Roger Lee proved that the Black-Scholes implied variance can not grow faster than linearly in log-moneyness. This paper investigates what happens in the Bachelier (or Normal) implied volatility world, making sure to cover the various aspects of vanilla option arbitrages.

keywords:

implied volatility, b.p. vol, Bachelier, Black-Scholes, European option, arbitrages

\pubvolume

xx

\issuenum1

\articlenumber1

\history\TitleOn the Bachelier implied volatility at extreme strikes

\AuthorFabien Le Floc’h

\AuthorNamesFabien Le Floc’h

\corresCorrespondence: fabien@2ipi.com

1 Introduction

Under the Bachelier (also known as normal, or b.p. vol) model, a drift-less underlying asset price is subject to the following stochastic differential equation:

where is a Brownian motion and is the Bachelier volatility.

The prices of European call and put options of maturity and strike are known in closed form and read Bachelier (1900)

(1)

(2)

where are respectively the normal distribution and cumulative normal distribution functions and is the discount factor to maturity.

In practice, the underlying asset is a forward rate, such as a forward swap rate for an interest rate swaption, or the spread between two commodity forward or future prices. As in the Black-Scholes model, the market prices of European options imply different values of the Bachelier volatility, depending on the strike and the time to maturity of the option considered.

Roger Lee proves that the Black-Scholes implied volatility asymptotics can not be arbitrary in Lee (2004): the implied distribution does not have finite moments if the square of the total implied variance grows faster than where is the log-moneyness , is the option strike, the underlying asset forward to maturity and is the Black-Scholes implied volatility for the given moneyness and maturity.

As a consequence, any implied variance extrapolation must be at most linear in the wings, a fact of great practical interest.

Earlier, Hodges derived simpler bounds on the Black-Scholes implied volatility based on the option slopes in Hodges (1996), later refined by Gatheral in Gatheral (1999). Benaim et al. Benaim and

Friz (2009); Benaim

et al. explore the Black-Scholes implied volatility asymptotics of various models including the SABR stochastic volatility model of Hagan et al. Hagan

et al. (2002).

With the advent of low or negative interest rates, practitioners have moved towards the use of the Bachelier model. Then, a natural question that arises is: what kind of extrapolation is acceptable in the Bachelier model?

We start with a tight upper asymptotic boundary of the Bachelier implied volatility. We continue by looking at the sufficient conditions for the existence of the distribution moments in terms of implied volatility. We conclude with a visualization of the boundary cases, both in the Black and in the Bachelier models.

2 Asymptotic upper bound of the Bachelier implied volatility

{Theorem}

The Bachelier implied volatility is bounded above by when or more precisely,

if such that then the Bachelier option price has arbitrages.

Proof.

In order for the model to be meaningful for option pricing, the forward price must be finite, that is . By dominated convergence, we must have

Let , we have

An expansion of the cumulative normal distribution is

(3)

When , taking the first term of the serie, we have then

or

(4)

For , .

As is monotone in its second argument, is bounded by when for all .

∎

The bound for negative strikes is very similar. In this case, we will rely on the put option price . Under the Bachelier model, we have . Let . When , the expansion of the cumulative normal distribution leads to .

3 Acceptable lower bound of the Bachelier implied volatility

In order to preserve arbitrage, the call and put prices must also obey

In terms of the variables and , this translates to

(5)

Let us consider , we have

According to the asymptotic expansion of the cumulative normal distribution function given by Equation 3 we have for sufficiently large:

For , we thus have

for sufficiently large.

∎

In similar fashion, it can be proven that a tighter lower bound is

(6)

for .

4 Relation between moments explosion and the Bachelier implied volatility

{Theorem}

If the Bachelier implied volatility is below as with and below as with , then the -th moment exists.

Proof.

Let be a function of class on , then, following the steps of Carr and Madan in (Carr

et al., 2001, appendix A), we have

Let , applying the above to and leads to

Given that the call and put prices are monotonically increasing in the volatility argument , it suffices to prove that the call integral converges for and put integral converges for .

The call integral will converge for , that is for .

Similarly, the put integral will converge for , that is for .

∎

{Corollary}

If the Bachelier implied volatility behaves like as , for , then all the moments exists.

5 Visualization of limiting cases

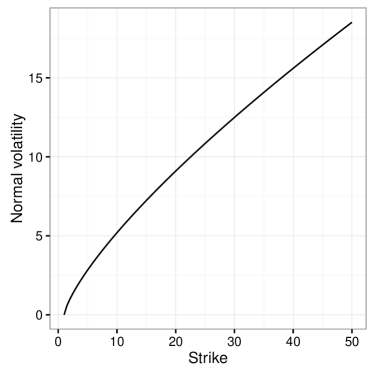

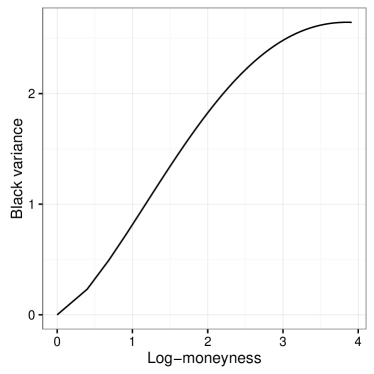

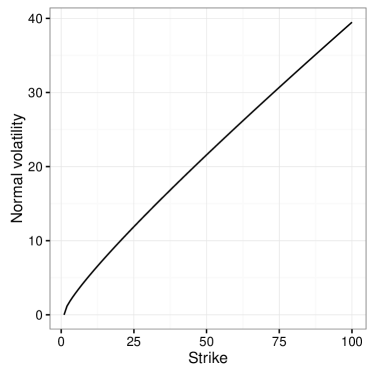

Figure 1 shows that the Black implied volatility will flatten in general for large strikes when the Bachelier implied volatility is of the form with .

(a) Bachelier

(b) Black

Figure 1: Black variance corresponding to the Bachelier normal volatility smile .

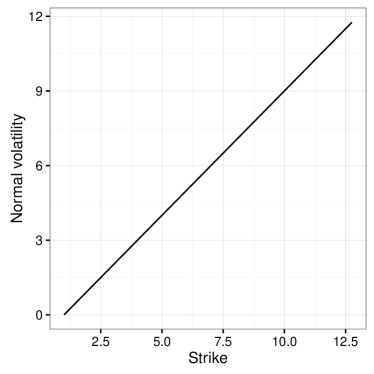

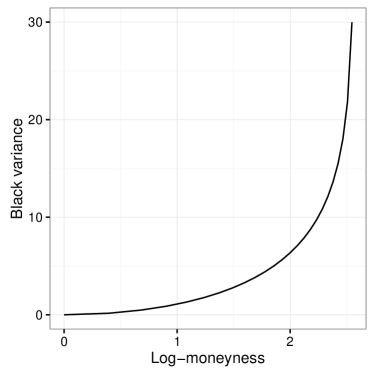

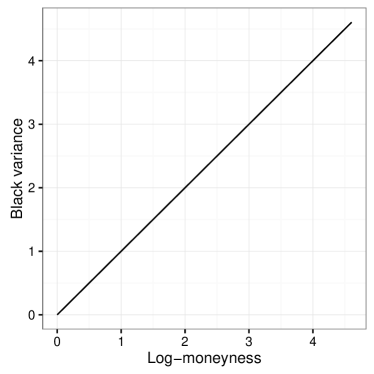

A linear normal volatility can lead to super-linear Black variance as in Figure 2.

(a) Bachelier

(b) Black

Figure 2: Black variance corresponding to the Bachelier normal volatility smile .

The limit case for Black volatilities, a linear Black variance looks almost linear (but is not) in the wings in terms of normal volatility (Figure 3).

(a) Bachelier

(b) Black

Figure 3: Bachelier normal volatility corresponding to the Black variance .

6 Conclusion

We have shown that the Bachelier implied volatility asymptotic for large strikes is bounded by the function , above for and below for to guarantee a proper behavior of the vanilla call option prices. For , this function guarantees the absence of arbitrages. The value of determines how many moments of the distribution are finite.

We leave to further research the refinement of the boundary with additional terms. Unlike the Black-Scholes case, there is, a priori, no exact simple closed form formula for the asymptotic in the Bachelier model.

\funding

This research received no external funding.

\conflictsofinterestThe authors declare no conflict of interest.

Acknowledgements.

Fruitful conversations with Gary Kennedy and Peter Carr.

\externalbibliographyyes

References

Bachelier (1900)

Bachelier, Louis. 1900.

Théorie de la spéculation.

In Annales scientifiques de l’École normale supérieure,

Volume 17, pp. 21–86.

Benaim and

Friz (2009)

Benaim, Shalom and Peter Friz. 2009.

Regular variation and smile asymptotics.

Mathematical Finance19(1), 1–12.

(3)

Benaim, Shalom, Peter Friz, and Roger Lee.

On Black-Scholes implied volatility at extreme strikes.

Frontiers in Quantitative Finance, 19.

Carr

et al. (2001)

Carr, P, D Madan, et al.. 2001.

Optimal positioning in derivative securities.

Quantitative Finance1(1), 19–37.

Gatheral (1999)

Gatheral, Jim. 1999.

The volatility skew: Arbitrage constraints and asymptotic behaviour.

Merrill Lynch.

Grunspan (2011)

Grunspan, Cyril. 2011.

A note on the equivalence between the normal and the lognormal

implied volatility: A model free approach.

Available at SSRN 1894652.

Hagan

et al. (2002)

Hagan, Patrick S, Deep Kumar, Andrew S Lesniewski, and Diana E Woodward. 2002.

Managing smile risk.

The Best of Wilmott, 249.

Hodges (1996)

Hodges, Hardy M. 1996.

Arbitrage bounds of the implied volatility strike and term structures

of european-style options.

The Journal of Derivatives3(4), 23–35.

Jäckel (2015)

Jäckel, Peter. 2015.

Let’s be rational.

Wilmott2015(75), 40–53.

Le

Floc’h (2014)

Le Floc’h, Fabien. 2014.

Fast and accurate analytic basis point volatility.

Available at SSRN 2420757.

Lee (2004)

Lee, Roger W. 2004.

The moment formula for implied volatility at extreme strikes.

Mathematical Finance14(3), 469–480.

Lorig

et al. (2015)

Lorig, Matthew, Stefano Pagliarani, and Andrea Pascucci. 2015.

Explicit implied volatilities for multifactor local stochastic

volatility models.

Mathematical Finance.

\appendixtitles

no

Appendix A Asymptotic expansions relating Black and Bachelier volatilities

Although the problem of converting Black volatilities (also called basis point volatilities or Bachelier volatilities) to normal volatilities can be solved quite efficiently by relying on inverting the Black-Scholes price through the nearly closed form representation of Le Floc’h Le

Floc’h (2014), or if the reverse is needed, through a good Black implied volatility solver such as the one of Jäckel Jäckel (2015), the behavior around the money is well described by the following simple and fast expansions:

•

Hagan simple second order approximation Hagan

et al. (2002)

(7)

•

Hagan fourth order approximation Hagan

et al. (2002)

(8)

•

The small time expansion of Grunspan Grunspan (2011)

(9)

Following their paper derivation, we can also find the inverse expression.

•

The third order Black implied volatility expansion of Lorig Lorig

et al. (2015)