FasterRisk: Fast and Accurate Interpretable Risk Scores

Abstract

Over the last century, risk scores have been the most popular form of predictive model used in healthcare and criminal justice. Risk scores are sparse linear models with integer coefficients; often these models can be memorized or placed on an index card. Typically, risk scores have been created either without data or by rounding logistic regression coefficients, but these methods do not reliably produce high-quality risk scores. Recent work used mathematical programming, which is computationally slow. We introduce an approach for efficiently producing a collection of high-quality risk scores learned from data. Specifically, our approach produces a pool of almost-optimal sparse continuous solutions, each with a different support set, using a beam-search algorithm. Each of these continuous solutions is transformed into a separate risk score through a “star ray” search, where a range of multipliers are considered before rounding the coefficients sequentially to maintain low logistic loss. Our algorithm returns all of these high-quality risk scores for the user to consider. This method completes within minutes and can be valuable in a broad variety of applications.

1 Introduction

Risk scores are sparse linear models with integer coefficients that predict risks. They are arguably the most popular form of predictive model for high stakes decisions through the last century and are the standard form of model used in criminal justice [4, 22] and medicine [19, 27, 34, 31, 41].

| 1. | Oval Shape | -2 points | |

| 2. | Irregular Shape | 4 points | |

| 3. | Circumscribed Margin | -5 points | |

| 4. | Spiculated Margin | 2 points | |

| 5. | Age 60 | 3 points | |

| SCORE |

| SCORE | -7 | -5 | -4 | -3 | -2 | -1 |

|---|---|---|---|---|---|---|

| RISK | 6.0% | 10.6% | 13.8% | 17.9% | 22.8% | 28.6% |

| SCORE | 0 | 1 | 2 | 3 | 4 | 5 |

| RISK | 35.2% | 42.4% | 50.0% | 57.6% | 64.8% | 71.4% |

Their history dates back to at least the criminal justice work of Burgess [8], where, based on their criminal history and demographics, individuals were assigned integer point scores between 0 and 21 that determined the probability of their “making good or of failing upon parole.” Other famous risk scores are arguably the most widely-used predictive models in healthcare. These include the APGAR score [3], developed in 1952 and given to newborns, and the CHADS2 score [18], which estimates stroke risk for atrial fibrillation patients. Figures 1 and 2 show example risk scores, which estimate risk of a breast lesion being malignant.

| 1. | Irregular Shape | 4 points | |

| 2. | Circumscribed Margin | -5 points | |

| 3. | SpiculatedMargin | 2 points | |

| 4. | Age 45 | 1 point | |

| 5. | Age 60 | 3 points | |

| SCORE |

| SCORE | -5 | -4 | -3 | -2 | -1 | 0 |

| RISK | 7.3% | 9.7% | 12.9% | 16.9% | 21.9% | 27.8% |

| SCORE | 1 | 2 | 3 | 4 | 5 | 6 |

| RISK | 34.6% | 42.1% | 50.0% | 57.9% | 65.4% | 72.2% |

Risk scores have the benefit of being easily memorized; usually their names reveal the full model – for instance, the factors in CHADS2 are past Chronic heart failure, Hypertension, Age75 years, Diabetes, and past Stroke (where past stroke receives 2 points and the others each receive 1 point). For risk scores, counterfactuals are often trivial to compute, even without a calculator. Also, checking that the data and calculations are correct is easier with risk scores than with other approaches. In short, risk scores have been created by humans for a century to support a huge spectrum of applications [2, 23, 30, 43, 44, 47], because humans find them easy to understand.

Traditionally, risk scores have been created in two main ways: (1) without data, with expert knowledge only (and validated only afterwards on data), and (2) using a semi-manual process involving manual feature selection and rounding of logistic regression coefficients. That is, these approaches rely heavily on domain expertise and rely little on data. Unfortunately, the alternative of building a model directly from data leads to computationally hard problems: optimizing risk scores over a global objective on data is NP-hard, because in order to produce integer-valued scores, the feasible region must be the integer lattice. There have been only a few approaches to design risk scores automatically [5, 6, 9, 10, 16, 32, 33, 38, 39, 40], but each of these has a flaw that limits its use in practice: the optimization-based approaches use mathematical programming solvers (which require a license) that are slow and scale poorly, and the other methods are randomized greedy algorithms, producing fast but much lower-quality solutions. We need an approach that exhibits the best of both worlds: speed fast enough to operate in a few minutes on a laptop and optimization/search capability as powerful as that of the mathematical programming tools. Our method, FasterRisk, lies at this intersection. It is fast enough to enable interactive model design and can rapidly produce a large pool of models from which users can choose rather than producing only a single model.

One may wonder why simple rounding of -regularized logistic regression coefficients does not yield sufficiently good risk scores. Past works [37, 39] explain this as follows: the sheer amount of regularization needed to get a very sparse solution leads to large biases and worse loss values, and rounding goes against the performance gradient. For example, consider the following coefficients from regularization: [1.45, .87, .83, .47, .23, .15, … ]. This model is worse than its unregularized counterpart due to the bias induced by the large term. Its rounded solution is [1,1,1,0,0,0,..], which leads to even worse loss. Instead, one could multiply all the coefficients by a constant and then round, but which constant is best? There are an infinite number of choices. Even if some value of the multiplier leads to minimal loss due to rounding, the bias from the term still limits the quality of the solution.

The algorithm presented here does not have these disadvantages. The steps are: (1) Fast subset search with optimization (avoiding the bias from ). This requires the solution of an NP-hard problem, but our fast subset selection algorithm is able to solve this quickly. We proceed from this accurate sparse continuous solution, preserving both sparseness and accuracy in the next steps. (2) Find a pool of diverse continuous sparse solutions that are almost as good as the solution found in (1) but with different support sets. (3) A “star ray” search, where we search for feasible integer-valued solutions along multipliers of each item in the pool from (2). By using multipliers, the search space resembles the rays of a star, because it extends each coefficient in the pool outward from the origin to search for solutions. To find integer solutions, we perform a local search (a form of sequential rounding). This method yields high performance solutions: we provide a theoretical upper bound on the loss difference between the continuous sparse solution and the rounded integer sparse solution.

Through extensive experiments, we show that our proposed method is computationally fast and produces high-quality integer solutions. This work thus provides valuable and novel tools to create risk scores for professionals in many different fields, such as healthcare, finance, and criminal justice.

Contributions: Our contributions include the three-step framework for producing risk scores, a beam-search-based algorithm for logistic regression with bounded coefficients (for Step 1), the search algorithm to find pools of diverse high-quality continuous solutions (for Step 2), the star ray search technique using multipliers (Step 3), and a theorem guaranteeing the quality of the star ray search.

2 Related Work

Optimization-based approaches: Risk scores, which model , are different from threshold classifiers, which predict either or given . Most work in the area of optimization of integer-valued sparse linear models focuses on classifiers, not risk scores [5, 6, 9, 32, 33, 37, 40, 46]. This difference is important, because a classifier generally cannot be calibrated well for use in risk scoring: only its single decision point is optimized. Despite this, several works use the hinge loss to calibrate predictions [6, 9, 32]. All of these optimization-based algorithms use mathematical programming solvers (i.e., integer programming solvers), which tend to be slow and cannot be used on larger problems. However, they can handle both feature selection and integer constraints.

To directly optimize risk scores, typically the logistic loss is used. The RiskSLIM algorithm [39] optimizes the logistic loss regularized with regularization, subject to integer constraints on the coefficients. RiskSLIM uses callbacks to a MIP solver, alternating between solving linear programs and using branch-and-cut to divide and reduce the search space. The branch-and-cut procedure needs to keep track of unsolved nodes, whose number increases exponentially with the size of the feature space. Thus, RiskSLIM’s major challenge is scalability.

Local search-based approaches: As discussed earlier, a natural way to produce a scoring system or risk score is by selecting features manually and rounding logistic regression coefficients or hinge-loss solutions to integers [10, 11, 39]. While rounding is fast, rounding errors can cause the solution quality to be much worse than that of the optimization-based approaches. Several works have proposed improvements over traditional rounding. In Randomized Rounding [10], each coefficient is rounded up or down randomly, based on its continuous coefficient value. However, randomized rounding does not seem to perform well in practice. Chevaleyre [10] also proposed Greedy Rounding, where coefficients are rounded sequentially. While this technique aimed to provide theoretical guarantees for the hinge loss, we identified a serious flaw in the argument, rendering the bounds incorrect (see Appendix B). The RiskSLIM paper [39] proposed SequentialRounding, which, at each iteration, chooses a coefficient to round up or down, making the best choice according to the regularized logistic loss. This gives better solutions than other types of rounding, because the coefficients are considered together through their performance on the loss function, not independently.

A drawback of SequentialRounding is that it considers rounding up or down only to the nearest integer from the continuous solution. By considering multipliers, we consider a much larger space of possible solutions. The idea of multipliers (i.e., “scale and round”) is used for medical scoring systems [11], though, as far as we know, it has been used only with traditional rounding rather than SequentialRounding, which could easily lead to poor performance, and we have seen no previous work that studies how to perform scale-and-round in a systematic, computationally efficient way. While the general idea of scale-and-round seems simple, it is not: there are an infinite number of possible multipliers, and, for each one, a number of possible nearby integer coefficient vectors that is the size of a hypercube, expanding exponentially in the search space.

Sampling Methods: The Bayesian method of Ertekin et al. [16] samples scoring systems, favoring those that are simpler and more accurate, according to a prior. “Pooling” [39] creates multiple models through sampling along the regularization path of ElasticNet. As discussed, when regularization is tuned high enough to induce sparse solutions, it results in substantial bias and low-quality solutions (see [37, 39] for numerous experiments on this point). Note that there is a literature on finding diverse solutions to mixed-integer optimization problems [e.g., 1], but it focuses only on linear objective functions.

3 Methodology

Define dataset (1 is a static feature corresponding to the intercept) and scaled dataset as , for a real-valued . Our goal is to produce high-quality risk scores within a few minutes on a small personal computer. We start with an optimization problem similar to RiskSLIM’s [39], which minimizes the logistic loss subject to sparsity constraints and integer coefficients:

| (1) | |||||

| such that |

In practice, the range of these box constraints is user-defined and can be different for each coefficient. (We use 5 for ease of exposition.) The sparsity constraint or integer constraints make the problem NP-hard, and this is a difficult mixed-integer nonlinear program. Transforming the original features to all possible dummy variables, which is a standard type of preprocessing [e.g., 24], changes the model into a (flexible) generalized additive model; such models can be as accurate as the best machine learning models [39, 42]. Thus, we generally process variables in to be binary.

To make the solution space substantially larger than , we use multipliers. The problem becomes:

Note that the use of multipliers does not weaken the interpretability of the risk score: the user still sees integer risk scores composed of values , . Only the risk conversion table is calculated differently, as where .

Input: dataset (consisting of feature matrix and labels ), sparsity constraint , coefficient constraint , beam search size , tolerance level , number of attempts , number of multipliers to try .

Output: a pool of scoring systems where is the index enumerating all found scoring systems with and and is the corresponding multiplier.

Our method proceeds in three steps, as outlined in Algorithm 1. In the first step, it approximately solves the following sparse logistic regression problem with a box constraint (but not integer constraints), detailed in Section 3.1 and Algorithm 2.

| (3) |

The algorithm gives an accurate and sparse real-valued solution .

The second step produces many near-optimal sparse logistic regression solutions, again without integer constraints, detailed in Section 3.2 and Algorithm 5. Algorithm 5 uses from the first step to find a set such that for all and a given threshold :

| (4) | |||

After these steps, we have a pool of almost-optimal sparse logistic regression models. In the third step, for each coefficient vector in the pool, we compute a risk score. It is a feasible integer solution to the following, which includes a positive multiplier :

where we derive a tight theoretical upper bound on . A detailed solution to (3) is shown in Algorithm 6 in Appendix A. We solve the optimization problem for a large range of multipliers in Algorithm 3 for each coefficient vector in the pool, choosing the best multiplier for each coefficient vector. This third step yields a large collection of risk scores, all of which are approximately as accurate as the best sparse logistic regression model that can be obtained. All steps in this process are fast and scalable.

Input: dataset , sparsity constraint , coefficient constraint , and beam search size .

Output: a sparse continuous coefficient vector with .

3.1 High-quality Sparse Continuous Solution

There are many different approaches for sparse logistic regression, including regularization [35], ElasticNet [48], regularization [13, 24], and orthogonal matching pursuit (OMP) [14, 25], but none of these approaches seem to be able to handle both the box constraints and the sparsity constraint in Problem 3, so we developed a new approach. This approach, in Algorithm 2, SparseBeamLR, uses beam search for best subset selection: each iteration contains several coordinate descent steps to determine whether a new variable should be added to the support, and it clips coefficients to the box as it proceeds. Hence the algorithm is able to determine, before committing to the new variable, whether it is likely to decrease the loss while obeying the box constraints. This beam search algorithm for solving (3) implicitly uses the assumption that one of the best models of size implicitly contains variables of one of the best models of size . This type of assumption has been studied in the sparse learning literature [14] (Theorem 5). However, we are not aware of any other work that applies box constraints or beam search for sparse logistic regression. In Appendix E, we show that our method produces better solutions than the OMP method presented in [14].

Algorithm 2 calls the ExpandSuppBy1 Algorithm, which has two major steps. The detailed algorithm can be found in Appendix A. For the first step, given a solution , we perform optimization on each single coordinate outside of the current support :

| (6) |

Vector is 1 for the th coordinate and 0 otherwise. We find for each through an iterative thresholding operation, which is done on all coordinates in parallel, iterating several () times:

| (7) |

where , and is a Lipschitz constant on coordinate [24]. Importantly, we can perform Equation 7 on all where in parallel using matrix form.

For the second step, after the parallel single coordinate optimization is done, we pick the top indices (’s) with the smallest logistic losses and fine tune on the new support:

| (8) |

This can be done again using a variant of Equation 7 iteratively on all the coordinates in the new support. We get pairs of through this ExpandSuppBy1 procedure, and the collection of these pairs form the set in Line 8 of Algorithm 2.

At the end, Algorithm 2 (SparseBeamLR) returns the best model with the smallest logistic loss found by the beam search procedure. This model satisfies both the sparsity and box constraints.

3.2 Collect Sparse Diverse Pool (Rashomon Set)

We now collect the sparse diverse pool. In Section 3.1, our goal was to find a sparse model with the smallest logistic loss. For high dimensional features or in the presence of highly correlated features, there could exist many sparse models with almost equally good performance [7]. This set of models is also known as the Rashomon set. Let us find those and turn them into risk scores. We first predefine a tolerance gap level (hyperparameter, usually set to ). Then, we delete a feature with index in the support and add a new feature with index . We select each new index to be whose logistic loss is within the tolerance gap:

| (9) |

We fine-tune the coefficients on each of the new supports and then save the new solution in our pool. Details can be found in Algorithm 5. Swapping one feature at a time is computationally efficient, and our experiments show it produces sufficiently diverse pools over many datasets. We call this method the CollectSparseDiversePool Algorithm.

3.3 “Star Ray” Search for Integer Solutions

The last challenge is how to get an integer solution from a continuous solution. To achieve this, we use a “star ray” search that searches along each “ray” of the star, extending each continuous solution outward from the origin using many values of a multiplier, as shown in Algorithm 3. The star ray search provides much more flexibility in finding a good integer solution than simple rounding. The largest multiplier is set to which will take one of the coefficients to the boundary of the box constraint at 5. We set the smallest multiplier to be 1.0 and pick (usually 20) equally spaced points from . If , we set to allow shrinkage of the coefficients. We scale the coefficients and datasets with each multiplier and round the coefficients to integers using the sequential rounding technique in Algorithm 6. For each continuous solution (each “ray” of the “star”), we report the integer solution and multiplier with the smallest logistic loss. This process yields our collection of risk scores. Note here that a standard line search along the multiplier does not work, because the rounding error is highly non-convex.

Input: dataset , a sparse continuous solution , coefficient constraint , and number of multipliers to try .

Output: a sparse integer solution with and multiplier .

We briefly discuss how the sequential rounding technique works. Details of this method can be found in Appendix A. We initialize . Then we round the fractional part of one coordinate at a time. At each step, some of the ’s are integer-valued (so is nonzero) and we pick the coordinate and rounding operation (either floor or ceil) based on which can minimize the following objective function, where we will round to an integer at coordinate :

| (10) | |||

where is the Lipschitz constant restricted to the rounding interval and can be computed as with if and otherwise. (The Lipschitz constant here is much smaller than the one in Section 3.1 due to the interval restriction.) After we select and find value , we update by setting . We repeat this process until is on the integer lattice: . The objective function in Equation 10 can be understood as an auxiliary upper bound of the logistic loss. Our algorithm provides an upper bound on the difference between the logistic losses of the continuous solution and the final rounded solution before we start the rounding algorithm (Theorem 3.1 below). Additionally, during the sequential rounding procedure, we do not need to perform expensive operations such as logarithms or exponentials as required by the logistic loss function; the bound and auxiliary function require only sums of squares, not logarithms or exponentials. Its derivation and proof are in Appendix C.

Theorem 3.1.

Let be the real-valued coefficients for the logistic regression model with objective function (the intercept is incorporated). Let be the integer-valued coefficients returned by the AuxiliaryLossRounding method. Furthermore, let . Let with if and otherwise. Then, we have an upper bound on the difference between the loss and the loss :

| (11) |

Note. Our method has a higher prediction capacity than RiskSLIM: its search space is much larger.

Compared to RiskSLIM, our use of the multiplier permits a number of solutions that grows exponentially in as we increase the multiplier. To see this, consider that for each support of features, since logistic loss is convex, it contains a hypersphere in coefficient space. The volume of that hypersphere is (as usual) where is the radius of the hypersphere. If we increase the multiplier to 2, the grid becomes finer by a factor of 2, which is equivalent to increasing the radius by a factor of 2. Thus, the volume increases by a factor of . In general, for maximum multiplier , the search space is increased by a factor of over RiskSLIM.

4 Experiments

We experimentally focus on two questions: (1) How good is FasterRisk’s solution quality compared to baselines? (§4.1) (2) How fast is FasterRisk compared with the state-of-the-art? (§4.2) In the appendix, we address three more questions: (3) How much do the sparse beam search, diverse pools, and multipliers contribute to our solution quality? (E.4) (4) How well-calibrated are the models produced by FasterRisk? (E.9) (5) How sensitive is FasterRisk to each of the hyperparameters in the algorithm? (E.10)

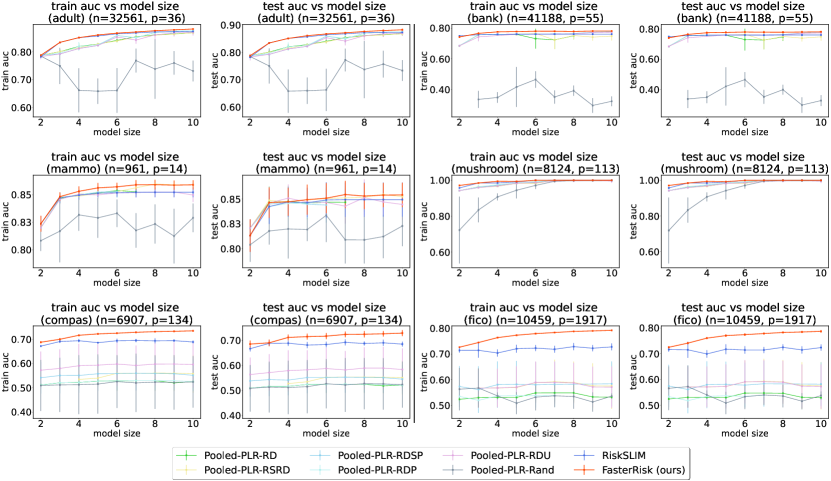

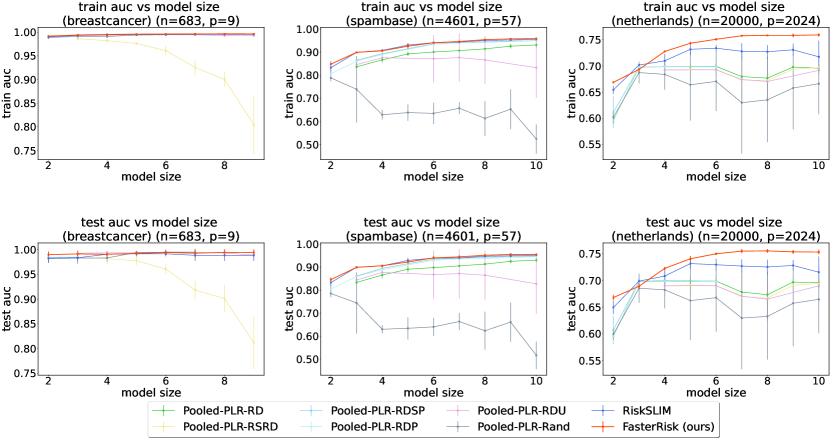

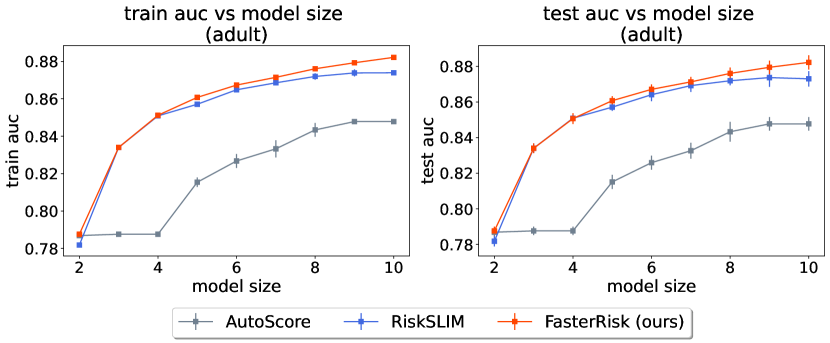

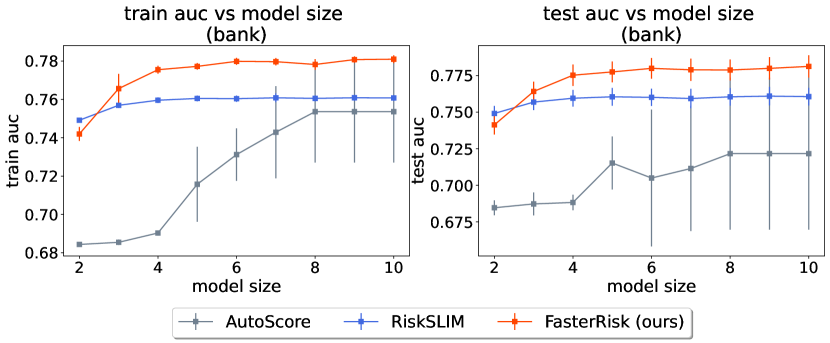

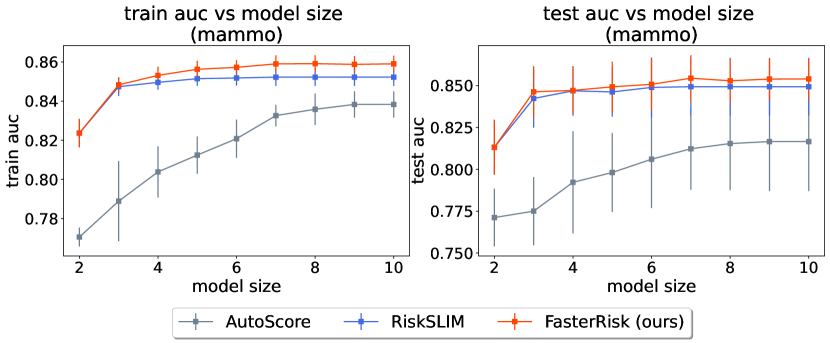

We compare with RiskSLIM (the current state-of-the-art), as well as algorithms Pooled-PLR-RD, Pooled-PLR-RSRD, Pooled-PRL-RDSP, Pooled-PLR-Rand and Pooled-PRL-RDP. These algorithms were all previously shown to be inferior to RiskSLIM [39]. These methods first find a pool of sparse continuous solutions using different regularizations of ElasticNet (hence the name “Pooled Penalized Logistic Regression” – Pooled-PLR) and then round the coefficients with different techniques. Details are in Appendix D.3. The best solution is chosen from this pool of integer solutions that obeys the sparsity and box constraints and has the smallest logistic loss. We also compare with the baseline AutoScore [44]. However, on some datasets, the results produced by AutoScore are so poor that they distort the AUC scale, so we show those results only in Appendix E.11. As there is no publicly available code for any of [10, 16, 32, 33], they do not appear in the experiments. For each dataset, we perform 5-fold cross validation and report training and test AUC. Appendix D presents details of the datasets, experimental setup, evaluation metrics, loss values, and computing platform/environment. More experimental results appear in Appendix E.

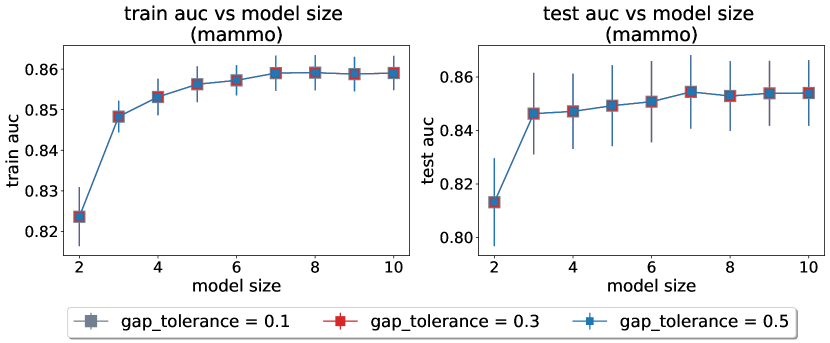

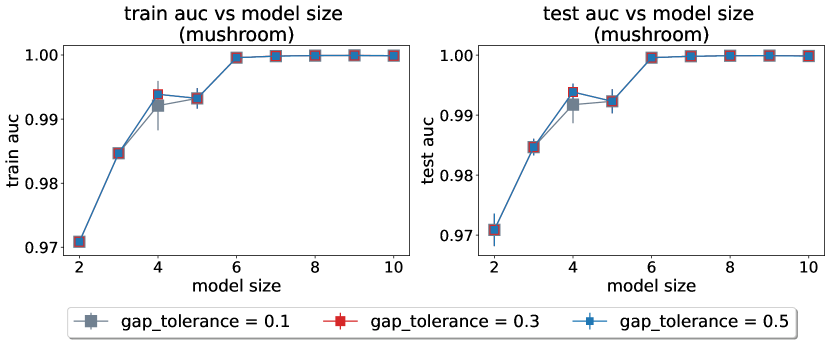

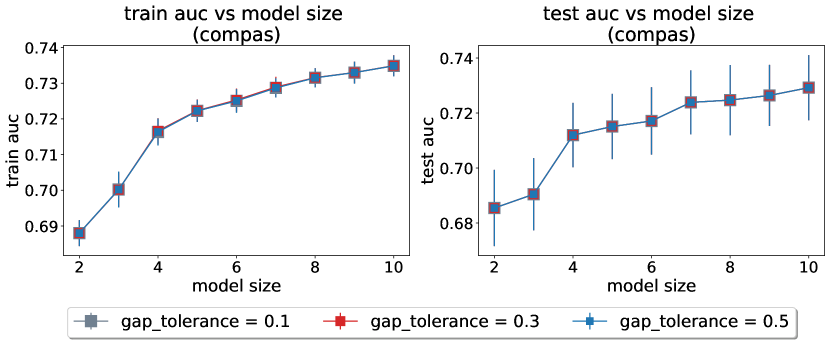

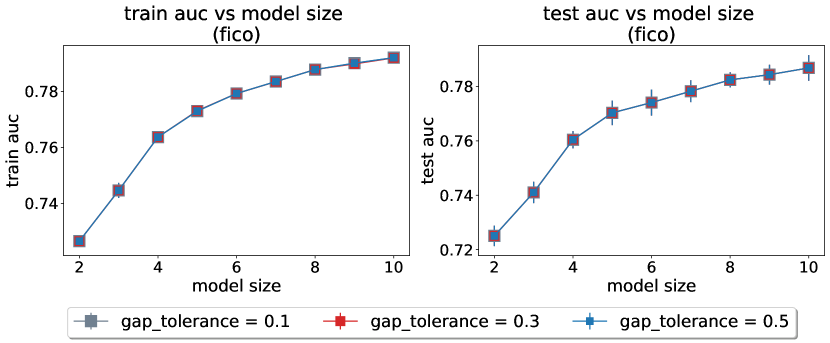

4.1 Solution Quality

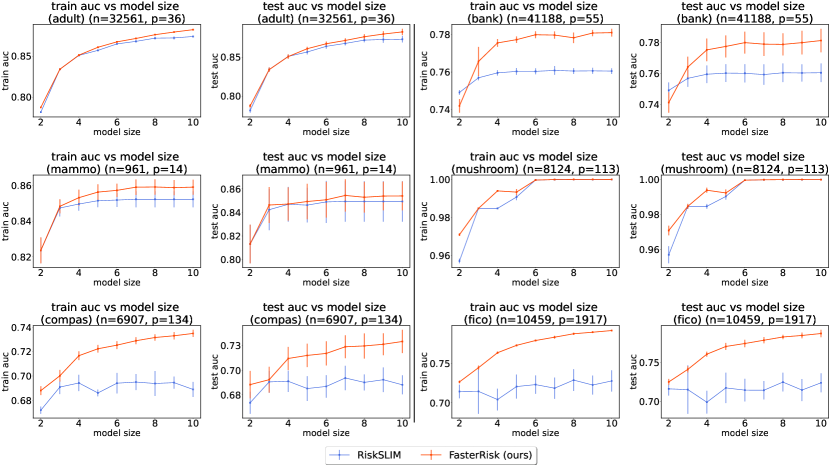

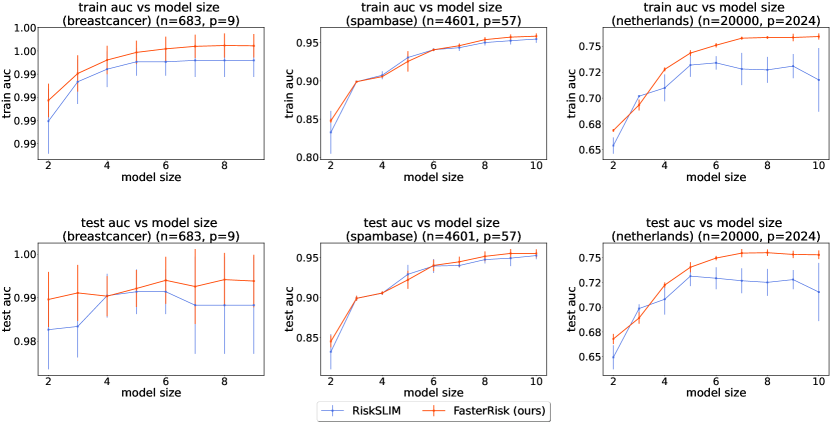

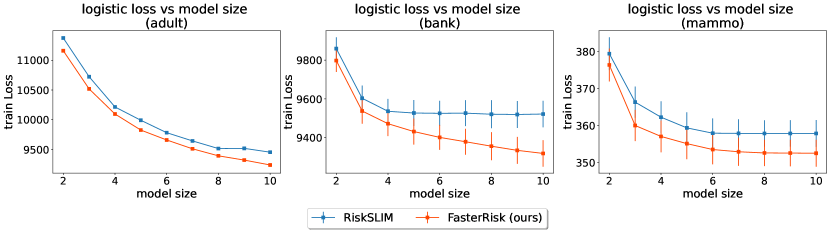

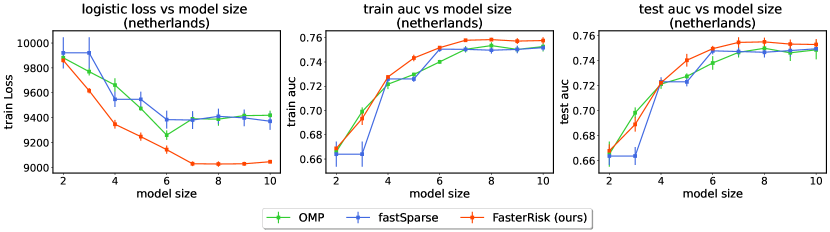

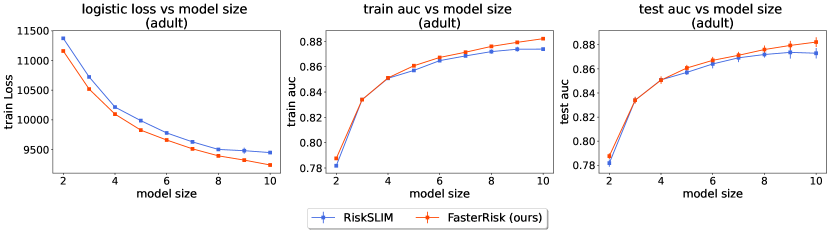

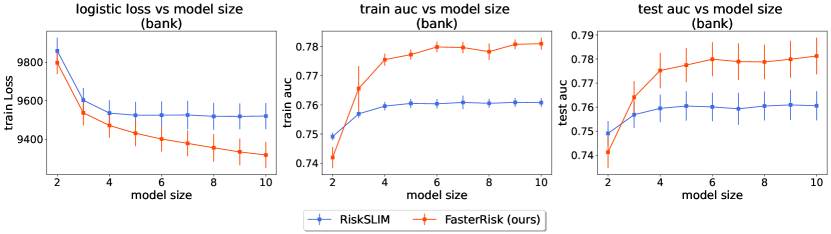

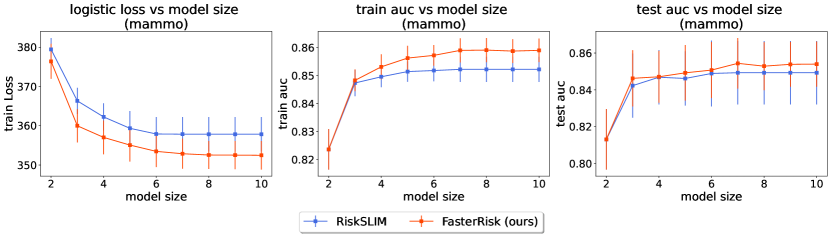

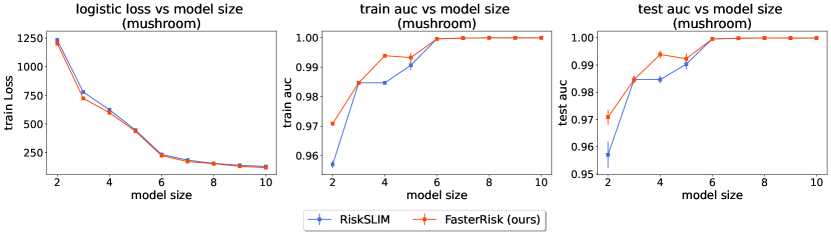

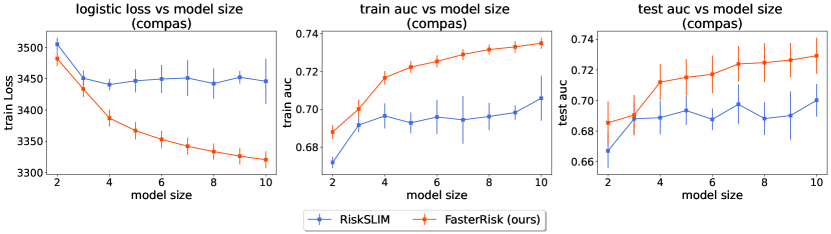

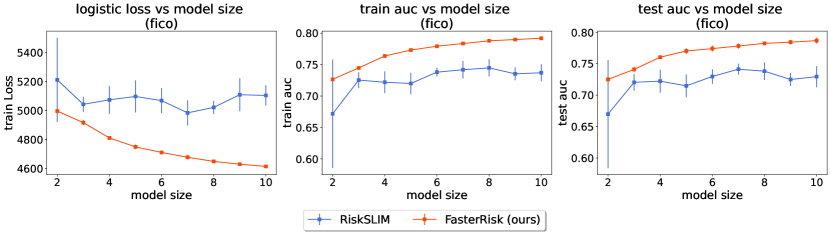

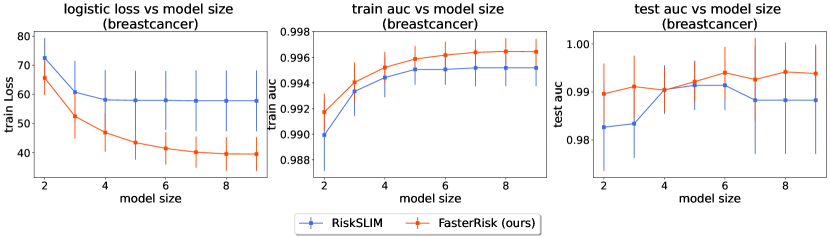

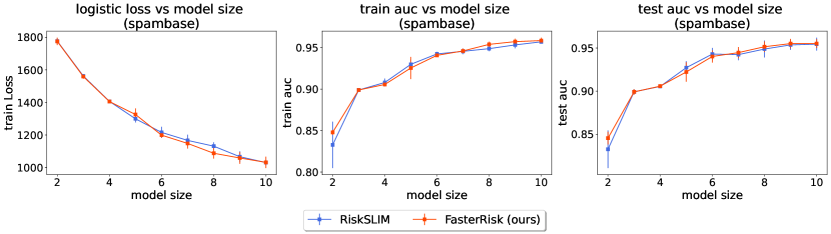

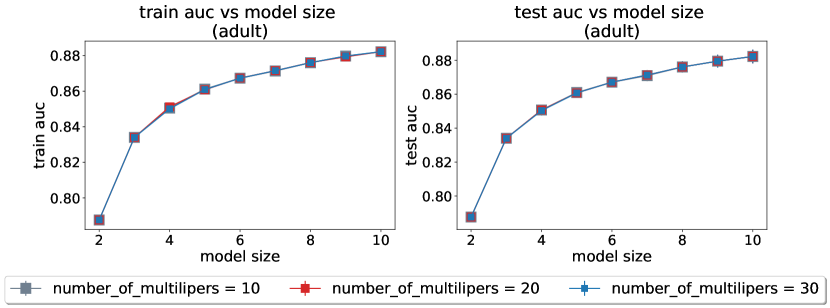

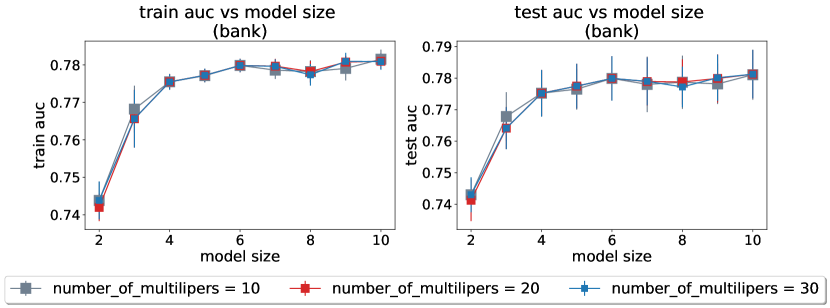

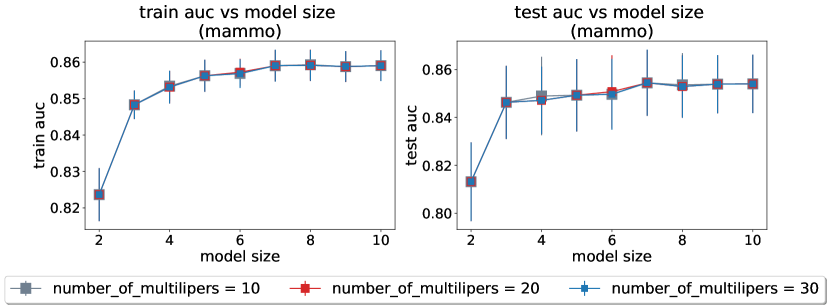

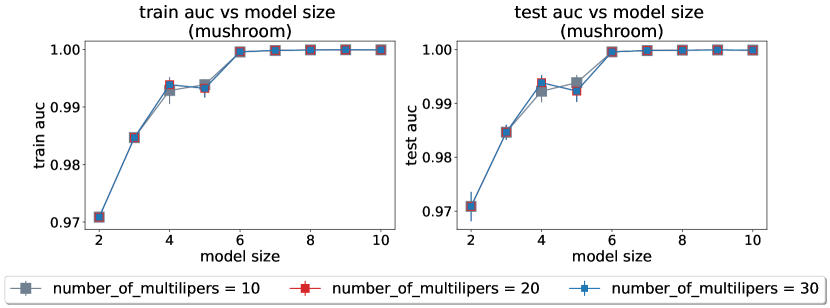

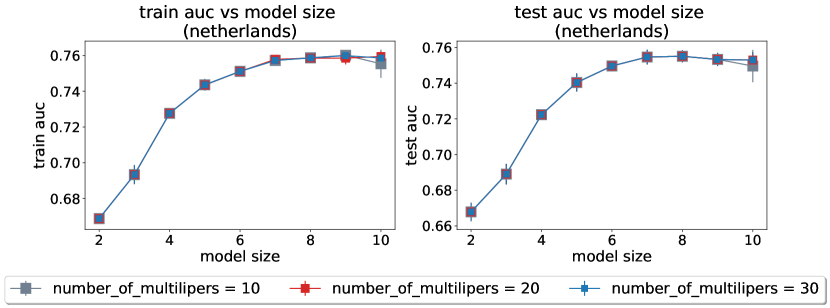

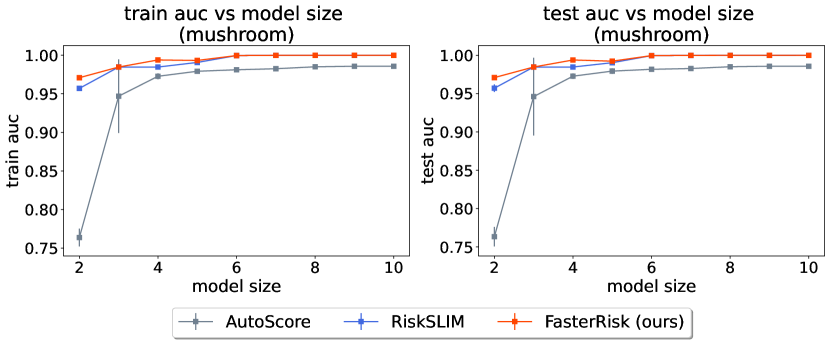

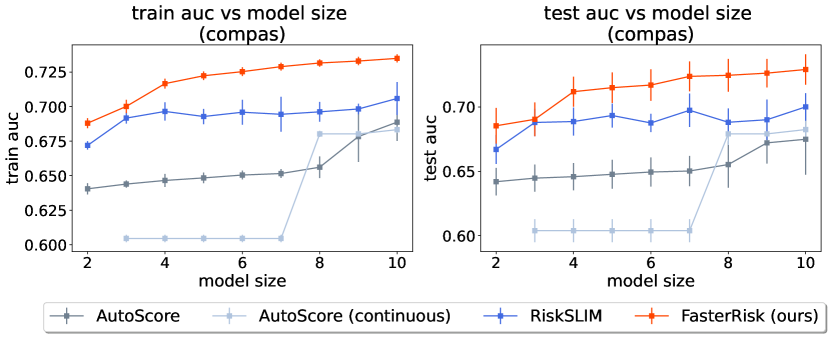

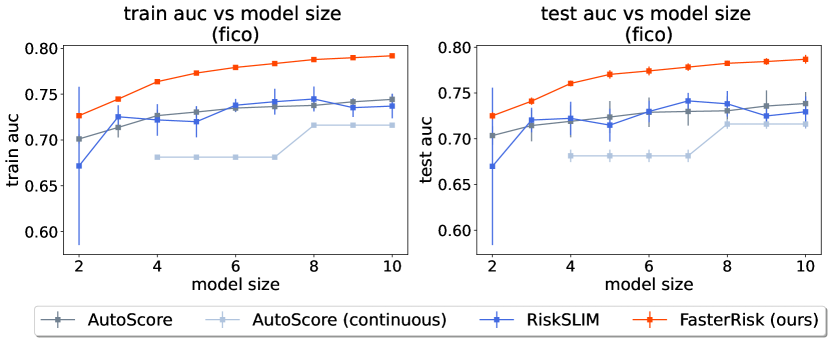

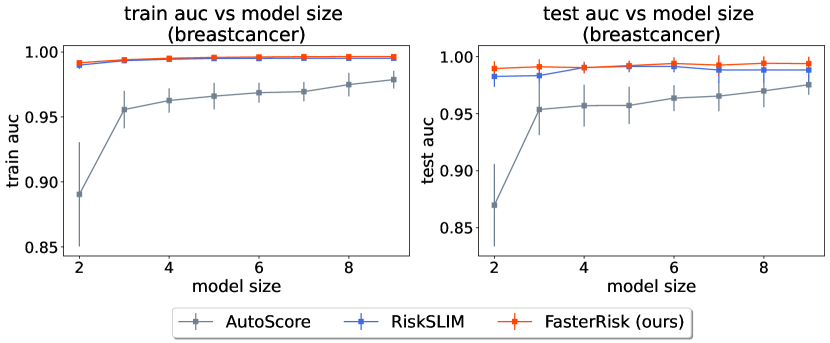

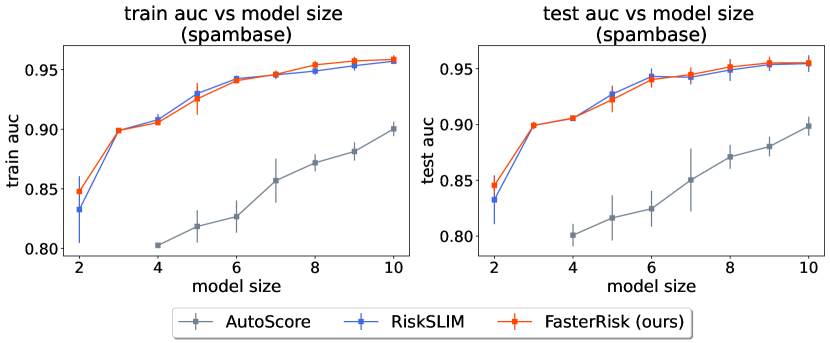

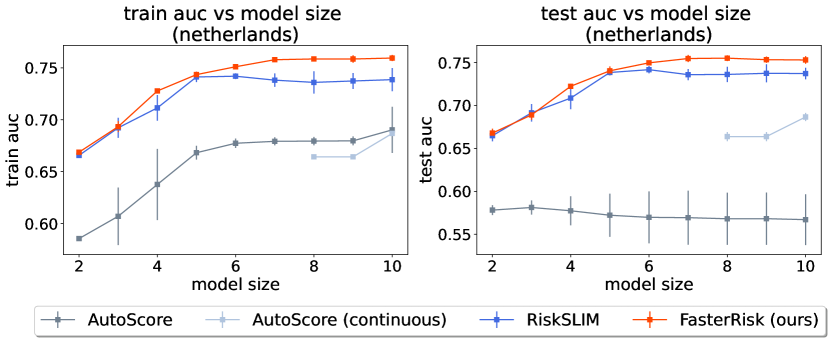

We first evaluate FasterRisk’s solution quality. Figure 3 shows the training and test AUC on six datasets (results for training loss appear in Appendix E). FasterRisk (the red line) outperforms all baselines, consistently obtaining the highest AUC scores on both the training and test sets. Notably, our method obtains better results than RiskSLIM, which uses a mathematical solver and is the current state-of-the-art method for scoring systems. This superior performance is due to the use of multipliers, which increases the complexity of the hypothesis space. Figure 4 provides a more detailed comparison between FasterRisk and RiskSLIM. One may wonder whether running RiskSLIM longer would make this MIP-based method comparable to our FasterRisk, since the current running time limit for RiskSLIM is only 15 minutes. We extended RiskSLIM’s running time limit up to 1 hour and show the comparison in Appendix E.8; FasterRisk still outperforms RiskSLIM by a large margin.

FasterRisk performs significantly better than the other baselines for two reasons. First, the continuous sparse solutions produced by ElasticNet are low quality for very sparse models. Second, it is difficult to obtain an exact model size by controlling regularization. For example, Pooled-PLR-RD and Pooled-PLR-RDSP do not have results for model size on the mammo datasets, because no such model size exists in the pooled solutions after rounding.

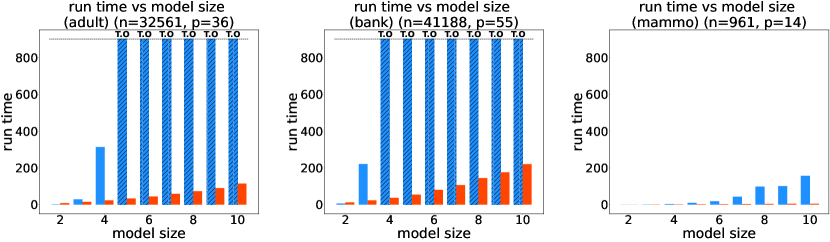

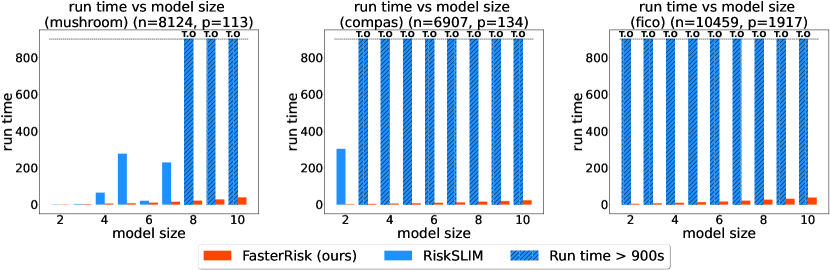

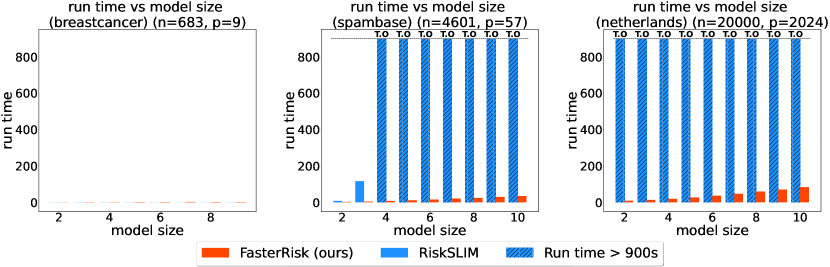

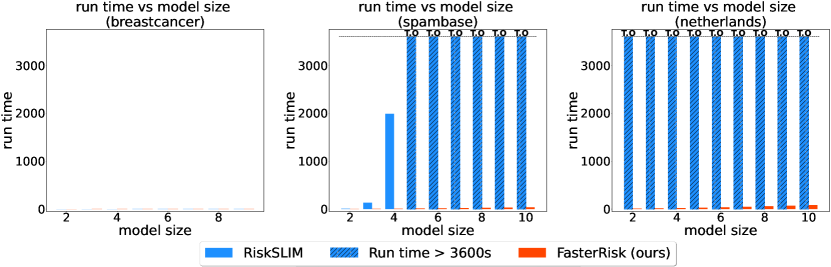

4.2 Runtime Comparison

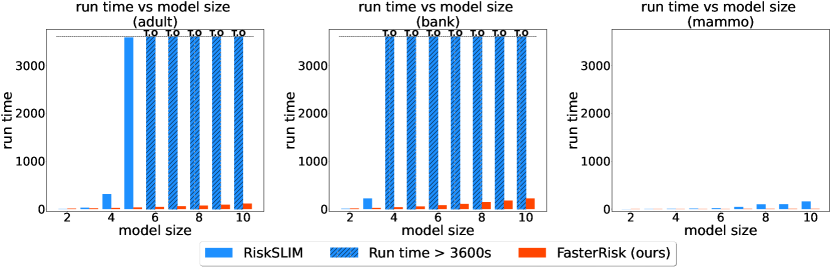

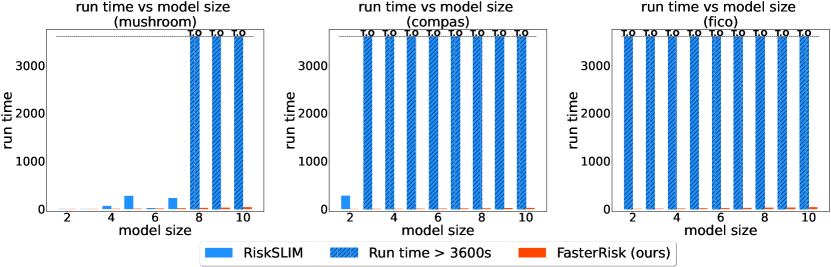

The major drawback of RiskSLIM is its limited scalability. Runtime is important to allow interactive model development and to handle larger datasets. Figure 5 shows that FasterRisk (red bars) is significantly faster than RiskSLIM (blue bars) in general. We ran these experiments with a 900 second (15 minute) timeout. RiskSLIM finishes running on the small dataset mammo, but it times out on the larger datasets, timing out on models larger than 4 features for adult, larger than 3 features for bank, larger than 7 features for mushroom, larger than 2 features for COMPAS, and larger than 1 feature for FICO. RiskSLIM times out early on COMPAS and FICO datasets, suggesting that the MIP-based method struggles with high-dimensional and highly-correlated features. Thus, we see that FasterRisk tends to be both faster and more accurate than RiskSLIM.

4.3 Example Scoring Systems

The main benefit of risk scores is their interpretability. We place a few example risk scores in Table 1 to allow the reader to judge for themselves. More risk scores examples can be found in Appendix F.1. Additionally, we provide a pool of solutions for the top 12 models on the bank, mammo, and Netherlands datasets in Appendix F.2. Prediction performance is generally not the only criteria users consider when deciding to deploy a model. Provided with a pool of solutions that perform equally well, a user can choose the one that best incorporates domain knowledge [45]. After the pool of models is generated, interacting with the pool is essentially computationally instantaneous. Finally, we can reduce some models to relatively prime coefficients or transform some features for better interpretability. Examples of such transformations are given in Appendix G.1.

| 1. | no high school diploma | -4 points | … | |

| 2. | high school diploma only | -2 points | + | … |

| 3. | age 22 to 29 | -2 points | + | … |

| 4. | any capital gains | 3 points | + | … |

| 5. | married | 4 points | + | … |

| SCORE | = |

| SCORE | -4 | -3 | -2 | -1 | 0 |

|---|---|---|---|---|---|

| RISK | 1.3% | 2.4% | 4.4% | 7.8% | 13.6% |

| SCORE | 1 | 2 | 3 | 4 | 7 |

| RISK | 22.5% | 35.0% | 50.5% | 65.0% | 92.2% |

| 1. | odoralmond | -5 points | … | |

| 2. | odoranise | -5 points | + | … |

| 3. | odornone | -5 points | + | … |

| 4. | odorfoul | 5 points | + | … |

| 5. | gill sizebroad | -3 points | + | … |

| SCORE | = |

| SCORE | -8 | -5 | -3 | 2 |

|---|---|---|---|---|

| RISK | 1.62% | 26.4% | 73.6% | >99.8% |

5 Conclusion

FasterRisk produces a collection of high-quality risk scores within minutes. Its performance owes to three key ideas: a new algorithm for sparsity- and box-constrained continuous models, using a pool of diverse solutions, and the use of the star ray search, which leverages multipliers and a new sequential rounding technique. FasterRisk is suitable for high-stakes decisions, and permits domain experts a collection of interpretable models to choose from.

Code Availability

Implementations of FasterRisk discussed in this paper are available at https://github.com/jiachangliu/FasterRisk.

Acknowledgements

The authors acknowledge funding from the National Science Foundation under grants IIS-2147061 and IIS-2130250, National Institute on Drug Abuse under grant R01 DA054994, Department of Energy under grants DE-SC0021358 and DE-SC0023194, and National Research Traineeship Program under NSF grants DGE-2022040 and CCF-1934964. We acknowledge the support of the Natural Sciences and Engineering Research Council of Canada (NSERC). Nous remercions le Conseil de recherches en sciences naturelles et en génie du Canada (CRSNG) de son soutien.

References

- Ahanor et al. [2022] Izuwa Ahanor, Hugh Medal, and Andrew C. Trapp. Diversitree: Computing diverse sets of near-optimal solutions to mixed-integer optimization problems. arXiv, 2022.

- Allam [2020] Mohamed Farouk Allam. Scoring system for the diagnosis of COVID-19. The Open Public Health Journal, 13(1), 2020.

- Apgar [1953] Virginia Apgar. A proposal for a new method of evaluation of the newborn infant. Current Researches in Anesthesia and Analgesia, 1953(32):260–267, 1953.

- Austin et al. [2010] James Austin, Roger Ocker, and Avi Bhati. Kentucky pretrial risk assessment instrument validation. Bureau of Justice Statistics, 2010.

- Billiet et al. [2017] Lieven Billiet, Sabine Van Huffel, and Vanya Van Belle. Interval coded scoring extensions for larger problems. In Proceedings of the IEEE Symposium on Computers and Communications, pages 198–203. IEEE, 2017.

- Billiet et al. [2018] Lieven Billiet, Sabine Van Huffel, and Vanya Van Belle. Interval Coded Scoring: A toolbox for interpretable scoring systems. PeerJ Computer Science, 4:e150, 04 2018.

- Breiman [2001] Leo Breiman. Statistical modeling: The two cultures. Statistical Science, 16(3):199–231, 2001.

- Burgess [1928] Ernest W Burgess. Factors determining success or failure on parole. Illinois Committee on Indeterminate-Sentence Law and Parole Springfield, IL, 1928.

- Carrizosa et al. [2013] E. Carrizosa, A. Nogales-Gómez, and D. Romero Morales. Strongly agree or strongly disagree?: Rating features in support vector machines. Technical report, Saïd Business School, University of Oxford, UK, 2013.

- Chevaleyre et al. [2013] Yann Chevaleyre, Frédéerick Koriche, and Jean-Daniel Zucker. Rounding methods for discrete linear classification. In International Conference on Machine Learning, pages 651–659. PMLR, 2013.

- Cole [1993] TJ Cole. Scaling and rounding regression coefficients to integers. Journal of the Royal Statistical Society: Series C (Applied Statistics), 42:261–268, 1993.

- Cranor and LaMacchia [1998] Lorrie Faith Cranor and Brian A LaMacchia. Spam! Communications of the ACM, 41(8):74–83, 1998.

- Dedieu et al. [2021] Antoine Dedieu, Hussein Hazimeh, and Rahul Mazumder. Learning sparse classifiers: Continuous and mixed integer optimization perspectives. Journal of Machine Learning Research, 22:135–1, 2021.

- Elenberg et al. [2018] Ethan R Elenberg, Rajiv Khanna, Alexandros G Dimakis, and Sahand Negahban. Restricted strong convexity implies weak submodularity. The Annals of Statistics, 46(6B):3539–3568, 2018.

- Elter et al. [2007] Matthias Elter, Rüdiger Schulz-Wendtland, and Thomas Wittenberg. The prediction of breast cancer biopsy outcomes using two cad approaches that both emphasize an intelligible decision process. Medical Physics, 34(11):4164–4172, 2007.

- Ertekin and Rudin [2015] Sëyda Ertekin and Cynthia Rudin. A bayesian approach to learning scoring systems. Big Data, 3(4):267–276, Dec 2015.

- FICO et al. [2018] FICO, Google, Imperial College London, MIT, University of Oxford, UC Irvine, and UC Berkeley. Explainable Machine Learning Challenge. https://community.fico.com/s/explainable-machine-learning-challenge, 2018.

- Gage et al. [2001] Brian F Gage, Amy D Waterman, William Shannon, Michael Boechler, Michael W Rich, and Martha J Radford. Validation of clinical classification schemes for predicting stroke. The Journal of the American Medical Association, 285(22):2864–2870, 2001.

- Kessler et al. [2005] Ronald C Kessler, Lenard Adler, Minnie Ames, Olga Demler, Steve Faraone, EVA Hiripi, Mary J Howes, Robert Jin, Kristina Secnik, Thomas Spencer, and et al. The world health organization adult ADHD self-report scale (ASRS): a short screening scale for use in the general population. Psychological Medicine, 35(02):245–256, 2005.

- Kohavi [1996] Ron Kohavi. Scaling up the accuracy of naive-bayes classifiers: A decision-tree hybrid. In Proceedings Knowledge Discovery and Data Mining (KDD), volume 96, pages 202–207, August 1996.

- Larson et al. [2016] Jeff Larson, Surya Mattu, Lauren Kirchner, and Julia Angwin. How we analyzed the COMPAS recidivism algorithm. ProPublica, May 23, https://www.propublica.org/article/how-we-analyzed-the-compas-recidivism-algorithm, 2016.

- Latessa et al. [2009] Edward Latessa, Paula Smith, Richard Lemke, Matthew Makarios, and Christopher Lowenkamp. Creation and validation of the Ohio risk assessment system: Final report. https://www.ocjs.ohio.gov/ORAS_FinalReport.pdf, 2009.

- Lee et al. [2022] Ji Yeon Lee, Byung-Ho Nam, Mhinjine Kim, Jongmin Hwang, Jin Young Kim, Miri Hyun, Hyun Ah Kim, and Chi-Heum Cho. A risk scoring system to predict progression to severe pneumonia in patients with COVID-19. Scientific Reports, 12(1):1–8, 2022.

- Liu et al. [2022] Jiachang Liu, Chudi Zhong, Margo Seltzer, and Cynthia Rudin. Fast sparse classification for generalized linear and additive models. In Proceedings of International Conference on Artificial Intelligence and Statistics (AISTATS), 2022.

- Lozano et al. [2011] Aurelie Lozano, Grzegorz Swirszcz, and Naoki Abe. Group orthogonal matching pursuit for logistic regression. In Proceedings of the International Conference on Artificial Intelligence and Statistics (AISTATS), pages 452–460, 2011.

- Mangasarian et al. [1995] Olvi L Mangasarian, W Nick Street, and William H Wolberg. Breast cancer diagnosis and prognosis via linear programming. Operations Research, 43(4):570–577, 1995.

- Moreno et al. [2005] Rui P Moreno, Philipp GH Metnitz, Eduardo Almeida, Barbara Jordan, Peter Bauer, Ricardo Abizanda Campos, Gaetano Iapichino, David Edbrooke, Maurizia Capuzzo, and Jean-Roger Le Gall. SAPS3 – from evaluation of the patient to evaluation of the intensive care unit. part 2: Development of a prognostic model for hospital mortality at ICU admission. Intensive Care Medicine, 31(10):1345–1355, 2005.

- Moro et al. [2014] Sérgio Moro, Paulo Cortez, and Paulo Rita. A data-driven approach to predict the success of bank telemarketing. Decision Support Systems, 62:22–31, 2014.

- Schlimmer [1987] Jeffrey Curtis Schlimmer. Concept acquisition through representational adjustment. PhD thesis, University of California, Irvine, 1987.

- Shang et al. [2020] Yufeng Shang, Tao Liu, Yongchang Wei, Jingfeng Li, Liang Shao, Minghui Liu, Yongxi Zhang, Zhigang Zhao, Haibo Xu, Zhiyong Peng, et al. Scoring systems for predicting mortality for severe patients with COVID-19. EClinicalMedicine, 24:100426, 2020.

- Six et al. [2008] A. Jacob. Six, Barbra E. Backus, and Johannes C. Kelder. Chest pain in the emergency room: value of the heart score. Netherlands Heart Journal, 16(6):191–196, 2008.

- Sokolovska et al. [2017] Nataliya Sokolovska, Yann Chevaleyre, Karine Clément, and Jean-Daniel Zucker. The fused lasso penalty for learning interpretable medical scoring systems. In 2017 International Joint Conference on Neural Networks (IJCNN), pages 4504–4511. IEEE, 2017.

- Sokolovska et al. [2018] Nataliya Sokolovska, Yann Chevaleyre, and Jean-Daniel Zucker. A provable algorithm for learning interpretable scoring systems. In Proceedings of International Conference on Artificial Intelligence and Statistics, pages 566–574. PMLR, 2018.

- Than et al. [2014] Martin Than, Dylan Flaws, Sharon Sanders, Jenny Doust, Paul Glasziou, Jeffery Kline, Sally Aldous, Richard Troughton, Christopher Reid, and William A Parsonage. Development and validation of the emergency department assessment of chest pain score and 2h accelerated diagnostic protocol. Emergency Medicine Australasia, 26(1):34–44, 2014.

- Tibshirani [1996] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288, 1996.

- Tollenaar and van der Heijden [2013] Nikolaj Tollenaar and P.G.M. van der Heijden. Which method predicts recidivism best?: a comparison of statistical, machine learning and data mining predictive models. Journal of the Royal Statistical Society: Series A (Statistics in Society), 176(2):565–584, 2013.

- Ustun and Rudin [2015] Berk Ustun and Cynthia Rudin. Supersparse linear integer models for optimized medical scoring systems. Machine Learning, pages 1–43, 2015. ISSN 0885-6125. doi: 10.1007/s10994-015-5528-6. URL http://dx.doi.org/10.1007/s10994-015-5528-6.

- Ustun and Rudin [2017] Berk Ustun and Cynthia Rudin. Optimized risk scores. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1125–1134, 2017.

- Ustun and Rudin [2019] Berk Ustun and Cynthia Rudin. Learning optimized risk scores. Journal of Maching Learning Research, 20:150–1, 2019.

- Ustun et al. [2013] Berk Ustun, Stefano Traca, and Cynthia Rudin. Supersparse linear integer models for predictive scoring systems. In Workshops at the Twenty-Seventh AAAI Conference on Artificial Intelligence, 2013.

- Ustun et al. [2017] Berk Ustun, Lenard A Adler, Cynthia Rudin, Stephen V Faraone, Thomas J Spencer, Patricia Berglund, Michael J Gruber, and Ronald C Kessler. The world health organization adult attention-deficit / hyperactivity disorder self-report screening scale for DSM-5. JAMA Psychiatry, 74(5):520–526, 2017.

- Wang et al. [2022] Caroline Wang, Bin Han, Bhrij Patel, and Cynthia Rudin. In Pursuit of Interpretable, Fair and Accurate Machine Learning for Criminal Recidivism Prediction. Journal of Quantitative Criminology, pages 1–63, 2022. ISSN 0748-4518. doi: 10.1007/s10940-022-09545-w.

- Wasilewski et al. [2020] Piotr Wasilewski, Bartosz Mruk, Samuel Mazur, Gabriela Półtorak-Szymczak, Katarzyna Sklinda, and Jerzy Walecki. COVID-19 severity scoring systems in radiological imaging–a review. Polish Journal of Radiology, 85(1):361–368, 2020.

- Xie et al. [2020] Feng Xie, Bibhas Chakraborty, Marcus Eng Hock Ong, Benjamin Alan Goldstein, Nan Liu, et al. Autoscore: A machine learning–based automatic clinical score generator and its application to mortality prediction using electronic health records. JMIR Medical Informatics, 8(10):e21798, 2020.

- Xin et al. [2022] Rui Xin, Chudi Zhong, Zhi Chen, Takuya Takagi, Margo Seltzer, and Cynthia Rudin. Exploring the whole rashomon set of sparse decision trees. In Proceedings of Neural Information Processing Systems, 2022.

- Zeng et al. [2017] Jiaming Zeng, Berk Ustun, and Cynthia Rudin. Interpretable classification models for recidivism prediction. Journal of the Royal Statistical Society: Series A (Statistics in Society), 180(3):689–722, 2017.

- Zhang et al. [2020] Chi Zhang, Ling Qin, Kang Li, Qi Wang, Yan Zhao, Bin Xu, Lianchun Liang, Yanchao Dai, Yingmei Feng, Jianping Sun, et al. A novel scoring system for prediction of disease severity in COVID-19. Frontiers in Cellular and Infection Microbiology, 10:318, 2020.

- Zou and Hastie [2005] Hui Zou and Trevor Hastie. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67(2):301–320, 2005.

Appendix to FasterRisk: Fast and Accurate Interpretable Risk Scores

Appendix A Additional Algorithms

A.1 Expand Support by One More Feature

Input: Dataset , coefficient constraint , and beam search size , current coefficient vector , and a set of found supports .

Output: a collection of solutions with for . All of these solutions include the support of plus one more feature. None of the solutions have the same support as any element of , meaning we do not discover the same support set multiple times. We also output the updated .

A.2 Collect Sparse Diverse Pool

Input: Dataset , a coefficient vector , an optimality gap tolerance , and the number of attempts .

Output: a set containing good sparse continuous solutions.

A.3 Round Continuous Coefficients to Integers

Input: Dataset , a sparse continuous solution , where .

Output: an integer-valued solution , where .

Appendix B Comments on Proof of Chevaleyre et al.

Chevaleyre et al. [10] proposed Greedy Rounding, where coefficients are rounded sequentially. While this technique provides theoretical guarantees for greedy rounding for the hinge loss, we identified a serious flaw in their argument, rendering the bounds incorrect. We elaborate on this matter in this appendix.

The flaw is in the proof of Lemma 7. The proof essentially shows that for each sample , there is at least one (from the set ) such that the inequality holds. However, the same that works for sample is not guaranteed to work for sample for the inequality. It is not clear whether there exists one that make all inequalities (for all samples in ) hold at the time.

To paraphrase, for each sample , the proof shows that we can pick a set of (either , , or ) so that the inequality holds individually. However, we can not rule out the case that intersection of these individual sets is empty.

Without this extra argument, there is a gap between the statement of Lemma 7 and the proof of Lemma 7. Then, the bound for the greedy algorithm in Theorem 8 will not hold in the paper.

Appendix C Theoretical Upper Bound for the Rounding Method, Algorithm 6

The following theorem (as also shown in the main paper) states that we can provide an upper bound on the difference of the total loss between the integer solution given by Algorithm 6 and the real-valued solution .

Theorem 3.1 (Loss incurred from rounding) Let be the real-valued coefficients for the logistic regression model with objective function . Let be the integer-valued coefficients returned by the Auxiliaryloss Rounding method, Algorithm 6. Furthermore, let . Let with if and otherwise. Then, we have an upper bound on the difference between the loss and the loss :

| (12) |

To prove Theorem 3.1, we need to use the following Lemma C.1, which states that during each successive step of rounding a real-valued coefficient to the integer value, the deviation can be characterized and bounded by the data features and the real-valued coefficient.

Lemma C.1.

Suppose we have rounded the first real-valued coefficients to integers. Then for the -th real-valued coefficient, if we set , then we have

| (13) |

where .

Proof.

Let be a binomial random variable so that with probability and with probability . For notational convenience, let us define the function . Then is a random variable, and the input to function , which is , takes on values either or .

The expectation of this random variable is

| # move inside the | ||||

| # substitute with | ||||

| # expand the square term |

Notice that because , , we have

and

| # similar as above |

Therefore, we have

| # plug in the two expectations above | ||||

| # split into two summation terms |

Since the expectation of is equal to , there exists a such that

| (14) |

Note that is the minimizer of because the other input value will take the value , which is greater than or equal to the expectation .

If we round to an integer by setting , then . We now have:

| # definition of and | ||||

| # substitute | ||||

| # is the minimizer of | ||||

| # Inequality 14 |

thus completing our proof.

∎

Proof of Theorem 3.1. For simplicity, let us first consider the case where we round coefficients sequentially from to . We claim that if at each step , we round , then for

| (15) |

We prove this by the principle of induction. Suppose for step , we have

Then, according to Lemma C.1 and the previous line, we have

| # Lemma C.1 | ||||

| # use a single sum |

For the base step , Lemma C.1 also implies that

Thus, Inequality (15) works for all . If we let , we have

| (16) |

Also, notice that this inequality holds for sequential rounding of any permutation of the feature indices , and the rounding order of the AuxiliaryLossRounding method is one specific feature order. Therefore, the Inequality (16) works for the AuxiliaryLossRounding method as well.

Lastly, we use Inequality 16 to derive an upper bound on the logistic loss of the AuxiliaryLossRounding method. Recall that our objective is:

| (17) |

The loss difference between the rounded solution and the real-valued solution can be bounded as follows:

| # Lipschitz continuity, see details below | ||||

| # Jensen’s Inequality, see details below |

There are two inequalities we need to elaborate in details, the second and the last inequalities (Lipschitz continuity and Jensen’s Inequaltiy).

Second Inequality (Lipschitz continuity):

The second inequality holds because the logistic loss is Lipschitz continuous. If the Lipschitz constant is , then we have . We now explain how we derive the Lipschitz constant with if and as stated in Theorem 3.1.

Since the logistic loss function is differentiable, the smallest Lipschitz constant of the function is . To see this, by the definition of the Lipschitz constant, we have . If we take the limit , the inequality still holds, . The left hand side converges to the absolute value of the derivative of at . Therefore, we have . Since this works for all , and we want to find the smallest Lipschitz value, we have .

For the logistic loss , the absolute value of the derivative is . Thus, if is lower-bounded so that , the smallest Lipschitz constant of the logistic loss is .

We can apply this fact to calculate a smaller Lipschitz constant for each sample’s term. If if and otherwise, then

Therefore, is a valid Lipschitz constant for the -th sample.

Last Inequality (Jensen’s inequality):

Jensen’s Inequality states that for any convex function . For this specific problem, let and let for a particular with probability . Then, we have

| # multiply and divide by | ||||

| # definition of , , and | ||||

| # Jensen’s Inequality | ||||

| # write out , , and explicitly | ||||

| # move inside |

Therefore, using Inequality 16, we can now bound the loss difference between the rounded solution and the real-valued solution as stated in Theorem 3.1:

∎

Appendix D Experimental Setup

D.1 Dataset Information

The dataset names, data source, number of samples and features, and the classification tasks can be found in Table 2. The datasets with results shown in the main paper (adult, bank, breastcancer, mammo, mushroom, spambase) were directly downloaded from this link: https://github.com/ustunb/risk-slim/tree/master/examples/data. The COMPAS dataset can be downloaded from this link: https://github.com/propublica/compas-analysis/blob/master/compas-scores-two-years.csv. The FICO dataset can be requested and downloaded from this website: https://community.fico.com/s/explainable-machine-learning-challenge. The Netherlands dataset is available through Data Archiving and Networked Services https://easy.dans.knaw.nl/ui/datasets/id/easy-dataset:78692.

For our experiments on the COMPAS, FICO, and Netherlands datasets, we convert the continuous features into a set of highly correlated dummy variables, with all entries equal to 1 or 0. By conducting experiments on these three datasets, we can test how well FasterRisk works for highly correlated features. We use the preprocessing steps as explained in Section C2 of [24]. We list the key preprocessing steps below.

COMPAS: In addition to the label “two_year_recid”, we use features “sex”, “age”, “juv_fel_count”, “juv_misd_count”, “juv_other_count”, “priors_count”, and “c_charge_degree”.

FICO: All continuous features are used.

Netherlands: In addition to the label “recidivism_in_4y”, we use features “sex”, “country of birth”, “log # of previous penal cases”, “11-20 previous case”, and “20 previous case”, “age in years”, “age at first penal case”, and “offence type”.

For each continuous variable , it is converted into a set of highly correlated dummy variables , where are all unique values that have appeared in feature column . For Netherlands, special preprocessing steps are performed for “age in years” (which is real-valued, not integer) and “age at first penal case”. Instead of considering all unique values in the feature column, we consider 1000 quantiles.

| Dataset | Source | N | P | Classification task |

|---|---|---|---|---|

| adult | [20] | 32561 | 36 | Predict if a U.S. resident earns more than $50,000 |

| bank | [28] | 41188 | 55 | Predict if a person opens account after marketing call |

| breastcancer | [26] | 683 | 9 | Detect breast cancer using a biopsy |

| mammo | [15] | 961 | 14 | Detect breast cancer using a mammogram |

| mushroom | [29] | 8124 | 113 | Predict if a mushroom is poisonous |

| spambase | [12] | 4601 | 57 | Predict if an e-mail is spam |

| COMPAS | [21] | 6907 | 134 | Predict if someone will be arrested 2 years of release |

| FICO | [17] | 10459 | 1917 | Predict if someone will default on a loan |

| Netherlands | [36] | 20000 | 2024 | Predict if someone will have any charge within 4 years |

D.2 Computing Platform

We ran all experiments on a TensorEX TS2-673917-DPN Intel Xeon Gold 6226 Processor with 2.7Ghz (768GB RAM 48 cores). For all experiments, we used only two cores because we observed using more cores did not improve the computational speed further.

D.3 Baselines

We compare with several baselines in our experiments.

RiskSLIM The current state-of-the-art method is RiskSLIM. We installed this package from the following GitHub link: https://github.com/ustunb/risk-slim111The license for this package is BSD 3-Clause license. The license can be viewed on the GitHub page.. RiskSLIM uses the IBM CPLEX MIP solver to do the optimization. The CPLEX version we used is 12.8.

Pooled Approaches For other baselines, we first found a pool of continuous sparse solutions by the ElasticNet [48] method and then rounded the coefficients to integers with different rounding techniques. Because ElasticNet has and penalties, we call this method the penalized logistic regression (PLR) approach. The best integer solution was selected from this pool based on which solution produces the smallest logistic loss while obeying the sparsity constraint and box constraints. These baselines correspond to the Pooled Approaches in Section 5.1 of [39], where Figure 11 and Figure 12 clearly show that pooled approaches are much better than traditional approaches. We include Unit Weighting and Rescaled Rounding as two additional rounding methods. The details of the pooled approach and the rounding techniques can be found in Section 5.1 of [39].

The ElasticNet method tries to solve the following optimization problem:

| (18) |

where [0,1] is a hyperparameter. By controlling , we choose the best model over Ridge ( =0), Lasso (=1), and Elastic net (). We generated 1,100 models using the glmnet package222We installed the package from the following GitHub link: https://github.com/bbalasub1/glmnet_python The package contains GNU license, which can be viewed on the GitHub website.. To do this, we first choose 11 values of 0, 0.1, 0.2, …, 0.9, 1.0. For each given , the package then internally and automatically selects 100 ’s equi-spaced on the logarithmic scale between and (the smallest value for such that all the coefficients are zero). We call this part the Pooled-PLR (Pooled Penalized Logistic Regression).

To convert each continuous sparse model to an integer sparse model, we applied the following rounding methods:

-

•

1) Pooled-PLR-RD: For each of the 1,100 PLR models in the pool, we first truncated all the coefficients (except the intercept ) to be within the range [-5,5] and did simple rounding: , and . The operation is defined as if and otherwise.

-

•

2) Pooled-PLR-RDU: For each solution, we rounded each of its coefficients to be 1 based on its signs: and This rounding technique is known as unit weighting or the Burgess method.

-

•

3) Pooled-PLR-RSRD: For each solution, we rescaled its coefficients by a factor so that and then rounded each rescaled coefficient to the nearest integer: and .

-

•

4) Pooled-PLR-Rand: For each model in the pool, for each coefficient, denote its fractional part by . We rounded each coefficient up to with probability and down to with probability . After all rounding was done, we selected the best model in the pool.

-

•

5) Pooled-PLR-RDP: For each model in the pool, we iterated through each coefficient and calculated the loss for both and and selected the rounding that minimizes the loss. This is called Sequential Rounding in [39].

-

•

6) Pooled-PLR-RDSP: we first rounded through Sequential Rounding (Method 5, just above), and then we applied Discrete Coordinate Descent (DCD) [39] to iteratively improve the loss by adjusting one coefficient at a time. At each round, DCD selects the coefficient and its new value that decreases the logistic loss the most.

As mentioned earlier, after we get the 1,100 integer sparse models via each rounding technique, we selected the best model from the pool based on which solution has the smallest logistic loss.

D.4 Hyperparameters Specification

We used the default values in Algorithm 1 for all hyperparameters. We reiterate the hyperparameters used in the experiments below.

-

•

beam search size: .

-

•

tolerance level for sparse diverse pool: (or 30%).

-

•

number of attempts to try for sparse diverse pool: .

-

•

number of multipliers to try: .

Performance is not particularly sensitive to these choices (see Appendix E.10). If , , are chosen too large, the algorithm will take longer to execute.

Appendix E Additional Experimental Results

E.1 Additional Results on Solution Quality

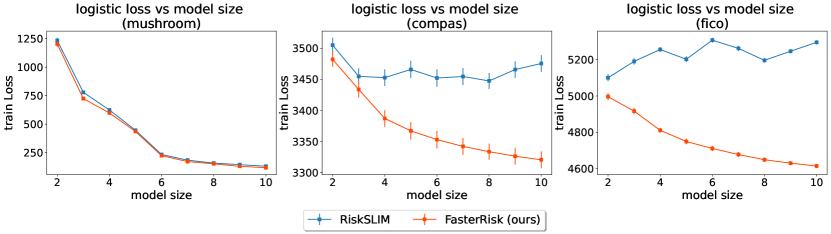

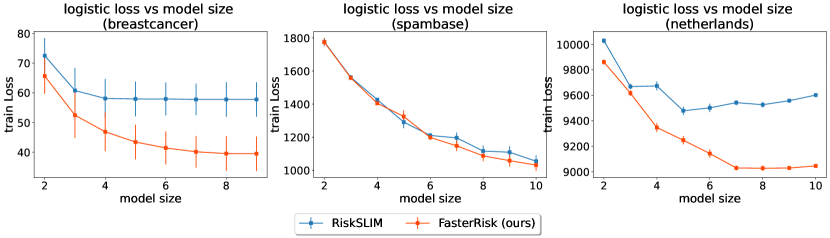

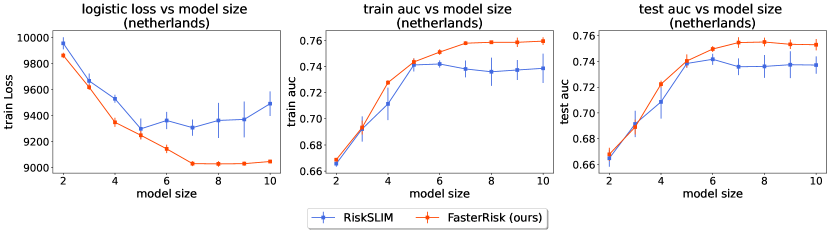

In addition to the six datasets we show in the main paper, we provide results on the breastcancer, spambase, and Netherlands datasets (see Section D.1 for more data information). The comparison of solution quality is shown in Figure 6. We see that FasterRisk outperforms both RiskSLIM and other pooled approaches, even with high dimensional feature spaces and in the presence of highly correlated features (the Netherlands dataset).

E.2 Additional Results on Direct Comparison with RiskSLIM

As RiskSLIM provides state-of-the-art performance, we compare it to FasterRisk in isolation to highlight the differences between the two approaches/algorithms. The results are shown in Figure 7 on the breastcancer, spambase, and Netherlands datasets.

E.3 Additional Results on Running Time

We also provide a runtime comparison between RiskSLIM and FasterRisk in Figure 8. Except for the small dataset breastcancer, RiskSLIM timed out in all other instances. In contrast, FasterRisk finishes running under 50s or 100s on all cases, showing great scalability, even in high dimensional feature space and in presence of highly correlated features (the Netherlands dataset).

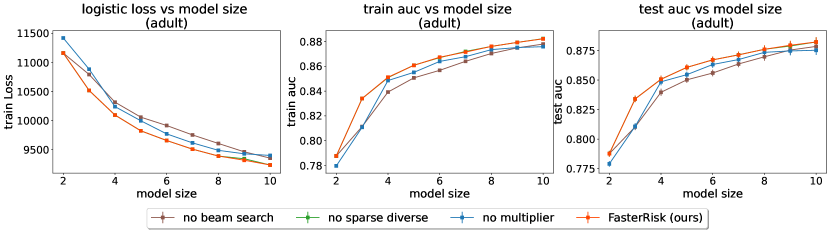

E.4 Ablation Study of the Proposed Techniques

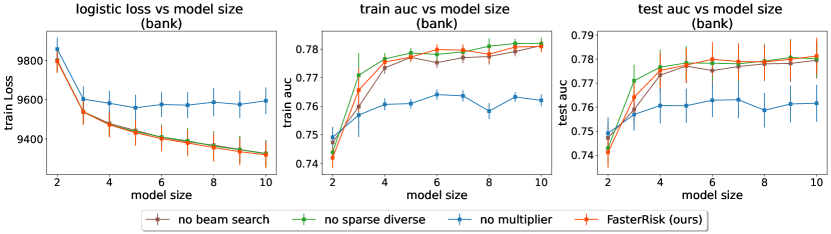

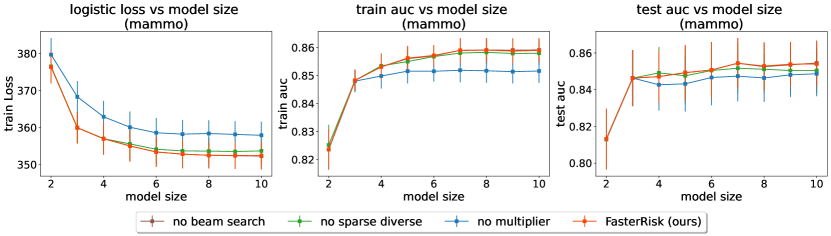

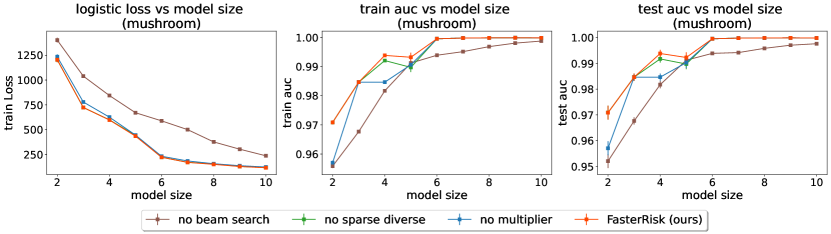

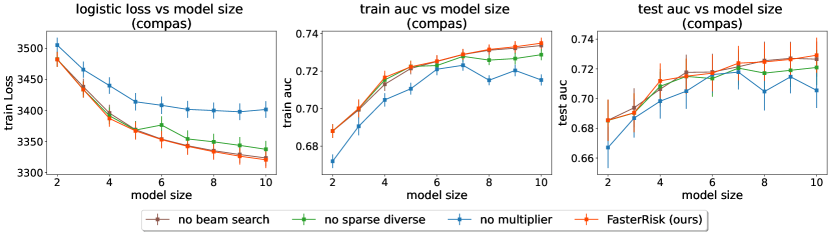

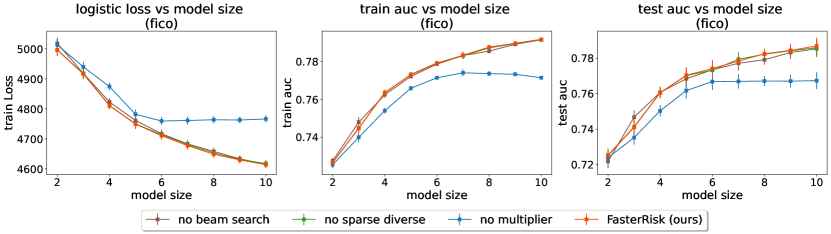

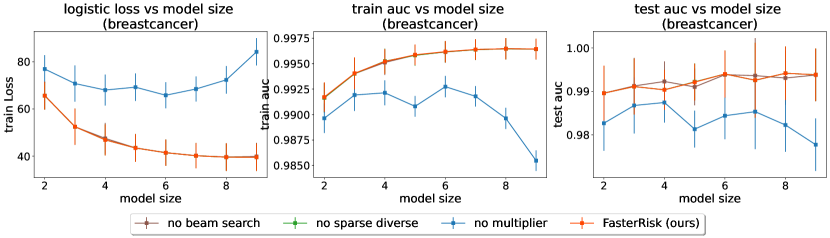

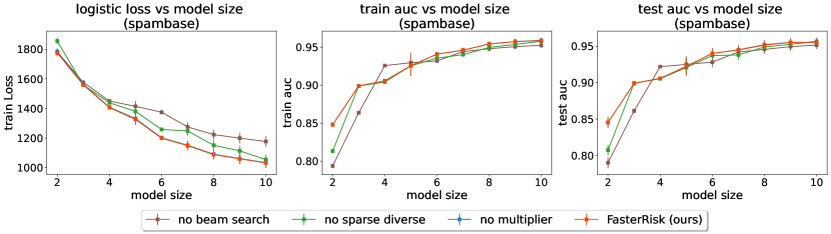

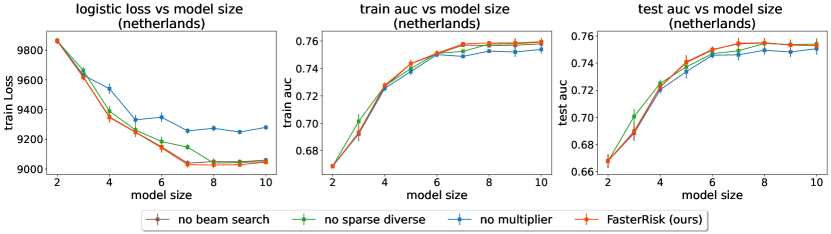

We investigate how each component of FasterRisk, including sparse beam search, diverse pool, and multipliers, contribute to solution quality. We quantify the contribution of each part of the algorithm by means of an ablation study in which we run variations of FasterRisk, each with a single component disabled.

The results are shown in Figure 9-11. “no beam search” means that the beam size is 1, so we expand the support by picking the next feature based on which new feature can induce the smallest logistic loss via the single coordinate optimization. “no sparse diverse” means that the sparse diverse pool contains only the solution by Algorithm 2, the SparseBeamLR method. “no multiplier” means that there is no “star ray search” of the multiplier. There is no scaling of coefficients or the data, so we think of this as setting multiplier to .

The ablation study shows that different parts of our algorithm provide the biggest benefit to different data sets — that is, there is no single component of the algorithm that uniformly assists with performance; instead, the combination of these techniques, working in concert, is responsible. We provide the detailed analysis of the contributions for each specific dataset in the figure captions.

E.5 Training Losses of FasterRisk vs. RiskSLIM

In the main paper, due to the page limit, we have only compared the training and test AUCs between RiskSLIM and our FasterRisk. Here, we provide the comparison of training loss (logistic loss) between these two methods. The results are shown in Figure 12. We can see that FasterRisk outperforms RiskSLIM in almost all model size instances and datasets.

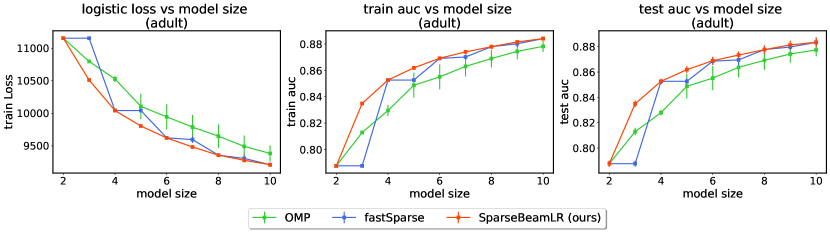

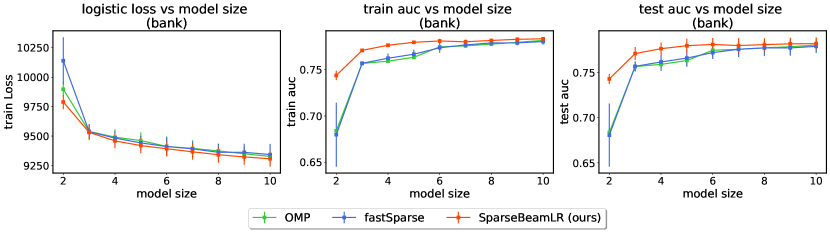

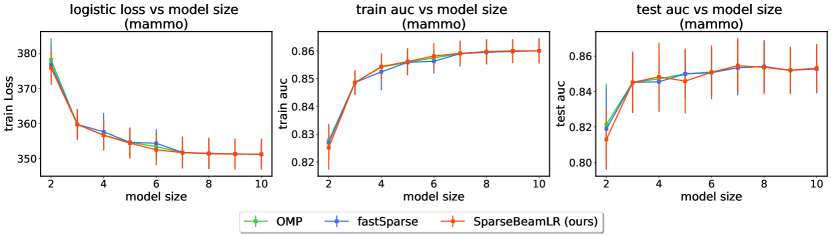

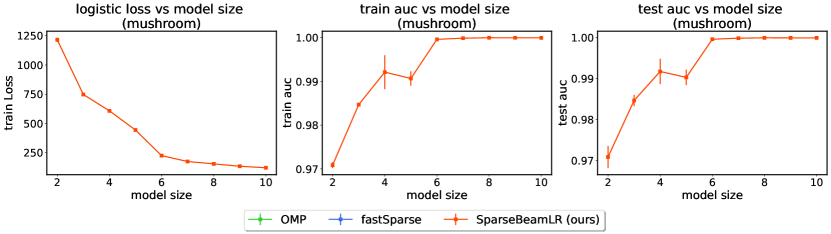

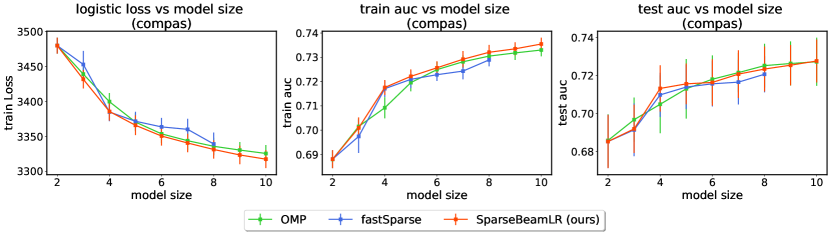

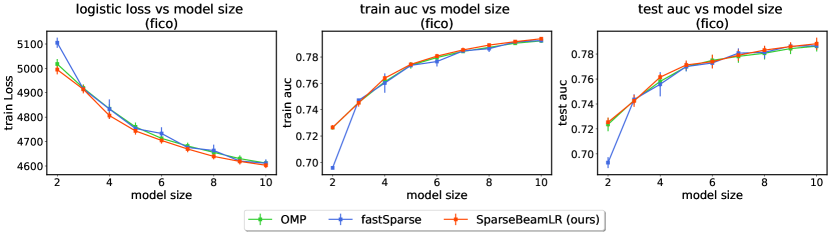

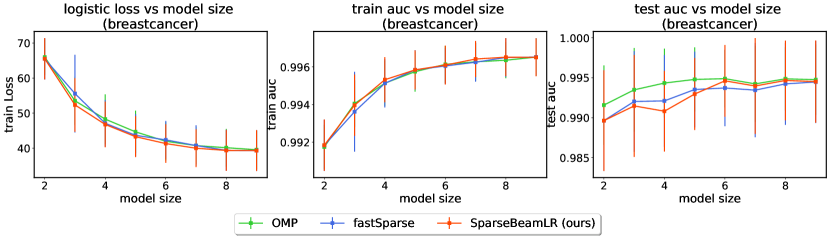

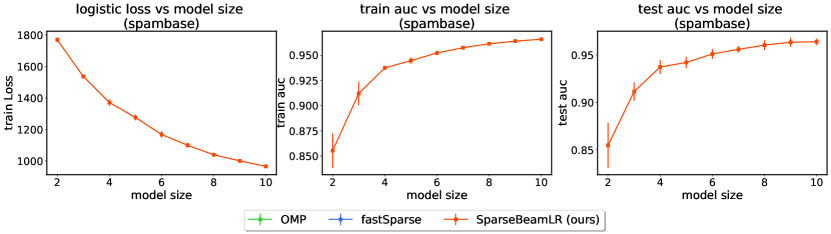

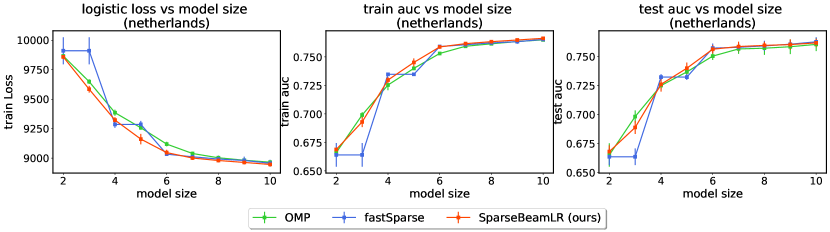

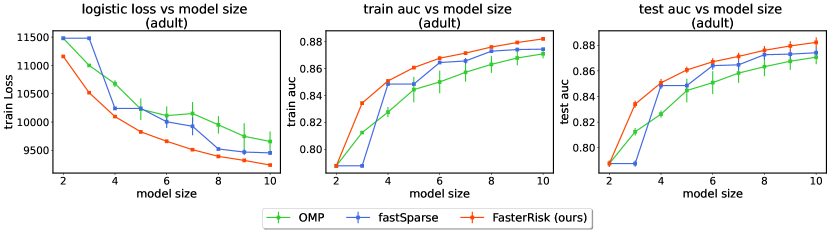

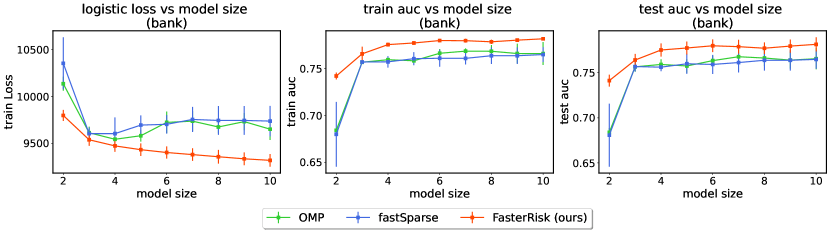

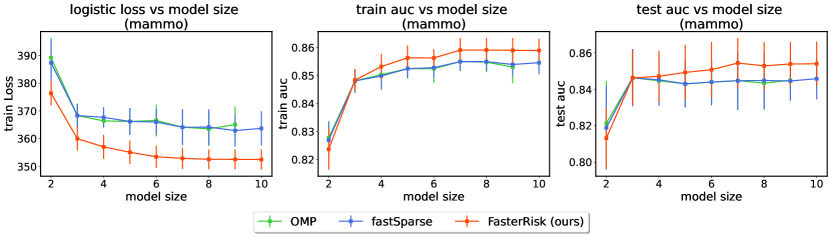

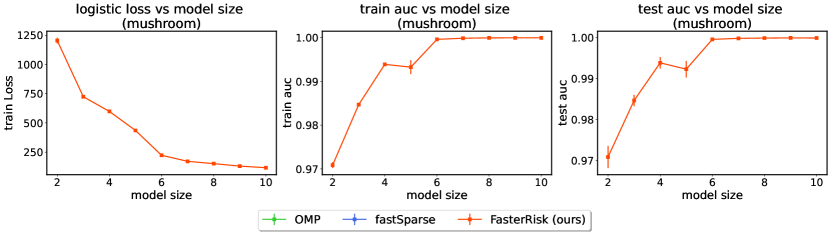

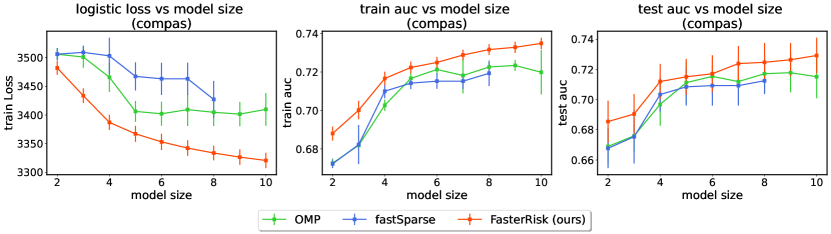

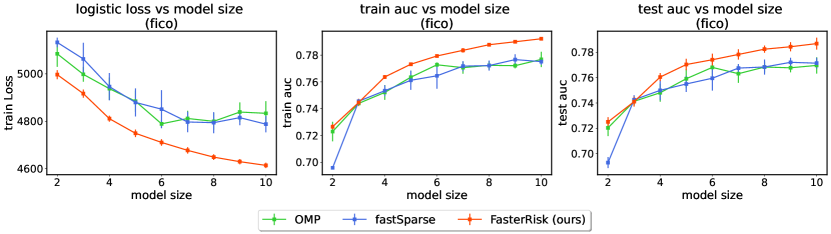

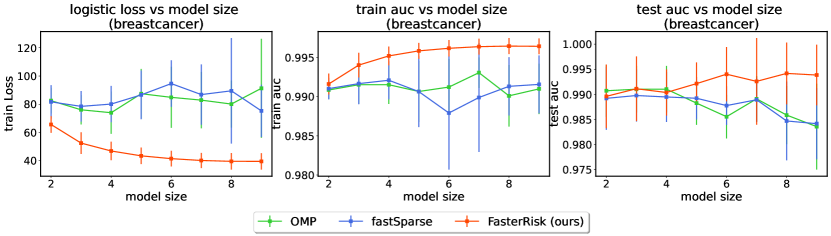

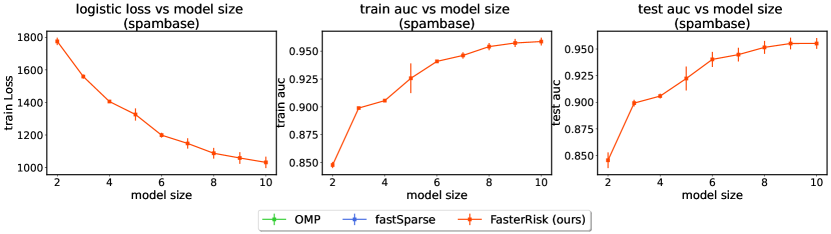

E.6 Comparison of SparseBeamLR with OMP and fastSparse

We next study how effective SparseBeamLR is in producing continuous sparse coefficients under the sparsity and box constraints. We compare with two existing methods, OMP [14] and fastSparse [24]. OMP stands for Orthogonal Matching Pursuit, which expands the support by selecting the next feature with the largest magnitude of partial derivative. fastSparse tries to solve the logistic loss objective with an regularization. For fastSparse, we use the default values (coefficient for the regularization) internally selected by the software. Specifically, the software first apply a large value to produce a super-sparse solution (with support size equal to 1 or close to 1). Then, in the solution path, the value is sequentially decreased until the produced sparse model violates the model size constraint.

The results are shown in Figure 13-15. Although OMP and fastSparse can somtimes produce high-quality solutions on some model size instances and datasets, SparseBeamLR is the only method that consistently produces high-quality sparse solutions in all cases.

OMP’s solution quality is usually worse than that of SparseBeamLR, and OMP could not produce coefficients that satisfy the box constraints on the mushroom and spambase datasets.

fastSparse also cannot produce coefficients that satisfy the box constraints on the mushroom and spambase datasets. Additionally, it is hard to control the regularization to produce the exact model size desired. In Figure 14, we do not obtain any model with model size equal to or in the solution path.

The limitations of OMP and fastSparse stated above are our main motivations for developing the SparseBeamLR method.

E.7 Comparison of FasterRisk with OMP (or fastSparse) Sequential Rounding

Having compared the continuous sparse solutions, we next compare the integer sparse solutions produced by OMP, fastSparse, and FasterRisk. After obtaining the continuous sparse solutions from OMP and fastSparse from Section E.6, we round the continuous coefficients to integers using the Sequential Rounding method as stated in Method 5 of D.3.

The results are shown in Figure 16-18. FasterRisk consistently outperforms the other two methods, due to higher quality of continuous sparse solutions and the use of multipliers.

E.8 Running RiskSLIM Longer

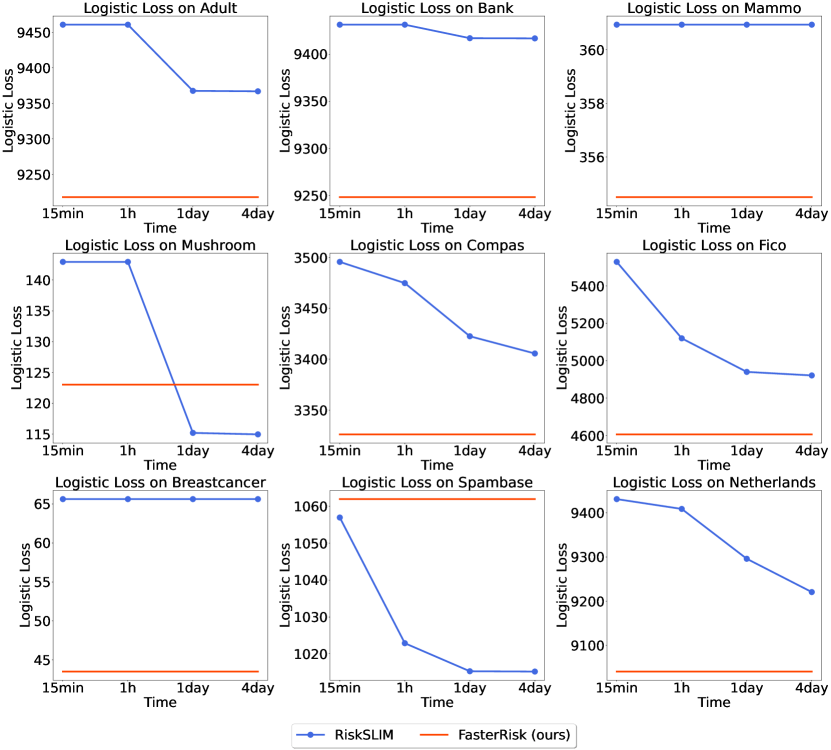

The experiments in Section 4 imposed a 900-second timeout, and RiskSLIM frequently did not complete within the 900 seconds. Here, we run RiskSLIM with longer timeouts (1 hour, and 4 days). We find that even with these long runtimes, FasterRisk still outperforms RiskSLIM in both solution quality and runtime.

Runtime is important for two reasons: (1) We may not be able to compute the answer at all using the slow method because it does not scale to reasonably-sized datasets. It could take a week or more to compute the solution for even reasonably small datasets. We will show this shortly through experiments. (2) Machine learning in the wild is never a single run of an algorithm. Often, users want to explore the data and adjust various constraints as they become more familiar with possible models. A fast speed allows users to go through this iteration process many times without lengthy interruptions between runs. This is where FasterRisk will be very useful in high stakes offline settings. FasterRisk’s pool of models is generated within 5 minutes, and interacting with the pool is essentially instantaneous after it is generated.

E.8.1 Solution Quality of Running RiskSLIM for 1 hour

We ran RiskSLIM for a time limit of 1 hour on all 5 folds and all model sizes (2-10). Thus, we ran experiments for 2 days per dataset. As a reminder, our method FasterRisk runs in less than 5 minutes (on all datasets). The results of logistic loss on the training set, AUC on the training set, and AUC on the test set are in Figures 19-21. FasterRisk still outperforms RiskSLIM in almost all cases, because it uses a larger search space.

E.8.2 Time Comparison of Running RiskSLIM for 1 hour

We plot the running time comparison between FasterRisk and RiskSLIM (with a time limit of 1 hour). The original time results with the 15-minute time limit are shown in Figure 5 and Figure 8.

E.8.3 Solution Quality of Running RiskSLIM for Days

We report results of running the baseline RiskSLIM for 4 days. Due to this long running time demand on our servers, we could not run this experiment on all folds and all model sizes, so we only run on the 3rd fold of the 5-CV split. We plot the logistic loss progression over time.

The results are shown in Figure 23. We see that FasterRisk still achieves lower loss than RiskSLIM even after letting RiskSLIM run for 4 days, again because FasterRisk uses a larger model class. The only exceptions are on the Mushroom and the Spambase datasets, where the logistic losses are close to each other.

The major disadvantage of letting an algorithm run for days is that it is challenging to interact with the algorithm, because one has to wait for the results between interactions – ideally this process would be instantaneous. Furthermore, there could be memory issues for the MIP solver if we let it run for days since the branch-and-bound tree could become too large.

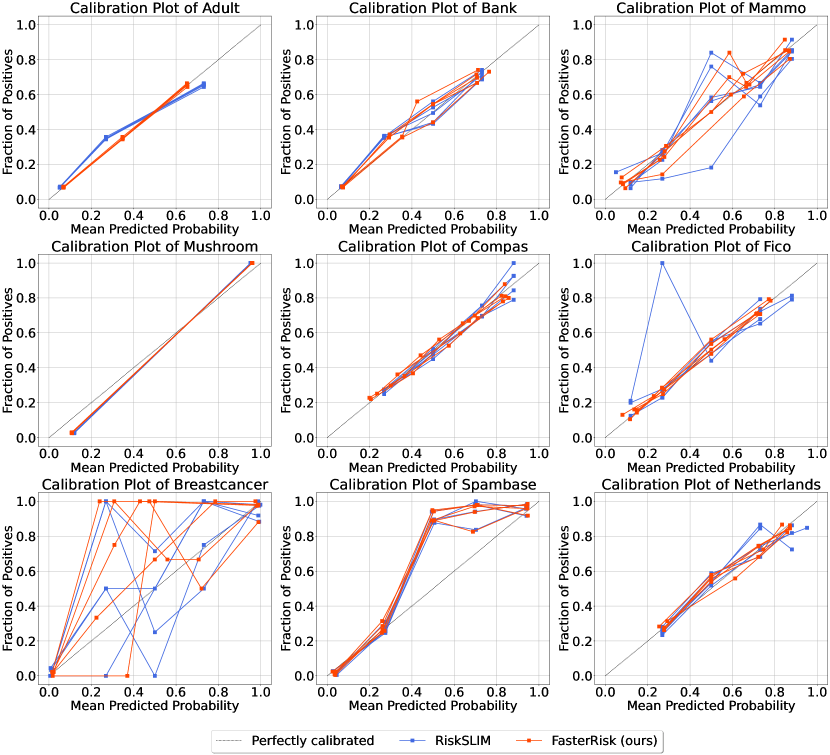

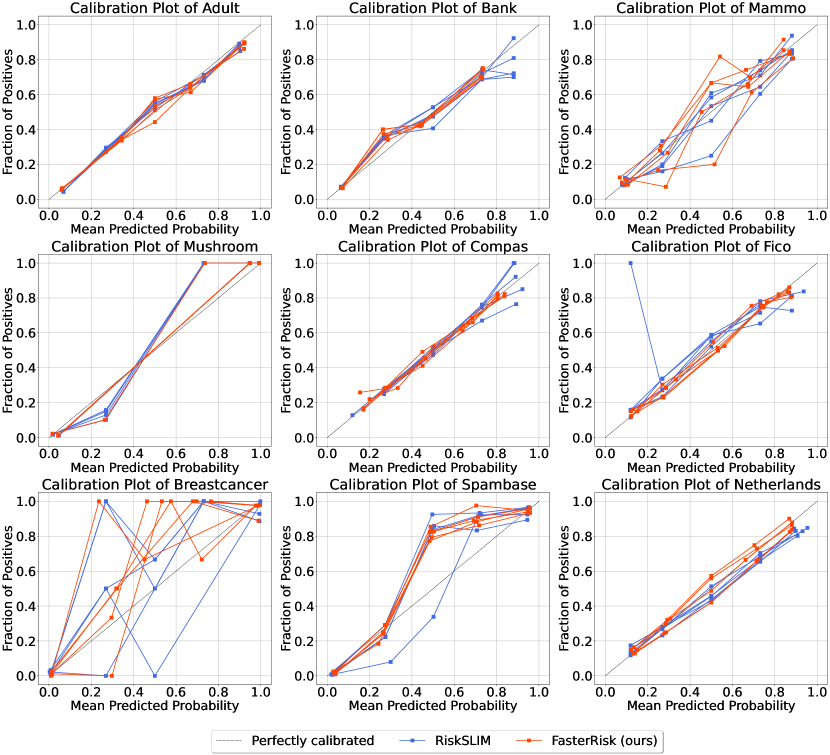

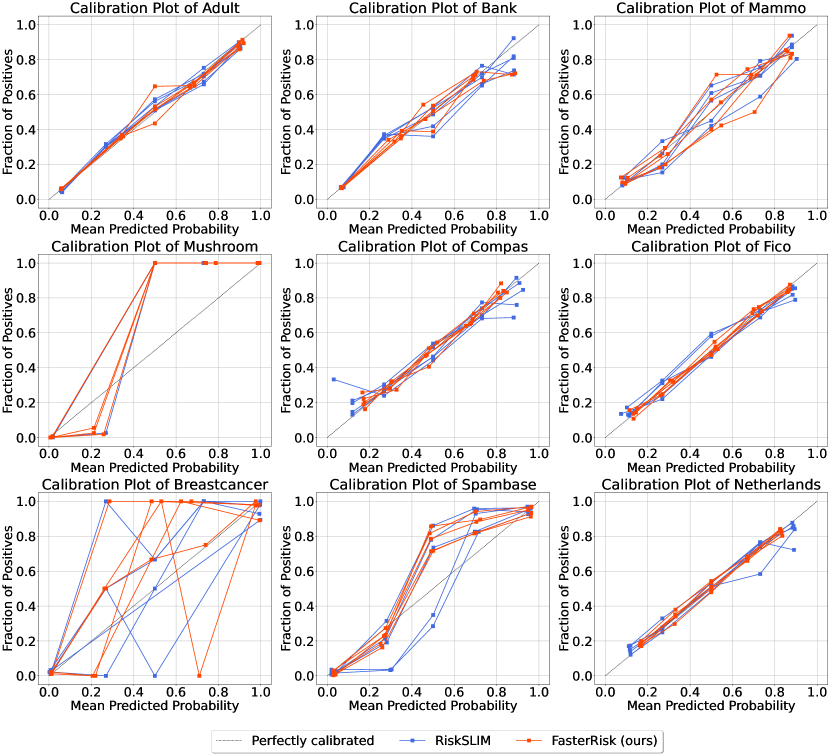

E.9 Calibration Curves

The calibration curves for RiskSLIM and FasterRisk are shown in Figures 24-26 with model sizes equal to 3, 5, and 7, respectively. We use the sklearn package333https://scikit-learn.org/stable/modules/generated/sklearn.calibration.calibration_curve.html from python to plot the figures. We use the default value for the number of bins (number of bins is 5) and the default strategy to define the widths of the bins (the strategy is “uniform”).

The calibration curves on the breastcancer and mammo datasets are more spread out than those on the other datasets. This is perhaps due to the limited number of samples in these datasets (both datasets have fewer than 1000 samples in total; see Table 2), which increases the variance in the calculation of the curves.

On other datasets, both methods have good calibration curves, showing consistency between predicted score and actual risk. However, as shown in Figures 19-21, FasterRisk has higher AUC scores, which means our method has higher discrimination ability than RiskSLIM.

E.10 Hyperparameter Perturbation Study

E.10.1 Perturbation Study on Beam Size

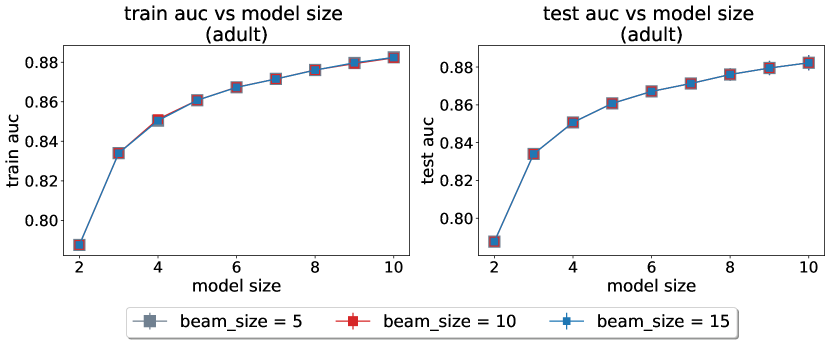

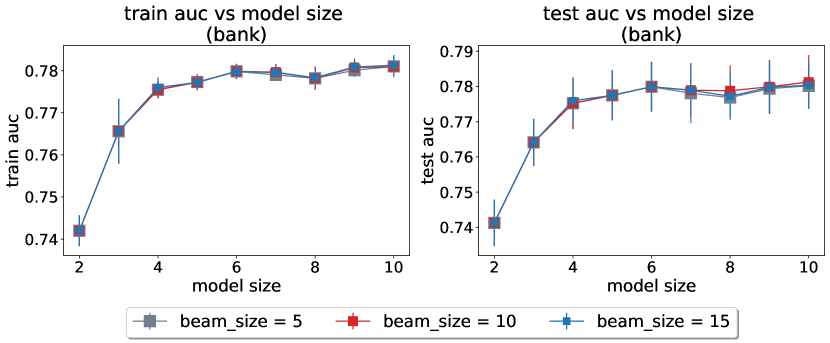

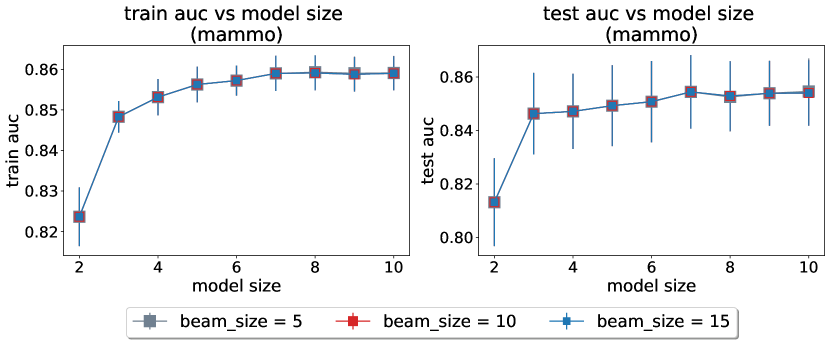

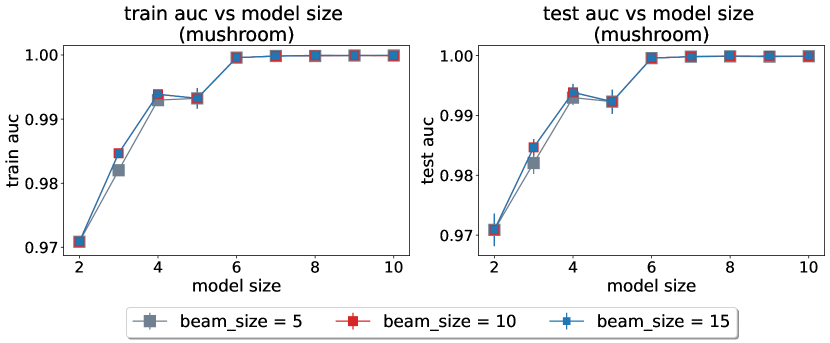

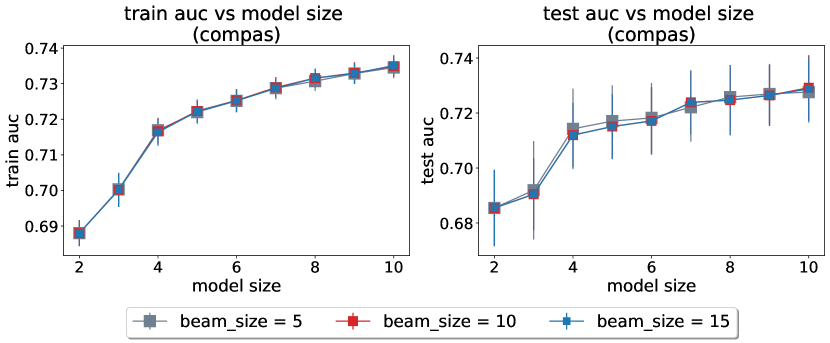

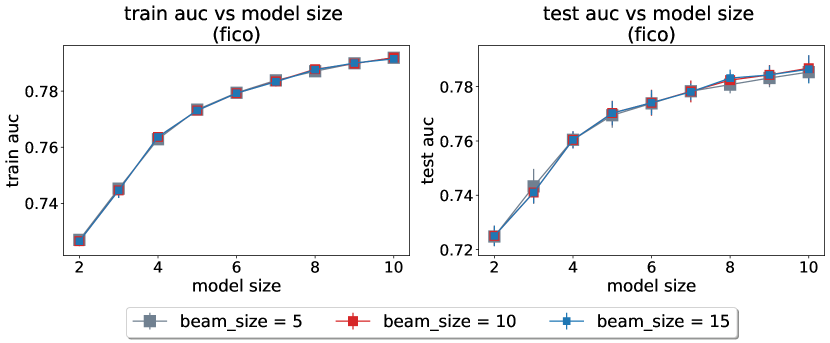

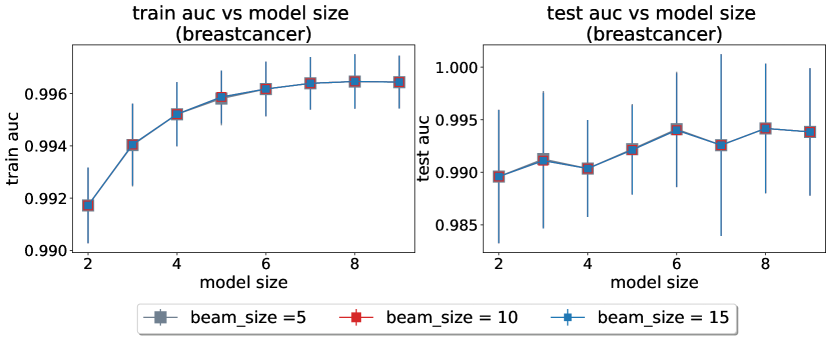

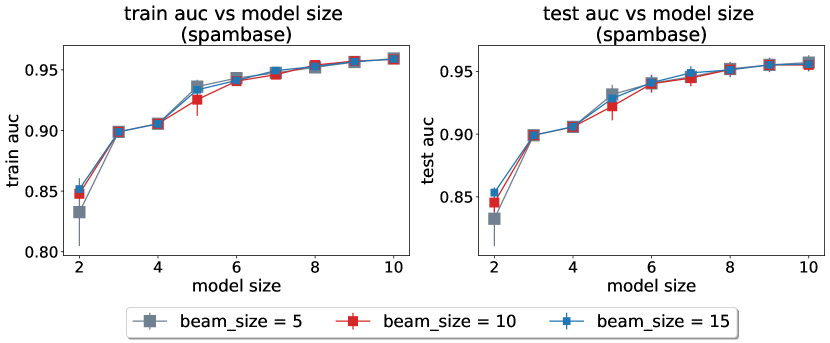

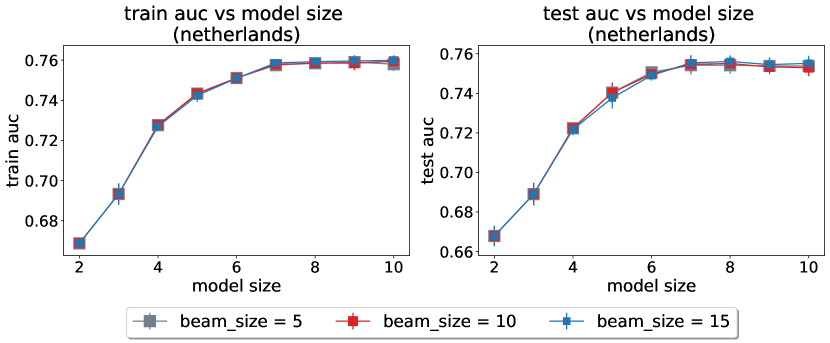

We perform a perturbation study on the hyperparameter beam size as mentioned in Appendix D.4. We set the beam size to 5, 10, and 15, respectively. The results are shown in Figures 27-29. The curves greatly overlap, confirming our previous claim that the performance is not particularly sensitive to the choice of .

E.10.2 Perturbation Study on Tolerance Level for Sparse Diverse Pool

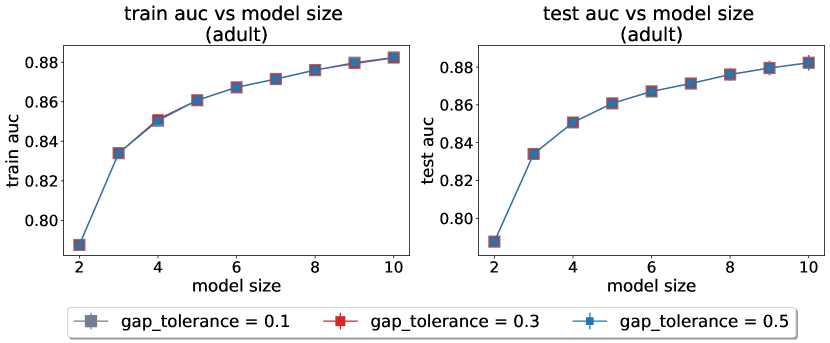

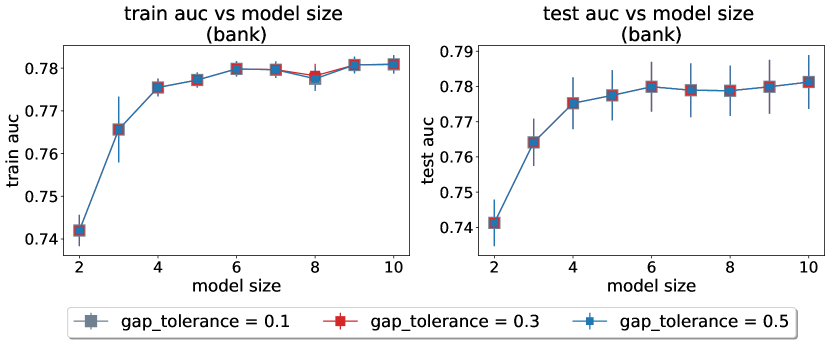

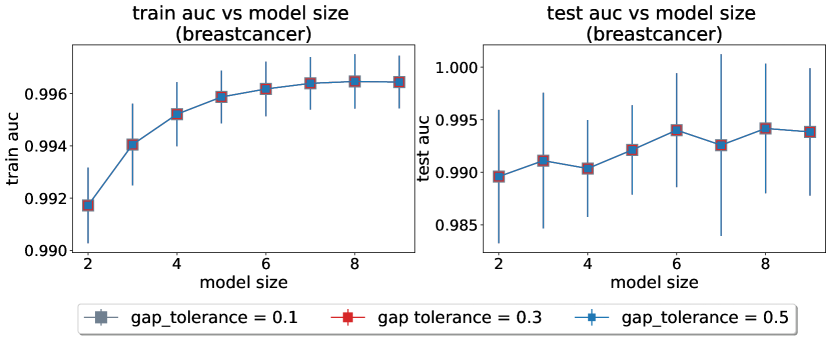

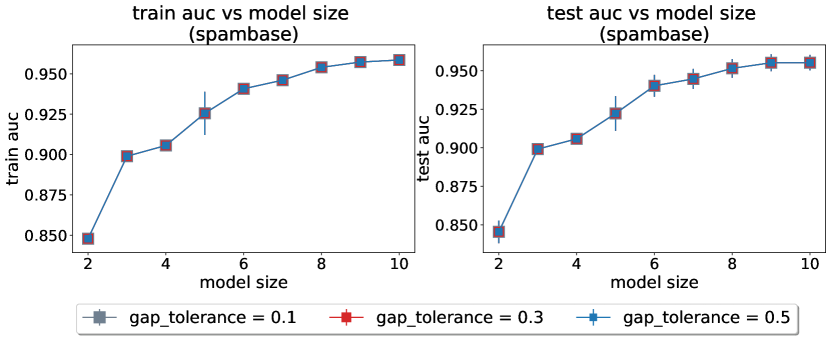

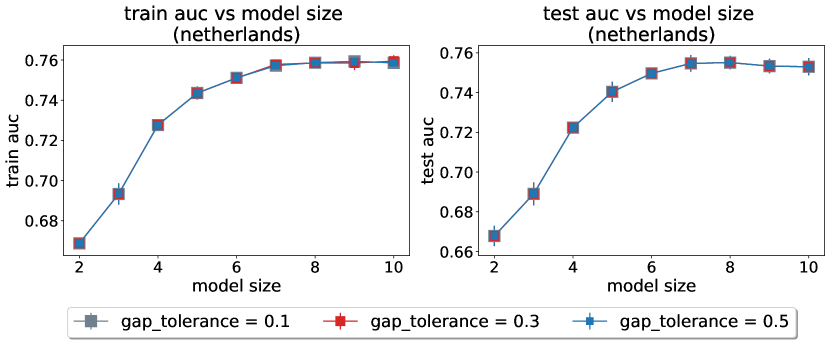

We perform a perturbation study on the hyperparameter tolerance level, , as mentioned in Appendix D.4. We set the tolerance level to 0.1, 0.3, and 0.5, respectively. The results are shown in Figures 30-32. The curves greatly overlap, confirming our previous claim that the performance is not particularly sensitive to the choice of value.

E.10.3 Perturbation Study on Number of Attempts for Sparse Diverse Pool

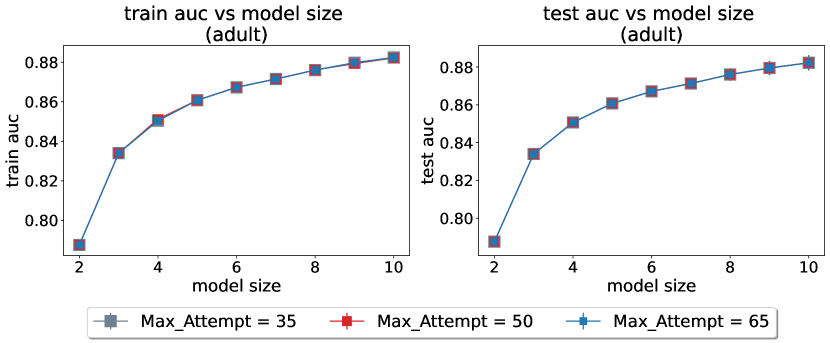

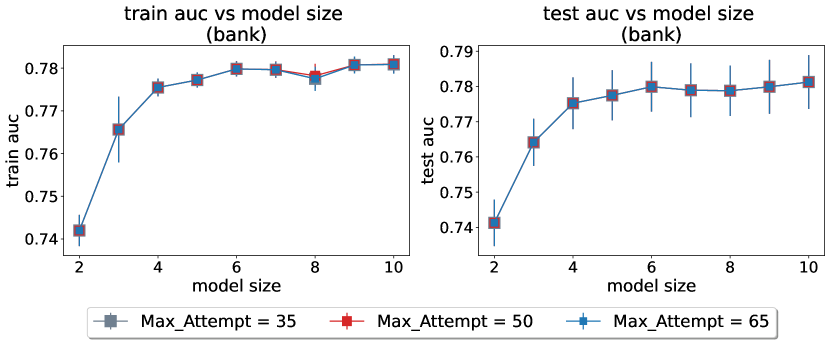

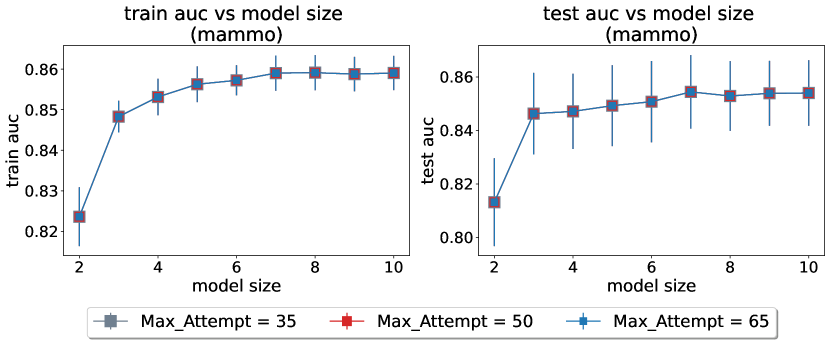

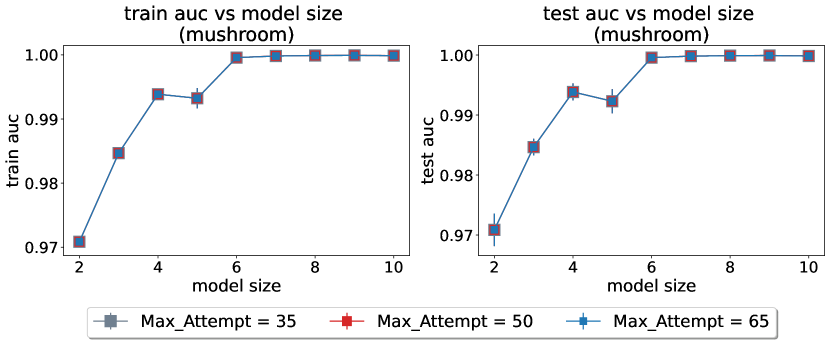

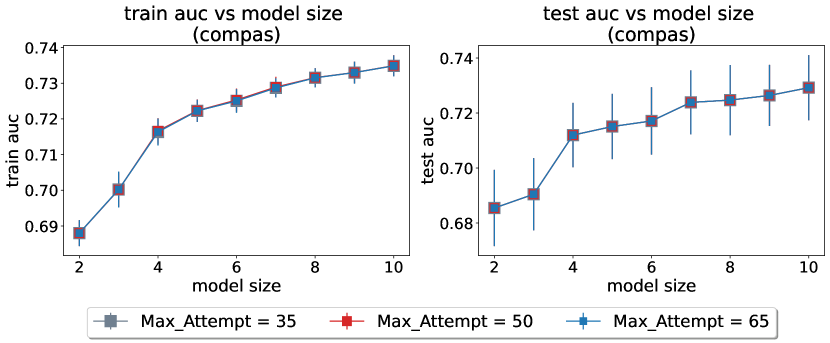

We perform a perturbation study on the hyperparameter for the number of attempts, , as mentioned in Appendix D.4. We have set the number of attempts to 35, 50, and 65, respectively. The results are shown in Figures 33-35. The curves greatly overlap, confirming our previous claim that the performance is not particularly sensitive to the choice of value for the hyperparameter.

E.10.4 Perturbation Study on Number of Multipliers

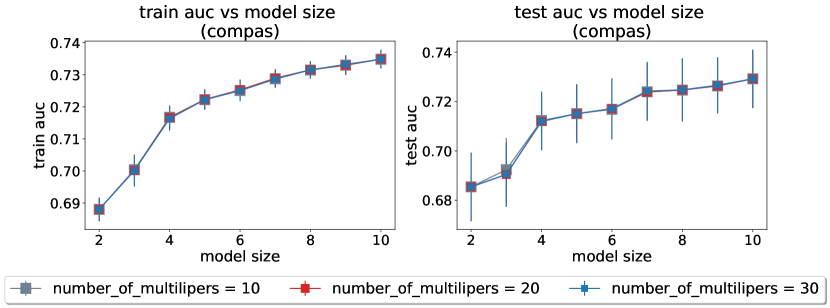

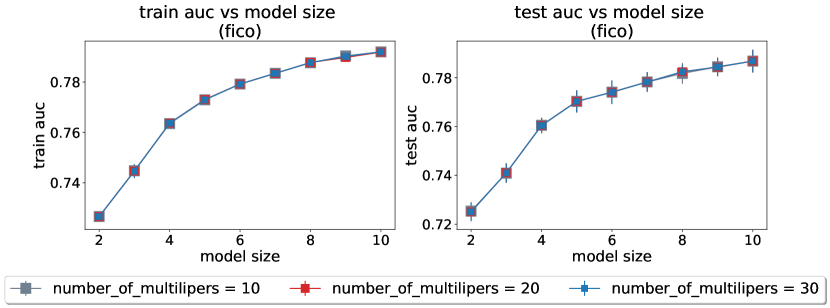

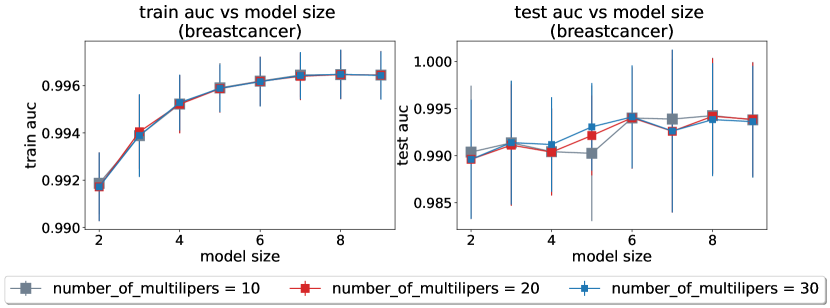

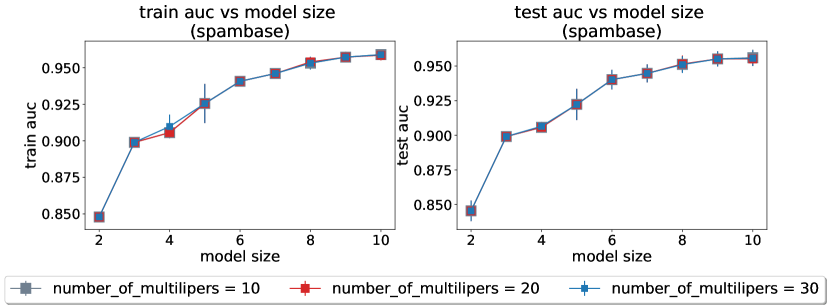

We perform a perturbation study on the hyperparameter for the number of multipliers, , as mentioned in Appendix D.4. We have set the number of multipliers to 10, 20, and 30, respectively. The results are shown in Figures 36-38. The curves greatly overlap, confirming our previous claim that the performance is not particularly sensitive to the choice of values for .

E.11 Comparison with Baseline AutoScore

We compare with the baseline AutoScore [44]. We set the number of features from 2 to 10 and use all other hyperparameters in the default setting. The results of training AUC and test AUC are shown in Figures 39-41. The plots of RiskSLIM are from experiments where we let RiskSLIM run for 1 hour. FasterRisk outperforms both RiskSLIM and AutoScore.

Appendix F Additional Risk Score Models

We provide additional risk score models for the readers to inspect.

Appendix F.1 shows risk scores with different model sizes on different datasets.

Appendix F.2 shows different risk scores with the same size from the diverse pool of solutions.

Specifically, Appendix F.2.1 shows different risk scores on the bank dataset (financial application), Appendix F.2.2 shows different risk scores on the mammo dataset (medical application), and Appendix F.2.3 shows different risk scores on the Netherlands dataset (criminal justice application).

F.1 Risk Score Models with Different Sizes

We also include a large model with size on the FICO dataset, please see Table 30.

| 1. | no high school diploma | -4 points | … | |

| 2. | high school diploma only | -2 points | + | … |

| 3. | married | 4 points | + | … |

| SCORE | = |

| SCORE | -4 | -2 | 0 | 2 | 4 |

|---|---|---|---|---|---|

| RISK | 1.2% | 4.1% | 13.1% | 34.7% | 65.3% |

| 1. | Call in Second Quarter | -2 points | … | |

| 2. | Previous Call Was Successful | 4 points | + | … |

| 3. | Employment Indicator 5100 | 4 points | + | … |

| SCORE | = |

| SCORE | -2 | 0 | 2 | 6 | 8 |

|---|---|---|---|---|---|

| RISK | 2.8% | 6.5% | 14.5% | 50.0% | 70.8% |

| 1. | Irregular Shape | 4 points | … | |

| 2. | Circumscribed Margin | -5 points | + | … |

| 3. | Age 60 | 3 points | + | … |

| SCORE | = |

| SCORE | -5 | -2 | -1 | 2 |

|---|---|---|---|---|

| RISK | 8.2% | 20.1% | 26.2% | 50.0% |

| SCORE | 3 | 4 | 7 |

|---|---|---|---|

| RISK | 58.5% | 66.6% | 84.9% |

| 1. | odoralmond | -5 points | … | |

| 2. | odoranise | -5 points | + | … |

| 3. | odornone | -5 points | + | … |

| SCORE | = |

| SCORE | -5 | 0 |

|---|---|---|

| RISK | 10.8% | 96.0% |

| 1. | prior_counts | -4 points | … | |

| 2. | prior_counts | -4 points | + | … |

| 3. | age | 4 points | + | … |

| SCORE | = |

| SCORE | -8 | -4 | 0 | 4 |

|---|---|---|---|---|

| RISK | 23.6% | 44.1% | 67.0% | 83.9% |

| 1. | MSinceMostRecentInqexcl7days | 3 points | … | |

| 2. | ExternalRiskEstimate | 5 points | + | … |

| 3. | ExternalRiskEstimate | 5 points | + | … |

| SCORE | = |

| SCORE | 0 | 3 | 5 | 8 | 10 |

|---|---|---|---|---|---|

| RISK | 13.7% | 24.0% | 33.4% | 50.0% | 61.3% |

| 1. | Clump Thickness | 3 points | … | |

| 2. | Uniformity of Cell Size | 5 points | + | … |

| 3. | Bare Nuclei | 3 points | + | … |

| SCORE | = |

| SCORE | 33 | 36 | 39 | 42 | 45 |

|---|---|---|---|---|---|

| RISK | 3.3% | 6.1% | 10.8% | 18.6% | 30.1 |

| SCORE | 48 | 51 | 54 | 57 | 60 |

| RISK | 67.0% | 77.6% | 85.5% | 91.0 | 94.5% |

| 1. | WordFrequency_Remove | 5 points | … | |

| 2. | WordFrequency_HP | -2 points | + | … |

| 3. | CharacterFrequency_$ | 5 points | + | … |

| SCORE | = |

| SCORE | -4 | -3 | -2 | -1 | 0 |

| RISK | 0.4% | 1.3% | 3.7% | 10.2% | 25.2% |

| SCORE | 1 | 2 | 3 | 4 | 5 |

| RISK | 50.0% | 74.8% | 89.8% | 96.3% | 98.7% |

| 1. | previous case | -5 points | … | |

| 2. | previous case or previous case | -4 points | + | … |

| 3. | # of previous penal cases | -2 points | + | … |

| SCORE | = |

| SCORE | -7 | -6 | 0 | |

|---|---|---|---|---|

| RISK | 50% | 74.6% | 83.4% | 99.2% |

| 1. | no high school diploma | -4 points | … | |

| 2. | high school diploma only | -2 points | + | … |

| 3. | age 22 to 29 | -2 points | + | … |

| 4. | any capital gains | 3 points | + | … |

| 5. | married | 4 points | + | … |

| SCORE | = |

| SCORE | -4 | -3 | -2 | -1 | 0 |

|---|---|---|---|---|---|

| RISK | 1.3% | 2.4% | 4.4% | 7.8% | 13.6% |

| SCORE | 1 | 2 | 3 | 4 | 7 |

| RISK | 22.5% | 35.0% | 50.5% | 65.0% | 92.2% |

| 1. | Call in Second Quarter | -2 points | … | |

| 2. | Previous Call Was Successful | 4 points | + | … |

| 3. | Previous Marketing Campaign Failed | -1 points | + | … |

| 4. | Employment Indicator 5100 | -5 points | + | … |

| 5. | 3 Month Euribor Rate 100 | -2 points | + | … |

| SCORE | = |

| SCORE | -5 | -4 | -3 | -2 | -1 |

|---|---|---|---|---|---|

| RISK | 11.2% | 15.1% | 20.1% | 26.2% | 33.4% |

| SCORE | 0 | 1 | 2 | 3 | 4 |

| RISK | 41.5% | 50.0% | 58.5% | 66.6% | 73.8% |

| 1. | Oval Shape | -2 points | |

| 2. | Irregular Shape | 4 points | |

| 3. | Circumscribed Margin | -5 points | |

| 4. | Spiculated Margin | 2 points | |

| 5. | Age 60 | 3 points | |

| SCORE |

| SCORE | -7 | -5 | -4 | -3 | -2 | -1 |

|---|---|---|---|---|---|---|

| RISK | 6.0% | 10.6% | 13.8% | 17.9% | 22.8% | 28.6% |

| SCORE | 0 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|

| RISK | 35.2% | 42.4% | 50.0% | 57.6% | 64.8% | 71.4% |

| 1. | odoralmond | -5 points | … | |

| 2. | odoranise | -5 points | + | … |

| 3. | odornone | -5 points | + | … |

| 4. | odorfoul | 5 points | + | … |

| 5. | gill sizebroad | -3 points | + | … |

| SCORE | = |

| SCORE | -8 | -5 | -3 | 2 |

|---|---|---|---|---|

| RISK | 1.62% | 26.4% | 73.6% | >99.8% |

| 1. | prior_counts | -5 points | … | |

| 2. | prior_counts | -5 points | + | … |

| 3. | prior_counts | -3 points | + | … |

| 4. | age 33 | 4 points | + | … |

| 5. | age 23 | 5 points | + | … |

| SCORE | = |

| SCORE | -10 | -9 | -6 | -5 | -4 |

|---|---|---|---|---|---|

| RISK | 25.9% | 29.4% | 41.3% | 45.6% | 50.0% |

| SCORE | -2 | -1 | 3 | 4 | 9 |

| RISK | 58.7% | 62.8% | 77.3% | 80.2% | 90.7% |

| 1. | MSinceMostRecentInqexcl7days | -4 points | … | |

| 2. | MSinceMostRecentInqexcl7days | 2 points | + | … |

| 3. | NumSatisfactoryTrades | 2 points | + | … |

| 4. | ExternalRiskEstimate | 3 points | + | … |

| 5. | ExternalRiskEstimate | 3 points | + | … |

| SCORE | = |

| SCORE | -2 | 0 | 1 | 2 | 3 |

|---|---|---|---|---|---|

| RISK | 6.7% | 13.2% | 18.2% | 24.4% | 32.0% |

| SCORE | 4 | 5 | 6 | 8 | 10 |

| RISK | 40.7% | 50.0% | 59.3% | 75.5% | 86.8% |

| 1. | Clump Thickness | 5 points | … | |

| 2. | Uniformity of Cell Size | 4 points | + | … |

| 3. | Marginal Adhesion | 3 points | + | … |

| 4. | Bare Nuclei | 4 points | + | … |

| 5. | Normal Nucleoli | 3 points | + | … |

| SCORE | = |

| SCORE | 55 | 60 | 65 | 70 | 75 |

|---|---|---|---|---|---|

| RISK | 8.6% | 14.6% | 23.5% | 35.7% | 50.0 |

| SCORE | 80 | 85 | 90 | 95 | 100 |

| RISK | 64.3% | 76.5% | 85.4% | 91.4 | 95.0% |

| 1. | WordFrequency_Remove | 5 points | … | |

| 2. | WordFrequency_Free | 2 points | … | |

| 3. | WordFrequency_0 | 5 points | + | … |

| 4. | WordFrequency_HP | -2 points | + | … |

| 5. | WordFrequency_George | -2 points | + | … |

| SCORE | = |

| SCORE | -4 | -3 | -2 | -1 | 0 |

| RISK | 0.6% | 1.6% | 4.4% | 11.4% | 26.4% |

| SCORE | 1 | 2 | 3 | 4 | 5 |

| RISK | 50.0% | 73.6% | 88.6% | 95.6% | 98.4% |

| 1. | previous case | -5 points | … | |

| 2. | previous case or previous case | -3 points | + | … |

| 3. | # of previous penal cases | -2 points | + | … |

| 4. | age in years | 1 points | + | … |

| 5. | age at first penal case | 1 points | + | … |

| SCORE | = |

| SCORE | -9 | -8 | -7 | -6 | -5 | -4 |

|---|---|---|---|---|---|---|

| RISK | 23.8% | 35.8% | 50.0% | 64.2% | 76.2% | 85.1% |

| SCORE | -3 | -2 | -1 | 0 | 1 | 2 |

| RISK | 91.1% | 94.8% | 97.0% | 98.3% | 99.1% | 99.5% |

| 1. | Age 22 to 29 | -2 points | … | |

| 2. | High School Diploma Only | -2 points | + | … |

| 3. | No High school Diploma | -4 points | … | |

| 4. | Married | 4 points | + | … |

| 5. | Work Hours Per Week 50 | -2 points | + | … |

| 6. | Any Capital Gains | 3 points | + | … |

| 7. | Any Capital Loss | 2 points | + | … |

| SCORE | = |

| SCORE | -5 | -4 | -3 | -2 | -1 |

|---|---|---|---|---|---|

| RISK | 0.8% | 1.4% | 2.6% | 4.6% | 8.1% |

| SCORE | 0 | 2 | 3 | 4 | 7 |

| RISK | 14.0% | 35.3% | 50.0% | 64.7% | 91.9% |

| 1. | Blue Collar Job | -1 points | … | |

| 2. | Call in Second Quarter | -2 points | + | … |

| 3. | Previous Call Was Successful | 3 points | + | … |

| 4. | Previous Marketing Campaign Failed | -1 points | + | … |

| 5. | Employment Indicator 5100 | -5 points | + | … |

| 6. | Consumer Price Index 93.5 | 1 points | + | … |

| 7. | 3 Month Euribor Rate 100 | -1 points | + | … |

| SCORE | = |

| SCORE | -5 | -4 | -3 | -2 | -1 |

|---|---|---|---|---|---|

| RISK | 7.9% | 11.5% | 16.3% | 22.7% | 30.6% |

| SCORE | 0 | 1 | 2 | 3 | 4 |

| RISK | 39.9% | 50.0% | 60.1% | 69.4% | 77.3% |

| 1. | Lobular Shape | 2 points | … | |

| 2. | Irregular Shape | 5 points | + | … |

| 3. | Circumscribed Margin | -4 points | + | … |

| 4. | Obscured Margin | -1 points | + | … |

| 5. | Spiculated Margin | 1 points | + | … |

| 6. | Age 30 | -5 points | + | … |

| 7. | Age 60 | 3 points | + | … |

| SCORE | = |

| SCORE | -1 | 0 | 1 | 2 | 3 |

|---|---|---|---|---|---|

| RISK | 19.8% | 25.9% | 33.2% | 41.3% | 50.0% |

| SCORE | 4 | 5 | 6 | 8 | 9 |

| RISK | 58.7% | 66.8% | 74.1% | 85.2% | 89.1% |

| 1. | odoranise | -5 points | … | |

| 2. | odornone | -5 points | + | … |

| 3. | odorfoul | 5 points | + | … |

| 4. | gill sizenarrow | 4 points | + | … |

| 5. | stalk surface above ringgrooves | 2 points | + | … |

| 6. | spore print colorgreen | 5 points | + | … |

| SCORE | = |

| SCORE | -5 | 0 | 2 | 4 | 5 |

|---|---|---|---|---|---|

| RISK | 0.5% | 50.0% | 89.2% | 98.6% | 99.5% |

| 1. | prior_counts | -3 points | … | |

| 2. | prior_counts | -3 points | + | … |

| 3. | prior_counts | -2 points | + | … |

| 4. | age 52 | 2 points | + | … |

| 5. | age 33 | 2 points | + | … |

| 6. | age 23 | 2 points | + | … |

| 7. | age 20 | 4 points | + | … |

| SCORE | = |

| SCORE | -8 | -6 | -4 | -3 | -2 | -1 | 0 |

| RISK | 11.3% | 18.7% | 29.3% | 35.7% | 42.7% | 50.0% | 57.3% |

| SCORE | 1 | 2 | 3 | 4 | 6 | 7 | 10 |

| RISK | 64.3% | 70.7% | 76.4% | 81.3% | 88.7% | 91.3% | 96.2% |

| 1. | MSinceMostRecentInqexcl7days | -4 points | … | |

| 2. | MSinceMostRecentInqexcl7days | 2 points | + | … |

| 3. | NetFractionRevolvingBurden | -2 points | + | … |

| 4. | ExternalRiskEstimate | 2 points | + | … |

| 5. | ExternalRiskEstimate | 2 points | + | … |

| 6. | AverageMInFile | 2 points | + | … |

| 7. | PercentTradesNeverDelq | 2 points | + | … |

| SCORE | = |

| SCORE | -4 | -2 | 0 | 2 | 4 | 6 | 8 | 10 |

|---|---|---|---|---|---|---|---|---|

| RISK | 8.0% | 14.9% | 26.0% | 41.4% | 58.6% | 74.0% | 85.1% | 92.0% |

| 1. | Clump Thickness | 4 points | … | |

| 2. | Uniformity of Cell Shape | 3 points | + | … |

| 3. | Marginal Adhesion | 3 points | + | … |

| 4. | Bare Nuclei | 3 points | + | … |

| 5. | Bland Chromatin | 3 points | + | … |

| 6. | Normal Nucleoli | 2 points | + | … |

| 7. | Mitoses | 4 points | + | … |

| SCORE | = |

| SCORE | 55 | 60 | 65 | 70 | 75 |

|---|---|---|---|---|---|

| RISK | 5.1% | 9.3% | 16.2% | 26.6% | 40.6 |

| SCORE | 80 | 85 | 90 | 95 | 100 |

| RISK | 56.3% | 70.8% | 82.1% | 89.6 | 94.2% |

| 1. | WordFrequency_Remove | 4 points | … | |

| 2. | WordFrequency_Free | 2 points | … | |

| 3. | WordFrequency_Business | 1 points | + | … |

| 4. | WordFrequency_0 | 4 points | + | … |

| 5. | WordFrequency_HP | -2 points | + | … |