Generalizing distribution of partial rewards for multi-armed bandits with temporally-partitioned rewards

Abstract.

We investigate the Multi-Armed Bandit problem with Temporally-Partitioned Rewards (TP-MAB) setting in this paper. In the TP-MAB setting, an agent will receive subsets of the reward over multiple rounds rather than the entire reward for the arm all at once. In this paper, we introduce a general formulation of how an arm’s cumulative reward is distributed across several rounds, called -spread property. Such a generalization is needed to be able to handle partitioned rewards in which the maximum reward per round is not distributed uniformly across rounds. We derive a lower bound on the TP-MAB problem under the assumption that -spread holds. Moreover, we provide an algorithm TP-UCB-FR-G, which uses the -spread property to improve the regret upper bound in some scenarios. By generalizing how the cumulative reward is distributed, this setting is applicable in a broader range of applications.

reward Delayed feedback Distributed cumulative reward

1. Introduction

The multi-armed bandit (MAB) is a framework within reinforcement learning to model sequential decision-making. In the classic MAB problem, an agent is faced with a finite set of different actions, known as arms. At each point in time, the agent selects one arm and, after pulling it, observes a reward from that arm. The reward is drawn from an arm-specific probability distribution, which is initially unknown to the agent. Given a finite number of rounds, the agent faces a trade-off between the exploitation of the arm with the highest expected reward and exploration to learn more about the expected rewards of the other arms. The objective of the agent is to accumulate as much reward as possible over rounds. The sum of the rewards collected over rounds is commonly referred to as a cumulative reward. To maximize the cumulative reward, the agent must minimize total regret. The total regret is the expected regret of not pulling the best arm.

Multi-arm bandit literature typically focuses on scenarios where the rewards are assumed to arrive immediately after performing an action. However, in many real-world scenarios, there is a delay between the execution of an action and the observation of its reward. This has been studied in classical delayed-feedback bandits [6, 7, 8]. In those studies, the reward is assumed to be concentrated in a single round that is delayed. This setting can be expanded by allowing the reward to be partitioned into partial rewards that are observed with different delays. This type of bandit problem, known as MAB with Temporally-Partitioned Rewards (TP-MAB), was introduced in a paper by Romano et al. [(2022)].

In the TP-MAB setting, the reward from an arm is distributed over multiple rounds. This means that instead of receiving the entire reward for the arm at once, an agent will receive subsets of the reward over multiple rounds. The per-round reward is defined as the partial reward observed by the agent in a single round. It is assumed that the per-round reward is the realization of a random variable with an unknown probability distribution. The cumulative reward of an arm is the sum of all the per-round rewards obtained by pulling an arm. The maximum delay until receiving the cumulative reward of an arm is assumed to be finite.

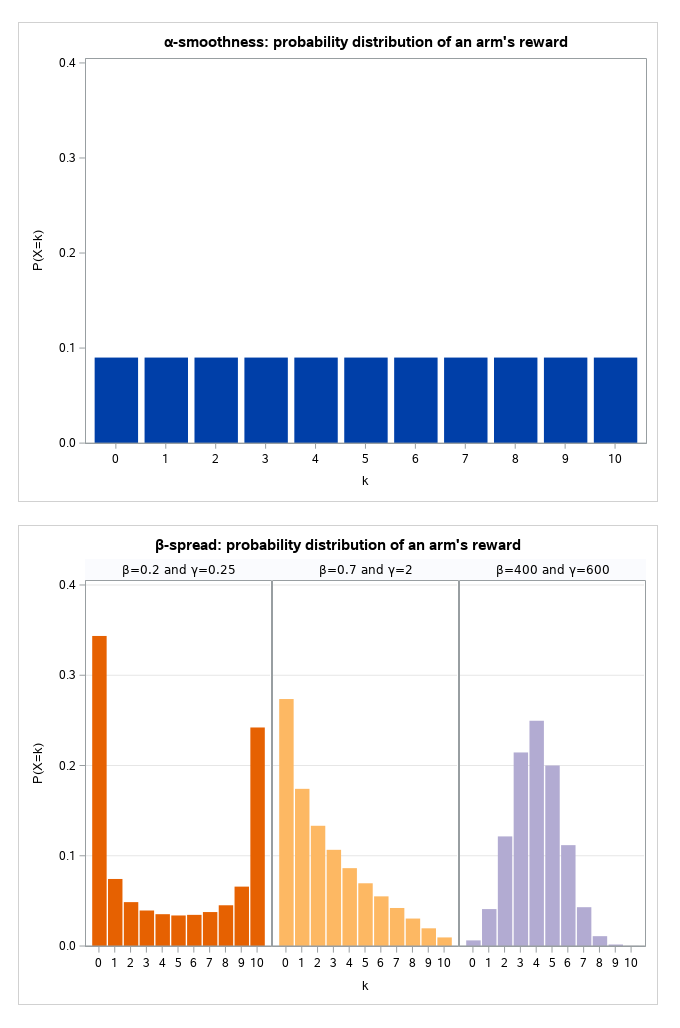

Romano et al. [(2022)] present -smoothness, a property that defines how an arm’s cumulative reward is distributed across several rounds. This property examines the reward seen across a group of rounds. If the -smoothness holds, the total reward seen in this group cannot be greater than a fraction of an arm’s maximum cumulative reward. The fraction is determined by the value of . The total cumulative reward divided by is the maximum total reward observed in a group of rounds.

Consider the following example to demonstrate -smoothness further. An agent needs to sell a certain product and is given a range of possible prices for that specific product. The agent should select a price, which corresponds to pulling an arm, to sell the product in the following month in a specific affiliate. The selected time horizon to sell the items is set to 30 days, and one round is equal to 1 day. Assume there are 300 items with a fixed price of three euros. The total cumulative reward is 900 euros. If no assumptions are made about how the whole reward will be distributed across the rounds, it is possible that all products may be sold on the final day. As a result, the setting is identical to the classic delayed feedback setting. According to Romano et al. [(2022)], it is not possible to construct algorithms with regret upper bounds that are better than those of the algorithms for the delayed-feedback situation.

To be able to construct better regret bounds, Romano et al. [(2022)] make an assumption that -smoothness holds. In the example described above, the group size might be set to five days, the -smoothness property will specify the maximum reward that may be observed in those five days. If we set to 6, then the total reward which can maximum received in 5 days is 150 euros. By assuming -smoothness with , the scenario in which an arm’s whole reward is obtained in the last round is not possible anymore. By characterizing the reward structure, Romano et al. [(2022)] succeed in providing algorithms that provide better asymptotic regret upper bounds than delayed-feedback bandit algorithms.

The -smoothness property states that the maximum reward in a group of consecutive rewards cannot exceed a fraction of the maximum reward. However, in many scenarios, there might be additional information available about how the cumulative reward is spread over the rounds. For example, the majority of the cumulative reward is observed in the first rounds, and the observed partial reward declines exponentially after that. The assumption of -smoothness does not fit well if the cumulative reward is not uniformly spread. This paper will introduce a more generalized way of formulating how an arm’s cumulative reward is distributed across several rounds. The scenarios where the cumulative reward is not uniformly spread over the rounds will be investigated. This will be studied by allowing the cumulative reward spread to be any function, such as a curve.

A motivating application could be on websites that provide Massive Open Online Courses (MOOCs). The most well-known MOOC providers are Coursera, Udacity, the Khan Academy, and edX. MOOC providers want to be able to provide students with useful recommendations for courses. This problem can be modeled as a TP-MAP problem. A course, which consists of a series of video lectures, might be thought of as an arm. A course can be recommended to a student by an agent, which corresponds to pulling an arm. When the student follows a course, the agent can observe partial rewards (e.g. by asking for a course rate or by checking the watch time retention). The cumulative reward is the sum of rewards from all video lectures in a course. If the -smoothness holds, the total reward observed in a collection of video lectures cannot be more than a fraction of the maximum cumulative reward of the course. However, many students watch the video lectures at the beginning of a course but never get to the course’s last few video lectures. As a result, the assumption of the -smoothness property does not really fit in such a case. Therefore, it might be interesting to investigate a more generalized way of formulating how an arm’s cumulative reward is distributed across several rounds.

The key contribution of this work is that it provides a more generalized way of describing how an arm’s cumulative reward is distributed across rounds. We introduce the -spread property to replace the -smoothness property.

We also propose an algorithm TP-UCB-FR-G that uses this new property. Similarly, tighter upper bounds can be achieved for this algorithm compared to TP-UCB-FR (Romano et al., 2022) under certain assumed distributions.

2. Background and Related Work

The classical multi-armed bandits (MAB) problem is the formulation of the exploitation-exploration dilemma inherent to reinforcement learning (Bubeck and Cesa-Bianchi, 2012a). In this problem, the learner has to choose between different actions (also called by arms). A choice is made in every round and is represented by pulling one of the arms. The successive plays of an arm are independent and identically distributed (Auer et al., 2002). We assume that reward for an arm is drawn from an unknown distribution on with mean . Regret is defined as the expected loss, due to the fact that a policy is not making the optimal choice. The regret function of an algorithm A after time steps is defined as follows (Auer et al., 2002):

The goal of algorithm A is to make sure that the received reward will be maximized and therefore minimize the regret function. To make sure this is achieved, it is important for a policy to make sure it explores potentially better arms but also exploits the currently known good choices.

Knowing this goal, the arms can be chosen optimistically via the Upper Confidence Index.

Based on this idea, Auer et al. [(2002)] proposed an algorithm called Upper Confidence Bound (UCB1) and proved that it has logarithmic regret.

The UCB1 algorithm (Auer et al., 2002) can be extended to work with delayed rewards. The seminal work of Joulani et al. [(2013)] proposes the concept of a partial monitoring setting, covering all previous, less general, work regarding feedback delays. In the delayed model, feedback on a decision made in timestep will be received at time step after the decision is made. The number of delayed time steps is denoted by . Note that using corresponds to the non-delayed model with instant feedback.

However, in real-world applications, it is common that the rewards that are received from pulling an arm are spread over an interval. These rewards are convoluted with each other (Wang et al., 2021). Underestimating the intervals leads to no theoretical result, and overestimating results in a worse performance (Wang et al., 2021). Past solutions required knowledge about the delay of the reward, which results in a non-anonymous setting (Joulani et al., 2013). This is not realistic, so Wang et al. [(2021)] demonstrated a method to establish an upper regret bound for the algorithm they use, removing the need for prior knowledge.

Romano et al. [(2022)] introduce a novel bandit setting, namely Multi-Armed Bandit with Temporally-Partitioned Rewards (TP-MAB). In this setting, a stochastic reward that is received by pulling an arm is partitioned over a finite number of rounds followed by the pull. In this study, two algorithms were designed: TP-UCB-FR and TP-UCB-EW. Both algorithms that were introduced used temporally spaced rewards, and it is shown that the upper regret bound for these two algorithms is respectively and , for TP-UCB-FR and TP-UCB-EW (Romano et al., 2022). TP-UCB-FR is an algorithm that uses UCB and Fictitious Realizations. In addition, this algorithm uses an -property that is defined by the researchers. At each point in time the agent pulls an arm . Subsequently, at each round the agent received a per-round reward . It is known to the agent which arm pull produced this reward. The time span over which the reward is partitioned is denoted by . In the definition of -smoothness, the value of is considered to be a factor of , thus . The random variable corresponds to the total reward the agent has observed for pulling arm at time , over the duration of consecutive rounds in group . The group index denotes rounds of observations that have already passed. It is defined as the sum of per-round rewards. .

The value of lies between 1 and , thus . Romano et al. [(2022)] define -smoothness as follows:

Definition 2.0.

(-smoothness) For , the reward is -smooth iff with and for each the random variables are independent and s.t. .

Because of the use of this specific property, there is no general function that can work in a broader variety of settings. As a remedy, we propose to use general distributions that can more accurately characterize how the received reward is partitioned. An example is a Beta-Binomial distribution. This probability distribution uses two parameters to determine its shape, and this can be implemented such that it determines the distribution of a received reward over time. Examples of this distribution can be seen in figure 1. Other discrete distributions over a finite domain can also be used, such as binomial distributions.

3. Problem Formulation

Consider a MAB problem with arms over a time horizon of rounds, where . At every round an arm is pulled. Unlike the delayed-reward bandit problem, the total reward is temporally partitioned over the set of rounds . Let denote the partitioned reward that the learner receives at round , after pulling the arm at round . The cumulative reward is completely collected by the learner at round . Each per-round reward is represented as the realization of a random variable with support 111Without loss of generality, we assume that the per-round rewards , and trivially, the same condition holds for the cumulative reward over rounds (). The cumulative reward collected by the learner from pulling arm at round is denoted by and it is the realisation of a random variable such that with support . Straightforwardly, we observe that .

Romano et al. [(2022)] have shown that, in practice, per-round rewards for an arm provide information on the cumulative reward of the arm. The authors introduce an -smoothness property that partitions the temporally-spaced rewards such that each partition corresponds to the sum of a set of consecutive per-round rewards. Formally, let be such that is a factor of . The cardinality of each partition, which we shall name ‘z-group’ from now on, is denoted by with . Similar to above, we can now define each z-group as the realisation of a random variable such that for every :

| (1) |

Finally, we note that has support . We can distinguish two cases when considering extreme values of :

-

(1)

Case: : All temporally-spaced rewards are placed in a single z-group over a time horizon.

-

(2)

Case: : The number of z-groups equals the number of temporally-spaced rewards over a time horizon.

The regret of any uniformly efficient policy applied to the assumption-free TP-MAB problem has a lower bound of (Romano et al., 2022):

| (2) |

In Romano et al. [(2022)], the authors manage to tighten this lower bound by assuming -smoothness. The attained bound is given by:

| (3) |

The -smoothness property ensures that all temporally-partitioned rewards contribute towards bounding the values of future rewards within the same window.

If the -smoothness holds, then the maximum cumulative reward in a z-group is equal for all z-groups . Therefore, we can say that , .

However, the assumption of -smoothness does not fit well if the cumulative reward is not evenly distributed across rounds. The goal of this paper is to generalize the spread of the rewards across z-groups.

To accomplish this, it should be investigated whether -smoothness can be replaced with a property that allows for the modeling of scenarios in which the cumulative reward is not distributed uniformly across rounds. In other words, we want to eliminate the assumption that every z-group has an equal probability of attaining a partial reward. Thus, we want to define a property that allows to differ across z-groups .

4. Solution approach: -spread property

The goal of this paper is to eliminate the assumption that every z-group has an equal probability of attaining a partial reward. Instead, the probability of partial reward occurring in a specific z-group will be represented by a discrete function over all possible values that gives probabilities to partial rewards being obtained in z-group for all . We introduce an arbitrary discrete probability distribution to describe the shape of this function. More formally:

Definition 4.0 (-spread).

Given a set of values with corresponding z-groups for every arm , and an arbitrary discrete probability distribution with a finite domain of size , -spread is defined as the set of weights such that for each , a unique corresponding weight exists. Let us define a random variable .

The probability of a partial reward being observed in a specific z-group is formalized by any arbitrary probability distribution of choice. For each reward point, the value of determines the z-group in which it is observed. As a result, every z-group can now contain a different amount of the maximum partial reward. Let be the probability mass function of the chosen distribution . We define the new upper bounds for the z-groups for every as:

| (4) |

Using this result, we can revise the original lower bound attained by Romano et al. [(2022)], as stated in Theorem 4.1.

Theorem 4.2.

The regret of any uniformly efficient policy applied to the TP-MAB problem with the -spread property is bounded from below by:

| (5) | ||||

Note that this lower bound resolves to the lower bound of (3) in case of -smoothness. The lower bound for the -spread setting is lower than the one in the -smoothness setting when

The lower bound is higher in the case this value exceeds 1. The proof of this theorem is given in the next section.

4.1. -spread regret lower bound

Proof.

Theorem 2.2 in the work by Bubeck and Cesa-Bianchi [(2012b)] gives the framework for this proof. We extend the version by Romano et al. [(2022)] by considering that, as the -spread property does not modify the cardinality of the z-groups, we can generalize to a setting where multiple rewards are earned by a single arm pull.

Let us define an auxiliary TP-MAB setting where:

-

•

only two arms exist with expected values and s.t. ¡ ¡ 1

-

•

upper bound on the reward for each arm is equal to the maximum upper bound, i.e.

-

•

The total rewards in each z-group, , are independent and the expected value of the rewards in each z-group is .

-

•

Total reward in z-group, , is a scaled Bernoulli random variable s.t.

-

•

Pulling an arm at time provides rewards that can all be observed immediately at the time of the pull.

In this proof of the lower bound, we trivially observe that finding the optimal arm in a setting in which all of the partial rewards are observed at once can never be more difficult than in a setting in which rewards are spread out over a set of rounds . Therefore, a lower bound in this defined setting gives a lower bound in our -spread setting.

To give an idea of how good an arm is compared to its maximum, we derive a new alternative mean for each arm as . Note that as mentioned before.

Let denote the expected number of times an arm is pulled over a set of rounds . To compute and , we can use the scaled reward values without loss of validity.

If we now consider a second, modified instance of the above TP-MAB setting, with the only difference being that arm 2 is now the optimal arm s.t. , we can show that the forecaster choosing the arms cannot distinguish between the different instances. This reasoning implies a lower bound on the number of times a sub-optimal arm is played. We know that is a continuous function and we can find a for each , such that:

| (6) |

The proof follows the steps given in the work by Bubeck and Cesa-Bianchi [(2012b)] to derive a lower bound for any uniform policy .

Step 1:

For this proof, we change the notation of the rewards slightly such that each variable in the sequence represents the cumulative reward of an arm when pulled times, at timestep and thus for represents the cumulative reward of an arm after the ’th pull at timestep . Using this notation, we can define the empirical estimate of as:

| (7) |

Using this, we define an event that links the behaviour of the original agent to the modified version

| (8) |

with

| (9) |

Using the change of measure identity defined in Bubeck and Cesa-Bianchi [(2012b)] and the second inequality in :

| (10) |

For the next step we use the fact that , Markov’s inequality and the fact that the policy is uniformly efficient (i.e. with ).

| (11) |

| (12) |

Step 2:

Again using Theorem 2.2 from Bubeck and Cesa-Bianchi [(2012b)] and observing that we always have:

-

(1)

-

(2)

-

(3)

we obtain:

Using the strong law of large numbers for the event s.t. , we conclude that , and that for we have .

Final step: deriving the lower bound

Using Equation (6) we know that, for :

where the theorem statement follows from the arbitrarity of the value of (Romano et al., 2022), substituting with and with , and summing over all the suboptimal arms.

∎

5. Algorithm for the -spread TP-MAB setting

In this section, we propose an algorithm that makes use of the -spread property in the TP-MAB setting. TP-UCB-FR-G is an extension of the algorithm TP-UCB-FR found in Romano et al. [(2022)].

5.1. TP-UCB-FR-G

The Generalised Temporally-Partitioned reward UCB with Fictitious Realisations algorithm (see algorithm 1) is based on the notion of Fictitious Rewards. With a data distribution function as input, the algorithm is able to give a proper judgment of an arm before all the delayed partial rewards are observed.

As detailed in Romano et al. [(2022)] this is realized by replacing the not yet received partial rewards with fictitious realizations, or in other words, the expected estimated rewards.

At round , the fictitious reward vectors are associated to each arm pulled in the span . These fictitious rewards are denoted by with , where , if (the reward has already been seen), and , if (the reward will be seen in the future). The corresponding fictitious cumulative reward is .

As input, the algorithm takes a smoothness constant , a maximum delay and a distribution function . The algorithm consists of two phases; the initialization phase, starting in line 2, and the loop phase, starting in line 5. In the initialization phase, each arm is pulled once. After that, the loop phase starts, where at each round , the Upper Confidence Bounds are determined for each arm by computing the estimated expected reward and confidence interval , detailed in 5.1. The algorithm then pulls the arm with the highest Upper Confidence Bound and observes its rewards.

The estimated expected reward is calculated as in Romano et al. [(2022)].

| (13) |

where is the number of times arm has been pulled by the policy up to round .

The confidence term is calculated as:

| (14) |

Theorem 5.1.

In the TP-MAB setting with -spread reward, the pseudo-regret of TP-UCB-FR-G after rounds is:

| (15) | ||||

Observe that , meaning the expected value of our random spread variable influences the upper bound of the algorithm. Another interesting factor is . This factor can be seen as an approximation of the ‘Index of Coincidence’ between rewards. This determines the probability of two reward points being observed in the same z-group. Its minimal value equals and occurs when the -smoothness property holds (uniform distribution). The value is maximal and equal to 1 if all rewards fall into one z-group. Friedman [(1987)] introduced the ‘Index of Coincidence’ to analyse the distribution of letters in cipher texts in order to find patterns that could help to decipher them.

Let us also analyse the resulting upper bound by comparing it to the upper bound found by Romano et al. [(2022)]. in case of -smoothness. For any other with the upper bound on the regret is lower and when , the upper bound is higher. The ‘Index of Coincidence’ with -smoothness equals its minimal value . Hence, using any other non-uniform distribution will result in a higher ‘Index of Coincidence’ and higher regret. This means that choosing a -spread distribution with a low mean and a high coincidence index will result in a better upper bound compared to choosing with rewards centered towards the end (high mean) and not spread out (high coincidence index). Let us continue by proving the theorem.

5.2. -spread regret upper bound

Proof.

The target of this proof is to derive an upper bound on the expected amount of regret for the algorithm. The approach can be divided into four steps. The first section contains a range of facts that are required for the proof. In the second section, the upper bound on the algorithm is derived by determining an upper bound on the sub-optimal arm pulls . This process consists of three steps:

-

(1)

First, we show that the probability that an optimal arm is estimated significantly lower than its mean is bounded by

-

(2)

Secondly, we show the probability of a sub-optimal arm being estimated significantly higher than its mean is bounded by

-

(3)

Finally, we evaluate how the algorithm performs in distinguishing the difference between the optimal and sub-optimal means.

These bounds and facts in the preliminary provide enough information to prove that the theorem holds.

5.2.1. Preliminaries

The relation between the expected amount of sub-optimal arm pulls and the regret of the algorithm is given by:

| (16) |

Let us define the true empirical mean of the cumulative reward of arm computed over arm pulls:

| (17) |

The value above assumes that it is known what the cumulative reward of an arm pull is, even if partial rewards are technically still to come in the future. We bound the difference between the true empirical mean and the observed empirical mean as follows:

| (18) |

| (19) |

| (20) |

| (21) |

Step (19) states that the difference between the true and observed mean comes from all future rewards that are yet to be observed for a maximum of arms that have been pulled. The closer to , the more pulled arms with yet-to-be-observed rewards exist. Therefore, this amount can be bounded by looping over all z-groups in (20) to calculate the maximum reward still to be observed and giving higher weight to late z-groups through index . Furthermore, (20) holds because of the -spread property.

The Chernoff-Hoeffding bound (version of Fact 1 in Auer et al. [(2002)]) is defined as follows: Let be random variables with common range such that . Let . Then, for all

| (22) |

5.2.2. Deriving the upper bound

For more detail, this section of the proof can also be found in the appendix with more sub-steps.

In line with the proof from Auer et al. (2002), the bound of expected sub-optimal arm pulls is bounded using the following summations:

| (23) |

where and are the empirical mean and the confidence term of the optimal arm as computed in the algorithm TP-UCB-FR-G, respectively. The represents the number of times the arm was pulled up to . and denote the empirical means and confidence terms for sub-optimal arms.

For (23) to hold, one of the following three inequalities have to hold as well (Auer et al., 2002):

| (27) |

| (28) |

| (29) |

| (30) |

where we used Hoeffding’s inequality (defined in step (22)) in step (30) and defined

In a similar way, the bound from (25) can be derived:

| (31) |

| (32) |

where we use the fact that by definition . All that is left to do is to derive a bound on the probability of (26). Let us assume that the following holds:

| (33) |

| (34) |

we can rewrite this, see (50) for more details, which gives us:

| (35) | ||||

Therefore, we pick such that:

| (36) | ||||

which makes sure that for the inequality in step (26) is always false. The last couple of steps are similar to the final steps in Romano et al. [(2022)] and theorem 1 of Auer et al. [(2002)]. We get:

| (37) | ||||

| (38) | ||||

| (39) | ||||

The theorem statement follows by the fact that

.

∎

6. Conclusions

In the TP-MAB setting, an agent will receive subsets of the reward over multiple rounds rather than the entire reward for the arm all at once. The reward structure must be characterized in order to provide algorithms with better asymptotic regret upper bounds than delayed-feedback bandit algorithms. Previous work introduced the -smoothness property to characterize the reward structure. The -smoothness property states that the maximum reward in a group of consecutive rewards cannot exceed a fraction of the maximum reward. However, if the cumulative reward of an arm is not distributed uniformly across rounds, the assumption of -smoothness does not fit well.

This paper introduces the -spread property, which provides a more generalized way to characterize the reward structure. In the -spread property, a probability mass function of any distribution is used to determine the maximum reward that can be obtained in a group of consecutive rounds. Depending on the scenario being modeled, the probability mass function can be defined as any distribution, such as a beta-binomial distribution. The maximum reward that can be obtained in group , which consists of rounds, is determined by multiplying the probability by the total cumulative reward of an arm. As a result, the -spread property can be used to model scenarios in which the maximum reward in a series of consecutive rewards varies between groups.

This paper presents the TP-UCB-FR-G algorithm for the TP-MAB setting, which exploits the -spread property. The upper bound for the TP-UCB-FR-G algorithm is , as proved in this paper. It was also demonstrated in this paper that when the -smoothness property is replaced by -spread, the upper regret bound can be reduced compared to the algorithm TP-UCB-FR of Romano et al. [(2022)] in case of certain distribution assumptions: distributions with low and low ‘Index of Coincidence’. In worse scenarios (high and index), the nature of the reward distribution forces the algorithm to have a higher upper bound on regret.

The -spread gives a significant advantage since it generalizes how the total cumulative award is assumed to be distributed across several rounds. Based on prior information about how the cumulative reward is distributed over the rounds, the probability distribution used in the -spread property can be determined. Consider a scenario in which the majority of the cumulative reward is observed in the first rounds, and the observed partial reward declines exponentially after that. Then we can incorporate this into the model by specifying a probability mass function that best fits this scenario.

Currently, the -spread property assumes that the total cumulative reward of an arm is distributed over groups, each consisting of rounds. In other words, the arbitrary probability distribution in the -spread is assumed to have a finite domain of size . Future research could look into whether it is possible to eliminate this assumption. It may be worthwhile to investigate how to replace the -value with a certain distribution rather than a constant value. Another potential future research topic related to the -value is to assign different -values to each arm, rather than having the same value assigned to each arm. Or one could look at having a completely different distribution per arm.

Moreover, future research could look at the maximum time span over which the reward is partitioned, denoted by . Currently, the assumption is that is fixed and consistent across arms. However, depending on the application, the maximum time span may differ depending on the arm being pulled. Therefore, future research could look into a setting that allows to set a different for each arm. Furthermore, while the is currently assumed to be finite, it may be interesting to see what happens if this assumption is removed. This paper made an effort to generalize the distribution of partial rewards the TP-MAB setting, but more research is needed to address the assumptions made. Finally, future work may involve analysing the exact impact and correlation of and the coincidence index on the regret upper bound of the algorithm TP-UCB-FR-G.

References

- (1)

- Auer et al. (2002) Peter Auer, Nicolò Cesa-Bianchi, and Paul Fischer. 2002. Finite-time Analysis of the Multiarmed Bandit Problem. Machine Learning 2002 47:2 47 (5 2002), 235–256. Issue 2. https://doi.org/10.1023/A:1013689704352

- Bubeck and Cesa-Bianchi (2012a) Sébastien Bubeck and Nicolò Cesa-Bianchi. 2012a. Regret Analysis of Stochastic and Nonstochastic Multi-armed Bandit Problems. Foundations and Trends in Machine Learning 5, 1 (2012), 1–122. https://doi.org/10.1561/2200000024

- Bubeck and Cesa-Bianchi (2012b) Sébastien Bubeck and Nicolò Cesa-Bianchi. 2012b. Regret Analysis of Stochastic and Nonstochastic Multi-armed Bandit Problems. CoRR abs/1204.5721 (2012). arXiv:1204.5721 http://arxiv.org/abs/1204.5721

- Friedman (1987) William Frederick Friedman. 1987. The index of coincidence and its applications in cryptanalysis. Vol. 49. Aegean Park Press California.

- Joulani et al. (2013) Pooria Joulani, András György, and Csaba Szepesvári. 2013. Online Learning under Delayed Feedback. (2013). https://doi.org/10.48550/arXiv.1306.0686

- Mandel et al. (2015) Travis Mandel, Yun-En Liu, Emma Brunskill, and Zoran Popović. 2015. The queue method: Handling delay, heuristics, prior data, and evaluation in bandits. In Twenty-Ninth AAAI Conference on Artificial Intelligence.

- Pike-Burke et al. (2018) Ciara Pike-Burke, Shipra Agrawal, Csaba Szepesvari, and Steffen Grunewalder. 2018. Bandits with delayed, aggregated anonymous feedback. In International Conference on Machine Learning. PMLR, 4105–4113.

- Romano et al. (2022) Giulia Romano, Andrea Agostini, Francesco Trovò, Nicola Gatti, and Marcello Restelli. 2022. Multi-Armed Bandit Problem with Temporally-Partitioned Rewards: When Partial Feedback Counts. (2022). https://trovo.faculty.polimi.it/01papers/romano2022multi.pdf.

- Wang et al. (2021) Siwei Wang, Haoyun Wang, and Longbo Huang. 2021. Adaptive Algorithms for Multi-armed Bandit with Composite and Anonymous Feedback. (2021). www.aaai.org

Appendix A Proofs

Theorem 15: Deriving the upper bound

Proof.

In line with the proof from Auer et al. [(2002)], the bound of expected sub-optimal arm pulls is bounded using the following summations:

| (40) |

where and are the empirical mean and the confidence term of the optimal arm as computed in the algorithm TP-UCB-FR-G, respectively. The represents the number of times the arm was pulled up to . and denote the empirical means and confidence terms for sub-optimal arms.

For (40) to hold, one of the following three inequalities have to hold as well (Auer et al., 2002):

| (44) |

| (45) |

| (46) |

| (47) |

where we used Hoeffding’s inequality (defined in step (22)) in step (47) and defined

In a similar way, the bound from (42) can be derived:

| (48) |

| (49) |

where we use that fact that by definition . All that is left to do is to derive a bound on the probability of (43). Let us assume that the following holds:

| (50) |

| (51) |

| (52) |

| (53) |

| (54) |

| (55) |

| (56) |

| (57) |

Therefore we pick such that:

| (58) |

which makes sure that for the inequality in step (43) is always false. The last couple of steps are similar to the final steps in Romano et al and theorem 1 of Auer et al. We get:

| (59) | ||||

| (60) |

| (61) |

The theorem statement follows by the fact that .

∎