Space-grid approximations of hybrid stochastic differential equations and first passage properties

Hansjoerg Albrecher

Faculty of Business and Economics,

University of Lausanne,

Quartier de Chambronne,

1015 Lausanne,

Switzerland

hansjoerg.albrecher@unil.ch and Oscar Peralta

Faculty of Business and Economics,

University of Lausanne,

Quartier de Chambronne,

1015 Lausanne,

Switzerland

oscar.peraltagutierrez@unil.ch

Abstract.

Hybrid stochastic differential equations are a useful tool to model continuously varying stochastic systems which are modulated by a random environment that may depend on the system state itself. In this paper, we establish the pathwise convergence of the solutions to hybrid stochastic differential equations via space-grid discretizations. While time-grid discretizations are a classical approach for simulation purposes, our space-grid discretization provides a link with multi-regime Markov modulated Brownian motions, leading to computational tractability. We exploit our convergence result to obtain efficient approximations to first passage probabilities and expected occupation times of the solutions hybrid stochastic differential equations, results which are the first of their kind for such a robust framework. We finally illustrate the performanced of the resulting approximations in numerical examples.

1. Introduction

Stochastic systems that enjoy some sort of modulation have attracted considerable attention in probability, both from applied and theoretical perspectives. Examples of these are Markov-modulated Poisson processes [14], Markov additive processes [5, Chapter XI] and regime-switching stochastic differential equations [28, Section II.2], which have found applications in risk theory [6, Chapter VII], queueing [27] and finance [13], just to name a few. The main appeal behind this framework comes from the flexibility when modelling phenomena whose parameters depend on random environmental factors. For instance, modulation may be used to model correlated catastrophic events in insurance, different workload regimes in a queue, or seasonal sentiment changes in financial markets. In case the modulation is Markovian, a robust toolbox of matrix-analytic methods has been developed to compute relevant qualities; see e.g. [9] and references therein.

In this manuscript, we are interested in a class of processes whose dynamics are described by a continuously varying component which arises as the solution of a stochastic differential equation, and an environmental finite-state component which is modelled after a jump process that may or may not be Markovian. Such a class of processes is referred to in the literature as hybrid stochastic differential equations (hybrid SDEs), which generically take the form

(1.1)

where is a Brownian motion, is the environmental process, and and are real functions which satisfy certain regularity conditions.

In particular, we will be interested in hybrid SDEs which exhibit the following characteristics:

•

The process is continuous and one-dimensional.

•

At a given instant, the environmental process switches state with an intensity that is dependent on the main component.

In simpler words, the class of hybrid SDEs we are interested in has components whose evolution is interlaced and dependent on each other. This contrasts with the Markov-modulated case, where one is able to draw a path of the environmental component without any knowledge of the main one (see [25]). In order to highlight this interlacing feature, in the literature such a model is referred to as hybrid SDEs with state-dependent switching; here we will simply call them hybrid SDEs for brevity.

Existence, uniqueness and stability properties for hybrid SDEs have been extensively studied in recent years [33, 24, 34]. Another stream of research lies in investigating efficient simulation methods of hybrid SDEs, most of them relying on adapating well-known convergence results into this considerably more challenging scenario [32, 25]. However, computing explicit probabilistic descriptors for such a class of processes has been proven challenging, even in simple scenarios. For instance, several descriptors for Markov-modulated Brownian motion have been explicitly obtained in the literature (see e.g. [4, 20, 11, 12, 26]), but virtually none of these results have been extended to hybrid SDEs, even in the Markovian case. Such a task seems intractable simply because the toolbox for general diffusions is considerably more limited than the one available for the Brownian motion.

Our contributions to the literature of hybrid SDEs are the following. In a first instance, we provide a novel pathwise approximation technique by means of a space-grid discretization, resulting in approximations which belong to the class of multi-regime Markov-modulated Brownian motions. The latter are processes that, when restricted to each band of the space-grid, behave like a Markov-modulated Brownian motion. While Wong-Zakai or Euler-Maruyama are the most common approximation methods for simulation of hybrid SDEs in the literature, our proposed approximation sets the course to exploit aspects that are currently only knowm for multi-regime Markov-modulated Brownian motions. As an example, we employ our pathwise approximation result to provide approximations for the descriptors for first exit times of a hybrid SDEs over a band , , using recent results on the stationary measures of multi-regime Markov-modulated Brownian motion in queueing theory [18, 1]. We remark that, to the best of our knowledge, this is the first attempt to compute first passage probabilities and expected occupation times for hybrid SDEs, even when reduced to the case in which the environmental process is Markovian.

The structure of this paper is as follows. In Section 2, we provide the proper framework to construct strong solutions to hybrid SDEs via the uniformization method and concatenation of paths. Later, in Section 3, we construct the proposed multi-regime Markov-modulated Brownian motion approximation, and prove its uniform convergence in probability to the original hybrid SDE over increasing compact intervals. This approximation result is carried over in two steps by considering an auxiliary process, which serves as a middle point to prove our main result in Theorem 3.6. In Section 4 we show how our convergence result can be applied to approximate first passage probabilities of hybrid SDEs, as well as its expected occupation times; some numerical examples of such approximations are explored as well. Finally, in Section 5 we provide a brief summary of our findings, along with a discussion on some avenues of further research.

2. Hybrid stochastic differential equations

Let us provide a precise description of a hybrid SDE and its solution , for which we require a complete probability space that supports the following independent components:

•

A standard Brownian motion ; this will dictate the continuously-varying nature of .

•

A Poisson process of a sufficiently large parameter , and a sequence of i.i.d. random variables: these will be used to describe the jump dynamics of , with marking the epochs at which jumps occur, and dictating where the th jump leads to.

Our first goal is to rigorously construct a pair that solves the hybrid SDE

(2.1)

where is an a.s. continuous real process,

is a càdlàg jump process with finite state space , , , and .

Furthermore, we require that is adapted to the -completed filtration generated by . A pair satisfying the aforementioned characteristics is called a strong solution of (2.1).

Remark 2.1.

In the context of classic Itô diffusions, a strong solution to an SDE needs to be adapted to the filtration generated by the driving noise component only. In the case of hybrid stochastic differential equations, there is an additional stochastic component, the environmental process , which is why the term ‘strong solution’ needs to be modified in the hybrid SDE framework.

In this paper we are interested in hybrid SDEs whose environmental process switches at a state-dependent rate. Specifically, we let evolve according to

(2.2)

for some family of intensity matrices which, at this stage, we assume to be continuous w.r.t. .

Note that (2.1) characterises part of the pathwise construction of . Indeed if was given, then we could solve during sojourn times of with fixed drift and diffusion coefficients, updating them at each jump time of . However, (2.2) does not tell us how is meant to be constructed, it only provides a distributional property, implying that one needs a construction whose characteristics coincide with (2.2). This would not be a problem if, for instance, , , for some intensity matrix ; in such a case of a Markov-modulated diffusion, the evolution of does not depend on the values of , and thus can be constructed via uniformization arguments using the Poisson process and the sequence only (see [25] for more details). In the general case of hybrid SDEs, the construction is more involved since evolves using information provided by . Below we discuss a construction developed in [3] which relies on using a related inhomogeneous uniformization argument. First, we state some assumptions needed.

Assumption 1.

For all , and are Lipschitz-continuous. i.e. there exists some such that

Assumption 2.

The family is uniformly bounded, i.e.

Under Assumption 1, we can guarantee the existence of a unique and strong solution to the (ordinary) stochastic differential equation (SDE)

(2.3)

for all , and , where is a time-shifted version of . In other words, corresponds to the solution of the SDE driven by , with coefficients and , and starting point . On the other hand, Assumption 2 tells us that the jumps of are dominated by those of a Poisson process of intensity , meaning that we can use the arrival points of as the (possible) jump epochs of .

The precise construction of is as follows. Let denote the arrival times of (with ). Define and , and for , let and : we have defined the processes and in . Since we want to be continuous, we ought to define . For , we decide if it jumps or not at time employing the values of and as follows:

(2.4)

Although at a first look (2.4) may look complex, we are simply using and in such a way that jumps to State at time with a mass given by the -th entry of the probability matrix , the uniformized version of (which we rigorously verify in Lemma 2.1). After having defined in , we construct in subsequent intervals by concatenating strong solutions of the type (2.3) with appropriate chosen values for , as well as using a decision rule similar to (2.4) to establish which states visits. More specifically, in a recursive manner, for and let

(2.5)

(2.6)

(2.7)

(2.8)

where , and

A few aspects that are straightforward to verify about this construction:

•

and are -adapted,

•

is continuous at , and thus, has a.s. continuous paths,

Note that is the unique solution to (2.1) under this particular construction of . Indeed, if we choose a different construction of , the process may take another form. For instance, use the r.v.’s instead of in (2.8); the process will then be different and so will .

We still need to verify that (2.2) holds, which we prove in a slightly more general scenario next. Recall that (2.2) only makes sense if is continuous w.r.t. . A generalization of this property for discontinuous is given by

(2.9)

(2.10)

where is the -completion of the -algebra generated by . In essence, (2.9) and (2.10) correspond to how inhomogeneous Markov jump processes are classically constructed through their integrated jump intensities/hazard rates (see e.g. [29, Ch. 13]). That (2.9) and (2.10) imply (2.2) for continuous is readily obtained by noting that

where we employed the continuity of too. For sake of completeness, we now show that (2.9) and (2.10) indeed hold; this proof is a simplified version of an analogous result found in [3].

Lemma 2.1.

Let be constructed via (2.5)-(2.8). Then (2.9) and (2.10) hold.

Proof.

Integrating with respect to the number and position of arrivals in , say ,

where in the first equality we used that on the event , for all by construction. Finally, for

completing the proof.

∎

We note that the construction of strong solutions for hybrid SDEs can be carried on in more general scenarios. For instance, Brownian-driven multidimensional hybrid SDEs with unbounded jump intensities are considered in [24], while the construction discussed in [3] concerns multidimensional past-dependent hybrid SDEs driven by Lévy processes.

3. Space-grid approximation of hybrid SDEs

Although solutions to state-dependent hybrid SDEs are easy to simulate following the steps in (2.5)-(2.8), studying their distributional properties is a challenging task (see [33] and references therein). Here we advocate to study hybrid SDEs using an approximation method via discretizing the space-grid.

Let be as in Section 2. For each , let and be a piecewise constant approximation of and on a space-grid of . In this paper, we assume the following properties.

Assumption 3.

For each :

•

and are right-continuous with left limits,

•

and ,

•

and are such that the stochastic differential equation

(3.1)

admits a strong and unique solution for all and ,

•

the space-grid has a finite cardinality.

Below we present an elementary stability condition that is useful for our forthcoming developments.

Lemma 3.1.

Let and be the solutions of (2.3) and (3.1), respectively, where , , and attain Assumptions 1 and 3. Then,

Proof.

The -uniform boundedness over compact intervals of is a standard result, which we briefly replicate below for the sake of completeness. Let , so that

By Cauchy-Schwartz,

By Doob’s inequality and Itô isometry,

By the Assumption 1, and must be at most linearly increasing, meaning that there exists some such that

Then,

where and . Gronwall’s lemma then yields

by letting , we get that . Now, since and , then and are at most linearly increasing as well. Given this, the statement concerning follows by analogous arguments to the previously presented.

∎

Remark 3.1.

Finding conditions under which a stochastic differential equation with discontinuous coefficients has a unique strong solution is an active area of research in recent years. For instance, in [21] it is established that (3.1) has a unique and strong solution for and general measurable function that attains certain integrability properties. In [22], the same result is established for Lipschitz-continuous functions and piecewise Lipschitz-continuous functions , both assumed to be bounded. Given the nature of and as piecewise constant approximations of and , and taking into account the existing results in [21] and [22], our setup allows for the case in which and are constant, and and are bounded functions. Other possible setups that produce strong and unique solutions to (3.1) ought to be studied on a case by case basis, a topic which goes beyond the scope of this manuscript.

Now, let be a càdlàg -adapted jump process whose jump intensities are of the form

(3.2)

with being a piecewise constant approximation of over the space-grid .

Under Assumption 3 and supposing that the path is somehow known, the solution to the hybrid SDE

(3.3)

can be constructed by a piecewise concatenation of paths, analogously to (2.5)-(2.6). The resulting process is such that, when restricted to a space interval and to the time intervals for which is equal to , behaves like a Brownian motion with drift and noise coefficient . In fact, the process falls within the class of multi-regime Markov-modulated Brownian motions studied in [18] (see [23] for an earlier reference in the case ). Heuristically speaking, since the functions , and are space-grid approximations of , and , one can expect that approximates the original solution . A main purpose of this paper is to formalize this statement.

Remark 3.2.

In the previous paragraph we did not specify how is constructed. This was on purpose: while it is straightforward to follow analogous steps to those in (2.7)-(2.8) to define , here we need to follow slightly different steps in order to guarantee the pathwise convergence of to . The specifics of such a construction are contained in Subsection 3.2.

To prove pathwise convergence of to as some of its parameters go to , we need to proceed with care. First we study the unique continuous strong solution to

(3.4)

where is the jump process constructed through (2.5)-(2.8), while is recursively defined by

(3.5)

The practicality of the process is essentially null. is an approximation to ; however, it needs and to be constructed. This does not mean that it is ill-defined; in fact, once is constructed (which can be done without issues following (2.5)-(2.8)), then simply arises as a concatenation of solution paths. Instead, the real usefulness of is in providing an intermediate step towards quantifying the approximation error : we will first measure (discretization error brought by and ) and then the discrepancy between and (discretization error brought by ).

3.1. Measuring .

In order to quantify the approximation error of to , let us first measure the uniform mean-square distance over compact time intervals between and in the case (that is, no switching occurs). Abusing notation for a brief moment, let us write , , and instead of , , and , respectively.

As usual, mean-square convergence implies convergence in probability, which in our case takes the following explicit form.

Corollary 3.3.

Suppose that and that there exists some such that

(3.13)

Then, for any ,

Proof.

Markov’s inequality and Theorem 3.2 imply that for any ,

The result follows by choosing .

∎

Corollary 3.3 implies that we can choose appropriate values of and which are dependent on , say and , such that

(3.14)

and then conclude that the path converges in probability to uniformly over increasing compact intervals. Here we choose and for some . In such a case, there exists some such that for all ,

(3.15)

where ; note that does not depend on the choice of or . In light of this, we assume the following.

Assumption 4.

There exists some and such that for each , the approximation (constructed as in (3.4) where the coefficients and now show an explicit dependence on via their superscript) satisfies

While it might seem that the proof in Theorem 3.2 can be easily modified to handle the general case , the switching caused by destroys the local martingale property of the involved stochastic integrals, and thus, the Burkholder-Davis-Gundy inequality no longer applies. For this reason, our approach is to study the discrepancy between and by concatenating paths at the time epochs for which switching can occur. We explicitly do this in the proof below.

Theorem 3.4.

Let and fix some small . As ,

where .

Proof.

First, we claim that

(3.16)

Indeed, using [16, Proposition 1], for sufficiently large

(3.17)

the first element in the product of the r.h.s. in (3.17) clearly converges to , while the second element is bounded by

Now, fix some large and for all let

Note that

where the last inequality follows by using Corollary 3.3 and (3.15) for all and , . Finally, for sufficiently large (large enough that for all ),

so that

∎

Now that we have assessed the convergence of to , we will continue with the discrepancy between and in the following section, which will ultimately lead to measuring the final error .

3.2. Measuring .

Assessing the discrepancy between and relies on the following key observation: is identical to in a compact interval if coincides with in that interval. Thus, the question of convergence of to may be posed as a question of if/when the process differs from . In order to answer this, we borrow the decoupling idea introduced in [3]. This concept relies on constructing the approximation (understood as the process with an explicit dependence on some parameter ; we omit such dependence in some places for notational convenience) in such a way that this process decouples or stops being identical to in an interval with a probability that tends to as . As announced in Remark 3.2, instead of constructing via (2.7)-(2.8), below we describe an alternative (but similar) technique that yields the distributional property (3.2) as well.

First, let us add an extra process which tracks the decoupling event of w.r.t. at the time epochs . Roughly speaking, we say a decoupling occurs at time if we can no longer guarantee that , but we can still guarantee that is identical to on . To properly define this, we consider a process taking values in , where will signify that the decoupling has not occurred by time , will signify that the decoupling occured exactly at time , and will signify that a decoupling occurred before time . More specifically, let , , ,

and recursively define for and ,

(3.18)

(3.19)

(3.20)

(3.21)

(3.22)

(3.23)

where , and .

Here the notation ‘’ for denotes ‘ is sampled from ’.

While Equations (3.18)-(3.20) are analogous to their counterpart (2.5)-(2.7), note that (3.21)-(3.23) are slightly more involved than (2.8). Nevertheless, the idea is similar: is constructed in such a way that at the uniformization epoch , it lands in State with probability . Indeed, if , then in order to land in , either

•

is in (with probability ), or

•

lands in and then gets sampled from the vector (with probability ).

In the second case, a decoupling is declared at that step and we let ; under these circumstances, by construction we can still guarantee that (compare (2.8) and (3.21)-(3.23)) and (compare (3.5) and (3.18)-(3.19)). Once a decoupling occurs, further jumps of at the uniformization epochs occur by sampling directly from the vector , which are points in time at which we can no longer guarantee that and are identical (ditto and ). Fortunately, since is thought to be close to , so is to , suggesting that the probability of a decoupling at a given step must be low. In the rest of the section, we investigate a stronger statement: decoupling occurs with low probability in any compact time interval.

Similarly to Assumption 4, let us now make explicit the dependence of , and on via a superscript. In order to obtain convergence rates of the decoupling of w.r.t. , we impose the following regularity condition on .

Assumption 5.

For a square matrix , let denote the norm defined by

The intensity matrix is -Hölder continuous, in the sense that there exists a constant such that for any ,

Furthermore, is right-continuous with left limits and converges uniformly to at a -rate, more specifically,

Remark 3.3.

Under Assumption 5, does not admit any discontinuities, however,

recall that -Hölder continuity is considerably less restrictive than Hölder- or Lipschitz-continuity. This means that we can mimic a discontinuous behaviour for at a point by considering instead some steep function which behaves like for sufficiently close .

Lemma 3.5.

Fix some small . Then,

(3.24)

Additionally, Equation (3.24) also holds when is replaced by .

Proof.

For notational convenience, let us write instead of , and instead of . Note that

(3.25)

By conditioning on the history of the processes up to time and letting

which proves (3.24). Finally, following the same set inclusions in (3.25), we get

since on the paths and are the same, then

so the result for the case follows by identical steps to those in (3.26).

∎

Now we are ready to prove the main result of the paper.

Theorem 3.6.

For any fixed ,

(3.27)

Proof.

Define the events

Given that on the event the paths and are identical, then

Taking this into account, by standard set inclusion/exclusion operations we get

(3.28)

Employing (3.28) and additional standard set operations lead to the inclusions

which in turn implies that

(3.29)

Since each one of the summands on the r.h.s. of (3.29) are shown to be as in Theorem 3.4, Lemma 3.5 and (3.29), respectively, the result follows.

∎

Theorem 3.6 essentially tells us that under Assumptions 1-5, there exists a sequence of multi-regime Markov-modulated Brownian motions that converge in probability to the solution of a hybrid stochastic differential equation, as well as their respective underlying processes and ; such a convergence occurs in a uniform sense over increasing compact intervals. In particular, this implies that any first passage times of , say into the set or , can be approximated by the corresponding first passage times of . In the next section, we exploit this to provide efficient approximations to certain first passage probabilities for hybrid stochastic differential equations.

4. First passage probabilities and expected occupation times for solutions of hybrid SDEs

Define the first passage times , (). For , we are interested in providing approximations for the Laplace transform of the first passage times,

for and . In essence, the functions and characterize the distributional law of the exit times of from the band . Employing the law of total probability, it is straightforward to reinterpret and as

where is an random variable independent of everything else; from now on, we adopt this reinterpretation.

In the existing literature, explicit solutions to and only exist in very simple scenarios: either and (see e.g. [19, Chapter 4]), or and are constant for all (see e.g. [20]). Moreover, we are as well interested in the present value of the expected ocupation times in State while below level , defined as

Similarly to and , here we reinterpret as

In this section we propose to exploit the approximations laid out in Theorem 3.6, along with the existing theory for multi-regime Markov-modulated Brownian motions, to provide an efficient approximation scheme based on computing

where and . Indeed, the convergence in probability over increasing compact intervals of Theorem 3.6 yields the convergence in probability of and to and , respectively. Due to the continuity of paths of and , this readily translates to the pointwise convergence of the functions and to and . Additionally, under the assumption , the dominated convergence theorem implies the convergence of to .

While the functions and are not readily available in the existing literature, we can compute them by embedding independent copies of the excursion into a certain recurrent queue on the strip (that is, a process reflected on the level boundaries and ). This procedure is similar to the ones exploited in [30, 31, 1] to provide finite-time ruin probabilities for multi-regime Markov-modulated risk processes or its subclasses. Below we spell out the details of our construction.

Let be a sequence of independent copies of . Here we assume that the total length of each excursion , say , has finite mean; this trivially holds if , or if either or have a finite mean. Additionally, let our probability space support three independent sequences of -distributed i.i.d. random variables , and . Based on the construction of multi-regime queues in [18, 1], here we define on a space grid (with , and ) modulated by the jump process that has a state space , both of which evolve as follows:

(1)

On the time interval with , let coincide with .

(2)

At time , one of three events happens:

•

If , let and for all .

•

If , let and for all .

•

If , let .

(3)

At time , one of two events happens:

•

If , let increase at unit rate up to reaching level , say, at time . Let for all .

•

If , let decrease at unit rate up to reaching level , say, at time . Let for all .

(4)

Let and for all .

(5)

Repeat Steps (1)-(4) for shifting the time accordingly in order to concatenate the excursions along with the increasing sequences , . This produces a process that regenerates at the epochs .

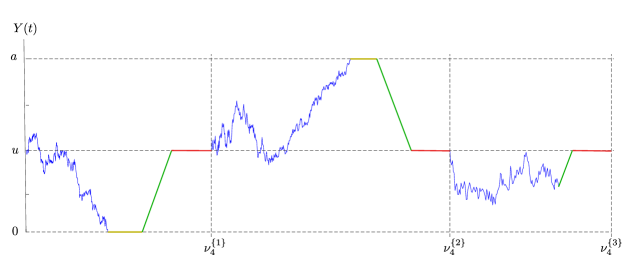

See Figure 4.1 for a graphic description of the aforementioned construction.

Figure 4.1. Queue model resulting from concatenating using Steps (1)-(4), which are shown in colors blue, mustard, green and red, respectively.

As pointed out earlier, the process falls within the class of multi-regime Markov-modulated Brownian motion queueing models (see [18, 1] for details), which has a law characterized by the level-dependent matrices with the following interpretation:

•

is the jump intensity of from to while is in level . We further specify the dependence on the level by employing intensity matrices and where

•

is the drift of at level while is in State (by convention we let for all ). We further specify this dependence on the level by employing diagonal matrices and where

•

is the diffusion coefficient of at level while is in State (by convention we let for all ). We further specify the dependence on the level by employing nonnegative diagonal matrices where

Under the previous considerations, the corresponding matrices for our particular model with state space take the form

where denotes the th canonical row vector, and denotes the diagonal matrix with the elements filling the diagonal. In [18], the authors provide an efficient algorithm to compute the steady state distribution of . In particular, using their method we are able obtain:

•

the steady state probability atoms for levels and while on the states in row vector form, say and where

•

the steady state probability atoms for level while on the State , say where

•

the steady state probability distribution function while on State over , say where

Below we link these quantities with the first passage probabilities and , as well as with the expected occupation times .

Theorem 4.1.

Suppose that . Then,

(4.1)

Moreover,

(4.2)

Proof.

The process regenerates at the epochs , all of which have a (common) finite first moment. This in turn implies that is positive recurrent, so by [17, Theorem 1],

where we used that .

Employing similar arguments we get

In short, with the help of the algorithms developed in [18], one is able to efficiently compute first passage probabilities and their expected occupation times for using Theorem 4.1, which in turn approximates the first passage probabilities and their expected occupation times for by virtue of Theorem 3.6. Below we explore a couple of synthetic examples.

Example 1.

Consider a three-state hybrid SDE evolving in the space-band with parameters

In essence, the process has a force pushing it upwards while is in any of the three states. The force is weakest while in State and strongest while in ; note that the difference between regimes is accentuated as gets closer to level . In the context of actuarial science, this may e.g. describe the case of the surplus process of an insurance company with three possibly occurring regimes, all with positive drift, but in some being more responsive with premium reductions when the surplus approaches .

This can be described, for instance, by an intensity matrix function of the form

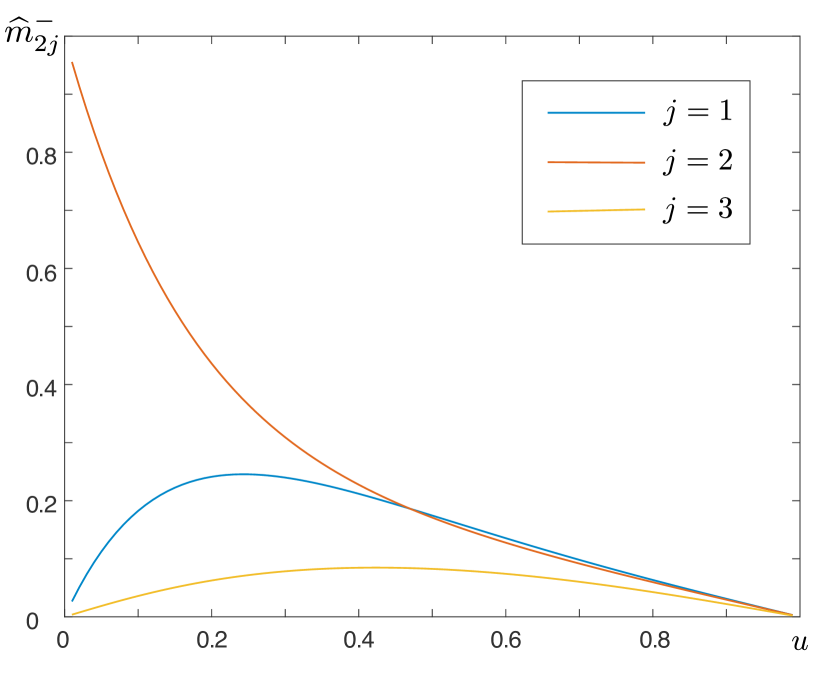

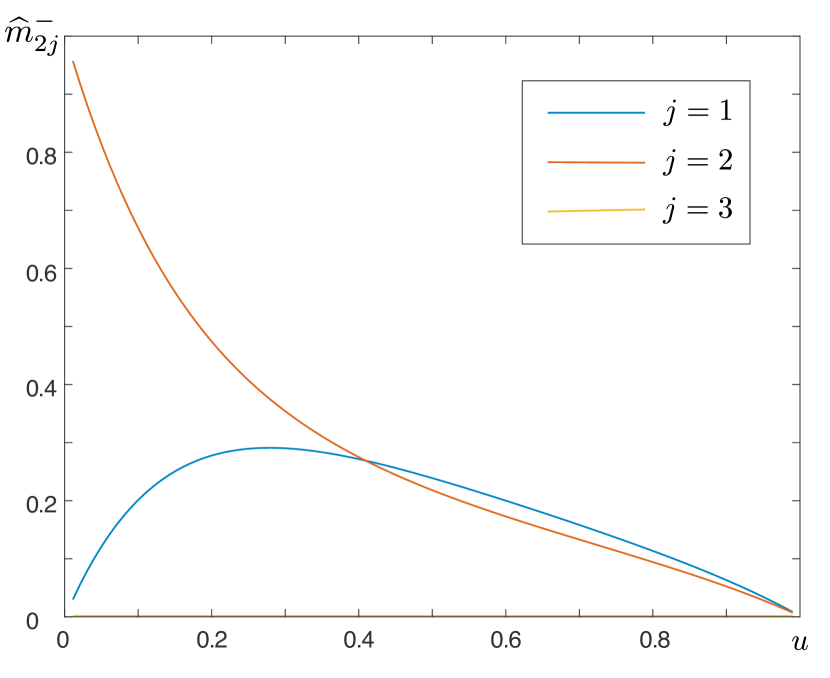

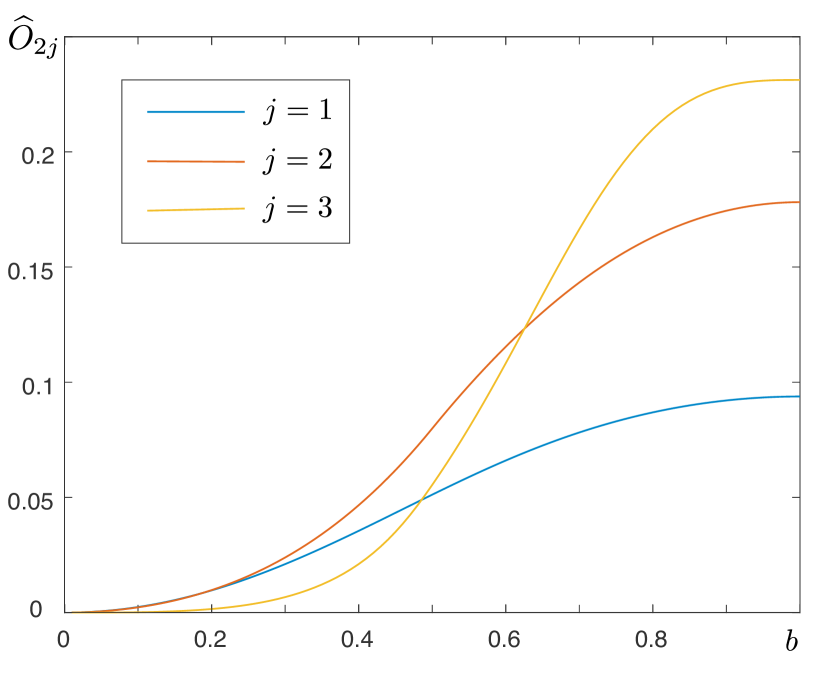

Employing the Matlab coded provided in http://www.hit.bme.hu/~ghorvath based on [18] together with Theorem 4.1, we are able to compute the first passage probabilities and expected occupation times of the multi-regime Markov-modulated Brownian motion that approximates . We perform such computations for , , and , with results shown in Figure 4.2.

Figure 4.2. Left: Plots of as a function of . Right: Plots of as a function of with . Each plot contains the cases .

For small values of , downcrossings of level are most likely while in State ; this can be explained by noting that the random oscillations while in State (the initial state of ) can produce a downcrossing before a switching even occurs. For medium values of , the probabilities of downcrossing level while in States and are comparable, both of which are considerably larger than that corresponding to State ; this is due to the state-dependent switching behaviour of which favours States and while the level is low, and and while the level is high. For high values of , the probability of downcrossing is uniformly low for all states. On the other hand, we can observe that the expected occupation time while in State is larger than that in State or uniformly over all ; this is a consequence of State being the initial state of the system.

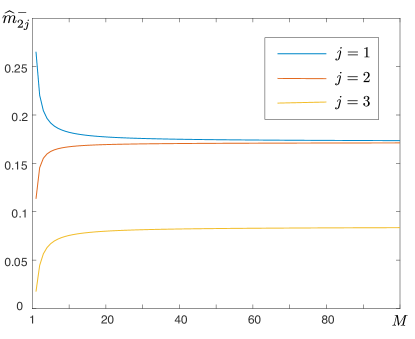

While Theorem 3.6 guarantees that converges to as the space-grid becomes denser, in Figure 4.3 we (empirically) show how fast this convergence happens.

Figure 4.3. Plots of as a function of for the cases .

As we can appreciate from the plot, convergence is quickly achieved, with differences between the cases being essentially negligible for .

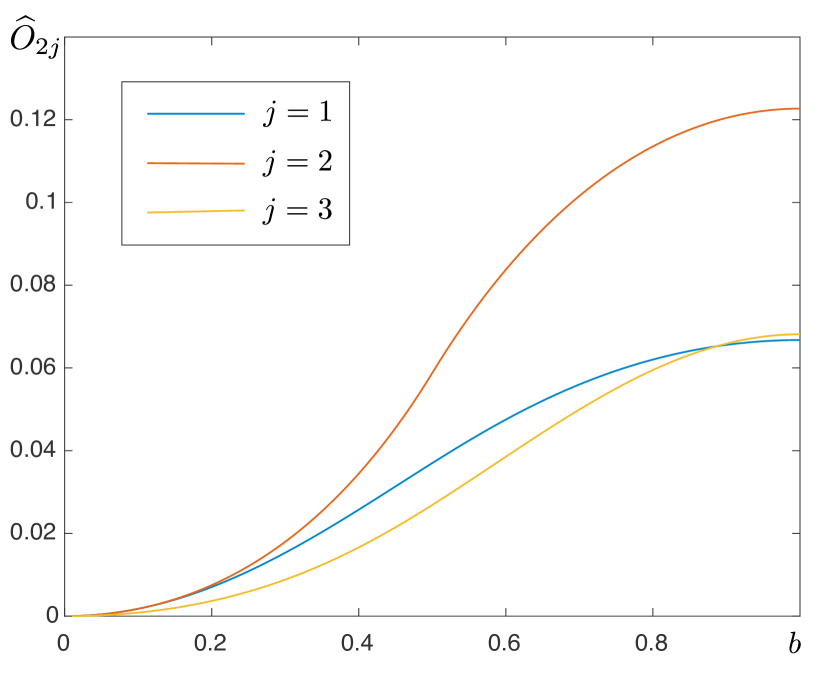

Example 2.

Consider now the same parameters as in Example 1, but take and . While this alternative scenario does not necessarily have an immediate practical interpretation, it does help to investigate some of the consequences of having a state which lacks any random noise behaviour. From Figure 4.4, we note that the downcrossing probabilities for States and are larger than those in Example 1; this is because now we have one of the states pushing the level process downwards. However, note that the probability of downcrossing while in State is null; this is because approaches as the level gets closer to , meaning that the process simply cannot cross level while in State . Moreover, we note that for large values of , the expected occupation time while in State is larger than in States or ; this suggests that before exiting the band , the process switches to and stays in State for a larger amount of time than in Example 1.

Figure 4.4. Left: Plots of as a function of . Right: Plots of as a function of with . Each plot contains the cases .

5. Summary and extensions

Under Assumptions 1-5, we considered the class of hybrid SDEs and their space-grid approximations, the latter belonging to a the family of multi-regime Markov-modulated Brownian motions. We provided a rigorous proof of their pathwise convergence, which holds in a probability sense uniformly over increasing compact intervals. As an application of our convergence result, we considered the challenging problem of identifying first passage probabilities and expected occupation times for solutions of hybrid SDEs, for which we suggest an approximate and computationally efficient answer which employs developments in the area of multi-regime Markov-modulated queues.

We point out that applications of our convergence result may also be used to approximate other (and possibly more complex) descriptors of hybrid SDEs. For instance, one can easily build hybrid SDEs with phase-type jumps by means of the fluidization method [8]. Other modifications and extensions which are straightforward to implement in our framework are the Omega model [2, 15], the Erlangian approximations for finite-time probabilities of ruin [7], and Parisian ruin problems with phase-type clocks [10].

Acknowledgement. The authors would like to acknowledge financial support from the Swiss National Science Foundation Project 200021_191984.

References

[1]

N. Akar, O. Gursoy, G. Horvath, and M. Telek.

Transient and first passage time distributions of first-and

second-order multi-regime Markov fluid queues via ME-fication.

Methodology and Computing in Applied Probability,

23(4):1257–1283, 2021.

[2]

H. Albrecher, H. U. Gerber, and E. S. Shiu.

The optimal dividend barrier in the Gamma–Omega model.

European Actuarial Journal, 1(1):43–55, 2011.

[3]

W. Allan, G. T. Nguyen, and O. Peralta.

Numerical simulation for solutions of hybrid stochastic differential

equations with complete past dependence driven by Lévy processes.

In preparation, 2022.

[4]

S. Asmussen.

Stationary distributions for fluid flow models with or without

Brownian noise.

Communications in Statistics. Stochastic Models, 11(1):21–49,

1995.

[5]

S. Asmussen.

Applied probability and queues, volume 2.

Springer, 2003.

[6]

S. Asmussen and H. Albrecher.

Ruin probabilities, volume 14.

World Scientific, 2010.

[7]

S. Asmussen, F. Avram, and M. Usabel.

Erlangian approximations for finite-horizon ruin probabilities.

ASTIN Bulletin: The Journal of the IAA, 32(2):267–281, 2002.

[8]

A. Badescu, L. Breuer, A. Da Silva Soares, G. Latouche, M.-A. Remiche, and

D. Stanford.

Risk processes analyzed as fluid queues.

Scandinavian Actuarial Journal, 2005(2):127–141, 2005.

[9]

M. Bladt and B. F. Nielsen.

Matrix-exponential distributions in applied probability,

volume 81.

Springer, 2017.

[10]

M. Bladt, B. F. Nielsen, and O. Peralta.

Parisian types of ruin probabilities for a class of dependent

risk-reserve processes.

Scandinavian Actuarial Journal, 2019(1):32–61, 2019.

[11]

L. Breuer.

Occupation times for Markov-modulated Brownian motion.

Journal of Applied Probability, 49(2):549–565, 2012.

[12]

B. D’Auria, J. Ivanovs, O. Kella, and M. Mandjes.

Two-sided reflection of Markov-modulated Brownian motion.

Stochastic Models, 28(2):316–332, 2012.

[13]

R. J. Elliott, T. K. Siu, L. Chan, and J. W. Lau.

Pricing options under a generalized Markov-modulated jump-diffusion

model.

Stochastic Analysis and Applications, 25(4):821–843, 2007.

[14]

W. Fischer and K. Meier-Hellstern.

The Markov-modulated poisson process (MMPP) cookbook.

Performance Evaluation, 18(2):149–171, 1993.

[15]

H. U. Gerber, E. S. Shiu, and H. Yang.

The Omega model: from bankruptcy to occupation times in the red.

European Actuarial Journal, 2(2):259–272, 2012.

[16]

P. W. Glynn.

Upper bounds on Poisson tail probabilities.

Operations Research Letters, 6(1):9–14, 1987.

[17]

P. W. Glynn.

Some topics in regenerative steady-state simulation.

Acta Applicandae Mathematica, 34(1):225–236, 1994.

[18]

G. Horváth and M. Telek.

Matrix-analytic solution of infinite, finite and level-dependent

second-order fluid models.

Queueing Systems, 87(3):325–343, 2017.

[19]

K. Itô and H. P. McKean.

Diffusion processes and their sample paths.

Springer Science & Business Media, 2012.

[20]

J. Ivanovs.

Markov-modulated Brownian motion with two reflecting barriers.

Journal of Applied Probability, 47(4):1034–1047, 2010.

[21]

N. V. Krylov and M. Röckner.

Strong solutions of stochastic equations with singular time dependent

drift.

Probability Theory and Related Fields, 131(2):154–196, 2005.

[22]

G. Leobacher and M. Szölgyenyi.

A strong order method for multidimensional SDEs with

discontinuous drift.

The Annals of Applied Probability, 27(4):2383–2418, 2017.

[23]

M. Mandjes, D. Mitra, and W. Scheinhardt.

Models of network access using feedback fluid queues.

Queueing Systems, 44(4):365–398, 2003.

[24]

D. H. Nguyen and G. Yin.

Modeling and analysis of switching diffusion systems: past-dependent

switching with a countable state space.

SIAM Journal on Control and Optimization, 54(5):2450–2477,

2016.

[25]

G. T. Nguyen and O. Peralta.

Wong–Zakai approximations with convergence rate for stochastic

differential equations with regime switching.

arXiv preprint arXiv:2101.03250, 2021.

[26]

G. T. Nguyen and O. Peralta.

Rate of strong convergence to Markov-modulated Brownian motion.

Journal of Applied Probability, 59(1):1–16, 2022.

[27]

N. Prabhu and Y. Zhu.

Markov-modulated queueing systems.

Queueing Systems, 5(1):215–245, 1989.

[28]

A. V. Skorokhod.

Asymptotic methods in the theory of stochastic differential

equations, volume 78.

American Mathematical Soc., 2009.

[29]

K. S. Trivedi and A. Bobbio.

Reliability and availability engineering: modeling, analysis,

and applications.

Cambridge University Press, 2017.

[30]

B. Van Houdt and C. Blondia.

Approximated transient queue length and waiting time distributions

via steady state analysis.

Stochastic Models, 21(2-3):725–744, 2005.

[31]

M. A. Yazici and N. Akar.

The finite/infinite horizon ruin problem with multi-threshold

premiums: a Markov fluid queue approach.

Annals of Operations Research, 252(1):85–99, 2017.

[32]

G. Yin, X. Mao, C. Yuan, and D. Cao.

Approximation methods for hybrid diffusion systems with

state-dependent switching processes: Numerical algorithms and existence and

uniqueness of solutions.

SIAM Journal on Mathematical Analysis, 41(6):2335–2352, 2010.

[33]

G. G. Yin and C. Zhu.

Hybrid switching diffusions: properties and applications,

volume 63.

Springer Science & Business Media, 2009.

[34]

S.-Q. Zhang.

Regime-switching diffusion processes: strong solutions and strong

Feller property.

Stochastic Analysis and Applications, 38(1):97–123, 2020.