Digital Asset Valuation: A Study on Domain Names, Email Addresses, and NFTs

Abstract.

Existing works on valuing digital assets on the Internet typically focus on a single asset class. To promote the development of automated valuation techniques, preferably those that are generally applicable to multiple asset classes, we construct DASH, the first Digital Asset Sales History dataset that features multiple digital asset classes spanning from classical to blockchain-based ones. Consisting of K transactions of domain names (DASHDN), email addresses (DASHEA), and non-fungible token (NFT)-based identifiers (DASHNFT), such as Ethereum Name Service names, DASH advances the field in several aspects: the subsets DASHDN, DASHEA, and DASHNFT are the largest freely accessible domain name transaction dataset, the only publicly available email address transaction dataset, and the first NFT transaction dataset that focuses on identifiers, respectively.

We build strong conventional feature-based models as the baselines for DASH. We next explore deep learning models based on fine-tuning pre-trained language models, which have not yet been explored for digital asset valuation in the previous literature. We find that the vanilla fine-tuned model already performs reasonably well, outperforming all but the best-performing baselines. We further propose improvements to make the model more aware of the time sensitivity of transactions and the popularity of assets. Experimental results show that our improved model consistently outperforms all the other models across all asset classes on DASH.

1. Introduction

Since its birth, the Internet has generated many digital assets, such as domain names, and works on their monetary appraisal date back to over two decades ago (Nguyen, 2001). Most research on automated digital asset valuation focuses on a single asset class (Wu et al., 2009; Wu and He, 2009; Tang et al., 2014; Dieterle and Bergmann, 2014; Bikadi et al., 2017; Liu et al., 2019; Deli̇baş, 2019; Nadini et al., 2021; Kapoor et al., 2022; Jain et al., 2022). Existing valuation methods rely heavily on expert knowledge and asset- and market-specific feature-engineering, whose cost reduces the potential for broadly applying the methods. Moreover, for many digital asset classes, there are no common testbeds or even no freely accessible data for studying valuation techniques, which raises the difficulties in making direct comparisons between methods, further limiting the progress in this research area.

With the goal of advancing the development of automated valuation methods, preferably those that are broadly applicable to multiple digital asset classes, we construct DASH, a Digital Asset Sales History dataset containing transactions of multiple representative asset classes. Specifically, DASH consists of sales history of domain names (DASHDN), email addresses (DASHEA), and non-fungible token (NFT)-based identifiers (DASHNFT), such as Ethereum Name Service (ENS) names (Section 3). Assets of the classes featured in DASH are challenging to assess due to their non-fungibility (Visconti, 2020). The valuation methods for these asset classes can potentially benefit from being collectively studied as they share the inherent property of being in some form of unique identifier.

To establish baseline performance on DASH, we design a set of features that apply to all the studied asset classes and build three conventional feature-based regression models (Section 4.2). We next explore approaches based on fine-tuning pre-trained language models (LMs) (Section 4.3). We find that the vanilla fine-tuned model performs reasonably well: without leveraging any handcrafted features or explicit expert knowledge, it surpasses two out of three conventional models on the average performance over all subsets of DASH. We further propose two improvements: (i) make the model more aware of the time sensitivity of transactions using a two-stage fine-tuning approach; (ii) append to the input sequence external knowledge about the popularity of assets. Experiments demonstrate that our improved model substantially reduces the mean squared logarithmic error (MSLE) by on average on the test set of DASH compared to the best-performing conventional model (Section 5).

Our main contributions are as follows.

-

•

We introduce DASH, the first digital asset transaction dataset that features multiple asset classes spanning from classical to blockchain-based ones. To our knowledge, (i) DASHDN is the largest freely accessible domain name transaction dataset; (ii) DASHEA is the only publicly available email address transaction dataset; and (iii) DASHNFT is the first NFT transaction dataset that focuses on identifiers.

-

•

We propose conventional feature-based models and deep learning models for DASH. In contrast to all previous works, we present the first study that leverages pre-trained language models for digital asset valuation and demonstrates that fine-tuning a pre-trained language model can deliver performance superior to conventional models.

-

•

We conduct a comprehensive ablation study and a detailed error analysis of the proposed models on the DASH dataset. We also discuss variants of our models and the limitation of the work. The dataset and code will be available at https://dataset.org/dash/.

2. Related Work

| DASHDN | DASHEA | DASHNFT | |

|---|---|---|---|

| # of transactions | |||

| Avg./Max. # of transactions per asset | / | / | / |

| Min./Med./Max. sales price (currency) | / / (USD) | / / (CNY) | / / (ETH) |

| standard deviation of sales price | |||

| Min./Med./Max. name length | / / | / / | / / |

| date range | 07/03/200606/30/2022 | 01/23/201106/30/2022 | 05/15/201906/30/2022 |

| # of suffixes | |||

| platforms (% of transactions) | Sedo (), Flippa () | FGLT () | OS (), X2Y2 (), LR () |

2.1. Transaction Data

2.1.1. Classical Assets

We are not aware of any existing email address transaction datasets. As for domain name transactions, past studies use different data, most of which are not publicly accessible (Wu and He, 2009; Dieterle and Bergmann, 2014; Lindenthal, 2014; Bikadi et al., 2017; Deli̇baş, 2019). The data released by (Liu et al., 2019) is the only publicly accessible dataset we know. Their released dataset consists of domain names, which are all .com domains, along with binary labels indicating whether the price is high or low based on pre-defined thresholds. The exact sales price and date are not available. In comparison, DASHDN has orders of magnitude more sales with the exact sales price and date, covering over different domain extensions. Some platforms (e.g., NameBio111https://namebio.com/) provide online domain name sales search services, but they do not support exporting data in batch freely.

2.1.2. Blockchain-Based Assets

Recent works have released several datasets regarding NFT transactions (Nadini et al., 2021; Kapoor et al., 2022; Mekacher et al., 2022). These datasets primarily focus on the NFTs’ image objects (Nadini et al., 2021; Kapoor et al., 2022), traits assigned by the NFT creators (Mekacher et al., 2022), and mentions in social media (Kapoor et al., 2022).

2.2. Valuation Approaches

We primarily discuss the works about valuing unique individual assets rather than predicting the price of fungible assets (e.g., the Bitcoin to USD price (Dutta et al., 2020)) or estimating the aggregate price of asset collections (e.g., the median price of four-letter .com domain names, the average price of Bored Ape Yacht Club (BAYC) (Jain et al., 2022)) over time. Various digital asset valuation methods, from theoretical to empirical, have been developed over the years (Wu et al., 2009; Wu and He, 2009; Tang et al., 2014; Dieterle and Bergmann, 2014; Meystedt, 2015; Bikadi et al., 2017; Liu et al., 2019; Deli̇baş, 2019; Visconti, 2020; Nadini et al., 2021; Kapoor et al., 2022; Mekacher et al., 2022). Most methods employed in recent research are conventional feature-based machine learning models (Liu et al., 2019; Deli̇baş, 2019; Nadini et al., 2021; Kapoor et al., 2022). They show the superior performance of random forest, eXtreme Gradient Boosting (XGBoost) (Chen and Guestrin, 2016), and Adaptive Boosting (AdaBoost) (Freund and Schapire, 1995) for the valuation of domain names or NFTs compared with other feature-based models given the same feature set. A few works on NFT valuation leverage deep learning models, but the models are mainly used as the image encoder to encode image-based NFTs (Nadini et al., 2021; Kapoor et al., 2022). Outside of academia, there are several well-established proprietary domain name appraisal systems from the industry, such as Estibot222https://www.estibot.com/ and GoDaddy Domain Appraisals333https://www.godaddy.com/domain-value-appraisal (GoValue). In particular, GoValue employs deep learning to leverage the vast amount of domain name transaction data available only to GoDaddy444https://www.godaddy.com/engineering/2019/07/26/domain-name-valuation/. Compared with all these works, we focus on methods generally applicable to multiple asset classes and demonstrate the effectiveness of models based on language model fine-tuning over previous methods in digital asset valuation.

2.3. Fine-Tuning Pre-Trained Language Models

The past few years have witnessed significant progress in various natural language understanding problems with the help of fine-tuning pre-trained high-capacity language models (Radford et al., 2018; Devlin et al., 2019). More recently, applications of language model fine-tuning to problems beyond natural language understanding have emerged, such as automated theorem proving (Polu and Sutskever, 2020) and playing chess (Stöckl, 2021). We follow this thread and explore the application to digital asset valuation, which is underexplored in previous research.

3. Data

3.1. Collection Methodology

3.1.1. Data Sources

We collect digital asset transaction data from a variety of data sources, summarized in the following.

-

•

Domain names: We track the domain name auctions hosted by sedo.com (Sedo) and flippa.com (Flippa). Additionally, we track the publicly disclosed buy-it-now sales and sales by negotiation completed on Flippa.

-

•

Email addresses: We track the email address auctions hosted by fglt.net (FGLT).

-

•

NFTs: We track sales of NFT-based identifiers, including ENS, Unstoppable Domains, and Decentraland Names reported by opensea.io (OpenSea), x2y2.io (X2Y2), and looksrare.org (LooksRare).

3.1.2. Filtering and Normalization

We filter out bundle sales and sales whose price is zero. For auctions, we only keep the “reserve met” and “no reserve” ones that have at least one bid. As ENS names are stored in a hashed form (Xia et al., 2021), we filter out ENS name transactions whose unhashed name is unknown. We convert the sales price to the dominant currency used in transactions of the corresponding asset class (i.e., USD, CNY, and ETH for domain names, email addresses, and NFTs, respectively) using the exchange rate at the transaction time.

3.1.3. Suspicious Transaction Detection

We notice suspicious transactions in the collected data. For example, the ENS name oneboy.eth has been traded between two Ethereum addresses over times, indicating that a single agent likely controls the two addresses and these sales are likely bogus. To reduce the potential negative impact of such transactions, we adopt the following strategies: (i) for each transaction of NFT from address to address , we remove if both and are involved in (but not necessarily together) at least two other transactions of ; (ii) for each transaction of email address , we remove if another transaction of happens after within seven days. We do not apply similar strategies to domain names because Sedo and Flippa have relatively high commission fees, making it expensive to initiate suspicious transactions.

The resulting transactions of domain names, email addresses, and NFTs constitute DASHDN, DASHEA, and DASHNFT, respectively, and . Each transaction in DASH comprises an asset identifier, a transaction date, and the corresponding sales price, along with the meta information of the asset that consists of the asset class and asset collection (if applicable). Note that the studied assets in DASH do not have name collisions so far, so an asset identifier alone can unambiguously represent an asset. The meta information offers additional information to distinguish between different assets that share the same identifier in case there are name collisions in the future.

3.2. Data Statistics

For convenience, we first formally define the name and suffix of an asset, which will be referred to in the rest of this paper: given an asset from DASH, its name refers to the substring of the identifier starting from the beginning to the first delimiter (exclusive), and its suffix refers to the substring after the first delimiter (exclusive). The delimiter is at sign for DASHEA and dot for DASHDN and DASHNFT. For example, the name and suffix of example.eth are example and eth, respectively; the name and suffix of email@example.com are email and example.com, respectively.

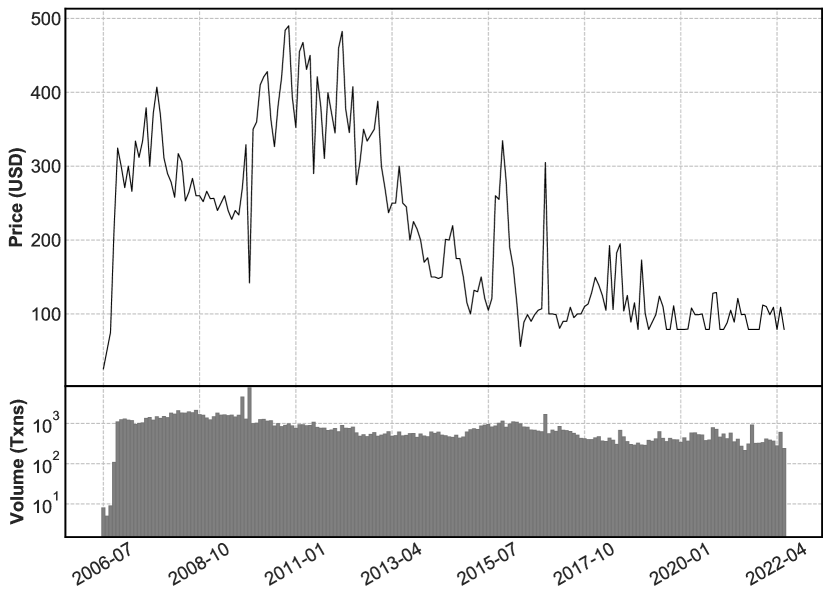

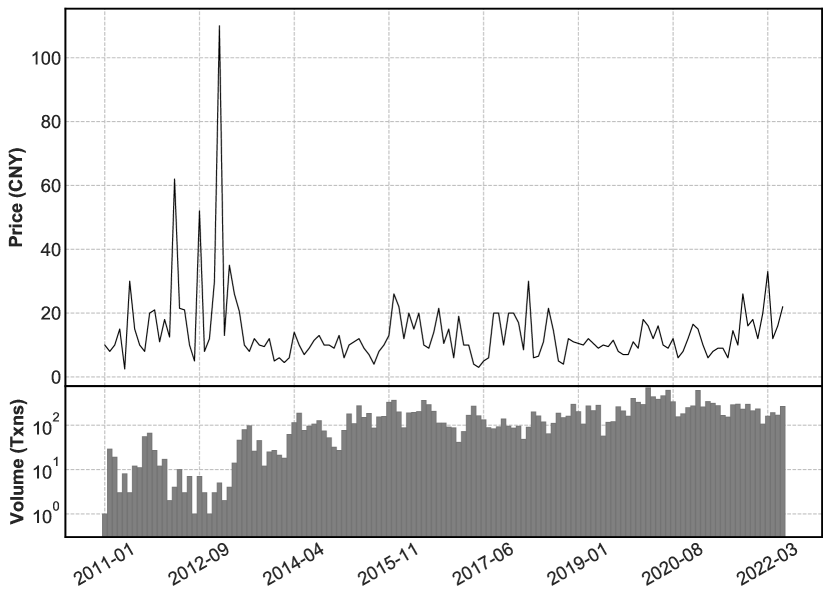

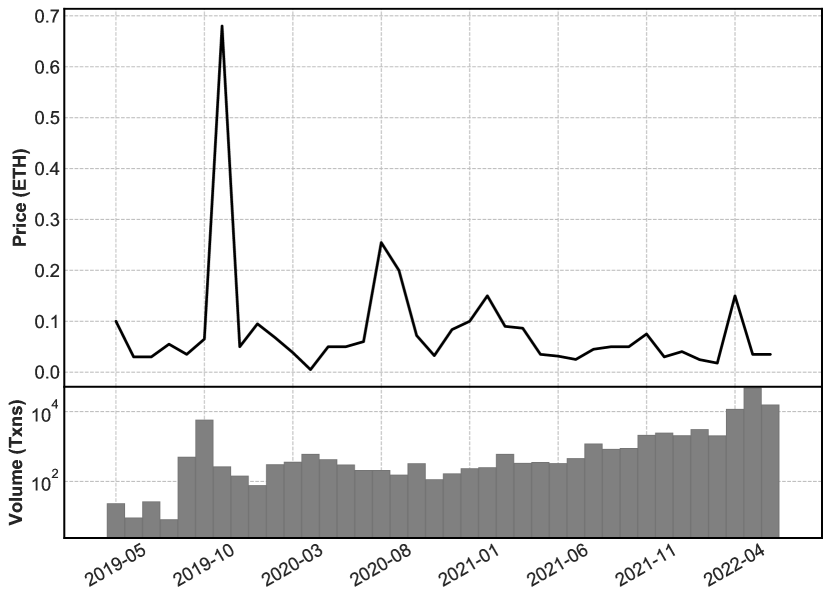

We summarize the statistics of DASH in Table 1. We see a considerable sales price range with a large standard deviation in every subset of DASH. Besides, most assets in DASH have only one transaction, and there are numerous different suffixes. These altogether provide evidence that DASH is a very challenging dataset for digital asset valuation. We plot Figure 1 to show an overall view of transaction distributions across time. Compared with DASHDN and DASHEA, the transactions in DASHNFT are less evenly distributed in terms of volume over time.

4. Approaches

4.1. Task Formulations

In this work, we enforce that transactions in the development set are newer (resp. older) compared with the training (resp. test) set. This is distinguished from many previous works, where training data can be newer than evaluation data (Deli̇baş, 2019; Kapoor et al., 2022). Specifically, we split the data by date, with the latest for testing, the next latest for development, and the earliest for training. We summarize the split in Table 2. As the date range in the split is different for different asset classes, to prevent time leakage, we train separate models for DASHDN, DASHEA, and DASHNFT.

| Date Range | # of Txns | ||

|---|---|---|---|

| Train | 07/03/2006 07/06/2019 | ||

| DASHDN | Dev | 07/07/2019 11/19/2020 | |

| Test | 11/20/2020 06/30/2022 | ||

| Train | 01/23/2011 09/11/2021 | ||

| DASHEA | Dev | 09/12/2021 01/13/2022 | |

| Test | 01/14/2022 06/30/2022 | ||

| Train | 05/15/2019 06/18/2022 | ||

| DASHNFT | Dev | 06/19/2022 06/27/2022 | |

| Test | 06/28/2022 06/30/2022 |

For consistency and clarity, we now introduce several notations and give a formal definition of the task. Given a set of transactions where , , and represent the asset identifier, price, and time of the transaction, respectively, and , we partition into , , and such that . The task is to learn from a model that takes as input an asset identifier, and outputs an estimation of the price as accurate as possible, measured by MSLE on and .

| Method | DASHDN | DASHEA | DASHNFT | Average | ||||

|---|---|---|---|---|---|---|---|---|

| Dev | Test | Dev | Test | Dev | Test | Dev | Test | |

| Mean | ||||||||

| AdaBoost | ||||||||

| Random Forest | ||||||||

| XGBoost | ||||||||

| Vanilla mBERT | ||||||||

| mBERT | ||||||||

| Method | DASHDN | DASHEA | DASHNFT | Average | ||||

|---|---|---|---|---|---|---|---|---|

| MSLE | MSLE | MSLE | MSLE | |||||

| XGBoost | – | – | – | – | ||||

| – length | ||||||||

| – suffix | ||||||||

| – character | ||||||||

| – # of tokens | ||||||||

| – vocabulary | ||||||||

| – trademark | ||||||||

| – TLD count | ||||||||

| mBERT | – | – | – | |||||

| – LM pre-training | ||||||||

| – 1st stage fine-tuning | ||||||||

| – 2nd stage fine-tuning | ||||||||

| – TLD count | ||||||||

4.2. Non-Neural Models

4.2.1. Mean Value Baseline

This simple model predicts a constant value that minimizes the MSLE on the training set. More formally, the constant value is the geometric mean price defined as

4.2.2. Feature-Based Regression Models

Following previous empirical studies (Section 2.2), we develop conventional feature-based models using random forest, XGBoost, and AdaBoost. Inspired by previous studies on drop catching and squatting (Miramirkhani et al., 2018; Xia et al., 2021), we design the following feature set reflecting the intrinsic value of identifiers, which applies to all the asset classes studied in this work.

-

•

Length: the length of the asset name in character.

-

•

Suffix: the asset suffix, represented by a one-hot vector.

-

•

Character: four binary features indicating (i) whether the asset name only contains alphabet letters, (ii) whether the asset name contains hyphens, (iii), whether all the characters in the asset name are numeric, and (iv) whether the asset name contains non-ASCII characters, respectively.

-

•

Number of tokens: we tokenize the asset name using morphological analysis (Virpioja et al., 2013) and consider the number of tokens as a feature.

-

•

Vocabulary: two binary features indicating (i) whether the asset name is a word and (ii) whether the asset name is an adult word, respectively.

-

•

Trademark: a binary feature indicating if the asset name appears in any trademark applications.

-

•

Top-level domain (TLD) count: the number of TLDs where the asset name is registered.

4.3. Neural Models

4.3.1. Vanilla mBERT

We follow the framework of fine-tuning a pre-trained high-capacity language model (Radford et al., 2018) and use multilingual BERT (mBERT) (Devlin et al., 2019) as the pre-trained model. Given an asset, we concatenate the name and suffix of the asset with the classification token [CLS] and separator token [SEP] in mBERT as the input sequence [CLS][SEP][SEP] to mBERT, with a linear layer on top of the final hidden state for [CLS] in the input sequence.

4.3.2. mBERT

We improve vanilla mBERT in two effective yet easy-to-implement ways:

-

(i)

Since transaction data is time sensitive, we propose a two-stage fine-tuning approach to highlight the relatively new transactions during training. Specifically, in the first stage, we first fine-tune the pre-trained mBERT on all transactions in . We then fine-tune the resulting model again in the second stage on the newest transactions in .

-

(ii)

We propose a modification to the input sequence of Vanilla mBERT to leverage external knowledge that helps approximate the popularity of the asset name but is not readily available in the pre-trained representation. Concretely, the modified input sequence is [CLS][SEP][SEP][SEP], where is a string of digits representing the TLD count (defined in Section 4.2).

5. Experiments and Discussions

5.1. Implementation Details

5.1.1. Feature Extraction

We employ Polyglot555https://github.com/aboSamoor/polyglot for morphological analysis. For vocabulary feature extraction, we use the vocabulary of GloVe.840B.300D (Pennington et al., 2014) and a self-collected adult word list666We will release the adult word list along with the code.. We look up trademark applications from April 1884 to December 2018 released by the United States Patent and Trademark Office. We leverage the DNS Census 2013 777https://archive.org/details/DNSCensus2013 to obtain TLD count.

5.1.2. Non-Neural Models

5.1.3. Neural Models

We implement vanilla mBERT and mBERT based on Transformers (Wolf et al., 2020). We use the multilingual uncased BERT-Base released by (Devlin et al., 2019). For vanilla mBERT, we fine-tune for three epochs. As for mBERT, we set to and fine-tune for one epoch in the first fine-tuning stage and three epochs in the second fine-tuning stage. We set the learning rate and batch size to and , respectively. All unspecified hyperparameters take the default values (Devlin et al., 2019).

5.2. Main Results

We report in Table 3 the performance of all models introduced in Section 4. XGBoost consistently performs the best among conventional feature-based models across all subsets of DASH. Vanilla mBERT, which does not leverage any handcrafted features or explicit expert knowledge, outperforms AdaBoost and random forest in average performance, showing the potential of language model fine-tuning for digital asset valuation. We see a significant reduction in MSLE relative to vanilla mBERT when employing the proposed improvements. Compared with XGBoost, the improved model mBERT substantially reduces the MSLE by (i.e., vs. ) on average on the test set of DASH ().

To measure the contribution of different components, we conduct ablation tests, where we remove one component from XGBoost or mBERT at a time. As shown in Table 4, the suffix, TLD count, and length features contribute the most to the performance of XGBoost. Every component of mBERT heavily impacts the overall performance. Specifically, compared with a single-stage fine-tuning on the entire (resp. the most recent portion of) training data, the two-stage fine-tuning reduces the MSLE by (resp. ) on average. Incorporating TLD count in the input sequence contributes to an average decrease of in MSLE. Furthermore, the MSLE increases by on average if we replace the pre-trained mBERT weights with randomly initialized weights.

5.3. Error Analysis

We perform an error analysis of XGBoost, vanilla mBERT, and mBERT on the development set to understand their difference and identify their limitations.

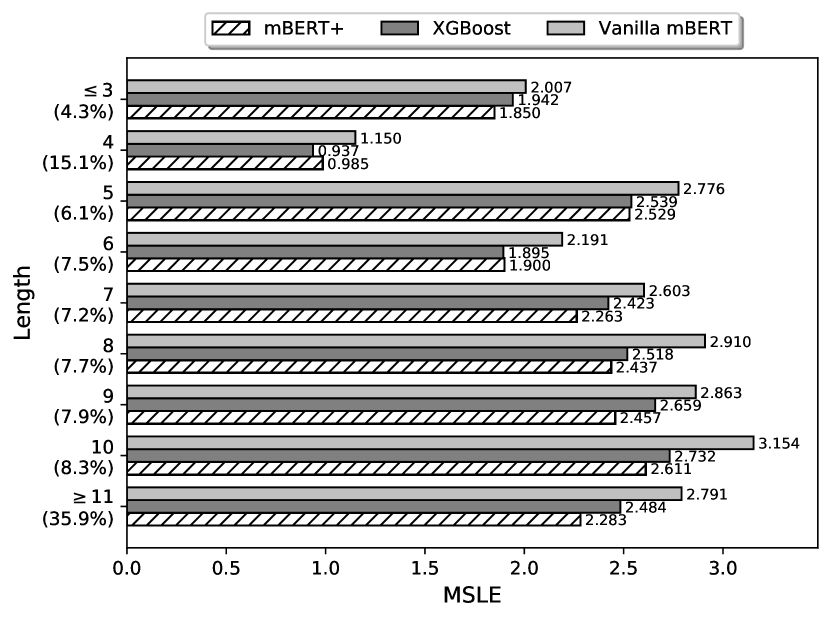

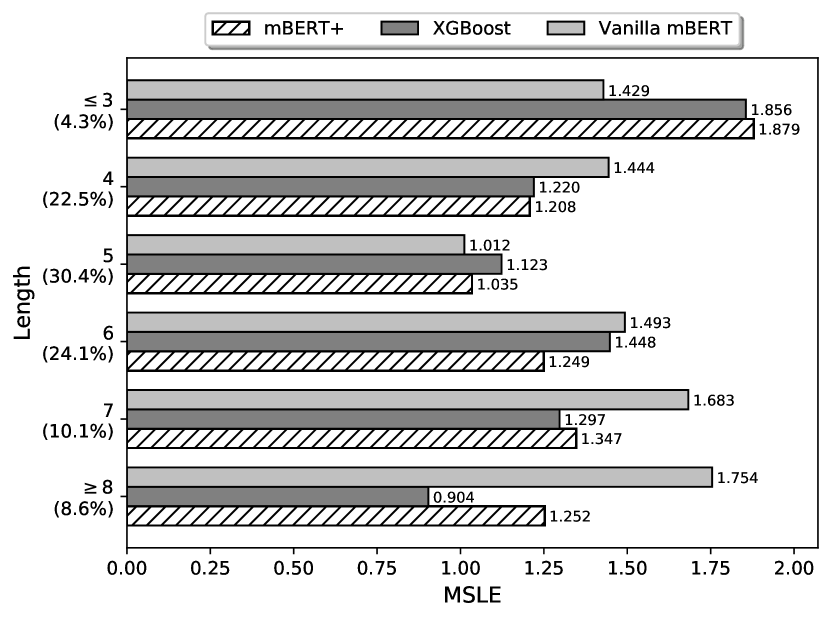

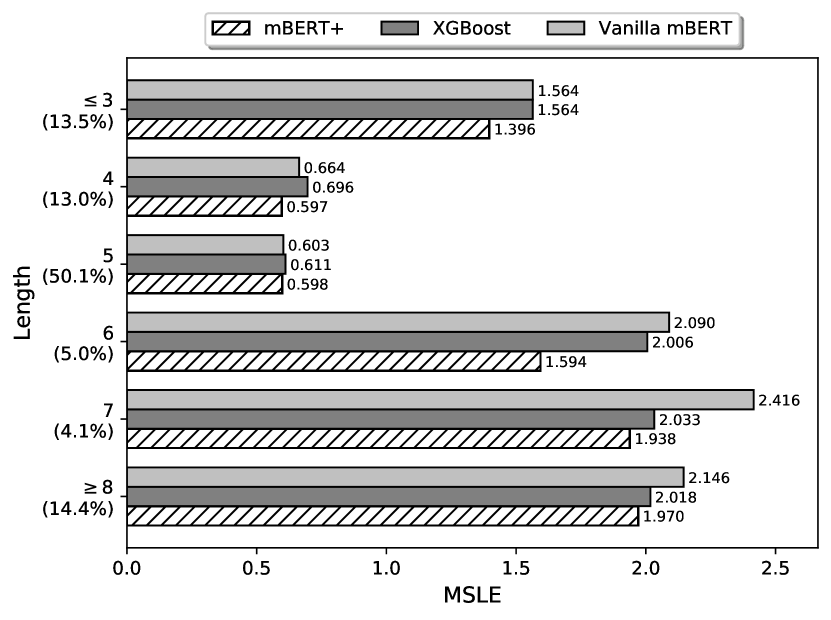

5.3.1. Name Length

We report the model performance with respect to different name length groups in Figure 2. We observe a clear difference in performance over different name length groups for all asset classes. Notably, all models for DASHDN and DASHNFT can give relatively accurate predictions when given an asset of name length four, and all models for DASHEA and DASHNFT perform relatively well when given an asset of name length five. XGBoost demonstrates a notable advantage over the other models in valuing email addresses longer than seven.

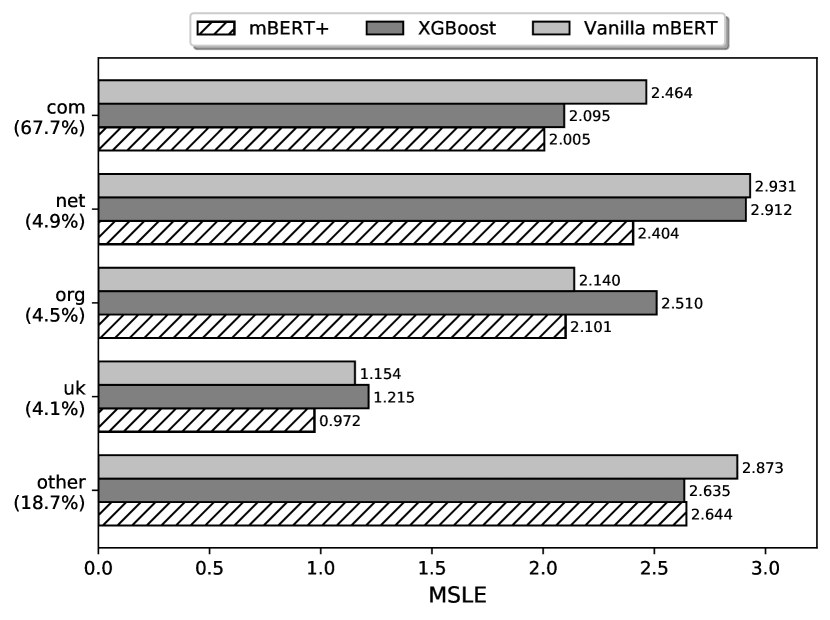

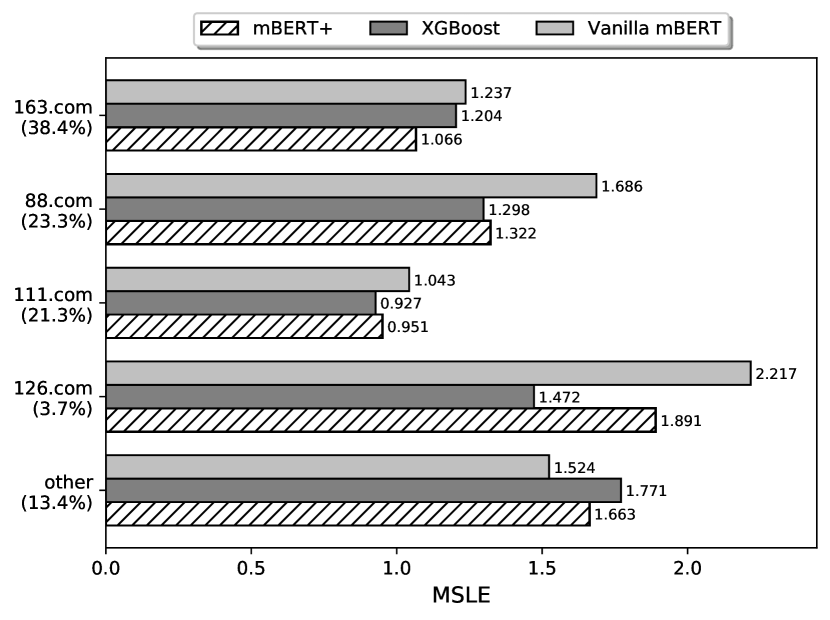

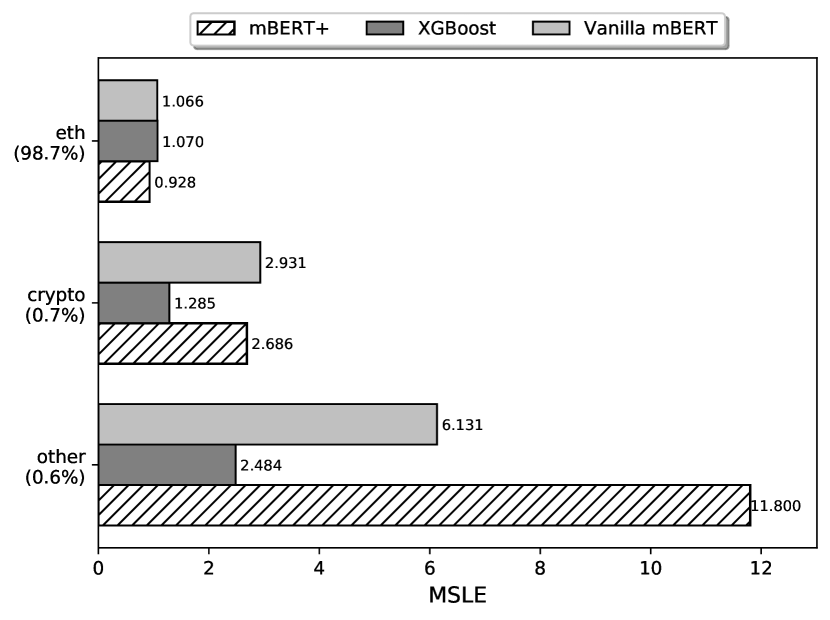

5.3.2. Suffix

We compare in Figure 3 the model performance for different suffixes. While, unsurprisingly, uncommon suffixes that fall under the “other” groups are relatively hard to assess for all asset classes, perhaps surprisingly, models perform worse than average on some common suffixes, including “net” in DASHDN and “126.com” in DASHEA. Although mBERT achieves the lowest MSLE in most groups, XGBoost considerably outperforms mBERT in a few groups, such as “other” in DASHNFT.

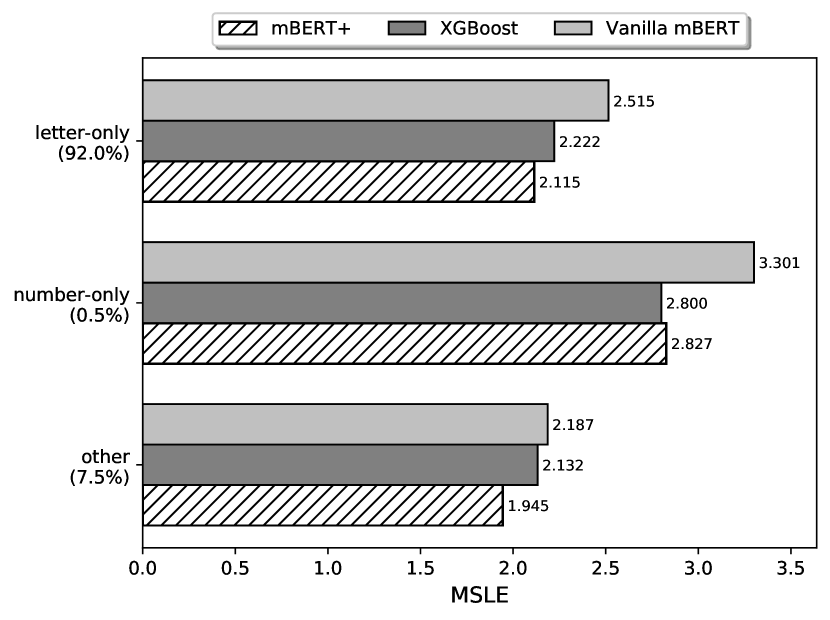

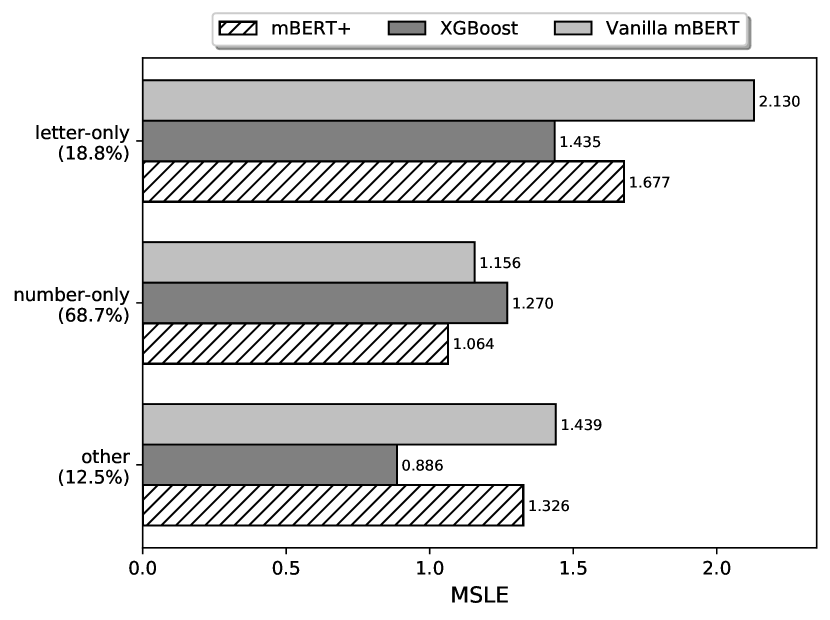

5.3.3. Name Character Set

We present the model performance grouped by the character set of the asset name in Figure 4. Interestingly, the relative difficulty in valuing number-only names varies greatly across asset classes. Besides, for all models and all asset classes, the appraisal of letter-only names is more challenging compared with names that fall into the “other” groups. XGBoost once again outperforms mBERT in several groups.

5.4. Further Discussions

5.4.1. Model Ensemble

Since the error analysis in Section 5.3 indicates XGBoost and mBERT are complementary in many aspects, we combine them by taking the geometric mean of their predictions. As shown in Table 5, the ensemble model achieves an MSLE reduction of on average compared with mBERT.

| Dev | Test | |

|---|---|---|

| DASHDN | (0.035) | (0.052) |

| DASHEA | (0.118) | (0.117) |

| DASHNFT | (0.066) | (0.085) |

| Average | (0.073) | (0.085) |

5.4.2. Pre-Trained Language Models

We study the impact of different pre-trained language models on the performance of neural models. We choose the following language models for comparison: English uncased BERT-Base (Devlin et al., 2019) (BERT), XLM-R-Base (Conneau et al., 2020) (XLM-R), and FNet-Base (Lee-Thorp et al., 2022) (FNet). We denote the vanilla fine-tuned model and the improved model with the pre-trained language model replaced by as vanilla and , respectively. To minimize time leakage risk, we report the performance on DASHNFT whose transactions in the development and test sets all happen after the release dates of the employed language models. As shown in Table 6, our improved model consistently outperforms the corresponding vanilla model regardless of the pre-trained language model used. Surprisingly, the relative strength of these pre-trained models differs dramatically between natural language understanding and digital asset valuation: XLM-R does not outperform mBERT in asset valuation, though XLM-R is superior to mBERT in multilingual natural language processing (Conneau et al., 2020); similarly, BERT does not outperform FNet, though FNet sacrifices some performance for speed compared with BERT (Lee-Thorp et al., 2022). Moreover, we find that monolingual pre-trained LMs can achieve performance close to multilingual pre-trained LMs (e.g., FNet vs. mBERT).

| Dev | Test | |

|---|---|---|

| Vanilla mBERT | ||

| Vanilla BERT | ||

| Vanilla XLM-R | ||

| Vanilla FNet | ||

| mBERT | ||

| BERT | ||

| XLM-R | ||

| FNet |

5.4.3. Non-Uniform Sample Weights

Motivated by the effectiveness of the proposed two-stage fine-tuning approach, we investigate whether we can improve the conventional model by emphasizing more on the relatively new transactions during training as well. We present the experimental results in Table 7, where we set the sample weights of the newest transactions to be two times the weights of the other transactions in the training data. We observe no substantial difference in average performance between XGBoost with and without non-uniform sample weights.

| Dev | Test | |

|---|---|---|

| DASHDN | (0.019) | (0.009) |

| DASHEA | (0.029) | (0.021) |

| DASHNFT | (0.011) | (0.021) |

| Average | (0.000) | (0.003) |

5.4.4. Comparison with a Commercial Model

We compare our models with GoValue, a state-of-the-art proprietary automated domain valuation tool from the industry (Section 2.2). Because (i) GoValue only gives the valuation result when the estimated price is between USD and USD, (ii) GoValue supports valuing neither internationalized domain names (IDNs) nor third-level domain names, and (iii) GoValue does not support bulk appraisal and has a limited query quota, we use a modified setting for the experiment, specified in the following.

-

•

We randomly sample from the test set of DASHDN transactions, in which the domain name is neither an IDN nor a third-level domain name, and the price is between USD and USD.

-

•

We call GoValue and our models to predict the price of every domain name in the samples. If the predicted price is below (resp. above ) USD, we change the prediction to (resp. ).

As shown in Table 8, all our conventional feature-based models and neural models significantly outperform GoValue by a large margin (). Note that although the result is highly suggestive of the superiority of our models, the result may not be conclusive enough because the comparison is arguably unfair for both GoValue and our models. Specifically, on the one hand, GoValue leverages unrivaled amounts of data available only to GoDaddy for model training; on the other hand, the distribution of the test samples is likely closer to that of the training set of DASHDN compared with GoValue’s training data. Nevertheless, the comparison can hardly be improved due to a lack of access to both the modeling details and training data of GoValue.

| MSLE | |

|---|---|

| GoValue | |

| AdaBoost | |

| Random Forest | |

| XGBoost | |

| Vanilla mBERT | |

| mBERT |

5.5. Limitations and Future Work

The data and models presented in this work focus on digital assets represented in texts without touching other modalities (e.g., images). Nevertheless, such a uniform representation makes our work a reasonably suitable starting point for studying general techniques that apply to multiple asset classes. We leave the study of valuing assets represented in other modalities for future work.

We are aware of some proprietary external knowledge sources (e.g., Google Trends888https://trends.google.com/) that contain potentially additional useful knowledge for building more accurate valuation models. However, we choose not to employ them in this paper to avoid dependence on proprietary business services and leave the study of leveraging them for future research. While this choice limits the best performance our models can attain, we believe it does not influence the main contributions of this paper and helps improve the accessibility and reproducibility of this work.

6. Conclusion

We present DASH, the first digital asset sales history dataset featuring multiple asset classes, including domain names, email addresses, and NFTs. We propose several valuation models for DASH, including conventional feature-based models and deep learning models, all applicable to multiple asset classes. We conduct comprehensive experiments to evaluate the proposed models on DASH and, for the first time, demonstrate that fine-tuning a pre-trained model can beat conventional models in digital asset valuation.

References

- (1)

- Bikadi et al. (2017) Zsolt Bikadi, Sapumal Ahangama, and Eszter Hazai. 2017. Prediction of Domain Values: High throughput screening of domain names using Support Vector Machines. arXiv preprint cs.CY/1707.00906 (2017). https://doi.org/10.48550/ARXIV.1707.00906

- Chen and Guestrin (2016) Tianqi Chen and Carlos Guestrin. 2016. XGBoost: A Scalable Tree Boosting System. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (San Francisco, California, USA) (KDD ’16). Association for Computing Machinery, New York, NY, USA, 785–794. https://doi.org/10.1145/2939672.2939785

- Conneau et al. (2020) Alexis Conneau, Kartikay Khandelwal, Naman Goyal, Vishrav Chaudhary, Guillaume Wenzek, Francisco Guzmán, Edouard Grave, Myle Ott, Luke Zettlemoyer, and Veselin Stoyanov. 2020. Unsupervised Cross-lingual Representation Learning at Scale. In Proceedings of the 58th Annual Meeting of the Association for Computational Linguistics. Association for Computational Linguistics, Online, 8440–8451. https://doi.org/10.18653/v1/2020.acl-main.747

- Deli̇baş (2019) Emrullah Deli̇baş. 2019. Domain Name Valuation: Characteristics & Price Exposed! Master’s thesis. Istanbul Şehir University.

- Devlin et al. (2019) Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. 2019. BERT: Pre-training of Deep Bidirectional Transformers for Language Understanding. In Proceedings of the 2019 Conference of the North American Chapter of the Association for Computational Linguistics: Human Language Technologies, Volume 1 (Long and Short Papers). Association for Computational Linguistics, Minneapolis, Minnesota, 4171–4186. https://doi.org/10.18653/v1/N19-1423

- Dieterle and Bergmann (2014) Sebastian Dieterle and Ralph Bergmann. 2014. A Hybrid CBR-ANN Approach to the Appraisal of Internet Domain Names. In Case-Based Reasoning Research and Development, Luc Lamontagne and Enric Plaza (Eds.). Springer International Publishing, Cham, 95–109. https://doi.org/10.1007/978-3-319-11209-1_8

- Dutta et al. (2020) Aniruddha Dutta, Saket Kumar, and Meheli Basu. 2020. A Gated Recurrent Unit Approach to Bitcoin Price Prediction. Journal of Risk and Financial Management 13, 2 (2020). https://doi.org/10.3390/jrfm13020023

- Freund and Schapire (1995) Yoav Freund and Robert E. Schapire. 1995. A desicion-theoretic generalization of on-line learning and an application to boosting. In Computational Learning Theory, Paul Vitányi (Ed.). Springer Berlin Heidelberg, Berlin, Heidelberg, 23–37. https://doi.org/10.1007/3-540-59119-2_166

- Jain et al. (2022) Shrey Jain, Camille Bruckmann, and Chase McDougall. 2022. NFT Appraisal Prediction: Utilizing Search Trends, Public Market Data, Linear Regression and Recurrent Neural Networks. arXiv preprint q-fin.ST/2204.12932 (2022). https://doi.org/10.48550/ARXIV.2204.12932

- Kapoor et al. (2022) Arnav Kapoor, Dipanwita Guhathakurta, Mehul Mathur, Rupanshu Yadav, Manish Gupta, and Ponnurangam Kumaraguru. 2022. TweetBoost: Influence of Social Media on NFT Valuation. In Companion Proceedings of the Web Conference 2022 (Virtual Event, Lyon, France) (WWW ’22). Association for Computing Machinery, New York, NY, USA, 621–629. https://doi.org/10.1145/3487553.3524642

- Lee-Thorp et al. (2022) James Lee-Thorp, Joshua Ainslie, Ilya Eckstein, and Santiago Ontanon. 2022. FNet: Mixing Tokens with Fourier Transforms. In Proceedings of the 2022 Conference of the North American Chapter of the Association for Computational Linguistics: Human Language Technologies. Association for Computational Linguistics, Seattle, United States, 4296–4313. https://doi.org/10.18653/v1/2022.naacl-main.319

- Lindenthal (2014) Thies Lindenthal. 2014. Valuable words: The price dynamics of internet domain names. Journal of the Association for Information Science and Technology 65, 5 (2014), 869–881. https://doi.org/10.1002/asi.23012

- Liu et al. (2019) Jian Liu, Xiangdong Zeng, Adam Ghandar, and Georgios Theodoropoulos. 2019. Data Driven Domain Appraisal: Extracting Information from Short Dense Texts. In 2019 IEEE Symposium Series on Computational Intelligence (SSCI). 2489–2496. https://doi.org/10.1109/SSCI44817.2019.9002904

- Mekacher et al. (2022) Amin Mekacher, Alberto Bracci, Matthieu Nadini, Mauro Martino, Laura Alessandretti, Luca Maria Aiello, and Andrea Baronchelli. 2022. Heterogeneous rarity patterns drive price dynamics in NFT collections. Scientific Reports 12, 1 (16 Aug 2022), 13890. https://doi.org/10.1038/s41598-022-17922-5

- Meystedt (2015) Aron Meystedt. 2015. What is my URL worth? Placing a value on premium domain names. Valuation Strategies 19, 2 (2015), 10–17,48.

- Miramirkhani et al. (2018) Najmeh Miramirkhani, Timothy Barron, Michael Ferdman, and Nick Nikiforakis. 2018. Panning for Gold.Com: Understanding the Dynamics of Domain Dropcatching. In Proceedings of the 2018 World Wide Web Conference (Lyon, France) (WWW ’18). International World Wide Web Conferences Steering Committee, Republic and Canton of Geneva, CHE, 257–266. https://doi.org/10.1145/3178876.3186092

- Nadini et al. (2021) Matthieu Nadini, Laura Alessandretti, Flavio Di Giacinto, Mauro Martino, Luca Maria Aiello, and Andrea Baronchelli. 2021. Mapping the NFT revolution: market trends, trade networks, and visual features. Scientific Reports 11, 1 (22 Oct 2021), 20902. https://doi.org/10.1038/s41598-021-00053-8

- Nguyen (2001) Xuan-Thao Nguyen. 2001. Cyberproperty and Judicial Dissonance: The Trouble with Domain Name Classification. George Mason Law Review 10, 2 (2001), 183–214.

- Pedregosa et al. (2011) Fabian Pedregosa, Gaël Varoquaux, Alexandre Gramfort, Vincent Michel, Bertrand Thirion, Olivier Grisel, Mathieu Blondel, Peter Prettenhofer, Ron Weiss, Vincent Dubourg, Jake Vanderplas, Alexandre Passos, David Cournapeau, Matthieu Brucher, Matthieu Perrot, and Édouard Duchesnay. 2011. Scikit-learn: Machine Learning in Python. Journal of Machine Learning Research 12, 85 (2011), 2825–2830.

- Pennington et al. (2014) Jeffrey Pennington, Richard Socher, and Christopher Manning. 2014. GloVe: Global Vectors for Word Representation. In Proceedings of the 2014 Conference on Empirical Methods in Natural Language Processing (EMNLP). Association for Computational Linguistics, Doha, Qatar, 1532–1543. https://doi.org/10.3115/v1/D14-1162

- Polu and Sutskever (2020) Stanislas Polu and Ilya Sutskever. 2020. Generative Language Modeling for Automated Theorem Proving. arXiv preprint cs.LG/2009.03393 (2020). https://doi.org/10.48550/ARXIV.2009.03393

- Radford et al. (2018) Alec Radford, Karthik Narasimhan, Tim Salimans, and Ilya Sutskever. 2018. Improving Language Understanding by Generative Pre-Training. Technical Report.

- Stöckl (2021) Andreas Stöckl. 2021. Watching a Language Model Learning Chess. In Proceedings of the International Conference on Recent Advances in Natural Language Processing (RANLP 2021). INCOMA Ltd., Held Online, 1369–1379.

- Tang et al. (2014) Jih Hsin Tang, Min Chu Hsu, Ting Yuan Hu, and Hsing-Hua Huang. 2014. A general domain name appraisal model. Journal of Internet Technology 15, 3 (1 May 2014), 427–431. https://doi.org/10.6138/JIT.2014.15.3.11

- Virpioja et al. (2013) Sami Virpioja, Peter Smit, Stig-Arne Grönroos, and Mikko Kurimo. 2013. Morfessor 2.0: Python Implementation and Extensions for Morfessor Baseline. Technical Report. 38 pages.

- Visconti (2020) Roberto Moro Visconti. 2020. The Valuation of Digital Intangibles: Technology, Marketing and Internet. Palgrave Macmillan Cham. https://doi.org/10.1007/978-3-030-36918-7

- Wolf et al. (2020) Thomas Wolf, Lysandre Debut, Victor Sanh, Julien Chaumond, Clement Delangue, Anthony Moi, Pierric Cistac, Tim Rault, Remi Louf, Morgan Funtowicz, Joe Davison, Sam Shleifer, Patrick von Platen, Clara Ma, Yacine Jernite, Julien Plu, Canwen Xu, Teven Le Scao, Sylvain Gugger, Mariama Drame, Quentin Lhoest, and Alexander Rush. 2020. Transformers: State-of-the-Art Natural Language Processing. In Proceedings of the 2020 Conference on Empirical Methods in Natural Language Processing: System Demonstrations. Association for Computational Linguistics, Online, 38–45. https://doi.org/10.18653/v1/2020.emnlp-demos.6

- Wu and He (2009) Zu-guang Wu and Hai-yi He. 2009. Domain Name Valuation Model Constructing and Emperical Evidence. In 2009 International Conference on Multimedia Information Networking and Security, Vol. 2. 201–204. https://doi.org/10.1109/MINES.2009.153

- Wu et al. (2009) Zu-guang Wu, Guo-hua Zhu, Rui Huang, and Bin Xia. 2009. Domain Name Valuation Model Based on Semantic Theory and Content Analysis. In 2009 Asia-Pacific Conference on Information Processing, Vol. 2. 237–240. https://doi.org/10.1109/APCIP.2009.194

- Xia et al. (2021) Pengcheng Xia, Haoyu Wang, Zhou Yu, Xinyu Liu, Xiapu Luo, and Guoai Xu. 2021. Ethereum Name Service: the Good, the Bad, and the Ugly. arXiv preprint cs.CR/2104.05185 (2021). https://doi.org/10.48550/ARXIV.2104.05185