A data-driven case-based reasoning in bankruptcy prediction

Abstract

There has been intensive research regarding machine learning models for predicting bankruptcy in recent years. However, the lack of interpretability limits their growth and practical implementation. This study proposes a data-driven explainable case-based reasoning (CBR) system for bankruptcy prediction. Empirical results from a comparative study show that the proposed approach performs superior to existing, alternative CBR systems and is competitive with state-of-the-art machine learning models. We also demonstrate that the asymmetrical feature similarity comparison mechanism in the proposed CBR system can effectively capture the asymmetrically distributed nature of financial attributes, such as a few companies controlling more cash than the majority, hence improving both the accuracy and explainability of predictions. In addition, we delicately examine the explainability of the CBR system in the decision-making process of bankruptcy prediction. While much research suggests a trade-off between improving prediction accuracy and explainability, our findings show a prospective research avenue in which an explainable model that thoroughly incorporates data attributes by design can reconcile the dilemma.

keywords:

Decision support systems , Bankruptcy prediction , Case-based reasoning , eXplainable AI1 Introduction

Bankruptcy refers to the circumstance in which an organization fails to satisfy its obligations, pay its due liabilities, and must consequently undergo debt restructuring or liquidation of its assets. Corporate bankruptcy is one of the main drivers of credit risk, and its economic consequences could be disastrous 52. The amount of corporate insolvency throughout the economy may impose considerable negative societal costs and has a structural role in the propagation of recessions 11. Given these consequences, bankruptcy prediction is crucial to inform the debt management and loan approval processes of financial institutions. Much research has examined bankruptcy prediction models. An accurate model benefits investors, creditors, auditors and government policymakers 25. However, obtaining accurate bankruptcy predictions is challenging. Typically, bankruptcy prediction is an imbalanced, high-dimensional, nonlinear classification problem that necessitates both precision and transparency in the prediction process 52, 23. In this study, we aim to create an automatic design case-based reasoning (CBR) system with an asymmetrical structure that can accurately predict bankruptcy and demonstrate interpretability in the decision-making process. In particular, we find that applying the asymmetrical function to calculate feature similarity is an effective way to enhance prediction accuracy by disentangling the asymmetrically distributed information existing in financial data, further boosting the economic interpretability of the optimized parameters.

Recently, classification techniques based on machine learning (ML) have gained much popularity in the field and have demonstrated impressive predictive accuracy. Contrary to traditional approaches, ML models like neural networks, random forest, or boosting machines have fewer data-related assumptions and can capture nonlinear dependencies in the feature-target relationship in a data-driven manner. These characteristics equip ML models with more flexibility to adapt to complex data. However, a major issue with the current generation of ML algorithms is that they prioritize accuracy above explainability. Thus, they have been criticized for their black-box character, meaning that a trained model does not clarify the transformation of feature values into a (bankruptcy) prediction 21. This opaqueness limits the applicability and value of ML in sensitive fields such as banking or healthcare. In addition, it is not straightforward how ML model predictions assist pre/post-bankruptcy decisions, such as, for example, aiding decision-makers to prevent bankruptcy a priori. Moreover, current legislation, such as the general data protection regulation (GDPR) in the European Union, further limits the application of black-box ML models. In particular, decisions based solely on automated processing are forbidden, and meaningful explanations of the rationale involved must be provided 72. The fields of interpretable ML and explainable AI aim at addressing these challenges by developing approaches that give accurate predictions and decision-making rationales, which allow humans to comprehend and trust the models and the recommendations they generate.

CBR is a promising approach for providing transparency and explainability in the process of bankruptcy prediction. Transparency is the explanation objective that enables people to comprehend and investigate how the calibrated model generated the forecast. It is intuitive to understand the concept of finding a solution for a new problem based on similar cases for which solutions are available. This understanding underlines the decision process in CBR 66. The natural explanation capability of the CBR system has increased its applications in a variety of domains 17, 55, 24, 61, 7, 76. It is especially valued by decision-support systems if it is desired to comprehend how the system generates a suggestion 56, such as when a doctor’s diagnosis is being supported 29, 42. The study of Cunningham et al. 22 shows that the explanation of predictions is important, and case-based explanations will significantly improve user confidence in the solution compared to rule-based explanations or only displaying the problem solution. In the context of bankruptcy prediction, reasons for a company’s insolvency can be analyzed by comparing its status with other similar companies, which is helpful for developing a rescue strategy. Additionally, distinct input variables provide additional information that contributes unequally to the prediction. Identification of the most relevant facts may be utilized to adjust a company’s future action choices for resolving insolvency. For instance, the determination of a merger with an insolvent company requires careful consideration. Several ML algorithms, including neural networks and random forest, have disregarded this crucial need. Meanwhile, the CBR method allows users to recognize which factors are essential for the decision-making process.

However, the current generation of CBR systems suffers from inaccuracy in bankruptcy prediction. In the CBR mechanism, it is vital for the CBR process to get the most similar instances from the available database. Thus, a successful CBR retrieval method relies heavily on domain expertise and design experience. Even for specialists, it is difficult to gain efficient domain knowledge and establish a priori the set of most effective parameters in similarity calculation functions to solve a particular issue. For instance, it is not straightforward to design a function and assign its parameters to compare the similarity between two companies. In this research, we consider a data-driven CBR system with an asymmetrical automated design to improve the accuracy of bankruptcy predictions. Cornerstones of the underlying methodology have originally been proposed by Li et al. 47. The results of the extensive experimental studies show the effectiveness of the asymmetrical local similarity function in escalating the prediction performance among the best ML models, such as XGBoost, random forest and neural network models. To further enhance the explainability of model predictions and clarify their use cases, we propose Shapley-CBR, an approach to evaluate the contributions of feature values to the model-predicted bankruptcy probability. Lastly, prior work on CBR systems does not study the economic meanings behind local parameters. We comprehensively show the explainability of the parameters and enhance the transparency in the asymmetrical CBR system.

1.1 Literature review

The prediction of bankruptcy for companies has been an extensively researched area since the late 1960s 3. Much of the current studies aim to develop more accurate models, which has contributed to the introduction of numerous algorithms for bankruptcy prediction 53, 64, 31, 43, 68, 30. Martin 53 presented a logistic regression to predict bankruptcy based on the data obtained from the Federal Reserve System. In the study of Härdle et al. 30, a support vector machine was used to predict the solvency or insolvency of companies. The results showed that SVMs are capable of extracting useful information from financial data and then labeling companies by giving them score values. The study from Sun and Shenoy 68 provided operational guidance for building Naive Bayes Bayesian network models for bankruptcy prediction using financial and accounting factors. In the last decade, neural network models experienced rapid development and increased their contributions to bankruptcy prediction research. Hosaka 33 applied convolutional neural networks to predict bankruptcy by presenting correspondence between financial ratios as grayscale images. In the study of Jardin 36, an ensemble of self-organizing neural networks was used in bankruptcy prediction. The results from the research showed that deep neural networks significantly increase the prediction accuracy that can be obtained with conventional methods. However, much of the studies in this stream of literature work on the improvement of the accuracy and ignore the investigation of its explainability in bankruptcy-based decision makings. Distinguishing from the literature, our study primarily endeavours to develop an explainable model with high-level predictability for bankruptcy prediction.

Especially, transparency and economic meanings are pivots in financial sectors. Several prior studies have applied the CBR system in bankruptcy prediction and business decision making 37, 2, 73, 18, 34. Jo et al. 37 compared the bankruptcy prediction performance of multivariate discriminant analysis, CBR, and neural networks. The results showed neural networks performed best. For the CBR, a simple weighted Euclidean metric model was used to measure similarities. In the study of Ahn and Kim 2, a hybrid CBR system using a genetic algorithm was proposed to optimize feature weights to increase bankruptcy prediction accuracy. The authors stated that the CBR system has a good explanation ability and high prediction performance over the other ML methods. However, the conclusion is ambiguous, and no experiments or case studies were conducted to substantiate the assertions. Chuang 18 developed three hybrid CBR methods for enhancing CBR performance in bankruptcy prediction. Although multiple experiments to compare their performance had been conducted, the study lacked comparison with other widely-used models and did not examine the explainability of CBR in bankruptcy prediction. In the study of Vukovic et al. 73, a CBR method combined with an optimization algorithm was used for credit scoring. The results showed that the proposed CBR method improved the performance of the traditional CBR system and outperformed the -nearest neighbour classifier. However, the study did not mention the explainability of the CBR method. The recent study of Li et al. 47 provided abundant empirical evidence that the asymmetrical CBR system can predict as accurately as the majority of ML models. However, the research did not examine its efficacy in predicting insolvency. Moreover, the lack of explainability in parameters still needed supplementation. Compared with the previous research, our study aims to examine and explore the transparency and explainability of CBR comprehensively.

Besides, in light of the significant drawback of black-box ML model implementations in the financial sector, a number of recent studies have focused on post-hoc approaches for explicating ML models. The most prevailing one is Shapley value, which is widely used in cooperative game theory, allocating the entire rewards to the players on the assumption that they are all cooperating 32. The value is the average marginal contribution of a player across all possible coalitions. The Shapley method has been applied in numerous fields, such as minimal cost spanning trees 10, risk capital allocation 5, closed-loop supply chain 75 and liability games 20. In recent years, its application has been extended to other sectors, e.g., improvement in the explainability of ML models 50. Lundberg et al. 49 investigated the explainability of the Shapley method in tree-based ML models, such as random forest, decision trees and gradient boosted trees. Li and Becker 46 applied the Shapley values to explain the predictive results of the support vector machine model for electricity price forecasting under consideration of market coupling. In the study of Jabeur et al. 35, the Shapley interaction values are used to explain the forecasting of the gold price with the XGBoost algorithm. The conservative business and banking sector are often resistive to revolutionary algorithms. It has raised the question that if the black-box model is explainable. The black-box nature of neural networks constrains their explainability in the results. According to Rudin 63, the applications of black-box ML models are criticized for high-stakes decision-making throughout society. This study employed Shapley value to enhance the explainable CBR system by evaluating the feature importance in the prediction probability of insolvency and providing decision support for rescuing an insolvent company.

The contribution of this article is threefold. Our method is first to consider utilising the asymmetrical nature of financial features to design and improve the CBR system. In particular, we examine the efficiency of the asymmetrical CBR system in solving bankruptcy prediction problems, which performs significantly better than the conventional distance-based CBR system and can perform as well as the widely used ML models, such as XGBoost and neural networks models. The reason behind this fact is that the asymmetrical local similarity function can better capture the asymmetrical properties that exist in financial features compared with existing other similarity functions. Our study provided a new research direction that a data-driven well-fitted model can not only escalate the prediction accuracy but enhance explainability. This can overcome the conflict between model accuracy and model intractability inaugurated by Barredo Arrieta et al. 6. Second, according to the study of Barredo Arrieta et al. 6, transparent ML models convey some degree of explainability by themselves. The levels of transparency can be evaluated based on three aspects, i.e., algorithmic transparency, decomposability and simulatability. Our study aims to examine and explore the transparency and explainability of CBR comprehensively in terms of the three aspects. In particular, we first illustrate that the fitted polynomial parameters in the proposed function can reveal the economic meanings for the similarity comparison, which enhance the algorithmic transparency and decomposability of the CBR system. It is useful for users to investigate the reasons behind bankruptcy. Third, the posterior probability estimator of CBR combined with a post-hoc explainability technique, Shapley value, is first developed for investigating the influence of features on the predicted insolvent probability. The applications of the Shapley-CBR concerned with bankruptcy-related decisions have been extensively investigated in empirical studies.

The rest of this paper is organized as follows. Section 2 is the data description. Section 3 introduces the asymmetrical CBR system. It is followed by the experiment design, introduced in Section 4. The experiment results and explanation instances are shown in Section 5 and Section 6. Section 7 concludes the paper.

2 Data description

The dataset applied in this study comes from the credit reform database provided by the Blockchain Research Center (BRC, https://blockchain-research-center.de/). It contains financial information from 20,000 solvent and 1,000 insolvent German companies. The last annual financial report of a company is used to predict its solvency in the next year. There are 28 variables, i.e., cash, inventories, equity, and current assets. The list of features is shown in Table 1.

| No. | Feature | No. | Feature |

|---|---|---|---|

| VAR1 | Cash | VAR15 | Accounts payable (A.P.) |

| VAR2 | Inventories | VAR16 | Sales |

| VAR3 | Current assets | VAR17 | Administrative expenses |

| VAR4 | Tangible assets | VAR18 | Amortization depreciation |

| VAR5 | Intangible assets | VAR19 | Interest expenses |

| VAR6 | Total assets | VAR20 | EBIT |

| VAR7 | Accounts receivable (A.R.) | VAR21 | Operating income |

| VAR8 | Lands and buildings | VAR22 | Net income |

| VAR9 | Equity | VAR23 | Increase inventories |

| VAR10 | Shareholder loan | VAR24 | Increase liabilities |

| VAR11 | Accrual for pension liabilities | VAR25 | Increase cash |

| VAR12 | Total current liabilities | VAR26 | A.R. against affiliated companies |

| VAR13 | Total long-term liabilities | VAR27 | A.P. against affiliated companies |

| VAR14 | Bank debt | VAR28 | Number of employees |

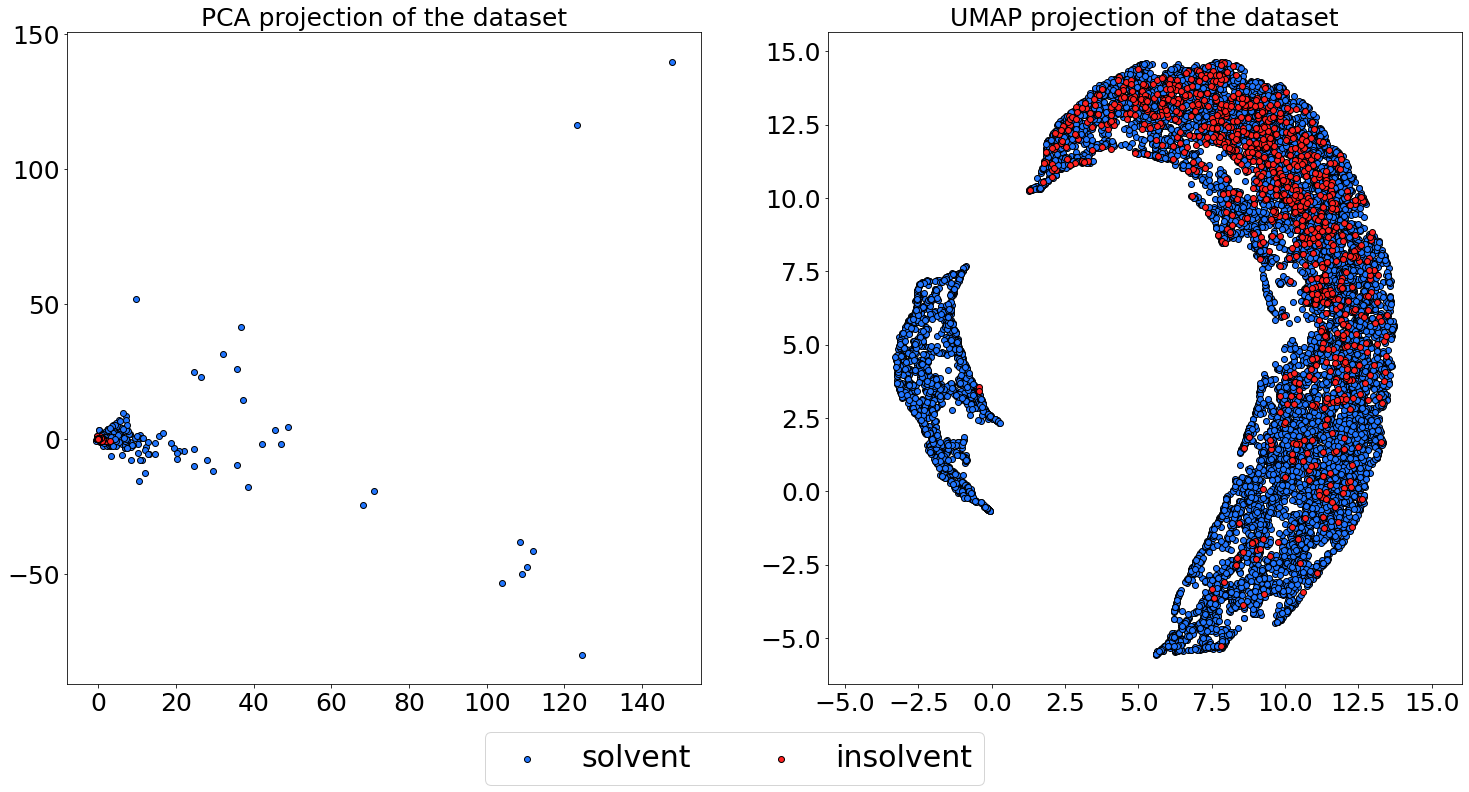

The dataset has been visualized in Figure 1, based on two-dimensionality reduction techniques, Principal Component Analysis (PCA), and Uniform Manifold Approximation and Projection (UMAP). From the PCA plot in Figure 1, we can see that the insolvent data points are agglomerated together, but clearly not enough to set them apart from the solvent ones. From the UMAP plot in Figure 1, the solvent data points are clearly separated into two groups. The fiscal year of companies in the small group was 2003 when Germany was experiencing a temporal recession, and the German government announced a set of policies to spur the economy 26. This is one reason that the small group is isolated from the main group. However, the insolvent data points are scattered, and there are no big clusters separating the sign sufficiently.

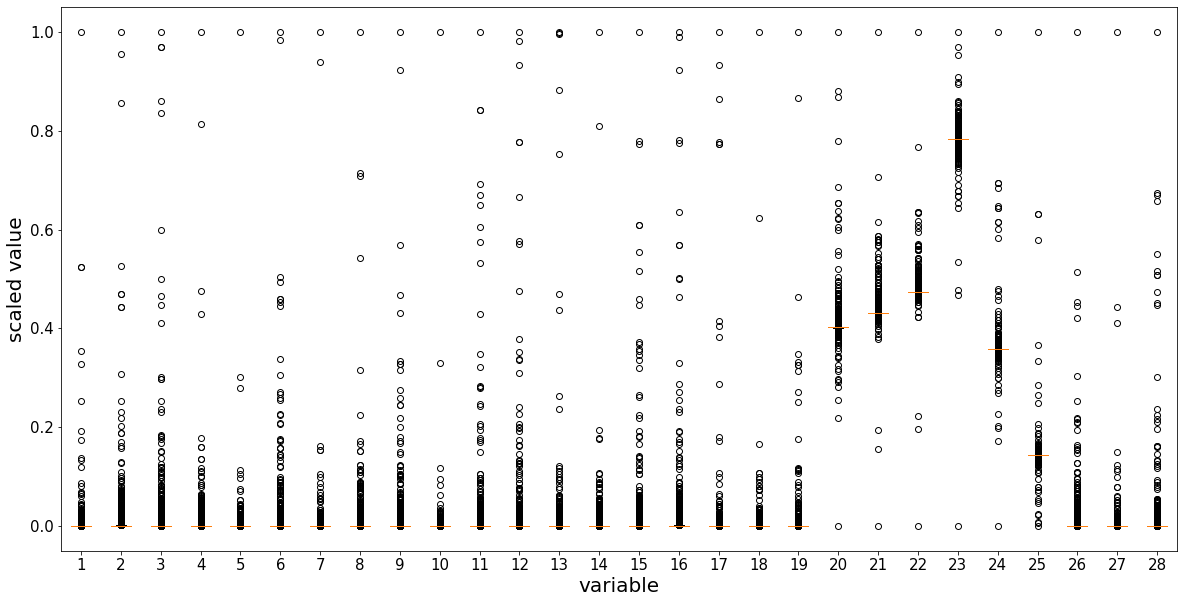

The scaled value (between 0 and 1) of each feature variable has been shown in Figure 2. From the figure, we can observe that those features are asymmetrically distributed. Such distributional property is common for financial data features. For instance, the majority of companies are small and medium-size, which often suffer from limited cash flow. By contrast, few are large companies that can dispose of large amounts of cash. Thus, it is reasonable to investigate the effectiveness of the asymmetrical similarity function when calculating similarities of cash or other features between a query company and its relatively smaller and larger companies, respectively.

3 Methodology

CBR is a typical explainable ML approach, the decision-making process of which is analogous to that of humans, i.e., a solution to unravel new problems can be considered based on past experiences. The logic framework of CBR typically includes four R steps 1: 1) To solve a new issue without a solution, previous cases with solutions are retrieved (R) to determine which are most similar to the current problem; 2) The solutions of the most similar problems are reused (R) to offer a solution for the new case. 3) Whether the new issue has been resolved can be revised (R); 4) The resolved new problem will be retained (R) in the case database for future use. Clearly, the most crucial of the four R steps is the first R, which entails retrieving the case database and identifying the most similar cases, as this influences the success of the subsequent decision-making process. By calculating the similarity of cases, it can be mathematically converted into a prediction problem.

3.1 Similarity calculation in CBR

CBR systems aim to find the most similar cases of a query case in the case base (dataset) and detect its solutions based on similar cases. In most cases, the similarity computation adheres to the local-global principle for customizing the similarity measure for each attribute and constructing a knowledge model, which is prevalent in attribute-based CBR systems 62. Given a query case and a case from a -dimensional database ( features), the distance between two cases on the th feature can be employed to measure the local similarity, which can be expressed as . The Euclidean distance metric has been commonly applied for distance-based CBR similarity measure in the area of financial distress prediction 44. Let express the global similarity between case and case , and be feature weights (). The mechanism for measuring similarity in Euclidean space could be derived from the distances between two cases on each feature, as denoted by ECBR and shown below:

| (1) |

The Manhattan distance metric is another extensively used distance-based measure of similarity in the field of CBR (MCBR). It could be demonstrated as follows:

| (2) |

In addition, the grey coefficient degrees have been developed for local similarity calculation (GCBR). Let expresses the case base (dataset) without case , and and represent the minimum and maximum distances of case and the case base on the th feature, respectively. The similarity between two cases on the foundation of weighted average of grey coefficient degrees can be calculated as follows:

| (3) |

where

| (4) |

3.1.1 Asymmetrical CBR

The design of the asymmetrical CBR (ACBR) also follows the local-global principle. In particular, the global similarity is measured by the square root of the weighted sum of the asymmetrical local similarities. The similarity between and can be described as follows:

| (5) |

where, for the attribute , is the local similarity function, and are attribute values from the case and , respectively. stands for the weight (global parameters) of the attribute . For the local (feature) similarity, asymmetrical polynomial functions are commonly used to measure the similarity of attribute-value 4. It can be represented as:

| (6) |

where stands for the difference between the maximum and minimum value of attribute in the dataset. and are the degree (local parameters) of polynomial functions. The similarities between a query case and all the cases in the dataset are calculated based on Equations (5) and (6). Thus, the global parameter and local parameters and are required to automatically design a data-driven CBR system without human involvement. The following subsection is to introduce how to obtain those parameters. A simple instance of the similarity calculation can be found in Appendix A.

3.2 Data-driven ACBR system design

In addition to the parameters , and , the ACBR system classifies a given query case by picking the most similar examples from the matching dataset. Then, majority voting is used to give the query case the class with the highest frequency among similar cases. Thus, the is the other parameter to be determined. The well-known -nearest neighbors method (-NN), which may be termed a non-parametric CBR, is used to find the parameter . In the -NN paradigm, a case is typically categorized by the majority vote of its distance-based neighbors. Indeed, the only parameter affecting the classification accuracy of the -NN model that must be calculated is . Cross-validated grid search across a parameter grid may be used to determine the best for a given dataset.

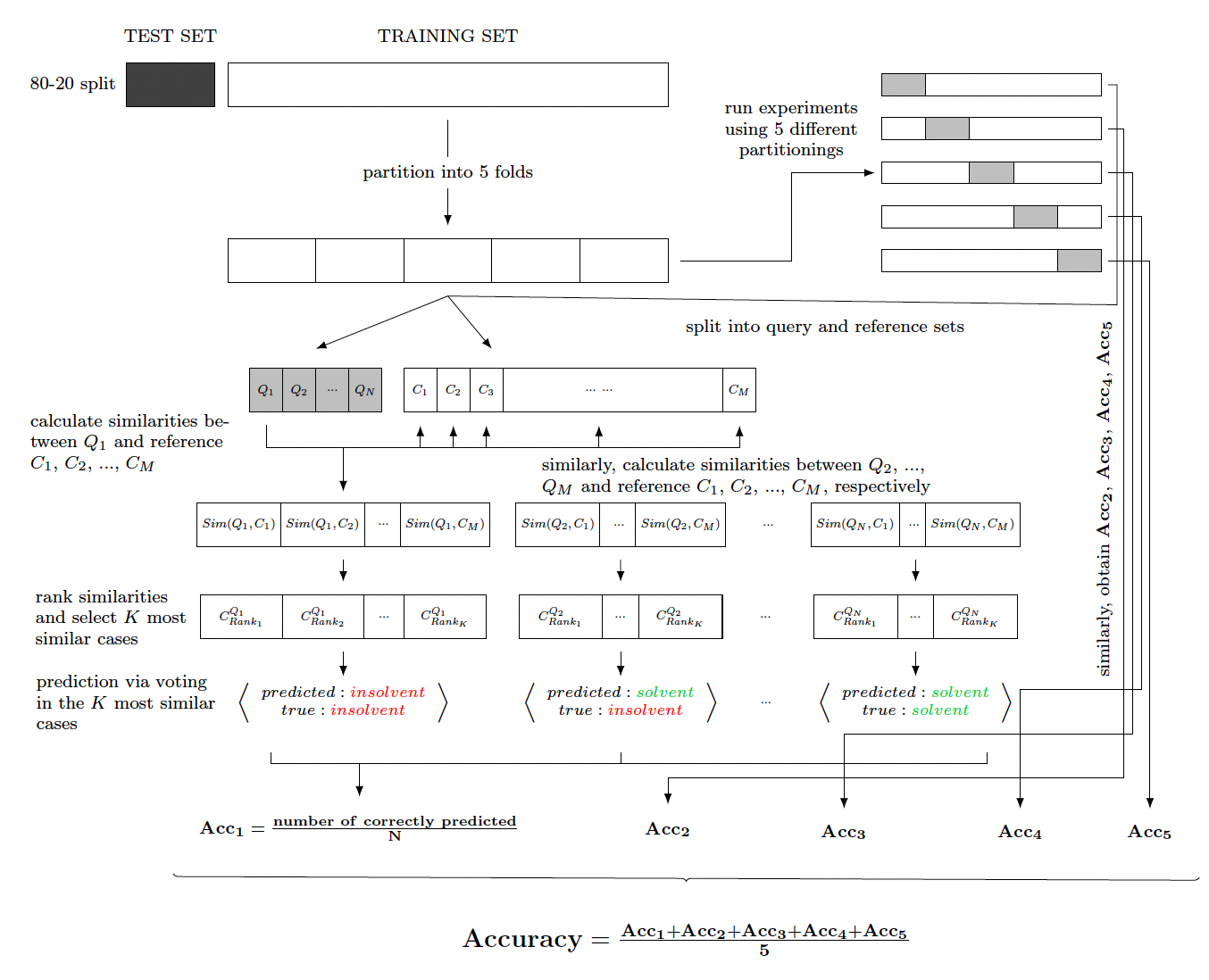

To obtain the , feature importance scoring methods are employed. Feature importance scoring is a task that calculates the relevance between the descriptive features and the target feature, which is commonly used in ML model design 77. In this study, six scoring methods are applied to generate six sets of global weights , which are Gini 16, Information entropy 41, Mutual information 40, Chi2 19, ANOVA 48 and ReliefF 39. The description of the methods can be found in Appendix B. Consequently, we create six CBR systems based on the generated weights. For each created CBR, the optimal local parameters, and of polynomial functions, will be searched and evaluated to find the optimal CBR system structure. However, the loss function is non-differentiable, which is an average accuracy calculated via 5-fold cross-validation. The illustration of the cost function can be seen in Figure 3.

Thus, particle swarm optimization (PSO) is applied for searching the optimal local parameters since the algorithm does not require that the optimization problem be differentiable as is required by classic optimization methods such as gradient descent used in training neural networks. PSO is a commonly used evolutionary algorithm. PSO is superior to other popular algorithms, such as genetic algorithms, in terms of efficiency and iteration while determining the optimal solution 74. Its popularity has increased because to its several advantages, which include resilience, efficiency, and simplicity. The other challenge is that the training process requires enormous calculations. Thus, parallel computing with GPU has been used to speed up the computation since the similarity calculation of cases is independent of each other and can be proceeded simultaneously. As we can see in Figure 3, the calculation of [, , …, ] can be conducted parallelly. The parallel computing for the similarity calculation is explained in Appendix C. The explanation of PSO can be found in Appendix D.

Finally, after evaluating the performance of the six designed ACBR systems through cross-validation, the best-validated one will be selected and used for bankruptcy prediction. The designing process of the proposed ACBR can be described as follows:

3.3 Probability of forecasting

A model is necessary to provide the likelihood of an event’s occurrence, not merely its anticipated categorization. It is crucial to convey the posterior probability in order to boost user trust in the CBR system’s answer 47. In particular, bankruptcy prediction is a binary classification problem with classes ( (solvent) or (insolvent)). Assume a dataset includes labeled cases , , and for a query case , is the number in the most similar cases belong to the class insolvent (), the estimate of the insolvent probability is given by:

| (7) |

However, it defies common sense to assume that each instance in the most comparable situations is given the same weight. The probability computation should favour the more similar scenario over the less similar case. Therefore, it is preferable to generalize this estimator by giving various probabilities to various related cases. Let the probabilities assigned to the most similar cases be , …, and the label if the th case belongs to the class and otherwise. These probabilities are greater than or equal zero, monotonically decreasing, and sum to 1: (constraints). Then the probability estimate of the insolvent is given:

| (8) |

The probabilities , …, are determined by maximizing the likelihood of the dataset . It is worth to note that the probabilities rather than probabilities are used. The is a regularization term to prevent obtaining log likelihood by assigning . Further, to reduce the constraints when optimizing log likelihood function to obtain the probabilities, a softmax representation is used:

| (9) |

where the parameters can be any value and constrained to be monotonically decreasing. Then, the estimate function of the insolvent probability becomes:

| (10) |

Let denote the class membership of . The likelihood of the cases dataset is:

| (11) |

where the different probability estimates are assumed to be independent as the dependent case is complicated to analyze. Finally, the log likelihood is given:

| (12) |

subject to the constraint:

The weighting parameters are determined by maximizing the log likelihood function.

3.3.1 Learning from prediction probability

The prediction probability provided by the CBR system, a number between zero and one, can be considered as an ex-ante bankruptcy risk signal, for instance, the creditworthiness of a company. In particular, the annual financial statement of companies can be used to calculate the scores of solvency in subsequent fiscal years, which can support some decision-making processes.

In addition, some insolvent companies are successfully merged by other companies as a form of an exit strategy, and some others invite new investors or sell liquid assets to get through financial distress, but others failed 58. It is important to consider the reorganization strategy before adopting a decision on a distressed firm’s options 15. To assist the investment and financing decisions, the prediction confidence in CBR can be used as an ex-post metric to examine a firm’s choice. In particular, the determination can be evaluated in terms of increasing the score of solvency. For instance, the efficiency of a capital injection can be measured based on the improvement of solvency confidence. Further, Shapley values are employed to show the contributions of financial variables to the improvement.

3.4 Shapley-CBR

Shapley-CBR is used to evaluate the feature importance for influencing the prediction probability of the CBR system. Shapley values are originally introduced as a pay-off concept from cooperative game theory 50. When referring to ML models, the notion of pay-off corresponds to the feature importance for predictive models in the presence of multicollinearity. This technique is necessary to retrieve the model using all feature subsets , where is the set of all features. Each feature is given a significance value, which indicates how that feature’s inclusion will affect the model’s prediction. A model and a model trained with that feature present and withheld, respectively, are used to calculate the effect. Then, given the current input , the pay-offs are computed as

| (13) |

The effects of excluding a feature depend on other features in the model, therefore the aforementioned differences are calculated for all potential subsets . After that, the Shapley values are calculated and applied as feature attributions. For a feature , the Shapley value can be presented as a weighted average of all possible differences:

| (14) |

As we are dealing with a binary response variable representing the active and default state of the companies, the term and can be rewritten as the predicted probabilities of the default and , when using the CBR model that includes the explanatory variable versus when using the CBR model that does not include the explanatory variable . Thus, Equation (13) becomes

| (15) |

It is worth noting that Shapley-CBR presents as an agnostic explainable AI concept that can be applied to the prediction probability irrespective of the model and data that generated it.

4 Experiment

In this section, we describe the experimental study’s principles and procedures. This section comprises five subsections. First, it is commonplace to observe missing values in financial data. To address the issue, we explain the basic concept of the CBR system regarding missing value. Next, data processing for model training is presented. It is then followed by a description of the performance measures used. Then, a list of benchmark models follows. Finally, we demonstrate the experimental design procedure.

4.1 Prediction with missing value

Missing values are always a pain in the neck. To control this obstacle in practice, some classification methods choose to remove all variables and observations which contain missings. This listwise deletion may lead to information loss, and new observations with missings are not predictable. Other methods solve the problem by using imputation. However, the process of replacing missing data with substituted values may introduce bias or affect the representativeness of the results. In our empirical study of evaluating models’ prediction performance, listwise deletion for missing data is implemented.

CBR is a robust and comparatively easy to handle technique, providing good performance with missing data 51. A value can be assigned as a feature similarity of two cases. For instance, for any local feature similarity calculation, if there are missings ( is missing, is missing or both and are missing), the is simply assigned to a value, such as 0.1. This characteristic enables the constructed CBR based on the existing dataset to easily adapt to any new coming cases. In our study, when there are missings, we assign the to 0.

4.2 Data processing

The application of re-sampling strategies to obtain a more balanced data distribution is an effective solution to the imbalance problem 13. The random under-sampling method is applied when training models in this study. This method involves randomly selecting cases from the majority class and removing them from the training dataset until a balanced distribution of classes is reached.

4.3 Performance measure

The evaluation of learned models is utmost important. Accuracy is the most frequently used gauge for bankruptcy model evaluation, which is the percentage of correctly classified individuals. Further, the misclassification cost aims to measure to what extent financial sectors can tolerate the misclassification results. The cost is the result of two types of errors: type I errors, in which a successful business is incorrectly labeled as failing, and type II errors, in which a failed company is misclassified as healthy. The false positive (FPR) and false negative rates (FNR) measure the probability of type I and II errors, respectively. The complementary metrics of FPR and FNR are true positive (TNR = 1 - FPR, sensitivity) and true negative rates (TPR = 1 - FNR, specificity), respectively. Compared with accuracy, the F-measure is a more helpful indicator for determining how well a prediction model performs for its users 13. When both FPR and FNR are low, the value of the F-measure is high. G-means computes the geometric mean of the accuracy of the two classes, the value of which is maximal when the balance of accuracy of FPR and FNR is achieved. In addition, AUC is a popular alternative measure of overall discriminatory power for prediction models 12. This metric has been widely used for evaluating bankruptcy prediction models 70, 69, 57. It is a more flexible performance measure because it provides a synthetic estimation of model accuracy that is totally independent of the proportion of classes and from any misclassification cost matrix 36. Besides, considering that the solvent and insolvent companies are of very different sizes, a balanced measure, Matthews correlation coefficient (MCC), is applied to evaluate the performance of the classifiers. The description of all the listed metrics can be found in Appendix E.

4.4 Benchmark models

In order to evaluate the efficiency and fidelity of the ACBR system, the experimental research employs three sets of benchmark models. First, the ECBR, MCBR, GCBR, EWCBR (Equally-weighted CBR), and EPCBR (Equally-polynomial CBR) are used as benchmarks to examine the efficiency of the asymmetrical local similarity function. In addition to comparing ACBR with the three distance-based CBR mentioned in Section 3, we also involve two asymmetrical CBR models, i.e., EWCBR and EPCBR, in this experiment. In particular, EWCBR treats the features with globally equal importance ( = 1/) and locally linear related ( = 1 and = 1) when constructing the CBR system. EPCBR adopts the optimally learned weights using the feature importance scoring methods while taking into account the local parameters equally ( = 1 and = 1). Second, eight well-known ML classifiers are used as benchmark models to assess the accuracy of ACBR system, namely logistic regression (LR), -nearest neighbor (-NN), decision tree (DT), support vector machine (SVM), Gaussian Naive Bayes (GNB), and multilayer perceptrons (MLP), Random Forest (RF) and XGBoost (XGB). The introduction of the benchmark models can be found in Appendix F. Third, we also investigate the efficiency of the different training metrics, i.e., Accuracy, AUC, F-measure, G-means and MCC.

4.5 Experimental design

As illustrated in Figure 3, the dataset is portioned into a train and test set, with an 80-20 split. The split is made by preserving the percentage of samples for each class. Then, the 5-fold cross-validated grid-search is used to optimize the models. Last, the out-of-sample performances are evaluated in terms of multiple measure metrics with the test dataset.

5 Results

This section shows the results of the out-of-sample prediction in the experiment to evaluate the efficiency and fidelity of the proposed CBR system. Specifically, we examine the effectiveness of the asymmetrical similarity function in comparison to others. Then, we compare the out-of-sample performance of the proposed CBR system to that of the most popular ML models. Finally, the accuracy of the proposed CBR system using several training metrics is investigated.

5.1 Out-of-sample performance comparison based on different local similarity functions

The classification results of the ACBR and the other five CBR benchmarks have been evaluated by the five measure metrics aforementioned, as shown in Table 2. From Table 2, we can observe that the ACBR performs overwhelmingly better than the other CBR systems. Particularly, the naïve benchmark EWCBR did not outperform the distance-based CBR as anticipated. In addition, we discover that EPCBR marginally improved its predictive performance by utilizing the learnt weights, but that the information provided by the global features is insufficient to improve the CBR system’s predictability considerably. In the meanwhile, the exceptional performance of the ACBR system demonstrates the efficacy of the asymmetrical similarity function, which can capture the prevalent asymmetrical characteristics in financial data characteristics.

| Accuracy | AUC | F-measure | G-means | MCC | |

|---|---|---|---|---|---|

| ECBR | 0.6675 | 0.7250 | 0.7483 | 0.7219 | 0.2389 |

| MCBR | 0.6823 | 0.7126 | 0.7595 | 0.7118 | 0.2286 |

| GCBR | 0.6203 | 0.6848 | 0.7115 | 0.6807 | 0.1926 |

| EWCBR | 0.6672 | 0.7101 | 0.7481 | 0.7083 | 0.2236 |

| EPCBR | 0.6826 | 0.7128 | 0.7597 | 0.7119 | 0.2288 |

| ACBR | 0.7528 | 0.7358 | 0.8106 | 0.7355 | 0.2704 |

-

•

Notes. The best values of each column are depicted in bold.

5.2 Out-of-sample performance of different ML models

The out-of-sample prediction results of the ACBR and eight benchmarks are shown in Table 3. From Table 3, we can observe that no classifier has the best performance across all measures. The finding is consistent with the results of research that conducted a similar experiment to evaluate ML models using a variety of metric measurements 59. In addition, the linear-based models exhibit impoverished prediction performance. The result is aligned with observations for insolvent/solvent classes in Figure 1, which are intuitively difficult to be distinguished by linear methods. The XGB performs the best among all models, followed by the ACBR, RF, and MLP, which all perform much better than the other models based on a number of measurement measures. Nonetheless, the MLP, XGB and RF did not indiscriminate their performance from the proposed CBR, indicating that the explainable model is capable of delivering a high degree of accuracy.

| Accuracy | AUC | F-measure | G-means | MCC | |

|---|---|---|---|---|---|

| LR | 0.4763 | 0.6885 | 0.5812 | 0.6426 | 0.1967 |

| -NN | 0.6436 | 0.7066 | 0.7298 | 0.7028 | 0.2170 |

| SVM | 0.4900 | 0.6724 | 0.5284 | 0.6097 | 0.2813 |

| DT | 0.6743 | 0.7028 | 0.7535 | 0.7020 | 0.2172 |

| GNB | 0.2202 | 0.5673 | 0.2703 | 0.3977 | 0.0961 |

| MLP | 0.7786 | 0.7109 | 0.8276 | 0.7065 | 0.2537 |

| RF | 0.7357 | 0.7525 | 0.7988 | 0.7522 | 0.2823 |

| XGB | 0.7590 | 0.7595 | 0.8154 | 0.7595 | 0.2976 |

| ACBR | 0.7528 | 0.7358 | 0.8106 | 0.7355 | 0.2704 |

-

•

Notes. The best values of each column are depicted in bold.

5.3 Out-of-sample evaluation with different training metrics

Table 4 shows the out-of-sample prediction results of ACBR system training with different metrics. From the table, we can observe that the ACBR system that utilizes accuracy has the best performance across all criteria. As with other ML models, the empirical findings indicate that accuracy is a reliable evaluation metric for training CBR systems.

| Accuracy | AUC | F-measure | G-means | MCC | |

|---|---|---|---|---|---|

| Accuracy | 0.7528 | 0.7358 | 0.8106 | 0.7355 | 0.2704 |

| AUC | 0.7121 | 0.7121 | 0.7814 | 0.7121 | 0.2340 |

| F-measure | 0.7025 | 0.7106 | 0.7744 | 0.7106 | 0.2303 |

| G-means | 0.7360 | 0.7231 | 0.7986 | 0.7229 | 0.2517 |

| MCC | 0.7331 | 0.7307 | 0.7967 | 0.7308 | 0.2589 |

-

•

Notes. The best values of each column are depicted in bold.

6 Explainability and decision support

One of the important characteristics of the CBR method is the interpretability of the prediction results. In this section, we conduct case studies to underline the insights provided by CBR.

6.1 Explainability in CBR

According to Barredo Arrieta et al. 6, the level of explainability of ML models can be evaluated by algorithmic transparency, decomposability and simulatability. Algorithmic transparency is related to the ability of users to understand the process followed by the model to produce any given output from its input data. Decomposability is the ability to interpret individual parts of a model. Simulatability indicates the ability of an ML model to be simulated or thought about strictly by a human.

The CBR level of explainability is summarized as follows:

-

•

Algorithmic transparency: It is obvious that analogous problems/cases serve as explanations for human users in the CBR decision-making process 66. However, the similarity measure cannot be fully observed. Thus, some mathematical and statistical analysis will be used for the analysis of the model.

-

•

Decomposability: The model comprises two functions, i.e., global similarity function and local similarity function. The similarity measure and the set of variables can be decomposed and analyzed separately. However, the number of variables may be too high and/or the similarity measure is too complex. It is not intuitively to understand the model. Thus, visualization will be helpful for user complete comprehension.

-

•

Simulatability: the complexity of the reasoning process matches human’s native capabilities for simulation and solving new problems. The process is understandable by a human.

In this part, we explain and investigate how to employ the CBR system to conduct the analysis of the prediction results and interpret the economic meanings of global and local parameters.

6.1.1 Results explanation based on similar cases

Applying CBR, similar cases can not only be used for prediction but for analogous analysis to detect the reasons for bankruptcy. Assume that there is a query company that has been correctly classified as being insolvent by applying the CBR system based on voting from the nine most similar companies (six are insolvent, and three are solvent). To analyze the potential reasons for bankruptcy, the three most similar companies of the company , (insolvent), (insolvent), and (solvent) can be retrieved, and some of their attributes are shown in Table 5. From the table, we can see that company obviously has higher sales than the other three companies. Especially, compared with and , it is not difficult to find that the company adopts a small profits but quick returns operation strategy. Moreover, the profit margin ratios () of , , and are 2.11%, 0.87%, 0.88%, 5.41%, respectively. Compared with two insolvent companies and , the profit margin ratio of the company has no obvious increase. The ratio of is less than that of . In addition, has a similar amount of accounts receivable with , while the accounts payable of is much higher than that of . Thus, the fallacious operation strategy would be one of the reasons which led to the bankruptcy of the company .

| Feature | ||||

|---|---|---|---|---|

| Accounts payable | 326,715.51 | 243,374.93 | 369,152.73 | 41,158.13 |

| Accounts receivable | 215,765.17 | 205,028.04 | 120,153.59 | 208,692.67 |

| … | … | … | … | … |

| Sales | 4,223,270.93 | 1,614,148.46 | 1,801,792.58 | 1,683,185.35 |

| … | … | … | … | … |

| Net income | 89,476.07 | 14,316.17 | 15,850.04 | 91,298.81 |

6.1.2 Results explanation based on prediction probability

According to the prediction probability calculation function introduced in the section 3.3, we can obtain the probability weights of the nine ( in the best-validated CBR) most similar companies , , , , , , , and , respectively. The prediction probability of can be calculated by summing the probability weights of , , , , and . Thus, there is a 65.26% confidence that will be an insolvent company.

6.1.3 Results explanation based on feature relevance

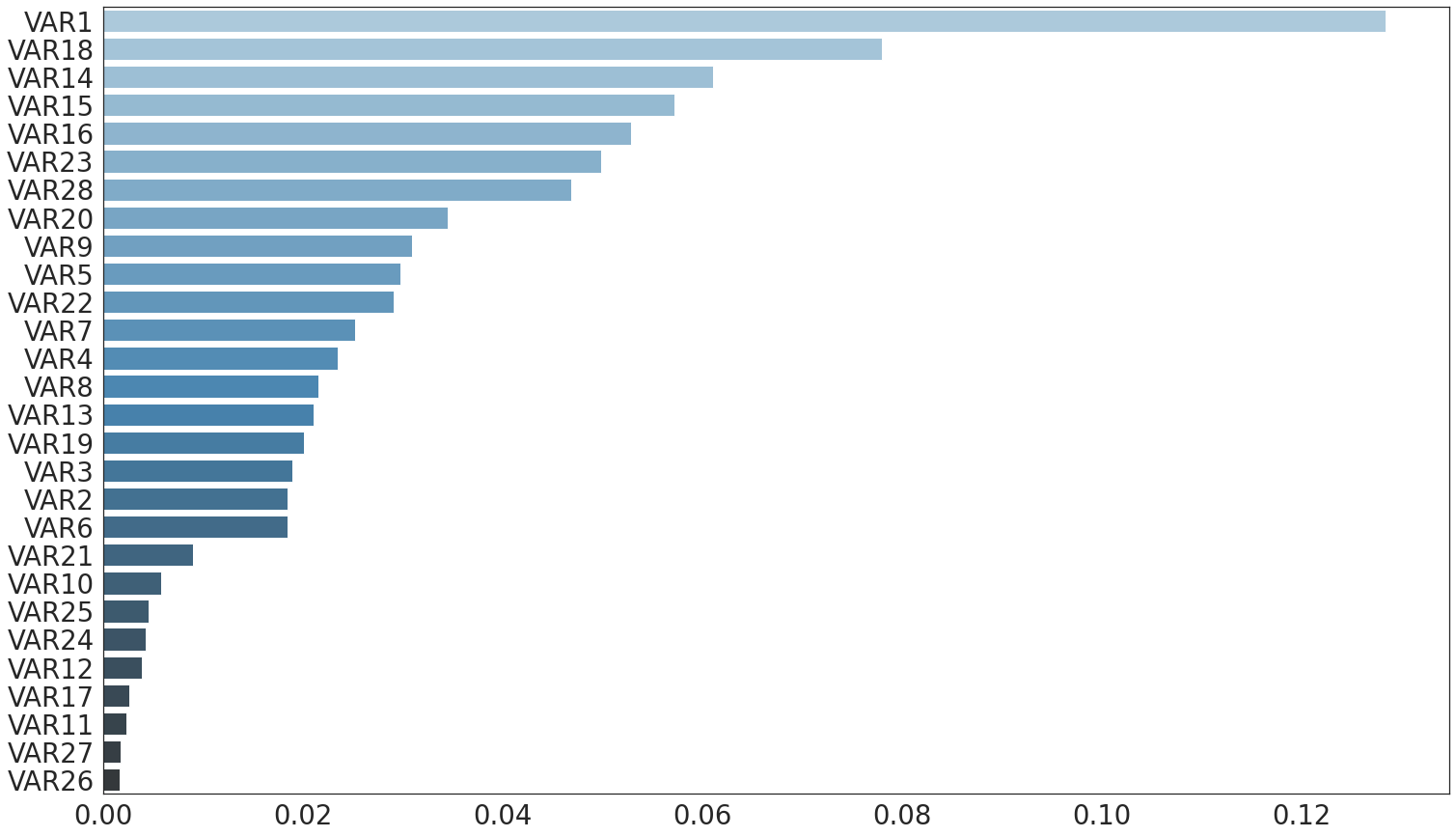

The weights of the attribute in the CBR global similarity function are important for analyzing the bankruptcy prediction. The weights have been scaled to the relevance scores, the sum of which is equal to 100%, as shown in Table 6. From the table, we can observe that accounts payable is the most important feature, which is money owed by a company to its suppliers shown as a liability on a company’s balance sheet. It is reasonable because accounts payable are debts that must be paid off within a given period to avoid default, directly causing insolvency. Besides, we can find that administrative expenses are not important for bankruptcy prediction. It is because the expense commonly incurs that are not directly tied to core functions such as production and sales.

| Feature | Relevance (%) | Feature | Relevance (%) |

|---|---|---|---|

| Accounts payable (A.P.) | 6.12 | Interest expenses | 3.80 |

| Sales | 5.32 | Bank debt | 3.79 |

| Equity | 5.07 | Tangible assets | 3.65 |

| Number of employees | 5.06 | Total long-term liabilities | 3.27 |

| Total current liabilities | 4.96 | A.R. against affiliated companies | 3.11 |

| Operating income | 4.55 | Increase inventories | 3.11 |

| Accounts receivable (A.R.) | 4.52 | Increase cash | 2.88 |

| Inventories | 4.28 | Increase liabilities | 2.78 |

| EBIT | 4.26 | Intangible assets | 2.61 |

| Cash | 4.12 | Shareholder loan | 2.59 |

| Net income | 3.94 | Accrual for pension liabilities | 2.45 |

| Amortization depreciation | 3.91 | A.P. against affiliated companies | 1.20 |

| Total assets | 3.82 | Lands | 0.79 |

| Current assets | 3.81 | Administrative expenses | 0.24 |

-

•

Notes. the tables presents the relevance of each feature. The sum of all the value is equal to 100.

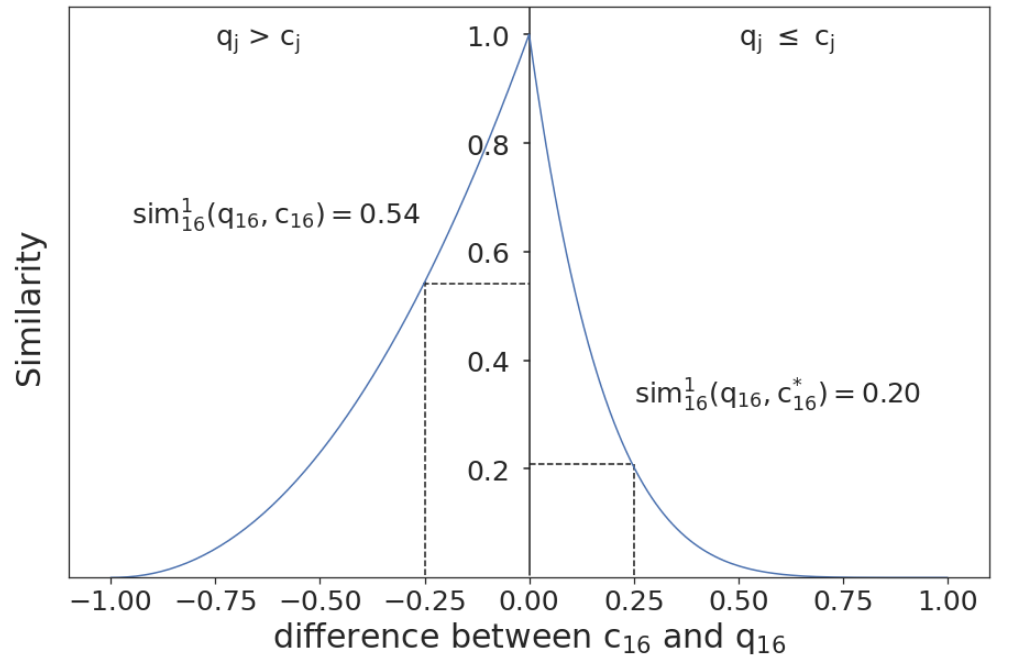

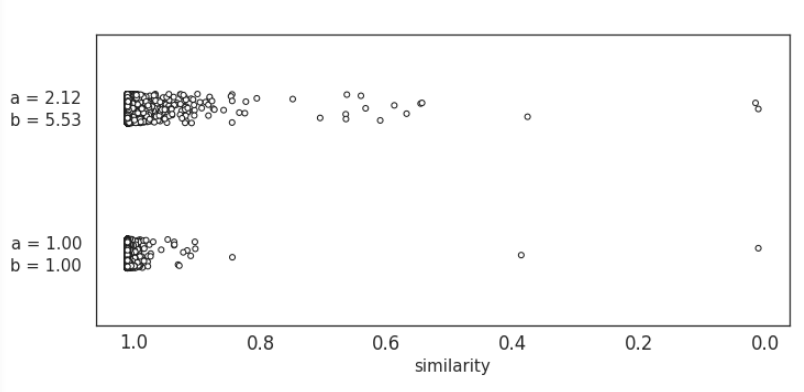

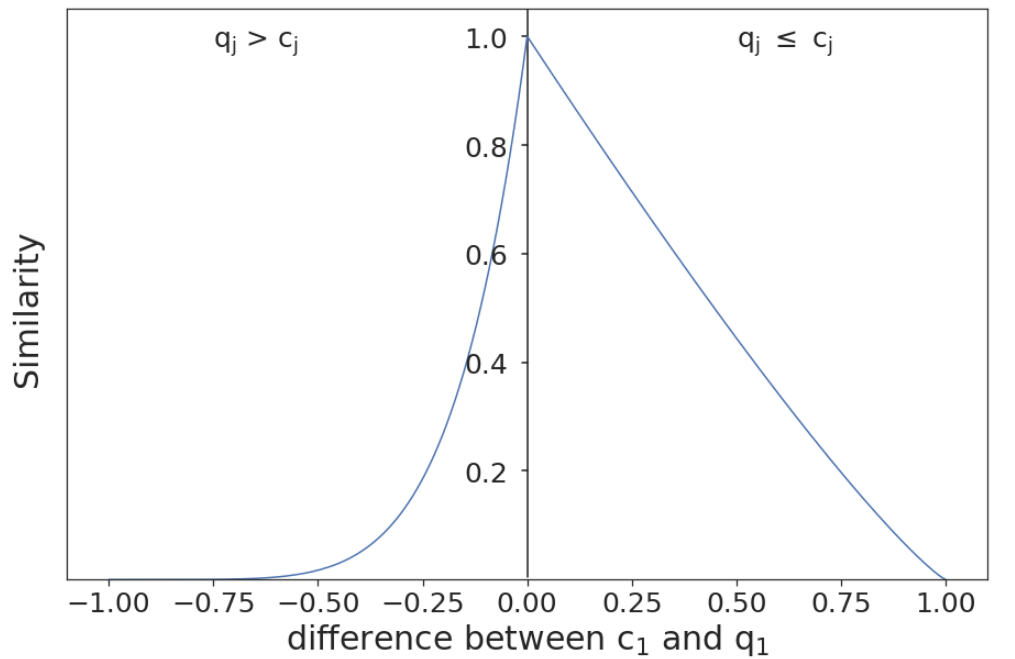

In addition, the polynomial characteristics of local functions grant flexibility to pursue more accurate classification. For example, when calculating the variable similarities between a company and a from companies dataset , assume that the difference between the VAR16 (Sales) from the and from the is 0.25, the similarity between the and can be calculated according to Equation (6). The illustration of the local similarity functions of the VAR16 is shown in Figure 4, in terms of , (parameters used in EWCBR) and , (ACBR), respectively. When and , the local similarity is equal to . Meanwhile, when and , the is equal to . This means that the polynomial function transforms the similarity value between and . Further, the calculated similarities between a and the from all the companies dataset using the local similarity equations with the two different sets of and can be seen in Figure 5. The value of the is the median value of all the . From the figure, we can clearly see the relative similarities distance are amplified, which makes companies more distinguishable from one another in terms of the VAR16. Moreover, in Figure 4(b), it can be seen that the value of is less than , which means, if the sales absolute difference between a company with smaller sales and a query company is same with the difference between a company with larger sales and the query (e.g. , as shown in Figure 4(b)), the former is more similar with the query company than the later (). One reason behind this fact is that a takeoff in sales is difficult to achieve by improving productivity and sales capability, while a decline in sales can occur on the basis of many causes, even a firm operation has not been reorganized 28. Thus, it is reasonable to consider a company with smaller sales to be more similar to a query than the one with larger.

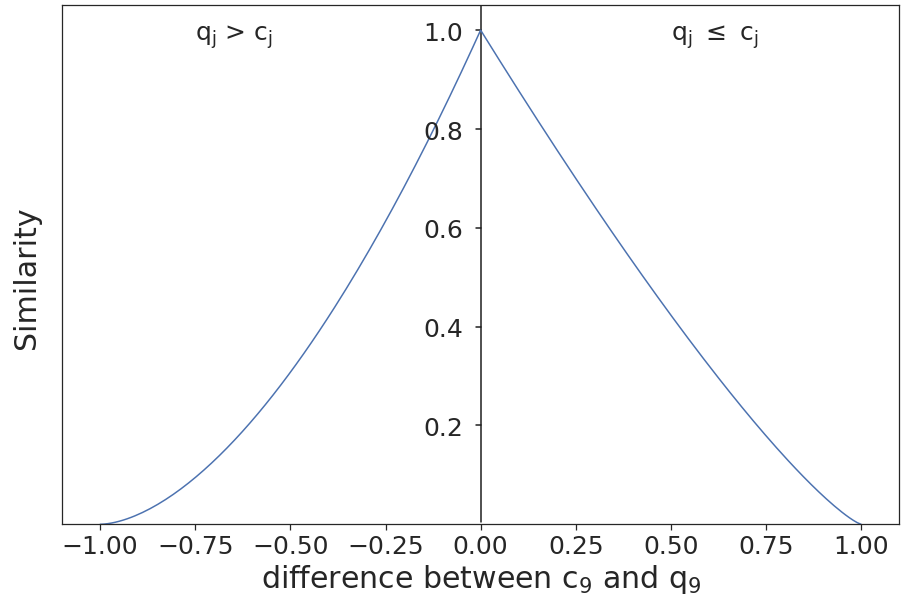

Obviously, the varying parameters of the different variables account for their distinct economic significance. For instance, the illustration of the local similarity functions of the VAR1 (Cash) in Figure 6 shows the distinguishing between cash and sales in the similarity calculation. The parameters and of local similarity are 5.86 and 1.17, respectively. This means that a query company is more likely to be similar to a company holding larger cash. It is reasonable because there is little evidence that excess cash has a substantial short-term effect on capital expenditures, acquisition spending, or dividend payments 60. Meanwhile, operating losses are the leading cause of cash flow constraints in businesses. Consistent with the literature, our findings indicate that the data-driven CBR system can effectively depict the similarity of companies attributed to revealing the nonlinear and asymmetric properties in economic data. It is interesting to find that the relatively stable properties of a company, such as Current assets ( and ), Tangible assets ( and ) and Equity ( and ), did not show an obvious asymmetric local similarity structure. The illustration of the local similarity functions of the VAR9 (Equity) is in Figure 7. In contrast, intangible assets, which are not physical in nature and stable, such as goodwill, brand recognition, patents, trademarks, and copyrights, present an obvious asymmetric local similarity property ( and ). The findings indicate that elastic features, such as Cash, show an asymmetric similarity structure while static features, such as Equity, show a relatively symmetric similarity structure.

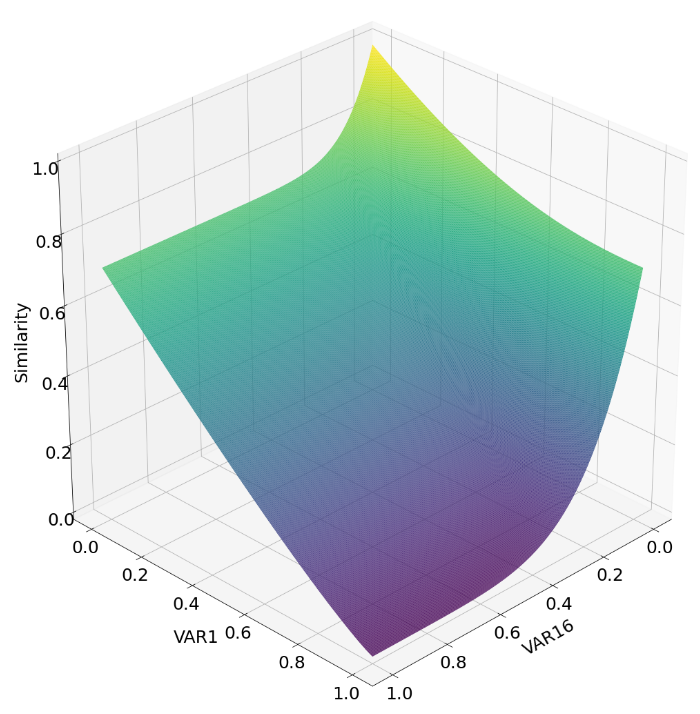

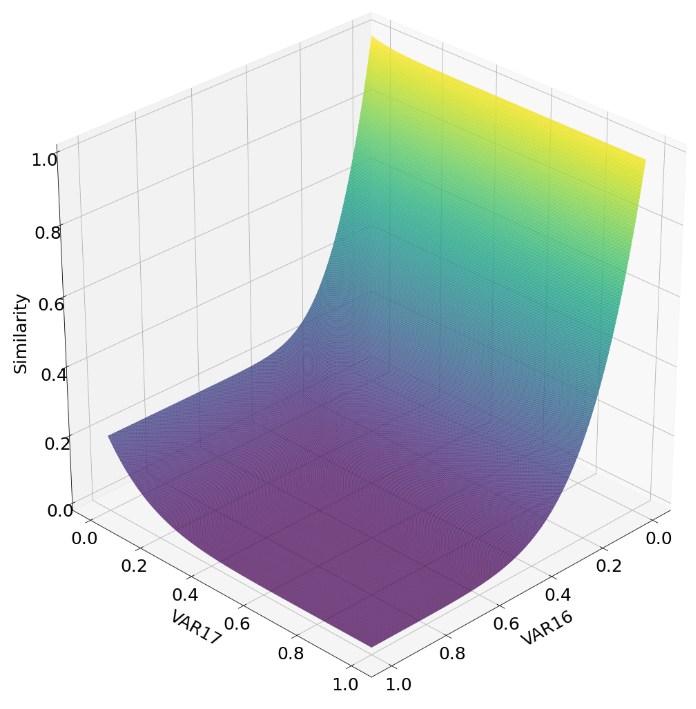

Further, we investigate the associative effect of features. According to the feature importance in Table 6, we assume the weights of Cash (VAR1) and Sales (VAR16) are 0.44 and 0.55, respectively. When comparing a query with a reference company with larger cash and sales ( and ), the similarity function can be illustrated in Figure 8. From the figure, we can observe the asymmetric similarity distribution. In particular, if the query and reference have a similar magnitude of sales (), the similarity between them decreases smoothly as the disparity in cash resources increases. Meanwhile, when the query and reference companies do not have comparable sales (), this will lead to more differentiation between firms in the decreasing of the disparity in cash resources. In addition, the weights of features, obviously, have a significant impact on their contribution to the computation of similarity. As shown in Figure 9, Administrative expenses (VAR17) have a limited influence on weighing up similarity in comparison to Sales. The rest parameters and of all the variables are shown in Appendix G.

6.2 Decision support for bankruptcy

In this section, we explore the application of CBR prediction probability to provide decision support regarding bankruptcy by conducting the case study of the prediction and analysis for an insolvent German company, i.e., Gerry Weber International AG. In particular, we first explain the results of Shapley-CBR. Then, through the case study of Gerry Weber, we show the application of CBR prediction probability as a bankruptcy risk indicator and elaborate on the decision support based on CBR system for the insolvent company.

6.2.1 Shapley-CBR

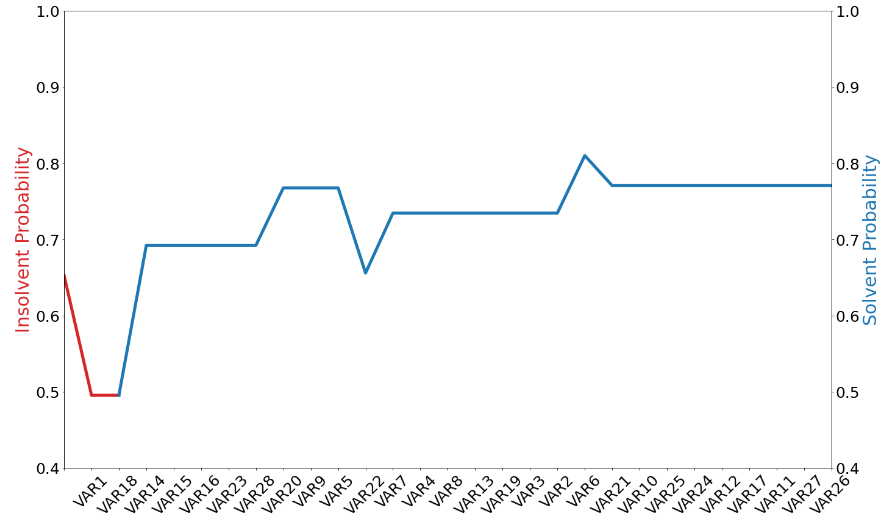

As aforementioned, the Shapley value can be used to explain the contributions of variables to the improvement of solvent confidence. The average absolute impact of Shapley value on the confidence is shown in Figure 10. From the figure, the results indicate that VAR1 (Cash) has the most decisive influence. It is reasonable because cash on hand is the most liquid type of asset. The most direct way to solve insolvency via investment is cash injection. An interesting point to note from the results is the importance of the variable VAR18 (Amortization and Depreciation) ranks second. Amortisation is the process by which debt is paid off with a fixed repayment schedule in regular installments over a certain time period. The insolvent company can negotiate with its creditors and modify the amortization profile of their benefits. For instance, the loan repayments being recalculated on a longer amortization profile can help the company resolve insolvency; meanwhile, it will give creditors get a better chance of recovering their debts compared with the situation the company goes into liquidation. Establishing effective reorganization proceedings with creditors is significantly helpful for the company to get through the financial distress. Moreover, the third and fourth important variables are VAR14 (Bank debt) and VAR15 (Account payable). Similar to amortization, negotiation with banks and vendors or suppliers to delay or restructure the debts or goods payments is an efficient way to increase the probability of discontinuing insolvency proceedings. By contrast, from Figure 10, we can find that administrative expenses (VAR12), accrual for pension liabilities (VAR17), A.P. against affiliated companies (VAR27), A.R. against affiliated companies (VAR26) are not important, which is consistent with our intuition.

6.2.2 Case study with Gerry Weber

Gerry Weber is a German fashion manufacturer and retailer based in Halle, established in 1973. In recent years, the fashion empire suffered from the decline in customer footfall in the city centers and the triumph of online trading. The self-administered insolvency proceedings opened in 2019. To get through the financial distress, several efforts have been adapted: 1) More than a hundred branches were closed, and numerous jobs were cut; 2) The existing shareholders were forced out of the company without compensation; 3) The financial investors are invited, which provide up to 49 million euros to satisfy its creditors and to finance operations. The insolvency proceedings claim was withdrawn in 2020. From Table 6.2.2, we can see that, in 2019, Gerry Weber filed for insolvency as predicted, based on the financial status in the fiscal year 2018. In the following year, after experiencing active self-remedy, the firm was solvent as predicted, and the confidence score recovered to 76%.

| Year | Prediction | Confidence | Description |

|---|---|---|---|

| 2017 | Solvent | 74% | Gerry Weber filed for insolvency in January 2019. Approximately 120 shops in Germany and in addition about 180 sales points in Europe were closed in April 2019. The insolvency proceedings were discontinued in January 2020. |

| 2018 | Solvent | 74% | |

| 2019 | Insolvent | 65% | |

| 2020 | Solvent | 76% | |

| 2021 | Solvent | 62% |

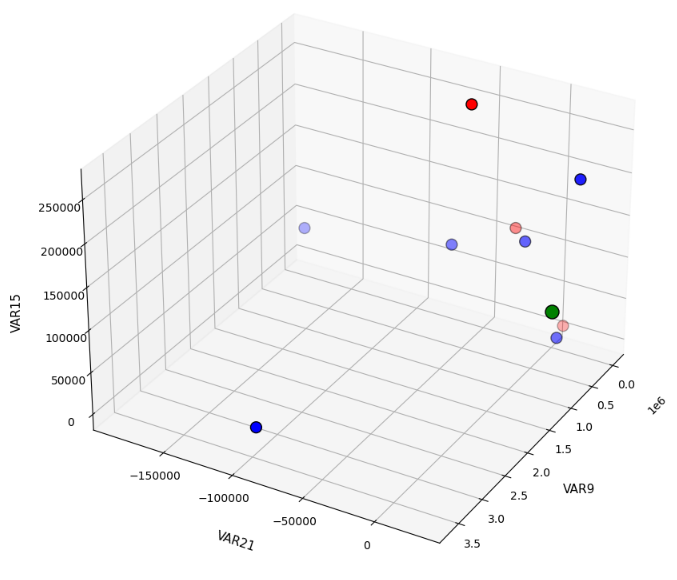

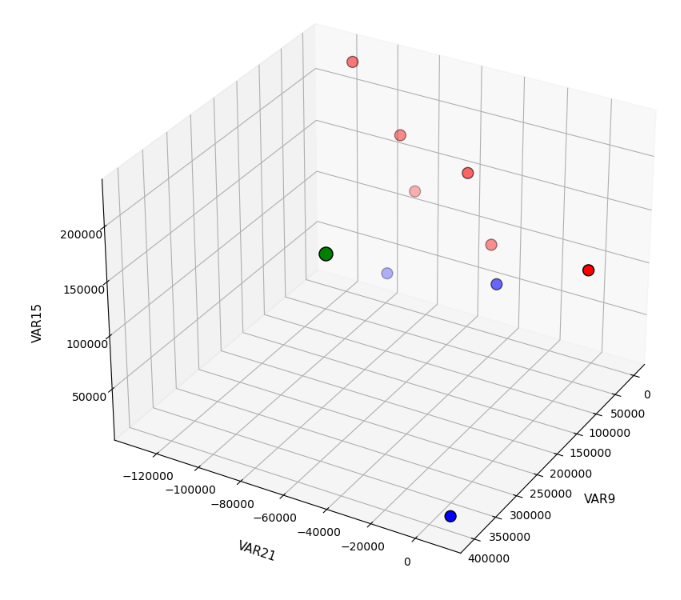

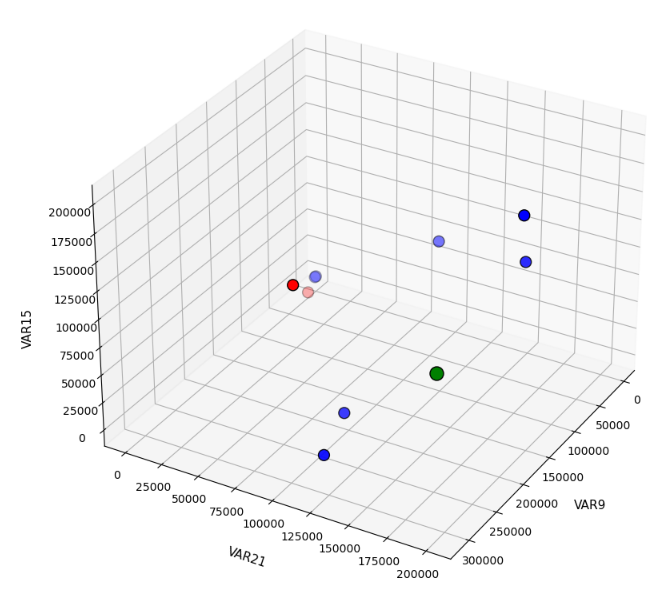

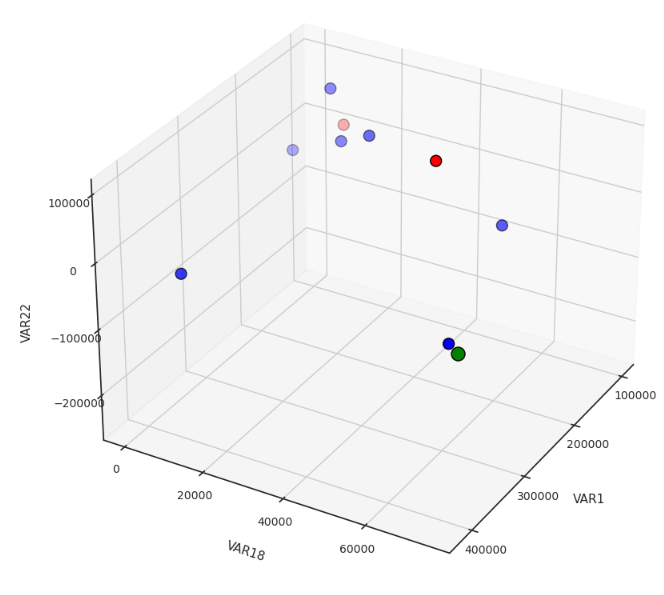

According to the financial variables from 2017 to 2019, which can be found in Appendix H, it is not surprising to find that Equity (VAR9) and Operation income (VAR21) experienced the most significant changes since it is intuitive to increase income and assets while decreasing the liabilities to solve insolvency. Figure 11 shows the alteration of its most similar reference companies in terms of the two variables against the other important feature, Accounts payable (VAR15). The green dot stands for Gerry Weber, while the blue and red dots stand for solvent and insolvent companies, respectively. From Figure 11(a), we can observe that the majority of the most similar companies have negative operation income in comparison to Gerry Weber. This indicates that the operating income of Gerry Weber tends to be negative. In the fiscal year 2018, as aforementioned, Gerry Weber was predicted to be insolvent in the following year. From Figure 11(b), we can observe that the operating income of Gerry Weber became negative and was the worst among its most similar referencing firms. It is interesting to find that all insolvent companies have larger accounts payable than Gerry Weber, and solvent similar companies have an identical level of account payable, which indicates that the accounts payable is not the main reason behind the insolvency of Gerry Weber. From Figure 11(c), we can find that Gerry Weber was dedicated to increasing VAR21 and VAR9, contributing to the discontinuance of the insolvency proceedings.

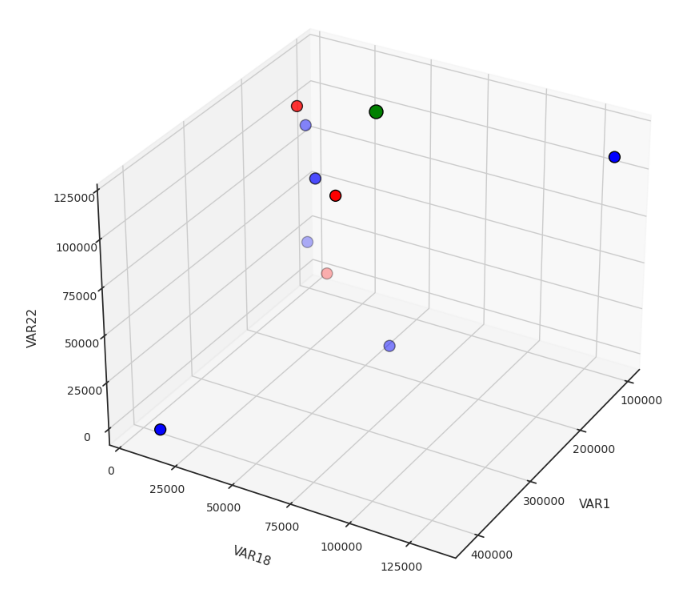

In addition, based on the analysis of the Shapley-CBR, we know the ranking of feature variables to increase the solvent prediction probability. However, from the three figures in Figure 11, we can observe that the company try to reduce the accounts payable, one of the most important features influencing prediction decision and prediction probability, but the changes are not significant. Thus, it is also important to investigate the efficiency of the applied solutions to solve the insolvency problem. In particular, we accumulatively replaced the feature variables of Gerry Weber in 2018 with the ones in 2019 following the feature ranking of the Shapley-CBR. From Figure 12, we can find that the change of VAR1 has reduced the insolvent probability. The accumulation of VAR1, VAR18 and VAR14 has reversed the insolvent situation, giving a 69% prediction probability for solvency. Subsequently, the rest of the changes are accumulating the solvency prediction confidence. It is interesting to find that the changes in VAR22 (Operating income) and VAR21 (Net income) decreased the solvency prediction confidence. In order to investigate the impact of the change of the VAR22, the data plot of Gerry Weber and its most similar reference companies in terms of the VAR22 against VAR1 and VAR18 is shown in Figure 13. From the figure, we can find that the increase in operating income makes Gerry Weber be more close to insolvent companies. The findings indicate that the increase in operating income and net income is not an efficient way to get rid of insolvency. The company in the financial dilemma should put more endeavour into changing the other financial status. For instance, we know that Operating Income = Gross Profit - Operating Expenses - Depreciation - Amortization. As we discussed, the reduction of depreciation and amortization or operating expenses, such as the deduction of staff wages or the layoff of employees, can effectively contribute to solvency. However, the extremely pursuing of such reduction targeting an increase in operating income does not benefit solving the insolvency problem.

7 Conclusion

This paper investigates a data-driven CBR system for bankruptcy evaluation. The traditional CBR highly depends on domain knowledge and prior experience, and the manually-design suffers from a low prediction accuracy. We apply an automatic procedure to design the retrieving in the CBR system. The parameters in the similarity calculation functions are automatically optimized, targeting the increase in prediction accuracy. The experimental results show that the CBR method performs competitively compared to the widely used classification ML methods. Moreover, the CBR approach distinguishes itself from other black-box ML methods by showing the interpretability of the prediction process and further providing useful information for bankruptcy-related decision-making. This characteristic is helpful for companies’ stakeholders, decision makers, and investors. In particular, we examine the level of the explainability of the CBR system in detail by analyzing the bankruptcy prediction process and conducting experiments to outline a unified view of explanation in the CBR system. The results show the scheme to explain the decision-making process based on the CBR system and explore more decisive information. Further, we extensively examine the efficiency of the local similarity functions in CBR system. The empirical results reveal the importance of asymmetrical polynomial local similarity function to increase the prediction accuracy in distance/similarity-based classification and exhibit the advantages how the asymmetrical polynomial parameters can better reflect practical economic meanings in the comparison of similar companies. The latter enhances the users’ conference and provides useful information to support stakeholders in making decisions. Our findings demonstrate a promising direction for future research by establishing a well-designed explainable model that can improve not only prediction accuracy but also increase explainability.

For future studies, several extensions of the current study can be developed. In the proposed approach, the design of global similarity is based on the existing feature scoring methods. In further research, we will explore a general way to detect the optimal feature weights. In addition, the maintenance of a CBR system is necessary, the costs of which may include the cost of adding new cases to strengthen the case base and refining existing cases 8. Maximization of the system effectiveness in supporting bankruptcy-related decisions will be worth investigating. Besides, the current study was carried out using the bankruptcy dataset, but the generality of the proposed CBR system ensures a possible application to other decision-support systems.

References

- Aamodt and Plaza (1994) Aamodt, A, Plaza, E (1994). Case-based reasoning: Foundational issues, methodological variations, and system approaches. AI Communications 7: 39–59. doi:10.3233/AIC-1994-7104. 1.

- Ahn and Kim (2009) Ahn, H, Kim, K (2009). Bankruptcy prediction modeling with hybrid case-based reasoning and genetic algorithms approach. Applied Soft Computing 9(2): 599–607. doi:10.1016/j.asoc.2008.08.002.

- Altman (1968) Altman, EI (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance 23(4): 589–609. URL: http://www.jstor.org/stable/2978933.

- Bach and Althoff (2012) Bach, K, Althoff, KD (2012). Developing case-based reasoning applications using mycbr 3, in: Agudo, BD, Watson, I (Eds.), Case-Based Reasoning Research and Development, Springer Berlin Heidelberg, Berlin, Heidelberg. 17–31.

- Balog et al. (2017) Balog, D, Bátyi, TL, Csóka, P, Pintér, M (2017). Properties and comparison of risk capital allocation methods. European Journal of Operational Research 259(2): 614–625. doi:https://doi.org/10.1016/j.ejor.2016.10.052.

- Barredo Arrieta et al. (2020) Barredo Arrieta, A, Díaz-Rodríguez, N, Del Ser, J, Bennetot, A, Tabik, S, Barbado, A, Garcia, S, Gil-Lopez, S, Molina, D, Benjamins, R, Chatila, R, Herrera, F (2020). Explainable artificial intelligence (xai): Concepts, taxonomies, opportunities and challenges toward responsible ai. Information Fusion 58: 82–115. doi:https://doi.org/10.1016/j.inffus.2019.12.012.

- Beddoe and Petrovic (2006) Beddoe, GR, Petrovic, S (2006). Selecting and weighting features using a genetic algorithm in a case-based reasoning approach to personnel rostering. European Journal of Operational Research 175(2): 649–671. doi:https://doi.org/10.1016/j.ejor.2004.12.028.

- Bensoussan et al. (2009) Bensoussan, A, Mookerjee, R, Mookerjee, V, Yue, WT (2009). Maintaining diagnostic knowledge-based systems: A control-theoretic approach. Management Science 55(2): 294–310. doi:10.1287/mnsc.1080.0908.

- Bentéjac et al. (2021) Bentéjac, C, Csörgő, A, Martínez-Muñoz, G (2021). A comparative analysis of gradient boosting algorithms. Artificial Intelligence Review 54(3): 1937–1967. doi:10.1007/s10462-020-09896-5.

- Bergantiños and Lorenzo-Freire (2008) Bergantiños, G, Lorenzo-Freire, S (2008). “optimistic” weighted shapley rules in minimum cost spanning tree problems. European Journal of Operational Research 185(1): 289–298.

- Bernanke (1981) Bernanke, BS (1981). Bankruptcy, liquidity, and recession. The American Economic Review 71(2): 155–159. URL: http://www.jstor.org/stable/1815710.

- Bradley (1997) Bradley, AP (1997). The use of the area under the roc curve in the evaluation of machine learning algorithms. Pattern Recognition 30(7): 1145–1159. doi:10.1016/S0031-3203(96)00142-2.

- Branco et al. (2016) Branco, P, Torgo, L, Ribeiro, RP (2016). A survey of predictive modeling on imbalanced domains. ACM Computing Surveys 49(2). doi:10.1145/2907070.

- Breiman (2001) Breiman, L (2001). Random forests. Machine Learning 45(1): 5–32. doi:10.1023/A:1010933404324.

- Cappelen et al. (2019) Cappelen, AW, Luttens, RI, Sørensen, EØ, Tungodden, B (2019). Fairness in bankruptcies: An experimental study. Management Science 65(6): 2832–2841. doi:10.1287/mnsc.2018.3029.

- Ceriani and Verme (2012) Ceriani, L, Verme, P (2012). The origins of the gini index: extracts from variabilità e mutabilità (1912) by corrado gini. The Journal of Economic Inequality 10(3): 421–443. doi:10.1007/s10888-011-9188-x.

- Chi et al. (1993) Chi, RT, Chen, M, Kiang, MY (1993). Generalized case-based reasoning system for portfolio management. Expert Systems with Applications 6(1): 67 – 76. doi:10.1016/0957-4174(93)90019-3. special Issue: Case-Based Reasoning and its Applications.

- Chuang (2013) Chuang, CL (2013). Application of hybrid case-based reasoning for enhanced performance in bankruptcy prediction. Information Sciences 236: 174–185. doi:10.1016/j.ins.2013.02.015.

- Cost and Salzberg (1993) Cost, S, Salzberg, S (1993). A weighted nearest neighbor algorithm for learning with symbolic features. Machine Learning 10(1): 57–78. doi:10.1023/A:1022664626993.

- Csóka et al. (2022) Csóka, P, Illés, F, Solymosi, T (2022). On the shapley value of liability games. European Journal of Operational Research 300(1): 378–386. doi:https://doi.org/10.1016/j.ejor.2021.10.012.

- Cui et al. (2006) Cui, G, Wong, ML, Lui, HK (2006). Machine learning for direct marketing response models: Bayesian networks with evolutionary programming. Management Science 52(4): 597–612. doi:10.1287/mnsc.1060.0514.

- Cunningham et al. (2003) Cunningham, P, Doyle, D, Loughrey, J (2003). An evaluation of the usefulness of case-based explanation, in: Ashley, KD, Bridge, DG (Eds.), Case-Based Reasoning Research and Development, Springer Berlin Heidelberg, Berlin, Heidelberg. 122–130.

- Dastile et al. (2020) Dastile, X, Celik, T, Potsane, M (2020). Statistical and machine learning models in credit scoring: A systematic literature survey. Applied Soft Computing 91: 106263. doi:https://doi.org/10.1016/j.asoc.2020.106263.

- Deng (1996) Deng, PS (1996). Using case-based reasoning approach to the support of ill-structured decisions. European Journal of Operational Research 93(3): 511–521. doi:https://doi.org/10.1016/0377-2217(95)00081-X.

- Ding et al. (2012) Ding, AA, Tian, S, Yu, Y, Guo, H (2012). A class of discrete transformation survival models with application to default probability prediction. Journal of the American Statistical Association 107(499): 990–1003. doi:10.1080/01621459.2012.682806.

- Dustmann et al. (2014) Dustmann, C, Fitzenberger, B, Schönberg, U, Spitz-Oener, A (2014). From sick man of europe to economic superstar: Germany’s resurgent economy. Journal of Economic Perspectives 28(1): 167–88. doi:10.1257/jep.28.1.167.

- Gardner and Dorling (1998) Gardner, M, Dorling, S (1998). Artificial neural networks (the multilayer perceptron)—a review of applications in the atmospheric sciences. Atmospheric Environment 32(14): 2627–2636. doi:10.1016/S1352-2310(97)00447-0.

- Golder and Tellis (2004) Golder, PN, Tellis, GJ (2004). Growing, growing, gone: Cascades, diffusion, and turning points in the product life cycle. Marketing Science 23(2): 207–218. doi:10.1287/mksc.1040.0057.

- Guessoum et al. (2014) Guessoum, S, Laskri, MT, Lieber, J (2014). Respidiag: A case-based reasoning system for the diagnosis of chronic obstructive pulmonary disease. Expert Systems with Applications 41(2): 267–273. doi:10.1016/j.eswa.2013.05.065.

- Härdle et al. (2011) Härdle, WK, Hoffmann, L, Moro, R (2011). Learning machines supporting bankruptcy prediction. Springer Berlin Heidelberg, Berlin, Heidelberg. 225–250. doi:10.1007/978-3-642-18062-0_7.

- Härdle et al. (2005) Härdle, WK, Moro, R, Schäfer, D (2005). Predicting Bankruptcy with Support Vector Machines. Springer Berlin Heidelberg, Berlin, Heidelberg. 225–248. doi:10.1007/3-540-27395-6_10.

- Hart (2017) Hart, S (2017). Shapley Value. Palgrave Macmillan UK, London. 1–5. doi:10.1057/978-1-349-95121-5_1369-2.

- Hosaka (2019) Hosaka, T (2019). Bankruptcy prediction using imaged financial ratios and convolutional neural networks. Expert Systems with Applications 117: 287–299. doi:10.1016/j.eswa.2018.09.039.

- Ince (2014) Ince, H (2014). Short term stock selection with case-based reasoning technique. Applied Soft Computing 22: 205–212. doi:10.1016/j.asoc.2014.05.017.

- Jabeur et al. (2021) Jabeur, SB, Mefteh-Wali, S, Viviani, JL (2021). Forecasting gold price with the xgboost algorithm and shap interaction values. Annals of Operations Research doi:10.1007/s10479-021-04187-w.

- Jardin (2021) Jardin, PD (2021). Forecasting corporate failure using ensemble of self-organizing neural networks. European Journal of Operational Research 288(3): 869–885. doi:10.1016/j.ejor.2020.06.020.

- Jo et al. (1997) Jo, H, Han, I, Lee, H (1997). Bankruptcy prediction using case-based reasoning, neural networks, and discriminant analysis. Expert Systems with Applications 13(2): 97–108. doi:10.1016/S0957-4174(97)00011-0.

- Kleinbaum (1994) Kleinbaum, DG (1994). Introduction to Logistic Regression. Springer New York, New York, NY. 1–38. doi:10.1007/978-1-4757-4108-7_1.

- Kononenko et al. (1997) Kononenko, I, Šimec, E, Robnik-Šikonja, M (1997). Overcoming the myopia of inductive learning algorithms with relieff. Applied Intelligence 7(1): 39–55. doi:10.1023/A:1008280620621.

- Kraskov et al. (2004) Kraskov, A, Stögbauer, H, Grassberger, P (2004). Estimating mutual information. Physical Review E 69: 066138. doi:10.1103/PhysRevE.69.066138.

- Kullback (1959) Kullback, S (1959). Information Theory and Statistics. Wiley, New York.

- Lamy et al. (2019) Lamy, JB, Sekar, B, Guezennec, G, Bouaud, J, Séroussi, B (2019). Explainable artificial intelligence for breast cancer: A visual case-based reasoning approach. Artificial Intelligence in Medicine 94: 42–53. doi:10.1016/j.artmed.2019.01.001.

- Lensberg et al. (2006) Lensberg, T, Eilifsen, A, McKee, TE (2006). Bankruptcy theory development and classification via genetic programming. European Journal of Operational Research 169(2): 677–697. doi:10.1016/j.ejor.2004.06.013. feature Cluster on Scatter Search Methods for Optimization.

- Li and Sun (2009) Li, H, Sun, J (2009). Predicting business failure using multiple case-based reasoning combined with support vector machine. Expert Systems with Applications 36(6): 10085–10096. doi:https://doi.org/10.1016/j.eswa.2009.01.013.

- Li et al. (2018) Li, L, Jamieson, K, DeSalvo, G, Rostamizadeh, A, Talwalkar, A (2018). Hyperband: A novel bandit-based approach to hyperparameter optimization. Journal of Machine Learning Research 18(185): 1–52. URL: http://jmlr.org/papers/v18/16-558.html.

- Li and Becker (2021) Li, W, Becker, DM (2021). Day-ahead electricity price prediction applying hybrid models of lstm-based deep learning methods and feature selection algorithms under consideration of market coupling. Energy 237: 121543.

- Li et al. (2022) Li, W, Paraschiv, F, Sermpinis, G (2022). A data-driven explainable case-based reasoning approach for financial risk detection. Quantitative Finance 0(0): 1–18. doi:10.1080/14697688.2022.2118071.

- Lin and Ding (2011) Lin, H, Ding, H (2011). Predicting ion channels and their types by the dipeptide mode of pseudo amino acid composition. Journal of Theoretical Biology 269(1): 64 – 69. doi:10.1016/j.jtbi.2010.10.019.

- Lundberg et al. (2020) Lundberg, SM, Erion, G, Chen, H, DeGrave, A, Prutkin, JM, Nair, B, Katz, R, Himmelfarb, J, Bansal, N, Lee, SI (2020). From local explanations to global understanding with explainable ai for trees. Nature Machine Intelligence 2(1): 56–67. doi:10.1038/s42256-019-0138-9.

- Lundberg and Lee (2017) Lundberg, SM, Lee, SI (2017). A unified approach to interpreting model predictions, in: Proceedings of the 31st International Conference on Neural Information Processing Systems, Curran Associates Inc., Red Hook, NY, USA. p. 4768–4777.

- Löw et al. (2019) Löw, N, Hesser, J, Blessing, M (2019). Multiple retrieval case-based reasoning for incomplete datasets. Journal of Biomedical Informatics 92: 103127. doi:10.1016/j.jbi.2019.103127.

- Mai et al. (2019) Mai, F, Tian, S, Lee, C, Ma, L (2019). Deep learning models for bankruptcy prediction using textual disclosures. European Journal of Operational Research 274(2): 743–758. doi:10.1016/j.ejor.2018.10.024.

- Martin (1977) Martin, D (1977). Early warning of bank failure: A logit regression approach. Journal of Banking & Finance 1(3): 249–276. doi:10.1016/0378-4266(77)90022-X.

- Mitchell (1997) Mitchell, TM (1997). Machine Learning. 1 ed., McGraw-Hill, Inc., USA.

- Morris (1994) Morris, BW (1994). Scan: A case-based reasoning model for generating information system control recommendations. Intelligent Systems in Accounting, Finance and Management 3(1): 47–63. doi:10.1002/j.1099-1174.1994.tb00054.x.

- Moxey et al. (2010) Moxey, A, Robertson, J, Newby, D, Hains, I, Williamson, M, Pearson, SA (2010). Computerized clinical decision support for prescribing: provision does not guarantee uptake. Journal of the American Medical Informatics Association 17(1): 25–33. doi:10.1197/jamia.M3170.

- Nagel and Purnanandam (2019) Nagel, S, Purnanandam, A (2019). Banks’ risk dynamics and distance to default. The Review of Financial Studies 33(6): 2421–2467. doi:10.1093/rfs/hhz125.

- Nishihara and Shibata (2021) Nishihara, M, Shibata, T (2021). The effects of asset liquidity on dynamic sell-out and bankruptcy decisions. European Journal of Operational Research 288(3): 1017–1035. doi:10.1016/j.ejor.2020.06.031.

- Novaković (2011) Novaković, J (2011). Toward optimal feature selection using ranking methods and classification algorithms. Yugoslav Journal of Operations Research 21(1). doi:0.2298/YJOR1101119N.

- Opler et al. (1999) Opler, T, Pinkowitz, L, Stulz, R, Williamson, R (1999). The determinants and implications of corporate cash holdings. Journal of Financial Economics 52(1): 3–46. doi:https://doi.org/10.1016/S0304-405X(99)00003-3.

- O’Roarty et al. (1997) O’Roarty, B, Patterson, D, McGreal, S, Adair, A (1997). A case-based reasoning approach to the selection of comparable evidence for retail rent determination. Expert Systems with Applications 12(4): 417 – 428. doi:10.1016/S0957-4174(97)83769-4.

- Richter and Weber (2013) Richter, MM, Weber, RO (2013). Case-Based Reasoning: A Textbook. Springer Publishing Company, Incorporated.

- Rudin (2019) Rudin, C (2019). Stop explaining black box machine learning models for high stakes decisions and use interpretable models instead. Nature Machine Intelligence 1(5): 206–215. doi:10.1038/s42256-019-0048-x.

- Shin and Lee (2002) Shin, KS, Lee, YJ (2002). A genetic algorithm application in bankruptcy prediction modeling. Expert Systems with Applications 23(3): 321–328. doi:10.1016/S0957-4174(02)00051-9.

- Song and Lu (2015) Song, YY, Lu, Y (2015). Decision tree methods: applications for classification and prediction. Shanghai Archives of Psychiatry 27(2): 130–135. URL: https://pubmed.ncbi.nlm.nih.gov/26120265.

- Sørmo et al. (2005) Sørmo, F, Cassens, J, Aamodt, A (2005). Explanation in case-based reasoning–perspectives and goals. Artificial Intelligence Review 24(2): 109–143. doi:10.1007/s10462-005-4607-7.

- Stoltzfus (2011) Stoltzfus, JC (2011). Logistic regression: A brief primer. Academic Emergency Medicine 18(10): 1099–1104. doi:10.1111/j.1553-2712.2011.01185.x.

- Sun and Shenoy (2007) Sun, L, Shenoy, PP (2007). Using bayesian networks for bankruptcy prediction: Some methodological issues. European Journal of Operational Research 180(2): 738–753. doi:10.1016/j.ejor.2006.04.019.

- Tian and Yu (2017) Tian, S, Yu, Y (2017). Financial ratios and bankruptcy predictions: An international evidence. International Review of Economics & Finance 51: 510–526. doi:10.1016/j.iref.2017.07.025.

- Tian et al. (2015) Tian, S, Yu, Y, Guo, H (2015). Variable selection and corporate bankruptcy forecasts. Journal of Banking & Finance 52: 89–100. doi:10.1016/j.jbankfin.2014.12.003.

- Vapnik (1998) Vapnik, VN (1998). Statistical Learning Theory. Wiley-Interscience.

- Voigt and Bussche (2017) Voigt, P, Bussche, Avd (2017). The EU General Data Protection Regulation (GDPR): A Practical Guide. 1st ed., Springer Publishing Company, Incorporated.

- Vukovic et al. (2012) Vukovic, S, Delibasic, B, Uzelac, A, Suknovic, M (2012). A case-based reasoning model that uses preference theory functions for credit scoring. Expert Systems with Applications 39(9): 8389–8395. doi:10.1016/j.eswa.2012.01.181.

- Wihartiko et al. (2018) Wihartiko, FD, Wijayanti, H, Virgantari, F (2018). Performance comparison of genetic algorithms and particle swarm optimization for model integer programming bus timetabling problem. IOP Conference Series: Materials Science and Engineering 332: 012020. doi:10.1088/1757-899x/332/1/012020.

- Zheng et al. (2019) Zheng, XX, Li, DF, Liu, Z, Jia, F, Sheu, JB (2019). Coordinating a closed-loop supply chain with fairness concerns through variable-weighted shapley values. Transportation Research Part E: Logistics and Transportation Review 126: 227–253. doi:https://doi.org/10.1016/j.tre.2019.04.006.

- Zhuang et al. (2009) Zhuang, ZY, Churilov, L, Burstein, F, Sikaris, K (2009). Combining data mining and case-based reasoning for intelligent decision support for pathology ordering by general practitioners. European Journal of Operational Research 195(3): 662–675. doi:https://doi.org/10.1016/j.ejor.2007.11.003.

- Zien et al. (2009) Zien, A, Krämer, N, Sonnenburg, S, Rätsch, G (2009). The feature importance ranking measure, in: Buntine, W, Grobelnik, M, Mladenić, D, Shawe-Taylor, J (Eds.), Machine Learning and Knowledge Discovery in Databases, Springer Berlin Heidelberg, Berlin, Heidelberg. 694–709.

Appendix

A Simple example of similarity calculation in CBR system