On the links between Stein transforms and concentration inequalities for dependent random variables

Abstract

In this paper, we explore some links between transforms derived by Stein’s method and concentration inequalities. In particular, we show that the stochastic domination of the zero bias transform of a random variable is equivalent to sub-Gaussian concentration. For this purpose a new stochastic order is considered. In a second time, we study the case of functions of slightly dependent light-tailed random variables. We are able to recover the famous McDiarmid type of concentration inequality for functions with the bounded difference property. Additionally, we obtain new concentration bounds when we authorize a light dependence between the random variables. Finally, we give a analogous result for another type of Stein’s transform, the so-called size bias transform.

1 Introduction

The so-called Stein’s method has proven to be a very powerful tool to characterize the distribution of random variables (or random processes) in many different contexts. In particular, Stein’s method is very well suited for proving the asymptotic normality of a sequence of random variables under very weak assumptions. The advantages of this technique are twofold. The first one is the possibility to quantify the distance in measure of some distribution to the normal distribution. Stein original paper [19] states a characterization of normality of a random variable through a class of equations that this random variable verifies. More concretely, for a real random variable and a positive constant , we have that if and only if

| (1.1) |

for all absolutely continuous functions for which the above expectations exists. The quantitative results that has been derived from these ideas rely on the unique solution of the differential equation

| (1.2) |

where is any fixed real valued measurable function with finite first moment for the standard Gaussian variable . The special case is of special importance since it allows to prove the characterization (1.1). The simple form of Equation (1.2) permit to write explicit solutions and then consider the regularity of those solutions. This path has been specially fruitful in quantifying the distance between the distribution of and the normal distributed variable (with the same variance ). Such ideas lead naturally to get Berry-Essen type of bounds (see for example [8]). A particular case of interest is when the random variable is itself function of a class of random variables . In that case, one can study the effect of each random variable on through a directional version of equation (1.2).

The second advantage of Stein’s method is the possibility to manage weak dependence in the random variables family . We refer to [9] for examples of those ideas to prove asymptotic normality. In this paper we consider another approach that is somewhat parallel to the characterization of Equation (1.2). Since in general a real valued random variable does not satisfies Equation (1.1), we can force the equality by introducing a new distribution called the zero bias transform of firstly defined in [12].

Definition 1.

Let be a random variable with mean zero and finite variance . The random variable has the zero bias distribution with respect to if

| (1.3) |

for any absolutely continuous function such that the expectations exists.

This definition gives naturally a mapping that associates to a random variable another random variable noted . Note that this construction is only distributional. In other terms, no dependence structure between and is forced by this definition. We will benefit from that in the proof of Theorem 5. One can legitimately ask for a justification of the existence of such a construction. Such considerations and more are recalled (for the sake of completeness) in the following proposition that is inspired by Lemma 2.1 from [12] and Proposition 2.1 from [7]).

Proposition 1.

Let be a random variable with mean zero and finite variance and let having the zero bias distribution with respect to , then

-

1.

The Gaussian distribution with mean zero and variance is the unique fixed point of the equation (1.3).

-

2.

The zero bias distribution is unimodal about zero and preserves symmetry.

-

3.

The distribution of is absolutely continuous with density given by

(1.4) -

4.

The distribution function of is given by

(1.5) -

5.

The support of is the closed convex hull of the support of , and is bounded whenever is bounded.

-

6.

for any constant .

Similarly to Equation (1.1), another characterization has been developed and put in good use, the so-called Poisson characterization. It says that a positive random variable has the Poisson distribution of parameter if and only if

| (1.6) |

for all function for which the left hand side exists. This second characterization leads naturally to a second mapping given in the following definition.

Definition 2.

Let be a positive random variable with mean finite. The random variable has the size bias distribution with respect to if for all such that , we have

In the case that is a discrete random variable with probability mass function or where have density , we obtain that

| (1.7) |

On asymptotic normality

It is possible to obtain a Berry-Essen type theorems for a random variable in the case that a bounded size bias or a zero bias coupling exist. The bounds applies for the Kolmogorov distance which is given by

where and are the distribution functions of the random variables and .

In the case of the zero bias transform, the next result [7, Theorem 5.1], only requires the construction of a bounded zero bias coupling.

Theorem 1.

Let be a random variable with zero mean and variance 1, and suppose that there exist , having the zero bias distribution of , defined in the same space satisfying , then

| (1.8) |

where and is a standard Gaussian random variable

For the size bias transform, besides the existence of a bounded size bias coupling, the calculation of terms involving a conditional expectation its also necessary [11, Theorem 2.1].

Theorem 2.

Let be a non negative random variable with finite mean and finite, positive variance , and suppose , have the size bias distribution of , may be coupled to so that , for some . Then with ,

| (1.9) |

where is a standard Gaussian random variable, and is given by

| (1.10) |

In some applications it is enough to use that , where is given by

| (1.11) |

in order to obtain [7, Theorem 5.6]

| (1.12) |

The last theorem can be used to prove normal approximation in discrete structures such that the number of crossings in graphs and trees [1, 2, 16] and the Betti numbers in random simplicial complexes[14]. The previous results give us information about the convergences rates in the normal approximation for the random variable , but this don’t give us information about concentration. This is one of the objectives of this work.

On stochastic domination

In order to exploit the result of Theorem 2, it is helpful to get domination results on quantities that involve the random variable . The task is then to be able to find couplings of the two variables and such that their difference remains small. One way to obtain such controls is to rely on stochastic domination. We say that is stochastically dominated by if for all increasing and bounded function ,

We denote that fact . In particular, the stochastic domination implies that the cumulative distribution functions are bounded one by the other : , . We also introduce a slightly different stochastic order. A random variable is stochastically dominated in the convex order by if for any convex function such that and , we have that

We will denote . This last definition implies in particular that and that the variance of is dominated by the variance of . This notion of stochastic order is often used in information theory where most of the entropy functions are in fact convex. The best advantage of this formulation is its flexibility since no specific coupling is imposed on the pair of random variables. Our following results will be formulated in the context of stochastic domination whereas in all the results given in the literature, the controls on are given by almost sure domination on a particular coupling. One can see that the two notions can be linked thanks to Strassen’s theorem (see [20]) that we recall here for completeness.

Theorem 3 (Strassen stochastic order).

Let and be such that then there exists a coupling which is a probability measure on with marginals having the same laws as and and such that

is such that .

We refer to [15] for a comprehensive proof of this theorem. The following result gives an easy but useful characterization of the stochastic domination. (see for example [18]).

Lemma 1.

Let and be two random variables, then the followings are equivalents

-

1.

.

-

2.

.

2 Subgaussianity and zero bias control

2.1 Real case

In this section, we explore some equivalence between properties on the Stein transform of a random variable and how light tailed the random variable actually is. For this purpose, we first introduce the notion of sub-Gaussian random variables. A real valued random variable is said to be sub-Gaussian of constant (and denoted by ) if for all , we have that

| (2.1) |

If we only assume that Equation (2.1) holds for positive (resp. negative) , we say that the random variable has a sub-Gaussian right tail, denoted (resp. sub-Gaussian left tail, denoted ). Obviously, a random variable that is both sub-Gaussian in its left and right tail is sub-Gaussian. In the following proposition, we sum up different sufficient conditions for a real valued random variable to be sub-Gaussian.

Proposition 2.

Let be a centered real valued random variable. We denote by its moment generating function. If for all , we have that , then is .

Proof.

Assume that a function satisfies the differential inequality so that

Then, by direct integration, we get that

which proves 1. ∎

In the next definition, we introduce the notion of weighted stochastic domination that will be key in our following results.

Definition 3.

Let and be two random variables and let be two positive constants. We say that is stochastically dominated in the weighted order with constant if for all increasing and positive function for which the expectations exists. We will denote this by .

Note that when the two constants and coincide, the previous definition is equivalent to . In the applications, we will always take and will be an upper bound of the variance of . In some sense, this definition is a stochastic domination weighted by the variances of the two variables. In the case that , the domination can be rewritten thanks to the equation into . This last formulation has the advantage to be define only thanks to the original random variable . In the following theorem, we give an equivalence between the weighted stochastic domination of by and the fact that is sub-Gaussian.

Theorem 4.

Let be a random variable with zero mean, variance finite and let his zero bias transform. Then, implies that has a sub-Gaussian right tail with constant . If , then has a sub-Gaussian left tail with constant . Moreover, if has density such that is concave, then .

We point out that the first implication of Theorem 4 is a slight generalization of an already known fact firstly shown in [10, Theorem 2.1]. In this result, the condition is of the form for a positive constant which would be quasi equivalent to . This case can be easily obtained with the same kind of arguments as a corollary of Theorem 4. We state this small result in Corollary 1. In fact, the result in [10] uses an almost sure domination that is not much stronger than stochastic domination as seen in Strassen’s theorem. When the constant is equal to 0, our condition is actually weaker since we allow the two constants and to be different. For the necessary condition, we see that the hypothesis is concave implies the fact that is sub-Gaussian of constant . It is actually a little stronger since it forces the density to remain under the density of a for sufficiently large. This is not the case for completely general sub-Gaussian random variables. The reader familiar with the notions of log-concavity will note that this means that the random variable is strongly log-concave (see [17, Definition 2.8] for a rigorous definition).

Proof of Theorem 4.

Notice that for any fixed , the function is increasing and convex so that the function verifies the conditions of Definition 3. Then

If denotes the moment generation function of , we obtain

that is

which implies by Proposition 2 that .

On the other hand, let be a gaussian random variable with zero mean, variance and density function . Using the Proposition 1 we obtain for any absolutely continuous increasing and convex function ,

where is the quotient of the densities of and . Using the zero bias characterization for the Gaussian distribution with the function , and the fact that the Gaussian distribution is the fixed point of (1.3), we obtain

Notice that . On the other hand, for the density of the Gaussian random variable , , therefore

But,

Also, since is increasing, the FKG inequality give us

for any increasing function . Observe that the hypothesis be concave implies that is increasing, then

that is, , which implies

i.e, . To show the result for the left tail, we only have to consider the random variable and see that is equivalent to . ∎

The following result only study the first implication of Theorem 4 when we add a little freedom in the control of by . The cost of this change is a different regime in the tail for large values. This behavior is sometimes referred as sub-Gamma right tail.

Corollary 1.

Let be a real-valued random variable of finite variance and such that for a positive constants and . Then, we obtain that

The proof of this result is very similar to the first part of Theorem 4. The main change is that the control of the function is now of the form

when . This allows to get the result. See [5] for more details on sub-Gamma random variables.

In the proof of Theorem 4, we have used a change of measure to a Gaussian random variable. This particular trick allows to use Stein’s equation for the Gaussian. If one wants to make a more general change of measure, a similar result can be derived for the necessary condition of Theorem 4. In this case, it is no more possible to stochastically dominate the random variable by but the two tails can still be compared up to a distortion term that depends on the measure we compare to. This is the purpose of the following proposition.

Proposition 3.

Let and be two random variables with zero mean, variance and densities and respectively. If exist such that

-

1.

is decreasing in ,

-

2.

for , is bounded by a constant , only depending of , where is the density of having the zero bias distribution of .

Then, for having the zero bias distribution of ,

| (2.2) |

Proof.

Using the formula (1.4) for the density of and a change of measure, we obtain for any ,

It follows that in the event , , then

Therefore, for all

∎

In Proposition 3, if we go back to taking a Gaussian random variable we obtain and once again, Strassen’s theorem allows to get . One advantage of Proposition 3 is to be able to consider a sub-Gaussian behavior of only for large values of . We use Proposition 3 in the following result.

Corollary 2.

Let be a random variable with zero mean, variance finite and density , where satisfies that

-

1.

, if ,

-

2.

, if .

Then, for all . In addition, if and if for every we have that then is smaller than in the convex order.

Proof.

Let be a gaussian random variable with mean zero, variance and density . The hypotesis implies that is decreasing for . Then from Proposition 3 we obtain for all .

On the other hand, the density of given in Equation (1.4) is for equal to

Using the hypothesis , for , we obtain that the function is increasing for , then

that is for all .

Finally by Definition 1 implies that . Also if for follows that , we obtain that the function has two sign changes and the sign sequence is , which implies (see for example Theorem 3.A.44 from [18]) that is smaller than in the convex order.

∎

Remark 1.

Notice that if , for , then integrating from to , we obtain , which implies that , where is the density of a Gaussian random variable with zero mean and variance , and . Then,

Analogously, if , if , we obtain and

2.2 Concentration of sums of weakly-dependent random variables

The subject of general functions of independent random variables is key for a enormous class of probabilistic models. It is well known that under mild conditions of the continuity of the function, one can show a concentration of measure phenomenon for the values of the function. The case when the random variables are slightly dependent is less classical and somewhat lacks of general results. In this section, we develop new ways to show concentration when we even permit a little dependence between the random variables. In particular, we are interested in the links between sub-Gaussianity of a multivariate function of random variables and zero-bias transforms of this function. To keep track of the effect of each random variable on the rest of the random variables, we define a notion of directional zero bias transform.

Definition 4.

Let be random variables with mean zero and finite variance . We define the directional zero bias distribution in the direction , as the random vector that satisfies

| (2.3) |

where is a real function on variables such that the expectations exist.

The first important remark is that no independence nor (un-)correlation of the random variables are necessary to be able to define the directional zero-bias transforms . The following proposition states the basic facts of this directional zero-bias transform. Some results are direct consequences of Proposition 1.

Proposition 4.

Let be random variables with mean zero and finite variance . Then

-

1.

The random variable has the same distribution as which is the classical zero-bias transform of Definition 1.

-

2.

If the random vector have a density, then the random variable have a density given by

(2.4) where is the joint density of .

-

3.

If is independent of , then

-

4.

for any constant .

Proof.

-

1.

If is a function that only depends of the entry , it follows that

but from the Definition 1, the first term of the above equation is equal to , therefore and have the same distribution.

-

2.

Choosing a function of the form , we have that , then

(2.5) From the last equation, it follows that the density of the random variable is equal to

(2.6) where is the joint density of .

- 3.

-

4.

The result follows using (2.5) and the function .

∎

We now state the main result of this section. It is stated for a random variable that is a sum of centered random variables but no independence is formally needed. It basically shows that if every random variable is sub-Gaussian in the sense that its zero bias transform can be upper bounded by the original random variable and if the cross directional zero bias transform is small then the sum of the variables inherits the sub-Gaussian behavior.

Theorem 5.

Let be random variables such that and . Suppose that

-

1.

for and his zero bias transform ,

(2.7) -

2.

for all ,

(2.8)

Then has sub-gaussian right tail of constant

We give some comments on the hypothesis of Theorem 5. One can note that the two conditions (2.7) and (2.8) could be unified into for every . We separated the two since they have different interpretations. Equation (2.7) is basically a sub-Gaussian hypothesis on the random variables as seen in Theorem 4. In the examples below, we detail various cases where one can show easily the condition (2.7). For the interpretation of Equation (2.8), Definition 4 gives directly that

then the hypothesis (2.8) is equal to

which finally writes as

| (2.9) |

for all increasing function such that the expectations exists. Note that this last condition holds if for all the random variables and are negatively associated. Indeed, by definition of negative association we have that for any pair of increasing functions and ,

Since the functions and are both increasing, we have directly the condition (2.8) for . Concentration of sum of random variables negatively associated is already known and the interested reader can take a look at [4] for example. To finish the comments on Theorem 5, we would like to give the following general interpretation for this result. A sum of sub-Gaussian random variables for which their cross Stein’s transform are small (in the sense of (2.8)) is itself sub-Gaussian.

In order to prove Theorem 5, we introduce a general form of Strassen’s theorem [15] that will be used in Lemma 2.

Theorem 6 (Strassen generalized domination).

Let be a partially ordered set for which the set

is closed in the product topology of . Let two probability measures on such that is stochastically dominated by . Then, there exist a coupling of law with marginals , and such that , - almost surely. The law of the coupling acts on the measurable space .

The following consequence of Strassen’s theorem allows us to deduce a almost sure control of the by for a specific coupling when we assume the weighted stochastic domination between and .

Lemma 2.

Let and be two random variables such that . Then, for all increasing and positive function there exist a coupling such that

Proof.

We introduce the following relation: Let be an increasing continuous and positive function and positive constants such that . We define as

| (2.10) |

We denote if and . Notice that is a partial order in . Indeed, because is positive and . Let and . Suppose that , then exist such that , but with , this implies that . As is a increasing function, we obtain , that is Notice that for all ,

that is, . Then, we obtain that , which implies , which is a contradiction, because we are supposing that . This proves transitivity.

Now notice that

which by the continuity of is a closed set. Now, the hypothesis implies that , and by Theorem 6 we obtain that exist a coupling of law such that , - almost surely. ∎

Proof of Theorem 5.

Let be a absolutely continuous increasing and convex function with continuous derivative. Using the Definition 4 with the function ,

From Corollary 4, it follows that for any . First, we see the case . The hypothesis with the Lemma 2, implies that for the function which is increasing continuous and positive, almost surely, then

Now, using the hypothesis implies that for any , with the function and the Lemma 2, that almost surely, then

Then, with the same argument and noticing that in each step we use a different coupling, we obtain

With a completely analogous reasoning, we obtain for any ,

On the other hand, , then for any , that is

Therefore, we get that

for any increasing continuous and positive function . Now, any increasing and positive function can be approximated by increasing continuous and positive functions, then we obtain from Theorem 4 that . ∎

2.3 Examples of applications of Theorem 5

In this section, we present four examples of increasing complexity that show the usefulness of Theorem 5. The first three examples deal with sums of light-tailed random variables for three different dependence structure. The last example allows us to tackle the case of general functions of weakly dependent random variables.

Example 1. (Dependency Neighborhoods)

We say that a collection of random variables has dependency neighborhoods with if for every we have that and is independent of . In particular, this property implies that for any .

Suppose, now, that the random variables have dependency neighborhoods . Then, we can apply Theorem 5 with the choice in (2.8) for every . Therefore

and has sub-Gaussian right tails of constant . In the special case where all are independents, we obtain that for all and which gives

As seen in the definition of the weighted stochastic domination, the constants are forced to be greater than the variance . In consequence, the most constants being equal to , the smaller the constant is. This case is typically adapted to random graphs where the dependence in the random variables is fairly local. In most of the classical cases (Erdós-Reyni random graphs for example), the dependence neighbor is microscopic (). In that case, the constant of full independence case is of the good order.

Example 2. (Linear combination of orthogonal random variables)

Let be a collection of orthogonal random variables with zero mean and unit variance. Assume that for all and for all . For any vector with non negative entries, define and . Finally, define

The variances of the variables are given by The two hypothesis on the class imply that for all and for all respectively. Indeed, for any increasing and positive function , consider the function and apply the Definition 3. Then, we obtain

Once again, one can see that when we assume that the random variables are independent, all the constants for . We are reduce to consider a sum of independent sub-Gaussian random variables. Hence, Theorem 5 shows that in that case is sub-Gaussian with . By analogy with Gaussian vectors, we see that the sub-Gaussian property is stable by linear combinations and the resulting sub-Gaussian constant behaves exactly in the same way than the variance for Gaussian random vectors.

Example 3. (Bounded random variables)

In this example, we consider the variable of Theorem 5 and assume that the random variables have compact support, namely , with , and we also assume that the random variables have unimodal density . Then, from direct calculation using (1.4), we obtain , which implies that

for any increasing and positive function such that the expectations exist and with the constants . Additionally, by (2.5) and the fact that is of compact support, we see that

In terms of weighted stochastic domination, the later is equivalent to with . Then, by Theorem 5, has sub-Gaussian tails of constant

If the random variables are independent, we can take , and obtain

Note that this last constant is equal to the constant of sub-Gaussian constant given by the classical Hoeffding’s inequality for sums of bounded independent variables. Once again, we see that Theorem 5 generalizes a classical result on sub-Gaussian concentration.

Example 4. (Function with bounded differences)

In this example, we are interested to see the consequences of our main theorem for functions of independent random variables. It is known in the concentration of measure community that a function that depends regularly on its entries and if no random variable have a “macroscopic” influence on the value of the function, then concentrates around its mean value . In this example, we obtain directly McDiarmid inequality on bounded difference functions (see [5] for a compehensive proof) by direct use of previous example. We say that a function has the bounded differences property if for some nonnegative constants ,

| (2.11) |

for .

Let be independent random variables in some space and let a function with bounded differences and consider the random variable . We can write as a sum of martingale differences for the Doob filtration as

| (2.12) |

where

| (2.13) |

The bounded differences property of implies that the support of the random variables is a subset of for some constants with . The independence of the random variables implies that the random variables are uncorrelated, then, we can use the previous example to obtain that has sub-Gaussian tails. Furthermore, if the support of the random variables is symmetric, meaning that , we obtain that , and

Note that the constant is precisely the constant of sub-Gaussianity present in [5, Theorem 6.2].

2.4 Hoeffding’s statistics

In this section, we present a concrete example where the random variables that come into play are naturally slightly dependent. The object of interest is the Hoeffding statistic given by

| (2.14) |

where be a random uniform permutation in the symmetric group and is an matrix with real entries. This random variable is of great interest in permutation test (see for example [7]), or in a kind of limit theorems, called Hoeffding combinatorial central limit theorems (see [13]). Concentration bounds for are given by [6, 10], where they obtain sub-Gamma right tails of type

| (2.15) |

or

| (2.16) |

We see in the sequel that our approach allows us to obtain sub-Gaussian tails for this statistics. By a direct calculation we obtain the first and second moments of the random variable ,

Define

| (2.17) |

The random variables only depend on the entries of the row of the matrix , then the support of the random variable lies in the interval , where . Then, using Example 3, we obtain that , with

which implies that for all ,

| (2.18) |

It is also posible to extend this concentration result to functions of the random variables . Indeed, for a -Lipschitz function, consider the random variable

Since the function only depends of the entries of the matrix , we obtain that is a function with bounded differences with constants . Then has sub-Gaussian tails with constant

which implies that for all ,

| (2.19) |

3 Sub Poisson and Size bias control

3.1 Size bias Coupling for real valued random variables

In this section we expose a similar result to Theorem 5 in the case of the size bias transform. In [3], the authors show that if a coupling such that almost surely exists then the random variable has a sub-Gamma (in fact sub-Poisson) right tail. The results presented below deal with the converse: What conditions are necessary to obtain a coupling between the two non-negative random variables and and such that almost surely? For any positive random variable with finite mean , the size bias transform exists as seen in Definition 2. When there exists a positive constant such that almost surely, the result [3, Lemma 2.1] shows that for all ,

| (3.1) |

This allows to obtain a concentration bounds of type [3, Theorem 1.3]

The authors refer to it as Gamma function bound since it decays at least as fast as the reciprocal of a Gamma function. We are interested in the converse problem, that is, to understand when we can obtain a bounded coupling.

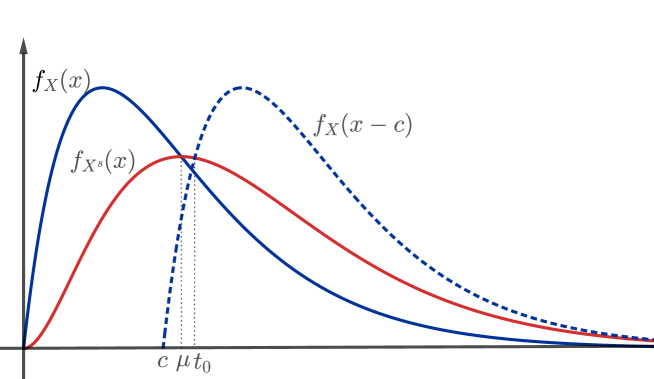

The next theorem give conditions for the existence of a bounded coupling when we have an inequality between the density (or the probability mass function) of the size bias transform and a right-shift of the density of the random variable. See Figure 1 for a visual interpretation. This condition is a density version of (3.1).

Theorem 7.

Let be a positive random variable with finite mean . Suppose that exist positive constants and such that

| (3.2) |

where is the probability mass function if is discrete or the density function if is absolutely continuous. Then, for having the size bias distribution of ,

| (3.3) |

Proof.

Equation (3.1) and Theorem 7 together show the equivalence between sub-Gamma concentration and the existence of a coupling such that . Given that we are in the case of positive random variables, by a direct calculation we obtain that if , then and if , then , so the constants and in the previous theorem are the ones corresponding to the context where a shift of the original density by upper bounds the density of . This way the condition (3.2) is satisfied, as we show in the Figure 1.

3.2 Sum of independent random variables

One of the most important properties of the size bias transform is that it has an easy explicit construction for sums of random variables. The case of sums of independent random variables is almost trivial since the construction rely only on randomly replacing a random variable for his size bias version with probability proportional to its mean, as shows the next result [7, Corollary 2.1].

Corollary 3.

Let , where are independent, nonnegative random variables with means . Let be a random index with distribution given by

independent of all other variables. Then, upon replacing the summand selected by with a variable having its size biased distribution, independent of for , we obtain

a variable having the -size bias distribution.

Note that there exists a general result that gives a method to obtain the size bias transform for a sum of dependent random variables. In this case, to replace a random variable by his size bias transform, it is necessary to adjust the remaining random variables conditionally to this new value. For further details see [7, Proposition 2.2].

The following result shows the behavior of the sum of independent random variables that have sub-Gamma concentration in the sense of Equation (3.1). As in Theorem 5, the sum inherits of the almost sure control of its size bias transform by a constant plus the original random variable.

Theorem 8.

Let be independent, nonnegative random variables with means , such that the size bias transform of each satisfies that , for some constants . Then, for we have that

It is interesting to see that the behavior of the constant in the result is fundamentally different from Theorem 5. Indeed, here the resulting constant is the maximum of all the constants .

Proof.

Let . Then, for each ,

Then, conditioning on , we obtain

∎

For a sanity check, one can note that for a Poisson random variable of parameter , and so if we have a class of Poisson random variables of parameters , we have trivially . But, since the sum of independent Poisson random variables is also Poisson, we have that which is coherent with the constant resulting of Theorem 8 where . Hence, Theorem 8 can be considered optimal in that sense.

References

- [1] Santiago Arenas-Velilla and Octavio Arizmendi. Convergence rate for the number of crossing in a random labelled tree. arXiv preprint arXiv:2209.09431, 2022.

- [2] Santiago Arenas-Velilla and Octavio Arizmendi. Crossings in randomly embedded graphs. arXiv preprint arXiv:2205.03995, 2022.

- [3] Richard Arratia and Peter Baxendale. Bounded size bias coupling: a Gamma function bound, and universal Dickman-function behavior. Probab. Theory Related Fields, 162(3-4):411–429, 2015.

- [4] A. D. Barbour, Lars Holst, and Svante Janson. Poisson approximation, volume 2 of Oxford Studies in Probability. The Clarendon Press, Oxford University Press, New York, 1992. Oxford Science Publications.

- [5] Stéphane Boucheron, Gábor Lugosi, and Pascal Massart. Concentration inequalities. Oxford University Press, Oxford, 2013. A nonasymptotic theory of independence, With a foreword by Michel Ledoux.

- [6] Sourav Chatterjee. Stein’s method for concentration inequalities. Probab. Theory Related Fields, 138(1-2):305–321, 2007.

- [7] Louis H. Y. Chen, Larry Goldstein, and Qi-Man Shao. Normal approximation by Stein’s method. Probability and its Applications (New York). Springer, Heidelberg, 2011.

- [8] Louis H. Y. Chen and Qi-Man Shao. A non-uniform Berry-Esseen bound via Stein’s method. Probab. Theory Related Fields, 120(2):236–254, 2001.

- [9] Louis H. Y. Chen and Qi-Man Shao. Normal approximation under local dependence. Ann. Probab., 32(3A):1985–2028, 2004.

- [10] Larry Goldstein and Ümit Işlak. Concentration inequalities via zero bias couplings. Statist. Probab. Lett., 86:17–23, 2014.

- [11] Larry Goldstein and Mathew D. Penrose. Normal approximation for coverage models over binomial point processes. The Annals of Applied Probability, 20(2):696 – 721, 2010.

- [12] Larry Goldstein and Gesine Reinert. Stein’s method and the zero bias transformation with application to simple random sampling. Ann. Appl. Probab., 7(4):935–952, 1997.

- [13] Wassily Hoeffding. A combinatorial central limit theorem. Ann. Math. Statistics, 22:558–566, 1951.

- [14] Matthew Kahle and Elizabeth Meckes. Erratum to “Limit theorems for Betti numbers of random simplicial complexes” [ MR3079211]. Homology Homotopy Appl., 18(1):129–142, 2016.

- [15] Torgny Lindvall. On Strassen’s theorem on stochastic domination. Electron. Comm. Probab., 4:51–59, 1999.

- [16] J.E. Paguyo. Convergence rates of limit theorems in random chord diagrams. arXiv preprint arXiv:2104.01134, 2021.

- [17] Adrien Saumard and Jon A. Wellner. Log-concavity and strong log-concavity: a review. Stat. Surv., 8:45–114, 2014.

- [18] Moshe Shaked and J. George Shanthikumar. Stochastic orders. Springer Series in Statistics. Springer, New York, 2007.

- [19] Charles Stein. A bound for the error in the normal approximation to the distribution of a sum of dependent random variables. In Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and Probability (Univ. California, Berkeley, Calif., 1970/1971), Vol. II: Probability theory, pages 583–602, 1972.

- [20] V. Strassen. The existence of probability measures with given marginals. Ann. Math. Statist., 36:423–439, 1965.