Dynamic Inventory Management with Mean-Field Competition 111The authors would like to thank Matt Loring and Ronnie Sircar for their helpful comments on an earlier draft.

Abstract

Agents attempt to maximize expected profits earned by selling multiple units of a perishable product where their revenue streams are affected by the prices they quote as well as the distribution of other prices quoted in the market by other agents. We propose a model which captures this competitive effect and directly analyze the model in the mean-field limit as the number of agents is very large. We classify mean-field Nash equilibrium in terms of the solution to a Hamilton-Jacobi-Bellman equation and a consistency condition and use this to motivate an iterative numerical algorithm to compute equilibrium. Properties of the equilibrium pricing strategies and overall market dynamics are then investigated, in particular how they depend on the strength of the competitive interaction and the ability to oversell the product.

keywords:

mean-field game, dynamic pricing, optimal control1 Introduction

This paper considers an optimal price setting model in which agents attempt to liquidate a given product inventory over a finite time horizon. Agents quote prices to potential buyers which affects both the revenue made on individual sales and the intensity at which sales are made. In addition, the intensity of sales is affected by the distribution of prices quoted across all agents, meaning the revenue rate of an individual agent is impacted by the effects of competition. When the finite time horizon is reached, each agent that has unsold units of the perishable good recovers a salvage cost for their remaining inventory, essentially selling it with an imposed penalty. We employ a mean-field game approach to the model which allows for more tractability in the analysis and computation of optimal pricing strategies compared to previous works.

Models of dynamic inventory pricing have been used in the past to dictate optimal pricing strategies for products which have a finite shelf life, notably fashion garments, seasonal leisure spaces, and airline tickets (see for example Gallego and Van Ryzin (1994), Anjos et al. (2004), Anjos et al. (2005), and Gallego and Hu (2014)). Some early work in dynamic inventory pricing restricts the underlying dynamics to be deterministic (see Jørgensen (1986), Dockner and Jørgensen (1988), and Eliashberg and Steinberg (1991)) which may allow for more tractability and further analysis of optimal policies, with or without considering competition. Models with stochastic demand have also been studied (see Gallego and Van Ryzin (1994) and Zhao and Zheng (2000)), but most results pertain to the case of a monopolistic agent without competition. The paper Gallego and Hu (2014) considers an oligopolistic market, but equilibrium with stochastic revenue streams is only classified in terms of a system of coupled differential equations. Instead of trying to analyse the solution to these equations, which is very computationally intense even for only two agents, the authors show that the stochastic game is well approximated by a deterministic differential game under suitable scaling of model parameters. The mean-field setting we consider can be thought of as allowing the number of agents to grow very large rather than the parameters which control the underlying dynamics. This retains most of the computational tractability of the single agent case which allows us to investigate the effects of competition.

Our model is a generalization of the single agent model considered in Gallego and Van Ryzin (1994), which we briefly summarize and refer to as the reference model when discussing the mean-field case. Specifically, agent’s hold a positive integer number of units of an asset and quote a selling price for each unit continuously through time. Sales occur at random times with an intensity that depends on the price quoted by the agent such that higher prices result in less frequent trades, creating a trade-off between large but infrequent revenue of quoting high prices, versus small but frequent revenue of low prices. Additionally, competition between agents is modelled by specifying that the sell intensity also depends on the distribution of prices quoted by all agents. Thus, an agent’s selling rate increases if other agents begin to quote higher prices. Our model setting is quite similar to the one in Yang and Xia (2013), especially in regards to the dynamics of agents’ inventory levels. The main difference is that our model allows prices to be continuous rather than being selected from a finite set of either high price or low price. Additionally, as a mean-field extension of one of the models presented in Dockner and Jørgensen (1988), Chenavaz et al. (2021) has a similar sell intensity to our work that depends on the distribution of prices quoted by all agents.

By working in a mean-field setting, our conditions for equilibrium do not require the solution to a coupled system of differential equations. Instead, equilibrium is classified by a single differential equation and a consistency condition. This lends itself to an efficient iterative algorithm which upon convergence yields a mean-field Nash equilibrium. The tractability of the equations which classify equilibrium allows us to easily demonstrate the resulting pricing strategies, and hence investigate how prices under the effects of competition compare to those of the reference model.

This style of model which relates intensity to price has also been used frequently in the literature on algorithmic trading. See for example Guéant et al. (2012), Guéant and Lehalle (2015), and Cartea and Jaimungal (2015). The main modelling differences in these works compared to those of dynamic inventory management already mentioned are the existence of an exogenous reference price process, relative to which optimal selling prices are quoted, and positive risk-aversion of the agent, both of which we also include in our model. In the financial setting of algorithmic trading, it is natural to give agents the ability to both buy and sell. This two-sided setting has also been heavily studied with similar intensity models, such as in Avellaneda and Stoikov (2008), Guéant et al. (2013), Cartea et al. (2014), and Cartea et al. (2017). These models are frequently applied in over-the-counter markets which are somewhat of a financial analogue to the consumer market setting which we envision in this work.

The tractability offered by a mean-field game framework over finite agent models has also led to their use in studying competition in other types of markets. In Chan and Sircar (2017) and Ludkovski and Yang (2017), the effects of competition through mean-field interaction are incorporated into models of energy production and commodity extraction. In Donnelly and Leung (2019), agents compete for a reward in an R&D setting with mean-field, in which earlier success yields greater rewards for the expended effort. In Li et al. (2019) agents expend effort to mine cryptocurrency, where an agent’s rate of mining depends on their hash rate as well as that of the entire population of miners. Our modeling framework has some similarities to these papers which allows us to employ a nearly direct adaptation of relevant numerical methods to compute equilibrium in our model.

A novel focus of our work is regarding how overall market behaviour is affected by features describing individual agents. In particular, we investigate how the magnitude of competitive interaction, the ability to oversell the asset (with penalty), and price caps affect the total wealth transferred from consumers in the market, the average price paid per unit asset, and the probability that a particular consumer will end up empty handed due to overselling of the asset. The dependence of market behaviour on these phenomena could be used to guide regulatory framework with the goal of achieving desired levels of various measurements of economic welfare.

The rest of the paper is organized as follows: in Section 2 we give an overview of the reference model, which is the single-agent equivalent to the mean-field setting we cover in more detail. In Section 3 we specify our model that incorporates the effects of competition, including the definition of equilibrium which we consider. In Section 4 we show several examples of numerically solving for equilibrium and investigate the effects of competition and other market phenomena. Section 5 concludes and longer proofs are contained in the Appendix, Section 6.

2 Reference Model

In this section, we introduce a reference model where we only consider one agent. Many aspects of the dynamics we consider are equivalent to those found in Gallego and Van Ryzin (1994) with some modifications made to the price process and agent’s performance criterion. Similarities can also be found with models pertaining to algorithmic trading, such as Guéant et al. (2012).

We work on a probability space with filtration satisfying the usual conditions, and assume that all random variables and stochastic processes are defined on the filtered probability space . We consider an agent who has to liquidate a certain quantity of a given product within a finite time horizon of length . The reference price process of the product is denoted by with dynamics

| (1) |

where is a constant, and is a Brownian motion.

We denote the agent’s spread process above the reference price by , so that she continuously quotes her selling price at at every time point, and is committed to sell one item222Note that selling one item may be understood as selling a block of units of the product, each block being of the same size. with the quoted price. Once the agent clears her inventory, she will stop trading. Her number of items sold follows a counting process denoted by . The superscript of denotes the dependence of the instantaneous intensity of this process on the spread process . Thus, the agent’s inventory satisfies

with initial value . As a consequence of her trades, the agent accumulates cash denoted by with dynamics given by

with given initial cash .

The agent’s goal is to optimize her expected P&L at time with an inventory penalty. Specifically, her value functional is

where and are positive constants. The objective functional consists of three parts. The first term in the expectation is the amount of cash at time . The second term corresponds to the salvage value of unsold items remaining at time , and the parameter represents a penalty for failing to sell all inventory by the end of the trading period. The running inventory penalty term penalizes deviation from zero during the entire trading horizon, so it can be interpreted as an urgency penalty, and the parameter acts as a risk control. Thus, the agent’s dynamic value function is

| (2) |

where the set of admissible controls consists of predictable processes on bounded from below by some large negative constant, .

To solve the optimal control problem described above, we consider the associated Hamilton-Jacobi-Bellman (HJB) equation along with terminal condition

| (3) | ||||

where is the indicator function that the inventory is non-zero. To solve the HJB equation, we use the excess value ansatz for given by

| (4) |

The first term is the current cash in hand, the second term accounts for the reference value of the current inventory, and the last term represents the expected profit or loss from liquidating items with both the terminal penalty and the running inventory penalty. Substituting the ansatz into HJB equation gives a system of ODEs with terminal condition given by

| (5) | ||||

To solve for the optimal feedback controls in terms of , we assume that the intensity function follows

| (6) |

where . Here is the sensitivity of the demand rate of the product with respect to the agent’s quoted price333Other forms of the intensity function can be used, but a particular property which is desired is that there is a unique maximizer of . We choose this exponential form for tractability reasons.. This means that the lower the quote is, the faster the item will be sold.

We delay a proof of existence and uniqueness of solution to Equation (5) until we have developed the control problem that incorporates multiple agents. The solution to Equation (5) is a special case of the solution to Equation (15) which appears in Proposition 3. A verification that solutions to the HJB equation (3) yield the value function defined in (2) is also postponed to the more general setting when we include competition (see Theorem 4).

Proposition 1 (Optimal Feedback Control)

The optimal feedback controls of the HJB equation are given by

- Proof

To intuitively understand the optimal feedback control form of the quote, note that the first term maximizes the rate of expected incoming profit, without any consideration for risk or terminal penalties. The quantity is the change of the expected future risk-adjusted P&L due to selling one item. Thus, the negative of this value, , represents the amount that the agent is willing to adjust her quote, positively or negatively, depending on the change of future risks and potential future profits by having one fewer item to sell.

Figure 1 shows the optimal quotes when Equation is numerically solved after substituting the optimal feedback controls in Proposition 1. We observe that the optimal quotes are decreasing in inventory level monotonically. This is sensible as the agents with more inventory have more urgency to sell the products and avoid the terminal penalty and uncertainty of the underlying price. In addition, the agent would lower her quotes in the early time interval to sell fast, and then increase her quotes near the terminal time . This is because at final time, the agent is more willing to benefit from a trading opportunity through proposing a higher quote and receiving a lower probability to sell.

We can also see that optimal quotes could be negative sometimes. This happens when there is a need to liquidate products at a very fast speed to avoid terminal penalty or underlying price risk. To avoid this situation, we could set the lower bound of admissible strategies to , or in the algorithmic trading context, the agent could use market order instead of limit order when negative quotes appear.

3 Competition Model

In this section we introduce a model with multiple agents, specify the dynamics of each agent’s inventory and wealth processes based on the prices they quote, and specify the optimization problem that each agent attempts to solve. Additionally, and distinct from the previous section with only one agent, we give the dynamics of the distribution of inventory across all agents in the mean-field limit, and finally we define the corresponding notion of equilibrium. This model is similar to that of Gallego and Hu (2014), and while we initially consider a finite number of agents we will only search for equilibrium in the mean-field limit of an infinite number of agents because this allows for more tractability and further analysis of the solution.

We consider a finite collection of agents indexed by aiming to liquidate shares of a given product. The reference price process is the same as Equation (1).

3.1 Inventory, Wealth, and Performance Criterion

Each agent chooses a spread process , but only actively posts a price when they hold non-zero inventory. Once their inventory reaches zero, their inventory state remains constant until time , effectively leaving the market. The mean spread chosen by all agents in the market is denoted by . Each agent has an associated inventory and wealth process denoted by and , respectively, and we assume all agents begin at time with the same maximum inventory . The superscripts of and are to indicate that the inventory and wealth processes of a single agent depend not only on their own strategy, but also on the mean strategy across all agents444We assume that dynamics depend on the distribution of spreads only through the mean spread, but other dependencies on the distribution of spreads across agents could also be implemented.. Keeping in mind that spreads are only posted by agents with non-zero inventory, the mean spread at time is equal to

The inventory and wealth of agent will changed based on the arrivals of a counting process denoted by which has instantaneous intensity given by for a function to be specified later. Thus, the inventory of agent changes according to the dynamics

When a transaction is executed with agent at time it occurs at a price of so that their wealth changes according to

We assume that, conditional on each spread process, the jump processes are independent. For a single agent with index , given fixed strategies for each other agent, their performance criterion is given by

| (7) |

3.2 Mean-Field Population Dynamics

We now proceed to the mean-field limit . Because the agents are homogeneous with respect to their inventory dynamics, wealth dynamics, and performance criteria, it is expected in equilibrium that they will employ Markov strategies with the same feedback form. Thus, we may consider a representative agent for all subsequent computations which allows us to suppress the index from all quantities. Suppose a representative agent chooses their spread according to the function such that

| (8) |

where represents the mean spread posted by all agents in the mean-field limit. An important quantity to track is the proportion of all agents that hold any particular value of inventory. For the inventory level , denote this proportion by which is equal to

Because all agents use the same feedback strategy , the process is equivalent to the law of the inventory process through the relation

and then the mean spread may be written as a weighted average

| (9) |

Further, any single agent with inventory leaves that state with intensity , which means there is a flow of agents from state to state at a rate of . Thus, the dynamics of each can be written (see Yang and Xia (2013) and Sun (2006)) as

| (10a) | |||

| (10b) | |||

| (10c) | |||

| and because each agent begins with maximum inventory the initial conditions are given by | |||

| (10d) | |||

3.3 Mean-Field Performance Criterion and Equilibrium

Each agent still wishes to maximize their expected terminal wealth subject to all other agents strategies being fixed. Inspection of Equations (9) and (10) show that for a fixed , the process is deterministic, and in this case the dynamics of a representative agent’s wealth and inventory do not have explicit dependence on , but only on . Thus, when specifying the performance criterion of a representative agent, it also will not depend on the entire flow of the population distribution , but only on the mean spread . For a given deterministic mean spread, we write the performance criterion as

Definition 2 (Markov Mean-Field Nash Equilibrium)

A Markov mean-field Nash equilibrium is a function which satisfies

for all function .

The interpretation of the equilibrium given in Definition 2 is that we seek a function which determines the strategy of all agents through the relation (8) such that no particular agent can increase their performance by deviating from that strategy. The analytical tractability of this problem over the finite-agent case is due to the fact that in the mean-field setting, no single agent can affect the dynamics of the whole population, as determined by Equation (10) by changing their own strategy. Finding the mean-field Nash equilibrium thus comes down to solving a single optimization problem along with checking a consistency condition. Specifically, we will take a mean spread process as given and solve for the optimal strategy for a representative agent in feedback form. Then we will check for the consistency relation that if every agent uses the computed strategy then the mean spread process, as determined by Equation (9) is given by , the same process initially given. If this holds then the feedback control is an equilibrium.

3.4 Mean-Field Optimization Problem

The intensity function for the representative agent states that her sales depend on both her own quote and the mean quote of all agents. We assume that is twice differentiable in both inputs. According to Dockner and Jørgensen (1988), the intensity should satisfy the following assumptions:

| (11a) | ||||

| (11b) | ||||

| (11c) | ||||

| (11d) | ||||

| (11e) | ||||

Condition (11a)-(11d) are standard assumptions in competition theory. Condition (11a) is equivalent to assuming a downward-sloping demand curve, that is, with a fixed mean quote a lower price quoted from the representative agent leads to higher demand. Condition (11b) states that an increase in the mean quote causes the sales of the representative agent to rise. Condition (11c) implies that if all agents raise their quotes by the same amount, their sales will decrease simultaneously. Condition (11d) implies that the higher the mean quote, the more difficult it is for the representative agent to increase her probability of selling by reducing her own quote. Conversely, if the mean quote is higher, the representative agent will lose market share more quickly when she raises her quote. Condition (11e) is a technical condition, originating from the strict concavity of the Hamiltonian with respect to quote (i.e., the control variable).

We assume that the instantaneous intensity is of the following form similar to (Chenavaz et al., 2021, (4.2))

| (12) | ||||

for constants . This assumption satisfies all the conditions stated in Equation (11). Compared to the single-agent intensity function defined in Equation (6), there is an extra term in the exponent that represents the competitiveness in the market whose strength is characterized by . Under this assumption, there are two drivers for faster execution: lower quoted price of one’s own, and higher mean quoted price of other market participants. This is consistent with the expected sales loss to competitors when one’s price becomes higher relative to the market price for the same product.

We briefly investigate the effect of the mean quote on the total sales of the market. First we consider the finite -player game, and then take to infinity. According to Equation (12), the intensity for the -th agent is

Suppose a representative agent, denoted by index , fixes her quote , and other agents increase their quotes by the same amount. The change in total market intensity then depends on the sum of the derivatives of individual intensities with respect to quotes of all other agents, which is

For sufficiently large , this quantity is negative. This means that if every agent except for the representative agent raises their quotes by the same amount, although the probability of selling for the representative agent increases, the total sales across all agents decrease, which is economically sensible.

For a given deterministic function , the representative agent optimizes

| (13) |

and the set of admissible controls is defined as

where is a non-negative constant lower bound. By the dynamic programming principle, we introduce the HJB equation with terminal condition associated to this optimization problem

| (14) | ||||

We use a similar ansatz as Equation (4) to solve the HJB equation.

Proposition 3 (Solution to HJB Equation)

-

Proof

See Appendix A.

We see in Proposition 3 that the feedback form of the optimal strategy is similar in form to the single agent case. There are two differences, one being a change based on immediate effects of competition which sees replaced , and the other is the fact that the change in expected future risk-adjusted P&L, represented by , will also be different from the corresponding term in Proposition 1. The terminal condition determines the optimal quotes at time regardless of equilibrium considerations, and inspection shows that these quotes will be smaller than the single agent case, as would be expected with the effect of competition. The same cannot necessarily be said for all without solving for equilibrium.

To show that the solution to the HJB equation is really the solution to the control problem, we prove the following verification theorem. In particular, this establishes that the strategy computed in the iterative algorithm of Section 4.1 are optimal given an assumed mean quote process.

Theorem 4 (Verification Theorem)

-

Proof

See Appendix B.

In the statement of Theorem 4, we make the technical assumption that the given mean quote, , is continuous. In fact, we only require that it is bounded, for technical reasons needed in the proof. However, this is not a restrictive assumption because any optimal strategy with a feedback form given by (16) will be continuous, and therefore bounded, and the resulting arising from all agents using this feedback control will also have these properties. Thus, the assumption is without loss of generality.

4 Numerical Experiments

In this section, we numerically solve for the equilibrium, and illustrate the behaviour of the optimal strategy , the mean spread , the inventory distribution across agents , and other quantities of interest.

4.1 Algorithm

Inspired by Li et al. (2019), we use the following algorithm to numerically find an equilibrium. First, for a given mean quote we solve the control problem, the optimality of which is ensured by our verification theorem. Then, we use the optimal individual quote to find the population dynamics. With these two solutions, we calculate the corresponding new mean spread and repeat this process until convergence. The details are as follows:

-

1.

We divide the entire time horizon into equidistant time grid. Initialize with a mean quote for every time point.

-

2.

Given any mean quote, , we solve the optimal control problem numerically. This is done with a fully explicit backward finite difference method to solve Equation (15) starting from time . This simultaneously gives the optimal control for the given mean quote, , in feedback form through Equation (16).

-

3.

With the optimal control given in feedback form, we compute the population process using Equation (10). This is also done numerically using a fully explicit forward finite difference method.

-

4.

We introduce a learning rate parameter to update the mean quote process. To reduce oscillations in searching for the equilibrium, we choose to be a small number, and we update the mean quote price according to

These steps are repeated until convergence of the sequence to within a specified tolerance555In the following numerical examples, we identify the algorithm as converged if the standard error of and is not more than . We do not claim that equilibrium is guaranteed to exist or is unique, but for all sets of parameters considered, convergence was attained and was found not to depend on the initializing . More numerical details and explanations can be found in Appendix C., and we drop the counting index in the final mean quote process.

Once convergence is attained, we will have found a function which satisfies the conditions of equilibrium given in Definition 2, given by .

4.2 Optimal Quotes in Equilibrium

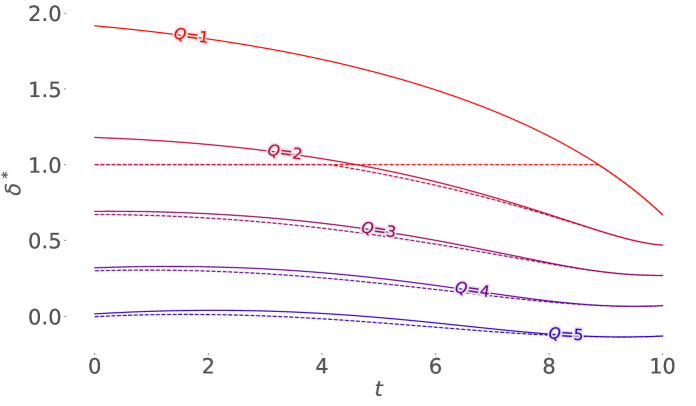

The optimal quotes are presented in Figure 2, as well as the mean quote in Figure 3 and the dynamics of the proportion process in Figure 4. From Figure 2, we observe that the optimal quotes in mean-field case shares the same decreasing pattern against inventory level with ones in one-agent case in Figure 1. In addition, for lower inventory levels () the optimal quotes are decreasing with time, whereas for higher inventory levels () the optimal quotes slowly increase early in the time interval and then decrease. This effect is caused by the changing nature of competition embedded in the mean spread (see Figure 3). At early times, everyone is posting small spreads, but as some agents begin to sell the mean spread quickly increases. For an agent that remains in a high inventory state, this increase in average price in the market creates less competition, and they begin to benefit themselves by quoting slightly higher prices.

In Figure 3, because each agent begins with maximum inventory , the mean quote begins at the optimal quote for that inventory level. It quickly rises as agents begin to sell inventory and move to lower inventory states, causing them to increase their quoted price. At later times the mean quote begins to decrease due to two effects. First, as time approaches the end of the trading period agents are incentivized to quote smaller prices to avoid the liquidation penalty. Second, more and more agents end up fully liquidating their positions, removing their large quoted prices from the market and thereby decreasing the mean. Figure 4 shows the distribution, , of the agents’ inventories through time. For this set of parameters, the majority of agents sell all of their inventory by time , indicated by the fact aht .

4.3 Comparison with Single-Agent Reference Model

Figure 5 compares the optimal quotes in the monopoly and mean-field cases. For lower inventory levels , the optimal quotes in multi-agent case are consistently lower than the ones in single-agent case. However, for the maximum inventory level , the optimal quotes in the multi-agent case are sometimes higher than in the single-agent case. This trend is because the optimal quotes corresponding to higher inventory levels tend to be lower than the mean quote in the market. Thus, the items in multi-agent case have a higher probability to be executed compared to the single-agent case as per Equation (12). As a result, the agent can be more aggressive by setting a higher quote in the multi-agent case.

4.4 Effect of Competitiveness on Equilibrium

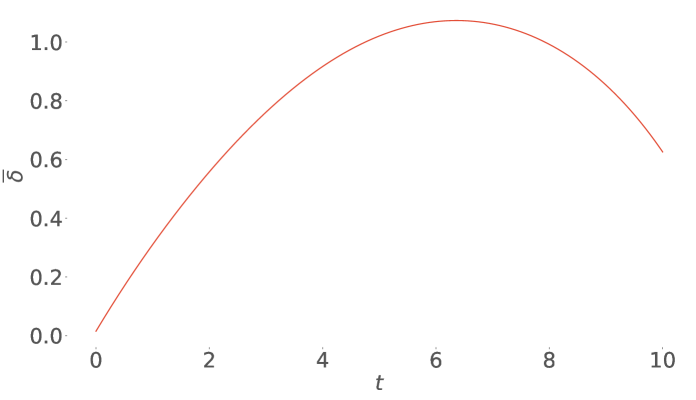

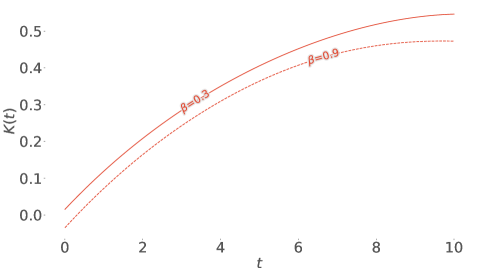

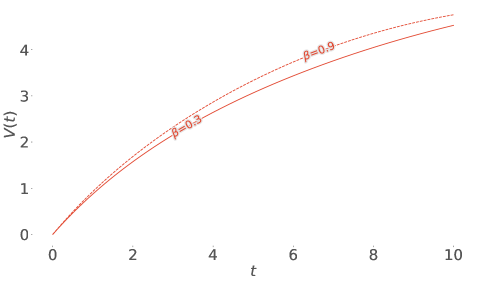

Figure 6 shows how the competitiveness parameter, , affects the optimal quotes. In general, higher competitiveness of the market brings the optimal quotes of different inventories closer together. However, note that higher competitiveness does always move the optimal quotes of different inventory levels in the same direction. For lower inventory levels, larger leads to lower optimal quotes, but for higher inventory levels the direction of price change depends on time. From figure 7, the mean quote is decreasing in at all points in time. This means more intense competition brings lower market quote price, which is economically sensible. In addition, we see that a larger proportion of agents end up selling their whole inventory when the competitiveness parameter is larger.

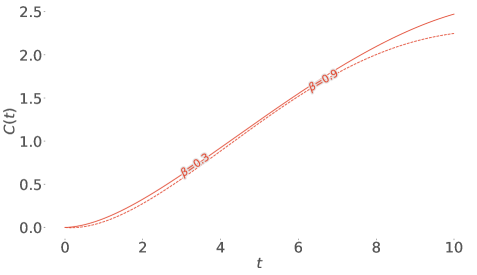

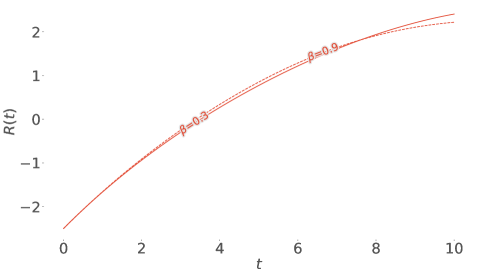

To illustrate the effects of competitiveness on the consumers and agents, we define cumulative cost , cumulative revenue and cumulative volume up to time as

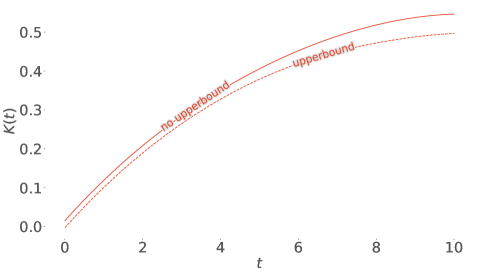

Cumulative cost corresponds to the total wealth paid by consumers up to time , and cumulative revenue represents the profits made by agents up to time . Theoretically, cumulative revenue should be equal to cumulative cost until terminal time when the penalty proportional to is realized, but to ensure is continuous, we preemptively charge this penalty in the form of , as if all agents stopped trading at time . With the above functions, we can compute the corresponding average transaction cost by

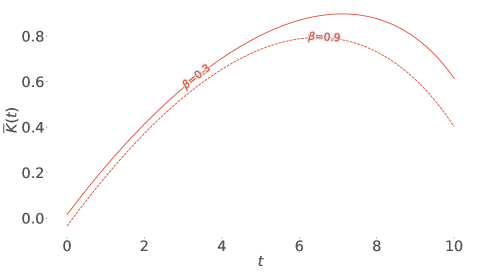

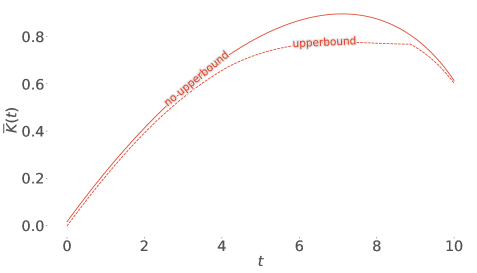

and the instantaneous average transaction cost by

The average transaction cost represents the average price consumers have paid for one unit of products up to time , and the instantaneous average transaction cost is the the average price to buy one unit at time .

In Figure 8, we can see that for this set of parameters, a higher value of competitiveness leads to lower cost, average cost and instantaneous average cost. This implies that consumers indeed benefit from a more competitive market with lower purchase prices. The instantaneous average cost shares a similar concave shape with the mean quote in Figure 7. This means that the best purchasing time for consumers is either the start or the end of the time horizon, consistent with the early bird price and closing sale in reality. Additionally, for the larger value of , the maximum of the curves and occur at earlier times. This means that the vendors will decrease price earlier in a more competitive market, and consumers indeed enjoy this lower market price earlier. In Figure 9, we can see that for this set of parameters, a higher value of competitiveness leads to a higher volume, but lower revenue near the terminal time. One interesting phenomenon is that, before the terminal time, we enter into a win-win situation for both agents and consumers with a higher value of competitiveness . We observe that for this time period, with higher demand of the market, a higher level of competitive interaction can boost the volume and cumulative revenue for agents and decrease the transaction cost for consumers simultaneously.

4.5 Effect of Upper Bound on Equilibrium

In this section, we impose an upper bound on admissible strategies. In reality, this price control is sometimes enforced by the government on the necessities, and we discuss how the behaviour of optimal strategy , the mean spread , and the inventory distribution changes under an additional price ceiling.

Suppose we define a new set of admissible controls by

where is the non-negative upper bound. Then the optimal feedback control becomes

The proof of uniqueness of the solution to HJB equation and verification theorem still stands with minor adjustments.

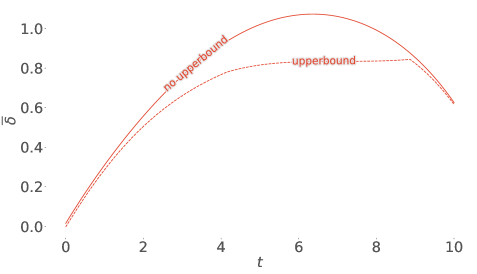

In Figure 10, we can observe that optimal quotes with the upper bound decrease for all inventory levels. This is consistent with our expectation that the competition becomes more intense with an upper bound on price, as the agents with initially lower prices will also try to keep their market share while others are lowering their prices. For lower inventory levels , the differences are more significant. This is due to the fact that agents with lower holdings tend to propose a higher quote, and that is where the restriction on pricing comes in. The optimal quotes converge at the terminal time, because the agents lower their price as much as possible for quick sales, at the level lower than the constraint.

In Figure 11, mean quote with the upper bound is always lower. At the beginning, the two lines are very close. As time goes by, more agents come to lower inventory levels and receive price restrictions, thus resulting in bigger differences between the mean quotes. Closer to the terminal time , the two lines approach each other again. This is because the distribution of inventory levels and the corresponding optimal quotes are similar near terminal time in these two scenarios, as shown in Figure 10 and Figure 11.

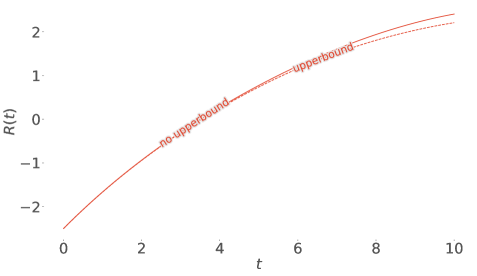

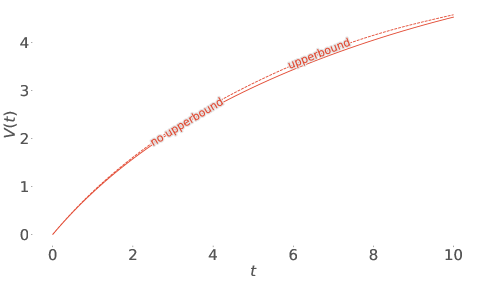

Figures 12 shows that the price limit boosts the sales volume but reduces revenue for the agents. We can see that consumers buy products at a lower price with price ceiling, which means the restriction on high prices is effective in reducing consumer expenditure under our setting666In reality, price ceiling does not always work out as intended. If it leads to a severe imbalance between supply and demand, this can in turn cause shortages and underground markets..

4.6 Effect of Overselling

In this section, we study the effects of overselling where agents are allowed to sell more volume of inventory than they have physically available during the trading period, and they must pay extra cost to clear out the negative inventory at terminal time. This phenomenon frequently happens in the tourism industry. For example, airlines oversell air tickets anticipating some cancellations or no-shows of the customer bookings. If everyone shows up, airlines may refuse boarding to certain passengers but must pay compensation depending on jusrisdiction.

We set the admissible inventory level set as , and is a non-positive constant. The new model under overselling setting is the same as the one in Section 3, except for the lower bound of inventory and the new value function

where and are all positive constants. Compared to Equation (13), we set different parameters and of terminal penalty for positive and negative inventory respectively. Here, the difference represents the extra expected compensation paid by agents in the case that consumers make a claim on the oversold units. Since overselling brings more inventory risk, we set parameters of running inventory penalty to discourage this behavior. Then the associated HJB equation is given by

We use the same ansatz in Proposation 3 to solve the above equations, and get the following ODEs

As overselling does not affect the term in the ODEs, the feedback form of the optimal control is still the same as Equation (16). We can show that the above ODEs of still has a unique solution under overselling setting, and the proof of verification theorem still stands with minor adjustments.

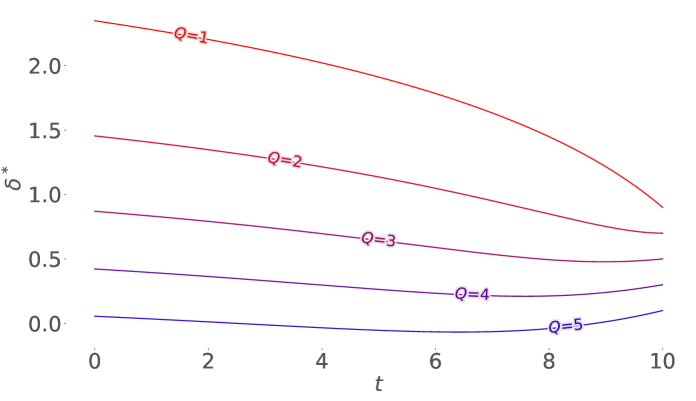

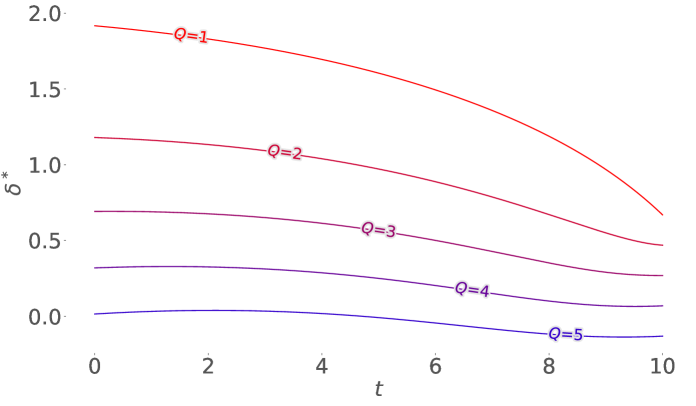

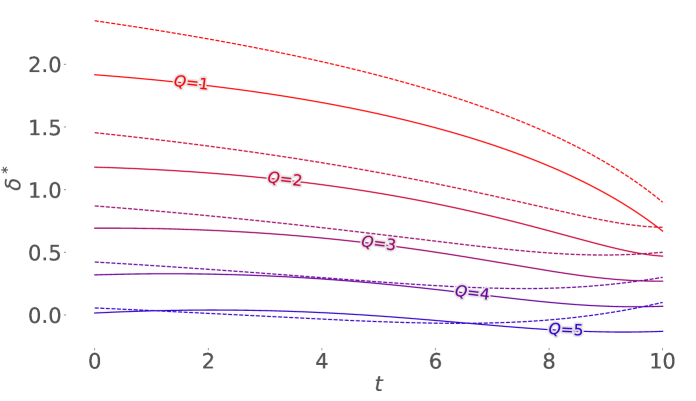

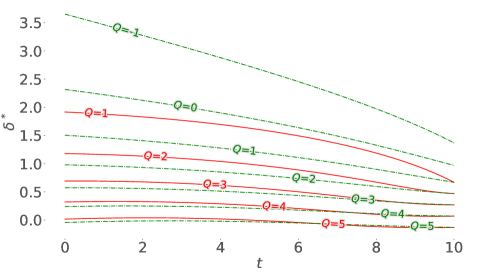

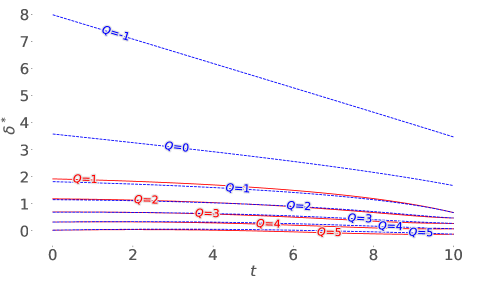

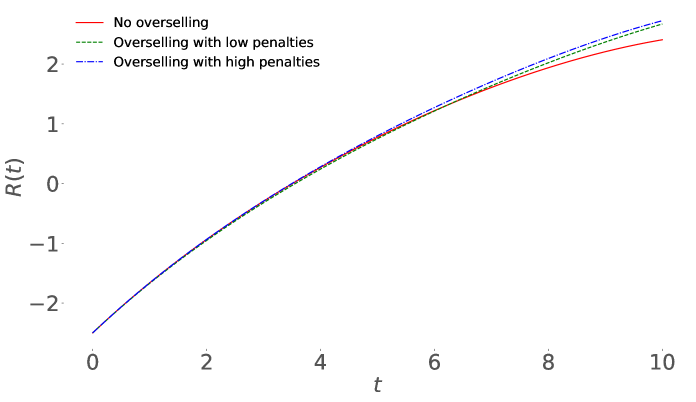

Figure 13 shows the change in optimal quotes when the ability to oversell is introduced, and it also indicates how the size of terminal penalty parameter and running inventory penalty parameter for negative inventory affects the change in quotes. As expected, the optimal quotes under overselling setting are still decreasing in inventory level monotonically. On the left of Figure 13, with smaller and , we can see that for all positive inventory levels, the optimal quotes with overselling are generally lower than the ones without overselling. On the right panel of Figure 13, with larger values of and , the quotes for positive inventory still generally decrease when overselling is allowed, but the effect of this feature is less pronounced. This indicates that higher value of and leads to higher optimal quotes across all inventory levels with overselling. Additionally, with stronger penalties for overselling, prices at early times are similar to prices when overselling is prohibited, but over time as more agents reach zero and negative inventory levels, the quoted prices become very large because these agents are only willing to sell at high prices to recoup the large overselling penalty.

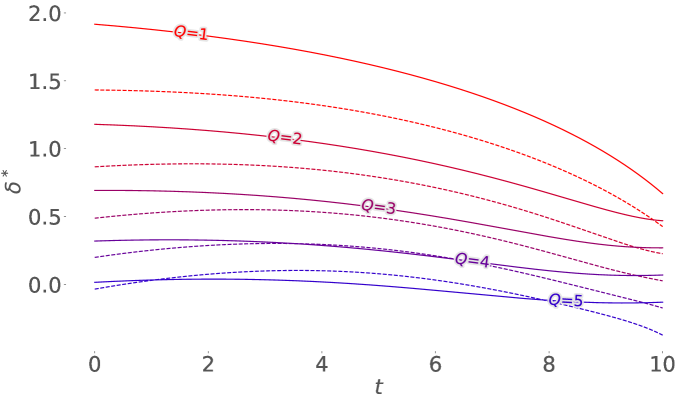

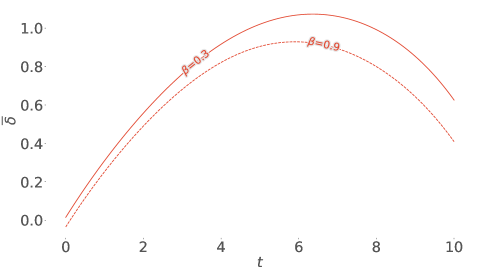

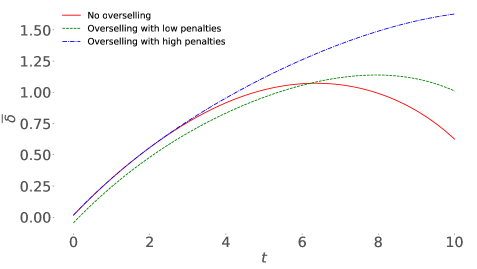

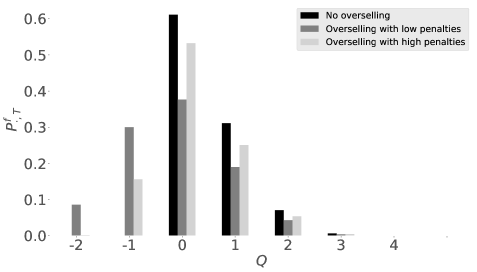

The left of Figure 14 shows the change in mean quotes when the ability to oversell is introduced. The solid line stands for the mean quote without overselling, and the dotted and dash-dotted curves represent overselling for different values of and . The effect of overselling depends also heavily on the penalty parameters for negative inventory levels. The crossing of mean quote without overselling and mean quote with overselling with low penalty is consistent with the result about optimal quotes in the left of Figure 13. In the beginning, agents who can oversell quote lower prices, thus resulting in lower mean quote. As time goes by, the optimal quotes with overselling get closer to the ones without overselling. In the meantime, more agents achieve negative inventory levels with much higher quotes, so the mean quote with overselling exceeds the one without overselling closer to terminal time. For mean quote without overselling and mean quote with overselling with high penalty, we can see that if the punishment for overselling is high enough, the mean quote with overselling can always be higher than the one without overselling. The right of Figure 14 compares the distributions of inventory at terminal time. The distribution of inventory at time with overselling follows a bell-shaped curve. With overselling, most agents stay at zero inventory, and there are more agents with negative inventory than the ones with positive inventory. With overselling, we can observe that higher terminal penalty parameter and running inventory penalty parameter for shorting indeed reduces the proportion of agents ending at negative inventory levels.

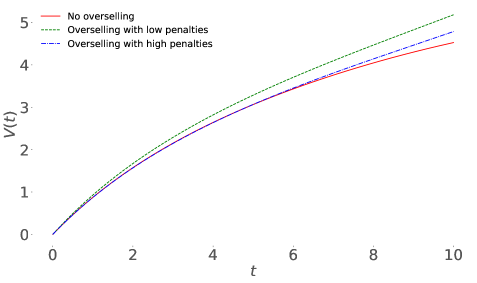

The cumulative cost , cumulative revenue , and cumulative volume are slightly modified when overselling is introduced, and we write them as

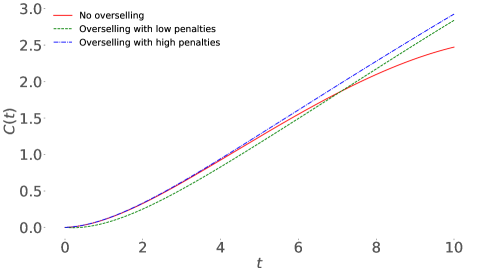

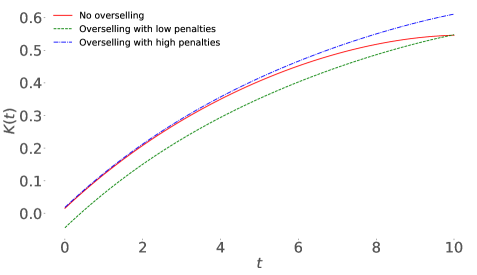

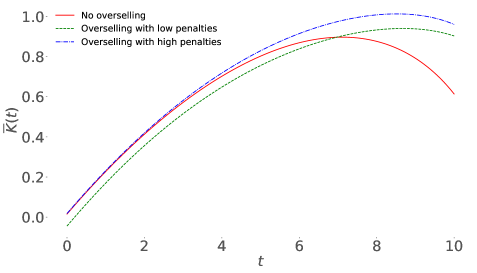

Figure 15 shows that regardless of the level of penalty, cumulative cost near the terminal time with overselling is higher. From the top right panel we see that overselling leads to higher traded volume, with smaller penalties leading to higher total volume traded. In the bottom left panel, the average transaction cost without overselling lies between the ones with overselling. When overselling with high penalties, overselling leads to higher average transaction cost. However, with low penalty, consumers indeed pay less on average to buy more because of overselling. This indicates that with the appropriate levels of penalty parameters and for overselling, agents can sell more products, while consumers pay almost the same average transaction cost at terminal time compared to the non-overselling case. In the bottom right panel, we can observe that the instantaneous average cost with overselling is always high close to the terminal time. This is due to the fact that the instantaneous fraction of oversold products is higher near the terminal time, thus raising up the unit price. It is generally more beneficial for consumers to purchase earlier to avoid higher price due to overselling.

Perhaps counterintuitive is the result that a higher overselling penalty can result in greater total revenue by agents, as seen in Figure 16. However, as the discussion of Figure 13 has shown, when overselling penalties are large, agents spend much of the time interval quoting prices as if they are not allowed to oversell. These prices are higher than the situation with weak overselling penalties, because those agents wish to lower prices and accelerate the rate of liquidating their inventory. With a large penalty, when most agents have sold off their positive positions, the market moves into an overselling regime where prices are much higher. This is why we see a deviation of the solid (no overselling) and dash-dotted (highly penalized overselling) curves in Figures 14 (left panel) and 15 (all panels) which becomes apparent around .

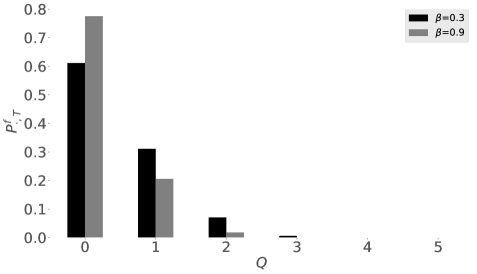

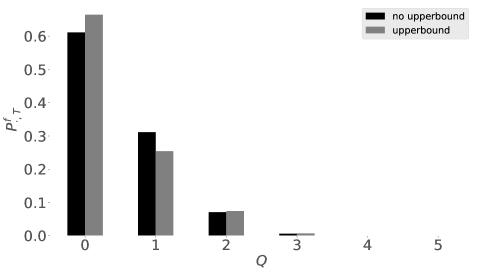

Our final investigation is on the effect of overselling on consumers from the perspective of cancellation. If more units of the product are sold than are physically available, then some consumers will end up empty handed. Depending on the industry, the compensation policy, and the consumer herself, she may be indifferent between having the product versus the compensation, but nevertheless the probability of being in this situation is of interest.

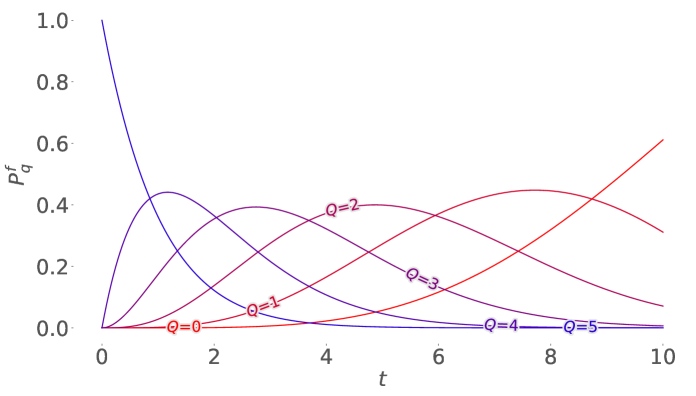

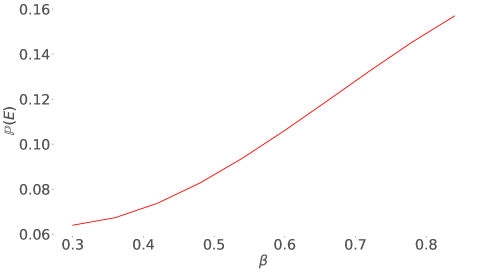

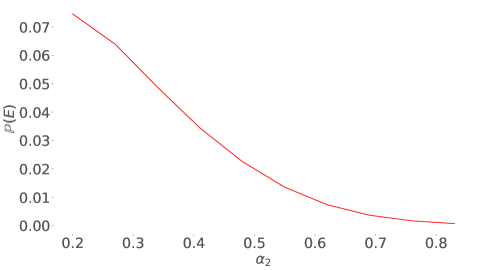

For one particular consumer at terminal time, we define event as the scenario of her product being cancelled due to overselling, and events as the scenario of her buying from agents who oversold share, . We assume that at the terminal time, agents who oversold randomly cancel orders due to shortage uniformly across all consumers they transacted with, so the cancellation probability for a particular consumer is given by

The left of Figure 17 shows how the value of competitiveness parameter effects this cancellation probability. We can see that the cancellation probability is increasing with competitiveness. With higher competitiveness, agents will generally lower their quotes, so the proportion of agents ending at negative inventory levels will increase. In the right panel of Figure 17, we can observe that higher penalty for overselling leads to a lower probability of cancellation. This is consistent with the result on the right of Figure 14 where we demonstrated that a higher terminal penalty parameter and running inventory parameter reduces the proportion of agents who oversold, thus decreases the cancellation probability. For consumers, there is a trade-off between the cancellation probability and the average transaction cost and instantaneous average cost, which is increasing in penalty parameters as per Figure 15.

5 Conclusion

We have formulated a model for dynamic inventory pricing which accounts for the effects of competition through a mean-field interaction. First, we introduce a reference model with one agent looking to liquidate a significant number of certain product. We expand our model into the case of infinite players. In our model, the realized sales of each agent is described by a doubly stochastic Poisson process, whose intensity depends on both one’s own quoted price and the distribution of quoted prices among all agents. Through the frequency of individual sales, agents compete with each other. This mean-field game system consists of two equations: the dynamic programming equation describing the optimality of representative agent, and the Kolmogorov forward equation governing the dynamics of the distribution of inventory across agents. The two equations are coupled by the consistency condition, which enables us to find the equilibrium by fixed point iterations. We numerically find an unique equilibrium. As expected, competition leads to more sales and lower mean quoted prices of the market as a whole. Interestingly, when market competition’s level increases, the optimal quoted prices for all inventory levels do not necessarily decrease all the time.

6 Appendix

A Proof of Proposition 3

-

Proof

Applying the first order conditions directly to term in Equation (15) leads to the optimizer result. It can be checked that the second order derivative of the sup term at is negative.

Equation (15) is of the form . To show existence and uniqueness of the solution to this equation, by the Picard-Lindelof theorem, the function need to be Lipschitz continuous.

The Lipschitz continuity property of implies the same for , where satifies

The Lipschitz continuity property of will be a result of showing that all directional derivatives of exist and are bounded for all .

The supremum is attained at in Equation (16). Thus, two separate domains for must be considered: and . First, consider , so that . Substituting this into the expression for yields

Taking partial derivatives of in this domain gives us

and this expression is bounded in . Thus, and are bounded in this domain, and so directional derivatives exist and are also bounded everywhere in the interior of the domain. On the boundary, directional derivatives exist and are bounded if the direction is towards the interior of the domain.

Now consider , which implies . The expression of in this domain is

Partial derivatives of are given by

So similarly to the first domain, directional derivatives exist and are bounded in the interior. On the boundary, they exist and are bounded in the direction towards the interior of the domain. Thus, we have existence and boundedness on the boundary towards every of the two domains. The directional derivative on the boundary is zero when the direction is parallel to the boundary. Existence and boundedness of directional derivatives for all allows us to show the Lipschitz continuity condition easily:

where is the curve which connects to in a straight line and is a uniform bound on the gradient of . This proves that there exists a unique solution to Equation (15).

B Proof of Theorem 4

-

Proof

We define a candidate value function . From Ito’s lemma we have

Let be an arbitrary admissible control and let be arbitrary. Then since satisfies Equation (15), the following inequality holds almost surely for every

Thus, taking an expectation of , we have

where exists due to the boundedness of . Therefore satisfies

This inequality holds for the arbitrarily chosen control , therefore

and letting we finally obtain

Now let be the control process defined as (16), then we have

and so satisfies

Therefore,

Combining the above results, we prove that

C Numerical Stability and Uniqueness of Equilibrium

We run the algorithm described in Section 3 100 times, each with a randomized initial value of mean quote, and check the converged value of mean quote obtained from the experiments. Over all 100 simulations, the average values of the mean quote at any time , , is of order to , while the corresponding standard errors are of order to , which is smaller than the tolerance used in the algorithm. Thus we conclude that the final value of is always the same, which shows that the algorithm is robust with respect to initial point, and numerically supports our argument that the equilibrium exists and is unique.

References

- Anjos et al. (2004) Anjos, M. F., R. C. Cheng, and C. S. Currie (2004). Maximizing revenue in the airline industry under one-way pricing. Journal of the Operational Research Society 55(5), 535–541.

- Anjos et al. (2005) Anjos, M. F., R. C. Cheng, and C. S. Currie (2005). Optimal pricing policies for perishable products. European Journal of Operational Research 166(1), 246–254.

- Avellaneda and Stoikov (2008) Avellaneda, M. and S. Stoikov (2008). High-frequency trading in a limit order book. Quantitative Finance 8(3), 217–224.

- Cartea et al. (2017) Cartea, Á., R. Donnelly, and S. Jaimungal (2017). Algorithmic trading with model uncertainty. SIAM Journal on Financial Mathematics 8(1), 635–671.

- Cartea and Jaimungal (2015) Cartea, A. and S. Jaimungal (2015). Optimal execution with limit and market orders. Quantitative Finance 15(8), 1279–1291.

- Cartea et al. (2014) Cartea, Á., S. Jaimungal, and J. Ricci (2014). Buy low, sell high: A high frequency trading perspective. SIAM Journal on Financial Mathematics 5(1), 415–444.

- Chan and Sircar (2017) Chan, P. and R. Sircar (2017). Fracking, renewables, and mean field games. SIAM Review 59(3), 588–615.

- Chenavaz et al. (2021) Chenavaz, R., C. Paraschiv, and G. Turinici (2021). Dynamic pricing of new products in competitive markets: A mean-field game approach. Dynamic Games and Applications 11(3), 463–490.

- Dockner and Jørgensen (1988) Dockner, E. and S. Jørgensen (1988). Optimal pricing strategies for new products in dynamic oligopolies. Marketing Science 7(4), 315–334.

- Donnelly and Leung (2019) Donnelly, R. and T. Leung (2019). Effort expenditure for cash flow in a mean-field equilibrium. International Journal of Theoretical and Applied Finance 22(04), 1950014.

- Eliashberg and Steinberg (1991) Eliashberg, J. and R. Steinberg (1991). Competitive strategies for two firms with asymmetric production cost structures. Management Science 37(11), 1452–1473.

- Gallego and Hu (2014) Gallego, G. and M. Hu (2014). Dynamic pricing of perishable assets under competition. Management Science 60(5), 1241–1259.

- Gallego and Van Ryzin (1994) Gallego, G. and G. Van Ryzin (1994). Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management science 40(8), 999–1020.

- Guéant and Lehalle (2015) Guéant, O. and C.-A. Lehalle (2015). General intensity shapes in optimal liquidation. Mathematical Finance 25(3), 457–495.

- Guéant et al. (2012) Guéant, O., C.-A. Lehalle, and J. Fernandez-Tapia (2012). Optimal portfolio liquidation with limit orders. SIAM Journal on Financial Mathematics 3(1), 740–764.

- Guéant et al. (2013) Guéant, O., C.-A. Lehalle, and J. Fernandez-Tapia (2013). Dealing with the inventory risk: a solution to the market making problem. Mathematics and financial economics 7(4), 477–507.

- Jørgensen (1986) Jørgensen, S. (1986). Optimal production, purchasing and pricing: A differential game approach. European Journal of Operational Research 24(1), 64–76.

- Li et al. (2019) Li, Z., A. M. Reppen, and R. Sircar (2019). A mean field games model for cryptocurrency mining. arXiv preprint arXiv:1912.01952.

- Ludkovski and Yang (2017) Ludkovski, M. and X. Yang (2017). Mean field game approach to production and exploration of exhaustible commodities. arXiv preprint arXiv:1710.05131.

- Sun (2006) Sun, Y. (2006). The exact law of large numbers via fubini extension and characterization of insurable risks. Journal of Economic Theory 126(1), 31–69.

- Yang and Xia (2013) Yang, J. and Y. Xia (2013). A nonatomic-game approach to dynamic pricing under competition. Production and Operations Management 22(1), 88–103.

- Zhao and Zheng (2000) Zhao, W. and Y.-S. Zheng (2000). Optimal dynamic pricing for perishable assets with nonhomogeneous demand. Management science 46(3), 375–388.