Solving Feynman-Kac Forward Backward SDEs Using McKean-Markov Branched Sampling

Abstract

We propose a new method for the numerical solution of the forward-backward stochastic differential equations (FBSDE) appearing in the Feynman-Kac representation of the value function in stochastic optimal control problems. Using Girsanov’s change of probability measures, it is demonstrated how a McKean-Markov branched sampling method can be utilized for the forward integration pass, as long as the controlled drift term is appropriately compensated in the backward integration pass. Subsequently, a numerical approximation of the value function is proposed by solving a series of function approximation problems backwards in time along the edges of a space-filling tree consisting of trajectory samples. Moreover, a local entropy-weighted least squares Monte Carlo (LSMC) method is developed to concentrate function approximation accuracy in regions most likely to be visited by optimally controlled trajectories. The proposed methodology is numerically demonstrated on linear and nonlinear stochastic optimal control problems with non-quadratic running costs, which reveal significant convergence improvements over previous FBSDE-based numerical solution methods.

Index Terms:

Least mean square methods, Monte Carlo methods, Nonlinear control systems, Optimal control, Partial differential equations, Stochastic processes, Trajectory optimization, Tree graphsI Introduction

The Feynman-Kac representation theorem establishes the intrinsic relationship between the solution of a broad class of second-order parabolic and elliptic partial differential equations (PDEs) to the solution of forward-backward stochastic differential equations (FBSDEs) (see, e.g., [1, Chapter 7]). Investigations over these FBSDEs were brought to prominence in [2, 3, 4], and they have been gaining traction as a framework to solve stochastic nonlinear control problems, including optimal control problems with quadratic cost [5], minimum-fuel (-running cost) problems [6], differential games [7, 8], and reachability problems [5, 9]. FBSDE-based numerical methods have also received interest from the mathematical finance community [10, 11, 12]. This is due to that fact that the Hamilton-Jacobi-Bellman (HJB) second order PDE appearing in stochastic optimal control can be solved via FBSDE methods with general nonlinear dynamics and costs. Although initial results demonstrate promise in terms of flexibility and theoretical validity, numerical algorithms which leverage this theory have not yet matured. For even modest problems, state-of-the-art algorithms often have issues with slow and unstable convergence to the optimal policy. Producing more robust numerical methods is critical for the broader adoption of FBSDE methods for real-world tasks.

FBSDE numerical solution methods broadly consist of two steps, a forward pass, which generates Monte Carlo samples of the forward stochastic process, and a backward pass, which iteratively approximates the value function backwards in time. Typically, FBSDE methods perform this approximation using a least-squares Monte Carlo (LSMC) scheme, which implicitly solves the backward SDE using parametric function approximation [11]. The approximate value function fit in the backward pass is then used to improve sampling in an updated forward pass, leading to an iterative algorithm which, ideally, improves the approximation, till convergence. Although FBSDE methods share a distinct similarity to differential dynamic programming (DDP) techniques [13, 14, 15], as they also involve forward and backward passes, the latter are, in general, less flexible. For most DDP applications a strictly positive definite running cost with respect to the control is required for convergence [16, Section 2.2.3]. Furthermore, in DDP the computation of first and second order derivatives of both the dynamics and the cost is necessary for the backward pass, making it challenging to apply this approach to problems where these derivatives cannot be computed analytically. In contrast, FBSDE techniques only require a good fit of the value function and the evaluation of its gradient.

A key feature of FBSDE methods is their ability to generate a parametric model for the value function over the entire time horizon which, in turn, can be used for the evaluation and assessment of the performance of closed-loop control policies. This feature differentiates both FBSDE and DDP methods from model predictive control (MPC) methods [17], which, in general, only produce the current-best optimal control signal, re-evaluated at every time step [18].

FBSDE methods provide an alternative to grid-based methods for solving PDEs, typically utilizing finite-difference, finite-element, or level-set schemes, which are known to scale poorly in high dimensional state spaces (). There is also ample research into the development of meshless methods for solving PDEs, such as radial basis function (RBF) collocation and RBF-finite difference (RBF-FD) formulations [19]. FBSDE methods share significant similarities with these methods, in the sense that the value function is approximated by solving the PDE over an unstructured set of collocation points. The primary drawback of RBF methods is that they do not offer an efficient method for choosing the collocation points, and since it is difficult to know a priori what the best points are, point selection might regress into a grid-based method. Specifically, sufficiently broad and dense sampling of a high-dimensional state space might require roughly the same number of collocation points as a grid-based method to be well-conditioned and to produce a quality estimate of the value function [20].

While Feynman-Kac-based FBSDE methods produce an unbiased estimator for the value function associated with HJB equations, a naïve application of the theory leads to estimators with high variance by producing sample trajectories away from the optimal one. Recent work has shown that Girsanov’s change of probability measures can be employed to make changes to the sampling in the forward pass without adding intrinsic bias to the estimator [5, 6, 8]. In other words, the drift appearing in the forward SDE as a consequence of the change of the probability measure can be employed to modify the sampling in the forward pass; this, in turn, requires appropriate accommodation for the change of measure and the associated conditional expectations in the backward pass.

In this work we expand upon the above ideas and invoke Girsanov’s theorem for Feynman-Kac FBSDEs in a broader setting than that of [5, 6, 8] and show that the forward sampling measure can be modified at will; this enables us to incorporate methods from other domains, namely, rapidly-exploring random trees (RRTs) (see, e.g., [21] and the recent survey in [22]), in order to more efficiently explore the state space during the forward pass. RRTs are frequently applied to reachability-type motion planning problems, by biasing the samples towards regions of the state space that have low density. Using RRTs in the forward sampling allows us to spread samples evenly over the reachable state space, increasing the likelihood that near-optimal samples are well-represented in the forward pass sample distribution. By sampling more efficiently and relying less on incremental approximations of the value function to guide our search, we can achieve faster and more robust convergence than previous FBSDE methods. In the backward pass, we take advantage of the path-integrated running costs and the estimates of the value function to produce a heuristic which weighs paths according to a local-entropy measure-theoretic optimization. Although local-entropy path integral theory and RRTs have been used together in [23], the method of this article is more closely related to the path-integral approach to control [14]. Our method, similarly, performs forward passes to broadly sample the state space, but, in contrast to [23], it follows each forward pass with a backward pass to obtain an approximation of the value function, and, consequently, obtain a closed-loop policy over the full horizon.

The primary contributions of this paper are as follows:

-

•

Providing the theoretical basis for the use of McKean-Markov branched sampling in the forward pass of FBSDE techniques.

-

•

Introducing an RRT-inspired algorithm for sampling the forward SDE.

-

•

Presenting a technique for concentrating value function approximation accuracy in regions containing optimal trajectories.

-

•

Proposing an iterative numerical method for the purpose of approximating the optimal value function and its policy.

This paper expands upon the authors’ prior work in [24], by: first, providing missing proofs and adding the details for proving all for stated theorems; second, providing a comprehensive discussion of the proposed algorithm; and third, by providing additional examples that further illustrate the theory and motivate the design choices of the proposed work.

The structure of the paper is as follows. Section II presents the stochastic optimal control (SOC) problem formulation, the on-policy value function representation, and the associated family of Hamilton-Jacobi equations. Next, Section III introduces a constructive series of alternative representations of the value function, first as the solution of “on-policy” FBSDEs which arise from the Feynman-Kac theorem, then as the solution of “off-policy” FBSDEs which arise from the application of Girsanov’s theorem, and finally as the minimizer of a local-entropy weighted optimization problem over the off-policy FBSDE distribution. Section IV discusses branched forward SDE sampling and its novel interpretation as a discrete approximation of the continuous-time theory of Section III. In Section V we propose the method of forward-backward rapidly exploring random trees for solving SDEs (FBRRT-SDE), a particular implementation of the representation introduced in Section IV. Finally, in Section VI we apply FBRRT-SDE to three problems and demonstrate its ability to solve nonlinear stochastic optimal control problems with non-quadratic running costs.

II Hamilton-Jacobi Equation and

On-Policy Value Function

In this section, we briefly introduce the stochastic optimal control (SOC) problem under consideration and its associated optimal value function, as well as the on-policy value function and its associated Hamilton-Jacobi PDE. Given an initial time and a complete filtered probability space on which the -dimensional standard Brownian (Wiener) process is defined, consider a stochastic system with dynamics governed by

| (1) |

over the interval , where is an -valued, progressively measurable state process on the interval , is a progressively measurable input process on the same interval taking values in the compact set , and , are the Markovian drift and diffusion functions, respectively.

For each , the cost over the time interval associated with a given control signal is

| (2) |

where is the running cost, and is the terminal cost. The stochastic optimal control (SOC) problem is to determine, given , the optimal value function , defined as

| (SOC) |

where is a set of admissible control processes satisfying the conditions described in the beginning of [1, Chapter 4, Section 3]. Among these conditions, must be progressively measurable, the SDE (1) must admit a unique solution under the control , and must be integrable.

Consider the HJB PDE [1, Chapter 7, (4.18)]

| (HJB) |

where,

| (3) |

and where is the partial derivative with respect to , is the gradient with respect to state , and is the Hessian with respect to state .

Assumption 1.

We assume that the following conditions hold for the problem data.

-

i)

are uniformly continuous, Lipschitz in , for all .

-

ii)

has sublinear growth in and has polynomial growth in .

-

iii)

exists and is bounded.

Under Assumption 1, there exists a unique viscosity solution to (HJB), there exists a unique weak solution to (1) under each admissible control process , and the viscosity solution has the representation (SOC) [1, Chapter 7, Theorem 4.4].

In addition to the optimal value function , we also seek to find an optimal feedback control policy . According to [1, Chapter 5, Definition 6.1], we define an admissible feedback control policy as a measurable function for which the SDE

| (4) |

has a weak solution. Due to the boundedness of , there exists an optimal feedback control policy , which satisfies

| (5) |

with the verification property that [1, Chapter 5, Theorem 6.6].

In this paper, instead of a direct solution of (HJB), we work with a class of arbitrary control policies and their associated “on-policy” value functions , and we use iterative methods to approximate and . We allow more general policies of the form , that is, is now a function of not only the state but also on an auxiliary variable .

The Hamilton-Jacobi (HJ) PDE for the on-policy value function corresponding to the policy is given by

| (HJ) |

where,

| (6) |

Assumption 2.

We will assume that is chosen such that the function in (6) satisfies the following properties:

-

i)

is uniformly continuous in , Lipschitz in .

-

ii)

has polynomial growth in .

Under Assumptions 1 and Assumption 2, (HJ) admits a unique viscosity solution [1, Chapter 7, Theorem 4.5]. However, for the ease of presentation henceforth we will impose additional regularity assumptions for the solutions of (HJ).

Assumption 3.

The PDE (HJ) admits a classical solution, that is, is continuously differentiable in , and twice continuously differentiable in .

Remark II.1.

Assumption 3 is rather strong for many optimal control problems. For a set of sufficient conditions for Assumption 3 to hold, one might refer, e.g., to [1, Chapter 7, Theorem 5.5] and [25, Chapter 4, Theorem 4.2, Theorem 4.4]. However, it is well-known that viscosity solutions can be approximated closely by classical solutions (see, for example, [1, Section 5.2]). Subsequently, our approach provides a numerical approximation of a wide class of optimal control problems, even ones that admit a unique viscosity solution. The numerical examples in Section VI demonstrate this claim.

In our approach, we use the continuous function to characterize the policy’s auxilary variable , henceforth letting . For notational conciseness we will further denote and . As it will be shown in Section III-B, under Assumptions 1-3, the classical solution of (HJ) has the interpretation

| (7) |

where satisfies the SDE

| (8) |

Also, in Section III-B we revisit the case of non-classical viscosity solutions, demonstrating that this interpretation is still valid under certain modifications.

III Feynman-Kac-Girsanov FBSDE Representation

III-A Off-Policy Drifted FBSDEs

In language originating from reinforcement learning, an “on-policy” method learns a value function from trajectory samples generated by following the same policy , whereas “off-policy” methods learn from trajectory samples generated by following a different policy [26]. Off-policy methods are generally more desirable because disentangling the sampling distribution from the target value function being learned allows for broader exploration and thus more rapid convergence to the optimal value function. Following this language, in stochastic control an “on-policy” method would sample from the FSDE (4) with drift to learn , but an “off-policy” method would sample from a different FSDE to learn . In this section we present an off-policy stochastic control method for representing . The on-policy version of the theory then arises naturally from a particular specialization.

The off-policy method utilizes the connection between the solution of a pair of FBSDEs and the on-policy value function solving (HJ). We first introduce a class of off-policy FBSDEs, and then provide a theorem establishing their connection to . We call this class of FBSDEs off-policy because the drift term of the FSDE is a random process that can be chosen at will.

As before, let be a complete, filtered probability space, and let be a Brownian process in the measure . Denote , and similarly for , and let refer to the expectation taken in the probability measure . Further, let be an arbitrary -progressively measurable process such that satisfies Novikov’s criterion ()[27, Lemma 9]. We call the pair of FBSDEs

| (9) | ||||||

| (10) |

where,

| (11) |

the off-policy drifted FBSDEs for the target policy and drift process . A solution to (9)-(10) is the triple of -adapted processes for which satisfies the FSDE (9) and satisfy the BSDE (10).

Theorem III.1.

Let Assumptions 1-3 hold, and let be a classical solution of (HJ). Assume is chosen such that (9) admits a unique square-integrable solution (i.e., it satisfies the properties of [1, Chapter 1, Theorem 6.16]) and satisfies Novikov’s criterion. Then, there exists a solution to the BSDE (9), and it holds that

| (12) | |||||

| (13) |

-a.s., and, in particular,

| (14) |

where,

| (15) |

Proof.

Since (9) has a square-integrable solution, there exists a solution to (10) which is unique and square-integrable because is Lipschitz in [1, Chapter 7, Theorem 3.2]. Girsanov’s theorem (see, e.g. [27, Theorem 10]) indicates that if we construct the measure from via the Radon-Nikodym derivative

| (16) |

where,

| (17) |

then the process

| (18) |

is Brownian in the newly constructed measure . A further consequence of Girsanov’s theorem (see e.g., [28, Chapter 5, Theorem 10.1]) is illustrated, through an abuse of notation, by substituting the relationship into the equations (9) and (10). Performing this substitution yields that the solution to (9-10) with the -Brownian process also solves the zero-drift FBSDE

| (19) | |||||

| (20) | |||||

with -Brownian .

Under Assumptions 1-2, [1, Chapter 7, Theorem 4.5] it follows that there exists a unique solution to the FBSDE

| (21) | ||||||

| (22) |

and holds -a.s., and, in particular, . Under Assumption 3, that is a classical solution, we also have that holds -a.s. [1, Chapter 7, (4.29)]. It follows that

| (23) |

Thus, by the uniqueness of solutions [1, Chapter 1, Definition 6.6; Chapter 7, Definition 2.1], it follows that also solves (21)-(22) and thus , hold -a.s..

A further consequence of Girsanov’s theorem is that and are equivalent measures [27], that is, iff for . Thus the previous statements said to hold -a.s. also hold -a.s..

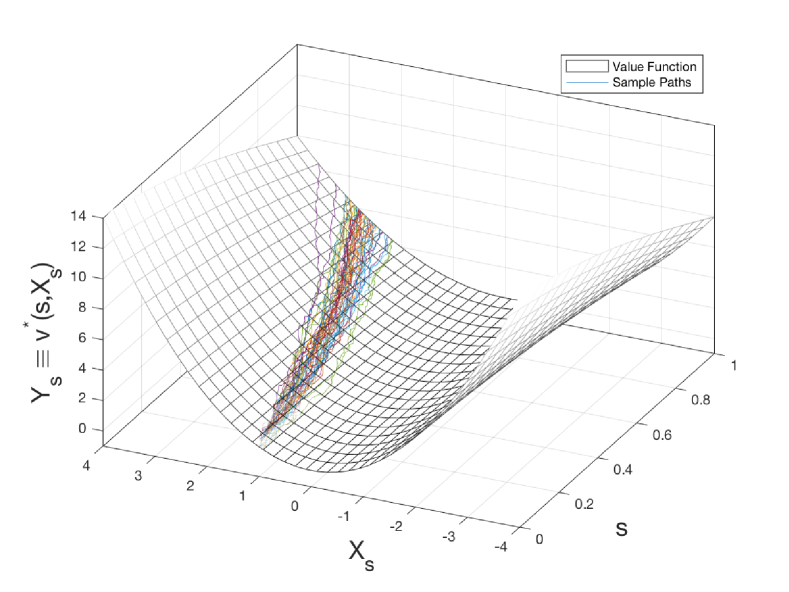

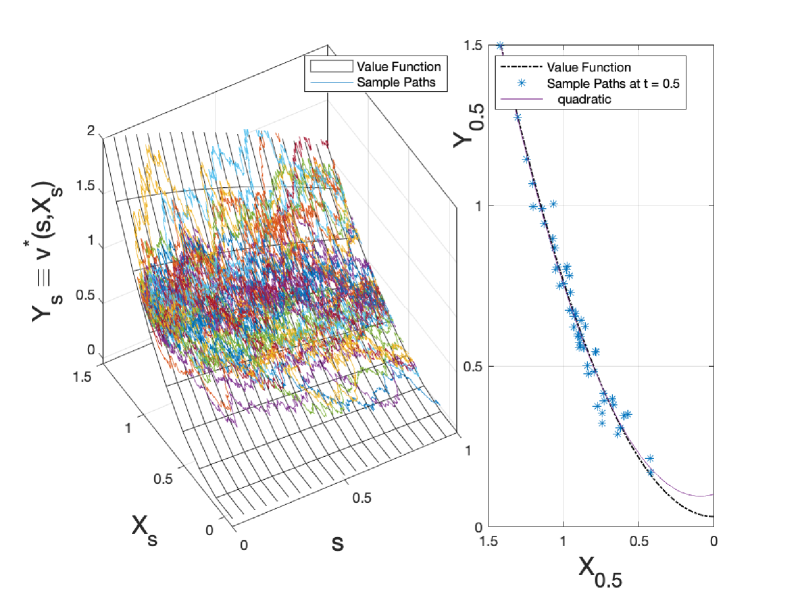

Example 1.

Consider the optimal control of the scalar linear system

whose value function is defined as the solution of

It can be verified that the value function is analytically expressed as

where

with corresponding optimal policy . For this example, let the target policy be the optimal policy , which can be computed analytically. For any adapted process , the associated drifted FBSDE is

with boundary conditions

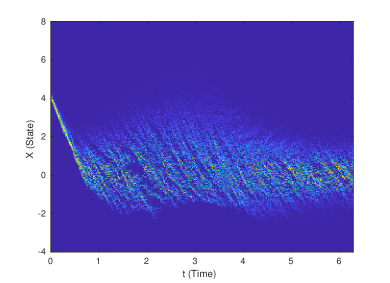

where we choose . We also have . The correspondence between the value function and the solutions to the above FBSDE for three different choices of , are illustrated in Fig. 1. The drift term in (c) generates a distribution for which matches the system guided by the optimal control policy.

Regardless of the drift value chosen, the process lies on the surface characterized by the function . Since, in general, function approximation has higher accuracy when interpolating in a region of dense samples compared to extrapolating in a region with no samples, the case in Fig. 1(c) is more desirable from an optimal control perspective, compared to Figs. 1(a) and 1(b), since the samples have a correspondence with the optimal trajectories.

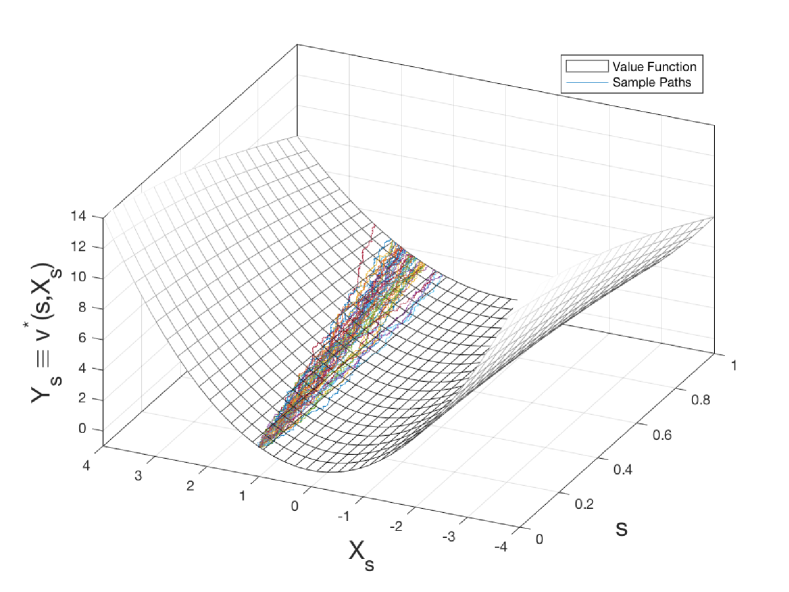

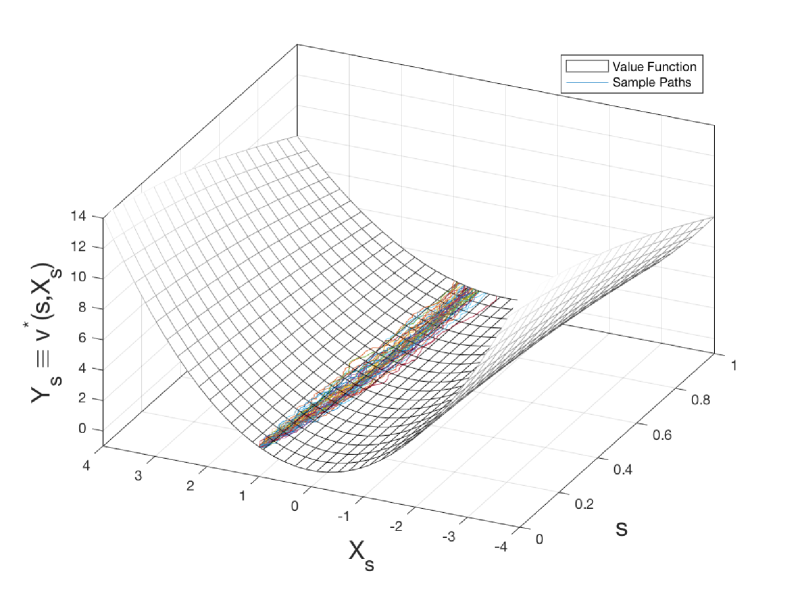

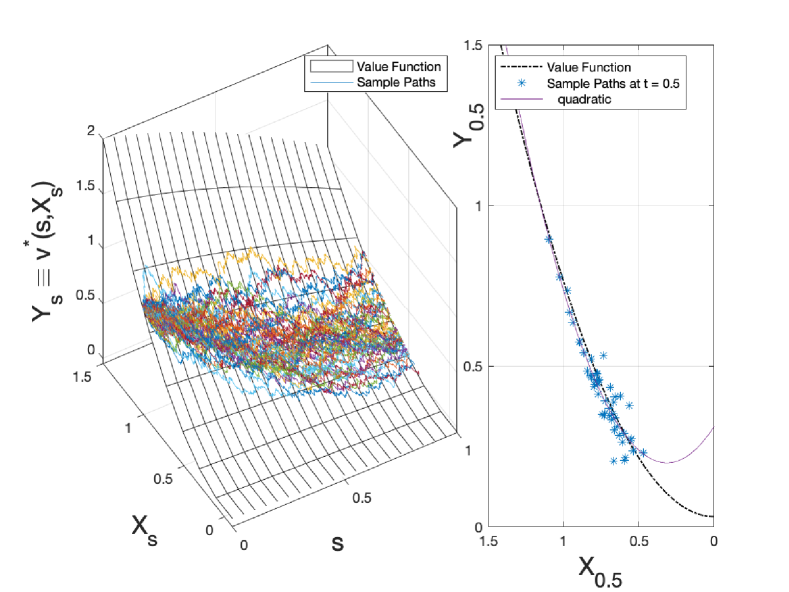

However, as illustrated in Fig. 2, there are other selections for the sampling policy outperforming the optimal control policy, yielding better function approximation. In this example, the function approximation at , is illustrated on the right hand side of Fig. 2. In particular, Fig. 2(b) illustrates that such a randomized optimal policy explores a larger region compared to a pure implementation of the optimal drift in Fig. 2(a), thus resulting in a more accurate approximation of the value function. In other words, a broader exploration of the state space contributes to better function approximations in the presence of numerical error that builds from recursive function approximation during the backward pass.

Example 1 and Fig. 1 illustrate the link between the drifted FBSDE and the value function. We can interpret this result in the following sense. We can pick an arbitrary process to be the drift term, which generates a distribution for the forward process in the corresponding measure . The BSDE yields an expression for using the same process used in the FSDE. The term acts as a correction in the BSDE to compensate for changing the drift of the FSDE. We can then use the relationship (14) to solve for the value function , whose conditional expectation can be evaluated in .

It should be noted that need not be a deterministic function of the random variable , as is the case with . For instance, it can be selected as for some appropriate function , producing a non-trivial joint distribution for the random variables .

A remarkable feature of the off-policy FBSDE formulation is that the forward pass is decoupled from the backward pass, that is, the evolution of the forward SDE does not explicitly depend on or (whereas in the Stochastic Maximum Principle formulations (see, e.g., [1, Chapter 3]) the decoupling is irremovable). This feature forms the basis of FBSDE numerical investigations of stochastic optimal control [29, 5]. The significant difference of Theorem III.1 in comparison to those results is that the focus is shifted here from the solution of (HJB) towards the broader class of functions satisfying the (HJ). This provides a stronger case for policy iteration methodologies, because the theory does not require, or expect, to be an optimal policy, as is in [29, 5]. Although not evaluated in this work, can be chosen according to design specifications other than estimating the optimal policy, such as to ensure the current policy is nearby the previously estimated policy.

III-B Interpretation of On-Policy Value Functions

When is a non-classical viscosity solution, may not exist everywhere and the expression (13) might not hold everywhere (see, e.g., the discussion in [4, p.46-47]). Nonetheless, we can modify Theorem III.1 to yield a similar result.

Proposition III.1.

Proof.

We now use this proposition to show the following result.

Corollary III.1.

III-C Local Entropy Weighing

As discussed in Section III-A, the disentanglement of the forward sampling from the backward function approximation provides the opportunity to employ broad sampling schemes to cover the state space with potential paths. However, fitting a value function broadly to a wide support distribution might degrade the quality of the function approximation since high accuracy of function approximation is more crucial in those parts of the state space that are in proximity to the optimal trajectories. Once forward sampling has been performed and some parts of the value function have been approximated, we can apply a heuristic in which sample paths closer to optimal trajectories are weighted more so as to concentrate value function approximation accuracy in those regions.

To this end, we propose using a bounded heuristic random variable to produce a new measure , the weighted counterpart to , defined as

| (27) |

In order to avoid underdetermination of the regression by concentrating a single or few samples, we select as

| (28) |

with , a tuning variable, and

| (29) |

is the relative entropy of which takes its minimum value when , the distribution in which all sampled paths have equal weight.

The minimizer of (28), which balances between the value of and the relative entropy of its induced measure, has a solution , given by [30, p. 2]

| (30) |

Henceforth, for simplicity, we let refer to this minimizer . During numerical approximation we can interpret the weights as a softmin operation over paths according to this heuristic, a method often used in the deep learning literature [31].

Theorem III.2.

Assume is selected such that is Brownian on the interval with respect to the induced measure . It then holds that

| (31) |

where is defined in (15). Furthermore, the minimizer of the optimization problem

| (32) |

over -measurable square integrable variables coincides with the value function .

Proof.

First, note that , , , , and are -measurable for . Thus, (12) and

| (33) |

hold -a.s.. We now show that they hold -a.s. as well. Since and is a probability measure, then is also a probability measure. Furthermore, since is bounded, -a.s.. It follows that and are equivalent measures because they reciprocally have strictly positive densities [32, Chapter 10, Remark 10.4]. The proof of Theorem III.1 shows that since these measures are equivalent, (12) and (33) hold -a.s. if and only if they also hold -a.s.. Since is Brownian in over the integral, the second term in the right hand side of (33) will drop out when taking the conditional expectation , yielding (31).

In the following section, we approximate the minimization of the right hand side of (32) over parameterized value function models to obtain an estimate of the value function.

To summarize, in this section we introduced three measures: (a) , the measure associated with the target policy for the value function , (b) , the sampling measure used in the forward pass to explore the state space, and (c) , the local-entropy weighted measure used in the backward pass to control function approximation accuracy.

In the this section we have provided the theoretical results justifying our approach for the case of continuous-time stochastic processes. In the next section we discuss how these each of these measures are represented numerically.

IV Branching Path LSMC

In this section we propose a novel discrete-time, finite-dimensional numerical scheme to produce the FSDE distribution, along with a procedure to solve for the value function in a backward pass using the BSDE. The FSDE distribution is represented as a branching-path tree and the BSDE is used to produce estimators, stepping backwards along each of the branching paths, to estimate the value function parameters using LSMC regression. Later on, in Section V, we propose particular choices for the drift process and the heuristic weight function used in the proposed FBRRT-SDE numerical method.

Henceforth, we assume a discrete-time partition of the interval , , for some partition length . For brevity, we abbreviate as and similarly for most other variables.

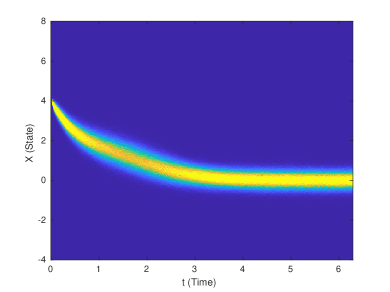

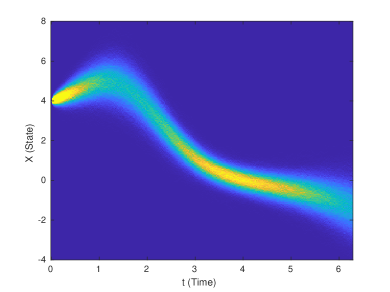

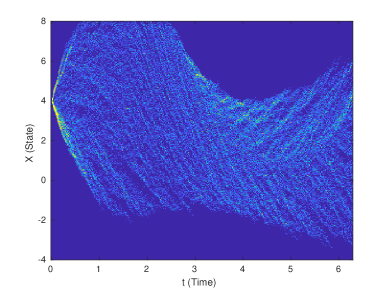

Fig. 3 motivates our approach, illustrating how the method is able to rapidly find the optimal distribution. An on-policy method assumes knowledge of an initial suboptimal control policy, sampled as in Fig. 3LABEL:sub@fig:distsubopt using the approach in [6] and the suboptimal value function is solved in that distribution. The on-policy method requires iterative improvement of the policy to produce a distribution which overlaps with the optimal distribution. However, if we begin with a sampling measure which broadly explores the state space as in Fig. 3LABEL:sub@fig:distrrt, we can produce an informed heuristic which weighs this distribution as in Fig. 3LABEL:sub@fig:distweight, so that the function approximation is concentrated in a near-optimal distribution. Thus, often, we need only one iteration to get a good approximation of the optimal value function and policy.

In Section IV-A we summarize the construction of a stochastically sampled tree, as a generalized data structure to approximate the FSDE distribution over the partition , and then, in Section IV-B, we demonstrate how this data structure can be interpreted as a series of McKean-Markov path measures to approximate the forward sampling distributions. Finally, in Section IV-C, we discuss how these measures can be used in the backward pass to approximate the BSDE solution by estimating the optimal value function.

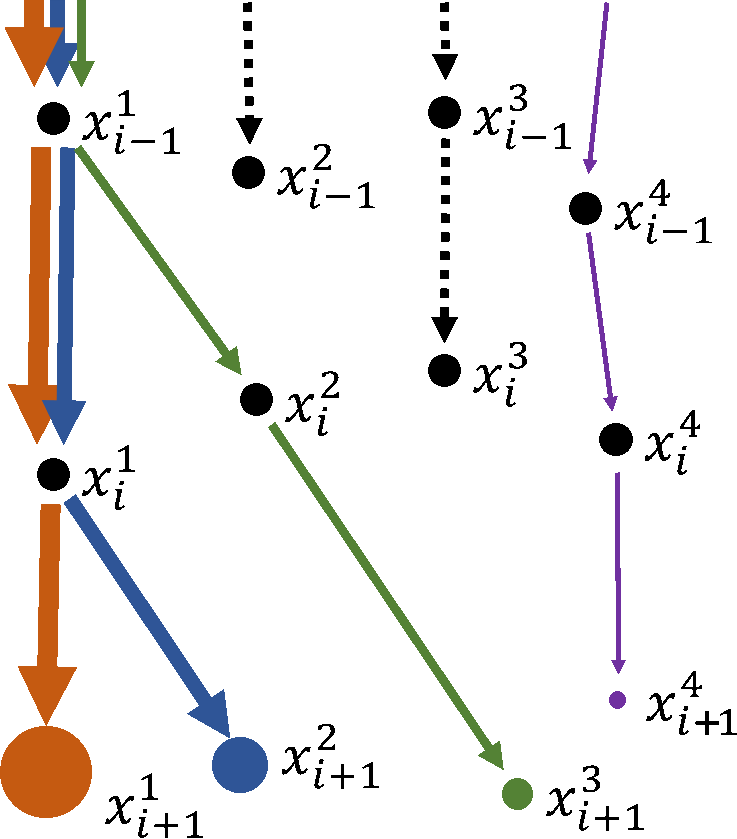

IV-A Forward SDE Branched Sampling

We begin by discussing the construction of a tree data structure representing the FSDE (9). In this section we only describe how edges of are added and what data is stored. Later, in Section V-A, we propose a specific methodology for selecting nodes for expansion and choosing the drift value. The tree is initialized with a root node at the initial starte and is constructed asynchronously as long as new nodes and directed edges are added using the following procedure.

Let be a state node in the tree at time selected for expansion, as the parent of a new edge. The drift (representing the random variable ) is sampled from some random function which can depend on both the state and the distribution of the nodes at that time. Independently, the noise is sampled . The child state node is computed using an Euler-Maruyama SDE step approximation of the FSDE (9),

| (34) |

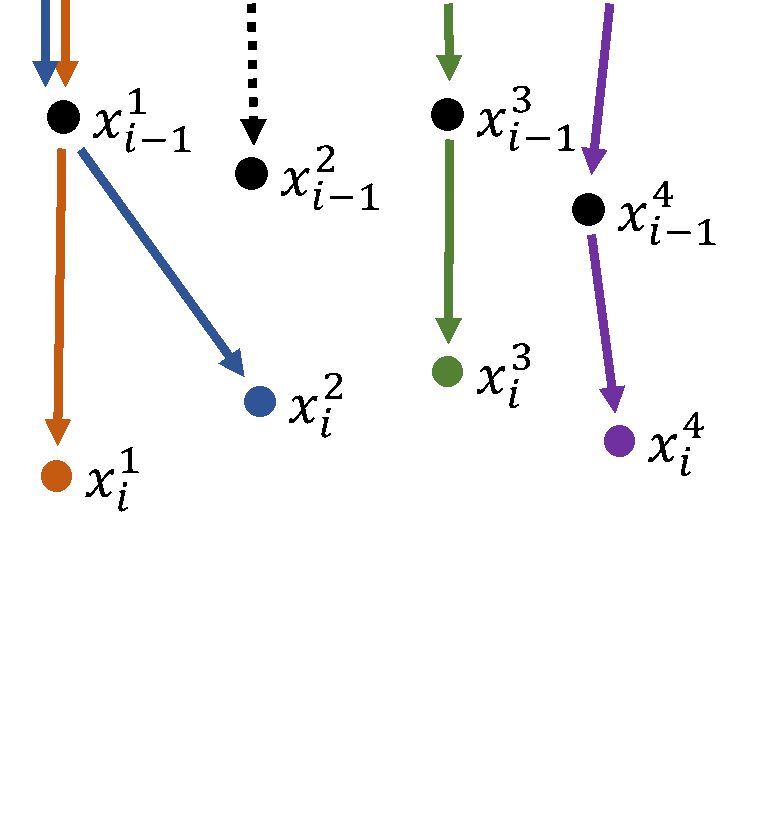

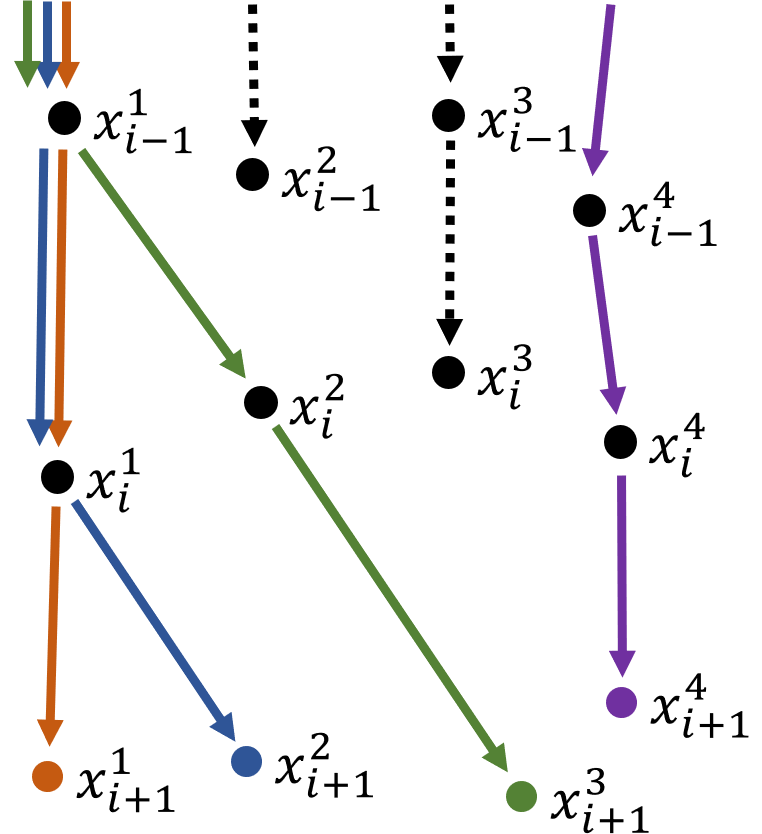

The edge is added to the tree, where is the data attached to the edge. A new parent can then be selected for expansion, including selecting the same parent again. Fig. 4 (a-b) illustrates the branching tree data structure.

IV-B McKean-Markov Measure Representation

We approximate the continuous-time sampling distributions with discrete-time McKean-Markov branch sampled paths, as presented in [34]. The tree data structure represents a series of path measures , each approximating the distribution where is the discrete-time random path defined as and is the inverse map from events on the path space to events on the sample space [33, Chapter 3]. Here, we use to refer to the set of random variables associated with the edges of the tree, including and . The empirical measure approximations are defined as

| (35) |

where is the Dirac-delta measure acting on sample paths

| (36) |

The notation indicates that this element is the sample of a random variable that is the ancestor of sample in the path , and similarly for the edge variables . Each node in the tree (alternatively called a particle) is associated with a unique path whose final term is . Figures 4(a)-(b) illustrate how each colored node at a particular time step is associated with its matching colored path, and that all of these paths collectively constitute the path measure.

It is worth noting that in this construction there is no requirement for and to agree over the interval . This property is illustrated by the fact that, for example, the path ending at in Fig. 4(a) is represented in but not represented in in Fig. 4(b). To see why such constructions are permissible in the proposed numerical scheme, notice that in the backward step (e.g., in Theorems III.1 and III.2) the measure is only employed to compute the instantaneous conditional expectation; thus, there is no sample path matching required when taking and to obtain , and when taking and to obtain .

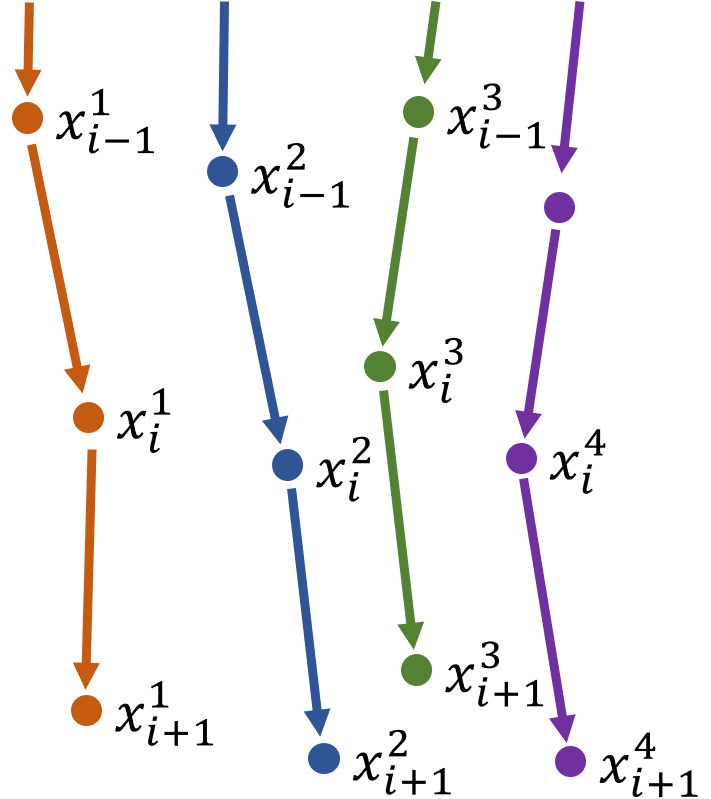

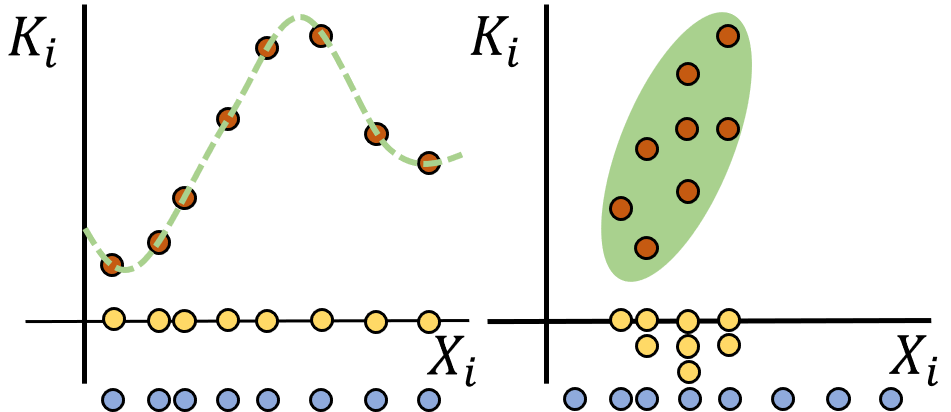

It can be observed in Fig. 4(b) that some edges are multiply represented in the distribution. If the drift term were restricted to be a deterministic function of (as is the case in [5, 6, 8]), such a construction would represent an unfaithful characterization of the path distribution because samples of the Brownian process are independent, and thus should be sampled as in Fig. 4(c). However, since itself is permitted to have a distribution, the overlapping of paths is justified as the drift having been selected so as to concentrate the paths in a certain part of the state space. Figure 5 illustrates why parallel sampling is naturally suited for representing deterministic functions and why branch sampling is necessary for representing nontrivial joint distributions .

For any arbitrary function evaluated on path , we have the almost sure convergence

| (37) |

as the number of particles , where is the ideal discrete-time approximation of the distribution under the Euler-Maruyama scheme [34, Section 4.1.2]. It follows from the change of variables theorem [35, Chapter 3, Theorem 3.6.1] that this expectation is exact up to the error due to time discretization

According to [36, Chapter 10, Theorem 10.2.2], when a linear growth condition in is imposed on , , and along with a few other conditions, the Euler-Maruyama scheme’s error varies as . When is constant with respect to , the error bound improves to [36, Chapter 10, Theorem 10.3.5]. Thus, our approximation converges with large numbers of particles and decreasing time intervals.

IV-C Path Integral Least Squares Monte Carlo

To approximate the measure in Theorem III.2 we use a path integral-weighted measure

| (38) |

where the weights for each heuristic value are

| (39) |

and is a normalizing constant. The heuristic value is calculated as , taking care to exclude so that its distribution remains Brownian.

In each step of the backward pass, we use and the value function approximation , parameterized by , where is the parameter space, to estimate the value function at the previous time step , by producing . We assume that the parameterizarion results in a function that is for all , and approximate the optimization in (32) as

| (40) |

where (15) is approximated as

| (41) |

The novelty of this method over classic LSMC [11], developed for parallel-sampled paths, comes from (a) the observation that introducing the drift process with a non-trivial joint distribution validates the choice of branch-sampled path distributions; (b) we can weigh regression points using a heuristic that acts on the entire path, not just the immediate states; and (c) weighing as in (39) has a particular interpretation as the selection of a measure with desirable properties for robustness using (28).

V Forward-Backward RRT-SDE

In this section, we present a novel algorithm (FBRRT-SDE) that uses rapidly exploring random trees to construct the graph of samples for solving the corresponding system of FBSDEs. The FBRRT-SDE algorithm is a particular numerical application of the generalized theory presented in Section IV. The ultimate goal of the FBRRT-SDE algorithm is to produce the set of parameters which approximate the optimal value function as . This is achieved by generating a forward pass to produce a graph representation of the path measures . Given that the optimal policy has the form (5), we define the target policy

| (42) | |||

so that it coincides with the optimal control policy when the value function approximation is exact. The backward pass uses , , and to produce , backwards in time. At each iteration of the algorithm, the policy cost associated with a set of parameterized policies is evaluated by sampling a parallel-sampled set of trajectories and computing the mean cost. At the end of each iteration, nodes with high heuristic value are pruned from the tree , and new nodes are added in the forward pass in the next iteration. This outer loop of the FBRRT-SDE algorithm is summarized in Algorithm 1.

V-A Kinodynamic RRT Forward Sampling

We desire sampling methods that seek to explore the whole state space, thus increasing the likelihood of sampling in the proximity of optimal trajectories. For this reason, we chose a method inspired by kinodynamic RRT [21]. The selection procedure for this method ensures that the distribution of the chosen particles is more uniformly distributed in a user-supplied region of interest, is more likely to select particles which explore the empty space, and is therefore less likely to oversample dense clusters of particles.

With some probability we choose the RRT sampling procedure, but otherwise we choose a particle uniformly from , each particle having equal weight. This ensures that dense particle clusters will still receive more attention. The choice of the parameter balances exploring the state space against refining the area around the current distribution.

For the drift values, that is, those sampled from the distribution left unspecified in Section IV-A, we again choose a random combination of exploration and exploitation. For exploitation we choose

| (43) |

and for exploration we choose

| (44) |

where the control is sampled randomly from a user-supplied set . For example, for minimum fuel () problems where the control is bounded as and the running cost is , we select because the policy (42) is guaranteed to only return values in this discrete set.

Algorithm 2 summarizes the implementation of the RRT-based sampling procedure that produces the forward sampling tree . The algorithm takes as input any tree with width and adds nodes at each depth until the width is , the desired tree width. In the first iteration there are no value function estimate parameters available to exploit, so we set to maximize exploration using RRT sampling.

V-B Path-Integral Dynamic Programming Heuristic

Next, we propose a heuristic design choice for the backward pass weighting variables , and justify this choice with theoretical analysis. A good heuristic will give large weights to paths likely to have low values over the whole interval . Thus, in the middle of the interval we care both about the current running cost and the expected cost. A dynamic programming principle result following directly from [25, Chapter 4, Corollary 7.2] indicates that

where is any control process in on the interval and is the measure produced by the drift . Following this minimization, we choose the heuristic to be the discrete approximation of

| (45) |

where is chosen identically to how the control for the drift is produced.

Although the theory up to this point does not require to be a feasible drift under the dynamic constraints of the SOC problem, for the proposed FBRRT-SDE algorithm the drift is always chosen as for some randomly selected . In practice, the running cost is approximated by Euler-Maruyama, and the optimal value function is approximated by the latest estimate of the value function . The running cost is computed in the forward sampling in line 21 of Algorithm 2.

Algorithm 3 details the implementation of the backward pass with local entropy weighting. Line 18 does not, theoretically, have an effect on the optimization, since it will come out of the exponential as a constant multiplier, but it has the potential to improve the numerical conditioning of the exponential function computation as discussed in [31, Chapter 5, equation (6.33)]. The value is, in general, a parameter which must be selected by the user. For some problems we choose to search over a series of possible parameters, evaluating each one with a backward pass and using the one that produces the smallest expected cost over a batch of trajectory rollouts executing the computed policy.

V-C Path Integral Erode

After the backward pass of the algorithm we obtain updated approximations of the value function along with the tree that represents the forward sampling path measures . To improve our approximation, we can use our value function estimates to create a new tree with new forward sampling measures via the heuristic in (45).

We have found experimentally that sampling a new tree from scratch is both wasteful and shows signs of catastrophic forgetting. That is, the subsequent backward pass performs worse, since it has lost data samples which were important to form good function estimates. On the other hand, simply adding more samples to the current tree can prove to be unsustainable in the long run. To keep the time complexity constant between iterations, we propose to bound the number of samples at each time step. After each backward pass we remove as many samples as were added in the forward pass, “eroding” the tree before the forward pass “expands” it.

The algorithm starts with a tree of width and ends with a tree of width at every depth. We begin at the end of the trajectory and remove the nodes with highest value until there are only nodes left at depth . We proceed in a similar fashion backwards down the tree, removing nodes with high values. However, due to the tree structure of the path measures, if we remove nodes that have children we disconnect the paths and ruin the assumed structure. Thus, we only remove nodes that have no children. The implementation of this algorithm is detailed in Algorithm 4.

V-D Function Approximation

In our implementation of the FBRRT-SDE algorithm, the value function is represented by 2nd order multivariate Chebyshev polynomials. Specifically, we use all products of the basis functions with polynomial degree 2 or lower, namely,

For better conditioning, points are first normalized to the interval based on a parameterized region of interest to obtain the basis functions .

V-E Computational Complexity

The computational complexity of the forward pass is dominated by the nearest neighbors search. In our implementation we use brute force search so the complexity of line 7 in Algorithm 2 is , but the complexity can be lowered to if a kd-tree is used for nearest neighbor search, instead. Thus, the forward pass complexity is (or with a kd-tree).

VI Numerical Examples

We evaluated the FBRRT-SDE algorithm by applying it to three challenging nonlinear stochastic optimal control problems. For all three problems, the terminal cost is taken to be a quadratic function centered at the origin and the running cost is taken to be an /min-fuel cost, which makes these problems challenging for traditional solution methods. For the first two problems the control input was restricted in the interval . For the third problem the control is restricted to .

VI-A Double Integrator

In order to compare the proposed FBRRT-SDE algorithm to the parallel sampled techniques in [6], which we denote below as parallel-sampled FBSDE, we considered the double integrator system with

with running cost, i.e.,

| (46) |

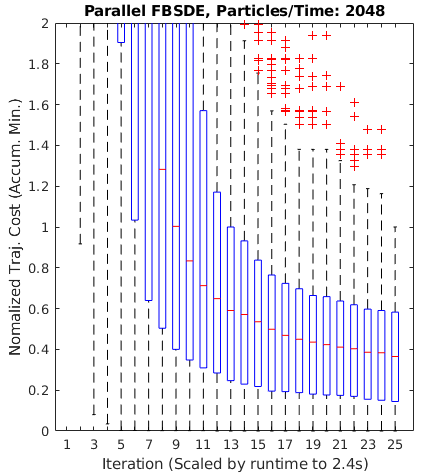

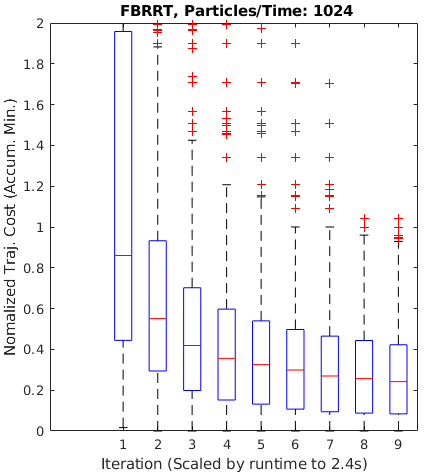

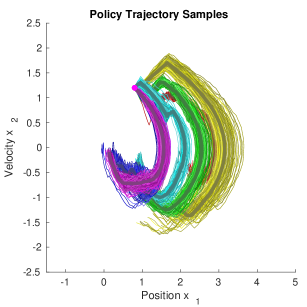

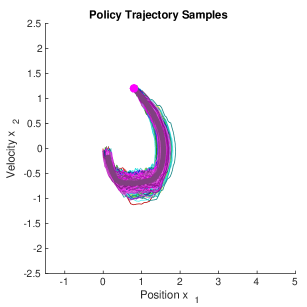

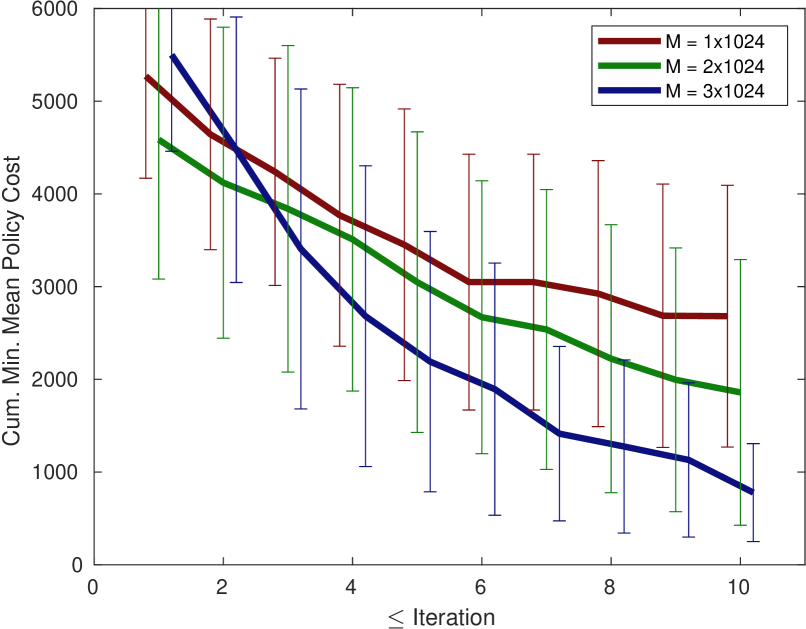

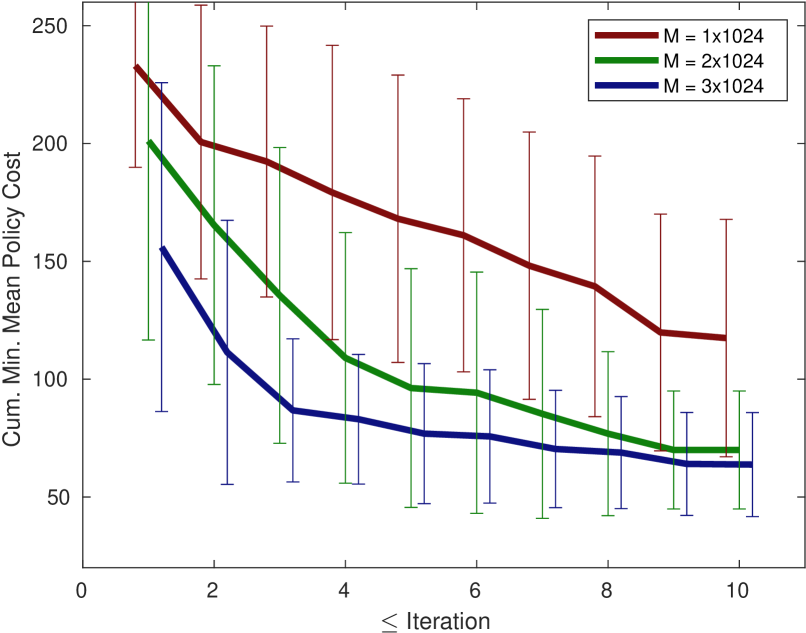

where are scalar parameters. When the system starts with positive position and velocity, the optimal policy is to decelerate to a negative velocity, coast for a period of time so that fuel is not used, and then accelerate to reach the origin. For this example, the number of particles per time step is , the number of time steps is , and the erode particle number is .

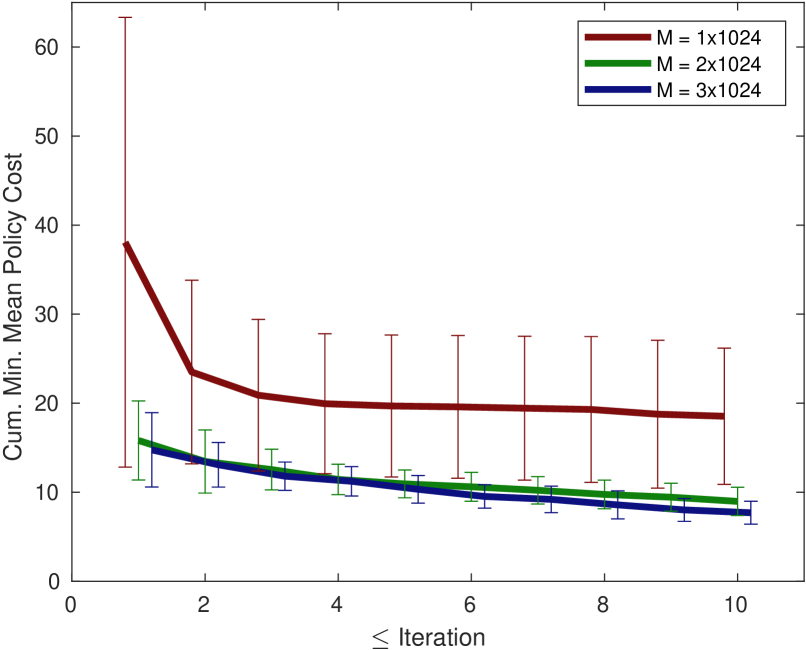

As shown in Figs. 6(c)-(d), the parallel-sampled FBSDE takes a significant number of iterations to begin converging to the near optimal policy, while the proposed method produces a near-optimal policy at the first iteration. The algorithm converges to the optimal policy.

We also compared the convergence speed and robustness of the two methods by randomly sampling different starting states and evaluated their relative performance over a number of trials. For each of random initial states we ran trials of each method for a number of iterations, each iteration producing an expected cost for the computed policy. We normalized the final costs across the initial states by dividing all costs for a particular initial state by the largest cost obtained across both methods. For each iteration, we assign the value of the accumulated minimum value across previous iterations for that trial, i.e., the value is the current best cost after running that many iterations, regardless of the current cost. We aggregated these values across initial states and trials into the box plots in Fig. 6. Since the FBRRT-SDE is significantly slower than the parallel-sampled FBSDE per iteration due to the nearest neighbors calculation, we scale each iteration by the runtime. Note that every iteration of FBRRT-SDE after the first one requires approximately half the runtime, since only half of the eroded tree needs resampling. In summary, the FBRRT-SDE converges faster using fewer iterations than the parallel-sampled FBSDE, and does so with half as many particle samples.

VI-B Double Inverted Pendulum

In order to study the proposed FBRRT-SDE algorithm on a highly nonlinear system in higher dimensions, consider the double inverted pendulum with state space dimension presented in [37], but with added damping friction to the joints. Thus, the dynamics are in the form , where is given in (48), where are scalar parameters of the system, and where . The associated optimal control problem is

| (47) |

where are scalar parameters. With our unoptimized implementation (where brute force search is used for nearest neighbors) this example takes approximately sec to complete the first iteration and sec to complete 10 iterations for ( sec and sec respectively for ).

| (48) |

Two initial conditions were evaluated, , where the bars are vertically down and motionless, and , where the angles of both bars are slightly perturbed from by . The number of time steps is taken to be and the erode particle number is selected as . The evaluation of these conditions over 30 trials with differing numbers of particles is provided in Fig. 7.

Since the initial conditions of the two experiments are close, their optimal values should also be close. Despite having comparable optimal values, the condition converges far more rapidly than the condition. Slightly perturbing the initial condition vastly improved the performance of the algorithm for this problem. The reason the condition performs poorly is likely because the system is very sensitive in that region and a localized policy results in a bifurcation of trajectory densities. If the differing groups of trajectories have similar heuristic values, the value function approximation tries to fit a function to groups of particles in different sides of the state space, resulting in poor accuracy for either group. When the condition is used, there is less ambiguity in which trajectory distributions are near-optimal, resulting in better performance.

VI-C Linearized Quadcopter

In order to demonstrate the proposed algorithm on a higher-dimensional system, we considered the linearized dynamics of a quadcopter having state space dimension , adapted from [38]. The dynamics are in the form , where

where are scalar parameters of the system, and where . The associated optimal control problem is

| (49) |

where are scalar parameters. With our unoptimized implementation (where brute force search is used for nearest neighbors) this example takes approximately sec to complete the first iteration and sec to complete 10 iterations for ( sec and sec respectively for ). The results are shown in Fig. 8.

For this example, most progress in terms of convergence occurs in the first iteration. Adding more particles significantly improved progress both in the first iteration and after several iterations. However, there were diminishing returns as the number of particles increased from to , likely due to the fact that the first iteration is already near optimal. Of interest is also the observation that the time required to solve this 8-dimensional problem was not significantly longer than the previous 4-dimensional example. This suggests that the time-complexity of the proposed method is more related to the complexity of the control problem itself rather than the dimensionality of the state space.

VII Conclusions and Future Work

We have proposed a novel generalization of the FBSDE approach to solve stochastic optimal control problems, combining branched sampling techniques with weighted least squares function approximation to greatly expand the flexibility of these methods. By leveraging the efficient space-filling properties of RRT methods, we have demonstrated that our method significantly improves the convergence properties of previous FBSDE numerical methods. We have shown how the proposed method works hand-in-hand with a local entropy-weighted LSMC method, concentrating function approximation in the regions where optimal trajectories are most likely to be dense. We have demonstrated that FBRRT-SDE can generate feedback control policies for high-dimensional nonlinear stochastic optimal control problems.

Several of the design choices exposed by our approach offer significant opportunities for further research. First, although in this paper we have employed the most basic of the RRT algorithms, there has been almost two decades of development in this field. Employing more elaborate methods may improve the forward sampling even further. In addition, in this paper we did not discuss state constraints or obstacles. Since RRT methods are naturally designed to accommodate obstacles, the methods proposed here should be extendable to those problems as well. For example, [1] reports a version of the Feynman-Kac theorem which involves FBSDEs with random stopping times and their relationship to boundary value PDEs.

Another area of research worth investigating is to find other methods of value function representation. In this paper, we use a rather simple parameterization of the value functions, though this simplicity offers some distinct benefits. Specifically, quadratic basis functions result in gradients that are linear, and policies that are typically stable. In regions where particles are sparse, the convexity of the value function representation naturally drives the system back towards the particle distribution. Further investigations might reveal other value function parameterizations with potentially better representation power than quadratic functions, while maintaining the benefits and the nice properties of quadratic basis functions.

References

- [1] J. Yong and X. Y. Zhou, Stochastic Controls: Hamiltonian Systems and HJB Equations. Springer Science and Business Media, 1999.

- [2] E. Pardoux and S. G. Peng, “Adapted solution of a backward stochastic differential equation,” Systems and Control Letters, vol. 14, no. 1, pp. 55–61, 1990.

- [3] S. Peng, “Backward stochastic differential equations and applications to optimal control,” Applied Mathematics and Optimization, vol. 27, no. 2, 1993.

- [4] N. El Karoui, S. Peng, and M. C. Quenez, “Backward stochastic differential equations in finance,” Mathematical Finance, vol. 7, no. 1, pp. 1–71, 1997.

- [5] I. Exarchos and E. A. Theodorou, “Stochastic optimal control via forward and backward stochastic differential equations and importance sampling,” Automatica, vol. 87, pp. 159–165, 2018.

- [6] I. Exarchos, E. A. Theodorou, and P. Tsiotras, “Stochastic -optimal control via forward and backward sampling,” Systems and Control Letters, vol. 118, pp. 101–108, 2018.

- [7] ——, “Game-theoretic and risk-sensitive stochastic optimal control via forward and backward stochastic differential equations,” in 55th IEEE Conference on Decision and Control, Las Vegas, NV, December 12-14 2016, pp. 6154–6160.

- [8] ——, “Stochastic Differential Games: A Sampling Approach via FBSDEs,” Dynamic Games and Applications, 2018.

- [9] H. M. Soner and N. Touzi, “A stochastic representation for the level set equations,” Communications in Partial Differential Equations, vol. 27, no. 9-10, pp. 2031–2053, 2002.

- [10] C. Bender and R. Denk, “A forward scheme for backward SDEs,” Stochastic Processes and their Applications, 2007.

- [11] F. A. Longstaff and E. S. Schwartz, “Valuing American options by simulation: A simple least-squares approach,” Review of Financial Studies, 2001.

- [12] J. Ma and J. Yong, Forward-Backward Stochastic Differential Equations and their Applications. Springer, 2007.

- [13] D. H. Jacobson and D. Q. Mayne, Differential Dynamic Programming. New York, NY: North-Holland, 1970.

- [14] E. A. Theodorou, Y. Tassa, and E. Todorov, “Stochastic differential dynamic programming,” in American Control Conference. Baltimore, MD: IEEE, 2010, pp. 1125–1132.

- [15] Y. Tassa, T. Erez, and W. D. Smart, “Receding Horizon Differential Dynamic Programming,” in Advances in Neural Information Processing Systems 20, 2008, pp. 1465–1472.

- [16] Y. Tassa, “Theory and implementation of biomimetic motor controllers,” Ph.D. dissertation, 2011.

- [17] G. Williams, N. Wagener, B. Goldfain, P. Drews, J. M. Rehg, B. Boots, and E. A. Theodorou, “Information theoretic MPC for model-based reinforcement learning,” in International Conference on Robotics and Automation, Singapore, May 29-June 3 2017, pp. 1714–1721.

- [18] C. E. Garcia, D. M. Prett, and M. Morari, “Model predictive control: theory and practice—a survey,” Automatica, vol. 25, no. 3, pp. 335–348, 1989.

- [19] S. Yensiri, “An Investigation of Radial Basis Function-Finite Difference (RBF-FD) Method for Numerical Solution of Elliptic Partial Differential Equations,” Mathematics, vol. 5, no. 54, 2017. [Online]. Available: http://www.mdpi.com/2227-7390/5/4/54

- [20] M. Li, W. Chen, and C. S. Chen, “The localized RBFs collocation methods for solving high dimensional PDEs,” Engineering Analysis with Boundary Elements, vol. 37, no. 10, pp. 1300–1304, 2013. [Online]. Available: http://dx.doi.org/10.1016/j.enganabound.2013.06.001

- [21] S. M. LaValle and J. J. Kuffner, “Randomized kinodynamic planning,” The International Journal of Robotics Research, vol. 20, no. 5, 2001.

- [22] I. Noreen, A. Khan, and Z. Habib, “Optimal path planning using RRT* based approaches: a survey and future directions,” Int. J. Adv. Comput. Sci. Appl, vol. 7, no. 11, pp. 97–107, 2016.

- [23] O. Arslan, E. A. Theodorou, and P. Tsiotras, “Information-theoretic stochastic optimal control via incremental sampling-based algorithms,” in IEEE Symposium on Adaptive Dynamic Programming and Reinforcement Learning, Orlando, FL, 2014, pp. 1–8.

- [24] K. P. Hawkins, A. Pakniyat, E. Theodorou, and P. Tsiotras, “Forward-Backward Rapidly-Exploring Random Trees for Stochastic Optimal Control,” in 60th IEEE Conference on Decision and Control, 2021, (submitted).

- [25] W. H. Fleming and H. M. Soner, Controlled Markov Processes and Viscosity Solutions. Springer Science and Business Media, 2006.

- [26] R. S. Sutton and A. G. Barto, Reinforcement learning: An introduction. MIT press, 2018.

- [27] G. Lowther, “Girsanov Transformations,” 2010. [Online]. Available: https://almostsure.wordpress.com/2010/05/03/girsanov-transformations/

- [28] W. H. Fleming and R. W. Rishel, Deterministic and Stochastic Optimal Control. Springer, 1975.

- [29] C. Bender and T. Moseler, “Importance sampling for backward SDEs,” Stochastic Analysis and Applications, vol. 28, no. 2, 2010.

- [30] E. A. Theodorou and E. Todorov, “Relative entropy and free energy dualities: Connections to path integral and KL control,” in 51st IEEE Conference on Decision and Control. Maui, HI: IEEE, December 10-13, 2012.

- [31] I. Goodfellow, Y. Bengio, and A. Courville, Deep Learning. MIT Press, 2016.

- [32] A. Pascucci, PDE and Martingale Methods in Option Pricing. Springer Science & Business Media, 2011.

- [33] S. Resnick, A Probability Path. Birkhäuser Verlag AG, 2003.

- [34] P. Del Moral, Mean Field Simulation for Monte Carlo Integration. Chapman and Hall/CRC, 2013.

- [35] V. I. Bogachev, Measure Theory. Springer Science & Business Media, 2007, vol. 1.

- [36] P. E. Kloeden and E. Platen, Numerical Solution of Stochastic Differential Equations. Springer Science and Business Media, 2013, vol. 23.

- [37] R. Tedrake, “Underactuated Robotics: Learning, Planning, and Control for Efficient and Agile Machines: Course Notes for MIT 6.832,” Working Draft Edition, vol. 3, 2009.

- [38] F. Sabatino, “Quadrotor control: modeling, nonlinear control design, and simulation,” 2015.

![[Uncaptioned image]](/html/2210.10534/assets/figures/kphawkins_profile_small.jpg) |

Kelsey P. Hawkins received B.S. degrees in Applied Mathematics and Computer Science from North Carolina State University in 2010 and the M.S. degree in Computer Science from the Georgia Institute of Technology in 2012. He is now a Ph.D. candidate in Robotics at the Georgia Institute of Technology in the Institute for Robotics and Intelligent Machines. His research interests include stochastic optimal control, differential games, and safe human-robot control design, with applications in autonomous driving, industrial robotics, and healthcare robotics. |

![[Uncaptioned image]](/html/2210.10534/assets/figures/AliPakniyatIEEE.jpeg) |

Ali Pakniyat (M’14) received the B.Sc. degree in Mechanical Engineering from Shiraz University in 2008, the M.Sc. degree in Mechanical Engineering from Sharif University of Technology in 2010, and the Ph.D. degree in Electrical Engineering from McGill University in 2016. After holding a Lecturer position at the Electrical and Computer Engineering department of McGill University, a postdoctoral research position in the department of Mechanical Engineering at the University of Michigan, Ann Arbor, and a postdoctoral research position in the Institute for Robotics and Intelligent Machines at Georgia Institute of Technology, he joined the department of Mechanical Engineering at the University of Alabama in 2021 as an Assistant Professor. His research interests include deterministic and stochastic optimal control, nonlinear and hybrid systems, analytical mechanics and chaos, with applications in the automotive industry, robotics, sensors and actuators, and mathematical finance. |

![[Uncaptioned image]](/html/2210.10534/assets/figures/theodorou.jpg) |

Evangelos Theodorou is an associate professor in the Daniel Guggenheim School of Aerospace Engineering at the Georgia Institute of Technology. He is also affiliated with the Institute of Robotics and Intelligent Machines. Theodorou earned a Bachelors and Masters degree in Electrical Engineering from the Technical University of Crete, Greece, a Masters degree in Computer Science and Engineering from the University of Minnesota, and a a Ph.D. in Computer Science from the University of Southern California. His research interests span the areas of stochastic optimal control, robotics, machine learning, and computational neuroscience. |

![[Uncaptioned image]](/html/2210.10534/assets/figures/tsiotras_small.jpg) |

Panagiotis Tsiotras (F’19) is the David and Andrew Lewis Chair Professor in the Daniel Guggenheim School of Aerospace Engineering at the Georgia Institute of Technology (Georgia Tech). He holds degrees in Aerospace Engineering, Mechanical Engineering, and Mathematics. He has held visiting research appointments at MIT, JPL, INRIA Rocquencourt, and Mines ParisTech. His research interests include optimal control of nonlinear systems and ground, aerial and space vehicle autonomy. He has served in the Editorial Boards of the Transactions on Automatic Control, the IEEE Control Systems Magazine, the AIAA Journal of Guidance, Control and Dynamics, the Dynamic Games and Applications, and Dynamics and Control. He is the recipient of the NSF CAREER award, the Outstanding Aerospace Engineer award from Purdue, and the Technical Excellence Award in Aerospace Control from IEEE. He is a Fellow of AIAA, IEEE, and AAS. |