Global optimization for the portfolio selection model with high-order moments

Abstract.

In this paper, we study the global optimality of polynomial portfolio optimization (PPO). The PPO is a kind of portfolio selection model with high-order moments and flexible risk preference parameters. We introduce a perturbation sample average approximation method, which can give a robust approximation of the PPO in form of linear conic optimization. The approximated problem can be solved globally with Moment-SOS relaxations. We summarize a semidefinite algorithm, which can be used to find reliable approximations of the optimal value and optimizer set of the PPO. Numerical examples are given to show the efficiency of the algorithm.

Key words and phrases:

portfolio selection model, high-order moments, Moment-SOS relaxation, perturbation sample average approximation2010 Mathematics Subject Classification:

90C31, 90C05, 90C301. Introduction

Let denote the investing proportion (the superscript ⊤ denotes the transpose operator). Let denote the random vector of portfolio return rate, whose distribution is supported in . The portfolio selection model with high-order moments (in this paper, we can also call it polynomial portfolio optimization, or PPO for short) is defined as

| (1.1) |

where is the expectation operator, is a polynomial loss function and is the set of all feasible investment proportions. Suppose short selling is not allowed, then we select

where is the vector of all ones. When short selling is allowed, we choose . In this paper, we assume short selling is not allowed unless given extra conditions. Consider

| (1.2) |

where is a vector of risk preference parameters such that each and . The is function of portfolio return and

| (1.3) |

for . In the above, each is called the th central moment of . Since the central moment is identically zero, it is ignored in the expression (1.2). In particular, is called skewness and is called kurtosis. There are various portfolio loss functions. We would like to remark that our method does not depend on certain polynomial parametric expressions of .

The portfolio selection problem is important in financial literature. The theory of Markowitz [1] is a fundamental work in this area. It quantifies the portfolio returns and risks by the mean and variance values of some random vector. So the Markowitz’s model is also called the mean-variance (M-V) model. The M-V model is a popular portfolio selection model. However, it can be very sensitive with input noises. Its performance is heavily dependent on the sampling quality. In addition, real world portfolio returns usually exhibit thick tails and asymmetry [2, 3]. Investors are interested in taking accounts of higher order moments in the decision making process [4]. Recently, higher order portfolio selection models are proposed such as the mean-variance-skewness (M-V-S) model [5] and the mean-variance-skewness-kurtosis (M-V-S-K) model [6]. Interestingly, these models can be seen as special cases of PPO, in a more general sense.

Apparently, the PPO (1.1) is a stochastic polynomial optimization problem. Suppose the explicit parametric expression of is known, then (1.1), as a polynomial optimization problem, can be solved globally by Moment-SOS relaxations [7, 8]. However, it is difficult to compute accurately in practice. This is because computing function expectation involves multi-dimensional integration. A natural approach is to apply sample average approximation (SAA) methods. That is, one can approximate by the sample average function

where each is a random sample following the distribution of . But it usually requires a huge size of samples to get a good approximation. In addition, the optimizer set may still not be well approximated if we replace by in (1.1), even if the coefficient vectors of are close. Indeed, it can be computationally expensive to extract such an inaccurate optimizer, before updating with new samples. To address these concerns, we consider using the perturbation sample average approximation (PSAA) method proposed in [9]. The PSAA model adds a convex regularization term to the standard SAA model. Compared to the standard SAA model, the PSAA method gives a more robust approximation of (1.1). With a proper choice of regularization parameter, the PSAA model can be globally solved by Moment-SOS relaxation at the initial relaxation order.

There is a lot of research work on portfolio optimization. Discussions on M-V models are given in [10, 11, 12]. Studies on higher order portfolio selection models are given in [13, 14]. We also refer to [15, 16, 17] and references therein for other kinds of portfolio selection models. The portfolio selection problem is a special stochastic optimization problem. The stochastic approximation (SA) and SAA are two major approaches of solving stochastic optimization. We refer to [18, 19] for a comprehensive introduction to stochastic optimization.

Contribution.

This article studies a new portfolio selection model with high-order moments, which is given as in (1.1). For an order , the objective function is a polynomial expectation with

for some nonnegative risk preference parameters that sum up to one. In applications, the order and parameters are dependent on the historic data or sample amount and investors’ personal risk preferences. In most portfolio selection models in the literature, is often selected as . To show the efficiency of our method, we make a numerical experiment using real world stock data and compute with order (see as in Example 4.3). We give a robust approximation of (1.1) with perturbation sample average approximations. This approximation can be solved globally by Moment-SOS relaxations. We show theoretically and numerically that the optimizer set of PSAA model gives a good approximation of the optimizer set of original PPO. An efficient semidefinite algorithm is proposed based on our method. We would like to remark that our method can give a convincing approximation of the optimizer set without any convex assumptions on the objective function. As far as we know, there is less work discussing about global optimality of nonconvex portfolio selection model, prior to our work. To sum up, our main contributions are the followings.

-

•

First, we introduce a general portfolio selection model with high-order moments, called PPO, which is given as in (1.1). This model is flexible with arbitrary moment orders and different risk appetites.

-

•

Second, we give a robust approximation of PPO with perturbation sample average approximations. The PSAA model is more computationally efficient compared to the standard SAA model. For proper samples and parameters, the optimizer set of PSAA is close to that of the original PPO.

-

•

Third, we propose a Moment-SOS algorithm to solve the PSAA model globally. Numerical experiments are given to show the efficiency of our algorithm.

2. Preliminaries

Notation

The symbol denotes the set of nonnegative integers, and denotes the set of real numbers. For , denotes the smallest integer that is bigger than or equal to . The is the -dimensional Euclidean space, and stands for the Euclidean norm. For a point and a scalar , denote . We use to denote the vector of all ones. The denotes the vector of all zeros except the th entry being one. Let . Denote by the real polynomial ring in , and denote by the set of polynomials with degrees no more than . For a polynomial , we use to denote its degree. For a tuple of polynomials , we denote . A symmetric matrix is said to be positive semidefinite or psd, if for all . We use to denote a matrix is psd. For two sets , denote the distance

| (2.1) |

For a given power vector , we denote the monomial

where the degree . For a degree , denote . The symbol denotes the monomial vector of with the highest degree , i.e.,

2.1. Polynomial optimization

A polynomial is said to be sum-of-squares (SOS) if it can be written as for some . We denote by the set of all SOS polynomials and denote for every degree .

Let be a tuple of real polynomials in . It determines a semi-algebraic set

| (2.2) |

Denote the cone of nonnegative polynomials on by

For a degree , denote . The quadratic module of is

For , we denote the th order truncation

| (2.3) |

The is a convex cone, and each is a convex cone in . For every , the containment relations hold that

The quadratic module is said to be archimedean if there is such that determines a compact set. Suppose is archimedean, then must be compact. Conversely, it may not be true. However, given is compact (i.e., for some radius ), one can always set such that also determines and is archimedean. It is clear that every is nonnegative on . If a polynomial over , then under the archimedean condition. This conclusion is often referenced as Putinar’s Postivstellensatz [20]. Interestingly, under some optimality conditions, if on , we also have . This result is shown in [22].

Consider a polynomial optimization problem

| (2.4) |

where and each are polynomials. Denote and let be given as in (2.2). Suppose is the global optimal value of (2.4). Then if and only if for every , i.e., . This implies a hierarchy of SOS relaxations of (2.4). For a degree , the th order SOS relaxation of (2.4) is

Its dual problem is the th order moment relaxation. Under some archimedean conditions, it is shown in [7] that as . In particular, the finite convergence is studied in [21, 22]. The polynomial optimization has broad applications, see [23, 24, 25, 26]. We refer to [27, 28, 29] for recent results of polynomial optimization. For a detailed review for polynomial optimization, we refer to monographs [30, 31, 32] and references therein.

2.2. Localizing and moment matrices

Denote by the real vector space that consists of truncated multi-sequences (tms) of degree . Each tms defines a Riesz functional on by

For convenience, we denote that

| (2.5) |

We say a tms admits a measure supported in if it satisfies for all . A special case is that admits the Dirac measure at the point . Then for every power vector , we have

In particular, it holds that

The problem for checking whether or not a tms admits a measure is called the truncated moment problem. We refer to [33, 34, 35] for more details on this topic.

Let and . For and a tms , there exists a symmetric matrix such that

| (2.6) |

where denote the coefficient vectors of respectively. The is called the th order localizing matrix of . For example, when and , we have

For the special case that , we define the th order moment matrix by

| (2.7) |

For example, when , we have

The moment and localizing matrices are useful in polynomial optimization. For a tuple of polynomials and a degree , define

| (2.8) |

The is a convex cone and it is the dual cone of , i.e.,

where the superscript ∗ denotes the dual cone.

3. Global portfolio optimization

For a portfolio consisting of assets, let be the random rate of portfolio return and be the investing proportion. Assume short selling is not allowed, then the PPO model is

| (3.1) |

where is given as in (1.2). Note the constraint can be ignored if short selling is allowed. For both cases, the constraining equation can be used to eliminate one variable, i.e.,

Let and . We define

| (3.2) |

It is clear that the PPO (3.1) is equivalent to

| (3.3) |

Similarly, when the short selling is allowed, the PPO is equivalent to the unconstrained optimization

| (3.4) |

The polynomial is bounded from below on the feasible set of (3.1), which is compact. A feasible point is a global minimizer of (3.3) if and only if is the global minimizer of (3.1). Suppose (3.4) is solvable with an optimizer, then a similar conclusion holds for the PPO with short selling allowed. Both (3.3)-(3.4) have fewer decision variables than the original PPO problems. So solving (3.3)-(3.4) saves computational expenses. In the following discussions, we focus on these reformulations (3.3)-(3.4).

3.1. PSAA model

In applications, the distribution of is typically unknown. But it is natural to assume the truncated moment information of can be well approximated by samplings and historic data. So we consider applying SAA methods to approximate as in (3.2).

Suppose are given samples that each identically follows the distribution of . Define the sample average function

| (3.5) |

The construction of guarantees that . If we further assume that every is independently identically distributed, then under some regularity conditions, we have

with probability one. This result is implied from the Law of Large Numbers [36]. Then we can approximate (3.3) by the following optimization

| (3.6) |

The above approximation is usually given from classic SAA methods. It is a deterministic polynomial optimization, which can be solved globally by Moment-SOS relaxations, see in Subsection 2.1. It has good statistical properties. By [19, Theorem 5.2] and [19, Theorem 5.3], we have the following convergent result.

Theorem 3.1.

Proof.

Let denote the feasible set of (3.3) and (3.6). Clearly, is compact. The and each are polynomials in , which are continuous in . So both (3.3) and (3.6) are solvable with nonempty optimizer sets . Assume the distribution of is supported in a compact set . For every fixed , the function as a polynomial in , is continuous and integrable over . Therefore, the assumptions of [19, Theorem 5.2] and [19, Theorem 5.3] are all satisfied. The conclusions can be directly implied by these two theorems. ∎

The conclusions of Theorem 3.1 depend on the compactness of the feasible set. Suppose short selling is allowed, the PPO is equivalent to an unconstrained optimization, see as in (3.4). In this case, it can be hard to ensure the global optimizer set of the SAA model is close to that of the original PPO. Indeed, it is not necessary to solve each SAA model very accurately, even for cases that short selling is not allowed. Because the performance of SAA model depends on the sampling quality and quantity, and to extract the global minimizer of (3.6) may require a high relaxation order. One can imagine that the computational expenses becomes very high if we need to solve the SAA model (3.6) every time when a new sample is generated. On the other hand, investors are interested in the best investing proportions, equivalently, the optimizer sets of PPO reformulations (3.3)-(3.4). So our goal is to get convincing approximations of global optimizers of PPO problems in an efficient way.

To achieve the goal, we consider using the perturbation sample average approximation method introduced in [9]. It adds a convex regularization term to the standard SAA model, which has some good computational properties. Denote

| (3.7) |

The PSAA model of (3.3) is

| (3.8) |

In the above, is given as in (3.5), is a small parameter, and is the monomial vector of with the highest degree , i.e.,

Similarly, the PSAA model for (3.4) is

| (3.9) |

It is worth noting that when , (3.8)–(3.9) are reduced to be standard SAA models. Suppose these standard SAA models are solvable with nonempty global minimizer sets, say . Then for each , the PSAA models (3.8)–(3.9) must also be solvable with optimizer sets, say respectively. In addition, and are both close to zero when is sufficiently small. It implies that solving PSAA models can also return reliable approximations for the original solution set of PPO, if are good approximations.

We would like to remark that PSAA models (3.8)–(3.9) are more robust than SAA models from the aspect of computational efficiency. The optimization problems (3.8)–(3.9) can be solved globally by Moment-SOS relaxations. For the special case that , the relaxation order may be high to return a global minimizer. But for a proper choice of , (3.8)–(3.9) can be solved globally with a unique minimizer, at the initial relaxation order. More details on this are given in the following subsection.

3.2. Moment-SOS relaxations

In this section, we study Moment-SOS relaxations for PSAA models. Denote the tuple of constraining polynomials

| (3.10) |

Suppose a tms satisfies for some point , then

where is given as in (2.5). If is a feasible point for (3.8), making , then we have

This follows from the defining equation of as in (2.3). It implies that

where is the tms cone given as in (2.8). In other words, we have

for . The and each are the th order moment and localizing matrices of and . It leads to the moment relaxation of (3.8):

| (3.11) |

Its dual problem is the SOS relaxation

| (3.12) |

where denotes the coefficient vector of the polynomial . The conic constraint means that , as a polynomial in , belongs to the truncated quadratic module . Similarly, we can get the moment relaxation of (3.9):

| (3.13) |

The SOS relaxation of (3.9) is

| (3.14) |

The optimization problems (3.11)–(3.14) are linear conic optimization problem with cones given by linear, second-order and semidefinite constraints.

For an optimization problem, we say its relaxation is tight if the relaxation has the same optimal value of the original problem. Then we give a sufficient and necessary condition such that (3.11) is a tight relaxation of (3.8).

Theorem 3.2.

Proof.

Let be optimal values of (3.8) and (3.11) respectively. Suppose is the global minimizer of (3.8). Since is feasible for (3.11), we have

Suppose is the global minimizer of (3.11) such that . Then for . It implies that , and each . This is because and that equals the th-entry of . Then the is feasible for (3.8) and

So and (3.11) is a tight relaxation of (3.8). Furthermore, we have is the global minimizer of (3.8).

3.3. A semidefinite algorithm

We propose a semidefinite algorithm to solve the perturbation sample average approximation of the portfolio selection model. When the short selling is not allowed, the PSAA model is given as in (3.8). When the short selling is allowed, the PSAA model is given as in (3.9).

Algorithm 3.4.

For the given sample points and a small parameter , do the following:

In Algorithm 3.4, every optimization problem can be solved efficiently by MATLAB software GloptiPoly3 [37] and SeDuMi [38]. In Step 2, there always exists that is big enough such that the optimization pair (3.11)–(3.12) is solvable. For (3.11), it is strictly feasible since is nonempty. On the other hand, when is big, i.e., , we have (3.12) also be strictly feasible. Then there is a strong duality between (3.11)–(3.12) and that each relaxation problem is solvable with a minimizer. Similar arguments can be applied in Step 3. When is big enough, the dual pair (3.13)–(3.14) is always solvable. We refer to [9, Theorem 3.3] for more details. In Step 4, the output point is feasible for the original PPO. Suppose the short selling is not allowed. Since is feasible for (3.12), we have for each , which implies

where refers to the th entry of the given matrix. In other words, we have , so is feasible for (1.1). When the short selling is allowed, the is always feasible since .

In previous discussions, we have shown that when is big enough, the moment relaxations (3.11) and (3.13) is solvable with a global optimizer. However, the optimizer set of the PSAA model may be far away from the optimizer set of the original PPO, if has a big value. To get a good approximation of the original optimizer set, a preferable value of can be such that for every , the moment relaxations are not solvable. Such a bound can be determined as follows. Suppose the short selling is not allowed, we solve

| (3.15) |

When the short selling is allowed, we solve

| (3.16) |

These are linear conic optimization problems with linear, second-order cone and semidefinite constraints. In applications, it is computational expensive to determine for each . So we usually select some small heuristic values of , i.e., or .

4. Numerical Experiments

In this section, we give some numerical examples to show the efficiency of Algorithm 3.4. The computation is implemented in MATLAB R2014a, in a computer with CPU 6th Generation Intel®Core®i5-6500 CPU and RAM 8 GB. The MATLAB software GloptiPoly3 [37] and SeDuMi [38] are used to solve PSAA models. For neatness of the paper, we only display four decimal digits to show computational results. In each example, for samples , we denote sample average functions

| (4.1) |

where is the portfolio return and each is given as in (1.3).

Example 4.1.

Suppose there are three stocks , and in the market, which allows for short selling. Let denote the random return rates of respectively. Assume are independent distributed and each follows a normal distribution, i.e.,

In the above, stands for a normal distribution with the mean value and the standard deviation . Consider the M-V-S model induced from (1.1)–(1.2) with the order and the risk preference vector

We compute the analytic object function of the M-V-S model

Since the short selling is allowed, the feasible set is

thus is the investment proportion of stock . We can equivalently reformulate the PPO into

| (4.2) |

It can be solved globally with Moment-SOS relaxations. The optimal value and solution of (4.2) are

It implies that the best investment proportion is

We make a sampling of with the sample size and get

For the PSAA model (3.9), it has the objective function , with

| (4.3) |

Apply Algorithm 3.4 to this PPO. We report all numerical results in Table 1. The is the regularization parameter. The “Solvable?” refers to the status of (3.11). The “Time” stands for the total CPU time of running Algorithm 3.4 with the unit second. The denotes the candidate solution of (1.1) solved from Algorithm 3.4. The gives an approximation for the optimal value of (1.1).

| Solvable? | Time | |||

|---|---|---|---|---|

| No | not available | not available | ||

| Yes | ||||

| Yes |

Example 4.2.

Assume that the short selling is not allowed. Let be three stocks, of which the random vector of return each follows a normal distribution. We report their expected returns (mean) and risks (covariance) in Table 2.

| Stocks name | Expected return | Covariance | ||

|---|---|---|---|---|

Consider the M-V model induced from (1.1)–(1.2) with the order and the risk preference vector

With the given data in Table 2, we get the analytic object function of the M-V model

By eliminating with the equality constraint , the PPO can be equivalently reformulated into

| (4.4) |

The represents the investment proportion of the stocks and , thus represents the investment proportion of the stock . The polynomial optimziation problem (4.4) can be solved globally by Moment-SOS relaxations. The optimal value and solution are

It implies that the best investment proportion is

Then we generate random samples of with different sizes. The sample averages for expected value and covariance of these samplings are reported in Table 3.

| Sample size | Stock name | Sample mean | Sample covariance | ||

|---|---|---|---|---|---|

Apply Algorithm 3.4. We report all numerical results in Table 4. The denotes the candidate solution of (1.1) solved from Algorithm 3.4. The gives an approximation for the optimal value of (1.1).

| Sample size | Time | ||||

|---|---|---|---|---|---|

From Table 4, when short selling is not allowed, it is clear that the SAA and PSAA have close solutions when the parameter is small. It shows that once SAA gives a good approximation of the original PPO, then so as PSAA with a proper parameter.

In the following example, we study the real stock data from the Chinese stock market. A high-order portfolio model is constructed in form of (1.1). We apply Algorithm 3.4 in this PPO problem to see its performance.

Example 4.3.

We select 4 stocks from the Chinese stock market for portfolio investment, which are Linhai Stock (), Shanghai Automotive (), Hangzhou Iron and Steel (), and CYTS (). We collected weekly stock closing prices from March 3, 2006 to March 25, 2021 in the Choice software database. For and for each , we use to denote the price of in week . Then the stock return of in week can be computed as

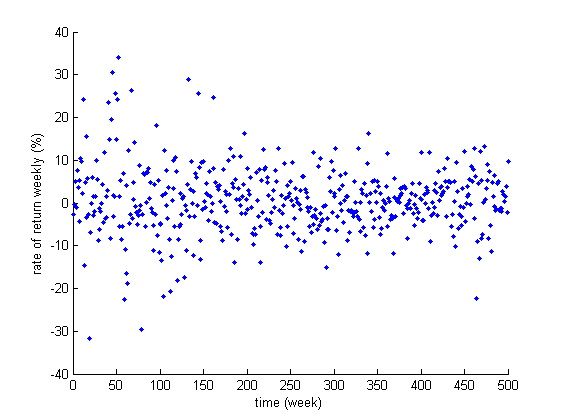

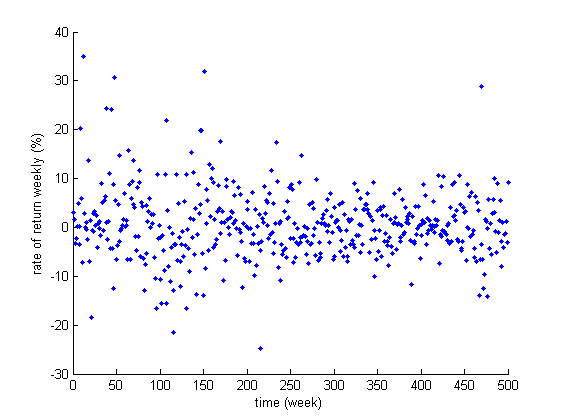

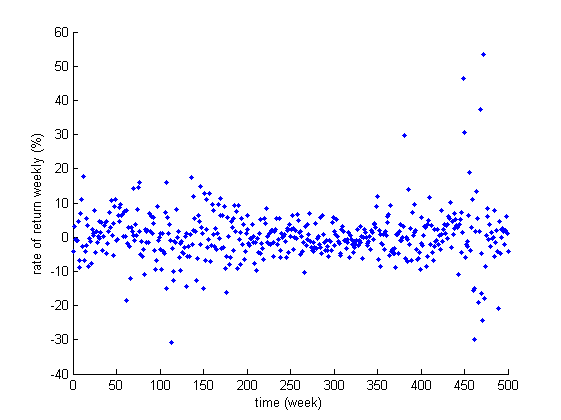

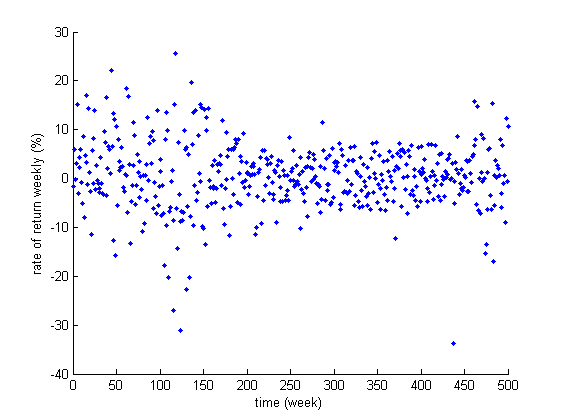

The weekly return rates of these four stocks from March 3, 2006 to March 25, 2021 are ploted in the following figures. The subfigures (a)-(d) shows the weekly return for - respectively.

It is easy to observe that the distribution of each stock returns is not normally distributed. They tend to be asymmetric, leptokurtic and heavy-tailed. For instance, the kurtosis in Figure 1 is of a sharp peaks and fat tail character. Therefore, the M-V model, which only uses the first and the second order moments, may not be efficient to give a promising investing plan. This is because many good properties of M-V model relies on the assumption that the stock returns follow a normal distribution. On the other hand, higher moments are important in measuring this probability distribution of the stock returns. For instance, the skewness can be used to measure the skew direction and degree of statistical data distribution. It also represents the asymmetric characteristics of statistical data. In financial literature, if the skewness is positive, it means that the positive returns are easy to generate. If the skewness is negative, it means that the potential risk is greater than the potential profit. Investors prefer the portfolio with a large skewness and dislike the yield with a large kurtosis.

Based on previous analysis, we consider a PPO model given as in (1.1)–(1.2) with . Assume the short selling is not allowed.

(i) We choose the risk preference vector as

With the sample size and the parameter , the PSAA model is

| (4.5) |

In the above, denote the investment proportion of the stocks Linhai Stock, Shanghai Automotive, Hangzhou Iron and Steel respectively. Then will be the investment proportion of the stock CYTS. Apply Algorithm 3.4. We get the candidate solution for the original PPO, and an approximation for its optimal value:

(ii) Next, we consider different parameter vector to compare numerical results of different investors’ preferences. In financial literature, the larger imply investors are the more risk-averse. Conversely, the smaller are, the more risk-appetite investors are. In particular, when , investors are extremely risk-averse and their only goal is to minimize the risk of their portfolio. When , investors are extremely fond of risk, and portfolio returns are the only factors that affect decision making. In our numerical experiments, we take three scenarios as follows.

The scenario 1, scenario 2, scenario 3 respectively reflect that the investor is risk neutral, risk aversion, and risk appetite. Apply Algorithm 3.4 in these three cases. We report all numerical results in Table 5. The denotes the candidate solution of (1.1) solved from Algorithm 3.4. The gives an approximation for the optimal value of (1.1).

| Scenario | ||

|---|---|---|

| 1 | ||

| 2 | ||

| 3 |

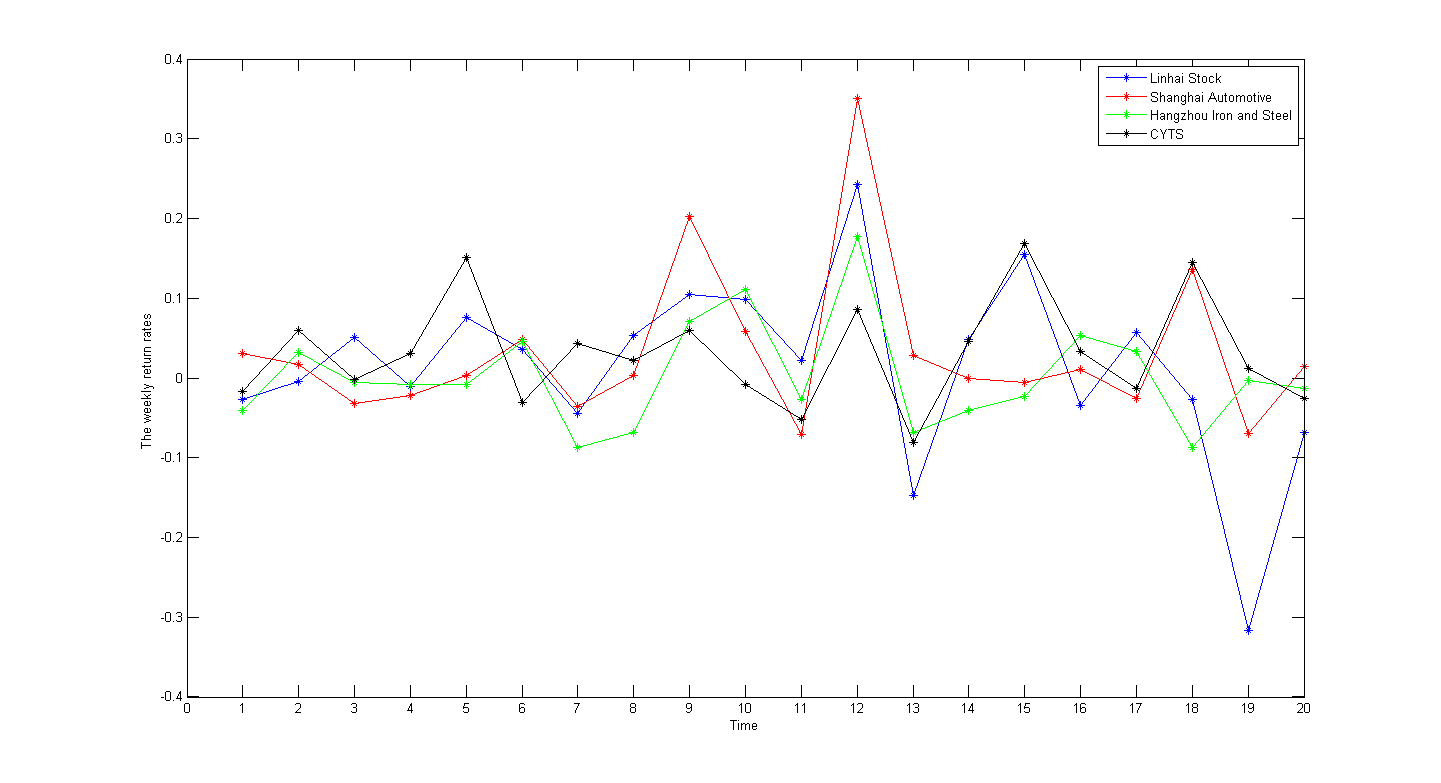

To better explain that the different risk attitude leads to different investing plan, we selected the weekly return rates of the four stocks in the first 20 weeks. The volatility of the return rate can be observed from Figure 2.

From Figure 2 and Table 5, we can see that risk appetite investors invest more in Shanghai Automotive stock than risk neutral investors and risk averse investors. This is because the return rate of Shanghai Automotive stock is more volatile than the others. Risk averse investors invest more in CYTS stock than risk neutral investors and risk appetite investors, because the return rate of CYTS stock is stable and the risk is low.

5. Conclusions

In this paper, we study a portfolio selection model with high-order moments. A polynomial portfolio optimization model is proposed, which can overcome the deficiencies of the M-V model and cater to investors with different risk appetites. To solve the PPO, we introduce perturbation sample average approximations. It gives a robust approximation of PPO and can be efficiently solved by Moment-SOS relaxations. We summarize a semidefinite algorithm for solving PSAA globally. The algorithm can be used to find reliable approximations of optimal value and optimizer set of the original PPO. Numerical experiments are given to show the efficiency of our methods.

References

- [1] Markowitz, H.: Portfolio selection. Journal of Finance 7(1), 77-91 (1952)

- [2] Jondeau, E., Rockinger, M.: Conditional volatility, skewness, and kurtosis: existence, persistence, and comovements. Journal of Economic dynamics and Control 27(10), 1699-1737 (2013)

- [3] Singleton, J.C., Wingender, J.: Skewness persistence in common stock returns. The Journal of Financial and Quantitative Analysis 21(3), 335-341 (1986)

- [4] Harvey, C.R., Siddique. A.: Conditional skewness in asset pricing tests. The Journal of Finance 55(3) 1263-1295 (2000)

- [5] Konno, H., Suzuki, K.: A mean-variance-skewness portfolio optimization model. Journal of the Operations Research Society of Japan 38(2), 173-187 (1995)

- [6] Davies, D.J., Kat, H.M., Lu. S.: Fund of hedge funds portfolio selection: A multiple-objective approach. Journal of Derivatives Hedge Funds 15(2), 91-115 (2009)

- [7] Lasserre, J.B.: Global optimization with polynomials and the problem of moments. SIAM J. Optim. 11(3), 796-817 (2001)

- [8] Laurent, M.: Sums of squares, moment matrices and optimization over polynomials. IMA Vol. Math. Appl. 149, pp. 157-270. Springer, New York (2009)

- [9] Nie, J., Yang, L., Zhong. S.: Stochastic polynomial optimization. Optim. Methods Softw. 35(2), 329-347 (2020)

- [10] Markowitz, H.: Mean-variance approximations to expected utility. European J. Oper. Res. 234(2), 346-355 (2014)

- [11] Rubinstein, M.: Markowitz’s “portfolio selection”: A fifty-year retrospective. The Journal of Finance 57(3), 1041-1045 (2002)

- [12] Steinbach, M.C.: Markowitz revisited: Mean-variance models in financial portfolio analysis. SIAM Review 43(1), 31-85 (2001)

- [13] Levy. H, Markowitz, H.M.: Approximating expected utility by a function of mean and variance. American Economic Review 69(3), 308-317 (1979)

- [14] Maringer, D., Parpas, P,: Global optimization of higher order moments in portfolio selection. J. Global Optim. 43(2-3), 219-230 (2009)

- [15] Black, F., Litterman, R.: Global portfolio optimization. Financial Analysts Journal 48(5), 28-43 (1992)

- [16] Goldfarb, D., Iyengar, G.: Robust portfolio selection problems. Math. Oper. Res. 28(1), 1-38 (2003)

- [17] Kolm, P.N., Tütüncü, R., Fabozzi, F.J., 60 years of portfolio optimization: Practical challenges and current trends. European J. Oper. Res. 234(2), 356-371 (2014)

- [18] Lan, G.: First-order and Stochastic Optimization Methods for Machine Learning. Springer (2020)

- [19] Shapiro, A., Dentcheva, D., Ruszczynski, A.: Lectures on Stochastic Programming: Modeling and Theory. SIAM (2021)

- [20] Putinar, M.: Positive polynomials on compact semi-algebraic sets. Indiana Univ. Math. J. 42(3), 969-984 (1993)

- [21] Nie, J.: Certifying convergence of Lasserre’s hierarchy via flat truncation. Math. Program. 142(1-2), 385-510 (2013)

- [22] Nie, J.: Optimality conditions and finite convergence of Lasserre’s hierarchy. Math. Program. 146(1-2), 97-121 (2014)

- [23] Fan, J., Nie, J., Zhou, A.: Tensor eigenvalue complementarity problems. Math. Program. 170(2), 507-539 (2018)

- [24] Guo, B., Nie, J., Yang, Z.: Learning diagonal Gaussian mixture models and incomplete tensor decompositions. Vietnam J. Math. 50(2), 421-446 (2022)

- [25] Nie, J., Tang, X.: Convex generalized Nash equilibrium problems and polynomial optimization. Math. Program. 198(2), 1485-1518 (2023)

- [26] Nie, J., Yang, L., Zhong, S., Zhou, G.: Distributionally robust optimization with moment ambiguity sets. J. Sci. Comput. 94(12), 1-27 (2023)

- [27] Huang, L., Nie, J., Yuan, Y.X.: Homogenization for polynomial optimization with unbounded sets. Math. Program. 200(1), 105-145 (2023)

- [28] Qu, Z., Tang, X.: A correlative sparse Lagrange multiplier expression relaxation for polynomial optimization (2022). arXiv:2208.03979

- [29] Nie, J., Yang, Z.: The multi-objective polynomial optimization (2021). arXiv:2108.04336

- [30] Nie, J.: Moment and Polynomial Optimization. SIAM (2023)

- [31] Henrion, D., Korda, M., Lasserre, J.B.: The Moment-SOS Hierarchy-Lectures in Probability, Statistics, Computational Geometry, Control and Nonlinear PDEs. World Scientific (2020)

- [32] Lasserre, J.B.: An Introduction to Polynomial and Semi-Algebraic Optimization. Cambridge University Press (2015)

- [33] Curto, R.E., Fialkow, L.A.: Truncated -moment problems in several variables. J. Operator Theory 54(1), 189-226 (2005)

- [34] Helton, J., Nie, J.: A semidefinite approach for truncated -moment problem. Found. Compu. Math. 12(6), 851-881 (2012)

- [35] Nie, J.: The -truncated -moment problem. Found. Compu. Math. 14(6), 1243-1276 (2014)

- [36] Ross, S.: A First Course in Probability. Pearson (2010)

- [37] Henrion, D., Lasserre, J.B., Lfberg, J.: GloptiPoly 3: moments, optimization and semidefinite programming. Optim. Methods Softw. 24(4-5), 761-779 (2009)

- [38] Sturm, J.F.: Using SeDuMi 1.02, a MATLAB toolbox for optimization over symmetric cones. Optim. Methods Softw. 11(1-4), 625-653 (1999)