Sparse PCA: a Geometric Approach

Abstract

We consider the problem of maximizing the variance explained from a data matrix using orthogonal sparse principal components that have a support of fixed cardinality. While most existing methods focus on building principal components (PCs) iteratively through deflation, we propose GeoSPCA, a novel algorithm to build all PCs at once while satisfying the orthogonality constraints which brings substantial benefits over deflation. This novel approach is based on the left eigenvalues of the covariance matrix which helps circumvent the non-convexity of the problem by approximating the optimal solution using a binary linear optimization problem that can find the optimal solution. The resulting approximation can be used to tackle different versions of the sparse PCA problem including the case in which the principal components share the same support or have disjoint supports and the Structured Sparse PCA problem. We also propose optimality bounds and illustrate the benefits of GeoSPCA in selected real world problems both in terms of explained variance, sparsity and tractability. Improvements vs. the greedy algorithm, which is often at par with state-of-the-art techniques, reaches up to 24% in terms of variance while solving real world problems with 10,000s of variables and support cardinality of 100s in minutes. We also apply GeoSPCA in a face recognition problem yielding more than 10% improvement vs. other PCA based technique such as structured sparse PCA.

Keywords: Linear Integer Optimization, PCA, Sparse PCA

1 Introduction

PCA (Pearson, 1901) is a popular data analysis technique. It is used in a variety of applications including finance, data imputation, image processing and genome analysis. PCA is of particular interest when the data matrix data has a high dimension . Yet, models resulting from PCA use all the features while sparsity of the PCs can be desired for various benefits. Sparse versions of PCA that use a reduced number of variables to build principal components were proposed to improve interpretability, enhance model’s predictive power or reduce operational costs (such as in finance) and investment costs (such as in spectroscopy). Solving the sparse PCA problem is particularly challenging due to the non-convexity of the problem.

1.1 Background

The optimization community has been studying several versions of sparse PCA problem for decades now. Most of the methods proposed fall into two broad categories. One of the categories aims at approximating the whole covariance matrix using sparse principal components; the loss function is typically of the form where is the covariance matrix and is constructed using problem variables. In this category, sparsity is generated using thresholding and/or regularization either directly in the objective function or in the constraints. Thresholding has been used as early as in (Jeffers, 1967). Limits of thresholding have also been documented (Cadima and Jolliffe, 1995), in particular key variables could be zeroed and highly correlated variables chosen together which ultimately could lead to inaccurate interpretations. The first algorithm to use penalization is SCOTLASS (Jolliffe et al., 2003). It was introduced then as a method for preserving the orthogonality constraints while sparsity was induced by constraints but, using this technique, the number of features used in the resulting sparse model is capped by and the method is not tractable for . Larger problems could be then tackled by the introduction of the LASSO method to generate PCs by adopting an penalized regression approach in the generation of the PCs (Zou et al., 2006) which, on one hand, allowed the number of variables used in the model to exceed but, on the other hand, sacrificed the orthogonality of the PCs and provided no guarantee on the optimality of the solution. (Shen and Huang, 2008; Witten et al., 2009) introduced iterative thresholding methods to tackle the sparse PCA problem building PCs iteratively. Other breakthroughs were achieved and successfully implemented including the GPower method using penalty which preserves orthogonality (Journee et al., 2008), scales for in 10,000s and in 1,000s and outperforms LASSO-based regression approach and greedy algorithm in terms of quality of solution and computation speed. Subsequent works using penalization to induce sparsity adopting optimization over Stiefel manifolds (Huang and Wei, 2019; Tan et al., 2021; Chen et al., 2020) and the Procrustes reformulation (Benidis et al., 2016) showed that solution quality and computation time could be further improved considering the same size of problems while preserving orthogonality. The state of the art in this category of works can then handle large instances in competitive time, delivers orthogonality of the PCs and can furthermore be adapted to variations of the sparse PCA problem including the structured sparse PCA (Jenatton et al., 2009; Li et al., 2017). Yet, the community is still making sizeable efforts to improve the variance captured. Indeed, most of these approaches come with no guarantee of the optimality of the solution and the control of the number of variables cannot be chosen with precision. Recent efforts in (Erichson et al., 2020) introduce penalization while keeping a loss function of the form which could theoretically achieve sparser principal components and achieve a tighter control over the number of nonzero variables (numerical tests in this paper focusing essentially on penalization). The number of variables used in the first category of works is often too high to enable interpretability or to be practical in several intended uses of sparse PCA.

The second category of approaches aims at having a strict control on the number of variables used. For a given number of variables, the objective sought is to maximize the variance captured using one or several principal components that have a support of cardinal . Rather than generating sparsity through penalization, this family of approaches aims at finding optimal or near optimal solutions for a defined number of features to be used. Initial work involved a greedy strategy as well as a branch-and-bound approach (Moghaddam et al., 2006). Optimal solutions were sought through semidefinite optimization modeling (SDO) (d’Aspremont et al., 2004). Further developments of this technique enabled tackling relatively big problems with optimality certificates (d’Aspremont et al., 2008). GPower technique was also adapted to propose a truncation approach in (Yuan and Zhang, 2011). Later, a novel technique that performs particularly well when the the decay of eigenvalue of the data matrix was proposed (Papailiopoulos et al., 2013). Although each sparse PC constructed is optimal, the set of PCs are constructed iteratively using deflation techniques of the data matrix, thus there is no guarantee of the overall optimality and orthogonality is sacrificed. Another track of work develops branch-and-bound approaches to construct optimal solutions while controlling . This enabled solving problems for in the 1,000s and but the PCs are then constructed by iteratively deflating (Berk and Bertsimas, 2019). More recent work combines branch-and-bound and SDO formulation to solve problems with in 10,000s and to near optimality in hours (Bertsimas et al., 2022; Li and Xie, 2020). Since the PCs are obtained by deflating , orthogonality is sacrificed. One variation of the sparse PCA tackled by this category of approaches includes additional constraints aiming at building sparse PCs with disjoint supports (Asteris et al., 2015). More recently, (Del Pia, 2022) proves that finding orthogonal principal components sharing the same support and maximizing the variance captured is a polynomial problem when the rank of the covariance matrix is fixed. The result is further extended to a special case of the disjoint supports sparse PCA problem when the cardinality of the disjoint supports is identical. This paper is theoretical and does not provide any numerical results so there is no indication regarding how the suggested approach would perform from a practical point of view. (Dey et al., 2022) also recently proposed the first algorithm that builds simultaneously orthogonal sparse principal components sharing the same support while upper-bounding the number of nonzero rows. The methods tackles problems for as high as 2000 in less than two hours and upper and lower bounds are provided for the optimal solution.

The two broad categories of approaches presented do not span all of the approaches that the machine learning community designed. Indeed, remarkable approaches aimed for instance at approximating the subspace generated by the principal components of the classic PCA algorithm were developed. (Johnstone and Lu, 2009) focuses on the principal components that correspond to the largest eigenvalues of the covariance matrix and generates sparsity through thresholding. (Ma, 2013) further improves the results achieved by this approach by proposing a novel iterative thresholding technique achieving tighter loss than comparable techniques.

1.2 Motivations and Contributions

As mentioned in the background section, one of the main approaches to construct sparse principal components that the machine learning community adopted is to add a constraint upper-bounding the number of nonzero variables. This approach is particularly relevant when the desired number of nonzero variables is low compared to the dimension of the data points. When upper-bounding the number of nonzero variables by an integer when is significantly lower, the maximization of the variance captured is more relevant than the minimization of the error where is the data matrix and is the constructed sparse matrix as the error is too large. Considering this approach, the machine learning community focused on constructing the PCs iteratively which does not guarantee the optimality of the overall solution (and actually yields sub-optimal solutions). Only very recent works (Del Pia, 2022; Dey et al., 2022) tackle the problem of building multiple orthogonal principal components at once to guarantee optimality when PCs share a common support (Del Pia, 2022; Dey et al., 2022) or when PCs have disjoint supports (Del Pia, 2022). Our main motivation is to bring a new method that upper-bounds the number of nonzero variables, builds multiple orthogonal principal components at once and scales further than existing methods when PCs share the same support or have block-disjoint supports. Furthermore, we also aim at providing guarantees on the quality of the solution found.

In the present paper, we propose a novel approach to sparse PCA that considers the left eigenvectors of (it is worth noting that all works on sparse PCA focus on the right eigenvectors). We derive then a geometrical interpretation of the resulting problem. This interpretation leads to a binary linear formulation that aims at approximating the original problem. This geometrical approach is versatile and can be adapted to several versions of sparse PCA problem. We introduce two formulations; one for a version in which all PCs share the same support and another version in which groups of PCs use disjoint supports (a generalization of the version imposing to PCs to have disjoint supports). Building on the versatility of the method, we also propose a formulation for the structured sparse PCA problem. We provide optimality gap bounds and test the proposed method on real world data sets. The geometrical approach we propose solves problem for in 10,000s and in 100s while preserving the orthogonality and controlling in minutes.

As we mentioned earlier, upper-bounding the number of nonzero variables is a desirable feature for practitioners whether the true principal components share the same support or not. While the method we propose could be used in the general case, practitioners might me even more interested in this technique when the data studied follows particular structures (eg. hyperspectral imagery and spectroscopy when the focus is on particular variables (Fu et al., 2017; Bertsimas et al., 2020), computer vision (Jenatton et al., 2009) or matching (Benidis et al., 2016) among others).

We summarize our contributions in this paper below:

-

•

We introduce a new approach to the sparse PCA problem based on left eigenvectors that leads to a geometrical interpretation of sparse PCA. We approximate the sparse PCA problem using binary linear optimization (BLO) and the introduction of cuts that improve the solution.

-

•

We prove that the optimal solution can be found using the approximation proposed in a finite number of steps and provide a theoretical optimality gap to the solution generated by the method we propose.

-

•

We propose formulations and algorithms (i) for sparse PCA problem in which all PCs share the same support, (ii) for a generalization of the version of PCA requiring that the PCs have disjoint support, and (iii) for the structured sparse PCA problem.

-

•

We test the proposed method on publicly available real world data sets and compare its performance vs. existing methods and show that the geometrical approach produces solutions of higher quality than alternative state-of-the-art methods.

The structure of the paper is as follows. In Section 2, we first study the sparse PCA problem when all principal components share the same support. We introduce the geometrical approach and offer interpretations and provide formulations, optimality gap bounds and related algorithm. In Section 3, we extend the geometric approach to the case in which the principal components have disjoint supports and to the structured sparse PCA problem. In Section 4, we compare GeoSPCA to other state-of-the-art sparse PCA techniques and we finally conclude in Section 5.

1.3 Notations and Definitions

In the remainder of this paper, we define a centered data matrix with data points and features. We refer to the number of features used to build a sparse PCA model by . All matrices and vectors in bold characters.

We note , the transpose of matrix . Consider the SVD decomposition of a real matrix , . We call the columns of (resp. ) the left (resp. right) eigenvectors of . Consider a non-negative integer, we note . We denote the column of a matrix . The scalar is the component of vector . The matrix is the diagonal matrix with a diagonal equal to the vector . Consider , we note the vector of such that if and , otherwise. If is a finite set, we note its cardinality. Consider a matrix and a vector , we note the matrix we obtain by suppressing all columns of such that . is the Frobenius norm. designates the number of nonzero coefficients of a vector or the number of nonzero rows of a matrix. For a non-negative integer, is the identity matrix of size . Given , we note any element of for a given non-negative integer and , and . It is easy to verify that (See Figure 1). We define finally the vector as the vector .

2 Sparse PCA problem with Principal components sharing the same support

In this section, we address the sparse PCA problem in which all the principal components share the same support. We first transform the problem to a left eigenvectors problem and derive a geometric interpretation of the problem. We then introduce a binary linear optimization approximation of the sparse PCA problem. We finally propose an algorithm that solves the approximation and that can find the optimal solution to the original problem.

2.1 An exact formulation using the left eigenvectors perspective

We consider the problem of maximizing the variance explained by a given number of sparse principal components that share the same support of cardinal less than or equal to . We write the problem as:

| (1) | ||||

where is the number of nonzero rows of . The principal components formed by the columns of share then the same support of cardinality at most . We transform the problem to let the left eigenvectors appear:

Proposition 1

Problem (1) is equivalent to:

| (2) | ||||

Proof We introduce a variable and consider that if and , otherwise. When , and , we have where and is the number of nonzero rows of . If the principal components are represented by the columns of , then ensures that the principal components are normalized and orthogonal. We note that if, in addition, we have , we have , but since , it means that if . Hence, the combination of and ensures that . Problem (1) can then be rewritten:

| (3) | ||||

The constraints can be dropped (the proof is detailed in Proposition 2). Consider the matrix obtained when the columns are removed from when . Problem (3) can then be written considering inner and outer problems as follows:

The inner problem is a standard PCA problem for the data matrix . We can now write the equivalent problem considering the left eigenvectors of :

By expanding the trace, we have then:

which is equivalent to:

as .

is the sum of the norms of the projections of in the subspace generated by the columns of . In other words, the problem is to find columns of that maximize the sum of the norms of their projections in a subspace of of dimension .

Proposition 2

Problem is equivalent to:

Proof

Consider an SVD decomposition of with , and such that is a diagonal matrix and . Consider now such that if and the columns of appear in in the indices for which in the same order as in . We can easily verify that which shows that and have the same nonzero eigenvalues and the same left eigenvectors.

2.2 Geometric approximation formulation

Although the problem has been transformed, the two main issues of the problem are still present; the objective function is not concave and we still need to deal with the non-convex orthogonality constraints. In this subsection, our objective is to provide a binary linear problem that approximates Problem (2). We first propose a linear approximation of the objective function and outline the geometric intuition supporting this approximation. We then replace the non-convex constraints by a set of linear constraints yielding the same optimal solutions. The approximation introduces a new parameter (noted ). We also show that optimal solutions of Problem (2) are also optimal solutions for the approximation if is chosen appropriately.

We start by addressing the non-concavity of the objective function. The underlying hypothesis when using PCA to tackle a data problem is that the data matrix can be written where is a matrix of rank and is a low-norm matrix representing noise, or second order phenomena or other perturbations that are to be ignored by PCA modelling. is found by projecting according to a set of orthonormal vectors , the columns of , . Since , we consider that .

When considering Problem , the objective function is the sum of the norms of the projections of columns of on the subspace generated by the columns of . Since the inner problem of problem is the standard PCA problem, and using the approximation we just mentioned, we can approximate the objective function as the sum of the norms of columns of instead of the sum of the norms of their projections whenever is small enough. We introduce then the parameter that bounds that norm of the difference of and its projection . This can be expressed by a constraint for a given :

that could be rewritten as follows:

| (5) |

We now consider the constraints . These constraints are difficult to work with as they are non-convex. Yet, does not appear in the objective function considered now. For a given , if we can find a sufficient condition for the existence of a that satisfies , then is feasible. Consider now . is a solution of the standard PCA problem for matrix .

Proposition 3

Problem is equivalent to the following formulation for any :

| (6) | ||||

Proof

The objective function of the inner problem of depends only on the existence of such that and . If such exists, the objective function is equal to . If verifies , then is a feasible solution of the inner problem of . Conversely, if the inner problem of is feasible then by definition .

We replace finally the constraints by eliminating the vectors for which we have . Consider , and such that if and otherwise. If , is not feasible and could be cut using the following inequality:

Hence, we derive the following approximate formulation for the sparse PCA problem with PCs sharing a common support:

| (7) | ||||

We note the value of the objective function of problem evaluated for an arbitrarily chosen optimal solution of problem for a chosen (if problem has several solutions, we choose one that minimizes ) and let us prove that an optimal solution to problem can be found using formulation (7):

Theorem 4

Consider an optimal solution of problem . There exists such that for any , optimal solutions of problem are optimal solutions of problem .

Proof By contradiction, consider and suppose that there exists such that is an optimal solution of problem and is not an optimal solution for problem which implies according to problem . Since is an optimal solution of problem and is feasible in (7) because , we have , which yields then:

i.e.

which means that is not feasible as it violates the constraint .

Since takes discrete and finite values as the number of is finite, we can choose such that the set of feasible solutions of problem remains the same as if to ensure that remains an optimal solution of problem . For example, we can consider and choose with .

Beyond the theoretical value of Theorem 4 as it shows that with an adequate , an optimal solution could be found. More practically, this theorem is also used in the design of a practical algorithm in Section 2.4 (Algorithm 2) can approach and find the optimal solution in a finite number of steps.

Although the objective function and the constraints of problem are linear, there are still potentially an exponential number of constraints (the number of subsets of [p] is ) which can hinder the tractability of the problem and we still need to assess the quality of the solution found by solving problem relative to the optimal solution of . We start by providing a theoretical bound that partially addresses the first question and further address practical and empirical aspects in Section 3. We also address the large number of constraints by proposing a simple separation procedure to generate useful constraints without including all the constraints in the problem.

Finally we note that the approximation is considered only to provide the reader with an intuition behind the approximation. is not a required assumption in any of the results of this paper.

2.3 Worst case upper bound

Before introducing an algorithm to solve Problem (7), we provide tight worst case upper bounds for the difference between the optimal value of Problem (2) and the value of the objective function of Problem (2) evaluated at an optimal solution of the approximation Problem (7). After showing the role plays in these bounds, we derive a straightforward way to derive an upper bound without knowing . The relationship between the worst case upper bound and furthermore enables us to design an algorithm that approaches an optimal solution of the original Problem (2). Furthermore, this algorithm finds the optimal solution to the original Problem (2) in a finite number of iterations.

Proposition 5

Consider an optimal solution of problem . Let be an optimal solution of problem for , then ; meaning that the difference between the optimal value of problem ,, and the value of the objective function of problem evaluated at , is bounded by . Furthermore, this bound is tight.

Proof Note the optimal value of problem , a solution to problem and s.t. , the value of the objective function of problem evaluated at . We have:

and

hence:

As , is feasible in Problem so

then .

We show now that the bound is tight. We build an example for . Consider and

and consider and . The columns of are illustrated in Figure 2. Let us first note that the value of the objective function of the optimal solution of problem is 2 and is given by taking . If , then is feasible in Problem and the optimal solution is given by and . If , then it is impossible to have ; the optimal solution is then and the value of the objective function of problem when is equal to as . Since can be taken as close as desired to , then the bound is tight.

This bound expresses the fact that the approximation is as good as the hypothesis that the matrix composed of the columns of the optimal support can be approximated with a matrix of rank . Even if is not known, we show in the implementation of Algorithm 2 that this bound is practical. We prove first that a bound can be found a priori by solving the classic PCA problem. We need first the following result:

Proposition 6

Consider that with and . Let be an optimal solution of problem . We have:

Furthermore, is feasible when in problem .

Proof We have:

When , since

then

and hence is feasible in Problem .

Corollary 7

Consider (i.e., is a solution to the classical PCA problem). We denote and the set of the indices of columns of with the highest norm. We have:

can be easily computed using classic PCA. Although is not known, the norm of the columns of can be computed and so is . Using the same notations as in Proposition 2 and Corollary 4, we have:

Corollary 8

The difference between the optimal value of problem , , and the value of the objective function of problem evaluated at , is bounded by .

2.4 Algorithm

We propose two algorithms. Algorithm 1 solves Problem (7) for a given parameter while Algorithm 2 starts without any knowledge on and then approaches the optimal solution of Problem (2) by exploring several values of while also updating the worst case upper bound.

We propose an implementation based on cut generation (Algorithm 1). We initially solve the problem without any of the constraints , and then iteratively add these constraints. If at iteration , the optimal solution found violates , then we add the constraint such that is the set of indices such that . Note that the computation of is inexpensive as it involves only the generation of an SVD decomposition of the matrix which is of size which can in done in .

While Algorithm 1 terminates as is finite and the while loop suppresses at least one element of , the number of iterations is still potentially exponential. However, in practice the algorithm is relatively fast and solves large real world problems in minutes as illustrated in Section 4.

We also use the proof of Theorem 4 to refine the search for . We have:

Lemma 9

We assume that Problem has a unique optimal solution. The function returning the value of the objective function of problem evaluated at the optimal value of problem depending on is a piece wise constant function.

Proof

We note denote the function as . For a value , returns the set of supports such that The cardinality of is finite as is finite. The cardinality of is increasing with respect to and is constant when is which proves the lemma.

Using this lemma, we can derive a method to efficiently select . Indeed, consider that we solve problem for a value and note , an optimal solution. It is easy to see that is constant for . We can then start with a large value of and iteratively update by computing where is a solution obtained and then input a new value for small enough as is constant on .

This also provides means to obtain tighter optimality gaps. Indeed, using Proposition 3 and starting with , which is large enough, we can store and update , the value of that achieves the largest value and since we have started with values of larger than the corresponding to the optimal solution of problem , then according to Proposition 3, the difference between the optimal solution of problem and is capped by .

We report then the following algorithm to solve or approximate problem and obtain .

Proposition 10

Algorithm 2 converges and for small enough, Algorithm 2 finds an optimal solution to (2) in a finite number of steps for large enough.

Proof We first note that Algorithm 2 converges as increases from an iteration to another by construction and is upper-bounded by .

We consider now an optimal solution of (2), and let . Suppose that is not empty. Consider any such that . Considering Algorithm 2, we know that . If then Algorithm 2 finds an optimal solution at the first iteration as is an optimal solution to problem (2) according to Theorem 4. Consider now such that such that . We show now that or . If , then is feasible in (7) and . We also have by construction of , . Since , we have and since is the optimal value of (2), then meaning that Algorithm 2 finds an optimal solution .

If , then according to Theorem 4. We conclude that if then .

Hence, since by construction, Algorithm 2 finds an optimal solution in less than steps.

If , then an optimal solution of (7) is also an optimal solution to (2) as all are equal and the Algorithm 2 finds the optimal solution at the first iteration.

We note that the number of values takes is lower than the number of feasible solution, which contributes to simplifying the problem. The condition in the while loop is a stopping criteria. It stops the search of a solution if no improvement is achieved after attempts after is updated. Of course, other stopping criteria could be considered in this algorithm.

We finally provide an additional upper-bound for the optimal solution of (2) that leverages on the history of search of Algorithm 2.

Proposition 11

Consider that Algorithm 2 generated cuts and note an optimal solution of (7) using the cuts generated. If , then is an optimal solution for (2). Otherwise, the optimal solution of (2) is upper-bounded by .

Proof We note a solution of (7) after generating cuts using Algorithm 2, the value taken by the objective function of (2) at and , the value objective function of (7) at the same point . We first note that is a decreasing function. Indeed, the optimal value of (7) can only decrease when we add constraints. We also note that for any , .

If , then for any , as is decreasing; and since , then so is optimal.

Otherwise, by construction, for any . We also have for any , ans is decreasing and we also have so so the optimal solution of (2) is indeed upper-bounded by .

2.5 Complexity assessment

There are two aspects that need to be considered to assess the theoretical efficiency of the proposed algorithms; the number of cuts generated) and the computational cost of each iteration.

Let us start by the number of cuts. As mentioned earlier, the number of cuts is potentially exponential. We provide here a theoretical example in which the number of cuts generated is exponential whatever the dimension chosen. We choose and and consider and . Consider the matrix such that , , for , and for , and otherwise. It is easy to verify that the norm of any column is strictly greater than 1 for and the norm of the two first columns is equal to 1. Is is also easy to verify that pair of columns , where is a sub-matrix of formed by its and columns and with . It is then easy to verify that the optimal solution of (2) is achieved with and for . We set now , then the only feasible solution for (7) is . Since for any , and the cuts generated cut one binary point at a time, then Algorithm 1 will have to cut all the binary points except the optimal solution before it reaches the optimal solution.

We examine now the cost of each iteration. Each iteration involves two steps (i) solving a BLO problem and (ii) a running a separation algorithm. As mentioned earlier, the separation algorithm consists of a classic PCA problem of dimension which can be solved by using an SVD decomposition in . Solving the BLO problem in Algorithm 1 is not trivial and the constraints matrix defines a polyhedron that has non-integer vertices in the general case. Yet, we can show that the BLO problem can be replaced by a much simpler algorithm. Indeed, at the first iteration of Algorithm 1 (no cut generated yet), the solution is obtained by choosing the columns of that have the largest norms. Suppose now that we are at iteration . If the separation algorithm finds a violated cut at iteration , the new cut generated cuts exactly one binary point which is the optimal solution found of iteration . This means that a solution of the BLO at iteration is defined by a set of vectors with the largest sum of norms that are different from the solutions of iterations . Since the BLO chooses the sets with largest sums of norms, a solution for the BLO of iteration has a sum of norms lower or equal to the sum of the binary solutions that were cut. Finding such solution could then be performed through tree search with a cost of as this process is then reduced finding the columns with the largest norms, then the set with the second largest sum of norms,…, then the set with the largest sum of norms. The actual computational cost of each iteration is then .

Since the cost of each iteration is modest, theoretically the potential issue would be with the number of iteration that could be theoretically exponential. Yet, in practice, high quality solutions are found in a tractable fashion for fairly large instances as we show in the following section using real-life data.

In addition, it is worth noting that our method does not require computing the covariance matrix . Since we are interested in particular in instances in which is large (and in general high dimension setting we have ), this results in dramatic reduction in memory requirements in addition to reductions in computation time.

Finally, although solving the BLO is computationally costly in theory, we have found that it is actually fast in practice when it comes to the BLO proposed in Algorithm 1. In Section 4, we illustrate how Algorithm 2 performs vs. other methods. We keep using the BLO because (i) solving the BLO using commercial solvers is so fast that Algorithm 2 already scales more than any other known method that tackles the problem considered in this section, (ii) the BLO could hold the opportunity to add tighter cuts (for potential future research) and (iii) too often, solving is deemed computationally costly while in practice it can be competitive, so we decided to illustrate the fact that considering BLO could be a valid approach to tackle high dimension problems.

3 Extension to the Disjoint Support Block Sparse PCA and the Structured Sparse PCA problems

We consider now the problem of maximizing the variance generated by sets of PCs such that the PCs of a same set share the same support while the supports of PCs of different sets are disjoint. We call this problem the Disjoint Support Block Sparse PCA (DSB SPCA) problem.

3.1 DSB SPCA Formulation

We note the desired cardinality of supports for each set and the number of PCs in each set. Following the same method to formulate problem , the problem can be written as follows:

| (8) | ||||

We first note that when , then formulation matches the sparse PCA problem with disjoint support as formulated in (Bertsimas et al., 2022). Following the same steps to construct problem , we obtain the following approximation for :

| (9) | ||||

3.2 Worst Case Scenario Upper Bound

We generalize Proposition 2 as follows:

Proposition 12

Let be an optimal solution of Problem (8). We note

Consider an optimal solution of Problem (9) for , then the difference between the optimal value of ,

and the value of the objective function of evaluated at ,

is bounded by . Furthermore, this bound is tight.

Proof Let be the optimal value of Problem , be a solution to Problem and

be the value of the objective function of Problem (8) evaluated at . We have

and

Hence,

is feasible in Problem so , then .

Proposition 3 and corollaries 4 and 5 are still applicable in the case of disjoint block supports and the proofs are almost identical.

3.3 Algorithm

Algorithm 1 can be easily adapted for the case of groups of PCs having disjoint supports

3.4 Structured Sparse PCA

In some applications of sparse PCA, additional properties to sparsity are needed either to further improve interpretability or to enhance performances in subsequent classification or regression. One of the notable applications of Structured Sparse PCA is image recognition in which the fact that the features selected need to be adjacent and/or form a particular 2D pattern (Jenatton et al., 2009). Another notable similar application is protein complex dynamics in which practitioners require that the 3D distance between the features to be limited and more recently, more abstract structures have been considered in genomics based on the interaction among different genes (Li et al., 2017).

The approximation can be adapted to virtually any pattern that can be defined by linear constraints. We propose a general formulation for the approximation Structured Sparse PCA problem following the same approach that lead us to propose problem and problem . We then illustrate this formulation for 2D data in Section 3.

Consider a set of subsets of that represent the patterns that are desired and a number of patterns that would be used to construct the PCs. In practice, patterns could represent a structure that is sought in the data; for instance, patterns could be related genes in genomics or 2D shapes in image recognition. We propose the following exact formulation:

| (10) | ||||

Following the same steps as the ones we used to build the approximation , we propose the following approximation for the structured sparse PCA problem for a given :

| (11) | ||||

This formulation can also be extended to the case in which the patterns are disjoint:

| (12) | ||||

(12) being a special case of problem (each pattern representing one group of PCs sharing the same support), optimality bounds and algorithm apply in this case for . Furthermore, if is not too large, all patterns that violate can be enumerated and eliminated before solving the problem. In this case, all the constraints of Problem (12) can be enumerated and and there is no need to use a cut generation algorithm.

4 Results

We aim in this section to illustrate the benefits of Geometric Sparse PCA (GeoSPCA) method in terms of variance explained, sparsity, predictive power and tractability. We also aim at comparing the performances obtained when building all the PCs at once vs. building them iteratively by deflating the data matrix.

We first explicit principles for the choice of and tuning of . We then test and compare GeoSPCA in the case of all PCs sharing the same support on real world data sets. We finally test GeoSPCA on a image recognition data set using its structured sparsity version including disjointedness constraints of problem .

All tests are conducted computations on an Intel Core i7-8750H CPU at 2.20GHz with 16Gb of RAM on Windows 10 Pro. The solver we used is Gurobi Optimizer 9.1 running with Python 3.6.5.

4.1 Choosing and

We base the approach we use to choose and on the the similarities GeoSPCA has with the classic PCA.

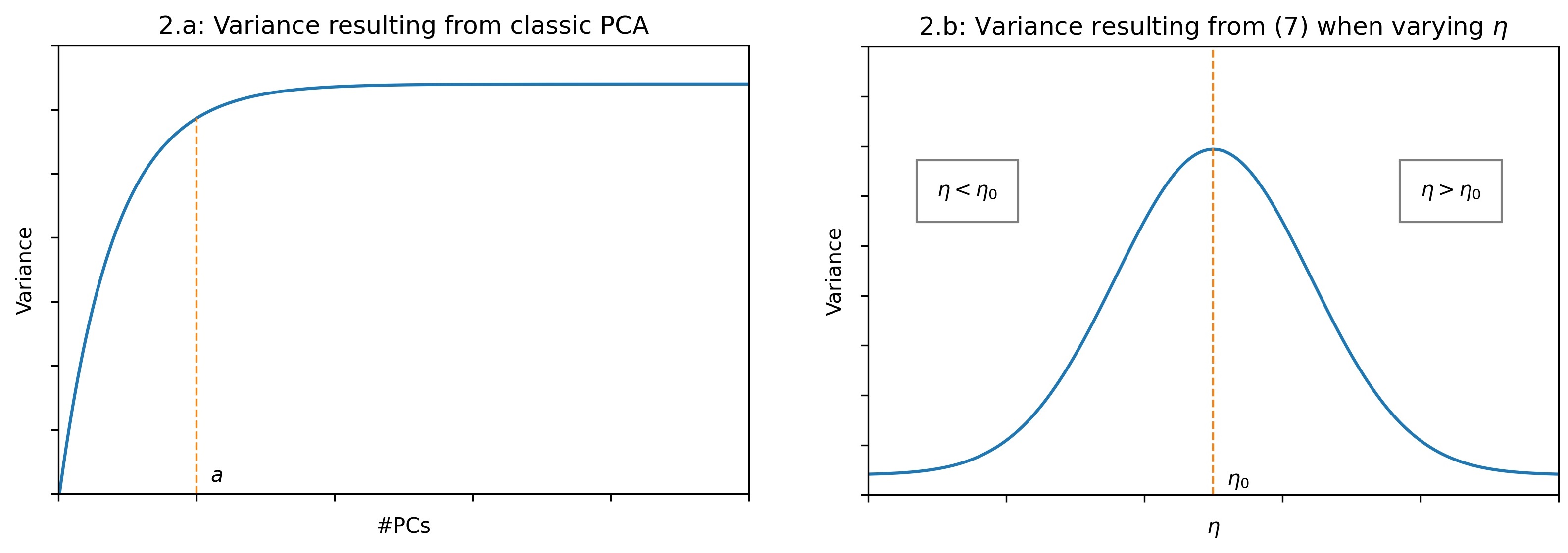

We first tune by finding a suitable number of PCs for the classic PCA following a standard procedure. Namely, could be chosen as the number of PCs beyond which the marginal gain in explained variance is limited (Figure 3a). If can be approximated by a matrix of rank , then a sub-matrix of composed of selected columns of can be approximated by a matrix of rank . Although, theoretically, could be approximated by a matrix of a rank lower than , this is could be the case in a real data setting but this would involve a special structure in the data; in particular, a subset of the columns of must be orthogonal to the remaining columns, or in other words, independence among variables would be required.

The parameter is found using Algorithm 2. We start by choosing that is large (for example ) and then Algotrithm 2 tightens the values of by updating . When for a (see Theorem 4), then is lower than the optimal value of (2). When then the optimal solutions of problem are cut from the feasible set of problem (Figure 3.b).

4.2 GeoSPCA with common support

We consider the problem of maximizing the variance explained from using a number of orthogonal PCs that have a common support of cardinal . We use the formulation to approximate problem . We use real world data sets of various natures and sizes to illustrate the benefits of GeoSPCA. In this subsection, we focus on the amount of explained variance, the benefit of building all PCs at once and the tractability depending on the size of the data set, the number of PCs and the cardinality chosen. We selected publicly available data sets that are widely used in the literature including Mturk (Cheng et al., 2016) which consists of descriptions of randomly chosen pictures using a bag of words, Colon (Alon et al., 1999) a colon cancer gene expression data set, Arcene a mass-spectrometric data aiming at detecting cancer patterns proposed at the NIPS 2003 Feature Selection Challenge (Guyon et al., 2007) and CGD (Wang et al., 2005), a gene expression data set used to classify breast cancers.

We compare GeoSPCA to other techniques that control the sparsity by imposing , the number of variables that are used in the sparse model. Comparison with other techniques in which sparsity is induced by regularization is not significant because achieving the level of sparsity that is achieved while controlling requires to choose a very large weight for the regularization which skews the objective function and produces ultimately low quality solutions. Since we are also aiming at choosing higher than 100 and in 10,000s; we choose PathSPCA (d’Aspremont et al., 2008) to illustrate the benefits of building all PCs at once as its performance is comparable to other techniques extracting iteratively (Papailiopoulos et al., 2013; Yuan and Zhang, 2011). Since this technique extracts one PC at each iteration, a deflation technique is needed. We choose Schur complement deflation for its empirical performance and ease of use (see (Mackey, 2009) for a description and a full discussion on deflation techniques). Sparse PCs found with this process are then orthogonalized. We also use a greedy algorithm directly inspired from (Moghaddam et al., 2006) and (d’Aspremont et al., 2008). We build the support of the solution by iteratively including the indices that maximize the increase in variace pactured from an iteration to another. We start with an empty set and we iteratively add indices to such that:

Greedy approaches have proven to be particularly effective and are often at par with state-of-the-art techniques (d’Aspremont et al., 2008; Bertsimas et al., 2022; Journee et al., 2008; Papailiopoulos et al., 2013).

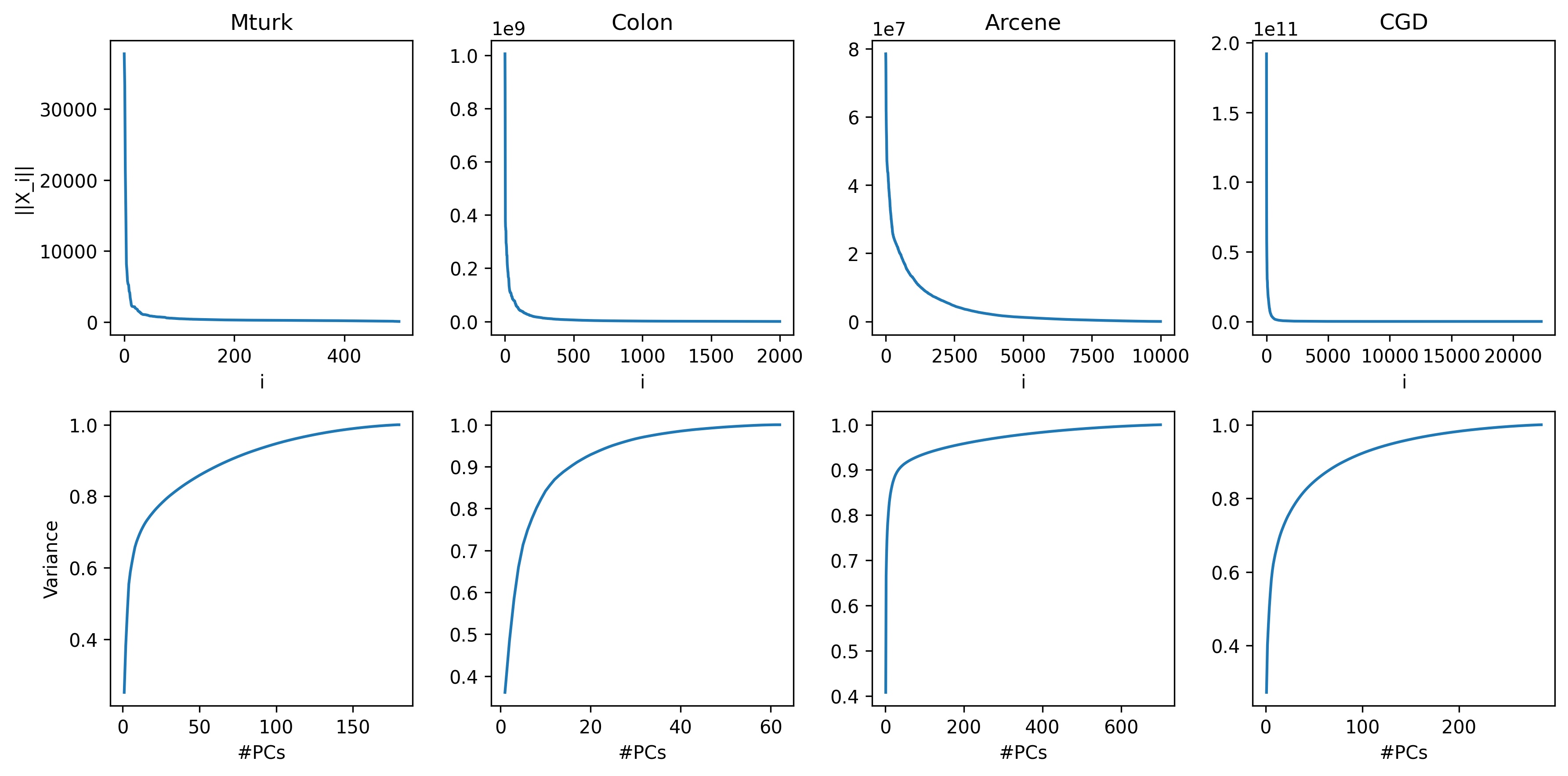

We report the sorted norms of the columns on for the different data sets considered in Figure 4 (Top). Formulation sheds a light on one reason the greedy approach performs well. Indeed, as explained in problem , the objective function is , so maximizing the variance captured from features is closely related to the norm of the columns related to these features. If some columns of have a much higher norm than the rest of the columns, they are likely to be selected by the greedy algorithm and their related variables are also likely to be in the support of the optimal solution. This is true for which is the case that is the most studied in the literature and many of the data sets considered in the literature have columns with a norm far exceeding the norms of the remaining columns.

We first conduct tests with PathSPCA using a constant number of features for the construction of each PC. After generating PCs, we count the total number of features used (we note that different PCs may use common features). We then conduct tests using Algorithm 1 using variables. Values of are chosen for illustration purposes and are also the result of the number of variables that the deflation method produces. Indeed, in all cases studied in this paper, PathSPCA often chooses to reuse variables that were used in previously constructed PCs. The cuts are generated as lazy constraints.

| Data set | k | Deflation | Greedy | GeoSPCA | GeoSPCA vs. Greedy | Time | GAP | #cuts | |

|---|---|---|---|---|---|---|---|---|---|

| Mturk | 8 | 16 | 5.62E+3 | 1.57E+5 | 1.59E+5 | +1.1% | 1s | 0% | 56 |

| 21 | 5.6E+3 | 1.66E+5 | 1.67E+5 | +1% | 1s | 1.7% | 44 | ||

| (180;500) | 26 | 8.73E+3 | 1.71E+5 | 1.74E+5 | +1.7% | 1s | 2.8% | 30 | |

| 29 | 8.7E+3 | 1.76E+5 | 1.78E+5 | +0.8% | 1s | 3.4% | 154 | ||

| 32 | 9.06E+3 | 1.8E+5 | 1.81E+5 | +0.4% | 1s | 4% | 1208 | ||

| Colon | 5 | 11 | 1.02E+9 | 4.57E+9 | 4.79E+9 | +4.9% | 1s | 1.7% | 120 |

| 12 | 1.97E+9 | 4.74E+9 | 4.92E+9 | +3.8% | 1s | 3.8% | 85 | ||

| (62;2,000) | 15 | 2.27E+9 | 5.41E+9 | 5.49E+9 | +1.5% | 1s | 8.4% | 562 | |

| 18 | 2.8E+9 | 5.9E+9 | 5.94E+9 | +0.6% | 1s | 12% | 384 | ||

| 33 | 3.81E+9 | 7.62E+9 | 7.6E+9 | -0.3% | 1s | 21.2% | 1214 | ||

| Arcene | 3 | 14 | 7.43E+7 | 8.2E+8 | 1.02E+9 | +24.2% | 1s | 0% | 6 |

| 22 | 8.7E+7 | 1.27E+9 | 1.5E+9 | +18.1% | 1s | 0% | 9 | ||

| (700; | 53 | 1.76E+8 | 2.74E+9 | 3.01E+9 | +9.7% | 1s | 1.6% | 7 | |

| 10,000) | 132 | 5.9E+8 | 5.83E+9 | 6.08E+9 | +4.4% | 1s | 4.1% | 35 | |

| 270 | 7.95E+8 | 9.78E+9 | 9.82E+9 | +0.4% | 45s | 7.1% | 590 | ||

| CGD | 11 | 23 | 5.11E+10 | 1.84E+12 | 1.89E+12 | +2.7% | 1s | 1% | 71 |

| (n,p) = | 43 | 1.09E+11 | 2.5E+12 | 2.63E+12 | +5.1% | 1s | 6.3% | 50 | |

| (286; | 58 | 1.91E+11 | 2.89E+12 | 3E+12 | +3.9% | 6s | 10.2% | 166 | |

| 22,283) | 85 | 2.82E+11 | 3.45E+12 | 3.54E+12 | +2.9% | 20s | 14.4% | 359 | |

| 174 | 3.25E+11 | 4.64E+12 | 4.67E+12 | +0.6% | 118s | 23% | 1308 |

We report results in Table 1. We first notice that deflation produces significantly lower explained variance vs. GeoSPCA and the greedy in all cases; sometimes by more than an order of magnitude. The illustrates the benefit of constructing all the PCs at once instead of doing so iteratively through deflation. Considering the Greedy approach, GeoSPCA outperforms this method in almost all cases by up to . When it comes to the variance explained by sparse PCA, even is significant as this implies, depending on the application considered, more lives saved or increased profits. Even theoretically, considering problem , when the vectors with the largest norms have a norm far exceeding the remaining columns (Figure 3), improving the explained variance by 1% is remarkable. We notice also that for Arcene and CDG data sets, the error has a greater norm compared to other data sets with respect to . This signals that the sparse PCA problem is harder to solve which explains the edge GeoSPCA has over a simple greedy approach.

Computation time for GeoSPCA did not exceed 2 mins while PathSPCA and the greedy approach needed several hours (and often tens of hours on CGD) to provide a solution (see Table 2. We note also that GeoSPCA does not need to compute or handle the covariance matrix which also contribute to drastically reduced computation time, especially for the largest instances. has 4.84 10E9 entries that, besides the inherent PathSPCA computation time, needs to be deflated to compute each PC. This already creates complications in the management of the memory capacity of most personal computers.

| Method | Mturk | Colon | Arcene | CGD |

|---|---|---|---|---|

| PathSPCA | 1 to 3s | 9 to 11s | 4 to 8 mins | 2 mins to 11 hours |

| Greedy | 2 to 10s | 4 to 20s | 2min to 8 hours | 4 mins to 51 hours |

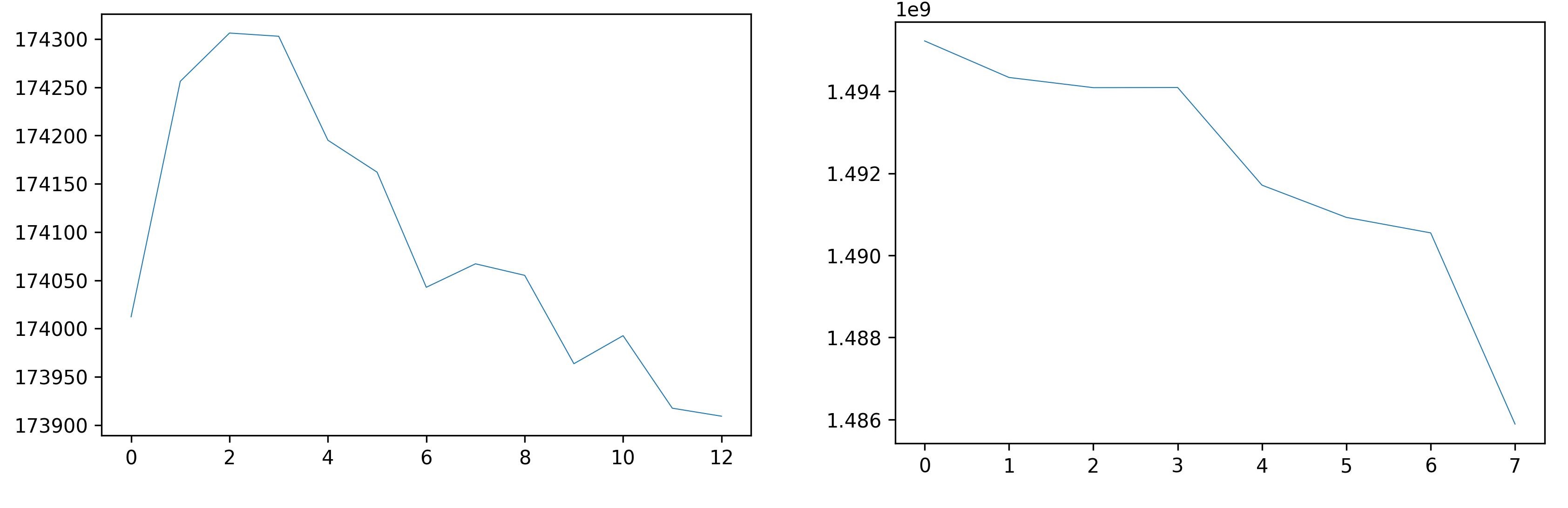

Still considering the same data sets and and values, we report in Figure 5 the evolution of the objective function of (2) in blue and (7) in orange as cuts are iteratively added in Algorithm 2 with respect to the number of cuts for the 3000 first cuts generated. For this experiment, we drop the lazy constraints feature in Gurobi. An optimal solution is found when the lowest value of (7) (in orange) is lower than a value of (2) (in blue). The green dotted line represents the lowest value of (7) achieved.

We also report for the same experiment with respect to in Figure 6. We chose instances in which the optimal value is found by Algorithm 2 (using Proposition 11 to prove it). For Mturk (left), we notice that Algorithm 2 reduces until the optimal solution is found at , then optimal solutions are cut and then decreases below the optimal solution value. For Arcene (right), the optimal solution is found at the first iteration, then the optimal solution is cut and decreases also to values below the optimal value.

4.3 Experiments for Structured Sparse PCA

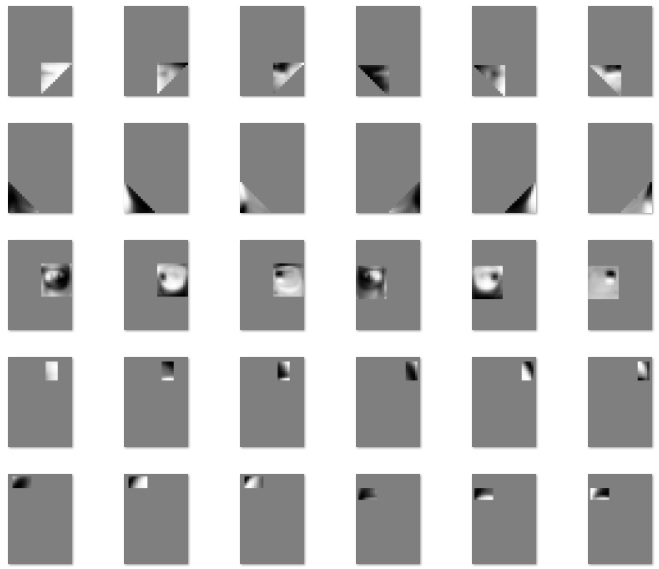

Imposing a structure in the variables to build the PCs can yield substantial benefits vs. PCA or sparse PCA in a number of applications including genomics and face recognition(Li et al., 2017; Jenatton et al., 2009). We test GeoSPCA in its structured version (12) (we will call it GeoSSPCA). We chose to use face recognition for its ease of interpretation to test the method and use the data set (Martinez and Kak, 2001). The data set consists of 2600 cropped pictures of the faces of 50 men and 50 women. For each person, 26 pictures are provided with the different face expressions and lightning configurations. In 12 of the 26 pictures, parts of the face is hidden either by black glasses or scarves (a sample of pictures is provided in Figure7).

We use as patterns triangles, rectangles and octagons with dimensions varying from 3 to 8 pixels as elements of the patterns set. We filter all patterns that violate the constraint (using the same notations as in (12)) so we solve only a BLO problem once as all remaining patterns verify this constraint. We choose and and report an example of PCs constructed while solving (12) in Figure8. We notice that the shapes and the location of the shape capture intuitive components of the face most of the time (eyes, mouth, shape of the jaw and forehead,…).

We follow the same procedure used in (Jenatton et al., 2009); the resolution of the images is reduced from to ; for each person represented in the data set, we use the 14 pictures in which the whole face is visible for training and test on the 12 pictures in which part of the face is hidden. We also use k-NN algorithm to classify the pictures after reducing the dimension using GeoSSPCA and compare to the precision achieved by Structured Sparse PCA(Jenatton et al., 2009) (using the modeling scheme proposed by the authors), and PCA depending on the number of PCs. For GeoSSPCA, we choose and increase to have a number of PCs varying from 10 to 70. A comparison of the precision is provided in Figure 9.

We note that the patterns can be written also as intersections of half spaces by modifying accordingly (12). However, the polyhedron resulting from the relaxation of the binary constraints leads to computational considerations that go beyond the scope of this paper.

4.4 Discussion

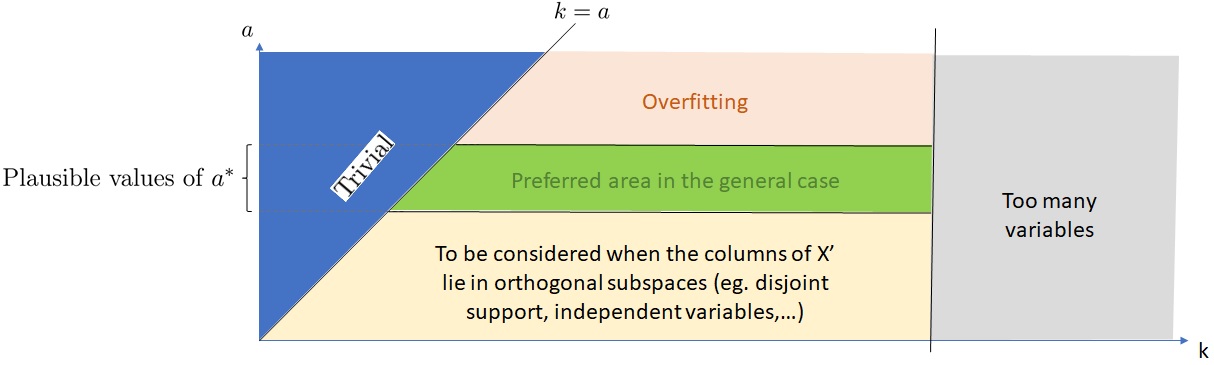

We deduct from the geometric interpretation of GeoSPCA some implications on good practices when using Sparse PCA in terms of choice of and . First on the choice of , if the matrix can be approximated with a matrix of rank , it seems unlikely that a submatrix of would need to be approximated by a matrix of rank higher than . Choosing a value higher than would lead to capture elements that were meant to be ignored such as noise and could then lead to over-fitting. It is however possible to consider values of that are lower than . If can be approximated by a matrix of rank , a submatrix could eventually be approximated by a matrix of rank if has columns that are orthogonal to other columns of , or in other words if the variables defined by the support of are independent from other features of . This is true when the supports of the PCs are disjoint for example as we have considered in the Structured Sparse PCA setting in the current section.

Regarding the choice of , we notice first that choosing leads to a trivial problem as an optimal solution can be constructed using the columns of that have the largest norm. In this case, columns can be projected into a space of dimension using with . On the other hand, cannot be chosen too big to preserve the putpose of sparse PCA. We provide a summary in Figure 10.

5 Conclusion

In this paper, we proposed GeoSPCA, a new approach to the sparse PCA problem building on a geometrical interpretation of the problem. We addressed in particular the case in which the PCs share a common support. We then illustrated the versatility of this method to the case in which PCs are organized in groups that have disjoint supports and further extended this adaptation to the Structured Sparse PCA problem. The experiments we conducted showed that GeoSPCA can tackle real world instances with a number of features in the 10,000s exceeding the performance of state-of-the-art approaches while providing high quality solutions in minutes.

We believe the method can be further applied to more variants of the Sparse PCA problem and can also be improved especially by generating more efficient cuts at each iteration of the algorithms proposed.

References

- Alon et al. (1999) U. Alon, N. Barkai, D. A. Notterman, K. Gish, S. Ybarra, D. Mack, and A. J. Levine. Broad patterns of gene expression revealed by clustering analysis of tumor and normal colon tissues probed by oligonucleotide arrays. Proceedings of the National Academy of Sciences, 96(12):6745–6750, 1999.

- Asteris et al. (2015) Megasthenis Asteris, Dimitris Papailiopoulos, Anastasios Kyrillidis, and Alexandros Dimakis. Sparse pca via bipartite matchings. In C. Cortes, N. Lawrence, D. Lee, M. Sugiyama, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 28. Curran Associates, Inc., 2015.

- Benidis et al. (2016) Konstantinos Benidis, Ying Sun, Prabhu Babu, and Daniel Palomar. Orthogonal sparse eigenvectors: A procrustes problem. In 2016 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pages 4683–4686, 2016.

- Berk and Bertsimas (2019) Lauren Berk and Dimitris Bertsimas. Certifiably optimal sparse principal component analysis. Mathematical Programming Computation, 11:381–420, 9 2019.

- Bertsimas et al. (2020) D. Bertsimas, D. Lahlou Kitane, N. Azami, and F.R. Doucet. Novel mixed integer optimization sparse regression approach in chemometrics. Analytica Chimica Acta, 1137:115–124, 2020.

- Bertsimas et al. (2022) Dimitris Bertsimas, Ryan Cory-Wright, and Jean Pauphilet. Solving large-scale sparse pca to certifiable (near) optimality. Journal of Machine Learning Research, 23(13):1–35, 2022.

- Cadima and Jolliffe (1995) Jorge Cadima and Ian T Jolliffe. Loading and correlations in the interpretation of principle compenents. Journal of applied Statistics, 22(2):203–214, 1995.

- Chen et al. (2020) EShixiang Chen, Shiqian Ma, Lingzhou Xue, and Hui Zou. An alternating manifold proximal gradient method for sparse principal component analysis and sparse canonical correlation analysis. INFORMS Journal on Optimization, 2(3):192–208, 2020.

- Cheng et al. (2016) Ting-Yu Cheng, Guiguan Lin, xinyang gong, Kang-Jun Liu, and Shan-Hung (Brandon) Wu. Learning user perceived clusters with feature-level supervision. In D. Lee, M. Sugiyama, U. Luxburg, I. Guyon, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 29. Curran Associates, Inc., 2016.

- d’Aspremont et al. (2004) Alexandre d’Aspremont, Laurent El Ghaoui, Michael I. Jordan, and Gert R. G. Lanckriet. A direct formulation for sparse PCA using semidefinite programming. CoRR, cs.CE/0406021, 2004.

- d’Aspremont et al. (2008) Alexandre d’Aspremont, Francis Bach, and Laurent El Ghaoui. Optimal solutions for sparse principal component analysis. J. Mach. Learn. Res., 9:1269–1294, June 2008.

- Del Pia (2022) Alberto Del Pia. Sparse pca on fixed-rank matrices. Mathematical Programming, 2022.

- Dey et al. (2022) Santanu S. Dey, Marco Molinaro, and Guanyi Wang. Solving sparse principal component analysis with global support. Mathematical Programming, 2022.

- Erichson et al. (2020) N. Benjamin Erichson, Peng Zheng, Krithika Manohar, Steven L. Brunton, J. Nathan Kutz, and Aleksandr Y. Aravkin. Sparse principal component analysis via variable projection. SIAM Journal on Applied Mathematics, 80(2):977–1002, 2020.

- Fu et al. (2017) Wei Fu, Shutao Li, Leyuan Fang, and Jón Atli Benediktsson. Adaptive spectral–spatial compression of hyperspectral image with sparse representation. IEEE Transactions on Geoscience and Remote Sensing, 55(2):671–682, 2017.

- Guyon et al. (2007) Isabelle Guyon, Jiwen Li, Theodor Mader, Patrick Pletscher, Georg Schneider, and Markus Uhr. Competitive baseline methods set new standards for the nips 2003 feature selection benchmark. Pattern Recognition Letters, 28(12):1438–1444, 2007.

- Huang and Wei (2019) Wen Huang and Ke Wei. Extending fista to riemannian optimization for sparse pca. Technical report, 2019.

- Jeffers (1967) J. N. R. Jeffers. Two case studies in the application of principal component analysis. Journal of the Royal Statistical Society. Series C (Applied Statistics), 16(3):225–236, 1967.

- Jenatton et al. (2009) Rodolphe Jenatton, Guillaume Obozinski, and Francis Bach. Structured sparse principal component analysis, 2009.

- Johnstone and Lu (2009) Iain M. Johnstone and Arthur Yu Lu. On consistency and sparsity for principal components analysis in high dimensions. Journal of the American Statistical Association, 104(486):682–693, 2009.

- Jolliffe et al. (2003) Ian T. Jolliffe, Nickolay T. Trendafilov, and Mudassir Uddin. A modified principal component technique based on the lasso. Journal of Computational and Graphical Statistics, 12(3):531–547, 2003.

- Journee et al. (2008) Michel Journee, Yurii Nesterov, Peter Richtarik, and Rodolphe Sepulchre. Generalized power method for sparse principal component analysis. Universite catholique de Louvain, Center for Operations Research and Econometrics (CORE), CORE Discussion Papers, 11, 11 2008.

- Li and Xie (2020) Yongchun Li and Weijun Xie. Exact and approximation algorithms for sparse pca, 2020.

- Li et al. (2017) Ziyi Li, Sandra Safo, and Qi Long. Incorporating biological information in sparse principal component analysis with application to genomic data. BMC Bioinformatics, 18(1):332, 2017.

- Ma (2013) Zongming Ma. Sparse principal component analysis and iterative thresholding. The Annals of Statistics, 41(2):772 – 801, 2013.

- Mackey (2009) Lester Mackey. Deflation methods for sparse pca. In D. Koller, D. Schuurmans, Y. Bengio, and L. Bottou, editors, Advances in Neural Information Processing Systems, volume 21. Curran Associates, Inc., 2009.

- Martinez and Kak (2001) A.M. Martinez and A.C. Kak. Pca versus lda. IEEE Transactions on Pattern Analysis and Machine Intelligence, 23(2):228–233, 2001.

- Moghaddam et al. (2006) Baback Moghaddam, Yair Weiss, and Shai Avidan. Spectral bounds for sparse pca: Exact and greedy algorithms. In Y. Weiss, B. Schölkopf, and J. Platt, editors, Advances in Neural Information Processing Systems, volume 18. MIT Press, 2006.

- Papailiopoulos et al. (2013) Dimitris Papailiopoulos, Alexandros Dimakis, and Stavros Korokythakis. Sparse pca through low-rank approximations. In Sanjoy Dasgupta and David McAllester, editors, Proceedings of the 30th International Conference on Machine Learning, volume 28 of Proceedings of Machine Learning Research, pages 747–755, Atlanta, Georgia, USA, 17–19 Jun 2013. PMLR.

- Pearson (1901) Karl Pearson. On lines and planes of closest fit to systems of points in space. The London, Edinburgh, and Dublin Philosophical Magazine and Journal of Science, 2(11):559–572, 1901.

- Shen and Huang (2008) Haipeng Shen and Jianhua Z. Huang. Sparse principal component analysis via regularized low rank matrix approximation. Journal of Multivariate Analysis, 99(6):1015–1034, 2008.

- Tan et al. (2021) Mingkui Tan, Zhibin Hu, Yuguang Yan, Jiezhang Cao, Dong Gong, and Qingyao Wu. Learning sparse pca with stabilized admm method on stiefel manifold. IEEE Transactions on Knowledge and Data Engineering, 33(3):1078–1088, 2021.

- Wang et al. (2005) Yixin Wang, Jan GM Klijn, Yi Zhang, Anieta M Sieuwerts, Maxime P Look, Fei Yang, Dmitri Talantov, Mieke Timmermans, Marion E Meijer-van Gelder, Jack Yu, Tim Jatkoe, Els MJJ Berns, David Atkins, and John A Foekens. Gene-expression profiles to predict distant metastasis of lymph-node-negative primary breast cancer. The Lancet, 365(9460):671–679, 2005.

- Witten et al. (2009) Daniela M. Witten, Robert Tibshirani, and Trevor Hastie. A penalized matrix decomposition, with applications to sparse principal components and canonical correlation analysis. Biostatistics, 10(3):515–534, 04 2009.

- Yuan and Zhang (2011) Xiao-Tong Yuan and Tong Zhang. Truncated power method for sparse eigenvalue problems. Journal of Machine Learning Research, 14, 12 2011.

- Zou et al. (2006) Hui Zou, Trevor Hastie, and Robert Tibshirani. Sparse principal component analysis. Journal of Computational and Graphical Statistics, 15(2):265–286, 2006.