Feedback Interacting Urn Models

Abstract

We introduce and discuss a special type of feedback interacting urn model with deterministic interaction. This is a generalisation of the very well known Eggenberger & Pólya (1923) urn model. In our model, balls are added to a particular urn depending on the replacement matrix of that urn and the color of ball chosen from some other urn. This urn model can help in studying how various interacting models might behave in real life in the long run. We have also introduced a special type of interacting urn model with non-deterministic interaction and studied its behaviour. Furthermore, we have provided some nice examples to illustrate the various consequences of these interacting urn models.

Keywords: Urn Model, Interaction, Cyclic.

1 Introduction

We devise a toy model inspired by the following real life examples. Let us consider two interacting stock markets, A and B. Suppose initially the stock market-A is assumed to have bullish tendency while stock market-B is assumed to have bearish tendency. These two stock markets operate alternately in mutually exclusive hours, for example, Tokyo stock market and New York stock market. Now due to the interaction between these two stock markets, each market may get influenced by the other. Our model is motivated by a natural question that might arise here: whether it is plausible for both the stock markets to change their nature in the long run due to the influence of the other. Another related example is in the context of the interaction between political preferences of two neighbouring states in USA during their elections. We know the states in USA hold state governor elections every four years but not necessarily simultaneously. Election results of one state can influence that of neighbouring state holding elections in a different cycle. Thus we can study two neighbouring states running different election cycles with tilt towards Republicans and Democrats respectively and analyse whether their political leanings can go through a change. We devise a toy model inspired by the following real life examples. Let us consider two interacting stock markets, A and B. Suppose initially the stock market-A is assumed to have bullish tendency while stock market-B is assumed to have bearish tendency. These two stock markets operate alternately in mutually exclusive hours, for example, Tokyo stock market and New York stock market. Now due to the interaction between these two stock markets, each market may get influenced by the other. Our model is motivated by a natural question that might arise here: whether it is plausible for both the stock markets to change their nature in the long run due to the influence of the other. Another related example is in the context of the interaction between political preferences of two neighbouring states in USA during their elections. We know the states in USA hold state governor elections every four years but not necessarily simultaneously. Election results of one state can influence that of neighbouring state holding elections in a different cycle. Thus we can study two neighbouring states running different election cycles with tilt towards Republicans and Democrats respectively and analyse whether their political leanings can go through a change.

We shall model these phenomena using urn models. Urn model is one of the simplest and most useful models considered in probability theory. There have been various extensions and generalizations of this model since its introduction by Eggenberger & Pólya (1923). In this work we shall consider a special extension of this model with multiple urns involving feedback interaction. We have considered cases where the interaction is deterministic and also cases where it is not. Similar interacting urn models have previously been studied in Chen et al. (2014), Launay & Limic (2012), Siegmund & Yakir (2005), Kaur & Sahasrabudhe (2019).

To begin with, we consider a 2-urn-2-color model. In this model, we are given two urns, both of which contain balls of two colors, say red and black. We shall motivate our model by the stock market example. However a similar explanation will hold for the political behaviour. The color red will correspond to the bearish tendency and the color black will be for the bullish tendency. The two stock markets may interact with each other in various ways. For example a trader in the market-B (which is initially bearish) will observe the outcome of the market-A in the previous session to decide his move. If the market-A has moved bullishly, the trader will put some weight for bullish nature, denoted by , while deciding his trade. However, if an inherently bullish market-A behaves bearishly in the previous session, the trader in market-B (which is bearish itself) will be sure to make a bearish trade. A trade in the stock market-A under the influence of the stock market-B will be defined analogously. Thus we define two replacement matrices, , as follows.

where . Initially in the first urn, black is the dominant color and in the second urn, red is the dominant color. We start with one ball of dominant color in each of the urns to signify their initial behaviour. An iterative process motivated by the stock market and the electoral example is then performed on these two urns. A ball is chosen from the first urn and its color is noted. The color of the chosen ball will correspond to the type of move in the stock market-A. Based on the color being red (bearish move) or black (bullish move), we reinforce the second urn (corresponding to the stock market-B) according to . It can be seen that corresponding to the red color (bearish move) we reinforce the red color (bearish move) only in the second urn. On the other hand corresponding to the black color (bullish move) both the colors are reinforced in the second urn with suitable weighing. Thereafter a ball is chosen from the second urn and a similar process is done. This process is then repeated, alternately applying it on both of the urns. Here and will denote the amount of influence of the other market on the markets A and B respectively.

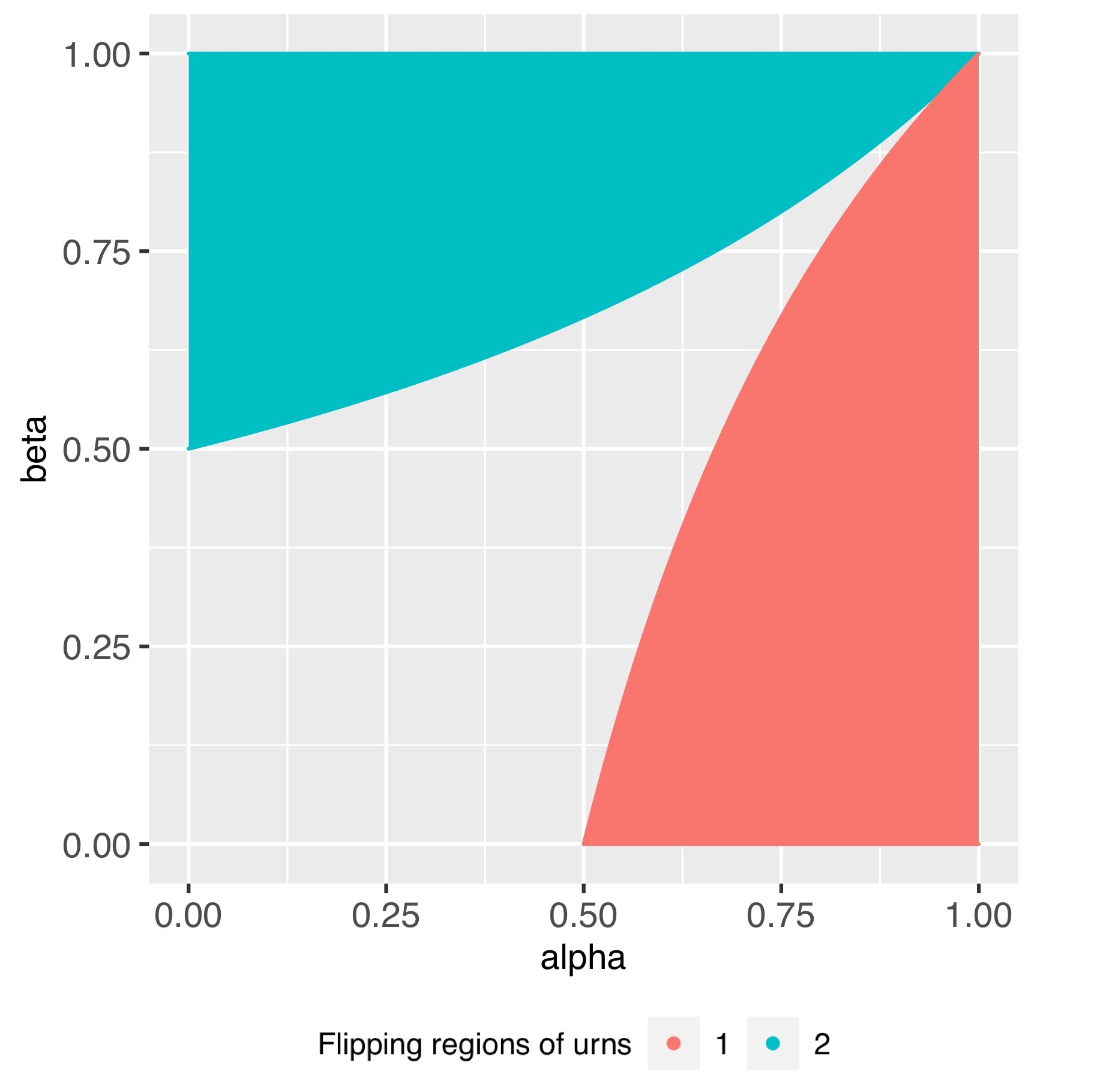

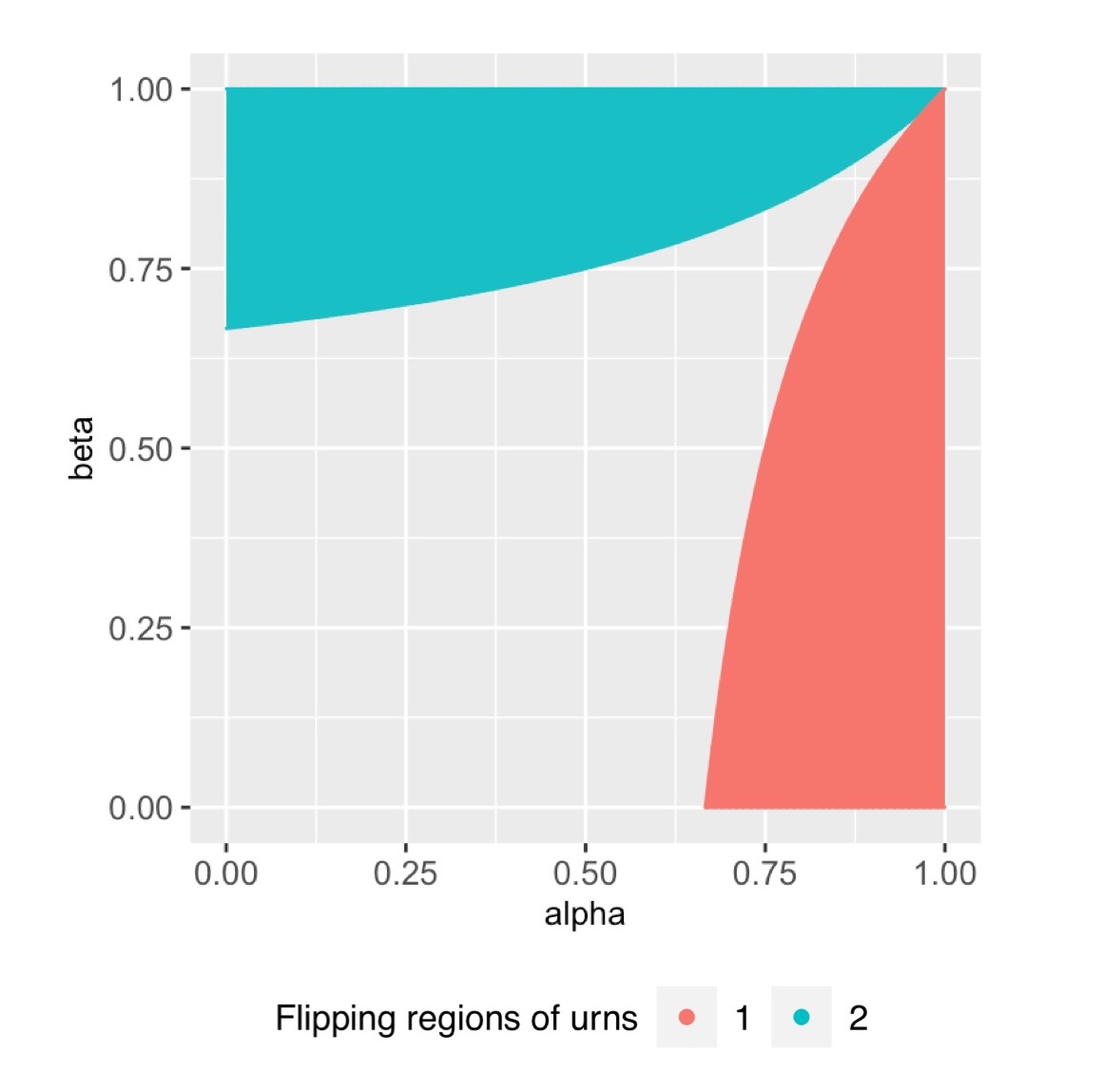

In this work, we say that a particular urn flips if the proportion of the dominant color of the urn becomes less than that of the other color. For instance in this model, we say that the first urn flips in the limiting case if the proportion of red balls becomes more than that of black balls. The flipping of the second urn can be understood analogously. It shall be shown that, both the urns can not flip simultaneously in the limiting case. In particular we shall show in Section 4.1 that,

| first urn flips iff | ||||

| and | ||||

| second urn flips iff | ||||

In this paper we shall extend the model to urns containing balls of colors () and different feedback interaction mechanisms shall be appropriately defined and analysed.

The paper is divided into the following sections. Section 2 introduces a feedback interacting urn model where the interaction is deterministic. We also compute the almost sure limits of the proportion vectors of the urns (i.e. the vector of the proportion of each color present in an urn) in this section. Section 3 considers a far more generalized interacting urn model where the interaction is non-deterministic. We further compute the almost sure limits of the proportion vectors of the urns for this generalized model. Section 4 discusses some nice and interesting consequences of the theorems developed in the earlier sections.

2 Feedback Interacting Urn Model with Deterministic Interaction

Here, we consider a deterministic cyclic interacting urn model. In this model, there are urns. Each of the urns may contain balls of different colors. The replacement matrices of the urns are given by , all of which are matrices. Initially there is at least one ball in each of the urns. The following iterative process is then performed:

-

1.

A ball is chosen from the first urn. The color of the ball is noted. Then, balls are added to the second urn according to based on the color of the ball chosen from the first urn.

-

2.

A ball is chosen from the second urn. The color of the ball is noted. Then, balls are added to the third urn according to based on the color of the ball chosen from the second urn.

-

3.

-

4.

A ball is chosen from the -th urn. The color of the ball is noted. Then, balls are added to the first urn according to based on the color of the ball chosen from the -th urn.

-

5.

Go to step(1).

Under this set-up, we have the following theorem.

Theorem 1.

Suppose is the following matrix:

| (2.1) |

We make the following two assumptions: (i) is a balanced (each row sum is 1) replacement matrix with all the entries non-negative for i=1,2,,m and (ii) is an irreducible matrix.

Let denote the composition vector of the th urn at the th stage, where . Define for . If we have the set-up described as above, then, we have the following result:

where is the left eigen-vector of the matrix corresponding to the eigen-value 1. Moreover all the entries of are strictly positive.

-

Proof of Theorem 1.We shall require the following lemma taken from Gouet (1997) to prove this theorem.

Lemma 1.

Let be an irreducible non-negative matrix and . Let be a sequence of non-negative normalized (sum of components=1) vectors such that , then if is the dominant eigen-vector of , we have the following convergence:

We can now proceed to prove this theorem. We can re-frame the given model in the following way. We combine all the urns into a single urn. The replacement matrix of the combined urn is the matrix , as given in Theorem 1. In the combined urn, the balls of first colors correspond to the balls in Urn-1, the balls of the next colors correspond to the balls in Urn-2 and so on. Let denote the composition of the th urn in the th stage. Also, let . In other words, is the composition vector of the combined urn at the -th stage. Let us denote by , the vector to indicate which color is chosen at the th stage from the combined urn. Note that, both and are dimensional row vectors. Hence, if the -th color is chosen at the -th stage, where ( is the canonical basis of ). We need to keep in mind that in the first step, the ball is chosen from urn-1, in the second step, the ball is chosen from urn-2 and so on in a cyclic manner. Suppose, is the sigma field generated by the set . Let us describe the distribution of . For where , we have,

(2.2) Similarly, when where and , we have:

(2.3) We shall now apply the Martingale version of Second Borel-Cantelli Lemma separately times on depending on whether is equal to for some . (Note that if is a vector, then denotes the -th component of ). We get the following equations using the distribution of given in (2.2) and (2.3). For where , we have,

(2.4) for . We have, . Thus, we get the following equations. For where , we have,

(2.5) Now, let us denote by , the sub-vector of formed by its first entries; by , the sub-vector of formed by its next entries and so on. Similarly, we define . Thus, we can rewrite the equations in (2.5) in the following manner. For where , we have,

(2.6) where, is the diagonal matrix with the diagonal entries, . We know that for the urn composition evolves as :

(2.7) There are cases depending on whether is equal to for some . We shall show the detailed calculation for only where . The calculations for the other cases can be done quite similarly. We have,

(2.8) where, is the diagonal matrix with the diagonal entries, . From (2.7) and (2.8), we have,

(2.9) Matching the first components of the vectors on the right and left side, we obtain,

(2.10) Now, we define, for . Note that, is the proportion vector of the th urn at the th stage(i.e. the first entry in denotes the fraction of balls of first color in urn- at the th stage, the second entry denotes the fraction of balls of second color in urn- at the th stage and so on).

Thus, the cesaro means will be, for . Using these notations, equation (2.10) boils down to :(2.11) Similarly, we get convergence equations:

(2.12) We can rewrite these equations as follows:

(2.13) Now, we shall combine all the equations into a single equation. Let . So, on combining all the equations into a single equation, we get:

(2.14) which implies that,

(2.15) where,

(2.16) We observe that, as and as . Thus as . We also observe that is bounded. This is because, . Thus is also bounded. Hence, we can obtain the following convergence,

(2.17) We now simply add the equations (2.15) and (2.17) to obtain,

(2.18) We know that is a non-negative irreducible stochastic matrix (by the assumption made in Theorem 1) and is a sequence of non-negative normalized vectors. Suppose, is the dominant eigen-vector of . Hence, on applying Lemma 1 to (2.18), we get,

(2.19) Let denote the sub-vector formed by the first entries of , denote the sub-vector formed by the next entries of and so on. Thus, we have, . We note that as as , we have as for . From the equation, , we obtain the following relations, , ,,. From these equations, we obtain that . Thus, is the dominant eigen-vector of the matrix . It can be shown similarly that is the dominant eigen-vector of the matrix for . Hence we can say that for . This completes the proof. ∎

We note that one of the main assumptions of Theorem 2 is that the matrix, is irreducible. This might be a difficult condition to verify in some situations. We thus provide below a necessary and sufficient condition to verify that is an irreducible matrix.

Lemma 2.

is an irreducible matrix iff is an irreducible matrix for .

-

Proof of Lemma 2.At first, let us prove the ’only if’ part. Thus, we need to prove that is an irreducible matrix assuming that is an irreducible matrix. Let us take a look at the powers of . has the following form,

(2.20) Continuing like this, will have the following form,

(2.21) Now, since is an irreducible matrix, this implies that for , a natural number such that . Note that the diagonal blocks of are non-zero only when . Moreover, we note that when , the diagonal blocks are where . Similarly, when , the diagonal blocks are where . Hence, for to be an irreducible matrix, must be an irreducible matrix for . This completes the proof of the only if (necessary condition) part.

Now let us prove the ’if’ part. Here, we are given that is an irreducible matrix for . We need to show that is an irreducible matrix. Before proving this, we need to prove two claims.

Claim 1.

Suppose, are both matrices, have non-negative entries and are balanced (each row sum is equal to 1). Suppose is an irreducible matrix. Then, given , such that, .

-

Proof of 1.We note that, . Since, sum of all entries in is 1, such that, . Also, since is irreducible, such that . Thus, for this we have, . ∎

Claim 2.

Suppose are two matrices with non-negative entries and are balanced (each row sum is equal to 1). Then satisfies the same properties as i.e. it is also balanced (each row sum is ).

2 can be proved simply by multiplying and . Now, let’s come back to the proof of the sufficiency part. Note that any sub-matrix in has the following form: for some . By 2, we know that is balanced (each row sum is 1). Setting and (irreducible) and thereafter using 1, we are done. This completes the proof of the if (sufficient condition) part and hence also the proof of Lemma 2. ∎

3 Feedback Interacting Urn Model with Non-Deterministic Interaction

Instead of working with a deterministic model as in Section 2, here we will work with a non-deterministic interacting urn model. Like in the previous case, we have urns and each of them may contain balls of different colors. The replacement matrices of the urns are given by , all of which are matrices. Also, there is an stochastic matrix, given by,

| (3.1) |

It is assumed that all the urns have at least one ball in them initially. Now the following iterative process is performed:

-

1.

A ball is chosen from the first urn. The color of the ball is noted. Then, an urn is randomly chosen from the urns based on the probability vector i.e. the first row of . Hence the first urn is chosen with probability , the second urn is chosen with probability and so on. Then, balls are added to the chosen urn according to the replacement matrix of that urn based on the color of the ball chosen from the first urn.

-

2.

A ball is chosen from the second urn. The color of the ball is noted. Then, an urn is randomly chosen from the urns based on the probability vector i.e. the second row of . Then, balls are added to the chosen urn according to the replacement matrix of that urn based on the color of the ball chosen from the second urn.

-

3.

-

4.

A ball is chosen from the -th urn. The color of the ball is noted. Then, an urn is randomly chosen from the urns based on the probability vector i.e. the -th row of . Then, balls are added to the chosen urn according to the replacement matrix of that urn based on the color of the ball chosen from the -th urn.

-

5.

Go to step(1).

We have the following theorem for this set-up.

Theorem 2.

As in Theorem 1, let denote the proportion vector of urn- at the -th stage. Let be a matrix defined as follows,

| (3.2) |

Let be the left eigen-vector of corresponding to the eigen-value . Suppose denotes the sub-vector formed by the first entries of , denotes the sub-vector formed by the next entries of and so on. We make the following two assumptions: (i) is a balanced (each row sum is 1) replacement matrix with all the entries non-negative for i=1,2,,m and (ii) is an irreducible matrix. If we have the set-up described as above, then, we have the following result:

-

Proof of Theorem 2.We shall construct a combined replacement matrix from these matrices. Let denote the -th block of . The matrix is constructed in such a way that for and otherwise. Let us give an example to illustrate how the matrix is constructed from the given replacement matrices. We give an example for the case when below,

As in the earlier proof, we re-frame the given model by combining all the urns into a single urn having replacement matrix as described above. Suppose the composition vector of the combined urn at the -th stage is given by . Here, is the composition vector for the number of balls that have been added to the -th urn due to color selection from the -th urn till time . So, is a dimensional vector for . We also introduce the following notations: , and so on. Thus all are dimensional row vectors. Let us denote by , the vector to indicate which color is chosen at the th stage from the combined urn. Note that, is a dimensional row vector. Hence, if the -th color is chosen at the -th stage, where ( is the canonical basis of ). We need to keep in mind that in the first step, the ball is chosen from urn-1, in the second step, the ball is chosen from urn-2 and so on in a cyclic manner. Suppose, is the sigma field generated by the set . Therefore, the distribution of is as described below. Let . For where we have,

(3.3) We shall now apply the Martingale version of Second Borel-Cantelli Lemma separately times on depending on whether is equal to for some . (Note that if is a vector, then denotes the -th component of ). We get the following equations using the distribution of given in (3.3). For where we have,

(3.4) We have, . Let denote the sub-vector of formed by the first entries, denote the sub-vector of formed by the next many entries and so on. From (3.4), we get the following set of equations in vector notation. For where we have,

(3.5) where is defined as,

(3.6) Note that is a matrix for . We know that for the urn composition evolves as in (2.7). There are cases depending on whether is equal to for some . We shall show the detailed calculation for only the last case i.e. when . The calculations for the other cases can be done quite similarly. Suppose, for some . Then, we have,

(3.7) where is matrix whose diagonal submatrices are and all other entries are . Similarly is matrix whose diagonal submatrices are and all other entries are . Therefore, from equation (2.7), we have,

(3.8) We note that, in the matrix product, , all the ’s will be replaced by . In, all the entries in the -th column are and all other columns are . Thus the matrix product looks like the following,

(3.9) Also, let us see what happens when we multiply with . We shall have, . Note that all the entries of are except the -th entry, which is . Here, . Returning back to our proof, we have the following equation,

(3.10) which implies,

(3.11) We remember from Theorem 1 that the proportion vector of the urn- at the -th stage is defined as, . Using these notations, equation (3.11) boils down to,

(3.12) Similarly, we get a total of almost sure convergence equations as .

(3.13) We can rewrite these equations as follows,

(3.14) and so on. Now, we shall combine all the equations into a single equation. Let . So, on combining all the equations into a single equation, we get,

(3.15) which implies that,

(3.16) where,

(3.17) and,

(3.18) We observe that, as and as . Thus as . We also observe that is bounded. This is because, . Thus is also bounded. Hence, we can obtain the following equation,

(3.19) We now simply add the equations (3.16) and (3.19) to obtain,

(3.20) We know that is a non-negative irreducible stochastic matrix (by the assumption made in Theorem 2) and is a sequence of non-negative normalized vectors. Suppose, is the dominant eigen-vector of . Hence, on applying Lemma 1 to (3.20), we get,

(3.21) Hence we obtain that, as for . This completes the proof. ∎

We shall see a nice application of Theorem 2 to an urn model in Section 4.

4 Some Interesting Consequences

In this section, we shall study some interesting consequences of Theorem 1 and Theorem 2. In Section 4.1 and Section 4.2, we shall see the application of Theorem 1 to a special deterministic -urn and -urn model respectively. In Section 4.3, we shall see the application of Theorem 2 to a special non-deterministic -urn model for any given natural number, .

4.1 The -Urn--Color Model

We consider a 2-urn-2-color model. In this model, we are given two urns, both of which contain balls of two colors say red (color 1) and black (color 2). The replacement matrices of the urns are and . Both and are non-random stochastic replacement matrices. The results obviously extend to non-random replacement matrices with constant row sums by obvious rescaling. and are defined as follows,

| (4.1) |

Note that, if and are reducible but not the identity matrix, then after possibly interchanging the names of the colors, they can be converted into upper triangular matrix (respectively lower triangular) as described above. It is assumed that both the urns have at least one ball in them initially and the iterative process mentioned in Section 2 is performed. As mentioned already in Section 1, we say that a particular urn flips if the composition of the dominant color of the urn becomes less than the average composition of the remaining colors. Under this set-up, we have the following corollary.

Corollary 1.

Under the set-up described above, we have the following:

-

1.

If and denote the proportion vectors of colors of first and second urn respectively then we have,

(4.2) -

2.

In the limiting case, either none of the urns flip or exactly one of them flips. However, both of the urns can not flip simultaneously in the limiting case.

-

Proof of Corollary 1.It can be easily shown that and both are irreducible matrices. Hence, from Lemma 2, we obtain that (as mentioned in Theorem 1) is an irreducible matrix. Thus all the assumptions of Theorem 1 are satisfied. Calculating the values of and and applying Theorem 1 proves the first part of the corollary.

For the second part, note that urn-1 flips if composition of the first color becomes more than the composition of the second color in the limiting case. Similarly, urn-2 flips if composition of the second color becomes more than the composition of the first color in the limiting case. We define two sets, , where and . Thus, we obtain that, urn- flips iff and urn- flips iff . We will now show that both the urns can’t flip simultaneously in the limiting case. Suppose, both the urns do flip simultaneously in the limiting case. This implies that which in turn implies that . On simplifying this, we obtain, , which is clearly a contradiction. This proves the second part of the corollary. ∎

For better understanding, we are attaching the graph depicting the intersection of the two curves in Figure 1. Here, the wire-frame is that of a unit square in . The two curves are shown in two different colors. In the limiting case, the two urns flip respectively in the regions exterior to the two curves. We observe that the two urns can not flip simultaneously in the limiting case.

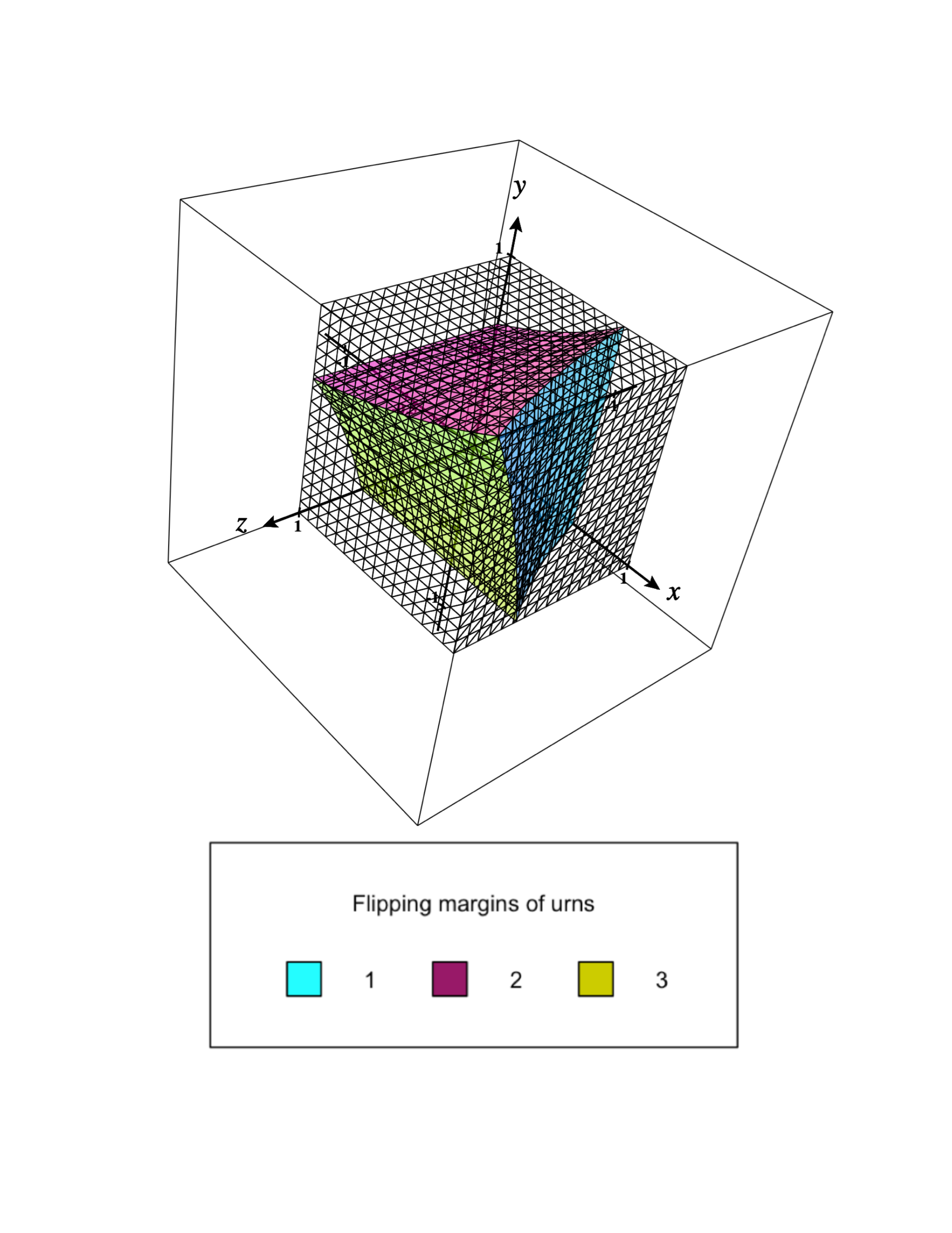

4.2 The -Urn--Color Model

We consider a -urn--color model. In other words, we have . The replacement matrices of the urns, are non-random stochastic matrices. Suppose, are given by,

| (4.3) |

where, . It is assumed that all the urns have at least one ball in them initially and the iterative process mentioned in Section 2 is performed. Under this set-up, we have the following corollary.

Corollary 2.

Under the set-up described above, no two urns flip simultaneously in the limiting case.

-

Proof of Corollary 2.It can be easily shown that , and are all irreducible matrices. Hence, from Lemma 2, we obtain that (as mentioned in Theorem 1) is an irreducible matrix. Thus all the assumptions of Theorem 1 are satisfied. Calculating the values of , , and applying Theorem 1 we obtain for ,

(4.4) Thus we obtain the following,

-

1.

-st urn flips if .

-

2.

-nd urn flips if .

-

3.

-rd urn flips if .

We need to show that no two urns can flip simultaneously in the limiting case. Suppose, the -st and -nd urn flip simultaneously in the limiting case. This implies that the equations and hold simultaneously. From these two equations, we obtain,

(4.5) which implies,

(4.6) This in turn implies that, or . As , we have, or . This is clearly a contradiction as we know that . This completes the proof of the corollary. ∎

-

1.

For better understanding, we are attaching the graph depicting the intersection of the three curves in Figure 2. In Figure 2, the wire-frame is that of a unit square in . The three curves are shown in three different colors. In the limiting case, the three urns flip respectively in the regions exterior to the three curves. We observe that no two urns can flip simultaneously in the limiting case.

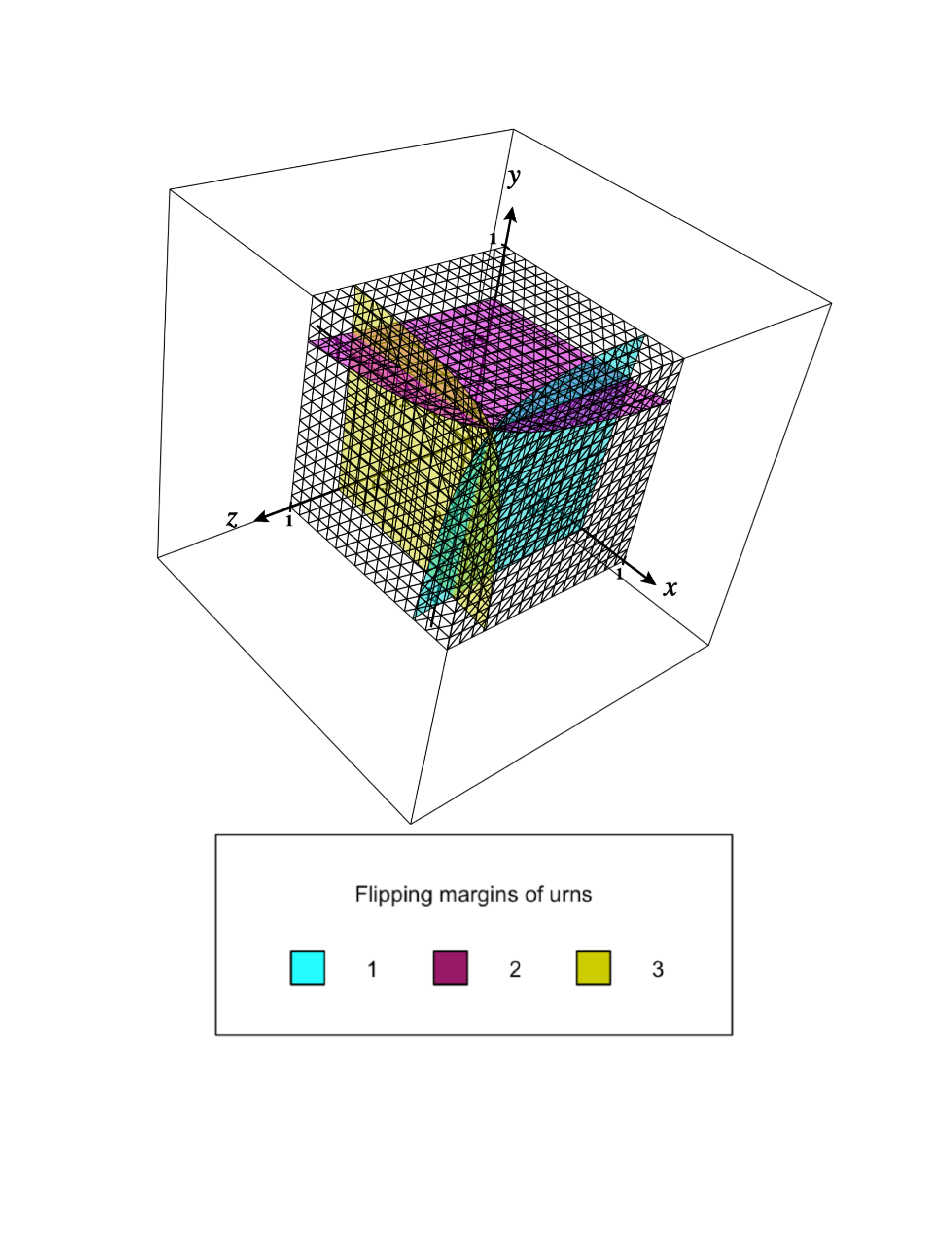

4.3 The -Urn--Color Model

We consider a -urn--color model i.e. we have . The replacement matrices of the urns are non-random stochastic matrices. The replacement matrices of the urns are defined as follows,

| (4.7) |

and so on, where, . Note that, the replacement matrices have been defined in such a way that color-1 is the dominant color of the first urn, color-2 is the dominant color of the second urn and so on. In the stochastic matrix (as defined in Section 3), all the entries are taken to be . It is assumed that all the urns have at least one ball in them initially and the iterative process mentioned in Section 3 is performed. Under this set-up we have the following corollary.

Corollary 3.

In the limiting case, depending on the values of , urns may flip simultaneously where . However, all the urns can never flip simultaneously in the limiting case.

-

Proof of Corollary 3.We shall apply Theorem 2 here. We know that, as for . We note that, in our case we have,

(4.8) Let . So we shall have,

(4.9) Thus, we shall get the following equations. For , we have,

(4.10) Let . Adding all the equations, we shall get, , where . We note that is left eigen-vector of corresponding to eigen-value . Once is obtained, we can obtain all the ’s from the equation, for . Note that,

(4.11) By simple calculation, it can be shown that,

(4.12) Let us now consider the first urn. From the equation , we obtain,

(4.13) Urn- flips if composition of the first color becomes less than the average composition of the other colors. Thus, urn- flips if . Substituting the values of for , we get that, urn- flips if,

(4.14) Similarly, we can obtain the condition of flipping for the remaining urns. Thus, we shall get a total of equations, where each equation represents the condition of flipping for a particular urn. We want to show that all the urns can not flip simultaneously in the limiting case. We shall prove this by the method of contradiction. Suppose all the urns do flip simultaneously. Then all the equations will hold simultaneously. Adding all the equations we get the following,

(4.15) which implies,

(4.16) This is clearly a contradiction as we know that, . Thus, we conclude that all the urns can never flip simultaneously in the limiting case. This completes the proof of the corollary. ∎

We shall give two graphical examples one for the case and the other for the case . This shall help in better understanding and also serve as a justification of the correctness of Corollary 3. In both Figure 3 and Figure 4, the wire-frame is that of a unit square and the curves are shown in different colors. As before, the urns flip in the regions exterior to the curves. We observe that in both Figure 3 and Figure 4, all the urns can not flip simultaneously in the limiting case.

Acknowledgement

The research of the first author was partly supported by MATRICS grant number MTR/2019/001448 from Science and Engineering Research Board, Govt. of India.

References

- (1)

- Chen et al. (2014) Chen, M.-R., Hsiau, S.-R. & Yang, T.-H. (2014), ‘A new two-urn model’, Journal of Applied Probability 51(2), 590–597.

- Eggenberger & Pólya (1923) Eggenberger, F. & Pólya, G. (1923), ‘Über die Statistik verketteter vorgänge.’, Z. Angewandte Math. Mech. 1, 279-289 .

- Gouet (1997) Gouet, R. (1997), ‘Strong convergence of proportions in a multicolor pólya urn’, Journal of Applied Probability 34(2), 426–435.

- Kaur & Sahasrabudhe (2019) Kaur, G. & Sahasrabudhe, N. (2019), ‘Interacting urns on a finite directed graph’, arXiv preprint arXiv:1905.10738 .

- Launay & Limic (2012) Launay, M. & Limic, V. (2012), ‘Generalized interacting urn models’, arXiv preprint arXiv:1207.5635 .

- Siegmund & Yakir (2005) Siegmund, D. & Yakir, B. (2005), ‘An urn model of Diaconis’, The Annals of Probability 33(5), 2036–2042.