Abstract

The classical algorithms for online learning and decision-making have the benefit of achieving the optimal performance guarantees, but suffer from computational complexity limitations when implemented at scale. More recent sophisticated techniques, which we refer to as oracle-efficient methods, address this problem by dispatching to an offline optimization oracle that can search through an exponentially-large (or even infinite) space of decisions and select that which performed the best on any dataset. But despite the benefits of computational feasibility, oracle-efficient algorithms exhibit one major limitation: while performing well in worst-case settings, they do not adapt well to friendly environments. In this paper we consider two such friendly scenarios, (a) “small-loss” problems and (b) IID data. We provide a new framework for designing follow-the-perturbed-leader algorithms that are oracle-efficient and adapt well to the small-loss environment, under a particular condition which we call approximability (which is spiritually related to sufficient conditions provided in (Dudík et al., 2020)). We identify a series of real-world settings, including online auctions and transductive online classification, for which approximability holds. We also extend the algorithm to an IID data setting and establish a “best-of-both-worlds” bound in the oracle-efficient setting.

Adaptive Oracle-Efficient Online Learning

| Guanghui Wang† | Zihao Hu† | Vidya Muthukumar‡ | Jacob Abernethy† |

| College of Computing† |

| School of Electrical and Computer Engineering‡ |

| School of Industrial and Systems Engineering‡ |

| Georgia Institute of Technology |

| Atlanta, GA 30339 |

| {gwang369,zihaohu,vmuthukumar8,prof}@gatech.edu |

1 Introduction

Online learning is a fundamental paradigm for modeling sequential decision making problems (Cesa-Bianchi & Lugosi, 2006; Shalev-Shwartz, 2011; Hazan, 2016). Online learning is usually formulated as a zero-sum game between a learner and an adversary. In each round , the learner first picks an action from a (finite) set with cardinality equal to . In the meantime, an adversary reveals its action . As a consequence, the learner observes , and suffers a loss , where . The goal is to minimize the regret, which is defined as the difference between the cumulative loss of the learner , and the cumulative loss of the best action in hindsight .

A wide variety of algorithms have been proposed for the goal of minimizing worst-case regret (without any consideration of computational complexity per iteration); see (Cesa-Bianchi & Lugosi, 2006; Shalev-Shwartz, 2011; Hazan, 2016) for representative surveys of this literature. These algorithms all obtain a worst-case regret bound of the order , which is known to be minimax-optimal (Cesa-Bianchi & Lugosi, 2006). Over the last two decades, sophisticated adaptive algorithms have been designed that additionally enjoy problem-dependent performance guarantees, which can automatically lead to better results in friendly environments. One of the most important example for this kind of guarantees is the so-called “small-loss” bound (Hutter & Poland, 2005; Cesa-Bianchi & Lugosi, 2006; Van Erven et al., 2014). Such a bound depends on the best cumulative loss in hindsight (i.e. ) instead of the total number of rounds (). Thus, this bound is much tighter than the worst-case bound, especially when the best decision performs well in the sense of incurring a very small loss. Another example is the “best-of-both-worlds” bound (Van Erven et al., 2014), which results in an even tighter regret bound for independent and identically distributed (IID) loss functions.

However, all of these algorithms applied out-of-the-box suffer a linear dependence on the number of decisions . This is prohibitively expensive, especially in problems such as network routing (Awerbuch & Kleinberg, 2008) and combinatorial market design (Cesa-Bianchi et al., 2014), where the cardinality of the decision set grows exponentially with the natural expression of the problem. Several efficient algorithms do exist, even for uncountably infinite decision sets, when the loss functions have certain special structure (such as linearity (Kalai & Vempala, 2005) or convexity (Zinkevich, 2003)). However, such structure is often absent in the above applications of interests.

Notice that the efficiency of the above specialized methods is usually made possible by assuming that the corresponding offline optimization problem (i.e., minimizing the (averaged) loss) can be solved efficiently. This observation motivates the oracle-efficient online learning problem (Hazan & Koren, 2016). In this setting, the learner has access to a black-box offline oracle, which, given a real-weighted dataset , can efficiently return the solution to the following problem:

| (1) |

The goal is to design oracle-efficient algorithms which can query the offline-oracle times each round. Concrete examples of such an oracle include algorithms for empirical risk minimization (Bishop, 2007), data-driven market design (Nisan & Ronen, 2007), and dynamic programming (Bertsekas, 2019).

As pointed out by Hazan & Koren (2016), the design of oracle-efficient algorithms is extremely challenging and such an algorithm does not exist in the worst case. Nevertheless, recent work (Daskalakis & Syrgkanis, 2016; Syrgkanis et al., 2016; Dudík et al., 2020) has introduced a series of algorithms which are oracle-efficient when certain sufficient conditions are met. Among them, the state-of-the-art method is the generalized-follow-the-perturbed-leader algorithm (GFTPL, Dudík et al., 2020), which is a variant of the classical follow-the-perturbed-leader (FTPL) algorithm (Kalai & Vempala, 2005). Similar to FTPL, GFTPL perturbs the cumulative loss of each decision by adding a random variable, and chooses the decision with the smallest perturbed loss as . However, the vanilla FTPL perturbs each decision independently, which requires to generate independent random variables in total. Moreover, the oracle in (1) can not be applied here since as it cannot handle the perturbation term. To address these limitations, GFTPL only generates a noise vector of low dimension (in particular, much smaller dimension than the size of the decision set) in the beginning, and constructs dependent perturbations based on the multiplication between the noise vector and a perturbation translation matrix (PTM). Therefore, the PTM critically ensures that the computational complexity for the noise generation itself is largely reduced. Furthermore, oracle-efficiency can be achieved by setting the elements in the PTM as carefully designed synthetic losses. Dudík et al. (2020) show that a worst-case optimal regret bound can be obtained when the PTM is admissible, i.e., every two rows are substantially distinct. This serves as a sufficient condition for achieving oracle-efficiency.

While these results form a solid foundation for general worst-case oracle-efficient online learning, it remains unclear whether problem-dependent, or data-adaptive bounds are achievable in conjunction with oracle-efficiency. In other words, the design of a generally applicable oracle-efficient and adaptive online learning algorithm has remained open. In this paper, we provide an affirmative answer to this problem, and make the following contributions.

-

•

We propose a variant of the GFTPL algorithm (Dudík et al., 2020), and derive a new sufficient condition for ensuring oracle-efficiency while achieving the small-loss bound. Our key observation is that while the admissibility condition of the PTM in GFTPL successfully stabilizes the algorithm (by ensuring that is small), it does not always enable adaptation. We address this challenge via a new condition for PTM, called approximability. This condition ensures a stronger stability measure, i.e., the ratio of and is upper-bounded by a universal constant for any , which is critical for proving the small-loss bound. In summary, we obtain the small-loss bound by equipping GFTPL with an approximable PTM, a data-dependent step-size and Laplace distribution for the perturbation noise. As a result of these changes, our analysis path differs significantly from that of Dudík et al. (2020). Our new condition of approximability is simple and interpretable, and can be easily verified for an arbitrary PTM. It shares both similarities and differences from the admissibility condition proposed in Dudík et al. (2020). We demonstrate this through several examples where one of the sufficient conditions holds, but not the other.

-

•

We identify a series of real-world applications for which we can construct approximable PTMs: (a) a series of online auctions problems (Dudík et al., 2020); (b) problems with a small adversary action space (Daskalakis & Syrgkanis, 2016); and (c) transductive online classification (Syrgkanis et al., 2016; Dudík et al., 2020). This is the first-time that the small-loss bound is obtained in all of these applications. To achieve this, we introduce novel PTMs and analysis for showing the approximability condition on these PTMs.

-

•

We achieve the “best-of-both-worlds” bound, which enjoys even tighter results when the data is IID or the number of leader changes is small. The main idea is to combine our proposed algorithm with vanilla FTL leveraging ideas from a meta-algorithm called FlipFlop introduced in Van Erven et al. (2014).

2 Related Work

Our work contributes to two bodies of work: oracle-efficient online learning and adaptive online learning. In this section, we briefly review the related work in these areas.

2.1 Oracle-efficient online learning

For oracle-efficient online learning, the pioneering work of Hazan & Koren (2016) points out that oracle-efficient methods do not exist when dealing with general hostile adversaries, which implies that additional assumptions on the problem structure have to be made. Daskalakis & Syrgkanis (2016) consider the setting in which the cardinality of the adversary’s action set is finite and small, and propose to add a series of “fake” losses to the learning history based on random samples from . They prove that for this setting an regret bound can be obtained. Syrgkanis et al. (2016) study the contextual combinatorial online learning problem, where each action is associated with a binary vector. They make the assumption that the loss function set contains all linear functions as a sub-class. The approach in Syrgkanis et al. (2016) constructs a set of synthetic losses for perturbation based on randomly-selected contexts, and achieves worst-case optimal bounds when all the contextual information can be obtained beforehand, or when there exists a small set of contexts that can tell each decision apart. Dudík et al. (2020) is the first work to focus on the general non-contextual setting, and propose the generalized FTPL algorithm. This algorithm generates a small number of random variables at the beginning, and then perturbs the learning history via the innter product between the PTM matrix and the random variables. The algorithm can be implemented efficiently by setting the entries of the PTM as carefully designed loss values. Niazadeh et al. (2021) consider a more complicated combinatorial setting where the offline problem is NP-hard, but a robust approximation oracle exists. For this case, they propose an online algorithm based on a multiplicative approximation oracle, and prove that it has low approximate regret, which is a measure weaker than regret, since it only compares with a fraction of the cumulative loss of the best decision in hindsight. Note that none of the aforementioned methods can be easily shown to adapt to friendly structure in data. Recently, several concurrent works (Block et al., 2022; Haghtalab et al., 2022a) investigate how to obtain tighter bounds oracle-efficiently in the smoothed-analysis setting where the distribution of data is close to the uniform distribution (Rakhlin et al., 2011; Haghtalab et al., 2022b). The main focus is to adapt to the VC dimension of the hypothesis class, rather than improve the dependence on the number of rounds .

In this paper, we mainly focus on the so-called the learning with expert advice setting (Cesa-Bianchi & Lugosi, 2006), where the action set is discrete, and the loss can be highly non-convex. On the other hand, efficient algorithms can be obtained even for continuous action sets when the loss functions have certain properties, such as linearity (Kalai & Vempala, 2005; Hutter & Poland, 2005; Awerbuch & Kleinberg, 2008), convexity (Zinkevich, 2003; Hazan et al., 2007) or submodularity (Hazan & Kale, 2012). Finally, we note that, in this paper we mainly focus on the full-information setting, where the learner can observe the whole loss function after the action is submitted. Oracle-efficient online learning has also been widely studied in the contextual bandit setting (Langford & Zhang, 2008; Dudik et al., 2011; Agarwal et al., 2014; Foster et al., 2018; Foster & Rakhlin, 2020). The nature of the oracle-efficient guarantees for the contextual bandit problem is much weaker compared to full-information online learning: positive results either assume a stochastic probability model on the responses given covariates (e.g. Foster et al. (2018); Foster & Rakhlin (2020)) or significantly stronger oracles than Eq. (1) (e.g. Agarwal et al. (2014)).

2.2 Adaptive online learning

In this paper, we focus on designing oracle-efficient algorithms with problem-dependent regret guarantees. Note that this kind of bound can be achieved by many inefficient algorithms in general, such as Hedge and its variants (Cesa-Bianchi & Lugosi, 2006; De Rooij et al., 2014; Luo & Schapire, 2015), follow-the-perturbed-leader (Kalai & Vempala, 2005; Van Erven et al., 2014) or follow-the-regularized-leader (Orabona, 2019). Small-loss bounds can also be obtained efficiently when the loss functions are simply linear (Hutter & Poland, 2005; Syrgkanis et al., 2016). On the other hand, in online convex optimization, small-loss bounds can be obtained when the loss functions are additionally smooth (Srebro et al., 2010; Orabona et al., 2012; Wang et al., 2020). However, these algorithms heavily rely on the special structure of the loss functions. In this paper, we take the first step to extend these methods to support the more complicated (generally non-convex) problems which appear in real-world applications.

Apart from the small-loss, there exist other types of problem-dependent bounds, such as second-order bound (Cesa-Bianchi et al., 2005; Gaillard et al., 2014), quantile bound (Chaudhuri et al., 2009; Koolen & Erven, 2015), or parameter-free bound (Luo & Schapire, 2015; Cutkosky & Orabona, 2018). Moreover, advanced adaptive results can also be obtained by minimizing more advanced performances measures other than regret, such as adaptive regret (Hazan & Seshadhri, 2007; Zhang et al., 2019), or dynamic regret (Zhang et al., 2018; Zhao et al., 2020). How to obtain these more refined theoretical guarantees in the oracle-efficient setting remains an interesting open problem.

3 GFTPL with Small-Loss Bound

In this section, we ignore computational complexity for the moment and we provide a new FTPL-type algorithm that enjoys the small-loss bound. We then show that the proposed algorithm can be implemented efficiently by the offline oracle in Section 4. Before diving into the details, we first briefly recall the definition of online learning and regret.

Preliminaries.

The online decision problem we consider can be described as follows. In each round , a learner picks an action . After observing the adversary’s decision , the learner suffers a loss where the loss function is known to the learner and adversary. The regret of an online learning algorithm is defined as

where is the cumulative loss of the best action in hindsight, and the expectation is taken only with respect to the potentially randomized strategy of the learner.

Our proposed algorithm follows the framework of GFTPL (Dudík et al., 2020). We first briefly introduce to the intuition behind this method. Specifically, in each round , GFTPL picks by solving the following optimization problem:

where is a -dimensional noise vector () generated from a uniform distribution, and is the -th row of a matrix , which is referred to as the perturbation translation matrix (PTM). Compared to vanilla FTPL, which generates random variables (one for each expert), GFTPL only generates random variables, where is much smaller than . Each expert is perturbed by a different linear combination of these random variables based on the PTM . The results of Dudík et al. (2020) rely on the following assumption on .

Definition 1.

(-admissibility (Dudík et al., 2020)) Let be a matrix, and denote as the -th row of , and the -th element of . Then, is -admissible if (a) , , such that ; and (b) , such that , then .

The -admissibility guarantees that every two rows in are significantly distinct. As pointed out by Dudík et al. (2020), this is the essential property required by GFTPL, and is used to stabilize the algorithm in the analysis, i.e., ensuring that is small. However, the adaptive analysis of inefficient FTPL (Hutter & Poland, 2005) (i.e. using a noise vector of dimension equal to the size of the decision set) reveals that this type of stability is insufficient. Instead, one needs to control the following and ,

| (2) |

the ratio of the probability of picking the -th decision in two consecutive rounds. We note that -admissibility is not sufficient to ensure this quantity is bounded, as we establish in the following counter-example lemma. (See Appendix A.1 for proof).

Lemma 1.

There is an instance of a -admissible , and a sequence , such that if we run GFTPL we can have for some and some .

To address this problem, we propose a new property for . Define as the -ball of size .

Definition 2.

(-approximability) Let . We say that is -approximable if

It may not be immediately obvious how we arrived at this condition, so let us provide some intuition. The goal of perturbation methods in sequential decision problems, going back to the early work of Hannan (1957), is to ensure that the algorithm is “hedging” across all available alternative decisions. A newly observed data point may make expert suddenly look more attractive than expert , as we have now introduced a new gap in their measured loss values. With this in mind, we say that is a “good” (i.e. approximable) choice for the PTM, if this gap can be overcome (hedged) by some small (i.e. likely) perturbation , so that makes up the difference. The inequality makes this property flexible and much easier to satisfy in real-world applications: we only need the gap approximation from above. Later, we will show that -approximability guarantees the required stability measure in (2), and thus is critical for the small-loss bound.

We want to emphasize two final points. First, the -approximability condition is purely for analysis purposes and we don’t need compute the quantity in response to and . Second, much of the computational and decision-theoretic challenges rest heavily on the careful design of . The PTM allows the algorithm to perform the appropriate hedging across an exponentially-sized set of experts with only dimensions of perturbation. As we demonstrate in the following example, we can always construct a -approximable , with , but at the expense of computational efficiency. The proposed will not generally be compatible with the given oracle, in the sense that the optimization problem underlying GFTPL cannot be written in the form of Eq. (1). In the next section, we will show how to address this problem via another condition on called implementablity.

Simple Example

For any online learning problem we may construct as follows. Let , and define the th row to be the binary representation of the index , with values instead of . We claim that this is -approximable, for . We can satisfy the condition of Definition 2, by setting . It is easy to see that for any we have , where the last inequality holds because for any .

Comparison beteeen -approximabilty (this paper) and -admissibility (Dudík et al., 2020)

We note that, although -approximability leads to a much tighter bound, it is not stronger than -admissibility. Instead, they are incomparable conditions. Specifically:

-

•

In Section 4.1 we demonstrate that when is binary, admissibility directly leads to approximability. As shown by Dudík et al. (2020), a binary and admissible exists in various online auctions problems, including VCG with bidder-specific reserves (Roughgarden & Wang, 2019), envy-free item pricing (Guruswami et al., 2005), online welfare maximization in multi-unit auction (Dobzinski & Nisan, 2010), and simultaneous second-price auctions (Daskalakis & Syrgkanis, 2016). We can directly obtain an approximable in such cases.

- •

-

•

In section 4.2, we show that, when the adversary’s action space is small, we can always construct a -approximable , while a -admissible does not exist in general.

-

•

In Appendix A.2, we show that in some cases a -admissible can be obtained while -approximability cannot be achieved.

Equipped with the -approximable PTM, we develop a generalized follow-the-perturbed-leader algorithm with the Laplace distribution for the noise 111Note that the Laplace distribution is not the unique choice to get the small-loss bound. In Appendix A.5, we prove that the perturbation indeed works for any . and a time-varying step size, which is summarized in Algorithm 1. This choice of Laplace distribution is significantly different from the choice of uniform distribution originally used by GTFPL: it turns out that a continuous distribution is required to satisfy Eq. (2) and thereby the small-loss bound. Note that here we ignored the time complexity and only focus on the regret. We will specify how to construct in the next section. For the proposed algorithm, we successfully obtain the following stronger stability property.

Lemma 2.

Assume is -approximable. Let . Then in each round , we have

Note that we replace the term in (2) with , as a time-varying step-size is used. Based on Lemma 2, we obtain the regret bound of Algorithm 1 as follows.

Theorem 1.

Assume is -approximable, and let . Algorithm 1, with for any , achieves the following regret bound:

| (3) |

Comparison to GFTPL (Dudík et al., 2020)

The original GFTPL algorithm has an regret bound. For the dependence on , our bound reduces to in the worst-case, and automatically becomes tighter when is small. On the other hand, for the dependence on other terms, we note that both and are lower bounded by , and their exact relationship depends on the specific problem. In Section 4, we show that for many auction applications, the two terms are on the same order. Moreover, in cases such as when is small, Algorithm 1 with an appropriate leads to regret bound, while the regret bound of GFTPL in Dudík et al. (2020) can blow up since can be infinitely small.

4 Oracle-efficiency and Applications

In this section, we discuss how to run Algorithm 1 in an oracle-efficient way. Following Dudík et al. (2020), we introduce the following definition.

Definition 3 (Implementability).

A matrix is implementable with complexity if for each there exists a dataset , with , such that ,

Based on Definition 3, it is easy to get the following theorem, which is similar to Theorem 2.10 of Dudík et al. (2020).

Theorem 2.

If is implementable, then Algorithm 1 is oracle-efficient and has a per-round complexity .

In the following sub-sections, we discuss how to construct approximable and implementable matrices in different applications.

4.1 Applications in online auctions

In this part, we apply Algorithm 1 to online auction problems, which is the main focus of Dudík et al. (2020). To deal with this sort of problems, we first transform Algorithm 1 to online learning with rewards setting, i.e., in each round , after choosing , instead of suffering a loss, the learner obtains a reward . For this case, it is straightforward to see that running Algorithm 1 on a surrogate loss directly leads to the small-loss bound. To proceed, we slightly change this procedure and obtain Algorithm 2. The main difference is that, we implement with the reward function , instead of the surrogate loss . This makes the construction of much easier. We have the following regret bound for Algorithm 2.

Corollary 1.

Let . Assume is -approximable w.r.t. and implementable with function . Then Algorithm 2 is oracle-efficient and achieves the following regret bound:

where is the cumulative reward of the best expert.

Next, we discuss how to construct the PTM in several auction problems.

Auctions with binary and admissible .

As shown by Dudík et al. (2020), in many online auction problems, such as the Vickrey-Clarkes-Groves (VCG) mechanism with bidder-specific reserves (Roughgarden & Wang, 2019), envy-free item pricing (Guruswami et al., 2005), online welfare maximization in multi-unit auction (Dobzinski & Nisan, 2010) and simultaneous second-price auctions (Daskalakis & Syrgkanis, 2016), there exists a binary PTM which is -admissible and implementable with rows where . For these cases, we have the following lemma. The proof is deferred to Appendix B.1.

Lemma 3.

Let be a binary matrix and -admissible, then is -approximable.

Note that, is binary and 1-admissible, so every two rows of Gamma differ by at least one element. This means that must, at the very least, include columns to encode each row. Combining this fact with Lemma 3 and Corollary 1, we can obtain an bound for all of the above problems. Compared to the original GFTPL algorithm, our condition leads to a similar dependence on and a tighter dependence on due to the improved small-loss bound. More details about the aforementioned auction problems and corresponding regret bounds can be found in Appendix B.2.

Level auction

The class of level auctions was first introduced by Morgenstern & Roughgarden (2015), and optimizing over this class enables a multiplicative approximation with respect to Myerson’s optimal auction when the distribution of each bidder’s valuation is independent from others. For this problem, the PTM in Dudík et al. (2020) is not easily to be shown approximable. To address this problem, we propose a novel way of constructing an approximable and implementable PTM. The key idea is to utilize a coordinate-wise threhold function to implement . Note that this kind of function can not be directly obtained. Instead, we create an augmented problem with a surrogate loss to deal with this issue. For level auction with single-item, -bidders, -level and -discretization level, our method enjoys an regret bound, which is tighter than the (note that ) of the original GFTPL both on its dependence on the number of rounds and auction parameters . Due to page limitations, we postpone the detailed problem description and proof to Appendix B.3.

4.2 Other applications

Oracle learning and finite parameter space

In many real-world applications, such as security game (Balcan et al., 2015) and online bidding with finite threshold vectors (Daskalakis & Syrgkanis, 2016), the decision set is extremely large, while the adversary’s action set is finite and small. For these problems, we can construct an implementable PTM based the following lemma, whose proof can be found in Appendix B.4.

Lemma 4.

Consider the setting with (), then there exists a -approximable and implementable with columns and complexity 1.

Combining Lemma 4 and Theorem 1, and configuring , we observe that our algorithm achieves a small-loss bound on the order of . On the other hand, because of the continuity of the loss functions in this setting, a -admissible PTM in general does not exist (as may approach 0). Therefore, our proposed condition not only leads to a tighter bound, but can also solve problems that the original GFTPL (Dudík et al., 2020) can not handle.

Transductive online classification

Finally, we consider the transductive online classification problem (Syrgkanis et al., 2016; Dudík et al., 2020). In this setting, the decision set consists of binary classifiers. In each round , firstly the adversary picks a feature vector , where . Then, the learner chooses a classifier from . After that, the adversary reveals the label , and the learner suffers a loss . We assume the problem is transductive, i.e., the learner has access to the adversary’s set of vectors at the beginning. For this setting, we achieve the following results (the proof is in Appendix B.5).

Lemma 5.

Consider transductive online classification with . Then there exists a 1-approximable and implementable PTM with columns and complexity 1. Moreover, Algorithm 1 with such a PTM and appropriately chosen parameters achieves regret.

Negative implementability

In the this paper we assume that the offline oracle can solve the minimization problem in (1) given any real-weights. In some cases, the oracle can only accept positive weights. This problem can be solved by constructing negative implementable PTM (Dudík et al., 2020). In most of the cases discussed above, negative implementable and approximable PTM exist. This is formally shown in Appendix B.6.

5 Best-of-Both-Worlds Bound: Adapting to IID data

In this section, we switch our focus to adapting between adversarial and stochastic data. While the GFTPL algorithm enjoys an -type regret bound on adversarial data, it is possible to obtain much better rates on stochastic data. For example, by setting all step sizes as , Algorithm 1 reduces to the classical FTL algorithm, which suffers linear regret in the adversarial setting but enjoys much tighter bounds when the data is IID or number of leader changes is small. To be more specific, we introduce the following regret bound for FTL.

Lemma 6 (Lemma 9, De Rooij et al. (2014)).

Let be the output of the FTL algorithm at round , the set of rounds where the leader changes, and the “mixability gap”222Here, we use the special definition of the mixability gap for the FTL algorithm. The details can be found in the second paragraph, page 1286 of De Rooij et al. (2014). at round . Then for any , the regret of FTL is bounded by

Note that since and , we know . For the i.i.d case, if the mean loss of the best expert is smaller than that of other experts by a constant, then due to the law of large numbers, the number of leader changes would be small, which results in a constant regret bound (De Rooij et al., 2014).

Our goal is to obtain a ”best-of-both-worlds” bound, which can ensure the small-loss bound in general, while automatically leading to tighter bounds for IID data like FTL. We will now design an algorithm that achieves such a bound by adaptively choosing between GFTPL and FTL depending on which algorithm appears to be achieving a lower regret. The essence of this idea was first introduced in the FlipFlop algorithm (De Rooij et al., 2014), who showed best-of-both-worlds bounds in the inefficient case. Our contribution in this section is to adapt this idea to the oracle-efficient setting. Denote as the attainable regret bound (as in Theorem 1) for running Algorithm 1 alone and to be that of FTL. In the following, we develop a new algorithm and prove that it is optimal in both worlds, that is, its regret is on the order of .

Initialization:

The proposed algorithm, named as oracle-efficient flipflop (OFF) algorithm, is summarized in Algorithm 3. The core idea is to switch between FTL and GFTPL (Algorthm 1) based on the comparison of the estimated regret. We optimistically start from FTL. In each round , we firstly pick based on the current algorithm , and then obtain the adversary’s action (line 2). Next, we compute the estimated bounds of regret of both algorithms until round (line 3). Specifically, let and be the set of rounds up to in which we run FTL and GFTPL. Then, the estimated regret of FTL in is given by and the estimated regret of GFTPL in can be bounded via Theorem 1:

| (4) |

where and we set . Note that, the two quantities defined above are the exact regret upper bounds of the two algorithms on their sub-time intervals up to round , due to the fact that the regret bounds provided in Lemma 6 and Theorem 1 are timeless. Moreover, note that the two values can be computed by the oracle. We compare the estimated regret of both algorithms, and use the algorithm which performs better for the next round (lines 4-8).

For the proposed algorithm, we have the following theoretical guarantee (the proof can be found in Appendix C).

Theorem 3.

Assume we have a -approximable , then Algorithm 3 is able to achieve the following bound:

where and .

The Theorem above shows that the regret of Algorithm 3 is the minimum of the regret upper bounds of GFTPL and FTL. Thus, it ensures the -type bound in the worst case, while automatically achieves the much better constant regret bound of FTL under iid data without knowing the presence of stochasticity in data beforehand.

6 Conclusion

In this paper, we establish a sufficient condition for the first-order bound in the oracle-efficient setting by investigating a variant of the generalized follow-the-perturbed-leader algorithm.

We also show the condition is satisfied in various applications. Finally, we extend the algorithm to adapt to IID losses and achieve a “best-of-both-worlds” bound. In the future, we would like to investigate

how to achieve tighter results for oracle-efficient setting, such as the second-order bound (De Rooij et al., 2014) and the quantile bound (Koolen & Erven, 2015).

Acknowledgments. We gratefully thank the AI4OPT Institute for funding, as part of NSF Award 2112533. We gratefully acknowledge the NSF for their support through Award IIS-2212182 and Adobe Research for their support through a Data Science Research Award. Part of this work was conducted while the authors were visiting the Simons Institute for the Theory of Computing.

References

- Agarwal et al. (2014) Agarwal, A., Hsu, D., Kale, S., Langford, J., Li, L., and Schapire, R. Taming the monster: A fast and simple algorithm for contextual bandits. In Proceedings of the 27th International Conference on Machine Learning, pp. 1638–1646, 2014.

- Awerbuch & Kleinberg (2008) Awerbuch, B. and Kleinberg, R. Online linear optimization and adaptive routing. Journal of Computer and System Sciences, 74(1):97–114, 2008.

- Balcan et al. (2015) Balcan, M.-F., Blum, A., Haghtalab, N., and Procaccia, A. D. Commitment without regrets: Online learning in stackelberg security games. In Proceedings of the 16th ACM conference on economics and computation, pp. 61–78, 2015.

- Bertsekas (2019) Bertsekas, D. Reinforcement learning and optimal control. Athena Scientific, 2019.

- Bishop (2007) Bishop, C. M. Pattern Recognition and Machine Learning. Springer, 2007.

- Block et al. (2022) Block, A., Dagan, Y., Golowich, N., and Rakhlin, A. Smoothed online learning is as easy as statistical learning. arXiv preprint arXiv:2202.04690, 2022.

- Cesa-Bianchi & Lugosi (2006) Cesa-Bianchi, N. and Lugosi, G. Prediction, Learning, and Games. Cambridge University Press, 2006.

- Cesa-Bianchi et al. (2005) Cesa-Bianchi, N., Mansour, Y., and Stoltz, G. Improved second-order bounds for prediction with expert advice. In Proceedings of the 18th Annual Conference on Learning Theory, pp. 217–232, 2005.

- Cesa-Bianchi et al. (2014) Cesa-Bianchi, N., Gentile, C., and Mansour, Y. Regret minimization for reserve prices in second-price auctions. IEEE Transactions on Information Theory, 61(1):549–564, 2014.

- Chaudhuri et al. (2009) Chaudhuri, K., Freund, Y., and Hsu, D. J. A parameter-free hedging algorithm. 22, 2009.

- Cutkosky & Orabona (2018) Cutkosky, A. and Orabona, F. Black-box reductions for parameter-free online learning in banach spaces. In Proceedings of the 31st Conference On Learning Theory, pp. 1493–1529, 2018.

- Daskalakis & Syrgkanis (2016) Daskalakis, C. and Syrgkanis, V. Learning in auctions: Regret is hard, envy is easy. In The 57th Annual Symposium on Foundations of Computer Science, pp. 219–228, 2016.

- De Rooij et al. (2014) De Rooij, S., Van Erven, T., Grünwald, P. D., and Koolen, W. M. Follow the leader if you can, hedge if you must. The Journal of Machine Learning Research, 15(1):1281–1316, 2014.

- Dobzinski & Nisan (2010) Dobzinski, S. and Nisan, N. Mechanisms for multi-unit auctions. Journal of Artificial Intelligence Research, 37:85–98, 2010.

- Dudik et al. (2011) Dudik, M., Hsu, D., Kale, S., Karampatziakis, N., Langford, J., Reyzin, L., and Zhang, T. Efficient optimal learning for contextual bandits. In Proceedings of the Twenty-Seventh Conference on Uncertainty in Artificial Intelligence, pp. 169–178, 2011.

- Dudík et al. (2020) Dudík, M., Haghtalab, N., Luo, H., Schapire, R. E., Syrgkanis, V., and Vaughan, J. W. Oracle-efficient online learning and auction design. Journal of the ACM, 67(5):1–57, 2020.

- Foster & Rakhlin (2020) Foster, D. and Rakhlin, A. Beyond ucb: Optimal and efficient contextual bandits with regression oracles. In Proceedings of the 37th International Conference on Machine Learning, pp. 3199–3210. PMLR, 2020.

- Foster et al. (2018) Foster, D., Agarwal, A., Dudik, M., Luo, H., and Schapire, R. Practical contextual bandits with regression oracles. In Proceedings of the 35th International Conference on Machine Learning, pp. 1539–1548, 2018.

- Gaillard et al. (2014) Gaillard, P., Stoltz, G., and Van Erven, T. A second-order bound with excess losses. In Proceedings of the 27th Annual Conference on Learning Theory, pp. 176–196, 2014.

- Guruswami et al. (2005) Guruswami, V., Hartline, J. D., Karlin, A. R., Kempe, D., Kenyon, C., and McSherry, F. On profit-maximizing envy-free pricing. In 16th Annual ACM-SIAM Symposium on Discrete Algorithms, pp. 1164–1173, 2005.

- Haghtalab et al. (2022a) Haghtalab, N., Han, Y., Shetty, A., and Yang, K. Oracle-efficient online learning for beyond worst-case adversaries. arXiv preprint arXiv:2202.08549, 2022a.

- Haghtalab et al. (2022b) Haghtalab, N., Roughgarden, T., and Shetty, A. Smoothed analysis with adaptive adversaries. In IEEE 62nd Annual Symposium on Foundations of Computer Science, pp. 942–953, 2022b.

- Hannan (1957) Hannan, J. Approximation to bayes risk in repeated play. Contributions to the Theory of Games, 3(2):97–139, 1957.

- Hazan (2016) Hazan, E. Introduction to online convex optimization. Foundations and Trends in Optimization, 2(3-4):157–325, 2016.

- Hazan & Kale (2012) Hazan, E. and Kale, S. Online submodular minimization. In Journal of Machine Learning Research, volume 13, pp. 2903–2922, 2012.

- Hazan & Koren (2016) Hazan, E. and Koren, T. The computational power of optimization in online learning. In Proceedings of the 48th annual ACM symposium on Theory of Computing, pp. 128–141, 2016.

- Hazan & Seshadhri (2007) Hazan, E. and Seshadhri, C. Adaptive algorithms for online decision problems. Electronic Colloquium on Computational Complexity, 88, 2007.

- Hazan et al. (2007) Hazan, E., Agarwal, A., and Kale, S. Logarithmic regret algorithms for online convex optimization. Machine Learning, 69(2-3):169–192, 2007.

- Hutter & Poland (2005) Hutter, M. and Poland, J. Adaptive online prediction by following the perturbed leader. Journal of Machine Learning Research, 6(22):639–660, 2005.

- Kalai & Vempala (2005) Kalai, A. and Vempala, S. Efficient algorithms for online decision problems. Journal of Computer and System Sciences, 71(3):291–307, 2005.

- Koolen & Erven (2015) Koolen, W. M. and Erven, T. V. Second-order quantile methods for experts and combinatorial games. In Proceedings of the 28th Conference on Learning Theory, pp. 1155–1175, 2015.

- Langford & Zhang (2008) Langford, J. and Zhang, T. The epoch-greedy algorithm for multi-armed bandits with side information. In Advances in Neural Information Processing Systems 20, pp. 817–824, 2008.

- Luo & Schapire (2015) Luo, H. and Schapire, R. E. Achieving all with no parameters: Adanormalhedge. In Proceedings of the 28th Conference on Learning Theory, pp. 1286–1304, 2015.

- Morgenstern & Roughgarden (2015) Morgenstern, J. H. and Roughgarden, T. On the pseudo-dimension of nearly optimal auctions. Advances in Neural Information Processing Systems 28, 2015.

- Niazadeh et al. (2021) Niazadeh, R., Golrezaei, N., Wang, J. R., Susan, F., and Badanidiyuru, A. Online learning via offline greedy algorithms: Applications in market design and optimization. In Proceedings of the 22nd ACM Conference on Economics and Computation, pp. 737–738, 2021.

- Nisan & Ronen (2007) Nisan, N. and Ronen, A. Computationally feasible vcg mechanisms. Journal of Artificial Intelligence Research, 29:19–47, 2007.

- Orabona (2019) Orabona, F. A modern introduction to online learning. arXiv preprint arXiv:1912.13213, 2019.

- Orabona et al. (2012) Orabona, F., Cesa-Bianchi, N., and Gentile, C. Beyond logarithmic bounds in online learning. In Proceedings of the 15th International Conference on Artificial Intelligence and Statistics, pp. 823–831, 2012.

- Rakhlin et al. (2011) Rakhlin, A., Sridharan, K., and Tewari, A. Online learning: Stochastic, constrained, and smoothed adversaries. 24, 2011.

- Roughgarden & Wang (2019) Roughgarden, T. and Wang, J. R. Minimizing regret with multiple reserves. ACM Transactions on Economics and Computation, 7(3):1–18, 2019.

- Shalev-Shwartz (2011) Shalev-Shwartz, S. Online learning and online convex optimization. Foundations and Trends in Machine Learning, 4(2):107–194, 2011.

- Srebro et al. (2010) Srebro, N., Sridharan, K., and Tewari, A. Smoothness, low-noise and fast rates. In Advances in Neural Information Processing Systems 23, pp. 2199–2207, 2010.

- Syrgkanis et al. (2016) Syrgkanis, V., Krishnamurthy, A., and Schapire, R. Efficient algorithms for adversarial contextual learning. In Proceedings of the 33rd International Conference on Machine Learning, pp. 2159–2168, 2016.

- Van Erven et al. (2014) Van Erven, T., Kotlowski, W., and Warmuth, M. K. Follow the leader with dropout perturbations. In Proceedings of The 27th Conference on Learning Theory, pp. 949–974, 2014.

- Wang et al. (2020) Wang, G., Lu, S., Hu, Y., and Zhang, L. Adapting to smoothness: A more universal algorithm for online convex optimization. In Proceedings of the 34th AAAI Conference on Artificial Intelligence, 2020.

- Zhang et al. (2018) Zhang, L., Lu, S., and Zhou, Z.-H. Adaptive online learning in dynamic environments. In Advances in Neural Information Processing Systems 31, pp. 1323–1333, 2018.

- Zhang et al. (2019) Zhang, L., Liu, T.-Y., and Zhou, Z.-H. Adaptive regret of convex and smooth functions. In Proceedings of the 36th International Conference on Machine Learning, pp. 7414–7423, 2019.

- Zhao et al. (2020) Zhao, P., Zhang, Y.-J., Zhang, L., and Zhou, Z.-H. Dynamic regret of convex and smooth functions. In Advances in Neural Information Processing Systems 33, pp. 12510–12520, 2020.

- Zinkevich (2003) Zinkevich, M. Online convex programming and generalized infinitesimal gradient ascent. In Proceedings of the 20th International Conference on Machine Learning, pp. 928–936, 2003.

Appendix A Omitted Proofs from Section 3

In this section, we provide the omitted proofs from Section 3.

A.1 Proof of Lemma 1

Recall that in GFTPL (Dudík et al., 2020), is picked by solving the following optimization problem:

where the entries of the random vector are sampled from a uniform distribution for some hyperparameter . Recall that to prove Lemma 1, we wish to find a counterexample of a -admissible PTM and a sequence such that the probability distribution induced by GFTPL yields for some and some . This precludes the possibility of obtaining a stronger small-loss bound on instances that only satisfy -admissibility and no other special properties.

In the following, we show that such a counterexample can be found in this case by exploiting the property of the bounded support of the distribution. We then demonstrate that a similar counterexample exists even if the uniform distribution is replaced by distributions with unbounded support.

A.1.1 Case 1: Uniform noise distribution (or, more generally, distributions with bounded support)

Fix experts and round . Suppose that we can obtain an implementable which is -admissible with column. In this case, is a scalar random variable, and we have

Similarly, at round we have

Since the probability density function of has bounded support, it is straightforward to pick appropriate loss functions such that lies outside the support of the density function while lies inside the support of the density function. As a consequence, we get while .

A.1.2 Case 2: Noise distributions with unbounded support

One may argue that the above bad case happens mainly because the noise density has bounded support. We now show that such counterexamples can also be constructed when the noise is generated from distributions with unbounded support, such as the Laplace distribution — with a slightly larger number of experts. Specifically, we consider experts and the PTM , which is 0.5-admissible with column. Then, we have

where we have defined , and as shorthand. Now, we pick loss functions such that and . Because and the distribution of has infinite support, we have . On the other hand, for round a similar argument yields

Now, we pick , and . For this choice, we get

which implies that . This in turn implies that , completing the proof of the counterexample. ∎

These counterexamples imply that the condition of -admissibility alone on the PTM is not sufficient to control the stronger stability measure required for a small-loss bound. Consequently, new assumptions on need to be introduced.

A.2 Counterexamples showing that -admissiblity does not necessarily lead to -approximability

In this paper, we introduced a new sufficient condition of -approximability that implies not only worst-case regret bounds but also regret bounds that adapt to the size of the best loss in hindsight. It is natural to ask about the relationship of this sufficient condition with -admissibility. In this section, we show that exist -admissible PTMs that do not satisfy -approximability. (Note that the reverse statement is also true: Lemma 4 constructs -approximable PTMs that are not in general -admissible.)

The counterexample is precisely the one used in Section A.1.2. That is, there are experts, and the PTM is given by . Note that is 0.5-admissible with one column. Further, we consider an output such that and . We proceed to show that this PTM is not approximable. To prove this, note that for some scalar to satisfy the requisite approximability condition, we need and . This is clearly unsatisfiable by any scalar .

A.3 Proof of Theorem 1

We now provide the detailed proof of Theorem 1. We begin by introducing some notation specific to this proof. We denote by the row of related to expert , and by the row related to the best-expert-in-hindsight . Further, denotes the row of related to expert and denotes the -th component of the row . We also denote the PDF of the noise vector at round , , as . Finally, the learner’s action set is denoted by .

Our proof begins with the framework used by typical FTPL analyses (Hutter & Poland, 2005; Syrgkanis et al., 2016; Dudík et al., 2020). We first divide the regret into two terms:

| (5) |

Above, the expectation is only with respect to the internal randomness of the learner and is the best decision in hindsight. Further, the expert

is usually referred to as the infeasible leader (Hutter & Poland, 2005) at round , since can only be obtained after is chosen.

Next, we bound the two terms of (5) respectively. Term 1 measures the stability of GFTPL by tracking how close its performance is to that of the idealized infeasible leader. We obtain the following upper bound on Term 1 which heavily leverages the key technical Lemma 2.

Lemma 7.

Assume that the PTM is -approximable, and Algorithm 1 is applied with , where and is some universal constant. Then for all we have:

Next, Term 2 measures the approximation error between the infeasible leader and the true best expert in hindsight. The following lemma, which is a simple extension of the classical be-the-leader lemma (Cesa-Bianchi & Lugosi, 2006), bounds Term 2.

Lemma 8.

Assume that the PTM is -approximable. Then, for all , we have

We prove Lemmas 2, 7, and 8 in Appendix A.3.1, A.3.2 and A.3.3 respectively. The proof of Theorem 1 follows by directly combining (5), Lemma 7 and Lemma 8.

A.3.1 Proof of Lemma 2

Note that we can write

Our approach will relate and for every : at a high level, a similar approach is also used in the analysis of contextual online learning for linear functions by Syrgkanis et al. (2016) (although several other aspects of our analysis are different). Then, for any fixed choice of we have

| (6) |

Above, denotes the indicator function and inequality is based on the fact that for any ,

| (7) |

and the final equality is because the support of is unbounded. To proceed, we introduce and prove the following lemma.

Lemma 9.

Suppose is -approximable. Then, there exists a vector such that

| (8) |

holds for all .

Proof.

For any fixed , if

then the required inequality always holds since the indicator function is upper bounded by . For the case when

assume that for some . Then

| (9) |

which implies

| (10) |

Above, the first inequality comes from (9) and the second inequality is based on Definition 2. This completes the proof of Lemma 9. ∎

Combining (LABEL:eqn:main:1:final) and Lemma 9, we get

This completes the proof. ∎

A.3.2 Proof of Lemma 7

We now use Lemma 2 to prove Lemma 7. Lemma 2 gives us

| (11) |

Above, the second inequality uses the fact that and for any . Next, we focus on bounding the second term in the R.H.S. of (11). We have

| (12) |

Above, inequality is based on the optimality of , inequality is due to the optimality of , inequality is because and , inequality is based on the optimality of , and the final inequality is due to the fact that is independent of and is zero-mean. Next, we bound each term in the R.H.S. of the above equation respectively.

For the second term, denote WLOG, we assume the upper bound in Lemma 2 holds for a large enough such that . Then, we have

| (13) |

Above, inequality is due to the fact that , and , inequality is based on the identity for , and the last inequality follows from the definition of .

We now control the last two terms of (LABEL:eqn:proof:lemma2:temp2). Since the distribution of is symmetric, the distributions of and are the same. Thus, we have

which gives us

| (14) |

Finally, we leverage the following lemma to complete the proof.

Lemma 10.

We have

A direct substitution of Lemma 10 obtains the desired control on the last two terms of (LABEL:eqn:proof:lemma2:temp2) and completes the proof. It only remains to prove Lemma 10 which we do below.

Proof.

Let , and we have for ,

| (15) |

Above, inequality is based on Jensen’s inequality, inequality follows from the expression of the moment-generating function of a Laplace distribution, and the final inequality follows from the identity for . This completes the proof. ∎

A.3.3 Proof of Lemma 8

Recall that the infeasible leader is given by

| (16) |

Recall that we set . Then, we have

| (17) |

where inequaliy is based on Lemma 3.1 of (Cesa-Bianchi & Lugosi, 2006). Because the learning rate sequence is non-increasing, we have . Thus, we get

| (18) |

Taking an expectation on both sides with respect to the randomness in the algorithm yields

| (19) |

where the first equality follows because the distribution of the Laplace noise is symmetric. The proof is finished by combining the above inequality with Lemma 10. ∎

A.4 Lower Bound for GFTPL

In this part, we introduce the lower bound for GFTPL. We first prove the following lemma.

Lemma 11.

Denote

| (20) |

then we have

| (21) |

Proof.

Considering the definitions of and , we have:

| (22) |

and

| (23) |

The required inequality can be shown by adding up the above two inequalities. ∎

We prove the lower bound result as follows.

Theorem 4.

Assume is -approximable, then Algorithm 1 with , where has the following regret lower bound:

Proof.

Remark

| (31) |

As goes to , both sides go to , which means our strategy competes the best expert in hindsight.

A.5 Extension to Perturbation

In this section, we extend our techniques to perturbation distributions that are exponential with respect to an -norm for any (note that corresponds to the case of the Laplace distribution). Specifically, we consider the probability density function

| (32) |

Recall that we have the following decomposition of regret:

| (33) |

A critical observation is that the proof of Lemma 2 relies on the triangle inequality

which is easily generalized to the -norm:

Following the proof of Lemma 2, we then get

| (34) |

where is now an upper bound on . As before, noting that and for any gives us

| (35) |

It remains to upper bound under the perturbation (as was previously done for the Laplace case). This is done in the following lemma.

Lemma 12.

Under the perturbation, we have

| (36) |

Proof.

Similar to the proof of Lemma 10, we have

| (37) |

where we use the fact that . Now we calculate

| (38) |

where the norm inequality is used. Setting gives us

| (39) |

and thus

| (40) |

∎

We now complete the proof extension. According to the proof of Lemma 5, for term 1 we have

| (41) |

where denotes an upper bound on that will be specified shortly. Above, we plug in to get the third inequality. For term 2, a similar argument to the proof of Lemma 8 gives

| (42) |

Thus, the total regret is upper bounded by

| (43) |

We do a brief comparison between the -perturbation and Laplace perturbation for the case when is a binary matrix. By Lemma 3 because . Then we get that the regret under the perturbation is

while by Theorem 1 the regret bound under the Laplace distribution is

We can see the regret bounds are the same. Since perturbation does not lead to an improvement on the regret bound and the Laplace distribution is easier to sample, we only consider the Laplace distribution in the main paper.

Appendix B Omitted Proof for Section 4

In this section, we provide the omitted proofs for Section 4.

B.1 Proof of Lemma 3

We begin by proving Lemma 3, which shows that any -valued PTM with distinct rows satisfies -approximability. We first state the following lemma which introduces a slightly stronger condition for -approximability.

Lemma 13.

Let be a matrix, and denote as the -th row of . If , , , such that for all rows , then is -approximable.

Proof.

Next, we construct a -approximable based on Lemma 13. Denote as the -th element of . , we set . Since , , we have . On the other hand, ,

| (45) |

For each term in the R.H.S. of the equality, we have

Note that since every two rows of differ by at least one element, there must exist one such that . This completes the proof of the lemma. ∎

Lemma 3 is simple but powerful, and can be applied to a broad variety of combinatorial auction problems. This is detailed next.

B.2 Auction Problems with a Binary

Imagine that a seller wants to sell items (that are either homogeneous or heterogeneous) to bidders. Each bidder has a combinatorial utility function and we use to denote the bidding profile vector of all bidders. In this work we consider truthful auctions, i.e. each bidder is incentivized to report his true valuation in the unique Bayes-Nash equilibrium of the auction. The -th bidder gets an allocation and pays the seller . Therefore, the utility of the bidder is given by .

An auction receives the bidding profiles of all bidders and determines how to allocate the items and how much to charge each bidder. We use to denote the revenue yielded by applying auction to the bidder profile . We consider a repeated auction setting in which the auctioneer faces different bidders on each round. The bidders may be of very heterogeneous types, so we do not make any assumptions on the bidder profile and assume that it can arbitrarily change from round to round. More formally: for each round , the learner chooses an auction while the adversary chooses a bidder profile . Then, the learner gets to know and receives the revenue . The goal of the learner is to compete the revenue earned by the best auction in hindsight. Following Dudík et al. (2020), if the revenue where , then we can scale all rewards by to ensure all rewards are in . After applying Algorithm 2, we scale the reward back to get the regret.

Now we briefly introduce auction problems that admit a binary-valued TPM . By Lemma 1 these are -approximable and by Theorem 1 these admit small-loss bounds.

VCG with bidder-specific reserves

For the standard VCG auction, multiple bidders can be simultaneously served if the allocation maximizes the total social welfare . Then the bidder who wins a set of items would pay the externality he imposes on others

The setting we discuss is slightly modified in the sense that we have a vector with -th component being the reserve value of the -th bidder. Any bidder whose valuation is smaller than will be eliminated. Then, we run the VCG auction for the remaining bidders.

Following Dudík et al. (2020), we discretize reserve prices and use the same therein to get the following small-loss bound:

Theorem 5.

We consider VCG auction with reserves for the single-item -unit setting, and the set of all feasible auctions is denoted by . Denote . Let be an binary matrix, where contains auctions in which each reservation price comes from , and consecutive columns correspond to binary encodings of each bidder, then is implementable. Running Algorithm 2 with such a yields

| (46) |

Proof.

The implementability of follows from Lemma 3.3 of Dudík et al. (2020). Since is binary and every two rows are distinct, by Lemma 3 we know it is -approximable. Using Corollary 1 we have

| (47) |

where we use the facts that , , and since is binary. According to Dudík et al. (2020), the optimal revenue in is upper bounded by that of :

| (48) |

Combining (47) and (48) while setting yield the proposed Theorem. ∎

Envy-free item pricing

Assume there are different items and we use to denote the vector of each item’s price. Bidders come one by one. The -th bidder greedily chooses a bundle which maximizes his utility and pays . Similar as the VCG with bidder-specific reserves, we also assume each price is discretized in the set .

Theorem 6.

We consider envy-free auction for single-minded bidders and heterogeneous items with infinite supply. Denote to be the set of all possible auctions and . Let be an binary matrix, where contains envy-free item auctions in which all prices come from and consecutive columns correspond to binary encodings of each item’s price. Then, is implementable and running Algorithm 2 with this value of yields

| (49) |

Proof.

As noticed in Dudík et al. (2020), we can consider a bidder who has valuation for the bundle of the -th item and valuations 0 for any other bundles. The revenue of auction on such a bidder profile is . Similarly, for the VCG auction with reserves , the revenue of a bidder who has a non-zero valuation would be . Based on the equivalence between envy-free auction and VCG auction with reserves, we can apply Theorem 5 with to get the following bound.

Online welfare maximization for multi-unit items

In this setting, we wish to allocate homogeneous items to bidders such that . Each bidder has a valuation function that maps the number of items he obtains to the utility. We assume is non-decreasing and . The objective is to maximize the total social welfare .

We denote the set of allocations which satisfy as . For the offline version of this problem, Dobzinski & Nisan (2010) propose a -approximation maximal in range (MIR) algorithm, which means maximizing the total social welfare on a set yields at least of the maximal social welfare on the whole . We now explain the composition of the set of allocations . We divide items into bundles of the same size and a possible distinct bundle with size which contains all the remaining items. contains all allocations about these bundles in the sense that all items in a bundle can only be simultaneously allocated. Finally the problem is converted to a knapsack problem and there exists an -approximation algorithm that runs in time.

For the construction of , we make some modifications to the original construction of Dudík et al. (2020) to get a binary-valued PTM. We first define ; note that . We denote to be the elements of in non-decreasing order. Then, we select to be a matrix. For any allocation , , and , we define where . Note that is -implementable because each column corresponds to a valid valuation function. In addition, we have the following result that bounds the regret with respect to the -approximation of the best revenue in hindsight.

Theorem 7.

Proof.

We first show that is -approximable. Since is a binary matrix, by Lemma 3 it suffices to show that does not possess two identical rows. This can be verified by noticing that and are binary encodings of and by applying indicator functions.

Simultaneous second-price auctions

We now consider the utility optimization problem from the point of view of a bidder repeatedly participating in a simultaneous second-price auction (with different bidders each time). In this problem, bidders want to bid for items. Each bidder has a combinatorial valuation function to describe valuations for different bundles and submits a bid vector for all items. If he gets an allocation , his payment profile is given , where is the vector of the second highest bids. In particular, his utility is given by . Each round the bidder chooses a bidder vector and the adversary chooses the second largest bidder’s vector. The goal is to find bidding vectors which compete with the best bidding vector in hindsight.

Following Dudík et al. (2020), we assume that both bids and the valuation function only take values in the discretized set . We also make the no-overbiddding assumption that and denote the set of feasible bidding vectors to be . Let be a matrix. For any , , denote . For a bidding vector and a vector of the second largest bids , we set . Note that this directly implies that is -implementable.

Theorem 8.

The aforementioned is -approximable. Thus, running Algorithm 2 for the simultaneous second-price auction on the discretized set yields

| (54) |

Proof.

Notice that is binary and the rows of come from component-wise threshold functions of the bidding vector. Therefore, for two different bidding vectors the corresponding two rows in would also be different. Thus, we can apply Corollary 1 to get

| (55) |

This completes the proof. ∎

B.3 Level auction

We consider the online level auction problem with single-item, -bidders, -level and -discretization level. We give only a brief review of this problem setting, and we refer the reader to Dudík et al. (2020) for a complete description. In each round of this problem, firstly an auctioneer picks non-decreasing thresholds from a discretized set for each bidder. Let be the collection of the auctioneer’s choices, where is -th the threshold for the -th bidder. Let be all possible auctions. We further make the following assumption on , which corresponds to as considered in (Dudík et al., 2020, Section 3.3).

Assumption 1.

Assume: (a) , there exists at least one pair , such that ; and (b) , , .

After is chosen, the bidders reveal their valuations. We denote the collection of the bidders’ valuations as . As a consequence, the auctioneer obtains a reward , which is calculated based on the following rule.

Definition 4 (The rule for level auction).

For each bidder , define the level index be the maximum such that , with when . For each round , all bidders whose level indexes are would be eliminated. If no bidder left, . Otherwise, the bidder with the highest level index wins the item, and pays the price (i.e., ) equal to the minimum bid that he could have submitted and still won the auction. On the same level, the tie-break rule is in favor of the bidder with the smallest bidding index.

In this framework the set of “experts” is the set of threshold configurations over all bidders. The regret of the auctioneer over iterations is the gap between the revenue generated by the online choice of threshold configurations and the revenue of the best set of thresholds in hindsight, i.e.

B.3.1 Algorithm and regret

We first discuss how to construct an approximable (see Definition 2) and implementable with small . Directly constructing is rather difficult. Thus, we first consider an augmented auction problem with bidders. Let be the set of possible auctions, and be the set of bidder profiles. We construct as follows:

Definition 5.

(a) Distinct auctions (first bidders): , there exists at least one pair , such that ; (b) distinct thresholds (first bidders): , , ; and (c) fixed thresholds for the -th bidder: , , for .

Comparing Assumption 1 and Definition 5, it can be seen that the elements in and have an one-to-one correspondence: , there only exists one , such that , , and vice versa.

In the augmented problem, at each round , firstly the auctioneer chooses from . At the same time, we let the bidders reveal , where is the bidder vector of the original problem, and is a -dimensional vector. Then, the auctioneer obtain a reward , where follows the auction rule in Definition 4. For , denote the related auction in as , and we have the following lemma.

Lemma 14.

We have , and

Proof.

Since the last element of is 0, so the -th bidder will always be at the 0-th level when computing , it will not change the reward at round . We note that, it does not mean the augmentation is not useful: designing a PTM for is much easier than for the original problem. ∎

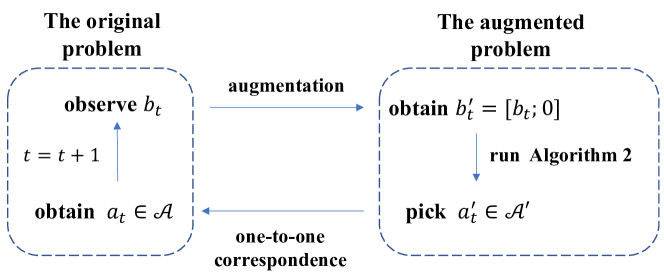

This lemma reveals a duality between the two problems: A low-regret and oracle-efficient algorithm for the augmented problem directly induces a low-regret and oracle-efficient algorithm for the original problem by replacing with its corresponding auction in . To help understanding, we illustrate the relationship between the original problem and the augmented problem in Figure 1.

Next, we propose to construct an approximable matrix for the augmented problem by using bid profiles in . For , , and , let a bidder vector be

| (56) |

where is a -dimension unit vector whose -th element is 1. Note that the construction here is to ensure that only the -th and the -th bidders are likely to win, which greatly simplifies our construction of the PTM. The following lemma illustrates how to construct the PTM and the corresponding vector which satisfy the -approximability condition.

Lemma 15.

Let be the set containing all defined in (56). Let be the matrix implemented from by assigning each to the columns of one-by-one. Then is -approximable.

Proof.

We first prove , then argue that it leads to -approximability.

For , . According to Definition 4, when , all bidders are at the 0-th level, so no bidder wins the item, and . Otherwise, bidder wins the item, and pays . Thus, . For , . Based on the third part of Definition 5, bidder is at the -th level. If , then bidder wins the item, and pays . Otherwise, bidder wins the item, and pays . In sum, we have holds for any .

Next, we prove the approximability based on Lemma 13. WLOG, consider one auction , and let be the row related to , which is a -dimensional vector based on Lemma 15. Our goal is to show that, there exists a vector , such that

Denote as the element of which is related to (see Lemma 15), and we discuss how to set as follows.

First, based on the second part of Definition 5, we have . Thus, combining (56), we know , , , such that , which is in turn equivalent to . In the column corresponding to , , , we have Intuitively, it means that, in this column, only auctions whose -th threshold for the -th bidder equals to yield the highest revenue, and these auctions outperform other auctions by least . Choosing the corresponding as , and setting for , makes . Since we need to ensure that the loss gap between and any other auctions by at least 1, we need to set for any , . It is obvious that and is -approximable according to Lemma 13.

∎

To illustrate the construction of , we provide an example for the case where and and inspect encodings with respect to a single bidder in Table 1.

| Auction | Coding | ||||||||||||

| … | … | … | … | ||||||||||

| … | … | … | … | ||||||||||

| … | … | … | h | … | |||||||||

| … | … | … | h | h | … | ||||||||

| … | … | … | g | h | … | ||||||||

| … | … | … | g | h | h | … | |||||||

| … | … | … | g | g | h | h | … | ||||||

| … | … | … | 0 | g | h | … | |||||||

| … | … | … | 0 | g | h | h | … | ||||||

| … | … | … | 0 | g | g | h | h | … | |||||

| … | … | … | 0 | 0 | g | g | h | h | … | ||||

| … | … | … | … | … | … | … | … | … | … | … | … | … | … |

B.4 Proof of Lemma 4

In this section, we prove Lemma 4, which yields oracle-efficient online learning with a very small output space. Recall that and we denote the adversary’s output space as . We construct as ,

It is straightforward to see that in this way is implementable with complexity 1. On the other hand, for each , we can find , such that . Thus, we can meet -approximability by choosing for action in round , where is a unit vector whose -th dimension is 1 and all other elements are 0. This completes the proof. ∎

B.5 Proof of Lemma 5

In this section, we prove Lemma 5, which yields oracle-efficient online learning for the transductive online classification problem. For this problem, we create a PTM with columns, which is configured as , .

It is clear that is implementable with complexity 1. Next, we prove that approximable. Let be the feature vector observed in round . Then there exists such that . If , then the equation of Definition 2 holds by setting . If , then the equation can be met by picking . This completes the proof of the lemma. It is worth noting that this choice of need not be -admissible for any .

B.6 Negative Implementability

When the oracle only accepts non-negative weights for minimizing the loss (or non-positive weights for maximizing the reward), Algorithms 1 and 2 cannot make use of the oracle directly, since the noise can be negative for Algorithm 1, and positive for Algorithm 2. To handle this issue, we consider two solutions: (a) constructing negative-implementable PTMs (first defined by Dudík et al. (2020)); (b) replacing the distribution of from the Laplace distribution with the (negative) exponential distribution. The former solution can be used in VCG with bidder-specific reserves, envy-free item pricing, problems with small and transductive online classification, while the latter is suitable for the level auction problem and multi-unit online welfare maximization.

B.6.1 Negative implementable PTM

To deal with negative weights, Dudík et al. (2020) introduce the concept of negative implementability:

Definition 6.

A matrix is negatively implementable with complexity if for each there exist a (non-negatively) weighted dataset , with , such that ,

Similar to Theorem 5.11 of Dudík et al. (2020), we have the following theorem.

Theorem 9.

Suppose the oracle can only accept non-negative weights (for minimizing the loss). If is implementable and negative implementable with complexity , then Algorithm 1 can achieve oracle-efficiency with per-round complexity .

For VCG with bidder-specific reserves and envy-free item pricing, (Dudík et al., 2020) show that there exist binary and admissible PTMs that are implementable and negative implementable. Then, based on Lemma 3, this kind of PTMs directly leads to approximable, implementable and negative implementable PTMs, so the oracle-efficiency and the small-loss bound can be achieved for these settings according to the theorem above.

Moreover, we can also find approximable, implementable and negative-implementable PTMs in the other mentioned applications of a) problems with a small output space and b) transductive online classification. For application a) recall that we constructed as . Then, it is straightforward to verify that this matrix can be negatively implemented by setting . For application b), recall that we set , . This PTM can be negatively implemented by simply setting , , which flips all elements of the binary matrix (for 0 to 1 and 1 to 0).

B.6.2 Negative exponential distribution

For the other auctions problems that we consider in this paper (i.e. multi-unit mechanisms and level auctions), the PTMs that we constructed are not negative implementable. However, we show that for these cases, Algorithm 2 with a negative exponential distribution is good enough to achieve the small-loss bound. This adjusted algorithm is summarized in Algorithm 4. Note that Algorithm 4 can directly use the oracle because is non-positive.

For Algorithm 4, we introduce the following theorem. Our key observation is that, in these settings, the approximable vector (i.e., the vector in Definition 2) is always element-wise non-negative, which makes the proof go through when using the negative exponential distribution.

Theorem 10.

Let . Assume is -approximable w.r.t. and implementable with function . Moreover, suppose , , the approximable vector is element-wise non-negative. Then Algorithm 4 is oracle-efficient and achieves the following regret bound:

Proof.

The proof is similar to that of Theorem 1, and here we only provide the sketch of the proof. For the relation between and , similar to (LABEL:eqn:main:1:final), we still have . The difference lies in (7): (corresponds to in Algorithm 4) therein has support on the non-positive orthant, since is non-negative, is always well-defined. Thus, the negative exponential distribution is enough to make the proof go through. Next, for the upper bound of term 1, let be the exponential distribution. Similar to the proof of Lemma 7, we have

where inequality follows from (LABEL:eqn:proof:lemma2:temp2), inequality is because and is non-negative, inequaliry is due the the optimality of , and the final inequality is based on the non-negativity of . Note that there are some extra terms since the distribution is no longer zero-mean. To proceed, the second term can be upper bounded by (13). For the third term, similar to (15), we have ,

| (58) |

where in the first inequality we make use of the moment generating function of the exponential distribution. Thus, we have

and

The proof can be finished by applying (58) and similar techniques as in the proof of Lemma 10 to bound term 2. ∎

Finally, we note that, as shown in the proof of Lemma 15, the approximable vector for the level auction problem is element-wise non-negative (0-1 vector), so Theorem 10 can be directly applied. In the following, we show that this conclusion can also be applied to the online welfare maximization for multi-unit items.

Lemma 16.

For multi-unit online welfare maximization, there exists an approximable vector with non-negative entries .

Proof.

By Lemma 13, it suffices to prove that for any there exists non-negative such that For multi-unit online welfare maximization (as illustrated in Appendix B.2), all items need to be allocated. There do not exist two rows and such that because the corresponding allocations and also preserve this partial order relation, which means for allocation there are unassigned items. We can simply take . Based on the aforementioned observation, there exists at least one index such that and , and thus

∎

Appendix C Proof of Theorem 3

In this section we prove Theorem 3, which is our oracle-efficient “best-of-both-worlds” bound, assuming that the adversary is oblivious. Then, based on the definitions, we know and only depend on the adversary (i.e., the past losses), and is independent of the randomness of the algorithm. This also applies to and .

The regret can be decomposed into two parts:

| (59) |

where

and

In round , there are four possible cases:

-

•

Case 1: , and .

Since after round , the algorithm does not switch, we have based on lines 4-8. On the other hand, let be the last round where the algorithm performs GFTPL, that is, . Then, in round , if we do the switch , thenMoreover, note that and are non-decreasing, and also . Combining with the fact that (since we do not feed losses to GFTPL from round to ), we have

so

If in round we use GFTPL and do not switch, then we have

thus

which implies that

-

•

Case 2: , and .

Since after round , we have , we get based on lines 4-8. On the other hand, We know that , so after round , there are 2 possibilities: 1) the algorithm remains to be FTL. For this case, we havewhere we use the fact that the mixability gap . It yields

2) The algorithm switches from . For this case, we have

so

-

•

Case 3: , and .

Since after round , we switch from , we have . On the other hand, in round , there are 2 cases: 1) After round , we switch the algorithm: . Thus,implying that

2) After round , the algorithm does not switch: . Thus,

so .

-

•

Case 4: , .

For this case, after round , we haveOn the other hand, let be the last round of the algorithm that plays FTL. So in round , there are 2 possible cases: 1) After , we switch from . In this case, we have:

so

2) After round , we still play FTL. Then, we have

so