Fitting State-space Model for Long-term Prediction

of the Log-likelihood of Nonstationary Time Series Models

Genshiro Kitagawa

Mathematics and Informatics Center, The University of Tokyo

Abstract The goodness of the long-term prediction in the state-space model was evaluated using the squared long-term prediction error. In order to estimate the model parameters suitable for long-term prediction, we devised a modified log-likelihood corresponding to the long-term prediction error variance. Trend models and seasonally adjusted models with and without AR component are examined as examples.

1 Introduction: State-Space Modeling of Time Series

1.1 State-Space Model and State Estimation

Consider the state-space model of a univaraite time series ;

| (1) | |||||

| (2) |

where is a -dimensional state vector, is an -dimensional system noise that follows a white noise with mean vector zero and variance-covariance matrix , and is the observation noise that follows a 1-dimensional Gaussian white noise with mean zero and the variance . , , and are , , and matrices, respectively. The initial state vector is assumed to follow the Gaussian distribution, . Many linear models used in time series analysis such as the AR model, ARMA model and various nonstationary models such as the trend model and the seasonal adjustment model are expressible in terms of the state-space models (Anderson and Moore (1979), Kitagawa (2020)).

In this paper, we shall consider the problem of estimating the state at time based on the set of observations . For , , and , the state estimation problem is referred to as the prediction, filter and smoothing, respectively. This state estimation problem is important in state-space modeling since many tasks such as one-step-ahead and multi-step-ahead prediction, interpolation, and likelihood computation for the time series can be systematically solved through the estimated state.

A generic approach to these state estimation problems is to obtain the conditional distribution of the state given the observations . Then, since the state-space model defined by (1) and (2) is a linear model, and moreover the noises and , and the initial state follow normal distributions, all these conditional distributions become normal distributions. Therefore, to solve the problem of state estimation of the state-space model, it is sufficient to obtain the mean vectors and the variance-covariance matrices of the conditional distributions.

For the linear state-space model, Kalman filter provides a computationally efficient recursive computational algorithm for state estimation (Kalman (1960), Anderson and Moore (1976)).

One-step-ahead prediction

| (3) |

Filter

| (4) | |||||

1.2 Likelihood Computation and Parameter Estimation for Time Series Models

Assume that the state-space representation for a time series model specified by a parameter is given. When the time series of length is given, the dimensional joint density function of specified by this time series model is denoted by . Then, the likelihood of this model is defined by . Using the conditional distribution of given the previous observations, the likelihood of the time series model can be expressed as a product of one-dimentional conditional density functions:

| (5) |

Here, if we define (empty set), then . By taking the logarithm of , the log-likelihood of the model is obtained as

| (6) |

Since is the conditional distribution of given the observation and it is, in fact, a normal distribution with mean and variance , it can be expressed as (Kitagawa and Gersch (1996))

| (7) |

Here, from the observation model, (2), and are obtained by

| (8) | |||||

| (9) |

Therefore, by substituting this density function into (6), the log-likelihood of this state-space model is obtained as

| (10) |

The maximum likelihood estiamtes of the parameters of the state-space model can be obtained by maximizing this log-likelihood function numerically. However, for univariate time series, we can assume that (Kitagawa (2020)). Actually, if , , , and are defined by

| (11) |

then it can be seen that the obtained Kalman gain is identical to . Therefore, in the filtering step, we may use and instead of and . Furthermore, it can be seen that the vectors and of the state do not change under these modifications. In summary, if is time-invariant and is an unknown parameter, we may apply the Kalman filter by setting . Since we then have from (10), this yields

| (12) |

1.3 Parameter Estimation and Criterion for Increasing Horizon Prediction of the State

For the state-space model, by repeating the one-step-ahead prediction step, we can perform increasing horizon prediction, that is, we can obtain and for .

The increasing horizon prediction

For , repeat

| (16) |

The long-term prediction is considered by many authors such as Judd and Small (2000), Sorjamaa et. al. (2007) and Xiong et. al. (2013). In this paper, we evaluate the goodness of the long-term prediction by the difference between the predictied value and the observed value

| (17) |

where -step-ahead prediction error is defined by and is defined by . We can also consider a modified log-likelihood for the long-term prediction defined by

| (18) |

where is obtained by . Note that, different from the case of one-step-ahead prediction errors, the long-term prediction errors, are not independent.

Given the predetermined prediction horizon , the optimal value of the parameter vector for -step-ahead prediction is obtained by maximizing this modified log-likelihood.

2 Examples

2.1 Trend models

2.1.1 The secon order trend model

We consider the second order trend model

| (19) |

where is the trend component that follows the second order trend component model and and are Gaussian white noise and , respectively. Note that this trend model can be expressed by a state-space model by

| (27) |

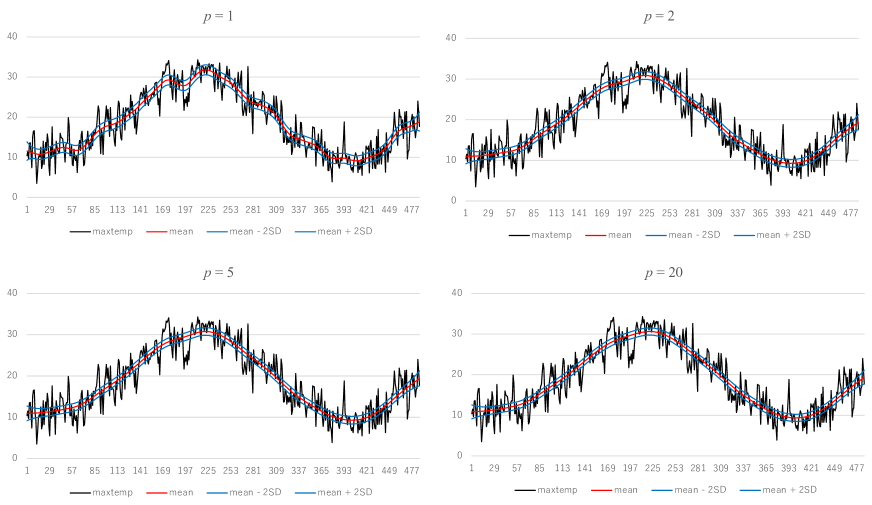

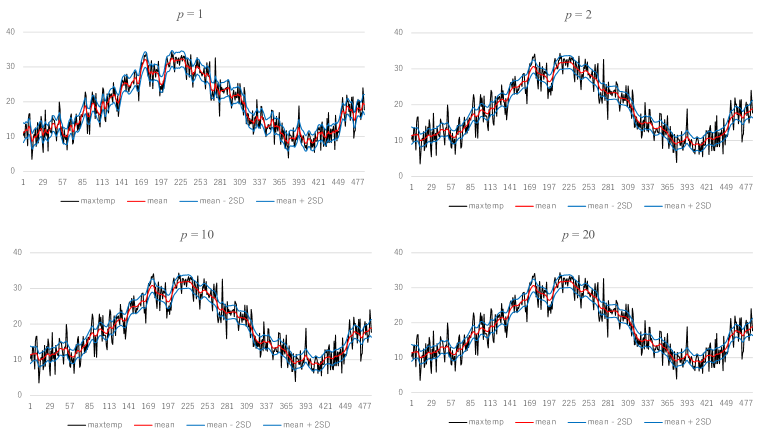

Figure 1 shows the trend estimates of the maxtemp data (daily maximum temperature data in Tokyo, N=486). Smoothed estimate (red) and 2SD interval are shown. Top left plot shows the estimates obtained by the ordinary maximum likelihood method, i.e., by . On the other hand, three other plots show the results obtained by modified log-likelihood criteria asumming and 20, respectively. It can be seen that the trend estimate by is considerably variable compared with other three estimates, and other three estimates obtained with resemble each other.

Table 1 shows the increasing horizon prediction error variances , , for various parameter estimation criteria , =1,(1),6,(2),20. The results for shown in the second column are the increasing horaizon prediction error variances of the model obtained by the maximum-likelihood method. In general, -element of the table shows the -step-ahead prediction error variance of the model whose parameter was obtained by maximizing the modified log-likelihood for -step-ahead prediction criterion (18). Naturally, the one-step-ahead prediction error variance attains the smallest value 9.89 with , but the long-term prediction error variances, i.e., for , becomes the largest among . The table also shows that the -step-ahead prediction error variance is the smallest at the criterion . For , the increase of the long-term prediction error varaince is not so significant and takes similar values for different . The last row of the table shows the average of the long-term prediction error varainces, , over for each .

| 1 | 2 | 3 | 4 | 5 | 6 | 8 | 10 | 12 | 14 | 16 | 18 | 20 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 9.89 | 10.02 | 10.05 | 10.07 | 10.07 | 10.08 | 10.13 | 10.15 | 10.16 | 10.17 | 10.20 | 10.22 | 10.20 |

| 2 | 10.92 | 10.52 | 10.52 | 10.53 | 10.53 | 10.53 | 10.56 | 10.58 | 10.58 | 10.59 | 10.62 | 10.64 | 10.62 |

| 3 | 11.93 | 11.18 | 11.16 | 11.16 | 11.16 | 11.16 | 11.18 | 11.19 | 11.20 | 11.20 | 11.22 | 11.24 | 11.22 |

| 4 | 12.78 | 11.60 | 11.57 | 11.55 | 11.55 | 11.55 | 11.55 | 11.55 | 11.56 | 11.56 | 11.58 | 11.59 | 11.58 |

| 5 | 13.62 | 12.07 | 12.02 | 12.00 | 12.00 | 11.99 | 11.97 | 11.98 | 11.98 | 11.98 | 12.00 | 12.01 | 12.00 |

| 6 | 14.46 | 12.58 | 12.51 | 12.48 | 12.48 | 12.46 | 12.43 | 12.43 | 12.43 | 12.43 | 12.44 | 12.45 | 12.44 |

| 7 | 15.82 | 13.60 | 13.51 | 13.47 | 13.47 | 13.45 | 13.41 | 13.40 | 13.40 | 13.40 | 13.41 | 13.42 | 13.41 |

| 8 | 17.32 | 14.52 | 14.41 | 14.35 | 14.35 | 14.33 | 14.26 | 14.25 | 14.24 | 14.24 | 14.24 | 14.24 | 14.24 |

| 9 | 18.58 | 15.22 | 15.09 | 15.02 | 15.02 | 14.98 | 14.90 | 14.88 | 14.88 | 14.87 | 14.86 | 14.87 | 14.86 |

| 10 | 19.23 | 15.39 | 15.23 | 15.15 | 15.15 | 15.11 | 15.02 | 15.00 | 14.99 | 14.99 | 14.98 | 14.98 | 14.98 |

| 11 | 20.40 | 15.88 | 15.70 | 15.62 | 15.61 | 15.57 | 15.46 | 15.43 | 15.42 | 15.41 | 15.40 | 15.40 | 15.40 |

| 12 | 20.88 | 15.99 | 15.80 | 15.71 | 15.71 | 15.66 | 15.55 | 15.53 | 15.52 | 15.51 | 15.50 | 15.51 | 15.50 |

| 13 | 22.18 | 16.64 | 16.43 | 16.33 | 16.33 | 16.27 | 16.15 | 16.11 | 16.11 | 16.10 | 16.08 | 16.08 | 16.08 |

| 14 | 23.56 | 17.28 | 17.04 | 16.93 | 16.93 | 16.87 | 16.73 | 16.69 | 16.68 | 16.67 | 16.65 | 16.65 | 16.66 |

| 15 | 25.22 | 18.00 | 17.72 | 17.59 | 17.59 | 17.52 | 17.35 | 17.31 | 17.30 | 17.28 | 17.26 | 17.26 | 17.26 |

| 16 | 27.35 | 18.79 | 18.46 | 18.30 | 18.30 | 18.22 | 18.01 | 17.95 | 17.94 | 17.92 | 17.89 | 17.87 | 17.89 |

| 17 | 30.28 | 20.38 | 20.01 | 19.82 | 19.82 | 19.72 | 19.48 | 19.41 | 19.40 | 19.37 | 19.33 | 19.31 | 19.33 |

| 18 | 32.65 | 21.51 | 21.10 | 20.89 | 20.89 | 20.78 | 20.52 | 20.43 | 20.42 | 20.39 | 20.35 | 20.32 | 20.35 |

| 19 | 33.84 | 21.88 | 21.46 | 21.25 | 21.25 | 21.14 | 20.88 | 20.80 | 20.79 | 20.77 | 20.72 | 20.71 | 20.73 |

| 20 | 35.03 | 22.49 | 22.07 | 21.87 | 21.86 | 21.76 | 21.51 | 21.44 | 21.43 | 21.41 | 21.38 | 21.37 | 21.38 |

| 21.51 | 16.09 | 15.89 | 15.80 | 15.80 | 15.75 | 15.64 | 15.61 | 15.60 | 15.59 | 15.58 | 15.59 | 15.58 |

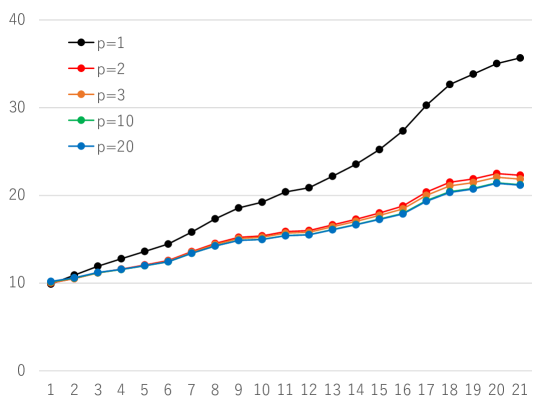

Figure 2 shows the increase of the long-term prediction error variance , for 1, 2, 3, 10 and 20. We can see that the long-term prediction error variances obtained by are significantly larger than other cases, and there is almost no difference in the prediction error variances among , 3, 10 and 20.

From the table and the figure, it can be concluded, at least for this data set, that the model with the maximum likelihood estimates of the patameter has the minimum one-step-ahead prediction error variance but has the largest long-term prediction error varainces. For this second order trend model yield a similar increasing horaizon prediction performances.

2.1.2 The first order trend model

Figure 3 and Table 2 show similar results for the first order trend model,

| (28) |

As can be seen in the figure, in this case, different from the case of , the estimated trends are wiggly and the change of the estimated trends by the selection of the prediction horaizon are not so significant.

From the table, it is seen that the one-step-ahead prediction error variances are smaller than those of the second order trend model for entire . Also, the increase of the prediction error variance with the increase of the prediction horaizon is not so large as the second order trend model. Further, it is interesting that the inreasing horaison predictive ability is almost the same for all criterion parameter . The table also shows that the increasing horizon prediction performance is quite similar for various choise of . Note that for the first order trend model, -step-ahead prediction error variance is obtained by

| (29) |

Compared with the results of the second order trend model, at least for the presend data, inspite of the wiggly trend estimate, the first order trend model has slightly better prediction ability than the second order trend model.

| 1 | 2 | 3 | 4 | 5 | 6 | 8 | 10 | 12 | 14 | 16 | 18 | 20 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 8.86 | 9.06 | 9.12 | 9.17 | 9.17 | 9.12 | 9.09 | 9.06 | 8.99 | 8.90 | 8.91 | 9.07 | 9.03 |

| 2 | 10.34 | 9.95 | 9.95 | 9.95 | 9.95 | 9.95 | 9.94 | 9.95 | 9.97 | 10.08 | 10.07 | 9.95 | 9.95 |

| 3 | 11.22 | 10.68 | 10.67 | 10.66 | 10.66 | 10.67 | 10.67 | 10.68 | 10.73 | 10.89 | 10.87 | 10.68 | 10.70 |

| 4 | 12.01 | 11.31 | 11.28 | 11.27 | 11.27 | 11.28 | 11.30 | 11.31 | 11.39 | 11.59 | 11.57 | 11.30 | 11.34 |

| 5 | 12.59 | 11.82 | 11.79 | 11.78 | 11.78 | 11.79 | 11.80 | 11.82 | 11.90 | 12.12 | 12.10 | 11.81 | 11.85 |

| 6 | 12.88 | 12.24 | 12.22 | 12.22 | 12.22 | 12.22 | 12.22 | 12.24 | 12.29 | 12.48 | 12.45 | 12.23 | 12.25 |

| 7 | 13.18 | 12.67 | 12.67 | 12.68 | 12.68 | 12.67 | 12.67 | 12.67 | 12.71 | 12.85 | 12.83 | 12.67 | 12.68 |

| 8 | 13.88 | 13.30 | 13.30 | 13.30 | 13.30 | 13.30 | 13.30 | 13.30 | 13.35 | 13.51 | 13.49 | 13.30 | 13.32 |

| 9 | 14.39 | 13.79 | 13.78 | 13.79 | 13.79 | 13.78 | 13.78 | 13.79 | 13.83 | 14.00 | 13.98 | 13.78 | 13.80 |

| 10 | 14.70 | 14.14 | 14.14 | 14.16 | 14.16 | 14.14 | 14.14 | 14.14 | 14.17 | 14.32 | 14.30 | 14.14 | 14.15 |

| 11 | 15.30 | 14.67 | 14.67 | 14.68 | 14.68 | 14.67 | 14.66 | 14.67 | 14.70 | 14.87 | 14.85 | 14.66 | 14.67 |

| 12 | 15.30 | 14.92 | 14.96 | 14.99 | 14.99 | 14.95 | 14.94 | 14.92 | 14.91 | 14.99 | 14.98 | 14.93 | 14.91 |

| 13 | 15.65 | 15.42 | 15.47 | 15.51 | 15.51 | 15.46 | 15.44 | 15.42 | 15.38 | 15.41 | 15.40 | 15.43 | 15.40 |

| 14 | 15.87 | 15.84 | 15.90 | 15.96 | 15.96 | 15.90 | 15.87 | 15.84 | 15.77 | 15.74 | 15.74 | 15.85 | 15.81 |

| 15 | 16.39 | 16.48 | 16.55 | 16.61 | 16.61 | 16.55 | 16.51 | 16.48 | 16.40 | 16.34 | 16.34 | 16.49 | 16.44 |

| 16 | 17.52 | 17.48 | 17.53 | 17.58 | 17.58 | 17.53 | 17.50 | 17.48 | 17.43 | 17.42 | 17.42 | 17.49 | 17.46 |

| 17 | 18.81 | 18.52 | 18.55 | 18.58 | 18.57 | 18.54 | 18.53 | 18.52 | 18.52 | 18.59 | 18.58 | 18.52 | 18.51 |

| 18 | 19.99 | 19.43 | 19.43 | 19.45 | 19.45 | 19.43 | 19.43 | 19.43 | 19.47 | 19.62 | 19.61 | 19.43 | 19.44 |

| 19 | 20.74 | 20.11 | 20.11 | 20.13 | 20.13 | 20.11 | 20.11 | 20.11 | 20.15 | 20.32 | 20.30 | 20.11 | 20.12 |

| 20 | 20.97 | 20.48 | 20.51 | 20.54 | 20.54 | 20.51 | 20.49 | 20.48 | 20.49 | 20.62 | 20.60 | 20.49 | 20.48 |

| 21 | 21.46 | 21.00 | 21.03 | 21.07 | 21.07 | 21.03 | 21.02 | 21.00 | 21.00 | 21.11 | 21.10 | 21.01 | 21.00 |

| 15.34 | 14.92 | 14.93 | 14.96 | 14.96 | 14.93 | 14.92 | 14.92 | 14.93 | 15.04 | 15.02 | 14.92 | 14.92 |

2.2 Seasonal adjustment model

2.2.1 Standard seassonal adjustment model

We consider here the seasonal adjustment model for the blsallhood data (Buleau of Labor Statistics, all food data, N=156, Kitagawa (2020)),

| (30) |

where and are the trend and the seasonal components that follow

| (31) |

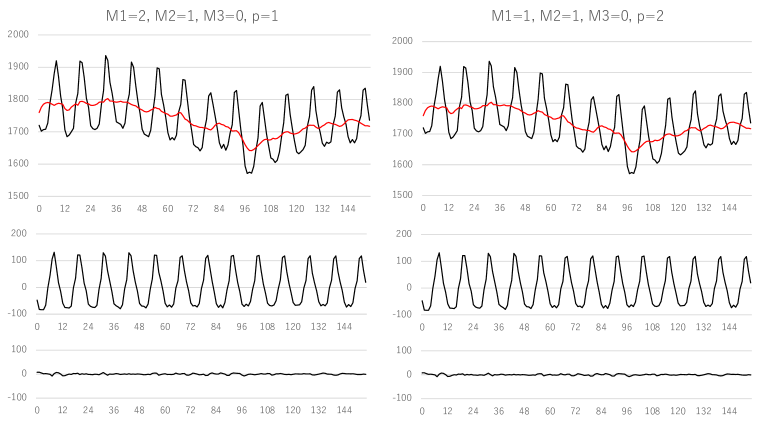

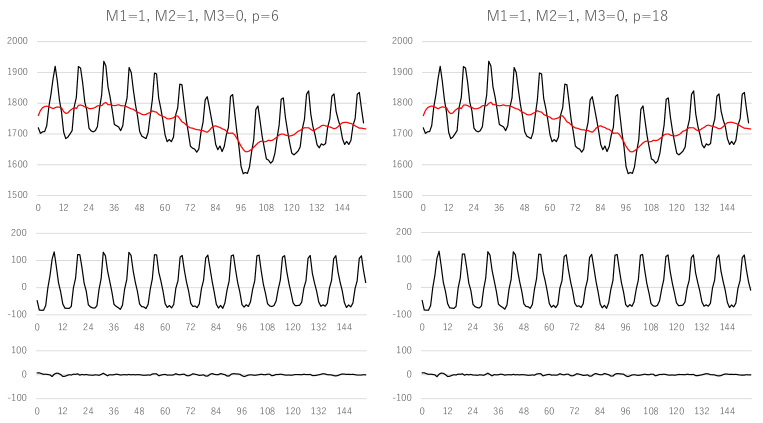

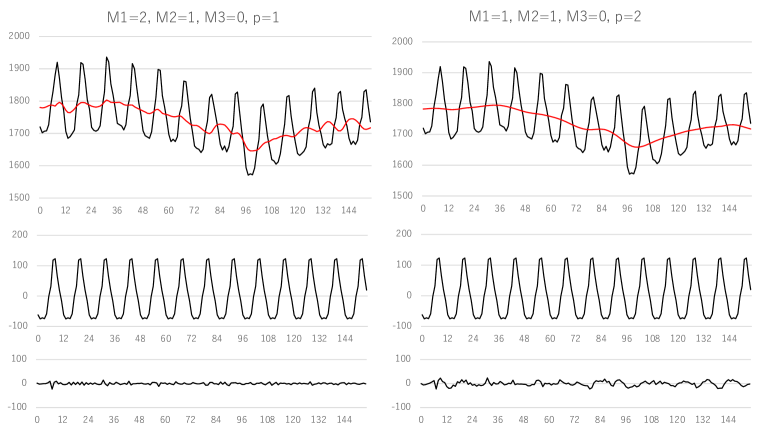

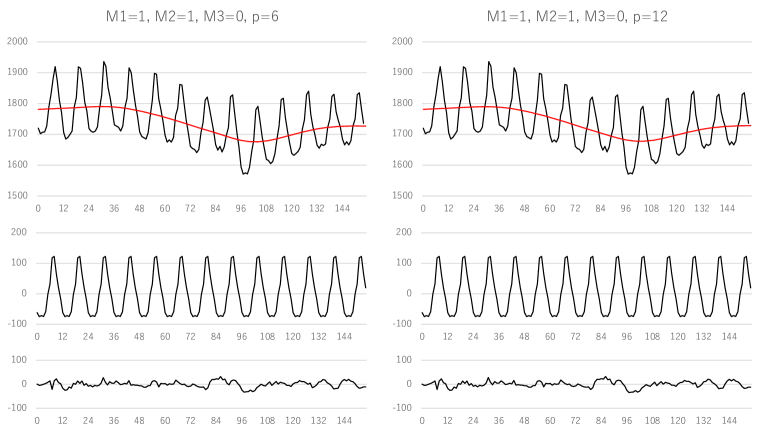

Figure 4 shows the decomposition of the data into trend, seasonal component and the observation noise. The left plot shows the case of the maximum likelihood estimate, i.e., obtained by . The right plot is the case of . It can be seen that compared with the standard results obtained by the maximum likelihood estimates, the estimated trend by =2 is smoother. Similarly, Figure 5 show the cases of =6 and 12. In these cases, the trend become further smoother. No significan difference is seen between the results of =6 and 12. The seasonal components are almost the same for all cases, and the observation noise components of and are almost identical.

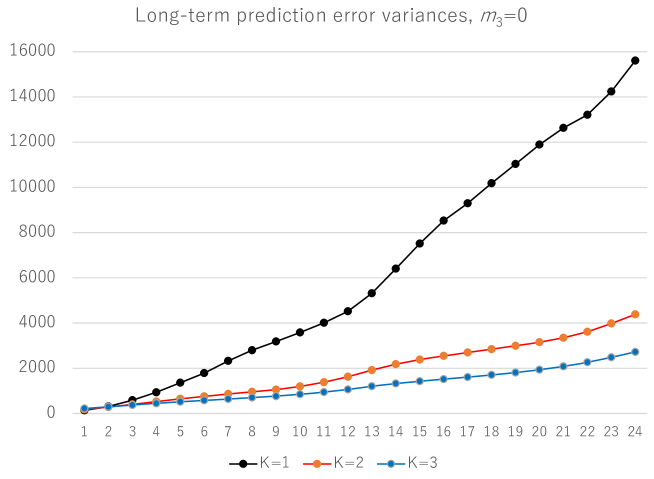

Table 3 shows the increasing horaizon prediction error variances of the seasonal adjustment model obtained with . In this case, the one-step-ahead prediction error variance of the maximum likelihood estiamte, obtained by , is 133 and is significantly smaller than other . This indicates that the maximum likelihood estimate has siginificantly better one-step-ahead prediction performance than the other . However, the increase of the variance for increasing prediction horaizon is significant and takes the largest long-term prediction variances for among all prediction horizon . For the prediction error varainces take similar values for entire . The last row of the table shows the average of the over for . This averaged prediction error variance is significantly large for =1 and takes similar values for . Note that this table suggests that if the increasing horaizon prediction is necessary it is very likely that we can obtain a good prediction performance by taking =6 or larger.

| 1 | 2 | 3 | 4 | 5 | 6 | 8 | 10 | 12 | 14 | 16 | 18 | 20 | 22 | 24 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 133 | 176 | 217 | 229 | 237 | 240 | 243 | 246 | 253 | 256 | 254 | 250 | 247 | 246 | 246 |

| 2 | 311 | 281 | 293 | 300 | 306 | 308 | 311 | 314 | 319 | 322 | 320 | 317 | 314 | 314 | 314 |

| 3 | 585 | 401 | 370 | 373 | 376 | 378 | 379 | 381 | 386 | 388 | 387 | 384 | 382 | 381 | 381 |

| 4 | 936 | 525 | 445 | 442 | 443 | 444 | 445 | 446 | 449 | 451 | 450 | 448 | 446 | 446 | 446 |

| 5 | 1359 | 646 | 516 | 507 | 506 | 506 | 507 | 507 | 510 | 511 | 511 | 509 | 508 | 507 | 507 |

| 6 | 1786 | 754 | 578 | 565 | 563 | 562 | 562 | 563 | 565 | 566 | 566 | 564 | 563 | 563 | 563 |

| 7 | 2324 | 863 | 641 | 624 | 620 | 619 | 619 | 619 | 621 | 622 | 622 | 620 | 619 | 619 | 619 |

| 8 | 2797 | 956 | 700 | 679 | 674 | 673 | 673 | 673 | 675 | 676 | 676 | 674 | 673 | 673 | 673 |

| 9 | 3183 | 1053 | 763 | 739 | 733 | 732 | 731 | 731 | 733 | 734 | 734 | 732 | 731 | 731 | 731 |

| 10 | 3582 | 1194 | 846 | 816 | 808 | 806 | 805 | 804 | 806 | 807 | 806 | 805 | 804 | 804 | 804 |

| 11 | 4010 | 1381 | 944 | 905 | 894 | 891 | 889 | 888 | 888 | 889 | 888 | 888 | 888 | 888 | 888 |

| 12 | 4520 | 1624 | 1062 | 1012 | 996 | 991 | 988 | 986 | 985 | 985 | 985 | 985 | 986 | 986 | 986 |

| 13 | 5317 | 1917 | 1203 | 1141 | 1122 | 1116 | 1112 | 1109 | 1106 | 1106 | 1106 | 1107 | 1108 | 1109 | 1109 |

| 14 | 6402 | 2179 | 1324 | 1252 | 1229 | 1222 | 1217 | 1213 | 1209 | 1209 | 1209 | 1210 | 1212 | 1213 | 1213 |

| 15 | 7515 | 2381 | 1425 | 1347 | 1323 | 1315 | 1310 | 1306 | 1302 | 1301 | 1302 | 1303 | 1305 | 1306 | 1306 |

| 16 | 8530 | 2548 | 1517 | 1436 | 1411 | 1403 | 1398 | 1394 | 1391 | 1391 | 1391 | 1392 | 1394 | 1394 | 1394 |

| 17 | 9296 | 2695 | 1607 | 1526 | 1502 | 1494 | 1489 | 1486 | 1484 | 1484 | 1484 | 1484 | 1485 | 1486 | 1486 |

| 18 | 10184 | 2844 | 1703 | 1621 | 1597 | 1590 | 1586 | 1583 | 1582 | 1584 | 1583 | 1582 | 1583 | 1583 | 1583 |

| 19 | 11034 | 2990 | 1809 | 1727 | 1704 | 1697 | 1694 | 1692 | 1692 | 1694 | 1693 | 1691 | 1691 | 1692 | 1692 |

| 20 | 11893 | 3152 | 1933 | 1849 | 1827 | 1821 | 1817 | 1816 | 1818 | 1821 | 1820 | 1817 | 1816 | 1816 | 1816 |

| 21 | 12633 | 3347 | 2080 | 1993 | 1969 | 1963 | 1960 | 1959 | 1962 | 1966 | 1964 | 1960 | 1959 | 1959 | 1959 |

| 22 | 13210 | 3612 | 2262 | 2166 | 2140 | 2133 | 2129 | 2128 | 2131 | 2134 | 2133 | 2129 | 2128 | 2128 | 2128 |

| 23 | 14240 | 3978 | 2482 | 2371 | 2339 | 2330 | 2326 | 2323 | 2324 | 2328 | 2326 | 2323 | 2323 | 2323 | 2323 |

| 24 | 15605 | 4383 | 2721 | 2592 | 2554 | 2543 | 2537 | 2533 | 2532 | 2534 | 2533 | 2531 | 2532 | 2533 | 2533 |

| 6308 | 1912 | 1227 | 1176 | 1161 | 1157 | 1155 | 1154 | 1155 | 1157 | 1156 | 1154 | 1154 | 1154 | 1154 |

Figure 6 shows the changes of increasing horizon prediction of the seasonal adjustment model for 1, 2 and 3. The curves for are visually indistiguishable from the curve for . From this figure, we can see that by using a greater than 2, the long-term prediction error variance can be reduced, instead of increasing the one-step-ahead prediction error variance .

We also considered the increasing-horizon prediction performance of the seasonal adjustment model with the first order trend model

| (32) |

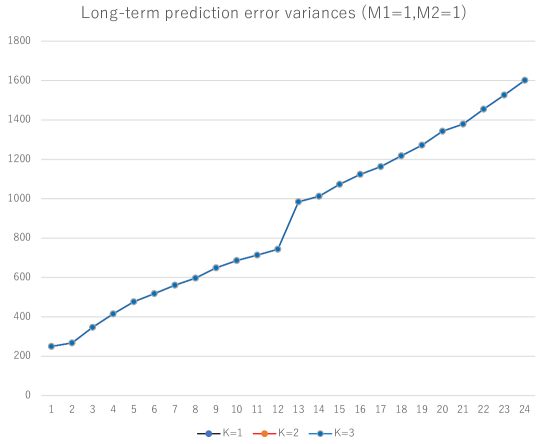

Unlike the previous case of the seasonal adjustment with the second order trend model, similarly to the case of first order trend model, the increasing horaizon prediction results are almost the same for entire . However, for and 16, the prediction error variances are larger than other cases. It is probable that the problem of optimization cased this anomalous phenomenon.

2.2.2 Seasonal adjustment model with AR component

Table 4 shows the long-term prediction error variances when we used the seasonal adjustment model with stationary AR component (Kitagawa and Gersch (1974), Kitagawa (2020)):

| (33) |

where is the stationary AR components that follows an AR model with order ,

| (34) |

. Compared with the Table 3 for the standard seasonal adjustment model without AR component, the one-step-ahead prediction error variance is smaller and the increase of the long-term prediction error variance for large is moderate, and no noticable changes are seen by the change of the prediction horaizon . The bottom row of the table shows that the minimum of the averaged prediction-error-variance is attained at . It can be seen that the averaged prediction error variaces are almost the same for , and then takes the smallest value at , and takes slightly larger values for and 24. The table also shows that, compared with the ordinary seasonal adjustment model, the seasonal adjustment model with AR component has high prediction performance over entire prediction horizon, .

| 1 | 2 | 3 | 4 | 5 | 6 | 8 | 10 | 12 | 14 | 16 | 18 | 20 | 22 | 24 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 102 | 102 | 102 | 102 | 102 | 102 | 184 | 184 | 184 | 184 | 184 | 184 | 184 | 184 | 184 |

| 2 | 187 | 187 | 187 | 187 | 187 | 188 | 209 | 209 | 209 | 209 | 209 | 209 | 209 | 210 | 210 |

| 3 | 281 | 281 | 281 | 281 | 281 | 282 | 336 | 336 | 336 | 336 | 336 | 336 | 336 | 336 | 336 |

| 4 | 369 | 369 | 369 | 369 | 370 | 370 | 368 | 368 | 368 | 368 | 368 | 368 | 368 | 370 | 370 |

| 5 | 455 | 455 | 455 | 455 | 454 | 454 | 457 | 457 | 457 | 457 | 457 | 457 | 457 | 459 | 459 |

| 6 | 517 | 517 | 517 | 516 | 516 | 516 | 484 | 484 | 484 | 484 | 484 | 484 | 484 | 488 | 488 |

| 7 | 590 | 590 | 590 | 589 | 587 | 586 | 547 | 547 | 547 | 547 | 547 | 547 | 547 | 551 | 551 |

| 8 | 643 | 644 | 643 | 643 | 639 | 637 | 569 | 569 | 569 | 569 | 569 | 569 | 569 | 574 | 574 |

| 9 | 682 | 683 | 682 | 682 | 677 | 675 | 622 | 622 | 622 | 622 | 622 | 622 | 622 | 627 | 627 |

| 10 | 734 | 734 | 734 | 733 | 730 | 727 | 658 | 658 | 658 | 658 | 658 | 658 | 658 | 666 | 666 |

| 11 | 793 | 793 | 792 | 792 | 790 | 788 | 740 | 740 | 740 | 740 | 740 | 740 | 740 | 746 | 746 |

| 12 | 878 | 879 | 878 | 878 | 878 | 877 | 805 | 805 | 805 | 805 | 805 | 805 | 805 | 814 | 814 |

| 13 | 1002 | 1003 | 1002 | 1002 | 1002 | 1002 | 932 | 932 | 932 | 932 | 932 | 932 | 932 | 941 | 941 |

| 14 | 1133 | 1134 | 1133 | 1133 | 1131 | 1131 | 1003 | 1003 | 1003 | 1003 | 1003 | 1003 | 1003 | 1016 | 1016 |

| 15 | 1247 | 1248 | 1247 | 1247 | 1243 | 1243 | 1088 | 1088 | 1088 | 1088 | 1088 | 1088 | 1088 | 1102 | 1102 |

| 16 | 1349 | 1350 | 1349 | 1349 | 1344 | 1343 | 1139 | 1139 | 1139 | 1139 | 1139 | 1139 | 1139 | 1157 | 1157 |

| 17 | 1440 | 1442 | 1440 | 1440 | 1434 | 1433 | 1204 | 1204 | 1204 | 1204 | 1204 | 1204 | 1204 | 1222 | 1222 |

| 18 | 1538 | 1539 | 1538 | 1537 | 1530 | 1527 | 1258 | 1258 | 1258 | 1258 | 1258 | 1258 | 1258 | 1280 | 1280 |

| 19 | 1634 | 1635 | 1634 | 1633 | 1624 | 1621 | 1327 | 1327 | 1327 | 1327 | 1327 | 1327 | 1327 | 1349 | 1349 |

| 20 | 1737 | 1739 | 1737 | 1737 | 1727 | 1724 | 1392 | 1392 | 1392 | 1392 | 1392 | 1392 | 1392 | 1417 | 1417 |

| 21 | 1842 | 1843 | 1842 | 1841 | 1833 | 1830 | 1479 | 1479 | 1479 | 1479 | 1479 | 1479 | 1479 | 1504 | 1504 |

| 22 | 1959 | 1959 | 1958 | 1958 | 1953 | 1951 | 1569 | 1569 | 1569 | 1569 | 1569 | 1569 | 1569 | 1597 | 1597 |

| 23 | 2135 | 2136 | 2134 | 2134 | 2131 | 2128 | 1689 | 1689 | 1689 | 1689 | 1689 | 1689 | 1689 | 1717 | 1717 |

| 24 | 2359 | 2360 | 2358 | 2358 | 2352 | 2350 | 1801 | 1800 | 1800 | 1800 | 1800 | 1800 | 1800 | 1832 | 1832 |

| 1067 | 1068 | 1067 | 1066 | 1063 | 1062 | 911 | 911 | 911 | 911 | 911 | 911 | 911 | 923 | 923 |

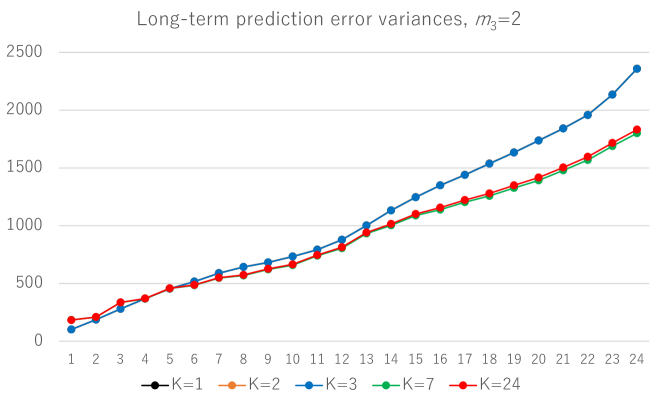

Figure 7 show the long-term prediction error variances for and 24. The curves for , 2 and 3 are visually indistinguishable. The curve for is slightly larger than that obtained by .

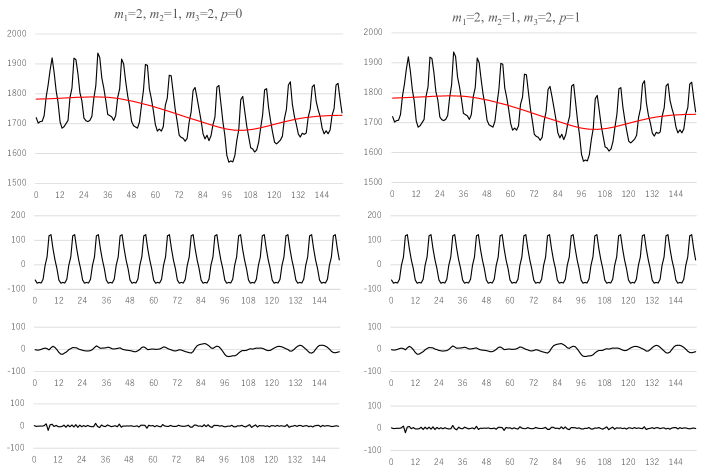

Figure 8 shows the decomposition of the time series into the trend, sesonal component, the AR component and the observation noise obtained by (left plot) and (right plot), respectively. This suggests that by selecting a value larger than 1, it is very likely to obtain a model that has high increasing horizon prediction performance. The results are indistinguishable.

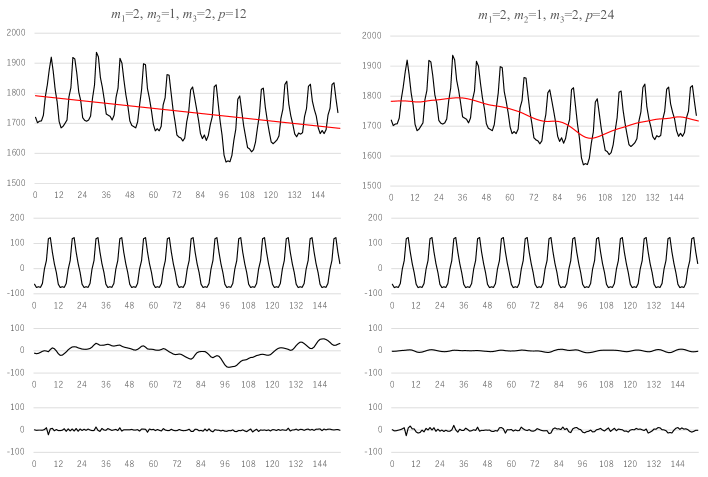

On the other hand, Figure 9 shows the cases obtained by (left plot) and 12 (right plot). For , the trend became a straight line and instead the AR component contains a drift. For , the trend is slightly more variable than the trend by or 2 and the AR component becomes very small.

From our expectation to the trend component, these estimate obtained by is a bit odd. However, this estiamte has high increasing-horizon prediction performance.

3 Concluding Remarks

By the three examples, it can be seen that by specifying the prediction horizon p of the modified log-likelihood larger than 1, we can get a good long-term prediction performance. The third example suggests that the seasonal adjustment model with AR component has resonable long-term prediction performance even with . This is probablly because the AR component can adapt to the local variation and increse the short-term prediction performance, but it does not diteriorate the long-term prediction because the prediction by stationary AR model converges to zero for large lead time.

Aknowledgements

This work was supported in part by JSPS KAKENHI Grant Number 18H03210.

References

- [1] Akaike, H. (1974). “A new look at the statistical model identification”. IEEE transactions on automatic control, 19(6), 716–723.

- [2] Akaike, H. (1980), “Seasonal adjustment by a Bayesian modeling”, J. Time Series Anal., 1, 1–13.

- [3] Anderson, B. D. O, and Moore, J. B. (2012). Optimal filtering. DOver Publications, New York.

- [4] Judd, K., and Small, M. (2000). “Towards long-term prediction”. Physica D: Nonlinear Phenomena, 136(1-2), 31–44.

- [5] Kitagawa, G. (1989). Non-Gaussian seasonal adjustment, Computers & Mathematics with Applications, Vol.18, No.6/7, pp. 503–514.

- [6] Kitagawa, G. (2020). Introduction to Time Series Modeling with Applications in R, Monographs on Statistics and Applied Probability 166, CRD Press, Chapman & Hall, New York.

- [7] Kitagawa, G. and Gersch, W. (1984), “A smoothness priors-state space modeling of time series with trend and seasonality”, J. Amer. Statist. Assoc., 79, 378–389.

- [8] Kitagawa, G. and Gersch, W. (1996), Smoothness Priors Analysis of Time Series, Lecture Notes in Statistics, 116, Springer, New York.

- [9] Konishi, S. and Kitagawa, G. (2008), Information Criteria and Statistical Modeling, Springer Series in Statistics, pp-273, Springer, New York.

- [10] Sorjamaa, A., Hao, J., Reyhani, N., Ji, Y., and Lendasse, A. (2007). “Methodology for long-term prediction of time series”. Neurocomputing, 70(16-18), 2861–2869.

- [11] Xiong, T., Bao, Y., and Hu, Z. (2013). “Beyond one-step-ahead forecasting: evaluation of alternative multi-step-ahead forecasting models for crude oil prices”. Energy Economics, 40, 405–415.

Appendix: Seasonal Adjustment Model with the First Order Trend Model

| 1 | 2 | 3 | 4 | 5 | 6 | 8 | 10 | 12 | 14 | 16 | 18 | 20 | 22 | 24 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 250 | 250 | 250 | 250 | 250 | 250 | 250 | 250 | 250 | 264 | 254 | 250 | 250 | 250 | 250 |

| 2 | 268 | 268 | 268 | 268 | 268 | 268 | 269 | 268 | 268 | 288 | 275 | 268 | 268 | 268 | 268 |

| 3 | 347 | 347 | 347 | 347 | 347 | 347 | 348 | 347 | 347 | 365 | 354 | 347 | 347 | 347 | 347 |

| 4 | 415 | 415 | 415 | 415 | 415 | 415 | 416 | 415 | 415 | 431 | 422 | 415 | 415 | 415 | 415 |

| 5 | 477 | 477 | 477 | 477 | 477 | 477 | 478 | 477 | 477 | 490 | 482 | 477 | 477 | 477 | 477 |

| 6 | 518 | 518 | 518 | 518 | 518 | 518 | 519 | 518 | 518 | 531 | 523 | 518 | 518 | 518 | 518 |

| 7 | 561 | 561 | 561 | 561 | 561 | 561 | 561 | 561 | 561 | 571 | 564 | 561 | 561 | 561 | 561 |

| 8 | 597 | 597 | 597 | 597 | 597 | 597 | 597 | 597 | 597 | 604 | 598 | 597 | 597 | 597 | 597 |

| 9 | 649 | 649 | 649 | 649 | 649 | 649 | 649 | 649 | 649 | 660 | 652 | 649 | 649 | 649 | 649 |

| 10 | 686 | 686 | 686 | 686 | 686 | 686 | 687 | 686 | 686 | 700 | 691 | 686 | 686 | 686 | 686 |

| 11 | 714 | 714 | 714 | 714 | 714 | 714 | 715 | 714 | 714 | 731 | 721 | 714 | 714 | 714 | 714 |

| 12 | 743 | 744 | 744 | 744 | 744 | 744 | 745 | 744 | 744 | 760 | 750 | 744 | 744 | 744 | 744 |

| 13 | 984 | 984 | 984 | 984 | 984 | 984 | 981 | 984 | 984 | 968 | 973 | 984 | 984 | 984 | 984 |

| 14 | 1012 | 1012 | 1012 | 1012 | 1012 | 1012 | 1010 | 1012 | 1012 | 1000 | 1003 | 1012 | 1012 | 1012 | 1012 |

| 15 | 1073 | 1073 | 1073 | 1073 | 1073 | 1073 | 1071 | 1073 | 1073 | 1065 | 1067 | 1073 | 1073 | 1073 | 1073 |

| 16 | 1124 | 1124 | 1124 | 1124 | 1124 | 1124 | 1123 | 1124 | 1124 | 1124 | 1121 | 1124 | 1124 | 1124 | 1124 |

| 17 | 1163 | 1163 | 1163 | 1163 | 1163 | 1163 | 1163 | 1163 | 1163 | 1173 | 1166 | 1163 | 1163 | 1163 | 1163 |

| 18 | 1218 | 1218 | 1218 | 1218 | 1218 | 1218 | 1219 | 1218 | 1218 | 1235 | 1223 | 1218 | 1218 | 1218 | 1218 |

| 19 | 1272 | 1272 | 1272 | 1272 | 1272 | 1272 | 1273 | 1272 | 1272 | 1292 | 1278 | 1272 | 1272 | 1272 | 1272 |

| 20 | 1343 | 1343 | 1343 | 1343 | 1343 | 1343 | 1344 | 1343 | 1343 | 1365 | 1350 | 1343 | 1343 | 1343 | 1343 |

| 21 | 1379 | 1379 | 1379 | 1379 | 1379 | 1379 | 1382 | 1379 | 1379 | 1415 | 1393 | 1379 | 1379 | 1379 | 1379 |

| 22 | 1455 | 1455 | 1455 | 1455 | 1455 | 1455 | 1459 | 1455 | 1455 | 1496 | 1472 | 1455 | 1455 | 1455 | 1455 |

| 23 | 1527 | 1527 | 1527 | 1527 | 1527 | 1527 | 1531 | 1527 | 1527 | 1570 | 1546 | 1527 | 1527 | 1527 | 1527 |

| 24 | 1601 | 1601 | 1601 | 1601 | 1601 | 1601 | 1604 | 1601 | 1601 | 1637 | 1616 | 1601 | 1601 | 1601 | 1601 |

| 891 | 891 | 891 | 891 | 891 | 891 | 891 | 891 | 891 | 906 | 896 | 891 | 891 | 891 | 891 |