Cross-Sectional Dynamics Under Network Structure: Theory and Macroeconomic Applications

[latest version: click here] )

Abstract

Many environments in economics feature a cross-section of units linked by bilateral ties. I develop a framework for studying dynamics of cross-sectional variables that exploits this network structure. It is a vector autoregression in which innovations transmit cross-sectionally via bilateral links and which can accommodate rich patterns of how network effects of higher order accumulate over time. The model can be used to estimate dynamic network effects, with the network given or inferred from dynamic cross-correlations in the data. It also offers a dimensionality-reduction technique for modeling high-dimensional (cross-sectional) processes, owing to networks’ ability to summarize complex relations among variables (units) by relatively few non-zero bilateral links. In a first application, I estimate how sectoral productivity shocks transmit along supply chain links and affect dynamics of sectoral prices in the US economy. The analysis suggests that network positions can rationalize not only the strength of a sector’s impact on aggregates, but also its timing. In a second application, I model industrial production growth across 44 countries by assuming global business cycles are driven by bilateral links, which I estimate. This reduces out-of-sample mean squared errors by up to 23% relative to a principal components factor model.

JEL codes: C32, E32, E37.

Key words: Vector Autoregression, Spatial Autoregression, Dynamic Network Effects, High-Dimensional Time Series, Sparse Factors, Input-Output Economy, Price Dynamics, Global Business Cycles.

1 Introduction

Numerous economic environments feature a cross-section of units connected by a network of bilateral ties. For example, countries are connected via flows of trade and capital, industries are linked through supply chains, and individuals in a society form a network by virtue of being acquainted to one another. As demonstrated theoretically and documented empirically,111See references in the following paragraph and subsequent literature review. networks can rationalize comovement in variables measured at the cross-sectional level; GDP across countries varies depending on demand and supply by trade partners, firms adjust their prices in response to price increases by suppliers, individuals receive information and form opinions by interacting with their social network.

What is less well understood, however, is how network-induced comovements play out over time. With regard to the timing of network effects, the literature considers two restrictive cases. The first assumes that innovations transmit via bilateral links contemporaneously (e.g. Acemoglu et al. (2012); Elliott et al. (2014)). This leads to a static framework and implies that connections of all order play out (simultaneously). For example, an individual talks to all their friends, who in turn talk to all their respective friends, etc., so that at each point in time everyone’s opinion incorporates those of all members of society and within the same period fully adjusts to any new information gathered by even its most distant member. This assumption is useful for steady state comparisons, i.e. for stduying long-term effects of permanent shocks. The second case posits that network effects materialize exactly one link per period (e.g. Long and Plosser (1983); Golub and Jackson (2010)). This assumption is tenable in theoretical contributions, but in empirical studies a period is defined by data and it remains an empirical question how far a shock travels through the network in one observational period.222The long-term effects of permanent shocks in this environment turn out to be the same as the effects in the static framework of contemporaneous linkages. See Section 2.2.2 and Section A.4.

I build an econometric framework to study the dynamics of cross-sectional variables when units are connected through a network. It is a vector autoregression (VAR), parameterized such that innovations transmit cross-sectionally only via bilateral links. Transmission is assumed to be uni-directional333i.e. either downstream or upstream, the distinction being relevant only for directed networks. and links fixed over time. The framework can accommodate rich patterns on how innovations travel along bilateral links over time, and, consequently, how network connections of higher order accumulate as time progresses. The interdependence of observations and arises as the interplay of temporal distance between periods and and cross-sectional distance between units and encoded by the network. Correspondingly, stationarity can be characterized in terms of eigenvalues of the network adjacency matrix and roots of an AR process defined by the timing of innovation transmission along a single link. This timing is fundamentally related to the frequency of network interactions relative to the frequency of observation.

The Network-VAR (NVAR) is useful in two rather distinct lines of empirical work with cross-sectional time series. On the one hand, it can be used to estimate dynamic network effects, i.e. to quantify how innovations transmit along bilateral links over time and come to shape cross-sectional dynamics. Thereby, the network can be taken as given or inferred from dynamic cross-correlations in the data, possibly aided by shrinking towards observed links. With both the network and effect-timing estimated, the NVAR is also applicable as a dimensionality-reduction technique for modeling high-dimensional processes. It assumes that dynamics are generated by innovation transmission along a (small) set of bilateral links among variables. Given the network, inference on the timing of network effects boils down to a linear regression with covariates that summarize lagged observations using bilateral links. Joint inference is implemented easily by iteration on analytically available conditional estimators, with Bayesian as well as frequentist interpretations. I illustrate each of these two model uses with a respective application.

In the first application, I estimate how sectoral productivity shocks propagate through the supply chain network and shape the monthly dynamics of Producer Price Indices (PPI) in the US economy. I show that the NVAR approximates the process of sectoral prices in a Real Business Cycle (RBC) input-output economy with time lags between the production of goods and their subsequent use as intermediaries in producing other goods. In turn, I estimate the timing of input-output conversion and its frequency relative to the monthly frequency of price observations. This allows me to determine the contribution of lagged input-output conversion in driving aggregate price dynamics and the impact of sectoral positions in the supply chain network on the timing at which sectoral price movements affect aggregate prices.

Preliminary results suggest that network positions have implications not only for the strength of sectoral shocks’ effects on aggregates – as documented in existing literature – but also for its timing, with no clear relationship between the two. How quickly a shock in a sector affects aggregate PPI is determined by the sector’s importance as an immediate – as opposed to further upstream – supplier to relevant sectors in the economy. Owing to their position at the top of supply chains, the response to price increases in energy-related sectors is estimated as particularly slow to unravel.

In the second application, I model industrial production growth across 44 countries by estimating an underlying network as relevant for dynamics. This provides a novel perspective on global business cycles by assuming that the dynamic comovement in economic activity across countries is the result of innovation transmission along bilateral links. The NVAR yields a sparse, yet flexible way of approximating (cross-sectional) processes even in high dimensions. Sparsity is obtained because dynamics are driven by bilateral links and because variables (units) can be connected even in absence of a direct link between them. As a result, the dynamic comovement of the whole, potentially high-dimensional time series can be modeled with relatively few non-zero bilateral links. This is reminiscent of the assumption that longer-term dynamics are driven by a set of shorter-term dynamics, which is upheld by the general class of VARMA() models. Flexibility is owed to the fact that the network is estimated and that the model can accommodate general patterns of how network effects of higher order accrue over time.

An equivalence result suggests that the NVAR is preferred to a factor model whenever cross-sectional dynamics are composed of many micro links rather than driven by a few influential units. This corresponds to the case of numerous sparse factors with differing sets of non-zero loadings across units, or, equivalently, a sparse, yet high-rank network adjacency matrix. In my application, the NVAR – with the network estimated by shrinking links to zero – leads to reductions in out-of-sample mean squared errors of up to 23% relative to a principal components factor model, in particular for horizons up to six months.

Related Literature

This paper adds to the growing literature on networks in econometrics.444See Bramoullé et al. (2016) and Graham (2020) for general references on networks in economics and econometrics. In particular, there is a large literature on spatial autoregressive models. It is mostly concerned with identifying network effects (and effects of other covariates) in a static framework of contemporaneous dependencies (e.g. Manski (1993); Lee (2007); Bramoullé et al. (2009)). In contrast, I analyze lagged network effects. Relative to other studies in this category (e.g. Knight et al. (2016); Yang and Lee (2019)), Zhu et al. (2017) cast them in an explicit time series model, generalizing the lag length and discussing stationarity and large -inference. I show that dynamics in this model – as evidenced by Granger causality at different horizons – are driven by innovation transmission along network connections of different order. In turn, I further generalize this mapping between network connections and dynamics, I discuss inference on both the timing of innovation transmission as well as on the network itself, and I illustrate the model’s merits as a dimensionality-reduction technique.

At a fundamental level, my work relates to Diebold and Yilmaz (2009, 2014), who map variance decompositions of VARs into networks with the goal of understanding dynamic connectedness.555Another way to represent dynamics by graphs is offered in Barigozzi and Brownlees (2018). In contrast, I map networks into VARs. In particular, I use a network to model the conditional mean function, restricting innovations to transmit via bilateral links. This leads to rich patterns of multi-step causality, connecting my work to Dufour and Renault (1998). Relative to other studies restricting time series models using networks (e.g. Pesaran et al. (2004); Barigozzi et al. (2022); Mehl et al. (2023); Caporin et al. (2023)),666Barigozzi et al. (2022) extend the model of Zhu et al. (2017) along a different dimension than I do, allowing for several connection-types to influence dynamics. I focus on a simple case of one variable per cross-sectional unit and one type of connection among units and I entertain this assumption of innovation transmission along bilateral links. This leads to a clear relation between the model’s time series properties on the one hand and the network and timing of network effects on the other. It also generates intuitive, analytical expressions for the estimators and allows me to examine the relation to factor models. Approaches for achieving shock identification using networks are discussed in Hipp (2020) and Dahlhaus et al. (2021). Bykhovskaya (2021) builds a time series model for the evolution of the network itself.

With my first application, I address the macroeconomic literature on production networks. It mostly assumes contemporaneous input-output conversion to show that networks amplify idiosyncratic shocks and generate cross-sectional comovement at a given point in time (Horvath, 2000; Foerster et al., 2011; Acemoglu et al., 2012; Bouakez et al., 2014; Giovanni et al., 2018; Giroud and Mueller, 2019). This framework is silent on how networks drive aggregate and cross-sectional dynamics.777Under contemporaneous interactions, network effects of all order play out simultaneously. In other words, network effects themselves are static; networks can only amplify existing dynamics – obtained thanks to agents’ intertemporal optimization problems in a structural model or due to persistence in shocks – but not drive dynamics themselves. See discussion in Section 2.2.2. Exceptions are Long and Plosser (1983) and Carvalho and Reischer (2021), who study a Real Business Cycle (RBC) economy with input-output conversion lagged by one period. The former show that lagged input-output conversion leads to endogenous business cycles, while the latter characterize aggregate persistence in this theoretical model and show that it matches well empirical measures of persistence. Building on their work, I allow for more general lags in input-output conversion, which leads to sectoral prices (and output) in the model following an NVAR. In turn, I estimate the extent to which input-output conversion is spread out over several periods and its frequency relative to the monthly frequency of price observations. This allows me to determine the contribution of lagged input-output conversion in driving dynamics of aggregate prices.

With the second application of the NVAR, this paper addresses the vast literature on dimensionality-reduction techniques for time series modeling. By reducing the number of parameters and using shrinkage priors (regularization), the proposed approach applies both of the two ways of addressing the large parameter problem in the Wold representation (see Geweke (1984)). Compared to reduced rank regression and factor models (Velu et al., 1986; Stock and Watson, 2002), it finds the linear combination that effectively summarizes the information in lagged values by relying on bilateral links among variables (cross-sectional units). As a result, it naturally incorporates sparse factors as locally important nodes in the network, and it can improve upon the poor forecasting performance of factor models in settings with a high dispersion in factor loadings across series (see e.g. Boivin and Ng (2006)),888This notably includes the case of sparse factors and units differing in the set of factors they load on. For analyses of sparse factors, see Onatski (2012) and Freyaldenhoven (2022). such in this paper’s application. Compared to shrinkage methods like Lasso (Tibshirani, 1996) or Ridge regression,999See Hsu et al. (2008) and Camehl (2022) for applications of Lasso in the context of VARs. it applies shrinkage to links – which in turn summarize the information in predictors – rather than to predictors themselves. This leads to additional parsimony as the same links are used to summarize information at all lags, though possibly using different orders of connection.101010Other approaches bridging sparse and factor models are usually interested in capturing the cross-sectional correlation in the errors left after factor extraction. See e.g. Fan et al. (2021).

The remainder of this paper is structured as follows. The model and its properties are discussed in Section 2. Section 3 treats inference. In Section 4, I study how input-output connections shape the dynamics of sectoral prices in the US economy, taking the network as given. In Section 5, I illustrate the merits of the NVAR as a dimensionality-reduction technique for modeling high-dimensional processes, and I apply it for forecasting cross-country industrial production. Section 6 concludes.

2 Lagged Network Effects & Cross-Sectional Dynamics

After providing some basic background on networks in Section 2.1, I present the NVAR in Section 2.2, building on a simple example. I explicitly examine the relation between the frequencies of network interaction and observation, and I discuss stationarity and the relation to contemporaneous network interactions. Estimation is deferred to Section 3.

2.1 Bilateral Connections in Networks

A network is represented by an adjacency matrix with elements . I consider a directed, weighted and possibly signed network, which means that shows the sign and strength of the link from cross-sectional unit to unit , with possibly. If , I say unit is not connected to unit . Self-links are permitted. The set of bilateral links give rise to a plethora of higher-order connections among units, referred to as walks.111111Whenever convenient to simplify notation, I write for the set of integers , .

Definition 1 (Walk).

A walk from to of length is the product of a sequence of links between units such that for , with , :

Put simply, a walk is the product of bilateral links that lead from unit to unit over some intermediary units, all of which are sequentially connected. Just as element in the matrix shows the walk from to of length one (direct link), simple matrix algebra reveals that contains the sum of walks from to of length .121212In the case of an unweighted and unsigned network, and so any walk , which means that contains the number of walks from to . I refer to this quantity as the th-order connection from to .

Consider the following example:

Even though unit is not directly connected to unit (), there exists a second-order connection via unit (). For example, in a production network, unit could be a supplier to unit , who in turn is a supplier to unit .

2.2 Lagged Innovation Transmission via Bilateral Links

The core assumption that underlies the proposed NVAR is that innovations to a process transmit cross-sectionally only via bilateral links. I assume links to be fixed and this transmission to operate only in one direction through the network. Specifically, the direct link from to , , is a vehicle for innovation transmission from to . Innovations can be cross-sectionally correlated. To simplify the exposition, I assume .

2.2.1 Simple Example: NVAR(1,1)

Let and , and consider the following VAR(1):

| (1) |

Taking to be proportional to the adjacency matrix of a network that connects the cross-sectional units, one obtains a process that relates the dynamics of the cross-sectional time series to the bilateral links among cross-sectional units.131313As explained in Section 2.2.2, I call this process NVAR(1,1). Long and Plosser (1983) derive such a process for sectoral output and prices in an RBC production economy with a one period delay in converting inputs into output.141414See Section C.1 and the discussion in Section 4. See also Carvalho and Reischer (2021). Golub and Jackson (2010) posit it to study societal opinion formation through friendship ties.

Under this process, the one period-ahead expectation of is proportional to a weighted sum of one period-lagged values of for all units to which is directly linked, with weights given by the strength of direct links : . In the example from Long and Plosser (1983), the price charged tomorrow by firms in sector is expected to be a weighted average of prices charged by their suppliers today. Dynamics of , as summarized by Granger-causality at horizons , are shaped by th order connections encoded in :

As a result, given all other variables , is useful in forecasting at horizon iff there is an th order connection from to . The strength of this relationship is determined by the strength of this connection, i.e. by the sum of all walks from to of length . Note that is also referred to as the Generalized Impulse Response Function (GIRF). It is generalized because it is not concerned with identification, but the derivative is taken with respect to (potentially correlated) reduced form errors in .

Fig. 1 provides an example. It depicts the Granger-causality pattern for the process in Eq. 1 and the network from Section 2.1. Each panel shows the network connection from to at different orders , , in blue, the decaying series for in red, and their product, the GIRF, in purple.151515I take purely for illustration purposes. As discussed in Section 2.2.2, it is not required for stationarity. By definition, the contemporaneous responses to all but a series’ own innovation are zero. From horizon onwards, the GIRF for every pair is proportional to the network connections from to of relevant order.

Notes: Panel shows in blue, in red and in purple.

Two points are worth highlighting. First, the relation between the shocked and responding unit in the network shapes not only the strength of the impulse-response, but also its timing. For example, while unit 2 is directly linked to unit 1 and therefore experiences the latter’s innovation with a lag of one period, unit 3 only has an indirect, second-order connection to unit 1 and is therefore impacted by its innovation only after two periods. Second, lagged network interactions can be a source of persistence, at the individual and aggregate level. Even without self-links – – and autocorrelation in disturbances , still persistently reacts to changes in and because of lagged spillover and spillback effects. For example, unit 3 is linked to 2, which itself is linked to unit 3. Therefore, after an initial adjustment to its own disturbance, unit 3 experiences further rounds of adjustments because its initial response led to a response of unit 2.161616For larger networks, such second-round responses can surpass the initial response and lead to a hump-shaped response. Generally, if unit has weak lower-order connections to but strong higher-order connections, we can have but for some and . This is behind the endogenous business cycles in Long and Plosser (1983).

These results relate to the discussion in Dufour and Renault (1998), who point out that Granger-causality can take the form of chains. Specifically, even if a series does not Granger-cause a series at horizon 1, under the presence of a third series , might Granger-cause at higher horizons as the causality could run from to to . They examine conditions under which noncausality at a given horizon implies noncausality at higher horizons. If innovations transmit only via bilateral links, these generally non-trivial conditions boil down to the existence of network connections of relevant order between the concerned variables (units under cross-sectional time series).

While useful for theoretical work such as Long and Plosser (1983) and Golub and Jackson (2010), the process in Eq. 1 is of limited use empirically as it entertains a very restrictive mapping between network connections and observed dynamics in . First, it presumes innovations travel through the network at the speed of one link per period, i.e. that the frequencies of network interactions and observation are equal. For instance, this implies that firms in sector do not adjust their price in response to price increases by suppliers situated two positions upstream of (suppliers of suppliers) earlier than with a lag of two periods.171717It also implies that their initial response cannot occur later than with a lag of two periods. Second, it assumes complete transmission at a single lag. For example, after a price increase by a supplier-sector , firms in sector fully adjust their own price after one period. Subsequent adjustments occur only to the extent that is also a supplier to other suppliers of , whose adjustments to induce further adjustments of . In the following, I extend the simple process above along both of these dimensions.

2.2.2 General Model: NVAR()

Let the cross-sectional time series evolve according to

| (2) |

with . This is a particular version of the network-autoregressive process in Zhu et al. (2017). I dub this process NVAR(). Compared to Eq. 1, setting allows connections of order lower than to affect dynamics at horizon .

Proposition 1 (Granger-Causality in NVAR()).

Let evolve as in Eq. 2. Assuming , Granger-causes at horizon iff there exists a connection from to of at least one order , where .181818See Proposition 2 and its proof in Appendix A. rounds up to the next integer.

The proof in Appendix A establishes that the GIRF is of the form

| (3) |

The coefficients are polynomials of . They show the importance of different connection-orders for the impulse response at a given horizon . Eq. 2 specifies that is shaped by lagged network interactions, whereby innovation transmission along a bilateral link takes periods to fully materialize.191919By this I mean the transmission from one unit to another disregarding the responses of other units. This transmission constitutes the whole impulse-response if two units do not share any higher-order connections: if , but , then for and zero otherwise. As elaborated on below, can be thought of as the overall strength of innovation transmission, while the individual elements in show the time profile of this transmission.202020They are allowed to be negative. For example, under , with signifies an initial overreaction and subsequent correction of unit ’s series after an innovation at units to which is connected. Note that it is assumed to be the same for all unit pairs .

The process evolves at frequency , which I shall call the network interaction frequency.212121As Eq. 2 and Eq. 3 make clear, denotes a frequency at which innovation transmission occurs over a set of time intervals, all of which are of integer length. If transmission happens at regular intervals, is simply the frequency at which it takes one period of time for an innovation to transmit (partially) along a direct link from one cross-sectional unit to another. However, as the subsequent discussion shows, under Normality of , is not unique, but one can write the process at an integer-multiple frequency of without changing its distributional properties. It might not coincide with the frequency of observation. In particular, if data is observed at a lower frequency than network interactions occur – as is likely the case for macroeconomic series –, then dynamics at horizon can be driven by connections of order higher than , as several rounds of transmission can happen in one period of observation. In addition, this leads to network-induced cross-sectional correlation in observed innovations even in absence of correlation in . In the following, I formalize this idea, first for stock, then for flow variables. Let the observed data be and assume .

Time-Aggregation of Lagged Transmission Patterns

If is a stock variable, we can write for some , i.e. we observe a snapshot of every periods. The dynamics of are represented by the state space system

| (4) | ||||

I dub this process NVAR() (for stock variables).

If , observational frequency either coincides with network interaction frequency () or is an integer-multiple thereof, which means that all are observed. Under Normality of , dynamics of are represented by an NVAR(), with :

For example, if network interactions occur at quarterly frequency, but observations are monthly, we have , and the observed monthly series depends on its value three months ago, six months ago, etc., up to months ago.

If , network interaction frequency is an integer-multiple of observational frequency such that we observe every periods. If is stationary,242424Section A.3 establishes that stationarity of the NVAR can be characterized in terms of eigenvalues of the network adjacency matrix and the time profile of network effects . dynamics of can be approximated arbitrarily well by the following restricted VARMA process:

| (5) |

for large and . The coefficients are polynomials of (or zero), and stacks all high-frequency innovations in-between the periods of observation and . The matrices are made up of blocks, all of which are polynomials in of the form of . Section A.2 illustrates for the case of and . For other cases with , the same result obtains as under .252525 We can write with and and deduce the process for by defining the auxiliary process . It is obtained by writing at the higher frequency given by as an NVAR(), as illustrated above. Then, contains a snapshot of every periods. This takes care of cases such as tri-weekly network interactions and monthly observations, or vice versa.

The time-aggregation of lagged transmission patterns has interesting implications for the mapping from network connectedness to dynamics. Consider . For ,

is composed of network-connections of order . Because is observed every periods, up to rounds of transmission can occur in one period of observation, and connections of order up to can matter at horizon . Regarding the innovations to the observed process, , we obtain that can be composed of connections of order , depending on which of the high-frequency innovations is behind the change in .262626If it is the first term, then network-connections do not matter: . If it is the second term, then only first-order connections matter: . If it is the last term, then connections of order matter. As a result, even if is not cross-sectionally correlated, there can be cross-sectional correlation in observed innovations if network interactions materialize at a higher frequency than data is observed.

If is a flow variable, we can write for provided that , i.e. the network interaction frequency either coincides with the observational frequency () or is an integer-multiple thereof.272727Analogous calculations apply if . Dynamics of are are represented by the state space system

| (6) | ||||

This is the NVAR() for flow variables. Analogous conclusions about the dynamics of can be drawn as in the case of stock variables.282828Again, can be approximated by a restricted VARMA process analogous to above. Also, can be composed of network-connections of order , depending on which of the terms in is responsible for the change in . Again, for , connections of order can matter, depending on which of the terms is behind the change in . Section A.2 contains details. For , no state space representation can be found for without assumptions that allow us to convert a flow variable from lower to higher frequency.

Contemporaneous Innovation Transmission Via Bilateral Links

The NVAR abstracts from contemporaneous network interactions, which feature prominently in the econometric literature on Spatial Autoregressive (SAR) models and the macroeconomic literature on production networks. In that case, the implicit assumption is that connections of all order materialize in any given period of observation:

Contemporaneous interactions rationalize the cross-sectional comovement among as the network-induced amplification of cross-sectionally uncorrelated, idiosyncratic shocks . Ultimately, contemporaneous interactions concern shock identification, which is not the focus of this paper. Instead, the interest lies in how networks shape innovation transmission over time, regardless of the origin of these innovations.

Contemporaneous links are useful for quantifying overall connectedness via networks, but they are silent on how networks drive dynamics.292929At least in absence of further structure, such as provided by a dynamic macroeconomic model with intertemporally linked optimization problems of agents who are impacted by disturbances to . In this case, even though within the same period idiosyncratic shocks travel through the whole network and effects of all order play out, agents can smooth adjustment to these (amplified) shocks over several periods. With contemporaneous network interactions, networks can only amplify dynamics but not cause them. Nevertheless, models with contemporaneous and lagged network interactions are related. By Proposition 8 in Section A.4, the (contemporaneous) response of to a (transitory or persistent) innovation to under contemporaneous interactions is equal to the long-run response of to a persistent innovation to under lagged interactions in a corresponding NVAR(). Specifically, for

we have

provided is stationary. Both responses are given by element of the Leontief inverse , which is a sufficient statistic for the long-term (or overall, static) cross-sectional comovement of interest. The difference between the two specifications is that, by taking a stance on the time profile of network interactions, contains information on how any such long-term effect materializes over time. In contrast, the timing of interactions is irrelevant if the interest lies only in steady state comparisons rather than transition dynamics. As shown in Section A.4, the same result applies even if only a snapshot or an average of realizations from such an NVAR() is observed every periods, .303030If sums are observed, the long-term response is scaled up by .

Note that the timing of the long-term response to a permanent shock provides evidence on the timing of this impulse-response more generally, regardless of the nature of the shock. This is because for any VAR, the response to a permanent shock is equal to the cumulative response to a temporary shock (to the same variable). Therefore, the fraction of the long-term response which materialized until horizon is equal to the area under the IRF to a temporary shock until horizon as a fraction of the total area. As a result, a slow long-term response to a permanent shock implies a persistent response to a temporary shock.

3 Inference

The NVAR can be used to estimate dynamic peer effects or model high-dimensional (cross-sectional) processes more generally, say for forecasting purposes. In either case, one might have data on the network and be willing to condition on it, or one might prefer to infer it from the data. In Section 3.1, I discuss the estimation of the time profile of network effects , conditioning on . In Section 3.2, I discuss joint inference on , with identified from dynamic cross-sectional correlations in the data, possibly aided by shrinking towards observed network links.

3.1 Timing of Network Effects

The first part of this section is devoted to the estimation of in the NVAR(). The second part deals with the case when data is observed at a higher frequency than network interactions take place, i.e. stock variables in the NVAR() with and flow variables in the NVAR() with .313131 The case of stock variables in the NVAR() with is subsumed in the first part (with straightforward adjustments), as all relevant realizations of the underlying NVAR() are observed, at least if the process is Gaussian. Also, under Gaussianity, the case of stock variables with can be written to fit in the second part. See Section 2.2.2. Details are in Section B.1.

NVAR()

The NVAR() from Eq. 2,

can be written as a linear regression:

| (7) |

where the matrix summarizes the information in lags of using first-order network connections:

| (8) |

Because the network is taken as given, the dependence of on it is suppressed.

Defining , we obtain the following Least Squares (LS) estimator for :

| (9) |

As usual, it is also the Maximum Likelihood (ML) estimator under Normality of and the posterior mean and mode under a Uniform prior for . Under , it yields the Ordinary LS (OLS) estimator, which takes the form of a pooled OLS estimator:

Section B.1 establishes consistency and asymptotic Normality of under large , large and large asymptotics. The derivations under large assume that the observed network adjacency matrix converges to some limit so that, for example, .

NVAR() with

As discussed in Section 2.2.2, if follows an NVAR() and a snapshot of is observed every periods, i.e. for , the dynamics of are represented by the state space system from Eq. 4:

and similarly if and are flow variables and for is observed (see Eq. 6).

In principle, an estimator for could be obtained by data augmentation. However, point identification is not guaranteed. For example, under and , the observed process follows

which suggests that is identified only up to sign. The identification problem is akin to estimating an AR() observed every periods, discussed in Palm and Nijman (1984),323232For that case, calculations in Section B.1 suggest that for general , under , the vector is jointly identified only up to sign. or estimating continuous time models using discrete time data (see e.g. Phillips (1973)). As in these cases, the mapping between the parameters in the high-frequency process and the parameters in the observed process is not bijective.333333Recall that, as discussed in Section 2.2.2, the observed process can be approximated arbitrarily well as a VARMA with coefficient-matrices equal to polynomials of .

As a remedy, Palm and Nijman (1984) suggest adding prior information. Recall that is the GIRF for units and that only share a first-order connection (see Section 2.2.2). The following prior induces smoothness in this GIRF by shrinking to a quadratic functional form:

This leads to the full-sample posterior

where , and is the analogue of for .

Conditioning on , and , the posterior can be obtained by treating the unobserved data in as parameters and finding first the joint posterior . This is implemented numerically using the Gibbs sampler of Carter and Kohn (1994), by iteratively drawing from and . As , the resulting posterior mode of converges to the ML estimator obtained using the Expectation-Maximization (EM) algorithm. Due to the identification problem, this mode may not be unique. For , the suggested Bayesian approach traces out all the modes and shows the extent of the identification problem. For , it remedies the identification problem as the posterior mean weighs these modes by shrinking to the quadratic function .

Using a hierarchical Bayes approach, the exact function to which is shrunk and the optimal amount of shrinkage can be inferred from the data by specifying uniform hyperpriors for and . As discussed in Giannone et al. (2015), under uniform hyperpriors, the shape of the posterior of hyperparameters coincides with that of the marginal likelihood, a measure of model fit and out-of-sample predictive ability. This leads to Normal and Gamma conditional posteriors:

where stacks along rows. The joint posterior is then obtained by augmenting the above Gibbs sampler with two additional iteration steps, drawing from and . Fixing , we impose , and the posterior mode of converges to the ML estimator for from the EM algorithm.

To estimate , an additional step is added to the Gibbs sampler. Using a uniform prior, we get an Inverse-Wishart conditional posterior:

where the matrix stacks along rows. Its mode is .

3.2 Joint Estimation: Network & Effect-Timing

No matter whether one is interested in estimating dynamic peer effects or approximating dynamics of cross-sectional processes, in many cases network data might be missing or it appears restrictive to condition on the available data. This section discusses joint estimation of . Again the first part deals with the estimation of an NVAR(), while the second part discusses the case of an NVAR() with .

NVAR()

To facilitate the estimation of , the NVAR() from Eq. 2,

can also be written as the linear regression

| (10) |

whereby , and the matrices , and stack , and along rows, respectively. To simplifty notation, I suppress the dependence of on and that of on .

To render jointly identified, I normalize . Alternatively, one could fix one to some value, with appropriate redefinitions of as well as , and . As elaborated on below, the former normalization is easier to implement. The latter facilitates asymptotic analysis, but requires in the true data generating process.343434Also, if is imposed, it requires knowledge on the sign of .

Suppose data on a network with elements is available. Under independent priors , we obtain a matrix-variate Normal conditional posterior for :

Its mean and mode, , is equal to the conditional optimizer for under a LS objective function with a Ridge-penalty:

| (11) |

As , the conditional posterior converges to a pointmass at . As , is inferred from the data alone. No domain restrictions on are imposed because any parameter value can be rescaled to yield , so that can be interpreted as a network.353535To enforce even under low , must be imposed. This leads to the high-dimensional Normal posterior being truncated to and considerably complicates the analysis, as both computing the mode and drawing from this distribution is computationally intensive. A Normal rather than Laplace prior (i.e. a Ridge rather than Lasso penalty) is chosen for analytical convenience.363636Under a Laplace prior, the posterior and its mode – the Lasso estimator –can only be derived analytically when imposing and shrinking to . Drawing from the resulting truncated matrix-variate Normal is computationally intensive. Imposing to be diagonal, its mode can be obtained by iterating on analytical expressions for a column of given all other columns.

Conditioning on , the joint posterior is again obtained by Gibbs sampling, iterating on the conditional posterior from above as well as and from Section 3.1. To impose the normalization , draws from are appropriately rescaled in every iteration. Setting , the posterior mode is equal to the GLS estimator (, obtained by iterating on and the conditional optimizers and of the objective function in Eq. 11 above. Fixing in addition , we obtain the OLS estimator of , for which consistency and asymptotic Normality under are established in Section B.2.

Analogously as done for and , under hierarchical modeling and a uniform or improper prior for , we obtain

The joint posterior is obtained by iterating on the six conditional posteriors.373737This suggests a possible way to select in a frequentist implementation: as part of the iterations on the conditional estimators and (and ) from above, add a step setting , the mode of . The resulting maximizes the MDD and hence out-of-sample predictive ability. See Giannone et al. (2015). As , we condition on the network , just as done in Section 3.1 above.

The network can be constructed as a combination of multiple link-types. Collecting the latter in the vector , we can set . To infer the network that best rationalizes the data, augment this specification with hyperpriors and . This results in conditional posteriors

where is s.t. . As , the conditional posterior of converges to a pointmass at zero and links are shrunk to zero. As , the conditional posterior of is centered at the OLS estimator from a regression of on .

NVAR(p,q) with

As in the estimation of , under an NVAR() with , joint inference on can be conducted relying on data augmentation. The joint posterior is obtained using the Gibbs sampler of Carter and Kohn (1994). As before, identification from data alone is not guaranteed, but the problem is ameliorated by shrinking to a known functional form and to a known or sparsely parameterized network . Note that the identification problem is irrelevant if only properties of the process at observational frequency are of interest.

4 Input-Output Links & Sectoral Price Dynamics

How do price innovations propagate across sectors in an economy? Given an observed price increase in, say, energy-related sectors, what is the expected path of aggregate prices? With sectors linked by an input-output network, the answers depend on the positions of the shocked (and responding) sector in the network as well as on the velocity at which a shock travels through the network.

The literature so far mostly assumed contemporaneous input-output conversion to show that the supply chain network amplifies idiosyncratic sectoral shocks – with stronger amplification for more central sectors – and that input-output linkages can rationalize the comovement of sectoral prices at a given point in time. Exceptions are Long and Plosser (1983) and Carvalho and Reischer (2021), who assume one-period-lagged input-output conversion. The former show that this leads to endogenous business cycles, while the latter characterize aggregate persistence in this theoretical model and show that it matches well empirical measures of persistence. In the following, I allow for more general lags in input-output conversion and estimate to what extent it can account for persistence in aggregate prices and, hence, whether input-output linkages can rationalize also the dynamic comovement of sectoral prices over time.

Consistent the literature, I consider the propagation of relative price changes induced by supply-side TFP shocks, as motivated by an input-output economy in the Real Business Cycle (RBC) tradition. Assuming that firms’ production in each sector requires the inputs produced in other sectors in the past periods, sectoral prices and output in this economy evolve at some model-frequency according to an NVAR(). The network is the input-output matrix, while show how input-sourcing is spread out over the periods. By estimating as well as the frequency of input-output conversion relative to my monthly frequency of observation, I determine the role of lagged input-output conversion in driving the observed dynamics of sectoral prices.

After theoretically motivating the analysis in Section 4.1, I discuss the data in Section 4.2 and the estimation procedure in Section 4.3. Results are presented in Section 4.4.

4.1 Theory

This section extends a benchmark input-output economy by introducing time lags in input-output conversion. The analysis is based on Carvalho and Tahbaz-Salehi (2019), who discuss a static economy. Details are provided in Section C.1.

Assume there are sectors, in each of which a representative firm produces a differentiated good by combining labor services and goods produced by other sectors , , using a Cobb-Douglas production function. Firms maximize profits, taking prices as given. The profits of firm in period are

where , and . denotes TFP in sector and the price of labor. is the amount of good used in the production at time . As discussed below, it can differ from the amount of good purchased in period , . shows the importance of good in the production of good . Under perfect competition and constant returns to scale (CRS) Cobb-Douglas production functions, prices are entirely determined by supply. Nevertheless, to show that the following results hold in general equilibrium and to obtain results for output dynamics, in Section C.1 I assume a representative household which supplies one unit of labor inelastically and exhibits log-preferences over the goods.

Different assumptions on the timing of input-output conversion lead to different dynamics of sectoral prices and output in this economy. Let denote the use of good purchased at time in the production of good at time . Most of the literature assumes that inputs are converted into outputs in the same period when they are produced and purchased, i.e. . This leads to a static economy with contemporaneous network effects. Dropping time-subscripts, we obtain the following equation for sectoral prices as a function of sectoral productivities and input-output relations summarized by the input-output matrix :

where , and is a vector of constants. This equation fully characterizes prices in this economy, whereby wages are taken as the numéraire.

To analyze dynamics under lagged input-output conversion, I assume perfect foresight.383838As discussed in Fan et al. (2023), this assumption is standard for modeling dynamic spatial economies, which are closely related to dynamic network economies. If, as in Long and Plosser (1983) and Carvalho and Reischer (2021), it takes one period to convert purchased inputs into output, then and sectoral prices approximately follow an NVAR(1,1):

where . is a vector of constants, is a vector of ones, contains sectoral labor shares and is wage growth in period . This process only deviates from an NVAR() to the extent that the numéraire changes in value. This result can trivially be extended to input-output conversion at single lags of arbitrary length; if it takes periods to convert inputs into output, approximately follows an NVAR() with coefficients in front of all but the th lag equal to zero.

Differences between the steady states in this economy and the above economy with contemporaneous interactions vanish as firms’ discount factor . However, while the latter is always in steady state, this economy is dynamic and after a disturbance to only asymptotically converges to steady state. For empirical analyses one has to take a stance on what a period in this model signifies relative to an observational period in the data.

Dynamics are driven by several lags if firms in their production at time use inputs produced in several past periods. To model this case, I assume that aggregates quantities of input purchased at different periods in the past using a Constant Elasticity of Substitution (CES) aggregator. This shortcut stands for frictions like stochastic or time-varying input delivery time and storage capacity constraints.393939As in the Long and Plosser (1983)-economy above, the presumption is that storage is done by the buyer. To keep the exposition tractable, let include amounts of good bought at and , and :404040This means that a good perishes after two periods, at least with regard to its suitability as an input in production. Therefore, the amount of good purchased at time can be used in production at periods and : .

with , and . An extension to general lengths is straightforward. The homogeneity of parameters implies that the time profile of input-sourcing is constant over time and across input-output pairs .

In the Cobb-Douglas case , sectoral prices approximately follow an NVAR(2,1):

where . Again, this relation is only approximate to the extent that the numéraire changes in value.414141Note that is the wage growth from to . Under a more general elasticity of substitution, excluding the case of perfect substitutability (), a similar result is obtained by log-linearizing around the steady state. Let a hat denote percentage deviation from steady state. We obtain

The elements of are scaled bilateral links , while contains scaled TFP deviations , with . These scalings vanish under perfect substitutability, . The vector is composed of elements . Hence, for general elasticities of substitution , the process of sectoral prices differs from an NVAR(2,1) not only to the extent that the numéraire changes, but also as sectoral output changes. The output-term vanishes as .

To sum up, under general lags in input-output conversion, the log of sectoral prices, now denoted by , evolves at some model-frequency approximately as an NVAR():

with and , where is proportional to the vector of TFP shocks, and where contains input shares , with . These restrictions render the process stationary.424242Berman and Plemmons (1979, p. 37) show that for an element-wise nonnegative matrix with row sums strictly smaller than 1, the absolute value of the largest Eigenvalue is strictly less than 1. Stationarity then follows by Proposition 5 in Section A.3.

Several assumptions are crucial for this result. First, perfect competition implies that prices equal marginal costs and prevents strategic price setting. Second, Cobb-Douglas production functions imply constant input shares regardless of prices and prevent upstream propagation of TFP shocks. This makes clear that the rows of contain the production recipes for firms in each sector, which firms adhere to in every period. Third, input-sourcing is constant over time and across input-output pairs , which leads to a homogeneous .434343A difference to the (unrestricted) NVAR() from Section 2 stands out: the domain restrictions imply that the impulse response to a shock in sector has the same sign for all units . The model can nevertheless rationalize price movements in opposite directions because in the same period some sectors experience positive, others negative shocks, while the remaining sectors differ in the extent to which they are impacted by the two owing to different positions in the network.

4.2 Data

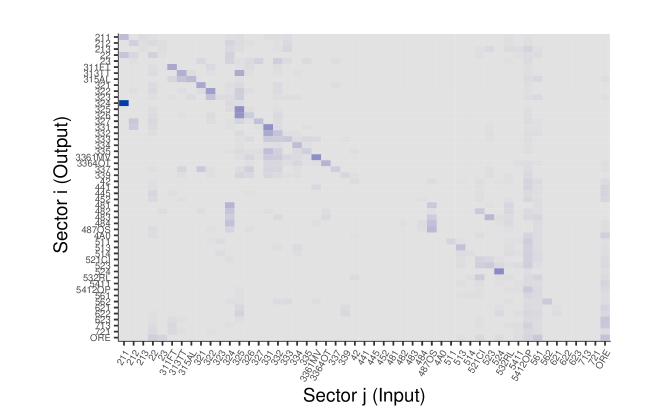

To construct , I use annual data on input-output matrices provided by the Bureau of Economic Analysis (BEA). Due to availability of PPI data, I consider the level of 64 mostly three- and four-digit sectors rather than the finer level of around 400 six-digit commodities (NAICS classification). The analysis is restricted to non-farm and non-governmental sectors. I take the input-output matrix for 2010, roughly the midpoint of the sample of sectoral Producer Price Indices (PPI) (see below). Following Acemoglu et al. (2016), links are calibrated as

where is the total value of goods and services purchased by sector from sector as determined by the corresponding entry in the BEA’s “use” table. The value of shows how many dollars worth of output of sector sector needs to purchase in order to produce one dollar’s worth of its own output.444444As discussed in Section C.1, the expression for in steady state changes slightly in economies with different lags of input-output conversion. For example, in the Long and Plosser (1983) economy, the above would need to be multiplied by , the inverse of the discount factor. Under Cobb-Douglas aggregation of inputs purchased in the past two periods, one would need to multiply by . For general CES aggregation, this constant is also a function of the elasticity . However, these differences in the proper calibration of vanish as . This calibration of assumes that firms’ input shares reported for the course of a year are equal to the unobserved input shares at higher frequency intervals.

Monthly data for the corresponding sector-level PPIs is obtained from the Bureau of Labor Statistics (BLS). Data availability narrows the analysis to 51 sectors and the time frame January 2005 - August 2022. This includes the Great Recession as well as the COVID-19 recession. More details on the matching of PPI and input-output data are provided in Section C.2.

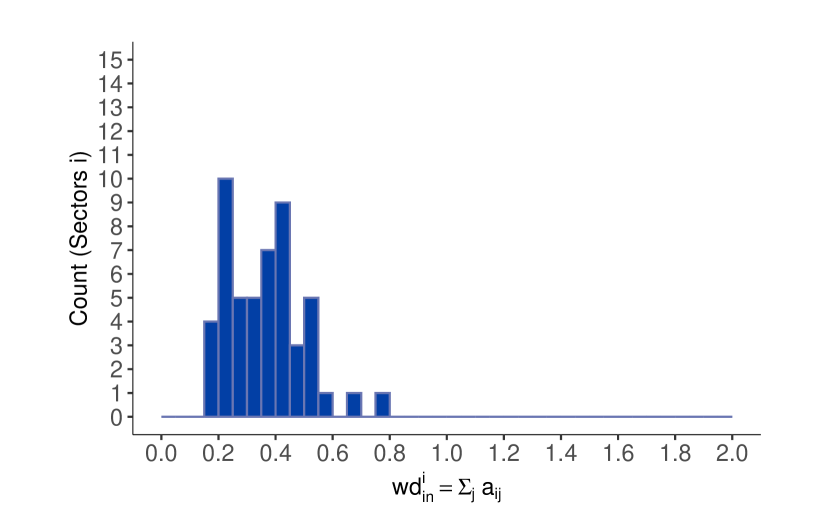

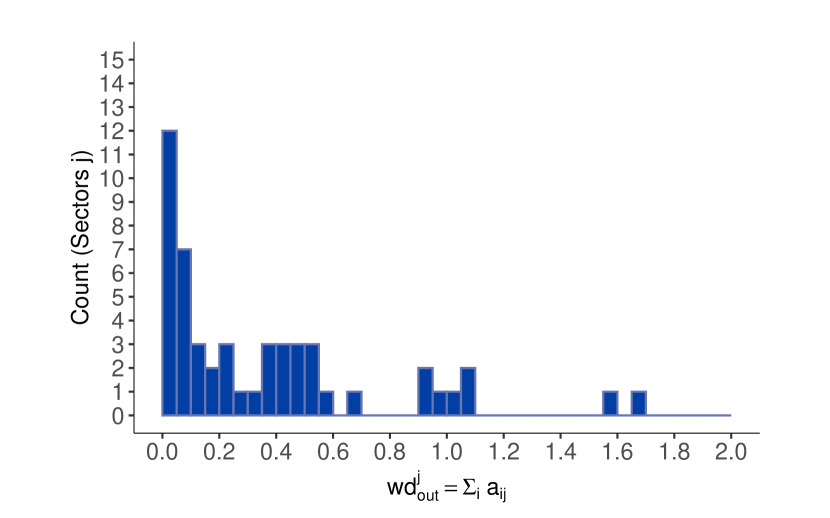

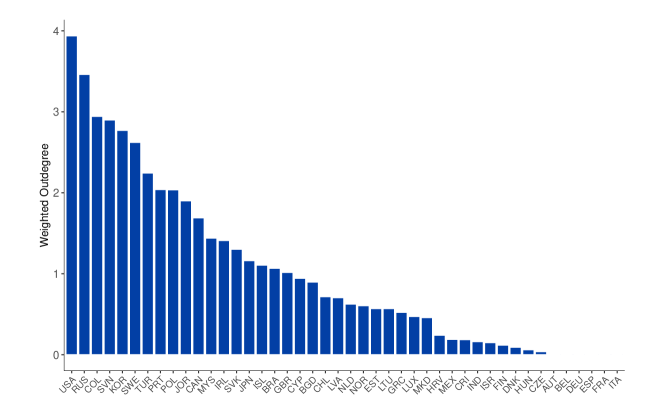

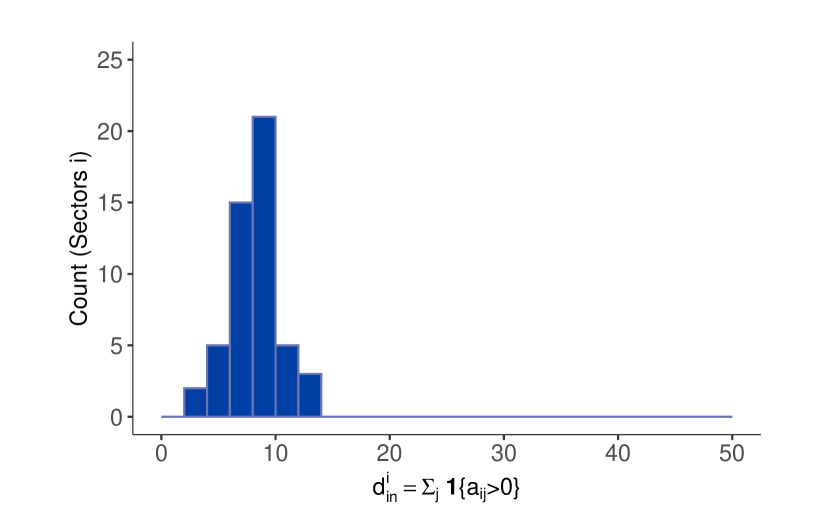

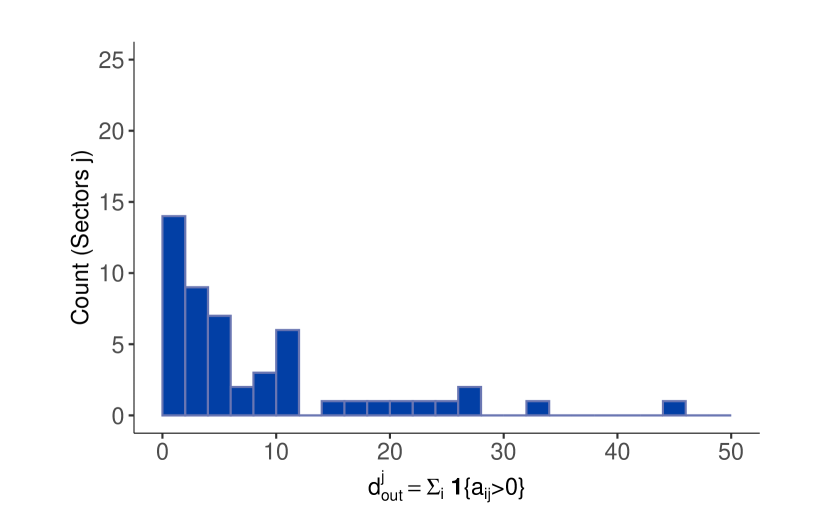

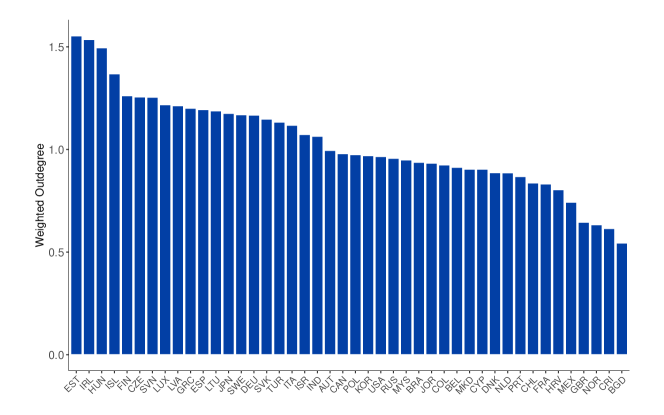

Notes: The left panel plots weighted in-degrees, equal to the column-wise sums of , which show the differing reliance on intermediate inputs across sectors. The right panel plots weighted out-degrees, equal to the row-wise sums of , which show the differing importance of a sector as a supplier to other sectors in the economy.

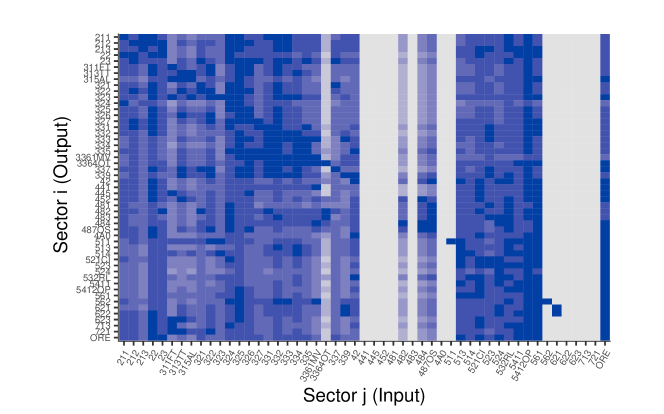

The majority of links in the network are weak. Even though the fraction of non-zero links is 73.55%, only 16.88% are above 0.01. Nevertheless, and as expected at this level of aggregation, this network density is much higher than the 3% reported for the finer level of 417 sectors in Carvalho (2014). As illustrated in the left panel of Fig. 2, weighted in-degrees, , lie below 1 for all sectors, as posited by theory. The heterogeneity in this statistic across sectors shows that they rely to different extent on intermediary inputs in production. The right panel shows the weighted out-degrees, , and illustrates that most sectors are specialized input-suppliers, while there are also a few general-purpose suppliers. The average distance in the network is 2.41. This means that each sector is on average 1.4 in-between suppliers away from other sectors. The longest distance, or diameter of the network, is 7, which means that it takes at most 6 in-between suppliers for a sector to reach another sector. Section C.2 contains more details on input-output data.

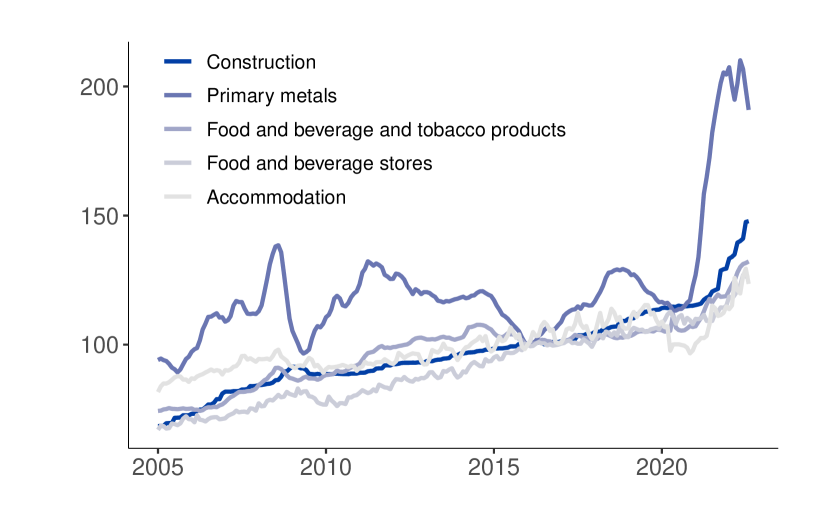

The left panel in Fig. 3 depicts the raw PPI series for a few sectors. It provides evidence of considerable heterogeneity in price dynamics across sectors, even disregarding the highly volatile energy-sectors.454545Table A-1 in Section C.2 lists the means, standard deviations and ranges of sectoral PPI changes. The right panel of Fig. 3 shows that an output-weighted average of sectoral PPIs included in the analysis replicates the actual aggregate PPI fairly well, despite the fact that some sectors are excluded due to data limitations.464646The aggregate PPI is obtained from the FRED database of the Federal Reserve Bank of St. Louis. Weights are constructed using sectoral output in 2010. Aggregate PPI shows a clear upward trend, with a smaller spike around the Great Recession as well as a very pronounced spike in the aftermath of the COVID-19 recession.474747The latter is included in the analysis because it contains potentially valuable information on how price shocks transmit through the input-output network. To render the PPI series stationary, I estimate and subtract a linear trend and a seasonality component for each sector .484848Given the raw series of the natural logarithm of PPI in sector , , I estimate where is the indicator function. In turn, I set and base the subsequent analysis on . In the theoretical model, any time trends in sectoral prices are due to idiosyncratic trends in sectoral TFP levels amplified by the network. However, for these trends the timing of network effects is irrelevant, just as it is irrelevant for the steady state. Therefore, given the goal of the present analysis, no information is lost by subtracting time trends.

Notes: The left panel shows the raw PPI series for a few selected sectors. The right panel compares the aggregate PPI from the FRED Database and the output-weighted average of PPIs of sectors included in the analysis.

Suggestive evidence that network proximity does not only have implications for the contemporaneous cross-sectional correlation of price changes across sectors, but also for dynamic correlations is provided in Fig. 4. The lightest-blue line plots the contemporaneous correlation of prices in two sectors against their distance(s). It reproduces for prices the finding in Carvalho (2014) that sectoral comovement decreases with the distance between sectors, although this relationship is much less pronounced at the higher level of disaggregation analyzed here. However, it is not only the contemporaneous comovement between sectors that decreases with distance, but also the comovement of sector ’s inflation with lagged values of sector ’s inflation is declining with the distance from sector to sector . This is illustrated by the remaining lines in Fig. 4, which show this correlation for lags ranging from one to twelve months in darker shades of blue. In fact, the downward slope is more pronounced for higher lags.494949Note that Fig. 4 plots mean correlations by distance and masks plenty of heterogeneity across sector-pairs.

Notes: The figure plots the average correlation of sectoral prices for different distances between them. The lightest blue line refers to contemporaneous correlations. Darker lines show the average correlation of a sector with lagged values of a sector as a function of the distance from to . Lags range from 0 to 12 months. The series refer to de-trended and de-seasonalized log PPIs.

4.3 Estimation

The theoretical analysis in Section 4.1 suggests that sectoral prices at some model-frequency evolve (approximately) as an NVAR():

Relative to the unconstrained estimation of discussed in Section 3.1, the model from Section 4.1 restricts and . To accommodate these restrictions, I drop from and impose the domain restrictions for and . For now, I assume that is uncorrelated across and with .

I consider Bayesian estimation of under Uniform priors for and . As a result, the posterior mode is equal to the Maximum Likelihood Estimator. The prior for is truncated to satisfy the additional domain restriction . The posterior is obtained numerically using the Sequential Monte Carlo (SMC) algorithm. Details are in Section C.3.

I allow the frequency of network interactions to differ from the frequency of observation and infer their relation from the data by model selection criteria. As in Section 2.2.2, let denote the observed series. I consider , which under monthly observations corresponds to quarterly, bi-monthly, monthly, bi-weekly and weekly network interactions, respectively. Also, I allow for lags up to 6 months to matter for dynamics.

4.4 Results

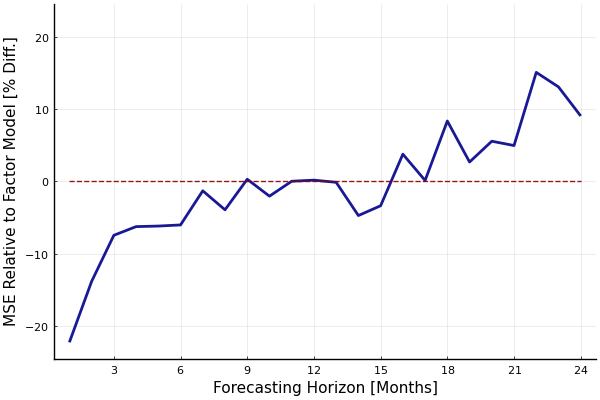

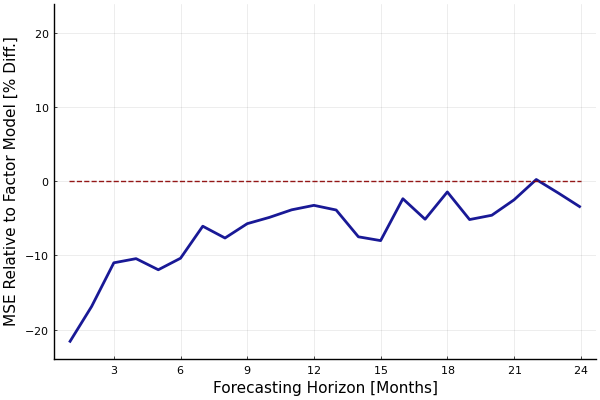

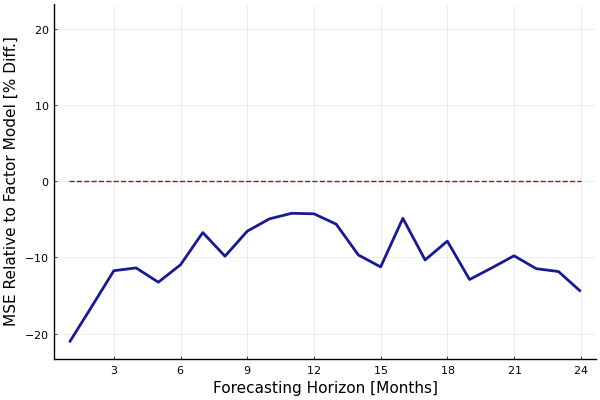

Table 1 reports the Marginal Data Density (MDD) for different specifications of the NVAR. The most preferred specification features monthly network interactions and lags up to six months. Model selection according to the Bayesian or Akaike Information Criteria lead to the same conclusion (see Table A-2). The subsequent analysis is based on this preferred NVAR().

| 1/3 | 19079 | 19044 | |||||

| 1/2 | 19384 | 18768 | 18690 | ||||

| 1 | 20153 | 20056 | 19675 | 19879 | 18899 | 20218 | |

| 2 | 17546 | 19570 | 19248 | 20142 | 18662 | 19636 | |

| 4 | 18517 | 19808 | 19754 | 19655 | 18904 | 19301 | |

| Notes: The table shows values for the natural logarithm of the Marginal Data Density (MDD) across model specifications. The values for (from top to bottom) refer to quarterly, bi-monthly, monthly, bi-weekly and weekly network interactions, respectively, while implies that the last months matter for dynamics. | |||||||

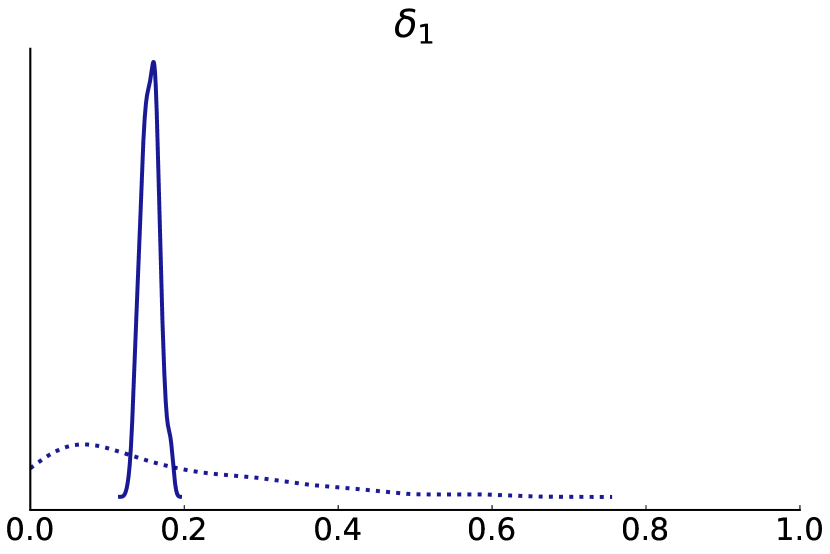

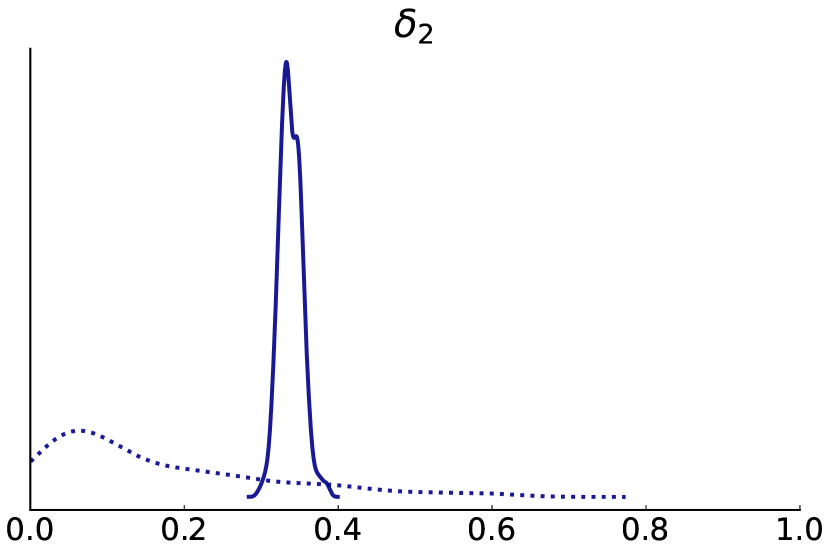

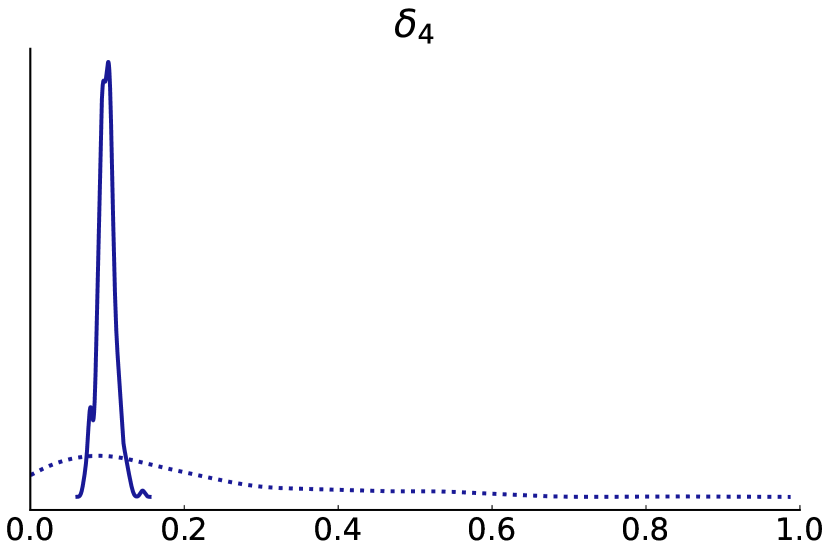

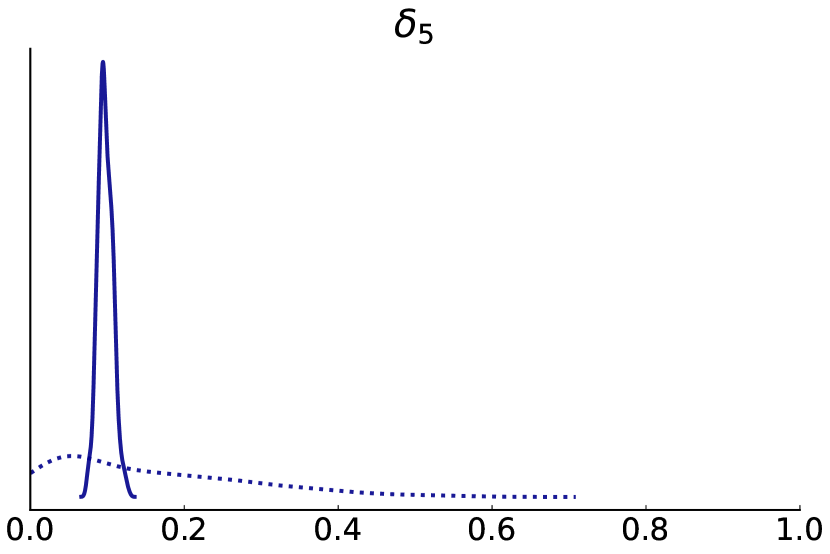

Table 2 reports the estimation results for . The first column shows the posterior mode or MLE, approximated by the Maximum A-Posteriori (MAP) estimator, i.e. the posterior draw (particle in the SMC algorithm) with the highest likelihood and posterior. It is very close to the posterior mean, reported in the second column. The tight 95% Highest Posterior Density (HPD) intervals – shown in columns three and four – together with the peaked marginal posteriors – shown in Fig. A-4 – illustrate that is estimated very precisely. This is not surprising as there are observations and only parameters.

| MAP | Mean | Low | High | |

| 0.1550 | 0.1557 | 0.1370 | 0.1745 | |

| 0.3460 | 0.3382 | 0.3168 | 0.3605 | |

| 0.2816 | 0.2865 | 0.2644 | 0.3129 | |

| 0.0915 | 0.0991 | 0.0785 | 0.1174 | |

| 0.1045 | 0.0975 | 0.0837 | 0.1135 | |

| Notes: The first column shows the Maximum Likelihood or Maximum A-Posteriori (MAP) Estimator, the second refers to the posterior mean, and Low and High report the bounds of the 95% Bayesian HPD credible sets. | ||||

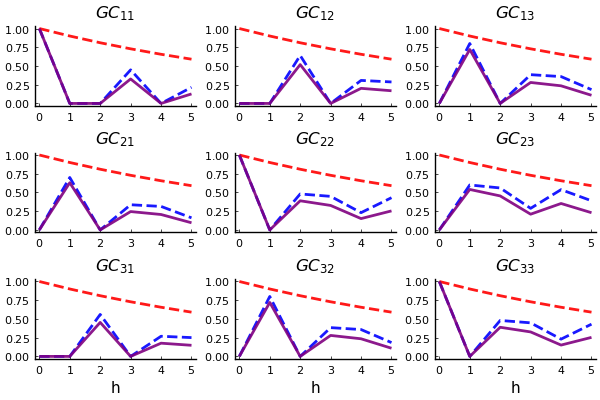

The dynamics of can be summarized by impulse response functions (IRF). By Section 2.2, under an NVAR(), the impulse response of at horizon comprises supply chain connections of order , with :

| (12) |

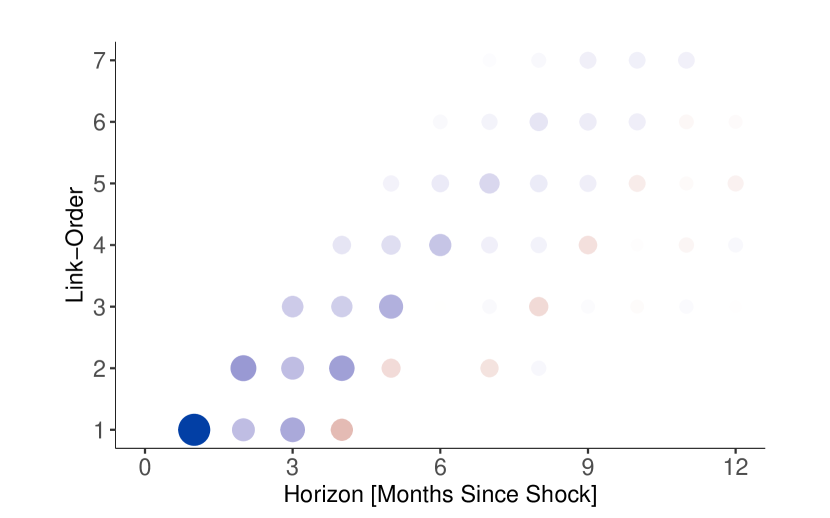

The coefficients are functions of and show the importance of (upstream) supply chain connections of different order for the response of sectoral prices at any one horizon . As the analysis abstracts from hetereogeneity in , these coefficients are constant across time and sector-pairs.

Fig. 5 illustrates this composition of impulse responses. The dots in the top left panel depict the coefficients with horizons on the x-axis and connection-orders on the y-axis. Higher values are represented by larger and darker dots. As stated above, under for , orders matter for propagation at horizon . Hence, there are dots aligned vertically at horizon . As time passes, a shock spreads through the network and reaches more distant nodes. The estimated determine the exact width and speed of this propagation, illustrated by the differing sizes and colors of the dots.

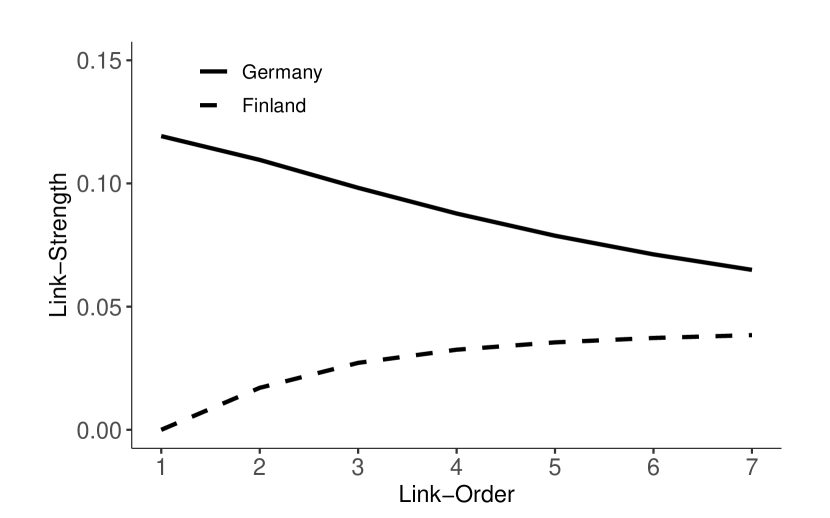

Notes: The top left panel shows the importance of different connection-orders for shock transmission as a function of the time elapsed since a shock took place. The top right panel shows the supply chain connections of different order from the sectors “Chemical Products” and “Truck Transportation” to the utilities sector, and the bottom panels show their resulting IRFs to an increase in the price of utilities by one standard deviation.

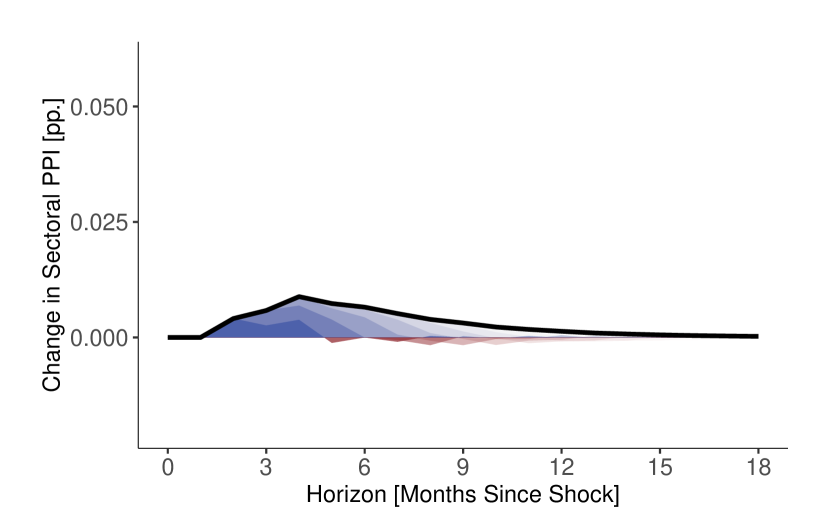

The top right panel in Fig. 5 shows the strength of network connections of different order from the sectors “Chemical Products” and “Truck Transportation” to the sector “Utilities”, respectively. The former sector is more dependent on utilities as a supplier than the latter, as evidenced by stronger network connections, in particular of first and second order. As Eq. 12 above makes clear, such network-connections are the second building block of impulse responses in the NVAR.

The lower panels of Fig. 5 illustrate the resulting impulse responses. The different shades of blue depict the individual terms , which show the contribution of network-connections of order to the impulse-response of to at horizon . Darker shades refer to network connections of lower order. As a result of its stronger network-connections to the utilities sector, the price of chemical products reacts more strongly to a one-standard deviation increase in the price of utilities than does the price of truck transportation. The price of chemicals rises quickly and peaks after two months. In contrast, the price of truck transportation increases slowly and remains slightly elevated without a noticeable peak. It is in particular the direct and second-order supply-chain connections that make up the difference between the two responses, in line with the top right panel. Longer-term responses are driven by higher-order connections and after nine months they are of similar size for the two sectors as they share similarly strong higher-order connections to the utilities sector.

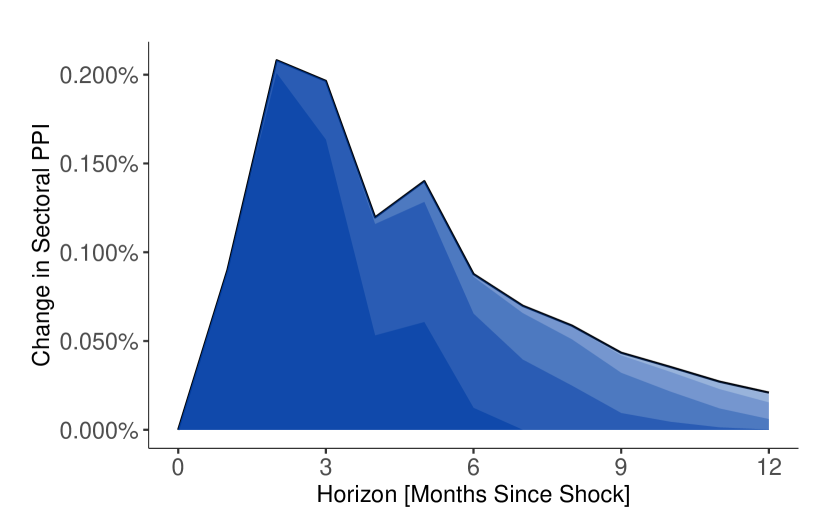

Existing literature uses a static framework of contemporaneous input-output conversion which shows that the effects of sectoral TFP shocks on aggregate prices are stronger for sectors with more central positions in the supply chain network. As discussed in Section 2.2, because , the effects under that framework are equal to the long-term responses of prices to permanent shocks in the present NVAR. As opposed to the static framework, the NVAR provides information on how the effects of a sectoral TFP shock on prices unfold over time. In the following, I focus on the responses of aggregate PPI, but the same analysis could be conducted for sector-pairs .

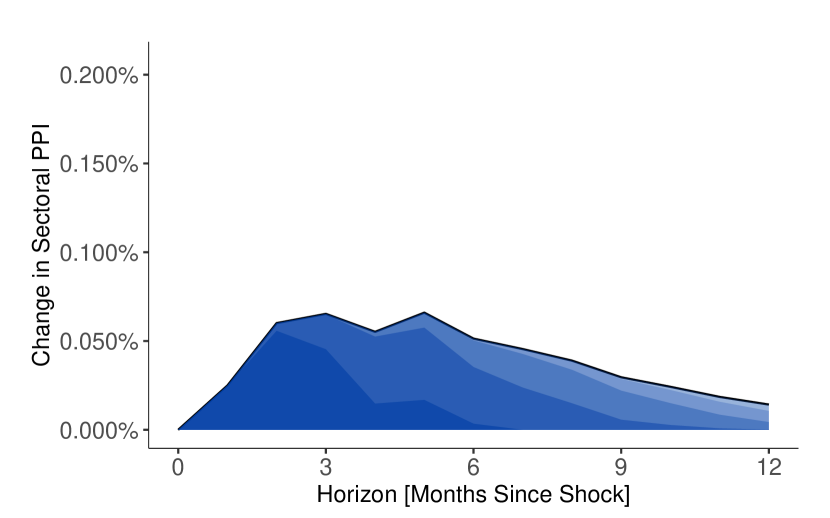

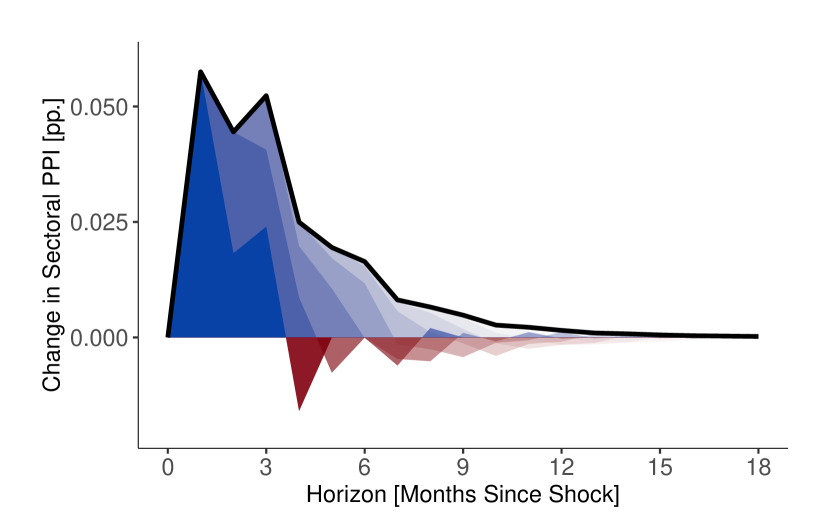

Notes: The left panel shows the time profile of the effect of sectoral price disturbances on aggregate PPI for a few selected sectors. The right panel relates the strength of the effect on aggregate PPI to its timing. The shock sizes are equal to one standard deviation of the respective sectoral disturbance.

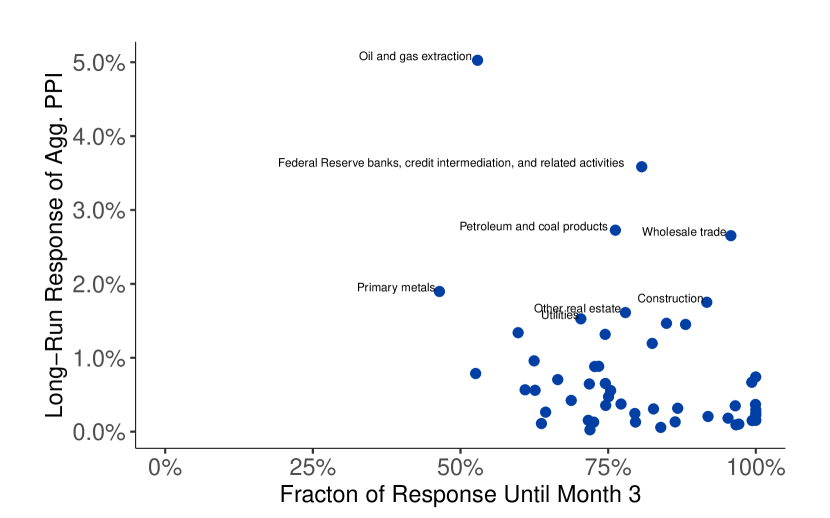

The left panel of Fig. 6 shows the time profiles of aggregate PPI responses to price increases in different sectors. It suggests that sectors differ in the speed at which they impact aggregate PPI. For example, the response of aggregate PPI to a shock to wholesale trade prices materializes rather quickly, while its response to an increase in the price of oil and gas extraction takes time. As revealed by the IRF discussion above, this is because wholesale trade connects to other sectors mostly as a direct or lower-order supplier, while the oil and gas extraction sector sits further upstream in its supply-chain relationships. In case of the aggregate PPI, the relevant counterpart is a weighted average of customer-sectors, with weights given by their contribution to aggregate output.

The right panel of Fig. 6 plots the strength of aggregate PPI responses against the fractions which materialize during the first quarter after the shock. Although stronger effects tend to take more time to realize, there is no clear relationship between the strength and timing of responses. For example, the construction and primary metals sectors have similar long-term effects on aggregate prices because other sectors (or the output-weighted average of them) have similar “overall” connections to both, as judged by the sum of connections of all order in the Leontief inverse.505050Put simply, when summing up the connections of all order from sectors to the construction sector and forming the weighted average using sectors’ output contributions, one gets a similar number as for the primary metals sector. See the expression for the Leontief inverse in Section 2.2. Yet the impact of price increases in the construction sector materializes much more quickly since this sector is more relevant as an immediate supplier to relevant sectors in the economy compared to the primary metals sector.

In sum, the present analysis confirms the result from the existing literature that the stronger the connections from sector to sector , the more pronounced is the response of sector ’s PPI to a price shock in sector . In addition, the analysis suggests that how fast sector responds depends on the importance of sector as a more immediate – rather than further upstream – supplier to sector . The exact mapping from network-connections to impulse responses is determined by the extent to which connections of different order matter at different horizons. This is true not only for prices in a sector , but also for a weighted average of sectoral prices, such as the aggregate PPI.

5 Forecasting Global Industrial Production Growth

How does economic activity co-move across countries? Given an expansion in one country, how do we expect economic activity in other countries to react? The international economics literature has long been interested in spillover and spillback effects across countries and the transmission of US shocks in particular. In this section, I shed light on global business cycles from a novel perspective, by assuming that the dynamic comovement in economic activity across countries is the result of bilateral connections, which I estimate. This is in starkest contrast with factor models, which in this context posit that it is the result of exposure to a few influential economies.

The previous section examined a case where an observed cross-sectional time series is arguably driven by one particular network of bilateral links for which data is available, and the interest lies in quantifying how network effects materialize over time. In this section, I consider the case where no network data is available, yet the assumption of an underlying network structure that shapes (cross-sectional) dynamics appears reasonable.515151Note that in principle the NVAR could be applied for general, not necessarily cross-sectional time series. I first provide some intuition on the merits of the NVAR as a tool for approximating cross-sectional time series in Section 5.1 and discuss the relation to alternative methods. The application to cross-country industrial production growth is set up in Section 5.2, with results presented in Section 5.3.

5.1 Modeling Cross-Sectional Processes by Sparse Networks

Consider the problem of approximating dynamics of a cross-sectional time series . Even for intermediate sizes of the cross-section, an unrestricted VAR() is not feasible. Modeling the series as an NVAR() process and estimating gives a sparse, yet flexible and interpretable alternative.

Sparsity is obtained by the assumption that innovations transmit cross-sectionally only via bilateral links. As a result, the information in the high-dimensional vector of potential covariates – the lagged values of – is compressed into a low-dimensional vector of regressors that summarizes this information using network connections:

Furthermore, because two units can be connected even in absence of a direct link between them, the dynamic, cross-sectional comovement may potentially be captured by relatively few non-zero bilateral links. In other words, can be sparse, leading to additional parsimony.525252However, if , can Granger-cause one period ahead only under an NVAR() with . See Proposition 1. Assuming that dynamic relations across all unit-pairs are driven by a relatively small set of bilateral links is akin to the assumption that longer-term dynamics are driven by a set of shorter-term dynamics, which is upheld by the general class of VARMA() models.

Flexibility is obtained because the connections in are estimated and because the NVAR() can capture rather general patterns of which connection-orders matter at which horizons, in particular for . The VARMA process in Eq. 5, which approximates the dynamics of under an NVAR() with , brings to mind functional approximation of the linear projection of on the information set at using a polynomial expansion in . Thereby, adding a term to the equation satisfies the two main requirements on basis functions, orthogonality and locality: the term i) adds new, orthogonal information to that captured by lower powers of , ii) adds different information across node-pairs , and iii) adds this information only at lag .

Comparison to Alternatives

There is a vast literature on modeling high-dimensional time series. The methods by which parsimony is induced can be roughly split into three categories.535353See Carriero et al. (2011) for an extensive discussion. Variable selection methods like Lasso or boosting aim at finding the most important predictors by excluding less relevant ones. Instead of imposing outright exclusion restrictions, shrinkage methods such as Ridge regression or Minnesota-type priors do that by downweighting less relevant ones. Finally, factor models and reduced rank regression models reduce dimensionality by summarizing a large set of predictors by a few linear combinations of them.

The NVAR combines insights from factor models and shrinkage methods. Compared to factor models, it offers a particular way of finding the linear combination that effectively summarizes the information in the high-dimensional set of predictors , namely by the set of bilateral links among cross-sectional units. Compared to shrinkage methods, the NVAR applies regularization to bilateral links , which in turn summarize the information in the predictors at all lags. As a result, it entertains the additional sparsity assumption that, for any variable , the same linear combinations of predictor-variables matter at all lags . Nevertheless, dynamics at different horizons are driven by different linear combinations, i.e. different sets of connection-orders, even more so if the network interaction frequency is allowed to be higher than the frequency of observation (see Proposition 1 and discussion in Section 2.2.2). This additional restriction can become important in higher dimensions.

The rank of the network adjacency matrix in the NVAR() is related to the number of factors in a factor model, arguably the most popular method for modeling high dimensional time series in macroeconomics. It is easy to see that an NVAR() permits a factor structure, with the number of factors given by the number of non-redundant columns in . The equivalence result in Section D.1 establishes in addition that, for large , a factor model can be cast as an NVAR() – with the number of factors again equal to the rank of – provided that the factors themselves evolve according to an NVAR(). Note that for , the latter condition just requires the factors to evolve according to a VAR(), while in case of a single factor, it requires the factor to follow an AR().

Based on these insights, the NVAR is expected to better capture cross-sectional dynamics when these are composed of many (seemingly neglibile) links rather than driven by a few influential units. And indeed, in many cases, we expect to be sparse, yet of close-to-full rank. For example, most countries trade only with a subset of other countries, but act as a significant trading partner to at least one other country. Similarly, most sectors supply only a small subset of other sectors in the economy, yet for most sectors we can find at least one other sector whose output or price-setting behavior critically depends on that of the sector in question. In principle, the same can apply not only for units in cross-sectional time series, but for variables in multivariate time series more generally.

Regardless of the rank of , the NVAR is expected to better capture the dynamics of for units with a dependence structure in (or factor loadings) that differs considerably from that of other units. As pointed out in Boivin and Ng (2006), the more dispersion there is in the factor loadings across series, the worse will be the forecasting performance of a factor model.545454Even if the number of factors is selected separately for each series, the forecasts for series that depend on less dominant factors are nevertheless more noisy than forecasts for series that depend on the most dominant factors. This is because including more estimated factors induces more sampling variability into the forecasts. This dispersion notably includes the case of weak factors, as captured by a sparse loading matrix (or a sparse adjacency matrix in the case of an NVAR). The NVAR naturally incorporates weak factors as locally important units in the network. Moreover, under the NVAR, sparsity of leads not only to cross-sectional differences in the strength of exposure to some given unit, but also to differences in the timing of this exposure555555See causality chain discussion in Section 2.2 and Proposition 1.. Therefore, the NVAR is further preferred to factor models whenever some notion of cross-sectional distance is expected to be relevant for the timing of impulse responses.

Even in case the NVAR offers no advantage to factor models in terms of modeling and forecasting cross-sectional dynamics, it may be preferred for other reasons. First, it estimates a network as relevant for dynamics and, relatedly, offers an interpretable way of approximating the dynamics in . Second, it facilitates the analysis of spillover and spillback effects as it estimates the whole set of bilateral Granger-causality patterns. Third, the estimated network offers a possible method for shock identification in high dimensions, the assumption being that the same bilateral links that rationalize lagged innovation transmission are also behind contemporaneous shock transmission.

5.2 Forecasting Setup

I use the NVAR to model the dynamics of monthly industrial production (IP) growth across countries. IP data is obtained from the IMF and OECD databases. Based on the raw data, I compute growth rates relative to the same month a year ago. Data availability narrows the sample to 44 countries and the time frame January 2001 to July 2022. In all of the following, I limit the analysis to pre-COVID-19. The data is summarized in Table A-3 in Section D.2.

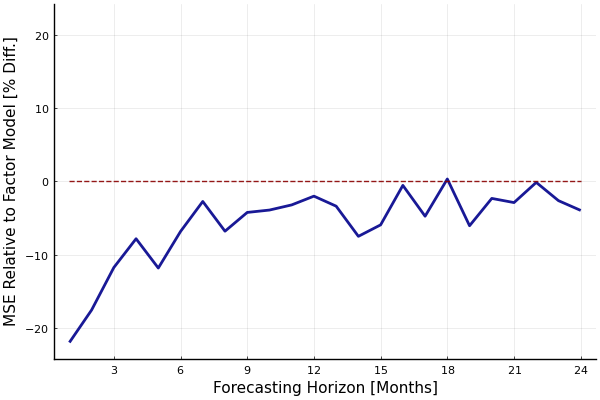

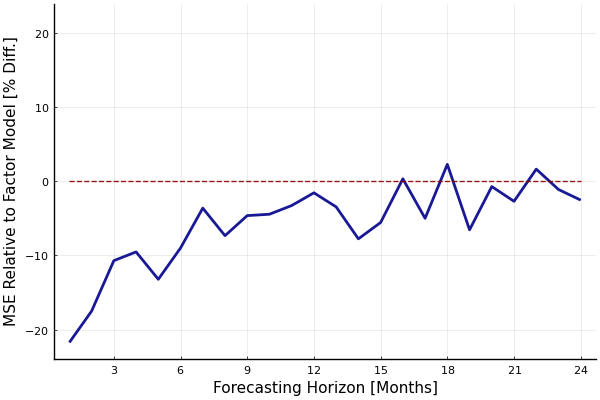

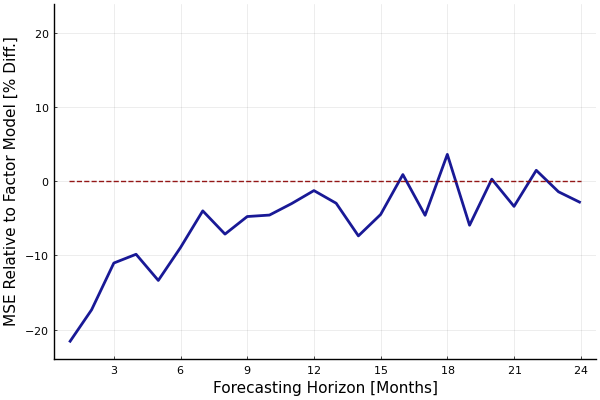

To assess forecasting performance, I first estimate an NVAR() as well as a factor model based on data from January 2001 to December 2017 and consider out-of-sample forecasting performance for horizons up to 24 months ahead. The sample is iteratively increased by one month and the analysis is repeated until the sample end date reaches December 2019. Forecasts for periods after January 2020 are excluded from the assessment.