The Burer-Monteiro SDP method can fail even above the Barvinok-Pataki bound

Abstract

The most widely used technique for solving large-scale semidefinite programs (SDPs) in practice is the non-convex Burer-Monteiro method, which explicitly maintains a low-rank SDP solution for memory efficiency. There has been much recent interest in obtaining a better theoretical understanding of the Burer-Monteiro method. When the maximum allowed rank of the SDP solution is above the Barvinok-Pataki bound (where a globally optimal solution of rank at most is guaranteed to exist), a recent line of work established convergence to a global optimum for generic or smoothed instances of the problem. However, it was open whether there even exists an instance in this regime where the Burer-Monteiro method fails. We prove that the Burer-Monteiro method can fail for the Max-Cut SDP on vertices when the rank is above the Barvinok-Pataki bound (). We provide a family of instances that have spurious local minima even when the rank . Combined with existing guarantees, this settles the question of the existence of spurious local minima for the Max-Cut formulation in all ranges of the rank and justifies the use of beyond worst-case paradigms like smoothed analysis to obtain guarantees for the Burer-Monteiro method.

1 Introduction

Semidefinite programs (SDPs) are a powerful algorithmic tool with wide-ranging applications in combinatorial optimization, control theory, machine learning and operations research. Notably, they yield optimal approximation algorithms for NP-hard problems like Max-Cut [GW95] and other constraint satisfaction problems [Rag08]. While interior-point algorithms and the ellipsoid method give polynomial time guarantees for solving semidefinite programs, memory becomes a bottleneck for relatively modest instance sizes. This has prompted research into scalable semidefinite programming algorithms—see [MHA20] for a recent survey.

One of the most popular methods for solving SDPs in practice is the one pioneered by Burer and Monteiro [BM03, BM05], which explicitly constrains the rank of the SDP solution for efficiency. Consider the celebrated Goemans-Williamson SDP relaxation for Max-Cut [GW95]:

| (MC-SDP) | ||||

Here denotes the set of all symmetric matrices and the cost matrix is typically the adjacency matrix of a weighted graph. (Note that (MC-SDP) can also be reformulated as a maximization SDP where the cost matrix is the Laplacian matrix , where is the diagonal degree matrix. The two formulations are equivalent since changing the diagonal of the cost matrix just corresponds to adding a constant to the objective value at each feasible point.) The above Goemans-Williamson SDP also gives a natural semidefinite programming relaxation for the Grothendieck problem [AN04], quadratic programming [Nes98, CW04], variants of community detection problems [Abb17], and other combinatorial optimization problems; in many of these settings the matrix may also have negative entries.

Instead of maintaining a solution in , the Burer-Monteiro method explicitly maintains a low-rank solution of the form where , and aims to solve the following optimization problem:

| (MC-BM) | ||||

where denotes the th row of , taken as a column vector, and denotes the Euclidean norm. We may also denote the objective of (MC-BM) as . We denote the feasible region as

(When is clear from the context or unimportant, we may just write .) Note that is a product manifold since it can be viewed as a Cartesian product of unit spheres in .

This formulation yields significant memory savings when by storing instead of and has the additional advantage of dropping the positive semidefiniteness constraint. On the other hand, (MC-BM) is a non-convex constrained optimization problem. Local optimization methods like Riemannian gradient descent and other heuristics for manifold optimization or constrained optimization are used to solve this non-convex problem with surprisingly good empirical results [BM03, BM05]. This motivates the following question:

When does the Burer-Monteiro method converge to a globally optimal solution?

This question has attracted much recent interest on the theoretical front. It is known that when the rank bound of the SDP solution is above the so-called Barvinok-Pataki bound (more formally, satisfies ), a globally optimal solution of rank at most is guaranteed to exist [Bar95, Pat98]. Moreover, below this bound, there exist instances for which (MC-BM) has a spurious local minimum [WW20]. When the rank bound is above the Barvinok-Pataki bound, Boumal, Voroninski, and Bandeira [BVB16, BVB18] showed that for generic instances,111By generic instances, we mean the guarantee holds for all cost matrices except a set of zero measure. any second-order critical point of (MC-BM) is globally optimal for (MC-BM), and thus is optimal for (MC-SDP) (their result also applies for a broad class of SDPs with equality constraints). Under such conditions, known algorithms converge to second-order critical points of (MC-BM), and polynomial-time convergence guarantees can be shown for smoothed instances [BBJN18, PJB18, CM19].

On the other hand, for general cost matrices , the best known bound only guarantees convergence to a global optimum of the Burer-Monteiro method when [BVB18, Cor. 5.11]. For general cost matrices of (MC-BM), there is a large range for the rank bound where we do not know whether the Burer-Monteiro method works. To the best of our knowledge, it was open whether there exists any instance (not specific to Max-Cut) where the Burer-Monteiro method fails above the Barvinok-Pataki bound. In fact, the authors of [BVB18] pose this question:

Our main theorem resolves this question by constructing an instance of (MC-BM) with a spurious local minimum (i.e., a local minimum which is not globally optimal) when is as large as (note that a spurious local minimum is also a spurious second order critical point). This result is contextualized in Figure 1.

Theorem 1.

For any and , there exist cost matrices for which the associated instance of (MC-BM) has a spurious local minimum.

Combining Theorem 1 with other existing results yields a clearer understanding of the optimization landscape and a characterization of the range of for which (MC-BM) can have spurious local minima. Furthermore, our result justifies the use of beyond worst-case paradigms like smoothed analysis to obtain global convergence guarantees for the Burer-Monteiro method. (See also Appendix A for a further discussion of prior work.)

Outline of paper.

We begin with Section 2 (Preliminaries) which provides necessary background for the construction of spurious local minima in Theorem 1. In Section 3, we list the main lemmas needed for Theorem 1 and show how Theorem 1 follows. Sections 4–6 contain proofs of these lemmas. In particular, Section 4 contains the proofs that our construction yields a spurious first and second-order critical point. Section 5 contains the proof that our construction yields a spurious local minimum. Section 6 contains constructions of a set of matrices needed in the proof of Theorem 1. Section 7 contains experiments, and we present potential follow-up directions in Section 8 (Conclusion).

2 Preliminaries

Section 2.1 gives an overview of the Riemannian geometry of (MC-BM). In Section 2.2, we use this geometry to give necessary conditions for local minimality and a characterization of global optimality. Section 2.3 provides an overview of Riemannian gradient descent, which is key to proving local minimality in Theorem 1 (see Section 5 for details). Section 2.4 contains definitions (including classes of matrices) used in the construction for Theorem 1.

2.1 Riemannian derivatives

is a smooth embedded submanifold of [BVB18, Prop. 1.2], and is furthermore an embedded Riemannian submanifold of [Bou22, Def. 3.55] if we equip the linearizations of at each point (known as the tangent spaces—defined below) with (a restriction of) the inner product on .

Proposition 1 (Tangent space [BVB18, Lem. 2.1]).

The tangent space to at , denoted , is the following subspace of :

Here, , denote the th rows of and respectively, taken as column vectors. (In other words, is the space of matrices row-wise orthogonal to .) We call an element of a tangent vector (at ).

The Riemannian gradient at , , is the orthogonal projection of the classical Euclidean gradient at onto , which yields the following expression (see Appendix B):

| (1) |

(Note that is a function of , although we write instead of, e.g., when is clear from context.) We take (1) to be the definition of from now on.

The Riemannian Hessian of Obj at , , is a linear, symmetric map from to given by the classical differential of (a smooth extension of) , projected to the tangent space [Bou22, Cor. 5.16]. This yields (see Appendix B):

for , where the linear map denotes the orthogonal projector onto , i.e., . In what follows, will only appear as part of a quadratic form, yielding the following cleaner expression:

for , where we used the fact that for any .

2.2 Necessary and sufficient conditions

Recall the definition of a local (and global) minimum:

Definition 1 (Local/global minimum).

Consider the program

where . is a local minimum if there exists such that if and , we have . is a global minimum if for all .

The following are standard necessary conditions for local optimality, and correspond to the first and second-order critical point criteria that need to be satisfied by any local minimum of (MC-BM) (see [BVB18, Prop 2.4]).

Proposition 3 (Second-order critical point [WW20, Prop. 4]).

A first-order critical point is additionally a second-order critical point if and only if

for all , and where is given in (1). (This is equivalent to .)

We say a critical point or local minimum is spurious if it is not globally optimal. Finally, we characterize which first-order critical points of (MC-BM) are globally optimal. Since second-order critical points and local minima are also first-order critical points, this also provides a characterization of optimality for them.

Proposition 4 (Characterization of optimality for first-order critical points).

2.3 Riemannian gradient descent

The analogue to gradient descent for optimizing over a smooth manifold is Riemannian gradient descent (see [Bou22, Ch. 4] for an introduction), which yields analogous analyses and guarantees. It includes as part of its specification a retraction [Bou22, Def. 3.47]. A rectraction on associates to each point a map which converts movement in the tangent space to movement on the manifold . We use the natural metric projection retraction [Bou22, Sec. 5.12], defined for as . With this definition, it is easy to see that is followed by a normalization of each row. This yields the following Riemannian gradient descent algorithm for (MC-BM):

Input: Initializer , step size .

For

2.4 Construction-specific definitions

Finally, we give a few miscellaneous technical definitions which will be used in our construction of a spurious local minimum for (MC-BM).

Definition 2 (Axial position).

We call the matrix

the axial position, where denotes the identity matrix in .

We use the term “axial position" because when we view as a Cartesian product of unit spheres in , corresponds to placing a single unit vector on both the negative and positive sides of each axis in .

The following sets of matrices will be important in our construction:

Definition 3 (Pseudo-PD, pseudo-PSD).

We say a matrix is pseudo-PD (“pseudo-positive definite”) if for all , where denotes the submatrix of formed by removing the th row and column. Similarly, we say that is pseudo-PSD (“pseudo-positive semidefinite”) if for all .

Definition 4 (Strictly pseudo-PD, strictly pseudo-PSD).

We say a matrix is is strictly pseudo-PD if it is pseudo-PD but not positive semidefinite. We say is strictly pseudo-PSD if it is pseudo-PSD but not positive semidefinite. (Note that in both cases we require , not .)

Clearly every strictly pseudo-PD matrix is also strictly pseudo-PSD, but the converse turns out to be false.

3 Main Claims and Outline

In this section we discuss the main claims and put them together to prove Theorem 1. We focus on the case where is even and and construct cost matrices for which is a spurious local minimum, since constructions for can be easily extracted from the former by padding with zeros. Before this, as a warm-up, we characterize those cost matrices for which is a spurious first and second-order critical point in the following two propositions. First-order and second-order criticality are necessary but not sufficient to establish that is a spurious local minima. While not strictly necessary for the proof of Theorem 1, Propositions 5 and 6 have far simpler proofs (see Section 4) and are interesting in their own right.

Proposition 5 (First-order critical point characterization for ).

For (MC-BM) when , the axial position is a first-order critical point if and only if the cost matrix takes the form

| (2) |

for some and . Furthermore, is additionally spurious if and only if .

Proposition 6 (Second-order critical point characterization for ).

For (MC-BM) when , the axial position is a second-order critical point if and only if the cost matrix takes the form

for some and pseudo-PSD . Furthermore, is additionally spurious if and only if is strictly pseudo-PSD.

It is not surprising that Propositions 5 and 6 allow you to arbitrarily change the diagonal of the cost matrix. Doing so simply corresponds to adding a constant to the objective value at each point and does not change the geometry of the problem.222One can easily check that the Riemannian derivatives at any point remain unchanged since in (1) will act as an offset.

Next, the following lemma provides a sufficient condition for to be a spurious local minimum. This is the most challenging of our results to prove, and we give the proof and discuss the challenges involved in Section 5.

Lemma 1 (Local minimum condition for ).

For (MC-BM) when , the axial position is a local minimum if the cost matrix takes the form

| (3) |

for some and pseudo-PD . Furthermore, is additionally spurious if is strictly pseudo-PD.

Actualizing Lemma 1 to construct a spurious local minimum requires the existence of strictly pseudo-PD matrices, which we posit in the following lemma:

Lemma 2 (Existence of strictly pseudo-PD matrices).

The set of strictly pseudo-PD matrices is nonempty for any .

We provide constructions of strictly pseudo-PD matrices in Section 6. Our main nonnegative construction takes the form , where is a random matrix. It is shown for all with high probability. One can show that when is sufficiently small, the principal submatrices of remain positive definite, while since is rank-deficient.

-

Proof of Theorem 1. Lemmas 1 and 2 imply that for even such that , there exists an instance of (MC-BM) with a spurious local minimum when . To construct a spurious local minimum for , we can simply use the construction for vertices and rank . The entries of the cost matrix that correspond to additional rows of elements of past can be set to 0, ensuring that these additional rows cannot affect the objective value. (See Appendix C for details.) ∎

One instantiation of our construction for is illustrated in Figure 2. In this visualization, we think of the nonnegative cost matrix as the adjacency matrix of a weighted graph, which is natural for (MC-BM). Each row of specifies the position of one of the vertices on the unit sphere in (for , the circle shown in gray). We illustrate “heavy” (higher weight) edges with solid lines, and “light” (lower weight) edges with dashed lines. Intuitively, each edge “pushes" its endpoints away from each other, with heavier edges pushing harder. We see by symmetry that this state is in equilibrium (each vertex is pushed equally clockwise and counter-clockwise), so the gradient is 0. Showing that this instance is indeed a local minimum is more involved, and requires arguing that if the vertices were perturbed slightly, the heavy edges would still approximately cancel out, and the main force on the vertices would be the light edges pushing the pairs and back to being diametrically opposite.333We provide an interactive visualization for the and cases at

https://vaidehi8913.github.io/burer-monteiro.

4 Warmup: proofs of first-order and second-order criticality

In this section we give the proofs of Propositions 5 and 6, which characterize cost matrices for which is first order critical and second order critical respectively. These propositions together motivate the pseudo-PSD property of cost matrices that are crucial in our construction. The reader is welcome to skip ahead to Section 5 for the proof of the main lemma about being a spurious local minimum.

See 5

-

Proof of Proposition 5. We first prove the first half of Proposition 5, which characterizes when is a first-order critical point. If takes the form (2) for some and , we can set where is our choice for the multiplier from Proposition 2. Observe then that , implying is indeed a first-order critical point. For the other direction, suppose that is a first-order critical point with associated multiplier (from Proposition 2), and consider the matrix , which can be expressed in the block form

for some and . Then implies and , and thus . Thus, indeed takes the form (2).

Now we prove the second half of Proposition 5: the characterization of when is a spurious first-order critical point. Supposing that the cost matrix takes the form (2) for some and (as we’ve shown is necessary for to be a first-order critical point), we show that is additionally spurious if and only if . Recall from above that the unique multiplier (from Proposition 2) associated with is precisely . Then it follows from Proposition 4 that is spurious if and only if

is not positive semidefinite. (Recall from Proposition 2 that at a first-order critical point.) We claim

(4) where denotes the Kronecker product. Indeed, this follows because the spectrum of , denoted , for two square, real matrices is given by

This, combined with the fact that , implies (4). ∎

As for the second proposition:

See 6

-

Proof of Proposition 6. We first prove the first half of Proposition 6, which characterizes when is a second-order critical point. Since any second-order critical point is also a first-order critical point, the first half of Proposition 5 implies it is necessary for the cost matrix to take the form (2) for some and for to be a second-order critical point. We will show that is additionally a second-order critical point if and only if the matrix from (2) is pseudo-PSD.

To this end, recall from the proof of Proposition 5 that the unique multiplier associated with when takes the form (2) is precisely . Then, writing

(5) clearly the condition for the second-order criticality of (Proposition 3) is equivalent to

(6) Define

to be the subspace of consisting of matrices with zeros on their diagonals. Note then that is precisely

(7) In other words, is the set of all matrices such that for all , and the other entries are completely arbitrary. Observe that (5) and (7) imply the second-order criticality condition (6) is equivalent to

(8) Next, note that (8) (and therefore (6)) is equivalent to

(9) since is closed under addition.

Thus, we have shown at this point that is a second-order critical point if and only if (9) holds. Now let for denote the -dimensional subspace of obtained by fixing the th entry to be 0 and letting all other entries vary arbitrarily. Observe that

Thus, we can reexpress the second-order criticality condition (9) as follows:

(10) (10) is equivalent to being pseudo-PSD.

As for the second half of Proposition 6, the characterization of when is a spurious second-order critical point, this follows immediately from the first half of Proposition 6 and the characterization of when is a spurious first-order critical point from Proposition 5 (since all second-order critical points are also first-order critical points). ∎

5 Proof of local minimality (Lemma 1)

In this section we give the proof of Lemma 1. Section 5.1 discusses the challenges involved, states the necessary sublemmas, and concludes with the proof of Lemma 1. Section 5.2 gives the proof of the most important sublemma (Lemma 3).

5.1 Challenges, key sublemmas, and the proof of Lemma 1

Challenges.

Unfortunately, arguing about the value of the objective function at some point near is challenging, and classical techniques for proving that is a local minimum fail. For example, [WW20], which constructs spurious local minima for (MC-BM) when , similarly first constructs spurious second-order critical points and then proves that they are additionally local minima. However, their proof follows because their spurious second-order critical points are non-degenerate [WW20, Def. 3], which corresponds to the rank of the Riemannian Hessian being sufficiently high. We show in Appendix D (Proposition 11) that for any instance of (MC-BM) when , all spurious second-order critical points are degenerate, meaning this approach will not work. Furthermore, there is no hope of using the positivity of a higher-order Riemannian derivative (e.g., the fourth derivative) to prove that is a local minimum, since it can be shown that all higher-order derivatives are degenerate. (See Appendix D for further discussion of these challenges.)

Overview and key sublemmas.

Thus, we provide a novel approach involving Riemannian gradient descent (Section 2.3). For the first sublemma below, recall that a neighborhood of a point is a set of the form for some . The proof is given in Section 5.2.

Lemma 3 (Convergence to a point with the same objective value).

Note that Lemma 3 does not imply convergence to itself; this is not actually true due to the degeneracy mentioned above. Instead, we show in the proof of Lemma 3 that is an antipodal configuration, i.e., it takes the form for some . Such antipodal configurations (of which is one) all have the same objective value and correspond in particular to “flat” directions from . For a given , it is not a priori clear which of these antipodal configurations it will converge to, so we argue convergence to some antipodal configuration.

In the proof of Lemma 3 in Section 5.2, we track convergence to an antipodal configuration via a potential , where . (Here, .) Clearly is 0 if and only if the input is antipodal. We show that decreases geometrically over the iterations of Riemannian gradient descent.

Next, we show via a smoothness argument that with sufficiently small step size, the objective is nonincreasing over the iterations of Riemannian gradient descent. The proof is given in Appendix E.

Lemma 4 (Obj is nonincreasing).

Lemmas 3 and 4 imply , and as a result the neighborhood in Lemma 3 certifies that is a local minimum. The details follow:

See 1

-

Proof of Lemma 1. We first show that if is pseudo-PD, then is a local minimum. We claim that the neighborhood from Lemma 3 certifies that is a local minimum. Indeed, let , and initialize Riemannian gradient descent at with step size , with defined as in Lemmas 3, 4. Per Lemma 3, we know that Riemannian gradient descent will converge to a point such that .

Since Obj is continuous, convergence in iterates translates to convergence in objective values, and thus the nonincreasing nature of Riemannian gradient descent from Lemma 4 implies . Then , and we are done.

Now we show that is additionally spurious if is strictly pseudo-PD. Indeed, this follows immediately from the last line of Proposition 5. (Recall that any local minimum is also a first-order critical point.) ∎

5.2 Proof of key sublemma: convergence to a point with the same objective value (Lemma 3)

In this section we prove Lemma 3, which is the main sublemma behind the proof of Lemma 1 in the last section. Taken together, the proof of Lemma 3 is by far the longest in this paper and will itself utilize several sublemmas given in this section (with some additional very minor claims proven in Appendix F). See the very end of this section for the proof of Lemma 3 itself.

Important setup for this section.

Throughout Section 5.2, we assume we are in the setting of Lemma 1 with pseudo-PD . Furthermore, we assume for simplicity that . This is without loss of generality because due to the feasibility constraint of (MC-BM), shifting the diagonal entries of the cost matrix just corresponds to adding the same constant to the objective value of each feasible point. In particular, it is easy to check that changing does not affect the geometry of the problem, i.e., the Riemannian derivatives at any point remain unchanged. As a result of these assumptions, the cost matrix in this section always takes the form

| (11) |

for some pseudo-PD . Finally, is always in this section. (We may sometimes write instead of for shorthand.)

To start, the following sublemma, which was described briefly in words in Section 5, provides the backbone of the argument. Recall once again that by a neighborhood of , we mean a set of the form for some , where as always denotes the Euclidean (or equivalently Frobenius) norm.

Lemma 5 (Decrease in the potential ).

Let the potential be defined as , where . Then there exists a neighborhood of and such that for any and , we have

| (12) |

Here, is the point reached by a single step of Riemannian gradient descent starting from with step size . (The notation is used as is reserved for something else in the proof.) is a constant which depends only on the instance of (MC-BM).

| Notation | Description |

|---|---|

| always for this section and may be used as a shorthand | |

| cost matrix taking the form (11) | |

| one pseudo-PD block of the cost matrix; see (11) | |

| potential; see Lemma 5 | |

| the axial position as in Definition 2; in matrix block form: over | |

| (an arbitrary point near ) | |

| perturbation matrix used to define ; see the line above | |

| (the point we get to with a gradient step from ) | |

| the retracted (row-normalized) (equivalently the result of taking a | |

| single step of Riemannian gradient descent from ) | |

| used to denote the th row of (taken as a column vector) for | |

| a given matrix | |

| and resp. for | |

| defined via their rows: | |

| and for all | |

| the th column of with its th entry removed (only used once!) | |

| the submatrix of formed by removing its th row and column | |

| minimum eigenvalue of the input | |

| the th standard basis vector | |

| Euclidean (or equivalently Frobenius) norm |

Proof.

We first provide a brief overview of the proof and introduce some notation. To begin, we will represent explicitly in the form , where should be thought of as a perturbation matrix. (Recall that is always in this section and may be used as a shorthand.) Using this representation, we derive explicit expressions for and then , where . Recalling the contents of Section 2.3, is followed by a normalization of each row. So takes a gradient step from but doesn’t normalize the rows, meaning (assuming ) . (Thus, we abuse notation here and extend the domain of to .) That said, it is easy to show , so bounding is sufficient. We are then able to bound by the right-hand side of (12) by taking the step size and to be sufficiently small and using the pseudo-PD property of .

We now delve into the technical details. We will unfortunately need to introduce a significant amount of notation as we go since we will be performing the above analysis in a row-wise manner. (Which is natural in some sense when we recall that is a product manifold formed by taking the Cartesian product of unit spheres in . And for product manifolds, geometric entities such as the tangent space and Riemannian derivatives can be expressed as products or concatenations of entities over the constituent manifolds.) As an aid, Figure 3 can be used as a reference for the notation used in this proof.

Letting denote respectively for , we first derive expressions for for all . Recall that with defined as in (1). Then

The second line uses the block form of , and the third line introduces new notation: we let be defined such that the th row of is for . The matrix is directly related to the potential ; indeed, .

Similarly, one can derive

Next, we define analogously to but using : the th row of is for . Thus, . (We abuse notation and extend the domain of to .) We will bound through in a row-wise manner. Using the expressions we have derived, we have for :

Then for ,

The hides terms that depend on the perturbation , but this will not matter as will be taken sufficiently small in the final step after a bound on is set. (The also hides terms that depend on the instance of (MC-BM), but these do not matter for our purposes.)

Then

| (13) | ||||

We now upper bound and lower bound starting with the former, which relies on the key observation that when , then is small, and when , then and are small. Formally,

| (14) | ||||

| (15) | ||||

| (16) |

(14) uses Cauchy-Schwarz (recall that are unit vectors by definition) and the fact that since by definition and . (And can be bounded similarly.) (15) uses Cauchy-Schwarz as well as the following key bound:

| (17) | ||||

where we have used Lemmas 11 and 12 from Appendix F. This bound is critical; a less tight bound would not work because may be much smaller than . The big notation in line (16) hides terms which depend on the instance of (MC-BM), but these don’t matter for our purposes.

We now turn our focus to lower bounding , which is the only place where we use the fact that is pseudo-PD. We have

| (18) | ||||

| (19) | ||||

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) |

(18) once again uses the key inequality (17) (and Cauchy-Schwarz) and also simply rewrote . (19) introduces the unfortunate notation , which denotes the th column of except the th entry of this column (aka ) has been removed. Recall that as always denotes the submatrix of formed by removing the th row and column. Then, (19) follows by observing that the inner two summations on the right side of (18) form a quadratic form which is precisely . In (20), we introduce the notation which denotes , where denotes the minimum eigenvalue of its argument. In other words, lower bounds the eigenvalues of for any , and the fact that follows from the fact that is pseudo-PD. (21) follows by expanding and noting that only the diagonal entries of are not covered. In (22) we simply rewrite , and (23) uses the key inequality (17). (24) simply uses .

Now going back to (13) and using the bounds on and , we have

where in the last line we took and then to be sufficiently small. Finally, recall that , and note also that the norm of each row of is at least 1.444This follows because takes the form of “a point on plus a tangent vector,” and because tangent vectors are row-wise orthogonal to their base, clearly adding one can only increase the norm of each row. Then Lemma 13 from Appendix F implies , and we are done. ∎

Next, we would like to extend the result of Lemma 5 to all consecutive pairs of iterates produced by Riemannian gradient descent and not just the first pair. This will be done shortly in Lemma 7, but in preparation we first show that as long as the iterates of Riemannian gradient descent stay in the neighborhood identified in Lemma 5, they form a Cauchy sequence where the distances between consecutive iterates decrease geometrically.

Lemma 6 (Iterates confined to neighborhood form Cauchy sequence).

Let denote the neighborhood, step-size bound, and constant identified in Lemma 5. Suppose Riemannian gradient descent with step size is initialized at some , and furthermore . Then for any , we have

Before starting the proof, note that we critically do not require . This will be important in the proof of Lemma 7.

Proof.

We have for :

Now, recall from Section 2.3 that is equal to followed by a normalization of each row. We claim

Indeed, this follows from applying Lemma 14 from Appendix F in a row-wise manner, where is chosen as the th row of , is chosen as the th row of , , and is set to the norm of the th row of . ( since is row-wise orthogonal to due to the former being a tangent vector.) Intuitively, we are just using the fact that retraction onto the sphere can only bring you closer to your starting point.

Next, note that

where is used to denote the classical Euclidean gradient. This follows because, as mentioned in Section 2.1, the Riemannian gradient is equal to the Euclidean gradient composed with an orthogonal projection, and an orthogonal projection can only decrease the norm. Now write where . Using the form of given in (11), it is easy to see that

where we used the fact that the Frobenius norm is submultiplicative. Then, note that by definition, . Connecting the dots, we have shown up to this point that

| (25) |

Using Lemma 5 and the fact that the iterates up to step are in , we have . (Note that when , we are critically relying on the fact that Lemma 5 does not require .) Furthermore, it is easy to see that always bounds the distance away from ; indeed, let with and note that

(25) and the contents of the previous paragraph imply the desired result. ∎

Now we finally extend Lemma 5 to all consecutive pairs of iterates produced by Riemannian gradient descent. This can of course be achieved by confining all iterates to the neighborhood identified in Lemma 5. The following lemma does this by initializing in an even smaller neighborhood of .

Lemma 7 (Riemannian gradient descent stays close to ).

Let denote the neighborhood, step-size bound, and constant identified in Lemma 5. Then there exists a neighborhood of such that if Riemannian gradient descent with step size is initialized at any , all future iterates lie in .

Proof.

We proceed by induction on the iterate counter , and will choose in the inductive step so that the proof goes through. since . Now suppose , and we will set independently of so that . We have

where we used Lemma 6 (which critically doesn’t require ).

Clearly is bounded and doesn’t depend on , so can be chosen sufficiently small so that . ∎

Finally, we give the proof of Lemma 3:

-

Proof of Lemma 3. We choose to be the neighborhood identified in Lemma 7 and pick with defined as in Lemma 5. Then due to Lemma 7, all iterates of Riemannian gradient descent with any step size initialized at any lie in , the neighborhood identified in Lemma 5. As a result, Lemma 6 implies that the sequence of iterates forms a Cauchy sequence, and since is complete, the iterates converge to some . Clearly as all iterates of Riemannian gradient descent lie on .

Also, Lemma 5 and the fact that all iterates lie in implies that the sequence converges to 0. Since is continuous, we have . It is easy to see that for , we have if and only if is antipodal, where as in Section 5, we say a point is antipodal if it takes the form for some . Thus, is antipodal. Note that is also antipodal, and it is easy to check that all antipodal points have the same objective value. (In particular, if the cost matrix takes the form (11) as we assume without loss of generality in this section, that objective value is 0.) ∎

6 Constructions of strictly pseudo-PD matrices (Lemma 2)

In this section we provide two proofs of Lemma 2, which posits the existence of strictly pseudo-PD matrices for . The first is a probabilistic construction and the second is deterministic. The former has the advantage of having nonnegative entries, which, combined with Lemma 1, results in “natural” cost matrices that can arise as the adjacency matrix of a weighted graph. For the latter deterministic construction, we also characterize the optimal solutions of the associated instances of (MC-SDP), revealing they have a qualitatively different structure than .

6.1 Probabilistic construction with nonnegative entries

Our random construction uses a random matrix with nonnegative entries such that for each , the submatrix formed by removing the th row of has non-negligible least-singular-value (and hence full rank). Each entry of is generated i.i.d. from a where for a sufficiently large constant . The final matrix is just , where is set appropriately. By construction is a matrix of rank ; hence has exactly one negative eigenvalue. In what follows denotes the th eigenvalue of (note that is symmetric in our case; hence all eigenvalues are real).

Proposition 7 (Randomized construction for Lemma 2).

There exists absolute constants such that the following holds for a given with . Suppose is a random matrix where each entry is generated i.i.d. from for and let with . Then, with probability at least , is nonnegative and strictly pseudo-PD. In particular,

-

(i)

for each , the submatrix formed by removing the th row and the th column of satisfies .

-

(ii)

every entry of is nonnegative.

-

(iii)

it is not positive semidefinite i.e., .

We remark that the constant in the exponent of the failure probability is arbitrarily chosen. We can make this an arbitrarily large constant, and adjust constants appropriately.

The proof of the above lemma using the following claim about the least singular value of square matrices. We remark that much stronger bounds on the least singular values are known in random matrix theory. We state and include a proof (which follows somewhat standard arguments) of the following claim which is more tailored for our needs.

Lemma 8.

Fix any with . Let be a random matrix, each entry of which is sampled for some . Then there exists absolute constants such that with probability at least , we have:

-

(i)

, where denotes the least singular value of .

-

(ii)

every entry of is in the interval .

Proof.

We will show separately that both the required properties hold with high probability, and do a union bound over the failure of these two events. Part (ii) of the claim just follows by applying standard Gaussian tail bounds for a fixed entry of the matrix, and then using a union bound over all the entries.

We now focus on part (i) of the claim. This follows a standard argument using anti-concentration bounds (or small ball probability). Let represent the columns of . The least singular value of can be lower-bounded using the leave-one-out distance which is defined as

| (26) |

where and is the perpendicular distance between and the subspace . The least singular value is related to by

| (27) |

We now lower-bound the leave-one-out distance . Fix a column . Let be any unit vector in the subspace orthogonal to ; note that such a direction exists since . Moreover, since the column where is the all-ones vector, we have where . From the anti-concentration of Gaussian , we have for an absolute constant ,

By picking , we have with probability at least ,

By applying a union bound over all the columns , we have with probability at least . By applying (27), we see that part (i) of the lemma also holds.

∎

Proof of Proposition 7.

Fix . The matrix can be written in terms of the submatrix as . Each submatrix is a random matrix in with i.i.d. entries drawn from with . By applying Lemma 8 with and choosing , we get that with probability at least that . Hence,

Applying a union bound over all proves the part (i) of the lemma.

Part (ii) follows since (and hence ) has nonnegative entries and only has diagonal entries. So all the off-diagonal entries of are nonnegative. The non-negativity of the diagonal entries follows from the positive semi-definiteness of the .

Finally part (iii) follows since is of rank ; hence , which gives the required bound. ∎

6.2 Deterministic construction

We provide another construction of strictly pseudo-PD matrices for any . Unlike the construction given in Appendix 6.1, this construction is fully deterministic. However, it includes both positive and negative entries, making it an arguably less natural cost matrix for a weighted graph.

Definition 5 (Almost-average matrix).

We define the almost-average matrix as follows:

Now we show that is strictly pseudo-PD:

Proof.

First we show that is not positive semidefinite. Consider a test vector of all 1’s:

So is an eigenvector with a negative eigenvalue.

Now we show for any . (Recall that denotes the submatrix of formed by deleting the th row and column.) To see this, note that is strictly diagonally dominant for any (for every row, the sum of the magnitudes of the non-diagonal entries is less than the magnitude of the diagonal entry). Any symmetric, strictly diagonally dominant matrix with nonnegative diagonal entries is positive definite. So is indeed positive definite. ∎

We additionally note that when the cost matrix takes the form (3) with defined as in Definition 5 (setting ), one can show that (MC-SDP) has a unique optimal rank-one solution. This implies in particular that if we view this instance of (MC-SDP) as a convex relaxation of a corresponding Max-Cut instance (albeit with perhaps unusual negative edge weights modeling “attractions”), the relaxation is tight. The following proposition will be used in Section 7 (Experiments).

Proposition 8 (Optimal solution for cost matrix arising from almost-average matrix).

Clearly one could extend Proposition 8 to the case where (28) is arbitrarily shifted by a diagonal matrix as in, e.g., Lemma 1, but we state it this way for simplicity and because we will use precisely matrices of the form (28) in Section 7 (Experiments). Proposition 8 is interesting because it provides an example of an instance of (MC-SDP) where and the unique globally optimal solution are qualitatively very different (e.g., one is rank and the other rank 1).

Before giving the proof of Proposition 8, we make the useful observation that any strictly pseudo-PSD (and therefore also strictly pseudo-PD) matrix has at most one negative eigenvalue.555Whenever we use the phrases “at most one negative eigenvalue,” “exactly one negative eigenvalue,” etc., we are counting for multiplicity. So, for example, if a matrix has the negative eigenvalue -2 with multiplicity 4, this is counted as four separate negative eigenvalues (and, e.g., such a matrix could not be strictly pseudo-PSD due to Lemma 9).

Lemma 9.

Let be a strictly pseudo-PSD matrix for any . Then has exactly one negative eigenvalue.

Proof.

Any strictly pseudo-PSD matrix has at least one negative eigenvalue by definition. We show that if has more than one negative eigenvalue, one can construct an instance of (MC-BM) which contradicts a theorem due to [BVB18]. (It is the same theorem which ultimately yields the result that when , (MC-BM) has no spurious second-order critical points.) Toward this goal, consider the instance of (MC-BM) with cost matrix

where we have defined for notational brevity. Due to Proposition 6, the axial position is a second-order critical point for this instance. Furthermore, it is easy to see that the multiplier associated with due to (1) is 0. Then Theorem 3.4 from [BVB18] gives that has at most

negative eigenvalue. Here, denotes the face of the convex feasible region of (MC-SDP) (also known as the elliptope) associated with . (In other words, is in the relative interior of ; see Definition 2.5 and Proposition 2.7 in [BVB18].) Above, we used the fact that due to [BVB18, Prop. 2.7].

Next, note that

where denotes the Kronecker product. Since the eigenvalues of are , this decomposition implies that if had more than one negative eigenvalue, would have more than one negative eigenvalue, a contradiction. ∎

Now we prove the main claim:

-

Proof of Proposition 8. will be used as shorthand for throughout this proof. Due to, e.g., [WW20, Prop. 1] or [BVB18, Prop. 2.8], is optimal if there exists some such that, defining , we have and .666This comes from the fact that if these conditions are satisfied, the primal-dual pair satisfies the KKT conditions of (MC-SDP), implying optimality since (MC-SDP) is a convex program. We claim these conditions hold when each entry of is set to . Indeed, can be observed directly. As for , note that

Since the spectrum of is , the spectrum of , denoted , is precisely

(29) Clearly , so all that is left is to check that all elements of are nonnegative. Due to Lemma 9, has at most one negative eigenvalue. (Note that any strictly pseudo-PD matrix is strictly pseudo-PSD.) Furthermore, we found in the proof that is strictly pseudo-PD (directly below Definition 5) that the all 1’s vector is an eigenvector of with eigenvalue . Thus, this is the single negative eigenvalue of . Finally, note that

so we conclude that . Thus, we have established that is optimal.

As for the uniqueness of , it is a classical result that is an extreme point of the feasible region of (MC-SDP) (aka the elliptope)—see for example Definition 2.6 and Proposition 2.7 in [BVB18] or Appendix F.1 in [WW20]. [WW20, Prop. 2] then gives that if strict complementary slackness holds, meaning , then is the unique optimal solution. Indeed, this follows due to (29), the fact that only has a single negative eigenvalue, and the fact that for . ∎

7 Experiments

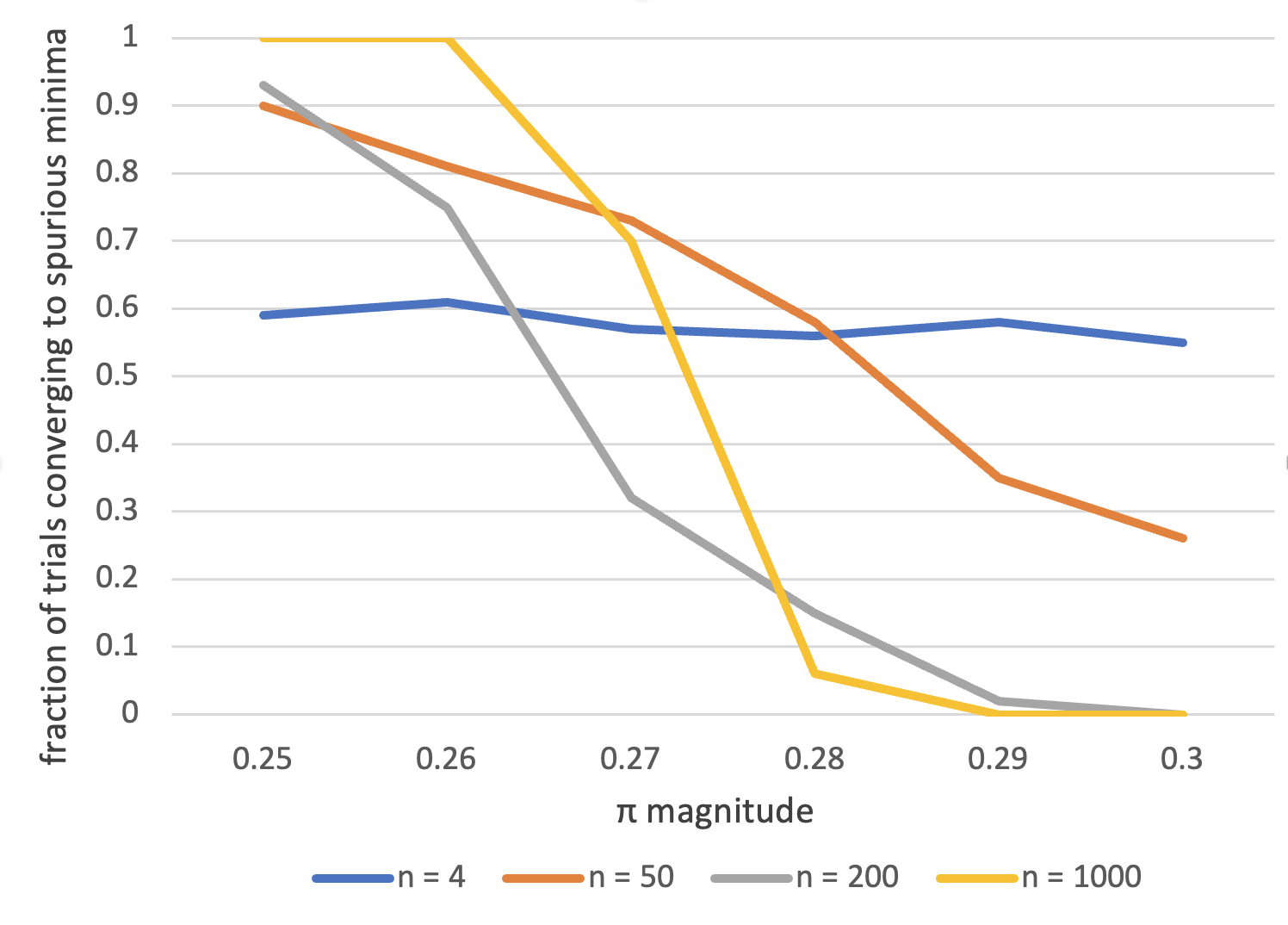

In this section, we empirically evaluate our construction of a spurious local minimum for (MC-BM) in the setting where (the largest possible value of before we are guaranteed to have no spurious minima). Our experiments suggest that the spurious local minima we construct have surprisingly large basins of convergence. (In comparison, our theoretical results only guarantee the existence of some positive measure basin of convergence.)

Our code and data can be found at https://github.com/vaidehi8913/burer-monteiro. This repository also contains a link to a visualizer for the and settings.

Instance generation.

For our experiments, we use the deterministic construction of pseudo-PD matrices given in Section 6.2. In other words, the cost matrix always takes the form

where is defined as in Definition 5 (setting ). We run trials for , each time setting . Recall that due to Lemma 1, the axial position is a spurious local minimum for such cost matrices. Furthermore, due to Proposition 8, we know precisely what the optimal value is for such instances, allowing us to distinguish whether the optimization algorithm converged to a spurious point or a global optimum.

Optimization setup.

We use the standard trust-region solver with default settings from the MATLAB manifold optimization package Manopt [BMAS14]. It is a second-order method which uses the gradient of the objective function (which we provide) and an approximation of the Hessian of the objective function found using finite differences (this is done automatically by their implementation).

Initialization.

In each trial, we sample the initialization point from a neighborhood of the axial position . We make use of the fact that is a product manifold and measure the distance to initialization in a row-wise manner, making the following definition:

Definition 6 (-close).

We say are -close if for all , where denotes the th row of .

For each trial, we choose a perturbation magnitude , which specifies how far from our initialization point will be. We then generate a perturbation matrix . Each entry of is drawn (a Gaussian distribution with variance ). This ensures that has approximately unit-norm rows. Then our initial point is given by

where normalizes each row of the input. This ensures that is effectively sampled a constant distance away from on in a uniformly chosen direction.

Data collection.

We report the fraction of trials in which the algorithm converged to a spurious point. We note that all trials we ran resulted in convergence to a point with objective value 0 (the objective value of our constructed spurious local minimum ) or to a point with the optimal (negative) objective value due to Proposition 8.

Results.

We provide a summary of our experimental results in Figure 4 and the full data in Figure 5. For , we ran 1000 trials for each reported value of . For we ran 100 trials for each , and for we ran 50 trials for each reported value of .

We note an interesting phase transition that seems to occur at . For perturbations greater than this threshold, the algorithm seems to almost always converge to a global optimum. Below this threshold, the algorithm seems to almost always converge to a spurious point. This threshold appears to get sharper as gets larger. This suggests there is some such that points -close to are very likely to converge to a spurious point, and vice versa. (It is also interesting that this family of cost matrices seems to have this phase transition at the same value for every .) All in all, our experiments suggest a much larger basin of convergence for spurious minima than our theoretical results guarantee.

| , | , | , | ||

|---|---|---|---|---|

| 0.55 | 0.26 | 0 | 0 | |

| 0.58 | 0.35 | 0.02 | 0 | |

| 0.56 | 0.58 | 0.15 | 0.06 | |

| 0.57 | 0.73 | 0.32 | 0.70 | |

| 0.61 | 0.81 | 0.75 | 1 | |

| 0.59 | 0.90 | 0.93 | 1 |

8 Conclusion

We show that the Burer-Monteiro method can fail for instances of the Max-Cut SDP, for rank up to . To the best of our knowledge, prior to our work it was unknown whether the Burer-Monteiro method could fail for any instance of any SDP with rank above the Barvinok-Pataki bound. We settle this question and thus justify the use of smoothed analysis to obtain guarantees for the Burer-Monteiro method.

There are many interesting potential follow-up directions to this work. We provide one construction of (MC-BM) instances with spurious local minima. Our construction has, and relies on, many interesting properties and symmetries. It is possible that some of these properties are necessary, and further analyzing this construction could give insight that allows us to fully characterize spurious minima for (MC-BM) instances. Analyzing this construction could also help us understand this interesting threshold phenomenon for (MC-BM) when —one dimension higher and there are not only no spurious local minima, there are no spurious second-order critical points at all. Another potential direction is seeing if similar techniques can be used to construct instances with spurious local minima for SDPs with other structures (not just Max-Cut).

Lastly, we note that a limitation of our work is that it only points to the existence of local minima, and does not give a full characterization of when we can expect local minima to exist. We also note that since this is a theoretical result about optimization landscapes, we do not foresee any adverse societal impacts of our work.

References

- [Abb17] Emmanuel Abbe. Community detection and stochastic block models: recent developments. The Journal of Machine Learning Research, 18(1):6446–6531, 2017.

- [AN04] Noga Alon and Assaf Naor. Approximating the cut-norm via grothendieck’s inequality. In Proceedings of the thirty-sixth annual ACM symposium on Theory of computing, pages 72–80. ACM, 2004.

- [Bar95] Alexander I. Barvinok. Problems of distance geometry and convex properties of quadratic maps. Discrete & Computational Geometry, 13:189–202, 1995.

- [BBJN18] Srinadh Bhojanapalli, Nicolas Boumal, Prateek Jain, and Praneeth Netrapalli. Smoothed analysis for low-rank solutions to semidefinite programs in quadratic penalty form. In COLT, 2018.

- [BM03] Samuel Burer and Renato D. C. Monteiro. A nonlinear programming algorithm for solving semidefinite programs via low-rank factorization. volume 95, pages 329–357. 2003. Computational semidefinite and second order cone programming: the state of the art.

- [BM05] Samuel Burer and Renato D. C. Monteiro. Local minima and convergence in low-rank semidefinite programming. Math. Program., 103(3, Ser. A):427–444, 2005.

- [BMAS14] N. Boumal, B. Mishra, P.-A. Absil, and R. Sepulchre. Manopt, a Matlab toolbox for optimization on manifolds. Journal of Machine Learning Research, 15(42):1455–1459, 2014.

- [Bou22] Nicolas Boumal. An introduction to optimization on smooth manifolds. To appear with Cambridge University Press, June 2022.

- [BVB16] Nicolas Boumal, Vlad Voroninski, and Afonso Bandeira. The non-convex burer-monteiro approach works on smooth semidefinite programs. In D. Lee, M. Sugiyama, U. Luxburg, I. Guyon, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 29. Curran Associates, Inc., 2016.

- [BVB18] Nicolas Boumal, Vladislav Voroninski, and Afonso Bandeira. Deterministic guarantees for burer-monteiro factorizations of smooth semidefinite programs. Communications on Pure and Applied Mathematics, 73, 04 2018.

- [CM19] Diego Cifuentes and Ankur Moitra. Polynomial time guarantees for the burer-monteiro method. arXiv: Optimization and Control, 2019.

- [CW04] M. Charikar and A. Wirth. Maximizing quadratic programs: extending grothendieck’s inequality. In 45th Annual IEEE Symposium on Foundations of Computer Science, pages 54–60, 2004.

- [GW95] Michel X. Goemans and David P. Williamson. Improved approximation algorithms for maximum cut and satisfiability problems using semidefinite programming. J. ACM, 42(6):1115–1145, nov 1995.

- [MHA20] Anirudha Majumdar, Georgina Hall, and Amir Ali Ahmadi. Recent scalability improvements for semidefinite programming with applications in machine learning, control, and robotics. Annual Review of Control, Robotics, and Autonomous Systems, 3(1):331–360, 2020.

- [MMMO17] Song Mei, Theodor Misiakiewicz, Andrea Montanari, and Roberto Imbuzeiro Oliveira. Solving sdps for synchronization and maxcut problems via the grothendieck inequality. In COLT, 2017.

- [Nes98] Yu Nesterov. Semidefinite relaxation and nonconvex quadratic optimization. Optimization Methods and Software, 9(1-3):141–160, 1998.

- [Pat98] Gábor Pataki. On the rank of extreme matrices in semidefinite programs and the multiplicity of optimal eigenvalues. Mathematics of Operations Research, 23(2):339–358, 1998.

- [PJB18] Thomas Pumir, Samy Jelassi, and Nicolas Boumal. Smoothed analysis of the low-rank approach for smooth semidefinite programs. In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018.

- [Rag08] Prasad Raghavendra. Optimal algorithms and inapproximability results for every csp? In Proceedings of the Fortieth Annual ACM Symposium on Theory of Computing, STOC ’08, page 245–254, New York, NY, USA, 2008. Association for Computing Machinery.

- [WW20] Irène Waldspurger and Alden Waters. Rank optimality for the Burer-Monteiro factorization. SIAM J. Optim., 30(3):2577–2602, 2020.

Appendix A Further discussion of prior work

The two most relevant papers to this work are [BVB18] and [WW20]. [BVB18] excludes the presence of spurious second-order critical points for (MC-BM) outside of a measure-zero set of cost matrices when . (Furthermore, their result extends to a broad class of smooth SDPs.) Additionally, [BVB18] shows that when , (MC-BM) has no spurious second-order critical points. [WW20] tightens the main lower bound of [BVB18] to and also shows that when , there exists a set of cost matrices with non-zero measure whose corresponding instances of (MC-BM) have spurious local minima.

It was open to the best of our knowledge whether there exists any instance of (MC-BM) with spurious second-order critical points when . (In fact, this question was open for the broad class of smooth SDPs analyzed in [BVB18]—see Section 6 in that paper.) We note that it is not clear how to extend the techniques of [WW20] to the setting of our paper since their constructions critically rely on a technical assumption (the existence of “minimally secant” matrices) which provably never holds when (as they note in Appendix B). As a result, our paper takes a different approach.

There has also been a line of work [BBJN18, PJB18, CM19] seeking to provide polynomial-time convergence guarantees to approximate global optima in a smoothed analysis setting. [BBJN18] in particular performs smoothed analysis on an unconstrained quadratically-penalized version of (MC-BM) (and its generalizations) and also provides a lower bound. However, their lower-bound construction does not apply to (MC-BM) itself (or its generalizations). (In particular, their lower-bound construction sets the cost matrix to be 0, which does not work in our setting.)

Finally, [MMMO17, Thm. 1] implies that when the cost matrix comes from a weighted graph with nonnegative weights on the edges (as is typical in Max-Cut relaxations), any spurious local minimum still achieves the globally optimal value up to an multiplicative error. We note that as mentioned in Section 1, there are many applications of (MC-SDP) where may have negative entries and where the solution value is not as important as the optimal SDP solution itself (which is used to recover some ground-truth solution). As we showed in Proposition 8, there exist instances of (MC-SDP) where the optimal solution and the spurious point are qualitatively very different.

Appendix B Toolbox

B.1 Proof of Proposition 4

Proposition 4 follows directly from Corollary 2.9 and Proposition 2.10 from [BVB18], which give analogous claims for a more general class of programs. In regards to Corollary 2.9 (the “if” direction), note that (MC-BM) trivially satisfies Assumption 1.1a (which is equivalent to the linear independence constraint qualification, aka LICQ, holding over the entire feasible region). Proposition 2.10 (the “only if” direction) requires strong duality, and strong duality holds for the convex program (MC-SDP) since it satisfies Slater’s condition.

B.2 Riemannian gradient and Riemannian Hessian for (MC-BM)

Proposition 9 (Riemannian gradient for (MC-BM)).

The Riemannian gradient of Obj at is given by

| (30) |

Here, denotes the th row of , taken as a column vector.

Proof.

For a smooth objective function over a Riemannian submanifold of a vector space [Bou22, Def. 3.55], the Riemannian gradient is given by the orthogonal projection of the Euclidean gradient to the tangent space [Bou22, Prop. 3.61]. Since is a Riemannian submanifold of [BVB18, Sec. 2.1], applying this yields

| (31) |

where the linear map denotes the orthogonal projector onto , i.e., . Since consists of those matrices in which are row-wise orthogonal to (Proposition 1), it is clear that the orthogonal projection of onto is found by going row by row over and each time deleting the component of row of which lies in the span of row of . In other words,

| (32) |

The Riemannian Hessian of Obj at , , is a linear, symmetric map from to . For a Riemannian submanifold of a vector space such as , this is given by the classical differential of (a smooth extension of) , projected to the tangent space [Bou22, Cor. 5.16].

We note that the Riemannian Hessian is the natural Riemannian analog of the Euclidean Hessian, and while the Euclidean Hessian of a function at can be thought of as a symmetric matrix containing the second-order partial derivatives of at , it is often best understood as a linear map defined via , where is the aforementioned “matrix form” of . With this viewpoint, is the directional derivative of the Euclidean gradient in the direction . Similarly, while the Riemannian Hessian of Obj at , , could be identified with a symmetric matrix,777Note that for a smooth manifold , is defined as , where denotes the tangent space (a vector space) at . ( is independent of .) it is best understood as a linear map , where denotes the “directional derivative” of the Riemannian gradient in the direction . (The correct definition of “directional derivative” in this case is the Riemannian connection [Bou22, Thm. 5.6].) As is standard, we take the latter form to be the definition of the Riemannian Hessian [Bou22, Def. 5.14].

Proposition 10 (Riemannian Hessian for (MC-BM)).

The Riemannian Hessian of Obj at , acting on , is given by

where the linear map denotes the orthogonal projector onto , i.e., . is defined as in (30).

Proof.

This follows immediately from Equation 2.7 in [BVB18], which provides an expression for the Riemannian Hessian for a more general class of programs. (Their expression for the multiplier , which they call —see Equation 2.5 in that paper, is more complicated as it is for a more general class of programs, which is why we derived the Riemannian gradient from first principles in the proof of Proposition 9. However, the two expressions for this multiplier are ultimately equivalent for (MC-BM) due to the uniqueness of the Riemannian gradient.) See also Section 7.7 of [Bou22] for exposition (including an expression for the Riemannian Hessian) for a very general class of programs encompassing (MC-BM). ∎

Appendix C Extending construction of spurious local minimum to

Lemma 10 allows us to extend our construction of a spurious local minimum for the case to . Indeed, it implies that our construction of a spurious local minimum for the instance of (MC-BM) with associated feasible region yields a construction of a spurious local minimum for the instance of (MC-BM) with associated feasible region , for all . Thus, one can construct an instance of (MC-BM) with a spurious local minimum when using the construction for the instance of (MC-BM) associated with .

We note that Lemma 10 also holds if you replace “spurious local minimum” with “spurious first-order critical point” or “spurious second-order critical point,” although we do not prove it here. However, the intuition is clear: we embed a “bad instance” into the higher-dimensional space, and design the cost matrix so that the bad instance does not interact with the added dimensions.

Lemma 10.

Proof.

We claim that the following construction works:

where is arbitrary except with the single restriction that all of its rows are unit vectors. Since is a local minimum for the instance of (MC-BM) with cost matrix and feasible region , there exists such that for with , we have . Now let with . Let denote the submatrix of consisting of the first rows. Then

since . Thus, is a local minimum.

To see that is spurious, the spuriousness of implies that there exists such that . Then define , where is once again some matrix whose rows are unit vectors. Then,

∎

Appendix D Further discussion of challenges for proving local minimality

In this section, we further discuss challenges associated with proving is a local minimum in a “traditional” way. For example, [WW20], which constructs spurious local minima for (MC-BM) when , similarly first constructs spurious second-order critical points and then proves they are additionally local minima. However, their proof follows because their spurious second-order critical points are non-degenerate [WW20, Def. 3 and Rem. 1], which corresponds to the rank of the Riemannian Hessian being sufficiently high. (See Remark 2 in that paper.) We show that every spurious second-order critical point for (MC-BM) is degenerate when is above the Barvinok-Pataki bound, meaning this approach won’t work:

Proposition 11 (Spurious second-order critical points are degenerate when ).

Proof.

Theorem 1.6 from [BVB18] gives that any spurious second-order critical point for (MC-BM) must be full rank, meaning . Let , where is defined as in (1). Then the first-order criticality of (Proposition 2) implies , meaning . We have (see Section 2.1):

| (33) |

for any . Here, stacks the columns of on top of one another to convert into a column vector, and denotes the Kronecker product. In (33), we used the fact that .

Degeneracy of higher-order derivatives at .

We know from Proposition 6 that is a spurious second-order critical point if and only if the cost matrix takes the form

| (34) |

for some and strictly pseudo-PSD . A natural question is whether higher-order Riemannian derivatives888See Section 10.7 of [Bou22] for an introduction to higher-order Riemannian derivatives. could be used to identify an additional condition under which is a (spurious) local minimum. For example, one may hope to show that when is additionally (strictly) pseudo-PD (the condition identified in Lemma 1), then the fourth derivative is positive. Unfortunately this is not possible, as one can show that all higher-order Riemannian derivatives at are degenerate when the cost matrix takes the form (34).

This follows via an examination of . Indeed, consider the subspace given by those matrices of the form

| (35) |

It is easily observed that is contained in the kernel of when the cost matrix takes the form (34). Furthermore, one can show that is orthogonal to the vertical space at [Bou22, Def. 9.24] when we consider the quotient manifold , where denotes the open subset of containing its rank elements and denotes the orthogonal group in dimension . Indeed, the vertical space at consists of all tangent vectors of the form where is skew-symmetric. (See, e.g., p. 6 of [WW20].) Thus, the vertical space at is precisely the subspace of taking the form

which is clearly orthogonal to .

Since tangent vectors in the subspace are in the kernel of but not in the vertical space,999In fact, one can show that when in (34) is pseudo-PD, then contains all tangent vectors which are in the kernel of but not in the vertical space. one may worry that following a smooth curve ( is an open interval of containing 0) such that could yield a decrease in the objective value for sufficiently small inputs . Indeed, one must rule out such behavior to prove is a local minimum.

Unfortunately, higher-order Riemannian derivatives at all also contain in their zero sets, so they cannot a priori be used to rule out this behavior. Recall that formally, the th Riemannian derivative of Obj is a tensor field of order [Bou22, Def. 10.76] given by , where denotes the total covariant derivative [Bou22, Def. 10.77]. (Elsewhere in the paper we have used to denote the classical Euclidean derivative, but the usage of in this section is different; the total covariant derivative is not (in general) the Euclidean derivative.) Furthermore, recall that tensor fields are pointwise objects, so we use the notation to denote the -linear function associated to a point . Then we have the following result:

Proposition 12 (Higher-order Riemannian derivatives at are degenerate).

Note that Proposition 12 of course additionally encompasses the cases where is pseudo-PSD, pseudo-PD, etc.

Proof.

For notational brevity, let be shorthand for in this proof. Let be a geodesic [Bou22, Def. 5.38] such that . ( is an open interval in containing 0.) A simple extension of Example 10.81 in [Bou22] implies

for any . (Here, note that , so is the “usual” th derivative of a function from (an open interval in) to .) Thus, it is sufficient to exhibit such a geodesic such that is constant over (implying ).

To construct this geodesic, we will take advantage of the fact that is a product manifold formed by the Cartesian product of unit spheres in . Recall that for the unit sphere with , the curve

(with the usual smooth extension at ) is a geodesic which traces the great circle on the sphere from in the direction . (See Example 5.37 in [Bou22].) Of course, .

Then, viewing in the form with the th entry corresponding to the th row in , we choose , where denote the th rows of (taken as column vectors). Then is a geodesic (e.g., [Bou22, Exerc. 5.39]) and . All that is left is to show that is constant. This follows due to the form of ; it is easy to check that for all sufficiently small , we have that is an antipodal configuration as defined in Section 5. (Recall that antipodal configurations take the form for some .) And it is easy to see that when the cost matrix takes the form (36), all antipodal configurations have the same objective value. ∎

Thus, we have identified (a subspace of) tangent vectors at which are not in the vertical space at and which lie in the zero sets of all higher-order Riemannian derivatives at . As a result, it is not clear how higher-order Riemannian derivatives at can be used to prove is a local minimum.

Appendix E Proof that Riemannian gradient descent is nonincreasing (Lemma 4)

We first restate a result from [Bou22] which yields a quadratic upper bound on the objective in the same style as the classic quadratic upper bound which holds in the Euclidean case when the Euclidean gradient is Lipschitz. (Indeed, the Riemannian gradient for (MC-BM) is Lipschitz, but defining Lipschitzness for the Riemannian gradient requires care [Bou22, Definition 10.44]. Proposition 13 is sufficient for our purposes since we only need a quadratic upper bound and don’t care about the actual value of the Lipschitz constant.)

Proposition 13 (Quadratic bound [Bou22, Lem. 10.57, abbreviated]).

We now give the proof of Lemma 5:

-

Proof of Lemma 4. Formally, our goal is to identify such that for any and , we have

with defined as the metric projection retraction for , as in Section 2.3. (In fact, we will show that when , our proof yields a strict decrease: .)

We apply Proposition 13 with , as clearly is compact. The fact that is continuous implies is continuous, and this together with the compactness of implies there exists some constant such that for all .

Pick to be the constant function which sends everything to , i.e., for all . Then for all and , we have .

Then Proposition 13 implies there exists some constant such that for , we have

Then for all , so setting yields the desired result. ∎

Appendix F Minor claims

In this section, we prove minor claims that are used in Section 5.

Lemma 11 (Close to orthogonal).

Let be such that . Then .

Proof.

We have

∎

Lemma 12 (Reverse triangle inequality with squares).

Let . Then

Proof.

Note that

The result follows by symmetry. ∎

Lemma 13 (Normalizing doesn’t increase the potential).

Set , and let be defined as in Lemma 5, although we abuse notation here and extend the domain to . Let be arbitrary except with the single restriction that the norm of each of its rows is at least 1, and let denote the matrix formed by normalizing each row of . Then .

Proof.

It is clearly sufficient to show that for all . ( denotes the th row.) This follows from Lemma 14 below. ∎

Lemma 14 (Metric projection is contractive).

Let be such that . Then for any , we have

Proof.

We have

In the second line, we used Cauchy-Schwarz and the fact that . ∎