Regret Bounds and Experimental Design for Estimate-then-Optimize

Abstract

In practical applications, data is used to make decisions in two steps: estimation and optimization. First, a machine learning model estimates parameters for a structural model relating decisions to outcomes. Second, a decision is chosen to optimize the structural model’s predicted outcome as if its parameters were correctly estimated. Due to its flexibility and simple implementation, this “estimate-then-optimize” approach is often used for data-driven decision-making. Errors in the estimation step can lead estimate-then-optimize to sub-optimal decisions that result in regret, i.e., a difference in value between the decision made and the best decision available with knowledge of the structural model’s parameters. We provide a novel bound on this regret for smooth and unconstrained optimization problems. Using this bound, in settings where estimated parameters are linear transformations of sub-Gaussian random vectors, we provide a general procedure for experimental design to minimize the regret resulting from estimate-then-optimize. We demonstrate our approach on simple examples and a pandemic control application.

Keywords Estimate-then-optimize, Experimental Design, Optimization under Uncertainty

1 Introduction

Consider a decision based on a model whose parameter vector is estimated from data. Examples include:

-

•

Choosing nonpharmaceutical interventions to prevent the spread of a virus given a structural epidemiological model of viral spread, where the model’s predictions depend on viral transmission parameters;

-

•

Choosing staffing levels in a hospital to ensure timely service and good health outcomes while controlling costs, given a structural queuing model for patient arrivals and the time required to deliver care;

-

•

Choosing rates at which to pump oil from several wells to maximize the amount of oil extracted, given a structural model for subsurface oil flow.

Perhaps the most common approach to solving this problem is to (1) estimate the parameter vector from data; and then (2) choose decision vector to maximize the value predicted by the structural model assuming this estimated parameter vector is correct. Mathematically, if our estimator is and our model is , the resulting decision is . This approach is sometimes called “estimate-then-optimize” (Farias, 2007; Hu et al., 2020).

While more sophisticated methods exist for choosing a decision based on data, such as Bayesian methods (Wu et al., 2018) and robust optimization (Bertsimas et al., 2018), they can be hard to implement. One barrier is the computation required by the more complex optimization problems they solve (e.g., for robust optimization). Another barrier is the need to integrate engineering and organizational structures that previously separated estimation from optimization. For example, a company may have a team of machine learning experts focused on estimation and a separate team trained in and focused on optimization, each with their own engineering systems. Thus, estimate-then-optimize is widely used in practice and it is valuable to understand and improve its performance.

In estimate-then-optimize, errors in the statistical estimation can lead to regret: the value of the decision made may be smaller than that of the best decision possible using the true parameters, . While this is understood intuitively to be important by practioners, past literature has not, to our knowledge, provided formal bounds for this regret nor considered how the experimental design used to gather data for estimation impacts regret.

Our contribution is a novel bound on the regret resulting from an estimate-then-optimize approach for smooth and unconstrained . We further show how this approach can inform the experimental design used to collect data for estimating . In particular, our results can help a user decide how much effort to allocate to parts of their parameters space so as to minimize regret. In a setting where the parameter estimate is known to be a linear transformation of a sub-Gaussian random vector, we provide bounds that depend on its covariance; this covariance term can consequently be used to minimize this asymptotic regret bound. We provide three examples: one in which the parameters are directly assumed to be normal, a pricing example using a logistic conversion model, and a more tangible real-world example of controlling a pandemic.

We envision this work will be of substantial interest to those who currently rely on the estimate-then-optimize paradigm to make decisions from data and are prevented by the barriers described above from moving away from estimate-then-optimize. For instance, a marketplace platform may use our result to select not only prices to use for an experiment, but also the proportion of participants to assign to each price so as to minimize the regret in finding the optimal price.

The rest of the paper is structured as follows. Section 2 overviews related work. Section 3 contains the main technical results and the prerequisite assumptions. Section 4 expands on said technical results in cases when the parameter estimates are assumed to be linear transformations of sub-Gaussian random vectors. Section 5 connects our work to experimental design. Section 6 demonstrates our method on three examples. Finally, section 7 concludes and mentions some future directions of this work.

2 Related Work

The general two-stage procedure of estimating parameters in an optimization problem and then solving using those predicted parameters has appeared in the literature in various forms.

From a statistical viewpoint, the framework presented in this paper can be viewed as optimizing some function in the presence of a model parameter (sometimes called a nuisance parameter), , which must first be estimated. Using this perspective, Foster and Syrgkanis (2019) derive fast rates of convergence when a condition called Neyman-orthogonality is satisfied, where the pathwise derivatives of with respect to and at their true values vanishes. However, this cross-derivative term is exactly the term which we consider in this work as (1) it is generally not equal to 0 except in very specific applications and (2) it governs the slower rate for the risk.

There has also been work done in similar settings in which one wishes to perform estimate-then-optimize in a “smarter” way. In (Elmachtoub and Grigas, 2022), the authors specifically tackle a contextual stochastic optimization problem, wherein the objective is linear and of the form Here the authors call this particular form “predict-then-optimize”. In particular, here the user is presented with a context drawn from some distribution, and the parameters of the objective function depend on . The standard estimate-then-optimize approach would be to run some off-the-shelf regression method to construct a prediction for based on past data of the form , and optimize the resulting program . The proposed solution is to aim the prediction of towards minimizing the objective value in the downstream optimization problem, dubbed the smart predict-then-optimize (SPO) loss. As minimizing this directly is intractable, the authors propose minimizing a convex surrogate. Later work, such as El Balghiti et al. (2019), analyze generalization and risk bounds for this particular approach.

We emphasize that this “predict-then-optimize” framework focuses on the loss for individual contexts, i.e. for a fixed . However, if one instead focuses on the average performance across chosen from the training set, then the overall loss would be of the form . We may encode this in our framework via setting and , and .

Ito et al. (2018) also consider the same estimate-then-optimize framework, wherein one optimizes using an estimate for the true . However, their work does not analyze the value of , but rather establishes that the estimate is generally biased for . They additionally describe a bias-correction procedure under which is affine in , but do not offer asymptotic analysis of our quantity of interest, .

Wilder et al. (2019) also consider the estimate-then-optimize framework, though in their case the optimization problem is combinatorial, i.e. the decision are discrete. Their approach is to (1) relax the combinatorial problem to a continuous one, (2) derive gradients of the objective with respect to the predictions, (3) use the closed-form gradients in a gradient-based optimization algorithm, and (4) round the resulting solution to the nearest integer. They also find that plays a fundamental role in their gradient derivations, and demonstrate their approach in detail on linear programming and submodular maximization problems. However, they only offer empirical evidence that their approach performs well, and obviously apply only to combinatorial problems.

Our work is also closely related to empirical risk minimization (ERM) (Vapnik, 1999) and sample average approximation (SAA) (Kim et al., 2015), though still different in important ways. In our setting, toward the goal of minimizing over , we consider the approximate minimizer for some estimator of . In ERM and SAA, toward the goal of minimizing over , one considers the approximate minimizer where are i.i.d. Except in trivial cases (such as those where do not depend on ), there is no way to construct an and so that the quantities match. Our setting is therefore different from ERM/SAA except in the special case where is linear in for all .

The idea of using sensitivity of output to parameters to guide data collection has also been explored, notably in the simulation community, e.g. Song and Nelson (2015) and Freimer and Schruben (2002) give two approaches for deciding on which parameters to collect more data in order to reduce the impact of input uncertainty on simulation output. However, these approaches do not consider the setting in which there is a decision to be optimized, whereas our approach is concerned with targeting parameters to make better decisions.

Finally, experimental design is a mature field within statistics which has explored the notion of optimal design for an experiment, where there are several notions of optimality (Pukelsheim, 2006). In the particular case of linear models, in which the experimenter has control over the proportion of samples to allocate to a set of linearly independent vectors which comprise the design matrix, various optimality criteria have been studied in the literature. A commonly used definition of optimality is -optimality, which reduces to minimizing the average variance of the regression coefficients. Similarly, -optimality instead considers minimizing the variance of a linear combination of the regression coefficients. When the decision variable is one-dimensional, our regret bound induces a -optimal design problem. More generally, our regret bound induces an -optimal design for a particular parameter system .

3 General Regret Bound for Estimate-then-Optimize

This section defines the estimate-then-optimize framework more formally and then states our general bound on regret and assumptions required by this bound.

In the estimate-then-optimize framework we are concerned with optimizing some smooth function where is a model parameter and . Here can equal or a subset thereof. The goal is to solve , where is unknown and must be estimated. Call . Note that here if , Assumption 3.1 must be satisfied, i.e. .

Below, we denote , i.e. the line segment between . Also (without a subscript) always denotes the Euclidean norm. Finally, for higher-than-second-order directional derivatives (as they appear in Taylor’s theorem), we denote to be

We consider an algorithm that first learns from a sample (say a sample generated under a distribution with mean ) and then learns by minimizing , where the second minimization step is exact.

Assumption 3.1 (First Order Optimality).

The minimizer satisfies

Assumption 3.2 (Strong Convexity).

The function is strongly convex with respect to in a neighorhood around for each , i.e. a universal exists such that

for all , for all .

Assumption 3.3 (Higher Order Smoothness).

There exist constants and such that the following derivative bounds hold:

-

•

For all ,

-

•

For all , ,

The higher order assumptions also appear in other literature, e.g. Foster and Syrgkanis (2019), where it is shown that they are easily satisfied. We then have the following theorem.

Theorem 3.4.

Under the above assumptions and when , the optimality gap of under the true , i.e. , is upper bounded by

4 Regret Bound for Linear Transformations of sub-Gaussian Random Vectors

We now consider a particular setting in which we place a distributional assumption on our estimate . In particular, suppose we have some dataset of size which we use to construct . Furthermore, assume this estimate is known to be a linear transformation of a sub-Gaussian random vector which has parameter 1 WLOG. This encompasses a wide class of random variables. In particular, normal random variables are a special case when taking the sub-Gaussian random vector to be an isotropic multivariate Gaussian with identity covariance and the linear transformation to be the square root of the covariance matrix. In the asymptotic regime, asymptotically normal estimators are therefore also included, e.g. from the central limit theorem or asymptotic theory governing maximum likelihood estimators. This is summarized in the following assumption.

Assumption 4.1.

We have an algorithm which, from a dataset of size , produces such that for positive definite and subG(1).

Assumption 4.2.

The set is open.

Also for notational convenience we define We then have the following lemma for converging to the strongly convex neighborhood.

Lemma 4.3.

There exist constants such that for sufficiently large, with probability at least .

This lemma then yields the following theorem.

Theorem 4.4.

With probability at least

5 Application to Experimental Design

We now imagine we have a class of experiments which informs us about the uncertain parameter . Each produces a different estimator and corresponding distribution, which is assumed to satisfy the distributional assumptions of Section 4. Our goal is to choose the experiment so as to minimize the upper bound derived previously in Theorem 4.4.

In particular, the theorem tells us that minimizing the trace of the variance term minimizes the upper bound on the regret. In the context of linear models, this is exactly equivalent to the -optimality criterion in experimental design (Pukelsheim, 2006) when using as a coefficient matrix. 111Using other scalar values related to the matrix would correspond to other criteria. For instance, minimizing the determinant (or equivalently log determinant), would correspond to -optimality, or minimizing the 2-norm would correspond to -optimality.

Therefore the problem is to minimize , where the decision variable is the experimental design which induces the form of

In the discussion and results above, we assume is known to us. However in practice, is unknown — it depends on the unknown value . We overcome this with a Bayesian approach: we place a prior on , and draw samples from the prior , which we then use to calculate . This then gives us access to We then solve the following problem

| (1) |

where in practice we replace the true expectation with an empirical average over draws from the prior.

6 Examples

This section provides three examples of how our method can be used to inform experimental design, as well as corresponding numerical experiments demonstrating the value of our method.

6.1 Experimental Design Under Normal Model Parameters from a Linear Model

We consider a particular setting for experimental design to which our method directly applies. Suppose we can get samples where are i.i.d. for each and are independent between .

First, for , define as the number of times was sampled. Then we define component-wise via

So in this case where is diagonal with

We see that minimizing the norm of the LHS is equivalent to minimizing the variance (for instance, the squared norm of the LHS is a distribution).

Now assume that . Since in this case is just a vector, we then denote

Now referring back to Theorem 4.4, we see that the quantity of interest is (since the trace and in this case correspond to the same scalar). So the objective is to minimize , subject to belonging to the class of allowed by our allocations .

At this point, we point out that this exactly coincides with -optimal experimental design. In particular, this is the special case that our linearly independent vectors for samples are the unit vectors in so that . Then standard results in -optimal experimental design (Pukelsheim, 2006) yield that, given a mass of unit to allocate across the vectors,

| (2) |

In practice, if one had say samples to allocate across the components, we would assign to component , rounding when necessary.

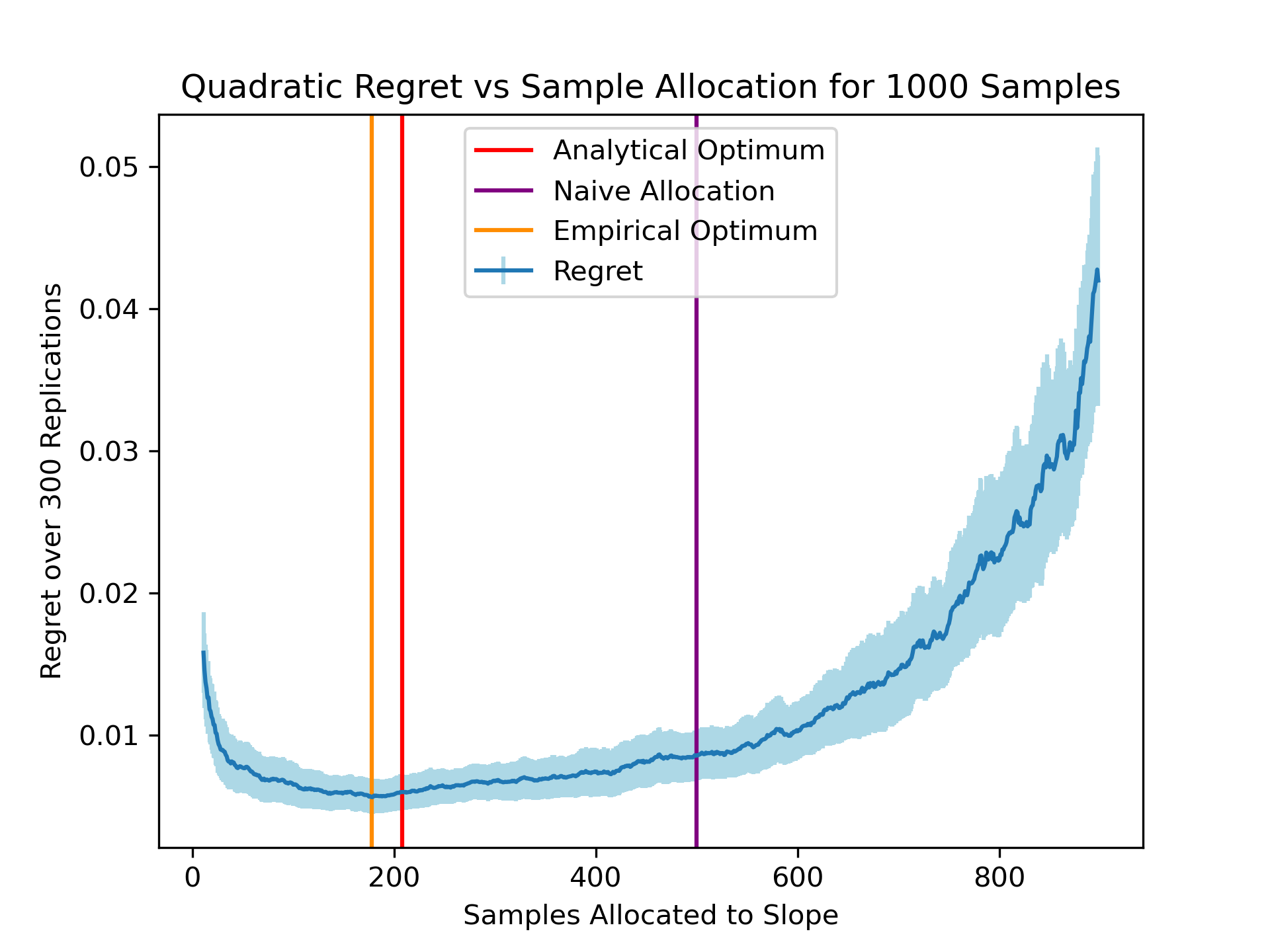

We now provide a simple problem to demonstrate our method on this setting. Consider which satisfies the assumptions of the theorem when . Suppose that we can sample . Here , and minimizing the bound corresponds to minimizing where is the total number of samples to allocate. Note that we do not have a constant term, as any samples used to estimate the constant term are wasted; we care about , and the constant term in does not interact with the decision variable .

For our experiment, we use the prior and . We repeated the method for 300 replications, where 100 draws from the prior are used for both optimization of the bound and evaluation of the regret. Figure LABEL:fig:quad shows the regret under the prior achieved by our method versus a uniform allocation which splits samples across and evenly.

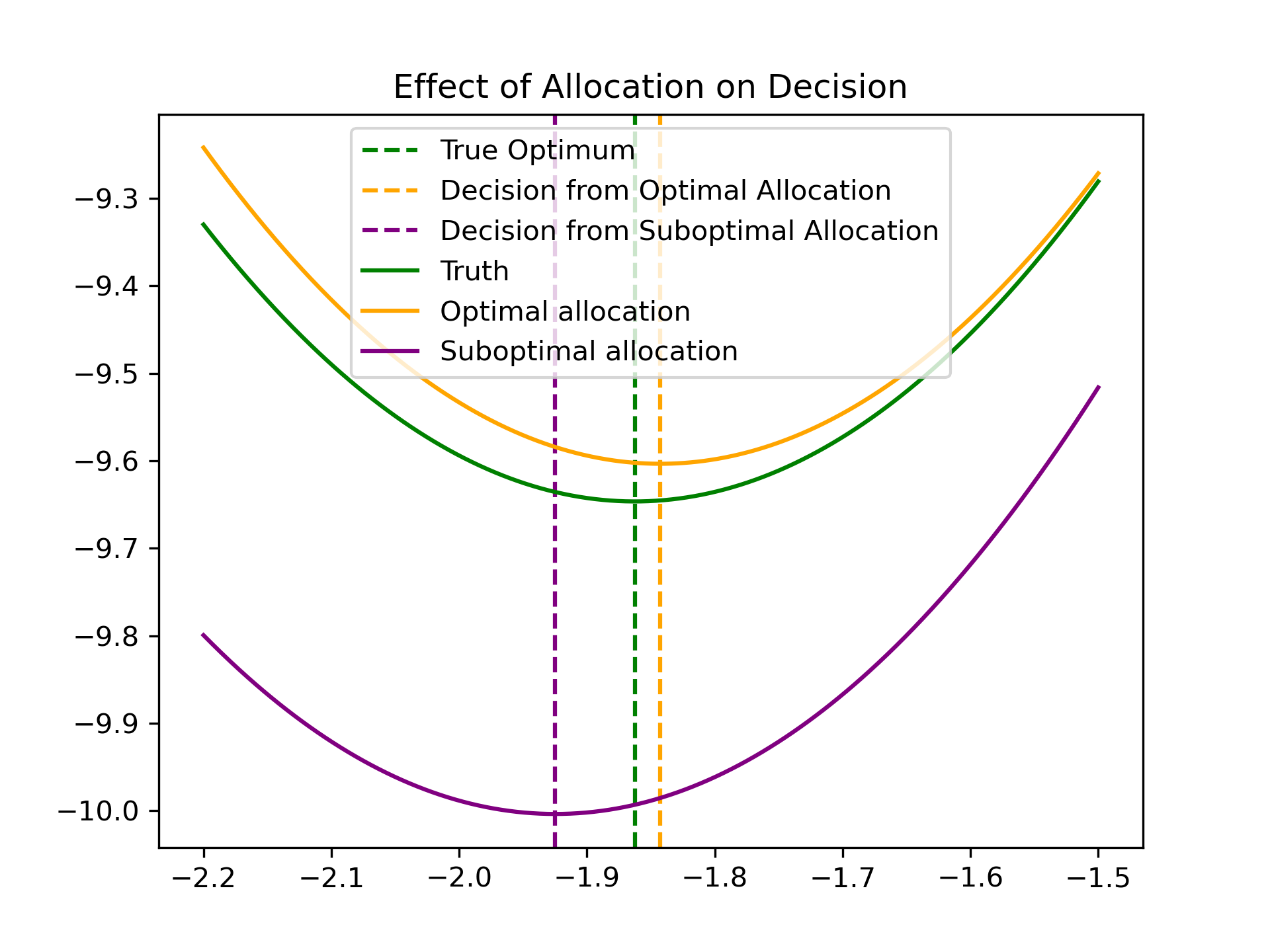

Figure 1b compares the estimated function against , showing that the resulting estimate yields a better decision for when using the optimal allocation.

6.2 Pricing Under Logistic Conversion

In this example, we consider pricing a product based on a data from a pricing experiment. We observe a sequence of customers arriving to a website or mobile app who are each presented with a price . For each customer, we observe whether they purchase (“convert”) or not, with the probability of purchase being governed by a logistic function of the price with parameter , i.e.

The objective function is then revenue, negated to yield a minimization problem:

Here we assume so that higher prices have lower purchase probability. We suppose that estimate-then-optimize is implemented by estimating via maximum likelihood estimation. From standard results for the maximum likelihood estimate for logistic regression (Hastie et al., 2009), we know that asymptotically where is a matrix with first column all ones, and second column corresponding to prices , and is a diagonal matrix with on the diagonal.

In this case, is given by

It is easy to show that satisfies the conditions of our theorem. For completeness, the proofs are provided in the supplementary material.

We consider a user who is designing an experiment to support selection of the best price. The user has access to historical data on prices and conversion, which she can use to construct a prior for . Using this data, she designs an experiment using samples constrained to use prices from among distinct prices. The user then uses maximum likelihood to estimate , and solving the corresponding revenue maximization problem. This yields the fixed price which she holds in place moving forward. The revenue of the selected price , under the true logistic model , is the quantity we wish to be as large as possible. The regret is the difference between this quantity and the revenue at the optimal price under the true logistic model.

We study this experimental design problem numerically via simulations. We simulate the procedure described above, where one must decide how to allocate samples (opportunities to sell the product to a customer) across prices to yield the selected price with the highest expected revenue, considering samples and prices.

We evaluate our method and a baseline method under a collection of multivariate normal priors for with covariance . The means of the priors for were chosen so that the value for which is at prices (avoiding boundaries). 100 draws from the prior were used for optimization and evaluation of regret.

Due to the computational cost of considering all partitions of 100 allocations among the 10 prices, we instead use random search to optimize the regret bound. In particular, we choose 1000 random allocations uniformly at random and return the allocation minimizing .

We then simulate 100 customer purchase decisions (conversions) using prices distributed among the 10 prices according to the best allocation found as well as according to the baseline uniform allocation, again using the logistic model and the held out ground truth . We again use maximum likelihood to derive estimates and , and their corresponding revenue maximizers .

Table 1 gives 95% confidence intervals for the resulting expected regrets from these two approximate revenue maximizers, and . We see that our optimized approach provides consistently lower regret than the baseline uniform allocation. We also note that in our experiments, we observed the scale of the regret scales as : see the supplementary material for more experiments for values of .

| Optimized Allocation | Uniform Allocation | |

|---|---|---|

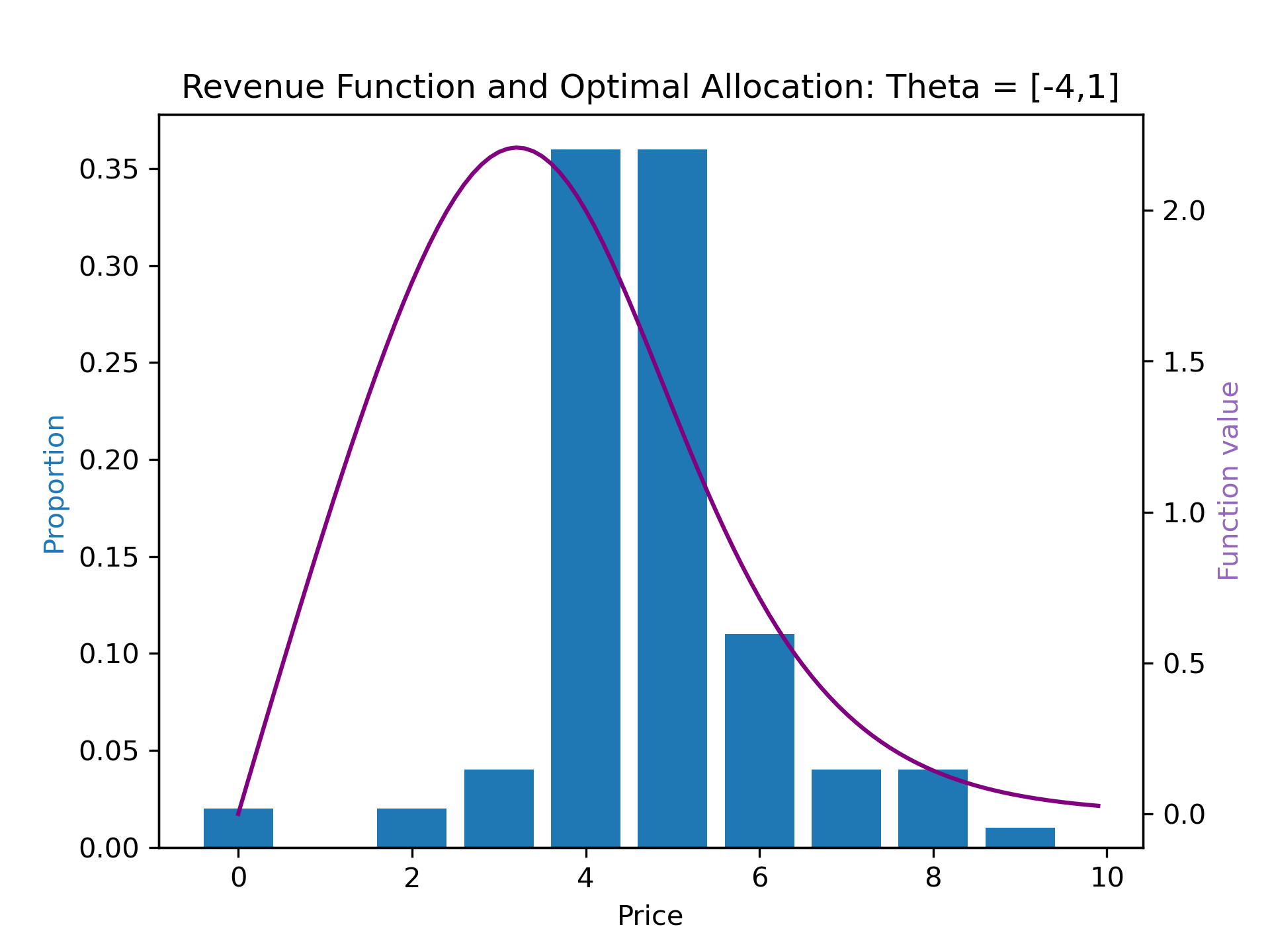

Figure LABEL:fig:price also shows an example of the optimal allocation found by our method. We can observe that, compared to a uniform sampling strategy, more samples are allocated near the peak of the function, yielding more information about the maximum. In particular, more samples are allocated slightly to the right where the conversion hovers around (at ), suggesting that the change in curvature there also yields more information than just the peak.

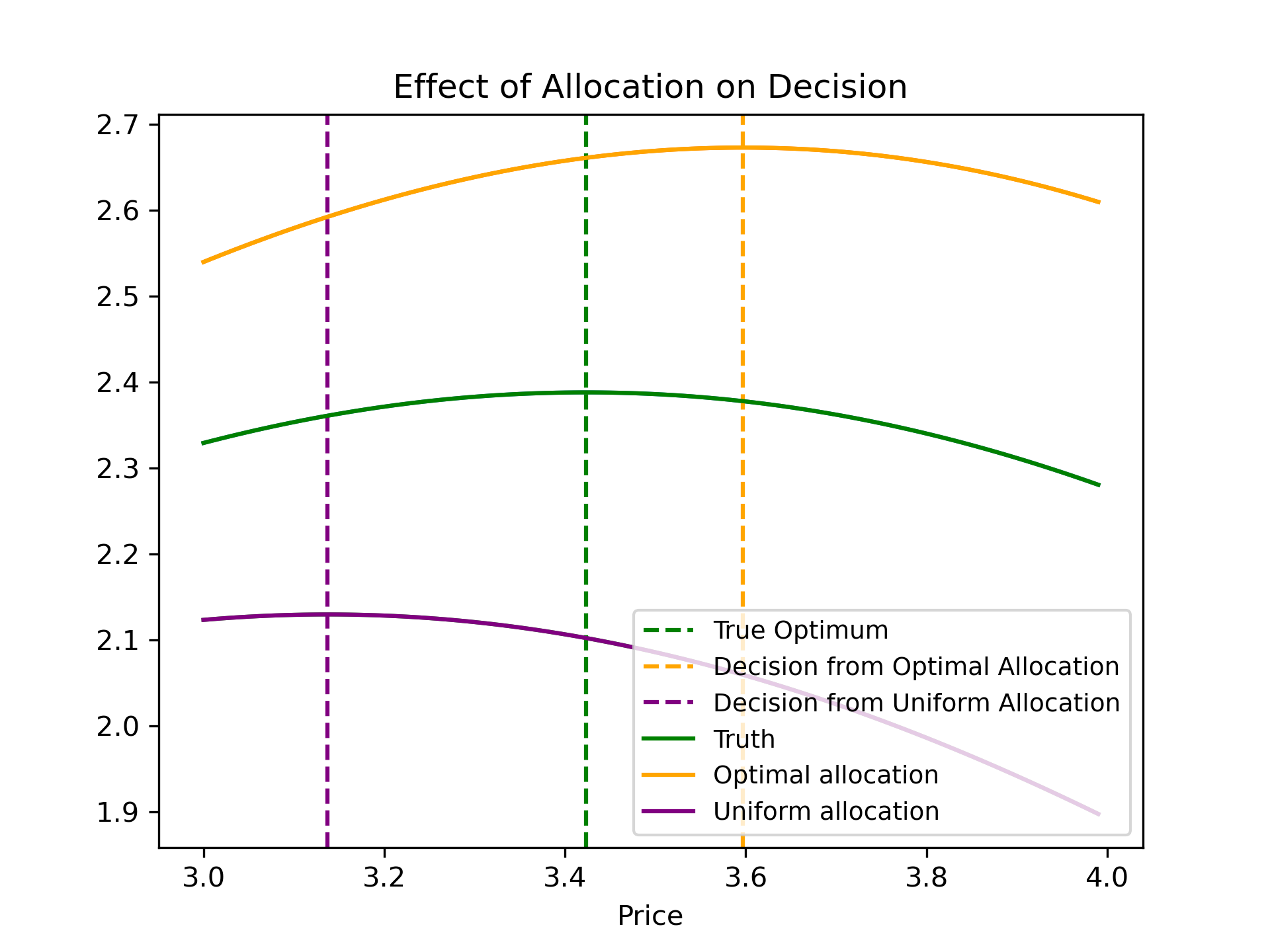

Finally, Figure 2b is the analogous figure of Figure 1b for this pricing problem. Here it shows, again for , the estimated function for coming from different allocations. We again see that the optimal allocation yields an estimated function whose optimizer is closer to the optimizer of the true function.

6.3 Application to Pandemic Control

We now apply our framework to controlling COVID-19 through regular testing as a university or city reopens, subject to uncertainty about contact among social groups.

We model viral spread via a multi-group SIR model (see, e.g., Guo et al. 2006), where people belong to one of social groups, indexed by , and to one of three disease states. A combination of social group and disease state is called a “compartment”. The three disease states considered are: Susceptible (S), someone who has never been infected; Infected (I), someone who is infected and can infect others; and Removed (R), someone who was previously infected, cannot infect others, and cannot be themselves infected. A person can be Removed either because they have recovered from their infection and developed immunity or because they were discovered through testing and isolated away from others. indicates the number of susceptible people from social group , and similarly for and .

In this model, the following differential equations describe how people move between disease states:

| (3) | ||||

| (4) | ||||

| (5) |

where is the size of the th group, describes the average rate at which infected individuals in group infect individuals of group if group were fully susceptible, is the rate at which individuals recover, and is the rate at which we test individuals in group .

In (3), a group- infected person infects people in group at rate , since only a fraction of people in group are susceptible. Multiplying by the number of group- infected individuals, , and summing across gives the rate at which people are removed from the susceptible compartment in (3) and added to the infected compartment in (4). Each infected person recovers at a rate and is tested at a rate , resulting in being subtracted in (4) and added in (5).

Our decision vector , which is the amount of testing we do, is limited by a capacity constraint for some fixed T.

We model , where is a global infectivity parameter and is the number of individuals of group that an infected individual of group interacts with per day.

The uncertain parameter vector is , which can be estimated before the university or city reopens from contact tracing data that can be obtained, with effort, from another university or city with similar social groups. Contact tracing an infected person in social group yields a sample of the vector , i.e. the numbers of people from each group with which that individual enjoyed social contact. We assume that , and each is independent. Letting be the number of contact traces of infected individuals in group , our estimate for is the sample mean of the observed samples for that element, i.e. , where is the th trace. Contact tracing requires time from a trained individual and so is limited. We write this constraint as .

Our objective function is the cumulative number of infected individuals over a finite horizon of 100 days, as given by the output of a simulation. We solve this for any fixed by optimizing over using L-BFGS-B. Partial derivatives in are calculated using finite differences. The optimized allocation is found via a closed form similar to Equation 2, and 1000 samples are used for optimization of the experiment design and the evaluation of the regret. The baseline allocates equal contact traces to the three groups. For more implementation details, refer to the supplement.

Results are shown in Table 2 for parameters

and varying , where an infected person arrives in group 2 at . We use an independent Gamma prior with shape and scale 1 for each , The mean for the prior was chosen so that the first two groups have significantly more contacts than the third, modeling heterogeneity in contact rates across social groups (Mossong et al., 2008).

Higher contact rates make it more important to provide sufficient testing in the first two groups compared to the third, and also make it more important to estimate the contact rates well in these two groups. Indeed, the optimized allocation allocates more contact traces to the subpopulations with more contacts and has significantly less regret.

| Allocation | Opt. Regret | Uni. Regret | |

|---|---|---|---|

| [5,4,1] | |||

| [17,12,1] | |||

| [57,42,1] | |||

| [172,126,2] |

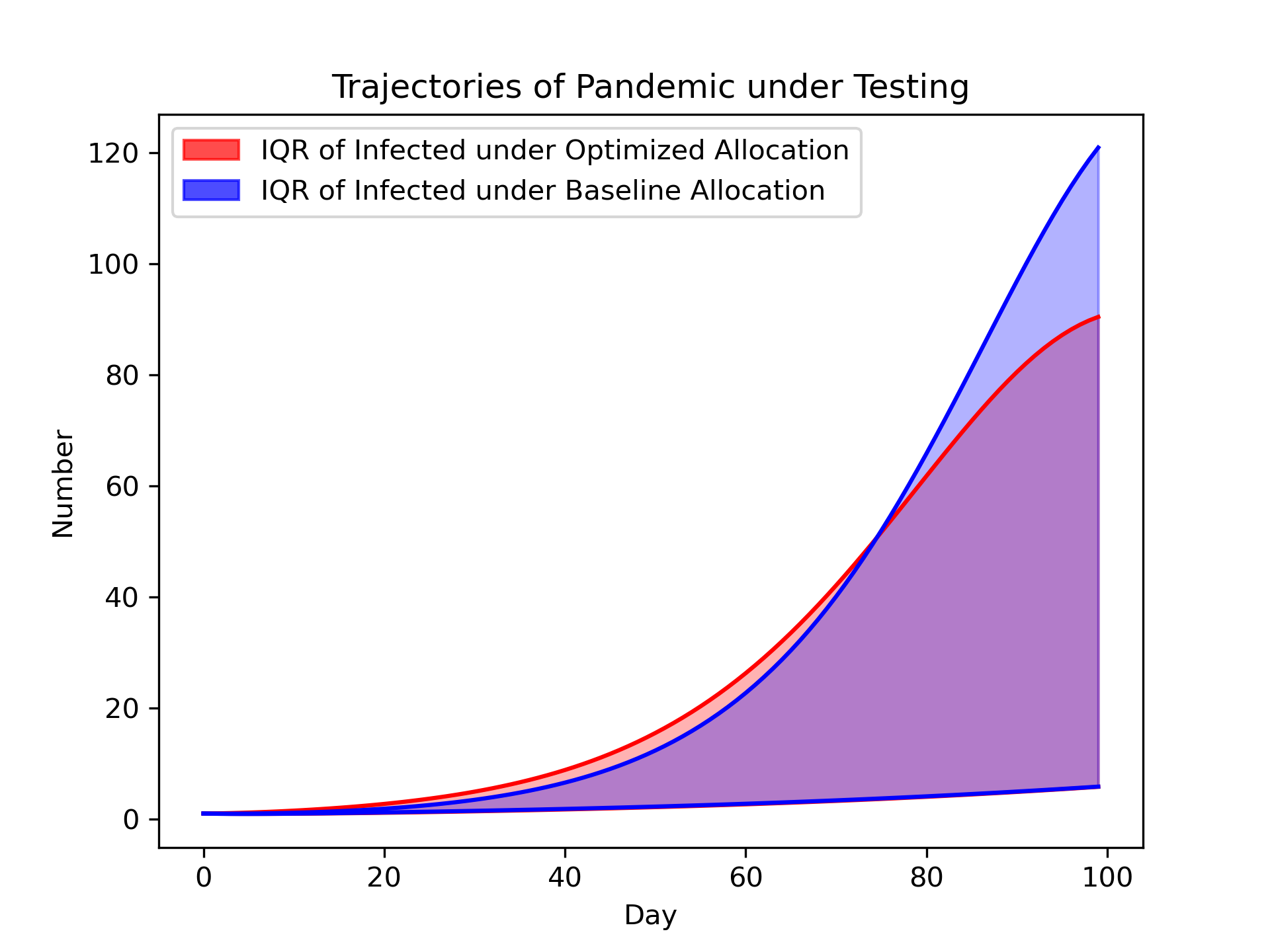

Figure 3 depicts the pandemic trajectories resulting from testing decisions made under the optimized and baseline allocations for a particular sample of . The trajectory under the optimized allocations yields notably fewer infections, demonstrating an improvement in health outcomes.

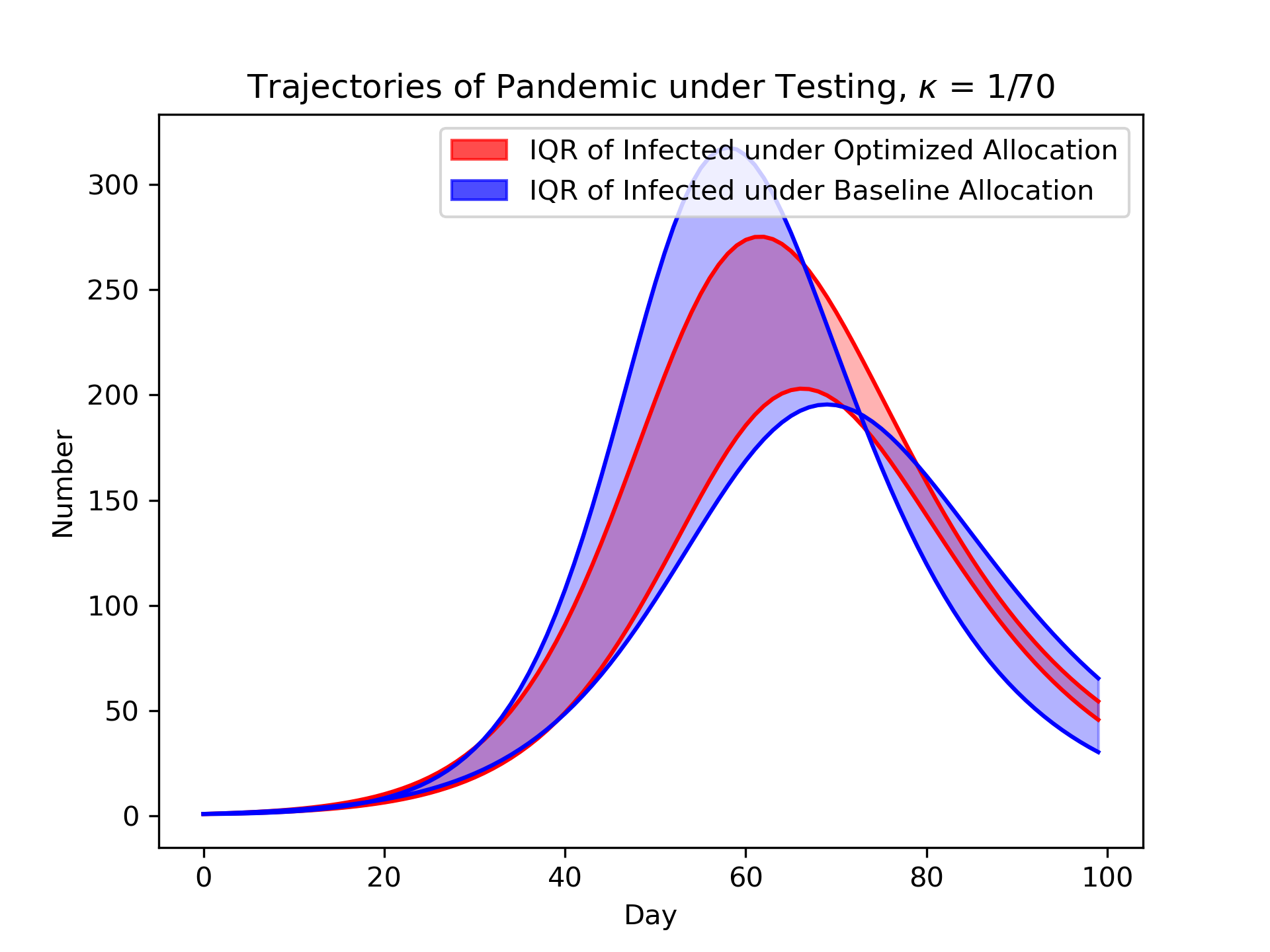

We also show results when we increase the transmissibility per contact parameter by 50%, from to (the case of decreasing the transmissibility significantly was not interesting as in either case the number of infected does go over one person). Table 3 shows the regrets for our optimized allocation versus the uniform allocation, where we change , the constraint on the number of contact traces performed. Figure 4 shows the corresponding infection trajectory plots over 1000 draws from the prior. Both demonstrate that using our method results in better testing decisions that improve health outcomes, even when a larger-scale outbreak occurs.

| Allocation | Opt. Regret | Uni. Regret | |

|---|---|---|---|

| [5,4,1] | |||

| [16,13,1] | |||

| [57,42,1] | |||

| [172,126,2] |

7 Conclusion

This work introduced a novel regret bound when using estimate-then-optimize and a method for using this bound to optimize the experimental design under distributional assumptions on the underlying model parameter. To justify our theory, we analyzed three examples in detail, including a realistic application to pandemic control.

There are several directions in theory and application which would address some limitations of our method.

From a theoretical perspective, it would be interesting to consider how our approach could be extended to make decisions about whether to use only a subset of the uncertain parameters . For instance, one may be able to conclude that because the regret is insensitive to some components of , it may be okay to drop them completely in the experiment while still maintaining a good decision.

Similarly, one could feasibly use a similar approach for the more general problem of model selection. In this case, the may be infinite-dimensional in order to capture non-parametric models. As such, we imagine more technical machinery would likely be necessary.

Finally, we are improving the ability to make decisions based on data. When this is used by those whose goals are aligned with the broader society, then this should tend to improve societal outcomes, but our results could also be used by those whose goals are not so-aligned.

References

- Farias [2007] V Farias. Revenue management beyond estimate, then optimize. Unpublished doctoral thesis, Stanford University, Stanford, CA, 2007.

- Hu et al. [2020] Yichun Hu, Nathan Kallus, and Xiaojie Mao. Fast rates for contextual linear optimization. arXiv preprint arXiv:2011.03030, 2020.

- Wu et al. [2018] Di Wu, Helin Zhu, and Enlu Zhou. A bayesian risk approach to data-driven stochastic optimization: Formulations and asymptotics. SIAM Journal on Optimization, 28(2):1588–1612, 2018.

- Bertsimas et al. [2018] Dimitris Bertsimas, Vishal Gupta, and Nathan Kallus. Data-driven robust optimization. Mathematical Programming, 167(2):235–292, 2018.

- Foster and Syrgkanis [2019] Dylan J Foster and Vasilis Syrgkanis. Orthogonal statistical learning. arXiv preprint arXiv:1901.09036, 2019.

- Elmachtoub and Grigas [2022] Adam N Elmachtoub and Paul Grigas. Smart “predict, then optimize”. Management Science, 68(1):9–26, 2022.

- El Balghiti et al. [2019] Othman El Balghiti, Adam N Elmachtoub, Paul Grigas, and Ambuj Tewari. Generalization bounds in the predict-then-optimize framework. Advances in neural information processing systems, 32, 2019.

- Ito et al. [2018] Shinji Ito, Akihiro Yabe, and Ryohei Fujimaki. Unbiased objective estimation in predictive optimization. In International Conference on Machine Learning, pages 2176–2185. PMLR, 2018.

- Wilder et al. [2019] Bryan Wilder, Bistra Dilkina, and Milind Tambe. Melding the data-decisions pipeline: Decision-focused learning for combinatorial optimization. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 1658–1665, 2019.

- Vapnik [1999] Vladimir Vapnik. The nature of statistical learning theory. Springer science & business media, 1999.

- Kim et al. [2015] Sujin Kim, Raghu Pasupathy, and Shane G Henderson. A guide to sample average approximation. Handbook of simulation optimization, pages 207–243, 2015.

- Song and Nelson [2015] Eunhye Song and Barry L Nelson. Quickly assessing contributions to input uncertainty. IIE Transactions, 47(9):893–909, 2015.

- Freimer and Schruben [2002] Michael Freimer and Lee Schruben. Collecting data and estimating parameters for input distributions. In Proceedings of the Winter Simulation Conference, volume 1, pages 392–399. IEEE, 2002.

- Pukelsheim [2006] Friedrich Pukelsheim. Optimal design of experiments. SIAM, 2006.

- Hastie et al. [2009] Trevor Hastie, Robert Tibshirani, Jerome H Friedman, and Jerome H Friedman. The elements of statistical learning: data mining, inference, and prediction, volume 2. Springer, 2009.

- Guo et al. [2006] Hongbin Guo, Michael Y Li, and Zhisheng Shuai. Global stability of the endemic equilibrium of multigroup sir epidemic models. Canadian applied mathematics quarterly, 14(3):259–284, 2006.

- Mossong et al. [2008] Joël Mossong, Niel Hens, Mark Jit, Philippe Beutels, Kari Auranen, Rafael Mikolajczyk, Marco Massari, Stefania Salmaso, Gianpaolo Scalia Tomba, Jacco Wallinga, et al. Social contacts and mixing patterns relevant to the spread of infectious diseases. PLoS medicine, 5(3):e74, 2008.

- Vershynin [2018] Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- Hsu et al. [2012] Daniel Hsu, Sham Kakade, and Tong Zhang. A tail inequality for quadratic forms of subgaussian random vectors. Electronic Communications in Probability, 17:1–6, 2012.

Appendix A Proofs

A.1 Proof of Theorem 3.4

Proof.

By taking the second order Taylor expansion on at , there exists such that

Observe that because is a convex set containing both and (it contains by construction and it contains by the assumption made in the statement of the theorem), and lies on a line between and .

By strong convexity, and because , we have that

Combining the previous two equations, we have

| (6) |

Now consider the second order Taylor expansion on with respect to , wherein we have that there exists such that

Using first-order optimality of , we can express this exactly as

which by the second-order smoothness assumption implies

Combining these with equation (1) yields

As the left is positive, so is the right, and we can square both sides to yield a valid inequality:

where the first inequality uses that and the second uses Cauchy-Schwarz.

As is not meaningful to consider, we assume so that dividing through by yields

| (7) |

Now we use a final Taylor expansion to conclude that there exists such that

| (8) |

Combining (2) with (3) yields

| (9) |

∎

A.2 Proof of Lemma 4.3

Proof.

We observe that under assumption 4.1, we have that

where and is the -dimensional identity matrix.

We then appeal to equation (3.7) in Vershynin [2018], which gives a high probability bound for the norm of a multivariate Gaussian.

In particular, we have that

for a universal constant and where .

Under assumption 4.2, we first observe that trivially . Furthermore, by definition of openness we know there exists some -ball . Since we desire that lies in this ball, we solve for such that

to yield the high probability event that lying in this ball.

This yields

For , we have that is positive for a valid bound.

Plugging this into the probability bound, we get the probability that is bounded above by .

Taking larger than, say, , we have an upper bound of .

So for sufficiently large, i.e. , taking the complementary event concludes the proof.

∎

A.3 Proof of Theorem 4.4

Proof.

By the previous theorem, when .

Therefore, the probability that

is bounded above by the sum of

-

•

the probability that .

-

•

the probability that ,

-

•

the probability that .

By the lemma, the probability that is bounded above by .

By Hsu et al. [2012], the probability that

is bounded above by Choosing yields the first term in bound.

For the little- term, the same bound from Hsu et al. [2012] yields

with probability . Taking the same yields a term which is (note and are within a constant factor corresponding to eigenvalues of .)

Then by the union bound, the probability that is bounded above by . Taking the complementary event completes the proof.

Finally, we note that, as a function of , the first trace term is the dominant term because is symmetric and PSD, and therefore all eigenvalues are nonnegative. Therefore the sum of the eigenvalues (the trace), or equivalently the 1-norm of the eigenvalues, is larger than the 2-norm (the second trace term), and also larger than the largest eigenvalue (the 2-norm term).

∎

Remark.

The choice of in the bound above is due to the following argument. Suppose lies in some compact set. Then there exists some upper bound on the regret, say . Then for large , an upper bound on the expected regret reduces to Minimizing this as a function of yields .

A.4 Verifying Assumptions for Pricing Example

One may easily derive the following

| (10) |

To verify the convexity assumptions, first note that setting (10) to 0 yields that the optimal solution satisfies

(This is not a closed form solution as the RHS depends on , but it shows that .)

Furthermore, the second derivative of with respect to is

| (11) |

Therefore we get

since we assumed . Also, for any , it is easy to see that this is bounded away from 0 for in a neighborhood around .

Furthermore, we observe that Equation (11) is clearly bounded for and for all since the logistic function decays exponentially.

Finally, it remains to check the Hessian of (10) with respect to . One can straightforwardly derive the expressions for the terms of the Hessian:

Each term in the Hessian includes a multiplicative factor of . Therefore for any and any , each term in the Hessian, and thus also its largest eigenvalue, must remain bounded as the logistic function decays exponentially.

Appendix B Implementation Details for Pandemic Example

For our pandemic application, we built a discrete-time simulation of the multi-group SIR model as described in the paper. In particular, for time , we have that

where denotes entrywise product and denotes a vector of ones. We treat as the output of the simulation, where recall that .

When optimizing with respect to the decision variable for a given , we use L-BFGS-B. Since L-BFGS-B is used for unconstrained problems, we reparameterized the problem to only have bounds on the variables instead of constraints. In particular, we define another set of variables , where is the proportion of testing capacity used by the first group, is the proportion of the testing capacity which remains that the second group uses. Therefore we may include , which is amenable to usage by L-BFGS-B.

We use finite difference estimates for the derivative term , with step size . In particular, we use

Finally, , the trace term is minimized in closed-form. In particular, it is easy to see that we have a problem of the form (after relaxing integrality)

| s.t. | |||

where for the variance of a random variable.

The Karush-Kuhn-Tucker conditions yield the closed-form solution

and we round the solution to the nearest integer (rounding the first two and taking the difference from as ). If is 0 (which we disallow as then no samples are collected), we set and decrement one of each with probability 0.5.

Appendix C Additional Experiments

C.1 Pricing

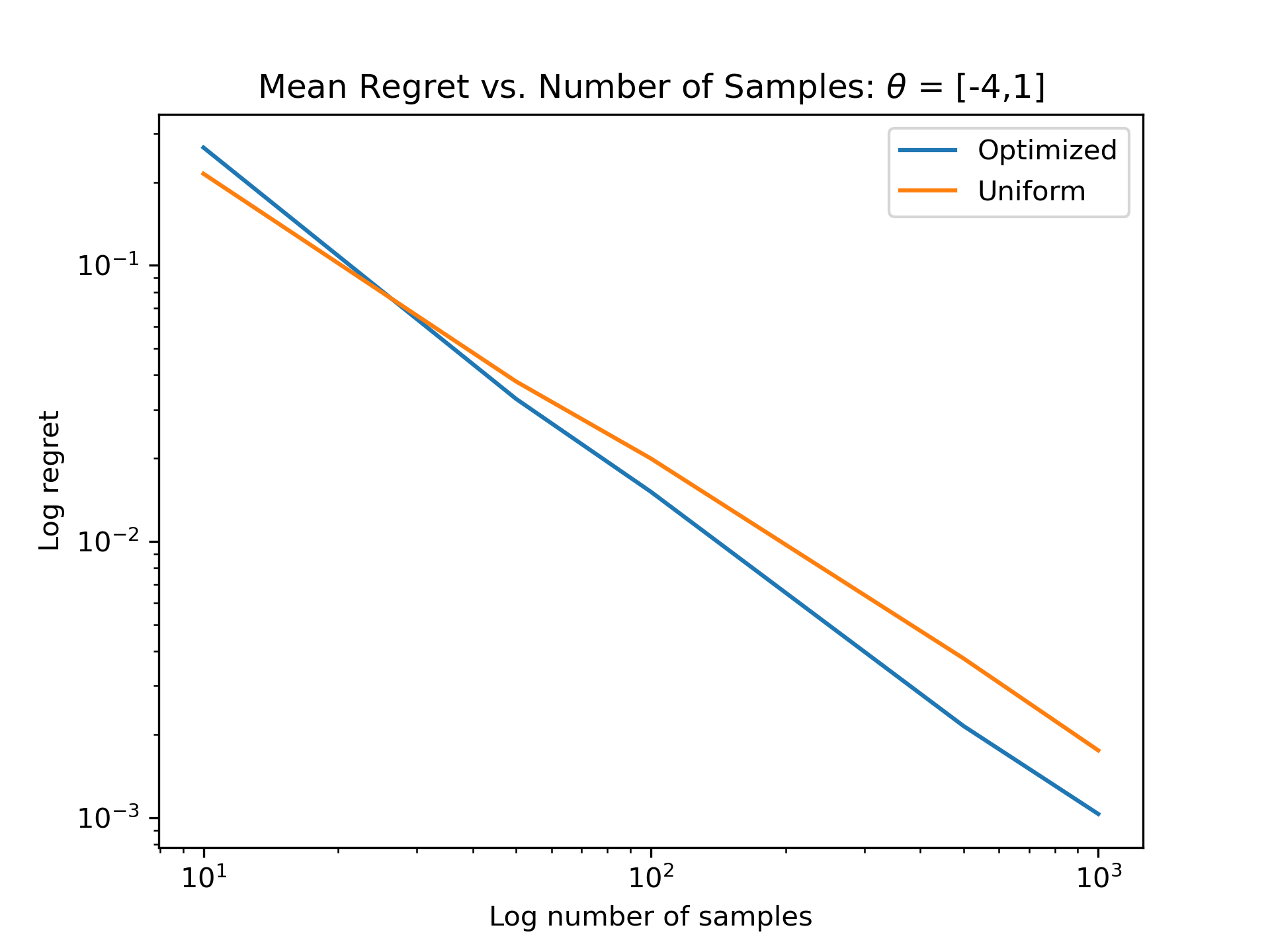

Figure 5 shows regret versus the number of samples used for the allocation, for a particular choice of . The linear relationship on the log-log scale confirms that the regret behaves as . This aligns with our regret bound behaving as , where the is obscured.

We also see from the above graph that the relative improvement of our optimal allocation improves as increase. Table 4 shows the regret of the optimal and uniform allocations for samples and more values of , showing further relative improvement relative to when .

| Optimized Allocation | Uniform Allocation | |

|---|---|---|

C.2 Pandemic

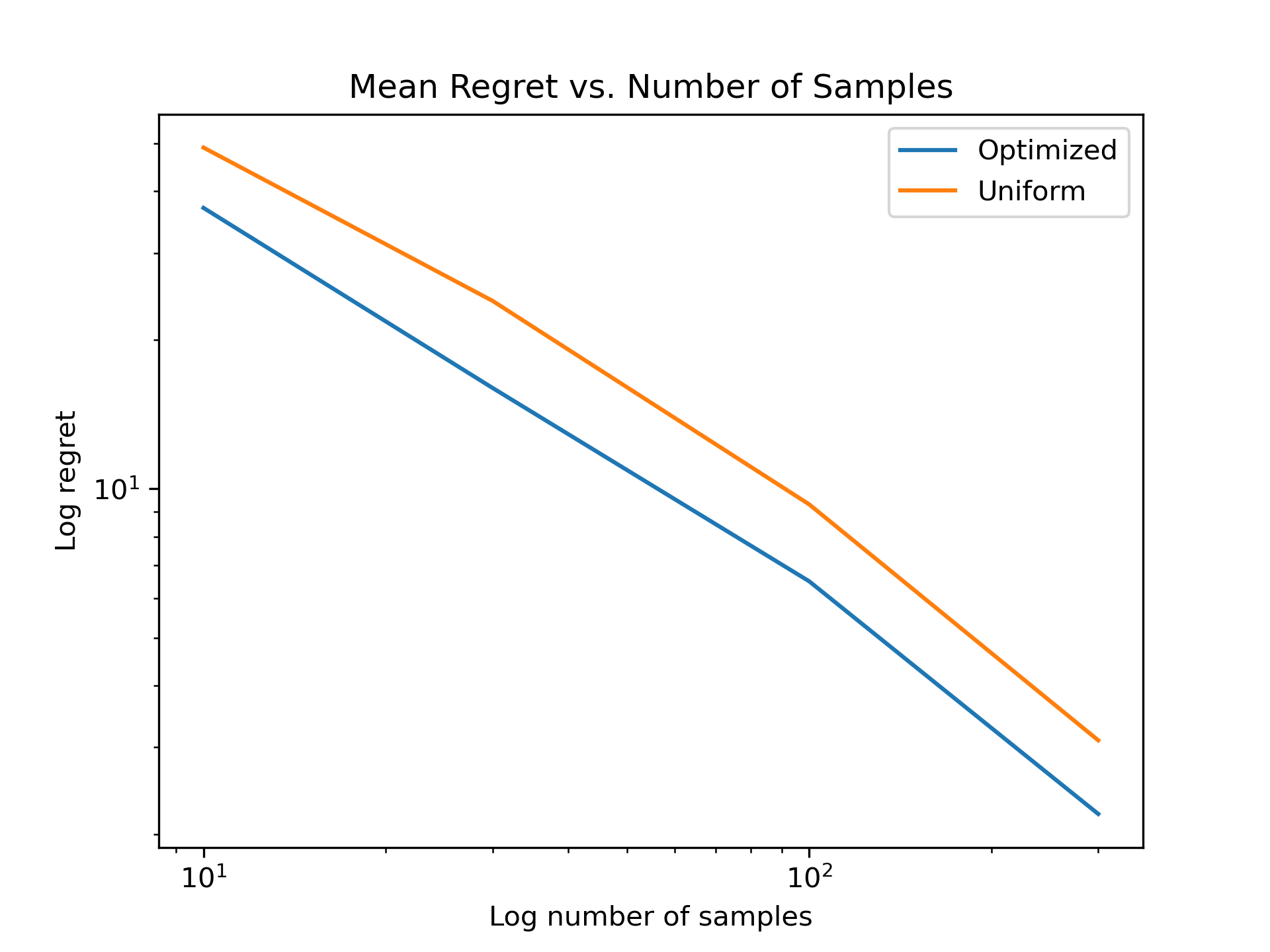

Figure 6 shows the analogous plot of regret vs number of samples allocated to Figure 5 from the pricing example. Again, we see the roughly linear relationship on the log-log scale confirms that the regret behaves as , agreeing with our bound.

Appendix D Code

Please find all code used at this anonymized repository: https://anonymous.4open.science/r/ExpDesign4ETO-DEB3/.