sorting=ynt \AtEveryCite\localrefcontext[sorting=ynt]

Leverage, Endogenous Unbalanced Growth, and Asset Price Bubbles††thanks: This paper is a significant revision of an earlier manuscript circulated under the title “Necessity of Rational Asset Price Bubbles in Two-Sector Growth Economies” [99].

Abstract

We present a general equilibrium macro-finance model with a positive feedback loop between capital investment and land price. As leverage is relaxed beyond a critical value, through the financial accelerator, a phase transition occurs from balanced growth where land prices reflect fundamentals (present value of rents) to unbalanced growth where land prices grow faster than rents, generating land price bubbles. Unbalanced growth dynamics and bubbles are associated with financial loosening and technological progress. In an analytically tractable two-sector large open economy model with unique equilibria, financial loosening simultaneously leads to low interest rates, asset overvaluation, and top-end wealth concentration.

Keywords: financial accelerator, land bubble, leverage, nonstationarity, phase transition, unbalanced growth.

JEL codes: D52, D53, E44, G12.

1 Introduction

An asset price bubble is a situation in which the asset price exceeds its fundamental value defined by the present value of dividends. History has repeatedly witnessed bubbly dynamics of asset prices. For instance, [108, Appendix B ] documents 38 bubbly episodes in the 1618–1998 period. In addition, bubbly fluctuations of asset prices have often been associated with financial crises, with significant economic and social costs [106]. Therefore, there is a substantial interest among policymakers, academics, and the general public in understanding why and how asset price bubbles emerge in the first place.

Since the seminal paper by [119], the macro-finance theory has typically assumed outright that the asset price equals its fundamental value. The dominant view of the literature seems to be that bubbles are either not possible in rational equilibrium models or even if they are, a situation in which asset price bubbles occur is a special circumstance and hence fragile.111This view is summarized well by the abstract of [133]: “Our main results are concerned with nonexistence of asset pricing bubbles in those economies. These results imply that the conditions under which bubbles are possible are relatively fragile.” [107] and [122] show that bubbles are nearly impossible in representative-agent models. In fact, [133] find that there is a fundamental difficulty in generating bubbles attached to dividend-paying assets in rational equilibrium models: their Theorem 3.3 and Corollary 3.4 show that when dividends from assets comprise a non-negligible share of the aggregate endowment—no matter how small the share is—bubbles are impossible.222In a recent review article on rational asset price bubbles, [101, §3.4 ] also provide clear explanations about the fundamental difficulty derived from [133, Theorem 3.3, Corollary 3.4 ]. Moreover and importantly, according to the bubble characterization result of [121, Proposition 7 ], a bubble exists if and only if future dividend yields are summable. With positive dividends, this is true only if the price-dividend ratio grows. These results imply that bubbles attached to real assets yielding positive dividends cannot occur in models with a steady state. In other words, the essence of asset price bubbles is nonstationarity. Although economists have long been trained and accustomed to studying stationary models, to understand asset price bubbles in dividend-paying assets, we need to depart from them.

The primary purpose of this paper is to take the first step towards building a macro-finance theory to think about asset price bubbles in dividend-paying assets. The key to understand such bubbles is a world of nonstationarity characterized by unbalanced growth, unlike a world of stationarity characterized by balanced growth. Even a small deviation from the world of stationarity will lead to vastly different insights on asset pricing. Furthermore, we show the tight connection between financial leverage and unbalanced growth, that is, whether the economy exhibits balanced or unbalanced growth is endogenously determined and crucially depends on the level of financial leverage.

We consider a simple incomplete-market dynamic general equilibrium model with a continuum of infinitely-lived heterogeneous agents. There is a representative firm with a standard neoclassical production function, where capital and land (in fixed aggregate supply) are used as factors of production. Because land yields positive rents, it may be interpreted as a variant of the [119] tree with endogenous dividends. Agents can save by investing in a portfolio of capital and land (real estate investment trust). Each period, agents are hit by productivity shocks and decide how much capital investment they make using leverage and how much to save through holding land. Capital investment and land price reinforce each other, with endogenous changes in land rents, generating a positive feedback loop: when the land price goes up, aggregate wealth increases, leading to large investments, which in turn increase land rents, future wealth, and the demand for land. The current land price is determined reflecting future changes in land rents and prices, which in turn affects the current aggregate wealth. Importantly, leverage affects the magnitude of this interaction and there are two possibilities for the long run behavior of the economy. One possibility is that the economy converges to the steady state. Another possibility is that the financial leverage of agents is sufficiently high so that the economy grows endogenously. We find that whether land prices reflect fundamentals or contain a bubble crucially depends on which growth regime the economy falls into.

Our first main result, the Land Bubble Characterization Theorem 1, establishes the tight link between leverage, the growth behavior of the economy, and asset pricing implications. When leverage is below a critical value, the interaction between land prices and capital investment is not strong enough to sustain growth and the economy converges to the steady state of zero growth (because land is a fixed factor) in the long run. In this case, aggregate capital, land price, and land rent all grow at the same rate in the long run, therefore exhibiting balanced growth, and land prices reflect fundamentals. However, when leverage exceeds the critical value, the positive feedback loop between capital investment and land price becomes so strong that the macro-economy suddenly loses its balanced growth property and the economy takes off to endogenous growth. While land prices grow at the same rate as the economy driven by the demand for land as a store of value, land rents grow at a slower rate driven by the demand for land as a production factor, generating a gap between the growth rates of land prices and rents. This unbalanced growth causes the price-rent ratio to rise without bound, which appears to be explosive, and leads to a land price bubble. Once the regime of the economy changes to the land bubble economy, the determination of the land price becomes purely demand-driven, i.e., the price continues to rise due to sustained demand growth arising from economic growth. In contrast, when the land price reflects fundamentals, it equals the present value of land rents and hence its determination is supply-driven. The demand-driven positive feedback loop is a distinctive feature of the land bubble economy. In this way, our Theorem implies that as the leverage is relaxed beyond the critical value, the dynamics of macroeconomic variables such as land prices, the price-rent ratio, and economic growth changes abruptly and qualitatively, which we refer to as a phase transition.333Phase transition is a technical term in natural sciences that refers to a discontinuous change in the state as we change a parameter continuously, for instance the matter changes from solid to liquid to gas as we increase the temperature. The analogy here is appropriate because the regime of the economy abruptly changes from fundamental to bubbly as we increase leverage. With the phase transition, the macro-economy shifts from a stationary world of balanced growth and fundamental value to a nonstationary world of unbalanced growth and bubble.

Moreover, by considering a standard constant elasticity of substitution (CES) production function where capital and land are used as inputs, we provide a complete characterization of the fundamental region and the land bubble region in terms of the underlying parameters of the economy such as financial leverage, overall productivity of the economy, and the elasticity of substitution in the production function. We show that for all values of the elasticity, the land bubble region always emerges if leverage gets sufficiently high. The leverage threshold decreases as the overall productivity of the economy rises (in the sense of first-order stochastic dominance), indicating the positive connection between technological innovations and asset price bubbles. This result is consistent with the narrative “asset price bubbles tend to appear in periods of excitement about innovations” highlighted by [134, p. 22 ]. To demonstrate the usefulness of our basic theory, we present a numerical example showing how changes in leverage or productivities lead to the emergence and collapse of land price bubbles and provide a discussion in light of Japan’s experience in the 1980s.

After presenting the baseline model, we extend it to an analytically tractable case of a two-sector large open economy with capital- and land-intensive sectors and derive our second main result. This Land Bubble Characterization Theorem 2 for trend stationary equilibria shows that a unique bubbly (fundamental) equilibrium exists if and only if leverage is above (below) the critical value and thus provides a complete characterization of land bubbles. Furthermore, as an application of the extended model, we study the relationship between low interest rates, asset prices, and wealth inequality. Our model shows that a sufficient increase in financial leverage leads to low interest rates, asset overvaluation, and greater top-end wealth concentration simultaneously.

Finally, we would like to add that our model incorporating the possibility of unbalanced growth dynamics provides a new perspective on constructing macro-finance theory. So long as the model allows for only balanced growth of a stationary nature in the long run, by model construction, asset price bubbles attached to real assets yielding positive dividends are impossible because land prices grow at the same rate as land rents in the long run. However, once the model features some mechanism that allows for unbalanced growth of a nonstationary nature, asset price bubbles emerge. These results imply that the fundamental difficulty in generating asset bubbles derived from [133, Theorem 3.3, Corollary 3.4 ] comes from a method of model construction where only balanced growth equilibrium emerges.

The rest of the paper is organized as follows. Section 2 presents the model. Section 3 characterizes the equilibrium system and the asymptotic behavior of the model. Section 4 shows that relaxing leverage leads to endogenous unbalanced growth and land price bubbles. Section 5 studies the relationship between low interest rates, asset price bubbles, and wealth inequality. Section 6 discusses the related literature. Proofs are deferred to Appendix A. Appendix B formally defines asset price bubbles and discusses basic properties.

2 Model

We extend the model of [109] by introducing a neoclassical production function and a production factor in fixed supply (land).

Agents

The economy is populated by a continuum of agents with mass 1 indexed by .444It is well known that using the Lebesgue unit interval as the agent space leads to a measurability issue. We refer the reader to [137] for a resolution based on Fubini extension. Another simple way to get around the measurability issue is to suppose that there are countably many agents and define market clearing as , where is agent ’s demand at time and is the per capita supply. A typical agent has the utility function

| (2.1) |

where is the discount factor and is consumption.

Productivity

The economy features no aggregate uncertainty but agents are subject to idiosyncratic risk. Every period, each agent independently draws investment productivity from a cumulative distribution function (cdf) satisfying the following assumption.

Assumption 1.

is absolutely continuous with .

The iid assumption is inessential but simplifies the analysis.555For a related model in a Markovian setting, see [100, §5 ]. The condition that takes values in (so for all ) implies that for all , so the productivity distribution has an unbounded support. This assumption guarantees that the economy has incomplete markets regardless of the interest rate. The absolute continuity of implies that the productivity distribution has no point mass except possibly at . This assumption is inessential but simplifies the analysis by avoiding cases. The condition implies that the mean productivity is finite, which is necessary for guaranteeing that aggregate capital is finite.

Production

Production uses capital and land as inputs, whose quantities are denoted by and . There is a representative firm with neoclassical production function . Markets for production factors are competitive and inputs are paid their marginal products. After production, capital depreciates at rate . To simplify notation, following [89], we introduce the function

| (2.2) |

For our analysis, only the function (not ) matters, as it constitutes aggregate wealth and hence plays an important role for the aggregate wealth dynamics.

We impose the following assumption on .

Assumption 2.

is homogeneous of degree 1, concave, continuously differentiable with positive partial derivatives, and satisfies

| (2.3) |

Note that the assumption in (2.3) is natural because includes the term in (2.2). A typical example satisfying Assumption 2 is the constant elasticity of substitution (CES) production function

| (2.4) |

where are parameters and is the reciprocal of the elasticity of substitution between capital and land.666The case reduces to the Cobb-Douglas form by taking the limit . In this case, a straightforward calculation yields

| (2.5) |

Land and REIT

The aggregate supply of land is exogenous and normalized to 1. In the background, there are perfectly competitive financial intermediaries who securitize land into a real estate investment trust (REIT), which agents can invest in arbitrary amounts. Because the economy features no aggregate uncertainty, REIT is risk-free; we thus often refer to REIT as bonds.

The gross risk-free rate between time and , denoted by , is determined as follows. Let be the aggregate capital and land price (excluding current rent) at time . Because the aggregate supply of land is 1, the aggregate land rent at time is . Therefore the gross risk-free rate (return on land) is

| (2.6) |

Budget constraint

At time , a typical agent starts with wealth carried over from the previous period. The time budget constraint is

| (2.7) |

where is consumption, is investment, and is bond holdings. Note that corresponds to saving and corresponds to borrowing, where in the latter case is the amount borrowed. An agent with productivity who invests generates capital at time . Therefore the time wealth is defined by

| (2.8) |

Leverage constraint

Agents are subject to the collateral or leverage constraint

| (2.9) |

where is the exogenous leverage limit. Here is the net worth (“equity”) of the agent after consumption. The leverage constraint (2.9) implies that capital investment cannot exceed some multiple of total equity, which is standard in the literature as well as commonly used in practice.777According to standard accounting practices for constructing the balance sheet, equity equals asset () minus liability (), which is . The leverage is defined as the ratio between asset and equity. The leverage constraint (2.9) is identical the one in [88]; see their Footnote 9 or [73] for a discussion of microfoundations of this type of constraint. Note that since and , (2.9) implies that equity must be nonnegative: . Furthermore, solving (2.9) for and noting that , we obtain

| (2.10) |

so the leverage constraint (2.9) is equivalent to the borrowing constraint (2.10).

3 Equilibrium

The economy starts at with some initial allocation of capital and land across agents. Loosely speaking, a competitive equilibrium is defined by individual optimization and market clearing. We first characterize the individual behavior and then formally define and analyze the rational expectations equilibrium.

3.1 Individual behavior

Because the economy features no aggregate risk, the sequence of aggregate capital and land price is deterministic. Individual agents take these aggregate variables as given and maximize utility (2.1) subject to the budget constraints (2.7), (2.8) and the leverage constraint (2.9).

Due to log utility, as is well known, the optimal consumption rule is . How agents allocate savings to capital investment or REIT depends on their productivity. If an agent with productivity invests, the gross return on investment is . Therefore an agent invests if and only if

| (3.1) |

where is the productivity threshold for investment and is the gross risk-free rate in (2.6).888If , the agent is indifferent between capital investment and REIT and hence the portfolio is indeterminate. We need not worry about such cases because is atomless by Assumption 1 and hence the measure of indifferent agents is zero. Whenever (3.1) holds, the agent chooses maximal leverage to invest (so the leverage constraint (2.9) binds). Therefore the optimal asset allocation is

| (3.2) |

3.2 Rational expectations equilibrium

We now derive equilibrium conditions. Because land is securitized into REIT, which is a risk-free asset, the market capitalization of bonds equals the land price . Therefore aggregating the time wealth ((2.8) with time shifted by 1) across agents, and using the definition of the risk-free rate (2.6), aggregate wealth becomes

| (3.3) |

where the last equality uses the homogeneity of . As noted before, we see that (not ) constitutes aggregate wealth. Multiplying to investment in (3.2), aggregating individual capital across agents, and noting that productivities are independent across agents, we obtain

| (3.4) |

Aggregating bond holdings in (3.2) across agents and noting that the market capitalization of bonds equals the land price , we obtain

| (3.5) |

where we need so that . Therefore we may define a rational expectations equilibrium as follows.

Definition 1.

Given the initial aggregate capital , a rational expectations equilibrium consists of a sequence of gross risk-free rate, productivity threshold, aggregate wealth, aggregate capital, and land price such that 1. satisfies (2.6), 2. satisfies (3.1), 3. satisfies (3.3), 4. satisfies (3.4), and 5. satisfies (3.5).

According to Definition 1, the equilibrium is characterized by a system of five nonlinear difference equations in five unknowns. The following proposition shows that we can reduce the equilibrium to a two-dimensional dynamics.

Proposition 1.

Interestingly, this model produces the financial accelerator: the real economy and the land price reinforce each other. To see this formally, an increase in the land price raises the current aggregate wealth by (3.3). But an increase in raises the next period’s aggregate capital and wealth through investment and production: see (3.4). Finally, this increased wealth feeds back into the land price through the demand for savings: see (3.5). As we shall see below, whether this positive feedback loop can sustain economic growth and high asset valuation depends on how high the leverage is.

3.3 Asymptotic behavior

Because our model features homothetic preferences, a constant-returns-to-scale production function, and a production factor in fixed supply (land), one may conjecture that the economy must admit a steady state. However, this intuition is incorrect and it turns out that there are two possibilities for the long run behavior of the model. One possibility is that the economy converges to a steady state, consistent with the intuition. Another possibility is that the economy endogenously grows without bound, despite the presence of a fixed factor. In this section we study the asymptotic behavior of the model qualitatively. The main reason for focusing on the asymptotic behavior is that whether or not economic growth takes off is crucial for asset pricing implications. To determine whether the economy will grow or not, we first present a heuristic but intuitive argument, followed by formal propositions.

Suppose that a rational expectations equilibrium exists, and as , conjecture that there exist constants and growth rate such that

| (3.8) |

Suppose for the moment that the production function takes the CES form (2.4). Then the land rent is given by

| (3.9) |

Regardless of the value of , we have as , so (2.6) implies . Substituting (3.8) into (3.7), assuming , and using (2.3), we obtain

Canceling and eliminating , we obtain the long-run growth rate condition

| (3.10) |

In order for the economy to grow as conjectured, we need . We obtain the leverage threshold for determining growth () or no growth () by setting in (3.10) and solving for :

| (3.11) |

To ensure that the numerator of (3.6b) is positive (so ) at , we introduce the following assumption.

Assumption 3.

Let be a random variable with cdf . The model parameters satisfy , or equivalently

| (3.12) |

Because is the gross return on capital for an agent with productivity when aggregate capital is infinite (hence the marginal product of capital takes the asymptotic value in (2.3)) and the propensity to save is , the condition (3.12) roughly says that the wealth of productive agents can grow and the take-off of economic growth is possible.

The following proposition characterizes the asymptotic behavior of the model.

Proposition 2.

Proposition 2 has two implications. First, when leverage is below the threshold in (3.11), a steady state of the aggregate dynamics (3.7) exists. Thus, if the initial aggregate capital equals this steady state value, then a rational expectations equilibrium with constant aggregate variables (stationary equilibrium) exists. Second, when leverage exceeds the threshold , a unique growth rate consistent with the heuristic argument above exists. Of course, this does not necessarily justify the heuristic argument, which we turn to next.

The elasticity of substitution between capital and land plays a crucial role in determining the asymptotic behavior of the model. However, we need to distinguish the elasticity of the production function (which is in the CES case (2.4)) and the elasticity of substitution between and in the function in (2.2), denoted by below in (3.13). As it turns out, it is this that plays a key role for generating land price bubbles. In this sense, we identify which elasticity matters.

When we consider the elasticity of substitution between and in the function , it is defined by the percentage change in relative factor inputs with respect to the percentage change in relative factor prices

| (3.13) |

The following lemma shows that any production function satisfying Assumption 2 has elasticity of substitution above 1 at high capital levels.

Note that the right-hand side of (3.14) is always above 1 regardless of model parameters. Motivated by Lemma 3.1, we introduce the following assumption.

Assumption 4.

The elasticity of substitution between capital and land defined by (3.13) exceeds 1 at high capital levels:

According to Lemma 3.1, always exceeds 1 at high capital levels, so Assumption 4 is relatively weak. In particular, it is satisfied for the CES production function (2.4).999Although the elasticity of () does not matter, [90] empirically find that it also exceeds 1. The importance of the intertemporal elasticity of substitution in macro-finance models is well known [74, 127, 92]. The analogy here is only superficial because 1. the relevant elasticity of substitution in our model is between capital and land, not between consumption in different periods, and 2. macro-finance models typically assume outright that the asset price equals its fundamental value. The following proposition establishes the existence of an equilibrium with endogenous growth, which justifies the heuristic argument above.

4 Leverage, unbalanced growth, and asset prices

In this section, we study the asset pricing implications of the model.

4.1 Phase transition to unbalanced growth with bubbles

We say that the model dynamics exhibits balanced growth if aggregate capital, land prices, and rents all grow at the same rate (potentially equal to zero) in the long run. Otherwise, we say that the model dynamics exhibits unbalanced growth. As we shall see below, whether the economy exhibits balanced or unbalanced growth is crucial for asset pricing implications.

Define the date-0 price of consumption delivered at time (the price of a zero-coupon bond with face value 1 and maturity ) by , with the normalization . The fundamental value of land at time is defined by the present value of rents

| (4.1) |

where is the land rent at time . We say that land is overvalued or exhibits a bubble if .

If we focus on the CES production function (2.4) and consider the case in Proposition 2(ii), then the order of magnitude of rents (3.9) satisfy

where is the elasticity of substitution at high capital levels in (3.14). As discussed after (3.9), the interest rate converges to . Using (4.1), the order of magnitude of the fundamental value is

In contrast, we know from Proposition 3 that . Therefore, in the long run, land prices grow faster than rents and hence we will have a land bubble (). Moreover, the fact that the economy grows faster than rents implies that the land bubble economy exhibits unbalanced growth and the price-rent ratio will continue to rise without bound. The following theorem, which is the first main result of this paper, formalizes this argument.

Theorem 1 (Land Bubble Characterization).

Suppose Assumptions 1–4 hold and let be the leverage threshold in (3.11). Then the following statements are true.

-

(i)

If , in any equilibrium converging to the steady state, we have for all . The economy exhibits balanced growth and the price-rent ratio converges.

-

(ii)

If , in the equilibrium in Proposition 3, we have for all . The economy exhibits unbalanced growth and the price-rent ratio diverges to .

Theorem 1 states that as leverage is relaxed beyond a critical value , the economy experiences a phase transition from balanced growth without bubbles to unbalanced growth with bubbles. Intuitively, when leverage is sufficiently relaxed, aggregate capital starts to grow rapidly and land prices are pulled by growing aggregate capital, rising at a faster rate than land rents, therefore exhibiting bubbles. Interestingly, when leverage is low enough, in the steady state equilibrium, even if leverage changes, there is no impact on the long-run economic growth rate: the economy exhibits exogenous growth. However, once leverage exceeds the critical value, the behavior abruptly changes to endogenous growth.101010In the growth literature, when the production function takes the CES form (2.4) with elasticity of substitution , it is known that the average and marginal productivity of capital converge to a positive constant as , which can generate endogenous growth. The possibility of endogenous growth with this property with a general production function was already recognized by [136, p. 72 ]; see also [77, pp. 68–69 ]. [105] study an endogenous growth model along this line, in which their condition G is similar to our Assumption 3. In our model, captures the asymptotic slope and is positive regardless of the value of . Our paper connects this property of generating endogenous growth to financial leverage and shows that the level of financial leverage determines whether the economy exhibits exogenous and balanced growth or endogenous and unbalanced growth.

A distinctive feature of the bubble economy is that the land price is purely demand-driven. Despite the fact that the interest rate asymptotically converges, the land price continues to increase without bound, deviating from the growth rate of land rents. This is purely driven by sustained demand growth for land arising from economic growth. On the other hand, when the land price reflects fundamentals, the price movement is mainly supply-driven because the price is determined as the present discount value of land rents, which is a supply factor generated from land. The demand-driven financial accelerator is a key feature of the land bubble economy.

Moreover and interestingly, once the economy enters the bubbly regime, the dynamics of the price-dividend ratio changes qualitatively as do macroeconomic variables such as investment, output, and wealth. That is, the ratio will rise without bound, which appears to be explosive. In contrast, as long as the economy stays in the fundamental regime, even if the ratio rises driven by the financial accelerator, it converges to the steady-state value and hence does not exhibit explosive dynamics. In our model, since there is a qualitative difference in the price-rent ratio between the bubbly and fundamental regimes, it is possible to connect our model to the econometric literature on bubble detection [125, 123, 124], which uses the price-dividend ratio and is considered to be important for policy considerations.111111Of course, in reality, if policymakers decide that the observed price-rent ratio appears to be too high, they tend to introduce leverage regulations. If leverage is sufficiently tightened so that the land bubble is no longer sustainable, the bubble will surely collapse and the economy will return to the fundamental regime. With loosening and tightening of leverage due to policy changes (in a way contrary to private agents’ expectations), the economy might switch back and forth between two regimes, with upward and downward movements in the price-rent ratio. In reality, this process may repeat itself.

4.2 Financial conditions and bubbles

Theorem 1 provides a positive connection between financial conditions (here leverage) and asset price bubbles. Although this connection is intuitive, it is not at all straightforward to obtain theoretically. It is well known since [81], [135], and [112] that financial constraints are necessary for supporting asset price bubbles in infinite-horizon models. The literature since the 2008 financial crisis has explicitly modelled the role of financial constraints. This literature shows that bubbles are more likely to arise when financial conditions get tighter, not looser, contrary to intuition.121212Examples include [114, 115], [91], [86], [102], [111], [97], [103], and [126], among others. All of these papers study intrinsically worthless assets (money) instead of bubbles attached to real assets. See [101, §4.3 ] for a review of this literature. In contrast, Theorem 1 shows bubbles emerge as leverage is relaxed, which is consistent with intuition as well as stylized facts that bubbly episodes tend to be associated with loose financial conditions [108]. The reason for these completely opposite results lies in the methodological difference in model building. In the existing literature, perhaps for simplicity, researchers tend to assume two productivity types of agents. In these models, although the two-type assumption seems innocuous, when financial conditions get looser, markets become complete and bubbles are impossible. In contrast, this effect is absent in our model because there are a continuum of types and markets are always incomplete (see the comment after Assumption 1). To our knowledge, our paper is the first in macro-finance that shows a positive connection between loose financial conditions (financial accelerator) and asset price bubbles attached to real assets.

Using the explicit expression for the leverage threshold (3.11) for generating bubbles, we obtain the following comparative statics. We provide a complete characterization of the fundamental region and the land bubble region in the elasticity-leverage plane.

Proposition 4 (Comparative statics).

Let be the leverage threshold in (3.11). Then is decreasing in , where for the productivity distribution we use first-order stochastic dominance: if for all . Furthermore, if the production function takes the CES form (2.4), then is constant for and decreasing in the elasticity of substitution for .

Proposition 4 implies that more patience, higher marginal product of capital, and higher productivity all decrease the leverage threshold for generating bubbles and hence make bubbles more likely to emerge. Intuitively, these changes strengthen the positive feedback loop between capital investment and land prices, allowing the take-off of economic growth.

As an example, set in the CES production function (2.4) and

| (4.2) |

so productivity is exponentially distributed with decay rate . A derivation in Appendix C implies that the leverage threshold (3.11) equals

| (4.3) |

Figure 1 divides the parameter space into regions where a land bubble emerges or not, where the horizontal axis is the elasticity of substitution and the vertical axis is leverage . Depending on whether leverage exceeds the critical value , a land bubble emerges or the land price reflects its fundamental value. When , because , the leverage threshold (4.3) is independent of . When , consistent with Proposition 4, the boundary of the bubbly and fundamental regime is downward-sloping in .

Proposition 4 has two important implications. First, as we can see in Figure 1, for all values of the elasticity parameter , including the Cobb-Douglas production function with , the land bubble region will always emerge when the financial leverage gets sufficiently high. Second, the fact that the leverage threshold decreases as the overall productivity of the economy increases (in the sense of first order stochastic dominance) implies that technological innovations and asset price bubbles are closely linked. This result is consistent with the stylized fact that “asset price bubbles tend to appear in periods of excitement about innovations” highlighted by [134, p. 22 ]. In addition, [134] also points out that bubbles may have positive effects on innovative investments and economic growth by facilitating finance. Even in our model, bubbles ease financing, allowing the take-off of economic growth, which in turn sustains growing bubbles.

4.3 Numerical example

We present a numerical example that shows how changes in leverage or productivities lead to the emergence and collapse of land price bubbles. As our focus is to present a theoretical framework that can be used as a stepping stone for a variety of applications, we consider a minimal illustrative example.

Consider the CES production function (2.4) and the exponential productivity distribution (4.2). A derivation in Appendix C yields

| (4.4) |

Therefore (3.7a) simplifies to

| (4.5) |

We numerically solve the model using the algorithm discussed in Appendix C.

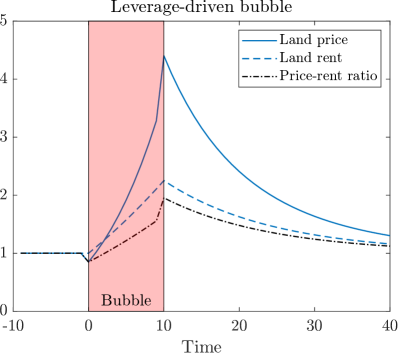

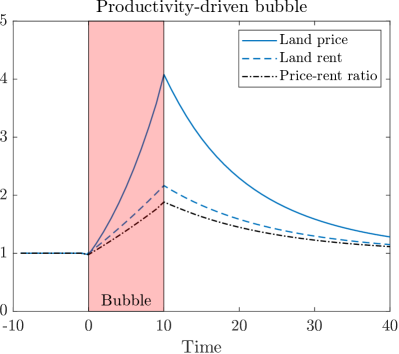

To illustrate the dynamics of land price bubbles and their collapse, suppose that financial condition (leverage) gets loose or the productivity of the economy rises so that the economy enters the bubbly regime. Suppose agents believe that these “good” conditions will persist forever and they actually do for a while. Once expectations change this way, macroeconomic variables such as aggregate capital, consumption, and land prices will all continue to rise with higher growth rates, while containing a land price bubble with a rising price-rent ratio. Suppose, however, that at some point, the situation unexpectedly changes and financial regulation severely tightens leverage or the productivity of the economy sufficiently declines so that the bubble is no longer sustainable. Then the bubble will surely collapse, and all macroeconomic variables will decline with a falling price-rent ratio. In this way, our model can describe the short-run onset of a bubble and its collapse.

Figure 2 shows two such numerical examples. The baseline parameter values are those used in Figure 1 and we set and so that agents are initially self-financing and the production function is Cobb-Douglas. The economy is initially in the fundamental steady state up to time , where we normalize the land price and rent to 1 for visibility. At , either the leverage increases to (left panel) or the average productivity increases to (right panel). In both cases, the economy takes off to the bubbly regime and land prices grow faster than land rents, as we can see from the steeper slope of the former. At , the parameters unexpectedly reverse to the baseline values and the economy reenters the fundamental regime. Then the bubble collapses and both land prices and rents decline.131313Note that during the leverage-driven bubble, the land price declines at . This is because output is predetermined through previous investments, and relaxing leverage makes agents substitute from bond to capital investment, reducing the demand for land. The opposite happens at the tightening stage and leads to land speculation. In contrast, during the productivity-driven bubble, this substitution effect is absent. In the course of these dynamics with the onset of land price bubbles and their collapse, the price-rent ratio rises and falls substantially.

In fact, this explanation is similar to what happened during Japan’s so-called “bubble period” in the 1980s. Various financial deregulation such as capital and interest rate liberalization and the introduction of derivatives such as convertible bonds and warrants in the early 1980s set the stage. Following the Plaza Accord on September 22, 1985 (that aimed to let the U.S. dollar depreciate relative to the Japanese yen and Deutsche Mark to curb the U.S. trade deficits), the Japanese yen appreciated from 240 JPY/USD to 150 within a year, causing a severe contraction in the manufacturing sector referred to as “endaka fukyō” (yen-appreciation recession). The Bank of Japan cut the official discount rate from 5.0% to 2.5% to stimulate the Japanese economy, which led to an expansion in the financial sector. At that time, Tokyo was believed to become a global financial hub. The “Japan money” flowed into the real estate sector and substantially increased the land price. For more details on Japan’s bubble economy in 1980s, see [101, §1.1 ] and the references therein.

5 Low rates, bubbles, and wealth inequality

In general, the equilibrium dynamics in Proposition 1 does not admit a closed-form expression. In this section we specialize the model to a two-sector large open economy, which is analytically more tractable. This model provides insights to the relationship between low interest rates, asset price bubbles, and wealth inequality.

5.1 Two-sector large open economy

Consider the special case where the production function is linear, so

| (5.1) |

with , which obviously satisfies Assumptions 2 and 4 with . This case can be interpreted as a two-sector economy in which the capital-intensive sector uses an technology and the land-intensive sector such as real estate, agriculture, or extraction of natural resources produces a constant rent every period. Because the marginal products and are constants, the dynamics (3.7) can be simplified. Furthermore, we consider a large open economy. By an “open” economy, as usual we mean that agents can lend to and borrow from an external source at a constant gross risk-free rate . By a “large” economy, we mean that in the long run, the amount of external debt (or savings) is negligible relative to the size of the economy.141414Another interpretation is that in a closed economy, the government issues debt so that the interest rate is constant over time and the size of government debt relative to the economy is negligible in the long run. This trick allows us to study a general equilibrium model that is stationary in some sense.

Let be the constant gross risk-free rate. Using the budget constraint (2.7), the definition of wealth (2.8) with , the optimal consumption rule , and the optimal asset allocation (3.2), individual wealth evolves according to

| (5.2) |

Obviously, the productivity threshold for investment is . Aggregating (5.2) across agents and noting that productivity is iid across agents, we obtain

| (5.3) |

where

| (5.4) |

is the risk premium (expected excess return) on unlevered capital investment. The aggregate wealth dynamics (5.3) implies that in an open economy, aggregate wealth grows at the constant gross growth rate

| (5.5) |

Let be aggregate external savings. Aggregating bond holdings in (3.2) across agents and noting that the market capitalization of bonds equals the land price plus external savings , it follows from (3.5) that

| (5.6) |

Since is proportional to , it also grows at rate . We now formally define an equilibrium in a large open economy as follows.

Definition 2.

Given the initial aggregate capital , a trend stationary equilibrium consists of gross risk-free rate , economic growth rate , productivity threshold , and a sequence of aggregate wealth, aggregate capital, land price, and external savings such that, 1. satisfies , 2. satisfies (5.5), 3. satisfies , 4. satisfies (5.3), 5. satisfies (3.4), 6. satisfies (5.6), and 7. as .

We call the equilibrium “trend stationary” because the aggregate dynamics becomes stationary after detrending by the growth rate . Note that condition 7 formalizes our “large” economy assumption. In any trend stationary equilibrium, the fundamental value of land (4.1) is constant at

We say that a trend stationary equilibrium is fundamental (bubbly) if () for all . The following theorem, which is the second main result of this paper, provides a complete characterization of trend stationary equilibria.

Theorem 2 (Land Bubble Characterization in trend stationary equilibria).

Suppose Assumptions 1, 3 hold and let be as in (3.11), (5.1). Then the following statements are true.

-

(i)

A unique fundamental trend stationary equilibrium exists if and only if , which satisfies , , and .

-

(ii)

A unique bubbly trend stationary equilibrium exists if and only if , which satisfies , , and

(5.7) where .

As we discuss in the related literature in Section 6, pure bubble models often admit a continuum of equilibria (models suffer from equilibrium indeterminacy) and hence model predictions are not robust. Once we consider bubbles attached to dividend-paying assets, Theorem 2 shows the uniqueness of equilibria and hence comparative statics are robust, which is important for applications.

5.2 Low interest rates and wealth inequality

Over the past four decades, a secular trend of declining interest rates and rising asset prices and wealth inequality has been observed in advanced economies [94]. Our model provides a framework that allows us to analyze asset price bubbles, thus making it possible to derive theoretical insights on the relationship between low interest rates, asset overvaluation, and top-end wealth concentration.151515Since the primary purpose of our paper is to construct a macro-finance theory to analyze asset price bubbles that can be a stepping stone for a variety of extensions, a full-blown quantitative analysis is beyond the scope.

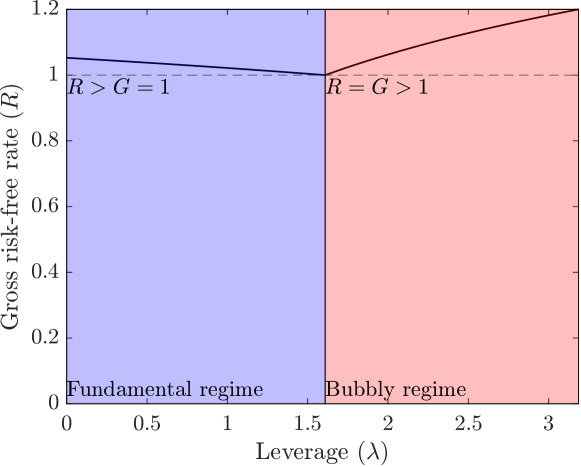

We start from the discussion of the interest rate. The following proposition shows that the equilibrium interest rate is V-shaped with respect to leverage (Figure 3).

Proposition 5.

Let everything be as in Theorem 2. Then the equilibrium gross risk-free rate is strictly decreasing (increasing) for ().

Proposition 5 implies that in the fundamental regime, financial loosening (relaxing leverage) leads to low interest rates. The intuition is as follows. As leverage is relaxed, productive entrepreneurs invest more, and ceteris paribus, their wealth growth rate increases. However, we know that in the fundamental regime, the aggregate economy does not grow. Because the aggregate wealth growth rate is the weighted average of individual wealth growth rates, it follows from accounting that the wealth growth rate of unproductive entrepreneurs (which is proportional to the gross risk-free rate) must decline. However, if leverage is relaxed further and exceeds the threshold , a phase transition occurs and the only possible trend stationary equilibrium becomes bubbly. This is because without bubbles, the interest rate would be less than one and land prices would become infinite, which is impossible in equilibrium.161616[100] provide a conceptually new idea of necessity of asset price bubbles and prove that bubbles necessarily arise in certain workhorse macroeconomic models. In our two-sector large open economy model, when , since the counterfactual gross risk-free rate without bubbles is less than one and land prices grow faster than land rents, the bubble necessity condition is satisfied. With a phase transition to the bubble economy, the growth behavior changes to endogenous growth, with the growth rates of production and land prices both increasing with leverage, leading to higher interest rates.

We next turn to wealth inequality. Because the individual wealth dynamics (5.2) is a random multiplicative process (logarithmic random walk), it does not admit a stationary distribution if agents are infinitely lived. To obtain a stationary wealth distribution, as is common in the literature, we consider a [140]-type perpetual youth model in which agents survive with probability every period, and deceased agents are replaced with newborn agents. If we assume that the discount factor already includes the survival probability and that the wealth of deceased agents is equally redistributed to newborn agents,171717It is straightforward to consider settings where there are life insurance companies that offer annuities to agents, there are estate taxes, or newborn agents start with wealth drawn from some initial distribution. the aggregate dynamics (5.3) remains identical to the infinitely-lived case. We discuss each case and in Theorem 2 separately.

If , then is constant. Define the relative wealth , where we have shifted the time subscript because is determined at time . Then dividing the equation of motion for wealth (5.2) by and using the equilibrium condition to eliminate , we obtain

| (5.8) |

where

| (5.9) |

If , then . Dividing the equation of motion for wealth (5.2) by and using the equilibrium condition to eliminate , we obtain

| (5.10) |

According to the definition in [79, §2 ], the stochastic processes (5.8) and (5.10) are both Markov multiplicative process with reset probability , which admit unique stationary distributions. To characterize the tail behavior of the wealth distribution, we introduce the following assumption.

Assumption 5.

The productivity distribution is thin-tailed, i.e., for all the productivity distribution has a finite -th moment: .

Assumption 5 is sufficient (but not necessary) for (5.11) below to have a solution. See [79, Fig. 2(c) ] for why this type of assumption is needed. The following proposition establishes the uniqueness of the stationary relative wealth distribution and characterizes its tail behavior.

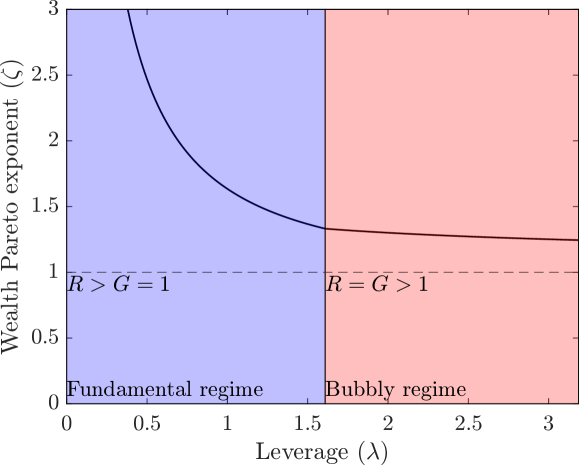

Proposition 6 (Wealth distribution).

Suppose Assumptions 1, 3, 5 hold, , agents survive with probability , and consider the unique trend stationary equilibrium established in Theorem 2 with interest rate and wealth growth rate . Then the following statements are true.

-

(i)

There exists a unique stationary distribution of relative wealth .

-

(ii)

The stationary distribution has a Pareto upper tail with exponent in the sense that exists.

- (iii)

-

(iv)

Letting be the Pareto exponents in the fundamental and bubbly regime determined by (5.11) given the equilibrium interest rate , we have .

As shown by Proposition 1 of [79], in (5.11) is convex is and , which explains the uniqueness of . Noting that by the definitions of in (5.4) and in (5.9), we obtain , which explains . Intuitively, follows from the fact that in equilibrium, the wealth distribution must have a finite mean (otherwise market clearing is not well defined). As , we obtain , which is known as Zipf’s law. The fact that the Pareto exponent is lower (top-end wealth inequality is higher) in the bubbly regime than in the fundamental regime corresponding to the same equilibrium interest rate is that the “growth shock” in (5.9) is multiplied by in the bubbly regime (see (5.10)), whereas it is multiplied by in the fundamental regime (see (5.8), and we have because . Figure 4 shows that the Pareto exponent is decreasing (top-end wealth inequality is increasing) in leverage. The intuition is as follows. In the fundamental regime, the interest rate decreases with leverage. While productive agents earn more due to the higher leverage, less productive agents earn less due to the lower interest rate, which widens the rate of return difference and leads to greater top-end wealth concentration. Once the economy enters the bubbly regime, the interest rate increases with leverage. While productive agents still earn more, the higher interest rate allows less productive agents to catch up. Therefore, the Pareto exponent sill decreases in the bubbly regime but the slope is less steeper. Together with Proposition 5, relaxation in leverage in the fundamental regime leads to low interest rates, asset price increase, and greater top-end wealth concentration, and if it is relaxed sufficiently, asset price bubbles simultaneously occur, with further wealth concentration at the top.

6 Related literature and discussion

The macro-finance literature stresses the importance of the financial accelerator, including [95], [110], [80], [128], [118], and [85], among others. In this literature, asset prices (land or stocks yielding positive dividends) reflect fundamentals. In contrast, we develop a macro-finance theory to analyze asset price bubbles. We identify economic conditions in relation to the financial accelerator under which land prices exceed the fundamental value, containing a bubble.

Regarding unbalanced growth, our paper is related to [78], [120], and [87]. There are two main differences from our paper. First, we use homothetic preferences and whether the economy exhibits balanced or unbalanced growth depends on the financial leverage, while these papers use non-homothetic preferences to generate unbalanced growth and do not consider financial frictions. Second, these papers abstract from asset pricing, including [71] who consider unbalanced growth under homothetic preferences.

Our paper is related to the large literature on monetary models initiated by seminal papers of [131], [81], [138], and [135]; see [101] for a recent review. Money is often called “pure bubbles” because it generates no dividends and hence is intrinsically worthless. The so-called “rational bubble literature” has almost exclusively focused on pure bubbles due to the fundamental difficulty of attaching bubbles to dividend-paying assets [133, Theorem 3.3, Corollary 3.4]. However, as [101, §4.7 ] argue, pure bubble models have fundamental limitations in describing stock, land, and housing price bubbles such as the lack of realism, the inability to define the price-dividend ratio, and equilibrium indeterminacy. Although some monetary equilibria are determinate [84, 132] (and likewise some non-monetary equilibria are indeterminate as in [93]), they require strong assumptions on preferences. We challenge the conventional view and study bubbles attached to real assets in a standard macro-finance model in which the price-dividend ratio is well-defined and the equilibrium is determinate.

To the best of our knowledge, [139, §7 ] provides the first example of bubbles attached to dividend-paying assets. While pioneering, his analysis is limited to giving an example in a fairly limited setting (two-period overlapping generations endowment economy with linear utility). [138, Proposition 1(c) ] appears to extend [139]’s result within a two-period overlapping generations production economy with capital, although [139]’s result is not acknowledged. [138, Proposition 1(c) ] also discusses that under some conditions, bubbles are necessary for the existence of equilibrium. However, as [101, §5.2 ] discuss in greater details, he did not provide a formal proof for these results. We generalize [139]’s idea and promote it to a standard macro-finance model with infinitely-lived heterogeneous agents.

Our paper studies asset price bubbles in an infinite-horizon incomplete-market model. In this regard, our paper is closely related to [112, 113, 114], [133], [98], and [83]. While these papers are based on endowment economies, we consider land price bubbles in a macro-finance model with investment and production, which is important for creating the land bubble economy through phase transition and endogenous growth.

With regard to a macro-finance model that shows bubbles attached to an asset with positive dividends, our paper is related to [75] and [72], who develop the so-called “risk-shifting models” of bubbles in which agents hold rational expectations and buy assets by borrowing. A critical assumption in this approach is the presence of asymmetric information, i.e., lenders cannot distinguish types of borrowers, which allows asset prices to exceed fundamentals (the same definition as ours). We focus on rational bubbles and abstract from asymmetric information but the two different approach should be viewed as complementary, not as a substitute. [76] provides an extensive survey on risk-shifting and rational bubbles approaches.

Finally, we would like to mention the connection to monetary theory, which includes seminal contributions by [117], [129, 130], and [116]. This literature studies money or real assets as a medium of exchange using a search-theoretic approach and liquidity premium is interpreted as bubbles. Changes in the tightness of liquidity constraints or in people’s belief affect the liquidity premium, generating fluctuations in asset prices. Our paper studies rational asset price bubbles attached to real assets in a competitive economy following the standard definition of bubbles (violation of the transversality condition),181818The term “transversality condition” has two meanings: one is the transversality condition (B.5) for asset pricing (which is violated under bubbles) and the other is that for optimality in infinite-horizon optimization problems (which is always satisfied). One should clearly distinguish the two. Also, our definition of asset price bubbles simply follows that in the literature; see for instance [138, Footnote 8 ], [82, Ch. 5 ], and [101, §2 ]. which is different from the liquidity premium. Obviously, the two approaches are complementary and provide different insights for the determination of asset prices.

7 Conclusion

Since the [119] asset pricing model, significant progress has been made in the modern macro-finance theory of asset prices. Although the term “asset price bubbles” are commonly discussed in the popular press and among policymakers, the conventional wisdom in the literature suggests that asset price bubbles are either not possible or even if they are, a situation in which bubbles occur is a special circumstance and hence fragile. Indeed, as shown by [133, Theorem 3.3, Corollary 3.4 ], there are fundamental difficulties in generating asset overvaluation in dividend-paying assets. Perhaps because of this difficulty and also because there is no benchmark macro-finance model to think about bubbles attached to real assets, it seems that there is a presupposition that asset prices should reflect fundamental values. In this paper, we have challenged this long-standing conventional view and have presented a new macro-finance framework to think about asset price bubbles attached to real assets.

The new finding we have uncovered is that whether asset prices reflect fundamentals or contain a bubble critically depends on whether the economy exhibits balanced growth of a stationary nature or unbalanced growth of a nonstationary nature. Asset pricing implications in a world of stationarity and a world of nonstationarity are markedly different. Constructing a dynamic general equilibrium macro-finance theory with incomplete markets and heterogeneous agents, we have established the Land Bubble Characterization Theorem 1, the first main result, showing that whether the economy exhibits balanced or unbalanced growth is endogenously determined and crucially depends on the level of the financial leverage. There exists a critical value of leverage above which a phase transition to unbalanced growth dynamics occurs, leading to land bubbles, while below which the economy keeps balanced growth in the long run and land prices reflect the fundamental value. Driven by a sufficiently strong financial accelerator, once the phase of the economy turns to the land bubble economy, the dynamics of macroeconomic variables such as land prices, the price-rent ratio, and economic growth changes abruptly and qualitatively. The price-rent ratio will rise without bound and the growth behavior changes to endogenous growth despite the presence of a fixed factor, i.e., land.

We extended the baseline model to an analytically tractable case of a two-sector large open economy with capital- and land-intensive sectors and have derived our second main result. This Land Bubble Characterization Theorem 2 for trend stationary equilibria shows that a unique bubbly (fundamental) equilibrium exists if and only if leverage is above (below) the critical value and thus provides a complete characterization of land bubbles. Furthermore, as an application, we have studied the relationship between low interest rates, asset prices, and wealth inequality. We have shown that as leverage is relaxed in the fundamental regime, it leads to low interest rates, asset price increase, and greater top-end wealth concentration. If it is sufficiently relaxed, asset price bubbles simultaneously occur, with further wealth concentration to the top. These dynamics are at least consistent with stylized facts over the past four decades in advanced economies.

Appendix A Proofs

A.1 Proof of Proposition 1

A.2 Proof of Proposition 2

We prove Proposition 2 by establishing a series of lemmas. Below, Assumptions 1–3 are in force. If a steady state exists, then (3.6a)–(3.7b) imply

| (A.1a) | ||||

| (A.1b) | ||||

where we have used .

Lemma A.1.

If , for any , there exists a unique solving (A.1a).

Proof.

We can rewrite (A.1a) as

| (A.2) |

Due to the concavity of , the right-hand side of (A.2) is strictly decreasing and tends to as by (2.3). Therefore (A.2) has a unique solution if and only if and

By Assumption 1, we have , so if . Therefore achieves a minimum at , and

where the last inequality uses (3.11). Therefore if , then , and there exists a unique satisfying (A.1a). ∎

Lemma A.2.

If , the dynamics (3.7) has a steady state.

Proof.

For any , let be the in Lemma A.1. As , the left-hand side of (A.2) tends to , so by the Inada condition. Then the left-hand side of (A.1b) tends to , while the right-hand side remains finite (because and ). As , we have , so the right-hand side of (A.1b) tends to , while the left-hand side remains finite. Therefore by the intermediate value theorem, there exits solving (A.1b) for , and hence there exists a steady state. ∎

Lemma A.3.

There exists a unique satisfying (3.10). Furthermore, if and only if .

Proof.

Letting , we can rewrite (3.10) as

| (A.3) |

Clearly is continuously differentiable in . Let . Then

Therefore by the intermediate value theorem, there exists such that . Since is a cdf and hence , we obtain

so the value of is unique. When , (A.3) implies that

By the implicit function theorem, . Therefore . Since is strictly increasing, we have if and only if , where . Setting in (3.10), solves

which gives (3.11). ∎

A.3 Proof of Lemma 3.1

Let and . Using (3.13) and applying l’Hôpital’s rule, we obtain

| (A.4) |

Therefore to prove the claim, it suffices to show for large enough . Since and is homogeneous of degree 1, we have , so

implying for large enough .

A.4 Proof of Proposition 3

We need the following lemma to prove Proposition 3.

Lemma A.4.

Let and suppose that for . Let . If , then

| (A.5) |

Proof.

Proof of Proposition 3.

We establish the claim by applying the local stable manifold theorem (see [104, Theorems 6.5 and 6.9 ] and [96, Theorem 1.4.2 ]), which is essentially linearization and evaluating the magnitude of eigenvalues. Since a complete proof is technical and tedious (see the appendix of [100] for a rigorous argument in a related model), we only provide a sketch.

Let . Then the steady state productivity threshold is . Around the steady state, combining (3.6a), (3.7a), and (2.3), the capital dynamics is approximately

where we define . Linearizing (3.6b) with respect to around , we have

| (A.7) |

where . By Lemma A.4, we have , where by Assumption 4. Substituting (A.7) into (3.7b) and using , we obtain

where . Noting that and solving for , we obtain

Therefore if we define and , the dynamics of near the steady state is approximately for the matrix

Clearly, the eigenvalues of are and because . Since is exogenous but is endogenous, for any sufficiently large (hence sufficiently close to 0), by the local stable manifold theorem, there exists a unique equilibrium path converging to the steady state 0. ∎

A.5 Proof of Theorem 1

Suppose and consider any equilibrium converging to the steady state. Then by definition converges to a finite positive number, so . By Lemma B.1, we have .

Next, suppose and consider the equilibrium in Proposition 3. By Assumption 4, we have . Take any . Then we can take such that for all . By Proposition 3, we have . Therefore for large enough , we have . By Lemma A.4, we have

Therefore for large enough , we have the order of magnitude

which is summable because . By Lemma B.1, we have for all . ∎

A.6 Proof of Proposition 4

That is decreasing in and are obvious. The monotonicity with respect to follows from the definition of first-order stochastic dominance and noting that is increasing in .

If the production function takes the CES form (2.4), as , we have

Clearly is decreasing in because . Therefore is decreasing in . ∎

A.7 Proof of Theorem 2

Lemma A.5.

In any trend stationary equilibrium, we have .

Proof.

Lemma A.6.

In a trend stationary equilibrium with , we have and .

Proof.

Lemma A.7.

In a trend stationary equilibrium with , we have , , and satisfies (5.7).

Proof.

If , then aggregate wealth grows exponentially. Dividing both sides of (5.6) and letting , it follows from condition 7 that . Using the definition of the gross risk-free rate and , we obtain

so . Iterating the no-arbitrage condition forward, we obtain

| (A.8) |

On the other hand, (5.6) and imply , so

| (A.9) |

Subtracting (A.8) from (A.9), we obtain

| (A.10) |

However, using , we obtain as by condition 7. Therefore letting in (A.10), we obtain . Then (5.6) implies

To show (5.7), it suffices to show . Aggregating individual wealth as in the derivation of (3.5), we obtain

where we have used and with . Since is exogenous, the initial aggregate wealth is uniquely determined. ∎

Lemma A.8.

Proof.

Proof of Theorem 2.

By Lemma A.5, a trend stationary equilibrium satisfies . By Lemmas A.6 and A.7, a trend stationary is fundamental (bubbly) if (). Furthermore, a unique trend stationary equilibrium exists if and only if such uniquely exists.

A.8 Proof of Proposition 5

A.9 Proof of Proposition 6

The uniqueness of the stationary relative wealth distribution follows from Proposition 3 of [79]. To show the Pareto tail result, define by (5.11) for . By Assumption 5, we have for all , and clearly is continuous. Assumption 1 implies (and hence ) with positive probability, so . Noting that by the definitions of in (5.4) and in (5.9), we obtain . Therefore by the intermediate value theorem, there exists such that . By Proposition 1 of [79], is unique.

By Assumption 1, the cdf is atomless. Therefore by Theorem 2 of [79], the stationary distribution of relative wealth has a Pareto upper tail with exponent in the sense that exists.

Since and implies , by Proposition 5 of [79] (where and correspond to in their paper), it follows that . ∎

References

- [1] Robert M Solow “A Contribution to the Theory of Economic Growth” In Quarterly Journal of Economics 70.1, 1956, pp. 65–94 DOI: 10.2307/1884513

- [2] Paul A. Samuelson “An Exact Consumption-Loan Model of Interest with or without the Social Contrivance of Money” In Journal of Political Economy 66.6, 1958, pp. 467–482 DOI: 10.1086/258100

- [3] Menahem E. Yaari “Uncertain Lifetime, Life Insurance, and the Theory of the Consumer” In Review of Economic Studies 32.2, 1965, pp. 137–150 DOI: 10.2307/2296058

- [4] William J. Baumol “Macroeconomics of Unbalanced Growth: The Anatomy of Urban Crisis” In American Economic Review 57.3, 1967, pp. 415–426

- [5] Robert E. Lucas “Asset Prices in an Exchange Economy” In Econometrica 46.6, 1978, pp. 1429–1445 DOI: 10.2307/1913837

- [6] Truman Bewley “The Optimum Quantity of Money” In Models of Monetary Economies Federal Reserve Bank of Minneapolis, 1980, pp. 169–210

- [7] William A. Brock and José A. Scheinkman “Some Remarks on Monetary Policy in an Overlapping Generations Model” In Models of Monetary Economies Federal Reserve Bank of Minneapolis, 1980

- [8] Michael C. Irwin “Smooth Dynamical Systems” New York: Academic Press, 1980

- [9] Charles A. Wilson “Equilibrium in Dynamic Models with an Infinity of Agents” In Journal of Economic Theory 24.1, 1981, pp. 95–111 DOI: 10.1016/0022-0531(81)90066-1

- [10] John Guckenheimer and Philip Holmes “Nonlinear Oscillations, Dynamical Systems, and Bifurcations of Vector Fields” 42, Applied Mathematical Sciences New York: Springer, 1983 DOI: 10.1007/978-1-4612-1140-2

- [11] Jean Tirole “Asset Bubbles and Overlapping Generations” In Econometrica 53.6, 1985, pp. 1499–1528 DOI: 10.2307/1913232

- [12] José A. Scheinkman and Lawrence Weiss “Borrowing Constraints and Aggregate Economic Activity” In Econometrica 54.1, 1986, pp. 23–45 DOI: 10.2307/1914155

- [13] Olivier Blanchard and Stanley Fischer “Lectures on Macroeconomics” Cambridge, MA: MIT Press, 1989

- [14] Larry E. Jones and Rodolfo Manuelli “A Convex Model of Equilibrium Growth: Theory and Policy Implications” In Journal of Political Economy 98.5, 1990, pp. 1008–1038 DOI: 10.1086/261717

- [15] Manuel S. Santos “Existence of Equilibria for Monetary Economies” In International Economic Review 31.4, 1990, pp. 783–797 DOI: 10.2307/2527016

- [16] Abhijit V. Banerjee and Andrew F. Newman “Risk-Bearing and the Theory of Income Distribution” In Review of Economic Studies 58.2, 1991, pp. 211–235 DOI: 10.2307/2297965

- [17] Wilbur John Coleman “Equilibrium in a Production Economy with an Income Tax” In Econometrica 59.4, 1991, pp. 1091–1104 DOI: 10.2307/2938175

- [18] Narayana R. Kocherlakota “Bubbles and Constraints on Debt Accumulation” In Journal of Economic Theory 57.1, 1992, pp. 245–256 DOI: 10.1016/S0022-0531(05)80052-3

- [19] Kiminori Matsuyama “Agricultural Productivity, Comparative Advantage, and Economic Growth” In Journal of Economic Theory 58.2, 1992, pp. 317–334 DOI: 10.1016/0022-0531(92)90057-O

- [20] Bruce C. Greenwald and Joseph E. Stiglitz “Financial Market Imperfections and Business Cycles” In Quarterly Journal of Economics 108.1, 1993, pp. 77–114 DOI: 10.2307/2118496

- [21] Nobuhiro Kiyotaki and John Moore “Credit Cycles” In Journal of Political Economy 105.2, 1997, pp. 211–248 DOI: 10.1086/262072

- [22] Manuel S. Santos and Michael Woodford “Rational Asset Pricing Bubbles” In Econometrica 65.1, 1997, pp. 19–57 DOI: 10.2307/2171812

- [23] Takashi Kamihigashi “Uniqueness of Asset Prices in an Exchange Economy with Unbounded Utility” In Economic Theory 12.1, 1998, pp. 103–122 DOI: 10.1007/s001990050212

- [24] Nobuhiro Kiyotaki “Credit and Business Cycles” In Japanese Economic Review 49.1, 1998, pp. 18–35 DOI: 10.1111/1468-5876.00069

- [25] Ben S. Bernanke, Mark Gertler and Simon Gilchrist “The Financial Accelerator in a Quantitative Business Cycle Framework” In Handbook of Macroeconomics 1 Elsevier, 1999, pp. 1341–1393 DOI: 10.1016/S1574-0048(99)10034-X

- [26] Charles P. Kindleberger “Manias, Panics, and Crashes” New York: John Wiley & Sons, 2000

- [27] Luigi Montrucchio and Fabio Privileggi “On Fragility of Bubbles in Equilibrium Asset Pricing Models of Lucas-Type” In Journal of Economic Theory 101.1, 2001, pp. 158–188 DOI: 10.1006/jeth.2000.2718

- [28] Ravi Bansal and Amir Yaron “Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles” In Journal of Finance 59.4, 2004, pp. 1481–1509 DOI: 10.1111/j.1540-6261.2004.00670.x

- [29] Robert J. Barro and Xavier Sala-i-Martin “Economic Growth” Cambridge, MA: MIT Press, 2004

- [30] Luigi Montrucchio “Cass Transversality Condition and Sequential Asset Bubbles” In Economic Theory 24.3, 2004, pp. 645–663 DOI: 10.1007/s00199-004-0502-8

- [31] Pietro Reichlin “Credit Markets and the Macroeconomy: Readings and Perspectives in Modern Financial Theory” In Credit Markets, Intermediation and the Macroeconomy Oxford University Press, 2004, pp. 856–892

- [32] Ricardo Lagos and Randall Wright “A Unified Framework for Monetary Theory and Policy Analysis” In Journal of Political Economy 113.3, 2005, pp. 463–484 DOI: 10.1086/429804

- [33] Guillaume Rocheteau and Randall Wright “Money in Search Equilibrium, in Competitive Equilibrium, and in Competitive Search Equilibrium” In Econometrica 73.1, 2005, pp. 175–202 DOI: 10.1111/j.1468-0262.2005.00568.x

- [34] Daron Acemoglu and Veronica Guerrieri “Capital Deepening and Nonbalanced Economic Growth” In Journal of Political Economy 116.3, 2008, pp. 467–498 DOI: 10.1086/589523

- [35] Narayana R. Kocherlakota “Injecting Rational Bubbles” In Journal of Economic Theory 142.1, 2008, pp. 218–232 DOI: 10.1016/j.jet.2006.07.010

- [36] Guido Lorenzoni “Inefficient Credit Booms” In Review of Economic Studies 75.3, 2008, pp. 809–833 DOI: 10.1111/j.1467-937X.2008.00494.x

- [37] Christian Hellwig and Guido Lorenzoni “Bubbles and Self-Enforcing Debt” In Econometrica 77.4, 2009, pp. 1137–1164 DOI: 10.3982/ECTA6754

- [38] Narayana R. Kocherlakota “Bursting Bubbles: Consequences and Cures” Unpublished manuscript, 2009

- [39] Yeneng Sun and Yongchao Zhang “Individual Risk and Lebesgue Extension without Aggregate Uncertainty” In Journal of Economic Theory 144.1, 2009, pp. 432–443 DOI: 10.1016/j.jet.2008.05.001

- [40] Dennis Epple, Brett Gordon and Holger Sieg “A New Approach to Estimating the Production Function for Housing” In American Economic Review 100.3, 2010, pp. 905–924 DOI: 10.1257/aer.100.3.905

- [41] Francisco J. Buera and Joseph P. Kaboski “The Rise of the Service Economy” In American Economic Review 102.6, 2012, pp. 2540–2569 DOI: 10.1257/aer.102.6.2540

- [42] Emmanuel Farhi and Jean Tirole “Bubbly Liquidity” In Review of Economic Studies 79.2, 2012, pp. 678–706 DOI: 10.1093/restud/rdr039

- [43] Francisco J. Buera and Yongseok Shin “Financial Frictions and the Persistence of History: A Quantitative Exploration” In Journal of Political Economy 121.2, 2013, pp. 221–272 DOI: 10.1086/670271

- [44] Narayana R. Kocherlakota “Two Models of Land Overvaluation and Their Implications” In The Origins, History, and Future of the Federal Reserve Cambridge University Press, 2013, pp. 374–398 DOI: 10.1017/CBO9781139005166.012

- [45] Guillaume Rocheteau and Randall Wright “Liquidity and Asset-Market Dynamics” In Journal of Monetary Economics 60.2, 2013, pp. 275–294 DOI: 10.1016/j.jmoneco.2012.11.002

- [46] Gadi Barlevy “A Leverage-Based Model of Speculative Bubbles” In Journal of Economic Theory 153, 2014, pp. 459–505 DOI: 10.1016/j.jet.2014.07.012

- [47] Markus K. Brunnermeier and Yuliy Sannikov “A Macroeconomic Model with a Financial Sector” In American Economic Review 104.2, 2014, pp. 379–421 DOI: 10.1257/aer.104.2.379

- [48] José A. Scheinkman “Speculation, Trading, and Bubbles”, Kenneth J. Arrow Lecture Series Columbia University Press, 2014 DOI: 10.7312/sche15902

- [49] Òscar Jordà, Moritz Schularick and Alan M. Taylor “Leveraged Bubbles” In Journal of Monetary Economics 76, 2015, pp. S1–S20 DOI: 10.1016/j.jmoneco.2015.08.005

- [50] Peter C.. Phillips, Shuping Shi and Jun Yu “Testing for Multiple Bubbles: Historical Episodes of Exuberance and Collapse in the S&P 500” In International Economic Review 56.4, 2015, pp. 1043–1078 DOI: 10.1111/iere.12132

- [51] Markus K. Brunnermeier and Yuliy Sannikov “On the Optimal Inflation Rate” In American Economic Review: Papers and Proceedings 106.5, 2016, pp. 484–489 DOI: 10.1257/aer.p20161076

- [52] Tomohiro Hirano and Noriyuki Yanagawa “Asset Bubbles, Endogenous Growth, and Financial Frictions” In Review of Economic Studies 84.1, 2017, pp. 406–443 DOI: 10.1093/restud/rdw059

- [53] Ricardo Lagos, Guillaume Rocheteau and Randall Wright “Liquidity: A New Monetarist Perspective” In Journal of Economic Literature 55.2, 2017, pp. 371–440 DOI: 10.1257/jel.20141195

- [54] Gadi Barlevy “Bridging between Policymakers’ and Economists’ Views on Bubbles” In Economic Perspectives 42.4 Federal Reserve Bank of Chicago, 2018 DOI: 10.21033/ep-2018-4

- [55] Peter C.. Phillips and Shuping Shi “Financial Bubble Implosion and Reverse Regression” In Econometric Theory 34.4, 2018, pp. 705–753 DOI: 10.1017/S0266466617000202

- [56] Walter Pohl, Karl Schmedders and Ole Wilms “Higher-Order Effects in Asset Pricing Models with Long-Run Risks” In Journal of Finance 73.3, 2018, pp. 1061–1111 DOI: 10.1111/jofi.12615

- [57] Gaetano Bloise and Alessandro Citanna “Asset Shortages, Liquidity and Speculative Bubbles” In Journal of Economic Theory 183, 2019, pp. 952–990 DOI: 10.1016/j.jet.2019.07.011

- [58] Nobuhiro Kiyotaki and John Moore “Liquidity, Business Cycles, and Monetary Policy” In Journal of Political Economy 127.6, 2019, pp. 2926–2966 DOI: 10.1086/701891

- [59] Peter C.. Phillips and Shuping Shi “Real Time Monitoring of Asset Markets: Bubbles and Crises” In Handbook of Statistics 42 Elsevier, 2020, pp. 61–80 DOI: 10.1016/bs.host.2018.12.002

- [60] Nicolae Gârleanu and Stavros Panageas “What to Expect When Everyone is Expecting: Self-Fulfilling Expectations and Asset-Pricing Puzzles” In Journal of Financial Economics 140.1, 2021, pp. 54–73 DOI: 10.1016/j.jfineco.2020.10.007

- [61] Franklin Allen, Gadi Barlevy and Douglas Gale “Asset Price Booms and Macroeconomic Policy: A Risk-Shifting Approach” In American Economic Journal: Macroeconomics 14.2, 2022, pp. 243–280 DOI: 10.1257/mac.20200041

- [62] Brendan K. Beare and Alexis Akira Toda “Determination of Pareto Exponents in Economic Models Driven by Markov Multiplicative Processes” In Econometrica 90.4, 2022, pp. 1811–1833 DOI: 10.3982/ECTA17984

- [63] Tomohiro Hirano, Ryo Jinnai and Alexis Akira Toda “Necessity of Rational Asset Price Bubbles in Two-Sector Growth Economies”, 2022 arXiv:2211.13100v4 [econ.TH]

- [64] Joel P. Flynn, Lawrence D.. Schmidt and Alexis Akira Toda “Robust Comparative Statics for the Elasticity of Intertemporal Substitution” In Theoretical Economics 18.1, 2023, pp. 231–265 DOI: 10.3982/TE4117

- [65] Pablo A. Guerron-Quintana, Tomohiro Hirano and Ryo Jinnai “Bubbles, Crashes, and Economic Growth: Theory and Evidence” In American Economic Journal: Macroeconomics 15.2, 2023, pp. 333–371 DOI: 10.1257/mac.20220015

- [66] Tomohiro Hirano and Alexis Akira Toda “Bubble Necessity Theorem” Revise and resubmit at Journal of Political Economy, 2023 arXiv:2305.08268 [econ.TH]

- [67] Takeo Hori and Ryonghun Im “Asset Bubbles, Entrepreneurial Risks, and Economic Growth” In Journal of Economic Theory 210, 2023, pp. 105663 DOI: 10.1016/j.jet.2023.105663

- [68] Guillaume Plantin “Asset Bubbles and Inflation as Competing Monetary Phenomena” In Journal of Economic Theory 212, 2023, pp. 105711 DOI: 10.1016/j.jet.2023.105711

- [69] Matthieu Gomez and Émilien Gouin-Bonenfant “Wealth Inequality in a Low Rate Environment” In Econometrica 92.1, 2024, pp. 201–246 DOI: 10.3982/ECTA19092

- [70] Tomohiro Hirano and Alexis Akira Toda “Bubble Economics” In Journal of Mathematical Economics 111, 2024, pp. 102944 DOI: 10.1016/j.jmateco.2024.102944

References

- [71] Daron Acemoglu and Veronica Guerrieri “Capital Deepening and Nonbalanced Economic Growth” In Journal of Political Economy 116.3, 2008, pp. 467–498 DOI: 10.1086/589523

- [72] Franklin Allen, Gadi Barlevy and Douglas Gale “Asset Price Booms and Macroeconomic Policy: A Risk-Shifting Approach” In American Economic Journal: Macroeconomics 14.2, 2022, pp. 243–280 DOI: 10.1257/mac.20200041

- [73] Abhijit V. Banerjee and Andrew F. Newman “Risk-Bearing and the Theory of Income Distribution” In Review of Economic Studies 58.2, 1991, pp. 211–235 DOI: 10.2307/2297965

- [74] Ravi Bansal and Amir Yaron “Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles” In Journal of Finance 59.4, 2004, pp. 1481–1509 DOI: 10.1111/j.1540-6261.2004.00670.x

- [75] Gadi Barlevy “A Leverage-Based Model of Speculative Bubbles” In Journal of Economic Theory 153, 2014, pp. 459–505 DOI: 10.1016/j.jet.2014.07.012