Efficient Convex PCA with applications to Wasserstein geodesic PCA and ranked data

Abstract.

Convex PCA, which was introduced in Bigot et al. [6], is a dimension reduction methodology for data with values in a convex subset of a Hilbert space. This setting arises naturally in many applications, including distributional data in the Wasserstein space of an interval, and ranked compositional data under the Aitchison geometry. Our contribution in this paper is threefold. First, we present several new theoretical results including consistency as well as continuity and differentiability of the objective function in the finite dimensional case. Second, we develop a numerical implementation of finite dimensional convex PCA when the convex set is polyhedral, and show that this provides a natural approximation of Wasserstein geodesic PCA. Third, we illustrate our results with two financial applications, namely distributions of stock returns ranked by size and the capital distribution curve, both of which are of independent interest in stochastic portfolio theory.

Key words and phrases:

Convex principal component analysis, optimal transport, Wasserstein space, Aitchison geometry, capital distribution curve, stochastic portfolio theory, distributional data1. Introduction

Principal component analysis (PCA) is a fundamental dimension reduction technique for revealing the underlying structure of the data. The standard Euclidean formulation of PCA operates by projecting the data orthogonally onto a lower dimensional subspace which minimizes the residual error, and can be solved analytically via the eigenvalue decomposition of the empirical covariance matrix. Modern challenges in data science motivated various extensions of Euclidean PCA, such as sparsity [38], exponential family PCA [13], functional PCA [34], principal geodesic analysis for manifold-valued data [21], to name a few. For systematic overviews of PCA and its variants we refer the reader to [1, 24].

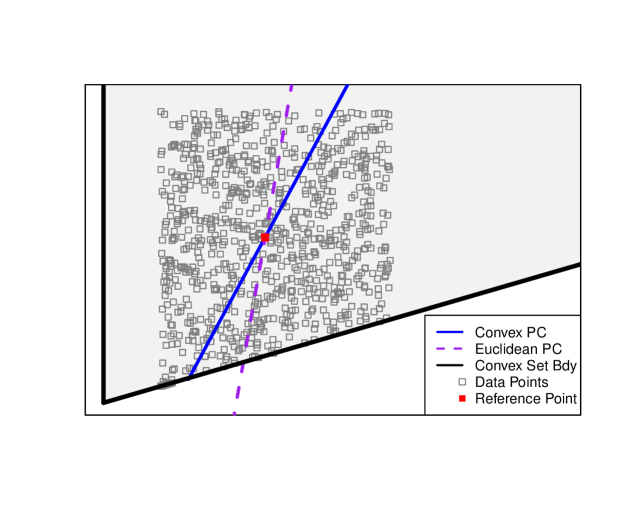

In this paper, we study convex PCA (CPCA) where the data is constrained to lie in a convex subset of a Hilbert space. CPCA was first introduced in [6] to study a notion of geodesic PCA (GPCA) on the Wasserstein space on an interval, where each data point is a probability distribution. This approach is based on the fact that the Wasserstein space (of order ) on an interval is isometric to a convex subset of an space (see Section 5.1). Statistical analysis of distributional data using optimal transport, and principal component analysis in particular, has attracted a lot of attention in recent years. For example, a “log” PCA on the Wasserstein space was studied in [9], while [28] introduced projection methods to perform PCA and regression for one-dimensional distributional data. Other recent statistical works include Wasserstein autoregressive models for distributional time series [37], Wasserstein PCA for circular measures [5], and regression models [12]. Also see [29] for an accessible introduction to optimal transport and its applications in statistics and machine learning. Apart from Wasserstein geodesic PCA, convex PCA is also useful in other settings. For example, in Section 6 we apply CPCA to a ranked data-set where each observation is a vector satisfying the convex constraint . In Figure 1 we compare Euclidean and convex PCA using a simulated two dimensional data-set, where the data is restricted to lie in a convex cone. Geometrically, the projection onto the Euclidean principal component (PC) may not lie in the convex set, making it difficult to interpret the result. By restricting the projected points to the convex set, we obtain (using the algorithm developed in Section 4) the convex PC. Note that the computation is more involved since the projection is no longer a linear operator.

1.1. Main contributions and organization of the paper

Our contribution in this paper is threefold. First, we obtain new theoretical results about CPCA concerning consistency and analytical properties of the objective function. Second, we present a numerical implementation of finite-dimensional CPCA when the convex state space is polyhedral, and apply it to solve a finite-dimensional approximation of Wasserstein geodesic PCA on an interval. Third, we provide two novel financial applications of CPCA motivated by stochastic portfolio theory [19] in mathematical finance.

We begin by recalling in Section 2 the formulation of convex PCA following the treatment of [6]. Convex PCA has two formulations, namely global and nested. In this paper, we focus on the nested version for interpretability and computational purposes. We also define a notion of explained variation in this context.

In Section 3 we study theoretical properties of CPCA, mostly in the finite dimensional case. We consider (i) consistency in measure, (ii) consistency of finite dimensional approximations of the underlying Hilbert space, and (iii) analytical properties of the objective function of an equivalent formulation of nested CPCA. These results place CPCA on a rigorous basis and pave the way for numerical implementation.

A computational algorithm for CPCA is the subject of Section 4. When the Hilbert space is finite dimensional and the convex set is polyhedral (i.e., given by the intersection of a finite collection of half spaces), we present an efficient algorithm which can be readily implemented. For especially large and high dimensional problems we also provide a C++ implementation that takes advantage of parallel computing techniques.111The codes are available at: https://github.com/stevenacampbell/ConvexPCA.

Wasserstein geodesic PCA on an interval is studied in Section 5. After recalling the isometry between the Wasserstein space and a closed convex subset of an space, we propose a natural finite dimensional approximation of Wasserstein geodesic PCA by projecting the data onto suitable subspaces of the underlying Hilbert space, and note that this approximation satisfies the consistency result in Section 3.2. Numerical implementation of Wasserstein GPCA was considered (among related approaches such as projected PCA) in [28] using a quadratic B-spline expansion of the distribution function. Here, our approximation is based on discretizing the transport map and is exact when all data points are in the given finite dimensional subspace.

Our work on CPCA was motivated by our previous paper [8] on stochastic portfolio theory (SPT). SPT is a mathematical framework introduced by Fernholz [19] for studying macroscopic properties of equity markets and portfolio selection. A key empirical observation of this theory is that the behaviours of stocks have a systematic dependence on their relative ranks (measured by market capitalization), and this dependence may be exploited by carefully constructed portfolios to outperform the market. In [8] we studied a portfolio optimization problem using rank-based portfolios and were led to quantify statistically the rank-based behaviours. In Section 5.3, we apply Wasserstein geodesic PCA to distributions of US stock returns ranked by size, and show that the first two convex principal components can be interpreted in terms of volatility and skewness. In Section 6 we consider the US capital distribution curve which captures market capitalization weights arranged in descending order. By viewing them as (ranked) compositional data under the Aitchison geometry of the simplex [18] and applying CPCA, we show that the projection onto the first convex principal component corresponds closely to market diversity, an entropy-like quantity which measures the concentration of market capital and correlates significantly with the relative performance of active portfolio managers. These properties have significant implications in the construction of macroscopic stochastic models of equity markets as well as portfolio selection.

Finally, in Section 7 we summarize our contributions and discuss possible directions for future research. The Appendix contains proofs of most technical results as well as further details of our numerical implementation.

2. Convex PCA

Convex PCA was originally proposed in [6] to study Wasserstein geodesic PCA on the real line. In this section we recall the general formulation of CPCA which has two versions, namely global and nested. We also give a definition of explained variation in this context. Wasserstein geodesic PCA will be revisited in Section 5 where we propose and implement a finite dimensional approximation.

Let be a Hilbert space (over ) with inner product and norm . The dimension of can be finite or infinite. In the latter case, we assume that is separable. For and , let and . Next, let be a given nonempty closed convex subset of which will serve as the state space of the data. In some theoretical results we will further assume that is compact.

If and are nonempty closed subsets of , we let

| (2.1) |

be the Hausdorff distance between and . It is well known that defines a metric on the space of nonempty and compact subsets of . In what follows is always a non-negative integer. For , we let be the dimension of the smallest affine subspace of containing .

Definition 2.1.

We endow the following spaces with the Hausdorff metric .

-

(i)

Let be the space of nonempty and closed subsets of .

-

(ii)

Let be the family of convex sets such that .

-

(ii)

Given a reference point , we let be the family of sets such that .

By [6, Proposition 3.2], if is compact then all three spaces in Definition 2.1 are compact. Also, by [6, Proposition A.3], is continuous on . If is a (nonempty) closed convex set, we let be the orthogonal projection which is well-defined by the Hilbert projection theorem.

We are almost ready to state the two versions of CPCA. Let be a Borel probability measure on representing the distribution of the data; in applications, is usually an empirical measure, say , where is the point mass at the data point . Let be an -valued random element whose distribution is . We assume has finite second moment, i.e., . We also let be a fixed reference point which is typically the mean of .

Definition 2.2 (Convex PCA).

Let be a Borel probability measure on with finite second moment, and . For , define

| (2.2) |

-

(i)

(Global CPCA) Given , a -global convex principal component (CPC) is a set such that

(2.3) -

(ii)

(Nested CPCA) Let . For , we say that is a -nested convex principal component (CPC) if there exist such that and, for each ,

(2.4)

In the Euclidean setting (i.e., ), the global and nested PCA problems are equivalent. Here, they are equivalent only when . Although solutions to the nested CPCA problem are generally not optimal in the global sense, they are easier to compute and interpret. Hence, we focus on nested CPCA in later sections. Using the compactness and continuity results cited above, it can be shown (see [6, Theorem 3.1]) that when is compact both the global and nested CPCA problems (2.3) and (2.4) have non-empty solution sets for any . Also, as long as is not supported on a -dimensional convex subset of , in (2.3) and (2.4) the objective values are unchanged if we restrict to sets of the form

| (2.5) |

where is a sequence of orthonormal vectors in [6, Propositions 3.3 and 3.4]. This representation will be used in the analysis in Sections 3 and 4. In (2.5), for an optimal set , we call the -th convex principal direction.222By an abuse of terminology, we also call it the -th convex principal component which is often used in the Euclidean context.

A useful concept in PCA is the proportion of explained variation. In the classical setting, it can be expressed in terms of the eigenvalues of the covariance matrix. Since the projection map is nonlinear when is not a subspace, eigenvalue decomposition is no longer available. Nevertheless, we may still define a notion of explained variation.

Definition 2.3 (Total and explained variation).

The total variation of the data with respect to a given reference point is defined by

| (2.6) |

To avoid triviality, we assume . Let . The proportion of variation explained by is defined by

| (2.7) |

Remark 2.4.

-

(i)

Clearly and, if , then . More generally, if is a sequence of global or nested CPCs, then is non-decreasing in . In this case, we may interpret as the additional variation explained by the -th component.

-

(ii)

Definition 2.3 reduces to the usual definition for Euclidean PCA if we let , and be an affine subspace containing .

-

(iii)

Since the definition of requires evaluating the projection map for individual data points, it is generally costly to compute for large data sets.

Proposition 2.5.

Let be compact, and let , , be an increasing sequence of convex subsets of . If , then pointwise on . Consequently, we have as .

Proof.

See Appendix A.1. ∎

3. Finite dimensional convex PCA

While infinite dimensional Hilbert spaces arise naturally in theory (e.g., Wasserstein geodesic PCA), in implementations we almost always work with a finite dimensional space due to approximation or discretization. In this section we establish some theoretical properties of CPCA mostly in the finite dimensional case. Sections 3.1 and 3.2 study consistency properties in measure and in the dimension of . In Section 3.3 we consider an equivalent formulation of nested CPCA and prove continuity and differentiability of the objective function.

3.1. Consistency in measure

In principal component analysis, as well as other statistical methodologies, consistency is a desirable, if not indispensable, property. In our context, by consistency we mean the stability of the optimization problems (2.3) and (2.4) as the input measure varies. For example, under i.i.d. sampling the empirical measure converges to the population as the sample size tends to infinity. In this subsection we provide consistency results in the spirit of [6, Section 6], thereby fixing a technical gap in [6, Lemma 6.1]. Using similar techniques, we study in Section 3.2 the stability of CPCA when the underlying Hilbert space is approximated by a sequence of finite dimensional subspaces.

In this subsection we assume that is a compact convex set. Let be the space of Borel probability measures on and equip it with the topology of weak convergence. Since is compact, weak convergence is equivalent to convergence in the -Wasserstein distance, for any (see e.g., [36, Theorem 6.9]). For later use, we recall that for , the -Wasserstein distance is defined by

| (3.1) |

where is the set of couplings of the pair . Also recall the functional defined by (2.2).

When stating and proving consistency results, it is convenient to formulate the optimization problems in terms of indicator functions. Given a subset of an ambient space, let be its indicator function which is on and on its complement. Then the global CPCA problem (2.3) is equivalent to

| (3.2) |

Similarly, the nested CPCA problem (2.4) can be written as

| (3.3) |

where is a given -nested CPC. Also, we will be using the notion of -convergence (denoted by ) whose definition is recalled in Appendix C. It also contains other relevant definitions and results, such as Kuratowski convergence of sets, that are used in the proofs.

We first give a fairly standard but general result which will serve as a framework for proving specific consistency statements.

Theorem 3.1 (General consistency).

Let be compact and convex. Let and . Suppose and in . Then

| (3.4) |

Moreover, if for , then any accumulation point of (under the Hausdorff distance) attains the infimum on the right hand side of (3.4).

To apply Theorem 3.1, we need to verify the condition . When this holds, we have convergence of the objective value as well as convergence of the solution in a suitable sense. Unfortunately, the proof of [6, Lemma 6.1], which verifies this condition and underlies the consistency statements there, contains a technical gap which we were able to fix only when is finite dimensional. Thus, in the remainder of this subsection we assume that is finite dimensional. The proofs of Theorem 3.1 and the following results are given in Appendix A.2 which also contains more discussion about the technical issues involved in [6, Lemma 6.1].

Theorem 3.2 (Consistency of global CPCA).

We also give an analogous consistency result for nested CPCA which is not explicitly treated in [6]. Note that it is formulated in terms of a subsequence because the convex PCs are not necessarily unique.

Theorem 3.3 (Consistency of nested CPCA).

Suppose , , and are as in Theorem 3.2. Suppose in , in and that . For each , suppose

is a sequence such that each is a -nested convex principal component. Then there is a subsequence along which the following statements hold:

-

(i)

For each we have .

-

(ii)

The sequence of sets is incresaing in and forms a sequence of nested convex principal components with respect to and .

- (iii)

3.2. Consistency of finite dimensional approximation

Convex PCA and Wasserstein geodesic PCA on the real line are generally infinite dimensional optimization problems. To implement them in practice, finite dimensional approximations are necessary. Using similar ideas as in Section 3.1, we formulate such an approximation and show its consistency as the dimension tends to infinity.

Let be an infinite dimensional separable Hilbert space and be a compact convex set. Let be an increasing sequence of finite dimensional vector subspaces of , such that is dense in . For example, we may consider an orthonormal basis and let . Let be the orthogonal projection onto . We impose the simplifying assumption that for each . Note that this condition holds in our finite dimensional approximation of Wasserstein geodesic PCA which will be treated in Section 5.

Let and , and consider the corresponding CPCA problems (3.2) and (3.3). Given , natural finite dimensional approximations of the CPCA problems can be formulated as follows. Let which is a compact convex subset of . Let and let be the pushforward of under . By definition, is defined by , for measurable. It is clear that . Now we may define the finite dimensional approximations by

| (3.5) |

where is given.

We give a consistency result for the global CPCA which is equivalent to nested CPCA when . While we expect that analogous results hold for the higher CPCs of the nested problem, the mathematical statements and proofs become much more messy and technical. To focus on the algorithms and applications, we do not pursue consistency further in this paper.

Theorem 3.4 (Consistency of finite dimensional approximation for global CPCA).

Suppose is compact and for each . For fixed, let

Then and hence the conclusions of Theorem 3.1 hold.

Proof.

See Appendix A.2. ∎

3.3. Analytical properties for nested CPCA

Now we focus on nested CPCA where is finite dimensional. Under suitable conditions, we establish continuity and differentiability of quantities involved in the optimization. This will allow us to study, in Section 4, numerical algorithms to implement CPCA in practice.

In this subsection we work under the following setting:

Condition 3.5 (Conditions for finite dimensional nested CPCA).

-

(i)

is finite dimensional and so is isomorphic to for some .

-

(ii)

There exist continuously differentiable convex functions such that the convex state space has the form

(3.6) -

(iii)

The data distribution is an empirical measure of the form .

-

(iv)

The interior of is non-empty and the reference point satisfies for all .

The form (3.6) is sufficiently flexible to handle many applications, including those in Sections 5 and 6. For example, if each is affine then is polyhedral, and if each is linear then is a polyhedral cone. Note that here we do not require to be compact.

To formulate the main results, we use the observation (see [6, Proposition 3.4] and (2.5)) that the nested CPCA problem can be solved by constructing a sequence of orthonormal vectors. For , we let

| (3.7) |

Define

| (3.8) |

and, for ,

| (3.9) |

By Theorem 3.6 below, is continuous on . This guarantees the existence of (as long as ). By [6, Proposition 3.4], the sets

form a sequence of nested convex principal components.

Now we establish some analytical properties of the function .

Theorem 3.6 (Continuity).

Using a recent generalized envelope theorem proved in [26] and recalled in Appendix C.3, we also study the differentiability of .

Theorem 3.7 (Differentiability).

Under Condition 3.5, the directional derivative

of exists for any and . Moreover, if and for each at most one constraint is binding (i.e., for at most one ), then is differentiable at .

Proof.

See Appendix A.2.6 where we also provide expressions of the directional directive and gradient of in terms of a Lagrangian and its saddle points. ∎

Remark 3.8.

In particular, if the Hausdorff dimension of is at most , then is differentiable almost everywhere on .

4. Implementation for polyhedral domains

In this section we provide an efficient implementation of nested convex PCA when the Hilbert space is finite dimensional and the convex domain is polyhedral. When combined with parallel computing techniques,333Our implementation, using R and C++, can be found at: https://github.com/stevenacampbell/ConvexPCA our algorithm can be applied to fairly large and high dimensional data-sets. Illustrative empirical examples, which are of independent financial interest, are presented in Sections 5 and 6.

As in Section 3 we let the Hilbert space be finite dimensional, so is isomorphic to a Euclidean space. To simplify the notations we assume without loss of generality that for some (the case is trivial). Elements of are regarded as column vectors. We say that a closed convex set is polyhedral if there exists an matrix and such that

| (4.1) |

If , we say that is a polyhedral convex cone. We remark that if is a compact convex set with non-empty interior, then it can be approximated arbitrarily well by convex polyhedrons under the Hausdorff metric (see [7, 33]).

Let be a convex polyhedron of the form (4.1) and consider, for a given reference point and empirical distribution , the nested CPCA problem which can be stated in the form (see (3.8) and (3.9))

| (4.2) |

where and

We begin by parameterizing the quantities involved. Write where is chosen such that . Suppose have been found and consider the second minimization problem in (4.2). Given , let where is an orthonormal basis of . Then with if and only if has the form where is a unit vector in . Thus (4.2) is equivalent to solving

| (4.3) |

where the constraint can be written in terms of and as

| (4.4) |

When , we may simply let and the equivalence still holds. See Figure 2 for an illustration. Finally, we express the constraint using hyperspherical coordinates. In particular, write where and

Now (4.3) is an unconstrained optimization problem in .

We proceed to discuss the algorithm, for which more details are given in Appendix B. For each , the inner minimization problem in (4.2) is easy to solve since can be identified with an interval. Specifically, we first compute the usual orthogonal projection, say , of onto . If is in , then is the optimal point. Otherwise, is the boundary point of which is closest to . This allows us to evaluate the objective . Algorithm B.1 gives the procedure for finding the boundary points. Using the differentiability of (and hence ) in (and hence in ), we can use standard gradient approximation (e.g. central differences) and gradient-based optimization methods to solve (4.2).

Example 4.1.

We illustrate our CPCA algorithm with the simulated data set shown in Figure 1. Here and is a convex cone indicated by the shaded region. The data is intentionally constrained to lie in a vertical strip so that the first Euclidean PC (dashed purple line) is almost vertical. Note that for data points near the lower left corner the Euclidean projections are outside . As shown in the figure, the first convex PC (solid blue line) is quite different from the Euclidean PC. Now the data points near the lower left corner are projected to the endpoint of the convex PC. We also compute the proportion of explained variation (Definition 2.3), which is 98% for the convex PC. This is slightly lower than 99% which is the variation explained by the Euclidean PC.

5. Wasserstein geodesic PCA

Distributional data arises when each data point can be regarded as a probability distribution. For instance, age distributions of countries, and empirical return distributions of financial assets, can be regarded as distributional data-sets. The Wasserstein metric (3.1) in optimal transport [35, 36] provides a natural geometric structure on spaces of probability distributions. As mentioned in Section 1, convex PCA was first introduced in [6] to study Wasserstein geodesic PCA on the real line. This is because the Wasserstein space , where is an interval and is the space of Borel probability measures on with finite second moment, is isometric to a closed convex subset of an space. After recalling the isometry and the relevant notations, we introduce a finite dimensional approximation for which the algorithms developed in Section 4 apply. We then apply Wasserstein geodesic PCA to analyze return distributions of stocks ordered by size.

5.1. Wasserstein space on an interval and geodesic PCA

For technical purposes, we let be a compact interval and leave the unbounded case for future research.444At a practical level, if the data set consists of compactly supported distributions (say empirical distributions), we can always choose a sufficiently large interval. In this case but we will still write the former since we are using the -Wasserstein metric. Let be a reference measure which is absolutely continuous with respect to the Lebesgue measure and has full support. A simple but useful example is the uniform distribution on . For any , there exists a non-decreasing mapping , which is unique -a.e., such that . Then, it is a well-known result in optimal transport that the Wassestein distance between is given by

| (5.1) |

The mapping defines a bijection from onto the space

which can be shown to be a compact convex subset of the separable Hilbert space . By (5.1), is isometric to the vector field via this mapping. (In [6] the isometry is defined in terms of which is also in .) We then define Wasserstein geodesic PCA on to be the convex PCA on . Note that a line segment in corresponds via the isometry to a geodesic in the Wasserstein space which is given in terms of McCann’s displacement interpolation [27]. In particular, the geometry does not depend on the choice of the absolutely continuous reference measure .

5.2. Finite dimensional approximation

Consider a collection of distributional data and a reference point (corresponding to in the general formulation). Let be the corresponding elements in which is the space of transport maps. We introduce a natural finite dimensional approximation of Wasserstein geodesic PCA.

The idea is simple: we approximate the interval using a refining sequence of partitions. For expositional simplicity and concreteness we focus on the dyadic partition , but other partitions may be used for computational purposes. For , let be the finite dimensional subspace consisting of functions such that is -a.e. constant on each subinterval corresponding to . Clearly by a standard density argument. Let be the orthogonal projection onto . By projecting and onto (see (5.3) below), we get along the lines of Section 3.2 a finite dimensional approximation of Wasserstein geodesic PCA. In particular, since (which corresponds to the transport map from to ) is piecewise constant, we approximate each by a discrete distribution supported on a set with at most elements. The following lemma shows that our approximation satisfies the condition and hence the consistency result in Theorem 3.4 applies.

Lemma 5.1.

For we have .

Proof.

Given , consider the orthogonal collection given by

| (5.2) |

where is the -th subinterval of , and is on and elsewhere.555Since is absolutely continuous, the values on do not matter. Then for we have

| (5.3) |

Clearly, if then is non-decreasing and maps into . So and is invariant under . ∎

Each (has a version which) can be written in the form

| (5.4) |

for some . Then if and only if

| (5.5) |

Thus can be identified with a convex polyhedral domain for appropriately defined and , and hence our algorithm developed in Section 4 applies. From (5.5), the matrix is bidiagonal, a feature which simplifies some of the computations. We remark that if each data point (more precisely each ) is already in , then our formulation is exact.

5.3. Ranked stock return distributions

In both empirical examples (here and in Section 6) of this paper we consider the US stock market using data provided by The Center for Research in Security Prices (CRSP) [10]. In this example, we consider daily market capitalizations and dividend-adjusted stock returns from January 1962 to December 2021.

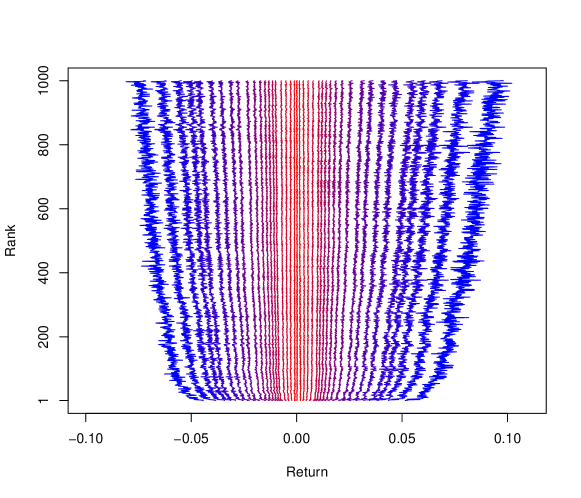

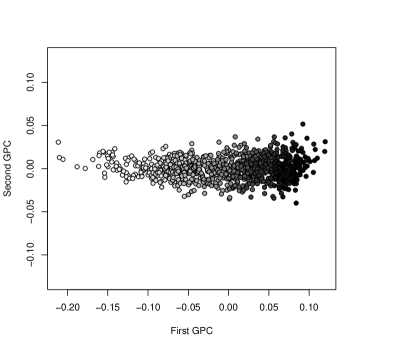

On each trading day, we consider the largest stocks (which differ from day to day) and consider their daily (arithmetic) returns.666Returns correspond to the ret variable in the CRSP database which is adjusted for stock splits and dividends. We arrange the returns according to the initial ranks of the stocks. Repeating this for each day, we obtain, for each rank , an empirical return distribution . More precisely, we have where is the return of the stock which was at rank on day . In stochastic portfolio theory it was observed that rank-based properties of stocks are useful in portfolio selection. For example, parameters (e.g. growth rates) of individual stocks are difficult to estimate but the corresponding rank-based quantities are more often much more stable. This phenomenon has inspired a large literature of rank-based diffusion models where the dynamics of a stock depends on its current rank (see e.g. [22] and the references therein). Understanding of the rank-based return distributions is relevant in constructing realistic rank-based models of the stock market. The data-set (consisting of empirical return distributions) is visualized in Figure 3.777We show here quantiles for and in , , , , , , , , , , , , , , , , , , , . These values are chosen for visualization purposes. Most importantly, we observe that small stocks tend to be more volatile and their return distributions are more positively skewed.

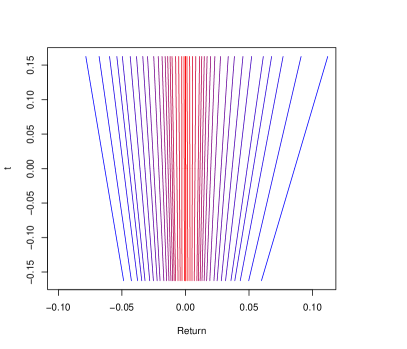

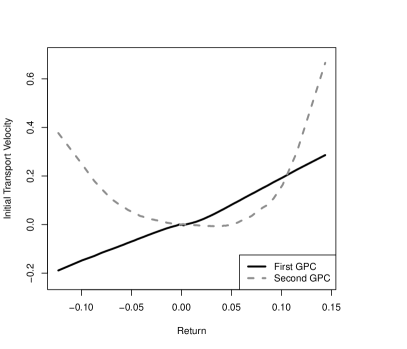

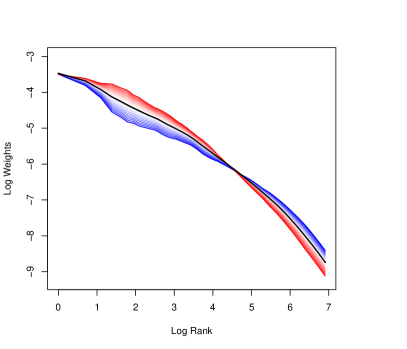

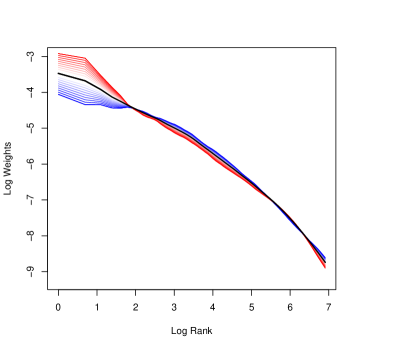

We perform nested Wasserstein geodesic PCA to analyze this data-set. We choose a sufficiently large interval which covers all returns, and use a dyadic partition ( with ) to obtain a finite dimensional nested CPCA problem as described in Section 5.2. We let the reference distribution be the uniform distribution on , and let be the (Wasserstein) barycenter of the return distributions. In Figure 4 we visualize the first two convex PCs (principal directions) which we also call the Wasserstein GPCs. In terms of the general notations of CPCA in Section 2, we visualize the curve for and . We also call this the perturbation of along . The first principal direction captures the volatility and the overall sknewness of the distribution, and explains alone of the variation (in the sense of Definition 2.3). The second principal direction can be interpreted in terms of additional skewness effects on the left and right tails of the distribution (note that the middle quantiles are almost unaffected), and contributes to a small increase of about in the explained variation. The projection of the data-set onto (identified with a subset of ) is shown in Figure 5(left).

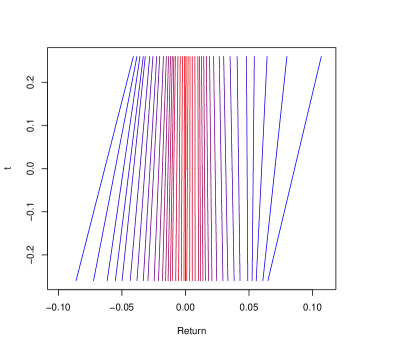

Note that in Figure 4 each quantile moves at constant velocity as the perturbation parameter varies. This is a feature of McCann’s displacement interpolation, under which each “particle” travels along a constant velocity straight line. More precisely, for each and , the perturbed distribution (corresponding to ) has the form for some vector field on the interval. In Figure 5(right) we plot the initial velocity fields and as functions of the return. Consistent with above, we see that is an asymmetric size effect and acts mostly on the tails.

6. Capital distribution curve under the Aitchison geometry

6.1. Financial background

Our second empirical example is about the capital distribution curve of the US stock market. We begin by defining this quantity and explaining its financial relevance. Let be the market capitalization of stock at time . The market weight of stock (relative to a given universe with stocks) is given by

| (6.1) |

The vector takes values in the open unit simplex

| (6.2) |

The capital distribution at time is given by the vector of ordered market weights given by

| (6.3) |

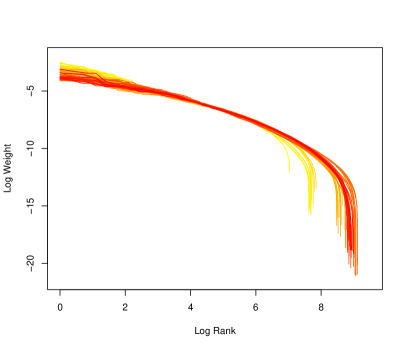

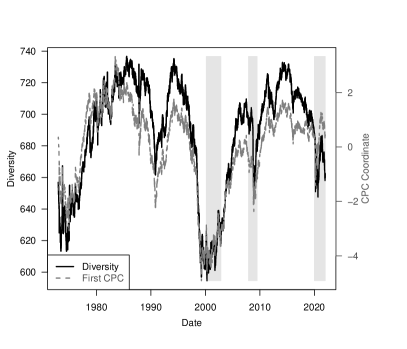

where are the (decreasing) order statistics of the market weights. Note that takes values in the ordered unit simplex . In Figure 6 (left) we plot the distribution curves (in log-log scale, i.e., ) of the whole US universe, where one curve is drawn for (early January of) each year from 1962 to 2021. A general observation is that the shape of the capital distribution is remarkably stable over time; capturing this stability is one of the main goals of the rank-based diffusion models mentioned in Section 5.3. Nevertheless, fluctuations of the capital distribution curve have significant financial implications. In particular, consider what is called in stochastic portfolio theory the market diversity which refers to the concentration of market capital. For example, we say that market diversity is low when most market capital is highly concentrated in the largest stocks, and market diversity is high if market capital is distributed more equally among the stocks. One way to measure market diversity is to use the function

| (6.4) |

where is a tuning parameter.888Here we use which is commonly used in the SPT literature. Other symmetric and concave functions on may be used, e.g., the Shannon entropy, and their qualitative behaviours are similar. Such functions are called measures of diversity in [19]. It was shown empirically, see e.g. [2, 19, 20], that the change in market diversity correlates positively with the performance of active portfolio managers relative to the capitalization-weighted market portfolio. Also see [8, 31] for recent empirical studies using the CRSP universe.

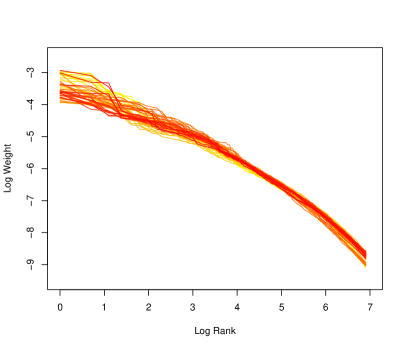

As seen in Figure 6(left), the number of stocks varies over time. To keep the dimension fixed, we consider in this section the daily capital distribution curves computed using the largest stocks (which vary each day) from January 1973 to December 2021. These curves are plotted in Figure 6(right). In December 1972, data from the Nasdaq Stock Exchange was added to the CRSP universe and caused a material change in the capital distribution. Hence for consistency we restrict to dates after this addition. On average, over the chosen period the top stocks capture more than of the total market capitalization. While each may be regarded as a probability distribution on the finite set , the set has no natural metric structure and so the Wasserstein metric may not be appropriate.999If we endow with the structure of a weighted graph, we may consider optimal transport along the lines of [25]. But CPCA cannot be applied, at least directly, to the resulting Wasserstein-like space which can be shown to be Riemannian. Rather, we endow the simplex with the Aitchison geometry in compositional data analysis [17], and use it to study fluctuations of the capital distribution curve using convex PCA. For our data, we expect that this geometry is more appropriate than the Euclidean one since it respects the relative (rather than absolute) scale of the components in the simplex and clearly distinguishes the boundary of the simplex from the interior.

6.2. Aitchison geometry

In this subsection we review the Aitchison geometry under which is an -dimensional Hilbert space. More details can be found in [17].

For , define its closure by

Now define the following operations on :

-

(i)

(Perturbation) For , define .

-

(ii)

(Powering) For and , define .

Under these operations, is an -dimensional real vector space. The identity element is the barycenter , and the additive inverse of is . Next define the Aitchison inner product by

| (6.5) |

With this is a Hilbert space. It is isometric with via the isometric log ratio transform given by

| (6.6) |

which has the form for a specific orthonormal basis.

The relevance of convex PCA stems from the following observation.

Lemma 6.1.

Under the Aitchison geometry, the ordered simplex is a polyhedral convex cone. In particular, we have , where

and is the Kronecker delta.

Proof.

Omitted. Note that is bidiagonal which is advantageous from the computational point of view. ∎

6.3. Convex principal components and market diversity

To perform nested CPCA for the capital distribution curves, we first map the data to via the isometric log ratio transform (6.6). After performing CPCA on the resulting polyhedral convex cone (see Lemma 6.1), we can interpret the result on the (ordered) simplex by applying the inverse transformation.

In Figure 7 we illustrate the perturbations about the average capital distribution curve (under the Aitchison geometry) along each of the first two convex principal directions. The proportion of explained variation is for the first principal direction and for the first two. Perturbations along the first principal direction correspond to tilting of the curve about a point near the center (in log-log scale) while fixing for the most part the largest stock. On the other hand, perturbations in the second principal direction may be interpreted in terms of (correlated) fluctuations of the largest few stocks relative to the rest of the universe.

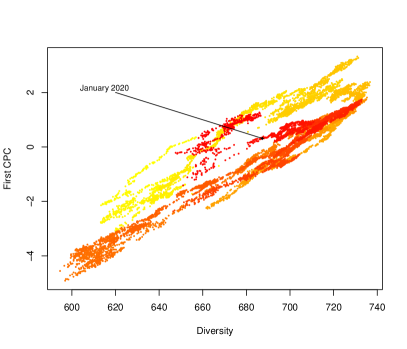

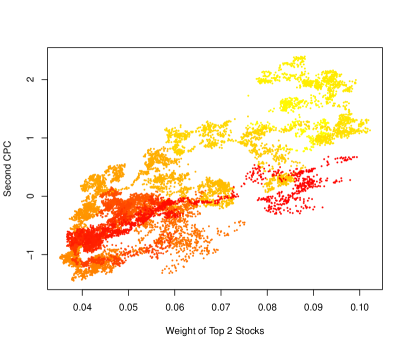

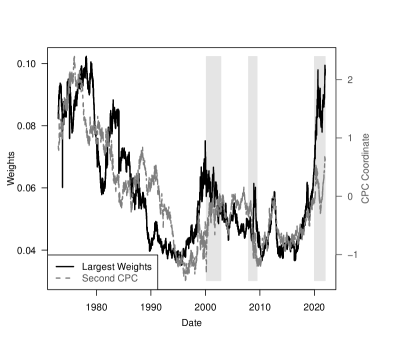

Remarkably, the first principal direction is closely related to the change in market diversity. In Figures 8 and 9 (left) we compare (i) the projected coordinates of the capital distribution curves on the first principal direction and (ii) market diversity measured by (see (6.4)) with . We observe that the two series are very strongly correlated. This finding gives a statistical justification for market diversity and suggests that it is an excellent one-dimensional summary of the capital distribution curve. We also observe that there appears to be a change in the relationship during the COVID health crisis. The relationship in Figure 8 seems to experience a parallel shift and the resulting points appear similar to those observed in the 1970s and 1980s. Turning to the second principal component (shown in Figures 8 and 9(right)), we observe a fairly significant positive correlation between the projected coordinate and the (relative and combined) weight of the largest two stocks. These findings suggest that the capital distribution curve is not as stationary as what Figure 6 and the rank-based diffusion models might suggest.

Taken together, the results of our CPCA suggest that the dominant features of the capital curve are the change in market diversity and the idiosyncratic fluctuations of the largest stocks. In future research, we plan to use these insights to improve existing rank-based models and their calibration.

7. Conclusion and discussion

In this paper we contribute to both the theory and application of convex PCA which was first introduced in [6]. We establish several new theoretical results mostly in the finite dimensional setting, and develop an efficient algorithm for solving large CPCA problems that is amenable to parallelization and complements the approach of [28]. This algorithm can be readily specialized to solve (a finite dimensional approximation of) Wasserstein geodesic PCA on a finite interval. We also provide two interesting financial applications.

We discuss here several directions for future research.

-

(i)

While we provide several consistency results in the finite dimensional case, infinite dimensional analogues of Theorems 3.2 and 3.3 remain open. In particular, we rely crucially on the compactness of the state space and that it has a nonempty interior. It appears that a different approach is needed for the general case.

-

(ii)

Existing works on Wasserstein geodesic PCA focus on the one-dimensional setting because the optimal transport maps are simply non-decreasing functions. In general, optimal transport maps are gradients of convex functions by Brenier’s theorem, but they are much less tractable when . Also, computation of the optimal transport map is much more expensive in multiple dimensions. Another direction of interest is to formulate probabilistic models for Wasserstein geodesic PCA and related algorithms.

-

(iii)

Our empirical study highlights behaviours of the capital distribution curve and rank-based properties of stocks. Naturally, we hope that these stylized properties are preserved in stochastic models of the equity market. While the statistical properties of individual asset prices have been intensively studied in financial econometrics (see e.g. [14]), it is not easy to combine them to formulate realistic macroscopic models involving hundreds or thousands of stocks. The rank-based models in stochastic portfolio theory, which are based on systems of interacting Itô processes, fail to capture short-term fluctuations that are relevant in portfolio selection, as they rely on the ergodic properties of Markov processes. On the other hand, dynamic factor models (see e.g. [4] and the references therein) capture the (possibly dynamic) correlation structure among asset returns but fail to reproduce macroscopic behaviours such as the stability of the capital distribution curve when compounded over time. The construction of realistic macroscopic models, with applications in portfolio management, is an important direction which we hope to address in future research.

Appendix A Proofs

A.1. Proofs from Section 2

A.1.1. Proof of Proposition 2.5

Lemma A.1.

Suppose is compact. Let be an increasing sequence of non-empty compact sets contained in and . Then where is the Hausdroff metric.

Proof.

By [6, Proposition 3.2]), is a compact metric space. Along a fixed subsequence there is a further subsequence along which for some compact . Since is compact, convergence under Hausdorff metric is equivalent to Kuratowski convergence (see Lemma C.5). By the definition of Kuratowski convergence (Definition C.4), for any there exists a sequence such that for each and . It follows that . On the other hand, it is easy to see that . Thus . Since the subsequence is arbitrary, we have that . ∎

A.2. Proofs from Section 3

A.2.1. Proof of Theorem 3.1

Lemma A.2.

Suppose is compact. If in then uniformly on .

Proof.

Note that is 1-Lipschitz for any . Since is compact, is uniformly bounded above. Thus, there exists a constant , independent of , such that is -Lipschitz on . By the Kantorovich-Rubenstein duality (see [36, (6.3)]), we have, for any ,

This completes the proof since by compactness of weak convergence is equivalent to convergence in . ∎

Proof of Theorem 3.1.

We proceed analogously to [6, Theorem 6.1]. As is continuous, by [15, Remark 4.8] the uniform convergence (proved in the lemma above) implies continuous convergence (Definition C.1). Moreover, by [15, Remark 4.9] continuous convergence implies -convergence. It follows that

Now [15, Proposition 6.20] gives, by the continuous convergence of , the finiteness of (by the boundedness of ), and the -convergence of the indicators, that

In view of the compactness of and Proposition C.3, this completes the proof. ∎

A.2.2. Proof of Theorem 3.2

We begin by noting a technical gap in [6, Lemma 6.1].

Remark A.3 (Technical gap in [6]).

In [6, Lemma 6.1], the authors constructed the translated sets and use them in the proof of -convergence in their Theorem 6.1. However, these sets may not be contained in . Indeed, for a counterexample it suffices to take to be the unit square in and to be one of its diagonals. Any translation of moves it, at least partially, outside of .

To overcome this technical issue, we assume that is finite dimensional and that has a nonempty interior containing the reference element . With these additional assumptions we are able to establish Theorem 3.2 and Theorem 3.3.

The following results are needed in the proof of Theorem 3.2. We say that sets are weakly linearly separable if there exists a non-zero linear functional and such that for all and .

Theorem A.4.

Let be finite dimensional and be non-empty, compact and convex sets that are not weakly linearly separable If are also non-empty, compact and convex sets with , as , then for almost all and as .

Proof.

This is a restatement of [32, Theorem 1.8.8] after noting that it holds for any finite dimensional real Hilbert space . ∎

Lemma A.5.

If is finite dimensional and are sets with , and , then and are not weakly linearly separable.

Proof.

We proceed by contradiction. If and are weakly linearly separable, there exits a non-zero linear functional and such that for all and . As , we must have for all . Choose and an -ball . Since is nonzero, there exists such that . Thus we get a contradiction. ∎

A.2.3. Proof of Theorem 3.3

The main argument (given after Lemma A.14) employs an induction on . The following lemmas are used for the induction step. In particular, the key ingredient is Lemma A.14 corresponding to part (iii) of the theorem.

We denote by the convex hull (of a set).

Lemma A.6.

Consider a Banach space over .

-

(i)

If are compact convex sets then so is .

-

(ii)

Let , , be compact convex sets and suppose there exists a compact set such that

for all . If and in Hausdorff distance then in Hausdorff distance.

Proof.

(i) Clearly is compact. By [11, Theorem 5.35] is compact. Clearly . To prove the reverse inclusion, let be given. Then there exists a sequence such that . For each , there exist and , such that . By compactness, there exists a subsequence along which , and . Thus .

(ii) First we note that in Hausdorff distance. Since is compact, by Lemma C.5 it suffices to show that . We now check the relevant conditions. (i) If then for some , and . By Hausdorff convergence there exists , such that and . Let . Then . (ii) Suppose for and is an accumulation point of . Then there exists a subsequence such that . Write where , and . Again by compactness there exists a further subsequence such that , and . So

∎

Lemma A.7.

Suppose . Let . If is either (i) a global or a (ii) nested -convex principal component, then .

Proof.

We will prove this result by contradiction. We will treat (i) as the result for (ii) is analogous. Suppose that . Then, there must exist an such that , where is the affine hull of . Additionally, we can take an open ball of sufficiently small radius about such that and . As it follows that . Now consider . It is clear that . Moreover, , (as by assumption), is convex, and is compact (see Lemma A.6). Hence and thus

by definition of . However, for any

Note here we have used that as . Also, as for any , . We conclude that

which contradicts of the optimality of . ∎

We introduce a linear transformation which will be useful in our argument.

Definition A.8.

Let be a compact and convex set in containing . For the affine span of and a vector, we define the linear transformation .

To prepare for the induction step, suppose Theorem 3.3 holds up to some . Let and take with according to the definition of . Similarly, take as in the statement of the Theorem. Define , and . Note that

It is easy to see from the compactness of that is compact.

Lemma A.9.

If then .

Proof.

We will use these sets to define linear transformations using Definition A.8. The required vector will be constructed as follows. By Lemma A.7, we have , and by definition, we have , . Consider the subspaces of given by and . Here, and throughout, for two subspaces of we will define to be their direct sum:

Since we have that either (i) , or (ii) as , there exists a such that is orthogonal to and . In this case, we fix such a to play the role of the defining vector in Definition A.8. In the former case (i), we instead take .

With this, we will now finally define

| (A.1) |

and

| (A.2) |

Next, it is important when taking the inductive step that the are consistent with . We show below that pointwise, and therefore, pointwise.

Lemma A.10.

If we have for all .

Proof.

We begin by showing the affine subspaces converge to in an appropriate sense. We recall that we must have in the Kuratowski sense (see Lemmas A.9 and C.5). Let . Consider an arbitrary orthonormal basis of and extend it to an orthonormal basis of , (where ). By definition every can be written as for some with if .

Let be arbitrary. By the Kuratowski convergence (Definition C.4) there exists a sequence with . By the compactness of the unit sphere we may extract a subsequence of the bases such that for some and all . Write . By the uniform boundedness of (as ) and the Bolzano-Weierstrass Theorem we may choose a further subsequence so that for some and all .

Using the convergence we write

As indices are such that for all we have that we may write (recall ). Notice that the convergent subsequence of bases is independent of the choice of (it relates only to ) so the same basis subsequence can be chosen for arbitrary . Thus, the representation for depending on holds for arbitrary . We conclude that . On the other hand, the orthogonality of is assured by the limit of an orthonormal sequence. Consequently, we have . As we conclude .

We will now collect these observations to prove the convergence of the projection. As the choice of basis is immaterial to the definition of the projection, the above tells us that for any subsequence we may find a further subsequence of projections that can be written in terms of some converging orthonormal bases of where (we can pick the subsequence so that ). Therefore,

As the subsequence was arbitrary, we are done. ∎

We pause here to briefly remark on the properties of our linear transformations.

Remark A.11 (Properties of and ).

We can notice that

-

(i)

,

-

(ii)

,

-

(iii)

, and;

-

(iv)

.

In (i) and (ii) we have used that . Before proceeding to our final analysis, we highlight two more important lemmas whose conclusions hold for our transformations. First, we have the following which can be proved as a straightforward consequence of the Uniform Boundedness Principle.

Lemma A.12.

If are pointwise bounded continuous linear operators with , and is continuous with for all then uniformly on compacts.

Second, we have the following standard result.

Lemma A.13.

If is such that uniformly on and is such that then .

Lemma A.14.

Let , , and with . If then, .

Proof.

As with the previous consistency results it suffices to show that (see Lemma C.6). We check the conditions in the definition (Definition C.4).

(i) Suppose . Define where and are determined through equations (A.1) and (A.2). We see that and that the convexity and compactness of is inherited by the linearity and continuity of . Next, we will see that in Hausdorff distance. By the boundedness (in operator norm) of the family , the set is contained in a (large) bounded set in . Since is finite dimensional, we can further take it to be compact. Thus, to get it suffices to show the Kuratowski convergence of to (see Lemma C.5):

(i′) Let and define . We have, in view of Lemma A.12 and Remark A.11(i), that uniformly on . Consequently, as , the convergence holds.

(ii′) Let and suppose is an accumulation point of . We have there exists a subsequence such that . By definition of there exists an such that . By compactness of extract a further subsequence such that . Applying the properties of (particularly Lemma A.13) we have

So, and we conclude .

With this established, let . Note that we must have that (see Remark A.11(iv) and argue by translation). By Lemma A.6 we have in Hausdorff distance as and . Here we also have is convex and compact (again by Lemma A.6), and . It remains to get a set that has the same properties, but is assured to be in . Define . Applying the same reasoning as in the proof of Theorem 3.2 we can make use of Theorem A.4 to get . As we are done with the first condition.

(ii) Let for . Suppose is an accumulation point of the . As we have (by Hausdorff convergence). We can conclude by compactness since for all . Hence, . Finally, by [6, Lemma A.4] and so, . This completes the proof. ∎

We are now ready to prove the theorem.

Proof of Theorem 3.3.

Since global and nested CPCA are equivalent when , the case is a consequence of Theorem 3.2.

We then argue by induction on . Suppose (i)-(iii) hold up to some . Then, along a subsequence for each and form a sequence of nested convex principal components. By Lemma A.7 the convex principal components are full dimensional. Specifically, and so all the assumptions of Lemma A.14 are satisfied for . Thus, (iii) holds for and we can then extract a further subsequence such that (i) and (ii) also hold up to . Thus by induction the theorem holds up to . ∎

A.2.4. Proof of Theorem 3.4

Proof of Theorem 3.4.

Note again by Lemma C.6 it suffices to show

We will prove the Kuratowski convergence via the definition (Definition C.4).

(i) Let be arbitrary and let . It is easy to verify that . To prove (i) it is sufficient to show that .

We will appeal to the equivalence of Kuratowski and Hausdorff convergence in the compact metric space (see Lemma C.5). First, if we have that is such that . Second, consider for and let be an accumulation point. There must exist a subsequence such that . By definition we have that each corresponds to at least one so that . By compactness of there exists a further subsequence and such that . Consider also . For all there exists an such that for sufficiently large we have , , and . Since is -Lipschitz, we have, for sufficiently large,

Since is arbitrary, we have . It follows that .

(ii) Let for . Suppose that is an accumulation point of . Then along some subsequence. As we have that (again by appealing to Kuratowski convergence). On the other hand, note that is compact so as we have that . We conclude which completes the proof. ∎

A.2.5. Proof of Theorem 3.6

We present directly the main argument, and the lemmas needed will be proved in the discussion to follow.

Proof of Theorem 3.6.

Write and consider

Since there are only finitely many data points, there exists such that the optimal has norm at most , for all and independent of . Without loss of generality, we may introduce an additional convex constraint , and we may choose such that . Let be the new convex state space which does not affect the solution. Define the correspondence

| (A.3) |

on . We now have

| (A.4) |

By Lemma A.15 below, is continuous, non-empty and compact valued. This, alongside the continuity of allows us to apply Berge’s Maximum Theorem (see Theorem C.10) to get that

is continuous on . This implies that , as an average of the continuous functions , is continuous. Berge’s Maximum Theorem also tells us that that the set of optimizers corresponding to each is upper-hemicontinuous, non-empty, and compact. By the strict convexity of in we have a unique optimizer. Hence, we also have that is a singleton. By Lemma C.8 this implies that it is continuous on when viewed as a function.∎

Lemma A.15.

Proof.

Clearly, is closed and convex as the intersection of the sub-level sets of continuously differentiable convex functions in . It is non-empty since by assumption on and . Moreover, by the last constraint is bounded for each fixed . Thus, it is compact by the Heine-Borel Theorem. Since is also convex and compact in it must define a closed interval. It remains to show that is continuous as a correspondence. To see this first consider the correspondence:

| (A.5) |

where solves for the intersection of the line with the feasible region boundary when . That is

and . Define similarly for the case when . Note that there are always two such points since by assumption the origin of the line, , is always in the interior of the feasible region and by the convexity of the region the line must exit (and hence intersect) the region at two points. By Lemma A.18 below the functions are continuous in . As a result, by Theorem C.9 is continuous as a correspondence and again by Theorem C.9 since is the convex hull of in , is also continuous as a correspondence. ∎

To prove the continuity of from (A.5) we will need some preliminary lemmas. The first is a technical result that states we can choose a full dimensional convex cone from the origin to intersect a portion of the boundary of a compact convex set with non-empty interior containing the origin. Heuristically, it says that we can shine a “flashlight” from the interior onto the boundary of a convex set.

Lemma A.16 (Flashlight lemma).

Let be a compact, convex set in for with non-empty interior containing the origin. Suppose and consider a ball of radius about , that does not contain . There exists a convex cone of rays from the origin with non-empty interior containing and (necessarily) intersecting such that .

Proof.

As by the homeomorphism we can restrict our attention to . Consider which is a dimensional sphere if , and distict points otherwise. Then, is an dimensional ball that lives in an affine subspace of that does not contain and satisfies . Let and notice that every ray in intersects at a point in . Furthermore, it is clear is full dimensional (as ) and . ∎

The second lemma characterizes the (local) solution of the equation defining the points where a constraint from in (A.3) is binding.

Lemma A.17.

Let and suppose there exists a non-zero solution to the equation

at for some . Then under the assumptions of Theorem 3.6 there exist an open set containing and a unique function such that and

In particular, if (resp. ) there exists an open set containing such that (resp. ) on .

Proof.

We begin by showing that by contradiction. Suppose that . Since is convex in the coordinate corresponding to we have that is a minimum of . However, by setting this minimality contradicts our assumption on which says . Hence, we conclude that . With this result, since we have assumed the existence of a solution to the equation we can apply the implicit function theorem to get the first result in the statement of the lemma. The second result follows taking as the preimage which is open by continuity and contains by assumption on . ∎

With this we can tackle the final result of this section.

Lemma A.18.

The functions and from (A.5) are continuous in .

Proof.

It suffices to consider . Begin by fixing a vector . The point is on the boundary of and so by Lemma C.13 this implies there is at least one such that

with . By Lemma A.17, for each for which this holds there exist an open set containing and unique functions such that and

With this established, let be the set of indices corresponding to the binding/active constraints at and let be the set of inactive constraints at (note ).

For each consider the set

Clearly by assumption. Since the are continuous, each is open. Let:

As the intersection of finitely many non-empty open sets containing , is open and non-empty. Moreover, if is in we have that for all .

Now consider the functions for given by

By the continuity of on this is continuous on . Moreover since is such that we have that is open and non-empty containing . Let

Again, is open and contains . In particular, each of the functions for are continuous on and the values of on correspond to boundary values of the level sets

Moreover, each boundary value is contained in where no other constraint is active.

Choose sufficiently small so that the ball is contained in and does not contain . Consider now our compact convex feasible set and its boundary . Since has non-empty interior by assumption, by translation we can apply Lemma A.16 to conclude there exists a cone of rays with origin and non-empty interior containing such that

Hence, since our open ball is in by assumption and every ray in intersects a boundary point (by the origin being in our convex set), we have that every ray in intersects a boundary point of our feasible set in . Since has non-empty interior and we can choose small enough so that . Translating by and scaling we obtain a ball of radius about such that every defines a ray from that intersects a boundary point in . That is, the boundary point corresponding to such a can only be associated with the boundary of a level set for some with .

Define . Clearly is open and contains . For every in , the intersection with the boundary of our feasible set is a boundary point of one of the level sets of for . Additionally, the intersection with each level set is given by a continuous function on . Taken together we have that for each , for some .

Finally, to see continuity at let and let . Let be such that . Since the are continuous on for each we have that there exists a () such that if then . Let . Since for any there is a active we have that if then:

as required since the same is also active at . Hence must be continuous at by definition of . Now since the choice of above was arbitrary in we conclude that is continuous. ∎

A.2.6. Proof of Theorem 3.7

Proof.

As in the proof of Theorem 3.6 we can again restrict to a feasible set contained in a closed ball with sufficiently large radius. Let be similarly defined as in (A.3). For each , let .

We look to apply Theorem C.11 to each subproblem in (A.4) for which we must verify the necessary assumptions. Note that as is finite dimensional Theorem C.11 (and Corollary C.12) applies to our setting once we verify the required conditions. For (i) is trivially convex. For (ii) it is clear that and , are jointly continuous in by assumption. For (iii) and (iv) we showed in Lemma A.15 that is compact valued and continuous for . For (v) this follows by our assumption on by setting . For (vi) since and are convex in for and for , , we have that Slater’s condition holds for every . This then implies that the saddle points of the Lagrangian are non-empty for every . Finally, (vii) holds since we have assumed the are continuously differentiable and it is clear this similarly holds true for the . Taken together, we obtain the result of Theorem C.11 for our problem which gives directional differentiability. Finally, to establish the points of differentiability, it suffices to note that the assumptions of Corollary C.12 hold trivially for our problem when zero or one constraint is binding at the solution corresponding to the choice . In fact, this is the only case where the assumptions hold since our minimization variable is one-dimensional. Averaging over the sub-problems indexed by gives the result in the statement of the Theorem.

We close by collecting here the form of the directional derivative and gradient for our value function. For the set of saddle points in Theorem C.11 corresponding to each inner problem we have that admits the directional derivative

where . Moreover, when is differentiable at some we have for the unique choice that the gradient takes the form

∎

Appendix B Algorithmic Considerations

We discuss here in greater detail the algorithm outlined in Section 4. In particular, we explain the evaluation of the value function and its gradient.

B.1. Optimization

We first touch on function evaluation. As mentioned in Section 4, for each , the inner minimization problem in (4.2) is easy to solve since can be identified with an interval. We first compute the usual orthogonal projection, say , of onto and check if is in . If so, then is the optimal point and otherwise, is the boundary point of which is closest to . Hence, to evaluate the objective we only need to be able to (i) verify if is in and (ii) efficiently find the boundary point(s) of for a given . The former is straightforward as it can be easily checked if . For (ii), we give the details of finding the boundary point(s) given by in Algorithm B.1.

Notice that the boundary points depend only on , and therefore are common for all the inner optimization problems in (4.2). Hence, for problems with an extremely large data set, the inner problems can be solved in parallel. On the other hand, since for extremely high dimensional problems the gradient is similarly high dimensional, it is often convenient to parallelize the gradient estimation process (e.g. by parallelizing independent central difference computations). For our purposes we implement the parallelization and function evaluation in C++ and rely on central differences for the gradient estimation. Since function evaluation is cheap using the aforementioned approach, this is a convenient way to recover the gradient.

Once this computational challenge is taken care of we can solve the resulting unconstrained optimization problem via a gradient descent approach or through other conventional solvers. Our implementation makes use of a variant of the Broyden–Fletcher–Goldfarb–Shanno (BFGS) algorithm in R available through the “nloptr” package [23]. Specifically, we take advantage of the “Rcpp” package [16] to integrate our C++ implementation with R and perform the optimizations.

For algorithms of this type a relevant question is the choice of the initial point or “guess” for the solution. This is particularly important for large problems, as if we can be intelligent about our initialization, we can substantially improve the convergence time. For our approach, we choose an initial point for each successive principal component that is suggested through an iterated application of traditional PCA techniques. The explicit choice, and the rationale behind it, will be made precise in the following discussion.

B.2. Choice of initialization point

We begin this discussion with an equivalent representation of the convex PCA objective function.

Proposition B.1 (Equivalent formulations of PCA and CPCA Problems).

Let and suppose is a dimensional subspace of . For

and denoting the CPCA objective as to make the dependence on explicit we have

-

(i)

, and;

-

(ii)

If there exists an such that then

Proof.

See Section B.3 below. ∎

Naturally, we are interested in the case where is given by the previous convex principal directions (where ). The first statement says that to solve the nested CPCA problem one may equivalently first project the data onto the orthogonal complement of the subspace spanned by the preceding principal directions and then perform the minimization. The second statement says that the solution to traditional Euclidean PCA () with full dimensional data can be recovered in the same way, but that we can further simplify to an unconstrained minimization in the nested formulation of the problem. That is, we can simply perform a Euclidean PCA on the projected data.

The key takeaway is given by the following corollary.

Corollary B.2.

Let and suppose there exists an such that . If then

Proof.

This says that the Euclidean principal component can be used to bound the value of the convex PCA problem using the representation in Proposition B.1. It is also clear that if none of the constraints defining are binding for all then the optimal values and minimizers of the two problems agree . Note that this also illustrates that, as with standard Euclidean PCA problems, the minimizer for convex PCA problems need not be unique. Most importantly, as Proposition B.1(i) says the minimizers of and in coincide, this observation suggests that a Euclidean principal direction for the projected data is a good initial guess for the convex principal direction. Indeed, they will coincide if no constraints are binding and so we expect that should be “close” to a true minimizer. Moreover, the direction is cheap to compute as it is the solution to a regular PCA problem. As a result, in our optimization routine we initialize our search at some to further accelerate convergence.

B.3. Proof of Proposition B.1

To verify this we will use the following notation:

Note that it is easy to see that for we have

| (B.1) |

Lemma B.3 (Iterated projection).

We have .

Proof.

Omitted. ∎

This will be used now to prove the following result which immediately gives us the first claim in our proposition. Namely, we now show that we may project the data while maintaining the set of minimizers.

Lemma B.4.

For we have

Proof.

If we have, for any ,

Note the fourth equality follows by Lemma B.3 as

Now, since the second term on the right hand side is constant in the claim in the lemma then follows after averaging over the . ∎

We now proceed to present a result whose statement implies the second claim of the proposition.

Lemma B.5.

For we have

and if for at least one then the minimizers coincide.

Proof.

It suffices to show the relation “” as the inequality “” is immediate. We have using the definition of the projection for that for any :

Now by the orthogonal decomposition for and linearity of the inner product

where the last equality follows by orthogonality. Hence we have:

Consequently for any with we get:

If then . Otherwise, and equality holds in the above with which is admissible for any with . Hence, it is clear that we have

from which the claimed equality follows.

It remains to see that if for at least one then the minimizers must coincide. It is clear that if then and so if then it is not a minimizer of the RHS as it can be strictly improved upon. Moreover, if and then the chain of inequalities derived above is strict so cannot be a minimizer of the RHS as is an improvement. We conclude that any minimizer of the RHS must be in from which the claim follows. ∎

With these results in hand, we formally summarize the conclusions below to complete the proof of the proposition.

Appendix C Miscellaneous definitions and results

C.1. Convergence of sets and functions

Throughout this subsection we let a metric space be given. For , we let be the set of all open neighborhoods of . Let , , and be functions from to .

Definition C.1 (Continuous convergence).

[15, Definition 4.7] We say that continuously converges to if for every and every neighborhood of there exists an integer and , such that for and we have .

Definition C.2 (-convergence).

[15, Proposition 8.1] We say that -converges to , denoted , if the following holds for all .

-

(i)

for any , with and;

-

(ii)

There exists , , with such that .

Proposition C.3.

[15, Theorems 7.8 and 7.23] Suppose that is compact and . Then is non-empty, , and if , then the accumulation points of belong to .

Definition C.4 (Kuratowski Convergence).

[15, Remark 8.2.] Let , . We say that the converges to in the sense of Kuratowski, denoted by , if

-

(i)

for all , there exists a constant and for such that , and;

-

(ii)

for all , , and for any accumulation point of , .

Lemma C.5.

[6, Remark A.2] Convergence with respect to the Hausdorff distance implies convergence in the sense of Kuratowski. Moreover, if is compact both notions of convergence coincide.

Lemma C.6.

[3, Proposition 4.15] If for then if and only if .

C.2. Correspondence and Berge’s Maximum Theorem

The following definitions and results, which can be found in [11], are used to prove Theorem 3.6. Recall that a correspondence maps each to a subset of . Here we assume that and are topological spaces. The graph of is defined by

Definition C.7.

Let be a correspondence and .

-

(i)

We say that is upper hemicontinuous at if for every neighborhood of , there is a neighborhood of such that implies .

-

(ii)

We say that lower hemicontinuous at the point if for every open set that intersects , there is a neighborhood of such that implies .

If is both upper and lower hemicontinuous at we say it is continuous at .

Lemma C.8.

A singleton-valued correspondence is upper hemicontinuous if and only if it is lower hemicontinous, in which case it is continuous as a function.

Theorem C.9.

Given , define a correspondence by . If each is continuous at some point then:

-

(i)

is continuous at .

-

(ii)

If is a locally convex topological vector space, then the correspondence is also continuous at .

Theorem C.10 (Berge’s Maximum Theorem).

Let be a continuous correspondence such that each is a nomempty compact subset of , and let be continuous. Define the value function by

and the correspondence of maximizers by

Then: is continuous and has non-empty compact values. Moreover, if either has a continuous extension to all of or is Hausdorff, then is upper hemicontinuous.

C.3. Generalized envelope theorem

The following result, taken from [26, Theorem 1] is used in the proof of Theorem 3.7. For convenience, we state the result using notations that are compatible with ours.

Theorem C.11 (Generalized envelope theorem).

Consider the problem

where , and and are real-vaued functions on . For consider the Lagrangian

and assume that the following regularity conditions hold.

-

(i)

The set is convex.

-

(ii)

The functions and , , are continuous on .

-

(iii)

The constraint set is compact for every .

-

(iv)

The correspondence is continuous.

-

(v)

For every there exist and such that and for .

-

(vi)

The set of saddle-points of , which has the form , is non-empty for every .101010For the definition of saddle point see [26, Section 2].

-

(vii)

The gradients with respect to , , exist and are jointly continuous in .

Then the directional derivatives of exist for and are given by

and the order of maximum and minimum does not matter.

Corollary C.12.

Suppose that in addition to the assumptions of Theorem C.11 the following conditions hold at a given :

-

(i)

is strictly concave in and is concave in , .

-

(ii)

and are continuously differentiable in .

-

(iii)

The Linear Independence Constraint Qualification (LICQ) holds. That is, the vectors are linearly independent for binding constraints .

Then the saddle-point is unique and the gradient of exists at and is given by

C.4. Miscellaneous results

The following lemma summarizes some properties of level sets of convex functions. Details can be found in [30].

Lemma C.13.

Let be convex. Then is open and convex. If is non-empty then the closure of is given by and . In particular, we have .

Now let be convex, and let . Suppose is nonempty. Then .

Acknowledgment

This work is partially supported by NSERC Grant RGPIN-2019-04419, a Seed Funding for Methodologists Grant from the Data Sciences Institute (DSI) at the University of Toronto, and an NSERC Alexander Graham Bell Canada Graduate Scholarship (Application No. CGSD3-535625-2019).

References

- [1] H. Abdi and L. J. Williams. Principal component analysis. Wiley Interdisciplinary Reviews: Computational Statistics, 2(4):433–459, 2010.

- [2] A. Agapova, R. Ferguson, and J. Greene. Market diversity and the performance of activelymanaged portfolios. The Journal of Portfolio Management, 38(1):48–59, 2011.

- [3] H. Attouch. Variational Convergence for Functions and Operators, volume 1. Pitman Advanced Publishing Program, 1984.

- [4] J. Bai and P. Wang. Econometric analysis of large factor models. Annual Review of Economics, 8:53–80, 2016.

- [5] M. Beraha and M. Pegoraro. Wasserstein principal component analysis for circular measures. arXiv preprint arXiv:2304.02402, 2023.

- [6] J. Bigot, R. Gouet, T. Klein, and A. López. Geodesic PCA in the Wasserstein space by convex PCA. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 53(1):1–26, 2017.

- [7] E. M. Bronshtein and L. Ivanov. The approximation of convex sets by polyhedra. Sibirskii matematicheskii zhurnal, 16(5):1110–1112, 1975.

- [8] S. Campbell and T.-K. L. Wong. Functional portfolio optimization in stochastic portfolio theory. SIAM Journal on Financial Mathematics, 13(2):576–618, 2022.

- [9] E. Cazelles, V. Seguy, J. Bigot, M. Cuturi, and N. Papadakis. Geodesic pca versus log-pca of histograms in the wasserstein space. SIAM Journal on Scientific Computing, 40(2):B429–B456, 2018.

- [10] Center for Research in Security Prices (CRSP). CRSP US Stock Database. http://www.crsp.org/products/research-products/crsp-us-stock-databases, 2021.

- [11] D. Charalambos and B. Aliprantis. Infinite Dimensional Analysis: A Hitchhiker’s Guide. Springer, 2006.

- [12] Y. Chen, Z. Lin, and H.-G. Müller. Wasserstein regression. Journal of the American Statistical Association, pages 1–14, 2021.

- [13] M. Collins, S. Dasgupta, and R. E. Schapire. A generalization of principal components analysis to the exponential family. Advances in Neural Information Processing Systems, 14, 2001.

- [14] R. Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2):223, 2001.

- [15] G. Dal Maso. An Introduction to -Convergence, volume 8. Springer Science & Business Media, 2012.

- [16] D. Eddelbuettel and R. François. Rcpp: Seamless R and C++ integration. Journal of Statistical Software, 40(8):1–18, 2011.