-

\thm@headsep

5plusminus\@begintheorem[]\xpatchcmd\cref@thmnoarg

Stressing Dynamic Loss Models

Abstract

Stress testing, and in particular, reverse stress testing, is a prominent exercise in risk management practice. Reverse stress testing, in contrast to (forward) stress testing, aims to find an alternative but plausible model such that under that alternative model, specific adverse stresses (i.e. constraints) are satisfied. Here, we propose a reverse stress testing framework for dynamic models. Specifically, we consider a compound Poisson process over a finite time horizon and stresses composed of expected values of functions applied to the process at the terminal time. We then define the stressed model as the probability measure under which the process satisfies the constraints and which minimizes the Kullback-Leibler divergence to the reference compound Poisson model.

We solve this optimization problem, prove existence and uniqueness of the stressed probability measure, and provide a characterization of the Radon-Nikodym derivative from the reference model to the stressed model. We find that under the stressed measure, the intensity and the severity distribution of the process depend on time and state, and hence the stressed model is not a compound Poisson process. We illustrate the dynamic stress testing by considering stresses on VaR and both VaR and CVaR jointly and provide illustrations of how the stochastic process is altered under these stresses. We generalize the framework to multivariate compound Poisson processes and stresses at times other than the terminal time. We illustrate the applicability of our framework by considering “what if” scenarios, where we answer the question: What is the severity of a stress on a portfolio component at an earlier time such that the aggregate portfolio exceeds a risk threshold at the terminal time? Furthermore, for general constraints, we propose an algorithm to simulate sample paths under the stressed measure, thus allowing to compare the effects of stresses on the dynamics of the process.

Keywords— Reverse Stress Testing, Compound Poisson Processes, KL divergence, Value-at-Risk, Conditional Value-at-Risk

1 Introduction

Since the 2007-08 financial crisis, there has been an increased focus in the insurance and financial sector on modelling and assessing rare but extreme events. Stress testing, which examines a model or system under extreme but realistic scenarios, has become a key aspect of risk management at financial institutions, as well as a vital tool for regulators [4]. In light of the regulatory requirements on stress testing, a large portion of the literature on stress testing is concerned with constructing plausible but adverse scenarios that result in a substantial stress on the model, see e.g., [6] and [22]. For example, [20] develop, in the context of solvency requirements, a stress testing methodology that provides multivariate adverse scenarios via the notion of a “least solvency likely event”. [15] construct non-parametrically the most likely scenarios that lead to losses exceeding a prespecified risk threshold. Connecting to systemic risk, [8] utilize vine copulas to perform stress tests to investigate systemic risk and contagion in financial networks. In an application to credit risk, [10] consider multi-period adverse scenarios whose plausibility is measured via the Mahalanobis distance of risk factors changes. [9] highlight the difficulty of choosing realistic but dangerous scenarios, which are essential for reliable stress tests. We also refer to [2] for a treatment of stress testing from a regulatory point of view.

An alternative approach to stress testing – sometimes termed reverse stress testing – is to first define an adverse or stressed state of the world, and then characterize the probability distribution leading to it, instead of defining a stress and searching for the corresponding adverse scenario. Fundamental to this framework is (a) the specification of stresses or probabilistic constraints and (b) solving an optimization problem to find the probability measure under which the model satisfies the stresses and is “close” to a reference probability measure. One key advantage of reverse stress testing is that it provides the entire stressed probabilistic model, allowing for a comparison of the stressed model with the reference model. In a discrete and static setting, [11] use the -divergence to incorporate constraints on events, which they term “views”, while [19] consider the -divergence and a constraint on the expected value of a risk factor. For general but static models, [25] and [24] consider stresses defined via changes in risk measures such as Value-at-Risk (VaR), distortion risk measures, and expected utilities, using the Kullback-Leibler (KL) and the Wasserstein distance, respectively.

While all the aforementioned works consider static settings, and thus do not capture the potential impact of a stress cascading through time, [10] and [5] highlight the need for understanding the effect of stress testing dynamic models. Indeed, in a plethora of settings the time-development of an insurance or financial portfolios’ profit and loss (P&L) is of interest, and thus also its evolution under adverse stresses. Examples in actuarial science include claims reserving ([21]), variable annuities which rely on accurate dynamic mortality models ([3]), optimal pension accumulation and withdrawal ([14]), and valuation and hedging of insurance risks ([13]). In all these examples, the key interest lies in the dynamics of the (stressed) P&L. Moreover, quantifying the stressed dynamics of extreme losses allows for adequate risk assessment and management interventions, see e.g., [21] for a detailed discussion.

The literature on stress testing in a dynamic setting, however, is limited with [10] and [5], who construct adverse scenarios in a multi-period and thus discrete-time setting within a credit risk context. As such, a comprehensive treatment of stress testing for dynamic loss models in continuous-time is missing. We fill this gap by developing a (reverse) stress testing approach for compound Poisson processes in a continuous-time setting, which allows for multiple stresses on portfolio components, stresses at terminal and earlier time points, and provide an algorithm that allows to simulate under the stressed probability measure. While the starting point is a compound Poisson process, we allow the stressed dynamics to fall in the class of stochastic processes with state dependent intensity and state dependent severity distributions. A key advantage of our framework is that it explicitly quantifies the dynamics of the stressed stochastic process over the entire time horizon. Furthermore, the developed algorithm allows for efficient simulation of the stressed processes and thus provides a methodology to estimate, e.g., future losses and risk measures, under the stressed scenarios.

In this work, we contribute to the stress testing literature by generalizing the reverse stress testing approach to a dynamic setting, via stressing a stochastic process at a fixed point in time and characterizing the dynamics of the processes under the stressed probability measure. In particular, we consider an insurance portfolio over a finite time horizon, which under the reference probability measure is modelled by a compound Poisson process. We then are interested in how the dynamics of the portfolio need to be changed so that, under the altered dynamics, stress(es) at the terminal time are attained. The stresses we consider are expectations of functions applied to the portfolio at the terminal time. This includes stresses on risk measures such as Value-at-Risk (VaR), VaR and Conditional Value-at-Risk (CVaR), and expected utility constraints. To find the stressed probability measure, we seek over equivalent probability measures on the path-space of stochastic processes the one under which the process attains the stresses and which minimizes the KL divergence to the reference measure. We solve the optimization problem, characterize the unique stressed probability measure and the stressed dynamics of the stochastic process. We find that under the stressed probability measure, the intensity and the severity distribution of the process both depend on state and time. Thus, in the spirit of reverse stress testing, our analysis informs how the effects of a stress on a Poisson process results in a marked point process with time and state dependence in both intensity and severity distribution. Differently from the static setting of reverse stress testing or the development of adverse scenarios, we require and are interested in a full characterization of the dynamics of the stochastic process under the stressed probability measure that lead to the constraint. Therefore, we also propose an algorithm to simulate sample paths under the stressed probability measures, and thus are able to illustrate the effects of a stress on the entire process.

Relevant for risk management purposes, we study a stress on VaR and a stress on VaR and CVaR jointly and provide illustrations of how the stochastic process is altered under these stresses. We further consider generalizations to multivariate compound Poisson processes and stresses at times earlier than the terminal time. For stresses on a sub-portfolio, we observe that the dependence between the sub-portfolios may amplify the stress. We illustrate the applicability of our framework by considering “what if” scenarios, where we examine what severity of stress on a portfolio component at an earlier time is needed such that the aggregate portfolio exceeds a risk threshold at the terminal time.

The paper is structured as follows. Section 2 introduces and solves the optimization problem, including an alternative representation of the change of measure and the stressed dynamics of the process. In Section 3, we discuss two applications: a stress on VaR of the process at the terminal time and a stress on VaR and CVaR jointly. In Section 4, we consider two extensions of our framework: first to allow for constraints that are not at the terminal time, and second to multivariate compound Poisson processes, where we examine the cascading effect a stress on one component of the process has on the other components. The algorithm for simulating the process under the stressed measure, which is used throughout the paper, is discussed in Section 5. The code is available at https://github.com/emmakroell/stressing-dynamic-loss-models.

2 Minimally Perturbed Compound Poisson Process

Let a filtered probability space be given and let denote the Borel -algebra of a set. We consider a one-dimensional jump process that satisfies the stochastic differential equation (SDE) under

where is a Poisson random measure. We assume for every and every that is -measurable and that is independent of . Thus, the random measure is -adapted and its future increments are independent of the past filtration. We further assume that has mean measure (also known as the compensating measure) given by

thus is a compound Poisson process with intensity and severity or jump size distribution . We denote by the compensated measure.

Throughout, we call the reference probability measure and denote by alternative probability measures on the same filtered probability space. For notational convenience, we write for the expected value under and set . To quantify discrepancies between probability measures, we use the Kullback-Leibler (KL) divergence [18]. The KL divergence of with respect to (also known as the relative entropy) is defined as

where we use the convention and denotes the Radon-Nikodym (RN) derivative of with respect to . For an overview of the properties of KL divergence, see, e.g., [27].

With this notation at hand, we first motivate the optimization problem which is central to this work. Consider an insurance portfolio modelled by a compound Poisson process under the reference measure . A modeller wishes to examine how the process is perturbed under stresses on its terminal value, i.e., on . Here, we consider stresses of the form , for functions and constants , . Examples of stresses include expected utility constraints and risk measure constraints such as Value-at-Risk (VaR) and Conditional Value-at-Risk (CVaR). For a specified stress, the modeller then seeks the most “plausible” probability measure under which the stochastic process achieves the stresses.

Specifically, we consider equivalent probability measures characterized by Girsanov’s theorem [23], i.e. those with RN derivatives of the form

where denotes the stochastic exponential and where is a predictable, non-negative random field on . To assure that is indeed a martingale, we assume that satisfies the following condition.

Definition 2.1.

The random field satisfies the Novikov condition on the interval if

We seek over probability measures of this form the one with minimal KL divergence to under which the process attains the constraints. Mathematically, we consider the following optimization problem.

Optimization Problem 2.2.

Let and for , where , and consider

where is the class of equivalent probability measures induced by Girsanov’s theorem, i.e.,

where is a predictable, non-negative random field satisfying Novikov’s condition on the interval .

Note that any probability measure is uniquely characterized by a random field . We refer to any predictable, non-negative random field that satisfies the Novikov condition on as a Girsanov kernel, denoted by . We further note that is convex since a convex combination of random fields is a random field and any convex combination of random fields satisfying the Novikov condition also satisfies the Novikov condition. In general, a change of measure induces a modified intensity and severity distribution that may be time and space dependent. Proposition 2.8 provides the exact characterization of the changes induced by the optimal measure change.

The next result provides the Girsanov kernel which characterizes the probability measure attaining the infimum in 2.2.

Theorem 2.3.

If a solution to 2.2 exists, it is given by with characterized by , where

| (1) |

are Lagrange multipliers such that the constraints hold, and denotes the -expectation conditional on the event that the process at time is equal to , i.e., . The solution is unique.

Proof.

Let , then the RN derivative has the representation

and the KL divergence of with respect to becomes

Let be Lagrange multipliers. The Lagrangian associated with this optimization problem can be written as

The time version of the associated value function for given Lagrange multipliers is defined as

where denotes the -expectation given that the process at time is equal to , i.e., .

Under the assumption that is Markov, so that we may write for some function , , the dynamic programming principle implies that the value function should satisfy the Hamilton-Jacobi-Bellman (HJB) equation:

| (2a) | ||||

| (2b) | ||||

where the linear operator is the -generator of , and acts on functions as follows:

Applying the first order conditions to the term in (2a), for fixed Lagrange multipliers, we obtain the optimal control in feedback form:

| (3) |

where . Inserting the feedback form of the control back into (2a), we obtain

| (4) |

For simplicity, we write whenever the probability measure is induced by given in (1). Conditions under which the Lagrange multipliers exist are discussed in Proposition 2.6. Next, we derive an alternative representation of the RN derivative associated with , when has the specific form given in (1). For this we first state a general result.

Theorem 2.4.

Define the functions

for some function with . Then, it holds -a.s. that

| (6) |

Proof.

Define the stochastic process , such that

Clearly, coincides with the left-hand side of (6). By Itô’s lemma we have that

| (7) |

and therefore is a local martingale. Moreover, due to the integrability and support of , is bounded, and therefore, is a true martingale.

Next, define the stochastic process , where . As is a Markov process, and by integrability of , is also a martingale, hence,

We aim to show that is -a.s constant for all . To this end, from Itô’s lemma we have that

Combining the above with (7), we have

As is a martingale, we also have that

Using this identity and substituting the expression for in terms of , yields

which, after inspecting the various terms, vanishes. Therefore, for some and all . As is a martingale, , moreover, . Therefore, , which proves the result. ∎

With the above result we obtain a succinct representation of the RN derivative associated with the Girsanov kernel from Theorem 2.3, which is in the spirit of [12].

Corollary 2.5.

For Lagrange multipliers such that and the Girsanov kernel given in Theorem 2.3, the measure induced by has RN derivative

Proof.

Finally, we provide the existence of a solution to 2.2 by discussing the existence of the Lagrange multipliers. In particular, we show that the Lagrange multipliers are solutions of a (possibly non-linear) system of equations.

Proposition 2.6.

Proof.

For and , we rewrite the constraint(s) from 2.2 using the RN derivative from Corollary 2.5 to obtain

Cancellation gives (8). ∎

We refer to the solution of 2.2, denoted by , as the stressed probability measure. Depending on the constraints, explicit expressions for may be available. We observe that whether Equation (8) has a solution depends on the choice of and , . One necessary condition for Equation (8) to have a solution is that each must be in the support of . This requirement means that the value of each constraint is such it is attainable by in some state of the world.

For the case of a single constraint, we can specify additional conditions on and such that a solution to Equation 8 exists.

Proposition 2.7.

If the cumulant generating function of , , satisfies for some with , then for all

| (9) |

there exists a unique solution to

| (10) |

Proof.

Let be in the interval given in Equation (9) and assume there exists , , such that the cumulant generating function of , , satisfies . The latter implies, by properties of the cumulant generating function, that for all . As is convex and twice differentiable, its derivative, , exists and is continuously increasing on . We observe that

Thus must take on all intermediate values between and

. Hence

there must exist an such that

| (11) |

Uniqueness of follows by increasingness of . Finally, rearranging (11) gives (10). ∎

Note that if is constant, the condition in Equation 9 becomes void. In that case, one must have for Equation 10 to have a solution. An example when the assumptions in Proposition 2.7 are fulfilled is when is bounded. In this case the cumulant generating function exists and is finite for all . Thus, as a consequence of the above proposition we obtain that any stress satisfying yields a solution to Equation 10. A case in point is VaR, which we discuss in detail in the Section 3. We further consider the case of two constraints, VaR and CVaR, and give explicit conditions under which a solution exists.

Under a stressed probability measure , the stochastic process is no longer a true compound Poisson process due to the time- and state-dependence of the Girsanov kernel . Indeed, the next result states the intensity process and the severity distribution of under .

Proposition 2.8.

The intensity process and severity distribution of the process under the stressed measure are, respectively,

Proof.

By Girsanov’s Theorem, the compensator of under is and thus the intensity of the process becomes:

We obtain the updated severity distribution from , by multiplying and dividing by the integral term in . ∎

Under the stressed measure , we refer to the intensity and the severity distribution as the stressed intensity and stressed severity distributions, respectively. Note that while in Proposition 2.8 we state the dynamics of under the optimal measure , the result holds for any fixed and not necessarily optimal Lagrange multiplier , , and corresponding .

Corollary 2.5 gives a concise representation of the RN derivative of the stressed measure as a function of the value of the process at terminal time only, i.e., of . This result, that the RN derivative of the stressed measure induced by perturbing a stochastic process is a function only of the terminal value of the process, is a priori not obvious. However, this representation of the RN derivative does not explicitly characterize the dynamics of the process under . Indeed, the stressed intensity process and severity distribution, see Proposition 2.8, are functions of the optimal random field given in Theorem 2.3. We moreover provide in Section 5 an algorithm to simulate sample paths of the process under the stressed probability measure.

3 Risk Measure Constraints

In this section, we apply our framework to a risk management context. Specifically, we consider constraints given by the two most widely used risk measures, Value-at-Risk (VaR) and Conditional Value-at-Risk (CVaR). For a constraint on VaR and joint constraints on VaR and CVaR, we examine the dynamics of under the stressed measure both analytically and numerically.

3.1 Value-at-Risk

We first examine a stress on VaR. The VaR of a random variable under a measure at level is defined as

where denotes the distribution function of under and we use the convention that . For notational simplicity, we write .

We implement a constraint in our framework by setting and in 2.2, which gives the constraint

| (12) |

When the distribution of under is continuous to the left of , then (12) is equivalent to requiring ; otherwise, it may be viewed as a probability constraint. Furthermore, must be chosen such that the constraint is attainable, meaning that must lie between the essential infimum and essential supremum of , a requirement on the choice of rather than the process .

Proposition 3.1.

Let and . The solution to 2.2 with constraint given by and is the measure characterized by the Girsanov kernel

| (13) |

where the Lagrange multiplier is given by

The solution is unique.

Proof.

Letting in Theorem 2.3, we have for any that

We find the optimal Lagrange multiplier by applying Proposition 2.6. For each , the corresponding measure has RN derivative given in Corollary 2.5. Thus, the constraint (12) becomes

Solving for gives the result, which is well-defined by the choice of and . ∎

We note that since , the optimal Lagrange multiplier is the log-odds ratio of the event under the reference and the stressed probability measures. If is chosen smaller than , corresponding to a downward stress on VaR, then it holds , and thus . Similarly, if is larger than , corresponding to an upward stress on VaR, we have , and thus .

The Girsanov kernel provides information on how the process is distorted under the stressed measure. More specifically, Proposition 2.8 states the stressed intensity and severity distributions, and that these are, in general, state and time dependent. The specific form of in this example leads to a few observations summarized in the next two propositions.

Proposition 3.2.

Let be a compound Poisson process with intensity rate and severity random variable , where has non-negative support. Let be given in Proposition 3.1, i.e., the Girsanov kernel associated with the solution to 2.2 and constraints and , where and . Then, satisfies for all ,

Moreover, if , then for all .

Proof.

If , then from the form of given in Proposition 3.1, we observe that the probabilities in the numerator and denominator of are both equal to 0 and thus for any .

Suppose that . Using the properties of a Poisson process over small time intervals, we obtain an approximation of for when is close to . Using that under , , where are i.i.d. severity random variables with distribution and is a Poisson process with intensity , we obtain for small

| (14) |

We split the case into two parts: first, we further assume that , then the probability in the numerator of is zero, thus substituting the approximation given in (14) gives

When , we have .

For the second part we further assume that . Substituting the short-time approximation (14) into both the numerator and denominator of , gives

which converges to 1 as . ∎

Proposition 3.3.

Let be a compound Poisson process with rate and severity random variable , where has non-negative support. Let be the intensity process of under the stressed measure that solves 2.2 with constraints and , where and . Then satisfies

Moreover, if , then for all , i.e., the stressed intensity is equal to the intensity under the reference measure .

Proof.

If , then by Proposition 3.2, for all and therefore for . Else, if , we have by dominated convergence:

∎

Finally, in the following example we examine a numerical example of a 15% upward stress on .

Example 3.4.

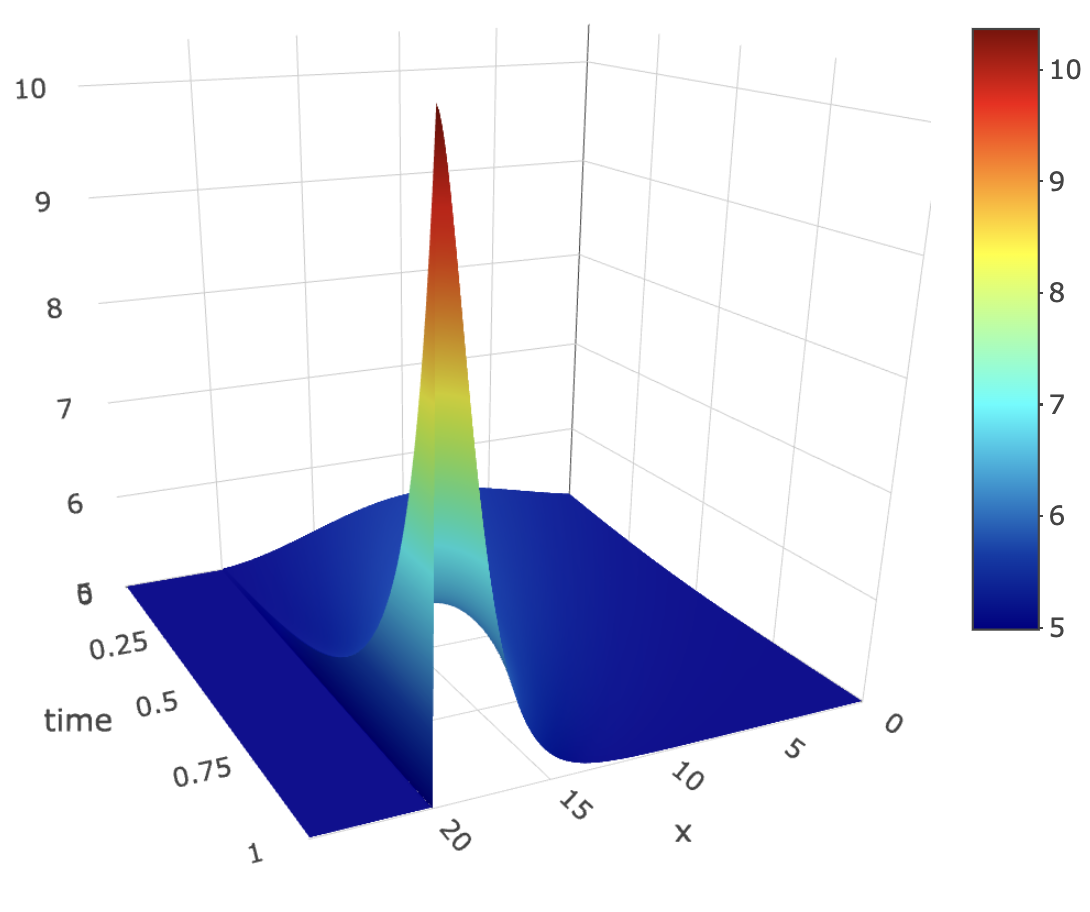

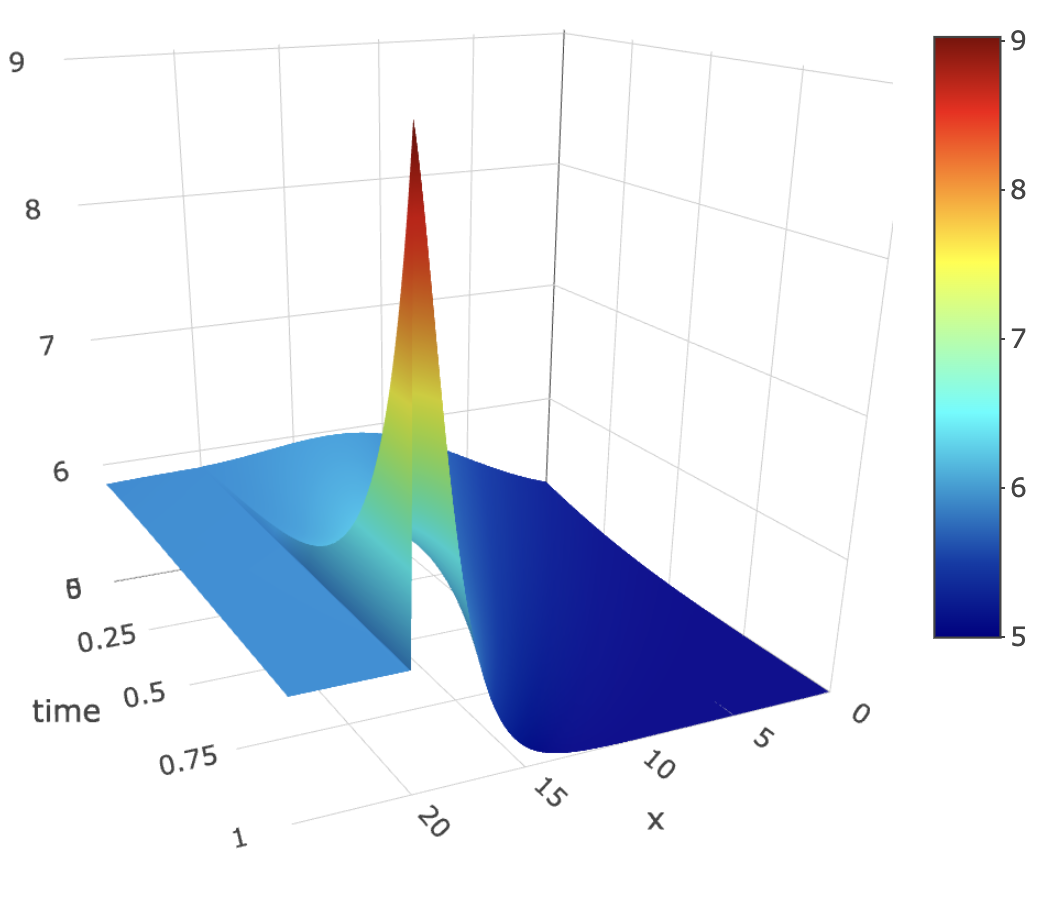

Here we illustrate how the dynamics of a compound Poisson process are altered for a constraint on VaR. Specifically, under the reference measure , we consider a compound Poisson process over the time horizon where , intensity , and the severity is Gamma distributed , where is the shape parameter and is the rate parameter (i.e., , ). With these parameters, the 90% quantile of is . We apply a stress composed of a 15% increase in VaR at the 90% level, resulting in of approximately 20. Simulation under the reference and the stressed measure is performed using methods described in Section 5, which requires in (13) to be plugged into Proposition 2.8.

Figure 1 shows the optimal intensity for times and . We see that if is greater than 20, then , i.e., the stressed intensity is the same as under the reference measure. We further observe at time , when is close to 0, is close to , and as approaches , approaches . These observations are consistent with Proposition 3.3.

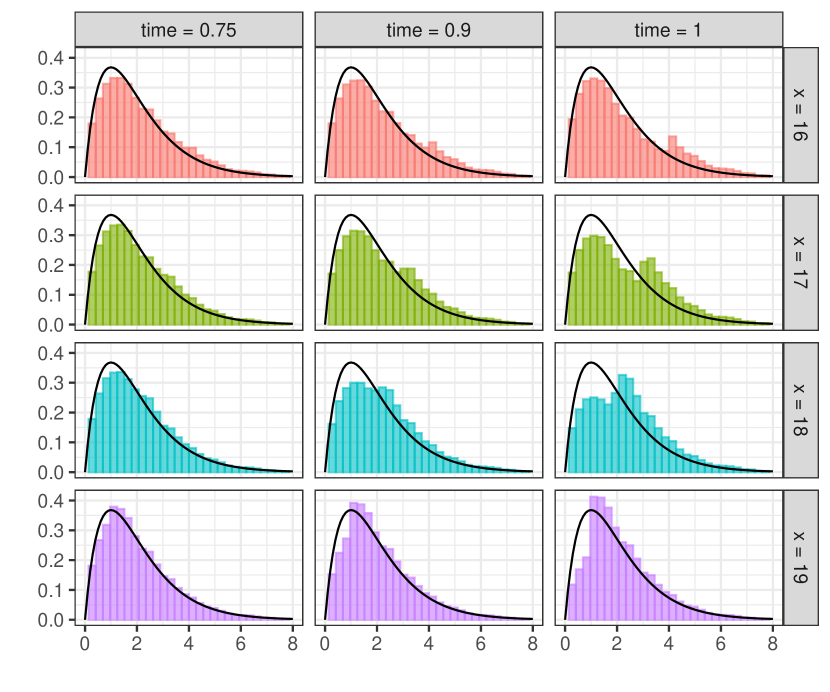

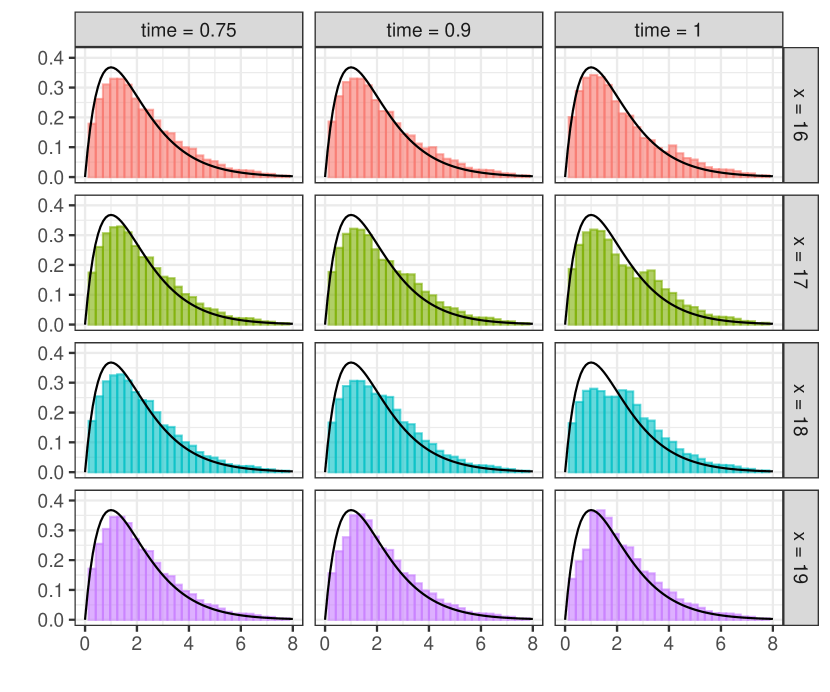

Figure 2 shows histograms of the stressed severity distribution for state space values and times . The black line depicts the density of the severity random variable under , which is . Consistent with Proposition 3.2, we see that the severity distributions are more distorted when is close to, but less than, . The change in the distribution also become more apparent as we approach terminal time. The distribution remains fairly close to the baseline at (left column), while we observe a significant change in the distribution at time 0.9 (middle column) and in particular at the terminal time, 1 (right column). At the terminal time, when 18 and 19, we observe that the stressed severity distributions has a larger right tail which is induced by the stress, while for and 17, the distribution is bimodal.

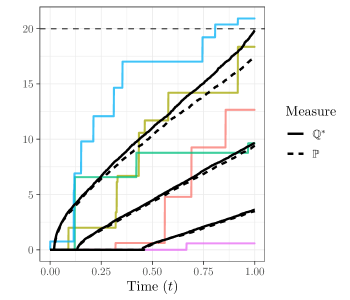

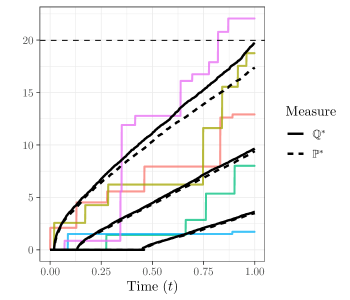

Select sample paths of under the stressed measure and their corresponding stressed intensity processes are shown in Figure 3. The black lines are the 10th, 50th, and 90th quantiles under both (solid line) and (dashed line). The dashed grey line is . Examine first the blue line – once the path crosses (the dashed grey line) in the left panel, the corresponding stressed intensity process (right panel) falls to the value of the intensity under the reference measure, i.e., . In contrast, the yellow path (left panel) never crosses , and thus continues to increase as . Paths which never get close to the value of have intensity processes that are not extensively distorted, i.e., is close to . This is consistent with our observations of Figure 1.

3.2 Conditional Value-at-Risk

Next, we examine the effect on the dynamics of under a stress on the risk measure CVaR. The CVaR, also called Expected Shortfall, of a random variable under a measure at level is [1]

For notational simplicity, we write .

Since the value of CVaR depends on that of VaR, we impose constraints on both risk measures. We exploit the representation

to write this optimization problem in the form of 2.2 using the following two constraints:

| (15) |

The solution to 2.2 with the above constraints is given in the next proposition.

Proposition 3.5.

Let denote the cumulant generating function of . Suppose , , and there exists an such that for all . Then the solution to 2.2 with constraints , , , and is the measure characterized by the Girsanov kernel

where is the solution to

| (16) |

and

Here, refers to the optimal Lagrange multiplier when only a VaR constraint is applied (Proposition 3.1). The optimization problem has a unique solution.

Proof.

First, we find the Girsanov kernel for given Lagrange multipliers . We compute

and the formula for , if the optimal Lagrange multipliers exist, follows from Theorem 2.3. Next, we show the existence of the Lagrange multipliers and their representation. By Corollary 2.5, the RN derivative of the measure that solves 2.2 with constraints (15) is

Using this representation of the RN derivative, the first constraint can be written as

Solving for gives

| (17) |

Analogously, we may write the second constraint as

Simplifying this expression and substituting in the above expression for gives

| (18) |

providing (16). To determine if (18) has a solution, we first rewrite for fixed the RN derivative using (17):

Therefore, the second constraint becomes

Simplifying the above expression gives

| (19) |

We observe that the right-hand side of (19) is the derivative of the cumulant generating function of evaluated at . We will denote the derivative of the cumulant generating function of by . Since moment generating functions are log-convex, is decreasing in . To show that there exists a solution to LABEL:{eq:eta2_eq_key}, we denote and .

We note that the sign of is as follows:

Corollary 3.6.

For , let and be the stressed and values, respectively. Define and . If , then , and if , then .

This follows directly from the proof of Proposition 3.5. If is continuous, . Thus, the sign of depends in a direct manner on the stress on CVaR while its dependence on the stress on VaR is indirectly through .

Proposition 3.7.

Let the severity distribution have non-negative support. Let be given in Proposition 3.5, i.e., the Girsanov kernel associated with the solution to 2.2 with constraints (15), where , , and there exists an such that for all . Then for all , satisfies

Moreover, if , then for any .

Proof.

First, if , then and , thus the probabilities in the numerator and denominator of from Proposition 3.5 are both 0, and the indicator functions in the expectations are both identically equal to 1. This gives

Second, if , we examine the limiting behaviour of . In addition to the approximation of derived in the proof of Proposition 3.2, we further use the properties of a Poisson process over short intervals to obtain an approximation of for , , as follows:

Using these two approximations, we consider two cases: first, if , then for we have

Taking the limit, we obtain

Else, if , we have

Taking the limit, we obtain

∎

Proposition 3.8.

Let the severity random variable with -distribution have non-negative support. Then, the limiting behaviour of is

Moreover, if , the stressed intensity is for any .

Proof.

If , we have by the previous proposition, so

If , we apply dominated convergence to obtain

∎

If the severity distribution under the reference measure is explicitly given, we may obtain the limit of for analytically. In keeping with our recurring example, let under , where is the shape and the rate parameter. Then the limiting behaviour of , if , is

where .

Finally, we examine the effect of joint stresses on both VaR and CVaR in the following numerical example:

Example 3.9.

Let be under a compound Poisson process over a time horizon with severity distribution and intensity , as in Example 3.4. We apply a stress of a 15% increase in VaR at the 90% level, as in Example 3.4, and a 12% increase in the CVaR at the 90% level.

Figure 4 displays for a grid of times and state space values in [0,25]. We see that if is greater than , then consistent with Proposition 3.8, . If is less than , we observe that at time , when is close to 0, is close to , and as approaches from below, approaches .

Figure 5 displays histograms of the stressed severity distribution for state space values and times . The black lines are the density of the severity distribution under , here . As in the VaR stress case (Example 3.4), we observe that the stressed severity distributions become more and more distorted from the reference distribution as time approaches . We note in this case, however, that the addition of the CVaR constraint has a smoothing effect on the tails. Compared to Figure 2, there is a reduced bimodal effect for 16 and 17, and less of a spike around 1, when 18 and 19.

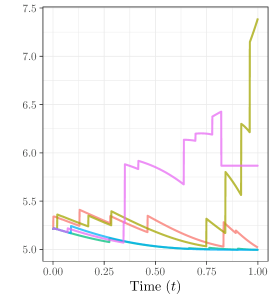

Figure 6 shows select sample paths of under (left panel) and their corresponding intensity processes (right panel). The black lines show the 10th, 50th, and 90th percentiles under both (solid) and (dashed). The horizontal dashed grey line corresponds to the stressed VaR, which is approximately 20. Comparing Figure 6 with Figure 3 (sample paths of for the VaR constraint only), we observe that the paths evolve similarly. However, in Figure 6 due to the additional CVaR constraint, if the path crosses the stressed intensity no longer falls to the baseline parameter, , but instead becomes constant equal to . A case in point is the magenta line, where the sample path crosses and the intensity process becomes constant equal to .

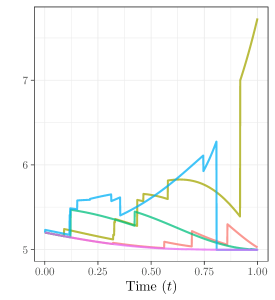

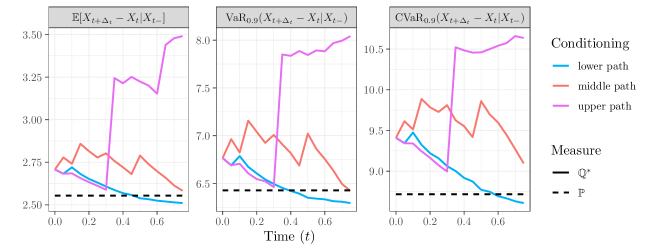

Finally, we turn to a risk-forecasting exercise that can be undertaken in this dynamic framework. At any time prior to the stress, , a risk manager may wish to forecast the expected losses in the next period. In particular, suppose they calculate risk measures of the increment , conditioning on the observed value , for . As the dynamics of the stressed loss process are known in our framework, we can forecast the future losses at all times. Figure 7 shows the expected value, VaR at the 90% level, and CVaR at the 90% level of the quarter-year increment , for times in . Three scenarios are shown under the stressed measure, which correspond to the paths in Figure 6 of the same colour. Clearly, under the baseline the expected value, VaR and CVaR are constant and thus independent of time and state. Under the stressed measure, however, the risk forecasts all depend on time and state. Moreover, the jumps in the underlying paths in Figure 6 lead to sharp increases in the risk forecasts in Figure 7. Furthermore, for the paths with fewer losses (blue and red), the risk measures tend to decrease when the underlying paths do not jump. However, the risk measures are increasing for the riskier scenario (purple). This risk forecasting exercise illustrates that the proposed dynamic framework leads to richer information for the risk manager, that cannot be obtained in a static setting.

4 Aggregate Portfolios and “What-if” Scenarios

Here we provide two extensions of our framework which allow for sensitivity testing of insurance portfolios. In Section 4.1, we solve the optimization problem when a stress is imposed at an earlier time than the terminal time and when we have two constraints at different times. In Section 4.2, we generalize the results to multivariate compound Poisson processes. Combining these extension allows for application of “what-if” scenarios in the spirit of Example 4.13. In that application, we consider an aggregate insurance portfolio and study how a stress at time on one of the sub-portfolios cascades through time and affects the aggregate portfolio. We observe that a stress on one sub-portfolio perturbs not only the other sub-portfolios but also the dependence between the sub-portfolios.

4.1 Stresses at Earlier Times

First, suppose that instead of imposing constraints at the terminal time , we impose constraints at an earlier time . This leads to the following optimization problem:

Optimization Problem 4.1.

Let , , and for . Consider

where is the class of equivalent probability measures given by

and is a predictable, non-negative process satisfying Novikov’s condition on .

Note that 4.1 is not a special case of 2.2 as the probability measures we seek over are induced by random fields that live on . The solution to this new optimization problem is as follows:

Proposition 4.2.

The optimal measure is characterized by the Girsanov kernel

and the corresponding RN derivative is given by

The solution is unique.

Proof.

First, we show that we can restrict to probability measures that are induced by a specific random field. For this let for a random field and define and moreover, denote its induced probability measure by . The KL-divergence then becomes

where the last inequality follows since and is a non-negative convex function that attains its minimum when with . Furthermore,

Thus we can indeed restrict to probability measures that are induced by random fields that are constant equal to 1 on , i.e., to

Next, we observe that this set of probability measures is equivalent to the following set

that is probability measures induced by random fields defined on . Thus, we showed that in 4.1 we can restrict to probability measures in . Restricting to provides an optimization problem that is of the form 2.2 and whose solution and uniqueness is given by Theorem 2.3, Corollary 2.5, and Proposition 2.6. ∎

Next, we impose constraints at both the terminal time and an earlier time , leading to the following optimization problem:

Optimization Problem 4.3.

Let , , and . Consider

where is the class of equivalent probability measures given by

and is a predictable, non-negative process satisfying Novikov’s condition on .

Proposition 4.4.

If a solution to 4.3 exists, it is given by with characterized by , where

and are Lagrange multipliers such that the constraints hold. Furthermore, the solution, if it exists, is unique.

Proof.

The Langrangian associated with the problem is

As before, we write

Thus, the associated value function at time is

We consider two cases: First, if , then is -measurable, so

where

This is a value function of the same form as in the proof of Theorem 2.3. Thus by the same procedure, we find that the optimal control is and

| (20) |

Second, if , then we write the value function as follows

where denotes the limit of as approaches from the right. satisfies the HJB equation

The optimal control is , and again using the Cole-Hopf change of variables and the Feynman-Kac Theorem, we obtain

Substituting in (20) and using the tower property of expectations, we obtain

Taken together, we have

and

∎

To obtain expressions for the optimal Lagrange multipliers, we note that Theorem 2.4 can be extended to show that if , then the RN density of the solution from Proposition 4.4 admits the form

| (21) |

This representation gives us the following system of equations for and :

Lemma 4.5.

There exists a unique solution to 4.3 if there exist Lagrange multipliers such that and the system of equations

has a solution.

Proof.

Rewriting the constraints using (21) concludes the proof. ∎

Observe that the proof of Proposition 4.4 can be generalized to a finite number of constraints at different time points, by splitting the value function into additional pieces. An alternative approach to obtain the stressed measure and the dynamics of the process under the stressed measure, is to increase the state space and introduce stopped processes. Specifically, suppose that we have a constraint of the form where , then, by introducing the set of stopped processes for , the original constraint can be viewed as a single constraint on a multi-variate process at terminal time, i.e., . Thus the approach in the next section, where we consider multivariate compound Poisson processes, can be applied to this new problem.

4.2 Multivariate Compound Poisson Processes

In this section, we consider a -dimensional compound Poisson process . We denote (random) vectors using bold font to distinguish them from (random) variables and scalars. We assume that, under , has mean measure

where is the -dimensional severity distribution and the scalar intensity. The optimization problem we consider in this section is a stress applied to one of the components of at time . For simplicity of notation, we stress throughout the first component of , i.e., .

Optimization Problem 4.6.

Let , and for , and consider

where is the class of equivalent probability measures induced by Girsanov’s theorem

and is a predictable, non-negative random field satisfying Novikov’s condition on .

The solution to 4.6 is given in the next proposition.

Proposition 4.7.

If there exists such that and

then 4.6 has a solution. The solution is the measure characterized by the Girsanov kernel

The solution is unique.

We omit the proof of Proposition 4.7 as it follows using steps similar to those in the proof of Theorem 2.3 and arguments in Section 4.1. Note that if a stress is applied at the terminal time, i.e., , then simplifies to a representation akin to that in Section 2. Next, we show that the optimal Girsanov kernel is a function of and only.

Corollary 4.8.

The optimal Girsanov kernel depends only on the first components of and , i.e.,

This follows since under the reference measure has independent increment and the severity distributions do not depend on states.

Next, we examine how the dynamics of change when moving from to a stressed measure . Specifically, we are interested in how the other components of the process, for are affected by a stress on . For this, we denote the marginal severity random variables by , and their distributions under the reference measure by . For a stressed distribution we write for and .

Proposition 4.9.

The stressed intensity and the stress joint severity distribution (solution to 4.6) are, respectively,

where we set and , since the stressed intensity and the stressed severity distribution only depend on the value of the stressed component .

Proof.

By Girsanov’s theorem, the compensator of under the stressed measure is . The result follows analogous to the proof of Proposition 2.8. ∎

Notice that under the stressed measure all components , , share the same stressed intensity process given in Proposition 4.9 and thus the dynamics of all components are distorted. We report the stressed marginal severity distributions , , in the next proposition.

Proposition 4.10.

The stressed marginal severity distributions of under (solution to 4.6) are

for and where is the joint severity distribution of the first and the components under .

Proof.

The result follows from Proposition 4.9 by integration. ∎

We note that the stressed marginal severity distribution of the first component of , , is equal to the stressed severity distribution in the 1-dimensional case (Proposition 2.8). The -th marginal severity distribution , , however, depends on the copula between . If is independent from , then the stressed marginal severity distribution of is equal to its distribution under , i.e., . If and are dependent under , a stress on leads to a stressed marginal severity distributions of which may depend on time and state . We illustrate in Example 4.12 how different copulas between alter the stressed severity distributions.

Even if the severity distributions are independent under , implying that , , the paths of the components of under are in general still dependent. This is due to the shared intensity process . In the next example, we construct a joint severity distribution of under such that the paths of and are independent under and .

Example 4.11.

We consider a bivariate compound Poisson process under with a specific dependence between the severity distributions, which we will refer to as the “independent mixture” distribution. Let and be distribution functions and let . Suppose the severity distributions are such that

where denotes the Dirac measure at . This choice implies that under if the process jumps, only or will jump. In particular, the parameter (resp. ) is the probability that (resp. ) jumps, conditional on the event that the process jumps.

Under the stressed measure (solution to 4.6) the stressed intensity of the process is, applying Proposition 4.9,

as . The joint stressed severity distribution becomes

where

Thus, under if jumps, only or jump. Moreover, the probability that (resp. ) jumps, given that the process jumps, is (resp. ).

Next, we show that the probability that jumps is identical under both and . For this, let denote a Poisson process with intensity under and a Poisson process with intensity under such that under and under , where for , are i.i.d. with distribution and respectively. Note that under the process is independent from the corresponding severity random variables. Thus we obtain, for all and small enough, that

Moreover, the marginal severity distribution of , conditional on the event that jumps, is under both and . Therefore, even though has under an intensity process that depends on , the change to the intensity and the change to the probability of the jump occurring to cancel, leaving the process unchanged.

If and are dependent, then the stressed measure affects the dependence between the paths. The next example examines how the dependence structure between and changes for different copulas of the joint severity distribution .

Example 4.12.

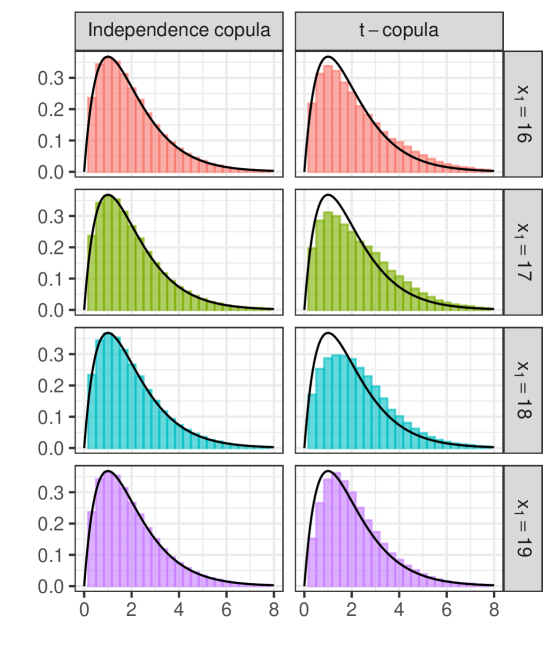

Under , we consider a bivariate compound Poisson process over the time horizon , , with marginal severity distributions and intensity . With these parameters, we have . We apply a 15% increase in VaR at the 90% level to the first component, i.e. . Figure 8 displays histograms of the stressed severity distribution at time for 16, 17, 18, and 19. The panels in the left column display the histograms under the assumption that are independent under , while the panels in the right column display the histograms under the assumption that have under a -copula with 3 degrees of freedom and correlation 0.8. The black line is the density of the severity under , . We observe that when the reference severity distributions are independent, the stressed severity distribution of the second component is unchanged from the reference model. However, when the severity distributions are dependent, the severity distribution of the second component gets distorted under the stressed measure. The distortion is most noticeable for and 18. As the second component of the process is only stressed indirectly, this distortion reflects a “spill-over” effect of the stress on the first component.

Figure 9 shows contour plots of the copula densities of for the same two choices of copulas for the severity distribution. We observe an increase in upper tail dependence between and under when the marginal severity distributions and are dependent. Table 1 reports the Spearman’s rank correlation coefficient between and under and , i.e. and , for different copulas. The 95% confidence intervals of the estimates are reported in brackets, computed using the method of [7]. When the severity distribution of and is the independent mixture from Example 4.11, is approximately 0 under both and . When and have independent severity distributions under , we observe an increase in correlation under , however it is not statistically significant at the 5% level. However, for most other choices of copulas, there is a statistically significant increase in the correlation under .

| Copula of under | ||

|---|---|---|

| Independent mixture | (0.019) | (0.020) |

| Independence copula | 0.674 (0.011) | 0.692 (0.012) |

| -copula, corr = 0.8, df = 1 | 0.668 (0.011) | 0.707 (0.011) |

| -copula, corr = 0.8, df = 3 | 0.661 (0.012) | 0.710 (0.011) |

| Gumbel copula, | 0.672 (0.012) | 0.691 (0.011) |

| Frank copula, | 0.671 (0.012) | 0.694 (0.012) |

Finally, we examine a simulation approach to “what-if” scenarios. We consider an insurance loss portfolio where one component of the portfolio () undergoes a stress at time and are interested in how the stress impacts the risk (measured via a risk measure) of the aggregate portfolio. In a risk management context one may be interested in the required severity of a stress on at time that leads to a breach of a risk threshold at the terminal time.

Example 4.13.

Suppose we have a bivariate process and impose a stress on for some . We then examine the effect of the stress on the VaR of the aggregate portfolio at the terminal time, i.e., on . Specifically, for , we calculate the minimal percentage increase in such that VaR at the 90% level of the aggregate portfolio is at least 5% larger under the stressed measure, i.e. .

Table 2 reports the corresponding increase in in percentage for different levels, where , , , and have under a -copula with 3 degrees of freedom and correlation 0.8. Since the stress increases the positive dependence between and , we see that a larger stress for smaller levels of is required to achieve the same increase in .

| Stress: % increase in | |

| 0.3 | 58.6 |

| 0.4 | 40.4 |

| 0.5 | 30.4 |

| 0.6 | 24.8 |

| 0.7 | 19.6 |

| 0.8 | 16.1 |

5 Simulating Under the Stressed Measure

To illustrate how a stress affects the dynamics of a compound Poisson process, we plot in the earlier examples different sample paths of the process, its intensity processes, and the severity distributions under the reference and the stressed probability measure. Key to simulating sample paths under the stressed measure is to (a) find the optimal Lagrange multiplier , and (b) calculate the Girsanov kernel , which then allows to estimate the stressed intensity and the stressed severity distribution using Proposition 2.8 To find the optimal Lagrange multiplier, we solve Equation 8 by estimating the required expectation using the Fourier space time-stepping (FST) algorithm [17]. For completeness, we recall the FST methodology in Section 5.1. To estimate the Girsanov kernel , which is given in Theorem 2.3, we again utilize the FST for calculating conditional expectations, see Section 5.2.

The code implementing the algorithms is available at https://github.com/emmakroell/stressing-dynamic-loss-models.

5.1 Fourier space time-stepping algorithm

In this section, we provide an algorithm to simulate paths of under the stressed measure, which is based on the Fourier space time-stepping (FST) algorithm [17]. FST is a method for efficiently solving partial integro-differential equations (PIDE) such as Equation 5 using fast Fourier transform methods. We briefly summarize the FST method before describing our algorithm for simulating under the stressed measure.

For a function , we denote its Fourier transform by and consider a PIDE with a general terminal condition :

| (22) |

where the linear operator is the -generator of the process . Using Fourier transform, we rewrite the above PIDE as

| (23) |

where is the characteristic function of . As (23) is a linear ODE, its solution is

| (24) |

Thus a solution to (22) is obtained by applying the inverse Fourier transform to (24).

To implement this procedure, we first create a grid in the state space variable and in the frequency domain, . One then computes via (24) on this grid to approximate the solution to the PIDE (23). Applying the inverse Fourier transform to we obtain , the solution to (22), on the state space grid. For detail on grid selection, we refer to [17].

5.2 Simulating Sample Paths

Next, we illustrate how the FST method can be used to calculate the stressed intensity, the stressed severity distributions, and how to simulate sample paths under a stressed measure. For simplicity, we state the algorithm for a one-dimensional compound Poisson process . We use the FST method to approximate (conditional) -expectations of functions applied to . Recall that both the optimal Girsanov kernel and the optimal Lagrange multipliers are computed by taking -expectations. Moreover, since is under a compound Poisson random variable, its characteristic function (under ) is given by the Lévy-Khintchine formula, i.e., , where is the characteristic function of the severity random variable under .

Algorithm 1 describes the process of simulating under a stressed measure . If the equations for the Lagrange multiplier are linear, a single application of FST will be sufficient. If the equations are however non-linear, we use a non-linear solver where the FST method is used to compute the equation for each iteration. To simulate paths of under the stressed measure , we compute and for a grid of times , and simulate forward at each time step with this intensity and severity distribution.

The method to compute the intensity and severity distribution is described in Algorithm 2. For this we first require the Girsanov kernel which is obtain by computing and using FST, and then taking their ratio. The intensity process is calculated via numerical integration with respect to . Finally, the severity distribution is obtained by re-sampling.

To implement the case when is bivariate, we follow the same procedure as in the univariate case, except that the jump distribution is now bivariate. Using the copula package [16], we set the desired marginal jump distributions and copula. Algorithm 2 is modified so that draws are taken from this joint distribution but the weights are computed using only the draws corresponding to the stressed (first) marginal distribution. The bivariate distribution is then re-sampled with these weights. We then simulate forward using Algorithm 1 with the two distorted marginal severity distributions and the shared distorted intensity process.

6 Conclusion

In a dynamic setting, we consider a risk management framework based on the concept of reverse stress testing where the reference model is a compound Poisson process, , over a finite time horizon ]. We solve the optimization problem where we seek the probability measure on the path-space of stochastic processes which has minimal KL-divergence from the reference measure and fulfills constraints which can be written as expected values of functions applied to the process at terminal time. We show that this solution is unique, and refer to it as the stressed measure. We characterize the Radon-Nikodym derivative of the stressed measure, and derive the dynamics of under it. We prove that under the stressed measure, is a generalized version of a compound Poisson process, where both the intensity and the severity distribution depend on time and state. For general constraints, we provide a simulation algorithm which allows to simulate sample paths of under the stressed measure.

Of particular interest are constraints on VaR and CVaR risk measures, for which we analyze in detail the dynamics of under the stressed measures. In the multivariate setting and for constraints at time points earlier than , we investigate how a stress on one component of the process alters the dependence between the components of the process and otherwise affects the components other than the one stressed. We find that for most dependence structures of the severity distribution, the stress increases the dependence between the portfolio components due to the shared intensity process, as well as changes in the the tail dependence of the process components. Finally, we consider a “what-if” scenario where we examine how severe a stress on a portfolio component needs to be to breach a risk threshold of the aggregate portfolio at a later time point. We find that smaller stresses are needed to the upper tail of a sub-portfolio to breach a VaR risk threshold as compared to stresses on the median or lower tails.

Acknowledgements

EK is supported by an NSERC Canada Graduate Scholarship-Doctoral. SJ and SP would like to acknowledge support from the Natural Sciences and Engineering Research Council of Canada (grants RGPIN-2018-05705, RGPAS-2018-522715, and DGECR-2020-00333, RGPIN-2020-04289). SP also acknowledges the support from the Canadian Statistical Sciences Institute (CANSSI).

References

- [1] Carlo Acerbi and Dirk Tasche “On the coherence of expected shortfall” In Journal of Banking & Finance 26.7 Elsevier, 2002, pp. 1487–1503 DOI: 10.1016/S0378-4266(02)00283-2

- [2] Siddique Akhtar and Iftekhar Hasan “Stress testing: Approaches, methods and applications” Risk Books, 2019 URL: https://www.risk.net/stress-testing-2nd-edition

- [3] Anna Rita Bacinello, Pietro Millossovich, Annamaria Olivieri and Ermanno Pitacco “Variable annuities: A unifying valuation approach” In Insurance: Mathematics and Economics 49.3 Elsevier, 2011, pp. 285–297

- [4] Basel Committee on Banking Supervision “Stress testing principles” In Quantitative Finance BIS, 2018 URL: https://www.bis.org/bcbs/publ/d450.pdf

- [5] Tony Bellotti and Jonathan Crook “Forecasting and stress testing credit card default using dynamic models” In International Journal of Forecasting 29.4 Elsevier, 2013, pp. 563–574 DOI: 10.1016/j.ijforecast.2013.04.003

- [6] Jeremy Berkowitz “A Coherent Framework for Stress Testing” In Journal of Risk 2.2, 2000, pp. 5–15 DOI: 10.21314/JOR.2000.021

- [7] Douglas G. Bonett and Thomas A. Wright “Sample size requirements for estimating Pearson, Kendall and Spearman correlations” In Psychometrika 65.1 Springer, 2000, pp. 23–28 DOI: 10.1007/BF02294183

- [8] Eike C. Brechmann, Katharina Hendrich and Claudia Czado “Conditional copula simulation for systemic risk stress testing” In Insurance: Mathematics and Economics 53.3 Elsevier, 2013, pp. 722–732 DOI: 10.1016/j.insmatheco.2013.09.009

- [9] Thomas Breuer and Imre Csiszár “Systematic stress tests with entropic plausibility constraints” In Journal of Banking & Finance 37.5 Elsevier, 2013, pp. 1552–1559 DOI: 10.1016/j.jbankfin.2012.04.013

- [10] Thomas Breuer, Martin Jandačka, Javier Mencı́a and Martin Summer “A systematic approach to multi-period stress testing of portfolio credit risk” In Journal of Banking & Finance 36.2 Elsevier, 2012, pp. 332–340 DOI: 10.1016/j.jbankfin.2011.07.009

- [11] Mathieu Cambou and Damir Filipović “Model Uncertainty and Scenario Aggregation” In Mathematical Finance 27.2, 2017, pp. 534–567 DOI: https://doi.org/10.1111/mafi.12097

- [12] Imre Csiszár “I-Divergence Geometry of Probability Distributions and Minimization Problems” In The Annals of Probability 3.1, 1975, pp. 146–158 URL: https://www.jstor.org/stable/2959270

- [13] Mikkel Dahl and Thomas Møller “Valuation and hedging of life insurance liabilities with systematic mortality risk” In Insurance: mathematics and economics 39.2 Elsevier, 2006, pp. 193–217

- [14] Russell Gerrard, Steven Haberman and Elena Vigna “Optimal investment choices post-retirement in a defined contribution pension scheme” In Insurance: Mathematics and Economics 35.2 Elsevier, 2004, pp. 321–342

- [15] Paul Glasserman, Chulmin Kang and Wanmo Kang “Stress scenario selection by empirical likelihood” In Quantitative Finance 15.1 Taylor & Francis, 2015, pp. 25–41 DOI: 10.1080/14697688.2014.926019

- [16] Marius Hofert, Ivan Kojadinovic, Martin Mächler and Jun Yan “Elements of copula modeling with R” Springer, 2018 DOI: 10.1007/978-3-319-89635-9

- [17] Kenneth R Jackson, Sebastian Jaimungal and Vladimir Surkov “Fourier space time-stepping for option pricing with Lévy models” In Journal of Computational Finance 12.2, 2008, pp. 1–29 DOI: 10.21314/JCF.2008.178

- [18] Solomon Kullback and Richard A Leibler “On information and sufficiency” In The Annals of Mathematical Statistics 22.1, 1951, pp. 79–86 URL: https://www.jstor.org/stable/2236703

- [19] Vaishno Devi Makam, Pietro Millossovich and Andreas Tsanakas “Sensitivity analysis with -divergences” In Insurance: Mathematics and Economics 100, 2021, pp. 372–383 DOI: 10.1016/j.insmatheco.2021.06.007

- [20] Alexander J McNeil and Andrew D Smith “Multivariate stress scenarios and solvency” In Insurance: Mathematics and Economics 50.3 Elsevier, 2012, pp. 299–308 DOI: 10.1016/j.insmatheco.2011.12.005

- [21] Michael Merz and Mario V Wüthrich “Modelling the claims development result for solvency purposes” In CAS E-Forum, Fall 2008, 2008, pp. 542–568 Citeseer

- [22] Attilio Meucci “Fully flexible views: Theory and practice” In Risks 21.10, 2008, pp. 97–102 URL: https://www.risk.net/derivatives/structured-products/1500207/fully-flexible-views-theory-and-practice

- [23] Bernt Øksendal and Agnès Sulem “Applied Stochastic Control of Jump Diffusions”, Universitext Springer, 2019 DOI: 10.1007/978-3-540-69826-5

- [24] Silvana M. Pesenti “Reverse Sensitivity Analysis for Risk Modelling” In Risks 10.141 MDPI, 2022 DOI: 10.3390/risks10070141

- [25] Silvana M. Pesenti, Pietro Millossovich and Andreas Tsanakas “Reverse sensitivity testing: What does it take to break the model?” In European Journal of Operational Research 274.2 Elsevier, 2019, pp. 654–670 DOI: 10.1016/j.ejor.2018.10.003

- [26] H. Pham “Continuous-time stochastic control and optimization with financial applications”, Stochastic Modelling and Applied Probability Springer Berlin Heidelberg, 2009 DOI: 10.1007/978-3-540-89500-8

- [27] Tim Van Erven and Peter Harremos “Rényi divergence and Kullback-Leibler divergence” In IEEE Transactions on Information Theory 60.7 IEEE, 2014, pp. 3797–3820 DOI: 10.1109/TIT.2014.2320500