Clustered Archimax copulas

Abstract

When modeling multivariate phenomena, properly capturing the joint extremal behavior is often one of the many concerns. Archimax copulas appear as successful candidates in case of asymptotic dependence. In this paper, the class of Archimax copulas is extended via their stochastic representation to a clustered construction. These clustered Archimax copulas are characterized by a partition of the random variables into groups linked by a radial copula; each cluster is Archimax and therefore defined by its own Archimedean generator and stable tail dependence function. The proposed extension allows for both asymptotic dependence and independence between the clusters, a property which is sought, for example, in applications in environmental sciences and finance. The model also inherits from the ability of Archimax copulas to capture dependence between variables at pre-extreme levels. The asymptotic behavior of the model is established, leading to a rich class of stable tail dependence functions.

keywords:

t1\thanksmarkt2

\thanksmarkt3

\thanksmarkt2

\thanksmarkt4

r1Corresponding author: simon.chatelain.ev@gmail.com

1 Introduction

The Archimax copula model introduced by Capéraà, Fougères and Genest (1997) has been advocated in Chatelain, Fougères and Nešlehová (2020) as a flexible way to model a group of variables whose asymptotic dependence is driven by a stable tail dependence function (stdf); or more precisely a random vector whose dependence structure follows an asymptotic extreme-value regime perturbed by the same distortion. However, as it is the case for rainfall over large territories for example, asymptotic independence between certain variables is likely to be present and this phenomenon cannot be handled by a single Archimax model without limiting the marginal dependence structure to be an (exchangeable) Archimedean copula. In financial applications, a stock portfolio might contain stocks from the same industry, causing them to be dependent in the extreme regime, while stocks from different industries might be asymptotically independent. Likewise, assuming the same distortion for all variables may not be realistic when the number of variables is large.

We propose a dependence model based on the survival copula of a nonnegative, real random vector of the form

where for all , are nonnegative random variables and are -dimensional random vectors which will be characterized later. More specifically, each of the vectors will be defined so as to have an Archimax survival copula, while conditional independence of the vectors given will introduce parsimony to the dependence model. This paper focuses on the survival copula of , which can subsequently be used in a copula model with arbitrary margins.

Stochastic representations involving a randomly scaled random vector are very common in the literature. For example, pseudo-polar representations exist for elliptical (see Fang, Kotz and Ng (1990)), generalized Pareto (see Ferreira and de Haan (2014)), Archimedean (see McNeil and Nešlehová (2009)) and Liouville (see Belzile and Nešlehová (2017)). Such constructions have garnered significant interest as models suited for extreme values; they can offer the flexibility needed to model across extremal dependence classes as shown in Huser, Opitz and Thibaud (2017), Wadsworth et al. (2017) and Huser and Wadsworth (2019). Engelke, Opitz and Wadsworth (2019) offer an extensive study of the extremal behavior of bivariate pseudo-polar vectors. As shown in Charpentier et al. (2014), Archimax copulas also allow a representation of the form ; the interpretation proposed by Chatelain, Fougères and Nešlehová (2020) is that of a radial variable distorting the vector characterized by a stdf and therefore representing the extremal regime. The aim of this paper is to propose a dependence model in a way that its higher-dimensional margins are Archimax copulas but with possibly different distortions or stdfs. There is also a connection to be made with Hofert, Huser and Prasad (2018) which have extended the class of Archimax copulas with completely monotone Archimedean generators to hierarchical constructions. Therein, hierarchies can be introduced either via the frailties or stdfs, but the extremal behavior is not elicited.

In this paper, we define the new class of clustered Archimax copulas. Building a model from this family is straightforward as it only requires specifying the Archimax clusters and the dependence between the radial variables . Under non-restrictive assumptions, the extremal behavior of the clustered Archimax copula is obtained and shown to be quite flexible. We find that different choices of popular Archimedean generators coupled with dependence models on the radial variables lead to various regimes falling under either asymptotic dependence or independence between clusters. Meanwhile, each Archimax cluster retains its flexibility in the extreme dependence regime. We also propose inference techniques to fit clustered Archimax copulas to data and illustrate with a data application on rainfall in France.

The paper is organized as follows. Section 2 contains preliminary notions; Section 4 defines the model; Section 4 presents results on its extremal behavior; Section 5 provides illustrative examples; Section 6 covers inference techniques; Section 7 contains the data application; finally, Section 8 concludes the paper with a discussion. Proofs are reported in Appendix A, while Appendix C formulates a conjecture extending Theorem 4.1.

2 Preliminaries

Copulas contain all the information pertaining to the dependence between the components of continuous random vectors. The decomposition of Sklar (1959) links the marginals and the joint distribution of a random random vector via a copula, which is simply a distribution function on the unit hypercube with standard uniform margins. Consider with margins . Then there exists a copula such that for any ,

Moreover, is unique if the margins are all continuous. There is also a version of Sklar’s decomposition for survival functions. That is, given the marginal survival functions and the joint marginal function , there exists a copula , called a survival copula of , such that for all ,

It can be shown that if , then (see Nelsen (2006)). There is a large amount of literature on dependence modeling via copulas; we refer to the monographs of Nelsen (2006), Durante and Sempi (2010) and Joe (2015).

One particular family of copulas, called Archimax, was introduced in two dimensions by Capéraà, Fougères and Genest (2000), and extended to arbitrary dimensions by Mesiar and Jágr (2013) and Charpentier et al. (2014). Generalizing both Archimedean and extreme-value copula families, Archimax copulas take the form, for all ,

| (2.1) |

where is an Archimedean generator with inverse and is a stdf. These two functional parameters are defined below.

Definition 2.1.

A non-increasing and continuous function which satisfies , and is strictly decreasing on , where , is called an Archimedean generator.

A function is called a -variate stable tail dependence function (stdf) if there exists a finite measure on the -dimensional unit simplex satisfying for all , such that for all ,

A -dimensional copula is called Archimax if it permits the representation (2.1) for some -variate stdf and an Archimedean generator with inverse , where by convention and .

In the special case when , one has that reduces to the extreme value copula with stdf defined for all by

Stable tail dependence functions were introduced by Huang (1992) and are given a characterization by Ressel (2013) in terms of homogeneity, convexity and boundary properties. In this paper, the -norm representation of stdfs is particularly useful. The following characterization, as discussed in Aulbach, Falk and Zott (2015), can be traced back to the work of Pickands (1975), de Haan and Resnick (1977), and Vatan (1985) on the representation of standard max-stable processes. Any -dimensional stdf can be written, for , as

| (2.2) |

for some positive random variables with unit mean. When , i.e., the stdf corresponding to asymptotic independence, then is simply an Archimedean copula given for all by

Conditions on for to be a copula were explored in McNeil and Nešlehová (2009), while conditions for and for (2.1) to be a copula were explored in Charpentier et al. (2014).

Archimax copulas also admit a stochastic representation, which this paper builds upon. Theorem 3.3 of Charpentier et al. (2014) states under conditions on and , that is the survival copula of a random vector

| (2.3) |

where is a positive random variable independent of . The distribution of is linked to the Archimedean generator via the Williamson- transform, i.e. and . We refer to McNeil and Nešlehová (2009) and Larsson and Nešlehová (2011) for more details. The survival function of is given, for any , by

| (2.4) |

Note in particular that the margins of are Beta. Specifically, for all . We interpret (2.3) as a dependence structure defined by a distortion (or radial) random variable applied to the extremal component .

Archimax copulas have a given extreme-value attractor, which motivates their use to model pre-extreme dependence. Recall that a function is regularly varying with index if and only if for all , as , denoted . When for , it is shown in Proposition 6.1 of Charpentier et al. (2014) that is in the maximum domain of attraction of the extreme-value copula , i.e., for any ,

| (2.5) |

where for any , . It is apparent that the Archimax family is fully flexible in the asymptotic regime, meaning that any extreme-value copula corresponds to a subclass of Archimax copulas that will be attracted to it.

3 Model specification and notation

As a first step towards the specification of clustered Archimax copulas, we need to introduce the notion of clusters to the random vector . To that end, let be a partition of into disjoint sets. Because the stochastic representation (2.3) only makes sense in dimensions two and higher, we shall require, throughout this paper, that for all . Note that singleton clusters could be included, but this would require more tedious notation. In this setup, and of course also . For convenience, we treat the subsets as ordered sets. This allows us to refer to the subvector of associated with the th cluster as or, in shorter notation, .

As we shall see shortly, a clustered Archimax copula is defined through a partition as well as stdfs and distortion variables. To ease the reading, we will use the notation and , where for each , is a -variate stdf and is a -monotone Archimedean generator, i.e., differentiable up to order with derivatives satisfying for all for and further is nonincreasing and convex on .

Definition 3.1.

A -variate copula is called clustered Archimax copula with cluster partition , stdfs , Archimedean generators respectively -monotone, and copula that we term the radial copula, if it is the survival copula of a random vector that satisfies the following:

-

(i)

For each , for some -dimensional random vector with survival function as in (2.4) and random variable is distributed as the inverse Williamson -transform of .

-

(ii)

The random vectors are mutually independent.

-

(iii)

The random vector is independent of and has copula .

Note that by Sklar’s Theorem, the joint distribution of in Definition 3.1 is fully determined by its copula and marginal distributions that are the inverse Williamson- transforms of .

In more explicit notation, Definition 3.1 states that, upon re-indexing so that is contiguous with ordered subsets, any clustered Archimax random vector admits the representation

| (3.1) |

As the name suggests, certain multivariate margins of a clustered Archimax copula are Archimax. Specifically, Theorem 3.3 of Charpentier et al. (2014) ensures that for each , the survival copula of is the -dimensional Archimax copula . In particular, in the boundary case when , the entire copula is Archimax. It also follows from the proof of the latter theorem that the survival copula of in (3.1) is the distribution function of

| (3.2) |

Throughout the paper, for each , we let be the vector that contains the components of corresponding to cluster . In particular, when is as in (3.1), then . Furthermore, analogously to and , for any vector and all , we denote by the subvector of associated with the th cluster . Accordingly, for all and , we use , and to denote the th entry of , and , respectively. Finally, unless otherwise stated, all operations involving one- and multi-dimensional vectors (random or not) should be understood as componentwise, e.g., for , .

4 Extremal properties

In this section, we investigate the extremal behavior of a clustered Archimax copula . The main result, Theorem 4.1 below, delineates the conditions under which is in a copula domain of attraction of some extreme-value copula and identifies the latter. Since the survival copula of in (3.1) is also the copula of , we will study the extremal behavior of .

The distortion vector has an effect on both inter- and intra-cluster dependence at extreme levels. Its extreme behavior is important, so it is natural to make the following two assumptions. The first concerns the properties of the margins of . Recall that a univariate random variable with distribution is in the maximum domain of attraction of a non-degenerate distribution , denoted or iff there exist sequences , such that, for any , as . Moreover, the Fisher-Tippett Theorem states that , up to location and scale, is either Fréchet (), Gumbel () or Weibull () with .

Assumption 4.1.

For a clustered Archimax copula as in Definition 3.1, assume that is the union of disjoint sets and , such that

-

(i)

if and only if for some .

-

(ii)

if and only if there exists an such that .

While the two cases above cover most widely considered Archimedean generators, we do conjecture an extension in Appendix C.1 that includes the boundary case and . If Assumption 4.1 holds, means that is heavy-tailed and this occurs if and only if , as shown in Theorem 2 in Larsson and Nešlehová (2011). In contrast, implies that by Proposition 2 in Belzile and Nešlehová (2017). By the same proposition, one then has that for and and for and . This means that under Assumption 4.1, the respective clustered Archimax copula is in the copula domain of attraction of an extreme-value copula if and only if is in the maximum domain of attraction of an extreme-value distribution with copula . Such a domain of attraction result requires further assumptions on the extremal behavior of the entire vector .

Assumption 4.2.

For a clustered Archimax copula as in Definition 3.1, assume that the reciprocal distortion vector is in the maximum domain of attraction of a multivariate extreme-value distribution with stdf given, for , by

for some positive random variables with unit mean.

It will become apparent in the next result that the choice of the aforementioned -norm representations for stdfs is convenient in this context. We are now in position to formulate the main result of this section.

Theorem 4.1.

Inter-cluster asymptotic independence can also be achieved if the distortions are asymptotically independent, as shown in the following corollary.

Corollary 4.1.

If are asymptotically independent, then for , the limiting stdf in (4.1) simplifies to

Remark 4.1.

Note that under the hypothesis of Theorem 4.1, the asymptotic behavior of has no influence on the form of .

The following corollary to Theorem 4.1 compares the inter-cluster stdf to that of the reciprocal distortions .

Corollary 4.2.

Under the hypothesis of Theorem 4.1, let . Then, for all and such that and for all ,

Remark 4.2.

It is worth noting that (4.1) elicits a new method to combine different stdfs in a non-trivial way. Since the second component of (4.1) does not reveal any new combination of stdfs, suppose for now that . For a given , we then automatically have that . Setting for all and all recovers the marginal stdf of the cluster . This marginal stdf is equal to

for , which itself is equal to by Proposition (6.1) of Charpentier et al. (2014). In the bivariate case, the form above is a special case of (7) in Engelke, Opitz and Wadsworth (2019). The attractor of the bivariate Archimax copula is in particular obtained as a special case of their Proposition 1 and Equation (6), see Sections 2.1 and 4 therein. The complete stdf, defined for all , by

essentially mixes the marginal cluster stdfs with the limiting stdf of . Simply put, Corollary 4.2 shows that this mixing results in a weaker asymptotic dependence between clusters than that of the reciprocal distortions , characterized by .

5 Insights into modeling

In this section, we provide examples of parametric families that can be used to construct clustered Archimax copulas. Simulating from single Archimax copulas has recently garnered attention, as methods have been advanced by Mai (2022) and Ng, Hasan and Tarokh (2022). Due to the popularity of Archimedean copulas, there is a wide array of parametric families for the distortions to choose from. When is -times differentiable, its inverse Williamson -transform has the density, given, for , by

viz. Eq. (2) in McNeil and Nešlehová (2010).

Example 5.1 (Clayton Generator).

Using the inverse Williamson -transform, one can obtain the distribution of in the case when is Clayton with parameter . In the Clayton case, as seen in McNeil and Nešlehová (2009), one has for ,

We can see that for any and ,

Thus if the -th cluster has a Clayton distortion, then its components are asymptotically independent from all other clusters since in Theorem 4.1.

Example 5.2 (Joe generator).

We now present synthetic examples of clustered Archimax copula based on the families presented above. By virtue of being constructed via the stochastic representation in Equation (3.2), random number generation from this model is straightforward. Recall that we do not require complete monotonicity of the Archimedean generators and therefore rely on the radial representation in Equation (2.3). Our simulation algorithm is a simple extension of Algorithm 4.2 in Charpentier et al. (2014). The R code to generate the samples is provided in the supplementary materials.

Algorithm 5.1.

Let be as in Definition 3.1. To simulate an observation from ,

-

1.

Simulate a vector . This can be done by simulating a vector and applying the transformations for each . Following McNeil and Nešlehová (2009), for ,

where is the right-hand derivative of .

-

2.

For each , generate an observation whose survival function is given, for any , by

-

3.

Construct by setting .

Remark 5.1.

In fact, the dependence structure of the distortions does not need to be defined via a copula, as long as it can be simulated from.

In order to illustrate the findings of Section 4, we use Algorithm 5.1 to generate samples from two clustered Archimax copulas, Model A and Model B described in Table 5.1; they differ only in the choice of their radial copula . In both cases, three trivariate Archimax copulas representing three clusters are combined to form a -dimensional dependence structure. The first cluster is defined by a Clayton-Gumbel Archimax copula, while the other two are defined by Joe-Gumbel Archimax copulas. The partition of is . Assumption 4.1 holds with and . Figures D.1 and D.2 in Appendix D represent samples drawn from Model A and B. It is clearly visible when comparing the off-diagonal 3-by-3 blocks that both models have the same intra-cluster dependence while having different inter-cluster dependence.

| Model A | Model B | |

|---|---|---|

| Radial (survival) copula | Gaussian, | Gumbel, |

| Radial extremal behavior | Asymptotic independence | Asymptotic dependence |

| specification | : Logistic, : Logistic, : Logistic, | : Logistic, : Logistic, : Logistic, |

| specification | : Clayton, : Joe, : Joe, | : Clayton, : Joe, : Joe, |

| Intra-cluster extremal dependence | Cluster 1: Asymptotic dependence Cluster 2: Asymptotic dependence Cluster 3: Asymptotic dependence | Cluster 1: Asymptotic dependence Cluster 2: Asymptotic dependence Cluster 3: Asymptotic dependence |

| Inter-cluster extremal dependence | Clusters 1-2: Asymptotic independence Clusters 1-3: Asymptotic independence Clusters 2-3: Asymptotic independence | Clusters 1-2: Asymptotic independence Clusters 1-3: Asymptotic independence Cluster 2-3: Asymptotic dependence |

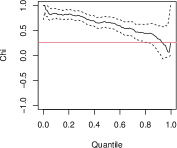

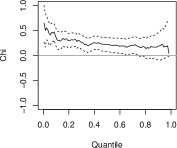

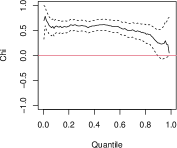

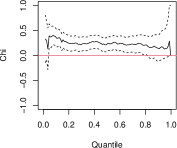

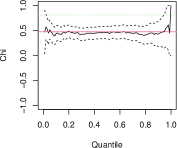

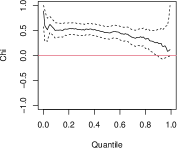

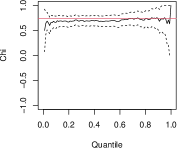

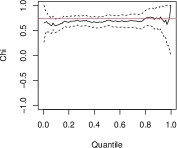

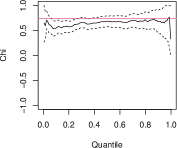

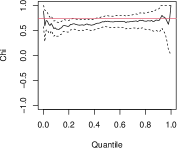

For both samples, we produce chi plots to represent extremal intra and inter-cluster dependence. Out of the 36 possible variable pairs, we chose 6 to cover all pairings of clusters . Figure 5.1 displays those of variables (intra-cluster ), (inter-cluster ) and (inter-cluster ). Figure D.3 in Appendix D pertains to the remaining three cluster pairings. Following Coles, Heffernan and Tawn (1999), for the pair , the quantity of interest is given, for , by

| (5.1) |

The well-known upper tail dependence coefficient of Joe (2015) is then simply expressed

| (5.2) |

provided the limit exists. For each , the values of are in fact equal for all and due to the fact that the logistic stdf is symmetric with respect to permutation of its arguments. Therefore, for each , we can simplify the notation by having with any such that . Both samples exhibit the same intra-cluster extreme dependence, with for the first cluster (see Figures 5.1 (a) and (b)), (see Figures D.3 (c) and (d)) for the second cluster and (see Figures D.3 (e) and (f)) for the third cluster. Note that the pairs , were chosen to be different while resulting in the same upper tail dependence coefficient. These values are the same within each cluster because was chosen to be exchangeable for each . The upper tail dependence coefficient of any bivariate copula in the domain of attraction of an extreme-value copula can be shown to be . We therefore obtain the true values of via (2.5), noting that the index of regular variation is equal to for any Clayton generator and equal to for any Joe generator .

Now, for and , let where and . As for the intra-cluster extreme dependence, this simplified notation is possible due to the fact that given a pair and , all values of such that and are equal. In Figures 5.1 (c) and (d) and D.3 (a) and (b), we have . As explained in Example 5.1, the choice of a Clayton generator forces cluster 1 to be asymptotically independent from clusters 2 and 3. In Figure 5.1 (e) we have . This is due to the fact that the Gaussian copula used to model the dependence between distortions forces asymptotic independence between clusters; see Example 4.1. However, Figure 5.1 (f) shows asymptotic dependence between clusters 2 and 3, i.e. . The value, approximately equal to , was obtained numerically by simulating from (4.1). Corollary 4.2 is illustrated by the fact that is lower than the upper tail dependence coefficient of .

6 Inference when is known

We first discuss inference for clustered Archimax copulas when the partition is known or hypothesized. In some cases, such as a portfolio containing stocks from distinct industries, this partition can be inherent to the dataset. When is unknown, one can employ clustering algorithms as discussed in Section 7.

From now on, let denote the -dimensional, continuous random vector of interest, whose underlying copula is clustered Archimax. For and let denote the distribution function of , recalling that by definition, and let be the -dimensional copula realization associated with , i.e., and has distribution . Finally, suppose that we observe a sample of i.i.d. replicates of with corresponding (unobserved) copula realizations .

Theorem 3.3 of Charpentier et al. (2014) implies that there exists a stochastic representation similar to (3.1) for the copula . We will lean on this representation to propose a method for inferring from . Given , we perform inference for , and separately. To ease the reading, we denote by the set

| (6.1) |

throughout the section, as well as in Appendix B. In Section 6.1, we briefly review how each individual cluster can be modeled using existing inference techniques for Archimax copulas. In Section 7.3, we propose a method for estimating the dependence between clusters.

6.1 Individual cluster inference

This section pertains to the estimation of each marginal Archimax copulas of the clustered Archimax copula . As such, inference methods have already been developed in Chatelain, Fougères and Nešlehová (2020) and more recently in Ng, Hasan and Tarokh (2022).

6.1.1 Estimating

We use a parametric approach to estimate the generators , which requires selecting a (possibly different) parametric family for each generator. Certain properties observed in the data can guide the user to specific choices of generators. For example, the presence of within-cluster lower tail dependence warrants the use of a Clayton generator. However, as explained in Example 5.1, this choice implies the asymptotic independence of and for all with . This consequence is desirable when studying the precipitation data in Section 7, but would not be appropriate, for instance, when modeling temperatures over the same region; see Davison, Huser and Thibaud (2013) for more details.

Once the parametric family of each generator is chosen, the parameters of remain to be estimated. For a given , our estimator of relies on the following remark.

Remark 6.1.

Any margin of an Archimax copula is itself Archimax with the same generator. In particular, for all , with as in (6.1), the distortions parameters and associated with and , respectively, are identical, i.e., .

Remark 6.1 suggests that for each , an estimator of also estimates . In view of this, we estimate by given, for and , by

| (6.2) |

where, for any , is the estimator defined in Section 7 of Chatelain, Fougères and Nešlehová (2020). These latter authors discuss the cases when the underlying generator is of the Clayton, Genest-Ghoudi, Frank or Joe families.

Remark 6.1 also suggests a simple way of assessing whether the partition is appropriate: if the underlying distribution is indeed a clustered Archimax with partition , then the hypothesis that for all must necessarily hold. We propose to test using the statistic given by

| (6.3) |

Although its definition involves three indices, we treat as a vector of dimension ; the specific ordering of its entries does not matter, as long as it is kept fixed. Because we expect that departures from the null will cause certain entries of to be large in absolute values, we test using either the supremum norm or the (squared) Euclidean norm of ; see Perreault, Nešlehová and Duchesne (2022) for similar hypothesis tests, albeit in a nonparametric context.

To derive the null distribution of , where is either the supremum or Euclidean norm, we exploit the fact that for any , is a function of two U-statistics with square integrable kernels (Chatelain, Fougères and Nešlehová, 2020, Section 7). Consequently, for any , is a function of several such U-statistics. Standard results about U-statistics (Hoeffding, 1948) and the delta method then imply that, under the null, is asymptotically Normal as , i.e., for some positive definite matrix of appropriate dimensions. In view of Slutsky’s Lemma and the Continuous Mapping Theorem, a test of approximate level then consists in rejecting whenever , where for some consistent estimator of . In the data application of Section 7, we use a jackknife estimator of derived from Section 2(c) of Arvesen (1969); see Appendix B for the implementation details.

6.1.2 Estimating

To estimate the stdfs , we exploit the fact that for any and , , where is the Pickands dependence function associated to . Specifically, we replace in this latter equation by its CFG-type estimator (Capéraà, Fougères and Genest, 1997), defined as follows. For , let be such that, for all and ,

| (6.4) |

where is the rank of among . Now, for with as in Definition 2.1, let

Then, for all and , the (endpoint-corrected) CFG-type estimator of is given by

| (6.5) |

We refer the reader to Section 3 of Chatelain, Fougères and Nešlehová (2020) for more details about the CFG-type estimator, as well as an alternative estimator based on that of Pickands (1981). The asymptotic behavior of the CFG and Pickands-type estimators is established under regularity conditions on both and ; see Section 4 in Chatelain, Fougères and Nešlehová (2020).

6.2 Inference for the dependence between distortions

To model the dependence between the components of , we suggest a parametric approach on the underlying copula . To this end, we make the assumption that belongs to a parametric family of -dimensional copulas, where the parameter space is of arbitrary dimension. We further assume the existence of a multivariate density for in order to proceed with a likelihood-based method. While we cannot observe directly, we may still derive the corresponding likelihood based on pseudo-observations.

We follow (3.2) and define the -dimensional random vector , for all and , by , so that has distribution . Now, fix and note that since for each , the density of the subvector of can be expressed, for , as

| (6.6) |

where and, for , is a density. Also note that, due to Sklar’s Theorem, the joint density of can be written, for and the copula density of , as

| (6.7) |

Now, let and recall that , , and are equal in distribution. The pseudo-copula observations can be plugged into the (pseudo) composite marginal log-likelihood (Varin, Reid and Firth, 2011) associated with the density of and given by

| (6.8) |

Due to the multi-dimensional integral in the expression of and the possibly large cardinality of , (6.8) will often be difficult to compute in practice. When the chosen parametric family for allows it, a natural approach for reducing the computational burden is to consider lower-dimensional margins to form the composite likelihood function. For example, when is a Gaussian copula, it seems reasonable to use the pairwise marginal likelihood

| (6.9) |

where , , and is the corresponding bivariate analogue of . For more details about composite likelihood estimation, we refer the reader to Cox and Reid (2004) and Varin, Reid and Firth (2011).

For some specific models, the similar yet simpler strategy underlying the estimation of in (6.2) can also be used. For example, let be a Gaussian copula with correlation matrix , so that is of length . For each with , one can first independently consider the bivariate log-likelihoods associated with in (6.9) to compute a set of pairwise parameters . These can then be averaged over to obtain a final estimate for . This is the approach we opt for in the application of Section 7.

Remark 6.2.

The composite log-likelihoods and in (6.8) and (6.9), respectively, depend on through in (6.7) (or its bivariate analogues in the case of ). The functions , and , , are assumed to be known. In practice, one can plug in the parametric estimates proposed in Section 6.1.1. While outside of the scope of this work, one could consider the feasibility of estimating the distortion parameters together with via pseudo-maximum composite likelihood.

7 Data illustration

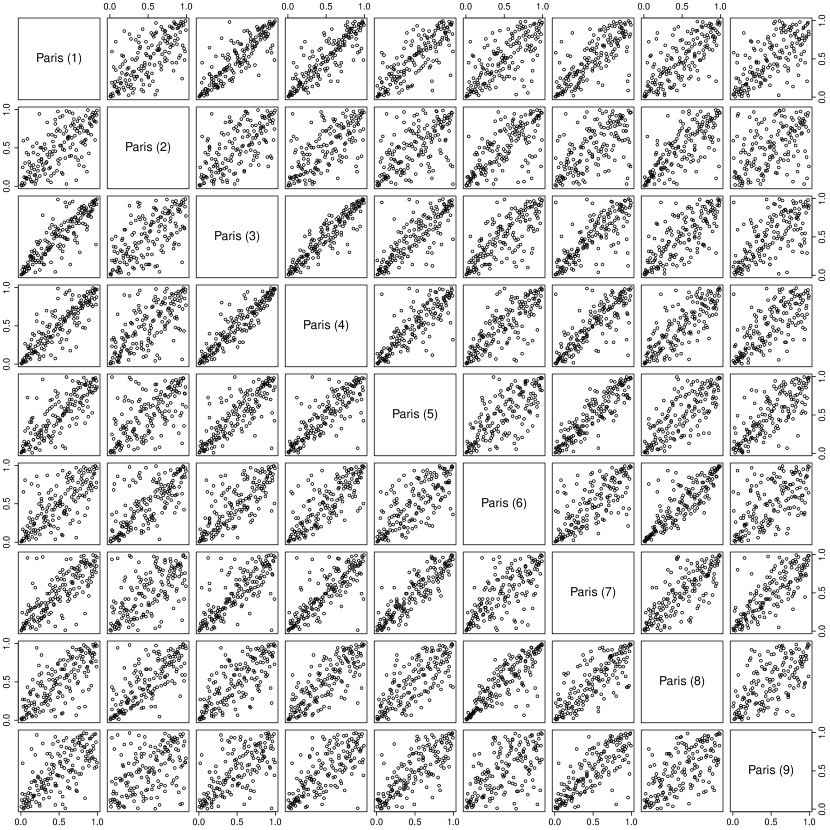

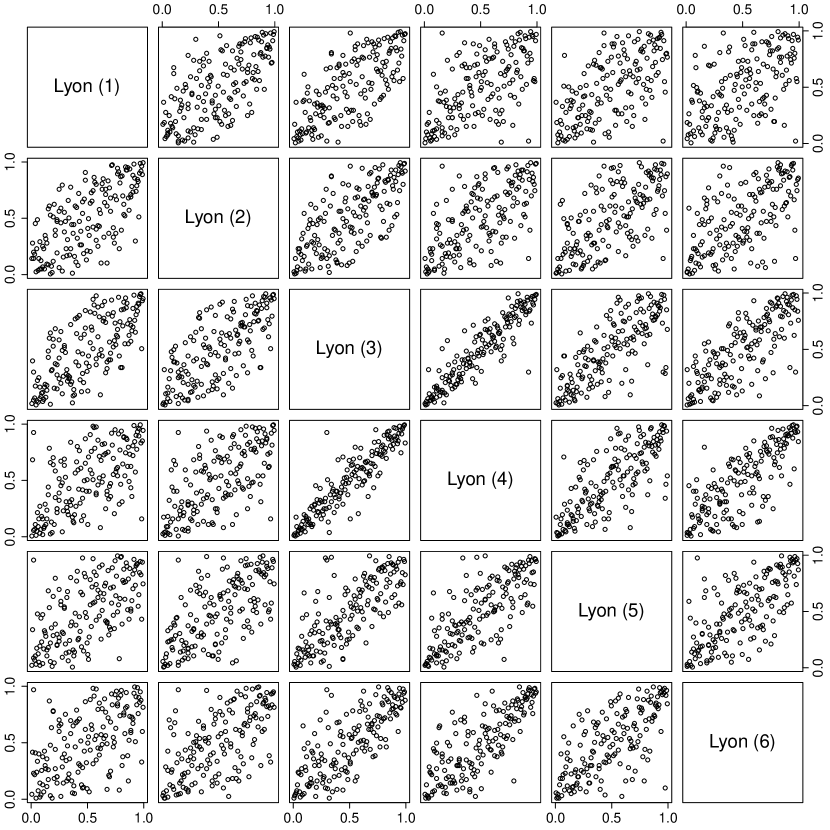

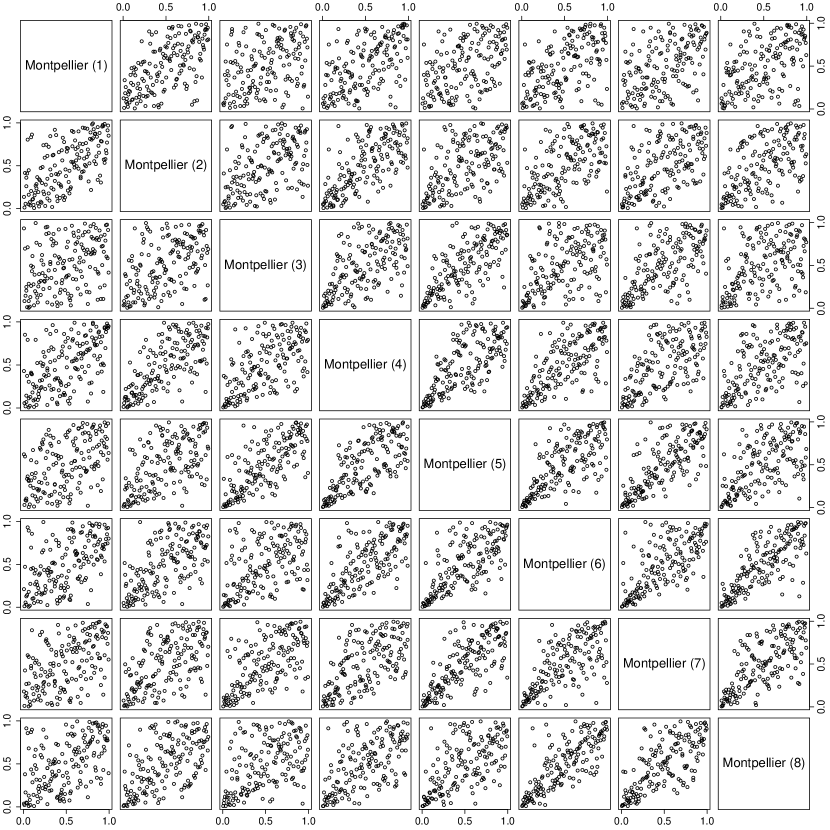

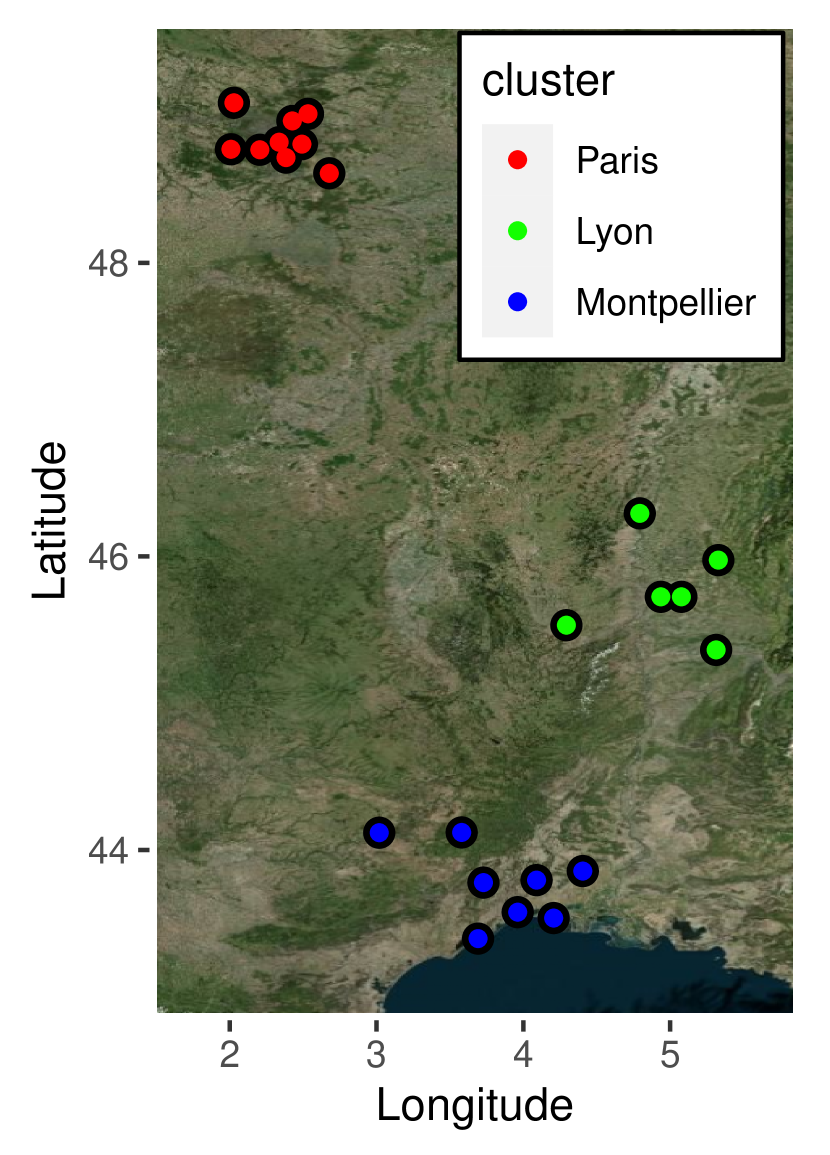

In this section, we illustrate the proposed methodology through an application to flood monitoring. The data, provided by Météo France, consists of daily precipitation amounts measured from 1976 to 2015, inclusively, at meteorological stations in France. As shown in Figure 7.1, the stations are agglomerated into three clusters centered around the cities of Paris (, 9 stations), Lyon (, 6 stations) and Montpellier (, 8 stations). We thus let be the partition underlying our model. When no such partition stems from the context of the application naturally, one can use the clustering techniques of, e.g., Bernard et al. (2013) or Saunders, Stephenson and Karoly (2021) to create a set of candidate partitions of distinct sizes. The number of clusters can then be settled heuristically with the help of standard clustering tools (e.g., a dendrogram), or by selecting the coarsest partition that yields a satisfactory fit.

Note that our application is purposely similar to that of Chatelain, Fougères and Nešlehová (2020), who fitted an Archimax copula to precipitation amounts (monthly maxima) measured at three nearby stations. The greater flexibility of clustered Archimax copulas allows us to increase the number of variables considered.

7.1 Data preprocessing

A preliminary analysis of the data reveals the presence of seasonality and temporal dependence within the univariate series. To mitigate the effect of seasonality, we consider only the observations from the months of September to December, inclusively, which encompass most of the extreme precipitation events. Since our primary focus is on extreme precipitations, we then take monthly maxima of the series, yielding a total of observations per station. The resulting series show no obvious sign of temporal dependence according to the Ljung-Box tests (Ljung and Box, 1978); note however that the asymptotic results of Chatelain, Fougères and Nešlehová (2020) upon which the present work relies hold for alpha-mixing sequences, meaning that temporal dependence vanishing with increasing lag is indeed allowed.

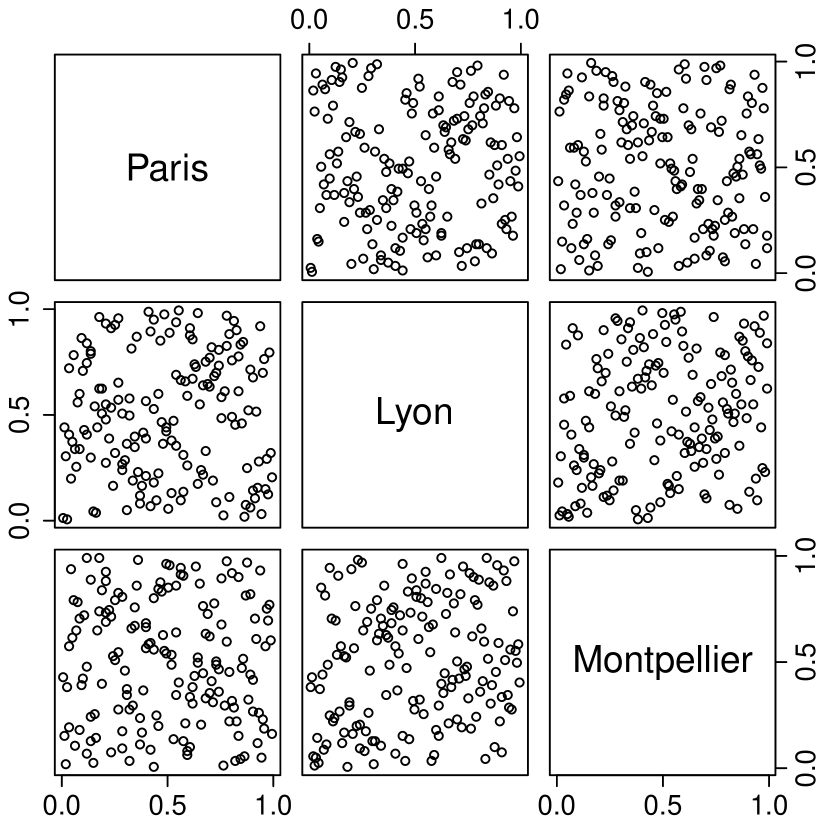

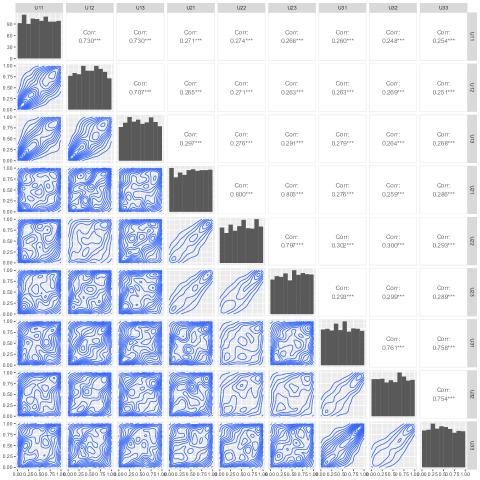

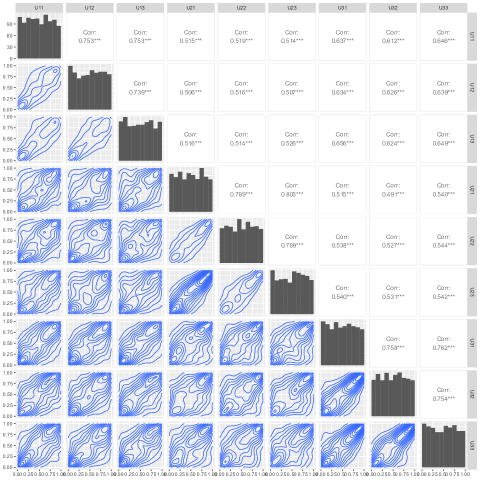

The pair plots of the scaled componentwise ranks of monthly maxima of precipitations involving only the most central station of each cluster are displayed in the right panel of Figure 7.1. They suggest a very weak dependence between precipitation maxima in Lyon and Montpellier, and an even weaker one, if at all, between any of these and the stations in Paris. In contrast, similar plots for all pairs of stations within the same cluster (Figures E.1–E.3) indicate much stronger dependencies. In these latter plots, we also note the presence of asymmetry; this is particularly pronounced in Figure E.1 (Paris).

As a final preliminary step, we used the procedure of Kojadinovic, Segers and Yan (2011) to test the hypothesis that the copula underlying each cluster of variables is an extreme-value copula. In all three cases, the test clearly rejects the hypothesis. This may be explained by the presence of masses of points near the bottom-left corner of many pair plots, combined with the fact that extreme-value distributions cannot allow lower-tail dependence. In contrast with extreme-value distributions, clustered Archimax copulas may indeed allow for both lower-tail and extremal dependence; in particular, letting be the Clayton generator leads to (pairwise) lower-tail dependence coefficients equal to , where is the Pickands dependence function characterizing the Archimax, as explained in Chatelain, Fougères and Nešlehová (2020).

7.2 Inference for and

The apparent lack of inter-cluster dependence in the right panel of Figure 7.1 and the presence of lower-tail dependence in the data suggest that the Clayton generators could be good candidates for modeling the distortions, as these would produce asymptotically independent clusters. We thus begin by formally testing whether defines three asymptotically independent clusters. To do so, we apply the test of independence for random vectors proposed by Kojadinovic and Holmes (2009). Because we are interested in asymptotic independence, we apply the test procedure not to our dataset of monthly maxima, but to the corresponding dataset of yearly maxima, which includes 40 observations per station; the corresponding matrix of empirical Kendall’s correlations is depicted in the left panel of Figure E.4 in the Appendix. The test yields a p-value of 0.16 for the global hypothesis of independence between the three clusters and a p-value above 0.35 for each of the three hypotheses of pairwise independence. Although the fact that only observations are available might arguably yield a test with limited power, we move on with our analysis assuming that the clusters are asymptotically independent and that Clayton generators are reasonable choices.

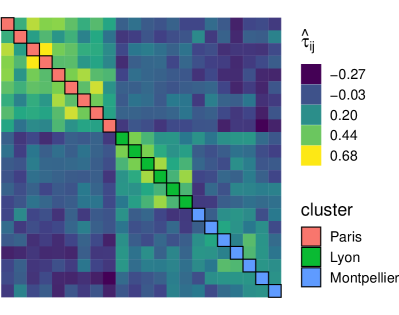

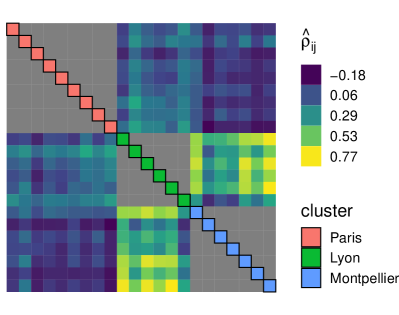

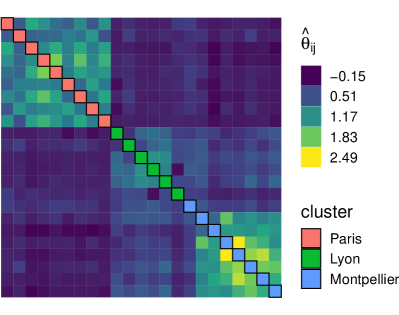

The next step is to estimate the parameters , and of the three Clayton generators. This involves computing, for each , the pairwise estimates ; these are gathered in a matrix illustrated in the left panel of Figure 7.2. The resulting distortion estimates, defined in (6.2), are (Paris), (Lyon) and (Montpellier), suggesting that the hypothesis of different distortions affecting the three clusters is reasonable.

At this point, one can already suspect a problem with the Montpellier cluster, as there seems to be strong discrepancies among the entries of its corresponding matrix in the left panel of Figure 7.2, violating the statement in Remark 6.1. To check this more formally, we perform the test described in Section 6.1.1 for the hypothesis that for all and such that . While the version of the test based on the supremum norm yields an acceptable p-value (approximately ), the version based on the Euclidean norm yields an approximate p-value of , thus rejecting at nominal level . Three similar cluster-specific tests, each involving only the pairwise distortion estimates from a single cluster, indeed reveal an anomaly with Montpellier; its corresponding approximate p-values are (supremum norm) and (Euclidean norm). A last series of entry-specific tests, each involving a single pairwise distortion estimate from the Montpellier cluster, strongly suggests that one particular station, the west-most station of the cluster, is at the root of the rejection. Concretely, the p-values associated with this latter station are below the nominal level 0.05, with most of them being smaller than . From the left panel of Figure 7.1, one can see that it effectively appears isolated from the other stations of the Montpellier cluster, as it is located on the other side of the Cévennes montain range. Removing its corresponding column from the data yields a new distortion parameter for the Montpellier cluster, as well as satisfactory p-values for the tests of and the preceeding test of asymptotic independence. We thus remove the problematic station from the data and redefine to be the ensuing partition of , assuming that the variables were re-indexed. Similarly, we now use to refer to the estimate of computed without the problematic station.

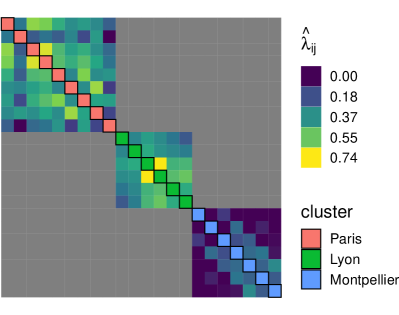

Given the new partition , we then construct, for each , the semi-parametric estimate of the stdf based on defined in (6.5). Note that for the estimated values of , Conditions 4.1 and 4.2 in Chatelain, Fougères and Nešlehová (2020) used for convergence of are met. To better visualize the strength of the dependence between stations of the same cluster, we also computed, for each and all such that , pairwise estimates of the upper tail dependence coefficients defined in (5.2). To this end, we note that when Clayton generators are used, in (2.5) and the estimator in (6.5) can be slightly modified to obtain an estimator of as follows. Recall the definition of in (6.1). For all , let , where has only two non-zero entries, those associated with the th and th stations, equal to one. Then, for any , one can estimate combining the identities and . Because the bivariate margins of an Archimax copula are also Archimax (Remark 6.1), we get that with . This leads to an estimator of given by . The resulting estimates are shown in the right panel of Figure 7.2. Although this is not required, we expect many of these estimates to be large; this is clearly the case for the Paris and Lyon clusters, and still true, perhaps to a lesser extent, for the Montpellier cluster.

7.3 Inference for

To capture the dependence between the components of , we suppose that their copula belongs to the family of Gaussian copulas with correlation parameters , which we estimate by , as defined at the end of Section 6.2. The resulting estimates are given by for the Paris-Lyon pair, for the Paris-Montpellier pair and for Lyon-Montpellier pair; their corresponding pairwise estimates, denoted in Section 6.2, are shown in the right panel of Figure E.4 in the Appendix. The results suggest in particular that the clusters centered around Paris and Montpellier are nearly independent, which is coherent with the fact they are the most distant pair of clusters among the three.

This application to rainfall illustrates some of the strengths of clustered Archimax copulas. Namely, we are able to model the dependence of multi-dimensional data that consists of groups of variables which are asymptotically dependent. Within each cluster, dependence is modeled in a fully flexible way, allowing for asymmetry. Inter-cluster dependence is modeled more parsimoniously while maintaining the possibility for both asymptotic dependence and independence. Finally, the proposed copula family allows to fit data at a pre-asymptotic level while boasting flexibility at the extreme level.

8 Discussion

The clustered Archimax model studied in this paper is related to several other articles in the literature. Hierarchical constructions based on Archimax copulas were proposed by Hofert, Huser and Prasad (2018). Specifically, their construction is based on the frailty representation of Archimax copulas, which only holds for completely monotone generators. Hierarchies can be induced via the frailties, the stdf, or both. It would be interesting to establish the attractor of their proposed hierarchical Archimax copula and compare it to that of the clustered Archimax copula. The extremal dependence structure of Liouville copulas is established in Belzile and Nešlehová (2017). The stochastic representation of Liouville copulas is similar to that of Archimax copulas, as they are survival copulas of vectors of the form , with a nonnegative random variable and a Dirichlet random vector. The work presented in this paper differs from this by replacing the Dirichlet component by a vector characterized by an stdf and by allowing for multiple distorting random variables , thus inducing a hierarchy (or clustering). Finally, Engelke, Opitz and Wadsworth (2019) establish the extremal dependence of bivariate vectors of the form for an extensive combination of asymptotic behaviors of both and . The attractor of the bivariate Archimax copula is in particular obtained as a special case of their Proposition 1 and Equation (6), see Sections 2.1 and 4 therein.

References

- Arvesen (1969) {barticle}[author] \bauthor\bsnmArvesen, \bfnmJames N.\binitsJ. N. (\byear1969). \btitleJackknifing U-Statistics. \bjournalAnn. Math. Statist. \bvolume40 \bpages2076–2100. \endbibitem

- Aulbach, Falk and Zott (2015) {barticle}[author] \bauthor\bsnmAulbach, \bfnmStefan\binitsS., \bauthor\bsnmFalk, \bfnmMichael\binitsM. and \bauthor\bsnmZott, \bfnmMaximilian\binitsM. (\byear2015). \btitleThe space of -norms revisited. \bjournalExtremes \bvolume18 \bpages85–97. \bdoi10.1007/s10687-014-0204-y \endbibitem

- Belzile and Nešlehová (2017) {barticle}[author] \bauthor\bsnmBelzile, \bfnmLéo R.\binitsL. R. and \bauthor\bsnmNešlehová, \bfnmJohanna G.\binitsJ. G. (\byear2017). \btitleExtremal attractors of Liouville copulas. \bjournalJ. Multivariate Anal. \bvolume160 \bpages68–92. \bdoihttps://doi.org/10.1016/j.jmva.2017.05.008 \endbibitem

- Bernard et al. (2013) {barticle}[author] \bauthor\bsnmBernard, \bfnmElsa\binitsE., \bauthor\bsnmNaveau, \bfnmPhilippe\binitsP., \bauthor\bsnmVrac, \bfnmMathieu\binitsM. and \bauthor\bsnmMestre, \bfnmOlivier\binitsO. (\byear2013). \btitleClustering of maxima: Spatial dependencies among heavy rainfall in France. \bjournalJ. Clim. \bvolume26 \bpages7929–7937. \endbibitem

- Breiman (1965) {barticle}[author] \bauthor\bsnmBreiman, \bfnmL.\binitsL. (\byear1965). \btitleOn some limit theorems similar to the arc-sin law. \bjournalTeor. Verojatnost. i Primenen. \bvolume10 \bpages351–360. \endbibitem

- Capéraà, Fougères and Genest (1997) {barticle}[author] \bauthor\bsnmCapéraà, \bfnmP.\binitsP., \bauthor\bsnmFougères, \bfnmA. L.\binitsA. L. and \bauthor\bsnmGenest, \bfnmC.\binitsC. (\byear1997). \btitleA nonparametric estimation procedure for bivariate extreme value copulas. \bjournalBiometrika \bvolume84 \bpages567–577. \bdoi10.1093/biomet/84.3.567 \endbibitem

- Capéraà, Fougères and Genest (2000) {barticle}[author] \bauthor\bsnmCapéraà, \bfnmPhilippe\binitsP., \bauthor\bsnmFougères, \bfnmAnne-Laure\binitsA.-L. and \bauthor\bsnmGenest, \bfnmChristian\binitsC. (\byear2000). \btitleBivariate distributions with given extreme value attractor. \bjournalJ. Multivariate Anal. \bvolume72 \bpages30–49. \endbibitem

- Charpentier et al. (2014) {barticle}[author] \bauthor\bsnmCharpentier, \bfnmA.\binitsA., \bauthor\bsnmFougères, \bfnmAnne-Laure\binitsA.-L., \bauthor\bsnmGenest, \bfnmC.\binitsC. and \bauthor\bsnmNešlehová, \bfnmJ. G.\binitsJ. G. (\byear2014). \btitleMultivariate Archimax copulas. \bjournalJ. Multivariate Anal. \bvolume126 \bpages118–136. \endbibitem

- Chatelain, Fougères and Nešlehová (2020) {barticle}[author] \bauthor\bsnmChatelain, \bfnmSimon\binitsS., \bauthor\bsnmFougères, \bfnmAnne-Laure\binitsA.-L. and \bauthor\bsnmNešlehová, \bfnmJohanna G.\binitsJ. G. (\byear2020). \btitleInference for Archimax copulas. \bjournalAnn. Statist. \bvolume48 \bpages1025–1051. \bdoi10.1214/19-AOS1836 \endbibitem

- Coles, Heffernan and Tawn (1999) {barticle}[author] \bauthor\bsnmColes, \bfnmS.\binitsS., \bauthor\bsnmHeffernan, \bfnmJ.\binitsJ. and \bauthor\bsnmTawn, \bfnmJ.\binitsJ. (\byear1999). \btitleDependence measures for extreme value analyses. \bjournalExtremes \bvolume2 \bpages339–365. \endbibitem

- Cox and Reid (2004) {barticle}[author] \bauthor\bsnmCox, \bfnmD. R.\binitsD. R. and \bauthor\bsnmReid, \bfnmN.\binitsN. (\byear2004). \btitleA Note on Pseudolikelihood Constructed from Marginal Densities. \bjournalBiometrika \bvolume91 \bpages729–737. \endbibitem

- Davison, Huser and Thibaud (2013) {barticle}[author] \bauthor\bsnmDavison, \bfnmAnthony C\binitsA. C., \bauthor\bsnmHuser, \bfnmRaphaël\binitsR. and \bauthor\bsnmThibaud, \bfnmEmeric\binitsE. (\byear2013). \btitleGeostatistics of dependent and asymptotically independent extremes. \bjournalMathematical Geosciences \bvolume45 \bpages511–529. \endbibitem

- de Haan and Resnick (1977) {barticle}[author] \bauthor\bparticlede \bsnmHaan, \bfnmLaurens\binitsL. and \bauthor\bsnmResnick, \bfnmSidney I.\binitsS. I. (\byear1977). \btitleLimit theory for multivariate sample extremes. \bjournalZ. Wahrscheinlichkeitstheorie und Verw. Gebiete \bvolume40 \bpages317–337. \bdoi10.1007/BF00533086 \endbibitem

- Durante and Sempi (2010) {bbook}[author] \bauthor\bsnmDurante, \bfnmFabrizio\binitsF. and \bauthor\bsnmSempi, \bfnmCarlo\binitsC. (\byear2010). \btitleCopula theory: an introduction. \bpublisherSpringer. \endbibitem

- Embrechts and Goldie (1980) {barticle}[author] \bauthor\bsnmEmbrechts, \bfnmPaul\binitsP. and \bauthor\bsnmGoldie, \bfnmCharles M.\binitsC. M. (\byear1980). \btitleOn closure and factorization properties of subexponential and related distributions. \bjournalJ. Austral. Math. Soc. Ser. A \bvolume29 \bpages243–256. \endbibitem

- Embrechts, Klüppelberg and Mikosch (1997) {bbook}[author] \bauthor\bsnmEmbrechts, \bfnmPaul\binitsP., \bauthor\bsnmKlüppelberg, \bfnmClaudia\binitsC. and \bauthor\bsnmMikosch, \bfnmThomas\binitsT. (\byear1997). \btitleModelling Extremal Events for Insurance and Finance. \bpublisherSpringer, \baddressNew York. \endbibitem

- Engelke, Opitz and Wadsworth (2019) {barticle}[author] \bauthor\bsnmEngelke, \bfnmSebastian\binitsS., \bauthor\bsnmOpitz, \bfnmThomas\binitsT. and \bauthor\bsnmWadsworth, \bfnmJennifer\binitsJ. (\byear2019). \btitleExtremal dependence of random scale constructions. \bjournalExtremes \bvolume22 \bpages623–666. \endbibitem

- Fang, Kotz and Ng (1990) {bbook}[author] \bauthor\bsnmFang, \bfnmKT\binitsK., \bauthor\bsnmKotz, \bfnmS\binitsS. and \bauthor\bsnmNg, \bfnmKW\binitsK. (\byear1990). \btitleSymmetric Multivariate and Related Distributions. \bpublisherChapman & Hall/CRC. \endbibitem

- Ferreira and de Haan (2014) {barticle}[author] \bauthor\bsnmFerreira, \bfnmAna\binitsA. and \bauthor\bparticlede \bsnmHaan, \bfnmLaurens\binitsL. (\byear2014). \btitleThe generalized Pareto process; with a view towards application and simulation. \bjournalBernoulli \bvolume20 \bpages1717–1737. \bdoi10.3150/13-BEJ538 \endbibitem

- Fisher and Tippett (1928) {binproceedings}[author] \bauthor\bsnmFisher, \bfnmRonald Aylmer\binitsR. A. and \bauthor\bsnmTippett, \bfnmLeonard Henry Caleb\binitsL. H. C. (\byear1928). \btitleLimiting forms of the frequency distribution of the largest or smallest member of a sample. In \bbooktitleMath. Proc. Cambridge Philos. Soc. \bvolume24 \bpages180–190. \bpublisherCambridge University Press. \endbibitem

- Gnedenko (1943) {barticle}[author] \bauthor\bsnmGnedenko, \bfnmBoris\binitsB. (\byear1943). \btitleSur la distribution limite du terme maximum d’une série aléatoire. \bjournalAnn. Math. \bvolume44 \bpages423–453. \endbibitem

- Hoeffding (1948) {barticle}[author] \bauthor\bsnmHoeffding, \bfnmWassily\binitsW. (\byear1948). \btitleA class of statistics with asymptotically normal distribution. \bjournalAnn. Math. Statist. \bvolume19 \bpages293–325. \endbibitem

- Hofert, Huser and Prasad (2018) {barticle}[author] \bauthor\bsnmHofert, \bfnmMarius\binitsM., \bauthor\bsnmHuser, \bfnmRaphaël\binitsR. and \bauthor\bsnmPrasad, \bfnmAvinash\binitsA. (\byear2018). \btitleHierarchical Archimax copulas. \bjournalJ. Multivariate Anal. \bvolume167 \bpages195–211. \bdoi10.1016/j.jmva.2018.05.001 \endbibitem

- Huang (1992) {bphdthesis}[author] \bauthor\bsnmHuang, \bfnmXin\binitsX. (\byear1992). \btitleStatistics of bivariate extreme values, \btypePhD thesis, \bpublisherErasmus universiteit, Rotterdam. \endbibitem

- Huser, Opitz and Thibaud (2017) {barticle}[author] \bauthor\bsnmHuser, \bfnmRaphaël\binitsR., \bauthor\bsnmOpitz, \bfnmThomas\binitsT. and \bauthor\bsnmThibaud, \bfnmEmeric\binitsE. (\byear2017). \btitleBridging asymptotic independence and dependence in spatial extremes using Gaussian scale mixtures. \bjournalSpat. Stat. \bvolume21 \bpages166–186. \endbibitem

- Huser and Wadsworth (2019) {barticle}[author] \bauthor\bsnmHuser, \bfnmRaphaël\binitsR. and \bauthor\bsnmWadsworth, \bfnmJennifer L.\binitsJ. L. (\byear2019). \btitleModeling Spatial Processes with Unknown Extremal Dependence Class. \bjournalJ. Amer. Statist. Assoc. \bvolume114 \bpages434–444. \bdoi10.1080/01621459.2017.1411813 \endbibitem

- Joe (2015) {bbook}[author] \bauthor\bsnmJoe, \bfnmHarry\binitsH. (\byear2015). \btitleDependence Modeling With Copulas. \bpublisherCRC Press. \endbibitem

- Kallenberg (2002) {bbook}[author] \bauthor\bsnmKallenberg, \bfnmOlav\binitsO. (\byear2002). \btitleFoundations of Modern Probability, \bedition2nd ed. \bpublisherSpringer. \bdoi10.1007/978-1-4757-4015-8 \endbibitem

- Kojadinovic and Holmes (2009) {barticle}[author] \bauthor\bsnmKojadinovic, \bfnmIvan\binitsI. and \bauthor\bsnmHolmes, \bfnmMark\binitsM. (\byear2009). \btitleTests of independence among continuous random vectors based on Cramér–von Mises functionals of the empirical copula process. \bjournalJ. Multivariate Anal. \bvolume100 \bpages1137–1154. \bdoihttps://doi.org/10.1016/j.jmva.2008.10.013 \endbibitem

- Kojadinovic, Segers and Yan (2011) {barticle}[author] \bauthor\bsnmKojadinovic, \bfnmI.\binitsI., \bauthor\bsnmSegers, \bfnmJ.\binitsJ. and \bauthor\bsnmYan, \bfnmJ.\binitsJ. (\byear2011). \btitleLarge-sample tests of extreme-value dependence for multivariate copulas. \bjournalCanad. J. Statist. \bvolume39 \bpages703–720. \endbibitem

- Larsson and Nešlehová (2011) {barticle}[author] \bauthor\bsnmLarsson, \bfnmMartin\binitsM. and \bauthor\bsnmNešlehová, \bfnmJohanna\binitsJ. (\byear2011). \btitleExtremal behavior of Archimedean copulas. \bjournalAdv. in Appl. Probab. \bvolume43 \bpages195–216. \endbibitem

- Ljung and Box (1978) {barticle}[author] \bauthor\bsnmLjung, \bfnmG. M.\binitsG. M. and \bauthor\bsnmBox, \bfnmG. E. P.\binitsG. E. P. (\byear1978). \btitleOn a measure of lack of fit in time series models. \bjournalBiometrika \bvolume65 \bpages297–303. \bdoi10.1093/biomet/65.2.297 \endbibitem

- Mai (2022) {barticle}[author] \bauthor\bsnmMai, \bfnmJan-Frederik\binitsJ.-F. (\byear2022). \btitleAbout the exact simulation of bivariate (reciprocal) Archimax copulas. \bjournalDepend. Model. \bvolume10 \bpages29–47. \endbibitem

- McNeil and Nešlehová (2009) {barticle}[author] \bauthor\bsnmMcNeil, \bfnmAlexander J.\binitsA. J. and \bauthor\bsnmNešlehová, \bfnmJohanna\binitsJ. (\byear2009). \btitleMultivariate Archimedean copulas, -monotone functions and -norm symmetric distributions. \bjournalAnn. Statist. \bvolume37 \bpages3059–3097. \endbibitem

- McNeil and Nešlehová (2010) {barticle}[author] \bauthor\bsnmMcNeil, \bfnmAlexander J.\binitsA. J. and \bauthor\bsnmNešlehová, \bfnmJohanna\binitsJ. (\byear2010). \btitleFrom Archimedean to Liouville copulas. \bjournalJ. Multivariate Anal. \bvolume101 \bpages1772–1790. \bdoi10.1016/j.jmva.2010.03.015 \endbibitem

- Mesiar and Jágr (2013) {barticle}[author] \bauthor\bsnmMesiar, \bfnmRadko\binitsR. and \bauthor\bsnmJágr, \bfnmVladimír\binitsV. (\byear2013). \btitle-dimensional dependence functions and Archimax copulas. \bjournalFuzzy Sets Syst. \bvolume228 \bpages78–87. \endbibitem

- Nelsen (2006) {bbook}[author] \bauthor\bsnmNelsen, \bfnmRoger B.\binitsR. B. (\byear2006). \btitleAn Introduction to Copulas, \bedition2nd ed. \bpublisherSpringer. \endbibitem

- Ng, Hasan and Tarokh (2022) {barticle}[author] \bauthor\bsnmNg, \bfnmYuting\binitsY., \bauthor\bsnmHasan, \bfnmAli\binitsA. and \bauthor\bsnmTarokh, \bfnmVahid\binitsV. (\byear2022). \btitleInference and Sampling for Archimax Copulas. \bjournalarXiv preprint arXiv:2205.14025. \endbibitem

- Perreault, Nešlehová and Duchesne (2022) {barticle}[author] \bauthor\bsnmPerreault, \bfnmSamuel\binitsS., \bauthor\bsnmNešlehová, \bfnmJohanna G.\binitsJ. G. and \bauthor\bsnmDuchesne, \bfnmThierry\binitsT. (\byear2022). \btitleHypothesis Tests for Structured Rank Correlation Matrices. \bjournalJ. Amer. Statist. Assoc. \bvolume0 \bpages1–12. \bdoi10.1080/01621459.2022.2096619 \endbibitem

- Pickands (1975) {barticle}[author] \bauthor\bsnmPickands, \bfnmJames\binitsJ. \bsuffixIII (\byear1975). \btitleStatistical inference using extreme order statistics. \bjournalAnn. Statist. \bvolume3 \bpages119–131. \endbibitem

- Pickands (1981) {binproceedings}[author] \bauthor\bsnmPickands, \bfnmJames\binitsJ. \bsuffixIII (\byear1981). \btitleMultivariate extreme value distributions. In \bbooktitleProceedings of the 43rd session of the International Statistical Institute, Vol. 2 (Buenos Aires, 1981) \bvolume49 \bpages859–878, 894–902. \endbibitem

- Ressel (2013) {barticle}[author] \bauthor\bsnmRessel, \bfnmPaul\binitsP. (\byear2013). \btitleHomogeneous distributions—and a spectral representation of classical mean values and stable tail dependence functions. \bjournalJ. Multivariate Anal. \bvolume117 \bpages246–256. \endbibitem

- Saunders, Stephenson and Karoly (2021) {barticle}[author] \bauthor\bsnmSaunders, \bfnmKR\binitsK., \bauthor\bsnmStephenson, \bfnmAG\binitsA. and \bauthor\bsnmKaroly, \bfnmDJ\binitsD. (\byear2021). \btitleA regionalisation approach for rainfall based on extremal dependence. \bjournalExtremes \bvolume24 \bpages215–240. \endbibitem

- Sklar (1959) {barticle}[author] \bauthor\bsnmSklar, \bfnmAbe\binitsA. (\byear1959). \btitleFonctions de répartition à dimensions et leurs marges. \bjournalPubl. Inst. Statist. Univ. Paris \bvolume8 \bpages229–231. \endbibitem

- Varin, Reid and Firth (2011) {barticle}[author] \bauthor\bsnmVarin, \bfnmCristiano\binitsC., \bauthor\bsnmReid, \bfnmNancy\binitsN. and \bauthor\bsnmFirth, \bfnmDavid\binitsD. (\byear2011). \btitleAn overview of composite likelihood methods. \bjournalStat. Sin. \bvolume21 \bpages5–42. \endbibitem

- Vatan (1985) {bincollection}[author] \bauthor\bsnmVatan, \bfnmPirooz\binitsP. (\byear1985). \btitleMax-infinite divisibility and max-stability in infinite dimensions. In \bbooktitleProbability in Banach spaces, V (Medford, Mass., 1984), \bvolume1153 \bpages400–425. \bpublisherSpringer. \bdoi10.1007/BFb0074963 \endbibitem

- Wadsworth et al. (2017) {barticle}[author] \bauthor\bsnmWadsworth, \bfnmJ. L.\binitsJ. L., \bauthor\bsnmTawn, \bfnmJ. A.\binitsJ. A., \bauthor\bsnmDavison, \bfnmA. C.\binitsA. C. and \bauthor\bsnmElton, \bfnmD. M.\binitsD. M. (\byear2017). \btitleModelling across extremal dependence classes. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume79 \bpages149–175. \endbibitem

Appendix A Proofs of Section 4

This section contains the proofs of the results from Section 4. We begin with auxiliary results in Section A.1; Theorem 4.1 and its Corollaries are proved in Sections A.2 and A.3, respectively.

A.1 Auxiliary results

The following proposition is used to prove Theorem 4.1 but is also of independent interest.

Proposition A.1.

Let be a random vector with joint survival function as in (2.4) for some stdf . Then belongs to the maximum domain of attraction of a multivariate extreme-value distribution with unit Fréchet margins and stdf .

Proof of Proposition A.1.

For the margins, recall that for each , . The survival function of is thus given by ; it is easily seen that . Now set . From Equation 3.13 in Embrechts, Klüppelberg and Mikosch (1997), for all , it then holds that as . Thus is in the domain of attraction of a multivariate extreme-value distribution with unit Fréchet margins and stdf if and only if for all ,

To show this, fix an arbitrary and observe that because as ,

for all sufficiently large. Now note that as , converges to for all and to for . Consequently,

as claimed. ∎

The following lemma determines the normalizing sequences needed for the proof of Theorem 4.1.

Lemma A.1.

Let be a clustered Archimax copula such that Assumptions 4.1 and 4.2 are satisfied. Then the following hold:

-

(i)

For each and , . Recall that for , where . Moreover, there exists a sequence of positive constants such that for all , as and as .

-

(ii)

For each and , . Moreover, there exists a sequence of positive constants such that for all , as and as , where .

Proof of Lemma A.1.

(i) Let and . We then have by assumption and owing to the fact that . By Proposition 3.1.1 in Embrechts, Klüppelberg and Mikosch (1997), there exists a sequence of positive constants such that for all , as . Because , for some sufficiently small. Using the lemma of Breiman (1965) and the fact that , we then have, for all and with ,

Indeed, as by the choice of normalizing constants . The convergence of the fraction in the above display is due to Breiman’s lemma. The Fisher-Tippett-Gnedenko Theorem (Fisher and Tippett, 1928; Gnedenko, 1943) implies that since and , . We also have that and are independent, positive, and for . By Breiman’s lemma, and

as .

(ii) Let and . The proof of the result relies again on Breiman’s lemma; see also Proposition 2(b) of Belzile and Nešlehová (2017). Since , Proposition 3.1.1 in Embrechts, Klüppelberg and Mikosch (1997) implies that there exist sequences of positive constants such that for all , as , and this for all . Recall that . Similarly to the proof of part (i), Breiman’s lemma then implies that for all and with ,

The convergence of the first part of the above is due to the choice of the normalizing constants . For the convergence of the second term, note that and by assumption, for some . Finally, since and are independent and positive, Breiman’s lemma implies that and that

as . This completes the proof. ∎

The lemma below establishes asymptotic independence between clusters in and clusters in .

Lemma A.2.

Proof.

Fix and recall that . The probability of interest can be written as follows, for and ,

where the first equality is due to the independence between and and the last equality is due to the independence of and . Next, consider the integrand as a sequence of functions defined on . Observe that for each ,

where is itself a sequence of functions on defined by

From the choice of , for all , , where . Moreover,

and

as . We therefore have a sequence of nonnegative functions bounding from above such that

Finally, note that

as since

as . The desired result then follows by the generalized Lebesgue dominated convergence theorem (see Theorem 1.21 in Kallenberg (2002), for example). ∎

We are now ready to prove Theorem 4.1.

A.2 Proof of Theorem 4.1

A random vector is in the maximum domain of attraction of the extreme-value distribution with Fréchet margins if and only if there exist sequences of positive constants , , so that, for all ,

This is a multivariate extension of Proposition 3.1.1 in Embrechts, Klüppelberg and Mikosch (1997), as used in Belzile and Nešlehová (2017). For each , set the sequences as done in Lemma A.1. Then the fact that the marginals of are Fréchet follows from the said Lemma. With the normalizing constants now set, the limit of interest is, for any fixed and, for convenience, let ,

| (A.1) |

where for , as in Lemma A.1 (ii) and for ease of notation, . Letting denote the power set of , (A.1) can be rewritten as

| (A.2) |

We now consider the subset of such that if and only if there exists so that and . As it turns out, the summands in (A.2) for which are asymptotically negligible. To see this, fix an arbitrary and pick so that and . Then for all ,

as by Lemma A.2.

Now, let be the subset of such that if and only if implies that . In other words, contains only sets of indices with . Let , define , and rewrite the summands in (A.2) with as follows:

where is indexed so that . Now consider the integrand as a sequence of functions defined on and observe that for each , , where is given, for each as above, by

Clearly, as , where

with

Moreover,

as . Therefore, we have a sequence of majorants for which the identity is satisfied. Now recall that the vector of reciprocal distortions has a limiting stdf defined in terms of the positive, unit-mean variables in Assumption 4.2. Therefore, pointwise, where for all ,

Now, integrating over the yields

Using the generalized Lebesgue dominated convergence theorem, we can thus conclude that for all ,

Analogously to , let contain only sets of indices with . Let and , define , and recall that for all . Next, for , rewrite the summands of (A.2) with as follows:

where is indexed as . Now consider the integrand as a sequence of functions defined on and observe that for each , , where is given, for all , by

Clearly, for all and as ,

Furthermore,

and, as ,

Analogously to the treatment of , we have a sequence of majorants such that . It remains to determine the limit of the sequence of functions defined for all by

By assumption, and are independent if and are therefore asymptotically independent as well. Using Proposition A.1 and the fact that for all and , one has that pointwise, where for all ,

Integrating the limit yields

Thus for all , the limit (A.1) is equal to

Recalling that , one obtains (4.1) by plugging in the appropriate Fréchet margins. ∎

A.3 Proofs of Corollaries 4.1 and 4.2

Proof of Corollary 4.1.

Let and recall that is the limiting stdf of , defined for all . Letting be a (uniformly) random permutation of yields the independence stdf . Due to the fact that, for all and , is independent of , plugging this into (4.1) yields, for all ,

By Proposition 6.1 in Charpentier et al. (2014), as mentioned in the Section 1, for each ,

This completes the proof.∎

Appendix B Jackknife estimation of the covariance matrix of

Here, we provide a consistent estimator of the asymptotic variance of , where is as in (6.3). Recall the definition of in (6.1). For each and , let be a version of based on all but the th observation; be the average of all such that, given , ; ; and . In particular, is a version of based on all but the th observation. It then follows from Theorem 9 of Arvesen (1969) that, for and ,

| (B.1) |

is a consistent estimator of .

Appendix C Conjectured extension of Theorem 4.1

As it is stated, Theorem 4.1 does not account for the boundary case when , which can occur. It would thus be desirable to replace Assumption 4.1 of Theorem 4.1 by the following requirement.

Assumption C.1.

For a clustered Archimax copula as in Definition 3.1, assume that is the union of disjoint sets , , and such that

-

(i)

if and only if for some .

-

(ii)

if and only if there exists an such that .

-

(iii)

if and only if and .

We conjecture that the variables whose distortions are in have the same asymptotic behavior as those whose distortions are in . More precisely, we surmise that the following statement holds.

Conjecture C.1.

One part of Conjecture C.1 is clear, namely that for . Indeed, for any such , the Corollary to Theorem 3 in Embrechts and Goldie (1980) implies that . So one can again find a sequence of positive constants ensuring that for all , as . The main difficulty in establishing the validity of Conjecture C.1 is the fact that, for and , the relation between the above normalizing sequence and the normalizing sequences for and is unclear. In order to prove the conjectured result, it suffices to prove three sister lemmas which are reported below. The first two, Lemmas C.1 and C.2, are analogous to Lemma A.2 and are proved therein. The third, Conjecture C.2, that states asymptotic independence between different clusters in , is the missing result that if established would prove Conjecture C.1.

Lemma C.1.

Under the hypothesis of Conjecture C.1, suppose that , , and . Let be a sequence of positive constants such that for all , as and as . Furthermore, let be a sequence of positive constants so that for all , as . Then for all ,

Proof of Lemma C.1.

The proof is quite similar to the one of Lemma A.2. Observe first that the assumed sequences and indeed exist, by Lemma A.1 and the discussion in the paragraph following Conjecture C.1. Fix some arbitrary and recall that . The probability of interest can be written as follows

Consider the integrand as a function defined on and note that for all , , where is given, for all by

As in the proof of Lemma A.2, for all ,

Moreover,

and

as . We therefore have a sequence of functions bounding from above such that

Finally, note that

as since and as . The desired result then follows from the generalized Lebesgue dominated convergence theorem. ∎

Lemma C.2.

Under the hypothesis of Conjecture C.1, suppose that , , and . Let such that for all , as and as . Furthermore, let be a sequence of positive constants so that for all , as . Then for all ,

Proof of Lemma C.2.

This proof is almost exactly the same as the proof of Lemma A.2. Again, the existence of the norming constants and follows from Lemma A.1 and the discussion in the paragraph following Conjecture C.1. Fix some arbitrary . We are interested in the limit as of

Consider the integrand as a function defined on . Observe that for each , where for all ,

From the choice of , for all ,

Moreover, since ,

and

as . We therefore have a sequence of functions bounding from above such that

Finally, note that

as since

as . Using the generalized Lebesgue dominated convergence theorem concludes the proof. ∎

Conjecture C.2.

Under the hypothesis of Conjecture C.1, suppose that , and . Let and be sequences of positive constants such that for all , and as . Then for all ,

Appendix D Additional figures for Section 5

Appendix E Additional figures for the data illustration of Section 7