On the Safety of Interpretable Machine Learning:

A Maximum Deviation Approach

Abstract

Interpretable and explainable machine learning has seen a recent surge of interest. We focus on safety as a key motivation behind the surge and make the relationship between interpretability and safety more quantitative. Toward assessing safety, we introduce the concept of maximum deviation via an optimization problem to find the largest deviation of a supervised learning model from a reference model regarded as safe. We then show how interpretability facilitates this safety assessment. For models including decision trees, generalized linear and additive models, the maximum deviation can be computed exactly and efficiently. For tree ensembles, which are not regarded as interpretable, discrete optimization techniques can still provide informative bounds. For a broader class of piecewise Lipschitz functions, we leverage the multi-armed bandit literature to show that interpretability produces tighter (regret) bounds on the maximum deviation. We present case studies, including one on mortgage approval, to illustrate our methods and the insights about models that may be obtained from deviation maximization.

1 Introduction

Interpretable and explainable machine learning (ML) has seen a recent surge of interest because it is viewed as a key pillar in making models trustworthy, with implications on fairness, reliability, and safety [1]. In this paper, we focus on safety as a key reason behind the demand for explainability. The motivation of safety has been discussed at a qualitative level by several authors [2, 3, 4, 5]. Its role is perhaps clearest in the dichotomy between directly interpretable models vs. post hoc explanations of black-box models. The former have been called “inherently safe” [3] and promoted as the only alternative in high-risk applications [5]. The crux of this argument is that post hoc explanations leave a gap between the explanation and the model producing predictions. Thus, unusual data points may appear to be harmless based on the explanation, but truly cause havoc. We aim to go beyond these qualitative arguments and address the following questions quantitatively: 1) What does safety mean for such models, and 2) how exactly does interpretability aid safety?

Towards answering the first question, we make a conceptual contribution in the form of an optimization problem, intended as a tool for assessing the safety of supervised learning (i.e. predictive) models. Viewing these models as functions mapping an input space to an output space, a key way in which these models can cause harm is through grossly unexpected outputs, corresponding to inputs that are poorly represented in training data. Accordingly, we approach safety assessment for a model by determining where it deviates the most from the output of a reference model and by how much (i.e., its maximum deviation). The reference model, which represents expected behavior and is deemed to be safe, could be a model well-understood by domain experts or one that has been extensively “tried and tested.” The maximization is done over a certification set, a large subset of the input space intended to cover all conceivable inputs to the model. These concepts are discussed further in Section 2.

Towards answering the second question, in Section 4 we discuss computation of the maximum deviation for different model classes and show how this is facilitated by interpretability. For model classes regarded as interpretable, including trees, generalized linear and additive models, the maximum deviation can be computed exactly and efficiently by exploiting the model structure. For tree ensembles, which are not regarded as interpretable, discrete optimization techniques can exploit their composition in terms of trees to provide anytime bounds on the maximum deviation. The case of trees is also generalized in a different direction to a broader class of piecewise Lipschitz functions, which we argue cover many popular interpretable functions. Here we show that the benefit of interpretability is significantly tighter regret bounds on the maximum deviation compared with general black-box functions, leveraging results from the multi-armed bandit literature. More broadly, the development of tailored methods for additional model classes is beyond the scope of this first work on the maximum deviation approach (the black-box optimization of Section 4.4 is applicable to all models but obviously not tailored). We discuss in Appendix B.5 some possible approaches, and the research gaps to be overcome, for neural networks and to make use of post hoc explanations, which approximate a model locally [6, 7, 8] or globally [9, 10].

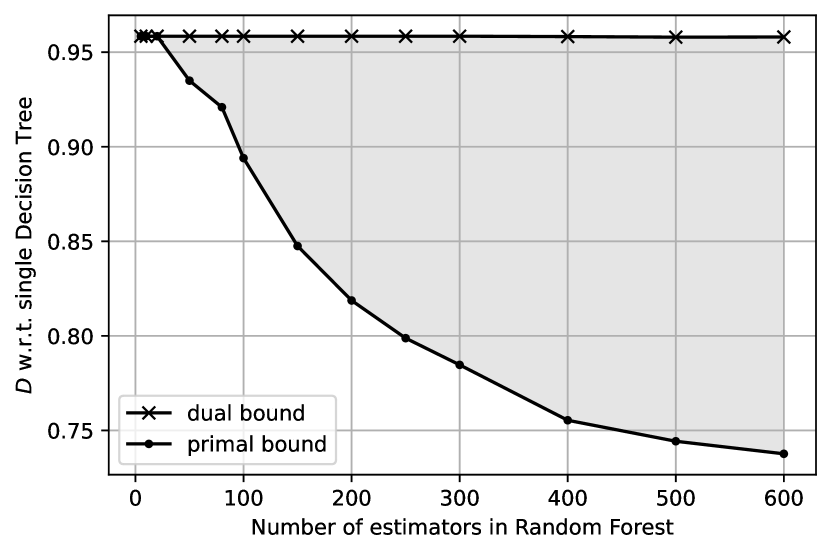

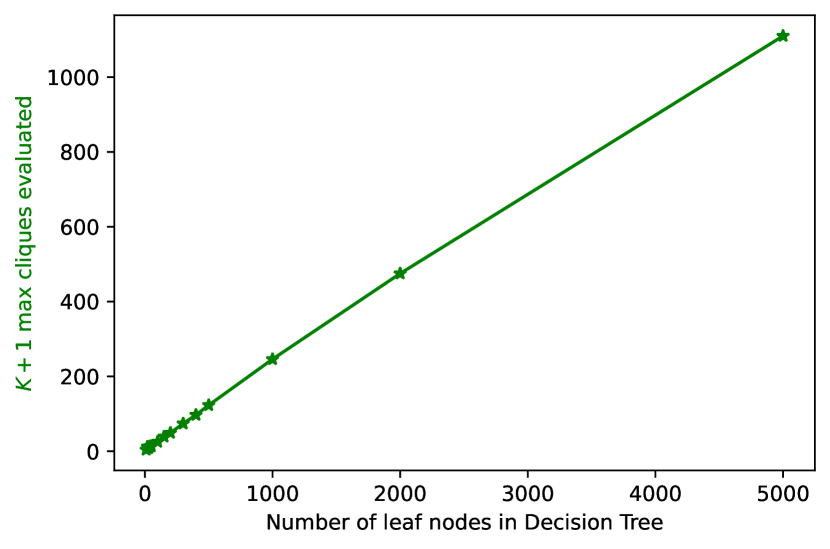

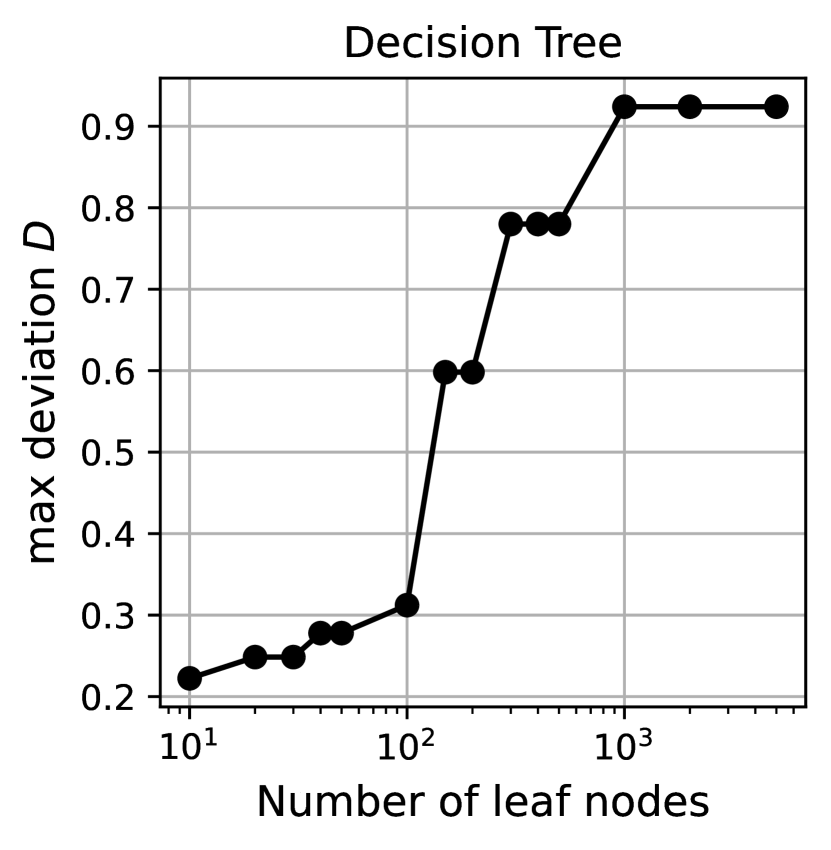

In Section 5, we present case studies that illustrate the deviation maximization methods in Section 4 for decision trees, linear and additive models, and tree ensembles. It is seen that deviation maximization provides insights about models through studying the feature combinations that lead to extreme outputs. These insights can in turn direct further investigation and invite domain expert input. We also quantify how the maximum deviation depends on model complexity and the size of the certification set. For tree ensembles, we find that the obtained upper bounds on the maximum deviation are informative, showing that the maximum deviation does not increase with the number of trees in the ensemble.

Overall, our discussion provides a more quantitative basis for safety assessment of predictive models and for preferring more interpretable models due to the greater ease of performing this assessment.

2 Assessing Safety Through Maximum Deviation

We are given a supervised learning model , which is a function mapping an input feature space to an output space . We wish to assess the safety of this model by finding its largest deviation from a given reference model representing expected behavior. To do this, we additionally require 1) a measure of deviation , where is the set of non-negative reals, and 2) a certification set over which the deviation is maximized. Then the problem to be solved is

| (1) |

The deviation is worst-case because the maximization is over all ; further implications of this are discussed in Appendix C. Note that (1) is different than typical robust training where the focus is to learn a model that minimizes some worst case loss, as opposed to finding regions in where two already trained models differ significantly.

We view problem (1) as only a means toward the goal of evaluating safety. In particular, a large deviation value is not necessarily indicative of a safety risk, as two models may differ significantly for valid reasons. For example, one model may capture a useful pattern that the other does not. We thus think that it would be overly simplistic to regard the maximum deviation as just another metric to be optimized in selecting models. What large deviation values do indicate, however, is a (possibly) sufficient reason for further investigation. Hence, the maximizing solutions in (1) (i.e., the ) are of as much operational interest as the maximum values (this will be illustrated in Section 5).

We now elaborate on elements in problem formulation (1).

Output space . In the case of regression, is the set of reals or an interval thereof. In the case of binary classification, while could be or , these limit the possible deviations to binary values as well (“same” or “different”). Thus to provide more informative results, we take to be the space of real-valued scores that are thresholded to produce a binary label. For example, could be a predicted probability in or a log-odds ratio in . Similarly for multi-class classification with classes, could be a -dimensional space of real-valued scores. In Appendix A, we discuss considerations in choosing the deviation function as well as models that abstain.

Reference model . The premise of the reference model is that it should capture expected behavior while being “safe”. The simplest case is for to be a constant function representing a baseline value, for example zero or a mean prediction. We consider the more general case where may vary with . Below we give several examples of reference models to address the natural question of how they might be obtained. The examples can be categorized as 1) existing domain-specific models, 2) interpretable ML models validated by domain knowledge, and 3) extensively tested and deployed models. The first two categories are prevalent in high-stakes domains where interpretability is critical.

-

1.

Existing domain-specific models: These models originate from an application domain and may not be based on ML at all. For example in consumer finance, several industry-standard models compute credit scores from a consumer’s credit information (the FICO score is the best-known in the US). Similarly in medicine, scoring systems (sparse linear models with small integer coefficients) abound for assessing various risks (the CHADS2 score for stroke risk is well-known, see the "Scoring Systems: Applications and Prior Art" section of [11] for a list of others). These models have been used for decades by thousands of practitioners so they are well understood. They may very well be improved upon by a more ML-based model, but for such a model to gain acceptance with domain experts, any large deviations from existing models need to be examined and understood.

-

2.

Interpretable models validated by domain knowledge: Here, an interpretable ML model is learned from data and is validated by domain experts in some way, for example by selecting important input features or by carefully inspecting the trained model. We provide two real examples: In semiconductor manufacturing, process engineers typically want decision trees [12] to model their respective manufacturing process (e.g. etching, polishing, rapid thermal processing, etc.) since they are comfortable understanding and explaining them to their superiors, which is critical especially when things go out-of-spec. Hence, a tree built from data (or any model in general) would only be allowed to make automated measurement predictions if the features it highlights (viz. pressures, gas flows, temperatures) make sense for the specific process. Similarly, in predicting failures of industrial assets such as wind turbines, some failure data is available to train models but experts in these systems (e.g. engineers) may also be consulted. They have knowledge that can help validate the model, for example which components are most likely to cause failures or which environmental variables (e.g. temperature) are most influential.

-

3.

Extensively tested and deployed models: A reference model may also be one that is not necessarily informed by domain knowledge but has been extensively tested, deployed, and/or approved by a regulator. For medical devices that use ML models, the US Food and Drug Administration (FDA) has instituted a risk-based regulatory system. Any system updates or changes, for instance changes in model architecture, retraining based on new data, or changes in intended use (e.g. use for pediatric cases for devices approved only for adults), need to either seek new approvals or demonstrate “substantial equivalence” by providing supporting evidence that the revised model is similar to a previously approved device. In the latter case, the reference model is the approved device and small maximum deviation serves as evidence of equivalence. As another example, consider a ML-based recommendation model for products of an online retailer or articles on a social network, where because of the scale, a tree ensemble may be used for its fast inference time as well as its modeling flexibility [13]. In this case, a model that has been deployed for some time could be the reference model, since it has been extensively tested during this time even though human validation of it may be limited. When a new version of the model is trained on newer data or improved in some fashion, finding its maximum deviation from the reference model can serve as one safety check before deploying it in place of the reference model.

Certification set . The premise of the certification set is that it contains all inputs that the model might conceivably be exposed to. This may include inputs that are highly improbable but not physically or logically impossible (for example, a severely hypothermic human body temperature of 27°C). Thus, while might be based on the support set of a probability distribution or data sample, it does not depend on the likelihood of points within the support. The set may also be a strict superset of the training data domain. For example, a model may have been trained on data for males, and we would now like to determine its worst-case behavior on an unseen population of females.

For tabular or lower-dimensional data, might be the entire input space . For non-tabular or higher-dimensional data, the choice may be too unrepresentative because the manifold of realistic inputs is lower in dimension. In this case, if we have a dataset , one possibility is to use a union of balls centered at ,

| (2) |

The set is thus comprised of points somewhat close to the observed examples , but the radius does not have to be “small”.

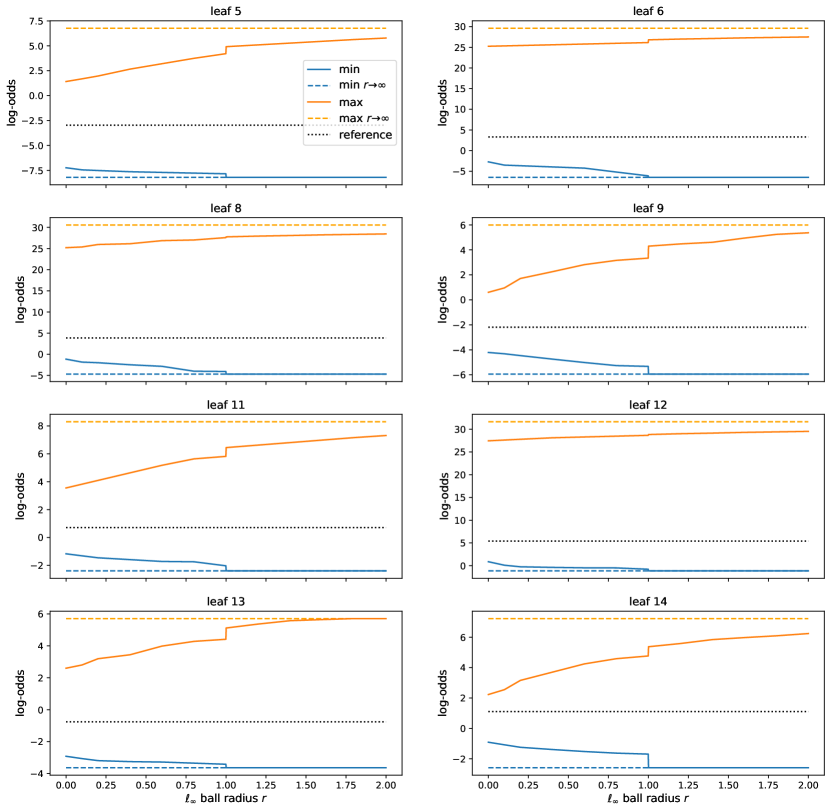

In addition to determining the maximum deviation over the entire set , maximum deviations over subsets of (e.g., different age groups) may also be of interest. For example, Appendix D.3 shows deviation values separately for leaves of a decision tree, which partition the input space.

3 Related Work

In previous work on safety and interpretability in ML, the authors of [3, 14] give qualitative accounts suggesting that directly interpretable models are an inherently safe design because humans can inspect them to find spurious elements; in this paper, we attempt to make those qualitative suggestions more quantitative and automate some of the human inspection. Furthermore, several other authors have highlighted safety as a goal for interpretability [2, 4, 15, 16, 5], but again without quantitative development. Moreover, the lack of consensus on how to measure interpretability motivates the relationship that we explore between interpretability and the ease of evaluating safety.

In the area of ML verification, robustness certification methods aim to provide guarantees that the classification remains constant within a radius of an input point, while output reachability is concerned with characterizing the set of outputs corresponding to a region of inputs [17]. A major difference in our work is that we consider two models, a model to be assessed and a reference , whereas the above notions of robustness and reachability involve a single model. Another important difference is that our focus is global, over a comprehensive set , rather than local to small neighborhoods around input points; a local focus is especially true of neural network verification [18, 19, 20, 21, 22, 23, 24, 25, 26, 27]. We also study the role of interpretability in safety verification. Works in robust optimization applied to ML minimize the worst-case probability of error, but this worst case is over parameters of rather than values of [28]. Thomas et al. [29] present a framework where during model training, a set of safety tests is specified by the model designer in order to accept or reject the possible solution.

We build on related literature on robustness and explainability that deals specifically with tree ensembles. Mixed-integer programming (MIP) and discrete optimization have been proposed to find the smallest input perturbation to ‘evade’ a classifier [30] and to obtain counterfactual explanations [31]. MIP approaches are computationally intensive however. To address this Chen et al. [32] introduce graph based approaches for verification on trees. Their central idea, which we use, is to discretize verification computations onto a graph constructed from the way leaves intersect. The verification problem is transformed to finding all maximum cliques. Devos et al. [33] expand on this idea by providing anytime bounds by probing unexplored nodes.

Safety has become a critical issue in reinforcement learning (RL) with multiple works focusing on making RL policies safe [34, 35, 36, 37]. There are two broad themes [38]: (i) a safe and verifiable policy is learned at the outset by enforcing certain constraints, and (ii) post hoc methods are used to identify bad regimes or failure points of an existing policy. Our current proposal is complementary to these works as we focus on the supervised learning setup viewed from the lens of interpretability. Nonetheless, ramifications of our work in the RL context are briefly discussed in Appendix C.

4 Deviation Maximization for Specific Model Classes

In this section, we discuss approaches to computing the maximum deviation (1) for belonging to various model classes. We show the benefit of interpretable model structure in different guises. Exact and efficient computation is possible for decision trees, and generalized linear and additive models in Sections 4.1 and 4.2. In Section 4.3, the composition of tree ensembles in terms of trees allows discrete optimization methods to provide anytime bounds. For a general class of piecewise Lipschitz functions in Section 4.4, the application of multi-arm bandit results yields tighter regret bounds on the maximum deviation. While some of the results in this section may be less surprising, one of our contributions is to identify precise properties that allow them to hold. We also show that intuitive measures of model complexity, such as the number of leaves or pieces or smoothness of functions, have an additional interpretation in terms of the complexity of maximizing deviation. More broadly, the development of methods specific to additional model classes is beyond the scope of a single work. We discuss in Appendix B.5 possible approaches and the advances needed for neural networks (beyond applying the black-box methods of Section 4.4) and to make use of post hoc explanations.

To develop mathematical results and efficient algorithms, we will sometimes assume that the reference model is from the same class as . In Appendix C, we discuss the case where may not be globally interpretable, but may be so in local regions. We will also sometimes assume that the certification set and other sets are Cartesian products. This means that , where for a continuous feature , is an interval, and for a categorical feature , is a set of categories. We mention relaxations of the Cartesian product assumption in Appendix B.2.

4.1 Trees

We begin with the case where and are both decision trees. A decision tree with leaves partitions the input space into corresponding parts, which we also refer to as ‘leaves’. We consider only non-oblique trees. In this case, each leaf is described by a conjunction of conditions on individual features and is therefore a Cartesian product as defined above. With denoting the th leaf and the output value assigned to it, tree is described by the function

| (3) |

and similarly for tree with leaves and outputs , . As discussed in [39, 40], rule lists where each rule is a condition on a single feature are one-sided trees in the above sense.

The partitioning of by decision trees and their piecewise-constant nature simplify the computation of the maximum deviation (1). Specifically, the maximization can be restricted to pairs of leaves for which the intersection is non-empty. The intersection of two leaves is another Cartesian product, and we assume that it is tractable to determine whether intersects a given Cartesian product (see examples in Appendix B.1).

For visual representation and later use in Section 4.3, it is useful to define a bipartite graph, with nodes representing the leaves of on one side and nodes representing the leaves of on the other. Define the edge set ; clearly . Then

| (4) |

4.2 Linear and additive models

In this subsection, we assume that is a generalized additive model (GAM) given by

| (5) |

where each is an arbitrary function of feature . In the case where for all continuous features , where is a real coefficient, (5) is a generalized linear model (GLM). We discuss the treatment of categorical features in Appendix B.2. The invertible link function is furthermore assumed to be monotonically increasing. This assumption is satisfied by common GAM link functions: identity, logit (), and logarithmic.

Equation (5) implies that and the deviation is a function of two scalars and . For this scalar case, we make the following intuitively reasonable assumption throughout the subsection.

Assumption 1.

For , 1) whenever ; 2) is monotonically non-decreasing in for and non-increasing in for .

Our approach is to exploit the additive form of (5) by reducing problem (1) to the optimization

| (6) |

for different choices of and where corresponds to and to . We discuss below how this can be done for two types of reference model : decision tree (which includes the constant case ) and additive. For the first case, we prove the following result in Appendix B.2:

Proposition 2.

Tree-structured . Since is piecewise constant over its leaves , , we take to be the intersection of with each in turn and apply Proposition 2. The overall maximum is then obtained as the maximum over the leaves,

| (7) |

Additive . For this case, we make the additional assumption that the link function in (5) is the identity function, as well as Assumption 2 below. The implication of these assumptions is discussed in Appendix B.2.

Assumption 2.

is a function only of the difference .

Then and the difference is also additive. Using Assumptions 2, 1 and a similar argument as in the proof of Proposition 2, the maximum deviation is again obtained by maximizing and minimizing an additive function, resulting in two instances of (6) with :

Computational complexity of (6). For the case of nonlinear additive , we additionally assume that is a Cartesian product. It follows that is a Cartesian product (see Appendix B.2 for the brief justification) and (6) separates into one-dimensional optimizations over ,

| (8) |

4.3 Tree ensembles

We now extend the idea used for single decision trees in Section 4.1 to tree ensembles. This class covers several popular methods such as Random Forests and Gradient Boosted Trees. It can also cover rule ensembles [41, 42] as a special case, as explained in Appendix B.3. We assume is a tree ensemble consisting of trees and is a single decision tree. Let denote the th leaf of the th tree in for , and be the th leaf , for . Correspondingly let and denote the prediction values associated with each leaf.

Define a graph , where there is a vertex for each leaf in and , i.e.

| (9) |

Construct an edge for each overlapping pair of leaves in , i.e.

| (10) |

This graph is a -partite graph as leaves within an individual tree do not intersect and are an independent set. Denote to be the adjacency matrix of . Following Chen et al. [32], a maximum clique of size on such a graph provides a discrete region in the feature space with a computable deviation. A clique is a subset of nodes all connected to each other; a maximum clique is one that cannot be expanded further by adding a node. The model predictions and can be ensembled from leaves in . Denote by the deviation computed from the clique . Maximizing over all such cliques solves (1). However, complete enumeration is expensive, so informative bounds, either using the merge procedure in Chen et al. [32] or the heuristic function in Devos et al. [33] can be used. We use the latter which exploits the -partite structure of .

Specifically, we adapt the anytime bounds of Devos et al. [33] as follows. At each step of the enumeration procedure, an intermediate clique contains selected leaves from trees in and unexplored trees in . For each unexplored tree, we select a valid candidate leaf that maximizes deviation, i.e.

| (11) |

Using these worst-case leaves, a heuristic function

| (12) |

provides an upper (dual) bound. In practice, this dual bound is tight and therefore very useful during the search procedure to prune the search space. Each clique provides a primal bound, so the search can be terminated early before examining all trees if the dual bound is less than the primal bound. We adapt the search procedure of Mirghorbani and Krokhmal [43] to include the pruning arguments. Appendix B.3 presents the full algorithm. Starting with an empty clique, the procedure adds a single node from each tree to create an intermediate clique. If the size of the clique is the primal bound is updated. Otherwise, the dual bound is computed. A node compatibility vector is used to keep track of all feasible additions.When the search is terminated at any step, the maximum deviation is bounded by .

The algorithm works for the entire feature space. When the certification set is a union of balls as in (2), some additional considerations are needed. First, we can disregard leaves that do not intersect with during the graph construction phase. A validation step to ensure that the leaves of a clique all intersect with the same ball in is also needed.

4.4 Piecewise Lipschitz Functions

We saw the benefits of having specific (deterministic) interpretable functions as well as their extensions in the context of safety. Now consider a richer class of functions that may also be randomized with finite variance. In this case let and denote the mean values of the learned and reference functions respectively. We consider the case where each function is either interpretable or black box, where the latter implies that query access is the only realistic way of probing the model. This leads to three cases where either both functions are black box or interpretable, or one is black box. What we care about in all these cases111For simplicity assume to be the identity function. is to find the maximum (and minimum) of a function . Let us consider finding only the maximum of as the other case is symmetric. Given that and can be random functions is also a random function and if is black box a standard way to optimize it is either using Bayesian Optimization (BO) [44] or tree search type bandit methods [45, 46]. We repurpose some of the results from this latter literature in our context showcasing the benefit of interpretability from a safety standpoint. To do this we first define relevant terms.

Definition 1 (Simple Regret [45]).

If denotes the optimal value of the function on the certification set , then the simple regret after querying the function times and obtaining a solution is given by, .

Definition 2 (Order c-Lipschitz).

Given a (normalized) metric a function is c-Lipschitz continuous of order if for any two inputs , and for we have, .

Definition 3 (Near optimality dimension [45]).

If is the maximum number of radius balls one can fit in given the metric and , then for the c-near optimality dimension is given by, .

Intuitively, simple regret measures the deviation between our current best and the optimal solution. The Lipschitz condition bounds the rate of change of the function. Near optimality dimension measures the set size for which the function has close to optimal values. The lower the value of , the easier it is to find the optimum. We now define what it means to have an interpretable function.

Assumption 3 (Characterizing an Interpretable Function).

If a function is interpretable, then we can (easily) find partitions of the certification set such that the function in each partition is c-Lipschitz of order .

Note that the (interpretable) function overall does not have to be c-Lipschitz of bounded order, rather only in the partitions. This assumption is motivated by observing different interpretable functions. For example, in the case of decision trees the partitions could be its leaves, where typically the function is a constant in each leaf (). For rule lists as well a fixed prediction is usually made by each rule. For a linear function one could consider the entire input space (i.e. ), where for bounded slope the function would also satisfy our assumption ( and ). Examples of models that are not piecewise constant or globally Lipschitz are oblique decision trees (Murthy et al., 1994), regression trees with linear functions in the leaves, and functional trees. Moreover, is likely to be small so that the overall model is interpretable (viz. shallow trees or small rules). With the above definitions and Assumption 3 we now provide the simple regret for the function .

1. Both black box models: If both and are black box then it seems no gains could be made in estimating the maximum of over standard results in bandit literature. Hence, using Hierarchical Optimistic Optimization (HOO) with assumptions such as being compact and being weakly Lipschitz [45] with near optimality dimension the simple regret after queries is:

| (13) |

2. Both interpretable models: If both and are interpretable, then for each function based on Assumption 3 we can find and partitions of respectively where the functions are and -Lipschitz of order and respectively. Now if we take non-empty intersections of these partitions where we could have a maximum of partitions, the function in these partitions would be -Lipschitz of order as stated next (proof in appendix).

Proposition 3.

If functions and are and Lipschitz of order and respectively, then the function is c-Lipschtiz of order , where and .

Given that is smooth in these partitions with underestimated smoothness of order , the simple regret after queries in the partition with near optimality dimension based on HOO is: , where . If we divide the overall query budget across the non-empty partitions equally, then the bound will be scaled by when expressed as a function of . Moreover, the regret for the entire can then be bounded by the maximum regret across these partitions leading to

| (14) |

Notice that for a model to be interpretable and are likely to be small (i.e. shallow trees or small rule lists or linear model where ) leading to a “smallish" and can be much in case 1. Hence, interpretability reduces the regret in estimating the maximum deviation.

3. Black box and interpretable model: Making no further assumptions on the black box model and assuming satisfies properties mentioned in case 1, the simple regret has the same behavior as (13). This is expected as the black box model could be highly non-smooth.

5 Case Studies

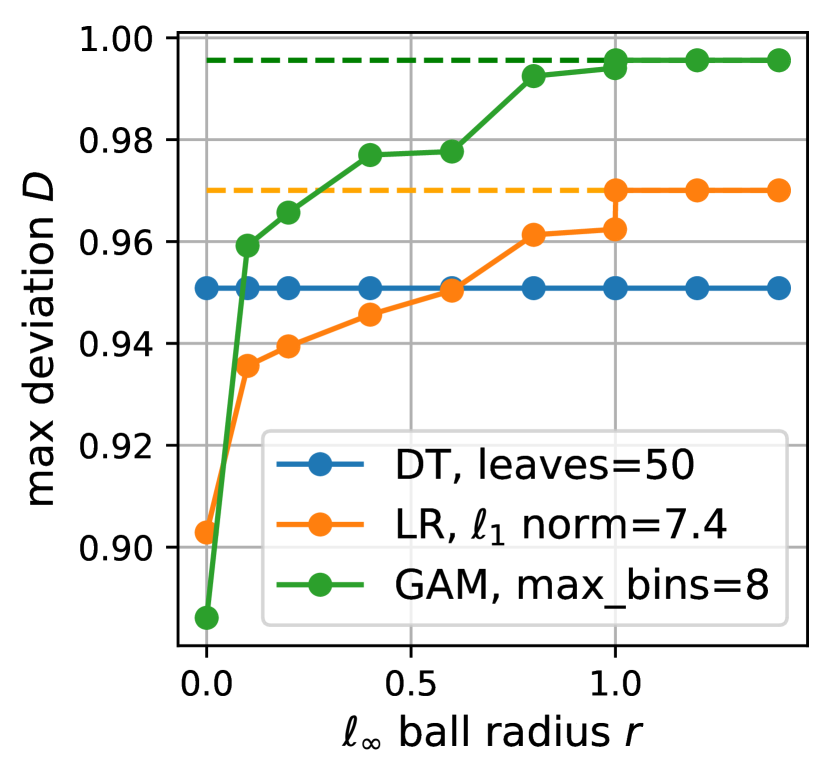

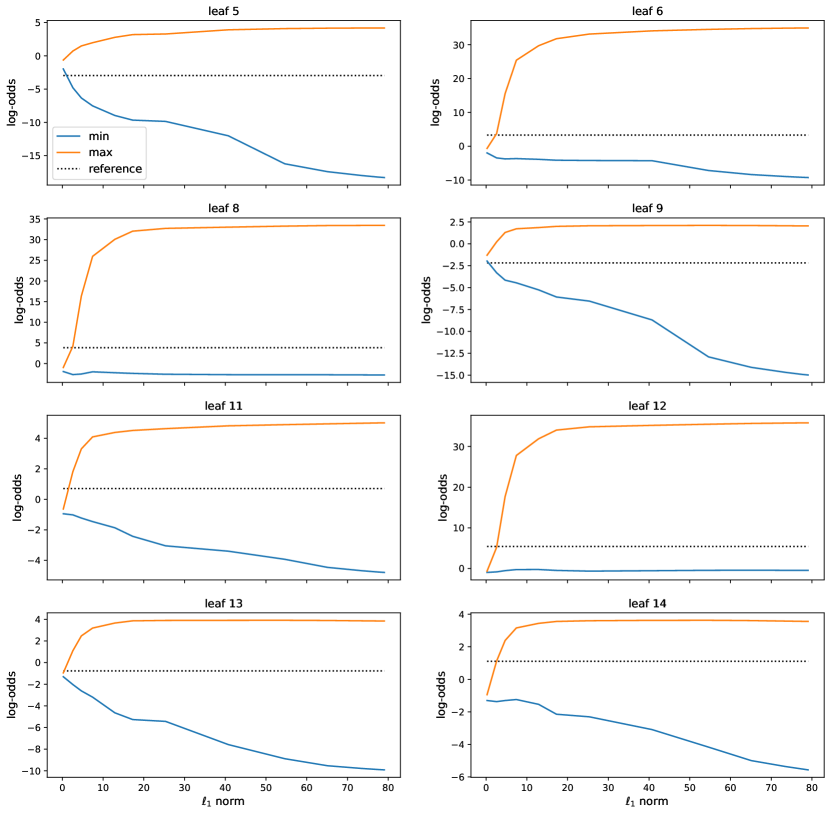

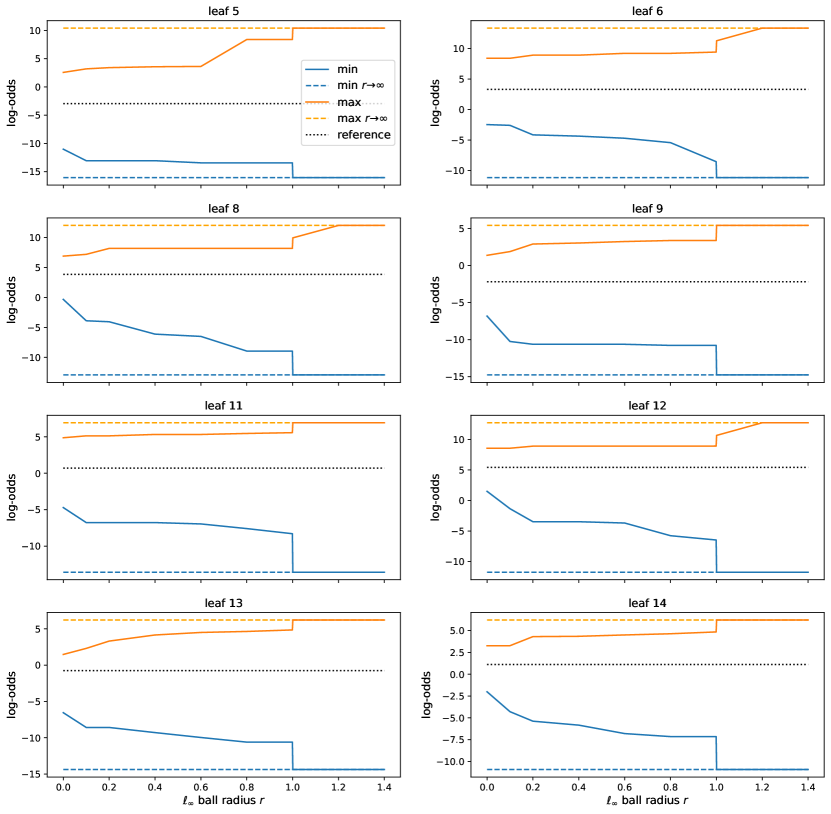

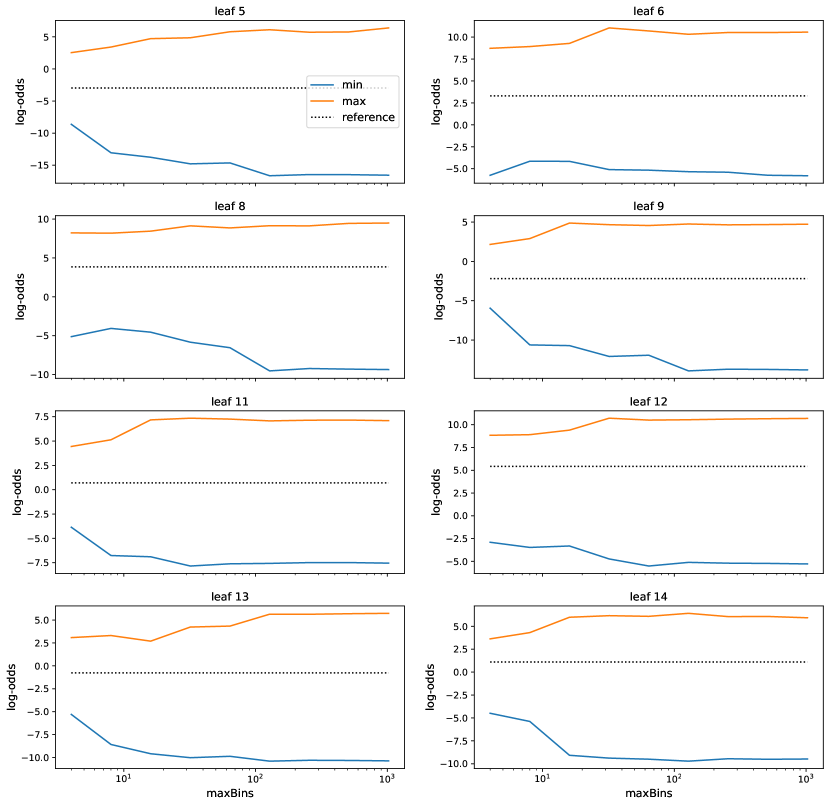

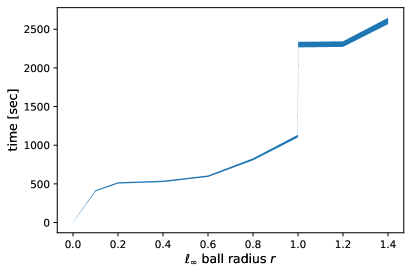

We present case studies to serve three purposes: 1) show that deviation maximization can lead to insights about models, 2) illustrate the maximization methods developed in Section 4, and 3) quantify the dependence of the maximum deviation on model complexity and certification set size (mostly in Appendix D). Two datasets are featured: a sample of US Home Mortgage Disclosure Act (HMDA) data (see Appendix D.2 for details), meant as a proxy for a mortgage approval scenario, and the UCI Adult Income dataset [47], a standard tabular dataset with mixed data types. A subset of results is shown in this section with full results, experimental details, and an additional Lending Club dataset in Appendix D. Since these are binary classification datasets, we take the deviation function to be the absolute difference between predicted probabilities of class 1. For the certification set , we consider a union of balls (2) centered at test set instances. While we have used the test set here, any not necessarily labelled dataset would suffice. The case yields a finite set consisting only of the test set, while corresponds to being the entire domain . We reiterate that the dependence of the certification set on a chosen dataset is only on (an expanded version of) the support of the dataset and not on other aspects of the data distribution.

To demonstrate insights from deviation maximization, we study the solutions that maximize deviation (the in (1)) and discuss three examples below.

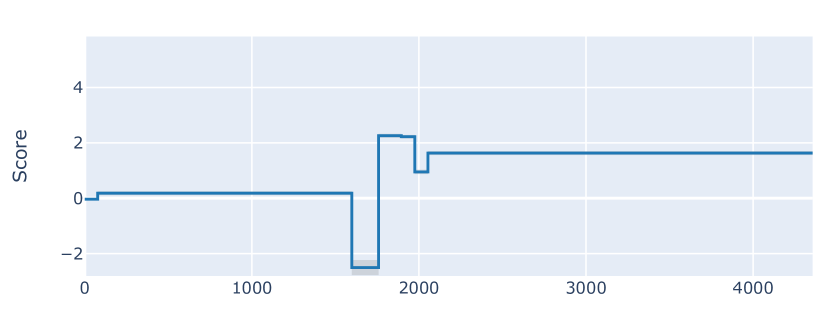

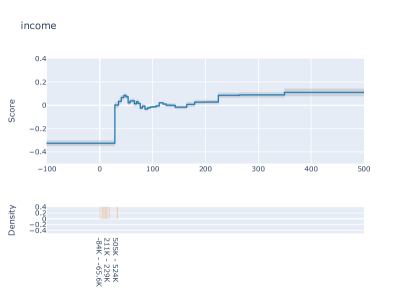

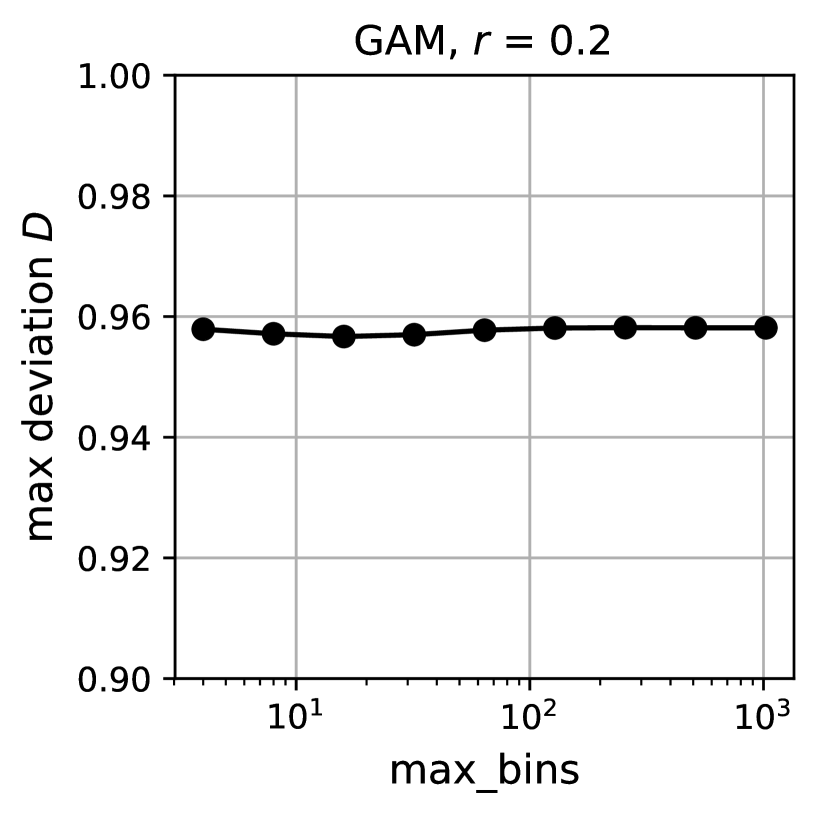

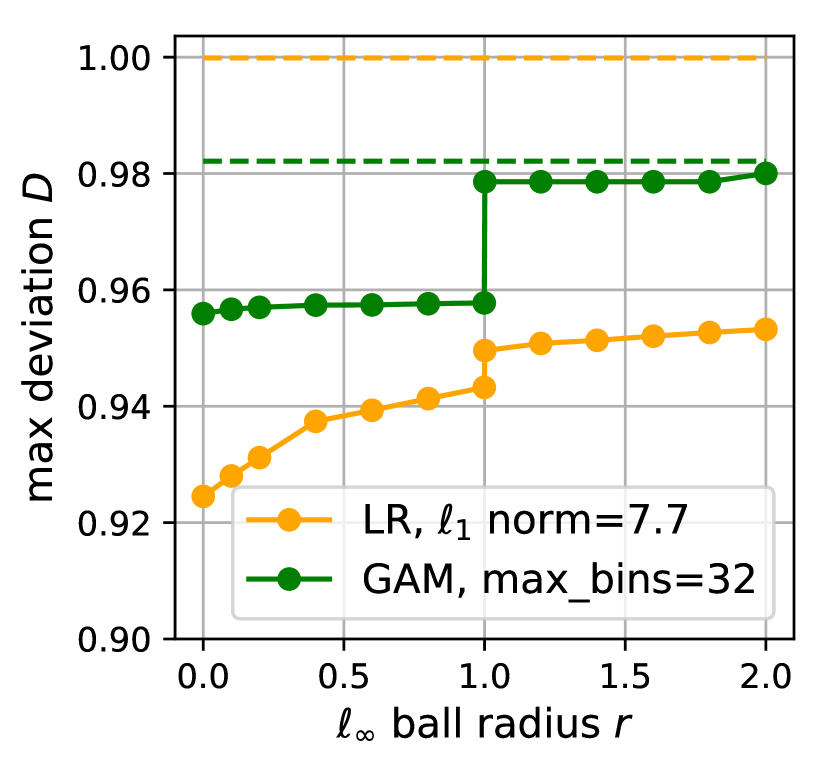

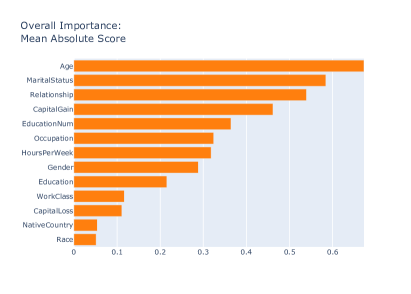

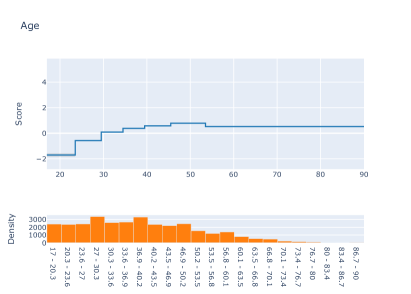

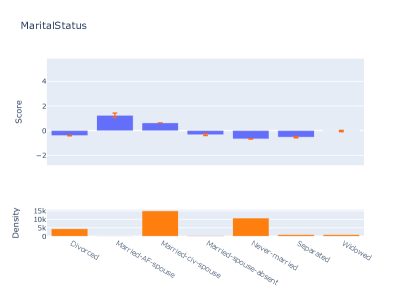

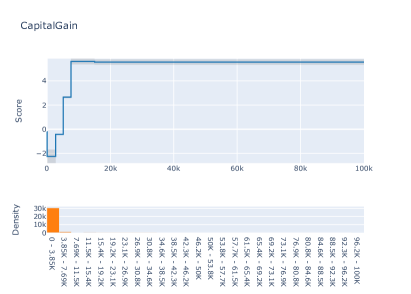

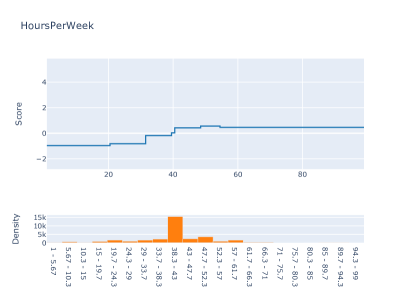

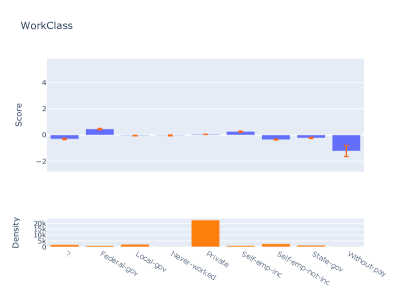

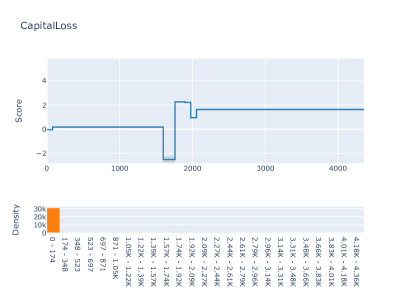

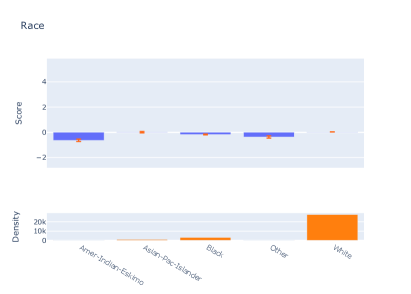

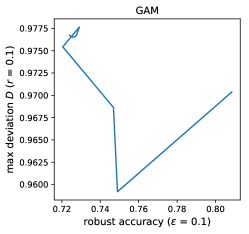

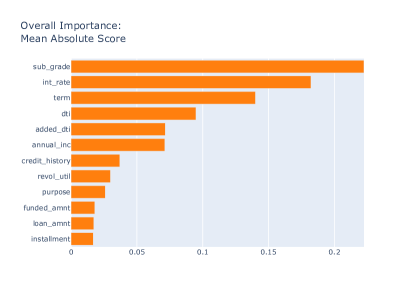

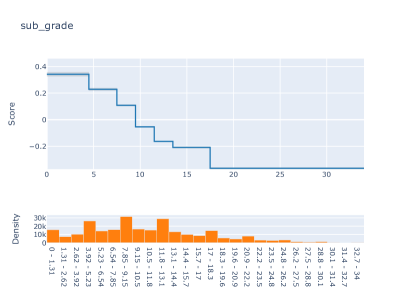

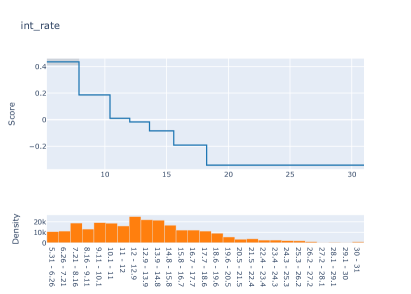

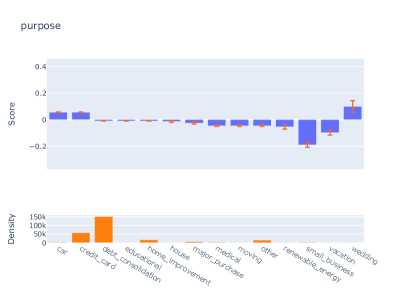

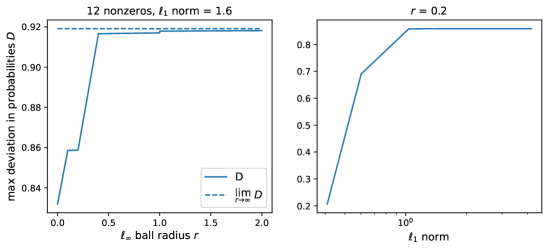

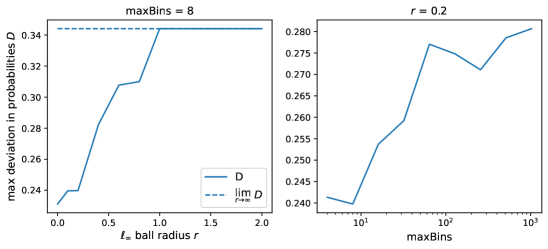

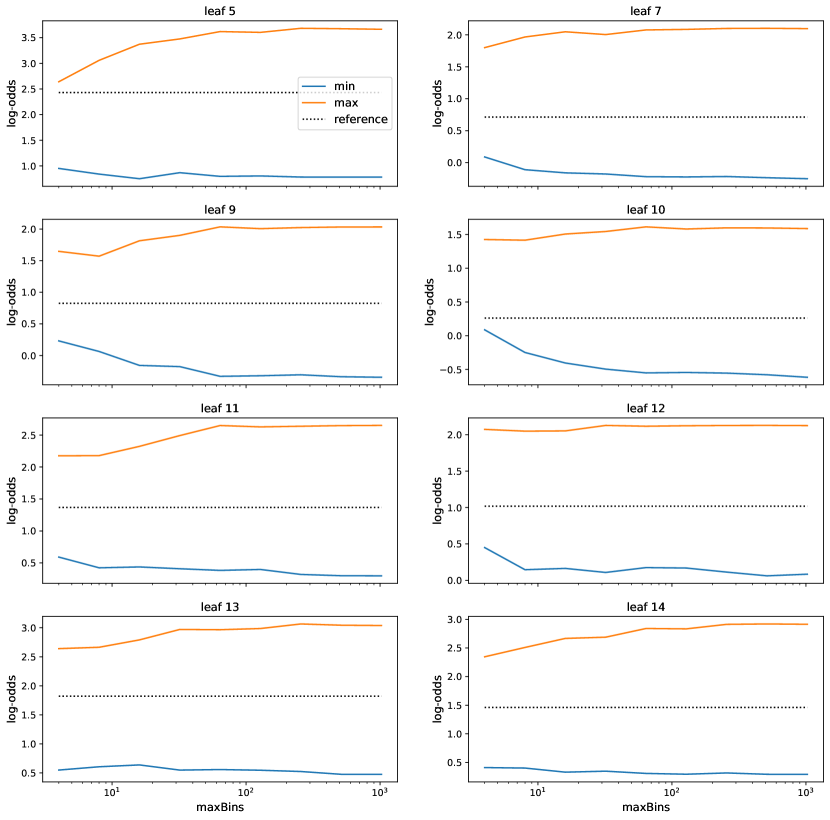

Identification of an artifact: The first example comes from the Adult Income dataset, where the reference model is a decision tree (DT) and is an Explainable Boosting Machine (EBM) [48], a type of GAM (plots of both in Appendix D.3). Here, the capital loss feature is the largest contributor to the maximum deviation (the discussion below Table 4 explains how this is determined), and Table 8 in Appendix D.3 shows that as the certification set radius increases, the maximizing values of capital loss converge to the interval . The plot of the GAM shape function for capital loss in Figure 1 shows that this interval corresponds to a curiously low value of the function. This low region may be an artifact warranting further investigation since it seems anomalous compared to the rest of the function, and since individuals who report capital losses on their income tax returns to offset capital gains usually have high income (hence high log-odds score). Note that this potential artifact was automatically identified through deviation maximization.

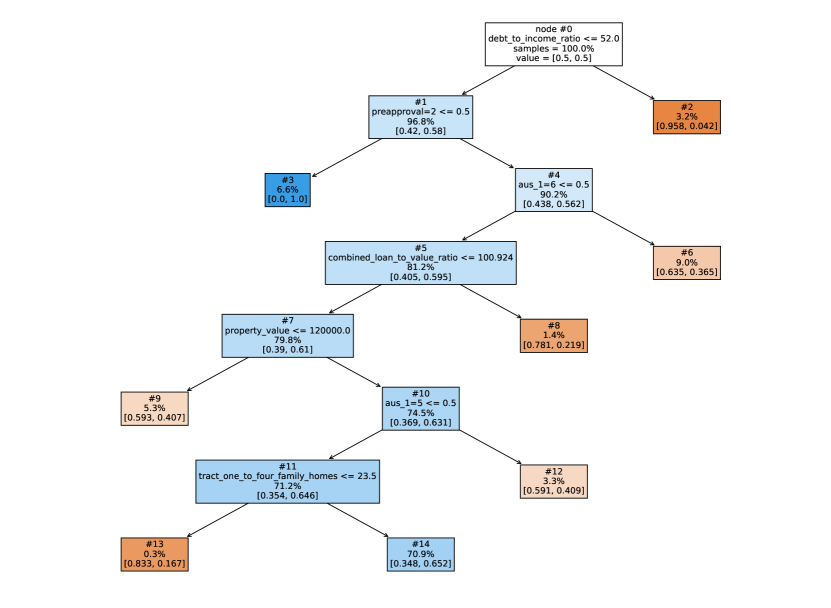

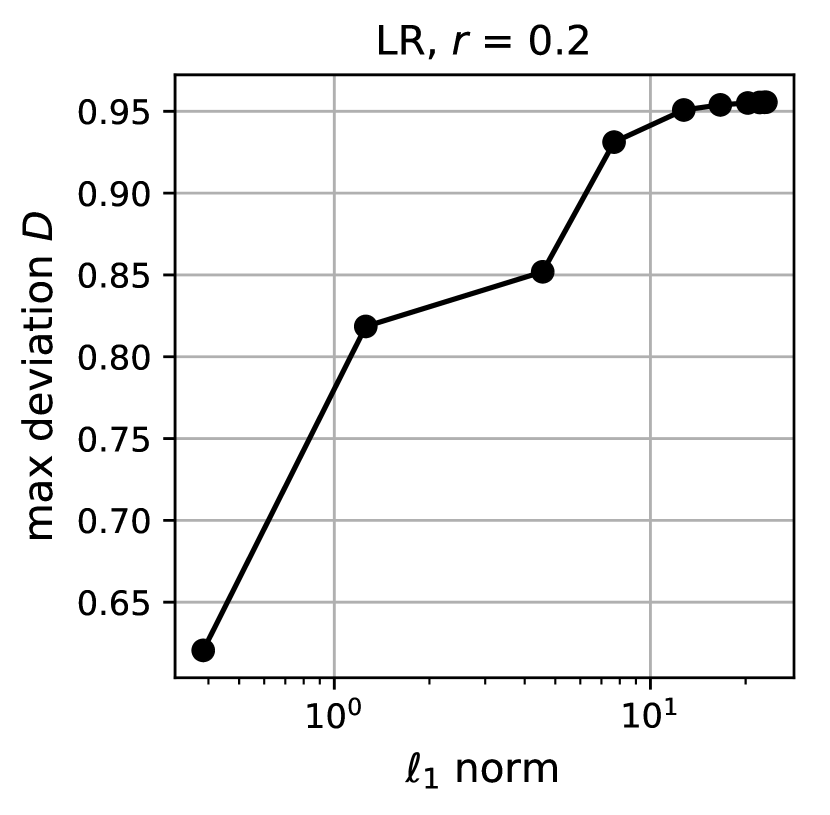

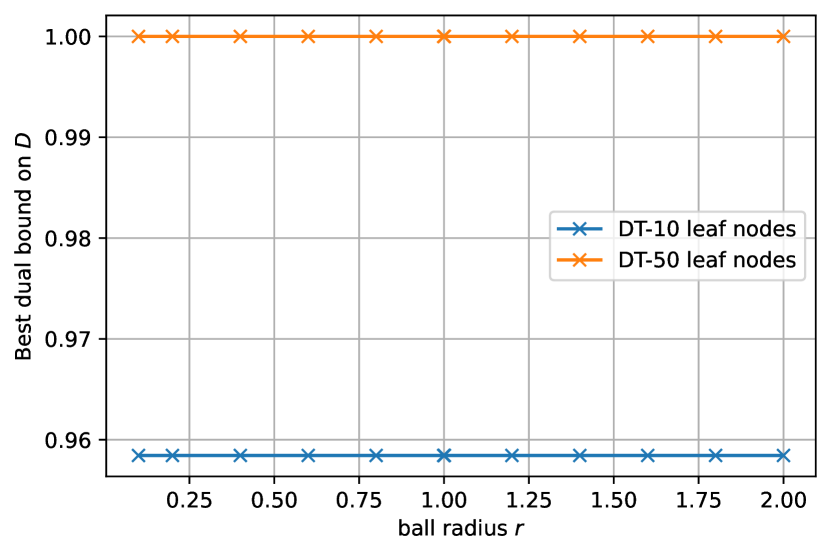

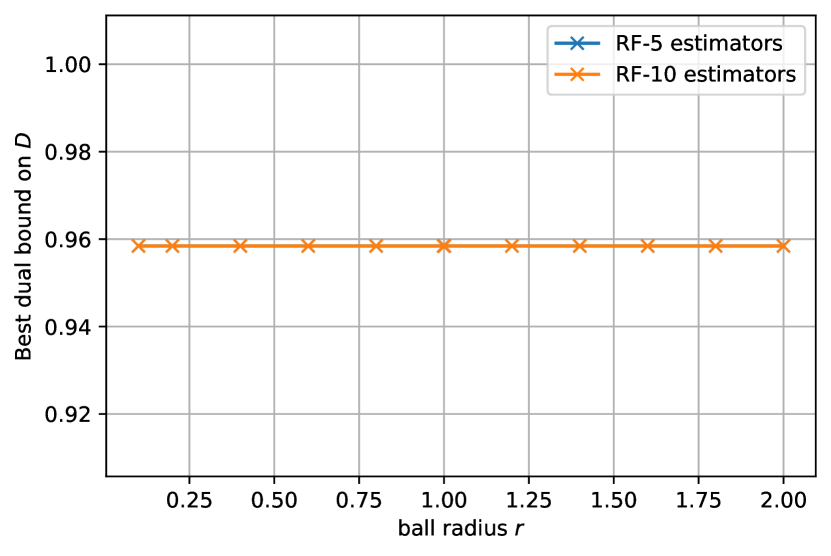

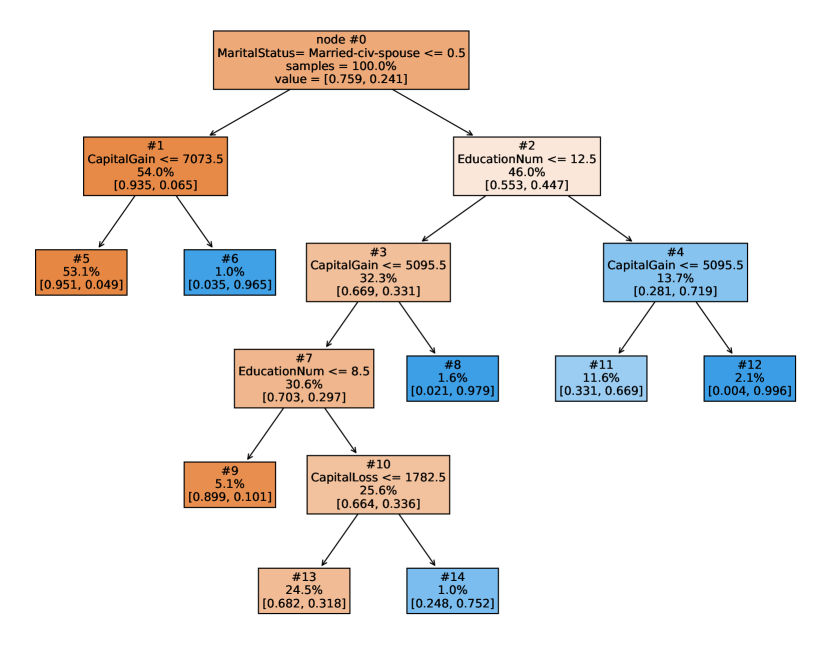

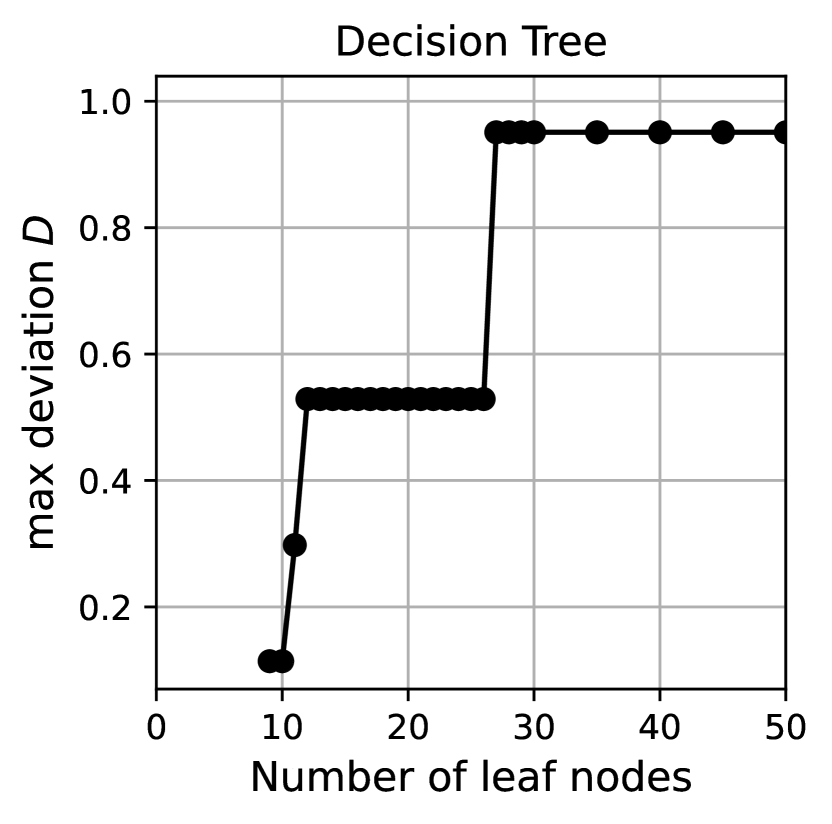

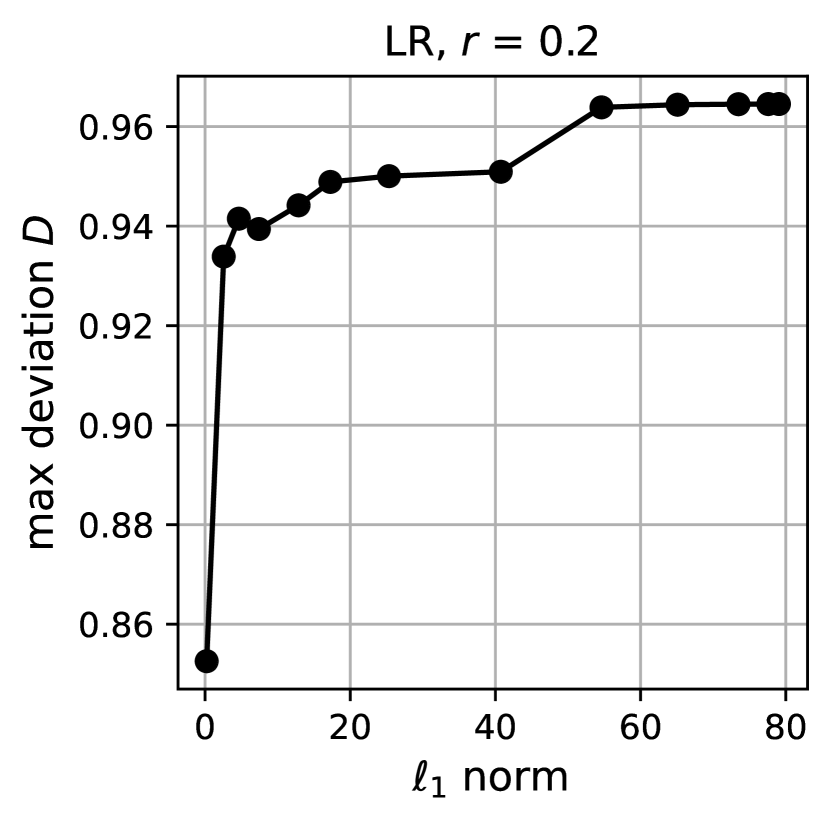

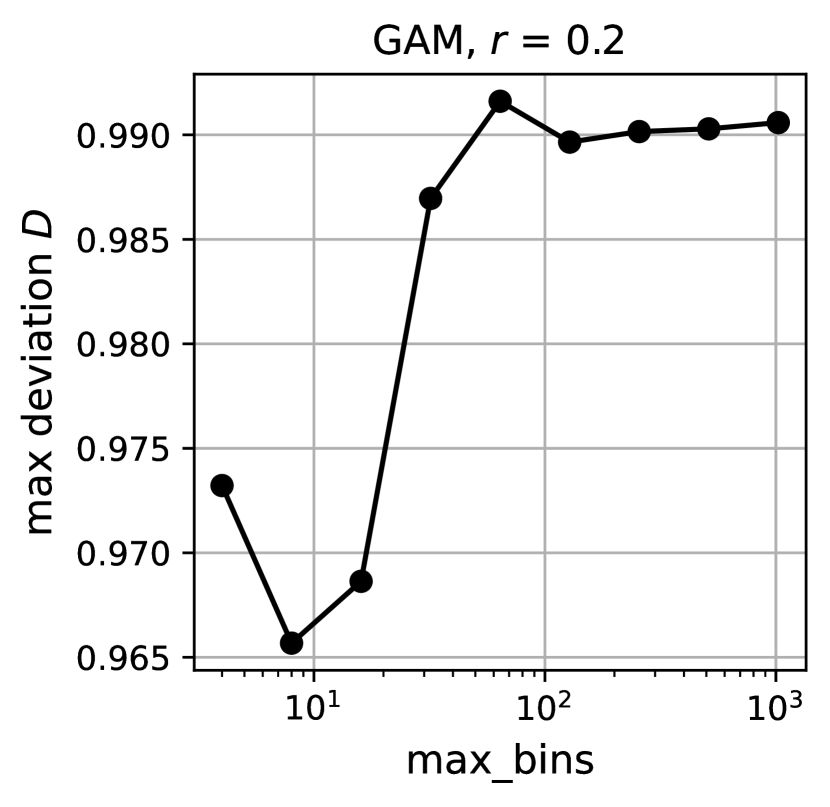

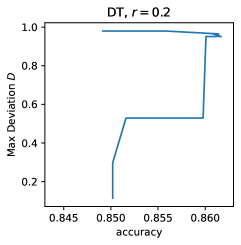

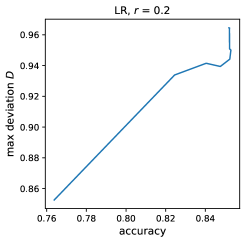

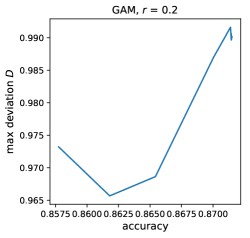

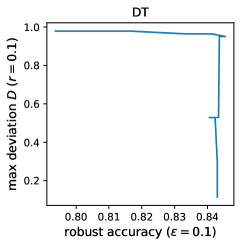

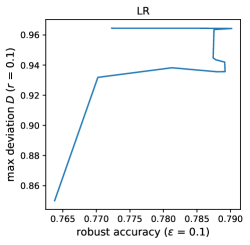

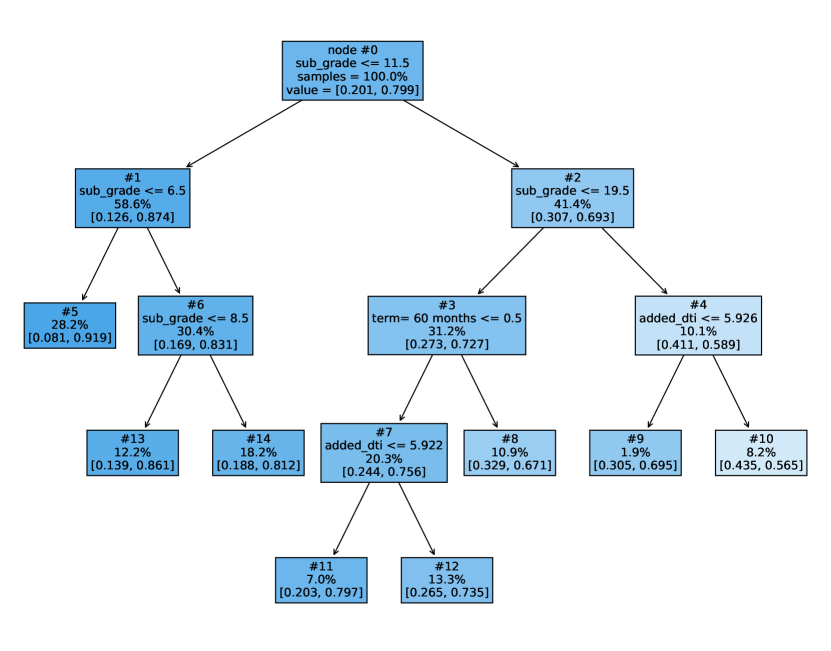

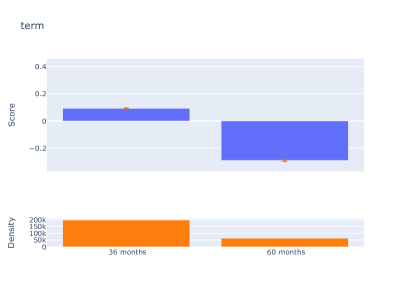

For the next two examples, we consider a simplified mortgage approval scenario using the HMDA dataset. Suppose that a DT (shown in Figure 3 in Appendix D.2) has been trained to make final decisions on mortgage applications. Domain experts have determined that this DT is sensible and safe and are now looking to improve upon it by exploring EBMs. (Logistic regression (LR) models are deferred to Appendix D.2 because they do not have higher balanced accuracy than .)

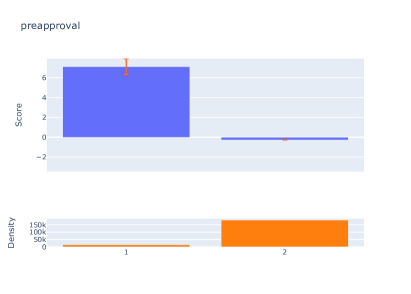

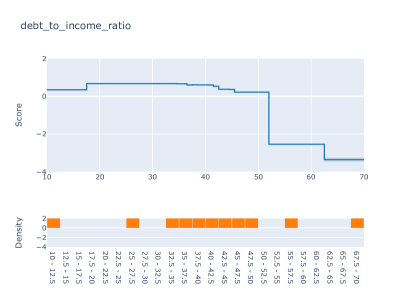

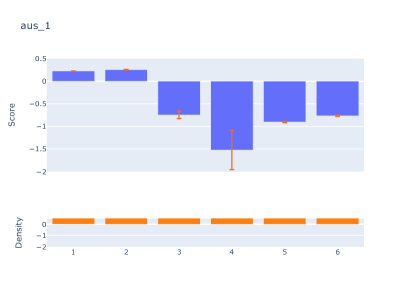

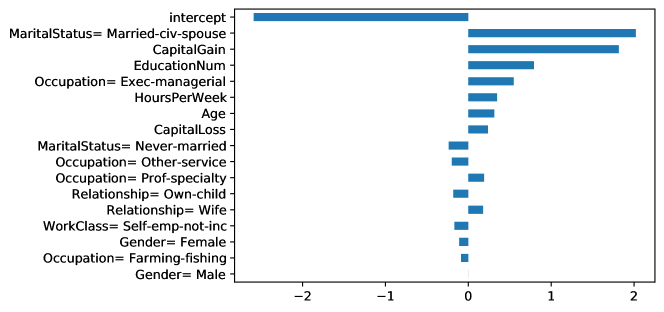

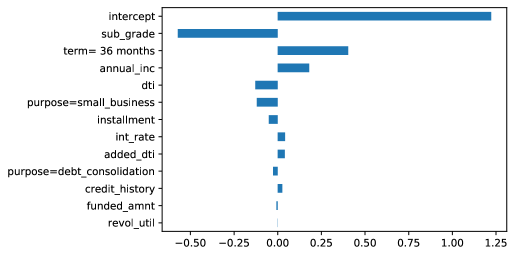

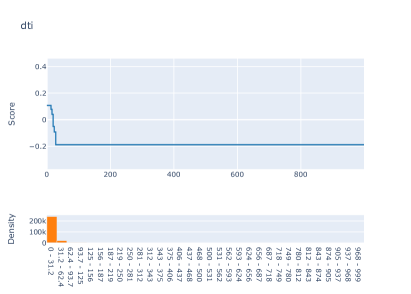

Conflict between , : We first examine solutions that result in the most positive difference between the predicted probabilities of an EBM with parameter max_bins=32 and the DT . These all occur in a leaf of (leaf 2 in Figure 3) where the applicant’s debt-to-income (DTI) ratio is too high ( 52%) and predicts a low probability of approval. The other salient feature of the solutions is that they all have ‘preapproval’=1, indicating that a preapproval was requested, which is given a large weight by the EBM in favor of approval (see Figure 4 in Appendix D.2, and Table 4 for more feature values). Thus and are in conflict. Among different ways in which the conflict could be resolved, a domain expert might decide that remains correct in rejecting risky applicants with high DTI, even if there is a preapproval request and the new EBM model puts a high weight on it.

| debt_to_income (%) | state | loan_to_value (%) | aus_1 | prop_value (000$) | income (000$) | |

|---|---|---|---|---|---|---|

| 0.0 | 46.0 | CA | 95.0 | 3 | 415 | 77.0 |

| 0.1 | [45.9 46.5] | none | [100. 100.92] | 1 | [120 120] | 28.5 |

| 0.2 | [45.5 46.5] | none | [100. 100.92] | 1 | [120 120] | 28.5 |

| 0.4 | [52. 52.] | none | [100. 100.92] | 1 | [120 120] | 28.5 |

| 0.6 | [52. 52.] | none | [100. 100.92] | 1 | [120 120] | 28.5 |

| 0.8 | [52. 52.] | none | [100. 100.92] | 1 | [120 120] | 28.5 |

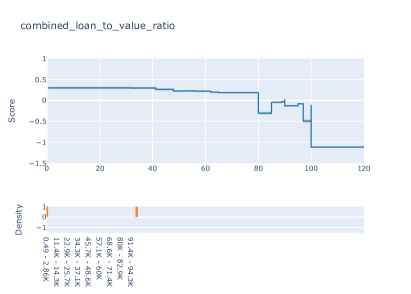

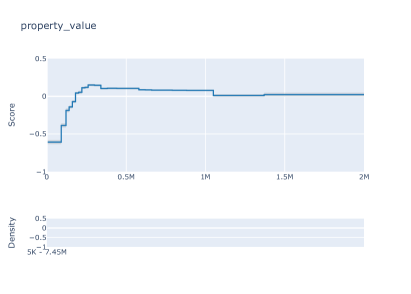

Trend toward extreme points, deviation can be good: We now look at solutions that yield the most negative difference between the predicted probabilities of and , for . Table 1 shows the 6 features that contribute most to the deviation (again see Appendix D.2 for details). All of these points lie in a leaf of (leaf 14 in Figure 3, denoted ) that excludes several clearer-cut cases, with the result being a less confident predicted probability of from . The feature values that maximize deviation tend toward extreme points of the region . Specifically, the values of the continuous features debt-to-income ratio, loan-to-value ratio, property value, and income all move in the direction of application denial. For the latter three features, the boundary of is reached as soon as , whereas for debt-to-income ratio, this occurs at . The movement toward extremes is expected for this since its relevant shape functions are mostly increasing or decreasing, as seen in Figure 4 in Appendix D.2. The same behavior is observed in other GAM and LR examples in Appendix D. In this example, a domain expert might conclude that the large deviation is in fact desirable because is providing varying predictions in in ways that make sense, as opposed to the constant given by . This shows that deviation maximization can work in both directions, identifying where the reference model and its assumptions may be too simplistic and giving an opportunity to improve the reference model.

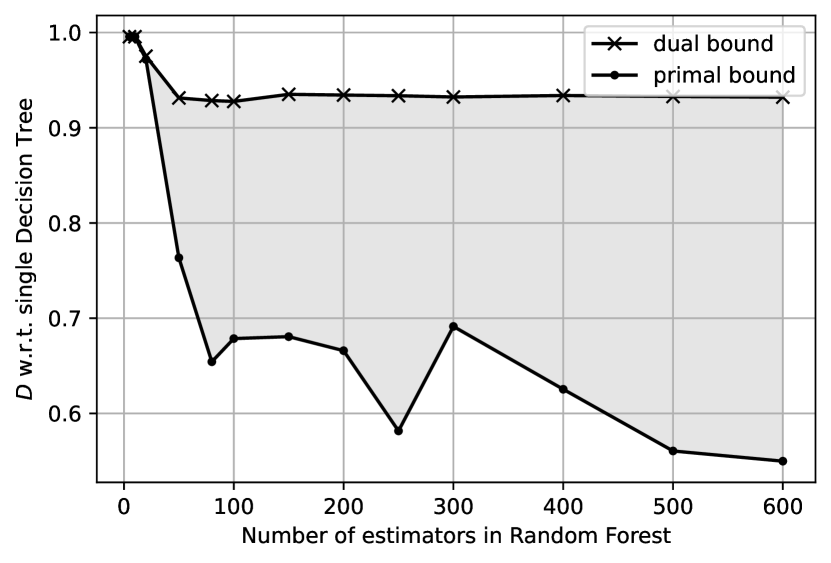

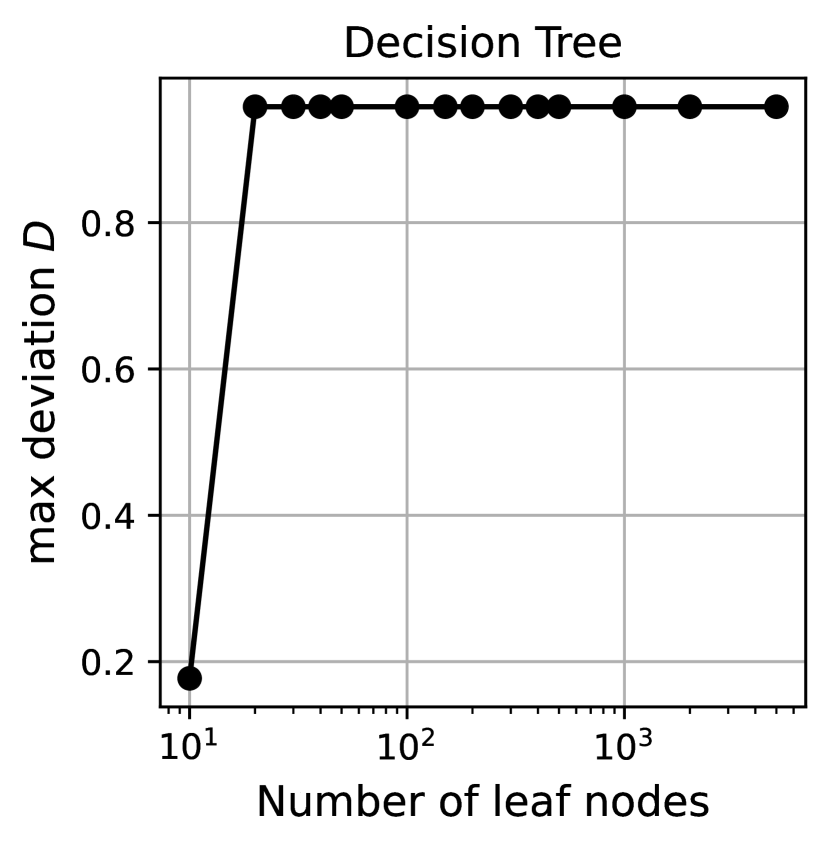

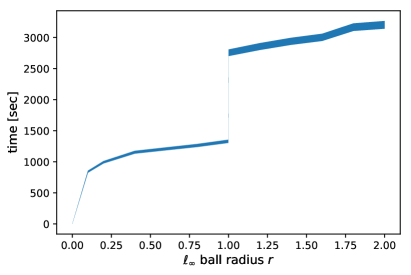

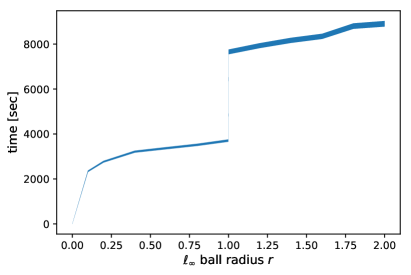

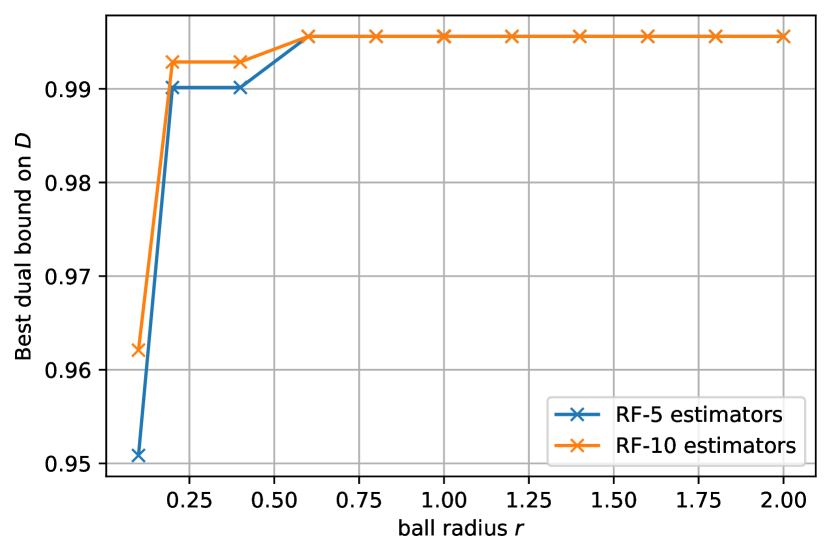

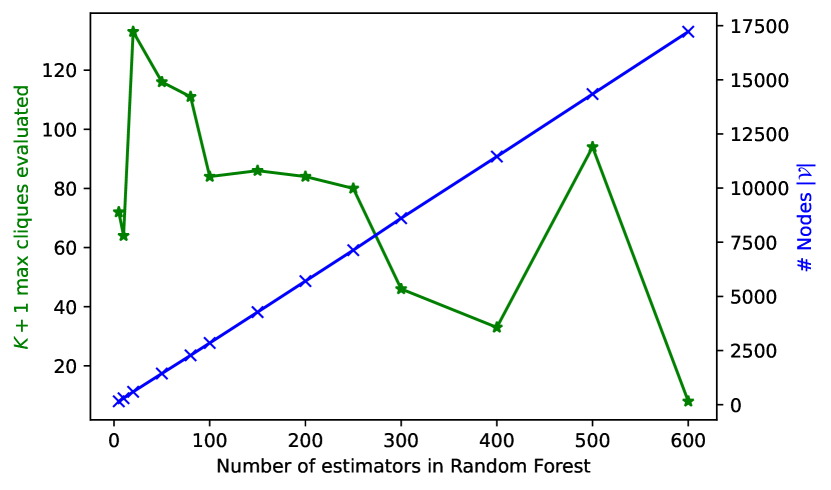

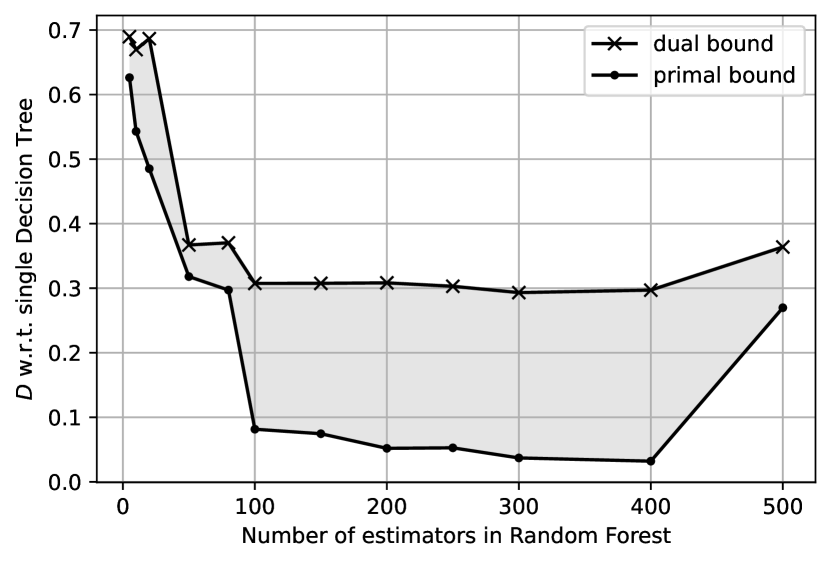

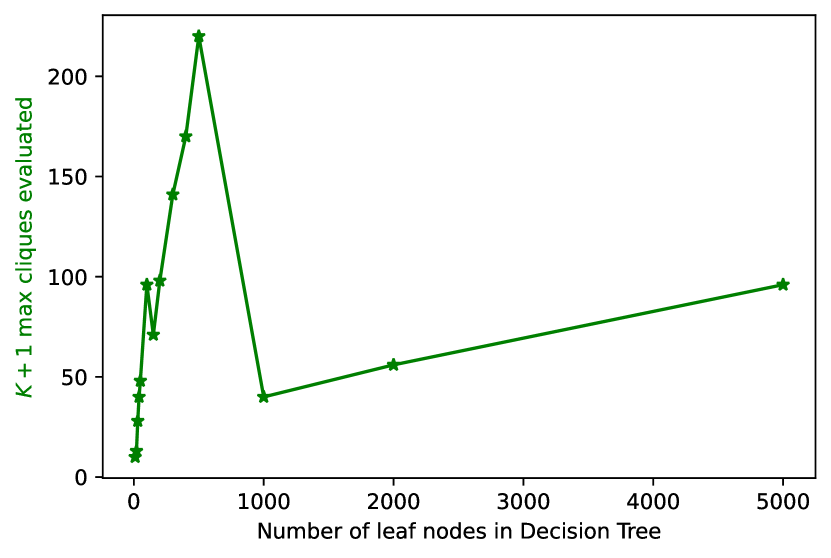

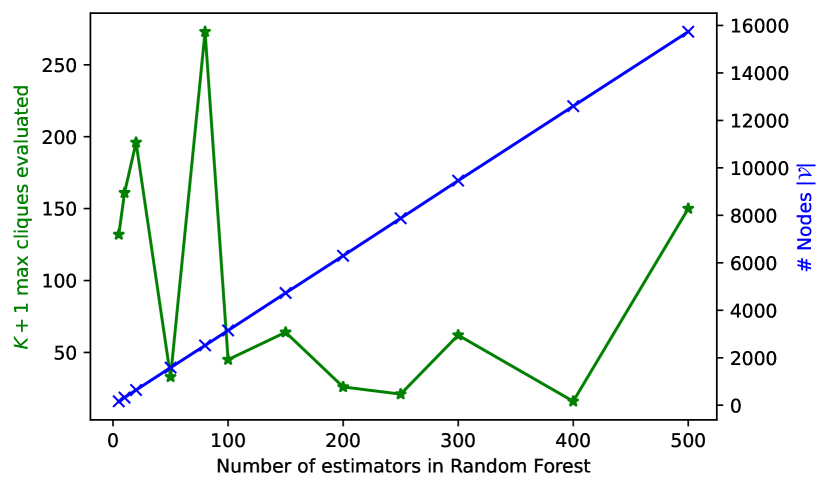

Maximum deviation vs. number of trees in a RF: In Figure 2, we highlight one result from a set of such results in Appendix D, showing maximum deviation as a function of model complexity, here quantified by the number of estimators (trees) in a Random Forest (RF). This is a demonstration of the method in Section 4.3, which in general provides bounds on the maximum deviation. In this case, the upper (“dual”) bound is informative enough to actually show a decrease as the number of estimators increases. The larger number of estimators increases averaging and may serve to make the model smoother.

6 Conclusion

We have considered the relationship between interpretability and safety in supervised learning through two main contributions: First, the proposal of maximum deviation as a means toward assessing safety, and second, discussion of approaches to computing maximum deviation and how these are simplified by interpretable model structure. We believe that there is much more to explore in this relationship. Appendices C and B.5 provide further discussion of several topics and future directions.

Acknowledgements

We thank Michael Hind for several early discussions on the topic of ML model risk assessment that inspired this work, and for his overall leadership on this topic. We also thank Dhaval Patel for a discussion on the industrial assets example in Section 2.

References

- Varshney [2022] Kush R. Varshney. Trustworthy Machine Learning. Independently Published, Chappaqua, NY, USA, 2022.

- Otte [2013] Clemens Otte. Safe and interpretable machine learning: A methodological review. In Computational Intelligence in Intelligent Data Analysis, pages 111–122. 2013.

- Varshney and Alemzadeh [2017] Kush R. Varshney and Homa Alemzadeh. On the safety of machine learning: Cyber-physical systems, decision sciences, and data products. Big Data, 5(3):246–255, September 2017.

- Doshi-Velez and Kim [2017] Finale Doshi-Velez and Been Kim. Towards a rigorous science of interpretable machine learning. arXiv preprint arXiv:1702.08608, 2017.

- Rudin [2019] Cynthia Rudin. Stop explaining black box machine learning models for high stakes decisions and use interpretable models instead. Nature Mach. Intell., 1(5):206–215, May 2019.

- Ribeiro et al. [2016] Marco Tulio Ribeiro, Sameer Singh, and Carlos Guestrin. “Why should I trust you?”: Explaining the predictions of any classifier. In Proceedings of the ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1135–1144, 2016.

- Lundberg and Lee [2017] Scott M. Lundberg and Su-In Lee. A unified approach to interpreting model predictions. In Advances in Neural Information Processing Systems, pages 4765–4774, 2017.

- Dhurandhar et al. [2018a] Amit Dhurandhar, Pin-Yu Chen, Ronny Luss, Chun-Chen Tu, Paishun Ting, Karthikeyan Shanmugam, and Payel Das. Explanations based on the missing: Towards contrastive explanations with pertinent negatives. In Advances in Neural Information Processing Systems, pages 592–603, 2018a.

- Buciluǎ et al. [2006] Cristian Buciluǎ, Rich Caruana, and Alexandru Niculescu-Mizil. Model compression. In Proceedings of the ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, 2006.

- Hinton et al. [2015] Geoffrey Hinton, Oriol Vinyals, and Jeff Dean. Distilling the knowledge in a neural network. arXiv:1503.02531, 2015.

- Rudin and Ustun [2018] Cynthia Rudin and Berk Ustun. Optimized scoring systems: Toward trust in machine learning for healthcare and criminal justice. Interfaces, 48(5):399–486, October 2018.

- Dhurandhar et al. [2018b] Amit Dhurandhar, Karthikeyan Shanmugam, Ronny Luss, and Peder Olsen. Improving simple models with confidence profiles. In Advances in Neural Information Processing Systems, pages 10296–10306, 2018b.

- Ilic and Kuvshynov [2017] Aleksandar Ilic and Oleksandr Kuvshynov. Evaluating boosted decision trees for billions of users, 2017. URL https://engineering.fb.com/2017/03/27/ml-applications/evaluating-boosted-decision-trees-for-billions-of-users/. Last accessed: 2021-10.

- Mohseni et al. [2021] Sina Mohseni, Zhiding Yu, Chaowei Xiao, Jay Yadawa, Haotao Wang, and Zhangyang Wang. Practical machine learning safety: A survey and primer. arXiv:2106.04823, 2021.

- Tomsett et al. [2018] Richard Tomsett, Dave Braines, Dan Harborne, Alun Preece, and Supriyo Chakraborty. Interpretable to whom? A role-based model for analyzing interpretable machine learning systems. In Proc. ICML Workshop Human Interpret. Mach. Learn., pages 8–14, 2018.

- Gilpin et al. [2018] Leilani H. Gilpin, David Bau, Ben Z. Yuan, Ayesha Bajwa, Michael Specter, and Lalana Kagal. Explaining explanations: An overview of interpretability of machine learning. In Proc. IEEE Int. Conf. Data Sci. Adv. Anal., pages 80–89, 2018.

- Huang et al. [2020] Xiaowei Huang, Daniel Kroening, Wenjie Ruan, James Sharp, Youcheng Sun, Emese Thamo, Min Wu, and Xinping Yi. A survey of safety and trustworthiness of deep neural networks: Verification, testing, adversarial attack and defence, and interpretability. Computer Science Review, 37(100270), 2020.

- Ehlers [2017] Rüdiger Ehlers. Formal verification of piece-wise linear feed-forward neural networks. In Automated Technology for Verification and Analysis, pages 269–286, 2017.

- Weng et al. [2018] Lily Weng, Huan Zhang, Hongge Chen, Zhao Song, Cho-Jui Hsieh, Luca Daniel, Duane Boning, and Inderjit Dhillon. Towards fast computation of certified robustness for ReLU networks. In Proceedings of the International Conference on Machine Learning, pages 5276–5285, July 2018.

- Wong and Kolter [2018] Eric Wong and Zico Kolter. Provable defenses against adversarial examples via the convex outer adversarial polytope. In Proceedings of the International Conference on Machine Learning, pages 5286–5295, 2018.

- Dvijotham et al. [2018] Krishnamurthy Dvijotham, Robert Stanforth, Sven Gowal, Timothy Mann, and Pushmeet Kohli. A dual approach to scalable verification of deep networks. In Proceedings of the Conference on Uncertainty in Artificial Intelligence, August 2018.

- Singh et al. [2018] Gagandeep Singh, Timon Gehr, Matthew Mirman, Markus Püschel, and Martin Vechev. Fast and effective robustness certification. In Advances in Neural Information Processing Systems, volume 31, 2018.

- Raghunathan et al. [2018] Aditi Raghunathan, Jacob Steinhardt, and Percy S. Liang. Semidefinite relaxations for certifying robustness to adversarial examples. In Advances in Neural Information Processing Systems, volume 31, 2018.

- Katz et al. [2019] Guy Katz, Derek A. Huang, Duligur Ibeling, Kyle Julian, Christopher Lazarus, Rachel Lim, Parth Shah, Shantanu Thakoor, Haoze Wu, Aleksandar Zeljić, David L. Dill, Mykel J. Kochenderfer, and Clark Barrett. The Marabou framework for verification and analysis of deep neural networks. In Computer Aided Verification, pages 443–452, 2019.

- Tjeng et al. [2019] Vincent Tjeng, Kai Y. Xiao, and Russ Tedrake. Evaluating robustness of neural networks with mixed integer programming. In Proceedings of the International Conference on Learning Representations, 2019.

- Anderson et al. [2020] Ross Anderson, Joey Huchette, Will Ma, Christian Tjandraatmadja, and Juan Pablo Vielma. Strong mixed-integer programming formulations for trained neural networks. Mathematical Programming, 183:3–39, 2020.

- Dathathri et al. [2020] Sumanth Dathathri, Krishnamurthy Dvijotham, Alexey Kurakin, Aditi Raghunathan, Jonathan Uesato, Rudy R. Bunel, Shreya Shankar, Jacob Steinhardt, Ian Goodfellow, Percy S. Liang, and Pushmeet Kohli. Enabling certification of verification-agnostic networks via memory-efficient semidefinite programming. In Advances in Neural Information Processing Systems, volume 33, pages 5318–5331, 2020.

- Lanckriet et al. [2002] Gert R. G. Lanckriet, Laurent El Ghaoui, Chiranjib Bhattacharyya, and Michael I. Jordan. A robust minimax approach to classification. J. Mach. Learn. Res., 3:555–582, December 2002.

- Thomas et al. [2019] Philip S Thomas, Bruno Castro da Silva, Andrew G Barto, Stephen Giguere, Yuriy Brun, and Emma Brunskill. Preventing undesirable behavior of intelligent machines. Science, 366(6468):999–1004, 2019.

- Kantchelian et al. [2016] Alex Kantchelian, J. Doug Tygar, and Anthony Joseph. Evasion and hardening of tree ensemble classifiers. In Proceedings of the International Conference on Machine Learning, pages 2387–2396, 2016.

- Parmentier and Vidal [2021] Axel Parmentier and Thibaut Vidal. Optimal counterfactual explanations in tree ensembles. In Proceedings of the International Conference on Machine Learning, pages 8422–8431, 2021.

- Chen et al. [2019] Hongge Chen, Huan Zhang, Si Si, Yang Li, Duane Boning, and Cho-Jui Hsieh. Robustness verification of tree-based models. Advances in Neural Information Processing Systems, 32:12317–12328, 2019.

- Devos et al. [2021] Laurens Devos, Wannes Meert, and Jesse Davis. Versatile verification of tree ensembles. In Proceedings of the International Conference on Machine Learning, pages 2654–2664, 2021.

- Amodei et al. [2016] Dario Amodei, Chris Olah, Jacob Steinhardt, Paul Christiano, John Schulman, and Dan Mané. Concrete problems in AI safety. arXiv:1606.06565, 2016.

- Zhu et al. [2019] He Zhu, Zikang Xiong, Stephen Magill, and Suresh Jagannathan. An inductive synthesis framework for verifiable reinforcement learning. In Proceedings of the ACM SIGPLAN Conference on Programming Language Design and Implementation, pages 686––701, 2019.

- Inala et al. [2020] Jeevana Priya Inala, Osbert Bastani, Zenna Tavares, and Armando Solar-Lezama. Synthesizing programmatic policies that inductively generalize. In Proceedings of the International Conference on Learning Representations, 2020.

- Rupprecht et al. [2020] Christian Rupprecht, Cyril Ibrahim, and Christopher J. Pal. Finding and visualizing weaknesses of deep reinforcement learning agents. In Proceedings of the International Conference on Learning Representations, 2020.

- García and Fernández [2015] Javier García and Fernando Fernández. A comprehensive survey on safe reinforcement learning. Journal of Machine Learning Research, 16(42):1437–1480, 2015.

- Yang et al. [2017] Hongyu Yang, Cynthia Rudin, and Margo Seltzer. Scalable Bayesian rule lists. In Proceedings of the International Conference on Machine Learning, page 3921–3930, 2017.

- Angelino et al. [2018] Elaine Angelino, Nicholas Larus-Stone, Daniel Alabi, Margo Seltzer, and Cynthia Rudin. Learning certifiably optimal rule lists for categorical data. Journal of Machine Learning Research, 18(234):1–78, 2018.

- Friedman and Popescu [2008] Jerome H. Friedman and Bogdan E. Popescu. Predictive learning via rule ensembles. Annals of Applied Statistics, 2(3):916–954, July 2008.

- Dembczyński et al. [2010] Krzysztof Dembczyński, Wojciech Kotłowski, and Roman Słowiński. ENDER: a statistical framework for boosting decision rules. Data Mining and Knowledge Discovery, 21(1):52–90, July 2010.

- Mirghorbani and Krokhmal [2013] M. Mirghorbani and P. Krokhmal. On finding -cliques in -partite graphs. Optimization Letters, 7(6):1155–1165, 2013.

- Auer [2002] Peter Auer. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research, 3:397–422, 2002.

- Bubeck et al. [2011] Sebastien Bubeck, Remi Munos, Gilles Stoltz, and Csaba Szepesvari. -armed bandits. Journal of Machine Learning Research, 12:1655–1695, 2011.

- Carpentier and Valko [2015] Alexandra Carpentier and Michal Valko. Simple regret for infinitely many armed bandits. In Proceedings of the International Conference on Machine Learning, pages 1133–1141, 2015.

- Dua and Graff [2017] Dheeru Dua and Casey Graff. UCI machine learning repository, 2017. URL http://archive.ics.uci.edu/ml.

- Nori et al. [2019] Harsha Nori, Samuel Jenkins, Paul Koch, and Rich Caruana. Interpretml: A unified framework for machine learning interpretability, 2019.

- Bartlett and Wegkamp [2008] Peter L. Bartlett and Marten H. Wegkamp. Classification with a reject option using a hinge loss. Journal of Machine Learning Research, 9(59):1823–1840, 2008.

- Cohen and Singer [1999] William W. Cohen and Yoram Singer. A simple, fast, and effective rule learner. In Proc. Conf. Artif. Intell., pages 335–342, 1999.

- Rückert and Kramer [2006] Ulrich Rückert and Stefan Kramer. A statistical approach to rule learning. In Proc. Int. Conf. Mach. Learn., pages 785–792, 2006.

- Wei et al. [2019] Dennis Wei, Sanjeeb Dash, Tian Gao, and Oktay Günlük. Generalized linear rule models. In Proceedings of the International Conference on Machine Learning, pages 6687–6696, June 2019.

- Koenker [2005] Roger Koenker. Quantile Regression. Cambridge University Press, 2005.

- Meinshausen [2006] Nicolai Meinshausen. Quantile regression forests. Journal of Machine Learning Research, 7(6):983–999, 2006.

- Petneházi [2019] Gábor Petneházi. QCNN: Quantile convolutional neural network. arXiv:1908.07978, 2019.

- Agarwal et al. [2021] Rishabh Agarwal, Levi Melnick, Nicholas Frosst, Xuezhou Zhang, Ben Lengerich, Rich Caruana, and Geoffrey E. Hinton. Neural additive models: Interpretable machine learning with neural nets. In Advances in Neural Information Processing Systems, volume 34, pages 4699–4711, 2021.

- Puri et al. [2021] Isha Puri, Amit Dhurandhar, Tejaswini Pedapati, Karthikeyan Shanmugam, Dennis Wei, and Kush R. Varshney. CoFrNets: Interpretable neural architecture inspired by continued fractions. In Advances in Neural Information Processing Systems, volume 34, pages 21668–21680, 2021.

- Meunier et al. [2022] Laurent Meunier, Blaise J Delattre, Alexandre Araujo, and Alexandre Allauzen. A dynamical system perspective for Lipschitz neural networks. In Proceedings of the International Conference on Machine Learning, pages 15484–15500, July 2022.

- Luss et al. [2021] Ronny Luss, Pin-Yu Chen, Amit Dhurandhar, Prasanna Sattigeri, Karthik Shanmugam, and Chun-Chen Tu. Leveraging latent features for local explanations. In Proceedings of the ACM SIGKDD International COnference on Knowledge Discovery and Data Mining, 2021.

- Weller [2019] Adrian Weller. Transparency: Motivations and challenges. In Explainable AI: Interpreting, Explaining and Visualizing Deep Learning, pages 23–40. 2019.

- Bastani et al. [2018] Osbert Bastani, Yewen Pu, and Armando Solar-Lezama. Verifiable reinforcement learning via policy extraction. In Advances in Neural Information Processing Systems, 2018.

- High Level Expert Group on Artificial Intelligence [2020] High Level Expert Group on Artificial Intelligence. Assessment list for trustworthy AI for self assessment. Technical report, European Commission, 2020. URL https://digital-strategy.ec.europa.eu/en/library/assessment-list-trustworthy-artificial-intelligence-altai-self-assessment.

- Sloane et al. [2021] Mona Sloane, Emanuel Moss, and Rumman Chowdhury. A silicon valley love triangle: Hiring algorithms, pseudo-science, and the quest for auditability. arXix:2106.12403, 2021.

- Arnold et al. [2019] Matthew Arnold, Rachel KE Bellamy, Michael Hind, Stephanie Houde, Sameep Mehta, Aleksandra Mojsilović, Ravi Nair, Karthikeyan Natesan Ramamurthy, Alexandra Olteanu, David Piorkowski, Darrell Reimer, John Richards, Jason Tsay, and Kush R. Varshney. FactSheets: Increasing trust in AI services through supplier’s declarations of conformity. IBM Journal of Research and Development, 63(4/5):6, 2019.

- Pedregosa et al. [2011] F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- Gill et al. [2020] Navdeep Gill, Patrick Hall, Kim Montgomery, and Nicholas Schmidt. A responsible machine learning workflow with focus on interpretable models, post-hoc explanation, and discrimination testing. Information, 11(3), 2020.

Checklist

-

1.

For all authors…

-

(a)

Do the main claims made in the abstract and introduction accurately reflect the paper’s contributions and scope? [Yes]

-

(b)

Did you describe the limitations of your work? [Yes] See Appendix C in particular.

-

(c)

Did you discuss any potential negative societal impacts of your work? [Yes] See Appendix C.

-

(d)

Have you read the ethics review guidelines and ensured that your paper conforms to them? [Yes]

-

(a)

-

2.

If you are including theoretical results…

-

(a)

Did you state the full set of assumptions of all theoretical results? [Yes]

-

(b)

Did you include complete proofs of all theoretical results? [Yes]

-

(a)

-

3.

If you ran experiments…

-

(a)

Did you include the code, data, and instructions needed to reproduce the main experimental results (either in the supplemental material or as a URL)? [No] The code is proprietary at this time due to our institutional obligations.

-

(b)

Did you specify all the training details (e.g., data splits, hyperparameters, how they were chosen)? [Yes] See Appendix D.

-

(c)

Did you report error bars (e.g., with respect to the random seed after running experiments multiple times)? [N/A] We report case studies assessing the safety of fixed models.

-

(d)

Did you include the total amount of compute and the type of resources used (e.g., type of GPUs, internal cluster, or cloud provider)? [Yes] See Appendix D.

-

(a)

-

4.

If you are using existing assets (e.g., code, data, models) or curating/releasing new assets…

-

(a)

If your work uses existing assets, did you cite the creators? [Yes]

-

(b)

Did you mention the license of the assets? [No] The HMDA data comes from the US government and does not appear to have a license.

-

(c)

Did you include any new assets either in the supplemental material or as a URL? [No]

-

(d)

Did you discuss whether and how consent was obtained from people whose data you’re using/curating? [N/A]

-

(e)

Did you discuss whether the data you are using/curating contains personally identifiable information or offensive content? [Yes] None of the data contain personally identifiable information, and the US Consumer Finance Protection Bureau indicates that they have modified the HMDA data to protect applicant and borrower privacy.

-

(a)

-

5.

If you used crowdsourcing or conducted research with human subjects…

-

(a)

Did you include the full text of instructions given to participants and screenshots, if applicable? [N/A]

-

(b)

Did you describe any potential participant risks, with links to Institutional Review Board (IRB) approvals, if applicable? [N/A]

-

(c)

Did you include the estimated hourly wage paid to participants and the total amount spent on participant compensation? [N/A]

-

(a)

Appendix A Additional Problem Formulation Details

Deviation function

For the case where the inputs , to are real-valued scalars (which covers binary classification and regression), while Assumption 1 was stated as a sufficient condition for tractable optimization with GAMs, it is also an intuitively reasonable requirement: the deviation should increase the farther is from in either direction. In addition, symmetry may be desirable, i.e. , to not favor one of the two models over the other. Both Assumptions 1 and 2 as well as symmetry are satisfied by monotonically increasing functions of the absolute difference, for example powers for .

For the case where as in multi-class classification, it may be advantageous for to decompose into a sum over output dimensions: , where , are the components of , . For example, the th power of the distance is separable in this manner.

Models that abstain

The formulation in Section 2 can also accommodate models that abstain from predicting (and possibly defer to a human expert or other fallback system). If , representing abstention, then we may set for any , where is an intermediate value less than the maximum value that can take [49]. The value might also be less than a “typically bad” value for , to reward the model for abstaining when it is uncertain.

Appendix B Additional Details on Deviation Maximization for Specific Model Classes

B.1 Trees

Rule lists

A rule list as defined by Yang et al. [39], Angelino et al. [40] is a nested sequence of IF-THEN-ELSE statements, where the IF condition is a conjunctive rule and the THEN consequent is an output value. If each rule involves a single feature (i.e., the conjunctions are of degree ), such rule lists are one-sided trees in the sense of Section 4.1. The number of leaves in the equivalent tree is equal to the number of rules in the list (including the last default rule).

Intersection of with a Cartesian product

If is also a Cartesian product, then determining whether the intersection is non-empty amounts to checking whether all of the coordinate-wise intersections with , , are non-empty. If is not a Cartesian product but is a union of balls (which are Cartesian products), then the intersection is non-empty if the intersection with any one ball is non-empty.

Relationship between Proposition 1 and [32, Theorem 1]

In the case of a -tree ensemble, [32, Theorem 1] bounds the complexity of exact robustness verification as , where is the maximum number of leaves in a tree and we assume that the feature dimension . In Proposition 1, we account for the possibly different numbers of leaves and in the two trees and , and we exactly enumerate the edges, .

Additive reference model

For the case where is a decision tree and is a generalized additive model, if the deviation function is symmetric, , then this case is covered in Section 4.2.

B.2 Linear and Additive Models

Categorical features

A function of a categorical feature can be represented in two ways, depending on whether is a GAM or a GLM. In the GAM case, we may use the native representation in which takes values in a finite set of categories. In the GLM case, is one-hot encoded into multiple binary-valued features , one for each category . Then any function can be represented as a linear function,

where is the value of for category .

Implication of Assumption 1

The second condition implies that the deviation increases or stays the same as moves away from in either direction.

Proof of Proposition 2.

Let and . Under Assumption 1.1, if , then

As increases from , also increases because is an increasing function, and increases or stays the same due to Assumption 1.2. Similarly, as decreases from , decreases, and again increases or stays the same. It follows that to maximize , it suffices to separately maximize and minimize , compute the resulting values of , and take the larger of the two. This yields the result. ∎

Implication of Assumption 2 and identity link function

These two assumptions imply that the deviation is measured on the difference between and in the space in which they are additive. For example, if and are logistic regression models predicting the probability of belonging to one of the classes, the difference is taken in the log-odds (logit) domain. It is left to future work to determine other assumptions under which problem (1) is tractable when and are both additive.

Cartesian product implies Cartesian product

In the cases of constant and additive , . In the decision tree case, since each leaf is a Cartesian product , the intersections are also Cartesian products where .

One-dimensional optimization complexities

For discrete-valued , is proportional to the number of allowed values . For continuous , it is common to use spline functions or tree ensembles as in constructing GAMs. In the former case, is proportional to the number of knots. In the latter, the tree ensemble can be converted to a piecewise constant function and is then proportional to the number of pieces. Lastly in the case where is linear and is an interval, because it suffices to evaluate the two endpoints.

Convex

If is a convex set, then in the cases of constant and additive , is also convex. In the case of tree-structured , and each leaf can be represented as a convex set, with interval constraints on continuous features and set membership constraints on categorical features. The latter can be represented as constraints on the one-hot encoding (see “Categorical features” paragraph above) for non-allowed categories . Hence is also convex.

As a specific example, suppose that is the product of independent constraints on each categorical feature and an norm constraint on the continuous features jointly. The maximization over each categorical feature has complexity as noted above, while the maximization of over continuous features lying in an ball has closed-form solutions for the common cases .

Relaxations of the Cartesian product assumption

If the certification set is not a Cartesian product, then one way to still bound the maximum deviation is to find the smallest Cartesian product that contains and maximize deviation over . As long as it is relatively easy to optimize linear functions over , then constructing such a Cartesian product is similarly easy. Another conceivable relaxation of the Cartesian product assumption is a Cartesian product of low-dimensional sets, not just one-dimensional.

B.3 Tree Ensembles

The full algorithm for clique search from Section 4.3 is presented in Algorithm 1. It uses as a node compatibility vector to keep track of valid leaves and a set of trees/partites not yet covered by the maximum clique. The algorithm starts with and empty clique and anytime bounds as . It starts the search with the smallest tree to limit the search space. This is typically . Each leaf is added to the intermediate clique in turn (Line 6). A stronger primal bound can be achieved if the traversal is ordered in a meaningful way. In particular, starting with nodes with the highest heuristic function value aids the algorithm to focus on better areas of the search space.

If the size of the clique is the primal bound is updated. Otherwise, the dual bound is computed. If the node is promising, the algorithm recurses to the next level. When the search is terminated at any step, the maximum deviation is bounded by .

Rule ensembles

Similar to the tree ensembles considered in Section 4.3, a rule ensemble is a linear combination of conjunctive rules, where the antecedent is a conjunction of conditions on individual features, and the consequent takes a real value if the antecedent is true and zero otherwise. They are produced by algorithms such as SLIPPER [50], that of Rückert and Kramer [51], RuleFit [41], ENDER [42] and have also been referred to as generalized linear rule models [52]. A rule ensemble can be converted into a tree ensemble by converting each conjunctive rule into an IF-THEN-ELSE rule list, which is a one-sided tree (see Appendix B.1). Specifically, the conditions in the conjunction are taken in any order, each condition is negated to become an IF condition, and the THEN consequents are all output values of zero. The final ELSE consequent, which is reached if all the IF conditions are false (and hence the original rule holds), returns the output value of the original rule. The number of leaves in the resulting tree equals the number of conditions in the conjunction plus one.

B.4 Piecewise Lipschitz Functions

Proof of Proposition 3.

Consider two inputs and then,

where, and . ∎

Other choices for : The results assumed to be the identity function, where . This choice of function clearly satisfies Assumptions 1 and 2. Again consistent with these assumptions we look at some other choices for . If were an affine function with a positive scaling such as where , then our result in equation 14 would be unchanged as only the Lipschitz constant of would change, but not its (underestimated) order. If the function were a polynomial or exponential however, no such guarantees can be made and we would be back to case 1.

B.5 Other Model Classes: Neural Networks and Post Hoc Explanations

For model classes beyond the ones discussed in Section 4, it appears to be a greater challenge to obtain reasonably tractable algorithms that guarantee exact computation of or bounds on the maximum deviation. Here we outline some future directions for neural networks and post hoc explanations.

Robustness verification for neural networks has attracted a great deal of attention and made considerable progress, with exact approaches including satisfiability modulo theory [24] and mixed integer programming [25, 26], and incomplete methods that compute bounds using bound propagation [22, 19], linear programming and duality [18, 20, 21], and semidefinite programming [23, 27]. However, all of these methods consider a single model, effectively comparing it to a constant. Robustness verification is thus essentially a single-model case of our problem (1) in which is a constant (and with an appropriate choice of the deviation function ). While we may expect that solutions to a two-model verification problem would leverage existing robustness verification methods, developing such solutions remains for future work. Furthermore, evaluation of robustness verification methods has largely been limited to local neighborhoods around input points (with typical radii in terms of normalized feature values). This limitation may also need to be addressed to enable evaluation of maximum deviation in the way envisioned in this paper.

It is also natural to ask whether post hoc explanations for the model can help. One way in which this could occur is if the post hoc explanation approximates the model by a simpler model and if the deviation function satisfies the triangle inequality . Then the maximum deviation in (1) would be bounded as

| (15) |

While we may choose to be interpretable so that the rightmost maximization is tractable, the middle maximization asks for a uniform bound on the deviation between and , i.e, the fidelity of . We are not aware of a post hoc explanation method that provides such a guarantee. Indeed, in general, the middle maximization might not be any easier than the left-hand one that we set out to bound.

A (practical) possibility may be to perform quantile regression [53] for a large enough quantile to learn , as opposed to minimizing expected error as is typically done. This may be an interesting direction to explore in the future as quantile regression algorithms are available for varied model classes including linear models, tree ensembles [54] and even neural networks [55]. More investigation is needed into whether quantile regression methods can provide approximate guarantees on the middle term in (15).

Assuming that uniform proxies in the above sense can be constructed, then for certain modalities or applications it may be possible to train highly accurate proxies. For instance for tabular data, Random Forests or boosted trees might very well replicate the behavior of a neural network, in which case the machinery introduced in Section 4.3 could be used. Even for other modalities such as text and images, interpretable models such as Neural Additive Models (NAMs) [56] and continued fraction networks (CoFrNets) [57] may prove to be sufficient in some cases.

Finally, there are recent architectures such as Lipschitz neural networks [58] which are adversarially robust and hence valuable in practice. Our analysis presented in Section 4.4 for piecewise Lipschitz models would be applicable here, where the simple regret of standard bandit algorithms for a given number of queries could be reduced to (14) as opposed to (13).

Appendix C Further Discussion

Worst-case approach

The formulation of (1) as the worst case over a certification set represents a deliberate choice to depend as little as possible on a probability distribution or a dataset sampled from one. As stated in Section 2, Certification Set paragraph, can depend at most on (an expanded version of) the support set of a distribution. The reason for this choice is because safety is an out-of-distribution notion: harmful outputs often arise precisely because they were not anticipated in the data. The trade-off inherent in this choice is that the maximum deviation may be more conservative than needed. The high maximum deviation values in e.g. Figure 11 may reflect this. Given definition (1) as a starting point in this paper, future work could consider variations that depend more on a distribution and are thus less conservative, but may also offer a weaker safety guarantee.

Choice of reference model

The proposed definition of maximum deviation (1) depends on the choice of reference model . Different choices will lead to different deviation values and, perhaps more importantly, different combinations of features that maximize the deviation. We have discussed possible choices in Section 2, and the results in Section 4 indicate that, as with the assessed model , interpretable forms for can ease the computation of maximum deviation. Beyond these guidelines, it is up to ML practitioners and domain experts to decide on appropriate reference models for their application (and there may be benefit to considering more than one). We mention an additional concern with the reference model in the Ethics Discussion.

For some real applications it may be difficult to come up with a globally interpretable reference model. But specific to particular scenarios it may be possible. For instance, it might be difficult to provide general rules for how to drive a car, but in specific scenarios such as there being an obstacle in front, one can suggest that you stop or turn, which is a simple rule. So our machinery could potentially be applied at a local level where the reference model is interpretable in that locality. This might help in “spot checking" a deployed model and estimating its safety by computing these maximum deviations in scrupulously selected (challenging) scenarios.

Impossible inputs in certification set

Mathematically simple sets such as Cartesian products and balls permit simpler algorithms for optimizing functions over them. Accordingly, these sets have been the focus of not only the present work but also the related literature on ML verification and adversarial robustness. However, they may not serve to exclude inputs that are physically or logically impossible from the certification set , and thus, the resulting maximum deviation values may be too large and conservative. Here it is important to distinguish between impossible inputs and those that are merely implausible (i.e., with low probability). Techniques for capturing implausibility have been proposed for contrastive/counterfactual explanations [8, 59], whereas we expect the set of impossible inputs to be smaller and more constrained. As a simple example from the Adult Income dataset, if we agree that a wife/husband is defined to be of female/male gender (regardless of the gender of the spouse), then the cross combinations male-wife and female-husband cannot occur. Future work can consider the representation and handling of such constraints.

White-box vs. grey-box models

In this paper, we have assumed full “white-box” access to both and , namely complete knowledge of their structure and parameters. Interesting questions may arise when this assumption is relaxed to different “grey-box” possibilities. For example, one could further investigate the third case in Section 4.4, where one of is black-box and the other is white-box interpretable. There may exist assumptions that we have not identified that would improve the query complexity compared to generic black-box optimization.

Other interpretability-safety relationships

This paper has focused on one relationship between the interpretability of a model and the safety of its outputs. It has not addressed other ways in which interpretability/explainability can affect the risk of a model (in the plain English sense, not the expectation of a loss function). For example, in regulated industries such as consumer finance, not providing explanations or providing inadequate ones can lead to legal, financial, and reputational risks. On the other hand, providing explanations is associated with its own risks [60]. These include the leakage of personal information or model information (intellectual property), an increase in appeals of decisions for the decision-making entity, and strategic manipulation of attributes (i.e. “gaming”) by individuals to gain more favorable outcomes.

Applicability to RL settings

In RL, if one views the actions as labels and state representation as features, one can build a tree, albeit likely a deep/wide one, to represent exactly the RL policy, where the probability distribution over the actions can be viewed as the class distribution in a normal supervised setting. Rolling up the states, creating leaves with multiple states, and simply averaging the probabilities for each action would yield smaller trees that approximate the policy. Our work lays a foundation where in principle we can also compare and that are policies using such tree representations. This may be related to a popular global explainability method [61] that samples policies and builds trees to explain them.

Ethics

The safety of machine learning systems has been called out by the European Commission’s regulatory framework [62]. The commission states seven key dimensions to be evaluated and audited by a cross-disciplinary team: (i) human agency and oversight, (ii) technical robustness and safety, (iii) privacy and data governance, (iv) transparency, (v) diversity, non-discrimination and fairness, (vi) environmental and societal well-being, and (vii) accountability. The second of these dimensions is safety. However, Sloane et al. [63] argue that algorithmic audits are ill-defined as the underlying definitions are vague. The proposed work helps fill that ill-definedness using a quantitative approach. One may argue against this particular choice of quantification, but it does start the community down the path toward being more concrete in its definitions.

As with many other technologies, the proposed approach may be misused. For example, the reference model may be chosen in a way that hides the safety concerns of the model being evaluated. Transparent documentation and reporting with provenance guarantees can help avoid this kind of purposeful deceit [64].

Appendix D Experiment Details and Additional Results

D.1 General Experiment Details

Data processing

We use the training set of each dataset to train models and the test set as the basis for evaluating maximum deviation, specifically as the set of centers for the balls in (2). Continuous features are standardized and categorical features are one-hot encoded. The norm is computed on the resulting normalized feature values.

Models

We use scikit-learn [65] to train decision tree (DT), logistic regression (LR), and Random Forest (RF) models. The corresponding complexity parameters are the number of leaves for DT (parameter max_leaf_nodes), the amount of regularization for LR (inverse penalty ), and the number of estimators/trees for RF (n_estimators). For additive models, we use Explainable Boosting Machines (EBM) from the InterpretML package [48] with zero interaction terms (so that the models are indeed additive). Smoothness is controlled by the max_bins parameter, the number of discretization bins for continuous features.

Deviation maximization

In all cases, when the certification set radius , maximum deviation can be computed simply by evaluating the models on the test set. For the case where , is a DT or RF, and is a DT, Algorithm 1 is used (on a bipartite graph if is a DT). The cases where is LR or EBM fall under the generalized additive case of Section 4.2. Given that is a DT, we use (7), (6) to determine the maximum deviation. For when is a union of balls, we maximize separately over each intersection between a ball and a leaf of and then take the maximum over the intersections.

Computation

All experiments were run on CPU nodes with 64GB memory. For decision trees and tree ensembles run times of Algorithm 1 were limited to hours, after which the best available bounds were used.

D.2 Home Mortgage Disclosure Act Dataset

Data source and pre-processing

The data is made available by the US Consumer Finance Protection Bureau (CFPB) under the Home Mortgage Disclosure Act (HMDA). We use the national snapshot from year 2018222https://ffiec.cfpb.gov/data-publication/snapshot-national-loan-level-dataset/2018 of “loan/application records,” which contain information on mortgage applications and their outcomes. According to their website, the CFPB has modified the data to protect applicant and borrower privacy.

We processed the 2018 loan/application records as summarized below. These steps were informed by Gill et al. [66] but not identical to theirs:

-

•

Restrict to complete, submitted applications with ‘action_taken’ (loan originated, application approved but not accepted by applicant, or application denied).

-

•

Create a binary-valued target variable representing approval by binarizing ‘action_taken’ (originated or approved , denied ).

-

•

Restrict to purchases of principal residences (the most consequential in terms of people’s lives, i.e., not refinances or for investment) and single-family homes.

-

•

Restrict to loans that are not “special” in any way: conventional loans, first mortgages, not manufactured homes, no non-amortizing features, etc.

-

•

Drop columns that are not applicable for site-built single-family homes.

-

•