One Arrow, Two Kills: An Unified Framework for

Achieving Optimal Regret Guarantees in Sleeping Bandits

Abstract

We address the problem of ‘Internal Regret’ in Sleeping Bandits in the fully adversarial setup, as well as draw connections between different existing notions of sleeping regrets in the multiarmed bandits (MAB) literature and consequently analyze the implications: Our first contribution is to propose the new notion of Internal Regret for sleeping MAB. We then proposed an algorithm that yields sublinear regret in that measure, even for a completely adversarial sequence of losses and availabilities. We further show that a low sleeping internal regret always implies a low external regret, and as well as a low policy regret for iid sequence of losses. The main contribution of this work precisely lies in unifying different notions of existing regret in sleeping bandits and understand the implication of one to another. Finally, we also extend our results to the setting of Dueling Bandits (DB)–a preference feedback variant of MAB, and proposed a reduction to MAB idea to design a low regret algorithm for sleeping dueling bandits with stochastic preferences and adversarial availabilities. The efficacy of our algorithms is justified through empirical evaluations.

1 Introduction

The problem of online sequential decision-making in standard -armed multiarmed bandit (MAB) is well studied in machine learning [4, 45] and used to model online decision-making problems

under uncertainty. Due to their implicit exploration-vs-exploitation tradeoff, bandits are able to model clinical trials, movie recommendations, retail management job scheduling etc., where the goal is to keep pulling the ‘best-item’ in hindsight through sequentially querying one item at a time and subsequently observing a noisy reward feedback of the queried arm [14, 5, 4, 1, 10]. However, from a practical viewpoint, the decision space (or arm space ) often changes over time due to unavailability of some items: For example, some items might go out of stock in a retail store, some websites could be down, some restaurants might be closed etc. This setting is studied in the multiarmed bandit (MAB) literature as sleeping bandits [22, 26, 20, 19], where at any round the set of available actions could vary stochastically [26, 13] or adversarially [19, 23, 20]. Over the years, several lines of research have been conducted for sleeping multi-armed bandits (MAB) with different notions of regret performance, e.g. policy, ordering, or sleeping external regret [8, 26, 39].

In this paper, we introduce a new notion of sleeping regret, called Sleeping Internal Regret, that helps to bridge the gaps between different existing notions of sleeping regret in MAB. We show that our regret notion can be applied to the fully adversarial setup, which implies sleeping external regret in the fully adversarial setup (i.e. when both losses and item availabilities are adversarial), as well as policy regret in the stochastic setting (i.e. when losses are stochastic). We further propose an efficient worst-case regret algorithm for sleeping internal regret. Finally we also motivate the implication of our results for the Dueling Bandits (DB) framework, which is an online learning framework that generalizes the standard multiarmed bandit (MAB) [5] setting for identifying a set of ‘good’ arms from a fixed decision-space (set of items) by querying preference feedback of actively chosen item-pairs [49, 2, 52, 35, 36]. The main contributions can be listed as follows:

-

•

Connecting Existing Sleeping Regret. The first contribution (Sec. 2) lies in relating the existing notions of sleeping regret given as:

-

–

The first one, sleeping external regret, is mostly used in prediction with expert advice [8, 16]. If the learner had played instead of at all rounds where was available, we want the learner to not incur large regret. It is well-used to design dynamic regret algorithms [28, 51, 11, 50, 46]. It has the advantage that efficient no-regret algorithms can be designed even when both and losses are adversarial.

-

–

The second one, called ordering regret, is mostly used in the bandit literature [23, 39, 21, 27]. It compares the cumulative loss of the learner, with the one of the best ordering that selects the best available action according to at every round. No efficient algorithm exists when both and are adversarial: either or should be i.i.d [23].

- –

-

–

-

•

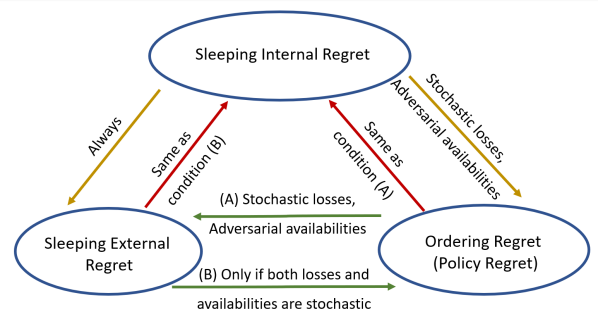

General Notion of Sleeping Regret. Our second and one of the primary contribution lies in introducing a new notion of sleeping regret, called Internal Sleeping Regret (1), which we show actually unifies the different notions of sleeping regret under a general umbrella (see Fig. 1): We show that (i) Low sleeping internal regret always implies a low sleeping external regret, even under fully adversarial setup. (ii) For stochastic losses is also implies a low ordering regret (equivalently policy regret), even under adversarial availabilities. Thus we now have a tool, Sleeping Internal Regret, optimizing which can simultaneously optimize all the existing notions of sleeping regret (and justifies the title of this work too!) (Sec. 2.3).

-

•

Algorithm Design and Regret Implications. The main contribution of this works is to propose an efficient algorithm (SI-EXP3, Alg. 1) w.r.t. Sleeping Internal Regret, and design an regret algorithm (Thm. 4). As motivated, the generalizability of our regret further implies external regret at any setting and also ordering regret for i.i.d losses Rem. 3. We are the first to achieve this regret unification with only a single algorithm (Sec. 3).

-

•

Extensions: Generalized Regret for Dueling-Bandits (DB) and Algorithm. Another versatility of Internal Sleeping Regret is it can be made useful for designing no-regret algorithms for the sleeping dueling bandits (DB) setup, which is a relative feedback based variant of standard MAB [52, 2, 7] (Sec. 4).

-

–

General Sleeping DB. Towards this, we propose a new and more unifying notion of sleeping dueling bandits setup that allows the environment to play from different subsets of available dueling pairs () at each round . This generalizes standard notion of DB setting where without sleeping, but also the setup of Sleeping DB for , [31].

- –

-

–

Optimal Algorithm Design. Having established this new notion of sleeping regret in dueling bandits, we propose an efficient and order optimal sleeping DB algorithm, using a reduction to MAB setup [32] (Thm. 5). This improves the regret bound of [31] that only get worst-case regret even in the simpler setting.

-

–

-

•

Experiments. Finally, in Sec. 5, we corroborate our theoretical results with extensive empirical evaluation (see Sec. 5). In particular, our algorithm significantly outperforms baselines as soon as there is dependency between and . Experiments also seem to show that our algorithm can be used efficiently to converge to Nash equilibria of two-player zero-sum games with sleeping actions (see Rem. 5).

Related Works. The problem of regret minimization for stochastic multiarmed bandits (MAB) is widely studied in the online learning literature [5, 1, 25, 3], and as motivated above, the problem of item non-availability in the MAB setting is a practical one, which is studied as the problem of sleeping MAB [22, 26, 20, 19], for both stochastic rewards and adversarial availabilities [19, 23, 20] as well as adversarial rewards and stochastic availabilities [22, 26, 13]. In case of stochastic rewards and adversarial availabilities the achievable regret lower bound is known to be , being the number of actions in the decision space . The well studied EXP algorithm does achieve the above optimal regret bound, although it is computationally inefficient [23, 19]. The optimal and efficient algorithm for this case is by [39], which is known to yield regret,111 notation hides the logarithmic dependencies..

On the other hand over the last decade, the relative feedback variants of stochastic MAB problem has seen a widespread resurgence in the form of the Dueling Bandit problem, where, instead of getting noisy feedback of the reward of the chosen arm, the learner only gets to see a noisy feedback on the pairwise preference of two arms selected by the learner [52, 53, 24, 47, 40, 38, 30, 41], or even extending the pairwise preference to subsetwise preferences [44, 9, 33, 36, 37, 17, 29].

Surprisingly, there has been almost no work on dueling bandits in sleeping setup, despite the huge practicality of the problem framework. In a very recent work, [31] attempted the problem of Sleeping DB for the setup of stochastic preferences and adversarial availabilities, however there proposed algorithms can only yield a suboptimal regret guarantee of . Our work is the first to achieve regret for Sleeping Dueling Bandits (see Thm. 5).

2 Problem Formulation

In this section, we introduce problem of sleeping multiarmed bandit formally, followed by the definition of Internal Sleeping Regret – a new notion of learner’s performance in sleeping MAB (Sec. 2.3). The last part of this section discusses the different notions of existing regret bounds in Sleeping MAB (Sec. 2.1) and their connections (Sec. 2.2, summarized in Fig. 1).

Problem Setting: Sleeping MAB.

Let be a set of arms. At each round , a set of available arms is revealed to a learner, that is asked to select an arm , upon which the learner gets to observe the loss of the selected arm. Note the sequence of item-availabilities as well as the loss sequence can be stochastic or adversarial (oblivious) in nature. We consider the hardest setting of adversarial losses and availabilities, which clearly subsumes the other settings as special cases (see Sec. 2.3 for details).

The next thing to understand is how should we evaluate the learner or what is the final objective? Before proceeding to our unifying notion of Sleeping MAB regret, let us do a quick overview of existing notions of sleeping MAB regret studied in the prior bandit literature.

2.1 Existing Objectives for Sleeping MAB

1. External Sleeping Regret.

2. Ordering Regret.

This second notion compares the performance of the learner on all rounds, with any fixed ordering of the arms, where denotes the set of all possible orderings of :

| (2) |

where denotes the best arm available in . Consequently, in this case, the learner’s regret is evaluated is evaluated against the best ordering .

It is known that no polynomial time algorithm can achieve a sublinear regret without stochastic assumptions on the losses or the availabilities , as the problem is known to be NP-hard when both rewards and availabilities are adversarial [23, 20, 19]. For adversarial losses and i.i.d. (where each arm is independently available according to a Bernoulli distribution), [39] proposed an algorithm with regret. For i.i.d. losses and adversarial availabilities, a UCB based algorithm with logarithmic regret was proposed in [23].

3. Policy Regret

A policy denotes here a mapping from a set of available actions/experts to an item. Let be the class of all policies. In this case, the regret of the learner is measured against a fixed policy is defined as:

| (3) |

where the expectation is taken w.r.t. the availabilities and the randomness of the player’s strategy [39]. As usual, in this case, the learner’s regret is evaluated is evaluated against the best policy .

2.2 Relations across Different Notions of Existing Sleeping MAB Regret

One may wonder how these above notions are related. Is one stronger than the other? Or does optimizing one implies optimizing the other? Under what assumptions on the sequence of losses and availabilities ? We answer all these questions in this section and also summarized them in Fig. 1.

1. Relationship between (ii) Ordering Regret and (iii) Policy Regret.

These two notions are very close, in principle they are equivalent in all practical contexts where they can be controlled. Note for stochastic losses and availabilities, it is easy to see both are equivalent, i.e. . In fact, even when either losses or the availabilities are stochastic, and losses are independent of the availabilities (which are the only settings in which algorithms exist for these notions), we can claim the same equivalence! See Sec. A.3 for a proof. Thus, for the rest of this paper, we will only work with Ordering Regret ().

2. Relationship between (i) External Sleeping Regret and (ii) Ordering Regret.

-

•

Does Ordering Regret (2) Implies External Regret (1)?

-

–

Case (i): Stochastic losses, Adversarial : Yes, in this case it does. Since losses are stochastic, let at any round , for all . Then,

where the first inequality simply follows by the definition of , being the best ordering in the hindsight, and by noting that for i.i.d. losses for any , .

-

–

Case (ii): Adversarial losses, Stochastic : The implication does not hold in this case. We can construct examples to show that it is possible to have but for some (see App. A). The key observation lies in making the losses dependent of availability .

-

–

-

•

Does External Regret (1) Implies Ordering Regret (2)? Clearly, this direction is not true in general, as indeed, it would otherwise contradict the hardness result for ordering regret: This is since minimizing ordering regret is known to be NP-Hard for adversarial and [23], while one can easily construct efficient regret algorithms for external regret in the fully adversarial setup, e.g. even our proposed algorithm SI-EXP3 achieves that (see Rem. 3). Let us analyze in a more case by case basis:

-

–

Case (i) Stochastic losses, Adversarial : No! Even for i.i.d. losses the implication does not hold for adversarial sleeping. To see this, we consider the following counter example with three arms (). Assume that the arms incur constant losses when they are available. During the first rounds, we set so that the worst arm is unavailable and during the last rounds, the best arm is the one that is sleeping, i.e., . Then, an algorithm that selects the first arm for and the worst arm for satisfies for any . Yet, because the algorithm chooses the worst arm instead of when .

-

–

Case (ii) Adversarial losses, Stochastic : The implication is not true in this case as well. We can simply do the same counter-example by taking i.i.d. availability sets: with probability and otherwise.

This essentially shows ordering regret is a stronger notion of regret compared to external regret.

-

–

To summarize the above relations, precisely, we present them pictorially in Fig. 1. However, it is already hard to keep track of the relations of so any different notions of regret! An even more daunting task is, which one to work with? Does optimizing one, necessarily guarantee a low regret in another? we are seeking for a more general sleeping notion that would imply both. To solve this, we introduce thereafter a new notion of sleeping MAB regret that unifies the above notions of regret under a general umbrella.

2.3 Internal Sleeping Regret: A New Performance Objective for Sleeping MAB

The notion of Internal Regret was introduced in the theory of repeated games [15], and largely studied in online learning since then, see among other [12, 42, 43, 8]. Roughly, a small internal regret for some pair implies at any round , learner would not have regretted playing , where she actually played arm- instead. Drawing motivation, for our sleeping MAB setup, we define the notion as follows:

Definition 1 (Internal Sleeping Regret).

For any pair of arms , the internal sleeping regret is

| (4) |

Typically, optimizing implies, we want that if the learner had played on all the rounds where he played and was available, he does not incur large regret. The strength of this notion is that it can be minimized efficiently (as detailed in Sec. 3) for general adversarial losses and availabilities which is the key behind our main results (see Rem. 3 and 4).

2.4 Generalizing Power of Internal Sleeping Regret

In this section, we discuss, how generalizes the other existing notions of sleeping regret as discussed in Sec. 2.1.

1. Internal Regret vs External Regret

We start by noting that following is a well-known result in the classical online learning setting [43] (without sleeping).

Lemma 2 (Internal Regret Implies External Regret Always[43]).

For any sequences , , and any algorithm, for all .

The proof follows from the regret definitions. Thus any uniform upper-bound on the internal regret, implies the same bound for the external regret up to a factor . The other direction is not true though!

2. Internal Sleeping Regret vs Ordering Regret

Lemma 3 (Internal Regret Implies Ordering (for stochastic Losses)).

Assume that the losses are i.i.d.. Then, for any ordering , we have

where is the set of arms such that .

Therefore, any algorithm that satisfies , also satisfies . The proof is deferred to the Sec. A.4.

Remark 1.

An interesting research direction for the future would be to see if the sleeping internal regret also implies the ordering regret for adversarial losses and stochastic availabilities? Our experiments seem to point into this direction (see App. D), but despite our efforts, we could not prove it. Such a result would in particular imply that any algorithm that can achieve sublinear regret w.r.t. sleeping internal regret (we in fact proposed such an algorithm in Sec. 3, see SI-EXP3), would actually satisfy a best-of-both worlds guarantee! That is if either the losses or the availabilities are stochastic, the algorithm it will in turn incur a sublinear regret w.r.t. ordering regret as well.

Remark 2.

3 SI-EXP3: An Algorithm for Minimizing Internal Sleeping Regret

We now consider the problem setting of Sleeping MAB Sec. 2 and propose an EXP3 based algorithm that is shown to yield sublinear sleeping regret guarantee. It is worth noting that, our algorithm applies to the hardest setting of adversarial losses and availabilities, which clearly subsumes the stochastic settings (losses or availabilities) as a special case: As proved in Thm. 4, our proposed algorithm SI-EXP3 achieves internal regret for any arbitrary sequence of losses and availabilities . Further the generalizability of our internal regret (see Fig. 1) implies external regret at any setting and also ordering regret for i.i.d losses, as detailed in Rem. 3.

Our regret analysis is inspired from the construction of [42] (see Section 3, Thm. 3.2) for the internal regret although the ‘sleeping component’ or item non-avilabilities is not considered. Another relevant work is [8], which designs an algorithm minimizing a variant of internal sleeping regret with a subtle difference: it considers time selection functions instead of sleeping actions. More precisely, the regret considered by [8] is of the form

Thus would correspond to the choice , but the dependence on the arm is not possible in their definition and makes the adaptation of their algorithm challenging. Furthermore, their regret bound (Thm. 18) only holds in the full information setting. It may be adapted to bandit feedback, but would yield a suboptimal regret (which is the internal regret upper-bound they obtain in Thm. 11 without the sleeping component) in comparison with Thm. 4. We now describe our main algorithm, SI-EXP3, for optimizing Internal Sleeping Regret.

3.1 Algorithm: SI-EXP3

The Sleeping-Internal-EXP3 (SI-EXP3) procedure is a two-level algorithm. At round , the master algorithm forms a probability vector over the arms, which is used to sample the played action . The vector is such that for any . A subroutine, based on EXP3 [5], combines sleeping experts indexed by , for . Each expert aims to minimize the internal sleeping regret . We detail below how to construct .

For any , we denote by the probability vector that moves the weight of from to ,

| (5) |

As usually considered in adversarial multi-armed bandits, for any active arm , we define the associated estimated loss . Furthermore, by abuse of notation, we also define for any , the loss

| (6) |

The subroutine then computes the exponential weighted average of the experts , by forming the weights

| (7) |

To avoid assigning mass from an active item to an inactive , the subroutine then normalizes those weights so that sleeping experts get mass

| (8) |

Finally, the master algorithms forms by solving the linear system

| (9) |

The existence and the practical computation of such a is an application of Lemma 3.1 of [42].

3.2 Regret Analysis of SI-EXP3

We now analyze the sleeping internal regret guarantee of Alg. 1 (Thm. 4), and also the implications to other notions of sleeping regret (Rem. 3).

Theorem 4.

Consider the problem of Sleeping MAB for arbitrary (adversarial) sequences of losses and availabilities . Let and . Assume that for any and . Then,

for all in .

The proof is postponed to Thm. 4. The learning rate can be calibrated online at the price of a small multiplicative constant by choosing a time-varying learning rate or by using the doubling-trick technique [12].

Remark 3.

The above theorem also implies a bound of order for the external sleeping regret by Lem. 2 and for the ordering regret when the losses are i.i.d. by Lem. 3. SI-EXP3 is the first to simultaneously achieve order-optimal sleeping external regret for fully adversarial setup as well as ordering regret for stochastic losses and this was possible owning to the versatility of Sleeping Internal Regret as summarized in Fig. 1.

4 Implications: Better Regret for Sleeping Dueling Bandits

In this section, we show the implication of our result to sleeping dueling bandits.

Motivation behind a generalized DB objective. We show interesting use-cases of our generalization such as when the user is asked at each round to choose two different actions . Note that in the dueling bandit literature, the user may choose replicated arms , and is expected to converge to an optimal pair . However, in many applications, this does not make sense to show users the same pair of items , rather it might be preferred to see their top-two choices, i.e we would expect the algorithm to converge to the best pair , (more motivating examples are provided after Rem. 4). Classical dueling bandit algorithms do not easily allow for such a restriction, whereas this can be easily achieved with our sleeping procedure.

4.1 Our Problem Setting: Sleeping Dueling Bandits (Sleeping DB)

We generalize the setting of for dueling bandits with adversarial sleeping of [31]. We consider the stochastic dueling bandit setting with a preference matrix such that is the probability of item to beat item in some round. Furthermore, we assume that their exists a total ordering of the arms , such that for all and all . This is for instance satisfied for utility-based preference matrices [2], or for Plackett-Luce model [6], where it is assumed that the items are associated to positive score parameters and for all .

Before each round , an adversary reveals a set of possible dueling pairs . We assume that if then . Furthermore, we denote for any by the set of possible adversaries for , and as usual by the set of available arms at time . After observing , the learner selects a pair of items and observes the result of the duel which follows a Bernoulli distribution with mean .

Performance: Internal Sleeping DB regret. We measure the learner’s regret w.r.t. the following regret measure:

| (10) |

Since the definition is inspired from internal regret, we term it as Internal Sleeping DB regret (or SI-DB in short) — the measure essentially evaluates the dueling choices of the learner against their best ‘available competitor’ according to .

Remark 4 (Generalizability of ).

It is noteworthy that if all pairs are available , then is the Condorcet Winner (CW) (see [52] for definition) for all rounds since respects total ordering. Thus, in this case, reduces to the standard CW-regret studied in DB [48, 52, 7]. Moreover, also generalizes the notion of Sleeping Dueling Bandit of [31] for the special case (i.e. when all pairs of the available items are feasible): This is since for this case we again have (owing to the total ordering assumption of ), and hence we can recover their notion of sleeping regret (see Eqn. (1) of [31]). Nevertheless, our new notion offers more flexibility as we now show with some application examples.

Motivating Examples: Practicability of .

(i.) Dueling bandits with non-repeating arms. A first example consists in choosing . Our algorithm will be forced to play two different items at every round. Such a restriction is new to dueling bandits although it makes sense in many applications, such as recommendation systems in which we may want to suggest pairs of different items. Our algorithm will converge to the best pair. An interesting question for future work is to generalize our strategy to any size (possibly larger than 2) of subsets of unique battling items. A similar setting was considered by [34] but they allow choosing replicate items.

(ii). Preference learning with categories. Another example comes from an application in which the arms may be grouped into different categories (or teams). For example, one may thing of a recommendation system for movies. The latter could be action movies, documentaries, TV series, or romantic movies. The system could be asked to suggest at every round movies from different categories to provide diversity into the suggestion. Our algorithm would simultaneously learn the best movies but also the best two categories. In addition, the possibility of sleeping allows the film collection to vary over time.

4.2 Sparring SI-EXP3: An Algorithm for Sleeping DB and Regret Analysis

Following the generic reduction from multi-armed bandit to dueling bandit from [32] (see Section ), we consider the following algorithm. We run two versions and of the internal sleeping regret algorithm of Thm. 4 in parallel. At each round , is chosen by , which is run on the availability sets and losses , . After is chosen, chooses , by using the availability sets and losses . We call the algorithm as Sparring SI-EXP3, following the classical nomenclature from [2] which first invented the idea of designing a DB algorithm by making two MAB algorithms competing against another, and famously termed it as ‘Sparring’.

Theorem 5.

Consider the problem setting of Sleeping DB defined above (Sec. 4) and let . Then, Sparring SI-EXP3 satisfies

The proof is postponed to App. C. As explained in Rem. 4, by choosing of the form for some subset , we retrieve the setting of [31]. Note that they provide distribution dependent upper-bounds while we present worst-case upper-bound. They show a high-probability regret bound of order for an UCB based algorithm, and a upper-bound on the expected regret of an algorithm based on empirical divergences. Their analysis are quite technical and non-trivial to adapt to general sets as our result. Furthermore , both their algorithms yield a worst-case regret of order while we only suffer .

5 Experiments

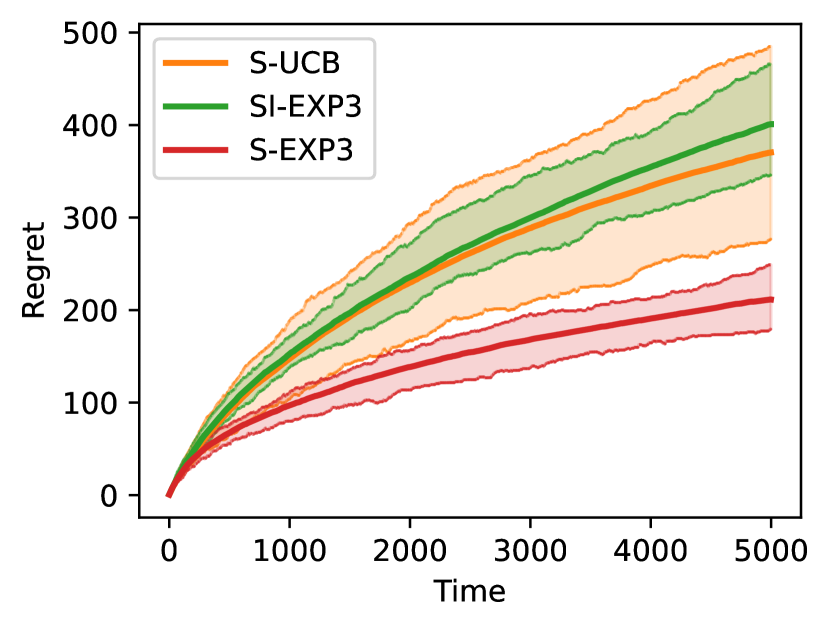

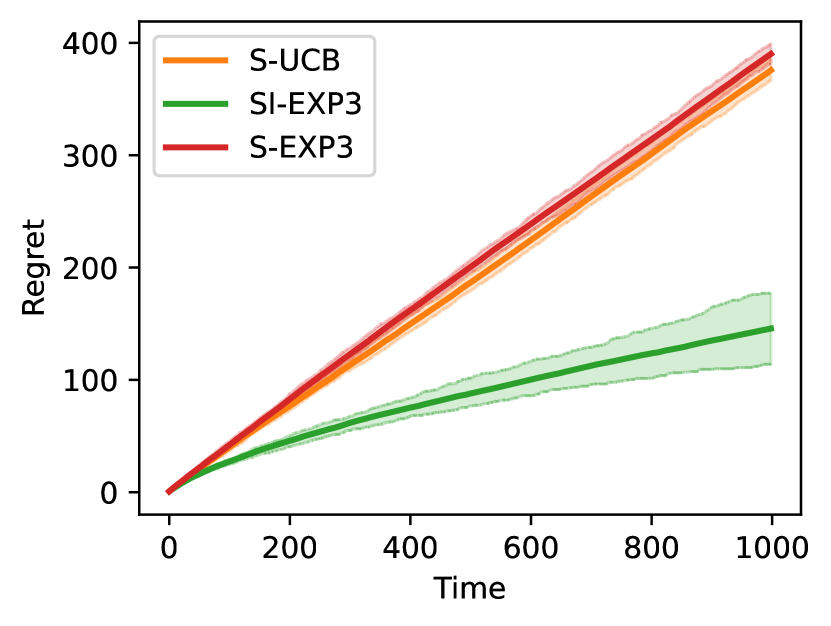

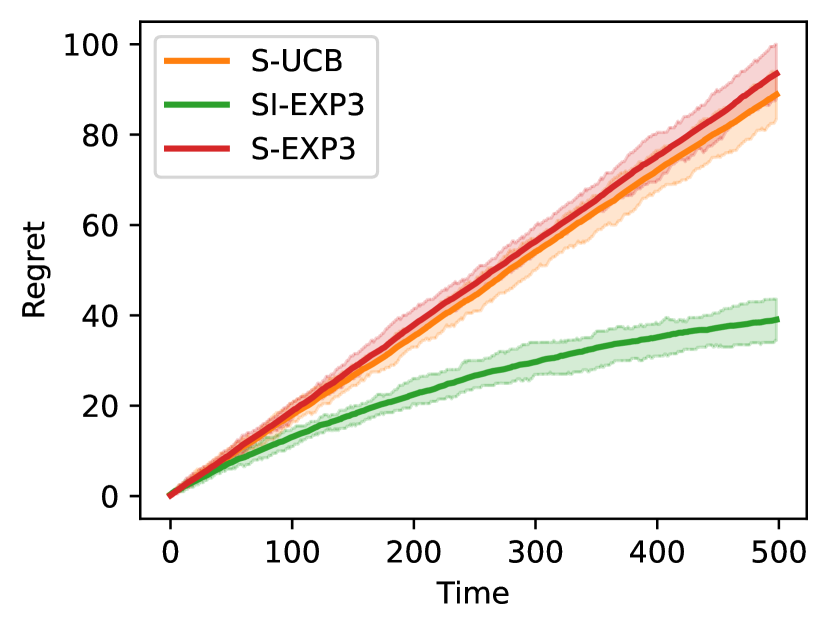

We provide synthetic experiments in sleeping multi-armed bandits. In all the experiments, we plot the policy regret for MAB (3). All experiments are averaged across runs. Further experiments (including some in the dueling setup) are provided in App. D. We compare the results of the following algorithms:

-

•

SI-EXP3: Alg. 1;

-

•

S-UCB: A sleeping UCB procedure [23] for ordering regret with stochastic losses;

-

•

S-EXP3: Sleeping-EXP3G [39] for ordering regret with adversarial losses and i.i.d. sleeping.

We compare to these two algorithms because they achieve state-of-the-art performance in their respective settings. The hyper-parameters of SI-EXP3 and of S-EXP3 are considered as time-varying hyper-parameters and set to .

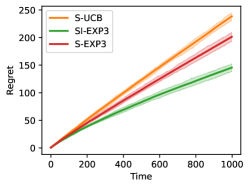

Stochastic environment.

The losses and availabilies for arms are i.i.d. and respectively follow Bernoulli distributions with mean and . The latter are uniformly sampled at the start of each run on . Rounds with no available arms are skipped.

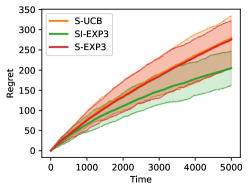

Dependent environment.

We consider the following semi-stochastic environment with . The pairs are still i.i.d. but the losses depend on the availabilities. The sets are first uniformly sampled among and . According to the values of , the loss vectors are then respectively and , where means that the arm is sleeping.

Rock-Paper-Scissors.

We consider a repeated two-player zero-sum game with payoff matrix

We assume that at the start of each round some action may be unavailable ( is uniformly sampled as in the previous environment). The game is then played on only. We consider an opponent that is playing the Nash equilibrium of the sub-games (i.e., the game with the payoff matrix restricted to ) and run each algorithm against that opponent.

Results.

The cumulative regrets are provided in Fig. 2. We find that as soon as there are dependencies between the loss vectors and availabilities, SI-EXP3 significantly outperforms the other two algorithms. This is not surprising: S-EXP3 and S-UCB were indeed designed to perform well with respect to the best fixed ordering. Typically, they first order the actions with respect to their average performance on all rounds, and play the best action that is available in . In case of dependency between and , the best ordering may vary over the rounds and S-UCB and S-EXP3 incur linear regret. Note that this situation can happen often in real life. An example is an internet sales site that wants to offer products. Some products are useless if others are out of stock. For instance, it is less interesting to offer the products of a cooking recipe if some of the ingredients are not available.

Remark 5 (Application to game theory with sleeping actions).

For sleeping two-player zero-sum games, the best policy to play depends on the actions available to the opponent: if Scissors is not available, then Paper is the best action, although when all actions are available the optimal policy is . For instance, the Nash equilibrium of restricted to (Rock, Paper), is (i.e., play Paper). Yet, here, all actions are on average equally good (i.e., taking the expectation over ); and S-UCB and S-EXP3 will converge to when Scissor is unavailable and incur linear regret. On the other hand, SI-EXP3 is able to leverage the dependence between and and choose the right action. In App. D, we provide an additional experiment with two-player zero-sum randomized games (with a random payoff matrix ). An intriguing question for future work is whether SI-EXP3 converges to the Nash equilibrium of each subgame (or whether it obtains sublinear regret against an adversary that plays the Nash of restricted to actions of ).

Perspectives

On a high level, the general theme of this work–to unify different notions of performance measure under a common umbrella and designing efficient algorithms for the general measure–can be applied to several other bandits/online learning/learning theory settings, which opens plethora of new directions.

Specifically as an extension to this work, some of the interesting open challenges could be: (i). to understand if sleeping internal regret also implies the ordering regret for adversarial losses but stochastic availabilities (see Rem. 1). (ii). to derive gap dependent bounds sleeping dueling bandit regret for stochastic preferences and adversarial sleeping, same as derived for its MAB counterpart in [23] or in a recent work [31] which though only gave suboptimal regret guarantees? (iii). to understand if our results can be extended to the subsetwise generalization of dueling bandits, studied as the Battling Bandits [35, 37, 29]; amongst many.

References

- Agrawal and Goyal [2012] Shipra Agrawal and Navin Goyal. Analysis of Thompson sampling for the multi-armed bandit problem. In Conference on Learning Theory, pages 39–1, 2012.

- Ailon et al. [2014] Nir Ailon, Zohar Karnin, and Thorsten Joachims. Reducing dueling bandits to cardinal bandits. In International Conference on Machine Learning, pages 856–864. PMLR, 2014.

- Audibert and Bubeck [2010] Jean-Yves Audibert and Sébastien Bubeck. Best arm identification in multi-armed bandits. In COLT-23th Conference on Learning Theory-2010, pages 13–p, 2010.

- Auer [2000] Peter Auer. Using upper confidence bounds for online learning. In Foundations of Computer Science, 2000. Proceedings. 41st Annual Symposium on, pages 270–279. IEEE, 2000.

- Auer et al. [2002] Peter Auer, Nicolo Cesa-Bianchi, and Paul Fischer. Finite-time analysis of the multiarmed bandit problem. Machine learning, 47(2-3):235–256, 2002.

- Azari et al. [2012] Hossein Azari, David Parks, and Lirong Xia. Random utility theory for social choice. Advances in Neural Information Processing Systems, 25, 2012.

- Bengs et al. [2021] Viktor Bengs, Róbert Busa-Fekete, Adil El Mesaoudi-Paul, and Eyke Hüllermeier. Preference-based online learning with dueling bandits: A survey. Journal of Machine Learning Research, 2021.

- Blum and Mansour [2007] Avrim Blum and Yishay Mansour. From external to internal regret. Journal of Machine Learning Research, 8(6), 2007.

- Brost et al. [2016] Brian Brost, Yevgeny Seldin, Ingemar J. Cox, and Christina Lioma. Multi-dueling bandits and their application to online ranker evaluation. CoRR, abs/1608.06253, 2016.

- Bubeck et al. [2012] Sébastien Bubeck, Nicolo Cesa-Bianchi, et al. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends® in Machine Learning, 5(1):1–122, 2012.

- Campolongo and Orabona [2021] Nicolo Campolongo and Francesco Orabona. A closer look at temporal variability in dynamic online learning. arXiv preprint arXiv:2102.07666, 2021.

- Cesa-Bianchi and Lugosi [2006] Nicolo Cesa-Bianchi and Gábor Lugosi. Prediction, learning, and games. Cambridge university press, 2006.

- Cortes et al. [2019] Corinna Cortes, Giulia Desalvo, Claudio Gentile, Mehryar Mohri, and Scott Yang. Online learning with sleeping experts and feedback graphs. In International Conference on Machine Learning, pages 1370–1378, 2019.

- Even-Dar et al. [2006] Eyal Even-Dar, Shie Mannor, and Yishay Mansour. Action elimination and stopping conditions for the multi-armed bandit and reinforcement learning problems. Journal of machine learning research, 7(Jun):1079–1105, 2006.

- Foster and Vohra [1999] Dean P Foster and Rakesh Vohra. Regret in the on-line decision problem. Games and Economic Behavior, 29(1-2):7–35, 1999.

- Gaillard et al. [2014] Pierre Gaillard, Gilles Stoltz, and Tim Van Erven. A second-order bound with excess losses. In Conference on Learning Theory, pages 176–196. PMLR, 2014.

- Ghoshal and Saha [2022] Suprovat Ghoshal and Aadirupa Saha. Exploiting correlation to achieve faster learning rates in low-rank preference bandits. In International Conference on Artificial Intelligence and Statistics, pages 456–482. PMLR, 2022.

- Hazan et al. [2021] Elad Hazan et al. Introduction to online convex optimization. arXiv:1909.05207, 2021.

- Kale et al. [2016] Satyen Kale, Chansoo Lee, and Dávid Pál. Hardness of online sleeping combinatorial optimization problems. In Advances in Neural Information Processing Systems, pages 2181–2189, 2016.

- Kanade and Steinke [2014a] Varun Kanade and Thomas Steinke. Learning hurdles for sleeping experts. ACM Transactions on Computation Theory (TOCT), 6(3):11, 2014a.

- Kanade and Steinke [2014b] Varun Kanade and Thomas Steinke. Learning hurdles for sleeping experts. ACM Transactions on Computation Theory (TOCT), 6(3):1–16, 2014b.

- Kanade et al. [2009] Varun Kanade, H Brendan McMahan, and Brent Bryan. Sleeping experts and bandits with stochastic action availability and adversarial rewards. 2009.

- Kleinberg et al. [2010] Robert Kleinberg, Alexandru Niculescu-Mizil, and Yogeshwer Sharma. Regret bounds for sleeping experts and bandits. Machine learning, 80(2-3):245–272, 2010.

- Komiyama et al. [2015] Junpei Komiyama, Junya Honda, Hisashi Kashima, and Hiroshi Nakagawa. Regret lower bound and optimal algorithm in dueling bandit problem. In COLT, pages 1141–1154, 2015.

- Lattimore and Szepesvári [2018] Tor Lattimore and Csaba Szepesvári. Bandit algorithms. preprint, 2018.

- Neu and Valko [2014a] Gergely Neu and Michal Valko. Online combinatorial optimization with stochastic decision sets and adversarial losses. In Advances in Neural Information Processing Systems, pages 2780–2788, 2014a.

- Neu and Valko [2014b] Gergely Neu and Michal Valko. Online combinatorial optimization with stochastic decision sets and adversarial losses. Advances in Neural Information Processing Systems, 27, 2014b.

- Raj et al. [2020] Anant Raj, Pierre Gaillard, and Christophe Saad. Non-stationary online regression. arXiv preprint arXiv:2011.06957, 2020.

- Ren et al. [2018] Wenbo Ren, Jia Liu, and Ness B Shroff. PAC ranking from pairwise and listwise queries: Lower bounds and upper bounds. arXiv preprint arXiv:1806.02970, 2018.

- Saha [2021] Aadirupa Saha. Optimal algorithms for stochastic contextual preference bandits. Advances in Neural Information Processing Systems, 34:30050–30062, 2021.

- Saha and Gaillard [2021] Aadirupa Saha and Pierre Gaillard. Dueling bandits with adversarial sleeping. Advances in Neural Information Processing Systems, 34, 2021.

- Saha and Gaillard [2022] Aadirupa Saha and Pierre Gaillard. Versatile dueling bandits: Best-of-both-world analyses for online learning from preferences. arXiv preprint arXiv:2202.06694, 2022.

- Saha and Gopalan [2018a] Aadirupa Saha and Aditya Gopalan. Battle of bandits. In Uncertainty in Artificial Intelligence, 2018a.

- Saha and Gopalan [2018b] Aadirupa Saha and Aditya Gopalan. Battle of bandits. In UAI, pages 805–814, 2018b.

- Saha and Gopalan [2019a] Aadirupa Saha and Aditya Gopalan. Combinatorial bandits with relative feedback. In Advances in Neural Information Processing Systems, 2019a.

- Saha and Gopalan [2019b] Aadirupa Saha and Aditya Gopalan. PAC Battling Bandits in the Plackett-Luce Model. In Algorithmic Learning Theory, pages 700–737, 2019b.

- Saha and Gopalan [2020] Aadirupa Saha and Aditya Gopalan. From pac to instance-optimal sample complexity in the plackett-luce model. In International Conference on Machine Learning, pages 8367–8376. PMLR, 2020.

- Saha and Krishnamurthy [2022] Aadirupa Saha and Akshay Krishnamurthy. Efficient and optimal algorithms for contextual dueling bandits under realizability. In International Conference on Algorithmic Learning Theory, pages 968–994. PMLR, 2022.

- Saha et al. [2020] Aadirupa Saha, Pierre Gaillard, and Michal Valko. Improved sleeping bandits with stochastic action sets and adversarial rewards. In International Conference on Machine Learning, pages 8357–8366. PMLR, 2020.

- Saha et al. [2021a] Aadirupa Saha, Tomer Koren, and Yishay Mansour. Adversarial dueling bandits. In International Conference on Machine Learning, pages 9235–9244. PMLR, 2021a.

- Saha et al. [2021b] Aadirupa Saha, Tomer Koren, and Yishay Mansour. Dueling convex optimization. In International Conference on Machine Learning, pages 9245–9254. PMLR, 2021b.

- Stoltz [2005] Gilles Stoltz. Incomplete information and internal regret in prediction of individual sequences. PhD thesis, Université Paris Sud-Paris XI, 2005.

- Stoltz and Lugosi [2005] Gilles Stoltz and Gábor Lugosi. Internal regret in on-line portfolio selection. Machine Learning, 59(1):125–159, 2005.

- Sui et al. [2017] Yanan Sui, Vincent Zhuang, Joel Burdick, and Yisong Yue. Multi-dueling bandits with dependent arms. In Conference on Uncertainty in Artificial Intelligence, UAI’17, 2017.

- Vermorel and Mohri [2005] Joannes Vermorel and Mehryar Mohri. Multi-armed bandit algorithms and empirical evaluation. In European conference on machine learning, pages 437–448. Springer, 2005.

- Wei et al. [2016] Chen-Yu Wei, Yi-Te Hong, and Chi-Jen Lu. Tracking the best expert in non-stationary stochastic environments. Advances in neural information processing systems, 29, 2016.

- Wu and Liu [2016] Huasen Wu and Xin Liu. Double Thompson sampling for dueling bandits. In Advances in Neural Information Processing Systems, pages 649–657, 2016.

- Yue and Joachims [2009] Yisong Yue and Thorsten Joachims. Interactively optimizing information retrieval systems as a dueling bandits problem. In Proceedings of the 26th Annual International Conference on Machine Learning, pages 1201–1208. ACM, 2009.

- Yue et al. [2012] Yisong Yue, Josef Broder, Robert Kleinberg, and Thorsten Joachims. The -armed dueling bandits problem. Journal of Computer and System Sciences, 78(5):1538–1556, 2012.

- Zhang et al. [2019] Lijun Zhang, Tie-Yan Liu, and Zhi-Hua Zhou. Adaptive regret of convex and smooth functions. In International Conference on Machine Learning, pages 7414–7423. PMLR, 2019.

- Zhao et al. [2020] Peng Zhao, Yu-Jie Zhang, Lijun Zhang, and Zhi-Hua Zhou. Dynamic regret of convex and smooth functions. Advances in Neural Information Processing Systems, 33:12510–12520, 2020.

- Zoghi et al. [2014] Masrour Zoghi, Shimon Whiteson, Remi Munos, Maarten de Rijke, et al. Relative upper confidence bound for the -armed dueling bandit problem. In JMLR Workshop and Conference Proceedings, number 32, pages 10–18. JMLR, 2014.

- Zoghi et al. [2015] Masrour Zoghi, Zohar S Karnin, Shimon Whiteson, and Maarten De Rijke. Copeland dueling bandits. In Advances in Neural Information Processing Systems, pages 307–315, 2015.

Supplementary: One Arrow, Two Kills: An Unified Framework for

Achieving Optimal Regret Guarantees in Sleeping Bandits

Appendix A Appendix for Sec. 2

A.1 Low ordering regret with Adversarial losses, Stochastic availabilities does not imply low external regret

Lemma 6.

There exists a sequence of i.i.d. availabilities and a sequence of losses (possibly depending on ), such that, there exists an algorithm with

as .

Proof.

We provide the following example. Consider a MAB problem with arms, . Suppose the problem encounters the following availability sets uniformly, i.e. for all and , where being the availability set at time . Further let us consider the adversarial (rather set dependent) loss sequence generated as follows:

where can be any arbitrary loss value. For this example, the best orderings are and , that get a cumulative loss equals to in expectation. Indeed,

Consider and algorithm that plays according to the ordering . Then, . It has thus no-regret with respect to any ordering . Yet, its internal regret with respect to action 1 is

This implies a ‘no-regret ordering regret learner’ does not imply a ‘no-regret external regret learner’ for any arbitrary sequence of adversarial losses, stochastic availabilities. ∎

A.2 Low ordering regret with Stochastic losses, Adversarial availabilities does imply low internal regret

Lemma 7.

Let be an i.i.d. sequence of losses. Then, for any sequence of availability sets such that may only depend on

for any algorithm.

Proof.

Consider stochastic losses such that are i.i.d. with mean for all , and any sequence of availability sets (that can only depend on information up to ). Let be an optimal ordering

Then, for all , . Let be the predictions of any algorithm. Let . Then,

where the inequalities are because for any . This concludes the proof. ∎

A.3 Equivalence of Policy and Ordering Regret

The policy regret is a stronger notion than ordering regret in general. From their definitions, we see

because for each ordering , one can associate a policy , such that . But, the other direction is not true in general. Indeed, in the example of Sec. A.1, the inequality is strict. This is due to the dependence between losses and availabilities. Yet, no existing efficient algorithm can handle such dependence neither for policy regret nor for ordering regret. In this appendix, we prove that when either losses or availabilities are i.i.d. with no dependence, then the two notions are equivalent.

Lemma 8 (Stochastic losses and adversarial availabilities).

Let be an i.i.d. sequence of losses. Then, for any sequence of availability sets such that may only depend on , then

for any algorithm.

Proof.

The proof follows from the observation that the best policy with i.i.d. losses is to play the available action with the smallest expected loss. Such a policy corresponds to the ordering for all . Note that this would not be true if could depend on . ∎

Lemma 9 (Adversarial oblivious losses and stochastic rewards).

Let be an arbitrary sequence of losses and be a sequence of i.i.d. availability sets. Then,

for any algorithm.

Proof.

It is important to note here that we consider an oblivious adversary for the loss sequence , which cannot depend on the randomness of . Let be a policy, then

where . Thus, the best policy corresponds to the choice

This policy corresponds to the ordering for . ∎

A.4 Low internal regret with Stochastic losses, Adversarial availabilities does imply low ordering regret

Lemma 10 (Internal Regret Implies Ordering (for stochastic Losses)).

Assume that the losses are i.i.d.. Then, for any sequence of availability sets such that may only depend on , for any ordering , we have

where is the set of arms such that .

Proof.

Let for all . Let be the best ordering such that . Note that for any ordering , we have . Thus, we can restrict ourselves to . Denote by , the best available item in . For any , we also define by the items that are better than . Then,

∎

Appendix B Proof of Thm. 4

Theorem 4.

Consider the problem of Sleeping MAB for arbitrary (adversarial) sequences of losses and availabilities . Let and . Assume that for any and . Then,

for all in .

Proof.

Let denotes the past randomness of the algorithm and the adversary at round . We respectively denote by and the conditional expectation and probability.

Note that follows the prediction of the exponentially weighted average forecaster on the losses . Noting that for all and , and applying the upper-bound on the exponentially weighted average forecaster yields for any (see Thm. 1.5 of [18])

| (11) |

Now, we compute the expectations. Note that , and are -measurable by assumption. Since almost surely, we have for all

Furthermore, by definitions of and , and denoting , we have

Appendix C Proof of Theorem 5

Theorem 5.

Consider the problem setting of Sleeping DB defined above (Sec. 4) and let . Then, Sparring SI-EXP3 satisfies

Proof.

Denote by and by . Then, using that , we have

| (13) |

Let us focus on the first term of the r.h.s, the other one can be analysed similarly.

where . The last inequality is because and for any . Note that does not depend on because of the total ordering assumption. Then, taking the expectation and summing over , we get

where the second to last inequality is by Theorem 4 by construction of which minimizes the internal regret. Similarly, we can show that

Substituting both upper-bounds into (13) concludes the proof. ∎

Appendix D Experiments

D.1 Additional experiments on sleeping multi-armed bandits

In this section, we run some additional experiments to compare the algorithms:

-

•

SI-EXP3: Our proposed algorithm Internal Sleeping-EXP3 described in Sec. 3;

-

•

S-UCB: The sleeping UCB procedure proposed by [23] for ordering regret with stochastic losses;

-

•

S-EXP3: The algorithm Sleeping-EXP3G designed by [39] for ordering regret with adversarial losses and stochastic sleeping.

Again, each experiment is run 50 times and the policy regret is plotted in Figure 3.

Random environment with dependence

This setup is similar to the dependent environment of Sec. 5 where the distribution of are uniformly sampled at the start of each run.

More precisely. We consider the following stochastic environment with . The pairs are i.i.d. and sampled as follows.

At the start of each run, five availability sets are sampled by including independently each action with probability . If a set contains no action, it is sampled again. Then, for each set , a mean vector is uniformly sampled on . Then, for , the availability set is drawn uniformly from and the losses of each arm is sample from a Bernoulli with parameter , where is such that .

Random two-player zero-sum games

This setup is similar to the Rock-Paper-Scissors environment of Sec. 5 but with players and a random payoff matrix.

At the start of each run, a payoff matrix is randomly sampled as follows. For each , , and :

Furthermore, availability sets are randomly sampled by including each action with probability . For each , we compute the Nash equilibrium of the game restricted to actions in . Note that for all . Then, for each , an availability set is uniformly sampled in . The algorithm is asked to choose an action and receives the loss , where is the action chosen by an optimal adversary that follows .

The optimal strategy in this case should be too also follow and would incur . Figure 3 (right) plots the cumulative pseudo-regret . As we can see, SI-EXP3 significantly outperforms S-UCB and S-EXP3. It would be worth to investigate if SI-EXP3 could be used to compute Nash equilibria in repeated two-player zero-sum games with non-available actions.

D.2 Experiments on sleeping dueling bandits

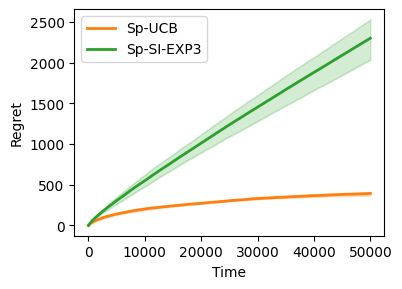

Dueling Bandits with non-repeating arms

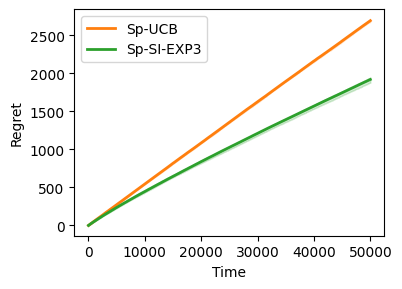

This experimental setup is motivated by the first example in Sec. 4.1 where we want the algorithm to converge to the top 2 items (best pair). We consider utility scores corresponding to the arms, and the preference matrix , with defined as indicating the probability of arm winning over arm . We repeat this experiment for independent runs, by sampling a random utility vector at the beginning of each run. We assume that all the arms are available for the first bandit. All the arms except the one chosen by the first bandit, is available to the second bandit. Each bandit runs its own custom algorithm (which can be UCB, SI-EXP3, etc.). Finally, the winning arm is decided according to and the loss is for the bandit that chose this arm and for the other bandit. In the figures below, we plot the Internal Sleeping DB regret for choices of Sp-UCB and Sp-SIEXP3 (Sparring UCB, SI-EXP3 where both bandits internally use the UCB algorithm and the SI-EXP3 algorithm respectively). In Fig. 4 we plot Sp-SIEXP3 and Sp-UCB and we see that in this relatively simple setting Sp-UCB outperforms Sp-SIEXP3.

Note that despite its surprisingly good performance in Fig. 4, especially for small number of arms, Sp-UCB has no theoretical guarantees for dueling bandits. It would be interesting to study whether such guarantees are possible or whether it has a linear worst-case regret. Furthermore, Sp-UCB strongly assumes a total and fixed ordering of stock performance. As we can see in the following example, Sp-SI-EXP3 works better as soon as there is some dependence between the preference matrix and the availabilities. It is also worth to emphasize that we could not compare with classical dueling bandit algorithm that are not suited for this setting.

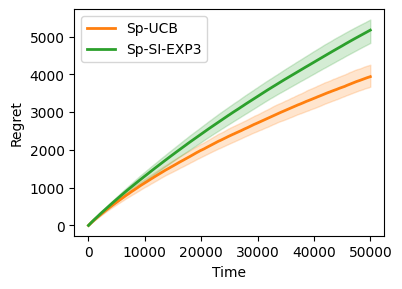

Preference Learning with Categories

In this experimental setup we have availability dependent utility matrices. This is motivated by the following setting: if one item of a category is unavailable, the overall utility values of all items in the category goes down. In the real world, this could be in a setting where I would want to watch a season of a show only if all the seasons are available. Concretely, we have different availability sets, where has all items available except . We also have utility vectors: . At each turn we randomly choose and select and . Similar to the previous setting, the first bandit chooses an available item and the second bandit chooses an available item except the one chosen by the first bandit. In Fig. 5, we choose the utility vectors as and we see that Sp-SIEXP3 significantly outperforms Sp-UCB.