\pkglogitr: Fast Estimation of Multinomial and Mixed Logit Models with Preference Space and Willingness to Pay Space Utility Parameterizations

John Paul Helveston

\Plaintitlelogitr: Fast Estimation of Multinomial and Mixed Logit

Models with Preference Space and Willingness to Pay Space Utility

Parameterizations

\Shorttitle\pkglogitr: Preference and WTP Space Logit Models in

\proglangR

\Abstract

This paper introduces the \pkglogitr \proglangR package for fast

maximum likelihood estimation of multinomial logit and mixed logit

models with unobserved heterogeneity across individuals, which is

modeled by allowing parameters to vary randomly over individuals

according to a chosen distribution. The package is faster than other

similar packages such as \pkgmlogit, \pkggmnl, \pkgmixl, and

\pkgapollo, and it supports utility models specified with “preference

space” or “willingness to pay (WTP) space” parameterizations,

allowing for the direct estimation of marginal WTP. The typical

procedure of computing WTP post-estimation using a preference space

model can lead to unreasonable distributions of WTP across the

population in mixed logit models. The paper provides a discussion of

some of the implications of each utility parameterization for WTP

estimates. It also highlights some of the design features that enable

\pkglogitr’s performant estimation speed and includes a benchmarking

exercise with similar packages. Finally, the paper highlights additional

features that are designed specifically for WTP space models, including

a consistent user interface for specifying models in either space and a

parallelized multi-start optimization loop, which is particularly useful

for searching the solution space for different local minima when

estimating models with non-convex log-likelihood functions.

\Keywordslogit, utility, preference, willingness to pay, discrete

choice models, \proglangR, maximum likelihood estimation

\Plainkeywordslogit, utility, preference, willingness to pay, discrete

choice models, R, maximum likelihood estimation

\Address

John Paul Helveston

George Washington University

Department of Engineering Management and Systems Engineering,

School of Engineering and Applied Sciences,

800 22nd St NW

Washington, DC 20052

E-mail:

URL: https://www.jhelvy.com

1 Introduction

Choice modeling is a well-established statistical method for assessing consumer preferences across a wide variety of fields. One of the most common approaches for modeling choice is the maximum likelihood estimation of multinomial logit models (McFadden1974), which is rooted in the theory of random utility models (Louviere2000; Train2009). The central assumption of these models is that individual consumers make choices that maximize an underlying random utility model, which can be parameterized as a function of a product’s observed attributes and a random variable representing the portion of utility unobservable to the modeler. These models produce estimates of the marginal utility for changes in each attribute relative to one another.

In many applications, modelers are interested in estimating marginal “willingness to pay” (WTP) for changes in product attributes. The typical procedure to obtain these estimates is to divide the estimated parameters of a “preference space” utility model by the negative of the price parameter. Despite this common practice, it can yield unreasonable distributions of WTP across the population in heterogeneous random parameter (or “mixed logit”) models (Train2005; Sonnier2007; Helveston2018). For example, if the parameters for the price attribute and another non-price attribute are both assumed to be normally distributed across the population, then the resulting WTP estimate follows a Cauchy distribution, implying that WTP has an infinite variance across the population.

An alternative approach is to re-parameterize the utility model into the “WTP space” prior to estimation. Estimating a WTP space model allows the modeler to directly specify assumptions of how WTP is distributed, which has been found to yield more reasonable estimates of WTP (Train2005; Sonnier2007; Daly2012). WTP space models have also been found to be more consistent with respondent’s true underlying preferences (Crastesa2014). Finally, since WTP estimates are independent of error scaling, they can be conveniently compared across different models estimated on different data.

Several statistical packages support the estimation of multinomial and mixed logit models with WTP space utility parameterizations. One of the most common approaches involves an adaptation of the generalized multinomial logit (GMNL) model (Fiebig2010) to fit WTP space models via an implementation of the scaled multinomial logit (SMNL) model, though this requires that the price parameter estimate and standard error be calculated post-estimation. Estimation of WTP space models via GMNL has been implemented in R with the \pkggmnl package (Sarrias2017) and in \proglangSTATA with the \pkggmnl package (Gu2013). WTP space models can also be estimated using the \pkgapollo (Hess2019) and \pkgmixl (Molloy2021) R packages as they allow the user to hand-specify any valid utility model. Finally, Professor Arne Rise Hole developed two \proglangSTATA packages that share a common syntax for estimating mixed logit models in the preference space (\pkgmixlogit) and WTP space (\pkgmixlogitwtp) (Hole2007). Many other packages exist for estimating a wider variety of logit models, but they are limited to preference space models. Of these, package \pkgmlogit (Croissant2020) is perhaps the most complete and widely used for estimating multinomial logit and mixed logit models in R via maximum likelihood estimation.

The \pkglogitr package is designed specifically to support the estimation of multinomial logit and mixed logit models models with either preference space or WTP space utility parameterizations. While \pkglogitr is less general in scope compared to more flexible packages like \pkgmixl and \pkgapollo, it offers other functionality that is particularly useful for estimating WTP space models and conveniently switching between preference and WTP space models. For example, given their non-linear utility specification, WTP space models often diverge during estimation and can be sensitive to starting parameters. To address this, the package includes a parallelized multi-start optimization loop to search for different local minima from different random starting points when minimizing the negative log-likelihood. The user interface is also more streamlined and simplified for estimating models in either space.

Package \pkglogitr is also computationally efficient and faster than other similar packages, including the \pkgmixl package which uses high performance C++ code to compile the log-likelihood function (Molloy2021) (though \pkgmixl can be accelerated considerably via multi-core processing). The performance gains are the result of a combination of design features, including how the choice probabilities are specified, avoiding redundant computation by pre-computing constant intermediate variables, and the use of analytic gradients that are optimized for efficiency.

The rest of the article is organized as follows: Section 2 provides an overview of the models supported by \pkglogitr, including multinomial and mixed logit models with preference space and WTP space utility parameterizations. Section 3 discusses several important implications of preference versus WTP space utility parameterizations on WTP estimates. Section 4 describes the software architecture and performance. Section 5 then introduces the \pkglogitr package, including examples of estimating multinomial and mixed logit models in both preference and WTP spaces as well as additional functionality for estimating weighted models and making predictions. Section 6 explains some limitations of WTP space models. Finally, Section 7 concludes the paper.

2 Models

2.1 The random utility model in two spaces

Random utility models assume that consumers choose the alternative from a set of alternatives that has the greatest utility . Utility is a random variable that is modeled as , where is the “observed utility” (a function of the observed attributes such that ) and is a random variable representing the portion of utility unobservable to the modeler.

Adopting the same notation as in Helveston et al. (Helveston2018), consider the following utility model:

| (1) |

where is the vector of coefficients for non-price attributes , is the coefficient for price , and the error term, , is an IID random variable with a Gumbel extreme value distribution of mean zero and variance .

This model is not identified since there exists an infinite set of combinations of values for , , and that will produce the same choice probabilities. In order to specify an identifiable model, Equation 1 must be normalized. One approach is to normalize the scale of the error term by dividing Equation 1 by , producing the “preference space” utility specification (Train2005):

| (2) |

The typical preference space parameterization of the multinomial logit model can then be written by rewriting Equation 2 with , , , and :

| (3) |

The vector in Equation 3 represents the marginal utility for changes in each non-price attribute (relative to the standardized scale of the error term), and represents the marginal utility obtained from changes in price (relative to the standardized scale of the error term). The coefficients and are only relative values rather than absolute and do not have units. Using this model, estimates of the marginal WTP for changes in each non-price attribute could be computed by dividing by , where the “hat” symbol indicates a parameter estimate.

An alternative approach to normalizing Equation 1 is to divide by instead of , resulting in the “WTP space” utility parameterization:

| (4) |

Since the error term in Equation 4 is scaled by , it can be rewritten by multiplying both sides by ) and renaming , ), and :

| (5) |

The vector in Equation 5 represents the marginal WTP for changes in each non-price attribute, and represents the scale of the deterministic portion of utility relative to the standardized scale of the random error term (also called the “scale parameter”). In contrast to the coefficients from the preference space model in Equation 3, the coefficients have absolute value with units of currency.

The \pkglogitr package can fit logit models with either utility parameterization, and it contains functions that facilitate the comparison of WTP estimates between models from the two model spaces.

2.2 Multinomial and mixed logit probabilities

By assuming that the error term in Equations 3 and 5 follows a Gumbel extreme value distribution, the probability that a consumer will choose alternative in choice situation follows a convenient, closed form expression, cf. Train (Train2009):

| (6) |

where is the deterministic portion of the utility model and is the number of alternatives in choice situation . The multinomial logit model assumes homogeneous preferences across the population and possess the independence of irrelevant alternatives (IIA) property, which means that the ratio of any two probabilities is independent of the functions determining any other outcome since

| (7) |

To relax this assumption and allow for heterogeneity of preferences across the population, the multinomial logit model can be extended to the random coefficients “mixed” logit model (McFadden2000) where probabilities are the integrals of standard logit probabilities over a density of parameters across people:

| (8) |

where is a density function and contains the parameters in the deterministic portion of the utility model, which are and for preference space models (Equation 3) and and for WTP space models (Equation 5). The mixed logit probability can be interpreted as a weighted average of the multinomial logit probability with weights given by the density .

Modelers often specify different mixing distributions for parameters in depending on assumptions of how preferences might be distributed across the population. For example, modelers may assume follows a log-normal or zero-censored normal distribution to force the price coefficient to remain positive—an assumption based on the logic that most people prefer price decreases rather than increases. Likewise, parameters in are often assumed to follow a normal distribution if it is unclear whether the utility parameters for attributes should be positive or negative.

2.3 Maximum likelihood estimation

Parameters in the preference or WTP space utility models can be estimated by maximizing the log-likelihood function. For the multinomial logit model, the log-likelihood is given by:

| (9) |

where if alternative is chosen in situation and otherwise, is the number of choice situations, is the number of alternatives in choice situation , and the probabilities are given by Equation 6.

For mixed logit models, the log-likelihood can be estimated using simulation to obtain estimates of in Equation 8 (Train2009). Over a series of iterations, parameters are drawn from and used to compute the logit probability in Equation 6. The average probabilities over all of the iterations, , are then used in place of in Equation 9 to compute the simulated log-likelihood. Should the data contain a panel structure where multiple observations come from the same individual, the product of the logit probabilities in Equation 6 over all trials for each individual must first computed and then averaged over the draws of each parameter drawn from (Train2009).

McFadden (McFadden1974) shows that the log-likelihood function is globally concave for linear-in-parameters utility models with fixed parameters. This implies that optimization algorithms should always arrive at a global solution when minimizing the negative log-likelihood for preference space models with fixed parameters. In contrast, WTP space utility models (as well as mixed logit models with either utility parameterization) have non-convex log-likelihood functions and thus are not guaranteed to arrive at a global solution. For these models, different optimization strategies should be used to minimize the negative log-likelihood, such as using a multi-start loop where the optimization algorithm is run multiple times from different random starting points to search for multiple local minima.

3 Implications of preference versus WTP space utility parameterizations

WTP estimates can be obtained from both preference and WTP space utility parameterizations. In the preference space utility model given by Equation 3, WTP is estimated as ; in the WTP space model given by Equation 5, WTP is simply . The choice of which approach to use can have important implications for estimates of WTP, and modelers should consider which outcomes and measures are most relevant to any one particular study when making a choice between the two parameterizations.

3.1 Distribution of WTP estimates across the population

Depending on the utility parameterization used, the distribution of WTP in mixed logit models can be sensitive to distributional assumptions of model parameters (Train2005; Sonnier2007). For example, in a preference space model, if and were each assumed to be normally distributed, then the WTP for marginal changes in would follow a Cauchy distribution, implying that WTP has an infinite variance across the population. This WTP distribution is not likely what the modeler had in mind when making individual distributional assumptions on and , but it is the implied result. In contrast, in a WTP space model the distribution of WTP for marginal changes in can be directly specified.

Several prior studies have also identified this issue, and all find that WTP space utility parameterizations yield more reasonable estimates of WTP. In a study on preferences for alternative-fuel vehicles, Train and Weeks (Train2005) found that while a preference space model with a log-normally distributed price coefficient fit the data better, it resulted in unreasonably large estimates of WTP; in contrast, a WTP space model produced much more reasonable estimates of WTP. Using a Bayesian approach, Sonnier et al. (Sonnier2007) similarly found that a preference space model with heterogeneity distributions for attribute and price coefficients resulted in poorly behaved posterior WTP distributions and that the problem was particularly bad in small sample settings. Finally, Daly et al. (Daly2012) show that when the price coefficient is modeled with a variety of popular distributions, including the normal, truncated normal, uniform, and triangular, the resulting distribution of WTP has infinite moments.

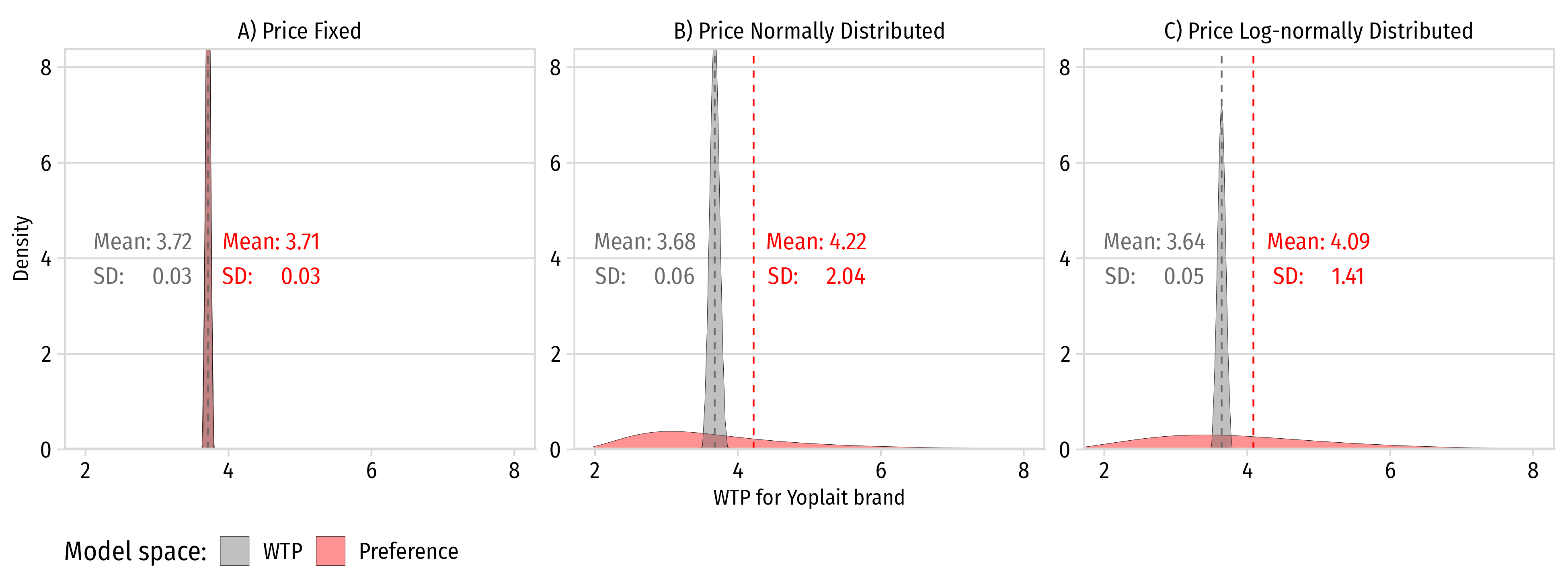

To illustrate this issue, consider an example of three preference space models with different assumptions on how the price parameter is distributed. This example uses the yogurt data set included in package \pkglogitr. In each model, coefficients for the yogurt brand ( in the preference space and in the WTP space) are modeled as normally distributed. However, the price parameter, , in the preference space model (and likewise the scale parameter, , in the WTP space model) is modeled three different ways: 1) as a fixed coefficient, 2) normally distributed, and 3) log-normally distributed.

Figure 1 compares the WTP distribution for the Yoplait brand across the population from each preference space and WTP space model. In the case where and are modeled as fixed coefficients (panel A), the WTP distributions from each model are identical. But when and are modeled as normally distributed (panel B), the WTP distribution from the preference space model changes dramatically. Since WTP in this case is the ratio of two normal distributions, the variance increases by two orders of magnitude and the mean shifts upward. A similar outcome occurs when and are modeled as log-normally distributed111Log-normal distributions are often used to force parameter positivity. (panel C). Note that the WTP distribution in the WTP space model remains nearly the same regardless of how was assumed to be distributed.

This example illustrates the sensitivity of the WTP distribution to modeling choices made in preference space utility models. In general, WTP space models yield more reasonable estimates of WTP distributions across the population, a consistent finding across multiple prior studies (Train2005; Sonnier2007; Das2009; Helveston2018).

3.2 Prediction

Whether preference space or WTP space utility models predict better is an empirical question that has not been definitively addressed in prior studies. Of the few studies that have estimated models in the WTP space, none have provided conclusive evidence that one parameterization systematically predicts better than the other. Both Sonnier et al. (Sonnier2007) and Train and Weeks (Train2005) found that a preference space parameterization fit the data better, but they also both found that the resulting estimates of WTP had unreasonably large tails. Das et al. (Das2009) also estimated both preference and WTP space models using data on preferences for landfill site attributes in Rhode Island, and they found nearly identical model fit on out-of-sample predictions with each model specification, though the WTP space model yielded more reasonable estimates of WTP.

3.3 Practical considerations

In addition to considerations of WTP estimates, model fit, and prediction, there are other practical implications to consider when choosing to estimate a preference versus WTP space model. Perhaps the simplest and most obvious distinction is that a WTP space model yields estimates of WTP without needing additional post-estimation calculations. And because WTP space coefficients have units of currency, they have a concrete meaning that can be immediately interpreted. In contrast, preference space model coefficients only have relative meaning along an abstract scale of utility, and modelers often compute WTP from preference space coefficients to help make results more interpretable.

Perhaps less obvious is the fact that WTP estimates can be directly compared with those from models estimated on other datasets since WTP coefficients are independent of error scaling. This is particularly convenient for comparing WTP estimates from different subsets of a dataset. In a preference space model, parameters are proportional to error scaling, and thus due to potential scale differences coefficients estimated from different data sets cannot be directly compared (Swait2003; Helveston2018). This also poses a challenge for comparative studies or literature reviews that seek to compare outcomes on similar topics across multiple studies.

Another perhaps less obvious implication of the preference space parameterization is the assumption that distributions of marginal utilities are independent across attributes, which induces a strong correlation structure among WTP values (Train2005). This can make it difficult to evaluate alternatives with different attribute levels since WTP cannot be added across attributes. In a WTP space model, this problem can be avoided by directly incorporating the correlation structure among WTP coefficients, and as a result dollar values can be summed to yield the total WTP for an alternative.

Finally, there is no theoretical basis for believing that marginal utilities versus marginal WTPs should follow standard distributions (e.g., normal and log-normal). In the absence of any theoretical basis for these assumptions, the modeler is left to consider differences in empirical outcomes, which as previously noted, there has not been much definitive evidence that models in one space systematically out-perform the other along all measures of significance.

4 Software architecture and performance

4.1 Design features for increased estimation speed

In maximum likelihood estimation (and simulated MLE for mixed logit models), the log-likelihood function is computed many times as the algorithm searches for parameters that minimize the negative of the log-likelihood via gradient descent. The \pkglogitr package uses several strategies to accelerate this process.

First, minimization of the negative log-likelihood is handled via the \pkgnloptr package, which is an \proglangR interface to \pkgNLopt—an open source program for nonlinear optimization started by Steven G. Johnson (Ypma2020). One benefit of using \pkgnloptr is that both the log-likelihood function and its gradient can be computed within the same function. This reduces redundant computations as many intermediate calculations are shared between the log-likelihood and its gradient. Furthermore, analytic gradients are implemented for both preference space and WTP space models and for multinomial and mixed logit models.

Another important feature is that the choice probabilities are reformulated to reduce the number of calculations needed to compute the log-likelihood function. Instead of using Equation 6 to compute the probability of each alternative in a choice set, the choice probability for the chosen alternative, , can be calculated as:

| (10) |

This results in a more stable and computationally faster calculation of the log-likelihood, which is simplified from Equation 9 as

| (11) |

In addition, \pkglogitr takes advantage of the fact that, except for the parameters, the data used in computing the log-likelihood function and its gradient do not change, enabling a considerable amount of memory reduction by pre-computing several intermediate computations that remain constant throughout the estimation process. For example, the gradient with respect to parameters of the log-likelihood in equation 11 for multinomial logit models can be written as follows:

| (12) |

In preference space models where , the partial derivative in equation 12 is:

| (13) |

In WTP space models where , the partial derivatives in equation 12 are:

| (14) |

The values of and in Equations 13 and 14 are constant and can be computed prior to starting the optimization loop. Furthermore, since , , and are already computed when calculating the log-likelihood, they can be used to quickly compute the analytic gradient with only a few additional calculations in each iteration of the algorithm.

Finally, the parallel package is also used to simultaneously estimate multiple models from different starting points when estimating a multi-start loop. For machines with multiple cores, this can dramatically increase the size of the solution space searched without substantially increasing estimation time.

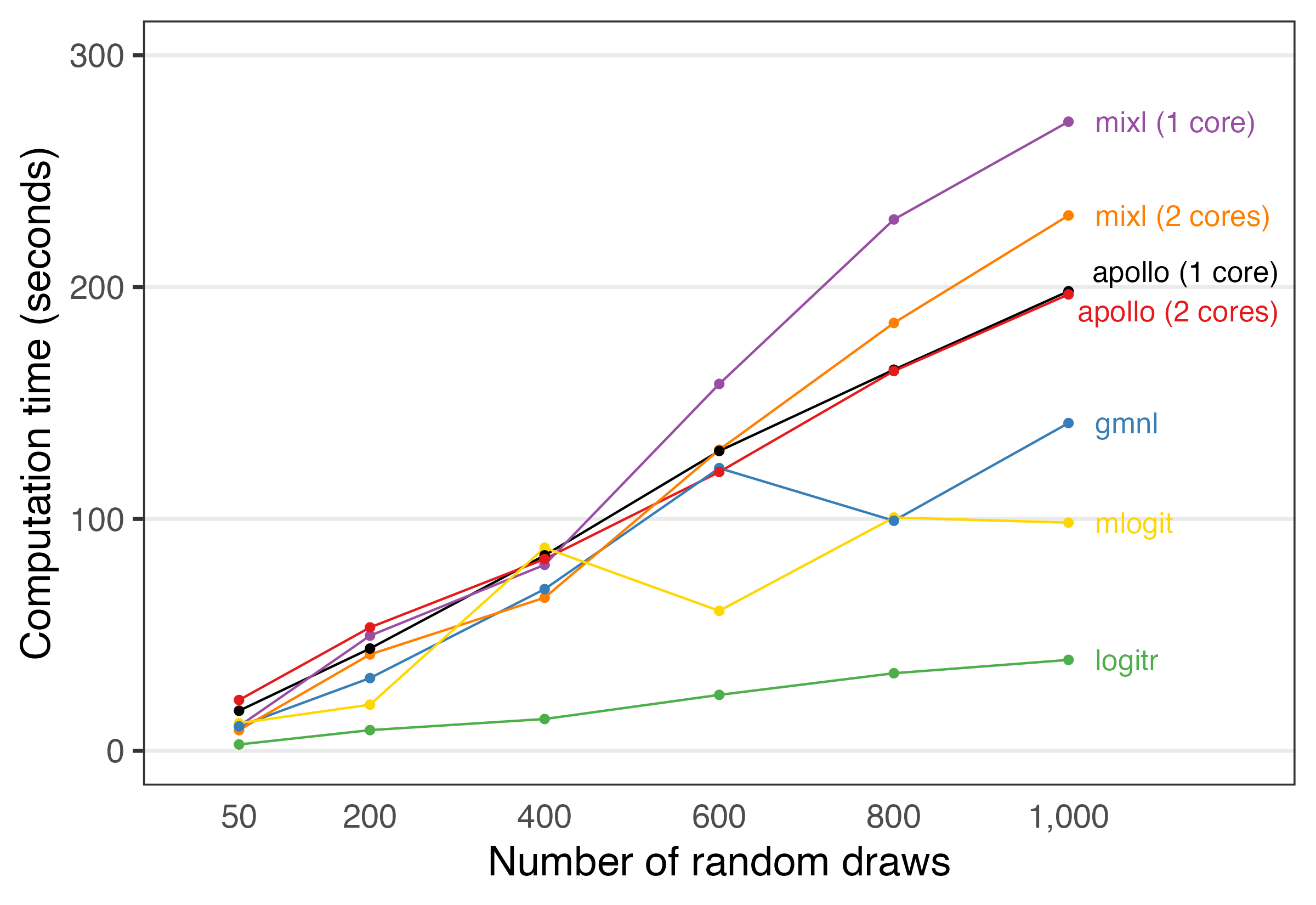

4.2 Performance benchmarking

The design features implemented in \pkglogitr result in impressive gains in overall efficiency compared to similar packages. To compare its performance, a preference space mixed logit model was estimated using \pkglogitr, \pkgmlogit, \pkgmixl, \pkggmnl, and \pkgapollo. Figure 2 shows the estimation time for each package plotted against the number of random draws used in the mixed logit model. The benchmark was carried out in a Google Colab notebook at https://colab.research.google.com/drive/1vYlBdJd4xCV43UwJ33XXpO3Ys8xWkuxx?usp=sharing.

With just 50 random draws, \pkglogitr is particularly fast, clocking in at 4.3 times faster than \pkgmixl with one core, 3.6 times faster than \pkgmixl with two cores, 5.1 times faster than \pkgmlogit, 4.5 times faster than \pkggmnl, 8.2 times faster than \pkgapollo with one core, and 10.6 times faster than \pkgapollo with two cores. The comparative difference decreases with higher numbers of draws, though even at 1,000 draws \pkglogitr is still over twice as fast as \pkgmlogit, the next-fastest package in the benchmark (see Table 1). Speeds could potentially be further improved by parallelizing elements of the gradient calculation. In addition, it is important to note that \pkgmixl in particular may perform better at very large numbers of draws (e.g. 10,000 or more) if used on a machine with a large number of cores.

Table 1: Comparison of package estimation times for a preference space mixed logit model with four normally-distributed random parameters.

| Estimation time (s) | Times slower than logitr | |||||||||||

| 50 | 200 | 400 | 600 | 800 | 1000 | 50 | 200 | 400 | 600 | 800 | 1000 | |

| logitr | 3 | 9 | 14 | 24 | 33 | 39 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 |

| mixl (1 core) | 11 | 50 | 80 | 158 | 229 | 271 | 3.9 | 5.6 | 5.8 | 6.6 | 6.8 | 6.9 |

| mixl (2 cores) | 9 | 42 | 66 | 130 | 185 | 231 | 3.2 | 4.7 | 4.8 | 5.4 | 5.5 | 5.9 |

| mlogit | 12 | 20 | 88 | 60 | 101 | 98 | 4.3 | 2.2 | 6.4 | 2.5 | 3.0 | 2.5 |

| gmnl | 11 | 31 | 70 | 122 | 99 | 141 | 3.8 | 3.5 | 5.1 | 5.1 | 3.0 | 3.6 |

| apollo (1 core) | 17 | 44 | 84 | 129 | 164 | 198 | 6.3 | 4.9 | 6.1 | 5.4 | 4.9 | 5.1 |

| apollo (2 cores) | 22 | 53 | 83 | 120 | 164 | 197 | 8.0 | 6.0 | 6.0 | 5.0 | 4.9 | 5.0 |

5 Using the \pkglogitr package

5.1 Installation

The \pkglogitr package can be installed from CRAN:

R> install.packages("logitr")

The development version can be installed from GitHub using the \pkgremotes package:

R> remotes::install_github("jhelvy/logitr")

The package is loaded in \proglangR with:

R> library("logitr")

5.2 Data format

The \pkglogitr package requires that data be structured in a data.frame and arranged in a “long” format (Wickham2014) where each row contains data on a single alternative from a choice observation. The choice observations do not have to be symmetric, meaning they can have a “ragged” structure where different choice observations have different numbers of alternatives. The data must include variables for each of the following:

-

•

Outcome: a dummy-coded variable that identifies which alternative was chosen (1 is chosen, 0 is not chosen). Only one alternative should have a 1 per choice observation.

-

•

Observation ID: a sequence of repeated numbers that identifies each unique choice observation. For example, if the first three choice observations had 2 alternatives each, then the first 6 rows of the obsID variable would be 1, 1, 2, 2, 3, 3.

-

•

Covariates: other variables that will be used as model covariates.

The \pkglogitr package contains several example data sets that illustrate this structure. The yogurt data set will be used as a running example throughout this paper to illustrate the key features of the package. The data set contains observations of yogurt purchases by a panel of 100 households (Jain1994). Choice is identified by the choice column, each choice observation is identified by the obsID column, and the columns price, feat, and brand can be used as model covariates:

R> head(yogurt) {CodeOutput} # A tibble: 6 x 7 id obsID alt choice price feat brand <dbl> <int> <int> <dbl> <dbl> <dbl> <chr> 1 1 1 1 0 8.1 0 dannon 2 1 1 2 0 6.10 0 hiland 3 1 1 3 1 7.90 0 weight 4 1 1 4 0 10.8 0 yoplait 5 1 2 1 1 9.80 0 dannon 6 1 2 2 0 6.40 0 hiland

This data set also includes an alt variable that determines the alternatives included in the choice set of each observation and an id variable that determines the individual as the data have a panel structure containing multiple choice observations from each individual.

5.3 Model specification interface

Models are specified and estimated using the logitr() function. The data argument should be set to the data frame containing the data, and the outcome and obsID arguments should be set to the column names in the data frame that correspond to the dummy-coded outcome (choice) variable and the observation ID variable, respectively. All variables to be used as model covariates should be provided as a vector of column names to the pars argument. Each variable in the vector is additively included as a covariate in the utility model, with the interpretation that they represent utilities in preference space models and WTPs in a WTP space model.

For example, consider a preference space model where the utility for yogurt is given by the following utility model:

| (15) |

where is price, is feat, and are dummy-coded variables for each brand (with the fourth brand representing the reference level). This model can be estimated using the logitr() function as follows:

R> mnl_pref <- logitr( + data = yogurt, + outcome = "choice", + obsID = "obsID", + pars = c("price", "feat", "brand") + )

The equivalent model in the WTP space is given by the following utility model:

| (16) |

To specify this model, simply move "price" from the pars argument to the scalePar argument:

R> mnl_wtp <- logitr( + data = yogurt, + outcome = "choice", + obsID = "obsID", + pars = c("feat", "brand"), + scalePar = "price" + )

In the above model, the variables in pars are marginal WTPs, whereas in the preference space model they are marginal utilities. Price is separately specified with the scalePar argument because it acts as a scaling term in WTP space models. While price is the most typical scaling variable, other continuous variables can also be used; for example, time could be used to obtain marginal estimates of “willingness to wait.”

Interactions between covariates can be entered in the pars vector separated by the * symbol. For example, an interaction between price with feat in the above preference space model could be included by specifying pars = c("price", "feat", "brand", "price*feat"), or even more concisely just pars = c("price*feat", "brand") as the interaction between price and feat will produce individual parameters for price and feat in addition to the interaction parameter.

Although the \pkglogitr model specification interface is a departure from the popular formula interface used in other similar packages such as \pkgmlogit, it was designed to be more uniform and streamlined for estimating either preference or WTP space models. For WTP space models in particular, using the formula interface can be confusing as it requires that covariates be additively specified (e.g., choice ~ price + feat + brand), which is inconsistent with the underlying WTP space utility model parameterization in which the price parameter () scales the WTP parameters.

For example, consider how the formula interface is used in the \pkggmnl package. Using \pkggmnl, WTP space models are specified by 1) modifying the price attribute in the data to be the negative of price prior to estimation, 2) specifying the model argument as "smnl", 3) additively including all parameters in the formula (including price) along with appropriate 0s and 1s in the additional formula components to properly specify a scaled multinomial logit model, 4) specifying a vector of TRUE and FALSE values to the fixed argument for every model parameter, and 5) providing starting values where the price / scale parameter is set to 1 for stability (otherwise the default value of 0 will be used, which usually results in a convergence failure). To estimate the previous example WTP space model using \pkggmnl, the data would first need to be formatted using the mlogit.data() function:

R> data_gmnl <- mlogit.data( + data = yogurt, + shape = "long", + choice = "choice", + id.var = ’id’, + alt.var = ’alt’, + chid.var = ’obsID’, + opposite = ’price’ + )

The model would then be estimated using the gmnl() function:

R> mnl_wtp <- gmnl( + data = data_gmnl, + formula = choice price + feat + brand | 0 | 0 | 0 | 1, + fixed = c(TRUE, FALSE, FALSE, FALSE, FALSE, TRUE, FALSE), + model = "smnl", method = "bhhh", + start = c(1, 0, 0, 0, 0, 0, 0) + )

Compared to the \pkglogitr interface, the above syntax is considerably more complex, and it is also not obvious that this specification will produce WTP estimates. The additive inclusion of price in formula is particularly confusing for a model that produces WTP estimates as it is inconsistent with the WTP space utility model. Finally, if the user fails to remember the specific set of preparation steps prior to estimation (such as taking the negative of price), results could be confusing.

The \pkgapollo and \pkgmixl packages can also be used to estimate WTP space models, but they require that the user hand-specify the utility model either as a function or string. While this provides greater flexibility in the types of models that can be estimated, it also requires much more effort by the user to carefully specify every model. Simple modifications, such as adding in one more variable, require that the user modify multiple settings, including modifying the starting parameter vector as well as re-defining the utility model function or string (among other potential required changes). Even with helpful guides and examples provided by the developers of these packages, more effort is required by the user to appropriately use these packages to estimate even the simplest of models.

These issues motivated the use of an alternative model specification interface for package \pkglogitr, with the goal of developing a syntax that is at least as intuitive as the formula interface but more uniform for estimating models in either the preference or WTP space.

5.4 Continuous and discrete variable coding

Variables are modeled in \pkglogitr as either continuous or discrete based on their data type. Numeric variables are modeled with a single “slope” coefficient, and character or factor type variables are modeled as categorical variables with dummy-coded coefficients for all but the first level, which serves as the reference level. For example, since the price variable in the yogurt data frame is a numeric variable, it will be modeled with a single coefficient representing the change in utility for marginal changes in price. In contrast, since brand is a character type with the levels "dannon", "hiland", "weight", and "yoplait", it will be modeled with three dummy-coded coefficients with the "dannon" brand set as the reference level as it is alphabetically first.

To change the reference level for discrete variables, modify the factor levels for that variable prior to model estimation with the factor() function. For example, the following code will set "weight" instead of "dannon" as the reference level for the brand variable:

R> yogurt2 <- logitr::yogurt R> yogurt2brand, + levels = c("weight", "hiland", "yoplait", "dannon") + ) R> levels(yogurt2

The logitr() function estimates preference space models by default. Once a model is estimated, the summary() function can be used to print a summary of the estimated model results to the console. For example, consider again the preference space model with price, feat, and brand as model covariates:

R> mnl_pref <- logitr( + data = yogurt, + outcome = "choice", + obsID = "obsID", + pars = c("price", "feat", "brand") + )

R> summary(mnl_pref) {CodeOutput} =================================================

Model estimated on: Tue Oct 04 11:58:55 2022

Using logitr version: 0.8.0

Call: logitr(data = yogurt, outcome = "choice", obsID = "obsID", pars = c("price", "feat", "brand"))

Frequencies of alternatives: 1 2 3 4 0.402156 0.029436 0.229270 0.339138

Exit Status: 3, Optimization stopped because ftol_rel or ftol_abs was reached.

Model Type: Multinomial Logit Model Space: Preference Model Run: 1 of 1 Iterations: 21 Elapsed Time: 0h:0m:0.02s Algorithm: NLOPT_LD_LBFGS Weights Used?: FALSE Robust? FALSE

Model Coefficients: Estimate Std. Error z-value Pr(>|z|) price -0.366555 0.024365 -15.0441 < 2.2e-16 *** feat 0.491439 0.120062 4.0932 4.254e-05 *** brandhiland -3.715477 0.145417 -25.5506 < 2.2e-16 *** brandweight -0.641138 0.054498 -11.7645 < 2.2e-16 *** brandyoplait 0.734519 0.080642 9.1084 < 2.2e-16 *** — Signif. codes: 0 ’***’ 0.001 ’**’ 0.01 ’*’ 0.05 ’.’ 0.1 ’ ’ 1

Log-Likelihood: -2656.8878790 Null Log-Likelihood: -3343.7419990 AIC: 5323.7757580 BIC: 5352.7168000 McFadden R2: 0.2054148 Adj McFadden R2: 0.2039195 Number of Observations: 2412.0000000

The summary includes information about the logitr() function call, the frequency of chosen alternatives, the optimization exit status, the estimated coefficients, the log-likelihood value at the solution, and several measures of model fit. In this example, three coefficients were estimated for the “brand” attribute, with "dannon" set as the default reference level.

These results indicate that, all else being equal, people in this sample on average preferred the “Yoplait” brand the most, followed by “Dannon” (the reference level, which would be 0 on the utility scale), “Weight Watchers”, and finally “Hiland”. The results also indicate that utility decreased by a value of -0.367 for every dollar increase in price, which is logically consistent with people preferring lower rather than higher prices, all else being equal.

Values from an estimated model can be extracted using methods designed for objects of class logitr, such as the following:

The estimated coefficients:

R> coef(mnl_pref) {CodeOutput} price feat brandhiland brandweight brandyoplait -0.3665546 0.4914392 -3.7154773 -0.6411384 0.7345195

The coefficient standard errors:

R> se(mnl_pref) {CodeOutput} price feat brandhiland brandweight brandyoplait 0.02436526 0.12006175 0.14541671 0.05449794 0.08064229

The log-likelihood:

R> logLik(mnl_pref) {CodeOutput} ’log Lik.’ -2656.888 (df=5)

The variance-covariance matrix:

R> vcov(mnl_pref) {CodeOutput} price feat brandhiland brandweight price 0.0005936657 5.729619e-04 0.001851795 1.249988e-04 feat 0.0005729619 1.441482e-02 0.000855011 5.092011e-06 brandhiland 0.0018517954 8.550110e-04 0.021146019 1.490080e-03 brandweight 0.0001249988 5.092011e-06 0.001490080 2.970026e-03 brandyoplait -0.0015377721 -1.821331e-03 -0.003681036 7.779428e-04 brandyoplait price -0.0015377721 feat -0.0018213311 brandhiland -0.0036810363 brandweight 0.0007779427 brandyoplait 0.0065031782

5.5 Estimating willingness to pay

Coefficients in preference space models reflect marginal changes in utility, which only have relative value. To make these coefficients more interpretable, modelers often divide the non-price parameters by the negative of the price parameter to obtain estimates of WTP (the negative of the price parameter is used so that marginal WTPs have a positive interpretation). This can be computed using the wtp() function:

R> wtp(mnl_pref, scalePar = "price") {CodeOutput} Estimate Std. Error z-value Pr(>|z|) scalePar 0.366555 0.024378 15.0361 < 2.2e-16 *** feat 1.340699 0.360539 3.7186 0.0002003 *** brandhiland -10.136219 0.583206 -17.3802 < 2.2e-16 *** brandweight -1.749094 0.181960 -9.6125 < 2.2e-16 *** brandyoplait 2.003848 0.143323 13.9813 < 2.2e-16 *** — Signif. codes: 0 ’***’ 0.001 ’**’ 0.01 ’*’ 0.05 ’.’ 0.1 ’ ’ 1

The wtp() function returns a data frame of the WTP estimates and standard errors. The coefficient labeled scalePar is the negative of the price coefficient from the preference space model, which can also be interpreted as the scale coefficient in the WTP space model as it scales all the WTP coefficients. Standard errors are estimated using the Krinsky and Robb parametric bootstrapping method (Krinsky1986).

In contrast to the preference space model coefficients, the WTP estimates above have units of currency (in this case $US dollars) and can be interpreted as how much the average person in the sample would be willing to pay for each feature, all else being equal. For example, the brand coefficients suggest that, relative to the “Dannon” brand, consumers are on average willing to pay an additional $2.00 for the “Yoplait” brand, -$1.75 for the “Weight Watchers” brand, and -$10.14 for the “Hiland” brand (negative WTPs indicate a relative preference for “Dannon”).

WTPs can also be directly estimated using a WTP space model. In this case, the pars argument should contain only attributes for which WTPs are to be estimate. The variable for “price” should be provided separately using the scalePar argument. For example, consider again the WTP space model with feat and brand WTP covariates:

R> set.seed(123) R> R> mnl_wtp <- logitr( + data = yogurt, + outcome = "choice", + obsID = "obsID", + pars = c("feat", "brand"), + scalePar = "price", + numMultiStarts = 10, + numCores = 1 + )

In the above example, a 10-iteration multi-start optimization loop was implemented by setting numMultiStarts = 10. This runs the minimization of the negative log-likelihood function 10 times from 10 different sets of random starting points (the first iteration uses all 0s except for the price parameter which starts at 1). This is recommended as WTP space models have a non-convex log-likelihood function and thus could have multiple local minimia. Note also that the multi-start loop can be parallelized by setting numCores to an integer greater than 1. The default value is one less than the total number of available cores, but numCores = 1 is used here to ensure reproducibility.

The WTP estimates have the same interpretation as those computed from the preference space model. In the summary output, a short summary of each iteration of the multi-start loop is provided first followed by the same summary information about the preference space model. Because a multi-start loop was used, only the summary of the “best” estimated model is returned (determined by the iteration with the largest log-likelihood value):

R> summary(mnl_wtp) {CodeOutput} =================================================

Model estimated on: Tue Oct 04 11:58:55 2022

Using logitr version: 0.8.0

Call: logitr(data = yogurt, outcome = "choice", obsID = "obsID", pars = c("feat", "brand"), scalePar = "price", numMultiStarts = 10, numCores = 1)

Frequencies of alternatives: 1 2 3 4 0.402156 0.029436 0.229270 0.339138

Summary Of Multistart Runs: Log Likelihood Iterations Exit Status 1 -2656.888 38 3 2 -2656.888 52 3 3 -2656.888 59 3 4 -2656.888 40 3 5 -2656.888 44 3 6 -2656.888 44 3 7 -2656.888 63 3 8 -2656.888 36 3 9 -2656.888 40 3 10 -2656.888 45 3

Use statusCodes() to view the meaning of each status code

Exit Status: 3, Optimization stopped because ftol_rel or ftol_abs was reached.

Model Type: Multinomial Logit Model Space: Willingness-to-Pay Model Run: 1 of 10 Iterations: 38 Elapsed Time: 0h:0m:0.04s Algorithm: NLOPT_LD_LBFGS Weights Used?: FALSE Robust? FALSE

Model Coefficients: Estimate Std. Error z-value Pr(>|z|) scalePar 0.366583 0.024366 15.0448 < 2.2e-16 *** feat 1.340593 0.355867 3.7671 0.0001651 *** brandhiland -10.135764 0.576089 -17.5941 < 2.2e-16 *** brandweight -1.749083 0.179898 -9.7226 < 2.2e-16 *** brandyoplait 2.003821 0.142377 14.0740 < 2.2e-16 *** — Signif. codes: 0 ’***’ 0.001 ’**’ 0.01 ’*’ 0.05 ’.’ 0.1 ’ ’ 1

Log-Likelihood: -2656.8878779 Null Log-Likelihood: -3343.7419990 AIC: 5323.7757559 BIC: 5352.7168000 McFadden R2: 0.2054148 Adj McFadden R2: 0.2039195 Number of Observations: 2412.0000000

In the above summary, iteration 1 converged to a solution with a log-likelihood value of -2656.888. While all of the iterations arrived at the same solution in this particular example, this is not always the case nor is it guaranteed. Because the previous examples are both fixed parameter models, the WTP estimates from the WTP space model are identical to those computed from the preference space model. The WTPs from each model can be quickly compared using the wtpCompare() function:

R> wtpCompare( + model_pref = mnl_pref, + model_wtp = mnl_wtp, + scalePar = "price" + ) {CodeOutput} pref wtp difference scalePar 0.3665546 0.3665832 0.00002867 feat 1.3406987 1.3405926 -0.00010605 brandhiland -10.1362190 -10.1357635 0.00045548 brandweight -1.7490940 -1.7490826 0.00001133 brandyoplait 2.0038476 2.0038208 -0.00002686 logLik -2656.8878790 -2656.8878779 0.00000106

In the above summary, the pref column contains the computed WTPs from the preference space model, and the wtp column contains the directly estimated WTPs from the WTP space model. The difference column is the computed difference between them. This is a helpful tool for assessing whether the two models converged to the same solution.

5.6 Estimating mixed logit models

The mixed logit model is a popular approach for modeling unobserved heterogeneity across individuals, which is implemented by assuming that parameters vary randomly across individuals according to a chosen distribution (McFadden2000). A mixed logit model is specified by setting the randPars argument in the logitr() function equal to a named vector defining parameter distributions. The current package version (0.8.0) supports the following distributions:

-

•

Normal: "n"

-

•

Log-normal: "ln"

-

•

Zero-censored normal: "cn"

Mixed logit models will estimate a mean and standard deviation of the underlying normal distribution for each random coefficient. Note that log-normal or zero-censored normal parameters force positivity, so when using these it is often necessary to use the negative of a value (e.g. for “price”, which typically has a negative coefficient). Mixed logit models in \pkglogitr assume uncorrelated heterogeneity covariances by default, though full covariances can be estimated using the correlation = TRUE argument. For WTP space models, the scalePar parameter can also be modeled as following a random distribution by setting the randScale argument equal to "n", "ln", or "cn".

The code below is an example of a mixed logit model where the observed utility for yogurts is , where is price, is feat, and are dummy-coded variables for brand. To model feat as well as each of the brands as normally-distributed, set randPars = c(feat = "n", brand = "n"). Since mixed logit models have a non-convex log-likelihood function, it is recommended to use a multi-start search to run the optimization multiple times from different random starting points. Mixed logit models typically take longer to estimate than fixed parameter models, so setting a larger number for numMultiStarts could take several minutes to complete.

Note that since the yogurt data has a panel structure (i.e. multiple choice observations for each respondent), it is necessary to set the panelID argument to the id variable, which identifies the individual. This will use the panel version of the log-likelihood (see (Train2009) section 6.7 for details).

R> set.seed(456) R> R> mxl_pref <- logitr( + data = yogurt, + outcome = ’choice’, + obsID = ’obsID’, + panelID = ’id’, + pars = c(’price’, ’feat’, ’brand’), + randPars = c(feat = ’n’, brand = ’n’), + numMultiStarts = 10, + numCores = 1 + )

R> summary(mxl_pref) {CodeOutput} =================================================

Model estimated on: Tue Oct 04 11:58:57 2022

Using logitr version: 0.8.0

Call: logitr(data = yogurt, outcome = "choice", obsID = "obsID", pars = c("price", "feat", "brand"), randPars = c(feat = "n", brand = "n"), panelID = "id", numMultiStarts = 10, numCores = 1)

Frequencies of alternatives: 1 2 3 4 0.402156 0.029436 0.229270 0.339138

Summary Of Multistart Runs: Log Likelihood Iterations Exit Status 1 -1266.550 34 3 2 -1300.751 64 3 3 -1260.216 35 3 4 -1261.216 43 3 5 -1269.066 40 3 6 -1239.294 56 3 7 -1343.221 59 3 8 -1260.006 55 3 9 -1273.143 52 3 10 -1304.384 59 3

Use statusCodes() to view the meaning of each status code

Exit Status: 3, Optimization stopped because ftol_rel or ftol_abs was reached.

Model Type: Mixed Logit Model Space: Preference Model Run: 6 of 10 Iterations: 56 Elapsed Time: 0h:0m:2s Algorithm: NLOPT_LD_LBFGS Weights Used?: FALSE Panel ID: id Robust? FALSE

Model Coefficients: Estimate Std. Error z-value Pr(>|z|) price -0.448338 0.039987 -11.2120 < 2.2e-16 *** feat 0.776990 0.193521 4.0150 5.944e-05 *** brandhiland -6.367360 0.520828 -12.2255 < 2.2e-16 *** brandweight -3.668683 0.307207 -11.9421 < 2.2e-16 *** brandyoplait 1.122492 0.203483 5.5164 3.460e-08 *** sd_feat 0.567495 0.225004 2.5222 0.01166 * sd_brandhiland -3.181844 0.371697 -8.5603 < 2.2e-16 *** sd_brandweight 4.097130 0.232495 17.6225 < 2.2e-16 *** sd_brandyoplait 3.261281 0.219902 14.8306 < 2.2e-16 *** — Signif. codes: 0 ’***’ 0.001 ’**’ 0.01 ’*’ 0.05 ’.’ 0.1 ’ ’ 1

Log-Likelihood: -1239.2944250 Null Log-Likelihood: -3343.7419990 AIC: 2496.5888500 BIC: 2548.6828000 McFadden R2: 0.6293690 Adj McFadden R2: 0.6266774 Number of Observations: 2412.0000000

Summary of 10k Draws for Random Coefficients: Min. 1st Qu. Median Mean 3rd Qu. Max. feat -Inf 0.3938347 0.7765564 0.7761956 1.1591475 Inf brandhiland -Inf -8.5118797 -6.3663393 -6.3644102 -4.2201174 Inf brandweight -Inf -6.4342648 -3.6720435 -3.6750045 -0.9090452 Inf brandyoplait -Inf -1.0817673 1.1169084 1.1141118 3.3162383 Inf

Since the feat and brand attributes were modeled as normally distributed across the population, each of these covariates have two parameters that describe the mean and standard deviation of a normal distribution. For example, the coefficients brandyoplait and sd_brandyoplait indicate that, relative to the “Dannon” brand, the marginal utility for the “Yoplait” brand follows a normal distribution across the population where . For mixed logit models, a summary of all random parameter distributions is printed at the bottom of the summary output. In this example, there appears to be less heterogeneity in preferences for the “Yoplait” and “Hiland” brands compared to the “Weight Watchers” brand, which has a larger standard deviation parameter.

Note that mixed logit models can sometimes produce negative values for the standard deviation parameters; in these cases, the parameters should be interpreted as positive. The negative values are an artifact of how the simulated MLE algorithm works. Since the normal distribution is symmetric, it does not matter if draws are generated with or , where is a standard normal and and are the mean and standard deviation parameters. By allowing the standard deviation parameter to be negative, the optimization is unconstrained, making it a much easier problem to solve.

5.7 Estimating WTP space mixed logit models

WTP space mixed logit models have the advantage of being able to directly specify the assumed distribution of WTP across the population. As with fixed parameter models, estimating a mixed logit WTP space model requires that price be separately specified with the scalePar argument. The randPars argument is used to specify random parameters. For example, the following can be used to estimate a model where the WTP distributions for feat and each brand is assumed to be normally distributed:

R> set.seed(6789) R> R> mxl_wtp <- logitr( + data = yogurt, + outcome = "choice", + obsID = "obsID", + panelID = ’id’, + pars = c("feat", "brand"), + scalePar = "price", + randPars = c(feat = "n", brand = "n"), + numMultiStarts = 10, + numCores = 1 + )

R> summary(mxl_wtp) {CodeOutput} =================================================

Model estimated on: Tue Oct 04 11:59:16 2022

Using logitr version: 0.8.0

Call: logitr(data = yogurt, outcome = "choice", obsID = "obsID", pars = c("feat", "brand"), scalePar = "price", randPars = c(feat = "n", brand = "n"), panelID = "id", numMultiStarts = 10, numCores = 1)

Frequencies of alternatives: 1 2 3 4 0.402156 0.029436 0.229270 0.339138

Summary Of Multistart Runs: Log Likelihood Iterations Exit Status 1 -1256.886 110 3 2 -1252.536 76 3 3 -1258.974 87 3 4 -1342.036 111 4 5 -1250.922 111 3 6 -1266.990 66 3 7 -1268.352 81 3 8 -1239.294 77 3 9 -1258.974 60 3 10 -1239.294 51 3

Use statusCodes() to view the meaning of each status code

Exit Status: 3, Optimization stopped because ftol_rel or ftol_abs was reached.

Model Type: Mixed Logit Model Space: Willingness-to-Pay Model Run: 8 of 10 Iterations: 77 Elapsed Time: 0h:0m:3s Algorithm: NLOPT_LD_LBFGS Weights Used?: FALSE Panel ID: id Robust? FALSE

Model Coefficients: Estimate Std. Error z-value Pr(>|z|) scalePar 0.448563 0.039982 11.2191 < 2.2e-16 *** feat 1.731133 0.491792 3.5201 0.0004315 *** brandhiland -14.223308 1.365310 -10.4176 < 2.2e-16 *** brandweight -8.172665 0.955928 -8.5495 < 2.2e-16 *** brandyoplait 2.503597 0.407192 6.1484 7.825e-10 *** sd_feat 1.266802 0.497472 2.5465 0.0108816 * sd_brandhiland -7.114726 0.944233 -7.5349 4.885e-14 *** sd_brandweight 9.130682 0.923411 9.8880 < 2.2e-16 *** sd_brandyoplait 7.270250 0.752617 9.6600 < 2.2e-16 *** — Signif. codes: 0 ’***’ 0.001 ’**’ 0.01 ’*’ 0.05 ’.’ 0.1 ’ ’ 1

Log-Likelihood: -1239.2939746 Null Log-Likelihood: -3343.7419990 AIC: 2496.5879491 BIC: 2548.6819000 McFadden R2: 0.6293691 Adj McFadden R2: 0.6266775 Number of Observations: 2412.0000000

Summary of 10k Draws for Random Coefficients: Min. 1st Qu. Median Mean 3rd Qu. Max. feat -Inf 0.8758265 1.730165 1.729359 2.584211 Inf brandhiland -Inf -19.0185364 -14.221025 -14.216712 -9.421990 Inf brandweight -Inf -14.3359189 -8.180155 -8.186754 -2.022659 Inf brandyoplait -Inf -2.4102743 2.491150 2.484915 7.394032 Inf

The summary shows the solution for iteration 8 out of the 10 multi-starts—the one with the largest log-likelihood value. Since the feat and brand WTPs were both modeled as normally distributed across the population, each of these covariates have two parameters that describe the mean and standard deviation of a normal distribution. The results again suggest that there is greater heterogeneity for the “Weight Watchers” brand compared to “Yoplait” and “Hiland”, which can be seen with its larger standard deviation coefficient and wider WTP range in the distribution summary at the bottom of the summary output. In fact, these results indicate that although the mean WTP for the “Weight Watchers” brand is still higher than that of the “Hiland” brand, the heterogeneity in WTP spans a much wider range.

In this case, since the price parameter was modeled as a fixed parameter, the WTP estimates from the preference space and those from the WTP space model are nearly identical:

R> wtpCompare( + model_pref = mxl_pref, + model_wtp = mxl_wtp, + scalePar = "price" + ) {CodeOutput} pref wtp difference scalePar 0.4483378 0.4485634 0.00022557 feat 1.7330459 1.7311326 -0.00191335 brandhiland -14.2021478 -14.2233082 -0.02116033 brandweight -8.1828533 -8.1726652 0.01018805 brandyoplait 2.5036744 2.5035970 -0.00007740 sd_feat 1.2657757 1.2668022 0.00102646 sd_brandhiland -7.0969787 -7.1147261 -0.01774740 sd_brandweight 9.1384873 9.1306816 -0.00780576 sd_brandyoplait 7.2741604 7.2702504 -0.00391001 logLik -1239.2944250 -1239.2939746 0.00045043

If, however, the price parameter in either model were modeled as a random parameter (which is controlled via the randScale argument), the resulting WTP estimates could be substantially different.

5.8 Weighted models

Sometimes the modeler may wish to differentially weight individual choice observations in model estimation. For example, if a particular group was over- or under-represented in a sample relative to that of a target population, the choice observations of that group could be weighted such that they have a stronger or weaker contribution to the log-likelihood in an attempt to balance the sample to match the proportions of the target population.

The cars_us data set that comes with the package includes a weights column and is useful for illustrating how to estimate weighted models. This data set contains 384 stated choice observations from a conjoint survey of U.S. car buyers fielded online using Amazon Mechanical Turk in 2012 and in person at the 2013 Pittsburgh Auto show (Helveston2015). Participants were asked to select a vehicle from a set of three alternatives, and each participant answered 15 choice questions. The data set contains variables for different types of vehicles ("hev", "phev10", "phev20", "phev40", "bev75", "bev100", "bev150"), different brands represented by the country of origin ("american", "japanese", "chinese", "skorean"), fast charging options ("phevFastcharge" and "bevFastcharge"), price ("price"), operating cost ("opCost"), and 0-60 mph acceleration time ("accelTime").

To compare the impact of the weights on the estimated parameters, an unweighted and weighted model are estimated, both in the WTP space to replicate the models estimated in Helveston et al. (Helveston2015). In both models, the argument robust = TRUE clusters the standard errors using the obsID variable for clustering, which should be done for weighted models. Standard errors can also be clustered at other levels by specifying a clusterID variable. For example, a common desired clustering is to cluster at the individual level in conjoint studies where survey respondents answer multiple sequential choice questions to account for potential correlations among these questions. The unweighted model is estimated with the following code:

R> set.seed(5678) R> R> mnl_wtp_unweighted <- logitr( + data = cars_us, + outcome = "choice", + obsID = "obsnum", + pars = c( + "hev", "phev10", "phev20", "phev40", "bev75", "bev100", "bev150", + "american", "japanese", "chinese", "skorean", "phevFastcharge", + "bevFastcharge","opCost", "accelTime"), + scalePar = "price", + robust = TRUE, + numMultiStarts = 10, + numCores = 1 + )

R> summary(mnl_wtp_unweighted) {CodeOutput} =================================================

Model estimated on: Tue Oct 04 11:59:52 2022

Using logitr version: 0.8.0

Call: logitr(data = cars_us, outcome = "choice", obsID = "obsnum", pars = c("hev", "phev10", "phev20", "phev40", "bev75", "bev100", "bev150", "american", "japanese", "chinese", "skorean", "phevFastcharge", "bevFastcharge", "opCost", "accelTime"), scalePar = "price", robust = TRUE, numMultiStarts = 10, numCores = 1)

Frequencies of alternatives: 1 2 3 0.34323 0.33507 0.32170

Summary Of Multistart Runs: Log Likelihood Iterations Exit Status 1 -4616.952 26 3 2 -4616.955 31 3 3 -4616.952 45 3 4 -4616.952 35 3 5 -4616.952 34 3 6 -4616.952 36 3 7 -4616.952 34 3 8 -4616.952 33 3 9 -4616.952 34 3 10 -4616.952 32 3

Use statusCodes() to view the meaning of each status code

Exit Status: 3, Optimization stopped because ftol_rel or ftol_abs was reached.

Model Type: Multinomial Logit Model Space: Willingness-to-Pay Model Run: 8 of 10 Iterations: 33 Elapsed Time: 0h:0m:0.1s Algorithm: NLOPT_LD