A Referable NFT Scheme

Abstract

Existing NFTs confront restrictions of one-time incentive and product isolation. Creators cannot obtain benefits once having sold their NFT products due to the lack of relationships across different NFTs, which results in controversial profit sharing. This paper proposes a referable NFT solution to extend the incentive sustainability of NFTs. We construct the referable NFT (rNFT) network to increase exposure and enhance the referring relationship of inclusive items. We introduce the DAG topology to generate directed edges between each pair of NFTs with corresponding weights and labels for advanced usage. We accordingly implement and propose the scheme under Ethereum Improvement Proposal (EIP) standards, indexed in EIP-5521. Further, we provide the mathematical formation to analyze the utility for each rNFT participant. The discussion gives general guidance among multi-dimensional parameters. The solution, as a result, shape the recognition of potential values hidden in isolated NFTs and raise the interest of communities toward the discovery of NFT derivatives. To our knowledge, this is the first study to build a referable NFT network, explicitly showing the virtual connections among NFTs.

Index Terms:

Blockchain, NFT, EIP Standard, DAGI Introduction

Non-fungible tokens (NFTs) [1] is built as EIP-721 [2] to exchange unique digital assets in the Ethereum platform [3]. It digitalizes on-chain assets into tokens, and specifies each token with a unique identifier tokenID within smart contracts. This significantly encourages and extends the on-chain token exchange from fungible to non-fungible ones which, not surprisingly, is now leading a wave of the next generation of a wide variety of applications covering virtual collectables, online tickets, digital arts, etc. Besides, NFT can be seamlessly incorporated with the protocols in decentralized finance (DeFi) [4] and the governance in blockchain communities [5]. To date111Data captured from https://nonfungible.com/reports [Q1-Q3 2022]., a total of of NFT sales has led to the traded volume reaching up to billion USD. The phenomenal trading activities reflect a sharp shift from traditional markets into the new Web3 world [6].

However, the lack of relationships between an NFT and its owner in existing NFT standards could result in controversial profit sharing if the creation of a new NFT refers to previous NFTs. The trades of NFTs are one-time in transferring and isolated across different users. An NFT creator cannot continuously obtain profits for his intellectual property once sold. The permanent reference relationship between NFTs, thus, becomes increasingly important. The reference topology will assist in establishing a sustainable incentive mechanism to economically inspire more and more users to devote their contributions to using, creating, and promoting NFTs. To fill the gap, we propose EIP-5521 that defines a referable NFT token (rNFT) standard. It extends the static NFT into a virtually extensible NFT network. Users under clear ownership inheritance do not have to create work completely independent from others, avoiding reinventing the same wheel. Here, we summarise contributions as follows:

Protocol Design (Sec.II). Our referable NFT scheme establishes the reference of ancestors when minting a new NFT with the reference relationship including both the referring and referred relationships, thus shaping a Direct Acyclic Graph (DAG) to represent the reference information. The scheme can provide reliable, trustworthy, and transparent historical records that every agreement can refer to in terms of profit sharing. Meanwhile, users are allowed to query, trace and analyze their relationship.

Standard Implementation (Sec.II). We implement a very succinct version and propose it to the Ethereum standard Git repository, indexed by EIP-5521. Our simplified proposal is a smart-contract driven standard used as a system-level function on blockchains. It builds and retains the backward reference relationship between old works and new works and is compatible with existing mainstream standards. At the time of writing, rNFT has attracted consistent discussions and attention on forums [7] and by several in-production projects (e.g., Briq [8]).

Incentive Analysis (Sec.III). We provide a clear and exact mathematical expression of the utility function of an rNFT user. rNFT helps to integrate multiple upper-layer incentive models and also involves multi-dimensional parameters. We accordingly analyze the payoff function under different parameters. Chasing an optimal strategy for players is possible but without certainty.

Further Discussions (Sec.IV). We provide an in-depth discussion of our proposed scheme in terms of its opportunities and challenges. rNFT can promote a wide range of new NFT derivatives that requires historical relations but also confronts many pending aspects for discovery such as multi-contract or CC0 license development.

An Intuitive Instance. The constructed relationship topology between each NFT forms a DAG. By adding the referring indicator, users can mint new NFTs (e.g. C, D, E) by referring to existing NFTs (e.g. A, B), while referred enables the referred NFTs (A, B) to be aware that who has quoted it (e.g. ; ; ). createdTimestamp is an indicator, based on block timestamp, used to show the creation time of NFTs (A, B, C, D, E).

Extending NFT Derivatives. Similar to traditional financial derivatives that are based on stocks, commodities, or other underlying assets, NFT derivatives mainly refer to financial instruments that center around the value of an underlying NFT asset. The key feature of these derivatives is to allow users to invest in NFTs without actually holding the physical NFT asset in the forms such as options, futures, swaps, and other financial instruments that are used for the trading or hedging of the underlying NFT asset’s price. However, this requires a relatively comprehensive history of records and credits. rNFT provides a foundation for atop derivative protocols, as siting to offer more complex investment strategies and risk management tools by establishing a reliable relationship among multiple linkable NFTs. The extension of NFT derivatives is an ongoing process and our solution gives an example for better connections.

Integration. Our scheme can be further integrated with mainstream techniques. We list two examples as the enlightenment. Firstly, the new rNFT can be combined with Graph Neural Network (GNN) [9] to achieve efficient queries and predictions of NFT. This is particularly useful for conducting automated labeling by NFT platforms such as OpenSea [10], or for NFT viewers to find more NFTs of the same kind. Secondly, AI detection [11] can be imported into the system for plagiarism detection, path recommendation, and strategy optimization. Due to the blur edges between the original artwork and copy-work, figure classification and identification in artificial intelligence is a fundamental tool for the detection of a rapidly growing NFT markets.

Backward Compatibility. As in Sec.II, an rNFT implements the existing ERC-721 interfaces [2] to enable the backwards compatibility. This allows the proposed rNFT to be seamlessly implemented on existing blockchain platforms such as Ethereum [3] where those existing ERC-721-compatible NFTs, such as the composable NFT: EIP-998 [12], can be referred by any subsequent rNFTs.

Related Standards (Tab.I). A series of NFT-related standards222Captured from Ethereum ERCs https://eips.ethereum.org/erc [Dec 2022]. haves been intensively proposed. We highlight the ones entering the final and last call stages due to their deterministic probability of being accepted by communities. (EIP-)3525 proposes the concept of semi-fungible token by introducing a triple scalar . ID acts the way as the 721 standards while additionally adding a quantitative feature value. 1155 proposes a multi-token standard that can combine either fungible tokens, non-fungible tokens, or other configurations (e.g. semi-fungible tokens). 2981 focuses on the royalty payment transferred between a buyer and a seller voluntarily. 4907 and 5006 propose rental NFTs by extending original settings with an additional role of user and a timing feature of expire. A user can only use an NFT within the expire duration, rather than transferring it. 2309 implements a consecutive transfer extension that enables batch creation, transfer, and burn methods by contract creators. The users can quickly and cheaply mint at most tokens within one transaction. 4400 extends 721’s customer role of being able to, for instance, act as an operator or contributor. 5007 introduces the functions of startTime and endTime set a valid duration that automatically enables and disables on-chain NFTs. 4906 extends the scope of Metadata that allows tracking changes by third-party platforms. 5192 proposes the idea of soulbound that binds an NFT to a single account, achieving special applications such as non-transferable and socially-priced tokens. Besides, we also provide more related standards with indirect impacts on NFTs in Tab.I).

| Standard | Platform | Feature | Application |

| EIP721 | Ethereum | Non-Fungible Token | Artwork/IP |

| EIP777 | Ethereum | Token Approval | |

| EIP1155 | Ethereum | Adding an attribute for groups | Game |

| EIP3525 | Ethereum | Additional attribute for semi-fungible | Finical Market |

| EIP2981 | Ethereum | Retrieving the royalty payment info | Royalty Payments |

| EIP4907 | Ethereum | Adding a new role and timer | Rental Market |

| EIP5006 | Ethereum | Adding the new role of user | Rental Market |

| EIP2309 | Ethereum | Consecutive token identifiers | Consecutive event |

| EIP4400 | Ethereum | Extend the consumer’s functionalities | Authorization |

| EIP5007 | Ethereum | On-chain time management | Lend Market |

| EIP4906 | Ethereum | Enable token metadata’s update | Upgrade |

| EIP5192 | Ethereum | Bound to a single account | Soulbound Items |

| This work | Ethereum | Referable connections | NFT Graph |

| EIP20 | Ethereum | Token API / Fungible Token | Vote/ICO |

| EIP223 | Ethereum | Token Recovery | |

| EIP998 | Ethereum | Composable Non-Fungible Token | Game/Ownership |

| EIP1238 | Ethereum | Non-Transferrable Non-Fungible Token | Badge |

| EIP1594 | Ethereum | Security Token Standard | Financial Securities |

| EIP1400 | Ethereum | Security Token Standard | Securities |

| EIP1404 | Ethereum | Simple Restricted Token Standard | Securities |

| EIP1410 | Ethereum | Partially Fungible Token Standard | |

| EIP1462 | Ethereum | Base Security Token | Securities |

| BEP20 | Binance | Fungible Token | Vote/Wrap Token |

| BEP721 | Binance | Non-Fungible Token | IP Products |

| ARC721 | Avalanche | Fungible Token | Wrap Other Tokens |

II Protocol Design and Implementation

In this section, we present the rNFT protocol, construction, and implementation, respectively.

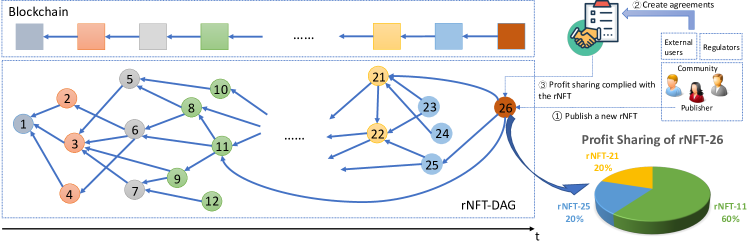

Notations. The notations used in this paper are listed as follows. is the timestamp of the block header. means a transaction that packs a particular rNFT and is a block at the height of released at time . represents the set of rNFTs, while is an rNFT released by user- at time with a set of that contains both the referring and referred relationship, respectively, i.e., and . Specifically, represents a collection of referring relationships made by an rNFT that connects several previous rNFTs such as where , denoted by the blue arrows in the rNFT-DAG, and follows the same notation with , and is accordingly updated when this gets referred by any future rNFTs. Note that the rNFT with generally indicates an (claimed to be) original item. is an agreement involving user , , , etc. The set of rNFTs constitutes a growing rNFT-DAG as depicted at the bottom of Fig. 1. Here, merely represents a logical relationship graph (or topology) rather than an actual DAG network. Matched color between the nodes in rNFT-DAG and the blocks on-chain indicates each is expected to be packed in the corresponding block with the same color as time goes by.

Protocol Design. The rNFT protocol aligns with the narrative of any same kind of smart contract (SC-)supported protocols. We extract the core processes and highlight our contributions.

Parameter Setup: The algorithm is used to create initial identities for users. The algorithm takes as input the security parameter , and outputs a key pair and corresponding addresses .

Transaction Creation: This algorithm takes as input the user’s private key , the transaction metadata , the payload , and outputs the created transaction that contains the signature from the creator.

Contract Execution: The algorithm takes as input the created transaction , and the state , and that contains the operating logic, and outputs the transited state .

The state includes the newly minted rNFT with the current state of referred relationships . Here, a pre-released rNFT is expected to be included in a transaction that will be subsequently packed by a valid block on a growing chain with finalization at the height of at time .

State Consensus: This algorithm takes as input the transaction , the smart contract and the state to be transited, and outputs the confirmed state , and the confirmed transaction .

We can observe that as soon as one from the community as the publisher at time publishes a new rNFT with a bunch of referring relationships collected in , and the corresponding emitted transaction is finalized by a valid block on the blockchain, any agreement will be able to enjoy a reliable, trustworthy, and transparent historical record about the items, referring relationships, and profit sharing to guarantee the fair trading later on.

Implementation. We implement the rNFT scheme by following the ERC standards, and propose the entire solution as indexed in EIP-5521, which is an extension of the ERC-721 protocol. Our solution adds two types of referable indicators, referring and referred, and a time indicator createdTimestamp in a new structure . The referring indicator (implemented by and ) enables a user, as the child, to inherit the ancestor NFTs. The referred indicator (by and ) makes a parent NFT builder be able to check who has referenced him. Also, we provide two optional advance indicators labels and profitSharing for additional functions like incentive distribution and attributes establishment. The time indicator is a block-level timestamp that assists in solving disputes. Specifically, we set five indicators as the parameter to implement the proposed scheme, as shown in Algorithm.1

-

-

referring: an out-degree indicator, showing the users this NFT refers to.

-

-

referred: an in-degree indicator, showing the users who referred this NFT.

-

-

createdTimestamp: a time-based indicator, comparing the timestamp of mint.

-

-

labels (Advanced): a list recording the attributes or categories of the rNFT.

-

-

profitSharing (Advanced): a list recording the profit sharing of referring, thus the size of profitSharing equaling to that of referring.

Here, we can observe that customizable attributes are also added following the referable indicators, for instance, a string array of labels can store a series of attributes given to a particular NFT, such as artwork, song, movie, animation, subtitle, screenshot, etc. Another optional but useful one could be a list recording the profit sharing among the owners whose NFTs have referred to this NFT. By complying with the record of profit sharing, fair and transparent on-chain or off-chain agreements can be achieved. Then, we also have six corresponding methods for the implementation.

-

-

: mint a new rNFT.

-

-

: set the referring list of an rNFT and update the referred list of each one in the referring list.

-

-

: set the referring list of an rNFT.

-

-

: set the referred list of the given rNFTs.

-

-

: get the referring list of an rNFT.

-

-

: get the referred list of an rNFT.

Based on the above functions, EIP-5521 makes involved rNFTs form a DAG that can explicitly show their relationship and entanglement. The protocol increases the incentive of existing NFTs where an NFT owner can obtain more revenues from the followers. In the next part, we give our theoretical analysis of incentive optimization within the rNFT ecosystem.

III Incentive Analysis

In this section, we discuss the incentive analysis. In total, we majorly consider three orthogonal principles. From the horizontal view (count by in/out degree), an rNFT that have been referred more times should gain much more incentives. From the vertical view (count by depth), an rNFT with a deeper reference index should accumulate more revenues. For the profit distribution, we additionally introduce the weight to ensure the distribution will be ended within finite rounds. We also set to measure the descending rate according to its depth for the subsequent users. Specifically, we set the following parameters:

-

-

Referring bandwidth (): measure the number of rNFTs that refer to this NFT at the same block height.

-

-

Referring depth (): measure the number of attached children in every single path of the branch. Here, is calculated by .

-

-

Threshold (): set the initial pay rate (anchoring its initial value ) when minting a new rNFT.

-

-

Weight (): set the weight for each referring edge (w.r.t. referring list ).

-

-

Rate (): adjust the descending rate of the income as the depth increases.

We consider the payoff function of each single existing rNFT user.

Definition 1

The payoff function of a user releasing an rNFT at the block height is made by

where represents accumulated income revenues during the following rounds while is the cost of minting this rNFT.

For the outcome, indicates the costs paid to the network. We can see that is minted at the round (according to its block height), with the minting fees of . Here, he can optionally pay a part of (measured by ) the entire charge at . But accordingly, the rest of the payment needs to be completed within the next rounds, where is calculated by and is a constant. The delayed payment will accompany by an interest rate . Instead of relying on a simple average assignment, we relate with individual weights of each rNFT. Specifically, we define as the weight of self-references with being the weights of all other cross-references .

We first give details for calculating the initial price . The initial paid is one-off. It contains a ratio list, where previous rNFTs are referred with being the ratio of profit sharing for -th rNFT in the referring list . Note that having to allocate the implies that a constant expense is mandatory for releasing each rNFT regardless of the size of the referring list . We obtain the calculation of as

Accordingly, the outcome function with compound interest is stated as

For the income, can obtain the accumulated rewards from all participants’ payments. The income is to collect same-height income (the horizontal dimension) iteratively for all valid rounds (the vertical dimension), where each round of income relates to actual participants . Also, we use the descending rate to adjust the valid rounds for profit distribution, which is set to be an inversely proportional relation. Based on the targeted rNFT’s position on-chain, we calculate its accumulated incomes from each following round. At the round , the relevant new set of minted rNFT that refer to is and the descending rate for each round is given by .

We note that the settings of and can be effectively used to adjust the trade-off between the income and outcome , hence leading to the payoff function . The higher weight of the self-reference, the lower the interest rate can be offered to encourage creative and original works. The higher weight of the cross-reference, the lower descending rate can be offered to works with various cross-references which are commonly acknowledged as mature products.

Then, we calculate round revenues. The revenue of the round is calculated as where is a constant. Similarly, the income at the round is . We thereby have the income function as

where is the depth for measuring valid rounds of profit distribution, calculated by . Based on the above equations, we obtain the payoff function as

Intuitively, we can conclude that the payoff revenues of each minted rNFT are positively proportional to the accumulative participants (namely, ) or valid references (), whereas negatively proportional to the round interest if not set to be . The more a user paid for the initial price (say ), the less round he needs to pay to the previous rNFTs. Similarly, the higher descending rate (cf. ) is set, the fewer rounds () can last for creating benefits. However, the overall payoff function relates to all parameters including , , , and is complicated. It is unpredictable to decide the dominant parameter since a surge of participants () may crowd into a certain round, causing significant impacts overwhelming to any other parameters. The surge of participants might be closely dependent on external stimulates which are unknown to the system view.

We further investigate the concavity of the payoff function. Let , , . Note that is an integer and always greater than 0, and are both between 0 and 1, hence and non-convex. This is an NP-hard problem that cannot be solved by typical convex optimization approaches. We omit the concrete exploration in this brief analysis but provide some possible solutions such as the Monte Carlo method or deep learning algorithms.

IV Applications and Discussions

IV-A Applications and Opportunities

Fair Incentive Design. The proposed rNFT scheme is particularly useful for scenarios where cross-references among NFTs are essential during the process of on-chain and off-chain profit sharing. A fair distribution mechanism must be established on top of existing observable relationships including inheritance, reference, and extension. For example, an artist may develop his NFT work based on a previous NFT: a DJ may remix his record by referring to two pop songs, or a movie may include existing pieces of clips, etc. Explicit reference relationships for existing NFTs and enabling efficient queries on cross-references make much sense to the markets for renting, exchanging and trading.

Broader Functionalities for NFT Markets. NFT provides basic functionalities covering mint and exchange. This merely supports limited scenarios that are based on in-time and one-time trades. rNFT extends the sustainability and usability of tokens that enable consecutive transactions and long-term retrieving. positively fostering interaction between NFT creators, collectors, and enthusiasts.

Promotion for More Integration. Aligning with the rapid NFT development, our solution can follow and promote a series of emerging trends and capabilities.

Mature technologies. As discussed in Sec.I, rNFT can be integrated with GNN for establishing NFT classification and predictions and with AI for plagiarism detection. Not surprisingly, rNFT can also be used to combine with traditional blockchain technologies such as off-chain (or layer-two [13]) executions for portable usage, or cross-chain bridges for trading between different networks.

Verifiable ownership&provenance. rNFT can be used to securely store and share information about the origin and history of an asset, as well as providing strong connections for proof of ownership.

DeFi/GameFi integration. rNFT can be designed for more NFT and DeFi derivatives due to its strong attachments to previous history. The users/players will get trusted much more easily. Using rNFT to represent in-game items or to provide a new level of ownership and scarcity in gaming experiences is a promising direction.

Physical goods and services. rNFT can help to Link NFTs to tangible goods and experiences, such as collectible merchandise, event tickets, and access to exclusive services, which is good to build a full view of user’s profile.

IV-B Challenges and Potential Solutions

Towards Cross-contract Invoke. Our protocol is implemented based on a singly invoked contract, which means that all minted NFTs should follow the same contract instructions. Each project can merely establish a topological graph within its project, rather than arbitrarily other contracts that require cross-invoke. As in an initial stage, our preliminary implementation gives a demo for expanding the potential usage scope and facilitating the development of the following protocols/standards. To realize a cross-contract target, we plan to implement a series of additional functions that are backward compatible with several existing standards (e.g., EIP-998). A good start is that our single-invoke implementation can be seamlessly extended to the next cross-invoke stage.

Ways of Feeding Price. The price oracle provides in-time prices feed to SC-enabled applications (e.g. DeFi protocols [4]). While many oracle designs have been implemented to provide data for fungible token prices, few attempts have been made to construct a price oracle for NFTs. NFTs are generally less frequently traded, therefore creating difficulties for third parties to observe and retrieve price data. Our proposed scheme can normally operate without incentive indicators, independent of the price oracle. But with advanced incentive designs, price oracle is critical for users who make trades and obtain rewards. The price will impact both the initial price and round interest , as well as will affect the behavioral trend from users. Embedding a secure and efficient oracle for feeding prices is of great importance.

Integrated Verification. The rNFT-DAG in our protocol can merely be used for reference only when rights need to be determined and certified without any compulsory measures in force in its current form. There could be risks that malicious rNFT publishers do not obey the protocol by not claiming the correct relationships with existing rNFT items, although the community could find out the mistakes in long-term observation. A potential solution is to have an automated verification scheme integrated into our protocol where the peers have the ability to conduct mutual verification, as well as the incentive scheme associated with the malicious reference can be accordingly established.

Deterministic Records with Low Latency. The createdTimestamp of each rNFT only covers the block-level timestamp (based on block headers), which does not support fine-grained comparisons such as transaction-level. The rNFT-DAG highly relies on the EIP-5521-driven smart contracts that run on blockchain (Ethereum in our context). The block interval of a dozen seconds if the Proof-of-Work (PoW) is used by default needs to be reduced to achieve lower latency. This is significantly important when ones aim at preemptive registration of rNFTs. On the other hand, PoW is a probabilistic consensus algorithm that commonly causes a rollback of the state of smart contracts, which lengthens the waiting period until the reference relationship takes effect. A workaround is to use deterministic consensus algorithms such as the Proof-of-Authority (PoA) or any other Ethereum-compatible BFT algorithms (e.g., Quorum [14]).

Complementary to CC0 License. CC0 refers to “Creative Commons 0” – a license that for the first time allows NFT holders to waive copyrights and other IP protections and significantly encourages the creation and extension of NFT derivatives associated with the original works [15]. This has been widely committed and adopted by many Web3 projects due to its attempt of eliminating the possible legal consequences associated with reference relationships between different NFT items and bring the items to a permissionless public domain – the spirit of true Web3. However, it becomes difficult for one, especially those who are large-scale, well-established, or have a well-deserved reputation, to build commercial brands on top of a CC0-based NFT once opting for CC0 License as he/she has no right to exclude others from using the same origin (the CC0-based item). Our proposed rNFT protocol fills the gap for these NFT holders and can be considered complementary to the existing CC0 License due to its explicit indication of reference relationships.

V Conclusion

In this paper, we propose a referable NFT (rNFT) scheme to improve the exposure and enhance the reference relationship of inclusive NFTs. We implement the scheme and propose the corresponding EIP-5521 standard to the community. We further establish the mathematical utility function to express the rNFT releasing and referring process. As far as we know, this is the first study that establishes a referable NFT network. By traversing it, a truly decentralized reference network comes to life to protect intellectual property and copyright and incentivizes creativity towards a fairer environment.

References

- [1] Q. Wang, R. Li et al., “Non-fungible token (NFT): Overview, evaluation, opportunities and challenges,” arXiv preprint arXiv:2105.07447, 2021.

- [2] E. William, S. Dieter, E. Jacob, and S. Nastassia, “Eip-721: Non-fungible token standard,” Jan. 2018. [Online]. Available: https://eips.ethereum.org/EIPS/eip-721

- [3] G. Wood et al., “Ethereum: A secure decentralised generalised transaction ledger,” Ethereum project yellow paper, vol. 151, no. 2014, pp. 1–32, 2014.

- [4] S. M. Werner, D. Perez, L. Gudgeon, A. Klages-Mundt, D. Harz, and W. J. Knottenbelt, “SoK: Decentralized finance (DeFi),” ACM Advances in Financial Technologies (AFT), 2022.

- [5] A. Kiayias and P. Lazos, “SoK: Blockchain governance,” ACM Advances in Financial Technologies (AFT), 2022.

- [6] Q. Wang, R. Li et al., “Exploring Web3 from the view of blockchain,” arXiv preprint arXiv:2206.08821, 2022.

- [7] “Forum discussion on referable NFT,” Available: https://ethereum-magicians.org/t/eip-x-erc-721-referable-nft/10310, 2022.

- [8] “Briq NFT,” Available: https://briq.construction/, 2022.

- [9] F. Scarselli, M. Gori, A. C. Tsoi, M. Hagenbuchner, and G. Monfardini, “The graph neural network model,” IEEE Transactions on Neural Networks (TNN), vol. 20, no. 1, pp. 61–80, 2008.

- [10] “Opensea,” Available: https://opensea.io/, 2022.

- [11] G. Kumar, K. Kumar, and M. Sachdeva, “The use of artificial intelligence based techniques for intrusion detection: a review,” Artificial Intelligence Review, vol. 34, pp. 369–387, 2010.

- [12] J. S. Matt Lockyer, Nick Mudge, “EIP-998: ERC-998 composable non-fungible token standard,” https://eips.ethereum.org/EIPS/eip-998, 2022.

- [13] L. Gudgeon, P. Moreno-Sanchez, S. Roos, P. McCorry, and A. Gervais, “SoK: Layer-two blockchain protocols,” in Financial Cryptography and Data Security (FC. Springer, 2020, pp. 201–226.

- [14] Consensys, “Quorum blockchain service,” https://consensys.net/docs/qbs//en/latest/, accessed 19-October-2022.

- [15] Flashrekt and S. D. Kominers, “Why NFT creators are going CC0,” https://a16zcrypto.com/cc0-nft-creative-commons-zero-license-rights, accessed 19-October-2022.