Constant Function Market Making, Social Welfare and Maximal Extractable Value111Work in progess.

Abstract

We consider the social welfare that can be facilitated by a constant function market maker (CFMM). When there is sufficient liquidity available to the CFMM, it can approximate the optimal social welfare when all users transactions are executed. When one of the agent has the role of proposing the block, and blockspace is scarce, they can obtain higher expected utility than otherwise identical agents. This gives a lower bound on the maximal extractable value exposed when blockspace is scarce.

1 Introduction

Constant function market makers (CFMMs) are one of the leading application of distributed consensus systems. These markets accurately report prices under the existence of off-chain markets and non-arbitrage condition [2]. In this paper, we explore the properties of the CFMM to aproximate Walrassian Equilibrium prices when players act sequentially with Walrasian demands. Moreover, we study welfare in a model exchange economy with random trader endowments, similar to that of [4] use to study automated market makers (AMMs) for securities with binary payoffs, motivated by prediction markets. We show that if the liquidity available to the CFMM asymptotically increases relative to the wealth of the traders arriving in a single period, it can approximate the optimal social welfare when all users transactions are executed. When one of the agent plays the role of proposing a block, and thus has the ability to censor transactions, they can obtain higher utility than otherwise identical agents when blockspace is scarce relative to transactions.

2 Preliminaries

2.1 Welfare in Walrasian equilibrium

Assume that all players share the same concave utility function . Each player have a vector of endowments drawn from a distribution . All players are utility maximizing price takers, thus given the price of endowments is , a player with endowment solves: {maxi*}—s— Δ’U(Δ’) \addConstraintp⋅Δ=p⋅Δ’. We denote by the that optimizes the problem and by . Then the Walrasian equilibrium price is defined as a price vector such that

By Arrow-Debreu [7], we have that if is strictly increasing, convex and the support of the endowments is bounded, then the Walrasian equilibrium exist. In this paper, we will constrain to the exchange economies with a unique Walrasian equilibrium. For a given set of endowments and a utility function , the social welfare in this game is defined as .

Now, assume that the number of player instances is a finite number . In this case, in order to find the Pareto optimal allocation, we will do the following. Consider a case with traders and assets . Each player, has a preference over the assets modeled by a utility function and is endowed with a non-negative vector of goods drawn from the distribution . Altogether, defines an exchange economy.

Without assuming inventory or storage (such as that of an AMM), the first requirement is that the assignment of goods to individuals not exceed the amounts available. We define the allocation of assets as a vector where denotes trader s bundle according to the allocation. The set of feasible allocation is defined as

and it contains all allocations of goods across individuals that, in total, exhaust the available amount of every good. Under sufficient good conditions, there exist a Walrasian equilibrium, and we can compute the Walrasian equilibrium allocations (WEA).

Now let be i.i.d with distribution . For each instance of , we can compute the Walrasian equilibrium price . And so, the Walrasian equilibrium price follows a distribution with . In this paper, we will assume that for a pure exchange economy with players and endowment distribution with bounded support, we have that and almost surely.

2.2 Constant function market makers

A constant function market maker (CFMM,see [1]) consist of a function , its reserves and transaction fees parameter . The element is the amount of assets available on the CFMM contract, while the function specifies the behavior of the contract. More specifically, if an agent wants to trade with the CFMM a vector of assets if

We say that the CFMM has no fees if . In this paper, we will assume fee-less CFMM except stated otherwise. The agents that add and remove liquidity on the CFMM are called liquidity providers. When adding and removing some reserves by these players, the marginal price of the CFMM can not change, that is, , see [2].

Examples 2.1.

In the following, we provide an incomplete list of examples of CFMM:

-

•

Uniswap V2 DEX has the CFMM defined as . If the tuple of initial reserves is and a trader wants to exchange some amount of tokens , she obtains .

-

•

Constant sum market makers , for some .

-

•

Constant geometric mean market maker , where and .

-

•

Constant min market maker . Observe that if a player with strictly increasing utility function trades with this market maker will reach a state with reserves of the form for some .

-

•

Quadratic-over-linear constant market maker defined in .

-

•

The Minecraft modification package market maker .

In this paper, we will not assume that players have a specific utility function. Therefore, we will need to state the general trade choice problem, similar to the problem stated in [2]. We have a player with strictly increasing and concave utility function with initial endowments . Then, a utility maximizing players that trades with a CFMM with constant function and reserves solves the problem

| subject to |

This problem is a convex problem, thus we can globally and efficiently solve this problem [2]. It is easy to show what the solution will satisfy . For a player with utility function and endowments and a CFMM with function and reserves , we denote the solution of the optimization problem as or if and are clearly specified. Observe that the solution of the optimization problem is not necesrly unique and therefore is not specified. However, we will see that in some conditions, choosing a solution for a specific the function can be extended smoothly.

2.3 Maximal extractable value

Maximal (also miner) extractable value, or MEV, usually refers to the value that privileged players can extract by strategically ordering, censoring, and placing transactions in a blockchain. In our context, this privileged players will be builders or Walrasian auctioneers, i.e. players responsible for constructing the new block or more generally responsible for allocating the goods an input of endowments and preferences revealed.

A formal definition of MEV can be seen in [3, 8]. In this paper, we will define the maximal extractable value as follows.

Definition 2.2.

Let be a builder with utility function and endowments . Let be an allocation mechanism and the set of transactions received by the builder. Then, we define the Walrasian MEV as

3 Constant function market makers with Walrasian demand

In this section, we study the social welfare when players interact with constant function market makers sequentially. We assume that there exist an exogenous liquidity provider with initial liquidity provided to a constant function market maker with convex function . All players share the same utility function and the endowments are drawn from a distribution . Except stated otherwise, we will assume that and are smooth maps.

3.1 Model

In each time period , an agent with endowment and convex, strictly increasing utility function trades in the constant function market maker. After a feasible trade , the liquidity is updated to . Assuming that all players are utility maximizing, we have that, at time the player solves the general trade choice problem computing . For a specific realization of endowments , we denote .

To define the notion of social welfare and optimal welfare in equilibrium, one need to define a notion of the equilibrium on the game. One could be tempted to define a generalization of the notion of Walrasian equilibrium provided in section 2.1. Equivalently, one could say that a reserve in the feasible set of a CFMM with curve is a Walrasian equilibrium for CFMM if

| (1) |

However, in general, there is no solution for the equation 1, see A for counterexample. So, to counterfactual compare different social welfare CFMM, we define the following exchange economy and notion of social welfare.

Definition 3.1.

A CFMM with Walrasian demands (CFMMWD) consists of a tuple . As previous described induces a stochastic process in the topological space . We say that a game is non-subsidizing if . In general, this equilibrium is not computable in polynomial time.

Observation: The stochastic process is in fact a Markov process with state space since a strategic player optimization problem just depends on its utility function, the current state and hers endowments.

Proposition 3.2.

If is a smooth map with boundaries, then is a manifold with boundaries. If vanishes in the boundaries, then is a manifold.

Proposition 3.3.

Let and are smooth and strictly concave functions. Then for a given solution on a initial tuple the function can be extended smoothly on all the domain.

Definition 3.4.

A CFMMWD is complete if the map defined as is differentiable, injective, image and with differential inverse. So, we can define the updating price stochastic process as

| (2) |

we denote by the stochastic equilibrium price defined as a solution of

| (3) |

Counterexample: Observe that in general does not exist. For example, consider the CFMM game with and is given by . Then, clearly we have that as . Since the image of is in , we have that does not exist.

Theorem 3.5.

Let be a complete CFMMWD with and with bounded support, then exists.

Proposition 3.6.

Let be distribution of endowments, utility function with unique Walrasian equilibrium . Let be convex and differentiable function and such that . Then, it holds that the sequence of stochastic prices of the CFMMWD converge to .

3.2 Welfare and average price

We define the notion of social welfare in CFMM with Walrasian demands. We will prove that, locally, the CFMM that provides more social welfare is the constant sum market maker with price . However, globally, we will prove that this is in general not true, leaving as an open question which function optimizes the social welfare for a given set of players with endowments and utility function .

Definition 3.7.

For a CFMMWD, we define the average social welfare as

We define the average quilibrium price as

In general does not need to exist, however there are sufficiently good conditions where this term is well-defined. Before doing that, we prove that locally the bests CFMM in terms of social welfare (without subsidizing) is the constant sum market maker with price .

Proposition 3.8.

Let be an initial liquidity, a concave utility function and . Let be the set of all smooth convex functions from to . Let be the WEP of the one-shoot model with utility function and distribution . Assume that . Then,

and the curve that is realized is . So, if a distribution over and , for some , and is sufficiently big, we have that:

As we mentioned, the does not necessarily exist, however, if the Markov process associated to the CFMM has a unique stationary distribution, then this value is well-defined. Moreover, the average of utilities not just converges in expectancy but also converges almost surely to .

Proposition 3.9 (Existence of Wf).

Let be a CFMMWD and its associated Markov process. If has a unique stationary distribution , and then

Now, let’s provide an example of the computation of a for a specific game. Assume that the CFMM has constant function and initial liquidity . Assume that the representative agent has a Cobb-Douglas utility function . The distribution of endowments is given by . Each round , the agent with endowment wants to solve {maxi*}—s— Δ’(Δ_1+x)(Δ_2+y) \addConstraintR_1+R_2+x+y=R_1+R_2 \addConstraintR_1+x≥0,R_2+y≥0 Easily, we obtain that if is or , the agent will not interact with the CFMM since he is already maximizing his utility function. On the other hand, if or , if possible, the agent will execute the trade, depositing of one asset and removing of the other one. Then the reserves of the CFMM behave as the following Markov chain process:

where is the random variable with distribution, , and .

Assume that are integers and . Computing the stationary distribution , we obtain that the probability that the Markov process is in the boundary set is . By, proposition 3.9 we have that

| (4) |

Similar to 3.8 one could think that the constant sum Market Maker provides more social welfare than all others CFMM, however this is not true.

Theorem 3.10.

There exists a utility function and a distribution of endowments such that the constant sum market maker with normal vector (i.e. does not maximize welfare. In other words, there exist such that

Proposition 3.11.

For a distribution of endowments and utility function and Walrasian equilibrium price , we have that for all .

where .

Proposition 3.12.

If the Markov process associated to have a stationary distribution , then we have that the average equilibrium price holds:

Theorem 3.13.

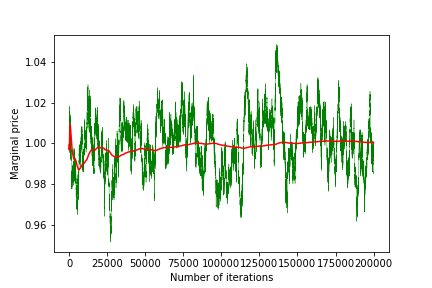

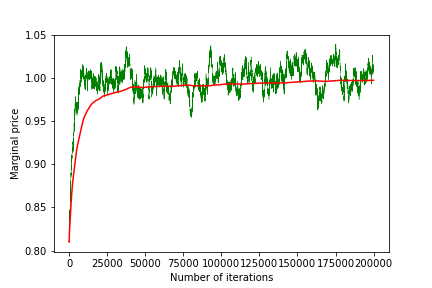

Assuming that is a convex complete CFMM an is a distribution with bounded support. Then sequence of average prices of the CFMMWD converges to . In other words, if the liquidity is sufficiently large, we have that the oracle price of the CFMM converges to the Walrasian equilibrium price.

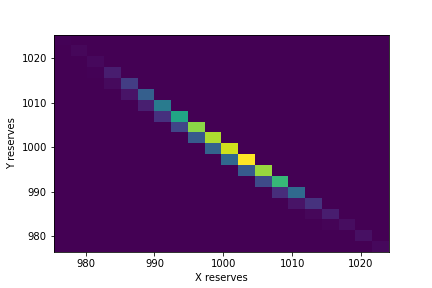

The proof of the theorem can be found in the appendix. Now, we will provide an example. Assume that players have Coubb-douglas utility function and that the distribution of endowments is given by . Then, by symmetry, one can easily prove that . We simulated the CFMM with Walrasian demand with Uniswap V2 curvature and . The initial reserves are set and respectively.

4 Maximal extractable value in exchange economy

In this section, we will try to lower bound the MEV in a Walrasian auctioneer mechanism with and without CFMM. Similar to the section 2.1, we assume that all players have a concave utility function and the endowments are drawn from a distribution . We assume that the players endowments and utility functions are truthfuly reported to the auctioneer. Assume the existence of a Walrasian auctioneer (in PBS this will be the builder) responsible for batching the transactions received and compute the Walrasian equilibrium price and the output allocations. However, due to computation limitation per period of time (gas limit in Blockchain context) the number of transactions that the builder can settle is bounded by some number . Moreover, we assume that this player share the same utility function and endowments distribution.

Now, we will lower bound the MEV that the builder can extract in different scenarios. In this context, a transaction will be a tuple . First, we will assume that there is no bribing and that the probability of a non-builder transaction being added is uniformly random. That is, if the builder received transactions, then .

Builder: In this context, the builder will be the responsible for executing the Walrasian equilibrium pricing algorithm for a given set of transactions . We will assume that the builder has the same utility function and initial endowments drawn from the distribution .

Definition 4.1.

We say that the builder is informed if he has access to the transactions (perfect signal). We say that a builder is a censorship builder if, for any given set of transactions , he can choose a subset of transactions and compute the Walrasian allocation of this subset. We say that a builder censorship-minimizer if he constructs the Walrasian allocation of any subset with maximal cardinality bounded by .

Similarly to [8], we define the MEV as an optimization problem.

Definition 4.2.

Let be the endowments of the builder and be the set of transactions received. Then, the MEV of an informed and censorship builder is: {maxi*}—s— BU(x_b(B∪{(U,Δ_b)})) \addConstraint B⊆T, —B— ≤N-1 In the case that the builder minimize censorship, the MEV is defined analogously by adding the constraint that .

In the limit cases, that is, if the number of transactions the MEV of the censorship-minimizer builder converges to the MEV of the censorship builder. Observe that in general, the MEV is greater than zero. For example, assume that we have , is the distribution that and the players have the Coubb-douglas utility function . Assume that the builder receives transactions. Two of the form and one of the form . Moreover, assume that the builder has of initial endowments. Then, if the builder adds all transactions, its final endowments are obtaining a total utility of . However, if the player censors the transaction , then his final endowments are leading to a utility of .

Proposition 4.3.

When the builder is uninformed, individually rational, and risk-averse, then they want to add as many transactions as possible in a block. More formally, an uninformed builder has non-censoring as a dominant strategy. Moreover, we have that

with following the distribution conditioned by one transaction being and being the Walrasian equilibrium. On the other hand, the expected utility of non-builder player is and so the difference between the value extracted from a builder and a non-builder players is

| (5) |

Proof.

By assumption made in preliminars, a risk averse agent will add as much transaction to reduce the risk of having a worst price than the Walrasian equilibrium price. Since, by the assumption, the agent is truthful, we have that the builder will always add its transaction and remove another one. In this case, by the assumption its expected is . ∎

The last proposition gives us a lower bound on the one block MEV in a pure exchange economy with random endowments. Similar lower bounds emerge in frequent batch auctions such as [9]. Moreover, we prove that with enough demand of exchange (that is ) the value extracted by the builder is strictly greater than the one extracted by a non-builder player. However, clearly if there is demand of exchange is because . In other words, a blockchain with unique validators per slot always have strict asymmetry of payoffs between validators and non-validators players if and only if there is sufficient demand of exchange through the chain.

4.1 MEV in CFMM

In this paper, we did not took into account the utility of the liquidity provider. Since, in general, any passive liquidity provider is weak against adverse selection. More formally, we have the following result. Let be a player with initial endowments , with utility function . There is no CFMM such that the solutions of the optimization problems:

—s— xU(x) \addConstraintc⋅x = c⋅R

—s— x-c⋅x \addConstraintC(x)=C(R)

and are have the same utility. The first optimization problem models the best response of the player if there is a referential market with price vector (the Walrasian equilibrium price). That is, the liquidity provided by the LP is significantly small compared to the one provided by the off chain market. The second optimization problem models how does the market react if the player posts a contract with initial reserves and CFMM .

Example: Assume that the constant function is and the utility of the LP is . Can we find a utility function such that the optimization problem share the same solution? Assume that the initial endowment is . Wlog, we can assume that the vector price is of the form . Then, the solution of the second optimization problem is realized in and so the utility is . On the other hand, the solution of he first optimization problem is given in and so the utility is and is strictly larger than for . Therefore, we have that an LP with utility function makes worse providing liquidity than rebalancing in the market.

Proposition 4.4.

Let be a strictly increasing concave utility function and open sets. Then, for all complete CFMM it holds for every in and initial reserves such that .

In other words, there is no CFMM that maximizes the trader’s utility and the utility of the LP providers at the same time. Or, in other words, the LP positions are always exposed to adversarial selection, even with agents with Walrasian demands.

Now, we will discuss the expected MEV generated by the CFMM. For a given CFMM with reserves . If validators’ endowments are drawn randomly from the set of endowments , then the expected MEV is . Observe that in this case, the reserves that maximize the welfare are the ones that maximize the MEV. An interesting question is which reserves (or point in the feasible set) minimizes the MEV. In presence of another off chain market maker and players that just values the non-risk asset the MEV is minimized when the marginal price of assets coincide off chain and in the CFMM (no arbitrage condition, see [2]). However, this is not true with players with Walrasian demands. More specifically, there are cases where the CFMM being in the Walrasian equilibrium price maximizes MEV but also there are games where the CFMM being in the Walrasian equilibrium price minimizes the MEV

Example: We have the same distribution of endowments as previous examples and utility function . Clearly, in this case the MEV is not minimized in reserves since taking the reserves .

5 Future Work

While in the special case of the model we analysed the MEV does not reduce social welfare, this is not in general the case. Characterising the loss in social welfare from MEV in a more general model where the validator has visibility into the content of transactions. This naturally motivates the design of variations of CFMMs that have higher social welfare. Another open problem is under what conditions does the average price of the CFMM converges to the Walrasian equilibrium and if so how does the MEV impact on the rate convergence.

References

- [1] Guillermo Angeris and Tarun Chitra “Improved price oracles: Constant function market makers” In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies, 2020, pp. 80–91

- [2] Guillermo Angeris et al. “Constant function market makers: Multi-asset trades via convex optimization” In arXiv preprint arXiv:2107.12484, 2021

- [3] Kushal Babel, Philip Daian, Mahimna Kelkar and Ari Juels “Clockwork finance: Automated analysis of economic security in smart contracts” In arXiv preprint arXiv:2109.04347, 2021

- [4] Rafael Frongillo, Nicholás Della Penna and Mark D Reid “Interpreting prediction markets: a stochastic approach” In Advances in Neural Information Processing Systems 25, 2012

- [5] Allen Hatcher “Algebraic topology”, 2005

- [6] Frederick S Hillier “Introduction to operations research”, 1967

- [7] Andreu Mas-Colell, Michael Dennis Whinston and Jerry R Green “Microeconomic theory” Oxford university press New York, 1995

- [8] Bruno Mazorra, Michael Reynolds and Vanesa Daza “Price of MEV: Towards a Game Theoretical Approach to MEV” In arXiv preprint arXiv:2208.13464, 2022

- [9] Conor McMenamin, Vanesa Daza and Matthias Fitzi “FairTraDEX: A Decentralised Exchange Preventing Value Extraction” In arXiv preprint arXiv:2202.06384, 2022

Appendix A Appendix(Work in Progress)

Proof 3.2: Clearly, we have that for all . In other words, all non-trivial elements are regular. By implicit function theorem, we have that is a manifold of dimension .

Proof 3.3 First, using Lagrangian and the implicit function theorem, we can prove that the function can be defined locally and is smooth. We can extend it globally since the maximum always exist and by continuity of the function

Proof 3.5: Let’s consider the map . Since and are continuous, we deduce that is continuous by using the convergence dominated theorem. Now, we will prove such that holds . Assume otherwise, then exist a sequence of points such that (where denotes the Euclidean distance and the frontier of the dimensional simplex). Since is compact, wlog we can assume that for some and that and for some and (taking subsequences). Since , we deduce that . However, since the support of the endowments is finite, we have that (is deduced from the fact that if is complete). But if , we would deduce that , leading to a contradiction. Therefore, exist such that . Since , using the Brouwer theorem [5], we have that exist such that .

Proof 3.6 Since the Walrasian equilibrium of the pure exchange economy is unique, we have that is enough to show that . Since the map is continuous, we have that . On the other hand, since , we have that uniformly at . So,

Proof 3.8 Clearly, using that we have that if then . Moreover, the feasible set associated to with reserves is . Now, We have to prove that . If we denote by the feasible set induced by . we have that . This holds from the fact that and is concave. By the upper bound constraints on , we have that holds all the optimization problem constraints and therefore we deduce the result. The second part is deduced immediately by taking expectancies.

Proof 3.9: If has a stationary distribution, then, since is bounded, we deduce it by the large law of numbers, for more details see [6].

Proof 3.10: Take Utility function . Assume endowments hold the distribution defined as . Let be the stationary distribution followed by the Markov process . Observe that in this CFMMWD, the utility of the player after the trade is bounded by . Therefore, we have that

where . Observe that

Now, we will prove that there exist a such that the CFMMWD holds for some . Take the constant product market maker . Now, for an endowment, we can compute the best trade. Assume that the current reserves of the CFMM are . The player will trade a quantity such that maximizes where . Computing it, we have that . On the other hand, the distribution of the reserves is uniquely determineted for the reserves . One can prove that exist and such that for and for . Therefore, we deduce that exits and is finite, deducing the result.

Proof 3.11: The proof is deduced from the fact that the probability of being in the border tends to zero as tends to infinity and the proposition 3.9.

Proof 3.13:

Lemma A.1.

Let be a sequence of CFMM with Walrasian demand with with . Assume that the support of the endowments is bounded. Then:

-

1.

is Ergodic for all , and so, we can consider the stationary distribution .

-

2.

Let be the state space of and closed set, then .

Proof.

-

1.

Since is compact, we have that every collection of measures are tight. Moreover, the Markov operator associated to the Markov process is Feller. Therefore, the statement is deduced by the Krylov-Bogolioubov theorem.

-

2.

This is equivalent to proof that positive random walks with negative drift have a stationary distribution. Since, we can approximate the Markov chain by sufficiently closer Markov chains.

The theorem then is deduced from approximating the CFMM by piece-wise linear CFMM and proving that the probability that the point is in the piece with price is zero. ∎

Proof 4.4: Let be the initial reserves of the CFMM. Take such that . Let be the reserves after the trade . Taking Lagrangian, we can show that . Since is convex, we have that

Since , we have that . Therefore, we deduce that there exist such that . Now we will proof that . Assume that , then we would have that . Since is concave, we have that the set is convex and so the line is tangent. This implies that , leading to a contradiction, therefore . Since is strictly increasing, we have that . On the other hand, holds the constraints of the first optimization problem, therefore, .