Bridging Distributional and Risk-sensitive Reinforcement Learning with Provable Regret Bounds

Abstract

We study the regret guarantee for risk-sensitive reinforcement learning (RSRL) via distributional reinforcement learning (DRL) methods. In particular, we consider finite episodic Markov decision processes whose objective is the entropic risk measure (EntRM) of return. By leveraging a key property of the EntRM, the independence property, we establish the risk-sensitive distributional dynamic programming framework. We then propose two novel DRL algorithms that implement optimism through two different schemes, including a model-free one and a model-based one.

We prove that they both attain regret upper bound, where , , , and represent the number of states, actions, episodes, and the time horizon, respectively. It matches RSVI2 proposed in Fei et al. (2021), with novel distributional analysis. To the best of our knowledge, this is the first regret analysis that bridges DRL and RSRL in terms of sample complexity.

Acknowledging the computational inefficiency associated with the model-free DRL algorithm, we propose an alternative DRL algorithm with distribution representation. This approach not only maintains the established regret bounds but also significantly amplifies computational efficiency.

We also prove a tighter minimax lower bound of for the case, which recovers the tight lower bound in the risk-neutral setting.

Keywords: distributional reinforcement learning, risk-sensitive reinforcement learning, regret bounds, episodic MDP, entropic risk measure

1 Introduction

Standard reinforcement learning (RL) seeks to find an optimal policy that maximizes the expected return (Sutton and Barto, 2018). This approach is often referred to as risk-neutral RL, as it focuses on the mean functional of the return distribution. However, in high-stakes applications, such as finance (Davis and Lleo, 2008; Bielecki et al., 2000), medical treatment (Ernst et al., 2006), and operations research (Delage and Mannor, 2010), decision-makers are often risk-sensitive and aim to maximize a risk measure of the return distribution.

Since the pioneering work of Howard and Matheson (1972), risk-sensitive reinforcement learning (RSRL) based on the exponential risk measure (EntRM) has been applied to a wide range of domains (Shen et al., 2014; Nass et al., 2019; Hansen and Sargent, 2011). EntRM offers a trade-off between the expected return and its variance and allows for the adjustment of risk-sensitivity through a risk parameter. However, existing approaches typically require complicated algorithmic designs to handle the non-linearity of EntRM.

Distributional reinforcement learning (DRL) has demonstrated superior performance over traditional methods in some challenging tasks under a risk-neutral setting (Bellemare et al., 2017; Dabney et al., 2018b, a). Unlike value-based approaches, DRL learns the entire return distribution instead of a real-valued value function. Given the distributional information, it is natural to leverage it to optimize a risk measure other than expectation (Dabney et al., 2018a; Singh et al., 2020; Ma et al., 2020). Despite the intrinsic connection between DRL and RSRL, existing works on RSRL via DRL approaches lack regret analysis (Dabney et al., 2018a; Ma et al., 2021; Achab and Neu, 2021). Consequently, it is challenging to evaluate and improve these DRL algorithms in terms of sample efficiency. Additionally, DRL can be computationally demanding as return distributions are typically infinite-dimensional objects. This complexity raises a pertinent question:

Is it feasible for DRL to attain near-optimal regret in RSRL while preserving computational efficiency?

In this work, we answer this question positively by providing computationally efficient DRL algorithms with regret guarantee. We have developed two types of DRL algorithms, both designed to be computationally efficient, and equipped with principled exploration strategies tailored for tabular EntRM-MDP. Notably, these proposed algorithms apply the principle of optimism in the face of uncertainty (OFU) at a distributional level, effectively balancing the exploration-exploitation dilemma. By conducting the first regret analysis in the field of DRL, we bridge the gap between computationally efficient DRL and RSRL, especially in terms of sample complexity. Our work paves the way for deeper understanding and improving the efficiency of RSRL through the lens of distributional approaches.

1.1 Related Work

Related work in DRL has rapidly grown since Bellemare et al. (2017), with numerous studies aiming to improve performance in the risk-neutral setting (see Rowland et al., 2018; Dabney et al., 2018b, a; Barth-Maron et al., 2018; Yang et al., 2019; Lyle et al., 2019; Zhang et al., 2021). However, only a few works have considered risk-sensitive behavior, including Dabney et al. (2018a); Ma et al. (2021); Achab and Neu (2021). None of these works have addressed sample complexity.

A large body of work has investigated RSRL using the EntRM in various settings (Borkar, 2001, 2002; Borkar and Meyn, 2002; Borkar, 2010; Bäuerle and Rieder, 2014; Di Masi et al., 2000; Di Masi and Stettner, 2007; Cavazos-Cadena and Hernández-Hernández, 2011; Jaśkiewicz, 2007; Ma et al., 2020; Mihatsch and Neuneier, 2002; Osogami, 2012; Patek, 2001; Shen et al., 2013, 2014). However, these works either assume known transition and reward or consider infinite-horizon settings without considering sample complexity.

Our work is related to two recent studies by Fei et al. (2020) and Fei et al. (2021) in the same setting. Fei et al. (2020) introduced the first regret-guaranteed algorithms for risk-sensitive episodic Markov decision processes (MDPs), but their regret upper bounds contain an unnecessary factor of and their lower bound proof contains errors, leading to a weaker bound. While Fei et al. (2021) refined their algorithm by introducing a doubly decaying bonus that effectively removes the factor 111A detailed comparison with Fei et al. (2021) is given in Section 8., the issue with the lower bound was not resolved. Achab and Neu (2021) proposed a risk-sensitive deep deterministic policy gradient framework, but their work is fundamentally different from ours as they consider the conditional value at risk and focus on discounted MDP with infinite horizon settings. Moreover, Achab and Neu (2021) assumes that the model is known.

1.2 Contributions

This paper makes the following primary contributions:

1. Formulation of a Risk-Sensitive Distributional Dynamic Programming (RS-DDP) framework. This framework introduces a distributional Bellman optimality equation tailored for EntRM-MDP, leveraging the independence property of the EntRM.

2. Proposal of computationally efficient DRL algorithms that enforce the OFU principle in a distributional fashion, along with regret upper bounds of . The DRL algorithms not only outperform existing methods empirically but are also supported by theoretical justifications. Furthermore, this marks the first instance of analyzing a DRL algorithm within a finite episodic EntRM-MDP setting.

3. Filling of gaps in the lower bound in Fei et al. (2020), resulting in a tight lower bound of for . This lower bound is dependent of and and recovers the tight lower bound in the risk-neutral setting (as ).

| Algorithm | Regret bound | Time | Space |

|---|---|---|---|

| RSVI | |||

| RSVI2 | |||

| RODI-Rep | |||

| RODI-MF | |||

| RODI-MB | |||

| lower bound | - | - |

2 Preliminaries

We provide the technical background in this section.

2.1 Notations

We write and for any positive integers . We adopt the convention that if and if . We use to denote the indicator function. For any , we define . We denote by the Dirac measure at . We denote by , and the set of distributions supported on , and the set of all distributions respectively. We use to denote a binary r.v. taking values and with probability and . For a discrete set and a probability vector , the notation represents the discrete distribution with . For a discrete distribution , we use to denote the number of atoms of the distribution . We use to denote omitting logarithmic factors. A table of notation is provided in Appendix A.

2.2 Episodic MDP

An episodic MDP is identified by , where is the state space, the action space, the probability transition kernel at step , the collection of reward functions at step and the length of one episode. The agent interacts with the environment for episodes. At the beginning of episode , Nature selects an initial state arbitrarily. In step , the agent takes action and observes random reward and reaches the next state . The episode terminates at with , then the agent proceeds to next episode.

For each , we denote by the (random) history up to step of episode . We define as the history up to episode . We describe the interaction between the algorithm and MDP in two levels. In the level of episode, we define an algorithm as a sequence of function , each mapping to a policy . We denote by the policy at episode . In the level of step, a (deterministic) policy is a sequence of functions with .

2.3 Risk Measure

Consider two random variables and . We assert that dominates , and correspondingly, dominates , denoted as and , if and only if for every real number , the inequality holds true. A risk measure, , is a function mapping a set of random variables, denoted as , to the real numbers. This mapping adheres to several crucial properties:

-

•

Monotonicity (M): ,

-

•

Translation-invariance (TI): ,

-

•

Distribution-invariance (DI): .

A mapping qualifies as a risk measure if it satisfies both (M) and (TI). Additionally, a risk measure that also adheres to (DI) is termed a distribution-invariant risk measure. This paper focuses exclusively on distribution-invariant risk measures, allowing us to simplify notation by denoting as .

We direct our attention to EntRM, a prominent risk measure in domains requiring risk-sensitive decision-making, such as mathematical finance (Föllmer and Schied, 2016), Markovian decision processes (Bäuerle and Rieder, 2014). For a random variable and a non-zero coefficient , the EntRM is defined as:

Given that EntRM satisfies (DI), we can denote as for . When possesses a small absolute value, employing Taylor’s expansion yields

| (1) |

Therefore, a decision-maker aiming to maximize the EntRM value demonstrates risk-seeking behavior (preferring higher uncertainty in ) when , and risk-averse behavior (preferring lower uncertainty in ) when . The absolute value of dictates the sensitivity to risk, with the measure converging to the mean functional as approaches zero.

2.4 Risk-neutral Distributional Dynamic Programming Revisited

Bellemare et al. (2017); Rowland et al. (2018) have discussed the infinite-horizon distributional dynamic programming in the risk-neutral setting, which will be referred to as the classical DDP. Now we adapt their results to the finite horizon setting. We define the return for a policy starting from state-action pair at step

Define , then it is immediate that

There are two sources of randomness in : the transition and the next-state return . Denote by and the cumulative distribution function (CDF) corresponding to and respectively. Rewriting the random variable in the form of CDF, we have the distributional Bellman equation

The distributional Bellman equation outlines the backward recursion of the return distribution under a fixed policy. Our focus is primarily on risk-neutral control, aiming to maximize the mean value of the return, as represented by:

Here, signifies that this is a multi-stage maximization problem. An exhaustive search approach is impractical due to its exponential computational complexity. However, the principle of optimality applies, suggesting that the optimal policy for any tail sub-problem coincides with the tail of the optimal policy, as discussed in (Bertsekas et al., 2000). This principle enables the reduction of the multi-stage maximization problem into several single-stage maximization problems. Let and denote the optimal return. The risk-neutral Bellman optimality equation can be expressed as follows:

Rewriting this in the form of distributions, we get:

3 Risk-sensitive Distributional Dynamic Programming

In this section, we establish a novel DDP framework for risk-sensitive control. For the risk-sensitive purpose, we define the action-value function of a policy at step as , which is the EntRM value of the return distribution, for each . The value function is defined as . We focus on the control setting, in which the goal is to find an optimal policy to maximize the value function, that is,

In the risk-sensitive setting, however, the principle of optimality does not always hold for general risk measures. For example, the optimal policy for CVaR may be non-Markovian or history-dependent (Shapiro et al., 2021).

EntRM satisfies independence property (also known as the independence axiom) in economics and decision theory (Von Neumann and Morgenstern, 1947; Dentcheva and Ruszczynski, 2013). For better illustration, we introduce some additional notations. We write or if or . This is different from the notion of stochastic dominance . In fact, (M) of EntRM implies that

Fact 1 (Independence property)

the following holds

Proof We only prove the case that . The case that follows analogously. For any two distributions and such that , we have

which implies . Thus for any distribution ,

This finishes the proof.

Moreover, the property (TI) entails that the EntRM value of the current return equals the sum of the immediate reward and the value of the future return

where we write . We will show that (I) and (T) suggest that the optimal future return consists in the optimal current return

These observations implies the principle of optimality. For notational simplicity, we write for two positive integers .

Proposition 1 (Principle of optimality)

Let be an optimal policy. Fixing , then the truncated optimal policy is optimal for the sub-problem .

Proof Suppose that the truncated policy is not optimal for this subproblem, then there exists an optimal policy such that

There exists a state with such that

where the inequality is due to (I) of . It follows that is a strictly better policy than for the subproblem from to . Using induction, we deduce that is a strictly better policy than . This is contradicted to the assumption that is an optimal policy.

Furthermore, the principle of optimality induces the distributional Bellman optimality equation in the risk-sensitive setting.

Proposition 2 (Distributional Bellman optimality equation)

The optimal policy is given by the following backward recursions:

| (2) | ||||

where denotes the CDF obtained by shifting to the right by . Furthermore, the sequence and represent the sequence of distributions corresponding to the optimal returns at each step.

Proof Throughout the proof we omit for the ease of notation. The proof follows from induction. Notice that and are the return distribution and value function for state at step following policy respectively. At step , it is obvious that is the optimal policy that maximizes the EntRM value at the final step. Fixing , we assume that is the optimal policy for the subproblem

In other words, :

It follows that ,

Hence is the optimal value function at step and is the optimal policy for the sub-problem from to . The induction is completed.

For simplicity, we define the distributional Bellman operator with associated model as

Denote by , then we can rewrite Equation 2 in a compact form:

| (3) | ||||

Discussion about the independence property

Another property closely related to (I) is the tower (T) property (Kupper and Schachermayer, 2009).

Definition 3 (Tower property)

A risk measure satisfies the tower property if for two r.v.s and , we have

where is taken w.r.t. the conditional distribution.

We can show that the following implications hold

: Suppose (T) holds. Let . Let be a binary r.v. independent of and . Given , we have

| (DI) | |||

Next, Fact 2 implies

Fact 2 (Mixture distribution)

Let for . Let be a discrete r.v. independent of with . Then .

It follows that

where the first and second implication is due to (M) and (T) of .

: Fix and . Using (T) leads to a decomposition of the risk-sensitive value function as follows:

We call it the risk-sensitive Value Bellman equation, which relates the action-value function at step to the next-step value functions . We can further derive the Value Bellman optimality equation with (M) and (T). Observe that

which implies the Value Bellman optimality equation

We make the following summary.

(i) Both (T) and (I) imply the principle of dynamic programming, but (I) is considered a weaker assumption than (T). This indicates that while both properties support the formulation of DP, (I) does so under less stringent conditions.

(ii) (I) inspires a distributional perspective in RSRL, leading to the concept of DDP. This perspective involves running DP in the language of random variables or distributions, as opposed to traditional scalar values. In contrast, (T) primarily supports the classical Value Bellman equation. It’s important to note that both distributional and classical DP contribute to the derivation of optimal policies. However, in our work, (I) plays a crucial and irreplaceable role. DDP, enabled by (I), facilitates the algorithm design and regret analysis in distributional RL, which is not achievable solely with (T).

Finally, the regret of an algorithm interacting with an MDP for episodes is defined as

Note that the regret is a random variable since is a random quantity. We denote by the expected regret. We will omit and for simplicity.

4 RODI-MF

In this section, we introduce Model- Free Risk-sensitive Optimistic Distribution Iteration (RODI-MF), as detailed in Algorithm 1.

We begin by establishing additional notations. For two Cumulative Distribution Functions (CDFs) and , the supremum distance between them is defined as . We define the distance between two Probability Mass Functions (PMFs) with the same support and as . Furthermore, the set denotes the supremum norm ball of CDFs centered at with radius . Analogously, represents the norm ball of PMFs centered at with radius .

In each episode, Algorithm 1 comprises two distinct phases: the planning phase and the interaction phase. During the planning phase, the algorithm executes an optimistic variant of the approximate Risk-Sensitive Distributional Dynamic Programming (RS-DDP), progressing backward from step to step 1 within each episode. This process results in a policy to be employed during the subsequent interaction phase. We offer further details about the two phases as follows:

Planning phase (Line 4-12). The algorithm undertakes a sample-based distributional Bellman update in Lines 5-7. To clarify, we append the episode index to the variables in Algorithm 1 corresponding to episode . For instance, represents in episode . Specifically, for visited state-action pairs, Line 6 essentially performs an approximate DDP. Let and . For a given tuple with , , the empirical transition model is defined as:

For any , the following holds:

Thus, the update formula in Line 6 of Algorithm 1 can be reformulated as:

Conversely, for unvisited state-action pairs, the return distribution remains aligned with the highest plausible reward . Subsequently, the algorithm calculates the optimism constants (Line 8) and applies the distributional optimism operator (Line 9) to obtain the optimistically plausible return distribution . The selection of will be elaborated later. The optimistic return distribution yields the optimistic value function, from which the algorithm derives the greedy policy to be applied during the interaction phase.

Interaction phase (Line 14-17). In Lines 15-16, the agent interacts with the environment under policy and refreshes the counts based on newly gathered observations.

4.1 Connection to Exponential Utility

Our analysis explores the relationship between EntRM and Exponential Utility (EU). The EU is defined as follows:

where it serves as an exponential transformation of the EntRM. Notably, this transformation preserves the order in the sense that for any non-zero , ,

Leveraging this property, we derive the distributional Bellman optimality equation in terms of EU as follows:

| (4) | ||||

Proposition 4 (Equivalence between EntRM and EU)

The policy , generated by Equation 4, is optimal for both the EntRM and EU. Moreover, the return distribution generated aligns with the optimal return distribution for EntRM.

Proof

The proof employs induction. The only difference between Equation 4 and Equation 2 lies in the policy generation step. For clarity, denote the quantities generated by the respective equations as and . The base case with is evident. It follows that for each , due to the preserved order under the exponential transformation. Subsequently, it holds that . Assuming for , we establish that , and . This completes the induction process.

We further present two important properties of EU, instrumental in formulating the regret upper bounds: Lipschitz continuity and linearity. Denote by the Lipschitz constant of with respect to the infinity norm , which satisfies:

Lemma 5 establishes a tight Lipschitz constant for EU, linking the distance between distributions to the difference in their EU values.

Lemma 5 (Lipschitz property of EU)

is Lipschitz continuous with respect to the supremum norm over with , Moreover, is tight with respect to both and .

The proof is deferred to Appendix B. It’s worth noting that as approaches zero, tends to zero, aligning with the observation that . Another key property of EU is the linearity:

This property significantly refines the regret bounds. In contrast, the non-linearity of EntRM may result in an exponential factor of in error propagation across time steps, potentially leading to a compounded factor of in the regret bound.

4.2 Distributional Optimism over the Return Distribution

For the purpose of clarity, we will focus on the scenario where in the subsequent discussion. The case for can be approached using analogous reasoning. We commence by formally defining optimism at the distributional level.

Definition 6

Given two CDFs and , we say that is more optimistic than if .

This definition aligns with the intuitive notion that a more optimistic distribution should possess a larger EntRM value. Given that the exponential transformation preserves order, is more optimistic than if and only if . Following the methodology of Keramati et al. (2020), we introduce the distributional optimism operator for a level as

This operator shifts the distribution down by a maximum of over , ensuring that the resulting function remains a valid CDF in and optimistically dominates all other CDFs within the same space222For a more comprehensive explanation, please refer to Liang and Luo (2023)..

Lemma 7

Let be a functional (not necessarily a risk measure) satisfying (M). For any , it holds that if , then . Moreover, it holds that

Proof

Consider any . By the definition of , we have . Therefore, for any , we have . Since dominates any in and considering (M) of , we arrive at the conclusion.

We define the EU value produced by the algorithm as and for all . Similarly, we define and for all . We define for any and introduce the good event as follows:

This event encapsulates the scenario where the empirical distributions concentrates around the true distributions with respect to the norm. Leveraging Lemma 11, (M) of EU, and inductive reasoning, we arrive at Proposition 8, which asserts that the sequence is consistently optimistic compared to the optimal value sequence .

Proposition 8 (Optimism)

Conditioned on event , the sequence produced by Algorithm 1 are all greater than or equal to , i.e.,

We first present a series of lemmas, specifically Lemma 9 through Lemma 11, which is used in the proof of Proposition 8.

Lemma 9 (High probability good event)

For any , the event is true with probability at least .

We will verify the distributional optimism conditioned on .

Lemma 10

For any and any with any , it holds that

Proof

Lemma 11 (Bound on the optimistic constant)

For any bounded distributions and any it holds that if , then

Proof Without loss of generality assume . By Lemma 10, for any

For any ,

Now we give the proof of Proposition 8.

Proof The proof proceeds by induction. We fix and consider each stage in reverse order. Consider the base case: for any such that

This equality holds because the reward received at stage is deterministic and hence the EU is simply the exponential of the scaled reward. For unvisited state-action pairs with , the EU is given by:

Here, the EU value defaults to , which is greater than or equal to the optimal EU value for any . Given these calculations, for any state , the EU value at stage satisfies , establishing the base case. Assuming that for stage , holds for all states , we now consider stage . For any visited state-action pair with , we apply Lemma 11 with , to obtain

given that for . We have

where the first inequality is due to (M), and the second inequality follows from the induction assumption. For unvisited state-action pairs at stage , the EU is calculated based on the maximum possible reward, ensuring that:

Finally, aggregating these values for any state at stage , we obtain:

completing the induction step and thereby the proof.

4.3 Regret Upper Bound of RODI-MF

Theorem 12 (Regret upper bound of RODI-MF)

For any , with probability , the regret of Algorithm 1 is bounded as

where is the Lipschitz constant of EntRM over .

Remark 13

Remark 14

For values of that are close to zero, an expansion using Taylor’s series reveals that the EntRM, , can be approximated by the sum of the expected cumulative reward and a term proportional to the variance of the cumulative reward, with higher-order terms contributing insignificantly. Considering that the reward lies in the interval , both the expected cumulative reward and its variance are bounded by terms linear and quadratic in , respectively. To balance the expected reward and the risk (as quantified by the variance), it is prudent to choose .

Remark 15

By choosing , we can eliminate the exponential dependency on and achieve polynomial regret bound akin to the risk-neutral setting. Therefore, DRL can achieve regret bound for RSRL with reasonable risk-sensitivity.

Proof We first prove the case . Define

and . For any and any , we let . The regret can be bounded as

where the last inequality follows from Lemma 31 and that both and are larger than 1. We can decompose as follows

Using the Lipschitz property of EU, we have

We can bound as

where the second inequality is due to Lemma 10. Observe that

where is a martingale difference sequence with a.s. for all , and . Since , we can bound recursively as

Repeating the procedure, we get

Thus

Now we bound each term separably. The first term can be bounded as

Observe that

thus we can bound the second term by Azuma-Hoeffding inequality: with probability at least , the following holds

The third term can be bounded as

Using a union bound and let , we have that with probability at least ,

where .

Now we consider the case . Using similar arguments, we arrive at

where the last inequality is due to that both and is larger than or equal to . We can finally get

4.4 Computational inefficiency of RODI-MF

While RODI-MF enjoys near-optimal regret guarantee, it suffers from computational inefficiency, especially in contexts with a large number of states or a long horizon. For better illustration, let’s consider a Markov Reward Process with states at each step. In this setup, the transition kernel is uniform () for any , and the reward function is bounded between 0 and 1 (). Starting from the final step , the return distribution is a Dirac delta function centered at . Applying the distributional Bellman equation at step at step , we get

Recall that represents the number of atoms (distinct elements) in a discrete distribution , indicating the memory required to store this distribution. Since for each , and is a uniform mixture of all shifted by , we find

Continuing this process backwards through the time steps:

This analysis shows that the number of atoms in the return distribution exponentially increases with the horizon , scaled by the number of states at each application of the distributional Bellman operator. As a result, the memory and computational requirements to implement an exact distributional RL algorithm like RODI-MF become prohibitive, particularly for problems with many states or a long horizon. This exponential growth in complexity highlights the computational challenges associated with RODI-MF and underscores the need for approximations for practical implementations.

5 DRL with Distribution Representation

To address the computational challenges in implementing the distributional Bellman equation, we introduce two versions of RODI-MF in the revised paper that utilize distribution representation. A widely used method of distribution representation is the categorical representation, as discussed in recent literature (Bellemare et al., 2023). This approach parameterizes the probability distribution at fixed locations. Specifically, we consider the simplest form of categorical representation that uses only two atoms. We refer to this as the Bernoulli representation. It represents the set of all discrete distributions with two distinct atoms, denoted as . The Bernoulli representation is formally defined as:

With the Bernoulli representation in mind, let’s consider distributional Bellman operator

This operator essentially performs two basic operations: shifting and mixing. Specifically, it shifts each next-step return distribution by the reward and then takes a mixture of these shifted distributions with the mixture coefficients . However, these operations might change and expand the support of the distributions, leading to:

To improve computational efficiency, we introduce the Bernoulli representation for . Let

be a Bernoulli representation of the true return distribution , where and are the left and right atoms, and is the probability at . Applying to , we obtain

The result is no longer a Bernoulli distribution but a categorical distribution with atoms. This demonstrates that the Bernoulli representation is not closed under

To overcome this issue, we introduce the Bernoulli projection operator. This operator serves as a mapping from the space of probability distributions to , and we denote it as . Algorithmically, we add a projection step immediately after the application of , resulting in a projected distributional Bellman operator . This projection ensures that each iteration of is representable using a limited amount of memory.

Note that the projection operator is not unique. Previous works (Bellemare et al., 2023) have developed projection operators aiming to find the best approximation to a given probability distribution, as measured by a specific probability metric. Our approach introduces a novel type of Bernoulli projection that preserves the ERM value, an essential aspect in risk-sensitive settings. Starting from a Dirac measure , we define the value-equivalent Bernoulli projection operator as:

where the probability is defined as

| (5) |

It is easy to verify that . Now we extend the definition to the categorical distributions as:

Given that , the linearity of EU implies

This verifies the value equivalence of .

To ensure the preservation of the value, the only requirement is that the interval covers the support of the input distribution, i.e., . The projection preserves the risk value of the original distribution, making it a powerful tool for efficient and accurate representation in DRL for RSRL.

Without the knowledge of MDP, RODI-MF deviates from the DDP in two crucial updates:

In RODI-MF, the approximate distributional Bellman operator is applied first, which relies on the empirical transition rather than the true transition . Then, the distributional optimism operator is used to generate an optimistic return distribution. Drawing from these observations, we propose two DRL algorithms with Bernoulli representation, differing in the order of projection and optimism operator. We term the two algorithms as RODI-Rep.

5.1 DRL with Bernoulli Representation

Given that , we set the uniform location parameters as

which is independent of . We represent each iterate by a Bernoulli distribution

where we overload the notation for and . Applying the approximate to the Bernoulli represented yields

With slight abuse of notation, we let

is a Bernoulli distribution with support not corresponding to and . Now, we propose two different algorithms differing in the order of projection and optimism operator.

Optimism-Then-Projection.

RODI-OTP applies the optimism operator first, followed by the projection operator:

Note that . For Bernoulli distribution, the optimism operator admits a simple form

Applying optimism operator to yields

We can simplify the update in a parametric form

Finally, we apply the projection rule (cf. Equation 5) to obtain

where

Remark 16

and are fixed (independent of ) and known. Therefore we can compute their values for all in advance.

Projection-Then-Optimism.

RODI-PTO applies the projection operator first, followed by the optimism operator:

The update can be represented in a parametric form

After applying optimism operator and projection operator, both RODI-OTP and RODI-PTO update the value functions and policies accordingly

Computational complexity. The time complexity of RODI-OTP and RODI-PTO is given as follows: i) computation of and : ; ii) parametric Bellman update: ; iii) projection: ; iv) optimism operator: ; v) computation of -function: ; vi) greedy policy: . Therefore, the total time complexity is given by

which is the same as that of RSVI2. The space complexity of both algorithm is given as follows: i) and : ; ii) : ; iii) trajectory : ; iv) probabilities : ; v) action-value function: . Therefore, their total space complexity is .

5.2 Optimism of DRL with Representation

While RODI-OTP and RODI-PTO adapts RODI-MF by Bernoulli representation, they maintain the optimism mainly due to the value-equivalence property of the projection operator.

Optimism of RODI-OTP.

For simplicity, we rewrite the update formula of RODI-OTP as

Define

which is the Bellman target that replaces by the true model . Note that is the distribution generated by the algorithm, which is Bernoulli represented, rather than the optimal distribution . Since

we have

We can prove the argument by induction. Fix . Suppose for any . It follows that

which implies for any . The induction is completed.

Optimism of RODI-PTO.

We rewrite the update of in RODI-PTO as:

Define

then we have

and are both Bernoulli distributions with the same support, thus

We have

Suppose for any . Since , we have

which implies for any . The induction is completed.

6 RODI-MB

We introduce the Model- Based Risk-sensitive Optimistic Distribution Iteration algorithm (RODI-MB, cf. Algorithm 2). Unlike its model-free counterpart, RODI-MB explicitly maintains and updates an empirical transition model within each episode, making it a model-based approach. However, RODI-MB also encounters issues with computational inefficiency. Remarkably, RODI-MB is equivalent to a non-distributional RL algorithm (Algorithm 3). This equivalence results in computational efficiency, as it operates on one-dimensional values rather than full distributions.

Planning phase (Line 5-14) Mirroring the structure of Algorithm 1, RODI-MB also employs approximate DDP in conjunction with the OFU principle. Initially, it applies the distributional optimism operator to the empirical transition model , resulting in an optimistic transition model . The algorithm then utilizes this optimistic model for the Bellman update, generating optimistic return distributions . The subsequent steps remain consistent with those outlined in Algorithm 1.

Interaction phase (Line 16-19) During the interaction phase, the agent engages with the environment using the policy and updates the counts and the empirical transition model based on newly acquired observations.

6.1 Distributional Optimism over the Model

In the RODI-MB algorithm, we introduce a nuanced approach to generating an optimistic transition model, , from the empirical transition model, . This approach is based on the concept of distributional optimism over the space of PMFs rather than CDFs. Specifically, the goal is to compute a return distribution, , from and the future return , such that with high probability.

The distributional optimism operator, , is defined for PMFs over the space with a level , and it operates differently from by also considering the future return distribution :

This operator selects a model from within the norm ball, , that yields the largest EntRM value, . This approach ensures that generates a model with optimistically biased estimates of the future returns, and it leverages an efficient method to achieve this (as detailed in Appendix C).

Given that Lemma 9 assures the high-probability event , the analysis primarily focuses on scenarios conditioned on . Additionally, due to the equivalence between EntRM and EU, the verification of optimism is conducted in terms of EU for .

Lemma 17 (Optimistic model)

For any and , we have

Proof

Use the definition of and the equivalence between EntRM and EU.

Lemma 18 (Optimism)

Conditioned on event , the sequence produced by Algorithm 2 are all greater than or equal to , i.e.,

The proof uses induction, paralleling the methodology in RODI-MF, and leverages Lemma 17 to ensure that the return distributions are optimistically biased.

Proof The induction begins with the terminal stage, , and progresses backwards. For the visited , we have

For the unvisited , it holds that . Thus for any . Assuming for . It follows that for the with

The first inequality is due to Lemma 17. The second inequality follows from the induction assumption. For the unvisited , we have . Since for any , the induction is completed.

6.2 Equivalence to ROVI

The Risk-sensitive Optimistic Value Iteration (ROVI) algorithm, as outlined in Algorithm 3, is a non-distributional approach that processes value functions directly, as opposed to handling return distributions. The RODI-MB algorithm, however, can be demonstrated to be equivalent to ROVI. This equivalence signifies that both algorithms generate the same policy sequence, implying that their resulting trajectories, denoted as , follow the same distribution. This relationship is grounded in the connection between the EntRM and EU, coupled with the linearity property of EU. To formalize this concept of algorithmic equivalence, we define:

Definition 19

For two algorithms and , we say that is equivalent to (vice versa) if for any , any , it holds that .

Under this definition, if two algorithms are equivalent, the trajectories or histories generated by their interactions with any MDP instance will follow the same distribution throughout the episodes. Consequently, these algorithms will enjoy the same regret.

Proof We focus on the case where , noting that the case for can be argued in a similar manner. Fix an arbitrary and . Let (and ) represent Algorithm 3 (and its corresponding policy sequence), while (and ) denote Algorithm 2 (and its respective policy sequence). To establish equivalence, we need to show that aligns with for the given history . By the definition of the two algorithms

If for any , then due to the monotonicity of the exponential function. We will prove that for any by the induction. The base case is evident as . Assuming for all for some , we have and

Given the same history , both algorithms share the empirical transition model , the count , and the optimism constants . Therefore, they also share the optimistic transition model . According to the update formula of Algorithm 3, for any with , we have

This equality also holds for the unvisited state-action pairs, thereby completing the proof of equivalence between Algorithm 2 and Algorithm 3.

6.3 Regret Upper Bound of RODI-MB/ROVI

Theorem 21 (Regret upper bound of RODI-MB/ROVI)

Proof The regret can be bounded as

We can decompose as follows

Using the Lipschitz property of EU

where the second inequality is due to Lemma 10. Term is bounded as

where is a martingale difference sequence with a.s. for all . In summary, we can bound recursively as

Repeating the procedure, we can get

It follows that

The following follows analogously: with probability at least ,

where .

Remark 22

Compared to the traditional/non-distributional analysis dealing with scalars, our analysis is distribution-centered, and we call it the distributional analysis. The distributional analysis deals with the distributions of the return rather than the risk measure values of the return. In particular, it involves the operations of the distributions, the optimism between different distributions, the error caused by estimation of distribution, etc. These distributional aspects fundamentally differ from the traditional analysis that deals with the scalars (value functions).

7 Regret Lower Bound

The section establishes a regret lower bound for EntRM-MDP, serving to understand the fundamental limitations of any learning algorithm in such settings. While previous works, like Fei et al. (2020), have approached this problem by drawing parallels to simpler models like the two-armed bandit, leading to lower bounds that are independent of , and , this approach does not capture the full complexity of MDPs.

In contrast, the approach motivated by Domingues et al. (2021) aims to derive a more comprehensive and tight minimax lower bound that incorporates these factors. For risk-neutral MDPs, the tight minimax lower bound has been established as , but extending this to the risk-sensitive domain is challenging due to the non-linearity of EntRM. In risk-neutral scenarios, the linearity of expectation allows for the interchange of the risk measure (expectation) and summation, simplifying the analysis. However, in the risk-sensitive setting, the non-linear nature of EntRM precludes such straightforward manipulations, necessitating novel proof techniques.

Assumption 1

Assume , and there exists an integer such that . We further assume that and .

Theorem 23 (Tighter lower bound)

Assume Assumption 1 holds and . Let . Then for any algorithm , there exists an MDP such that for we have

Remark 24

As , it recovers the tight lower bound for risk-neutral episodic MDP (see Domingues et al., 2021).

Remark 25

The two conditions in Assumption 1 are used in the our paper and Domingues et al. (2021) to simply the proof. Technically, we can relax these conditions to any MDP with and , which is modestly large. In particular, condition (i) allows us to consider a full -ary tree with nodes, which implies that all the leaves are at the same level in the tree. The proof can be generalized to any by arranging the states in a balanced, but not necessarily full, -ary tree. We can also technically relax condition (ii) to the case . In this case, the resulting bounds will replace by .

7.1 Fixing Lower Bound

Fei et al. (2020) presents the following lower bound.

Proposition 26 (Theorem 3, Fei et al. (2020))

For sufficiently large and , the regret of any algorithm obeys

However, a critical reassessment of the proof reveals inaccuracies that necessitate a revision of the lower bound. The main issue lies in the derivation of the second inequality in the proof provided by Fei et al. (2020), specifically:

The authors establish the second inequality based on the following fact

Fact 3 (Fact 5, Fei et al. (2020) )

For any , the function is increasing and satisfies .

In fact, we can only use Fact 3 to derive , which combined with the first inequality yields

which, notably, does not capture the dependency on and as the original lower bound suggested. Consequently, the corrected version of the lower bound is more conservative and does not reflect the exponential influence of the risk factor and the horizon on the regret. This corrected proposition reads:

Proposition 27 (Correction of Theorem 3, Fei et al. (2020))

For sufficiently large and , the regret of any algorithm obeys

7.2 Proof of Theorem 23

We define as the KL divergence between two Bernoulli distributions with parameters and . We define the probability measure induced by an algorithm and an MDP instance as

where is the probability measure induced by a policy and , which is defined as

The probability measure for the truncated history can be obtained by marginalization

We denote by and the probability measure and expectation induced by and . We omit and if it is clear in the context.

Proof Fix an arbitrary algorithm . We introduce three types of special states for the hard MDP class: a waiting state where the agent starts and may stay until stage , after that it has to leave; a good state which is absorbing and is the only rewarding state; a bad state that is absorbing and provides no reward. The rest states are part of a -ary tree of depth . The agent can only arrive from the root node and can only reach and from the leaves of the tree.

Let be the first parameter of the MDP class. We define and . We denote by the set of leaves of the tree. For each , we define an MDP as follows. The transitions in the tree are deterministic, hence taking action in state results in the -th child of node . The transitions from are defined as

The transitions from any leaf are specified as

where for some constants and to be determined later. and are the second and third parameters of the MDP class. Observe that and are absorbing, therefore we have . The reward is a deterministic function of the state

Finally we define a reference MDP which differs from the previous MDP instances only in that for all . For each and , we define the MDP class

The total expected ERM value of is given by

where the second equality follows from the fact that the reward is non-zero only after step , the third equality is due to that the agent gets into absorbing state when . Define for each and , then it is not hard to obtain that

For an MDP , the optimal policy starts to traverse the tree at step then chooses to reach the leaf and performs action . The corresponding optimal value in any of the MDPs is . Define , then the expected regret of in can be bounded below as

The first inequality holds by setting . The second inequality holds by letting since for . The last equality follows from the fact that

and the definition of .

The maximum of the regret can be bounded below by the mean over all instances as

Observe that it can be further bounded if we can obtain an upper bound on

, which can be done by relating each expectation to the expectation under the reference MDP .

By applying Fact 5 with , we have

By Pinsker’s inequality, it implies that

Since and only differs at stage when , it follows from Fact 6 that

By Lemma 32, we have for and . Consequently,

where the second inequality is due to the Cauchy-Schwartz inequality and the fact that .

It follows that

Choosing maximizes the lower bound

Since and , we have and . Choose and use the assumption that to obtain that . Now we choose and if . Such choice of and guarantees the assumption of Lemma 32 and that , . Finally we use the fact that to obtain

Theorem 23 recovers the tight lower bound for standard episodic MDP, implying that the exponential dependence on and in the upper bounds is indispensable. Yet, it is not clear whether a similar lower bound holds for , which is left as a future direction.

8 Discussion

In this section, we provide a comprehensive comparison of DRL algorithms (RODI-MB, RODI-MF), DRL with distribution representation (RODI-OTP, RODI-PTO), RSVI2 (Fei et al., 2021), RSVI (Fei et al., 2020), and UCBVI (Azar et al., 2017) in terms of regret guarantees and computational complexity. The comparison is also succinctly encapsulated in Table 1.

8.1 Numerical Results

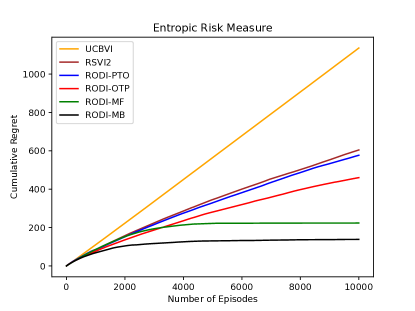

To validate the empirical performance of our algorithms, we conducted numerical experiments comparing RODI-MB, RODI-MF, and RODI-Rep with the risk-neutral algorithm UCBVI (Azar et al., 2017), RSVI in Fei et al. (2020), and RSVI2 in Fei et al. (2021).

The experimental setup involved an MDP with states, actions, and a horizon , mirroring the setup in Du et al. (2022). The MDP consists of a fixed initial state denoted as state 0, and additional states. The agent started in state 0 and could take actions from the set , transitioning to one of the states in in the next step. The transition probabilities and reward functions were defined as follows for :

This MDP was designed to be highly risky, with the risk-neutral optimal policy leading to a mean reward of 0.5 but with a chance of receiving no reward. A risk-sensitive policy might prefer the last action , which offers slightly less mean reward but a more consistent return, indicating lower risk.

We set and . The results, as illustrated in Figure 1, demonstrates the regret ranking of these algorithms :

Figure 1 includes the following key observations:

(i) Advantage of distributional over non-Distributional algorithms: DRL algorithms (RODI and RODI-Rep) outperforms non-distributional algorithms, demonstrating the effectiveness of distributional optimism over bonus-based optimism.

(ii) Performance of RODI vs. RODI-Rep: While RODI shows better performance than RODI-Rep, the latter offers a balance between statistical and computational efficiency.

(iii) Comparison of RODI-Rep with RSVI2: RODI-Rep demonstrates advantages over RSVI2 in terms of sample efficiency, while also maintaining computational efficiency.

8.2 Theoretical Comparisons

8.2.1 RODI vs. RSVI2

We first provide theoretical justifications regarding the regret ranking of RSVI (Fei et al., 2020), RSVI2 (Fei et al., 2021), RODI-MF, and RODI-MB, which demonstrates the advantage of distributional optimism over bonus-based optimism used in RSVI and RSVI2. A key observation regarding the ranking of their value functions is that:

This ordering will be formally presented in Equation 6. The last part of this inequality sequence indicates that all these value functions are indeed optimistic. Given that the level of optimism is mirrored in the value functions, we can deduce:

Considering the relationship between regret and the optimistic value function

it is intuitive that a smaller or less optimism induces reduced regret. Consequently, their regret can be ranked as:

which explains Figure 1. The regret bounds of RODI should at least match those of RSVI2, explaining the ranking of their regret bounds reported in Table 1:

Despite sharing same regret bounds with RSVI2, RODI outperforms RSVI2 both theoretically and empirically. Formally speaking, let denote the value functions generated by RSVI, RSVI2, and RODI-MB respectively. Let denote the distribution generated by RODI-MF. We omit for simplicity.

Proposition 28

Fix . The comparison of their values is as follows:

| (6) | ||||

The proof is detailed in Appendix B. Both RSVI and RSVI2 use exploration bonuses, defined as and respectively, where represents the model estimation error

Both and are formulated as a multiplier times . Notably, , referred to as the the doubly decaying bonus (Fei et al., 2021), decreases its multiplier exponentially across stages , contrasting with in RSVI. In comparison, RODI directly incorporates optimism into the return distribution using an optimism constant . Our distributional analysis establishes a connection between and the bonus via the Lipschitz constant of EU:

where denotes the Lipschitz constant of EU over the distributions supported in . This distributional perspective posits that RSVI and RSVI2 design bonuses to offset the error in value estimates, which is bounded by the product of the Lipschitz constant of EU and the error in the return distribution:

Under the distributional perspective, the multiplier in the bonus is interpreted as the Lipschitz constant that links the return estimation error to the value estimation error . The Lipschitz constant decreases exponentially in as the range of the return distribution narrows. Furthermore, used in RSVI2 is not improvable in the sense that its corresponding Lipschitz constant is proven to be tight, as shown in Lemma 5.

In conclusion, bonus-based optimism requires an exponentially decaying multiplier or Lipschitz constant, whereas distributional optimism functions directly at the distributional level, obviating the need for a multiplier. Next, we theoretically justify the regret ranking of RODI-OTP and RODI-PTO, which interpolates between RODI and RSVI2.

8.2.2 RODI-Rep vs. RSVI2

We delve into the analysis by first explaining why RODI-PTO achieves marginally lower regret compared to RSVI2, and subsequently, we justify the advantage of RODI-OTP over RODI-PTO.

Near-equivalence between RSVI2 and RODI-PTO.

We can show the near-equivalence between RSVI2 and RODI-PTO using induction. Let and denote the value functions generated by RODI-PTO and RSVI2 respectively. We start with the base case that . By the construction of RODI-PTO, we have

verifying the equivalence at step . Now fix . Suppose the following holds

Recall the recursion of in RODI-PTO

It follows that

where the last inequality becomes equality if . By the definition of projection, we obtain

which implies

Then we have . The induction is completed. Moreover, it holds that for every if for every . This condition is likely to be met for large values of , considering that

Advantage of RODI-OTP over RSVI2

Let and denote the value functions generated by RODI-OTP and RSVI2 respectively. The recursion of in RODI-OTP writes

Fix . Note that

then we have

Remark 29

This explains why RODI-OTP achieves an order of magnitude improvement in regret compared with RSVI2 as well as RODI-PTO, as the ”optimism level ratio” of RODI-OTP to RSVI2 at step is quantifiable by

Remark 30

The difference in the optimism level between the two algorithms stems from originates from their respective approaches to bounding the estimation error:

Specifically, RSVI2 treats as a variable within the range . However, since is deterministic and known, the bonus can be refined by acknowledging

where .

Why OTP is better than PTO.

The superiority of OTP over PTO can be substantiated through an insightful observation about the optimization problem:

| (7) | ||||||

| s.t. | ||||||

Let be the optimal solution to this problem. It turns out that the optimal solution is given by , aligning with the OTP principle. Fixing , we interpret as the empirical Bellman operator applied to . Suppose is optimistic relative to the true distribution , i.e., . Define , which is the exact Bellman operator applied to . Given that

the optimal solution satisfies

Hence, the optimal solution is optimistic over . The nature of the optimization problem compels to be the Bernoulli distribution with support that necessitates minimal optimism over . Notably, the PTO solution is also a feasible solution. Consequently, OTP induces less optimism than PTO:

This analysis elucidates the inherent advantage of the OTP approach over PTO. By inverting the order of the projection and optimism operators, OTP not only ensures an optimism over the true distribution but also guarantees that the induced optimism is minimal and necessary.

8.3 Distributional Perspective

The distributional perspective is crucial in both the algorithm design and the regret analysis of RODI, offering advantages and novel approaches.

8.3.1 Algorithm design

Revisiting RSVI2: RSVI2 effectively operates as a model-based algorithm, implicitly maintaining an empirical model through visiting counts. We rewrite the key step in RSVI2 as:

Here, is chosen to ensure optimism:

Distributional perspective: In contrast, the distributional perspective leads to a fundamentally different algorithm design. The primary distinction of RODI is its implementation of return distribution iterations based on approximate distributional Bellman equation. When , RODI transitions to a risk-neutral algorithm, unlike RSVI2, where the log term becomes constant. RODI also introduces distributional optimism, yielding optimistic return distributions without needing a multiplier, unlike bonus-based optimism. This approach not only contrasts sharply with bonus-based methods but also demonstrates improved theoretical and empirical performance.

8.3.2 Regret analysis

Our regret analysis, which we term distributional analysis, stands apart from traditional scalar-focused approaches. This analysis is centered around the distributions of returns rather than the risk values of these returns. It involves various distributional operations, including understanding the optimism between different distributions and the errors caused by distribution estimation. These elements fundamentally differ from classical analysis methods that focus on scalars (value functions). Let’s highlight some novel aspects of our distributional analysis compared to traditional approaches (Fei et al., 2020, 2021).

(i) Distributional optimism. Traditional analysis typically employs OFU to construct a series of optimistic value functions. In contrast, our distributional approach implements optimism directly at the distribution level, leading to a sequence of optimistic return distributions. This involves defining a high probability event under which the true return distribution is close to the estimated one within a certain confidence radius, followed by the application of a distributional optimism operator.

(ii) Lipschitz continuity and linearity in EU. We leverage key properties of EU, such as Lipschitz continuity and linearity, that are crucial in establishing regret upper bounds. The Lipschitz continuity of EU relates the distance between distributions to their EU values’ difference. In contrast, EntRM is non-linear w.r.t. the distribution, potentially introducing a factor of in error propagation across time steps, leading to a compounded factor of in the regret bound.

(iii) Better interpretability. Both RODI and RSVI2 share a same regret bound of

From the distributional perspective, the exponential term is interpreted as the Lipschitz constant of EntRM, highlighting the impact of EntRM’s nonlinearity on sample complexity. A larger Lipschitz constant implies a greater estimation error in values, thus leading to a more unfavorable regret bound.

9 Closing Remarks

In this paper, we present a novel framework for risk-sensitive distributional dynamic programming. We then introduce two types of computationally efficient DRL algorithms, which implement the OFU principle at the distributional level to strike a balance between exploration and exploitation under the risk-sensitive setting. We provide theoretical justification and numerical results demonstrating that these algorithms outperforms existing methods while maintaining computational efficiency compared. Furthermore, we prove that DRL can attain near-optimal regret upper bounds compared with our improved lower bound.

Looking forward, there are several promising avenues for future research. Our current regret upper bound has an additional factor of compared to the lower bound, and it may be possible to eliminate this factor through further algorithmic improvements or refined analysis techniques. Additionally, extending the DRL algorithm from tabular MDP to function approximation settings would be an interesting and valuable direction for future investigation. Lastly, it would be worthwhile to explore whether our DDP framework can be applied to other risk measures beyond the ones considered in this paper.

Appendix A Table of Notation

Appendix B Missing Proofs

B.1 Missing Proofs in Section 4

Proof of Lemma 5

Proof We first provide the proof for the case . For any , without loss of generality we assume , otherwise we switch the order.

For the case , we assume .

Thus for EU. To show the tightness of the constant, consider two scaled Bernoulli distributions and , where are some constants. It holds that

where the last equality holds since (independent of ). More formally, we have

Proof of Lemma 9

Fact 4 ( concentration bound, Weissman et al. (2003))

Let be a probability distribution over a finite discrete measurable space . Let be the empirical distribution of estimated from samples. Then with probability at least ,

Lemma 9 does not directly follow from a union bound together with Fact 4 since the case need to be checked.

Proof Fix some . If , then we have . A simple calculation yields that for any

It follows that

The event is true for the unseen state-action pairs. Now we consider the case that . By Fact 4 , we have that for any integer

Thus,

Applying a union bound over all and rescaling leads to the result.

Lemma 31

Let , it holds that .

B.2 Missing Proofs in Section 6

B.3 Missing Proofs in Section 7

Proof of Lemma 32

Proof Fix , let . It is immediate that

Therefore is strictly convex, increasing in and decreasing in . By Taylor’s expansion, we have that

for some () or (). In particular, for any such that it follows that

where the first inequality follows from the fact that is increasing in and the second inequality is due to that .

Lemma 32

If , and , then .

Fact 5 (Lemma 1, Garivier et al. (2019))

Consider a measurable space equipped with two distributions and . For any -measurable function , we have

where and are the expectations under and respectively.

Fact 6 (Lemma 5, Domingues et al. (2021))

Let and be two MDPs that are identical except for their transition probabilities, denoted by and , respectively. Assume that we have , Then, for any stopping time with respect to that satisfies

B.4 Missing Proofs in Section 8

Proof of Proposition 28

Proof Recall that

We can prove the above inequalities by induction. We only show the proof for . Assume that

induction

for all is equivalent to . Given the linearity of EU, we have

On the other hand,

Therefore,

Since , we have . for all implies .

Observe that

which implies that

Appendix C Additional Property of EntRM

We state some lemmas about the monotonicity-preserving property and their proofs here. The results hold for general risk measures satisfying the monotonicity-preserving property.

Lemma 33

Let be a risk measure satisfying (I). For any and such that and ,

Proof Let and . It holds that

The result follows from (I)

Lemma 34

Let be a risk measure satisfying (I) and be an arbitrary integer. If (and for some ) then for any (and ).

Proof The proof follows from induction. Note that and , therefore by Lemma 33 we have . Suppose that for some it holds that . Since

and , it follows that

The induction is completed. If in addition for some , the proof follows analogously by replacing the inequality to the strict inequality and the fact that .

Lemma 35 (Monotonicity-preserving under pairwise transport)

Let be a risk measure satisfying the monotonicity-preserving property. Suppose and satisfies . For any and any such that

It holds that .

Proof Observe that

By Lemma 33, it suffices to prove . The result follows from the definition and the fact that and .

Lemma 36 (Monotonicity-preserving under block-wise transport)

Suppose and satisfies . It holds that for any satisfying if and otherwise.

Proof Fix . We rewrite the assumption imposed to as for and for , where each . It will be shown that there exists a sequence satisfying and such that , then the proof shall be completed.

sequence is constructed as follows: at the -th iteration, we transport probability mass of to the probability mass of . Specifically, we start from moving to the least number that satisfy and sequentially move to the next one if there is remaining mass. The iteration stops until all the mass are transported. Repeating the procedure for times we obtain . The inequality for each iteration follows from Lemma 35.

Recall that the distributional optimism operator over space of PMFs with level and future return as

By Lemma 36, can be computed as follows

-

•

sort in the ascending order such that

-

•

permute in the order of

-

•

move probability mass of the first states sequentially to the -th state

The computational complexity of the three steps are , , and . Therefore the computational complexity of applying in Line 6 of Algorithm 2 is only .

References

- Achab and Neu (2021) M. Achab and G. Neu. Robustness and risk management via distributional dynamic programming. arXiv preprint arXiv:2112.15430, 2021.

- Azar et al. (2017) M. G. Azar, I. Osband, and R. Munos. Minimax regret bounds for reinforcement learning. In International Conference on Machine Learning, pages 263–272. PMLR, 2017.

- Barth-Maron et al. (2018) G. Barth-Maron, M. W. Hoffman, D. Budden, W. Dabney, D. Horgan, D. Tb, A. Muldal, N. Heess, and T. Lillicrap. Distributed distributional deterministic policy gradients. arXiv preprint arXiv:1804.08617, 2018.

- Bäuerle and Rieder (2014) N. Bäuerle and U. Rieder. More risk-sensitive markov decision processes. Mathematics of Operations Research, 39(1):105–120, 2014.

- Bellemare et al. (2017) M. G. Bellemare, W. Dabney, and R. Munos. A distributional perspective on reinforcement learning. In International Conference on Machine Learning, pages 449–458. PMLR, 2017.

- Bellemare et al. (2023) M. G. Bellemare, W. Dabney, and M. Rowland. Distributional Reinforcement Learning. MIT Press, 2023. http://www.distributional-rl.org.

- Bertsekas et al. (2000) D. P. Bertsekas et al. Dynamic programming and optimal control: Vol. 1. Athena scientific Belmont, 2000.

- Bielecki et al. (2000) T. R. Bielecki, S. R. Pliska, and M. Sherris. Risk sensitive asset allocation. Journal of Economic Dynamics and Control, 24(8):1145–1177, 2000.

- Borkar (2001) V. S. Borkar. A sensitivity formula for risk-sensitive cost and the actor–critic algorithm. Systems & Control Letters, 44(5):339–346, 2001.

- Borkar (2002) V. S. Borkar. Q-learning for risk-sensitive control. Mathematics of operations research, 27(2):294–311, 2002.

- Borkar (2010) V. S. Borkar. Learning algorithms for risk-sensitive control. In Proceedings of the 19th International Symposium on Mathematical Theory of Networks and Systems–MTNS, volume 5, 2010.

- Borkar and Meyn (2002) V. S. Borkar and S. P. Meyn. Risk-sensitive optimal control for markov decision processes with monotone cost. Mathematics of Operations Research, 27(1):192–209, 2002.

- Cavazos-Cadena and Hernández-Hernández (2011) R. Cavazos-Cadena and D. Hernández-Hernández. Discounted approximations for risk-sensitive average criteria in markov decision chains with finite state space. Mathematics of Operations Research, 36(1):133–146, 2011.

- Dabney et al. (2018a) W. Dabney, G. Ostrovski, D. Silver, and R. Munos. Implicit quantile networks for distributional reinforcement learning. In International conference on machine learning, pages 1096–1105. PMLR, 2018a.

- Dabney et al. (2018b) W. Dabney, M. Rowland, M. G. Bellemare, and R. Munos. Distributional reinforcement learning with quantile regression. In Thirty-Second AAAI Conference on Artificial Intelligence, 2018b.

- Davis and Lleo (2008) M. Davis and S. Lleo. Risk-sensitive benchmarked asset management. Quantitative Finance, 8(4):415–426, 2008.

- Delage and Mannor (2010) E. Delage and S. Mannor. Percentile optimization for markov decision processes with parameter uncertainty. Operations research, 58(1):203–213, 2010.

- Dentcheva and Ruszczynski (2013) D. Dentcheva and A. Ruszczynski. Common mathematical foundations of expected utility and dual utility theories. SIAM Journal on Optimization, 23(1):381–405, 2013.

- Di Masi and Stettner (2007) G. B. Di Masi and Ł. Stettner. Infinite horizon risk sensitive control of discrete time markov processes under minorization property. SIAM Journal on Control and Optimization, 46(1):231–252, 2007.

- Di Masi et al. (2000) G. B. Di Masi et al. Infinite horizon risk sensitive control of discrete time markov processes with small risk. Systems & control letters, 40(1):15–20, 2000.

- Domingues et al. (2021) O. D. Domingues, P. Ménard, E. Kaufmann, and M. Valko. Episodic reinforcement learning in finite mdps: Minimax lower bounds revisited. In Algorithmic Learning Theory, pages 578–598. PMLR, 2021.

- Du et al. (2022) Y. Du, S. Wang, and L. Huang. Provably efficient risk-sensitive reinforcement learning: Iterated cvar and worst path. In The Eleventh International Conference on Learning Representations, 2022.

- Ernst et al. (2006) D. Ernst, G.-B. Stan, J. Goncalves, and L. Wehenkel. Clinical data based optimal sti strategies for hiv: a reinforcement learning approach. In Proceedings of the 45th IEEE Conference on Decision and Control, pages 667–672. IEEE, 2006.

- Fei et al. (2020) Y. Fei, Z. Yang, Y. Chen, Z. Wang, and Q. Xie. Risk-sensitive reinforcement learning: Near-optimal risk-sample tradeoff in regret. arXiv preprint arXiv:2006.13827, 2020.

- Fei et al. (2021) Y. Fei, Z. Yang, Y. Chen, and Z. Wang. Exponential bellman equation and improved regret bounds for risk-sensitive reinforcement learning. Advances in Neural Information Processing Systems, 34, 2021.

- Föllmer and Schied (2016) H. Föllmer and A. Schied. Stochastic finance. In Stochastic Finance. de Gruyter, 2016.

- Garivier et al. (2019) A. Garivier, P. Ménard, and G. Stoltz. Explore first, exploit next: The true shape of regret in bandit problems. Mathematics of Operations Research, 44(2):377–399, 2019.

- Hansen and Sargent (2011) L. P. Hansen and T. J. Sargent. Robustness. In Robustness. Princeton university press, 2011.

- Howard and Matheson (1972) R. A. Howard and J. E. Matheson. Risk-sensitive markov decision processes. Management science, 18(7):356–369, 1972.

- Jaśkiewicz (2007) A. Jaśkiewicz. Average optimality for risk-sensitive control with general state space. The annals of applied probability, 17(2):654–675, 2007.

- Keramati et al. (2020) R. Keramati, C. Dann, A. Tamkin, and E. Brunskill. Being optimistic to be conservative: Quickly learning a cvar policy. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 4436–4443, 2020.

- Kupper and Schachermayer (2009) M. Kupper and W. Schachermayer. Representation results for law invariant time consistent functions. Mathematics and Financial Economics, 2:189–210, 2009.

- Liang and Luo (2023) H. Liang and Z.-q. Luo. A distribution optimization framework for confidence bounds of risk measures. arXiv preprint arXiv:2306.07059, 2023.

- Lyle et al. (2019) C. Lyle, M. G. Bellemare, and P. S. Castro. A comparative analysis of expected and distributional reinforcement learning. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 4504–4511, 2019.

- Ma et al. (2020) X. Ma, L. Xia, Z. Zhou, J. Yang, and Q. Zhao. Dsac: Distributional soft actor critic for risk-sensitive reinforcement learning. arXiv preprint arXiv:2004.14547, 2020.

- Ma et al. (2021) Y. Ma, D. Jayaraman, and O. Bastani. Conservative offline distributional reinforcement learning. Advances in Neural Information Processing Systems, 34, 2021.

- Mihatsch and Neuneier (2002) O. Mihatsch and R. Neuneier. Risk-sensitive reinforcement learning. Machine learning, 49(2):267–290, 2002.

- Nass et al. (2019) D. Nass, B. Belousov, and J. Peters. Entropic risk measure in policy search. In 2019 IEEE/RSJ International Conference on Intelligent Robots and Systems (IROS), pages 1101–1106. IEEE, 2019.

- Osogami (2012) T. Osogami. Robustness and risk-sensitivity in markov decision processes. Advances in Neural Information Processing Systems, 25:233–241, 2012.

- Patek (2001) S. D. Patek. On terminating markov decision processes with a risk-averse objective function. Automatica, 37(9):1379–1386, 2001.

- Rowland et al. (2018) M. Rowland, M. Bellemare, W. Dabney, R. Munos, and Y. W. Teh. An analysis of categorical distributional reinforcement learning. In International Conference on Artificial Intelligence and Statistics, pages 29–37. PMLR, 2018.

- Shapiro et al. (2021) A. Shapiro, D. Dentcheva, and A. Ruszczynski. Lectures on stochastic programming: modeling and theory. SIAM, 2021.

- Shen et al. (2013) Y. Shen, W. Stannat, and K. Obermayer. Risk-sensitive markov control processes. SIAM Journal on Control and Optimization, 51(5):3652–3672, 2013.

- Shen et al. (2014) Y. Shen, M. J. Tobia, T. Sommer, and K. Obermayer. Risk-sensitive reinforcement learning. Neural computation, 26(7):1298–1328, 2014.

- Singh et al. (2020) R. Singh, Q. Zhang, and Y. Chen. Improving robustness via risk averse distributional reinforcement learning. In Learning for Dynamics and Control, pages 958–968. PMLR, 2020.

- Sutton and Barto (2018) R. S. Sutton and A. G. Barto. Reinforcement learning: An introduction. MIT press, 2018.

- Von Neumann and Morgenstern (1947) J. Von Neumann and O. Morgenstern. Theory of games and economic behavior, 2nd rev. 1947.

- Weissman et al. (2003) T. Weissman, E. Ordentlich, G. Seroussi, S. Verdu, and M. J. Weinberger. Inequalities for the l1 deviation of the empirical distribution. Hewlett-Packard Labs, Tech. Rep, 2003.

- Yang et al. (2019) D. Yang, L. Zhao, Z. Lin, T. Qin, J. Bian, and T.-Y. Liu. Fully parameterized quantile function for distributional reinforcement learning. Advances in neural information processing systems, 32, 2019.

- Zhang et al. (2021) P. Zhang, X. Chen, L. Zhao, W. Xiong, T. Qin, and T.-Y. Liu. Distributional reinforcement learning for multi-dimensional reward functions. Advances in Neural Information Processing Systems, 34:1519–1529, 2021.