Setting Interim Deadlines to Persuade††thanks: Thanks to Pavel Kocourek, Yiman Sun, Jan Zápal, Inés Moreno de Barreda, Jeff Ely, Jean Tirole, Péter Esö, Margaret Meyer, Colin Stewart, Francesc Dilmé, Ansgar Walther, Ole Jann, Maxim Ivanov, Egor Starkov, Ludvig Sinander, Maxim Bakhtin, Rastislav Rehák, Vladimír Novák, Arseniy Samsonov, and the audiences at OLIGO 2022, SING17, CMiD2022, EEA-ESEM Congress 2022, and EWMES 2022 for helpful comments.

Abstract

A principal funds a multistage project and retains the right to cut the funding if it stagnates at some point. An agent wants to convince the principal to fund the project as long as possible, and can design the flow of information about the progress of the project in order to persuade the principal. If the project is sufficiently promising ex ante, then the agent commits to providing only the good news that the project is accomplished. If the project is not promising enough ex ante, the agent persuades the principal to start the funding by committing to provide not only good news but also the bad news that a project milestone has not been reached by an interim deadline. I demonstrate that the outlined structure of optimal information disclosure holds irrespective of the agent’s profit share, benefit from the flow of funding, and the common discount rate.

Keywords:

dynamic information design, informational incentives, interim deadline, multistage project.

JEL

Classification Numbers: D82, D83,

G24, 031.

1 Introduction

The development of any innovation requires investment of both time and capital, while the outcome of this investment is inherently stochastic. Usually, the investor, being the principal, retains the option to stop funding the innovative project if at some point it proves unsuccessful. It is widely documented that the agent running the project tends to prefer the principal to postpone the stopping of the funding to enjoy either the extra funds or an additional chance to turn her research idea into a success story.111Agency conflict in which the agent prefers the principal to postpone abandoning the project that the agent is working on is studied in Admati and Pfleiderer, (1994); Gompers, (1995); Bergemann and Hege, (1998, 2005); Cornelli and Yosha, (2003). In such an agent-principal relationship, the agent’s technological expertise and the quality of her innovative idea often allow her to manipulate the principal by designing how and when the outcomes of the research and development process are announced.

Recently, venture capital firms have started to pour billions into startups focused on the development of quantum computers, which are known for their technological complexity and difficulty of construction. The economic viability of quantum computing is questioned by a number of experts; however, the startups promise the investors a completed product in the foreseeable future.222”The Quantum Computing Bubble.” Financial Times, August 25, 2022. For instance, a quantum startup PsiQuantum announced to potential investors that it hopes to develop a commercially-viable quantum computer within five years and managed to raise more than million in 2019.333”Bristol Professor’s Secretive Quantum Computing Start-Up Raises £179m.” The Telegraph, November 16, 2019.

This paper studies the implications of the agent’s control of information during the progress of a research and development project when the agent and the principal disagree about the timing of when to abandon the research idea. I ask: What is the degree of transparency to which an agent should commit before starting to work on an innovative project? In particular, which terms for self-reporting on the progress of the project should a startup propose while discussing the term sheet with a venture capitalist? As I show, depending on the properties of the project, the startup would strategically choose both the timing for the disclosure of updates on the progress of the project and the type of news it discloses - either good or bad.

I study a game between a startup and an investor. The startup controls the information on the progress of the project and has the power to propose the terms for self-reporting on it to the venture capitalist.444I discuss the reasoning behind this assumption in Section 3.2. The startup has an intertemporal commitment power and commits to a dynamic information policy, which can be interpreted as designing the terms of the contract specifying how the information on the progress of the project is disclosed over time as the project unfolds. In return, the investor continuously provides funds and chooses when to stop funding the project.

The project has two stages and evolves stochastically over time toward completion, conditional on continuous investment in it. The completion of each of the stages of project occurs according to a Poisson process. The completion of the first stage serves as a milestone, such as the development of a prototype, while completion of the second stage achieves the project. The investor gets a lump-sum project completion profit if and only if he stops investing after the project is completed and before an exogenous project completion deadline, and the startup prefers the principal to postpone stopping the funding.555I discuss the reasons for the presence of the project completion deadline in Section 3.1.

As the investor receives the reward only after a prolonged period of investment, he initially invests without being able to see if the investment is worthwhile. Hence, it is individually rational for the investor to start investing only if he is sufficiently optimistic regarding the future of the project. An important feature of the setting that I consider is that the information is symmetric at the outset: not only the investor, but also the startup is unable to find out if the project will bring profit to the investor or not - this can be inferred only as time goes on and some evidence is accumulated. The only tool that the startup has for persuading the investor to start investing is the promise of future reports on the progress of the project.

Clearly, the good news about the completion of the project is valuable to the investor as it helps him to stop investing in a timely manner. Further, as evidence regarding the project accumulates over time, failure to pass the milestone in a reasonable time makes the project unlikely to be accomplished in time - and the investor prefers to stop investing after observing such bad news. When designing the information policy, the startup chooses optimally between the provision of these two types of evidence in order to postpone the investor’s stopping decision for as long as possible.

I show that the startup’s choice of information policy depends on the ex ante attractiveness of the project for the investor. The attractiveness is captured by the flow cost-benefit ratio of the project. Thus, a project is relatively more attractive ex ante to the investor when its flow investment cost is lower, its project completion profit is higher, or the Poisson rate, at which completion of one stage of the project occurs, is higher.

When the project is sufficiently attractive ex ante to the investor, promises to provide information only on the completion of the project serve as a sufficiently strong incentive device to motivate the investor to start the funding at the outset. Further, the future news on the completion of the project does not harm the total expected surplus generated by the interaction of the startup and investor, while the future news on the project being poor decreases the surplus that the startup can potentially extract from the investor. Accordingly, the startup commits to providing only the good news, but not the bad news on the project in the future: it discloses the completion of the project and postpones the disclosure in order to ensure the extraction of as much surplus as possible from the investor. In the context of quantum computing, the startup optimally chooses and announces to the venture capitalist the date by which it plans to have a fully developed quantum computer. When the date comes, the startup reports completion if the quantum computer has been completed; if not, the startup reports the completion as soon as it occurs.

The situation changes when the project does not look promising to the investor ex ante. In that case, if the startup commits to disclosing only the completion of the project, the investor will not have the sufficient motivation to start investing in it. Thus, the startup extends the information policy to encompass not only the good news but also the bad. As in the case of the promising project, the startup discloses the project’s completion and does so without any postponement, thereby fully exploiting its preferred incentive tool. In addition, the startup sets a date at which the bad news is released if the milestone of the project has not yet been reached - this date is the interim reporting deadline.

Setting the interim deadline, the startup chooses a deterministic date, which it optimally postpones. As the startup prefers the investor to postpone stopping the funding, it prefers the interim deadline to be at a later expected date. Further, the completion of the stages of project according to a Poisson process makes both the startup and the investor risk-averse with respect to the date of the interim deadline. Thus, the startup prefers to set the interim deadline at a deterministic date and to postpone it as late in time as possible in order to extract all the surplus from the investor. In the context of quantum computing, the startup optimally chooses and announces a fixed date by which it plans to have a prototype of the quantum computer. When the date comes, reporting having the prototype at hand convinces the investor to continue the funding, and reporting not having the prototype leads to termination of the project.

Finally, I demonstrate that the outlined structure of the optimal information disclosure holds for a broad class of preferences of the startup and the investor. I allow for profit-sharing between the startup and the investor, varying degrees of the startup’s benefit from the flow of funding, and exponential discounting, and show that the startup prefers not to set any interim deadlines whenever the project is sufficiently promising to the investor. The future disclosure of the completion of the project promises investor profit in exchange for a prolonged investment, while the disclosure of the stagnation of the project at the interim deadline promises investor only saved costs, as further investment stops. Thus, when the project is attractive, the startup can make the funding and the beneficial experimentation relatively longer by setting no interim deadlines.

2 Related literature

My paper is related to the literature on dynamic information design. The closest paper in this strand of literature is by Ely and Szydlowski, (2020). Similarly to my paper, they study the optimal persuasion of a receiver facing a lump-sum payoff to incur costly effort for a longer time. In my model, as in theirs, the sender is concerned to satisfy the beginning-of-the-game individual rationality constraint of the receiver when choosing the information policy. Further, the “leading on” information policy in Ely and Szydlowski, (2020) has a similar flavor to the “postponed disclosure of completion” information policy in my paper: promises of news on completion of the project serve as an incentive device sufficient to satisfy the receiver’s individual rationality constraint.

However, there are several substantial differences between Ely and Szydlowski, (2020) and my paper. While in their model the state of the world is static and drawn at the beginning of the game, in my model it evolves endogenously over time, given the receiver’s investment. As a result, the initial disclosure used in the “moving goalposts” policy in Ely and Szydlowski, (2020) cannot provide additional incentives for the receiver in my model. The sender in my model uses another incentive device to incentivize the receiver to opt in at the initial period: she commits to an interim deadline at which she discloses that the first stage of the project is not completed.

Another closely related paper is by Orlov et al., (2020). The main similarity to my paper lies in the sender’s incentive to postpone the receiver’s irreversible stopping decision. The sender in their paper prefers to backload the information provision, which is in line with the properties of the optimal information policy in my paper. However, there are a number of substantial differences between our papers. In Orlov et al., (2020), the sender does not have the intertemporal commitment power. Further, the receiver obtains a payoff at each moment of time, and thus the sender does not need to persuade the receiver to opt in at the beginning of the game.

Ely, (2017); Renault et al., (2017); Ball, (2019) also analyze dynamic information design models. However, their papers focus on persuading a receiver who chooses an action and receives a payoff at each moment of time, whereas in my paper the receiver takes an irreversible action and receives a lump-sum project completion payoff. Henry and Ottaviani, (2019) consider a dynamic Bayesian persuasion model in which, similarly to my model, the receiver needs to take an irreversible decision. However, the incentives of the sender and receiver differ from my model: the receiver wants to match the static state of the world and the sender is concerned with both the receiver’s action choice and with the timing of that choice. Basak and Zhou, (2020) study dynamic information design in a regime change game. The optimal information policy in their model resembles the interim deadline policy in my model: at a fixed date, the principal sends the recommendation to attack if the regime is substantially weak by that time.

My paper is also related to the literature on the dynamic provision of incentives for experimentation (Bergemann and Hege,, 1998, 2005; Curello and Sinander,, 2020; Madsen,, 2022). The closest papers in this strand of literature are by Green and Taylor, (2016) and Wolf, (2017). Similarly to my model, both papers consider design of a contract regarding a two-stage project, in which the completion of stages arrives at a Poisson rate. In Green and Taylor, (2016), there is no project completion deadline and the quality of the project is known to be good, while in Wolf, (2017) the quality of the project is uncertain. In contrast to my paper, both papers focus on a canonical moral-hazard problem and give the power to design the terms of the contract to the investor (principal) rather than the startup (agent). In particular, the contract in Green and Taylor, (2016) specifies the terms for the agent’s reporting on the completion of the first stage of the project. Similarly to my model, the optimal reporting takes the form of a deterministic interim deadline: at a principal-chosen date, the agent truthfully reports if she has already completed the first stage, which determines the further funding of the project.666In a broad sense, my paper also relates to the small strand of theoretical literature on dynamic startup-investor and startup-worker relations under information asymmetry (Kaya,, 2020; Ekmekci et al.,, 2020). However, while these papers focus on the signaling of the type of startup, I study the provision of information by the startup on the progress of the project.

3 The model

3.1 Setup

I consider a game between an agent (she, sender) and a principal (he, receiver). Time is continuous and there is a publicly observable deadline , .777The results for the setting without a deadline are easily obtained by considering . They are presented in Appendix E. For each , the principal chooses sequentially to invest in the project or not . The flow cost of the investment is constant and given by . The choice of at some is irreversible and induces the end of the game.888The absence of the principal’s commitment to an investment policy and the irreversibility of the stopping decision capture the venture capitalist’s option to abandon the project, e.g., in the case of its negative net present value.

The assumption that the project needs to be completed in finite time is natural in many economic settings. The main interpretation for is an expected change in market conditions that renders the project unprofitable. In the context of a research and development project, could stand for the date at which the competitor’s innovative product is expected to enter the market, or the date at which the competitor is expected to get a patent on the competing innovation.

The state of the world at time is captured by the number of stages of the project completed by , , and the project has two stages, . The state process begins at the state and, conditional on the continuation of the investment by the principal, it increases at a Poisson rate . Information on the number of stages completed is controlled by the agent. Thus, when making investment decisions, the principal relies on the information provided by the agent.

The project brings the profit if and only if the second stage of the project has been completed by the time of stopping, and a payoff of , otherwise. I assume that all of the profit goes to the principal. This assumption simplifies the exposition without affecting the main results of the paper. I relax this assumption and consider the profit-sharing between the agent and the principal in Section 6.

There is a conflict of interest between the agent and the principal as the agent benefits from using the funds provided by the principal for running the project, possibly diverting them for her benefit. Thus, the agent faces the flow payoff of and wants the principal to postpone his irreversible decision to stop as long as possible.

I study the agent’s choice of information provision to the principal. The agent chooses an information policy to maximize her expected long-run payoff. I assume that the agent has the power to announce and commit to a policy. An information policy is a rule that for each date and for each past history specifies a probability distribution on the set of messages . The history includes all past and current realizations of the process and all past message draws and principal’s action choices.

When choosing an information policy, the agent faces a rich strategy space. First, she can choose if the information on the completion of the first, or second, stage of the project will be disclosed by the policy. Second, she can choose how to disclose the completion of a stage of the project: for instance, to do so immediately or to postpone the disclosure.

The timing of the game is as follows. First, at , the agent publicly commits to an information policy . Second, at each the principal observes the message generated by the information policy and makes her investment decision. The game ends when the principal chooses to stop investing or at , if he keeps investing until . I assume that whenever indifferent about investing or not, the principal chooses to invest, and whenever indifferent about disclosing information or not, the agent chooses not to disclose.

Throughout the paper, I use the following intuitive notational convention: for any two dates at which the principal stops investing, and ,

3.2 Discussion of assumptions

The main interpretation of the considered dynamic information design problem is the contracting between the agent (startup) and the principal (investor) on the terms of reporting on the completion of stages of the project that are not publicly observed. The terms could take the form of a proposed formal reporting schedule or a schedule of meetings with the investor. Non-observability of the stage completions stems from the fact that, while the technology is being developed in the lab, the principal either does not have sufficient expertise to assess the progress or the full access to the lab.

I assume that the principal does not have the power to propose the terms for reporting to the agent and, e.g., make her fully disclose the progress achieved in the lab. The most natural interpretation of such an asymmetry in the bargaining power is the asymmetry in the market for private equity: there are sufficiently many investors willing to invest in a particular technology or sufficiently few startups working on the technology.999In the alternative interpretation of the model, contracting concerns internal corporate research and development and takes place between the leading researcher and the headquarters of a company. The leading researcher’s bargaining power in proposing the terms for disclosure again stems from the market asymmetry: the specialists having the desired level of expertise might be in a short supply. For instance, investors’ interest in quantum computing has grown markedly in recent years, while there are reports of a shortage of human capital in this industry.101010”The Quantum Computing Bubble.” Financial Times, August 25, 2022.111111“Quantum Computing Funding Remains Strong, but Talent Gap Raises Concern”, a report by McKinsey Digital, https://www.mckinsey.com/business-functions/mckinsey-digital/our-insights/quantum-computing-funding-remains-strong-but-talent-gap-raises-concern/. Another example is the communication software industry, which has recently experienced increased investment activity.121212”This Is Insanity: Start-Ups End Year in a Deal Frenzy.” Best Daily Times, December 07, 2020.

As the agent enjoys the power of full control over the information on the progress of the project, she is completely free to offer what is disclosed and when. In particular, the contract between the agent and the principal can specify that the completion of the second stage of the project is disclosed with a delay rather than immediately. The agent who has an advantage in expertise over the principal can rationalize such a condition by saying that before the success is reported to the principal, it is worth re-checking the data, which takes time.

Even though the principal can not dictate to the agent which information and how she should disclose, the principal can potentially hire an external monitor who would visit the lab and prepare an additional report on the progress of the project. In that case, the contract signed between the agent and the principal will account for both free information that the agent promised to provide and additional costly information which the principal obtains with the help of a monitor. In the baseline version of the model, I assume that the principal can not use the help of a monitor. This can be rationalized by the shortage of experts in the field, which makes hiring a monitor prohibitively costly. Alternative interpretation is that the agent restricts the principal’s access to additional information on the progress of the project by stating that a potential information leak would put the technology being developed at risk.131313In particular, this rationale was used to restrict the investors’ access to information on the progress of the project in the case of Theranos, see ”What Red Flags? Elizabeth Holmes Trial Exposes Investors’ Carelessness.” The New York Times, November 04, 2021.

The information policy relies upon the agent’s commitment power, which holds not only within each date but also between the dates. The agent’s commitment within each date follows from prohibitively high legal costs of cooking up the evidence. The agent’s intertemporal commitment stems from the rigidity of terms and form of reporting fixed in the contract that the agent and the principal sign at the outset of the game.

4 No-information and full-information benchmarks

4.1 No-information benchmark

First, I consider the simple case when the information policy is given by : the same message is sent for all histories and all dates . Thus, the agent provides no information regarding the progress of the project. As I demonstrate, in this case the principal starts investing in the project if and only if it is sufficiently promising for the principal from the ex ante perspective and invests until a deterministic interior date.

As no news arrives, the principal bases his decision about when to stop investing on his unconditional belief regarding the completion of the second stage of the project. I denote the unconditional belief that stages of the project were completed by , by , i.e., . The state of the world is fully determined by given by

The principal’s sequential choice of can be restated equivalently as the choice of deterministic stopping time chosen at .141414Note that the dynamic belief system that he faces is deterministic in a sense of being fully specified from perspective. Given the principal’s continuous investment, the probability of completion of the second stage of the project, , increases monotonously over time, making obtaining the payoff more likely. However, postponing the stopping is costly.

To decide on , the principal trades off the flow benefits and flow costs of postponing the stopping decision, while keeping the individual rationality constraint in mind. The flow cost of postponing the stopping for is given by and the flow benefit is given by .151515To observe this, note that the probability of the completing both the first and second stages within a very short time is negligibly small; thus, during some , the principal receives the project completion payoff iff the first stage has already been completed. Thus, the necessary condition for the principal’s stopping at some interior moment of time is given by

| (1) |

Let

the ratio of the flow cost of investment to the gross project payoff normalized using , the rate at which a project stage is completed in expectation. The intuitive interpretation of is the flow cost-benefit ratio of the project. is an inverse measure of how ex ante promising the project is for the principal. (1) is equivalently given by161616Here I WLOG express the flow benefits and flow costs of investing for the principal in different units of measurement.

| (2) |

and presented graphically in Figure 1. As the state process transitions monotonously from to and then to , first increases and after some time starts to decrease. Thus, the principal has two candidate interior stopping times satisfying (2), and . The principal prefers to postpone stopping to , as during the flow benefits are higher than the flow costs.

left plot: postponing stopping increases the chance of getting a project payoff ;

right plot: principal trades off costs and benefits and optimally stops at .

The forward-looking principal can guarantee himself a payoff of if he does not start investing at . Thus, he will choose to start investing at only if his flow gains accumulated up to are larger than his flow losses, and his expected payoff is given by

| (3) |

Geometrically, the integral in (3) represents the difference between the shaded areas in Figure 2 that correspond to the accumulated gains and losses. The principal starts investing at if, given and , the normalized cost-benefit ratio is low enough, so that the shaded area of the accumulated gains is at least as large as that of the accumulated losses. I denote such a cutoff value of by and summarize the principal’s choice without information in Lemma 1.

left plot: ; the project deadline is distant and decision-irrelevant;

right plot: ; the project deadline is close, which leads to lower expected benefits of investing.

In both plots the expected accumulated gains are higher than the losses, so the principal starts to invest at .

Lemma 1.

Assume no information regarding the progress of the project arrives over time. Denote the time at which the principal stops investing by . If , then the principal does not start investing in the project, i.e., . If , then the principal’s choice of stopping time is given by

| (4) |

the closed-form expressions for and are presented in the proof in Appendix C.

4.2 Full-information benchmark

Here, I consider the case in which the information policy is given by : and the message is sent for all such that , . Thus, the principal fully observes the progress of the project at each .171717This benchmark corresponds to equilibrium in the setting, where the principal has the full power to propose the terms of self-reporting to the agent. I characterize the cutoff level of the cost-benefit ratio below which the principal is willing to start investing. Further, I show that the principal chooses to stop when no stages of the project are completed and the project completion deadline is sufficiently close.

At each , the principal uses the information on the number of stages completed to decide either to stop investing or to postpone the stopping. The news on completion of the second stage of the project makes the principal stop immediately, as this way he immediately receives the project payoff and stops incurring the costs of further investment. If only the first stage of the project is completed, the principal faces the following trade-off. The instantaneous probability that the second stage will be completed during is given by , which is constant over the time. Thus, the expected benefit of postponing the stopping for is given by . Meanwhile, the expected cost of postponing the stopping is given by . As a result, if , then the principal who knows that the first stage of the project has already been completed invests until either the completion of the second stage or until the project deadline is reached.

Consider now the case in which the principal knows that the first stage has not yet been completed. The principal’s trade-off with respect to the stopping decision is now more involved. Postponing the stopping for leads to the completion of the first stage of the project with the instantaneous probability . Completion of the first stage of the project at some implies that the principal receives the continuation value of the game, conditional on having the first stage completed. I denote the continuation value of the principal at time under full information and conditional on the completion of first stage of the project by . This is given by181818See the derivation in the proof of Lemma 2 in the Appendix.

| (5) |

The principal’s expected benefit from postponing the stopping for is given by and the cost of postponing the stopping is, as before, given by . The continuation value, , shrinks over time and approaches as the project deadline approaches. This is because the shorter the time left before the project deadline, the less likely it is that the second stage of the project will be completed before . If at some , and given that no stages are completed yet, the expected net benefit of investing reaches , it is optimal for the principal to stop at that .191919If at the expected benefit of investing becomes lower than the cost, then, after , the net expected benefit remains negative. Thus, it is optimal for the principal to stop investing precisely at . I denote this date by and plot it in Figure 3.

As the principal has an incentive to stop at only if he knows that the first stage or the milestone of the project has not been reached, the economic interpretation of is that it is the interim deadline that the principal sets for the project. If the milestone has not been reached by the interim deadline, then it is sufficiently unlikely that the project will be completed before the project deadline . Thus, it is optimal for the principal to “give up” on the project and stop investing at . If the milestone is reached by the interim deadline, then the principal has an incentive not to stop investing until either the second stage is completed or is hit.

Finally, given the plan to stop either at the interim deadline, or at the completion of the second stage of the project, it is individually rational to start investing only if the principal’s expected payoff from the perspective is non-negative. I denote the upper bound for the normalized cost-benefit ratio such that the principal starts investing at by . Intuitively, : whenever the principal is willing to start investing under no information, he is also willing to start under the full information. I summarize the principal’s choice under full information in Lemma 2.

Lemma 2.

Assume that the progress of the project is fully observable at each moment in time. If , where , then the principal does not start investing in the project. If , the principal invests either until the random date at which the second stage of the project is completed, , or until the interim deadline, , at which he stops if the first stage has not yet been completed. Formally, the time at which the principal stops investing is a random variable given by:

where and the expression for is presented in the proof in Appendix C.

Assume now that the agent chooses which information to provide to the principal. As for the principal is not willing to start investing even under full information, there is no way in which the agent can strategically conceal the information to her benefit. In Section 5, I assume and analyze how the agent can strategically provide information on the progress of the project and extract the principal’s surplus.

5 Agent’s choice of information policy

In this Section, I present how the agent’s choice of information policy changes with the ex ante attractiveness of the project, which is captured by the cost-benefit ratio . In Section 5.1, I start with Proposition 1 which summarizes the comparative statics result. In Sections 5.2-5.3, I proceed with the detailed discussion of the economic mechanisms that determine the outlined structure of the optimal information policy. Throughout Section 5, I maintain the following technical assumption:

Assumption 1.

.

For the sake of a clearer exposition, this assumption rules out the case in which is so low that whenever the principal is willing to start investing in the no-information benchmark, he invests until . Relaxing this assumption does not change the the comparative statics result in Proposition 1 qualitatively.202020I discuss the implications of relaxing this assumption in the proof of Proposition 1.

5.1 The structure of optimal information disclosure

Proposition 1.

There exist cost-benefit ratio cutoffs , and , such that, depending on the cost-benefit ratio of the project, the optimal information policy has the following form:

-

1.

when , the agent provides no information and the principal invests until ;

-

2.

when , the agent discloses only the completion of the second stage of the project and does that with the postponement;

-

3.

when , the agent immediately discloses the completion of the second stage of the project whenever it occurs and specifies a deterministic interim deadline, at which it discloses if the first stage is already completed;

-

4.

when , the agent provides no information as the principal’s long-run payoff is non-positive even under full information.

Figure 4 illustrates Proposition 1 and presents the partition of the cost-benefit ratio space based on the corresponding forms of the optimal information policy.

The structure of optimal disclosure presented in Proposition 1 follows the simple and intuitive pattern. The lower is the value of cost-benefit ratio, the higher is ex ante attractiveness of the project to the principal. First, for , the project is so attractive that the principal is willing to keep investing until the project deadline even in the no-information benchmark. Thus, there is no need to disclose any information. For the higher values of , there emerges a room for strategic disclosure, and the higher is the value of (i.e., the lower is the ex ante attractiveness of the project), the more information the agent has to disclose to incentivize the principal. For , the project gets so unattractive that the principal can not strictly benefit from investing even in the full-information benchmark. In this extreme case, the agent chooses not to disclose any information.

The most important part of the result in Proposition 1 demonstrates which additional pieces of information the agent chooses to disclose and when she chooses to discloses them as gets higher and higher. When , the agent discloses only the completion of the second stage of the project and does not promise any information on the completion of the first stage of the project. Further, as increases from to , the agent adjusts the timing of the disclosure: she postpones the disclosure of the second stage completion less and less and discloses immediately for . For , the agent not only discloses the completion of the second stage of the project immediately, but also provides information on the completion of the first stage at the interim deadline that she optimally chooses.

In the subsequent Sections, I provide details on the mechanisms that shape the aforementioned comparative statics results. I omit the trivial case of non-disclosure under and start the discussion from the optimal information policy under .

5.2 Postponed disclosure of project completion

In this Section, I restrict attention to and explain why the optimal information policy has the particular form presented in the Proposition 1: the agent discloses only the completion of the project and does this with the postponement.

5.2.1 Agent’s problem

To characterize the agent’s choice of information policy, I consider an equivalent problem, in which the agent directly chooses the stochastic history-contingent length of investment subject to the principal’s individual rationality constraints that ensure optimality of such action process for the principal. An investment schedule is a random variable defined on the probability space and adapted to the filtration generated by the stochastic process . As I demonstrate in Section 5.2.2, restricting attention to random variables adapted to the natural filtration of is without loss of generality for the agent’s equilibrium expected payoff when .212121In other words, there is no need for external randomization devices to optimally incentivize the principal when .

Informally, an investment schedule is a random variable with support specified by a rule that suggests when to stop investing depending on the history of previous realizations of the number of completed stages .222222The stopping rules from the no-information and full-information benchmarks are given in Lemmas 1 and 2, respectively. Further examples of such rules include “stop 1 minute after the second stage of the project is completed” and “stop at if only the first stage of the project is completed by ”. The agent chooses this rule at . captures the belief about two stages of the project completed by , the random time of stopping in the future, and captures the expected length of investment from perspective.

Given an investment schedule , the long-run payoff of the agent and the principal are given, respectively, by

As an investment schedule is an action recommendation rule, the action recommendations generated by this rule have to be obedient for the principal. In other words, at each date and for each possible history the principal’s actions suggested by have to be optimal for the principal. An object useful for characterizing if an investment schedule generates obedient action recommendations is given by the principal’s continuation value at some interim date promised by the investment schedule . This continuation value depends on the beliefs of the principal.

As the principal does not commit to a policy at , he rationally updates his belief given an investment schedule and assesses the costs and benefits of either further following the investment schedule provided by the agent or deviating from it. The absence of stopping by some date and, thus, the fact that the game continues at serves as a source of inference for the principal. First, he forms a belief regarding the number of completed stages of the project by , conditional on the game still continuing at , . Second, he forms a belief regarding the number of completed stages of the project at the random date of stopping in the future, , .

Given the absence of stopping by , the principal’s expected payoff promised by the schedule is given by . The principal’s expected payoff from stopping at is given by . The principal’s continuation value at given the investment schedule is the difference between these two expected payoffs, I denote it by :

| (6) |

This way of formulating the continuation value is intuitive: if the continuation value gets negative then it is not valuable to continue investing for the principal, and he is better-off stopping immediately rather than following the schedule. The following Lemma shows the necessary and sufficient conditions for an investment schedule to generate obedient action recommendations for the principal.

Lemma 3.

An investment schedule is the principal’s best response to at least one information policy if and only if

| (7) |

where is the principal’s optimal continuation value in the absence of any additional information from the agent starting from the date .

ensures that the principal does not want to stop before the date of stopping suggested by the investment schedule is reached, and ensures that the principal does not want to continue conditional on reaching the date of stopping suggested by the investment schedule. Conditions from Lemma 3 constitute the system of constraints for the agent’s problem.

As the agent chooses an investment schedule to maximize her long-run payoff, the constraint is inactive at optimum.232323Otherwise, the agent can prolong the expected funding by choosing a different . Thus, without loss of generality, I omit this constraint from the agent’s problem, and the problem that the agent solves at is given by

| (8) | ||||

where is the set of stopping times with respect to the natural filtration of . As the principal’s choice to postpone the stopping of funding is costly, it is natural to interpret the system of constraints in (8) as the system of principal’s individual rationality constraints.

The agent’s problem is complex, and thus I solve it in steps. First, I characterize the investment schedule, which solves the relaxed version of (8) with the principal’s individual rationality constraints only for some initial periods. Second, I demonstrate that there exists an investment schedule solving the relaxed agent’s problem and satisfying the full system of the principal’s individual rationality constraints (7). This investment schedule pins down optimal information policy.

5.2.2 Solution to the relaxed agent’s problem

In this Section, I consider the relaxed agent’s problem and discuss its solution. This sheds light on the technical intuition behind the key properties o the optimal information policy. The agent’s relaxed problem for the parametric case of is given by (8) with the principal’s individual rationality constraint only for . The agent’s relaxed problem for the parametric case of is given by (8) with the principal’s individual rationality constraint only for .

Consider the agent’s long-run payoff given an investment schedule, . This can be restated equivalently as follows:

| (9) | ||||

The solution to the agent’s relaxed problem for both considered parametric cases follows a simple idea: the optimal investment schedule ensures that the total surplus is maximal and that the principal’s surplus is minimal. Consider a schedule such that the stopping occurs after the completion of the second stage of the project, unless the project deadline was hit, i.e., the schedule satisfies the condition . Such a schedule leads to

| (10) |

Given a schedule satisfying (10), if is individually rational for the principal at date then the total surplus generated achieves its upper bound and is given by , which depends on the exogenously given project deadline and the profit . However, the stopping only after the second stage completion is not individually rational for the principal at when the cost of funding is sufficiently high, the profit is sufficiently low, or the expected time until a project stage completion is sufficiently high.

Lemma 4 elaborates on the cost-benefit ratio cutoff value : it distinguishes the case in which stopping only after the second stage completion is individually rational at from the case in which it is not. Based on this partition, when , I call the project ex ante promising for the principal.

Lemma 4.

For each there exists , , such that if then an investment schedule in which stopping after happens with probability one is individually rational at (not individually rational at ) for the principal.

For , the schedule is individually rational for the principal at , and it maximizes the total surplus. In addition to choosing , it is optimal for the agent to choose the investment schedule with a higher expected date of stopping the funding to extract all the principal’s surplus subject to his individual rationality constraints. For , the agent chooses such that the principal’s individual rationality constraint at is binding. As a result, , i.e., the principal gets his no-information benchmark payoff given by .

For , as in the no-information benchmark the principal invests until with certainty, the agent chooses the investment schedule as to postpone the start of information provision at least until . Further, the agent chooses with a higher expected date of stopping so that the principal’s individual rationality constraint at is binding. The absence of stopping until at least and the fact that individual rationality constraint binds at taken together imply that , i.e., from perspective, the principal gets her no-information benchmark payoff, which is non-negative and given by (3).

The next Lemma summarizes the necessary conditions for an investment schedule to solve the agent’s relaxed problem when the project is promising. These conditions are shared both by the relaxed problem formulated for the case of and the relaxed problem formulated for the case of . The conditions that are both necessary and sufficient for an investment schedule to solve the agent’s relaxed problem are presented in the Proof of Lemma 5.

Lemma 5.

Assume . If an investment schedule solves agent’s relaxed problem, then

-

1.

with probability one, stopping occurs after ;

-

2.

, where is the principal’s expected payoff in the no-information benchmark, given by (3).

5.2.3 Optimal information policy

In this Section, I show that there exists an information policy that both solves the agent’s relaxed problem and satisfies the full system of the individual rationality constraints. Given this, as Lemma 5 describes the solution to the relaxed problem, it also sheds light on the properties of the optimal information policy for the case of a promising project. These properties have a clear-cut economic interpretation as an investment schedule can be easily interpreted in terms of action recommendations for the principal.

An investment schedule can be without loss of generality implemented using a direct recommendation mechanism - a simple policy which has , where received at date is a recommendation to continue investing at for the principal and received at date is a recommendation to stop investing at .242424The connection between an investment schedule and a direct recommendation mechanism implementing the schedule is simple: whenever, based on the evolution of the state process, suggests stopping the funding, the direct recommendation mechanism sends the message . Keeping this in mind, it is clear from Lemma 5 that the optimal information policy has to satisfy the following conditions. First, whenever the agent recommends the principal to stop, the second stage of the project is already completed. Second, the recommendation to stop is postponed so that the principal’s individual rationality constraint is binding, which manifests in . The first condition presents the key feature of the optimal information policy for the case of promising project: the agent discloses the completion of the second stage of the project, but stays silent regarding the completion of the first stage of the project. The intuition behind the agent’s choice is simple: a recommendation to stop when no stages of the project are completed and the project deadline is close does indeed incentivize the principal; however, it also reduces the total surplus generated that can be extracted via the agent’s control of information. Meanwhile, the recommendation to stop when the two stages of the project are completed incentivizes the principal without reducing the total surplus generated. When , a partially informative policy that discloses only the completion of the second stage provides sufficient incentives to the principal, and thus the agent uses it.252525The “leading on” information policy in Ely and Szydlowski, (2020) is similar: the only information that the policy provides is that the task is already completed and, thus, it is time to stop investing.

I proceed with obtaining an investment schedule that not only satisfies the conditions in Lemma 5 and solves the relaxed problem, but also satisfies the full system of the principal’s individual rationality constraints in Lemma 3. Ensuring both is non-trivial. For instance, consider a mechanism that implements an investment schedule solving the agent’s relaxed problem and assume it recommends to continue for , then at recommends stopping if the second stage is already completed, but recommends to continue at all the subsequent dates . A no stopping recommendation drawn at reveals that the state is either or . Clearly, after sufficient time passes after , the principal would attach a high probability to the second stage already being completed and would potentially be tempted to deviate from the recommendation to continue.262626In other words, drifts down over time and can get negative at some date. However, a direct recommendation mechanism that implements an optimal investment schedule exists. I present it in Proposition 2.

Proposition 2.

Assume . The optimal mechanism does not provide a recommendation to stop during . At , if the second stage of the project is already completed, then the mechanism recommends the principal to stop. If the second stage of the project is not yet completed, then the mechanism recommends the principal to stop at the moment of its completion . Formally,

where is chosen such that , i.e., the respective constraint in the system of principal’s individual rationality constraints is binding.

The recommendation mechanism starting from generates recommendations to stop if the second stage is completed. As the recommendation to stop comes immediately at the completion of the second stage for all , hearing no recommendation to stop reveals that the state is either or . Further, as time goes on, the principal attaches a higher and higher probability to the state being , which ensures obedience to the recommendation to continue at each date. Further, the start of information provision is sufficiently postponed to ensure that the principal’s individual rationality constraint is binding either at or at .

The choice of is driven by extraction of the principal’s surplus and depends on in an intuitive way. First, consider the case , the principal is willing to start investing and invests until in the no-information benchmark. The agent’s optimal choice is to set . Given such an information policy, the principal does not stop at , the date of stopping in the no-information benchmark, and with probability one continues to invest during even though the mechanism provides absolutely no information for all . This is driven by the fact that the expected benefit from stopping at some future date and obtaining the project payoff with certainty compensates the flow losses of investing during .272727Similarly to the “leading on” information policy in Ely and Szydlowski, (2020), the promises of future disclosure of the completion of the project are used as a “carrot” to make the receiver continue investing beyond the point at which he stops in the no-information benchmark. Further, the agent sufficiently postpones to ensure that she extracts the principal’s surplus and the principal gets precisely .

In the case , the principal is not willing to start in the no-information benchmark as his expected payoff from investing is negative. Thus, the agent chooses to guarantee that the principal gets his reservation value and is thus willing to start investing at . The value of is relatively lower as compared to the previous case: as the project is less attractive, to provide the principal sufficient incentives, the agent needs to start the information provision regarding the completion of the project earlier.

Finally, there exist many information policies that both solve the relaxed agent’s problem and satisfy the full system of constraints (7). This constitutes an important advantage for the agent: she can choose an optimal policy that is easier to implement from the real-world perspective, depending on the particular environment. In the optimal mechanism from Proposition 2, the recommendation to stop at some date depends only on the current state of the world . In an alternative delayed disclosure mechanism, the recommendation to stop arrives with a pre-specified delay after the second stage was completed. Thus, the recommendation depends only on the past history and not on the current state of the world. In an optimal delayed disclosure mechanism, the delay becomes smaller as more time passes. I characterize such a mechanism in Appendix D.282828The rich set of optimal direct recommendation mechanisms in my model encompasses both mechanisms in which the information provision depends only on the current state, similarly to the optimal mechanism in Ely and Szydlowski, (2020), and the mechanisms that use delay, similarly to the delayed beep from Ely, (2017).

Recall that, as Lemma 5 suggests, the key idea of the optimal information policy is that the agent postpones the disclosure of the completion of the project to extract more surplus, which makes the principal’s individual rationality constraint bind. The higher the cost-benefit ratio of the project becomes, the higher additional value the agent’s information policy needs to provide to the principal to ensure that his active individual rationality constraint is satisfied. The implication of this for the optimal information policy is presented in Lemma 6.

Lemma 6.

Assume . Given the recommendation mechanism implementing an optimal investment schedule , for a fixed Poisson rate , the expected length of investment decreases in the cost-benefit ratio .

The intuition is that the higher the cost-benefit ratio of the project becomes, the sooner after the second stage of the project is completed the agent recommends the principal to stop. For the cost-benefit ratio as high as , the agent provides the recommendation to stop immediately at the date of completion of the second stage of the project. Further, for , the optimal information policy satisfying the conditions in Lemma 5 ceases to be individually rational for the principal. As I show in the next Section, for , in addition to immediate disclosure of the project completion, the agent provides the information regarding the completion of the first stage of the project.

5.3 Immediate disclosure of completion and an interim deadline

When , the project is not promising for the principal and any investment schedule in which stopping occurs after with probability one violates the principal’s individual rationality constraint. In other words, from the ex ante perspective the future reports disclosing only the completion of the project do not motivate the principal to start investing. Thus, an investment schedule that provides an individually rational expected payoff to the principal should assign a positive probability not only to stopping after the completion of the project, but also to stopping in either state , when no stages of the project are completed, or state , when only the first stage of the project is completed. I present the necessary conditions for an investment schedule to be optimal when the project is not promising in Lemma 7.

Lemma 7.

Assume . If an investment schedule solves agent’s problem, then it satisfies the conditions

-

1.

conditional on no completed stages of the project, stopping of the funding happens with a positive probability;

-

2.

conditional on one completed stage of the project, stopping of the funding happens with probability zero;

-

3.

conditional on two completed stages of the project, stopping of the funding happens immediately (at ) and with probability one.

Stopping when only the first stage of the project is already completed is clearly inefficient. In state , the principal prefers to continue investing until the completion of the second stage and this principal’s incentive to wait is aligned with the agent’s incentive to postpone the stopping. Further, stopping in state does not help overcome the problem of the violated individual rationality constraint under . Meanwhile, assigning a positive probability to stopping when no stages are completed helps to overcome the problem of violated individual rationality constraint, as the principal benefits from stopping at some date when the first stage of the project is not yet completed and the project deadline is sufficiently close. Further, the agent clearly prefers the stopping of funding after the completion of the second stage rather than in state as the former does not harm the total surplus generated. Thus, a schedule that is optimal assigns probability to immediate stopping when the second stage is completed.

Lemma 7 implies that in an investment schedule, optimal for the agent, stopping after the completion of the second stage of the project happens immediately and stopping also happens given that no stages of the project are completed - i.e., at the interim deadline chosen by the agent, which I denote by . Thus, Lemma 7 drastically simplifies the strategy space in the agent’s design problem: it is only left to characterize the optimal interim deadline. At the outset of the game, the agent designs a device that privately randomizes over the interim deadlines . That is, the agent publicly chooses a distribution , then an interim deadline is drawn according to it and privately observed by the agent. Next, the information starts to flow. The action recommendation to stop the funding satisfies the following investment schedule

| (11) |

where the principal knows only the distribution , but not the draw of .

Given that the completion of the second stage of the project is disclosed immediately, stopping at the interim deadline in state leads to a loss of expected further investment flow for the agent, and a potential savings from abandoning a “stagnating” project for the principal. The agent’s payoff can be without loss of generality restated as the expected loss in future investment due to stopping at the interim deadline in state (rather than at ). Given this, the agent’s problem can be expressed as

| (12) |

subject to the system of the principal’s individual rationality constraints, which also have a natural interpretation as the expectation of principal’s savings on the future investment, which discontinues at in state , minus the loss in the project completion profit due to stopping the funding at in state .292929The principal’s long-run payoff is given in (44).

Inspecting the agent’s expected loss in future investment in (12) reveals that if the agent postpones the interim deadline , then two effects arise. First, the probability that stopping at the interim deadline will happen decreases. Second, the expected loss in total surplus due to stopping at the interim deadline rather than at decreases. Thus, the agent’s expected loss in future investment is decreasing in the date of interim deadline and the agent prefers an interim deadline with a later expected date.

Agent’s choice of the interim deadline distribution is affected by the two factors. First, as the expected loss in future investment in (12) is decreasing and convex in the date of the interim deadline, and thus the agent is risk-averse with respect to random interim deadlines. Thus, given some random interim deadline, the agent directly benefits from inducing a mean-preserving contraction. Second, the agent benefits from inducing a mean-preserving contraction indirectly. Inspecting the principal’s long-run payoff for some fixed reveals that the principal is also risk-averse with respect to random interim deadlines. Thus, inducing a mean-preserving contraction makes the principal better-off and relaxes the individual rationality constraint at , hence, allowing the agent to postpone the expected interim deadline further. As a result the optimal for the agent interim deadline takes the form of a deterministic date. In other words, it is optimal for the agent to publicly announce the interim deadline at the outset, so that the principal knows it.

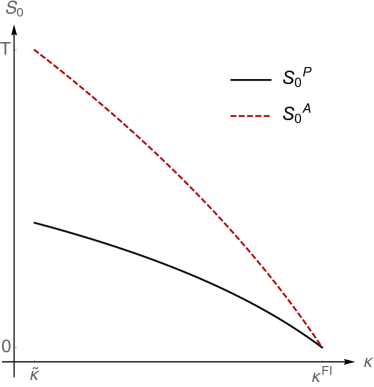

The agent has an incentive to postpone the interim deadline and uses her control of the information environment to postpone the deadline as much as possible so that the principal’s individual rationality constraint at binds. Figure 5 demonstrates the principal’s long-run payoff as a function of the interim deadline, which I denote by . It is maximized at the principal-preferred interim deadline , which was characterized in Lemma 2. The agent-preferred interim deadline yields the principal’s expected payoff of .

The next Proposition summarizes the optimal investment schedule, which can be without loss of generality implemented using a direct recommendation mechanism:

Proposition 3.

Assume . The optimal information policy is given by a direct recommendation mechanism that generates

-

(a)

the recommendation to stop at the moment of completion of the second stage of the project, , and

-

(b)

a conditional recommendation to stop at the publicly announced interim deadline . At , stopping is recommended with certainty if the first stage of the project has not yet been completed.

Formally,

where is chosen so that the principal’s individual rationality constraint at is binding, i.e., .

A stopping recommendation at any date other than the interim deadline fully reveals that project is accomplished. Further, observing a recommendation to stop at the interim deadline, the principal learns that the milestone of the project has not yet been reached and becomes sufficiently pessimistic that the project will be completed by .

A notable feature of the optimal information policy when the project is ex ante unattractive is its uniqueness. The only optimal instrument through which the agent fine tunes the incentive provision to the principal is the choice of interim deadline, and there is a unique optimal way to set the deadline to make the principal’s individual rationality constraint bind.

I proceed by considering the comparative statics of the interim deadline. Both the agent-preferred and the principal-preferred interim deadline, and , respectively, increase in the exogenous deadline . This is because less time pressure relaxes the principal’s individual rationality constraint and allows the agent to postpone the deadline further in order to extract the principal’s surplus.

As the cost-benefit ratio increases up to , the agent-preferred deadline converges to the principal-preferred deadline. An increase in the cost-benefit ratio of the project makes the principal’s individual rationality constraint tighter.303030This is because the increase in makes the principal’s instantaneous benefit from waiting decrease, and the normalized instantaneous cost of waiting becomes higher. As a result, for a higher , in the absence of completion of the first stage, the principal is willing to wait for a shorter time before stopping. Thus, both the interim deadline preferred by the principal and the interim deadline chosen by the agent are lower for a higher . Further, for a higher the agent has to choose an information policy relatively closer to the full-information benchmark to ensure that the individual rationality constraint at is satisfied. Hence, the agent-chosen interim deadline approaches , the interim deadline preferred by the principal. The comparative statics of and with respect to the cost-benefit ratio of the project are presented in Figure 6.

6 General preferences

In this Section, I allow for profit-sharing between the agent and the principal, varying degree of the agent’s benefit from the flow of funds, and exponential discounting, and demonstrate that the optimal information policy still has the same properties as in the baseline model.

First, I assume that the agent and the principal share the project completion profit : the principal gets , while the agent gets , . Thus, now the agent benefits not only from the flow of funds provided by the principal for running the project but also from the share in the profit. The assumption that the agent gets a share in the project completion profit is natural in many situations. In particular, the research documents that the entrepreneurs in innovative startups are up to some extent driven by giving vent to their entrepreneurial mindset and bringing their innovative ideas to life (Gundolf et al.,, 2017). In such a context, a positive profit share of the agent captures that the agent is motivated by the success of the project.

Second, I assume that given a flow cost of incurred by the principal, the agent obtains a flow benefit . can be interpreted as the agent’s marginal benefit from using the funds provided by the principal for funding the project. Alternatively, for the loss of of the amount of the transfer at each date can be interpreted as the transaction costs. Finally, setting for some allows for abstracting from the agent’s motives for diverting the funds and considering the agent motivated only by the success of the project.

Third, I allow for exponential discounting at a rate . Thus, the present value of a profit obtained at a date is given by and the present value of a stream of funding up to date is given by . The following Proposition demonstrates that given the more general preference specification, the structure of the optimal disclosure, present in the baseline model, preserves.

Proposition 4.

-

(a)

When the cost-benefit ratio of the project is low, , the optimal investment schedule satisfies , i.e., the agent recommends the principal to stop only after the completion of the second stage of the project.

-

(b)

When , the optimal investment schedule assigns positive probability both to the stopping in state and state , i.e., the agent not only discloses the completion of the second stage of the project, but also specifies an interim deadline for the completion of the first stage.

Similarly to the baseline model, allowing the principal to stop after the project completion brings profit to the principal and thus leads to a relatively higher total surplus, which the agent can extract. Meanwhile, allowing the principal to stop at the interim deadline does not increase total surplus and serves solely as an expected payoff transfer from the agent to the principal. To see that, note that stopping when the first stage of the project is still incomplete allows the principal to save on the further costs of funding the project when over time the project proves to be “unsuccessful”. This can not be beneficial for the agent as she does not internalize the costs of running the project. Further, stopping at the interim deadline is strictly detrimental for the agent as she strictly prefers the principal to postpone the stopping of funding when no stages of the project are completed.313131The probability of project success and stock of obtained funds are non-decreasing in the date of stopping irrespective of the number of the completed stages of the project.

When the project is sufficiently ex-ante attractive, the agent can motivate the principal to start funding the project without promising to stop the stagnant project at the interim deadline, and this is strictly beneficial for the agent. Thus, when the project is promising, the agent sets no interim deadlines, which in expectation gives her more funds and more experimentation for free.

7 Conclusion

A transparent flow of information is crucial for the successful management of any innovative project. However, the researcher, who controls the information on the progress of the project, often tends to have different motives than the investor. This leads to the question of how a researcher chooses the transparency of the flow of information about the progress of a project in order to manipulate the investor’s funding decisions. I address this question in a dynamic information design model in which the agent commits to providing information to the principal with an incentive to postpone the principal’s irreversible stopping of the funding.

I contribute to the dynamic information design literature by studying the problem of the dynamic provision of information regarding the progress of a multistage project, which evolves endogenously over time and needs to be completed before a deadline. I show that the agent’s choice of which pieces of information to provide and when depends on the project being either ex ante attractive for the principal or not. In the case of a promising project, the agent provides only the good news that the project is completed and postpones the reports. In the case of an unattractive project, to motivate the principal to start funding the project the agent not only reports the completion of the project, but also helps the principal to find out when the project stagnates. To achieve this, the agent announces an interim deadline for the project – a certain date at which she recommends the principal to cut the funding of the project if the milestone of the project has not been reached.

References

- Admati and Pfleiderer, (1994) Admati, A. R. and Pfleiderer, P. (1994). Robust financial contracting and the role of venture capitalists. The Journal of Finance, 49(2):371–402.

- Ball, (2019) Ball, I. (2019). Dynamic information provision: Rewarding the past and guiding the future. Available at SSRN 3103127.

- Basak and Zhou, (2020) Basak, D. and Zhou, Z. (2020). Panics and early warnings. PBCSF-NIFR Research Paper.

- Bergemann and Hege, (1998) Bergemann, D. and Hege, U. (1998). Venture capital financing, moral hazard, and learning. Journal of Banking & Finance, 22(6-8):703–735.

- Bergemann and Hege, (2005) Bergemann, D. and Hege, U. (2005). The financing of innovation: Learning and stopping. RAND Journal of Economics, pages 719–752.

- Cornelli and Yosha, (2003) Cornelli, F. and Yosha, O. (2003). Stage financing and the role of convertible securities. The Review of Economic Studies, 70(1):1–32.

- Curello and Sinander, (2020) Curello, G. and Sinander, L. (2020). Screening for breakthroughs. arXiv preprint arXiv:2011.10090.

- Ekmekci et al., (2020) Ekmekci, M., Gorno, L., Maestri, L., Sun, J., and Wei, D. (2020). Learning from manipulable signals. arXiv preprint arXiv:2007.08762.

- Ely, (2017) Ely, J. C. (2017). Beeps. American Economic Review, 107(1):31–53.

- Ely and Szydlowski, (2020) Ely, J. C. and Szydlowski, M. (2020). Moving the goalposts. Journal of Political Economy, 128(2):468–506.

- Gompers, (1995) Gompers, P. A. (1995). Optimal investment, monitoring, and the staging of venture capital. The Journal of Finance, 50(5):1461–1489.

- Green and Taylor, (2016) Green, B. and Taylor, C. R. (2016). Breakthroughs, deadlines, and self-reported progress: Contracting for multistage projects. American Economic Review, 106(12):3660–99.

- Gundolf et al., (2017) Gundolf, K., Gast, J., and Géraudel, M. (2017). Startups’ innovation behaviour: An investigation into the role of entrepreneurial motivations. International Journal of Innovation Management, 21(07):1750054.

- Henry and Ottaviani, (2019) Henry, E. and Ottaviani, M. (2019). Research and the approval process: The organization of persuasion. American Economic Review, 109(3):911–55.

- Kaya, (2020) Kaya, A. (2020). Paying with information. Available at SSRN 3661779.

- Madsen, (2022) Madsen, E. (2022). Designing deadlines. American Economic Review, 112(3):963–97.

- Orlov et al., (2020) Orlov, D., Skrzypacz, A., and Zryumov, P. (2020). Persuading the principal to wait. Journal of Political Economy, 128(7):2542–2578.

- Renault et al., (2017) Renault, J., Solan, E., and Vieille, N. (2017). Optimal dynamic information provision. Games and Economic Behavior, 104:329–349.

- Wolf, (2017) Wolf, C. (2017). Informative milestones in experimentation. University of Mannheim, Working Paper.

Appendix

A Notational conventions

The state process is given by , defined on the probability space , . Its natural filtration is denoted by . Throughout Appendices B and C, the following notational conventions are used:

1. I denote the random time at which the th stage of the project is completed by . Formally, is a continuously distributed random variable that represents the first hitting time of .

2. Consider some stopping time . Whenever “” stands as a term in an inequality, it stands for a realization of the stopping time and it should be read as “for each and corresponding ”.

Example 1. “” should be read as “, for all ”.

Example 2. “for all ” should be read as “for all , for all ”.

3. The continuation value of the agent at time , given , and conditional on :

4. The total (continuation) surplus at time , given , and conditional on :

5. Shorthand for posterior beliefs:

B The principal’s continuation value

Here I present the alternative formulation of the principal’s continuation value (6). This helps me to study some of its properties for further use in Appendix C. The continuation value of the principal at time and given the investment schedule is given by (6). Postponing the stopping for brings a benefit in the form of project completion payoff iff the second stage of the project is completed within . As follows the Poisson process, the probability of two increments in a very short time is negligibly small. Thus, during some , the principal gets the project completion payoff iff the first stage of the project has already been completed at some earlier time. Thus, postponing the stopping for brings the principal with probability . The second stage is not completed within with the complementary probability of . The principal’s continuation value is thus given by

Differentiating both sides w.r.t. and considering yields

which, after rearranging becomes

| (13) |

C Proofs

Proof of Lemma 1.

The beliefs regarding the number of stages of the project completed by time , , evolve according to the Poisson process. The principal’s unconditional beliefs are given by and for any such that the game still continues,

| (14) | |||||

where and , . The principal’s problem is given by

| (15) |

I start with analyzing the choice of for the interior solution case, . F.O.C. for (15) is given by

| (16) |

or, equivalently, . There are two values satisfying (16): and , . At each the principal receives a net positive payoff flow. Thus, stopping at is not optimal and the only candidate for optimal stopping is .323232 is a local minimum of the objective. Further, one can obtain the closed form expression for the interior stopping time from (16):

| (17) |

where denotes the negative branch of the Lambert function. is well-defined for any .

Thus, the solution to (15) could potentially be , , or . I proceed with a useful lemma.

Lemma 8.

The following is true regarding the principal’s continuation value in the no-information benchmark, : if , then .

Proof.

The principal’s continuation value in the no-information benchmark is given by

| (18) |

Further,

for all and for all . Thus, increases for , decreases for , and , which establishes the result. ∎

Lemma 8 implies that if and the principal chooses to opt in at , then , , i.e., he invests until . This implies that the solution to (15) is either or .

Finally, at the principal chooses to start investing or not. The condition for the principal to start investing at is given by

| (19) |

To specify the set of parameters for which (19) is satisfied, I obtain the cutoff value of given and . Such a parameterization is intuitive: above the cutoff level corresponds to a project with sufficiently high normalized cost-benefit ratio and implies that the principal does not opt in. I denote this cutoff by . This solves (19) holding with equality. Two cases are possible.

Case 1: . This inequality is satisfied when either or Given , (19) holding with equality becomes

Solving it for yields .

Case 2: . This inequality is satisfied when Given , (19) holding with equality becomes

where (recall that )

and

Consequently,

Let . Note that, by definition, . Then , and so

It follows that is nonnegative whenever , which is equivalent to

Finally, putting the two cases together yields

| (20) |

∎

Proof of Lemma 2.

The principal chooses sequentially given the observed realizations of . Whenever the principal observes , he immediately chooses and gets .

Consider the case , i.e., the first stage of the project has already been completed. As follows a Poisson process, in expectation it would take units of time for the second stage to be completed and its completion brings the principal the value of . Thus, the necessary and sufficient condition for the principal to invest at when is given by

Assume that holds and ; thus, the principal chooses to invest at . In that case, the principal invests until . To see this, recall that the only news that the principal can receive given is the completion of the second stage of the project, , which leads to immediate stopping. At each such that , choosing yields an instantaneous expected payoff of , while choosing yields an instantaneous expected payoff of . Thus, suffices for the principal to invest until .