus on contributions which follow pure strategy Nash equilibrium.

Definition 3 (Pure Strategy Nash Equilibrium (PSNE)).

A contribution profile is said to be Pure Strategy Nash equilibrium (PSNE) if, ,

where is the contribution of all agents except agent .

Efficacy of PSNE Contributions. PSNE is the standard choice of solution concept in CC literature [12, 13, 29, 30]. Zubrickas [12] shows that for an appropriate refund bonus (see Eq. 3), their PSNE strategies are the unique equilibrium of the mechanism. Moreover, Cason and Zubrickas [38] empirically validate the effectiveness of these PSNE strategies using real-world experiments.

Given the contributions , we can compute the set of the projects that are funded and unfunded at equilibrium. Throughout the paper, we refer to the funding of at equilibrium as socially efficient equilibrium. We next define budget surplus.

Definition 4 (Budget Surplus (BS)).

There is enough overall budget to fund each project , i.e., .

We refer to the scenario as Budget Deficit (BD). In CC literature, it is also natural to assume that [12]. That is, there is sufficient interest in each available project’s funding. Hence, when there is surplus budget, it is optimal to fund all the projects, i.e., .

Further, we assume that agents do not have any additional information about the funding of the public projects. This assumption implies that their belief towards the projects’ funding is symmetric. This is a standard assumption in CC literature [12, 13].

3.3 Single Project Civic Crowdfunding

Provision Point Mechanism with Refunds (PPR)

. For single project CC, i.e., , Zubrickas [12] proposes PPR which employs the following refund scheme ,

| (2) |

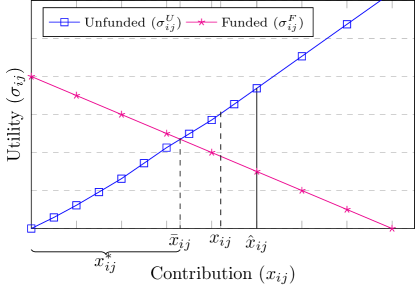

Each agent ’s equilibrium contributions are defined such that its funded utility is greater than or equal to its unfunded utility, i.e., . We depict such a situation with Figure 2. The author shows that the project is funded at equilibrium222In other words, the introduction of refunds results in the funding of the public project being the unique Nash equilibrium of the game when . That is, “bad” Nash equilibria where the project is not funded are filtered out. when , and that it is PSNE for each agent to contribute or the amount left to fund the project, whichever is minimum. More formally,

Theorem 1 ([12]).

In PPR, with and , the set of PSNEs are if , where . Otherwise, the set is empty.

We have as the upper-bound of the equilibrium contribution, . In PPR, the PSNE strategies in Theorem 1 are the unique equilibrium of the game when,

| (3) |

Funding Guarantees.

For single project CC, Damle et al. [13] show that the project is funded at equilibrium for any refund scheme that satisfies Condition 1. Trivially, one may observe that the refund scheme in PPR, i.e., , , also satisfies Condition 1. Damle et al. [13] propose other refund schemes which satisfy Condition 1 and are exponential or polynomial in . We remark that our results hold for any refund scheme satisfying Condition 1.

4 Funding Guarantees for Combinatorial CC under Budget Surplus

For CC under Budget Surplus (Def. 4) sufficient overall budget exists to fund all the projects. Theorem 2 shows that despite the sufficient budget, projects may not get funded as the set of equilibrium contributions for an agent may not exist. Unlike Theorem 1, agents may not have well-defined contributions satisfying PSNE. The non-existence results due to the uneven distribution of budget among the agents. Hence, agents with higher budgets exploit the mechanism to obtain higher refunds while ensuring the projects remain unfunded.

Theorem 2.

Proof.

Consider projects and agents s.t. Def. 4 is satisfied, i.e., . We can easily construct game instances where there exists non-empty s.t. . To satisfy Budget Surplus (Def. 4), must have enough budget so that the agents in can fund all the projects.

Each agent receives a funded utility for contributing towards project . That is, as . The agent may also receive an unfunded utility of for project . Since is monotonically increasing (Condition 1), . We depict this scenario with Figure 2. Observe that and intersect at the upper-bound of the equilibrium contribution, (Theorem 1), where . For any , . The rest of the proof (see Appendix A.1) shows that s.t. which in turn is not possible at equilibrium due to discontinuous utility structure at . ∎

Observe that if any project is funded at equilibrium then the equilibrium set can not be empty, contradicting Theorem 2. Corollary 1 captures this observation.

Corollary 1.

With Corollary 1, we prove that Budget Surplus is not sufficient to fund every project at equilibrium. To this end, we next identify the sufficient condition to ensure the funding of every project, under Budget Surplus.

Subset Feasibility

With and in Theorem 2’s proof, we assume a specific distribution on agents’ budget. To resolve this, we introduce Subset Feasibility which assumes a restriction on each agent’s budget distribution. Informally, if each agent has enough budget to contribute (see Figure 2) for , , then Subset Feasibility is satisfied for . Formally,

Definition 5 (Subset Feasibility for (SFM)).

Claim 1.

Given any whose equilibrium contributions satisfy , we have SFP BS.

Claim 1 follows from trivial manipulation (see Appendix A.2). Similarly, we have BS SFP. From Claim 1, it is welfare optimal to fund every available project under . Theorem 3 indeed proves that under SFP each project gets funded at equilibrium, thereby generating optimal social welfare. The formal proof is available in Appendix A.3.

Theorem 3.

Given and satisfying CM (Condition 1) such that is satisfied, at equilibrium all the projects are funded, i.e., if . Further, the set of PSNEs are:

.

Theorem 3 implies that, under SFP, the socially efficient equilibrium (with ) is achieved. Intuitively, under SFP combinatorial CC collapses to simultaneous single projects; and thus, we can provide closed-form equilibrium contributions. However, SFP is a strong assumption and, in general, may not be satisfied. In fact, the weaker notion of Budget Surplus itself may not always apply. Therefore, we next study combinatorial CC with Budget Deficit.

5 Impossibility of Achieving Socially Efficient Equilibrium for Combinatorial CC under Budget Deficit

We now focus on the scenario when there is Budget Deficit, i.e., . In this scenario, only a subset of projects can be funded. Unfortunately, identifying the subset of projects funded at equilibrium is challenging. In CC, the agents decide which projects to contribute to based on their private valuations and available refund. This circular dependence of the equilibrium contributions and the set of funded projects make providing analytical guarantees challenging on the funded set. To analyze agents’ equilibrium behavior and funding guarantees, we fix our focus on the subset of projects that maximize social welfare, i.e., (Def. 1).

In this section, we first show that funding at equilibrium is, in general, not possible for any satisfying Condition 1. Second, we prove that even with the stronger assumption of Subset Feasibility of the optimal welfare set, i.e., SF, we may not achieve socially efficient equilibrium due to agents’ strategic deviations. Last, we show that computing an agent ’s optimal deviation, given the contributions of the other agents , is NP-Hard.

5.1 Welfare Optimality at Equilibrium

Consider the following example instance.

Example 1.

Let and . Let with .

In Example 1, the maximum funded utility agent 1 can receive from project 1 is and unfunded utility . On the other hand, the agent obtains a utility of when contributing to project 2. Hence at equilibrium, project 2 gets funded, although it is welfare optimal to fund project 1. Thus, socially efficient equilibrium is not achieved.

nameProcedure

Example 1 is one pathological case where the agent with high valuation has zero budget, leading to sub-optimal outcome at equilibrium. Hence, we next strengthen the assumption on the budgets of the agents. Let be the non-trivial welfare optimal subset and we assume that Subset Feasibility is satisfied for , i.e., SF. Recall that with SF, we assume that every agent has enough budget to contribute in . Theorem 4 shows that despite this strong assumption, achieving socially efficient equilibrium may not be possible.

Theorem 4.

Given an instance of , a unique non-trivial may not be funded at equilibrium even with Subset Feasibility for , SF, for any set of satisfying Condition 1.

Proof.

We provide a proof by construction for and where one of the agents has an incentive to deviate when is funded. Procedure 1 presents the steps to construct the instance. We first select the target cost of the project , i.e. . Given under Condition 1, we can always find an for agent . At , funded utility is equal to unfunded utility (Figure 2). Trivially, . The rest of the proof shows that the construction defined in Procedure 1 is always possible for any refund scheme satisfying Condition 1 (see Appendix A.4). ∎

5.2 CCC with Budget Deficit: Optimal Strategy

Theorem 4 implies that may not be funded at equilibrium even when satisfies Subset Feasibility. In other words, w.l.o.g., an agent may have an incentive to deviate from any strategy that funds . Motivated by such a deviation, we now address the question: Given the total contribution by agents towards each project , can the agent compute its optimal strategy? We answer this question by (i) showing that such an optimal strategy may not exist if an agent’s contribution space is continuous, i.e., , and (ii) if contributions are discretized, then computing the optimal strategy is NP-Hard.

MIP-CC: Mixed Integer Program for CC. We first describe the general optimization for an agent to compute its optimal strategy (i.e., contribution). Assume that the agents have contributed denoted by . For agent ’s optimal strategy, we need to maximize its utility given and other variables such as the refund scheme and bonus budget . Figure 3 presents the formal MIP, namely MIP-CC, which follows directly from agent utility (Def. 2).

s.t. // Budget Constraint // Remaining Contribution // Defining Indicator Variable

MIP-CC: Optimal Strategy May Not Exist.

We now show that MIP-CC (Figure 3) may not always admit well-defined contributions.

Example 2.

Let and s.t. both agents are identical, i.e., each has the same value for each and . Additionally , and . Let the agents have budget s.t. , where is the upper bound equilibrium contribution for the single project case (see Figure 2).

Theorem 5.

Given an instance of and for any set of satisfying Condition 1, an agent ’s optimal strategy may not exist.

Proof.

We use proof by construction. In Appendix A.5, we show that for Example 2, given agent 1’s contribution we can create an instance of s.t. the set of indicator variable s in MIP-CC can be either or . Then, we show that agent 2’s utility becomes for with strategy and for with strategy where . As , agent 2’s utility for increases. But for , only is possible and agent 2 receives the utility (strictly less than utility for ). Due to this discontinuity in the utilities, no optimal exists, i.e., optimal strategy does not exist. ∎

MIP-CC-D. In order to overcome the above non-existence, we discretize the contribution space. More concretely, an agent can contribute where and the smallest unit of contribution. With this restriction on an agent’s contribution, the search space in MIP-CC (Figure 3) becomes discrete and finite. Consequently, agent ’s optimal strategy always exist. To distinguish MIP-CC with a discrete contribution space, we refer to it as MIP-CC-D.

5.2.1 MIP-CC-D: Finding Optimal Strategy is NP-Hard.

We now show that solving MIP-CC for discrete contributions (i.e., MIP-CC-D) is NP-hard.

Theorem 6.

Given an instance of with discrete contributions and for any set of satisfying Condition 1, computing optimal strategy for agent , given the contributions of , is NP-Hard.

Proof.

We divide the proof into two parts. In Part A, we design a MIP tuned for a specific case of combinatorial CC comprising identical projects with a refund scheme satisfying . We prove that the MIP is NP-Hard by reducing it from KNAPSACK. Then, in Part B, we show that this MIP reduces to MIP-CC-D. That is, any solution to MIP-CC-D can be used to determine a solution to MIP in polynomial time, implying that MIP-CC-D is also NP-Hard. The formal proof is available in Appendix A.6. ∎

Corollary 2.

Given an instance of with discrete contributions and for any set of satisfying Condition 1, if all agents except , , follow a specific strategy that funds , then computing the optimal deviation for agent is NP-Hard.

6 Experiments

Motivation. Theorem 4 proves that the optimal subset may not be funded at equilibrium due to agents’ strategic deviations. However, computing an agent’s optimal deviation is also NP-Hard (Corollary 2). These observations highlight that computing closed-form equilibrium strategies in Budget Deficit Combinatorial CC, similar to Theorem 1 and Theorem 3, for agents is challenging. Given this challenge and the hardness of strategic deviations, agents may employ heuristics to increase utility [39, 40]. We next propose five heuristics for agents to employ in practice and study their impact on agent utilities and the welfare generated.

6.1 Heuristics and Performance Measures

Heuristics.

Given the conflict between agent utilities and ’s funding (Theorem 4), we propose the following heuristics for agent , for each project , to employ in practice and observe their utility vs. welfare trade-off.

-

1.

Symmetric:

-

2.

Weighted:

-

3.

Greedy-: Greedily contribute in descending order of the projects sorted by

-

4.

Greedy-: Greedily contribute in descending order of the projects sorted by

-

5.

OptWelfare: , and evenly distribute the remaining budget across

Agents contribute the minimum amount of what is specified by the five heuristics and the amount left to fund the project. We consider OptWelfare as the baseline (preferred) heuristic since it generates optimal welfare, i.e., funds .

Performance Measures.

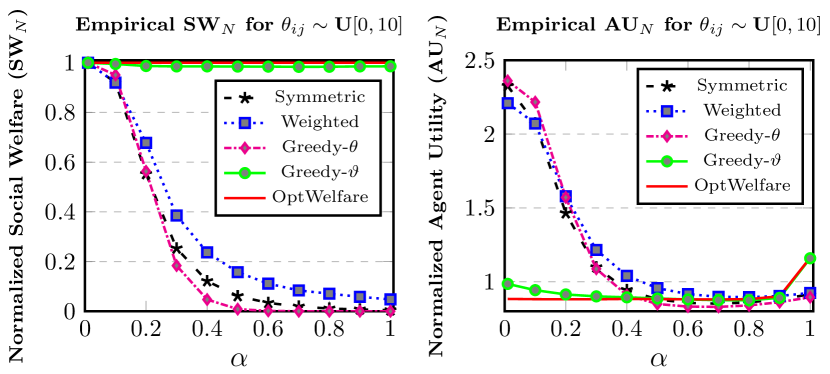

To study the welfare vs. agent utility trade-off, we consider the following performance measures: (i) Normalized Social Welfare (SWN) – Ratio of the welfare obtained and the welfare from and (ii) Normalized Agent Utility (AUN) – Ratio of the agent utility obtained w.r.t. to the utility when each agent has enough budget to play its PPR contribution (see Theorem 1).

We compare the heuristics when fraction of the total agents deviate, i.e., choose heuristic {Symmetric, Weighted, Greedy-, Greedy-}. The remaining fraction of agents use the baseline OptWelfare.

6.2 Simulation Setup and Results

Setup.

We simulate the combinatorial CC game with , and and PPR refund scheme (Eq. 2).333The experimental trends presented remain same for different pairs, such as , , and . We sample s, for each and , using (i) Uniform Distribution, i.e., , and (ii) Exponential Distribution, i.e., Exp(). Here, is the rate parameter. When , we get agents whose per-project valuations differ significantly. For ), the agents have approximately similar per-project valuations.

We ensure and for each project and that the properties Budget Deficit and Subset Feasibility for are satisfied. We run each simulation across k instances and observe the average SWN and AUN for each of the five heuristics. We depict our observations with Figures 4 and 5 when . The results for Exp() are presented in Appendix C.

Average SWN and AUN.

Figure 4 depicts the results when . We make three main observations. First, deviating from the baseline heuristic (OptWelfare) is helpful only when few agents deviate, i.e., for smaller values of . Despite such a deviation, we observe that the corresponding decrease in social welfare is marginal. On the other hand, the increase in reduces the amount of the contributions, and the projects remain unfunded, reducing the social welfare and the agent utilities. Second, deviating from OptWelfare always increases the average agent utility – at the cost to the overall welfare. Third, Greedy- almost mimics OptWelfare, for both SWN and AUN.

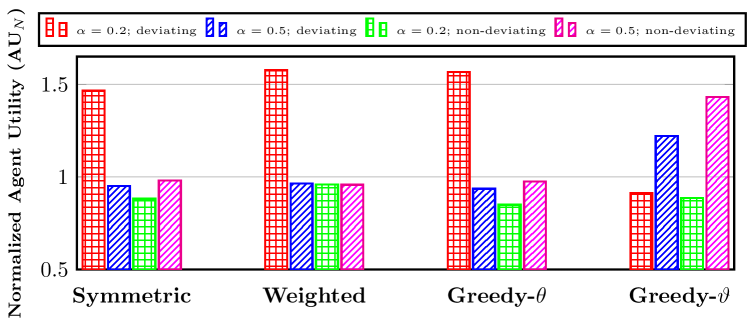

AUN for Deviating vs. Non-deviating Agents.

In Figure 5, we compare the average utility for the agents who deviate versus those who do not. We let fraction of the agents deviate and follow the other four heuristics. From Figure 5, we observe that upon deviating to Symmetric, Weighted or Greedy-, the fraction of agents obtain higher AUN (red grid bars) compared to the remaining non-deviating agents who do not deviate (green grid bars). In contrast, Greedy- shows non-deviation to be beneficial. Since Greedy- performs close to OptWelfare, the AUN for deviation remains low compared to OptWelfare. Crucially, the deviation is not majorly helpful when many agents deviate. When , we see comparable average AUN for agents who deviate and those who do not (blue lined vs. magenta lined bars, respectively). While deviating to Greedy- remains non-beneficial.

Discussion and Future Work.

From Figures 4 and 5, we see that Greedy- performs similar to OptWelfare (which funds ). Thus, as the number of projects increases, to maximize social welfare, it may be beneficial for the agents to adopt Greedy- instead of deriving sophisticated strategies based on (since computing is NP-Hard).

Generally, it is challenging to determine PSNE contributions for combinatorial CC with budgeted agents. We propose four heuristics and study their welfare and agent utility trade-off. Future work can explore other heuristics that achieve better trade-offs and welfare guarantees. One can also study strategies that perform better on average such as Bayesian Nash Equilibrium. From the experiments, we observe that deviating from OptWelfare may increase agent utility. Thus, one can explore strategies such as -Nash Equilibrium, which approximates a worst-case increase in utility with unilateral deviation. Approximate strategies may also be desirable since finding optimal deviation is NP-Hard. However, the approximation must provide a desirable trade-off between agent utility and welfare.

7 Conclusion

This paper focuses on the funding guarantees of the projects in combinatorial CC. Based on the overall budget, we categorize combinatorial CC into (i) Budget Surplus and (ii) Budget Deficit. First, we prove that Budget Surplus is insufficient to guarantee projects’ funding at equilibrium. Introducing the stronger criteria of Subset Feasibility guarantees the projects’ funding at equilibrium under Budget Surplus. However, for Budget Deficit, we prove that the optimal welfare subset’s funding can not be guaranteed at equilibrium despite Subset Feasibility. Next, we show that computing an agent’s optimal strategy (and consequently, its optimal deviation), given the contributions of the other agents, is NP-Hard. Lastly, we propose specific heuristics and observe the empirical trade-off between agent utility and social welfare.

References

- London [2021] Mayor London. The impact of community crowdfunding, 2021. URL https://www.london.gov.uk/what-we-do/regeneration/funding-opportunities/make-london/impact-community-crowdfunding.

- Van Montfort et al. [2021] Kees Van Montfort, Vinitha Siebers, and Frank Jan De Graaf. Civic crowdfunding in local governments: Variables for success in the netherlands? Journal of Risk and Financial Management, 14(1):8, 2021.

- Diederich et al. [2016] Johannes Diederich, Timo Goeschl, and Israel Waichman. Group size and the (in) efficiency of pure public good provision. European Economic Review, 85:272–287, 2016.

- Goodspeed [2017] Robert Goodspeed. Community and urban places in a digital world. Digital World. City & Community, 16(1):9–15, 2017.

- Chandra et al. [2017] Praphul Chandra, Sujit Gujar, and Yadati Narahari. Referral-embedded provision point mechanisms for crowdfunding of public projects. In AAMAS, pages 642–650, 2017.

- Wang et al. [2021] Guanhua Wang, Runqi Guo, Yuko Sakurai, Muhammad Ali Babar, and Mingyu Guo. Mechanism design for public projects via neural networks. In AAMAS, pages 1380––1388, 2021.

- Yan and Chen [2021] Xiang Yan and Yiling Chen. Optimal crowdfunding design. In AAMAS, pages 1704–1706, 2021.

- Cason et al. [2021] Timothy N Cason, Alex Tabarrok, and Robertas Zubrickas. Early refund bonuses increase successful crowdfunding. Games and Economic Behavior, 2021.

- Kickstarter [2022] Kickstarter. Kickstarter — Wikipedia, the free encyclopedia. https://en.wikipedia.org/w/index.php?title=Kickstarter, 2022.

- Spacehive [2022] Spacehive. Spacehive - crowdfunding for local projects. https://www.spacehive.com/, 2022.

- Stroup [2000] Richard L Stroup. Free riders and collective action revisited. In Public Choice Essays in Honor of a Maverick Scholar: Gordon Tullock, pages 137–150. Springer, 2000.

- Zubrickas [2014] Robertas Zubrickas. The provision point mechanism with refund bonuses. Journal of Public Economics, 120:231–234, 2014.

- Damle et al. [2021] Sankarshan Damle, Moin Hussain Moti, Sujit Gujar, and Praphul Chandra. Designing refund bonus schemes for provision point mechanism in civic crowdfunding. In PRICAI, page 18–32, 2021.

- Chen et al. [2021] Yiling Chen, Biaoshuai Tao, and Fang-Yi Yu. Cooperation in threshold public projects with binary actions. In IJCAI, pages 104–110, 2021.

- Soundy et al. [2021] Jared Soundy, Chenhao Wang, Clay Stevens, and Hau Chan. Game-theoretic analysis of effort allocation of contributors to public projects. In IJCAI, pages 405–411, 2021.

- Brandl et al. [2022] Florian Brandl, Felix Brandt, Matthias Greger, Dominik Peters, Christian Stricker, and Warut Suksompong. Funding public projects: A case for the nash product rule. Journal of Mathematical Economics, 99:102585, 2022.

- Moulin [1994] Hervé Moulin. Serial cost-sharing of excludable public goods. The Review of Economic Studies, 61(2):305–325, 1994.

- Moulin and Shenker [2001] Hervé Moulin and Scott Shenker. Strategyproof sharing of submodular costs: budget balance versus efficiency. Economic Theory, 18(3):511–533, 2001.

- Dobzinski et al. [2018] Shahar Dobzinski, Aranyak Mehta, Tim Roughgarden, and Mukund Sundararajan. Is shapley cost sharing optimal? Games and Economic Behavior, 108:130–138, 2018. ISSN 0899-8256. doi: https://doi.org/10.1016/j.geb.2017.03.008. URL https://www.sciencedirect.com/science/article/pii/S0899825617300520.

- Dobzinski and Ovadia [2017] Shahar Dobzinski and Shahar Ovadia. Combinatorial cost sharing. In ACM EC, pages 387–404, 2017.

- Birmpas et al. [2019] Georgios Birmpas, Evangelos Markakis, and Guido Schäfer. Cost sharing over combinatorial domains: Complement-free cost functions and beyond. In ESA, pages 1–17, 2019.

- Ohseto [2000] Shinji Ohseto. Characterizations of strategy-proof mechanisms for excludable versus nonexcludable public projects. Games and Economic Behavior, 32(1):51–66, 2000.

- Aziz and Shah [2021] Haris Aziz and Nisarg Shah. Participatory budgeting: Models and approaches. In Pathways Between Social Science and Computational Social Science, pages 215–236. Springer, 2021.

- Aziz and Ganguly [2021] Haris Aziz and Aditya Ganguly. Participatory funding coordination: Model, axioms and rules. In Algorithmic Decision Theory (ADT), pages 409–423, 2021.

- Sreedurga et al. [2022] Gogulapati Sreedurga, Mayank Ratan Bhardwaj, and Y Narahari. Maxmin participatory budgeting. arXiv preprint arXiv:2204.13923, 2022.

- Aziz et al. [2022] Haris Aziz, Sujit Gujar, Manisha Padala, Mashbat Suzuki, and Jeremy Vollen. Coordinating monetary contributions in participatory budgeting. arXiv preprint arXiv:2206.05966, 2022.

- Bagnoli and Lipman [1989] Mark Bagnoli and Barton L Lipman. Provision of public goods: Fully implementing the core through private contributions. The Review of Economic Studies, 56(4):583–601, 1989.

- Healy [2006] Paul J Healy. Learning dynamics for mechanism design: An experimental comparison of public goods mechanisms. Journal of Economic Theory, 129(1):114–149, 2006.

- Chandra et al. [2016] Praphul Chandra, Sujit Gujar, and Y Narahari. Crowdfunding public projects with provision point: A prediction market approach. In ECAI, pages 778–786, 2016.

- Damle et al. [2019a] Sankarshan Damle, Moin Hussain Moti, Praphul Chandra, and Sujit Gujar. Civic crowdfunding for agents with negative valuations and agents with asymmetric beliefs. In IJCAI, pages 208–214, 2019a.

- Damle et al. [2019b] Sankarshan Damle, Moin Hussain Moti, Praphul Chandra, and Sujit Gujar. Aggregating citizen preferences for public projects through civic crowdfunding. In AAMAS, pages 1919–1921, 2019b.

- Padala et al. [2021] Manisha Padala, Sankarshan Damle, and Sujit Gujar. Learning equilibrium contributions in multi-project civic crowdfunding. In WI-IAT, pages 368––375, 2021.

- Börgers and Krahmer [2015] Tilman Börgers and Daniel Krahmer. An introduction to the theory of mechanism design. Oxford University Press, USA, 2015.

- Chakrabarty and Swamy [2014] Deeparnab Chakrabarty and Chaitanya Swamy. Welfare maximization and truthfulness in mechanism design with ordinal preferences. In Proceedings of the 5th conference on Innovations in Theoretical Computer Science, pages 105–120, 2014.

- Alegre [2020] Porto Alegre. Case study 2-porto alegre, brazil: participatory approaches in budgeting and public expenditure management, 2020.

- HudExchange [2022] HudExchange. Participatory budgeting. https://www.hudexchange.info/programs/participatory-budgeting/, 2022.

- Lawler [1977] Eugene L Lawler. Fast approximation algorithms for knapsack problems. In 18th Annual Symposium on Foundations of Computer Science (sfcs 1977), pages 206–213. IEEE, 1977.

- Cason and Zubrickas [2017] Timothy N Cason and Robertas Zubrickas. Enhancing fundraising with refund bonuses. Games and Economic Behavior, 101:218–233, 2017.

- Zou et al. [2010] James Zou, Sujit Gujar, and David Parkes. Tolerable manipulability in dynamic assignment without money. In AAAI, pages 947–952, 2010.

- Lubin and Parkes [2012] Benjamin Lubin and David C Parkes. Approximate strategyproofness. Current Science, pages 1021–1032, 2012.

Appendix A Proofs

This section presents the formal proofs for the results covered in the main paper.

A.1 Proof of Theorem 2

Theorem.

Proof.

Consider the set of projects and agents s.t. Def. 4 is satisfied, i.e., . Denote as the set of agents whose overall budget is such that even if they contribute their entire budget none of the project gets funded.444E.g., There exists an agent with budget less than . Also note that, we do not assume to be unique. This implies . The remaining set of agents must have enough budget to fund all the projects (from Def. 4).

Note that, each agent receives a funded utility for contributing towards project . That is, the funded utility decreases with the increase in contribution. The agent may also receive an unfunded utility of for project . Since is monotonically increasing (Condition 1), increasing the contribution increases the refund. We depict this scenario with Figure 2. Observe that the plot between funded and unfunded utility w.r.t. contributions meet at the upper-bound of the equilibrium contribution (as defined in Theorem 1), where funded utility is equal to the unfunded. For any contribution , the agent receives a greater unfunded utility.

Consider a scenario where the agents in do not have sufficient budget and thus contribute less than . Let . Now, we have as the remaining amount to fund the set . In order to fund , the remaining agents in may need to contribute where (refer Figure 2). At , the unfunded utility is more. Hence, the agents contribute , s.t. and , i.e., the contributions are not well-defined. ∎

A.2 Proof of Claim 1

Claim.

Given any whose equilibrium contributions satisfy , we have SFP BS.

Proof.

From the definition of SFP, . As , we have , i.e., Budget Surplus is also satisfied. ∎

A.3 Proof of Theorem 3

Theorem.

Given and satisfying CM (Condition 1) such that is satisfied, at equilibrium all the projects are funded, i.e., if . Further, the set of PSNEs are:

.

Proof.

For a given refund scheme and corresponding , each agent ’s budget satisfies, using SFP, . Let each agent ’s final contribution ; where . Since , the project gets funded, and each agent obtains a utility of .

W.l.o.g., let us assume that agent contributes s.t. . Then , we can construct the following two deviations for :

-

1.

. For any less than , the project is not funded and .

-

2.

. For any , the project is funded but the funded utility reduces, i.e., .

In both the cases, we obtain the following,

Therefore,

From Def. 3, are PSNE and every project gets funded. ∎

A.4 Proof of Theorem 4

Theorem.

Given an instance of , a unique non-trivial may not be funded at equilibrium even with Subset Feasibility for , SF, for any set of satisfying Condition 1.

Proof.

We provide a proof by construction for and where one of the agents has an incentive to deviate when is funded. Procedure 1 presents the general steps to construct the instance. Informally, we first select the target cost of the project , i.e. , to be any positive real value. Given under Condition 1, we can always find an for agent . At , funded utility is equal to unfunded utility (refer Figure 2). Trivially, . We now prove that the construction defined in Procedure 1 is always possible.

Line 3. We select such that . We are required to prove that such a will always exist. When , it must be true that, . If then (i.e., funded utility equals unfunded utility), since by construct, contradicting Condition 1. Hence , when . As is continuous w.r.t. , we can always chose s.t. .

Line 4. We choose s.t., . It is possible since .

Line 5. We let and . Then, select . Observe that, we can always select since .

Given the above, and the values and ; we arrive at . Hence, , i.e., the welfare optimal subset is and is unique.

Line 6. To ensure , i.e., Subset Feasibility of , we set and . Note that, , Budget Deficit is also satisfied. Thus, Procedure 1 returns valid instance, say , of .

Next, note that, in , agent 1 contributes and agent 2 must contribute to fund project 1 and to achieve socially efficient equilibrium. If agent 2 does not deviate, it will receive an utility . However, let agent 2 unilaterally deviate and contribute to project 2. As , project 2 gets funded and agent 2 obtains a utility of . From Line 5 in Procedure 1, we know that , hence agent 2 will deviate, implying is not funded at equilibrium for the game. ∎

A.5 Proof of Theorem 5

Theorem.

Given an instance of and for any set of satisfying Condition 1, an agent ’s optimal strategy may not exist.

Proof.

From Example 2, let agent 1 contribute its entire budget to project 1, i.e., and . Now we solve MIP-CC for agent 2. Since and (see Eq. 3), the overall budget is enough to fund only a single project. That is, as agent 1 has contributed to project 1, agent 2 can (at best) fund only project 1. So the set of indicator variable s in MIP-CC can be either or .

Computing Optimal Strategy. We have the following cases:

-

: This is possible when agent 2 contributes to project 1, resulting in project ’s funding. The utility agent 2 gets is .

-

: Agent 2 may opt to contribute in all the 3 projects in order to grab the maximum refund. As the refund shares from sum exactly to , agent 2 can grab the entire bonus from projects 2 and 3 by contributing any arbitrary positive value, . However, agent 2 must contribute less in project 1 since, . Hence, project 1 becomes unfunded. For optimal strategy, agent 2 must maximize the refund from project 1, i.e., . Therefore, is not well-defined as satisfies CM. So the overall utility by deviating for agent 2 becomes where an optimal is not defined.

∎

A.6 Proof of Theorem 6

Theorem.

Given an instance of with discrete contributions and for any set of satisfying Condition 1, computing optimal strategy for agent , given the contributions of , is NP-Hard.

Proof.

For completeness, we first re-write MIP-CC-D (see Figure 3) for discrete contributions. Let denote the discrete contribution set where is the smallest unit of contribution. Now, the following optimization defines MIP-CC-D for agent without the sub-script “". Note that, Eq. A1 is merely the optimization presented in Figure 3 with the added constraint on the contribution set.

| (A1) |

We first construct an optimization problem MIP, which we show is equivalent to the KNAPSACK problem in Part A. In Part B, we show that the MIP reduces to MIP-CC-D implying MIP-CC-D is also NP-Hard.

A.6.1 Part A: Designing MIP (Eq. A2)

For our proof, we consider a refund scheme and bonus budget which is the same for each project . satisfies CM (Condition 1) such that the refund share satisfies . 555An example of such a refund scheme can be where and . Now we define the MIP as follows.

| (A2) |

We now prove that the MIP defined in Eq. A2 is NP-Hard. The MIP can be re-written as,

We reduce the MIP problem from the NP-complete problem: given items with weights and value , capacity and value , does there exist a subset such that and ? Given an instance of the problem, we build an instance of the above MIP as follows:

-

The set of projects is the set of items. The amount left for funding the project is . The budget of the agent is .

-

The value of each project to the agent is, , i.e., .

We can see that the utility obtained by choosing a set of projects is exactly equal to the value of choosing set of items in the KNAPSACK problem i.e, . Also note that the budget constraint is satisfied if and only if the capacity constraint is satisfied. It follows that a solution with value at least exists in the KNAPSACK problem if and only if there exists a set of projects whose social welfare in the above instance is at least .

Thus, we reduce MIP from KNAPSACK implying MIP is NP-Hard. ∎

We next show that MIP in Eq. A2 also reduces to MIP-CC-D.

A.6.2 Part B: Reducing MIP to MIP-CC-D

Before we show the reduction, we define the following handy notations for the objectives of MIP-CC-D and MIP.

| “MIP-CC-D” | ||||

| “MIP in Eq. A2” |

Further let, denote the tuple of feasible solutions to MIP-CC-D and denote the set of feasible solutions to MIP.

Given an instance of MIP we construct an instance of MIP-CC-D using the following conditions,

-

P1.

For each project , we have s.t. .

-

P2.

Let the remaining contribution be .

Using P1 and P2, we now show that any implies that .

Claim I.

For the specific setting defined by P1-P2 and given and as the tuple of feasible solutions to MIP-CC-D and MIP in Eq. A2, respectively, we have .

Proof.

For the proof, we show that given any solution , we can also construct a solution . That is, given , we can construct as follows. Let if and if .

We now have to show that ’s construction does not break feasibility of a solution in MIP-CC-D. Observe that, from Eq. A1,

-

•

Trivially, we have and . That is, the budget constraint and project’s funding conditions are satisfied.

-

•

If , then both and hold.

-

•

Likewise, if then both and hold.

Hence for every we can construct s.t., . Hence every solution that is feasible for MIP is also feasible for MIP-CC-D. ∎

With this, consider the following claim.

Claim II.

For the specific setting defined by P1-P2 and any fixed , let where and and . Then , such that , .

Proof.

Given a fixed , observe that,

Hence, where if and .

To conclude the proof, we now show that the contribution set is also feasible. To this end, observe that from the claim statement we have . Further, since for each , we have by construction and for each we have , the second feasibility condition is also met. ∎

We can trivially observe that where if and . Let , then and from Claim II, , hence . That is,

Given that (i) the feasibility set of MIP is a subset of the feasibility set of MIP-CC-D and (ii) is also feasible to MIP since and , we have . Hence is also optimal to MIP.

A.7 Proof of Corollary 2

Corollary 1.

Given an instance of with discrete contributions and for any set of satisfying Condition 1, if all agents except , , follow a specific strategy that funds , then computing the optimal deviation for agent is NP-Hard.

Proof.

Let agents follow a specific strategy and contribute to the projects s.t. is not funded. For any such strategy, given contributions, agent ’s optimal deviation is again given by MIP-CC-D. Hence NP-Hardness follows directly from Theorem 6. ∎

Appendix B Illustration of Procedure 1 for PPR

To further clarify the impossibility presented in Theorem 4, we demonstrate Procedure 1 when is the PPR refund scheme (Eq. 2). As required, consider a setting with and . Let and . We choose which implies using Theorem 1. That is, . Now, fix . This also implies . The upper bound on the equilibrium contribution, , is possible for the value . Select , to get . This also implies , i.e., and . Despite this, agent 2 will deviate since .

Appendix C Exponential Distribution

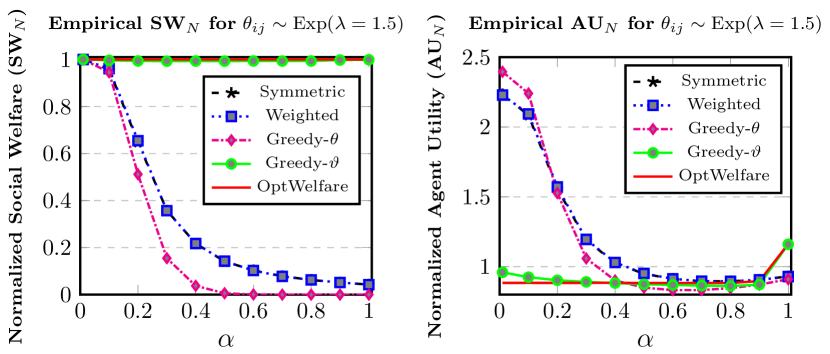

We now provide the results when agents sample their valuations using the Exponential distribution, i.e., for each agent and for the project , let . Here, is the rate parameter. Figure 6 depicts the empirical Normalized Social Welfare (SWN) and Normalized Agent Utility (AUN).

Despite the difference in sampling s, we observe that the overall trend in AUN and SWN is the same as that reported for the Uniform case (in the main paper). That is, agent deviation is helpful only for smaller s. And that such a deviation results in only a marginal decrease in the overall welfare obtained.

These results further suggest that agents may prefer the strategy Greedy- as the number of projects increases. One can also study the notion of -Nash Equilibrium for these cases and provide theoretical bounds on the tolerance vis-a-vis the social welfare.