Linear Regression with Centrality Measures

Abstract

This paper studies the properties of linear regression on centrality measures when network data is sparse – that is, when there are many more agents than links per agent – and when they are measured with error. We make three contributions in this setting: (1) We show that OLS estimators can become inconsistent under sparsity and characterize the threshold at which this occurs, with and without measurement error. This threshold depends on the centrality measure used. Specifically, regression on eigenvector is less robust to sparsity than on degree and diffusion. (2) We develop distributional theory for OLS estimators under measurement error and sparsity, finding that OLS estimators are subject to asymptotic bias even when they are consistent. Moreover, bias can be large relative to their variances, so that bias correction is necessary for inference. (3) We propose novel bias correction and inference methods for OLS with sparse noisy networks. Simulation evidence suggests that our theory and methods perform well, particularly in settings where the usual OLS estimators and heteroskedasticity-consistent/robust -tests are deficient. Finally, we demonstrate the utility of our results in an application inspired by De Weerdt and Dercon (2006), in which we consider consumption smoothing and social insurance in Nyakatoke, Tanzania.

Keywords: networks, diffusion centrality, eigenvector centrality.

JEL Classification Codes: C18, C21, C81.

1 Introduction

A large and rapidly growing body of work documents the influence of networks in a wide range of economic outcomes: peer effects drive academic achievement, production networks shape shock propagation in the macroeconomy, social networks affect information- and risk-sharing with important implications for development (see Sacerdote 2011, Carvalho and Tahbaz-Salehi 2019 and Breza et al. 2019 for recent reviews). Many other examples abound.

One particular strand of research has fruitfully explored the relationship between an agent’s network position and their economic outcomes. For example, Hochberg et al. (2007) considers the network of venture capital firms and finds that better-networked firms successfully exit a greater proportion of their investments. Meanwhile, Cruz et al. (2017) examines the social networks in the Philippines and shows that more central families are disproportionately represented in political offices. Similarly, Banerjee et al. (2013) studies the problem of diffusing microfinance in India and establishes that seeding information to more central agents led to greater participation in the program.

In these papers, researchers often estimate linear models by ordinary least squares (OLS), using centrality measures as explanatory variables. Centrality measures are node-level statistics that capture notions of importance in a network. Since nodes can be important for many reasons, a variety of centrality measures exist, each capturing a particular aspect of network position. For example, the degree centrality of an agent reflects the number or intensity of their direct links, while eigenvector centrality is designed so that influence of agents is proportional to that of their connections. The correlation between an outcome variable and a particular centrality measure may be revealing about the types of interactions that drive a given economic phenomenon: an outcome that is well-predicted solely by degree is likely to be determined in an extremely local manner, whereas one that is more strongly associated with eigenvector centrality may involve non-linear interactions between agents that are further apart. As such, when researchers estimate these correlations and test their statistical significance, they frequently do so with the goal of drawing conclusions about the economic significance of various centrality measures and the implied mechanisms for outcome determination. Such an exercise is credible only if the OLS estimator is close to the estimand, and if the chosen test statistic (typically the heteroskedasticity-consistent/robust -statistics) is well described by its asymptotic distribution (standard normal for -statistics) in finite sample.

However, network data have two features that may threaten the statistical validity of OLS. Firstly, networks may be sparse, with many more agents than links per agent. This could happen because interactions are observed with low frequency, or because the interactions in question are rare. Chandrasekhar (2016) argues that many economic networks are sparse, providing evidence from commonly used social network data (e.g. AddHealth; Karnataka Villages (Banerjee et al. 2013); Harvard social network (Leider et al. 2009)). Sparsity poses a challenge to estimation and inference: if networks are largely empty, there might not be enough variation in centrality measures to identify the parameters of interest. Despite its importance, sparsity has received relatively little attention in the network econometrics literature.

Secondly, the observed network may differ from the true network of interest. Centrality measures are often calculated on data which are obtained by survey or constructed using some proxy for interaction between agents, though subsequent analysis would frequently treat the true network as known. Ignoring measurement error may thus lead to estimates that perform poorly. A growing literature works with networks that are assumed to be measured with error. However, they generally do not consider sparse settings. This is important since sparsity and measurement error are mutually reinforcing: sparser networks contain weaker signals, which are in turn more difficult to pick out from noisy measurements. The upshot is that OLS estimators computed on sparse, noisy networks may have particularly poor properties. Asymptotic theory that ignore these features will provide similarly poor approximations to their finite sample behavior. Consequently, estimation and inference procedures based on these theories may lead to invalid conclusions about the economic significance of centrality measures.

This paper studies the statistical properties of OLS on centrality measures in an asymptotic framework which features both measurement error and sparsity. Our analysis is centered on degree, diffusion and eigenvector centralities, which are among the most popular measures. Our contribution is threefold: (1) We characterize the amount of sparsity at which OLS estimators become inconsistent with and without measurement error, finding that this threshold varies depending on the centrality measure used. Specifically, regression on eigenvector centrality is less robust to sparsity than that on degree and diffusion. This suggests that researchers should be cautious about comparing regressions on different centrality measures, since they may differ in statistical properties in addition to economic significance. (2) We develop distributional theory for OLS estimators under measurement error and sparsity. We restrict ourselves to sparsity ranges under which OLS is consistent, but we find that asymptotic bias can be large even in this case. Furthermore, the bias may be of larger order than variance, in which case bias correction would be necessary for obtaining non-degenerate asymptotic distributions. Additionally, we find that under sparsity, the estimator converges at a slower rate than is reflected by the usual heteroskedasticity-consistent(hc)/robust standard errors, requiring a different estimator. (3) In view of the distributional theory, we propose novel bias-corrected estimators and inference methods for OLS with sparse, noisy networks. We also clarify the settings under which hc/robust -statistics are appropriate for testing.

Our theoretical results are derived in an asymptotic framework where networks are modeled as realizations of sparse random graphs. As , the expected number of links per agent grows much more slowly than . Because our statistical model captures important features of real world data, we expect our methods to be reliable for estimation and inference with sparse, noisy networks. We provide simulation evidence supporting this view. The utility of our results is also evident from an application inspired by De Weerdt and Dercon (2006), where we conduct a stylized study of consumption smoothing and social insurance in Nyakatoke, Tanzania.

Our choice of asymptotic framework poses technical challenges. Firstly, the eigenvectors and eigenvalues of sparse random graphs are difficult to characterize. We draw on recent advances in random matrix theory (Alt et al. 2021a; b; Benaych-Georges et al. 2019; 2020) to overcome this challenge. Secondly, spectral norms of random matrices concentrate slowly in sparse regimes. Instead, we develop bounds for moments of noisy adjacency matrices by relating them to counts of particular graphs, in the spirit of Wigner (1957) (see Chapter 2 of Tao 2012 more generally). Finally, in order for bias correction to improve mean-squared error, the bias needs to be estimated at a sufficiently fast rate. Because variance is of lower order than bias, a naive plug-in approach does not work for estimating higher order bias terms, although it is sufficient for the first order term. We leverage this fact to recursively construct good estimators for higher order terms.

Related Literature

Our work is most closely related to papers that study linear regression with centrality statistics. To our best knowledge, we are the first to study linear regression with diffusion centrality, though there exist prior work on eigenvector centrality. Le and Li (2020) studies linear regression on multiple eigenvectors of a network assuming the same type of measurement error as this paper. They focus on denser settings than we do and provide inference method only for the null hypothesis that the slope coefficient is . We are concerned only with eigenvector centrality, which is the leading eigenvector, but our results cover the sparse case as well as tests of non-zero null hypotheses (more details in Remark 5). Our paper is also related to Cai et al. (2021), which proposes penalized regressions on the leading left and right singular vectors of a network. They consider networks that are as sparse as the ones we study, but their networks are observed with an additive, normally distributed error (more details in Remark 4). Outside of the linear regression setting, Cheng et al. (2021) considers inference on deterministic linear functionals of eigenvectors. They study symmetric matrices with asymmetric noise, proposing novel estimators that leverage asymmetry to improve performance when eigengaps are small. We focus on symmetric matrices with symmetric noise and study the plug-in estimator in which eigenvector is estimated using the noisy adjacency matrix in place of the true matrix.

Our paper also relates to a growing literature that considers sampling and measurement error in networks. Chandrasekhar and Lewis (2016) examines settings in which researchers have access to a panel of networks, but which are constructed using only a partial sample of nodes or edges. Thirkettle (2019) studies a similar missing data problem, but in a cross-sectional setting with only one network. It is concerned with forming bounds on centrality statistics and does not consider subsequent linear regression. Griffith (2022) considers the censoring in network data, which arises when agents are only allowed to list a fixed number of relationships during the sampling process. The above papers study missing data problems under the assumption that the observed network is without error. We assume that the entirety of one network is observed but with error. Lewbel et al. (2021) studies measurement error in peer effects regression, finding that 2SLS with friends-of-friends instruments is valid as long as measurement error is small. They do not discuss centrality regressions.

This paper is also connected to the nascent literature on the statistical properties of sparse networks. A strand of this literature is concerned with network formation models that can give rise to sparsity in the observed data. Dong et al. (2020) and Motalebi et al. (2021) consider modifications to the stochastic block model. A more general model takes the form of inhomogeneous Erdos-Renyi graph, which are generated by a graphon with a sparsity parameter that tends to zero in the limit (see for instacne Bollobás et al. 2007 and Bickel and Chen 2009). Our paper takes this approach. Yet another model for sparse graphs is based on graphex processes, which generalizes graphons by generating vertices through Poisson point processes (see Borgs et al. 2018, Veitch and Roy 2019 and references therein). Our choice of inhomogeneous Erdos-Renyi graphs is motivated by their prevalence in econometrics (Section 3 of De Paula 2017 and Section 6 of Graham 2020a provide many examples), as well as tractability considerations. To our best knowledge, few papers have tackled the challenges that sparse networks pose for regression. Two notable exceptions study network formation models, which take the form of edge-level logistic regressions (Jochmans 2018; Graham 2020b). A separate literature considers estimation of peer effects regressions involving sparse networks using panel data (Manresa 2016; Rose 2016; De Paula et al. 2020). Here, sparsity is an assumption used to justify regularization methods. We consider a node-level regression in a cross-sectional setting with one large network.

More generally, we contribute to the literature on measurement error models, in which economic outcomes are driven by unobserved latent variables, although proxies or noisy measurements of these variables exist. For recent reviews, see Hu (2017) and Schennach (2020). Classical measurement error is an additive noise that is (conditionally) independent of the unobserved regressor and has a long history (e.g. Adcock 1878). When the underlying network is noisily observed, centrality statistics face errors which are non-linear and non-separable. General non-classical measurement error problems have been studied in cross-sectional (e.g. Matzkin 2003; Chesher 2003; Evdokimov and Zeleneev 2022) and panel data settings (e.g. Griliches and Hausman 1986; Evdokimov 2010; Evdokimov and Zeleneev 2020). These papers typically assume that observations can be grouped into units across which the latent variable and measurement error are independent. This excludes our setting, since centrality statistics of any given agent depends on the entire network.

The rest of this paper is organized as follows. Section 2 describes the set-up of our paper. Section 3 presents the theoretical results. Simulation results are contained in Section 4. In Section 5, we apply our results to the social insurance network in Nyakatoke, Tanzania. Section 6 concludes the paper with our recommendations for empirical work. All proofs are contained in Appendix A.

2 Set-Up and Notation

In this section, we introduce notation before describing our econometric model and the asymptotic framework.

We use the following notation. When is a vector or matrix, and refer the and component of respectively. Similarly, if or are defined, we use to denote the full vector or matrix respectively. is the transpose of . When is a square matrix, denotes the eigenvalue of while denotes the corresponding eigenvector. When is a symmetric real function, denotes the eigenvalue of the corresponding Hillbert-Schmidt integral operator, , while is the corresponding eigenfunction. For deterministic, monotone sequences and , we write if and if . indicates that , where . We write to mean and similarly for . Let be the vector of ’s. For two matrices and , let denote their entrywise (Hadamard) product. Finally, denotes the set of integers from to .

2.1 Econometric Framework

For simplicity, suppose that there are no covariates besides centrality. Suppose also that the data-generating process yields which are independent and identically distributed. is the observed outcome of interest. is an unobserved latent type that will be used to construct the network. In lieu of , we observe either the true adjacency matrix , or a noisy version, . is an matrix whose , , records the link intensities between agents and . is some estimate of .

Consider the regression:

where is a network centrality measure of type . We do not observe , it can be exactly computed using , or estimated using . The parameter of interest is . After defining the data-generating process for the latent and observed networks, Assumption 3 will provide conditions allowing us interpret as the slope coefficient in the linear conditional expectation function of on .

In the following, we describe (i) the data-generating process for and via the ’s and (ii) the use of and in computing/estimating centrality statistics for OLS estimation. Throughout our discussion, we motivate econometric framework through the example of consumption smoothing via informal insurance:

Example 1.

Suppose we are interested in the relationship between informal insurance and consumption smoothing. This is a question that has been studied by De Weerdt and Dercon (2006); Udry (1994); Kinnan and Townsend (2012) and Bourlès et al. (2021) among many others. Here, we might posit that agents which are more central in the informal insurance network can better smooth consumption. To test this hypothesis, we are interested in the regression where is variance in ’s consumption and is centrality in the informal insurance network. is then the reduction in consumption variance associated with being more central. In the informal insurance network, records the probability that lends money to or vice versa in the event of an adverse income shock. However, is hard to obtain by surveys. Instead, we observe the matrix of actual loans , which is a noisy measure of .

Data-Generating Process for and

Let be an symmetric adjacency matrix. We assume that the relationship between two agents in a network is solely determined by their unobserved latent types through the graphon :

Assumption 1 (Graphon).

Suppose and is such that:

Let and , define:

We set for and normalize for all .

In this model, any two agents have a relationship that is between and . We can think of this as a measure of intensity, reflecting factors such as duration of friendship, frequency of interaction, or similarity in personalities. Alternatively, it could be the probability with which a relationship is observed. is a parameter that we will let go to at various rates. As we will explain in Section 2.2, this is a theoretical device that will help us understand the behavior of the OLS estimator when the network is sparse. We restrict our attention to symmetric matrices because eigenvector centrality, one of the most popular network centrality measures, may not be well-defined when the adjacency is not symmetric. We also ignore the trivial case when , in which case the network is always empty. Finally, we note that defining is without loss of generality since we have placed no functional form restrictions on .

Example 2 (continues=ex:leading).

Suppose that indexes the riskiness of a villager’s income as a result of the crops they choose to cultivate. Assumption 1 posits that the relationship between two villagers depends only on their respective income risks. For example, if , then farmers with similar income risks have higher link intensities between them. can also incorporate other observed or unobserved farmer characteristics, such as place of residence, farming skills or gregariousness. Together with the choice of , the graphon is a rich model of linking behavior.

When is observed, we say that there is no measurement error. This setting provides a useful benchmark. When is not observed, we assume that we have access to the noisy version, , generated as follows.

Assumption 2 (Measurement Error).

The adjacency matrix with measurement error is the matrix symmetric , where for ,

We set for . since . Furthermore,

The form of measurement error we consider randomly rounds into zero or one in proportion to the intensity of the true relationship. Conditional on , this is an additive error with a mean of , and which is independent across agent pairs. Formally, we are assuming a conditionally independent dyad (CID) model for . This model is commonly used in econometrics (see for instance Section 3 of De Paula 2017 or Section 6 of Graham 2020a) and is fairly general. By the Aldous-Hoover Theorem (Aldous 1981; Hoover (1979)), all infinitely exchangeable random graphs have such a representation. Roughly, this corresponds to sampling from a large population in which the labels of agents do not matter. Measurement error of this form can arise due to limitations in data collection, or because networks are constructed by proxy. We provide examples of data that fit our measurement error model at the end of this subsection. Importantly, however, it excludes strategic network formation for , in which agents’ decision to form or report links depends on that of the others.

Finally, we also assume that measurement error is independent of conditional on . Together with the CID assumption, measurement error on the network is additive white noise, akin to the type studied in classical measurement error models. In our setting, the key econometric challenge arises because is unobserved. This is exacerbated by the fact that additive, white noise errors in the network translates into non-linear measurement error in centrality statistics, introducing complications in the analysis.

Remark 1.

The challenges that this form of measurement error poses are most severe in cross-sectional data. Intuitively, given long panel data on the networks, we would be able to estimate well using entry-wise averages of the networks over time.

Example 3 (continues=ex:leading).

Assumption 2 is reasonable in the context of our leading example. Here, each entry of the unobserved represents the probability of loans. However, records actual loans, which are realizations of Bernoulli(). The conditional independence assumption means that conditional on friendship, the decision of to lend to is independent of the decision of to lend to . This might be the case if the loan amounts are small relative to the income shortfall, so that any agent’s decision to lend to does not significantly reduce their need to borrow. Alternatively, such a condition might be satisfied if borrowing is private, so that friends of cannot coordinate their lending decisions.

The remainder of this subsection lists examples of network data that could be described by our data-generating process.

Example 4.

Carvalho et al. (2021) studies the propagation of shocks through production networks during the Great East Japanese Earthquake of 2011. In the ideal production network, records the value of ’s sales to as a proportion of the value of ’s total sales. In turn, depends on and , which might index the quality of a firm’s product, with higher quality firms requiring more and higher quality inputs. However, these variables are not observed. Instead, the authors have access to data from a credit reporting agency which includes supplier and customer information for firms. The authors explicitly note two limitations in their data: “First, it only reports a binary measure of interfirm supplier-customer relations… we do not observe a yen measure associated with their transactions. Second, the forms used by [the credit agency] limit the number of suppliers and customers that firms can report to 24 each.” Suppose firms only report suppliers from whom they receive delivery during the month in which the forms are filed. Then a supplier that sends fewer inputs are more likely to be omitted in any given month. Abstracting away from concerns about network censoring (see Griffith 2022), the conditional independence assumption would also be satisfied if the delivery schedules for suppliers are independent.

Example 5.

Xu (2018) studies how patronage affected the promotion and performance of bureaucrats in the Colonial Office of the British Empire. In the ideal network for measuring patronage, records intensity of the friendship between and . Here, might index traits such as gregariousness, polo skills and drinking habits among others. Bureaucrats having more in common with their patrons may be more likely to be recommended for promotion. However, the link intensity between bureaucrats are not observed. Instead, the paper proxies for relationships using indicators for shared ancestry, membership of social groups (such as the aristocracy) or attendance of the same elite school or university. In this context, our data-generating process means that bureaucrats who are closer are more likely to satisfy the above criteria for connection. The conditional independence assumption would be satisfied if the lack of observation are independent across agent pairs, e.g. if some university records were randomly lost.

Centrality Statistics and OLS Estimation

Given our adjacency matrices and , we now define centrality statistics and the OLS estimators that are based on them.

Centrality measures are agent-level measures of importance in a network. Many centrality measures exist, each capturing a different aspect of network position. However, they are all functions of and can be exactly computed in the no measurement error ase. We focus on three popular measures: degree, diffusion and eigenvector centralities. While they are most intuitive when is binary, centrality measures should be understood as functions of general weighted (symmetric) adjacency matrices. Except where noted, our definitions are standard (see e.g. Jackson 2010; Bloch et al. 2021).

Definition 1 (Degree Centrality).

Degree centrality computed on the adjacency matrix is the vector:

Agent ’s degree centrality is simply the sum of row in . If is binary, degree centrality is the number of agents with whom has a relationship.

Definition 2 (Diffusion Centrality).

For a given and , diffusion centrality computed on the adjacency matrix is the vector:

Proposed by Banerjee et al. (2013), diffusion centrality captures the influence of agent in terms of how many agents they can reach over periods. Consider again the case of binary . Then the of is the number of walks from to that are of length , which can be thought of as the influence of on in period . Diffusion centrality for agent is simply sum of their influence on all other agents in the network over time up to period , with a decay of per period. Bramoullé and Genicot (2018) provides further discussion on the theoretical foundations of diffusion centrality. In practice, researchers often choose to be , so that effectively as . An extension of our results to this case is in preparation.

Definition 3 (Eigenvector Centrality).

For a given , eigenvector centrality computed on the adjacency matrix is the vector:

where is the eigenvector corresponding to the eigenvalue of with the largest absolute value (leading eigenvalue).

Eigenvector centrality is based on the idea that an individual’s influence is proportional to the influence of their friends. That is, for some , we seek the following property:

| (1) |

The eigenvectors of solve the above equations, with being the corresponding eigenvalue. By the Perron-Frobenius Theorem, the leading eigenvector is the unique eigenvector that be chosen so that every entry is non-negative, motivating its use as a centrality measure. The leading eigenvector of related matrices also emerges as the measure of influence in popular models of social learning (e.g. DeGroot 1974)

The leading eigenvector is well-defined only if the largest eigenvalue of has multiplicity 1, that is, if . To ensure that this occurs with high probability, we introduce the following assumption specific to eigenvector centrality:

Assumption E1.

Suppose .

Note also that eigenvectors are defined only up to scale: if satisfies Equation 1, so will for any . Eigenvector centrality is commonly defined to have length (e.g. Banerjee et al. 2013; Cruz et al. 2017), although researchers sometimes scale eigenvectors so that its standard deviation is 1 (Chandrasekhar 2016; Banerjee et al. 2019). Of the two papers that have considered the statistical properties of regression on eigenvector centrality, Cai et al. (2021) sets the length to , claiming it to be a normalization. Le and Li (2020) does not fix the length, though their goal is essentially to recover the projection and not itself. We depart from the literature by leaving as a free parameter. We will analyse the properties of regression on eigenvector centrality, making their dependence on explicit. As we explain in Section 3.1, the choice of is not innocuous and can have implications for estimation and inference.

This paper focuses on the above three centrality measures, which are intimately related (Bloch et al. 2021). When , . Furthermore, as shown by Banerjee et al. (2019), if ,

We can thus understand the centrality measures as lying on a line, motivating our notational choice. Notably, we do not discuss betweenness and closeness centralities. These are path-based measures of centrality,which do not have clearly defined counterparts in the graphon. We conjecture that their analysis require a different statistical framework and defer it to future work.

Example 6 (continues=ex:leading).

In the context of risk sharing and social insurance, we can interpret

-

•

as the probability-weighted number of friends who will lend to or borrow from .

-

•

as the probability-weighted number of friends who will lend to or borrow from directly or through their friends. is the maximum length of the borrowing chain. For example if is , can borrow from friends of friends but not friends of friends of friends. is the increased difficulty of borrowing from a person that is one step further, e.g. of borrowing from friends of friends relative to borrowing from a friend directly.

-

•

as requiring the borrowing ability of to be proportional to the borrowing ability of their friends. Implicitly, this means agents can form borrowing chains that are arbitrarily long.

In the no measurement error case, the estimators of interest are:

Definition 4 (OLS Estimators without Measurement Error).

Suppose is observed. For , define the OLS estimators for to be

When networks are observed with errors, we assume that network centralities are estimated using in place of :

Definition 5 (Centralities with Measurement Error).

Suppose is observed but not . Define:

The corresponding OLS estimators are thus defined:

Definition 6 (OLS Estimators with Measurement Error).

Suppose is observed but not . For , define the OLS estimators for to be

Next, define the regression residuals.

Definition 7 (Regression Residuals).

For , define:

| (2) | ||||

| (3) |

We conclude this section by stating assumptions on the moments of conditional on :

Assumption 3.

Suppose

-

(a)

.

-

(b)

.

-

(c)

.

In the above assumption, (a) justifies linear regression. To see this, write:

where the middle equality follows from the fact that for some function . The subsequent equality follows because – or equivalently – are independently and identically distributed. Meanwhile, (b) and (c) control the amount of heterogeneity across different ’s. (c) implies the upper bound in (b). We introduce for notational convenience.

2.2 Sparse Network Asymptotics

To better capture the behavior of estimators when agents in the networks have few relationships with one another, we study their properties under sparse network asymptotics. Following Bollobás et al. (2007) and Bickel and Chen (2009), we want to consider settings in which as . is not an empirical quantity. It is a theoretical device to ensure that the sequence of models we consider remains sparse even as .

In many settings, a vector or matrix is said to be sparse if many of the entries are . In our setting, we say that and are sparse if their row sums – that is, the actual or observed degrees of agents respectively – are small. Because the entries of are restricted to be binary, having low degrees is the same as having many entries which are . We do not restrict the entries of , so that row sums could be small even if no entry takes value , as long as each non-zero entry is small. Sparsity of should therefore be understood as referring to low intensities of relationship between agents, but which gives rise to observed networks, , that are sparse in the conventional sense.

To see how gives rise to sparsity, suppose for example that . Then the network is dense and each agent has total relationships that are roughly of order in expectation. That is,

corresponding to a situation in which each agent is linked to many others. In practice, however, researchers may face sparse networks, in which each agent has few or weak relationships. Choosing leads to networks that remain sparse as increases. For example, if we set for some , then,

That is, each agent has a bounded number of relationships in expectation. A sequence of that goes to more quickly corresponds to data which is more sparse.

To understand the effect of sparsity on OLS estimation, we therefore study how the statistical properties of and change as we vary the rate at which . Our goal is to obtain theoretical results that better describe the properties of estimators under sparsity by explicitly modeling its effects. Such an approach has proven fruitful in statistics (e.g. in Bickel and Chen 2009; Bickel et al. 2011 and Wang 2020), but also in econometrics. Notably, Graham (2020b) lets a parameter analogous to here go to at rate to model the fact that individuals at an online market place purchase a bounded number of products in the limit, even though the selection tends to infinity.

A key motivation for our choice of framework is analytical tractability. Our definitions imply that conditional on , is a sparse inhomogeneous Erdos-Renyi graph, allowing us to borrow results from the random graph literature. However, modeling as comprising many low intensity links is also reasonable from an economic perspective. In the seminal paper titled “The Strength of Weak Ties”, Granovetter (1973) argues that lower intensity links, which constitute most of any given person’s relationships, are the key drivers of many important social and economic outcomes. For example, in tracing the network of job referrals, the author finds that 83% of recent job changers in a Boston suburb found their new jobs through friends whom they saw fewer than twice a week, and who were only “marginally included in the current network of contacts”. The author further notes: “It is remarkable that people receive crucial information from individuals whose very existence they have forgotten.” A series of empirical work has found evidence in favor of the weak ties theory across diverse applications such as innovation (e.g. Reagans and Zuckerman 2001), economic development (e.g. Eagle et al. 2010) and job referrals (e.g. Rajkumar et al. 2022). This theory lends credence to our econometric model, in which an unobserved network of weak ties not only drives economic effects but also generates a sparse observed network.

As a theoretical device, bears semblance to drifting alternatives in local power analysis (also known as Pitman drift; see Rothenberg 1984). Suppose we want to compare the power of tests for the hypothesis against . Asymptotic analysis with a fixed is not useful since consistent tests have power that converges to in probability under all alternatives, so that we cannot meaningfully differentiate between these tests. One interpretation of such a failure is that the asymptotic model fails to capture reality: in the limit, is large relative to the sampling noise which is of order . In practice, sampling noise can be large relative to the parameter of interest. Local power analysis employs the alternative hypothesis . As such, goes to at the same rate as sampling noise. Intuitively, as the sample size gets larger, the testing problem also becomes harder. The upshot is that the testing problem is non-trivial even in the limit, better modeling the finite sample problem.

A similar approach is taken in the weak instruments literature, which is concerned with the instrumental variable regressions in which the relevance condition is barely satisfied. To understand the resulting statistical pathologies, Staiger and Stock (1997) propose to model the strength of the instrument as decaying to at rate , so that strength of the signal in the first stage estimation is on par with sampling uncertainty. This approach has since led to long and productive lines of inquiry (see Andrews et al. 2019 and references therein).

Our drifting parameter serves a similar purpose: by letting , we better capture the statistical properties of estimators when networks are sparse. While we do not focus on any reference level of sparsity, comparing across levels of sparsity will prove instructive.

3 Theoretical Results

In this section, we present our theoretical results about the property of OLS estimators under varying amounts of sparsity. In Section 3.1, we characterize the level of sparsity at which consistency of and fails. The upshot is that measurement error renders OLS estimators less robust to sparsity. In particular, eigenvector centrality is less robust to sparsity than degree under measurement error. Section 3.2 presents distributional theory for and under regimes of sparsity for under which they are consistent. This leads to tools for bias correction and inference with sparse and noisily measured networks.

3.1 Consistency

This section presents the rates on at which and are consistent. We also discuss the role of in ensuring the consistency of and .

We first consider the case when the true network , is observed:

Theorem 1 (Consistency without Measurement Error).

As such, we have consistency of OLS for degree and diffusion centralities provided that the network is not too sparse. Under extreme sparsity, variation in becomes much smaller than variation in and it is not possible to learn about . In the case of eigenvector centrality, consistency requires conditions on the normalization factor but not on . This is because directly controls the variance of , so that it is able to undo the effect of sparsity in the absence of measurement error.

Our result is similar in spirit to Conley and Taber (2011), which studies the properties of difference-in-difference (DiD) estimators when there are few treated unit. In an asymptotic framework that takes the number of treated units to be fixed, the DiD estimator is similarly inconsistent in the limit. More generally, consistency of OLS with i.i.d. data requires , where is the variance of the regressor. Theorem 1 instantiates this condition for centrality regressions under sparsity.

Interestingly, the choice of matters even when the network is dense. To see why, suppose so that . Then . Note that it is independent of . We can then write:

Under our assumptions, . Therefore, is necessary for the consistency of .

The above example, together with Theorems 2 and 5 in the next section, makes clear that has important implications for the statistical properties of and . We can understand this phenomenon by analogy to OLS with i.i.d. observations, in which we are able to consistently estimate but not .

To our knowledge, we are the first to emphasize the importance in choosing appropriately. Cai et al. (2021), which studies eigenvector regressions under a different model for measurement error, sets to claiming it to be a normalization. In the formulation of Le and Li (2020), appears only implicitly and they do not prove consistency of . Instead, they show that . We remark that changing amounts to changing the definition of . The parameter of interest ultimately depends on the researcher. From the perspective of consistency, however, models with are strictly preferable to those with . And as we will see in Theorem 5, particular choices of may be useful for inference.

We next consider the case with measurement error:

Theorem 2 (Consistency with Measurement Error).

Theorem 2 gives the rates at which OLS regression on each centrality is consistent under measurement error. We summarize the rates from Theorems 2, together with that from 1, in Figure 1.

Under measurement error, is consistent under less sparsity than and , even when we set . In other words, is less robust to sparsity than and . This occurs because eigenvectors are poorly behaved under sparsity. The rate in Equation (4) arises because this is the point at which the leading eigenvector of ceases to be informative about the leading eigenvector of . To be specific, the rate in Equation (4) is the threshold for eigenvector delocalization. Above this threshold, eigenvectors of the noise ( in our case) are delocalized, meaning that each component is small and roughly of the same order. This ensures that the eigenvectors of is close to that of . Below this threshold, eigenvector localization occurs (Alt et al. 2021a). That is, the mass of the leading eigenvector concentrates on the agent who happens to have the largest realized degree, which is purely a result of chance. In turn, the leading eigenvector is also noise, rendering inconsistent. On the other hand, consistency of and only requires the mean of to concentrate to that of , which occurs as long as .

An important implication of our result is that centrality measures may have differing predictive value for outcomes in sparse regimes ,not only because they differ in economic significance, but also because they differ in statistical properties. In particular, suppose diffusion centrality leads to estimates which are significantly different from at some level , while eigenvector does not. If the underlying networks are sparse, it would be erroneous to conclude that diffusion centrality is structurally meaningful while eigenvector is not, since sparsity might be driving the observed results.

Finally, let us compare the rates in Theorem 2 with those in Theorem 1. As Figure 1 shows, measurement error renders OLS less robust to sparsity. While and are consistent as long as , and now require that . Whereas did not require any conditions on for consistency, does. Moreover, this requirement is more stringent than that on and . OLS on eigenvector centrality is therefore more sensitive to measurement error than on degree or diffusion.

Remark 2.

To improve the robustness of eigenvector centrality to sparsity, we can consider regularizing . Appendix C considers such an approach and finds that consistency with regularized eigenvector obtains when .

Remark 3.

Theorem 2 does not determine the behavior of when . Up to this threshold, we know by Alt et al. (2021b) that OLS is inconsistent only because the eigenvectors of are localized. To our knowledge, recent developments in random matrix theory do not provide any description of eigenvectors below threshold. As such, it is not clear what type of pathologies arises below and how that might affect the behavior of . Description of eigenvalues is more complete: below this point, we know that (see Alt et al. 2021a; Benaych-Georges et al. 2019; Benaych-Georges et al. 2020). Since the estimated eigenvalues are noise, we conjecture that the estimated eigenvectors are as well. If so, we would not expect to be consistent.

3.2 Distributional Theory

In this section, we study the asymptotic distributions of and under sparsity and measurement error. We focus on regimes of under which each estimator is consistent and find that measurement error still leads to asymptotic bias. Specifically,

Furthermore, the bias may be of larger order than the variance of in the sense that

In this case, it would not be possible to obtain a non-degenerate limiting distribution without bias correction. To see this, write:

Suppose we chose . Then , where is some non-degenerate distribution. However, diverges to or depending on the sign of . On the other hand, suppose we chose so that is bounded. Then since . That is, its limit is degenerate. Bias correction is thus necessary for inference.

We propose bias-correction and corresponding inference methods based on and . Bias correction is ineffective for . Instead, we propose a data-dependent choice of that leads to convenient properties. Appendix C provides an alternative strategy for regularizing eigenvector centrality.

3.2.1 Centralities without Measurement Error ()

Our first result states that heteroskedasticity-consistent (hc) or robust -statistics yield vaild inference in the absence of measurement error.

Theorem 3.

Our formulation of the -statistic highlights that inference on and does not require the sparsity parameter to be specified. This is important since is in general not identified (Bickel et al. 2011) and follows from the convenient fact that the -statistic is self-normalizing. Intuitively, the sparsity terms in the numerator and the denominator are of the same order, so that they “cancel out”. Hansen and Lee (2019) makes a similar observation in the context of cluster-dependent data: although the means of such data converge at a rate that changes based on the dependence structure within each cluster, this rate does not need to be known for estimation and inference, due to the aforementioned self-normalizing property.

We note that , . These are the rates of convergence for and respectively. In the absence of sparsity (i.e. if = 1), the rate of convergence is faster than . This is because having a network amounts to observations. Asymptotically, the regressor has much more variation than the regression error , leading to the higher rate of convergence. Finally, we note that .

In the presence of measurement error, however, the above result does not obtain. The next two subsections presents distributional theory for and , and .

3.2.2 Degree and Diffusion Centrality under Measurement Error (, )

For and , measurement error leads to bias and also slows down the rate of convergence. This is the content of the following theorem:

Theorem 4 (Inference – Degree and Diffusion).

Our results are stated in terms of and – estimators for bias and variance – though they should be understood as statements about the true bias and variance of the estimators in combination with statements about estimation feasibility. Note also that results for specializes to that for when setting .

When (case (c)), our result asserts that the hc/robust variance estimator is consistent for the variance of . However, that is no longer the case when then (cases (a) and (b)). Here, we find that become biased. That is, is not centered at . The bias of comprises only one term. However, bias for comprises an exponentially growing number of terms. In addition to eigenvector localization, this provides another intuitive explanation for the poor properties of the eigenvector centrality, since as Banerjee et al. (2019) proves, can be considered the limit of diffusion centrality as . Comparing cases (a) and (b) with (c) also shows that the asymptotic distributions for are discontinuous in at .

Additionally, we see that the asymptotic variance of differs from that which is estimated by hc/robust standard error. Note that the difference in asymptotic variance is not the result of bias estimation. In particular, replacing with its limit in probability will not change the asymptotic variance of . This stands in contrast to settings such as Regression Discontinuity Design, in which estimation of the asymptotic bias leads to larger asymptotic variance in the relevant test statistic (Calonico et al. 2014). In order to not alter the asymptotic variance, bias must be estimated at a sufficiently fast rate. This is not trivial for . Bias of the comprises terms of the form . However, the naive plug-in estimator does not converge sufficiently fast for . Using the fact that is a good estimator of , we recursively construct good estimators for when , which can then be used to construct . The resulting estimator does not have a closed form expression. We provide explicit formula for in Tables 9 and 10.

Hypothesis Testing

Our theory suggests the following test for . Consider testing the hypothesis against by

where is the CDF of the standard normal distribution. One-sided tests can be constructed by modifying the rejection rule in the usual way. It is immediate that:

Corollary 1 (Inference for and ).

If , .

When , needs to be centered by subtracting instead of . We will refer to this form of centering as bias correction for . As we explained at the start of Section 3, bias correction is necessary for to attain a non-degenerate limiting distribution when asymptotic bias is of larger order than variance. Indeed, . As such, if ,division by blows up .

In the bias for , terms with larger ’s dominate those with smaller ’s. When is dense enough, terms with small ’s may actually much smaller than so that they can be ignored. With only the stipulation that however, a non-degenerate asymptotic distribution can only be achieved when all terms are included.

Confidence Intervals

Because estimates variance only when , the usual confidence intervals based on need not attain nominal coverage. This failure occurs for two countervailing reasons. Firstly, the quantity is meant to estimate,

However, under-estimates variance of when . That is,

On the other hand, the bias in means that

The second term in the above equation can be large, such that may exceed . This turns out to be the case in our application in Section 5.

To obtain confidence intervals for consider the following:

Definition 8.

For and a given , let

and

Finally, let .

The following is immediate:

Corollary 2 (Confidence Interval).

We can obtain one-sided confidence intervals by modifying the bounds as usual. More generally, as long as is a confidence interval for and is a confidence interval when , their unions will produce a confidence interval for unconditionally. In particular, it is always valid to set . This can be useful when it is not important to exclude from the confidence interval. For example, suppose we want one-sided confidence intervals that upper bounds . We can then consider using

If , . For the reasons discussed above, we can also have

As before, such a situation arises in our application (Section 5).

Bias Correction

Since the bias of the OLS estimators and can be estimated, it is reasonable to consider the following bias-corrected estimators:

Definition 9 (Bias-Corrected Estimators).

For , define

Bias-corrected estimators have faster rates of convergence:

Corollary 3.

Suppose . For ,

For reference, .

3.2.3 Eigenvector Centrality under Measurement Error ()

We next consider inference on . Eigenvector centrality can be badly biased under sparsity, which makes inference challenging. However, strategic choices of can overcome many of these issues. We first introduce the following simplifying assumption:

Assumption E2 (Finite Rank).

Suppose has rank :

| (6) |

where for all and if ,

Furthermore, suppose that

In Equation (6), we express in terms of its eigenfunctions . Assumption E2 implies that the true network has low-dimensional structure and is satisfied by many popular network models, such as the stochastic block model (Holland et al. 1983, also see Example 7 below) and random dot product graphs (Young and Scheinerman 2007). This assumption is also commonly found in the networks literature (e.g. Levin and Levina 2019; Li et al. 2020), and the matrix completion literature more generally (e.g. Candès and Tao 2010; Negahban and Wainwright 2012; Chatterjee 2015; Athey et al. 2021). Importantly, existing papers on inference with eigenvectors (Le and Li 2020; Cai et al. 2021) also make this assumption. Note also that Assumption E2 implies Assumption E1.

Example 7 (Stochastic Block Model).

The Stochastic Block Model (SBM) is one of the earliest statistical models of networks. It assumes that individuals fall into groups and that the true network depends only on group membership. For example, suppose that a classroom has two groups: jocks, nerds. The SBM posits that the strength of the tie between any jock and any nerd are the same. Analogously for that between any two jocks or any two nerds, though all three ties can be of different intensity. Suppose the proportion of each group is and that the link probability is . Then the graphon is a step-function on with -steps and rank . It is visualized in Figure 2.

With the low-rank asumption, we can consider the asymptotic distribution of in a few cases.

Theorem 5 (Inference – Eigenvector).

Note that the statistics above do not require or to be specified. This is useful since estimating may be challenging in addition to being unidentified (Bickel et al. 2011).

Our result describes the asymptotic distribution , which depends on and . Case (a) gives conditions under which inference with hc/robust -statistic is appropriate. As with and , the usual test works if . However, it also works if provided that is small. On the other hand, if is large, case (b) suggests that we get behavior that is more in line with that of and when target parameters are non-zero. However, to obtain the result in case (b), we require very strong conditions on due to greater difficulty in controlling the behavior of estimated eigenvector, as the discussion following Theorem 4 explains.

When , the differences in case (a) and (b) arise because controls the relative sizes of network measurement error and regression error. The latter dominates if is sufficiently small and has the advantage of being easy to characterize. Hence, in the absence of compelling reasons for choosing to be other values, researchers can consider choosing for statistical convenience. In particular, if is chosen so that case (a) obtains, then usual hc/robust variance estimator based -statistic and confidence interval have the expected properties. We propose such an below. However, we stress that a smaller also implies a lower rate of convergence. In effect, we are changing the model from one with faster but unknown rate of convergence, to one with a rate that is slower but estimable.

Finally, our result here suggests the use of the bias-corrected estimator, as with degree and diffusion centrality:

Choice of

The following data-dependent choice is convenient:

Corollary 4.

Suppose is estimated. If satisfies Equation (7),

Since , the above choice of satisfies the conditions in case (a)(iii) of Theorem 5, accommodating close to the maximum possible amount of sparsity for . It also obviates the need for bias correction since the bias is always of lower order than the variance at this rate. Furthermore, such an has intuitive appeal since it implies that

In words, scaling the estimated eigenvectors to means that the outer product of is the best rank-1 approximation of . In proposing eigenvector centrality, Bonacich (1972) in fact cites this property as one of the key motivations, arguing that can be interpreted as the “social interaction potential” of a given agent.

Remark 4.

Remark 5.

Le and Li (2020) provides methods for testing the hypothesis when . They accommodate regressions on multiple eigenvectors, but in a setting with only one eigenvector, their result asserts that the -statistic with the homoskedastic variance estimator can be used to test the hypothesis that . Theorem 5 does not cover regression on multiple eigenvectors but it accommodates greater sparsity and facilitates tests of for .

4 Simulations

In this section, we present simulation evidence to support our theory. We will consider the unobserved adjacency matrix defined as

In other words, the graphon is . The observed adjacency matrix is , where for , . , .

Our regression model is:

where are centrality measures calculated on . In this simulation, we draw , , where and for all . We will set . As before, is used when is observed, and is used when only is observed.

We revisit our three sets of results in turn: inconsistency under sparsity, bias correction and normal approximation.

4.1 Inconsistency Under Sparsity

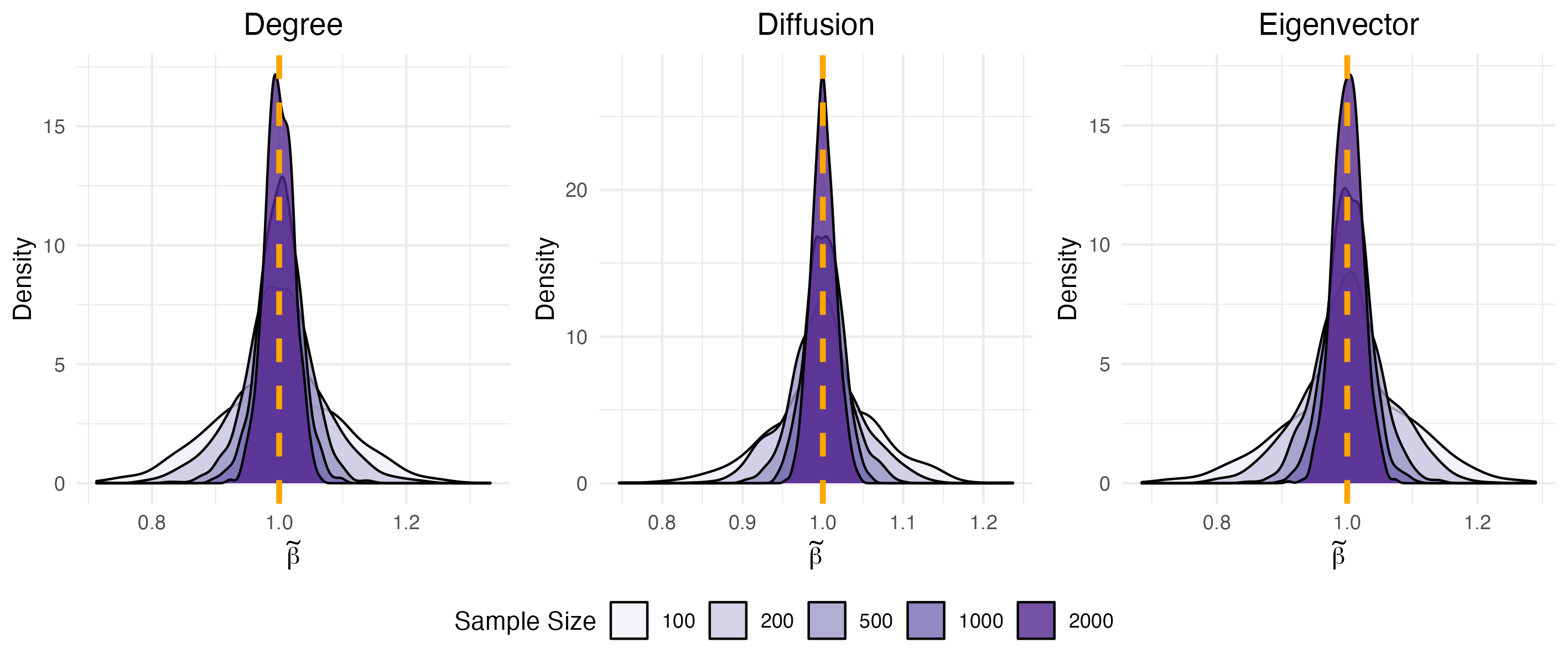

The first regime of interest is . Theorem 1 asserts that and are consistent. is consistent provided that for eigenvector centrality.

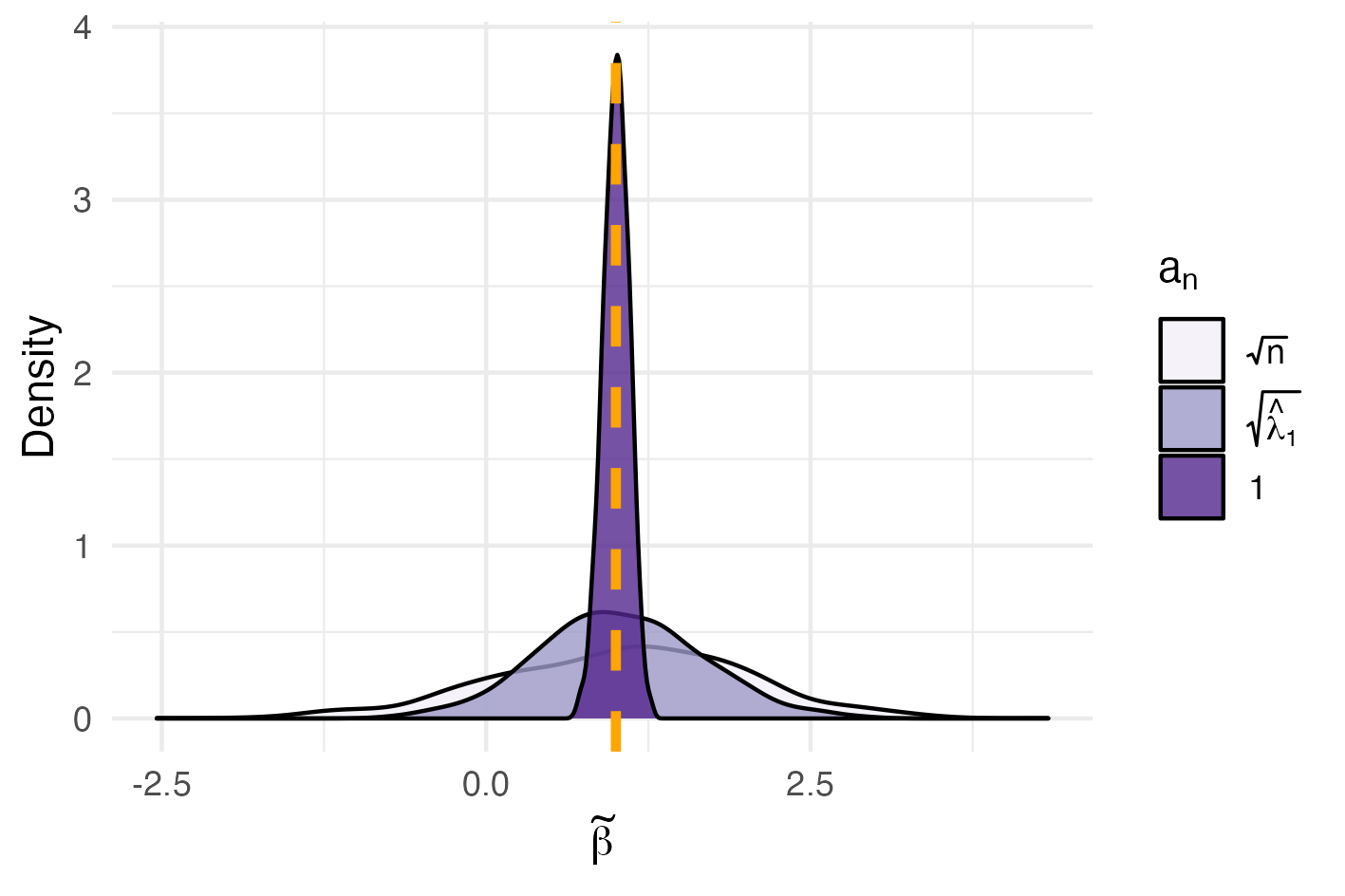

We start with the last claim, which is supported by Figure 5. For , we see that the choice of scaling clearly affects how well the estimator is able to concentrate around . The plots for larger values of are qualitatively similar. This also hints at the trade-off that made in Theorem 5: we can choose so that the distribution of is easy to characterize, but this will slow down the rate of convergence. Since this subsection concerns current practice, we will set for its remainder.

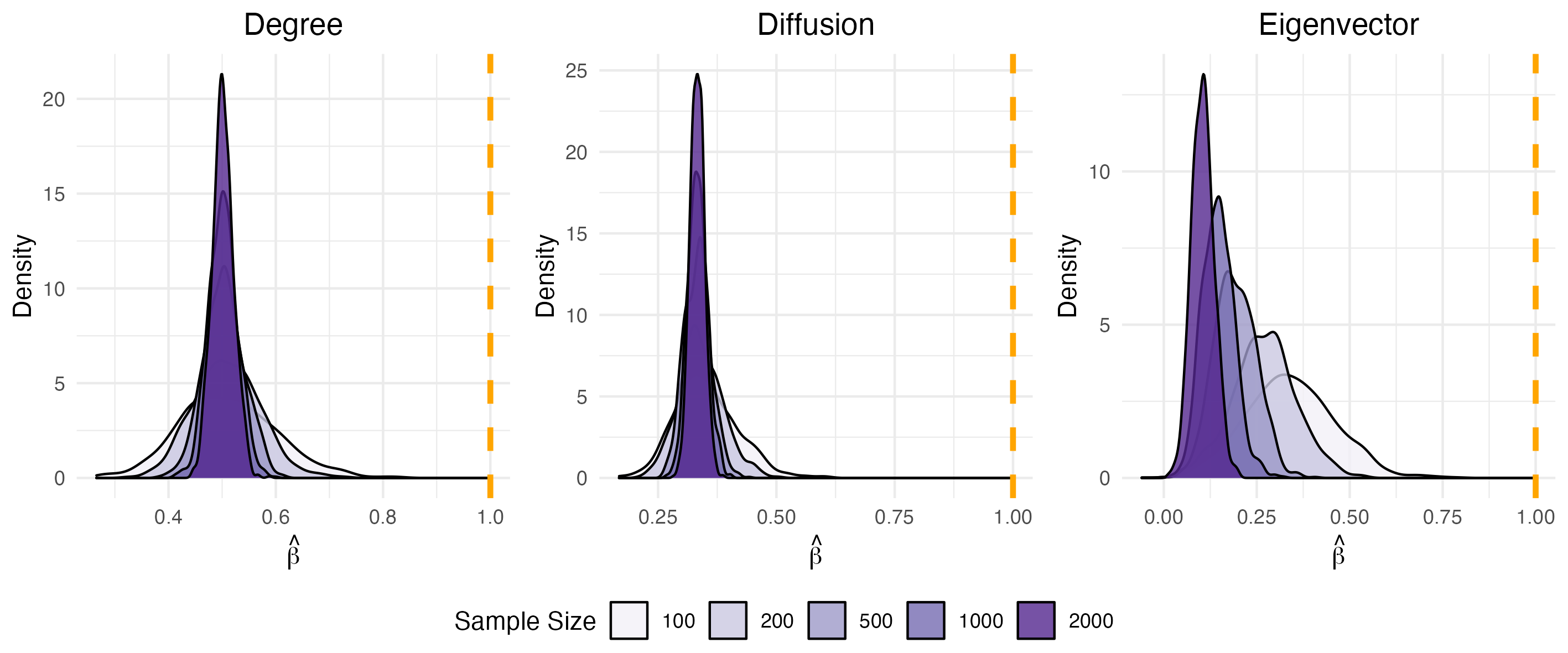

We return to the first claim concerning consistency of when . Figure 5 indeed shows the distribution of for each . The estimators concentrate around as increases, in line with our result. However, Theorem 2 asserts that , and are all inconsistent when . Their distributions, presented in Figure 5, concords with our result. Indeed, we see that and are attenuated by constant amount as , while converges in probability to .

Finally, we consider the case when . In this regime, and are consistent but is not. We see suggestive evidence of this in Figure 7, where is drifting further away from as increases. The opposite occurs with and . Though the rate of convergence is slow, it is visible.

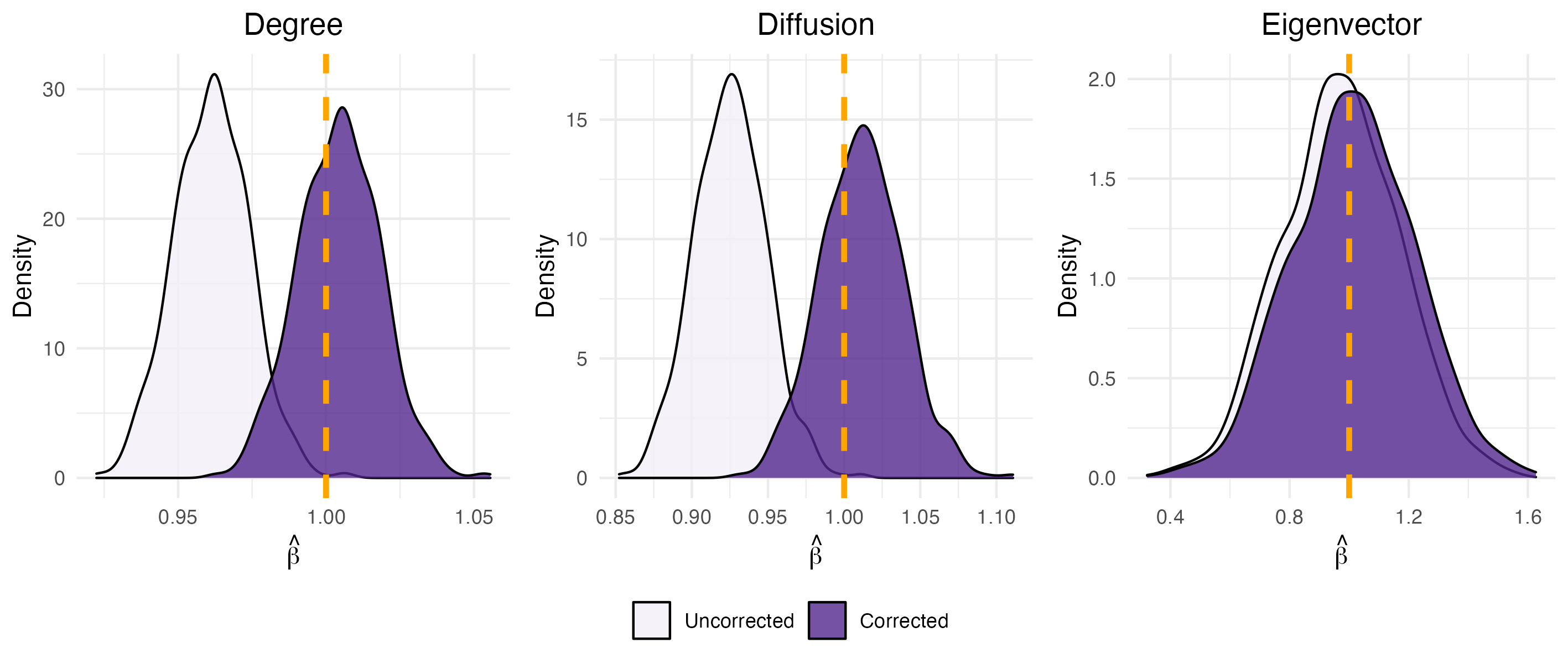

4.2 Bias Correction

Even in regime dense enough such that , and are consistent, they can still be subject to biases that affect their rates of convergence. This motivates the bias-corrected estimators in Definition 9. In this subsection, we study the effects of bias correction in the regime .

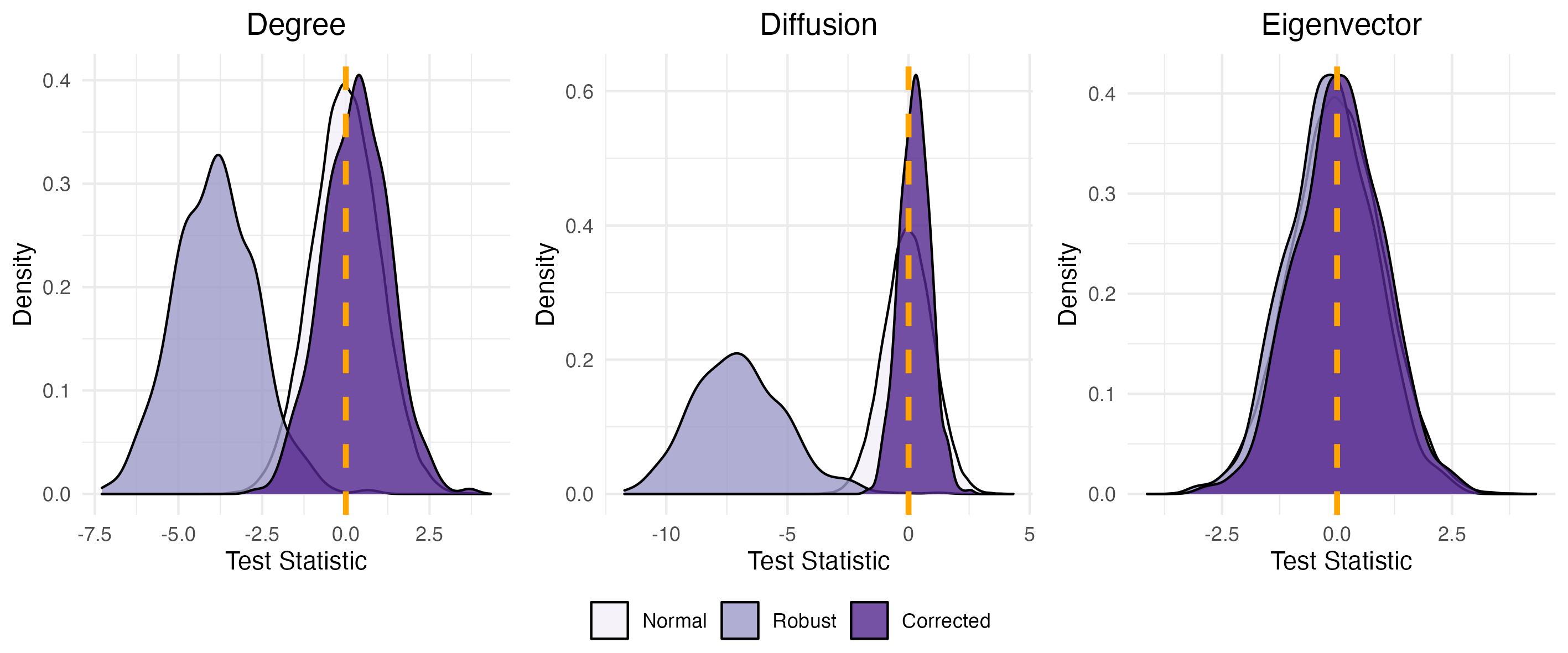

4.3 Distributional Theory

Finally, we investigate the quality of the normal approximations proposed in Theorems 4 and 5. As before, we consider the regime . Figure 8 presents the distribution of test statistics (in purple) which our theorems predict have the standard normal distribution (in gray). We see that the two distributions are indeed close. It is also common for applied researcher to compute the usual -statistic with heteroskedaticity consistent (robust) standard errors and conduct inference under the assumption that it has a standard normal distribution. For comparison, we include the distribution of the t-statistic (in lavender). Corollary 4 justifies the use of this statistic when but our theory for degree and diffusion centralities is based on a different statistic. Indeed, we see that the robust -statistic can be quite far from the standard normal distribution in both location and dispersion. This suggests that our method would lead to more reliable tests.

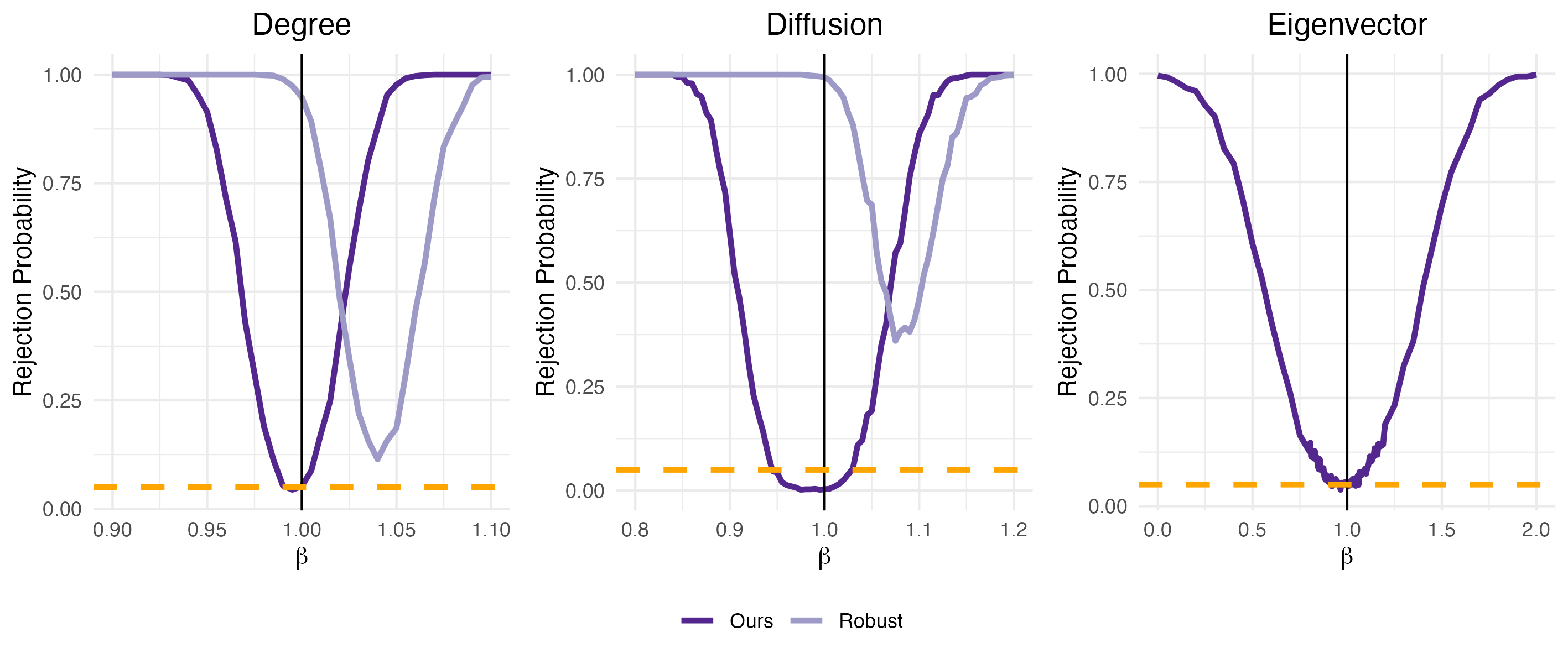

We next examine the size and power of tests based on our distributional theory. We consider testing the hypothesis against at 5% level of significance. Table 1 presents size of the test when is correctly specified. For degree and diffusion centralities, our theory provides test statistics which differ from the robust -statistic. As we see from the table, the test for degree controls size well. The test for diffusion centrality is more conservative. This is because our estimator is upward-biased in finite sample when there are no other covariates. Tests for degree and diffusion centralities that are based on the robust -statistic has Type I error over 50% across all sample sizes. For eigenvector centrality, our theory predicts that the robust -statistic will perform well Indeed, it has size close to 5%. We also consider testing the hypothesis . Power for this test is presented in Table 2. For this null hypothesis, our theory suggests the use of the robust -statistic. Reassuringly, the tests all have power close to . To understand how power changes as we vary the alternative hypothesis, we hone in on the case where and . Figure 9 presents the rejection probability of our test under various alternatives. We see that the our tests control size and have good power. Comparatively, tests based on the robust -statistic have poor size control when . Furthermore, they can have poor power against particular alternatives owing to the bias. We conclude that our tests have desirable properties and are preferred to the test with robust -statistic when networks are sparse and observed with noise.

| Statistic | Sample Size | ||||||||||

| 100 | 200 | 500 | 1000 | 2000 | |||||||

| 0.1 | Degree | Ours | 0.055 | 0.052 | 0.067 | 0.062 | 0.065 | ||||

| Robust | 0.573 | 0.645 | 0.680 | 0.662 | 0.670 | ||||||

| Diffusion | Ours | 0.010 | 0.004 | 0.007 | 0.003 | 0.004 | |||||

| Robust | 0.859 | 0.883 | 0.883 | 0.868 | 0.897 | ||||||

| Eigenvector | 0.054 | 0.060 | 0.046 | 0.052 | 0.046 | ||||||

| Degree | Ours | 0.066 | 0.065 | 0.067 | 0.058 | 0.065 | |||||

| Robust | 0.286 | 0.422 | 0.556 | 0.701 | 0.778 | ||||||

| Diffusion | Ours | 0.006 | 0.001 | 0.002 | 0.008 | 0.003 | |||||

| Robust | 0.621 | 0.729 | 0.805 | 0.888 | 0.933 | ||||||

| Eigenvector | 0.045 | 0.055 | 0.050 | 0.056 | 0.038 | ||||||

| Degree | Ours | 0.072 | 0.049 | 0.051 | 0.037 | 0.062 | |||||

| Robust | 0.580 | 0.761 | 0.944 | 0.993 | 0.999 | ||||||

| Diffusion | Ours | 0.015 | 0.009 | 0.005 | 0.001 | 0.004 | |||||

| Robust | 0.863 | 0.944 | 0.993 | 1.000 | 1.000 | ||||||

| Eigenvector | 0.053 | 0.049 | 0.036 | 0.067 | 0.056 | ||||||

| Statistic | Sample Size | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 200 | 500 | 1000 | 2000 | ||||||

| 0.1 | Degree | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | ||||

| Diffusion | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| Eigenvector | 0.880 | 0.993 | 1.000 | 1.000 | 1.000 | |||||

| Degree | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| Diffusion | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| Eigenvector | 0.994 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| Degree | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| Diffusion | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| Eigenvector | 0.860 | 0.972 | 0.997 | 1.000 | 1.000 | |||||

5 Empirical Demonstration

In this section, we demonstrate the relevance of our theoretical findings via an application inspired by De Weerdt and Dercon (2006).222The data is obtained from Joachim De Weerdt’s website: https://www.uantwerpen.be/en/staff/joachim-deweerdt/public-data-sets/nyakatoke-network/. In the developing world, social insurance is an important mechanism for smoothing consumption, because of restricted access to formal credit markets (Rosenzweig 1988; Udry 1994; Fafchamps and Lund 2003; Kinnan and Townsend 2012, among many others). De Weerdt and Dercon (2006) examines the case of Nyakatoke, a village with 120 households in rural Tanzania, and find that social insurance helps households to smooth consumption following health shocks. The data they use comprises five rounds of panel data on household consumption, illness among other covariates, collected from February to December 2000. The authors also had access to social network data collected during the first round of the survey, in which households were asked for the identities of those who they depend on or depend on them for help. The authors then regress a household’s change in consumption following illness on the mean consumption of their network neighbors, finding evidence of positive co-movements.

Another way to demonstrate the effect of social insurance on consumption smoothing could be to regress variance in consumption on network centrality measures. Specifically, the regression:

where is variance in food expenditure and is a centrality measure. The above regression could be preferred to the authors’ specification if we are unsure about the covariates that reflect social assistance. For example, it might be a household’s stock of savings that co-move with the decision to lend to their friends, rather than their own consumption. We might also be interested in more complex patterns of assistance, which could be summarized in an appropriate centrality measure, but which might not be tractable with covariates.

The above regression requires information on network of social insurance, in which each entry records the probability lends money to over the survey period. We can consider obtaining proxies for this network using one of the following:

-

Unilateral Social (US). if either or names the other household as a party that they could depend on or which depends on them for help.

-

Bilateral Social (BS). only if both and names the other household as a party that they could depend on or which depends on them for help.

-

Unilateral Financial (UF). if either or lends money to the other at least once over the survey period.

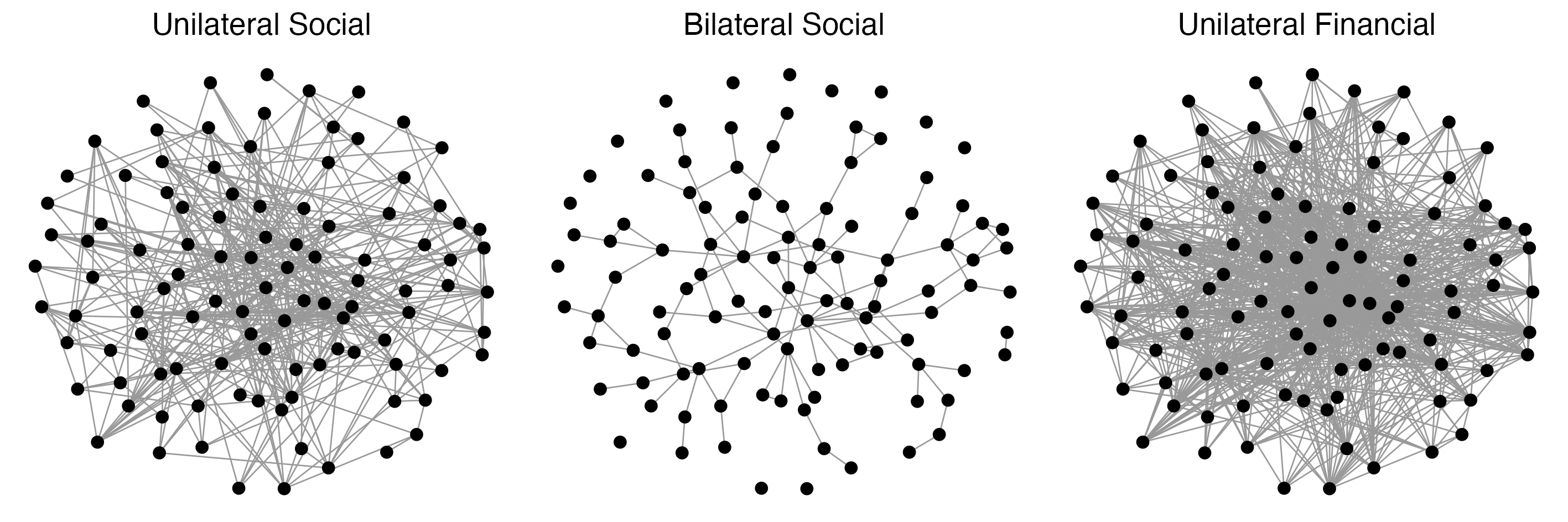

The authors study US and BS. We also consider UF since self-reported loan data is available. The networks are plotted in Figure 10 and the degree distributions are described in Table 3. In a village with households, mean degree in all three networks are less than . We might therefore be concerned that . By construction, US is much less dense than BS. Due to the availability of five panels, UF is denser than the other two.

| () | Mean | Median | Min | Max |

|---|---|---|---|---|

| Unilateral Social | 8.10 | 7 | 0 | 31 |

| Bilateral Social | 2.32 | 2 | 0 | 10 |

| Unilateral Transfer | 10.48 | 8 | 1 | 77 |

Regression results are presented in Table 4. In this exercise, , and . We first note that estimated attenuation factor is the smallest (i.e. furthest from 1) in the sparsest network BS. This is in line with our result that bias is . Diffusion centrality is generally estimated to be less attenuated, because is small . As the last column shows, bias correction can lead to substantially different estimates. Table 4 also presents -values for tests of the two-sided hypothesis that . Centrality statistics on BS appears to be more predictive of the variance in food consumption than that on US and UF. This highlights that researchers should not choose their network proxies on the criteria of sparsity alone. In the case of Nyakatoke, evidence suggests that US reflects “desire to link”, rather than actual risk-pooling (Comola and Fafchamps 2014), such that US is a noisier proxy than BS. By the same account, the large number of discrepancies between reporting by borrowers and lenders of the same loan suggests that the loan data is subject to severe mis-reporting (Comola and Fafchamps 2017), rendering it an equally poor proxy. Among the centrality statistics on BS, eigenvector has the least predictive power by far. We reiterate our warning that eigenvector centrality is less robust to sparsity than degree and diffusion, such that the -values might reflect the poor statistical properties of the measure, rather than its lack of economic significance.

| Estimate | p-value | Atten. | Bias Corr. | ||

|---|---|---|---|---|---|

| Unilateral Social | Degree | -1064 | 0.67 | 0.91 | -1172 |

| Diffusion | -4274 | 0.77 | 1.00 | -4292 | |

| Eigenvector | -12353 | 0.86 | 0.91 | -13548 | |

| Bilateral Social | Degree | -11604 | 0.06 | 0.74 | -15592 |

| Diffusion | -23672 | 0.16 | 0.94 | -25212 | |

| Eigenvector | -10543 | 0.93 | 0.78 | -13434 | |

| Unilateral Financial | Degree | -412 | 0.70 | 0.96 | -429 |

| Diffusion | -4559 | 0.74 | 1.00 | -4561 | |

| Eigenvector | -15040 | 0.77 | 0.96 | -15699 |

Finally, we present one-sided confidence intervals for values of based on our results. These are useful for putting bounds on parameter values. In our example, a lower bound could be intuitively interpreted as the limits to informal risk-sharing, a quantity which could be useful for policymakers deciding whether or not to provide agricultural insurance. We focus on BS since it appears to be the only informative network. Results for degree and diffusion are presented in Table 5. Our confidence intervals leads to tighter lower bound than the those based on the robust -statistic. Results for eigenvector are omitted since our theory is based on the usual robust -statistic.

| 90% | 95% | 99% | ||

|---|---|---|---|---|

| Degree | Ours | (-18835, ) | (-20015, ) | (-22680, ) |

| Robust | (-25050, ) | (-28862, ) | (-36012, ) | |

| Diffusion | Ours | (-34715, ) | (-38867, ) | (-50112, ) |

| Robust | (-56938, ) | (-66368, ) | (-84058, ) |

6 Conclusion

In this paper, we studied the properties of linear regression on degree, diffusion and eigenvector centrality when networks are sparse and observed with error. We show that these issues threaten the consistency of OLS estimators and characterize the amount of sparsity at which inconsistency occurs. In doing so, we find that eigenvector centrality is less robust to sparsity than the others and that the statistical properties of the corresponding regression is sensitive to the scaling.

Additionally, we show that an asymptotic bias arises whenever the true slope parameter is not and that the bias can be of larger order than the variance, so that bias correction is necessary to obtain a non-degenerate limiting distribution from the OLS estimator. Finally, we provide estimators for the bias and variance which, together with our central limit theorem, facilitates inference under sparsity and measurement error. We confirm our theoretical results via simulations, which suggest that our approximation result works better for estimation and inference when networks are sparse, particularly when compared to the use of robust standard errors and the associated -statistics. Finally, we demonstrate the relevance of our theoretical results by studying the social insurance network in Nyakatoke, Tanzania.

In sum, our results suggest that applied researchers view their results with caution when applying OLS to sparse, noisy networks. Specifically, comparing the statistical significance of eigenvector centrality with degree or diffusion may yield misleading conclusions since they differ not only in economic significance but also statistical properties. Provided that the networks are not too sparse, the usual -test is valid for null hypothesis that the slope parameter is . However, alternative inference procedures will be necessary for other null hypotheses. Additionally, there may be scope for improving estimation by the use of bias-corrected estimators. Estimation and inference under extreme sparsity remains an open question, though as (Le et al. 2017) show, parametric models such as the Stochastic Block Model may point to a way forward.

References

- Adcock (1878) Adcock, R. J. (1878). A problem in least squares. The Analyst 5(1), 53–54.

- Aldous (1981) Aldous, D. J. (1981). Representations for partially exchangeable arrays of random variables. Journal of Multivariate Analysis 11(4), 581–598.

- Alt et al. (2021a) Alt, J., R. Ducatez, and A. Knowles (2021a). Extremal eigenvalues of critical Erdős–Rényi graphs. The Annals of Probability 49(3), 1347–1401.

- Alt et al. (2021b) Alt, J., R. Ducatez, and A. Knowles (2021b). Poisson statistics and localization at the spectral edge of sparse Erdős–Rényi graphs. arXiv preprint arXiv:2106.12519.

- Andrews et al. (2019) Andrews, I., J. H. Stock, and L. Sun (2019). Weak instruments in instrumental variables regression: Theory and practice. Annual Review of Economics 11(1).

- Athey et al. (2021) Athey, S., M. Bayati, N. Doudchenko, G. Imbens, and K. Khosravi (2021). Matrix completion methods for causal panel data models. Journal of the American Statistical Association 116(536), 1716–1730.

- Banerjee et al. (2013) Banerjee, A., A. G. Chandrasekhar, E. Duflo, and M. O. Jackson (2013). The diffusion of microfinance. Science 341(6144), 1236498.

- Banerjee et al. (2019) Banerjee, A., A. G. Chandrasekhar, E. Duflo, and M. O. Jackson (2019). Using gossips to spread information: Theory and evidence from two randomized controlled trials. The Review of Economic Studies 86(6), 2453–2490.

- Benaych-Georges et al. (2019) Benaych-Georges, F., C. Bordenave, and A. Knowles (2019). Largest eigenvalues of sparse inhomogeneous Erdős–Rényi graphs. The Annals of Probability 47(3), 1653–1676.

- Benaych-Georges et al. (2020) Benaych-Georges, F., C. Bordenave, and A. Knowles (2020). Spectral radii of sparse random matrices. In Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, Volume 56, pp. 2141–2161. Institut Henri Poincaré.

- Bickel and Chen (2009) Bickel, P. J. and A. Chen (2009). A nonparametric view of network models and Newman–Girvan and other modularities. Proceedings of the National Academy of Sciences 106(50), 21068–21073.

- Bickel et al. (2011) Bickel, P. J., A. Chen, and E. Levina (2011). The method of moments and degree distributions for network models. The Annals of Statistics 39(5), 2280–2301.

- Bloch et al. (2021) Bloch, F., M. O. Jackson, and P. Tebaldi (2021). Centrality measures in networks. arXiv preprint arXiv:1608.05845.

- Bollobás et al. (2007) Bollobás, B., S. Janson, and O. Riordan (2007). The phase transition in inhomogeneous random graphs. Random Structures & Algorithms 31(1), 3–122.

- Bonacich (1972) Bonacich, P. (1972). Factoring and weighting approaches to status scores and clique identification. Journal of mathematical sociology 2(1), 113–120.

- Borgs et al. (2018) Borgs, C., J. T. Chayes, H. Cohn, and N. Holden (2018). Sparse exchangeable graphs and their limits via graphon processes. Journal of Machine Learning Research 18, 1–71.

- Bourlès et al. (2021) Bourlès, R., Y. Bramoullé, and E. Perez-Richet (2021). Altruism and risk sharing in networks. Journal of the European Economic Association 19(3), 1488–1521.

- Bramoullé and Genicot (2018) Bramoullé, Y. and G. Genicot (2018). Diffusion centrality: Foundations and extensions.

- Breza et al. (2019) Breza, E., A. Chandrasekhar, B. Golub, and A. Parvathaneni (2019). Networks in economic development. Oxford Review of Economic Policy 35(4), 678–721.

- Cai et al. (2021) Cai, J., D. Yang, W. Zhu, H. Shen, and L. Zhao (2021). Network regression and supervised centrality estimation. Available at SSRN 3963523.

- Calonico et al. (2014) Calonico, S., M. D. Cattaneo, and R. Titiunik (2014). Robust nonparametric confidence intervals for regression-discontinuity designs. Econometrica 82(6), 2295–2326.

- Candès and Tao (2010) Candès, E. J. and T. Tao (2010). The power of convex relaxation: Near-optimal matrix completion. IEEE Transactions on Information Theory 56(5), 2053–2080.

- Carvalho et al. (2021) Carvalho, V. M., M. Nirei, Y. U. Saito, and A. Tahbaz-Salehi (2021). Supply chain disruptions: Evidence from the great east japan earthquake. The Quarterly Journal of Economics 136(2), 1255–1321.

- Carvalho and Tahbaz-Salehi (2019) Carvalho, V. M. and A. Tahbaz-Salehi (2019). Production networks: A primer. Annual Review of Economics 11, 635–663.

- Chandrasekhar (2016) Chandrasekhar, A. (2016). Econometrics of network formation. The Oxford handbook of the economics of networks, 303–357.

- Chandrasekhar and Lewis (2016) Chandrasekhar, A. and R. Lewis (2016). Econometrics of sampled networks. Working Paper.

- Chatterjee (2015) Chatterjee, S. (2015). Matrix estimation by universal singular value thresholding. The Annals of Statistics 43(1), 177–214.

- Chen et al. (2011) Chen, L. H., L. Goldstein, and Q.-M. Shao (2011). Normal approximation by Stein’s method, Volume 2. Springer.

- Chen et al. (2021) Chen, Y., C. Cheng, and J. Fan (2021). Asymmetry helps: Eigenvalue and eigenvector analyses of asymmetrically perturbed low-rank matrices. Annals of statistics 49(1), 435.

- Cheng et al. (2021) Cheng, C., Y. Wei, and Y. Chen (2021). Tackling small eigen-gaps: Fine-grained eigenvector estimation and inference under heteroscedastic noise. IEEE Transactions on Information Theory 67(11), 7380–7419.

- Chesher (2003) Chesher, A. (2003). Identification in nonseparable models. Econometrica 71(5), 1405–1441.

- Comola and Fafchamps (2014) Comola, M. and M. Fafchamps (2014). Testing unilateral and bilateral link formation. The Economic Journal 124(579), 954–976.

- Comola and Fafchamps (2017) Comola, M. and M. Fafchamps (2017). The missing transfers: Estimating misreporting in dyadic data. Economic Development and Cultural Change 65(3), 549–582.

- Conley and Taber (2011) Conley, T. G. and C. R. Taber (2011). Inference with “difference in differences” with a small number of policy changes. The Review of Economics and Statistics 93(1), 113–125.

- Cruz et al. (2017) Cruz, C., J. Labonne, and P. Querubin (2017). Politician family networks and electoral outcomes: Evidence from the philippines. American Economic Review 107(10), 3006–37.

- De Paula (2017) De Paula, A. (2017). Econometrics of network models. In Advances in economics and econometrics: Theory and applications, eleventh world congress, pp. 268–323. Cambridge University Press Cambridge.

- De Paula et al. (2020) De Paula, A., I. Rasul, and P. Souza (2020). Recovering social networks from panel data: identification, simulations and an application.

- De Weerdt and Dercon (2006) De Weerdt, J. and S. Dercon (2006). Risk-sharing networks and insurance against illness. Journal of development Economics 81(2), 337–356.

- DeGroot (1974) DeGroot, M. H. (1974). Reaching a consensus. Journal of the American Statistical association 69(345), 118–121.

- Dong et al. (2020) Dong, H., N. Chen, and K. Wang (2020). Modeling and change detection for count-weighted multilayer networks. Technometrics 62(2), 184–195.

- Eagle et al. (2010) Eagle, N., M. Macy, and R. Claxton (2010). Network diversity and economic development. Science 328(5981), 1029–1031.

- Eldridge et al. (2018) Eldridge, J., M. Belkin, and Y. Wang (2018). Unperturbed: spectral analysis beyond davis-kahan. In Algorithmic Learning Theory, pp. 321–358. PMLR.

- Evdokimov (2010) Evdokimov, K. (2010). Identification and estimation of a nonparametric panel data model with unobserved heterogeneity. Technical report, Citeseer.