Data-Driven Quickest Change Detection in (Hidden) Markov Models

Abstract

The paper investigates the problems of quickest change detection in Markov models and hidden Markov models (HMMs). Sequential observations are taken from a (hidden) Markov model. At some unknown time, an event occurs in the system and changes the transition kernel of the Markov model and/or the emission probability of the HMM. The objective is to detect the change quickly, while controlling the average running length (ARL) to false alarm. The data-driven setting is studied, where no knowledge of the pre-, post-change distributions is available. Kernel-based data-driven algorithms are developed, which can be applied in the setting with continuous state, can be updated in a recursive fashion, and are computationally efficient. Lower bounds on the ARL and upper bound on the worst-case average detection delay (WADD) are derived. The WADD is at most of the order of the logarithm of the ARL. The algorithms are further numerically validated on two practical problems of fault detection in DC microgrid and photovoltaic systems.

Index Terms:

Maximum Mean Discrepancy, Kernel Method, Fault Detection, Non-i.i.d..I Introduction

In the problem of quickest change detection (QCD), sequential observations are generated from a stochastic process. At some unknown time (change-point), an event occurs and causes the data-generating distribution to undergo a change. The objective is to quickly detect the change, while controlling the false alarm rate. This QCD problem has been widely studied in the literature [3, 4, 5, 6, 7]. It models a wide range of applications, e.g., fault detection in DC microgrids [8], quality control in online manufacturing systems [9], spectrum monitoring in wireless communications [10], early detection of epidemics [11] and signal processing in genetic area [12].

Most existing studies investigate the setting where pre- and post-change samples are independent and identically distributed (i.i.d.), respectively. In [13, 14, 15], the authors prove that the CuSum algorithm is optimal when the samples are i.i.d.. However, the i.i.d. assumption may not hold in practice, e.g., in photovoltaic systems [16], samples are not independent over time. In [17, 18, 19, 20], the general QCD problem for the non-i.i.d. setting is studied, where the approaches are model-based with known pre- and post-change distributions. In [21, 22, 23], the case where samples are generated from a Markov model is investigated. In these literature, both the pre- and post-change distributions are known exactly, and therefore those algorithms may not be applicable if such information is unavailable or the performance may degrade significantly if such information is inaccurate. In this paper, we first study QCD problem in Markov models under the data-driven setting, where neither the pre- nor the post-change transition kernel is known. We then focus on the more challenging hidden Markov models (HMMs), where the pre- and post-change transition kernels and emission probability distributions are unknown.

I-A Related Works

For Markov models, the data-driven setting where the pre- and the post-change transition kernels are unknown is studied in, e.g.,[24, 25]. QCD in Markov models with known pre-change and unknown post-change transition kernels is investigated in [24]. The maximum likelihood estimate (MLE) of the unknown post-change transition kernel is employed to construct a generalized CuSum-type test. However, this method only works for finite state Markov chains or parameterized Markov transition kernels, which is not applicable to general problems with continuous state. QCD in Markov models with both pre- and post-change transition kernels unknown is studied in [25], where a kernel-based method is developed. A kernel method of maximum mean discrepancy (MMD) [26] is employed to construct a CuSum-type test. The kernel MMD method for data-driven QCD under the i.i.d. setting is also investigated in e.g., [27, 28]. However, they focus on the case with i.i.d. samples, and thus their approach cannot be directly applied to our Markov models.

In [29, 30, 31, 32, 33], QCD in HMMs is studied. All these studies investigate the model-based setting with both pre- and post-change information known. However, the information may not be accurate or available in practice, especially when the change is due to some unexpected fault. In [29], the model-based setting with known pre- and post-change distributions for QCD in HMMs with a finite state space is investigated. The -norm of products of Markov random matrices are employed to construct a CuSum test. This approach however only applies to HMMs with a finite state space. In [30], the same problem is investigated. The ratio of the -norms of products of Markov random matrices is employed to construct the log-likelihood in their Shiryayev–Roberts–Pollak test. In [32], a recursive algorithm is designed for the same problem. A quasi-generalized likelihood ratio is employed to update the algorithm in a recursive fashion. The proposed approach however only applies to HMMs with two states and does not generalize to problems with a continuous state space. QCD in HMMs under Bayesian setting is studied in [31], which assumes the change point follows some prior distribution. All the above studies investigate QCD in HMMs with a finite state space and need both the pre- and post-change transition kernels and emission probability distributions.

In [33], QCD in auto-regressive (AR) model is studied, where observations are i.i.d. before the change and follow an AR model after the change. A computationally efficient algorithm is proposed. However, for the data-driven setting, only the lower bound on average running length (ARL) is provided. QCD in AR models is also studied in [16], where the likelihood ratio is approximated using a data-driven method. However, the authors did not provide any theoretical guarantee.

I-B Major Contributions

We develop kernel-based data-driven algorithms for QCD in (hidden) Markov models. We keep a sample buffer of size . Once the buffer is filled, we calculate the MMD between samples in the buffer and a reference batch of pre-change samples. We use this MMD to construct a CuSum-type test. Subsequently, we clear the buffer and continue sampling. The statistic has a negative drift, causing the CuSum to fluctuate around 0 before the change. After the change, it has a positive drift, leading the CuSum to exceed the threshold quickly. We theoretically demonstrate that the lower bound on ARL increases exponentially with the threshold and that the upper bound on the worst-case average detection delay (WADD) is linear in the threshold for both Markov models and HMMs. Hence, the WADD is at most in the logarithm order of the ARL. This result matches with the result of QCD under the model-based setting. Combined with the universal lower bound on the WADD in [17], our algorithm is optimal at the order-level. The primary difficulty in our proof arises from the fact that the samples are generated from (hidden) Markov models, and thus it is essential to explicitly characterize the bias in the MMD estimate for the analysis of ARL and WADD.

When this paper was in preparation, the first version of [25] was posted where the ARL lower bound grows linearly with the threshold, which indicates overly frequent false alarms. Later [25] provides an improved result that the ARL is at least exponentially in the threshold and the upper bound on WADD is linear in the threshold. However, the lower bound on ARL in [25] requires the threshold to be sufficiently large. Here we do not need such assumption. In addition, [25] focuses on Markov models. To the best of the authors’ knowledge, we are the first to develop data-driven algorithms for QCD in HMMs with theoretical performance guarantees and order-level optimal performance. Our algorithm has a complexity of for every samples, whereas the computational complexity in [25] is . Our simulation results also demonstrate that our algorithm has a smaller WADD for a given ARL, and is computationally efficient.

We conduct extensive experiments on synthetic data and two practical fault detection problems in power systems. The numerical results show that for fault detection in DC microgrids, our algorithm outperforms the algorithm proposed in [25] in data-driven settings. For line-to-line fault detection in photovoltaic systems, our data-driven algorithm outperforms the model-based methods if applied with inaccurate system knowledge in [34, 35].

This journal paper provides complete proofs for the results, which were omitted due to space limitation in the conference papers [1, 2]. Moreover, we also add extensive experiments on practical applications of fault detection in DC microgrid and photovoltaic systems, and compare our algorithms with existing approaches.

II Problem Formulation

Markov Models: Consider a Markov chain defined on a probability space with for each and . Define the transition kernel for the Markov chain , where is the transition probability density of given and denotes the probability simplex on . The transition probability density changes at an unknown time from into .

Hidden Markov Models: The state of the Markov chain cannot be observed directly. Instead, we have access to an observable sequence which is adjoined to the Markov chain such that is a Markov chain. For any measurable set , the following condition holds:

Let be the emission probability. At some unknown time , the transition kernel changes from to and/or the emission probability changes from to .

The objective is to detect the change quickly subject to false alarm constraints. In this paper, we investigate the data-driven setting, where are unknown.

Let be a stopping time and let () be the probability measure (expectation) when the change happens at time . Let () be the probability measure (expectation) if no change happens. There is a reference sequence of samples from transition kernel [25, 28, 27]. Use to denote the -field generated by . For HMMs, there is a reference sequence of observations generated from a HMM with transition kernel and emission probability . Denote the hidden state by . Also use to denote the -field generated by . Define the ARL and the WADD for :

| (1) | |||

| (2) |

Here the ARL quantifies the frequency of false alarms, and the WADD demonstrates the number of samples required to trigger an alarm. The objective is to minimize the WADD under the ARL constraint:

| (3) |

where is some pre-specified constant. We assume that the Markov chains with transition kernels and are uniformly ergodic [25, 24], i.e., for any measurable and

| (4) | |||

| (5) |

where and denote the invariant distributions for Markov models with transition kernels and , and , are some constants. It can be demonstrated that under , the invariant distribution of is , and under , the invariant distribution is . Let and be the marginal distribution of the observation under the invariant distribution by and , respectively.

II-A Maximum Mean Discrepancy

In this section, we provide a brief introduction to kernel mean embedding and MMD [36, 26]. Consider a positive definite kernel function : , in a reproducing kernel Hilbert space (RKHS) denoted by . Let be the inner product in the RKHS. For any , we have and Following the reproducing property, any function , . In this paper, we study a bounded kernel function , i.e., . Let be the kernel mean embedding of a probability distribution . For a characteristic kernel , if and only if the probability and are identical[26]. The definition of MMD between distribution and is as follows:

| (6) |

The squared MMD can be written equivalently as [37]:

| (7) |

III Markov Models

In this section, we present our results for Markov models. Markov chains with distinct transition kernels may generate identical stationary distributions [25]. As a result, a straightforward extension of existing QCD methods designed for the i.i.d. setting [27, 28], which estimates the MMD between stationary distributions and , may not be work even . To address this issue, we utilize the second-order Markov chain [25]. We define the product -algebra on , which is generated by the collection of all measurable rectangles as follows: Define the second-order probability measure on measurable space as follows: where and are elements of the -algebra. According to Lemma 1 in [25], if the transition kernels are distinct, the second-order probability measures are distinct. The kernel function and MMD discussed in Section II-A can be straightforwardly extended to the space of .

It can be easily shown that under (), the second-order Markov chain is uniformly ergodic. We then construct the test statistic and the stopping rule using the second-order Markov chain. Our approach is to estimate the MMD between the invariant measures of the second-order Markov chains, and employ this estimate to construct a CuSum-type test.

As a first step, we divide the samples into non-overlapping blocks of . Let , be the second-order Markov chains. For the observation sequence, the pre-change stationary distribution is and the post-change stationary distribution is . For the reference sequence , the stationary distribution is . For the -th block, , define the empirical measure of as where is the Dirac measure. Similarly, we can define . The MMD can then be computed using (II-A). Define where is a positive constant that will be determined later. Then, our stopping time is defined as

| (8) |

where is a predetermined threshold.

Our algorithm can be updated in a recursive fashion: Furthermore, for every block with size the computational complexity for MMD is . At time , there are non-overlapping blocks in total. Thus, the total computational complexity up to time is . In contrast, the algorithm in [25] uses overlapping blocks and has an overall computational complexity of .

Intuitively, when is large, we have that before the change and after the change. For , the test statistic has a negative drift before the change, causing the CuSum to fluctuate around , while after the change, it has a positive drift, leading the CuSum to exceed the threshold quickly.

We present the upper bound on the WADD of (8) in the following theorem. Define and

Theorem 1.

The WADD for the stopping time in (8) can be upper bounded as follows:

| (9) |

Proof.

Let be the index of the last sample within the block where the change occurs. Thus, samples after are generated from transition kernel . Moreover, we have . Let

It can be shown that Denote by . Firstly, for any and we have that

According to the definition of , it can be shown that

| (10) |

It then suffices to bound and to employ (10) iteratively. By the triangle inequality and Markov inequality, we have that

| (11) |

The last inequality in (11) is from Proposition 1, which can be found in Appendix -A. Let , for any and we get and thus . Therefore,

| (12) |

This concludes the proof. ∎

Note that . Thus, the upper bound increases linearly with the threshold and the batch size .

We now derive a lower bound on the ARL, which increases exponentially with the threshold . Let . Due to the fact , there always exists a large such that . Define a function . We choose a constant such that . Note that is a continuous function of , with and as . Thus, there always exists such a value for .

Theorem 2.

The ARL of in (8) can be lower bounded exponentially in the threshold :

Proof.

Let and We first show that for any , Since , we have that for any ,

where (a) is from the triangle inequality, and (b) is from Proposition 2, which will be given later. Therefore, we have that

Let , we get . Therefore,

| (13) |

Define as and for some Following the definition of , it can be shown that

| (14) |

We then bound . For any , we have

where the last inequality is from (13). Therefore is a non-negative supermartingale. Hence

where the first inequality is from [27, Lemma A.2] and [38, Theorem 7.9.2]. Then we can get

We then have that

where the indicator function if , otherwise . This further suggests that

This concludes the proof. ∎

It is worth noting that and are independent of . Therefore, the lower bound on ARL increases exponentially with the threshold . For any stopping time with , the detection delay is at least (according to the universal lower bound result in [17]). By Theorem 2, we choose the threshold to guarantee the false alarm constraint. By Theorem 1, this further implies that our algorithm attains a detection delay of . This result matches with (order-level) the universal lower bound in [17] for the general non-i.i.d. setting.

IV Hidden Markov Models

In this section, we present our results for HMMs. Similar to Markov models, for the HMMs, with distinct transition kernels and and/or emission probability distributions, their stationary distributions and/or the induced marginal distributions of the observations may remain identical.

We generalize the idea of using second-order Markov chain in Section III to the HMMs and explore higher-order HMMs. Denote the -th order HMM by:

and the corresponding -th order observation sequence: It is worth noting that the -th order HMM is an HMM, and remains uniformly ergodic. To simplify notation, let and be the marginal distributions of the -th order observation under the corresponding stationary distributions.

For simplicity of the presentation, we focus on the case with , and introduce the following assumption. This assumption guarantees that and are distinct (as shown in Lemma 2 in Appendix -D), thus ensuring the detectability of the change. Utilizing a higher order model will lead to a relaxed assumption than Assumption 1, although it will introduce additional computational cost. Generalization to a higher order model is straightforward.

Assumption 1.

There exist such that

Let be the second-order observation and be the second-order hidden state. Based on Lemma 2 and Assumption 1, it can be shown that . Let denote the observation at time of the second-order reference sequence. We partition the samples into non-overlapping blocks of size . For the -th observation block, where , we obtain second-order samples and the empirical distribution for this block is . Similarly, for the -th reference block, we have We then can calculate the MMD between these two empirical distributions using (II-A).

We define our test statistic as The offset is to ensure that the test statistic has a negative drift prior to the change and a positive drift after the change. Then, we define our stopping time as

| (15) |

This algorithm can be updated recursively and the computational complexity for samples is (see Section III).

Intuitively, when is large, we have that prior to the change and after the change. Thus, by selecting a offset , the test statistic has a negative drift before the change while after the change, it has a positive drift. Let . We then provide the upper bound on the WADD.

Theorem 3.

The WADD for the stopping time in (15) can be upper bounded as follows:

| W | ||||

| (16) |

The proof is similar to Theorem 1. An important step is to show that the expectation of the MMD between the marginal distribution of the stationary distribution and the empirical probability under and the MMD between and under is upper bounded, which is shown in Proposition 3 (see Appendix -E).

We now provide a lower bound on the ARL of in (15), which increases exponentially with the threshold . One key step is to establish a high-probability bound on the sum of two MMDs between and () (see Proposition 4 in Appendix -F). The main challenge is that the McDiarmid’s inequality [39] cannot be applied to HMMs. Let . Due to the fact that , there always exists a large that . Define a function as follows: , where is defined in Proposition 4. We choose a constant such that . Note that is a continuous function of , with , as . Therefore, there always exists such a value for .

Theorem 4.

The lower bound on the ARL in (15) increases exponentially with the threshold :

The proof is similar to the one for Theorem 2 and is omitted.

V Numerical Results

V-A Synthetic Data

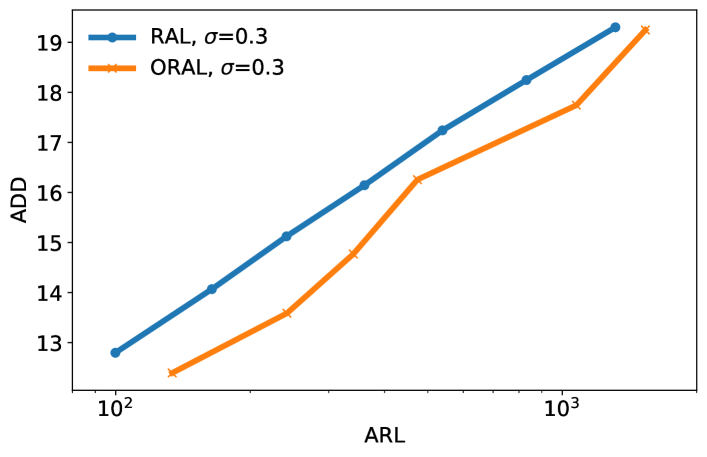

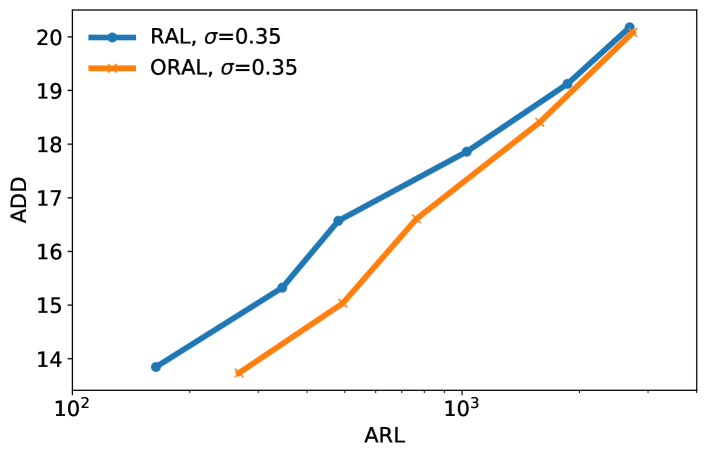

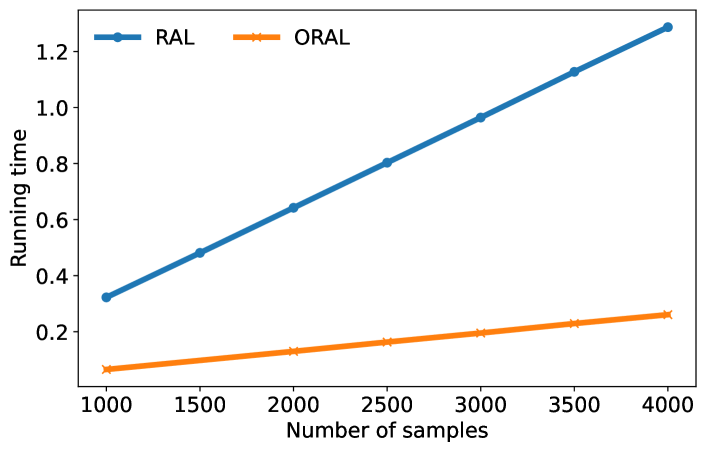

We refer the algorithm introduced in [25] as RAL (oveRlApping bLocks) and the proposed algorithm in this paper as ORAL (nOn-oveRlApping bLocks). We then compare their performance. We consider a case where the transition kernel of a Markov model changes from to . We utilize the Gaussian kernel function , with the bandwidth parameter . We choose and test two different values of , and respectively. We select [40] which attains the best tradeoff between ADD and ARL. To compare the ADD and the ARL, in Figs 3 and 3, we plot the ADD as a function of the logarithm of ARL by adjusting the threshold. Additionally, we provide a comparison of the computational complexity in Fig 3, showing the running time in relation to the overall number of samples (on Intel W-2295 CPU).

Figs 3 and 3 clearly demonstrate that our approach outperforms the approach in [25], i.e., for a given ARL, our method requires fewer samples to detect the change. Furthermore, both methods exhibit a linear relationship between the ADD and the logarithm of ARL, which aligns with our WADD upper bounds derived in this paper. Fig 3 demonstrates the computationally efficiency of our algorithm.

V-B Fault Detection in DC Microgrid

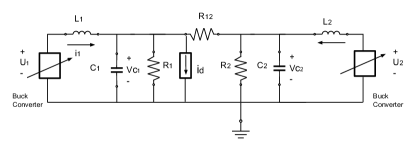

We consider a discrete state space model of a DC microgrid. The circuit for this model is shown in Fig 5. There are two buck converters and the reference voltage V for both. For generator 1, set the inductance mH, the capacitance mF, the parallel resistor and the droop gain of the buck converter is . For generator 2, set the inductance mH, the capacitance mF, the parallel resistor , the droop gain .

Due to a certain current source load or a line-to-ground fault, there is a current source in parallel with and we use to denote this disturbance. The change of this disturbance indicates the presence of a fault in either the load itself or a line to ground fault. According to the circuit, we derive the following discretized state space equations for this system:

where is the system state and is the disturbance for the -th time period and the time step is ms. Then we detect the different changes of the disturbance .

Set and respectively. We choose the Gaussian kernel function and we pick that achieves the best ADD and ARL tradeoff. Firstly, we only change the mean of the distribution of disturbance. For the pre-change, follows . After the change point, the distribution of the process fault changes into . In Table I, we provide the ADD and ARL with a group of thresholds.

We then change the variance of the distribution of disturbance. For the pre-change, follows . After the change point, the distribution of the process fault changes into . The results can be found in Table II. Finally, we change both the mean and variance. For the pre-change, follows . After the change point, the distribution of the process fault changes into . In Table III, we provide the ADD and ARL with a group of thresholds. From the above Tables, it can be seen that for both algorithms, the ADD grows with the log of ARL linearly. Moreover, our method outperforms the method in [25], i.e., for the same level of ARL, our method needs less samples to raise an alarm.

| RAL,=0.45 | ADD | 7.29 | 7.44 | 7.57 | 7.73 |

| ARL | 13465 | 21489 | 26889 | 37432 | |

| ORAL,=0.45 | ADD | 5.80 | 6.01 | 6.18 | 6.62 |

| ARL | 13839 | 19697 | 23361 | 42792 | |

| RAL,=0.5 | ADD | 7.30 | 7.45 | 7.58 | 7.73 |

| ARL | 13414 | 21668 | 26865 | 37737 | |

| ORAL,=0.5 | ADD | 5.79 | 6.01 | 6.20 | 6.64 |

| ARL | 13881 | 19614 | 23255 | 42684 | |

| RAL,=0.55 | ADD | 7.44 | 7.66 | 7.97 | 8.12 |

| ARL | 57148 | 79165 | 138884 | 185535 | |

| ORAL,=0.55 | ADD | 6.20 | 6.51 | 6.76 | 7.26 |

| ARL | 43347 | 76092 | 90716 | 161087 |

| RAL,=0.45 | ADD | 49.83 | 53.98 | 57.63 | 60.43 |

| ARL | 4799 | 6609 | 8744 | 10469 | |

| ORAL,=0.45 | ADD | 50.45 | 53.11 | 56.8 | 60.01 |

| ARL | 5404 | 7222 | 9216 | 11923 | |

| RAL,=0.5 | ADD | 64.54 | 71.03 | 76.04 | 81.09 |

| ARL | 15479 | 22094 | 27274 | 33262 | |

| ORAL,=0.5 | ADD | 60.00 | 65.89 | 69.85 | 75.34 |

| ARL | 13309 | 19227 | 22570 | 30724 | |

| RAL,=0.55 | ADD | 87.38 | 96.74 | 112.46 | 120.71 |

| ARL | 50650 | 82322 | 177690 | 245290 | |

| ORAL,=0.55 | ADD | 80.08 | 88.25 | 96.98 | 111.58 |

| ARL | 43726 | 78065 | 100750 | 191223 |

| RAL,=0.45 | ADD | 7.05 | 7.13 | 7.22 | 7.37 |

| ARL | 4576 | 7623 | 8513 | 9743 | |

| ORAL,=0.45 | ADD | 5.10 | 5.16 | 5.25 | 5.52 |

| ARL | 4276 | 6298 | 8294 | 11432 | |

| RAL,=0.5 | ADD | 7.14 | 7.31 | 7.47 | 7.67 |

| ARL | 16348 | 22836 | 29068 | 35411 | |

| ORAL,=0.5 | ADD | 5.25 | 5.44 | 5.62 | 6.12 |

| ARL | 13682 | 18080 | 24296 | 39112 | |

| RAL,=0.55 | ADD | 7.29 | 7.54 | 7.92 | 8.03 |

| ARL | 51673 | 83208 | 151070 | 211081 | |

| ORAL,=0.55 | ADD | 5.61 | 5.97 | 6.25 | 6.99 |

| ARL | 45251 | 65933 | 98174 | 157802 |

V-C Fault Detection in Photovoltaic System

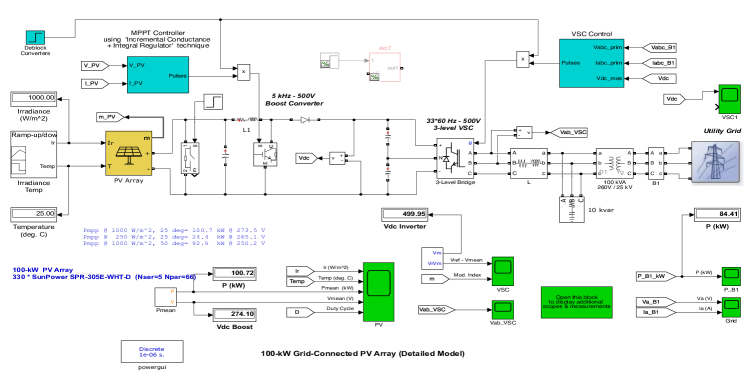

In this section, we implement the proposed algorithm to a simulated Photovoltaic (PV) system to detect the line-to-line fault. An auto-regressive process can be used to model faulty signal and noise in the PV system [16], which is an HMM. In Fig 4 we show our simulated PV system in Matlab by applying the toolbox SimPowerSystems. In our system, there is one 100-kW PV panel array with 5 × 66 PV modules as the input, a boost converter, a three-level voltage source converter (VSC), a 25-kV grid as the output and the simulation time step is . We choose the maximum power point tracking (MPPT) with Incremental Conductance and Integral Regulator technique as our system controller. We consider a line-line fault, which is simulated by a timed breaker. During the change, the breaker is closed and the positive output of the PV array is connected to the negative output. We set the breaker resistance to . Without requiring the knowledge of current or power, we only need the output voltage of the PV system to run our algorithm. Set . We choose the Gaussian kernel function and we pick .

We compare our approach with a model-based change detection algorithm [34, 35], where adaptive filters are combined with the CuSum algorithm to detect the change. We design a Kalman filter for our PV system. Then the output residual signals should follow Gaussian distributions with zero mean. The change in the system will lead to a change in the mean and variance of the Gaussian distributions. The construction of the Kalman filters needs the entire knowledge of the PV circuits, which is hard to obtain in the data-driven setting. Hence, we measure the mean and variance of the residual signals with the unmatched Kalman filter, where only one parameter, the input capacitance , is different from the ideal model. Then a CuSum algorithm is applied.

| Model Based,=1 | ADD | 20.03 | 23.74 | 24.53 | 26.37 | 30.51 |

| ARL | 224.59 | 257.9 | 265.04 | 277.36 | 319.36 | |

| Model Based,=0.5 | ADD | 19.91 | 23.47 | 25.51 | 28.27 | 29.54 |

| ARL | 76.05 | 130.49 | 145.29 | 231.98 | 285.81 | |

| ORAL | ADD | 20.55 | 22.36 | 23.55 | 27.45 | 31.05 |

| ARL | 4485.85 | 5014.53 | 5228.55 | 5589.60 | 5840.61 |

In Table IV, we provide the ADD and ARL with different thresholds. It shows that for the same level of ADD, our method achieves a larger ARL, which demonstrates that our method outperforms the model-based method with unmatched system information.

VI Conclusion

In this paper, we investigated the data-driven quickest change detection problem, focusing on both Markov models and HMMs. We developed kernel-based detection algorithms and analyzed the bias in MMD estimates for both Markov models and HMMs. Moreover, we established theoretical lower bound on ARL and upper bound on WADD. We demonstrated that the WADD is at most in the logarithm of the ARL. Combined with the universal lower bound on the WADD in [17], our approach is optimal at order-level. Furthermore, in the case of Markov models, compared with existing state-of-the-art study in the same setting, our theoretical bounds are more stringent and our algorithms are computationally efficient. Our algorithm is the first data-driven one for QCD in HMMs with theoretical performance guarantees. Simulation results demonstrate the performance of our proposed algorithms.

-A Proposition 1 and Proof

Recall that ( ) and are the invariant measure and empirical measure of under (), respectively. The proof of Theorem 1 uses the following upper bounds of the expectation of their MMD.

Proposition 1.

and .

Proof.

Recall that the samples in this paper are non-i.i.d., we define the coefficient under and under .

Lemma 1.

Under and respectively, for , we have

Note the kernel is bounded. Then, Therefore, we have that

| (17) |

Moreover, . Since is a constant, there exists an upper bound on the expectation of MMD between the empirical measure and invariant measure for each block. The proof under follows similarly. ∎

-B Proof of Lemma 1

We provide the proof under . The proof under can be derived in the same way. It can be shown that

| (18) |

where (a) is due to the absolute value inequality and (b) is due to the uniformly ergodicity.

-C Proposition 2 and Proof

Define and Let Then is defined as

We derive a proposition that provides a high-probability bound on the sum of two MMDs between the invariant measure and the empirical measure.

Proposition 2.

For any , and ,

Proof.

For any and , we define a function

| (19) |

When there is no change, the Markov chains and are uniformly ergodic. Then it can be shown that the Markov chain is uniformly ergodic. For any , and , it can be easily shown that

-D Sufficient Condition to Guarantee Detectability

Lemma 2.

For any , if the conditional distributions , then we have

| (21) |

-E Proposition 3 and Proof

Proposition 3.

and .

For HMMs, we define the coefficients under and under .

Lemma 3.

Under and , respectively, for , we have and

Based on Lemma 3, the proof of Proposition 3 follows the proof of Proposition 1 in Appendix -A thus is omitted here. We then provide the proof of the first inequality in Lemma 3. The proof of the second inequality can be derived via the same process. For and , we have that

| (24) |

Due to the uniform ergodicity of , it follows that Thus, it follows that

| (25) |

-F Proposition 4 and Proof

Proposition 4.

Proof.

For any and , we define two functions

| (27) | ||||

| (28) |

We then have that

For any ,

| (29) |

where

| (30) |

For any , we have that where

| (31) | ||||

| (32) |

By [39, Theorem 3.1], which is a generalization of the McDiarmid’s inequality to uniformly ergodic Markov chains, we have that for any , Given any , are independent. Thus by McDiarmid’s inequality, we have that for any Let , , we have that . Then it follows that

| (33) |

Further applying Proposition 3 concludes the proof. ∎

References

- [1] Q. Zhang, Z. Sun, L. C. Herrera, and S. Zou, “Data-driven quickest change detection in Markov models,” in Proc. IEEE Int. Conf. Acoust. Speech Signal Process. (ICASSP), pp. 1–5, IEEE, 2023.

- [2] Q. Zhang, Z. Sun, L. C. Herrera, and S. Zou, “Data-driven quickest change detection in hidden Markov models,” in Proc. IEEE Int. Symp. Inf. Theory (ISIT), pp. 2643–2648, IEEE, 2023.

- [3] H. V. Poor and O. Hadjiliadis, Quickest Detection. Cambridge University Press, 2009.

- [4] A. Tartakovsky, I. Nikiforov, and M. Basseville, Sequential Analysis: Hypothesis Testing and Changepoint Detection. CRC Press, 2014.

- [5] L. Xie, S. Zou, Y. Xie, and V. V. Veeravalli, “Sequential (quickest) change detection: Classical results and new directions,” IEEE J. Sel. Areas Inf. Theory, vol. 2, no. 2, pp. 494–514, 2021.

- [6] V. V. Veeravalli and T. Banerjee, “Quickest change detection,” Academic press library in signal processing: Array and statistical signal processing, vol. 3, pp. 209–256, 2013.

- [7] M. Basseville and I. V. Nikiforov, Detection of Abrupt Changes: Theory and Application, vol. 104. Prentice Hall Englewood Cliffs, 1993.

- [8] K. Gajula, V. Le, X. Yao, S. Zou, and L. Herrera, “Quickest detection of series arc faults on DC microgrids,” in Proc. IEEE Energy Convers. Congr. Expo. (ECCE), pp. 796–801, IEEE, 2021.

- [9] T. L. Lai, “Sequential changepoint detection in quality control and dynamical systems,” Journal of the Royal Statistical Society. Series B (Methodological), pp. 613–658, 1995.

- [10] L. Lai, Y. Fan, and H. V. Poor, “Quickest detection in cognitive radio: A sequential change detection framework,” in Proc. IEEE Glob. Telecom. Conf. (GLOBECOM), pp. 1–5, 2008.

- [11] M. Baron, V. Antonov, C. Huber, M. Nikulin, and V. Polischook, “Early detection of epidemics as a sequential change-point problem,” Longevity, Aging and Degradation Models in Reliability, Public Health, Medicine and Biology, LAD, pp. 7–9, 2004.

- [12] J. J. Shen and N. R. Zhang, “Change-point model on nonhomogeneous Poisson processes with application in copy number profiling by next-generation DNA sequencing,” Ann. Appl. Statist., vol. 6, no. 2, pp. 476–496, 2012.

- [13] M. Pollak, “Optimal detection of a change in distribution,” Ann. Statist., pp. 206–227, 1985.

- [14] G. V. Moustakides, “Optimal stopping times for detecting changes in distributions,” Ann. Statist., vol. 14, no. 4, pp. 1379–1387, 1986.

- [15] Y. Ritov, “Decision theoretic optimality of the CUSUM procedure,” Ann. Statist., pp. 1464–1469, 1990.

- [16] L. Chen, S. Li, and X. Wang, “Quickest fault detection in photovoltaic systems,” IEEE Trans. Smart Grid, vol. 9, no. 3, pp. 1835–1847, 2016.

- [17] T. L. Lai, “Information bounds and quick detection of parameter changes in stochastic systems,” IEEE Trans. Inform. Theory, vol. 44, no. 7, pp. 2917–2929, 1998.

- [18] A. G. Tartakovsky and V. V. Veeravalli, “General asymptotic Bayesian theory of quickest change detection,” Theory of Prob. and App., vol. 49, no. 3, pp. 458–497, 2005.

- [19] M. Baron and A. Tartakovsky, “Asymptotic optimality of change-point detection schemes in general continuous-time models,” Sequential Analysis, vol. 25, no. 3, pp. 257–296, 2006.

- [20] A. G. Tartakovsky, “On asymptotic optimality in sequential changepoint detection: Non-iid case,” IEEE Trans. Inform. Theory, vol. 63, no. 6, pp. 3433–3450, 2017.

- [21] B. Yakir, “Optimal detection of a change in distribution when the observations form a Markov chain with a finite state space,” Lecture Notes-Monograph Series, pp. 346–358, 1994.

- [22] A. M. Polansky, “Detecting change-points in Markov chains,” Computational statistics & data analysis, vol. 51, no. 12, pp. 6013–6026, 2007.

- [23] B. Darkhovsky, “Change-point problem for high-order Markov chain,” Sequential Analysis, vol. 30, no. 1, pp. 41–51, 2011.

- [24] J.-G. Xian, D. Han, and J.-Q. Yu, “Online change detection of Markov chains with unknown post-change transition probabilities,” Commun. Stat. - Theory Methods, vol. 45, no. 3, pp. 597–611, 2016.

- [25] H. Chen, J. Tang, and A. Gupta, “Change detection of Markov kernels with unknown post change kernel using maximum mean discrepancy,” arXiv preprint arXiv:2201.11722, 2022.

- [26] B. K. Sriperumbudur, A. Gretton, K. Fukumizu, B. Schölkopf, and G. R. Lanckriet, “Hilbert space embeddings and metrics on probability measures,” J. Mach. Learn. Res., vol. 11, pp. 1517–1561, 2010.

- [27] T. Flynn and S. Yoo, “Change detection with the kernel cumulative sum algorithm,” in Proc. IEEE Conf. Decis. Control (CDC), pp. 6092–6099, IEEE, 2019.

- [28] S. Li, Y. Xie, H. Dai, and L. Song, “Scan B-statistic for kernel change-point detection,” Sequential Analysis, vol. 38, no. 4, pp. 503–544, 2019.

- [29] C.-D. Fuh, “SPRT and CUSUM in hidden markov models,” Ann. Statist., vol. 31, no. 3, pp. 942–977, 2003.

- [30] C.-D. Fuh, “Asymptotic operating characteristics of an optimal change point detection in hidden Markov models,” Ann. Statist., vol. 32, no. 5, pp. 2305–2339, 2004.

- [31] C.-D. Fuh and A. G. Tartakovsky, “Asymptotic Bayesian theory of quickest change detection for hidden Markov models,” IEEE Trans. Inform. Theory, vol. 65, no. 1, pp. 511–529, 2018.

- [32] C.-D. Fuh and Y. Mei, “Quickest change detection and Kullback-Leibler divergence for two-state hidden Markov models,” IEEE Trans. Signal Proc., vol. 63, no. 18, pp. 4866–4878, 2015.

- [33] Z. Sun and S. Zou, “Quickest change detection in autoregressive models,” arXiv preprint arXiv:2310.08789, 2023.

- [34] F. Gustafsson and F. Gustafsson, Adaptive Filtering and Change Detection, vol. 1. Wiley New York, 2000.

- [35] Z. Liu and H. He, “Sensor fault detection and isolation for a lithium-ion battery pack in electric vehicles using adaptive extended Kalman filter,” Appl. Energy, vol. 185, pp. 2033–2044, 2017.

- [36] A. Berlinet and C. Thomas-Agnan, Reproducing kernel Hilbert spaces in probability and statistics. Springer Science & Business Media, 2011.

- [37] A. Gretton, K. M. Borgwardt, M. J. Rasch, B. Schölkopf, and A. Smola, “A kernel two-sample test,” J. Mach. Learn. Res., vol. 13, no. 1, pp. 723–773, 2012.

- [38] R. G. Gallager, “Discrete stochastic processes,” OpenCourseWare: Massachusetts Institute of Technology, 2011.

- [39] A. Havet, M. Lerasle, E. Moulines, and E. Vernet, “A quantitative Mcdiarmid’s inequality for geometrically ergodic Markov chains,” Electron. Commun. Probab., vol. 25, pp. 1–11, 2020.

- [40] “RBF (Gaussian) kernel description.” https://scikit-learn.org/stable/modules/generated/sklearn.metrics.pairwise.rbf_kernel.html. Accessed: 2023-10-16.