Allowing for weak identification when testing GARCH-X type models

Abstract

In this paper, we use the results in Andrews and Cheng (2012), extended to allow for parameters to be near or at the boundary of the parameter space, to derive the asymptotic distributions of the two test statistics that are used in the two-step (testing) procedure proposed by Pedersen and Rahbek (2019). The latter aims at testing the null hypothesis that a GARCH-X type model, with exogenous covariates (X), reduces to a standard GARCH type model, while allowing the “GARCH parameter” to be unidentified. We then provide a characterization result for the asymptotic size of any test for testing this null hypothesis before numerically establishing a lower bound on the asymptotic size of the two-step procedure at the 5% nominal level. This lower bound exceeds the nominal level, revealing that the two-step procedure does not control asymptotic size. In a simulation study, we show that this finding is relevant for finite samples, in that the two-step procedure can suffer from overrejection in finite samples. We also propose a new test that, by construction, controls asymptotic size and is found to be more powerful than the two-step procedure when the “ARCH parameter” is “very small” (in which case the two-step procedure underrejects).

Keywords: Boundary, weak identification, testing.

1 Introduction

In a GARCH-X type model, the variance of a generalized autoregressive conditional heteroskedasticity (GARCH) type model is augmented by a set of exogenous regressors (X). Naturally, the question arises if the more general GARCH-X type model can be reduced to the simpler GARCH type model. Statistically speaking, the problem reduces to testing whether the coefficients on the exogenous regressors are equal to zero. As noted in Pedersen and Rahbek (2019) (PR hereinafter), the testing problem is non-standard due to the presence of two nuisance parameters that could possibly be at the boundary of the parameter space. In addition, under the null hypothesis, one of the nuisance parameters, the “GARCH parameter”, is not identified when the other, the “ARCH parameter”, is at the boundary. In order to address this possible lack of identification, PR suggest a two-step (testing) procedure, where rejection in the first step is taken as “evidence” that the model is identified. In the second step, the authors then impose an “additional assumption”, which implies that a specific entry of the inverse information equals zero, to obtain an asymptotic null distribution of their second-step test statistic that is nuisance parameter free. There are two potential problems with this two-step procedure. First, it may not control (asymptotic) size, i.e., its (asymptotic) size may exceed the nominal level, for reasons similar to those that invalidate “naive” post-model-selection inference (see e.g., Leeb and Pötscher, 2005, 2008). In addition, the aforementioned “additional assumption” may not be satisfied, which may possibly aggravate the problem. Second, the two-step procedure may, due to its two-step nature and despite the possible lack of (asymptotic) size control, have poor power in certain parts of the parameter space, as suggested by simulations in PR.222The simulation results in Appendix D of PR show that the two-step procedure has a null rejection frequency below the nominal level for “very small” values of the ARCH parameter; see also Section 5.

In this paper, we use the results in Andrews and Cheng (2012) (AC hereinafter), extended to allow for parameters to be near or at the boundary of the parameter space,333Here, the parameter space is equal to a product space; see Cox (2022) for related results in the context of more general shapes of the parameter space. to derive the asymptotic distributions of the two test statistics used in PR under weak, semi-strong, and strong identification (using the terminology in AC). These asymptotic distribution results, in turn, allow us characterize the asymptotic size of any test for testing the null hypothesis that the coefficients on the exogenous regressors are equal to zero. We numerically establish lower bounds on the asymptotic sizes of the two-step procedure proposed by PR as well as a second testing procedure proposed by PR that assumes that the ARCH parameter is known to be in the interior of the parameter space. These bounds are given by 6.65% and 9.48%, respectively, for a 5% nominal level, which implies that the two testing procedures do not control asymptotic size (at the 5% nominal level).444These lower bounds (also) apply if the “additional assumption” and, in case of the second testing procedure, the assumption that the ARCH parameter is in the interior of the parameter space are satisfied; see Remark 1 for details. Furthermore, we propose a new test based on the second-step test statistic of PR that uses plug-in least favorable configuration critical values and, thus by construction, controls asymptotic size.

In a small simulation study, we find that our asymptotic theory provides good approximations to the finite-sample behaviors of the tests, or testing procedures, that we consider. In particular, we find that the testing procedures proposed by PR can suffer from overrejection in finite samples. Furthermore, we find that our new test has greater power than the two-step procedure for “very small” values of the ARCH parameter, a presumably empirically important region of the parameter space. This finding is line with the intuition that the two-step procedure, in some sense, “sacrifices” power for such parameter constellations due to its two-step nature.

The remainder of this paper is organized as follows. In Section 2, we introduce the testing problem as well as the two testing procedures proposed by PR. In Section 3, we present the asymptotic distribution results. Section 4 presents the characterization result for asymptotic size and obtains the lower bounds on the asymptotic sizes of the two testing procedures proposed by PR. It also introduces our new test. The result of our simulation study are presented in Section 5. Additional material, including proofs, is relegated to the Appendix.

Throughout this paper, we use the following conventions. All limits are taken “as ”. denotes a vector of zeros (of suitable dimension) with a one in the position. For any matrix , denotes the entry with row index and column index . Furthermore, means that , where denotes the Euclidean norm. Lastly, “for all ” abbreviates “for all sequences of positive scalar constants for which ”.

2 Testing problem

For ease of exposition, we consider a simple version of the GARCH-X(1,1) model with a single exogenous variable (as in PR). In particular, the model is given by

| (1) |

where and

| (2) |

with .555For ease of reference, we adopt the notation in AC, where governs the identification strength of (see (4) below) and is always identified. Here, is observed and is unobserved. The true parameter space for , i.e., the space of all possible true values of , is given by , where

for some , , , and .

The model is estimated by quasi-maximum likelihood. In particular, the objective function is given by (- times) the Gaussian-based conditional quasi log-likelihood function, i.e., , where

and where . The quasi-maximum likelihood estimator is given by

where denotes the optimization parameter space with

for some , , , , and . Note that, given the definitions of and , (the true values of) , , and are allowed to be at the boundary of the optimization parameter space.

While our asymptotic distribution results are useful for analyzing a wide range of testing problems, we are mainly interested in testing

| (3) |

As pointed out in PR, this testing problem is non-standard in that, under , there are two nuisance parameters that may be at the boundary of the (optimization) parameter space, and . Furthermore, when is at the boundary () then is not identified under . To see this, note that, given , we have

| (4) |

and, thus, . In words, under , implies that the distribution of the data does not depend on , i.e., and (with ) are observationally equivalent.

Let denote a generic test statistic for testing (3) and let cvn,1-α denote the corresponding nominal level critical value, which may depend on . The size of the test that rejects when is given by Sz, where denotes the true parameter space for and where denotes the distribution of . We say that a test controls size if Sz. We note that “uniformity” (over ) is built into the definition of SzT and that whether a test controls size crucially depends on . Typically, it is infeasible to compute SzT. Therefore, we rely on asymptotic approximations. In particular, we approximate the (“finite-sample”) size of a test by its asymptotic size, which is given by

While “still” depends on , it generally only does so through a finite-dimensional parameter, making its evaluation “easier”. We say that a test controls asymptotic size if AsySz. In large samples, AsySzT provides a good approximation of SzT so that a test that controls asymptotic size can be expected to “approximately” control size. Therefore, in what follows we focus on whether or not a given test, or testing procedure, controls asymptotic size.

2.1 Testing procedures proposed by PR

Given the non-standard nature of the testing problem in (3), PR propose a two-step procedure to deal with the presence of nuisance parameters on the boundary of the parameter space as well as the lack of identification of when . In the first step, PR propose to test using the corresponding (rescaled) quasi-likelihood ratio statistic

where with and where666Note that other estimators of are available (see Section 3 for the “definition” of ): For example, evaluated at or ; similarly, one could evaluate at . Note that Andrews (2001) also considers (rescaled) quasi-likelihood ratio statistics of the form where . We note that does not depend on .

Here, with . The asymptotic null distribution of can be derived using the results in Andrews (2001) (see e.g., Theorem 2.1 in PR) and, although not available in closed form, can easily be simulated from. If is not rejected, then is not rejected. If is rejected, then PR conclude that . Given that , the nuisance parameter is identified and the only remaining “problem” is that may still be at the boundary (). In the second step, PR then suggest to test (3), under the maintained assumption that , using the corresponding (rescaled) quasi-likelihood ratio statistic

where with and where .777Alternatively, we could evaluate at or use (see footnote 6) evaluated at or . In this context, PR make an “additional assumption” on the dependence between and that implies that a certain entry of the inverse of the information matrix equals zero when . This, in turn, implies that the asymptotic null distribution of simplifies to , where . Formally, the two-step procedure (TS) is defined as follows: Reject if

where and denote the quantiles of and the asymptotic distribution given in (14) with and unknown quantities replaced by consistent estimators (see e.g., Appendix B), respectively.888PR do not formally define their two-step procedure in that they do not define the nominal levels that ought to be used in the two steps, say and . Here, we take . Of course, given the results in this paper, it is in principle possible to choose and in order to ensure that AsySz. We refrain from doing so, however, because, given the results in this paper, the motivation for using a two-step procedure is rendered obsolete; see e.g., the new test. While it is possible to derive the asymptotic null distribution of without this “additional assumption”, PR refrain from doing so.999If , or rather for some , then it is straightforward to test (3) using the approach in Ketz (2018), without any assumptions on the dependence between and .

PR also mention that if it is a priori known that then one may directly test (3) using and their suggested critical value, . We refer to this test as the “second testing procedure (of PR)”. Formally, the second testing procedure (S) is defined as follows: If , reject if

There are several potential issues with the above testing procedures. First, the intuition underlying the two-step procedure is based on the assumption that the first-step test never makes a type I error. This assumption, however, cannot hold and a type I error in the first step may very well propagate to the type I error of the overall (two-step) procedure.101010The only way for the first-step test to never make a type I error is to take the nominal level of the corresponding test equal to zero. This, however, would lead the first-step test (as well as the two-step procedure) to have zero power. Relatedly, may be close to zero relative to the sample size; see Section 3 for details. In that case, the probability of rejecting exceeds the first-step nominal level and is only weakly identified such that the asymptotic distribution result for that takes to be (strongly) identified may only provide a very poor approximation to its actual finite-sample distribution. The latter may also be an issue for the second testing procedure. In both cases, one may be worried that the testing procedure does not control asymptotic size. As mentioned above, asymptotic size depends on . For sake of brevity, the definition of is given in Appendix A.

3 Asymptotic distribution results

As shown in the recent literature (see e.g., Andrews and Guggenberger, 2010, AC), asymptotic size is intrinsically linked to the asymptotic distribution of the test statistic under (drifting) sequences of true parameters. Let denote the true parameter for . In the context at hand, the following (sets of) sequences are key:

In what follows, we use the terminology “under ” to mean “when the true parameters are for any , “under ” to mean “when the true parameters are for any with and any ”, and “under ” to mean “when the true parameters are for any , any , any with if or and , and any if or if ”. We note that under sequences of true parameters for which with , identification of is weak, while under sequences of true parameters for which but , identification of is semi-strong.

All claims in this section, including the following, are verified in Appendix A. Under , we have and when , while when .

3.1 Results for including asymptotic distribution for

First, we derive results for close to zero, i.e., . To that end, let , where is the concentrated extremum estimator of for given , i.e.,

and where is the minimizer of the concentrated objective function , i.e.,

With a slight abuse of notation, we let whenever , which occurs when for all . Under , admits the following quadratic expansion in around for given :

| (5) |

where the remainder satisfies

for all and where

Here, denotes the left/right partial derivatives of with respect to , where

and where

In particular,

where

and where

is defined below. Next, define the empirical process by

Under , , where denotes weak convergence and where is a mean zero Gaussian process with bounded continuous sample paths and covariance Kernel given by

| (9) |

for , where .111111The last equality follows by the definition of . Furthermore, we have that

for . Let

Then, under , we have

| (10) |

where

and where

Next, let

such that the quadratic expansion in (5) can be written as

Note that the first two terms do not depend on . As a result, following Andrews (1999, 2001), it can then be shown that the (scaled and demeaned) minimizer of with respect to for given asymptotically behaves like the minimizer of the “asymptotic version” of over an appropriately defined parameter space for .

3.1.1 Asymptotic distribution for

In particular, under with , we have

| (11) |

where

Here,

and

Next, let

and, with a slight abuse of notation, let whenever . Then, we have the following first main result of this paper. Namely, under with , we have

| (12) |

and121212Note that .

| (13) |

The corresponding asymptotic distribution results for and are obtained similarly, by replacing with and , respectively.

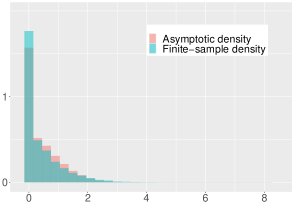

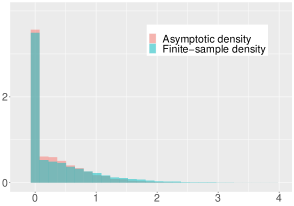

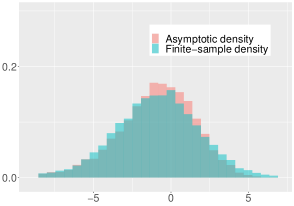

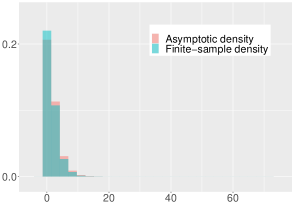

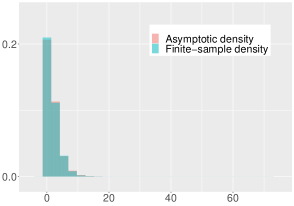

Figure 1 shows the asymptotic and finite-sample () densities of for several values of and ; see Section 4 for details on the data generating process (dgp) and Appendix B for details on how the asymptotic distribution is simulated.131313Figure 4 in Appendix C plots the corresponding distributions for the elements of . We observe that the asymptotic distribution provides a good approximation to the finite-sample distribution. Furthermore, we observe that identification strength strongly impacts the distribution of , with large deviations from normality. When , the distribution of is (almost) completely flat with point masses at the boundaries of the optimization parameter space as well as at 1; recall that whenever . And, as increases, the distribution of starts to resemble the normal distribution (centered at the true value, , and truncated to the support ). This observation is in line with the asymptotic distribution results for ; see Section 3.2.

The asymptotic distribution result in (13) allows us to derive the asymptotic distributions of and under with . Let denote the selection matrix that (among ) selects the entries pertaining to and let . Then, the asymptotic distribution of under with is given by

| (14) |

We note that for we recover the asymptotic distribution of under , see also Theorem 2.1 in PR. The asymptotic distribution of under with is given by141414If and are independent, in which case PR’s “additional assumption” is also satisfied, then is diagonal and the asymptotic distributions of and simplify. Letting and as well as and , we have, for , with . Furthermore, we have . Letting , the asymptotic distribution of , for example, is then given by

| (15) |

where ,

and

The results in (14) and (15) provide us with the asymptotic distributions of and , respectively, for true values of that are close to the boundary relative to the sample size, , which are permitted under . Together, these results allow us to determine the asymptotic null rejection frequencies of the testing procedures proposed by PR under empirically relevant values of . These asymptotic null rejection frequencies play a crucial role in determining whether the testing procedures control asymptotic size; see Section 4.

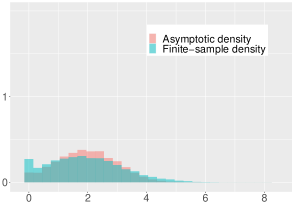

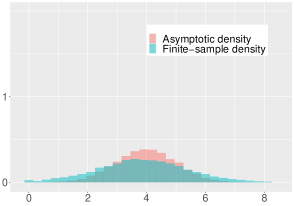

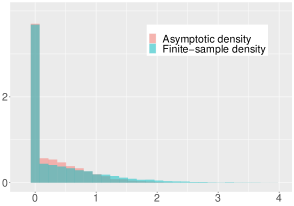

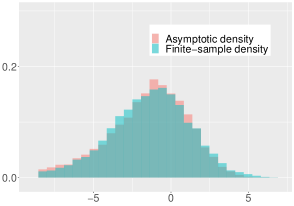

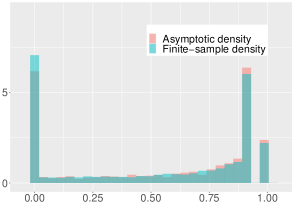

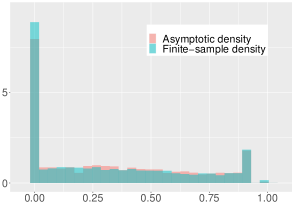

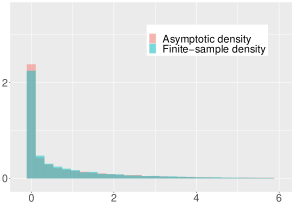

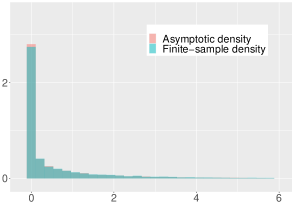

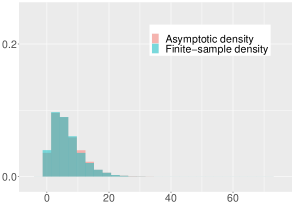

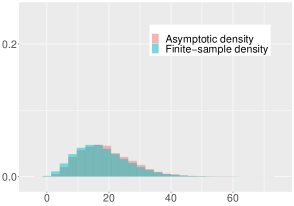

Figure 2 shows the asymptotic and the finite-sample () densities of and for the same dgp that underlies Figure 1. While the asymptotic distribution of provides a very good approximation to its finite-sample distribution, the asymptotic distribution of seems to be first-order stochastically dominated by its finite-sample distribution. However, looking at Figure 3, which reproduces the top row of Figure 2 with 10,000, this seems to be a “small sample” phenomenon.

3.1.2 Results for (and )

Under with , we have that

| (16) |

uniformly over , where

Furthermore, we have that is uniquely minimized at with . It can then be shown that under and under with , where the latter result ensures that (17) holds; see the discussion below Assumption D1 in AC.

3.2 Asymptotic distribution for

Under , we have

| (17) |

where the remainder satisfies

for all , where . Here, and denote the vector of first-order left/right partial derivatives and the matrix of second-order left/right partial derivaties of with respect to , respectively. Define

and

Then (17) can be rewritten as

where

Note that

where

Then, under , we have , where

and , where , such that

| (18) |

Let

Then, under , we have

| (19) |

where and where

Furthermore, under , we have

| (20) |

Let be the selection matrix that selects (among ) the entries pertaining to and and define . Also, let

where

and define . Then, the asymptotic distribution of , under , is given by

| (21) |

In the following section, we use the foregoing asymptotic distribution results to analyze the asymptotic size of the two testing procedures proposed by PR.

4 Asymptotic size and a new test

First, we provide a characterization result for asymptotic size that holds for any test for testing (3). To that end, let

and

Furthermore, let denote the asymptotic rejection probability of the test (that uses ) under with and , where . Similarly, let denote the asymptotic rejection probability of the test under with , , , and , where . Lastly, let be such that for any with , , , and and for some with , , , and , where denotes the finite-sample rejection probability of the test under . We can now state our characterization result for AsySzT.

The proof follows along the lines of the proof of Lemma 2.1 in AC and is given in Appendix A, along with the verification of all claims made in this section.

Next, we consider the two testing procedures proposed by PR. We have

where denotes the quantile of , and

We note that and depend on through , , and .

Since and under with , , , and , we have that

where with . Now, let

and . Furthermore, let denote the quantile of and note that . It can be shown that is strictly monotonically increasing (decreasing) in if (), while if ; this result is in line with and extends the result in PR. It then follows, from Theorem 2.1 in Kopylev and Sinha (2011), that

| (22) |

where denotes the cumulative distribution function of a random variable with degree of freedom . Noting that is strictly increasing in , we have that is bounded from above by for ; this number is obtained by evaluating (22) at .

In what follows, we determine lower bounds on and by numerically evaluating and at certain choices of . Similarly, we determine a lower bound on (22) by numerically evaluating at certain choices of such that (and by plugging the resulting value into ). Combining the above lower bounds then provides us with lower bounds on AsySzTS and AsySzS.

The numerical evaluation is based on the following dgp, which is inspired by PR (see their Appendix D). is such that follows an AR(1), i.e.,

| (23) |

where

We note that, given the above , the “additional assumption” of PR is satisfied if and only if . In what follows, we take and obtain results for ; details on the numerical evaluation can be found in Appendix B. We find that where is given by , , , , and . Furthermore, we find that where is as before, except that (and ). Lastly, we find that where is given by , , , , , and so that .151515This lower bound is increasing in , e.g., we have where is as before except that and so that . We refrain from reporting results for larger due to the decreasing accuracy in the numerical evaluation (as approaches 1). Noting that , we obtain the following Corollary to Proposition 1.

Corollary 1.

Given as defined in Appendix A with , AsySz and AsySz at .

Remark 1.

We note that the two lower bounds obtained in Corollary 1 also apply if is restricted to satisfy the “additional assumption” in PR and, in case of the second testing procedure, the assumption that . This is due to the point-wise nature of the assumptions and the “suprema” in the definitions of SzT and AsySzT. For example, the “additional assumption” in PR is only imposed at and does not exclude sequences of true parameters that are such that and for all , while .

Figure 2 shows that the (asymptotic) distribution of does not vary a lot with , at least for the particular under consideration. This motivates our suggestion to test (3) using combined with a plug-in least favorable configuration critical value (PI-LF); in what follows, the resulting test is abbreviated as -. In the context at hand, we have to consider two identification scenarios ( and ) that result in two different asymptotic null distributions of . The idea is simple: in each scenario, all unknown quantities/parameters of the asymptotic distribution of that are consistently estimable are replaced by estimators. For the remaining parameters, we determine the least favorable configuration, i.e., we determine under which values of these parameters the quantile of the asymptotic distribution is maximized. The corresponding quantile then serves as critical value for the scenario under consideration. Finally, the maximum of the thus obtained critical values and constitutes our proposed PI-LF. We note that, under with and , and are not consistently estimable, while, under with , , , and , is not consistently estimable. Our final implementation follows the above (“general”) approach with two twists. First, under with and , we restrict the search of the least favorable configuration to values of and that satisfy ; this condition is motivated by the condition (see e.g., Mikosch and Starica, 2000) that is also imposed by . Second, if , then we only consider the critical value obtained from the scenario, because the probability of observing under with , , , and approaches 0. See Appendix B for more details on the construction of critical values. By design, we have the following result.

Corollary 2.

Given as defined in Appendix A, AsySz for .

5 Monte Carlo

In this section, we use simulations to assess (i) how well the finite-sample null rejection frequencies of the different tests, or testing procedures, that we consider are approximated by the foregoing asymptotic theory and (ii) how these tests compare in terms of (finite-sample) power. We generate data from the model given in (1), (2), and (23). We use a burn-in phase of 100 observations and set the starting values for the and series equal to zero. The sample size (after discarding the burn-in observations) is equal to 500. The number of simulations is 1,000. Table 1 shows the finite-sample rejection frequencies (in %) of the likelihood ratio test for testing (), the two-step procedure (), the second testing procedure (), and the test that uses together with PI-LF (-) at the 5% nominal level for different true parameter constellations. Throughout, is set equal to 1, while , , , , and are varied as indicated in the table.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

| 0.2 | 0.2 | 0.2 | 0.64 | 0 | |||||||

| 0.5 | 0.5 | 0.5 | 0.5 | 0 | |||||||

| 0 | 0 | 0 | 0 | 0.99 | |||||||

| 0 | 0.05 | 0.1 | 0.11 | 0.3 | |||||||

| 0 | 0.05 | 0.1 | 0 | 0.05 | 0.1 | 0 | 0.05 | 0.1 | 0 | 0 | |

| 3.1 | 22.9 | 57.5 | 14.0 | 36.0 | 65.2 | 40.6 | 57.5 | 79.1 | 70.5 | 99.0 | |

| 2.0 | 21.9 | 56.6 | 3.4 | 25.8 | 59.7 | 5.6 | 29.9 | 62.9 | 6.2 | 8.2 | |

| 11.0 | 45.6 | 77.9 | 9.0 | 41.1 | 73.3 | 8.3 | 37.2 | 68.9 | 6.9 | 8.2 | |

| - | 5.3 | 34.5 | 67.7 | 4.8 | 30.9 | 61.9 | 4.0 | 26.8 | 57.1 | 3.9 | 0.0 |

Columns (1), (4), (7), (10), and (11) of Table 1 report null rejection frequencies for , , and - (). We see that the asymptotic null rejection probabilities that underlie the lower bounds on asymptotic size obtained in Section 4 provide good approximations to the corresponding finite-sample rejection frequencies. In particular, column (1) shows an 11% rejection frequency of , which is close to the corresponding asymptotic rejection probability of 9.48%. Similarly, columns (10) and (11) show rejection frequencies of 6.2% and 8.2% for , which are close to the corresponding asymptotic rejection probabilities of 6% and 6.65%, respectively; note that and .161616Here, 6.7 appears to be large enough for the asymptotic theory obtained for to provide a good approximation, which is corroborated by a rejection frequency of close to 100%. Furthermore, Table 1 reveals that has null rejection frequencies below the nominal level for “very small” values of (see columns (1) and (4)); this is not surprising given the nature of the two-step procedure and the low rejection frequency of for such values of . For the dgps considered in columns (1)–(9) our numerical evaluations show that is the (unique) least favorable configuration for . As a result, the - offers sizeable power gains over for “very small” values of (see columns (2), (3), (5), and (6)), where the latter, by continuity of the power curve, in some sense “sacrifices” power. Not surprisingly, for large(r) values of the power ranking is reversed (see columns (8) and (9)).

References

- Andrews (1999) Andrews, D. W. K. (1999). Estimation When a Parameter Is on a Boundary. Econometrica 67(6), 1341–1383.

- Andrews (2001) Andrews, D. W. K. (2001). Testing When a Parameter Is on the Boundary of the Maintained Hypothesis. Econometrica 69(3), 683–734.

- Andrews and Cheng (2012) Andrews, D. W. K. and X. Cheng (2012). Estimation and Inference With Weak, Semi-Strong, and Strong Identification. Econometrica 80(5), 2153–2211.

- Andrews and Guggenberger (2010) Andrews, D. W. K. and P. Guggenberger (2010). Asymptotic Size and a Problem With Subsampling and With the m out of n Bootstrap. Econometric Theory 26(2), 426–468.

- Cox (2022) Cox, G. (2022). Weak Identification with Bounds in a Class of Minimum Distance Models. arXiv:2012.11222.

- Hansen (1996) Hansen, B. E. (1996). Inference when a nuisance parameter is not identified under the null hypothesis. Econometrica 64(2), 413–430.

- Ketz (2018) Ketz, P. (2018). Subvector inference when the true parameter vector may be near or at the boundary. Journal of Econometrics 207(2), 285–306.

- Kopylev and Sinha (2011) Kopylev, L. and B. Sinha (2011). On the asymptotic distribution of likelihood ratio test when parameters lie on the boundary. Sankhya B 73, 20–41.

- Leeb and Pötscher (2005) Leeb, H. and B. M. Pötscher (2005). Model selection and inference: Facts and fiction. Econometric Theory 21(1), 21–59.

- Leeb and Pötscher (2008) Leeb, H. and B. M. Pötscher (2008). Can one estimate the unconditional distribution of post-model-selection estimators? Econometric Theory 24(2), 338–376.

- Mikosch and Starica (2000) Mikosch, T. and C. Starica (2000). Limit theory for the sample autocorrelations and extremes of a GARCH (1, 1) process. The Annals of Statistics 28(5), 1427–1451.

- Pedersen and Rahbek (2019) Pedersen, R. S. and A. Rahbek (2019). Testing GARCH-X Type Models. Econometric Theory 35(5), 1012–1047.

Appendix A Definition of , verification of claims in Sections 3 and 4, and proof of Proposition 1

First, we define . [Details to be added.]

The claim in the last paragraph before Section 3.1 follows from Lemma 3.1 in AC by verifying Assumptions A and B3 in AC. [Details to be added.]

Next, we show that equation (5) holds, which amounts to verifying Assumptions C1 and C4 in AC. [Details to be added.]

Next, we verify the weak convergence result for , which amounts to verifying Assumptions C2 and C3 in AC. [Details to be added.] Note that

Then, equation (9) is obtained by noting (i)

where the second to last equality uses for , (ii)

and (iii)

To show that , note that, by definition, we have

where

since is not a function of . Furthermore, we have

Now, given , we have

and the desired result follows.

Next, we derive . The expected value entering , see equation (3.6) in AC, is given by

such that

cf. Assumption C5 in AC. The desired result then follows using similar observations to those used in the derivation of .

Equation (10) follows from Lemma 9.1 in AC, upon verification of Assumptions C2, C3, and C5 in AC. [Details to be added.]

Equation (11) follows from arguments analogous to those underlying Theorem 1(a) in Andrews (2001). [Details to be added.] Similarly, equations (12) and (13) follow from combining the arguments underlying Theorem 3.1 in AC and Theorem 1(b) and (c) in Andrews (2001). [Details to be added.] Furthermore, equations (14) and (15) follow from arguments analogous to those underlying Theorem 2(b) in Andrews (2001). [Details to be added.]

Equation (16) follows from Lemma 3.2(b) in AC. [Details to be added.] To gain intuition for this result, note that, under with , the equivalent of the above function is given by

| (24) |

which is minimized over , since

Then, noting that (since all elements of are nonpositive), we have that the minimum of (24) over is equal to zero.

Next, we show that is uniquely minimized at with . [Details to be added.]

The two claims in the last sentence of Section 3.1.2 follow from Lemmas 3.3 and 3.4 in AC, respectively. [Details to be added.]

Next, we show that equation (17) holds. [Details to be added.]

Equation (18) holds given the definition of . [Details to be added.]

Equations (19) and (20) follow from combining the arguments underlying Theorem 3.2 in AC and Theorem 1(b) and (c) in Andrews (2001). [Details to be added.] Similarly, equation (21) follows from arguments analogous to those underlying Theorem 2(b) in Andrews (2001). [Details to be added.]

Proof of Proposition 1.

[Details to be added.] ∎

Next, we show that and under with . [Details to be added.]

Lastly, we show that is strictly monotonically increasing (decreasing) in if (). [Details to be added.]

Appendix B Computational details

In what follows, we let and denote discretized versions of and , respectively.

B.1 Evaluation of asymptotic distribution for

The asymptotic distributions displayed in Figures 1–4 as well as the asymptotic rejection probabilities and are evaluated using simulation. The underlying dgp is given in (1), (2), and (23). To simulate from , we use the method of Hansen (1996). In particular, we obtain the draw from by computing

where are iid , independent across , and where are generated according to (23) (with and ) using a burn-in phase of 100 observations. Here and in what follows, .

We approximate and by

and

respectively, where are generated similarly to .

Together, this allows us to obtain the draw from . The corresponding draws of the “asymptotic versions” of the relevant estimators and test statistics can then be obtained using the formulae in Section 3.1.1 with in place of for a total of draws.

We use 10,000, 100,000, and with .

B.2 Evaluation of

In order to evaluate , it suffices to evaluate with . As before, the underlying dgp is given in (1), (2), and (23). We approximate with by

where and . Here, is generated according to (1), (2), and (23) (with and ) using a burn-in phase of 100 observations.

We use 100,000.

B.3 Computation of critical values

B.3.1 and critical value for testing using

Under with and , is consistently estimated by (as ). Let denote with unknown quantities replaced by consistent estimators, i.e., by estimators that are consistent under with and . To simulate from , we use the method of Hansen (1996). In particular, we obtain the draw from by computing

where are iid , independent across . Here, we use the fact that . Furthermore, we estimate and by

and

respectively. Then, the draw from , the “estimated counterpart” to , is given by

The draw of , the “estimated counterpart” to , can then be approximated by evaluating over using the corresponding formulae in Section 3.1.1. We note that and thus the draw of do not depend on . Finally, the quantile of the empirical distribution of draws from provides us with an estimate of the quantile of the asymptotic distribution of under with . We denote this quantile by .

The draw of , the “estimated counterpart” to , is approximated in a similar fashion. And we take the quantile of the empirical distribution of draws from as estimator of the quantile of the asymptotic distribution of under with and , which we denote by .

B.3.2

Under with , , and , is consistently estimated by . Here, we do not impose and estimate by

where

Then, we estimate by

Finally, let and define

where are independent random variables with degree of freedom and 2 that are independent of the random variable that is equal to 0, 1, and 2 with probabilities , 1/2, and , respectively. Here, the subscript indicates the quantile of the random variable in parentheses. Note that under with , , , and such that , consistently estimates the quantile of .

B.3.3 Plug-in least favorable configuration critical value

The plug-in least favorable configuration critical value that we propose is given by

where

and where is a finite grid.

In our simulations, we use 10,000, , , and

We chose the grids relatively coarsely to keep the computation cost of the Monte Carlo simulations low. For empirical applications, we recommend the use of finer grids. We also note that there is no need to include values of greater than in .

Appendix C Additional graphs