Predicting the State of Synchronization of Financial Time Series using Cross Recurrence Plots

††thanks: Identify applicable funding agency here. If none, delete this.

Abstract

Cross-correlation analysis is a powerful tool for understanding the mutual dynamics of time series. This study introduces a new method for predicting the future state of synchronization of the dynamics of two financial time series. To this end, we use the cross-recurrence plot analysis as a nonlinear method for quantifying the multidimensional coupling in the time domain of two time series and for determining their state of synchronization. We adopt a deep learning framework for methodologically addressing the prediction of the synchronization state based on features extracted from dynamically sub-sampled cross-recurrence plots. We provide extensive experiments on several stocks, major constituents of the S&P100 index, to empirically validate our approach. We find that the task of predicting the state of synchronization of two time series is in general rather difficult, but for certain pairs of stocks attainable with very satisfactory performance111Paper submitted to and under consideration at Pattern and Recognition Letters..

Index Terms:

Cross Recurrence Plot, Synchronization, Convolutional Neural Network, Financial Time SeriesI Introduction

Time series prediction and classification in finance is significantly challenging due to the complexity, multivariate nature, and non-stationary nature of time series in this domain[Murphy, 1999]. Security trading and price dynamics in financial markets are particularly complex due to the interacting nature and inter-connectedness of their underlying driving forces and determinants leading to significant co-movements in stocks’ prices. The characterization and modeling of multivariate time series dynamics have long been discussed in the financial literature, where the prevailing approach is that based on classical econometric theory. Among the multivariate linear models, the most widespread ones are vector autoregressive (VAR) models [Lütkepohl, 1999, Lütkepohl, 1991], vector moving averages and ARMA (autoregressive moving average) models [Reinsel, 1993] and cointegrated VAR models [Juselius, 2006]. Widespread is the use of multivariate conditional heteroskedasticity GARCH-type, see e.g. [Bauwens et al., 2006] for a review, multivariate stochastic volatility models [Harvey et al., 1994], and more methods based on the realized volatility [Chiriac and Voev, 2011, e.g.].

Among the non-linear models the threshold autoregressive model [Tong, 1978], smooth transition autoregressive [Dijk et al., 2002] and Markov switching models [Krolzig, 2013] are nowadays standard approaches. Alternatives include non-parametric methods, functional coefficient [Chen and Tsay, 1993a] and nonlinear additive AR models [Chen and Tsay, 1993b], recurrence analysis, and neural networks. The complexity of modern financial markets running over the so-called limit-order book mechanism is, however, characterized by typical non-linear, noisy, and often non-stationary dynamics. In addition, the high-dimensional nature of the limit-order book flow and complexity of the interactions within it constitute severe limits in the applicability of classic econometric methods for its modeling and forecasting. Besides a very limited number of analytical and tractable models for the order flow and price dynamics in limit-order books [Cont et al., 2010, Huang and Kercheval, 2012, Hawkes, 2018, e.g.], machine learning methods have received much attention [Heaton et al., 2017, Dixon et al., 2020], as they are naturally appealing in this context.

By considering the stock market as a complex system, it is natural to apply such methods for addressing those prediction problems where the application setting and assumptions beneath standard econometric techniques are stringent or inadequate. Indeed, it has extensively been shown that, in financial applications, deep learning (DL) models are often capable of outperforming traditional approaches due to their ability to learn complex data representations based on end-to-end data-driven training, see e.g. [Sezer et al., 2017, Zhang et al., 2019, Tran et al., 2019, Passalis et al., 2020, Shabani et al., 2022a, Haselbeck et al., 2022]. DL models have been adopted for a variety of problems ranging from price prediction [Khare et al., 2017, Fons et al., 2021, Bhandari et al., 2022, Basher and Sadorsky, 2022, Xu and Zhang, 2021], limit-order book-based mid-price prediction [Zhang et al., 2019, Tran et al., 2019, Shabani et al., 2022a, Shabani and Iosifidis, 2020, Shabani et al., 2022b], and volatility prediction [Kyoung-Sook and Hongjoong, 2019, Liu, 2019, Christensen et al., 2021].

Whereas the target of the above literature is generally the analysis and prediction of single time series, this paper focuses on an analysis of stock pair co-movements. Several trading strategies can be put into play to take advantage of co-movements and exploit statistical arbitrages, including pair-trading, portfolio management, or relative and convergence trading strategies applied at an intraday level, e.g., see [Guo et al., 2017] for an overview. While DL provides a basis for prediction given a set of descriptive features, the issue of how to detect and quantify co-movements remains to be addressed. This paper suggests the use of recurrence analysis based on Cross Recurrence Plots (CRP) for detecting and extracting features indicative of stocks’ shared dynamics or co-movements, along with a deep learning framework for predicting whether certain pairs of stocks will exhibit a shared dynamics in the future (in the sense specified in Section II). Not only in the view of extending the ML and applied econometrics literature in this direction, but the possibility of forecasting epochs of time series synchronization is likewise relevant for practitioners.

For detecting and quantifying co-movements or more generally shared dynamical features in time series, the standard econometric approach is that of cross-correlation analysis, e.g., [Tsay, 2005, Chapter 8]. This intuitive linear approach, based on the estimation and perhaps forecasting of cross-correlation matrices, appears to be an element of a much wider theory and methodological approach that has been explored and developed in the last years within a broader generic non-financial setting. Simple cross-correlation analysis has been remarkably extended and generalized towards methods that help explore co-movements between time series within non-linear, noisy, and non-stationary systems of very complex dynamics, either financial [Ma et al., 2013, Bonanno et al., 2001, Ramchand and Susmel, 1998] or not [Webber Jr. and Zbilut, 1994, Marwan and Kurths, 2002, Lancia et al., 2014].

Recurrent analysis [Webber and Marwan, 2015] explores the reconstruction of a phase-space using time-delay embedding for quantifying characteristics of nonlinear patterns in a time series over time [Takens, 1981]. This is done by calculating the so-called Recurrence Plot [Eckmann et al., 1995], the core concept of which is to identify all points in time that the phase-space trajectory of a single time series visits roughly the same area in the phase-space. Recurrence plot analysis has no assumptions or limitations on dimensionality, distribution, stationarity, and size of data [Webber and Marwan, 2015]. These characteristics make it suitable for multidimensional and non-stationary financial time series data analysis. The CRP [Marwan, 1999] is an extension of the recurrence plot, introduced to analyze the co-movement and synchronization of two different time series. The CRP indicates points in time that a time series visits the state of another time series, with possibly different lengths in the same phase-space. These concepts are discussed in further detail in Section II.

In this paper, we propose a method for predicting the state of synchronization over time of two multidimensional 222Throughout the paper, with uni- or multi- variate we refer to the nature of the analyses (RP as opposed to CRP), and with one- or multi- dimensional we refer to the nature of the time series. That is, the RP (as presented in equation (2)) provides a univariate analysis of a single one-dimensional time series, while the CRP (as presented in latter equation (3)) a multivariate analysis of two one-dimensional or multi-dimensional time series. financial time series based on their CRP. In particular, we use the CRP to quantify the co-movements and extract the binary representation of its diagonal elements as the prediction targets for a DL model. For predicting the state of synchronization at the next epoch we employ a Convolutional Neural Network (CNN) that uses as inputs CRPs independently calculated from data-crops obtained by applying fixed-size sliding windows on the time series. Our extensive experiments on 12 stocks of the S&P100 index selected from different sectors show that the proposed method can predict the synchronization of stock pairs with satisfactory performance.

The remainder of the paper is organized as follows. Section II introduces in detail the concepts and theory behind the CRP, with an outlook on its applications in financial and economic problems. Our proposed approach for predicting time instances of time series’ synchronization is presented in Section III. Empirical results on real market data are provided in Section IV, whilst Section V provides conclusions.

II Financial Time Series Recurrence Analysis

Recurrence in the analysis of time series, seen as a nonlinear dynamic system, is the repetition of a pattern over time. The visualization of recurrences in the dynamics of a time series can be expressed via a RP or recurrence matrix[Webber and Marwan, 2015]. In other words, the RP represents the recurrence of the phase-space trajectory to a state. The phase-space of a -dimensional time series with observations , with being the row-vector representing a generic observation at time , is calculated using the time-delay embedding method. State in the phase-space is obtained by

| (1) |

where denotes the delay and is the embedding dimension, , and can, respectively, be determined with the Average Mutual Information Function (AMI) method[Fraser and Swinney, 1986] and the False Nearest Neighbors (FNN) method of [Kennel et al., 1992]. For a uni-dimensional time series is a row vector of size , for a -dimensional times series is a row vector of size . The recurrence state matrix of the reconstructed phase-space, known as Recurrence Plot (RP), at times and , is defined as

| (2) |

where is a threshold distance value, is the Heaviside function, and is the euclidean distance. Due to the underlying embedding (1), is defined for i up to . If two states and are in an -neighbourhood the value of is equal to , otherwise is .The value of highly affects the output of RP. When is too small or too large, the RP cannot identify the true recurrence of states. There are different approaches for finding the best value for in the literature [Webber and Marwan, 2015]. We follow the guidelines provided in [Schinkel et al., 2008] for selecting . The values on the diagonal line of RP are equal to one (i.e., ) because in that case the two states introduced to are identical. The diagonal line of RP is called the Line Of Identity (LOI). Recurrence quantification measures derived from RPs, such as recurrence rate (RR), percent determinism (DET), and maximum line length in the diagonal direction (Dmax) [Webber and Marwan, 2015], give insights about the dynamic behavior of time series. These measures have been used in financial research to analyze the behavior of financial data, e.g. [Bastos and Caiado, 2011, Fabretti and Ausloos, 2005, Yin and Shang, 2016, Hołyst et al., 2001, Zbilut, 2005]. The RP of a time series can be used as a data transformation method for time series prediction. A method employing the RP of seven financial time series to train a deep neural network for predicting the market movement is proposed by [Hailesilassie, 2019]. Several authors have suggested an RP forecasting approach via DL. A feature extraction method exploiting the RP for parsing a DL algorithm is proposed by [Li et al., 2020]. On the other hand, RP can be treated as images enabling the use of different computer-vision techniques for the forecasting task, e.g. [Sood et al., 2021] uses autoencoders or [Han et al., 2021, e.g.] uses a CNN.

The CRP of two multi-dimensional time series [Wallot, 2019] corresponds to an extension of RP which explores the co-movement of two time series, and allows the study of the non-linear dependencies between them. Let us denote by and the phase-space states of the time series and of length and , respectively. The Cross-Recurrence (CR) states of the reconstructed state-space a time and are calculated by

| (3) |

with and . Here and are defined as in (1). defines the concept of synchronization and the way synchronization between two financial time series measured: an -neighbourhood of the embeddings , at epochs . We denote the full cross-recurrence matrix, known as cross-recurrence plot (CRP) extracted for and as , obtained through

| (4) |

The CRP corresponds to a matrix of dimension , which may not be square, as the time series and may have different lengths, i.e., .

For , of equal length the is a square matrix. Opposed to the (univariate) recurrence analysis of one time series (with itself, RP in equation (2)), the diagonal entries of the CRP are either 1 or 0, as the two time series may or may not be synchronized at , , see e.g. Figure 3. In the CRP of two time series the LOI is replaced by a distorted diagonal, called the Line Of Synchronization (LOS). The LOS reveals the relationship between the two time series in the time domain. In particular, it provides a non-parametric function containing information about the time-rescaling of the two time series, that further allows their re-synchronization [Marwan et al., 2002].

As the time series we consider in our application are multidimensional (), we point out that the CRP is indeed a Multidimensional Cross-Recurrence Plot (MdCRP) [Wallot, 2019] where , are row-vectors rather than scalars, and , are -dimensional row vectors rather than -dimensional row vectors, as opposed to the conventional CRP based on one-dimensional time series. Yet the above discussion is general and applies to both cases, and is in any case a scalar equal to either 0 or 1. For multidimensional time series, the entries of each of the two time series require normalization in each dimension before estimating the MdCRP [Wallot, 2019], e.g. with the -score.

Financial time series co-movement analysis using the CRP and LOS is studied in [Crowley, 2008, Guhathakurta et al., 2014, He and Huang, 2020]. [Tzagkarakis and Dionysopoulos, 2016] analyses the inter-dependencies of the stock market index and its associated volatility index, further proposing a method for the LOS estimation based on a corrupted CRP.

Furthermore, it is important to notice that financial time are often represented as multivariate instance. Indeed, the most basic source of financial data generally provide information about volumes along with prices. Despite the use of multidimensional inputs being effective and commonly found across several applications [Webber and Marwan, 2015], existing CRP applications on market data are broadly limited to the use of one-dimensional series only (e.g. prices or volatilities) [Webber and Marwan, 2015, Orlando and Zimatore, 2018, Addo et al., 2013, Bastos and Caiado, 2011].

III Proposed Method

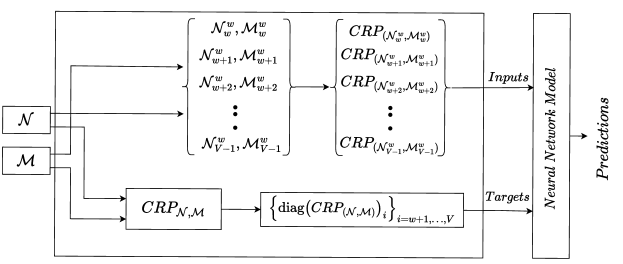

We exploit the CRP to quantify the co-movement of two multidimensional time series and observed continuously over a common period of length . Our goal is to predict whether at a certain epoch (e.g. a certain calendar day), and are synchronized in the state-space embedding -neighbourhood given by (3).

Assume two generic time series and are observed over the non-overlapping time-domains and of respective length and , their CRP corresponds to a matrix where the element expresses the state of synchronization at the -th time instance of the first time series () and at the -th time instance of the second (), in terms of the -neighbourhood of the states and , as expressed by (3). With the domains being non-overlapping there are no epochs and such that in (the same) calendar time, and the state of synchronization at a same calendar time cannot be determined. Indeed, for a fixed , the column-vector reports for the epochs (past or future with respect to ) whether state-space embedding is in the same -neighbourhood of .

In this light, if the domains of and only partially overlap over a region of length , for our forecasting purpose their non-overlapping regions and are irrelevant and can be discarded. On the other hand, over , their overlapping time instances and correspond to the same calendar epochs, i.e. , and are of actual relevance. Over the common domain , the CRP corresponds to a square matrix () with a well-defined diagonal expressing the state of synchronization at , e.g. answering whether at the (same) calendar day , and are synchronized or not.

This justifies the required form for the input data, corresponding to two (multidimensional) time series and observed over a common period of equal length , with . Since the essence of time series forecasting is that of predicting the future from the past, the data from the past needs to be representative for the -step ahead forecast. Trivially, this implicitly requires to be a continuous set of times for the given sampling frequency. That is, there should be no gaps between days or epochs, namely, . Furthermore, in order to calculate (3), we require the time-series to be non-corrupted over in all its multivariate entries, i.e. without missing values.

The above requirements are generally met for the financial time series of our interest. The only constraints are that of using data for stocks traded at the same exchange (same trading days and observed festivities), and that of selecting stocks not subject to delisting in the period of interest. As a precaution, we suggest inspecting the data for missing values due to data-quality issues related to the data provider, or unlikely security-related events such as trading halts.

Aligned with the general rationale of time series forecasting, we aim at predicting the one-step-ahead synchronization status between and at epoch , based on some lagged historical records available up to time , that is based on some suitable set of feature observed or extracted over past epochs. For let us denote by and the sub-sample of and of the most recent observations up to and including epoch , that is

Let us denote by the CRP computed from and (with embedding dimension , lag and ). At epoch , is used as the input of the neural network for predicting the state of synchronization at . Within this framework, there are input-target pairs. The first pair corresponds to the input and target , the last to the input and target . The prediction target at epoch corresponds to the state of synchronization at , provided by the (diagonal) entry of the CRP computed for the entire times series , . In particular, the state of synchronization at any epoch is provided by the diagonal of , i.e.,

| (5) |

so that corresponds to the targets for the inputs . The above corresponds to a framework where inputs are created dynamically by using CRPs computed over sub-sampled time series obtained by applying sliding windows of a fixed size. Note that is not analogous to the sub-matrix obtained from by considering its rows and columns from to . In the entire data in and accounts for the time series normalization and furthermore tunes the parameter . is thus truly dependent on the cropped times series data , , while is not. In a forecasting context our approach is feasible and unbiased as it does not use any future information following the one available at . Note that, in general, nothing prevents from choosing the embedding size and lag parameter differently for the CRP computation of the targets and for the CRP computations of the inputs.

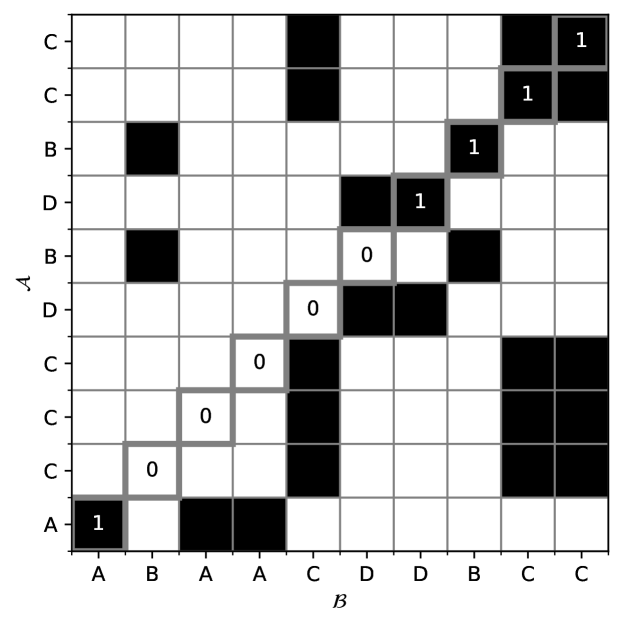

A simple example with two one-dimensional time series clarifies how we extract the input features and prediction targets. Consider the two time series and of 10 observations:

Figure 3 depicts their CRP, i.e., (for simplicity computed with , and ). The diagonal line of the CRP is highlighted and includes the values of the recurrence states. The diagonal line shows that the behavior of and at timestamps between and to is synchronized, therefore at these timestamps the prediction targets are set to 1 (the actual value of the Heaviside function in (3)). By, for instance, setting , we aim at predicting states of synchronization. The first prediction concerns the synchronization at epoch , based on the , that is, the CRP calculated from the first three observations of and . The prediction of the synchronization at epoch , is based on the CRP calculated on observations 2 to 4, i.e. on . The procedure is repeated up to epoch , where , calculated from the observations 7 to 9, is used for predicting .

To practically implement the underlying DL model that maps each input to its corresponding output, consider that each input consists of a matrix of zeros and ones that can be considered analogous to an image. Therefore we can rely on well-established classification models. In particular, we employ a Convolutional Neural Network (CNN). Such a neural network is well-suited for capturing the spatial relationships between the features in their input, which in our case correspond to the 0-1 features encoded in the entries of . Note that in the CRP calculation and are -score normalized before computing (3).

We use a CNN architecture formed by two convolutional and one fully-connected layer, as illustrated in Figure 2. The neural network involves the typical blocks of the CNN architecture. The convolutional layers adaptively learn the spatial relationships of inputs, the Rectified Linear Unit (ReLU) activation introduces nonlinearity to the model, and the max-pooling layer provides down-sampling operations reducing the size of the feature map by extracting the maximum value in each patch from the input feature map. The current CNN is chosen based on a grid search over different network architectures, layers’ types and sizes, aimed at maximizing the F1-score and showing the feasibility of our CRP-based DL approach.

IV Experiments

IV-A Data

Our analyses rely on daily adjusted closing prices and daily number of traded shares (volumes) for 12 representative constituents of the S&P100 index in the period from December 31st, 2014 to November 29th, 2021 ( trading days). The data is retrieved from Yahoo Finance. These 12 stocks are selected based on their market capitalization and their market sector. For each sector we select the first two stocks of highest-but-comparable capitalization, a practice well-supported by financial theory [Fama and French, 1993]. Market sectors provide a natural grouping for securities: analyses conducted at a sector level are a common practice for granting comparability and robustness of the results, as across market sectors the dynamics of economic variables are well-known to be asymmetric. Table I lists our stock selection. Each stock is expressed as a trivariate time series consisting of daily prices, volumes, and returns. This way, CRPs express temporal similarities in joint terms of the price level, traded volume, and daily return, providing a generalized definition of similarity in time-series dynamics at a multivariate level.

For our bivariate analysis on two time series we have pairs of stocks. For each stock pair, we use the first of the data for training ( days) and the last for testing ( days). As the future input instances should not affect the training process, the order of the input data during the training is fixed. The input and targets of the train data and the test data are, respectively,

| Inputs: | |||

| Targets: |

where and for the training set and and for the test set. We train the neural network once over the data for all the picks of the stock pairs. This pooled approach is a common practice in closely-related Machine Learning literature [Ntakaris et al., 2018, Tran et al., 2019, e.g.] and supported e.g. by the empirical findings of [Sirignano and Cont, 2019], suggesting the existence of an universal price formation mechanism (model), and thus price dynamic, not specific for individual assets. In practice, the input and output data is the concatenation of the individual pairs’ inputs-targets. For example, for a set window size , for the train set the input-target data consists of examples, that is pairs of cross-recurrent matrices and (scalar) targets, where . In the training phase, the training data is used to estimate the optimal weights of the CNN. The test data is then parsed to the estimated CNN and the quality of the network outputs is evaluated against the actual targets. Details are provided in the following two subsections.

| Sector | Ticker | Stock name |

|---|---|---|

| Electronic Technology (ET) | INTC | Intel Corporation |

| Electronic Technology | QCOM | Qualcomm Inc. |

| Energy Minerals (EM) | XOM | Exxon Mobil Corporation |

| Energy Minerals | CVX | Chevron Corporation |

| Finance (F) | JPM | JP Morgan Chase & Co. |

| Finance | V | Visa Inc. |

| Health Technology (HT) | JNJ | Johnson & Johnson |

| Health Technology | PFE | Pfizer, Inc. |

| Retail Trade (RT) | HD | Home Depot, Inc. (The) |

| Retail Trade | WMT | Walmart Inc. |

| Technology Services (TS) | MSFT | Microsoft Corporation |

| Technology Services | GOOG | Alphabet Inc. |

For the training of the CNN we adopt the ADAM optimizer with the following hyper-parameters: learning rate (reduced by a factor of every epochs), momentum parameters and , batch size and epoch size . Across the epochs we keep track of the F1-score on the validation set, which is set to the last 15% portion of the training set. For our classification task we adopt the binary cross-entropy loss. As the target classes are unbalanced, the loss is weighted for the targets’ class proportion. Details on the filter sizes, kernel sizes and the max pooling size are provided in Figure 2.

With respect to the CRP computations, throughout our analyses the embedding dimension is set to 2 or 3 (estimated via FNN method) based on input type, and the delay parameter is set to . Values , , , and are used for the threshold . These hyper-parameters are selected according to the guidelines and discussion in [Schinkel et al., 2008] and [Wallot, 2019]. The same values are applied for both the computation for the CRP related to the targets and the CRPs related to the inputs.

In our experiments we consider two different choices for the window-size hyperparameter, namely days. With the above settings, days, , and days. For , are square matrices of size and a square matrix of size on whose diagonal are found the relevant targets, i.e. , .

IV-B Experiments Results

Stock pairs from the same sector or two different sectors with different co-movement behaviors can provide comprehensive experimental data to show the ability of the proposed method in predicting the state of synchronization. To evaluate the performance of our proposed method, all pairs of stocks are used as the input of the method. We collect all pairs of stocks and for each pair, we follow the steps of the proposed method (Fig 1) to create the inputs and targets. We stack the input-target pair-specific data to create a single train and test set for all pairs.

Tables II and III, show the performance of our proposed approach for all pairs of stocks using two types of input: (price, volume) and (price, return, volume) respectively. Given that the target classes are generally imbalanced, the preferred reference performance metric is the F1 score. Yet, we also include accuracy, precision, and recall to have a clearer overview of the classification performance. For robustness, we run our experiments over a range of values for the window-size and threshold hyperparameters, a setup that further clarifies the effect of these hyperparameters on prediction performance.

Results for the (price, volume) time-series input are provided in Table II, results for the (price, return, volume) input in Table III. In general, our results show that the task of predicting the state of synchronization is not only feasible, but, under our setup, quite satisfactory. Indeed our preferred performance F1 metric is as high as 84%. Yet, as expected, the results appear to be sensible to the choice of the window size and threshold parameter. In particular, the performance metrics decrease in their values as the threshold parameter and the window size increase. This means that stricter -neighbourhoods are easier to predict and that the relevant information for the prediction of the synchronization state is found in the most recent instances of the CRP. This suggests the existence of patterns in the data that are strongly indicative of close -neighbourhoods, for which the prediction is very satisfactory. I.e. the CNN detects clear patterns indicative of the fact that the day-ahead synchronization is likely to be very strong (the -neighbourhoods is tight), indeed, as increases, the performance metric decrease, indicating that the model indeed detects strong evidence of “strong” day-ahead synchronization. Regarding, the window size, Long-lagged CRP information appears to introduce noise in the system without providing any predictive gains, aligned with the intuition that further-in-time information is less and less related to the current state of the system and of little use for prediction.

Suspecting that the use of prices and returns might be redundant, since they are closely related to each other, we also run a second experiment involving volumes and returns only. It is interesting to note that the inclusion of the returns does not seem to provide any advantage with respect to the (price, volume) input time series, but rather the opposite effect. It is indeed expected that the inclusion of further input variables complicates the patterns in the CRP chessboard so that under the same network architecture the performance metrics decrease. Furthermore, and aligned with the above, in additional experiments here not reported, we included squared returns (as a gross measure of daily volatility) finding that they also appear to have a detrimental on the performance metrics and prediction task. This perhaps suggests that the network architecture needs to scale up with the complexity of the input data (number of time series) that reasonably induces more complex patterns in the CRP.

| Accuracy | Precision | Recall | f1-score | ||

|---|---|---|---|---|---|

| 10 | 0.45 | 0.960 | 0.886 | 0.818 | 0.848 |

| 10 | 0.55 | 0.981 | 0.842 | 0.762 | 0.796 |

| 10 | 0.65 | 0.992 | 0.836 | 0.684 | 0.737 |

| 10 | 0.75 | 0.997 | 0.999 | 0.647 | 0.727 |

| 30 | 0.45 | 0.957 | 0.877 | 0.804 | 0.836 |

| 30 | 0.55 | 0.979 | 0.821 | 0.752 | 0.782 |

| 30 | 0.65 | 0.991 | 0.816 | 0.684 | 0.732 |

| 30 | 0.75 | 0.996 | 0.998 | 0.539 | 0.571 |

| 50 | 0.45 | 0.956 | 0.861 | 0.808 | 0.832 |

| 50 | 0.55 | 0.982 | 0.907 | 0.719 | 0.784 |

| 50 | 0.65 | 0.993 | 0.907 | 0.668 | 0.737 |

| 50 | 0.75 | 0.997 | 0.935 | 0.665 | 0.739 |

| 60 | 0.45 | 0.954 | 0.850 | 0.814 | 0.831 |

| 60 | 0.55 | 0.976 | 0.775 | 0.730 | 0.751 |

| 60 | 0.65 | 0.992 | 0.937 | 0.633 | 0.703 |

| 60 | 0.75 | 0.997 | 0.816 | 0.689 | 0.737 |

| 80 | 0.45 | 0.950 | 0.827 | 0.809 | 0.818 |

| 80 | 0.55 | 0.979 | 0.839 | 0.725 | 0.769 |

| 80 | 0.65 | 0.990 | 0.776 | 0.666 | 0.707 |

| 80 | 0.75 | 0.997 | 0.820 | 0.709 | 0.753 |

| Accuracy | Precision | Recall | f1-score | ||

|---|---|---|---|---|---|

| 10 | 0.45 | 0.946 | 0.858 | 0.802 | 0.827 |

| 10 | 0.55 | 0.973 | 0.810 | 0.733 | 0.765 |

| 10 | 0.65 | 0.988 | 0.776 | 0.694 | 0.728 |

| 10 | 0.75 | 0.995 | 0.795 | 0.664 | 0.711 |

| 30 | 0.45 | 0.943 | 0.845 | 0.800 | 0.820 |

| 30 | 0.55 | 0.971 | 0.789 | 0.742 | 0.763 |

| 30 | 0.65 | 0.987 | 0.760 | 0.678 | 0.711 |

| 30 | 0.75 | 0.996 | 0.998 | 0.601 | 0.667 |

| 50 | 0.45 | 0.938 | 0.826 | 0.785 | 0.804 |

| 50 | 0.55 | 0.971 | 0.795 | 0.731 | 0.758 |

| 50 | 0.65 | 0.987 | 0.758 | 0.667 | 0.702 |

| 50 | 0.75 | 0.995 | 0.998 | 0.503 | 0.505 |

| 60 | 0.45 | 0.938 | 0.823 | 0.788 | 0.804 |

| 60 | 0.55 | 0.967 | 0.752 | 0.735 | 0.743 |

| 60 | 0.65 | 0.987 | 0.756 | 0.654 | 0.692 |

| 60 | 0.75 | 0.996 | 0.955 | 0.595 | 0.657 |

| 80 | 0.45 | 0.933 | 0.805 | 0.788 | 0.796 |

| 80 | 0.55 | 0.967 | 0.755 | 0.730 | 0.742 |

| 80 | 0.65 | 0.989 | 0.893 | 0.616 | 0.677 |

| 80 | 0.75 | 0.995 | 0.998 | 0.548 | 0.586 |

V Conclusion

Predicting the co-movement of two multidimensional time series is a relevant task for the financial industry that supports potential trading strategies based on their interrelationships. This paper contributes to the literature by providing (i) a method relying upon the CRP to quantify the time series coupling over time, (ii) DL model for the prediction of the time series synchronization state, (iii) the use of a multidimensional time-series representation of the inputs involving prices, volumes and returns. Furthermore, (iv) we conduct extensive analyses on real stock market data from different sectors. The results show that the proposed setup can effectively predict the one-day-ahead synchronization of two-time series. Interesting future research direction would be to investigate the applicability of such an approach to a high-frequency domain where the high-dimensional nature of the raw data may provide valuable information for analyzing and predicting the coupling in settings that are known to be characterized by high levels of noise.

Acknowledgments

The research received funding from the Independent Research Fund Denmark project DISPA (project No. 9041-00004), and the European Union’s Horizon 2020 research and innovation programme under the Marie Skłodowska-Curie project BNNmetrics (grant agreement No. 890690).

References

- [Addo et al., 2013] Addo, P. M., Billio, M., and Guegan, D. (2013). Nonlinear dynamics and recurrence plots for detecting financial crisis. The North American Journal of Economics and Finance, 26:416–435.

- [Basher and Sadorsky, 2022] Basher, S. A. and Sadorsky, P. (2022). Forecasting bitcoin price direction with random forests: How important are interest rates, inflation, and market volatility? Machine Learning with Applications, 9:100355.

- [Bastos and Caiado, 2011] Bastos, J. A. and Caiado, J. (2011). Recurrence quantification analysis of global stock markets. Physica A: Statistical Mechanics and its Applications, 390(7):1315–1325.

- [Bauwens et al., 2006] Bauwens, L., Laurent, S., and Rombouts, J. V. (2006). Multivariate garch models: a survey. Journal of applied econometrics, 21(1):79–109.

- [Bhandari et al., 2022] Bhandari, H. N., Rimal, B., Pokhrel, N. R., Rimal, R., Dahal, K. R., and Khatri, R. K. (2022). Predicting stock market index using lstm. Machine Learning with Applications, 9:100320.

- [Bonanno et al., 2001] Bonanno, G., Lillo, F., and Mantegna, R. (2001). High-frequency cross-correlation in a set of stocks. Quantitative Finance, 1(1):96–104.

- [Chen and Tsay, 1993a] Chen, R. and Tsay, R. S. (1993a). Functional-coefficient autoregressive models. Journal of the American Statistical Association, 88(421):298–308.

- [Chen and Tsay, 1993b] Chen, R. and Tsay, R. S. (1993b). Nonlinear additive arx models. Journal of the American Statistical Association, 88(423):955–967.

- [Chiriac and Voev, 2011] Chiriac, R. and Voev, V. (2011). Modelling and forecasting multivariate realized volatility. Journal of Applied Econometrics, 26(6):922–947.

- [Christensen et al., 2021] Christensen, K., Siggaard, M., and Veliyev, B. (2021). A machine learning approach to volatility forecasting. Available at SSRN.

- [Cont et al., 2010] Cont, R., Stoikov, S., and Talreja, R. (2010). A stochastic model for order book dynamics. Operations research, 58(3):549–563.

- [Crowley, 2008] Crowley, P. M. (2008). Analyzing convergence and synchronicity of business and growth cycles in the euro area using cross recurrence plots. The European Physical Journal Special Topics, 164(1):67–84.

- [Dijk et al., 2002] Dijk, D. v., Teräsvirta, T., and Franses, P. H. (2002). Smooth transition autoregressive models—a survey of recent developments. Econometric reviews, 21(1):1–47.

- [Dixon et al., 2020] Dixon, M. F., Halperin, I., and Bilokon, P. (2020). Machine learning in Finance, volume 1406. Springer.

- [Eckmann et al., 1995] Eckmann, J.-P., Kamphorst, S. O., Ruelle, D., et al. (1995). Recurrence plots of dynamical systems. World Scientific Series on Nonlinear Science Series A, 16:441–446.

- [Fabretti and Ausloos, 2005] Fabretti, A. and Ausloos, M. (2005). Recurrence plot and recurrence quantification analysis techniques for detecting a critical regime. examples from financial market inidices. International Journal of Modern Physics C, 16(05):671–706.

- [Fama and French, 1993] Fama, E. F. and French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of financial economics, 33(1):3–56.

- [Fons et al., 2021] Fons, E., Dawson, P., Zeng, X.-j., Keane, J., and Iosifidis, A. (2021). Augmenting transferred representations for stock classification. In IEEE International Conference on Acoustics, Speech and Signal Processing, pages 3915–3919.

- [Fraser and Swinney, 1986] Fraser, A. M. and Swinney, H. L. (1986). Independent coordinates for strange attractors from mutual information. Physical review A, 33(2):1134.

- [Guhathakurta et al., 2014] Guhathakurta, K., Marwan, N., Bhattacharya, B., and Chowdhury, A. R. (2014). Understanding the interrelationship between commodity and stock indices daily movement using ace and recurrence analysis. In Translational Recurrences, pages 211–230. Springer.

- [Guo et al., 2017] Guo, X., Lai, T. L., Shek, H., and Wong, S. P.-S. (2017). Quantitative trading: algorithms, analytics, data, models, optimization. Chapman and Hall/CRC.

- [Hailesilassie, 2019] Hailesilassie, T. (2019). Financial market prediction using recurrence plot and convolutional neural network. Unpublished manuscript.

- [Han et al., 2021] Han, D., Orlando, G., and Fedotov, S. (2021). Identification of the nature of dynamical systems with recurrence plots and convolution neural networks: A preliminary test. arXiv preprint arXiv:2111.00866.

- [Harvey et al., 1994] Harvey, A., Ruiz, E., and Shephard, N. (1994). Multivariate stochastic variance models. The Review of Economic Studies, 61(2):247–264.

- [Haselbeck et al., 2022] Haselbeck, F., Killinger, J., Menrad, K., Hannus, T., and Grimm, D. G. (2022). Machine learning outperforms classical forecasting on horticultural sales predictions. Machine Learning with Applications, 7:100239.

- [Hawkes, 2018] Hawkes, A. G. (2018). Hawkes processes and their applications to finance: a review. Quantitative Finance, 18(2):193–198.

- [He and Huang, 2020] He, Q. and Huang, J. (2020). A method for analyzing correlation between multiscale and multivariate systems—multiscale multidimensional cross recurrence quantification (mmdcrqa). Chaos, Solitons & Fractals, 139:110066.

- [Heaton et al., 2017] Heaton, J. B., Polson, N. G., and Witte, J. H. (2017). Deep learning for finance: deep portfolios. Applied Stochastic Models in Business and Industry, 33(1):3–12.

- [Hołyst et al., 2001] Hołyst, J., Żebrowska, M., and Urbanowicz, K. (2001). Observations of deterministic chaos in financial time series by recurrence plots, can one control chaotic economy? The European Physical Journal B-Condensed Matter and Complex Systems, 20(4):531–535.

- [Huang and Kercheval, 2012] Huang, H. and Kercheval, A. N. (2012). A generalized birth–death stochastic model for high-frequency order book dynamics. Quantitative Finance, 12(4):547–557.

- [Juselius, 2006] Juselius, K. (2006). The cointegrated VAR model: methodology and applications. Oxford university press.

- [Kennel et al., 1992] Kennel, M. B., Brown, R., and Abarbanel, H. D. (1992). Determining embedding dimension for phase-space reconstruction using a geometrical construction. Physical review A, 45(6):3403.

- [Khare et al., 2017] Khare, K., Darekar, O., Gupta, P., and Attar, V. (2017). Short term stock price prediction using deep learning. In 2017 2nd IEEE international conference on recent trends in electronics, information & communication technology (RTEICT), pages 482–486. IEEE.

- [Krolzig, 2013] Krolzig, H.-M. (2013). Markov-switching vector autoregressions: Modelling, statistical inference, and application to business cycle analysis, volume 454. Springer Science & Business Media.

- [Kyoung-Sook and Hongjoong, 2019] Kyoung-Sook, M. and Hongjoong, K. (2019). Performance of deep learning in prediction of stock market volatility. Economic Computation & Economic Cybernetics Studies & Research, 53(2).

- [Lancia et al., 2014] Lancia, L., Fuchs, S., and Tiede, M. (2014). Application of concepts from cross-recurrence analysis in speech production: An overview and comparison with other nonlinear methods. Journal of Speech, Language, and Hearing Research, 57(3):718–733.

- [Li et al., 2020] Li, X., Kang, Y., and Li, F. (2020). Forecasting with time series imaging. Expert Systems with Applications, 160:113680.

- [Liu, 2019] Liu, Y. (2019). Novel volatility forecasting using deep learning–long short term memory recurrent neural networks. Expert Systems with Applications, 132:99–109.

- [Lütkepohl, 1991] Lütkepohl, H. (1991). Introduction to multiple time series analysis. Springer Science & Business Media.

- [Lütkepohl, 1999] Lütkepohl, H. (1999). Vector autoregressions. Unpublished manuscript, Institut füur Statistik und Ökonometrie, Humboldt-Universität zu Berlin.

- [Ma et al., 2013] Ma, F., Wei, Y., and Huang, D. (2013). Multifractal detrended cross-correlation analysis between the chinese stock market and surrounding stock markets. Physica A: Statistical Mechanics and its Applications, 392(7):1659–1670.

- [Marwan, 1999] Marwan, N. (1999). Investigation of climate variability in NW Argentina using quantitative analysis of recurrence plots. Norbert Marwan.

- [Marwan and Kurths, 2002] Marwan, N. and Kurths, J. (2002). Nonlinear analysis of bivariate data with cross recurrence plots. Physics Letters A, 302(5):299–307.

- [Marwan et al., 2002] Marwan, N., Thiel, M., and Nowaczyk, N. R. (2002). Cross recurrence plot based synchronization of time series. Nonlinear Processes in Geophysics, 9(3/4):325–331.

- [Murphy, 1999] Murphy, J. J. (1999). Technical analysis of the financial markets: A comprehensive guide to trading methods and applications. Penguin.

- [Ntakaris et al., 2018] Ntakaris, A., Magris, M., Kanniainen, J., Gabbouj, M., and Iosifidis, A. (2018). Benchmark dataset for mid-price forecasting of limit order book data with machine learning methods. Journal of Forecasting, 37(8):852–866.

- [Orlando and Zimatore, 2018] Orlando, G. and Zimatore, G. (2018). Recurrence quantification analysis of business cycles. Chaos, Solitons & Fractals, 110:82–94.

- [Passalis et al., 2020] Passalis, N., Tefas, A., Kanniainen, J., Gabbouj, M., and Iosifidis, A. (2020). Temporal bag-of-features learning for predicting mid price movements using high frequency limit order book data. IEEE Transactions on Emerging Topics in Computational Intelligence, 4(6):774–785.

- [Ramchand and Susmel, 1998] Ramchand, L. and Susmel, R. (1998). Volatility and cross correlation across major stock markets. Journal of Empirical Finance, 5(4):397–416.

- [Reinsel, 1993] Reinsel, G. C. (1993). Vector ARMA Time Series Models and Forecasting, pages 21–51. Springer US, New York, NY.

- [Schinkel et al., 2008] Schinkel, S., Dimigen, O., and Marwan, N. (2008). Selection of recurrence threshold for signal detection. The european physical journal special topics, 164(1):45–53.

- [Sezer et al., 2017] Sezer, Berat, O., Ozbayoglu, Murat, A., Dogdu, and Erdogan (2017). An artificial neural network-based stock trading system using technical analysis and big data framework. In Southeast Conference, pages 223–226.

- [Shabani and Iosifidis, 2020] Shabani, M. and Iosifidis, A. (2020). Low-rank temporal attention-augmented bilinear network for financial time-series forecasting. In 2020 IEEE Symposium Series on Computational Intelligence (SSCI), pages 2156–2161. IEEE.

- [Shabani et al., 2022a] Shabani, M., Tran, D. T., Kanniainen, J., and Iosifidis, A. (2022a). Augmented bilinear network for incremental multi-stock time-series classification. arXiv preprint arXiv:2207.11577.

- [Shabani et al., 2022b] Shabani, M., Tran, D. T., Magris, M., Kanniainen, J., and Iosifidis, A. (2022b). Multi-head temporal attention-augmented bilinear network for financial time series prediction. arXiv preprint arXiv:2201.05459.

- [Sirignano and Cont, 2019] Sirignano, J. and Cont, R. (2019). Universal features of price formation in financial markets: perspectives from deep learning. Quantitative Finance, 19(9):1449–1459.

- [Sood et al., 2021] Sood, S., Zeng, Z., Cohen, N., Balch, T., and Veloso, M. (2021). Visual time series forecasting: An image-driven approach. In Proceedings of the Second ACM International Conference on AI in Finance. Association for Computing Machinery.

- [Takens, 1981] Takens, F. (1981). Detecting strange attractors in turbulence. In Dynamical systems and turbulence, Warwick 1980, pages 366–381. Springer.

- [Tong, 1978] Tong, H. (1978). On a Threshold Model in Pattern Recognition and Signal Processing. Sijhoff & Noordhoff.

- [Tran et al., 2019] Tran, D. T., Iosifidis, A., Kanniainen, J., and Gabbouj, M. (2019). Temporal attention-augmented bilinear network for financial time-series data analysis. IEEE Transactions on Neural Networks and Learning Systems, 30(5):1407–1418.

- [Tsay, 2005] Tsay, R. S. (2005). Analysis of financial time series. John Wiley & Sons.

- [Tzagkarakis and Dionysopoulos, 2016] Tzagkarakis, G. and Dionysopoulos, T. (2016). Restoring corrupted cross-recurrence plots using matrix completion: Application on the time-synchronization between market and volatility indexes. In Recurrence Plots and Their Quantifications: Expanding Horizons, pages 241–263. Springer.

- [Wallot, 2019] Wallot, S. (2019). Multidimensional cross-recurrence quantification analysis (mdcrqa)–a method for quantifying correlation between multivariate time-series. Multivariate behavioral research, 54(2):173–191.

- [Webber and Marwan, 2015] Webber, C. L. and Marwan, N., editors (2015). Recurrence Quantification Analysis. Springer International Publishing.

- [Webber Jr. and Zbilut, 1994] Webber Jr., C. L. and Zbilut, J. P. (1994). Dynamical assessment of physiological systems and states using recurrence plot strategies. Journal of applied physiology, 76(2):965–973.

- [Xu and Zhang, 2021] Xu, X. and Zhang, Y. (2021). Network analysis of corn cash price comovements. Machine Learning with Applications, 6:100140.

- [Yin and Shang, 2016] Yin, Y. and Shang, P. (2016). Multiscale recurrence plot and recurrence quantification analysis for financial time series. Nonlinear Dynamics, 85(4):2309–2352.

- [Zbilut, 2005] Zbilut, J. P. (2005). Use of recurrence quantification analysis in economic time series. In Economics: Complex Windows, pages 91–104. Springer.

- [Zhang et al., 2019] Zhang, Z., Zohren, S., and Roberts, S. (2019). Deeplob: Deep convolutional neural networks for limit order books. IEEE Transactions on Signal Processing, 67:3001–3012.