Modelling Large Dimensional Datasets with Markov Switching Factor Models

Abstract

We study a novel large dimensional approximate factor model with regime changes in the loadings driven by a latent first order Markov process. By exploiting the equivalent linear representation of the model, we first recover the latent factors by means of Principal Component Analysis. We then cast the model in state-space form, and we estimate loadings and transition probabilities through an EM algorithm based on a modified version of the Baum-Lindgren-Hamilton-Kim filter and smoother that makes use of the factors previously estimated. Our approach is appealing as it provides closed form expressions for all estimators. More importantly, it does not require knowledge of the true number of factors. We derive the theoretical properties of the proposed estimation procedure, and we show their good finite sample performance through a comprehensive set of Monte Carlo experiments. The empirical usefulness of our approach is illustrated through an application to a large portfolio of stocks.

Keywords: Large Factor Model, Markov Switching, Baum-Lindgren-Hamilton-Kim Filter and Smoother, Principal Component Analysis, Stock Returns.

JEL Codes: C34, C38, C55, G10.

1 Introduction

This paper develops a comprehensive approach for the analysis of large dimensional models exhibiting an approximate factor structure, in which the loadings are subject to regime shifts driven by a first order latent Markov process. We label these large dimensional Markov Switching factor models.

Since the works of Hamilton (1989), and Diebold and Rudebusch (1996), and inspired by the seminal paper of Goldfeld and Quandt (1973), Markov switching models have been widely used in the empirical analysis of macroeconomic and financial time series data: Hamilton (2016) gives an overview from a macroeconomic perspective, and Doz et al. (2020) present recent evidence of their usefulness for turning-point detection and macroeconomic forecasting; Guidolin (2011), and Ang and Timmermann (2012), provide a comprehensive survey in relation to financial markets; see also Qu and Zhuo (2021) and references therein for more recent advances. However, to the very best of our knowledge, the existing literature has focused on small dimensional Markov switching models, which are not applicable to high dimensional cross-sections. We aim at filling a gap in the literature by studying Markov switching models as applied to large panels.

There now exists strong empirical evidence that macroecononomic and financial variables exhibit an approximate factor structure, as stressed in Giannone et al. (2021). This nature of the data naturally leads to approximate latent factor specifications as a tool to model time series comovement in large dimensional cross-sections. For example, following the seminal contribution of Chamberlain and Rothschild (1983), static approximate factor representations have been considered in Connor and Korajczyk (1986) to develop measures of portfolio performance, and in Stock and Watson (2002a, b) to forecast large macroeconomic panels and to build indexes of macroeconomic activity. The full inferential theory is developed by Bai (2003). Settings allowing for dynamic factor representations have been also extensively studied: see Forni et al. (2017) and references therein. A broad overview of large factor models is provided in Stock and Watson (2016). To the very best of our knowledge, the vast majority of existing contributions has looked at the linear setting. However, this may not be flexible enough to accommodate the discrete regimes typically observed in macroeconomic and financial series.

A number of contributions have extended linear static factor models to allow for discrete shifts in the loadings by assuming that these shifts are driven by an observable state variable. A first and growing stream of literature assumes that this state variable is a deterministic time index, which leads to a factor model with structural instability in the loadings: see Breitung and Eickmeier (2011), Corradi and Swanson (2014), Baltagi et al. (2016), Cheng et al. (2016), Barigozzi et al. (2018), Barigozzi and Trapani (2020), Duan et al. (2023), among others, and Bai and Han (2016) for a survey of the literature. The presence of structural breaks implies that regime changes are not recurrent and are related to events such as technological changes or shifts in monetary policy regimes. Alternatively, the states could be driven by the realisation of an observable stationary variable with respect to a reference value, in which case a threshold factor model would arise: see Massacci (2017, 2023). Under this set up, regimes are recurrent and associated to cyclical events such as business and financial cycles. Smoothly varying loadings are considered in Motta et al. (2011) and Pelger and Xiong (2022). Finally, Chen et al. (2023) follow Su and Wang (2017) and propose a time-varying matrix factor model with smooth changes in the loadings driven by a time index.

In this paper, we are interested in large dimensional factor models in relation to recurrent regime changes. A major drawback of threshold factor models is that they require a priori identification of the state variable. This may lead to model misspecification and unreliable empirical findings should the wrong state variable be employed to identify the regimes. In order to overcome this problem, we resort to the two-state Markov switching model of Goldfeld and Quandt (1973) with a latent state variable, and we extend it to allow for an underlying large dimensional factor structure. Within this setting, we make the following major methodological contributions: we propose an algorithm to estimate the conditional state probabilities, as well as the loadings and the factors; and we derive the asymptotic properties of the estimators for loadings and factors. Remarkably, our results do not require knowledge of the true number of factors in any regime, and they are robust to the number of factors being unknown and estimated. This is an important aspect of our paper. Estimating the number of factors is challenging in a linear setting, as evidenced by the high number of relevant contributions: Bai and Ng (2002), Alessi et al. (2010) and Ahn and Horenstein (2013), develop model selection criteria; Kapetanios (2010), Onatski (2010), and Trapani (2018), propose inferential procedures. Dealing with an unknown number of factors clearly becomes even more engaging in the presence of regimes driven by a latent state variable and it therefore is an important contribution of our paper.

To the very best of our knowledge, the literature on large dimensional Markov Switching factor models is still in its infancy. However, two existing contributions are important to discuss. First, Liu and Chen (2016) study a model similar to ours, but their definition of common factors differs from ours in that they consider factors that are pervasive along the time dimension rather than along the cross-sectional dimension. As a consequence, their idiosyncratic components are assumed to be white noise. Second, Urga and Wang (2022) study a set up similar to ours, with two important differences: they assume a priori knowledge of the number of factors; they consider a model with serially homoskedastic idiosyncratic components. In addition, the Maximum Likelihood estimation approach of Urga and Wang (2022) adapts the EM algorithm by Rubin and Thayer (1982) and Bai and Li (2012) to the case of Gaussian mixtures, where the weights are given by the probability of the latent variables to be in a given regime. Note that, to the very best of our knowledge, no existing contribution has formally proved that in the factor model case the EM algorithm is a contraction, namely that it converges to the Maximum Likelihood estimator. The approach in Urga and Wang (2022) leads to estimators for the unknown parameters that do not have closed form solutions. This in an additional important difference with respect to our approach, which instead leads to closed form solutions.

Our approach is as follows. We introduce an algorithm to estimate factors, loadings, and transition probabilities, which extends to high dimensional factor models the state-space approach advanced in Hamilton (1989) and Kim (1994) to handle low dimensional Markov switching autoregressive models. In particular, we generalize the the Baum-Lindgren-Hamilton-Kim filter and smoother, the original version of which was proposed to estimate Markov-switching VAR models: for example, see the reviews by Guidolin (2011), Krolzig (2013), Hamilton (2016), and Guidolin and Pedio (2018). An important feature of our approach is that it provides closed form expressions for all estimators. Even more remarkably, we not require a priori knowledge of the number of factors in each regime, which is instead needed by Urga and Wang (2022).

We obtain our theoretical results by exploiting the well known property that a factor model with neglected discrete regime changes admits an equivalent representation with a higher number of factors: for example, see the discussions in Breitung and Eickmeier (2011), Barigozzi et al. (2018), and Duan et al. (2023), in the case of structural breaks; and Massacci (2023) for threshold factor models. We use this property to estimate the latent factors by means of Principal Component Analysis (PCA) as applied to the linear representation. We then input these estimated factors into our algorithm, which allows us to recover the loadings and the transition probabilities. We then derive the asymptotic properties of the estimator for the loadings: we prove the asymptotic normality; we characterise the bias, which is induced both by the well known identification problem, and by the incomplete information related to the underlying data generated process. We also study the asymptotic properties of the estimated factors, which are obtained by projecting the data onto the estimated loadings. We corroborate our theoretical results through a comprehensive set of Monte Carlo experiments, which confirm the good finite sample properties of the estimation procedure we propose.

Finally, we assess the empirical validity of our model through an application to a large set of U.S. stock returns. Markov switching models have been widely used to capture the cyclical behaviour of small-dimensional portfolios of financial assets: see Guidolin (2011), and Ang and Timmermann (2012), and references therein. We contribute to this literature by applying the Markov switching factor model to a large dimensional portfolio of financial assets. Our results show that the regimes described by the model closely follow U.S. business cycle dynamics. In addition, an inspection of the estimated loadings allows us to identify level and slope factors. Therefore, our model could be employed to explain cross-sectional differences in average returns, and to then run conditional asset pricing tests when the regimes are driven by a latent first order Markov process. This would complement the findings in Massacci et al. (2021), who identify the regimes based on the return from the underlying stock market.

The rest of the paper is organised as follows. Section 2 introduces the two-state model. Section 3 describes the estimation algorithm. Section 4 derives the asymptotic theory. Section 5 presents two further results related to estimation of the number of factors and to underspecification of the number of regimes. Section 6 briefly discusses the issue of unobserved heterogeneity. Section 7 runs a comprehensive set of Monte Carlo experiments. Section 8 applies our model to a large number of industry equity portfolios. Finally, Section 9 concludes. Details about the estimation algorithm are given in Appendix A. Mathematical derivations are collected in Appendices B and C.

Notation

We denote as the Kronecker product, with the Hadamard (element-wise) product, and with the element-wise ratio. For a vector we denote its Euclidean norm as . For a matrix we denote the spectral norm as , where indicates the largest eigenvalue of . If , then, we sometimes use the same notation to denote also the Frobenius norm . Indeed, and since it is always true that , then, bounding the Frobenius or the spectral norm is asymptotically equivalent.

For a scalar discrete random variable , the notation is its probability mass function computed using the true value of the parameters. For random variables and the notations and are the expectation and conditional expectation given , respectively, computed with respect to the true distributions and which in turn are computed using the true value of the parameters. If, in place of the true value of the parameters, we use an estimate of the parameters, say , then we adopt the notations , , and , respectively.

Finally, we let be the identity matrix of dimension , an -dimensional vector of ones, and any matrix or vector of zeros whose dimensions depend on the context.

2 Markov switching factor model

2.1 Setup

We study a two-state large dimensional Markov switching factor model. Formally, we consider

| (1) | ||||

| (2) |

We assume that the elements of the vector process of observable dependent variables have zero mean, and we consider the more general case in which they are allowed to have mean different from zero in Section 6; is the vector process of latent factors such that is fixed and , for ; is the matrix of factor loadings with rows equal to , for and ; is the vector process of idiosyncratic components with innovations . Note that we allow the elements of to be both serially and cross-sectionally weakly correlated, and we refer to Section 4 for the specific assumptions. It is also important to point out that the number of factors within each state is allowed to be unknown.

The model in (1) and (2) explicitly allows for two regimes: the case in which the number of states is actually underspecified is dealt with in Section 5.2. Also, the number of factors and is allowed to change between the regimes: in this, our approach is more general than in Liu and Chen (2016), who assume that and the dimension of the factor space is a priori the same between the two regimes.

As it is standard in the literature, we assume that follows a discrete-state, homogeneous, irreducible and ergodic, first-order Markov chain such that

with matrix of transition probabilities

| (3) |

Defining the vector of state indicators

| (4) |

allows us to write the transition equation

| (5) |

where is a discrete-valued zero mean martingale difference sequence whose elements sum to zero. Because, , follows an ergodic Markov chain, thus, there exists a stationary vector of probabilities satisfying:

Hence, the elements of are long-run or unconditional state probabilities. In particular, we have , such that

| (10) |

where , for , by Assumption 1 in Section 4 below, which makes the Markov chain irreducible. In particular, (3) and (10) are related by (see, e.g., Guidolin and Pedio, 2018, Chapter 9)

| (11) |

Finally, unlike the low-dimensional model of Diebold and Rudebusch (1996), we do not specify the factor dynamics. In particular, Diebold and Rudebusch (1996) allow for regime-specific factor mean, whereas the loadings do not vary: in this setting, the variance of the dependent variables remains constant over time. On the other hand, the large-dimensional model in (1) and (2) allows for regime-specific covariance matrix of : this is relevant for modelling both macroeconomic variables and financial returns, as stressed in McConnell and Perez-Quiros (2000), and Perez-Quiros and Timmermann (2000, 2001), respectively. We will exploit this feature in the empirical analysis in Section 8, where we will use the model in (1) and (2) to model returns from a large equity portfolio.

2.2 State space representation

Let the vector process be defined as

| (12) |

Let and , where and are matrices. The model in (1), (2) and (5) admits the equivalent state space representation111Note that .

| (13) | ||||

Under standard assumptions, the term is identifiable up to a relabelling of the states. This means that the indices of the states can be permuted without changing the law governing the process for : on this, see Section 3 in Leroux (1992). Also note that, even for given , identification of and , and therefore of the elements of , is in general possible only up to an invertible linear transformation (see Bai, 2003).

2.3 Linear representation

Model (13) is observationally equivalent to a model with one change point affecting the loadings of all units (Barigozzi et al., 2018). It can then be rewritten as the linear factor model

| (14) |

where . Then and may be estimated by standard Principal Component Analysis (PCA) (Stock and Watson, 2002a, b; Bai, 2003). Since PCA gives, as , consistent estimators of the factors up to premultiplication by an invertible matrix (see Bai, 2003), for ease of exposition we first consider estimation of the model in (13) by treating as known. We then briefly review the implementation of PCA and its effect on the estimation of the model in Section 3.3.

2.4 Log-likelihood

We follow Bai and Li (2016) and estimate only the diagonal elements of and in (2). The parameters of interest are then partitioned as

so that the vector of parameters of interest, denoted as , is defined as

Let , , where is an vector, is an vector. These are -dimensional realizations of the stochastic processes and , respectively. Moreover, let be the -algebra generated by the random variables , for ; in a similar way, define as the -algebra generated by the random variables , for . And for simplicity we write and .

The likelihood function, denoted by , can be decomposed as

| (15) |

in the last step we account for the fact that , since it does not depend on the parameters of our model, as we do not specify any dynamic model for the process .

Furthermore, following Krolzig (2013, Section 6.2), we have

| (16) |

Here, to avoid heavier notation, we use the same notation both for a generic dimensional realization of the process and for the -algebra generated by the random variables . Notice that the sum is over possible values since, given a realization for , the realizations of are given by for all .

Following the approach by Doz et al. (2012), and Barigozzi and Luciani (2019), and the one by Bai and Li (2016), all developed for QML estimation of linear factor models, for we consider a misspecified Gaussian quasi-likelihood of an exact factor model. This implies that the idiosyncratic components are treated as if they were cross-sectionally uncorrelated. In addition, we also neglect serial correlation in the idiosyncratic components, thus treating them as if they were weak white noise processes. This approach is similar to the one also followed in Urga and Wang (2022). It is important to stress that we are not assuming that the idiosyncratic components are uncorrelated, as we are just considering likelihood estimation of a misspecified model. In the linear case, Bai and Li (2016), and Barigozzi and Luciani (2019), show that such misspecification is asymptotically negligible as . Under this setup, and using the Markov property of , up to omitted constant terms we have

| (17) | ||||

where . Note that in this case the likelihood (16) is not Gaussian; rather, it is a mixture of Gaussian distributions. Finally, again by the Markov property of , we can write

| (18) |

3 Estimation

In this section, we assume that the data generating process is characterised by two regimes as in the model in (1) and (2). In Section 5.2 we study the case in which the model is underspecified and the data generating process exhibits a higher number of regimes. We also assume that the dimension of the vector in (14) is known. Should this not be the case, the dimension of can be determined using information criteria such as those proposed in Bai and Ng (2002), Alessi et al. (2010) and Ahn and Horenstein (2013), or inferential techniques such as those developed in Onatski (2010), and Trapani (2018). This issue is discussed also in Section 5.1. For example, in the empirical analysis in Section 8, we use the criteria developed in Ahn and Horenstein (2013).

In what follows, Section 3.1 defines the steps of the proposed Expectation Maximization (EM) algorithm. Section 3.2 describes the Baum-Lindgren-Hamilton-Kim filter and smoother. Section 3.3 details the estimator for the factor space. Section 3.4 discusses the estimator for the parameters. Section 3.5 deals with initialization and convergence of the algorithm.

3.1 EM algorithm

The algorithm outlined in this section is a generalization of the procedure proposed by Krolzig (2013, Chapter 5). The EM algorithm is made of two steps repeated at each iteration . The E step involves taking the expected value of the log-likelihood derived from (15) conditional on given an estimate of the parameters , namely

The M step solves the constrained maximization problem with respect to , that is

| (19) |

where the constraints ensure that probabilities add up to one. In principle, in the M step we should also account for the term , which however in our context does not depend on any parameter.

It is well known that the iteration of these steps produces a series of increasing log-likelihoods. Indeed, does not contribute to the convergence of the EM algorithm (see Dempster et al., 1977, and Wu, 1983). Moreover, if the maximum is identified and unique, then the EM algorithm will eventually lead to the Maximum Likelihood estimator of . As shown below, the solution of the M step can be computed using the expressions given in (17) and (18). This solution is unique and in closed form. Therefore, no identification issue arises due to multiple maxima, or related to the existence of such maxima.

3.2 Baum-Lindgren-Hamilton-Kim filter and smoother

From (17) and (18), in order to compute the expected likelihood in the E step we need to compute , , and .

We start by considering the case in which both is observed and the true value of the parameters is known, while we postpone the discussion of the estimation of the factors to Section 3.3. Then, for the E step we just need to compute , since in this case and are independent for all . This is accomplished by means of a generalization the Baum-Lindgren-Hamilton-Kim filter and smoother explained in detail in Appendix A.1. It is an iterative procedure through which we first compute the sequences of conditional one-step-ahead predicted probabilities , such that , and filtered probabilities such that . Second, by means of those sequences, we compute the sequence of smoothed probabilities such that .

The final recursions for the filtered probabilities are given by (e.g., see Krolzig, 2013, Chapter 5.1, and Hamilton, 1989)

| (20) |

where

| (23) |

The filter can be started by setting either , or, equivalently, .

3.3 Estimating the factor space

In order to estimate the factors , and their dimension , we exploit the fact that the Markov switching factor model in (1) is observationally equivalent to a linear factor model with common factors and factor loadings : see Section 2.3 and, in particular, equation (14). The number of factors in (14) can be estimated using methods already available in the literature: for example, see Bai and Ng (2002), Onatski (2010), Ahn and Horenstein (2013), and Trapani (2018). The factors can be estimated by PCA as follows. First, the estimator of the loadings matrix is obtained as times the normalized eigenvectors corresponding to the largest eigenvalues of the sample covariance matrix . Second, the factors are estimated by linear projection of the data onto the estimated loadings:

| (25) |

This is the same approach followed by Stock and Watson (2002a). It is also the dual approach of the one adopted by Bai (2003). Consistency of and follow from Lemma 1 and Lemma 5(a) in Appendix B, respectively. Note that the steps described in this section do not require knowing the latent state indicator , and they can be carried out independently. Because of these results, and can also be treated as independent for all . As a consequence, the Baum-Lindgren-Hamilton-Kim filter described in Section 3.2 can be implemented by just replacing the true factors with their estimator defined in (25).

3.4 Estimating the parameters

At each iteration of the EM algorithm, the filtered and smoothed probabilities, given in (20) and (24), respectively, and the smoothed cross-probabilities given in (A.16), are computed using an estimator of the parameters and an estimator of the factors. Hereafter, we denote as , , and such estimators. This defines the E step.

In the M step we have to solve the constrained maximization problem in (19). Here we just give the final results, while we refer to Appendix A.2 for their derivation. The estimates of the loadings , , are given by

| (26) |

and, consistently with the fact that we use a mis-specified likelihood with uncorrelated idiosyncratic components, we set

| (27) | ||||

where is the th row of . Concerning the estimates of which are subject to the adding up condition,

| (28) |

By letting be the last iteration of the EM algorithm, we define our final estimator of the parameters as , as given by (26), (27), and (28). The final estimator of is defined as , i.e., obtained by running one last time the Baum-Lindgren-Hamilton-Kim filter using the final estimates of the parameters.

3.5 Initialization and convergence of the EM algorithm

To start the algorithm we need initial estimators for the parameters. Specifically, we set , as defined in Section 3.3. Then, given also as in (25), let , and we set . Finally, we set

where and . This initialization implicitly identifies state 1 as the most probable one, i.e., it is the state with largest unconditional probability as defined in (11).

We say that the EM algorithm converged at iterations , where is the first value of such that:

for some a priori chosen threshold .

4 Asymptotic theory

In what follows, Section 4.1 states the assumptions, whereas Section 4.2 presents the asymptotic properties of the estimators.

4.1 Assumptions

For ease of reference, let us write (1) and (14) in scalar notation as

We consider the following set of assumptions, which generalizes to our framework the settings in Bai (2003) and Massacci (2017).

Assumption 1.

Factors.

-

(a)

For , and all , and .

-

(b)

For , as , , where is positive definite, and is any sequence such that (i) and (ii) .

Assumption 1 restricts the factor processes , for , so that appropriate moments exist. The sequence can be random or deterministic, and it is introduced to account for the fact that we estimate the expected value of , and not its actual value. Assumption 1 implies that , for , thus ruling out the possibility that any of the states is absorbing, as discussed in Section 2. It also implies that for , as ,

| (29) |

where is positive definite and

| (30) |

In particular, note that (29) allows the covariance matrix of to be state-dependent, as advocated in Massacci (2023). It is also easy to see that if , then for all

| (31) |

Assumption 2.

Loadings.

-

(a)

For , all , and all , , where is independent of , , and .

-

(b)

For , as , , where is positive definite.

-

(c)

As , , where is .

-

(d)

For any full rank matrix , .

According to Assumption 2, loadings are nonstochastic and factors have a nonnegligible effect on the variance of within each regime. The condition in part (d) ensures that the regimes are identified and it is analogous to the alternative hypothesis in the test for change in loadings developed in Pelger and Xiong (2022). This condition is trivially satisfied if , since the number of factors changes between regimes; if instead , then part (d) rules out the possibility that the columns of are a linear combination of the columns of , in which case the regimes cannot be separately identified. From Assumption 2 it also follows that, as ,

| (32) |

and

| (37) |

Assumption 3.

Part (b) of Assumption 3 controls the amount of cross-sectional correlation we can allow for. It implies the usual assumption for approximate factor models of nondiagonal idiosyncratic covariances , . Note that the sequence has the same role as in Assumption 1, which we refer to for further comments. Part (b) of Assumption 3 also implies

and hence for , and for all . Part (c) of Assumption 3 limits time dependence, and it is guaranteed together with part (a) if we assume finite 8th order cumulants for the bivariate process . Notice that the constant in the three parts of the assumption does not have to be the same one.

Assumption 4.

Weak dependence between common and idiosyncratic components. For , and all , and all ,

where is as in Assumption 1(b), and is independent of and .

Assumption 4 limits the degree of dependence between factors, state variable , and idiosyncratic components.

Assumption 5.

Assumption 5 guarantees a unique limit for , as stated in Lemma 6 in Appendix B. By assuming distinct eigenvalues, we can uniquely identify the space spanned by the eigenvectors, which are linear combinations of the columns of . Notice that is block diagonal because of (31).

Assumptions 1 to 5 are sufficient to prove the consistency of the estimators we propose. In order to derive their asymptotic distributions, we further introduce the following Assumptions (6) and (7).

Assumption 6.

Moments and Central Limit Theorems.

-

(a)

For , all , all and all ,

where is independent of , , , and .

-

(b)

For , all and all ,

where is independent of , , , and .

- (c)

-

(d)

For all , as ,

where for

and .

Parts (a) and (b) of Assumption 6 are suitable moment bounds, whereas parts (c) and (d) are central limit theorems.

Assumption 7.

Rates. As , and .

Assumption 7 imposes standard restrictions on the convergence rates.

Define the matrix as

| (38) |

where and is the diagonal matrix containing the first eigenvalues of sorted in decreasing order. In Lemma 6 we prove that

| (39) |

where is the diagonal matrix of the first eigenvalues of in decreasing order, and is the corresponding matrix of eigenvectors such that . Likewise define , for , which is an matrix such that . Thus, by Lemma 7 we have

| (40) |

where is the matrix such that . Therefore, because of (30), (39), and by Lemma 8 according to which ,

| (41) |

4.2 Asymptotic results

For , let , where is the last iteration of the EM algorithm as defined in Section 3.4. For given and , let be the estimator for such that and . The following theorem states the asymptotic distribution of .

Theorem 1.

Theorem 1 shows that the estimator for is subject to two sources of bias. The first is standard and it is induced by the usual indeterminacy due to the latency of both factors and loadings, and it is captured by the invertible matrix defined in (38) (see Bai, 2003). If we assume , then becomes a rotation, namely an orthogonal matrix. However, additional restrictions on the loadings are necessary to reduce to the identity: for a discussion on identification of factors see inter alia Bai and Ng (2013). The second source of bias is induced by defined in (42), which depends on the probability of the state being asymptotically correctly estimated. If the unconditional probability of being in state were correctly estimated with probability one, that is, if , as , then and would consistently estimate a linear transformation of .

Therefore, estimates a linear transformations of and , with weights determined by and , respectively. This second source of bias is due to the fact that the process is latent, and it is specific to Markov switching models. As such, it does not affect threshold or structural break models, in which the state is identified with probability one.

Theorem 1 has implications for the estimation of the regime specific loadings , . To see this, let , for , and consider the partition

| (43) |

where , and , , are . Then, from Theorem 1, for any given , as , we obtain

| (44) |

and

| (45) |

This means that columns of , , estimate two different linear transformations of the columns of . We can distinguish two cases. On the one hand, if , as assumed for example in Liu and Chen (2016), there is no need to know the true values of and to get consistent estimates of the space spanned by the true loadings in the two different regimes. Indeed, in this case and have an even number of columns, equal to , and from the first line of (4.2) and (4.2) we see that we can consider the first half of the columns of either or as an estimator of a linear transformation of and the second half of the columns of either or as an estimator of a linear transformation of . Hence, we can define the following estimators of the loadings:

| (46) |

or

| (47) |

where denotes the first elements of , and denotes the second elements of , for and . The property of these estimators are formalized in the following corollary, which is a direct consequence of Theorem 1, and of (4.2) and (4.2).

Corollary 1.

This corollary has some interesting implications. If we strengthen Assumption 2(c) to add the identification constraint , which is natural given Asssumption 2(d), then it is immediate to see that and , as , in other words which is now a block-diagonal matrix (see (41) and recall that is block-diagonal by construction). It follows that if the unconditional probability of being in a given state were correctly estimated with probability one, so that, as , we had , then, as , for we have , which implies , while . These results, which allow for a clear separation of and , hold only under the restrictive assumption . However, in general it is not possible to verify such condition and the two sets of estimators and or and will estimate consistently only a linear combination of the true loadings in both regimes.

On the other hand, if , we need consistent estimators of and in order to be able to isolate the first columns of and the last columns of , respectively. Therefore, if we only know that without knowing their true values, then we can consistently estimate a linear transformation of the columns of , but nothing can be said about , .

Theorem 1 describes the asymptotic properties of the estimator for the factor loadings and . Complementary results can be obtained with respect to the estimated factors associated to the loading matrices and . Formally, the true factors that correspond to and are and , respectively, and their estimators are and , respectively. The following theorem states the asymptotic distribution of these estimators.

Theorem 2.

In general, and so also . Then, because of Theorem 1, the estimator is biased and it is straightforward to see that the asymptotic covariance in Theorem 2 is positive definite. Note that if we know that holds, then we can build consistent estimators for linear combinations of , , by simply regressing onto the estimators or which are defined in (46) and (47), respectively, and, as shown in Corollary 1, are consistent for linear transformation of . Formally, this means we can build the sequence of factor estimators by running the cross-sectional regressions

| (48) |

or

| (49) |

If the unconditional probability of being in a given state is correctly estimated then as , and Theorem 2 is redundant: in this case, asymptotic normality of (48) and of (49) follows from arguments analogous to those in Bai (2003). In the more general case we are considering, the asymptotic distribution of is stated in the following theorem (an analogous result holds for and it is omitted for brevity).

Theorem 3.

According to Theorem 3, estimates the space spanned by either or , for , with , depending on which the true underlying regime is in period .

5 On the number of regimes and factors

This section deals with two further issues related to the model in (1) and (2). Section 5.1 studies estimation of the number of factors. Section 5.2 discusses the consequences of an underspecified model.

5.1 Estimating the number of factors

Theorems 1 and 2 rely on the factor estimator obtained from the equivalent linear representation in (14). This estimator does not embed any information related to the likelihood of observing a regime at a given point in time , for and . We now study the property of the estimator for the dimension of the factor space that is obtained when such information is accounted for.

Formally, for , consider the covariance matrix

| (50) |

where : includes information about the regimes through the estimated sequence . Define the vectors

and the matrices

For , with , let be the diagonal matrix containing the first eigenvalues of in decreasing order. Finally, let be the matrix estimator for , which is obtained as times the normalized eigenvectors corresponding to the largest eigenvalues of the sample covariance matrix in (50). The following theorem characterises the mean square convergence of for a given value of .

Theorem 4.

Theorem 4 extends Theorem 1 in Bai and Ng (2002) and Theorem 3.4 in Massacci (2017) to the case of the Markov switching factor model in (1) and (2). For with , the theorem shows that estimates a linear combination of the vector and not just of . It implies that the dimension of the estimated underlying factor space is even when the available information about the regimes is accounted for. Imperfect knowledge of the regimes therefore leads to an enlarged factor space: this makes our setting analogous to large dimensional change point factor models, as previously discussed in Section 2.3. This complements what proved in Breitung and Eickmeier (2011), and Corradi and Swanson (2014), who show that model misspecification in the form of omitted discrete regime shifts leads to an inflated number of factors.

The result in Theorem 4 has practical implications. Let us assume that the number of factors is constant across regimes, as in Liu and Chen (2016). Then, if the estimated number of factors is even, we can easily recover the number of factors within each regime. If the estimated number is odd and greater than one, there might be a neglected regime, as discussed in Section 5.2 below. Obviously if we find evidence of just one common factor, then only the idiosyncratic covariances can be regime specific, while the loadings remain constant.

5.2 The case of an underspecified number of regimes

Up to know we have a priori assumed that the data are generated according to the model with two regimes in (1) and (2). This is consistent with existing empirical studies employing Markov switching models: for example, see Diebold and Rudebusch (1996). However, in some cases the underlying data generating process of the dependent variables of interest displays a higher number of regimes: for example, Guidolin and Timmermann (2006) show that the joint distribution of stock and bond returns requires a four-state model. Therefore, the two-regime specification in (1) and (2) leads to model misspecification in case the joint distribution of the dependent variables is characterised by a higher number of regimes.

We now study the case in which the model is underspecified and the data are generated by a process with a number of regimes that is finite and greater than two.

Since the number of regimes is finite, without loss of generality we consider the model with three regimes

| (52) |

and let

Suppose that only two regimes are accounted for. Given a natural ordering of the regimes, this means that we have to consider two cases, namely: and ; and . The model in admits the following two equivalent two-regime representations

| (53) | ||||

where the loadings are defined as , , , , the latent state process is defined as

the idiosyncratic covariance matrices are defined as , , , , and the transition probabilities are equal to

For , define the vector of parameters , where

Let be the normalised log-likelihood function of . Assume that

| (54) |

In a likelihood sense, the condition in (53) captures a larger regime shift for than for . Further, let be the generic maximum likelihood estimator for the parameter of an underspecified model that allows for only two regimes when in fact the data generating process is given by (52).

We proceed by contradiction, see also Appendix C for more details. If were an estimator for , then

| (55) |

which leads to a contradiction since is the estimated log-likelihood function. On the other hand, if were an estimator for , then

Therefore, when one regime is neglected, the maximum likelihood estimator estimates the regimes that maximise the likelihood according to the inequality in (54). Provided that a sufficient number of iterations is done, the EM algorithm proposed in Section 3 delivers an estimator that is close enough to the maximum likelihood estimator, such that the inequality in (54) is preserved: see Meng and Rubin (1993, 1994). Therefore, the EM algorithm delivers the estimator for the underspecified representation that is associated to the highest likelihood. This result is consistent with the homologous finding in Bai (1997), and Bai and Perron (1998), in relation to regression models with structural instability. Therefore, our result is the potential starting point for an inferential procedure on the number of regimes in large dimensional Markov switching factor models. It is also important to note that any neglected regime will be accounted for by an enlarged factor space, as discussed in Section 2.3.

6 Unobserved heterogeneity

The model in assumes no individual effects. However, these may be important when modelling macroeconomic series as in Diebold and Rudebusch (1996). In our set up, individual effects can be introduced by extending Bai and Li (2012, 2016) and considering

| (56) |

where , for , and captures the individual effect of cross-sectional unit within regime . The vectors and introduce unobserved heterogeneity. If the state variable driving the regimes were observable, the resulting identification problem could be solved by expressing the model in terms of deviations of from the conditional means within each regime: on this, see Massacci et al. (2021). However, since the state variable in is latent, this strategy no longer is applicable since the state is not observable with probability one. For this reason, we express the model in terms of the deviation of from the unconditional mean.

Formally, consider the vector of centred variables defined as

where , . If , has the same expected value in both regimes, and . In the more general case in which , unconditional demeaning leads to a larger factor space of dimension . The additional two factors and take only two values, namely or , depending on whether or , respectively, for . In this case, the equivalent linear representation in holds with and . The measurement equation in of the state space representation remains valid with and . Therefore, the tools developed in this paper can be applied to the sample counterpart of , namely to , which consistently estimates as . Corollary 1 holds accordingly with respect to and instead of with respect to and only, respectively, for .

7 Monte Carlo

We set and . At each time period , we simulate the vector of data according to (1) and (2). This requires to simulate the latent state , the loadings and , the factors and , and the idiosyncratic components .

We simulate the latent state according to (5), where has entries and , so that and . This configuration corresponds to the unconditional probabilities to be equal to and . Then, we generate the innovations of the VAR in (5) as follows: at each given we generate and (i) if and then ; (ii) if and then ; (iii) if and then ; (iv) if and then .

We set the number of factors in each state to , . The common component is generated according to model (1). Let , , . The entries of and are generated from a distribution. The matrices and are then transformed in such a way that and are diagonal matrices. The factors are such that , , and satisfy , where each component of is such that , , with and .

The idiosyncratic components are generated according to (2), where , , with diagonal and banded. Specifically, the entries of are generated from a and those of are generated from a , while is a Toeplitz matrix with on the th diagonal for and zero elsewhere, and, finally is a Toeplitz matrix with on the th diagonal for and zero elsewhere. We set . Moreover, each component of is such that , , , with and . Finally, we set the average noise-to-signal ratio across all simulated time series to be .

We simulate the model above 100 times for different values of , , , and . The EM is run allowing for at most 100 iterations and using a convergence threshold equal to . We initialize the algorithm using PCA as described in Section 3.5. Since the states are identified only up to a permutation at each iteration of the algorithm we assign label 1 to the state with the highest estimated unconditional probability.222Note that the initialization such that is not empirically feasible, as it leads to no convergence of the EM algorithm. We conjecture that this has to do with the relabelling issue discussed in Section 2.2, since for both states are equally likely.

Results are collected in Tables 1-4 and are organised as follows: , , , in Table 1; , , , in Table 2; , , , in Table 3; , , , in Table 4.

The first four columns of Tables 1-4 report the mean and, between brackets, the corresponding standard deviation over all replications of the estimated diagonal entries of the transition matrix , , of the unconditional probabilities , estimated as , .

| MSE() | avg. iter | |||||||

|---|---|---|---|---|---|---|---|---|

| 250 | 100 | 0.89 | 0.64 | 0.76 | 0.24 | 0.97 | 0.02 | 13.78 |

| 500 | 100 | 0.90 | 0.68 | 0.76 | 0.24 | 0.98 | 0.01 | 12.55 |

| 750 | 100 | 0.90 | 0.69 | 0.75 | 0.25 | 0.98 | 0.01 | 12.71 |

| 1000 | 100 | 0.90 | 0.69 | 0.75 | 0.25 | 0.98 | 0.01 | 12.05 |

| 250 | 200 | 0.89 | 0.64 | 0.76 | 0.24 | 0.97 | 0.01 | 11.98 |

| 500 | 200 | 0.89 | 0.68 | 0.75 | 0.25 | 0.97 | 0.01 | 21.23 |

| 750 | 200 | 0.89 | 0.68 | 0.75 | 0.25 | 0.97 | 0.02 | 37.37 |

| 1000 | 200 | 0.90 | 0.69 | 0.75 | 0.25 | 0.98 | 0.02 | 36.22 |

| MSE() | avg. iter | |||||||

|---|---|---|---|---|---|---|---|---|

| 250 | 100 | 0.89 | 0.62 | 0.77 | 0.23 | 0.97 | 0.02 | 20.14 |

| 500 | 100 | 0.90 | 0.68 | 0.76 | 0.24 | 0.98 | 0.02 | 15.28 |

| 750 | 100 | 0.90 | 0.69 | 0.76 | 0.24 | 0.98 | 0.02 | 14.43 |

| 1000 | 100 | 0.90 | 0.66 | 0.77 | 0.23 | 0.98 | 0.01 | 14.07 |

| 250 | 200 | 0.89 | 0.62 | 0.77 | 0.23 | 0.98 | 0.02 | 11.95 |

| 500 | 200 | 0.89 | 0.67 | 0.75 | 0.25 | 0.98 | 0.01 | 20.21 |

| 750 | 200 | 0.89 | 0.69 | 0.75 | 0.25 | 0.98 | 0.01 | 19.17 |

| 1000 | 200 | 0.90 | 0.69 | 0.75 | 0.25 | 0.98 | 0.01 | 21.82 |

| MSE() | avg. iter | |||||||

|---|---|---|---|---|---|---|---|---|

| 250 | 100 | 0.88 | 0.46 | 0.81 | 0.19 | 0.97 | 0.04 | 19.32 |

| 500 | 100 | 0.89 | 0.65 | 0.76 | 0.24 | 0.97 | 0.03 | 14.63 |

| 750 | 100 | 0.90 | 0.67 | 0.76 | 0.24 | 0.97 | 0.03 | 14.46 |

| 1000 | 100 | 0.90 | 0.68 | 0.76 | 0.24 | 0.97 | 0.03 | 13.83 |

| 250 | 200 | 0.87 | 0.48 | 0.78 | 0.22 | 0.97 | 0.03 | 13.72 |

| 500 | 200 | 0.89 | 0.65 | 0.75 | 0.25 | 0.97 | 0.02 | 10.40 |

| 750 | 200 | 0.89 | 0.67 | 0.75 | 0.25 | 0.97 | 0.02 | 10.86 |

| 1000 | 200 | 0.90 | 0.68 | 0.75 | 0.25 | 0.97 | 0.01 | 10.81 |

| MSE() | avg. iter | |||||||

|---|---|---|---|---|---|---|---|---|

| 250 | 100 | 0.91 | 0.38 | 0.86 | 0.14 | 0.98 | 0.04 | 17.40 |

| 500 | 100 | 0.90 | 0.65 | 0.77 | 0.23 | 0.97 | 0.03 | 20.36 |

| 750 | 100 | 0.90 | 0.67 | 0.76 | 0.24 | 0.97 | 0.03 | 17.20 |

| 1000 | 100 | 0.90 | 0.68 | 0.76 | 0.24 | 0.98 | 0.03 | 16.61 |

| 250 | 200 | 0.89 | 0.41 | 0.83 | 0.17 | 0.97 | 0.03 | 14.55 |

| 500 | 200 | 0.89 | 0.66 | 0.76 | 0.24 | 0.97 | 0.02 | 13.41 |

| 750 | 200 | 0.90 | 0.67 | 0.76 | 0.24 | 0.97 | 0.02 | 14.56 |

| 1000 | 200 | 0.90 | 0.68 | 0.76 | 0.24 | 0.98 | 0.02 | 11.96 |

Since the loadings are not identified, in the fifth column of Tables 1-4 we report the multiple coefficient obtained from regressing the columns of onto the columns of , thus correcting for the bias described in Theorem 1. Namely, we compute

The closer this number is to one, the closer is the space spanned by the columns of to the space spanned by the columns of (see Doz et al., 2012).

In the sixth column of Tables 1-4 we report the MSE of the estimated common components defined as

where .

In the last column of Tables 1-4 we report the average number of iterations needed for the EM algorithm to converge.

The results in Tables 1-4 confirm the empirical validity of the estimation procedure detailed in Section 3. In all four scenarios, as and increase the estimators , , and all converge to the true values of the corresponding parameters. In addition, and MSE() are very to and , respectively. Finally, note that the average number of iterations declines almost monotonically as and increase. Overall, our Monte Carlo findings provide evidence in support of the estimation algorithm proposed in Section 3.

8 Empirical analysis

In this section we show how the methodological framework we propose can be used to model a large set of stock returns. This relates our work to a vast literature that models stock return dynamics using Markov switching specifications. Perez-Quiros and Timmermann (2000, 2001) document business cycle asymmetries in U.S. stock return dynamics using decile-sorted portfolios. Ang and Bekaert (2002), and Guidolin and Timmermann (2008), study portfolio allocation in international equity markets under regime switching. In a multi asset setting, Guidolin and Timmermann (2006) describe the joint distribution of equity and bonds under regime switching. Guidolin (2011), and Ang and Timmermann (2012), provide a review of the literature. We contribute to this stream of literature by characterizing stock return dynamics with a Markov switching model in a large dimensional setting. To the very best of our knowledge, we are the first to do so. In what follows, Section 8.1 describes the data and the empirical model specification, Section 8.2 discusses the estimated regime probabilities, and Sections 8.3 and 8.4 present the findings for estimated loadings and factors.

8.1 Data and model specification

The vector of observable dependent variables in is made of the monthly value weighted returns in excess of the risk-free rate from the industry portfolios kindly made publicly available on Kenneth French website.333See https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html. Consistently with the discussion in Section 6, the unconditional mean of is equal to , which means that the returns have been demeaned along the time series dimension over the whole sample period. To obtain a balanced panel, the sample period runs from July 1969 through December 2021, a total of time periods.

8.2 Regime probabilities

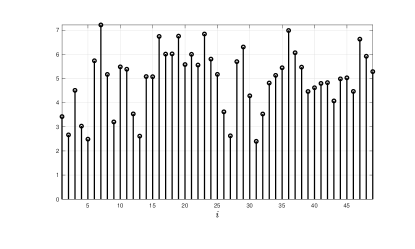

Using the selection criterion of Ahn and Horenstein (2013) as applied to the equivalent linear representation in (14), we find that the dimension of the vector is equal to common factors. As commonly assumed in the related literature (see Ang and Timmermann, 2012), we let the number of regimes be equal to two. Therefore, there is one common factor in each regime, so . Based on this result, we apply the algorithm detailed in Section 3. The EM algorithm converges in just 22 iterations (see Figure 1). The realisation of the estimator for the matrix of conditional probabilities in (3) is equal to

The estimated unconditional probability for regime is equal to the sample average , for . It follows that and .444By computing the unconditional probability using their analytical formulas in (11), we get and . Therefore, regime is approximately four times more frequent than regime .

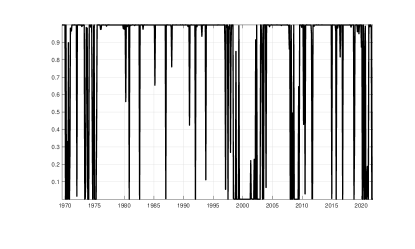

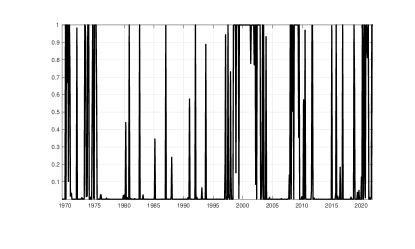

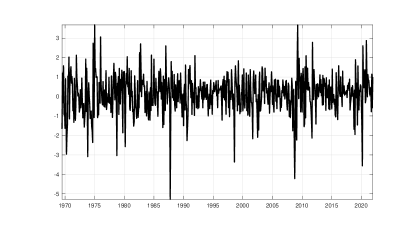

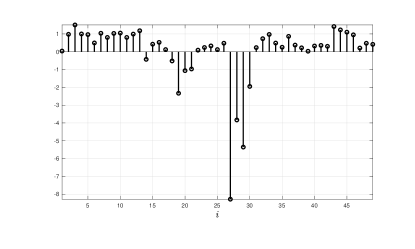

In order to provide an economic understanding of the regimes described by the model, Figure 2 plots the sequences of estimates and , for . These series are negatively and positively correlated, respectively, with the NBER recession indicator, with correlation coefficients equal to -0.303 and 0.303, respectively.555The NBER recession indicator is publicly available at https://fred.stlouisfed.org/series/USREC. Therefore, the state is related to periods of economic expansions, whereas the state is more likely to occur during recessionary phases. This is consistent with the empirical frequency of the states, since expansions occur more often than recessions. Our model therefore captures regime changes in equity markets related to business cycle dynamics.

|

-

•

This figure plots the value of the maximized expected conditional log-likelihood computed using the estimated factors, i.e., (see also (19)), as a function of the EM iterations .

|

|

| (a): | (b): |

-

•

This figure plots the series of the estimated conditional probabilities (panel (a)) and (panel (b)), for , estimated from the Markov switching factor model in (13).

8.3 Factors and loadings - Linear factor model

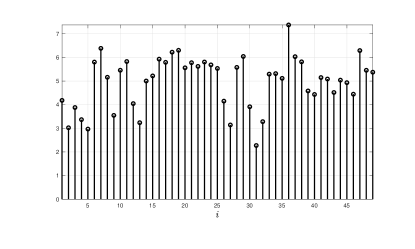

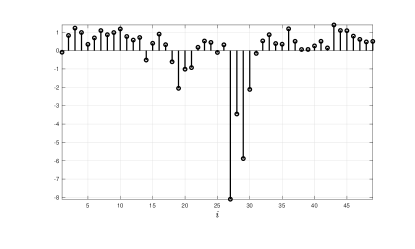

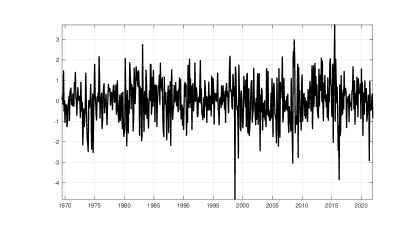

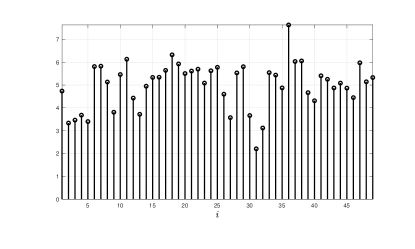

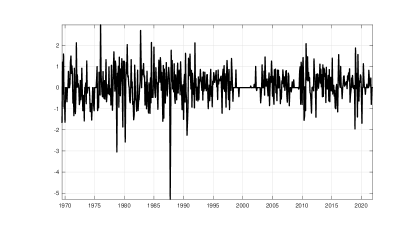

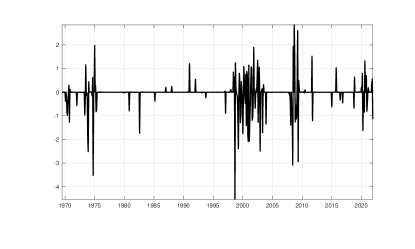

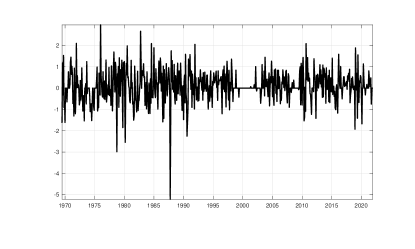

Following the sequential order dictated by our estimation procedure, we first consider estimated factors and loadings for the equivalent linear representation in (14), namely the loadings matrix with columns , , having elements , , and the 2-dimensional vector of factors , , both obtained via PCA as explained in Section 3.3. The estimated loadings are displayed in Figure 3 and the estimated factors are displayed in Figure 4.

|

|

| (a): | (b): |

-

•

This figure plots the sequences of estimated loadings (panel (a)) and (panel (b)), for , estimated from the linear factor model in (14).

|

|

| (a): | (b): |

-

•

This figure plots the series of the estimated factors (panel (a)) and (panel (b)), for , estimated from the linear factor model in (14).

The estimated loadings associated to all have the same sign. On the other hand, the loadings associated to have both positive and negative signs. To aid understanding of the factors, we study the correlation between them and the six observable factors considered in Fama and French (2016), namely: the value-weighted return on the market portfolio in excess of the one-month Treasury bill rate (); size (); value (); profitability (); investment (); momentum (). The correlations displayed in Table 5 show that the first estimated factor is strongly correlated with the market return , it is reasonably correlated with , and , and it is only mildly correlated with and . On the other hand, the second estimated latent factor does not exhibit any substantial correlation with any of the observable factors we consider. The first factor in the equivalent linear representation is then likely to be a market factor, while it is more difficult to give economic interpretation to the second factor.

| 0.96 | 0.05 | |

| 0.40 | -0.06 | |

| -0.13 | -0.06 | |

| -0.14 | 0.12 | |

| -0.32 | -0.12 | |

| -0.26 | -0.08 |

-

•

This table reports the correlation coefficients between the estimated factors and from the equivalent linear specification in (14) and the following six observable factors from Fama and French (2016): the value-weighted return on the market portfolio in excess of the one-month Treasury bill rate (); size (); value (); profitability (); investment (); momentum ().

8.4 Factors and loadings - Markov switching factor model

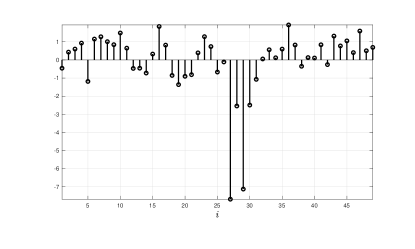

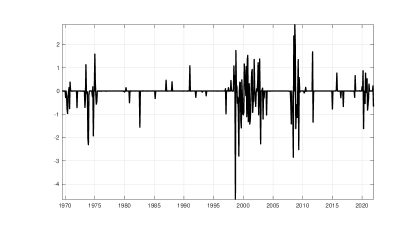

We then turn to the estimated loadings and factors from the Markov switching factor model in (1). Since we have , the estimators for , for , are readily available from (46) or (47). Figure 5 shows the estimated loadings and (panels (a) and (b), respectively), and and (panels (c) and (d), respectively), for . As expected from Corollary 1, the two sets of estimators are similar, although not identical, since they are consistent for different linear transformations of the true loadings. In particular, the correlation between and is , whereas that between and is .

Next, by projecting the data onto the estimated loadings weighted by the probability of being in a given state, we obtain the estimated scalar factors and , for and , as given in (48) and (49), respectively. These are shown in Figure 6. Finally, Table 6 displays the correlations between the estimated latent factors and the observable factors , , , , , and described in Section 8.3. From the results in Table 6, we can see that , which estimates according to (48), is strongly correlated with , and reasonably correlated with , and . As for , the estimate for from (48), it is correlated with . A similar picture comes from and , thus confirming the validity of our theoretical results.

| 0.74 | 0.01 | 0.74 | -0.02 | |

| 0.32 | 0.07 | 0.32 | -0.03 | |

| -0.17 | 0.06 | -0.17 | 0.06 | |

| -0.06 | 0.02 | -0.06 | 0.10 | |

| -0.22 | -0.06 | -0.13 | -0.01 | |

| -0.01 | -0.23 | -0.01 | -0.17 |

-

•

This table reports the correlation coefficients between the estimated factors , , , and from the Markov switching factor model in (1) according to (48) and (49), and the following six observable factors from Fama and French (2016): the value-weighted return on the market portfolio in excess of the one-month Treasury bill rate (); size (); value (); profitability (); investment (); momentum ().

9 Concluding remarks

This paper develops estimation and inferential theory for high dimensional factor models with discrete regime changes in the loadings driven by a latent first order Markov process. Our estimator employs a EM algorithm based on a modified version of the Baum-Lindgren-Hamilton-Kim filter and smoother. Remarkably, the estimator does not need knowledge of the number of factors in either states. It only requires the true number of factors in the equivalent linear representation, which can be estimated using existing techniques. We derive convergence rates and asymptotic distributions of the estimators for factors and loadings, and we show their good finite sample performance through an extensive set of Monte Carlo experiments. Finally, we empirically validate our methodology through an application to a large set of stock returns.

Our work can be extended along several dimensions. Two are worth mentioning. Our model allows for two regimes and the case of multiple states to capture richer dynamics is worth exploring. The challenging task of making inference on the number of regimes is also worth considering. These extensions are part of our research agenda.

References

- Ahn and Horenstein (2013) Ahn, S. C. and A. R. Horenstein (2013). Eigenvalue ratio test for the number of factors. Econometrica 81, 1203–1227.

- Alessi et al. (2010) Alessi, L., M. Barigozzi, and M. Capasso (2010). Improved penalization for determining the number of factors in approximate static factor models. Statistics and Probability Letters 80, 1806–1813.

- Ang and Bekaert (2002) Ang, A. and G. Bekaert (2002). International asset allocation with regime shifts. Review of Financial Studies 15, 1137–1187.

- Ang and Timmermann (2012) Ang, A. and A. Timmermann (2012). Regime changes and financial markets. Annual Review of Financial Economics 4, 313–337.

- Bai (1997) Bai, J. (1997). Estimating multiple breaks one at a time. Econometric Theory 13(3), 315–352.

- Bai (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica 71, 135–171.

- Bai and Han (2016) Bai, J. and X. Han (2016). Structural changes in high dimensional factor models. Frontiers of Economics in China 11, 9–39.

- Bai and Li (2012) Bai, J. and K. Li (2012). Statistical analysis of factor models of high dimension. The Annals of Statistics 40, 436–465.

- Bai and Li (2016) Bai, J. and K. Li (2016). Maximum likelihood estimation and inference for approximate factor models of high dimension. The Review of Economics and Statistics 98, 298–309.

- Bai and Ng (2002) Bai, J. and S. Ng (2002). Determining the number of factors in approximate factor models. Econometrica 70, 191–221.

- Bai and Ng (2013) Bai, J. and S. Ng (2013). Principal components estimation and identification of static factors. Journal of econometrics 176, 18–29.

- Bai and Perron (1998) Bai, J. and P. Perron (1998). Estimating and testing linear models with multiple structural changes. Econometrica 66(1), 47–78.

- Baltagi et al. (2016) Baltagi, B. H., Q. Feng, and C. Kao (2016). Estimation of heterogeneous panels with structural breaks. Journal of Econometrics 191, 176–195.

- Barigozzi et al. (2018) Barigozzi, M., H. Cho, and P. Fryzlewicz (2018). Simultaneous multiple change-point and factor analysis for high-dimensional time series. Journal of Econometrics 206, 187–225.

- Barigozzi and Luciani (2019) Barigozzi, M. and M. Luciani (2019). Quasi maximum likelihood estimation and inference of large approximate dynamic factor models via the EM algorithm. Technical Report arXiv:1910.03821.

- Barigozzi and Trapani (2020) Barigozzi, M. and L. Trapani (2020). Sequential testing for structural stability in approximate factor models. Stochastic Processes and their Applications 130, 5149–5187.

- Breitung and Eickmeier (2011) Breitung, J. and S. Eickmeier (2011). Testing for structural breaks in dynamic factor models. Journal of Econometrics 163, 71–84.

- Chamberlain and Rothschild (1983) Chamberlain, G. and M. Rothschild (1983). Arbitrage, factor structure, and mean-variance analysis on large asset markets. Econometrica 51, 1281–1304.

- Chen et al. (2023) Chen, B., E. Y. Chen, and R. Chen (2023). Time-varying matrix factor model. Technical report, University of Rochester, New York University and Rutgers University.

- Cheng et al. (2016) Cheng, X., Z. Liao, and F. Schorfheide (2016). Shrinkage estimation of high-dimensional factor models with structural instabilities. The Review of Economic Studies 83, 1511–1543.

- Connor and Korajczyk (1986) Connor, G. and R. Korajczyk (1986). Performance measurement with the arbitrage pricing theory: A new framework for analysis. Journal of Financial Economics 15, 373–394.

- Corradi and Swanson (2014) Corradi, V. and N. R. Swanson (2014). Testing for structural stability of factor augmented forecasting models. Journal of Econometrics 182, 100–118.

- Dempster et al. (1977) Dempster, A. P., N. M. Laird, and D. B. Rubin (1977). Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 39, 1–38.

- Diebold and Rudebusch (1996) Diebold, F. X. and G. D. Rudebusch (1996). Measuring business cycles: A modern perspective. Review of Economics and Statistics 78, 67–77.

- Doz et al. (2020) Doz, C., L. Ferrara, and P.-A. Pionnier (2020). Business cycle dynamics after the great recession: An extended markov-switching dynamic factor model. Technical report, ffhalshs-02443364.

- Doz et al. (2012) Doz, C., D. Giannone, and L. Reichlin (2012). A quasi maximum likelihood approach for large approximate dynamic factor models. The Review of Economics and Statistics 94(4), 1014–1024.

- Duan et al. (2023) Duan, J., J. Bai, and X. Han (2023). Quasi-maximum likelihood estimation of break point in high-dimensional factor models. Journal of Econometrics 223, 209–236.

- Fama and French (2016) Fama, E. F. and K. R. French (2016). Dissecting anomalies with a five-factor model. Review of Financial Studies 29(1), 69–103.

- Forni et al. (2017) Forni, M., M. Hallin, M. Lippi, and P. Zaffaroni (2017). Dynamic factor models with infinite-dimensional factor space: Asymptotic analysis. Journal of Econometrics 199, 74–92.

- Giannone et al. (2021) Giannone, D., M. Lenza, and G. E. Primiceri (2021). Economic predictions with big data: The illusion of sparsity. Econometrica (forthcoming) 89(5), 2409–2437.

- Goldfeld and Quandt (1973) Goldfeld, S. M. and R. E. Quandt (1973). A Markov model for switching regressions. Journal of Econometrics 1, 3–15.

- Guidolin (2011) Guidolin, M. (2011). Markov Switching Models in Empirical Finance. In D. M. Drukker (Ed.), Missing Data Methods: Time-Series Methods and Applications (Advances in Econometrics), Volume 27 Part 2, pp. 1–86. Emerald Group Publishing Limited, Bingley.

- Guidolin and Pedio (2018) Guidolin, M. and M. Pedio (2018). Essentials of time series for financial applications. Academic Press.

- Guidolin and Timmermann (2006) Guidolin, M. and A. Timmermann (2006). An econometric model of nonlinear dynamics in the joint distribution of stock and bond returns. Journal of Applied Econometrics 21, 1–23.

- Guidolin and Timmermann (2008) Guidolin, M. and A. Timmermann (2008). International asset allocation under regime switching, skew, and kurtosis preferences. Review of Financial Studies 21, 889–935.

- Hamilton (1989) Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica 57, 357–384.

- Hamilton (2016) Hamilton, J. D. (2016). Macroeconomic Regimes and Regime Shifts. In J. B. Taylor and H. Uhlig (Eds.), Handbook of Macroeconomics, Volume 2A, pp. 163–201. Elsevier.

- Kapetanios (2010) Kapetanios, G. (2010). A testing procedure for determining the number of factors in approximate factor models with large datasets. Journal of Business & Economic Statistics 28(3), 397–409.

- Kim (1994) Kim, C.-J. (1994). Dynamic linear models with markov-switching. Journal of Econometrics 60, 1–22.

- Krolzig (2013) Krolzig, H.-M. (2013). Markov-switching vector autoregressions: Modelling, statistical inference, and application to business cycle analysis, Volume 454. Springer Science & Business Media.

- Leroux (1992) Leroux, B. G. (1992). Maximum-likelihood estimation for hidden markov models. Stochastic Processes and their Applications 40(1), 127–143.

- Liu and Chen (2016) Liu, X. and R. Chen (2016). Regime-switching factor models for high-dimensional time series. Statistica Sinica 26, 1427–1451.

- Massacci (2017) Massacci, D. (2017). Least squares estimation of large dimensional threshold factor models. Journal of Econometrics 197(1), 101–129.

- Massacci (2023) Massacci, D. (2023). Testing for regime changes in portfolios with a large number of assets: A robust approach to factor heteroskedasticity. Journal of Financial Econometrics 21(2), 316–367.

- Massacci et al. (2021) Massacci, D., L. Sarno, and L. Trapani (2021). Factor models with downside risk. Working paper, King’s College London, University of Cambridge and University of Nottingham.

- McConnell and Perez-Quiros (2000) McConnell, M. M. and G. Perez-Quiros (2000). Output fluctuations in the united states: What has changed since the early 1980’s? The American Economic Review 90(5), 1464–1476.

- Meng and Rubin (1993) Meng, X.-L. and D. B. Rubin (1993). Maximum likelihood estimation via the ECM algorithm: A general framework. Biometrika 80, 267–278.

- Meng and Rubin (1994) Meng, X.-L. and D. B. Rubin (1994). On the global and componentwise rates of convergence of the EM algorithm. Linear Algebra and its Applications 199, 413–425.

- Motta et al. (2011) Motta, G., C. M. Hafner, and R. Von Sachs (2011). Locally stationary factor models: Identification and nonparametric estimation. Econometric Theory 27, 1279–1319.

- Onatski (2010) Onatski, A. (2010). Determining the number of factors from empirical distribution of eigenvalues. The Review of Economics and Statistics 92, 1004–1016.

- Pelger and Xiong (2022) Pelger, M. and R. Xiong (2022). State-varying factor models of large dimensions. Journal of Business and Economic Statistics 40, 1315–1333.

- Perez-Quiros and Timmermann (2000) Perez-Quiros, G. and A. Timmermann (2000). Firm size and cyclical variations in stock returns. Journal of Finance 55, 1229–1262.

- Perez-Quiros and Timmermann (2001) Perez-Quiros, G. and A. Timmermann (2001). Business cycle asymmetries in stock returns: Evidence from higher order moments and conditional densities. Journal of Econometrics 103, 259–306.

- Qu and Zhuo (2021) Qu, Z. and F. Zhuo (2021). Likelihood ratio based tests for markov regime switching. Review of Economic Studies 88, 937–968.

- Rubin and Thayer (1982) Rubin, D. B. and D. T. Thayer (1982). EM algorithms for ML factor analysis. Psychometrika 47, 69–76.

- Stock and Watson (2002a) Stock, J. H. and M. W. Watson (2002a). Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association 97, 1167–1179.

- Stock and Watson (2002b) Stock, J. H. and M. W. Watson (2002b). Macroeconomic forecasting using diffusion indexes. Journal of Business and Economic Statistics 20, 147–162.

- Stock and Watson (2016) Stock, J. H. and M. W. Watson (2016). Dynamic Factor Models, Factor-Augmented Vector Autoregressions, and Structural Vector Autoregressions in Macroeconomics. In J. B. Taylor and H. Uhlig (Eds.), Handbook of Macroeconomics, Volume 2, pp. 415–525. Elsevier.

- Su and Wang (2017) Su, L. and X. Wang (2017). On time-varying factor models: Estimation and testing. Journal of Econometrics 198(1), 84–101.

- Trapani (2018) Trapani, L. (2018). A randomized sequential procedure to determine the number of factors. Journal of the American Statistical Association 113, 1341–1349.

- Urga and Wang (2022) Urga, G. and F. Wang (2022). Estimation and inference for high dimensional factor model with regime switching. Working Paper, Bayes Business School and Peking University.

- Wu (1983) Wu, J. C. F. (1983). On the convergence properties of the EM algorithm. The Annals of Statistics 11, 95–103.

Appendix A Details of estimation

A.1 Baum-Lindgren-Hamilton-Kim filter

For simplicity of notation, in this appendix we will consider both the factors and the true values of the parameters to be known. To simplify notation, let and , so that , , and therefore, in the following, we can just use as defined in (4), without the need of referring also to . Then, for any , we use the notation

| (A.1) |

Notice also that, since is independent of for all , because we consider the factors as observed, we can always write .

The one-step-ahead predictions and the filtered probabilities are computed by means of the following steps which are similar to the Hamilton filter, see, e.g., Krolzig (2013, Chapter 5.1) and Hamilton (1989).

Then, the one-step-ahead predicted probabilities are obtained through the prior probability

| (A.2) |

So that, because of (A.1), we have

| (A.3) |

The update involves the posterior probability:

| (A.4) |

Then, since depends on only through and it depends on only through

| (A.5) |

Let,

| (A.8) | ||||

| (A.12) |

Further, notice that, from (A.1) and (A.12), the denominator of (A.4) be written as:

| (A.13) |

Taking into account (A.1), (A.2), (A.5), and (A.13), the filtered probabilities are obtained from (A.4) as

| (A.14) |

where is computed as in (A.12). The filter can started by setting either , or, equivalently, .

We then run the Kim smoother, see e.g., Krolzig (2013, Chapter 5.2) and Kim (1994). Notice that (recall that and ):

which by (A.1) implies that the sequence of smoothed probabilities is given by

| (A.15) |

This backward recursion is initiated at which is the last iteration of the filter in (A.14).

Finally, for the implementation of the EM algorithm we need to compute also the smoothed cross-probabilities, see Krolzig (2013, Chapter 5.A.2),

| (A.16) |

A.2 M-step

In the M step we have to solve the constrained maximization problem in (19). Let us start with estimation of . From (16), we have:

| (A.17) |

where is a positive normalization constant.666Specifically, we have: so . Therefore, from (17), (19), and (A.17), if we observed , the first order conditions would be:

| (A.18) |

where is the th component of .

Then, by substituting (17) into (A.18), and by replacing true factors with estimated ones, we get

| (A.19) |

and, consistently with the fact that we use a mis-specified likelihood with uncorrelated idiosyncratic components, we set

| (A.20) | ||||

where is the th row of .

Moving to estimation of , from (16), we have:

| (A.21) |

where is the same positive normalization constant as in (A.17). And, because of (18) and (A.21), if we observed the derivatives with respect to the generic th element of , i.e, , , would be (treating as known)

| (A.22) |

Now, from (19) and (A.21), the first order conditions are:

| (A.23) |

where is the -dimensional vector of Lagrange multipliers, thus it has positive entries. Then, from (A.22)

| (A.24) |

By collecting all 4 terms deriving from (A.24) into a vector, we have

| (A.25) |

where is defined in (A.16). Finally, from the first order conditions (A.23), we must have:

| (A.26) |

Let , and let . Then, (A.26) gives

| (A.27) |

By applying the adding up condition to (A.27):

| (A.32) | ||||

| (A.39) |

which implies . Therefore, from (A.27),

| (A.40) |

Appendix B Mathematical proofs

Define Let and . For , and , define

| (B.1) |

B.1 Lemmas

Lemma 7.

Lemma 8.

Lemma 10.

Lemma 11.

B.2 Proofs of Lemmas

Proof of Lemma 1.

Consider , and as defined in (38). By the definition of eigenvectors and eigenvalues, , where is the diagonal matrix of the first largest eigenvalues of in decreasing order, and is times the matrix of eigenvectors of corresponding to its largest eigenvalues. Note that and by Assumptions 1 and 2. We then have

which implies

Taking into account (B.1), after some algebra we have

| (B.2) |

It follows that

| (B.3) |

where

Consider and note that

so that

given Assumption 3(b), by Lemma A.1(a) in Massacci (2017), which implies that

| (B.4) |

Consider now,

since

and

by Assumption 3(c), then

and

| (B.5) |

Also

and

| (B.6) |

by Assumptions 2 and 4. Finally,

and

| (B.7) |

by Assumptions 2 and 4. By combining (B.3) - (B.7), and since , then

and the result stated in the lemma follows. ∎

Proof of Lemma 2.

Starting from , consider

Note that

by Assumption 2 and Assumption 3(b), so that

Further

by Lemma 1 and Assumption 3(b). It thus follows that

Moving on to , we have

Note that

with

so that

Further

by Assumption 6(a). It follows that

As for , consider

We have

by Lemma 1, Assumption 6(c) and Assumption 2. Also,

by Assumption 6(b) and Assumption 2. It follows that

Finally, for we have

Note that

by Assumption 2 and Assumption 6(c). Further,

with

by Assumption 2 and Assumption 6(c), so that taking into account Lemma 1 we have

It follows that

which completes the proof of the lemma. ∎

Proof of Lemma 3.

Consider

| (B.8) |

Using the identity in (B.2), we have

| (B.9) |

Consider

We have

by Lemma 1, Assumption 2, and the fact that, given , by Assumption 3(b) we have

| (B.10) |

Further

by Assumptions 2 and 3(b). Therefore,

| (B.11) |

Consider now

We have

and consider

with

by Assumption 3(c). Therefore, taking into account Lemma 1,

Further,

by Assumptions 2 and 6(a). Therefore,

| (B.12) |

Consider now

We have

and

by Assumptions 2 and 6(b). Therefore,

by Lemma 1. Further

by Assumptions 2 and 6(b). Therefore

| (B.13) |

Finally,

We have

with

by Assumptions 2 and 6(b). Further

by Assumptions 2 and 6(b). Therefore,

| (B.14) |

Combining equations (B.9) through (B.14), we obtain

| (B.15) |

From (B.8), (B.15) and Lemma 1, we obtain

which completes the proof of the lemma.

∎

Proof of Lemma 4.

Given the identity in (B.2), we can write

| (B.16) |

Consider

where

by Lemma 1, equation (B.10), and Assumption 3(a), and

by Assumptions 2(a), Assumption 3(a), and Assumption 3(b), so that

| (B.17) |

Consider now

We have

with

by Assumptions 3(a) and 3(c). Therefore, taking into account Lemma 1,

Further,

by Assumptions 3(a) and 6(a). Therefore,

| (B.18) |

Consider now

We have

with

by Assumptions 2, 3(a) and 4. Taking into account Lemma 1,

Further,

by Assumptions 2, 3(a) and 6(a). Therefore,

| (B.19) |

Finally,

Consider first

with

by Assumptions 2(a), 3(a), and 4, so that

Also,

by Assumption 3(c). Therefore,

| (B.20) |

By combining (B.16) through (B.20), we have

which completes the proof of the lemma. ∎

Proof of Lemma 5.

Starting from (a), and taking into account (14), consider

and note that

so that we have

which leads to

| (B.21) |

The result in (a) follows by taking into account Assumption 6(d), Lemma 3 and Lemma 4. As for (b), adding and subtracting terms we have

| (B.22) |

Taking into account the results in (a), it follows that

| (B.23) |

From (B.21), we also have that

and taking into account Assumptions 2 and 6(c), and Lemma 3,

| (B.24) |

Combining (B.22) through (B.24), it follows that

which shows (b) and completes the proof of the lemma. ∎

Proof of Lemma 6.

We proceed by following steps analogous to those in the proof of Proposition 1 in Bai (2003), and we develop the proof of the lemma for the sake of completeness. Given , pre-multiply both sides of the identity by to obtain

Given , write with and . We thus have

| (B.25) |

where

by Lemma 2. Let