Benefits of Permutation-Equivariance in

Auction Mechanisms

Abstract

Designing an incentive-compatible auction mechanism that maximizes the auctioneer’s revenue while minimizes the bidders’ ex-post regret is an important yet intricate problem in economics. Remarkable progress has been achieved through learning the optimal auction mechanism by neural networks. In this paper, we consider the popular additive valuation and symmetric valuation setting; i.e., the valuation for a set of items is defined as the sum of all items’ valuations in the set, and the valuation distribution is invariant when the bidders and/or the items are permutated. We prove that permutation-equivariant neural networks have significant advantages: the permutation-equivariance decreases the expected ex-post regret, improves the model generalizability, while maintains the expected revenue invariant. This implies that the permutation-equivariance helps approach the theoretically optimal dominant strategy incentive compatible condition, and reduces the required sample complexity for desired generalization. Extensive experiments fully support our theory. To our best knowledge, this is the first work towards understanding the benefits of permutation-equivariance in auction mechanisms.

1 Introduction

Optimal auction design [30] has wide applications in economics, including computational advertising [18], resource allocation [16], and supply chain [4]. In an auction, every bidder has a private valuation profile over all items, and accordingly, submits her bid profile. An auctioneer collects the bids from all bidders, and determines a feasible item allocation to the bidders as well as the prices the bidders need to pay. Consequently, every bidder receives her utility. From the auctioneer’s perspective, the optimal auction mechanism is required to maximize her revenue, defined as the sum of all bidders’ payments. From the aspect of the bidders, the optimal auction mechanism needs to incentivize every bidder to bid their truthful valuation profiles (truthful bidding). This is summarized as the dominant strategy incentive compatible (DSIC) condition; i.e., truthful bidding is always the dominant strategy for every bidder [25].

The optimal auction mechanism can be approximated via neural networks [12, 29, 10]. The “approximation error”, or the “distance” to the DSIC condition, is usually measured by the ex-post regret, defined as the gap between the bidder’s utility of truthful bidding and the utility when her bid profile is only the best to herself (selfish bidding), while the bid profiles of all other bidders are fixed in both cases [12]. When a bidder’s ex-post regret is , truthful bidding is her dominant strategy. Therefore, the optimal auction design can be modeled as a linear programming problem, where the object is to maximize the expected revenue subject to the expected ex-post regret being for all bidders [12]. Another major consideration in learning the optimal mechanism is the generalizability to unseen data, usually measured by the generalization bound, i.e., the upper bound of the gap between the expected revenue/ex-post regret and their empirical counterparts on the training data [12].

In this paper, we consider the popular setting of additive valuation and symmetric valuation [12, 29, 10]. The additive valuation condition defines the valuation for a set of items as the sum of the valuations for all items in this set. The symmetric valuation condition assumes the joint distribution of all bidders’ valuation profiles to be invariant when bidders and/or items are permutated. This setting covers many applications in practice. For example, when items are independent, the additive valuation condition holds. Moreover, if the auction is anonymous or the order of the items is not prior-known, the symmetric valuation condition holds.

We demonstrate that permutation-equivariant models have significant advantages in learning the optimal auction mechanism as follows. (1) We prove that the permutation-equivariance in auction mechanisms decreases the expected ex-post regret while maintaining the expected revenue invariant. Conversely, and equivalently, the permutation-equivariance promises a larger expected revenue, when the expected ex-post regret is fixed. (2) We show that the permutation-equivariance of auction mechanisms reduces the required sample complexity for desirable generalizability. We prove that the -distance between any two mechanisms in the mechanism space decreases when they are projected to the permutation-equivariant mechanism (sub-)space. This smaller distance implies a smaller covering number of the permutation-equivariant mechanism space, which further leads to a small generalization bound [12].

We further provide an explanation for the learning process of non-permutation-equivariant neural networks (NPE-NNs). In learning the optimal auction mechanism by an NPE-NN, we show that an extra positive term exists in the quadratic penalty of the ex-post regret based on the result (1). This term serves as a regularizer to penalize the “non-permutation-equivariance”. Moreover, this regularizer also interferes the revenue maximization, and thus affects the learning performance of NPE-NNs. This further explains the advantages of permutation-equivariance in auction design.

Experiments in extensive auction settings are conducted to verify our theory. We design permutation-equivariant versions of RegretNet (RegretNet-PE and RegretNet-test) by projecting the RegretNet [12] to the permutation-equivariant mechanism space in the training and test stage respectively. The empirical results show that permutation-equivariance helps: (1) significantly improve the revenue while maintain the same ex-post regret; (2) record the same revenue with a significantly lower ex-post regret; and (3) narrow the generalization gaps between the training ex-post regret and its test counterpart. These results fully support our theory.

Related works. Myerson completely solves the optimal auction design problem in one-item auctions [23]. However, solutions are not clear when the number of bidders/items exceeds one [12]. Initial attempts have been presented on the characterization of optimal auction mechanisms [20, 26, 9] and algorithmic solutions [1, 2, 27]. Remarkable advances have been made in the required sample complexity for learning the optimal auction mechanism in various settings, including single-item auctions [5, 21, 16], multi-item single-bidder auctions [11], combinatorial auctions [3, 32], and allocation mechanisms [24]. Machine learning-based auction design (automated auction design) have obtained considerable progress [6, 7, 31]. The optimal auction design is modeled as a linear programming problem [6, 7]. However, early works suffer from the scalability issues that the number of the constraints grows exponentially when the bidder number and the item numbers increase. To address this issue, recent works propose to learn the optimal auction mechanism by deep learning. RegretNet is designed for multi-bidder and multi-item settings [12]. Then, RegretNet is developed to meet more restrictive constraints, such as the budget condition [14] and the certifying strategyproof condition [8]. Rahme et al. [29] propose the first equivariant neural network-based auction mechanism design method with significant empirical advantages. Ivanov et al. [17] propose a RegretFormer which (1) introduces attention layers to RegretNet to learn permutation-equivariant auction mechanisms, and (2) adopts a new interpretable loss function to control the revenue-regret trade-off. Duan et al. [10] extend the applicable domain to contextual settings. All these works make remarkable contributions in designing new algorithms from the empirical aspect only. However, the theoretical foundations are still elusive. To our best knowledge, our paper is the first work on theoretically studying the benefits of permutation equivariance in auction design via deep learning.

2 Notations and Preliminaries

Auction. Suppose bidders are bidding items in an auction. Every bidder has her bidder-context (feature) , while every item is associated with its item-context (feature) . The bidder has a private valuation for the item , which is sampled from a conditioned distribution . The value profile is unknown to the auctioneer. For the simplicity, we define , , , , and .

Every bidder submits a bid profile to the auctioneer according to her valuation profile. Then, the auctioneer determines a feasible item allocation and corresponding payments as per an auction mechanism . Consequently, every bidder receives her utility as

The auction mechanism consists of an allocation rule and a payment rule , where is the probability of allocating item to the bidder , and is the price that the bidder should pay. To avoid allocating an item over once, the allocation rule is constrained such that for all . Every in our notations can be replaced by . Thus, we can define the similar notations: , and .

Optimal auction mechanism. An auction mechanism is defined to be dominant strategy incentive compatible (DSIC), if truthful bidding is always a dominant strategy of every bidder; i.e.,

for all , , and . In addition, an auction mechanism is called individually rational (IR), if for any bidder-contexts , any item-contexts , any bidder , valuation profile and bid profile , truthful bidding always leads to a non-negative utility, i.e.,

If an auction mechanism is DSIC and IR, a rational bidder with an obvious dominant strategy will play it (bidding truthfully). Moreover, an optimal auction mechanism is required to maximize the auctioneer’s expected revenue .

Auction design. The ex-post regret for the bidder is defined as

An auction mechanism is DSIC, if and only if for any value profile , bidder-context , and item-context . Suppose the payment rule satisfies , which implies that each bidder has a non-negative utility. Then, the auction design can be modeled as a linear programming problem that maximizes the expected revenue subject to the expected ex-post regret . Without loss of generality, the ex-post regret may refer to the average of all bidders’ ex-post regrets.

Definition 2.1.

Suppose the network’s parameter is , and the bidder ’s empirical payment and ex-post regret are defined as and , where the sample set is i.i.d. sampled from the following prior distribution, .

Equivariant mapping. We define a mapping as -equivariant if for two chosen group linear representations and and any in group .

Definition 2.2 (Permutation-Equivariant Mapping).

A permutation-equivariant mapping is defined to be that for any instance , and permutation matrices and , we have .

In this paper, we consider the bidder-permutation and item-permutation . Specifically, we define a mapping is bidder-symmetric or item-symmetric, if or , respectively. Moreover, we define an auction mechanism as bidder-symmetric or item-symmetric, if the allocation rule and the payment rule are both bidder-symmetric or item-symmetric.

Orbit averaging. For any feature mapping , the orbit averaging on is defined as where and are two chosen group representations acting on the feature spaces and , respectively. Orbit averaging can project any mapping to be equivariant:

Proposition 2.3.

Orbit averaging is a projection to the equivariant mapping space , i.e., and . In particular, if is already equivariant, then .

Moreover, and refer to the utility and the ex-post regret induced by and . For the simplicity, we denote the orbit averagings that modify the auction mechanism to be bidder-symmetric, item-symmetric, and bidder/item-symmetric by bidder averaging , item averaging , and bidder-item aggregated averaging . Besides, a detailed proof of the feasibility of the projected mechanisms can be found in Appendix A.1.

Hypothesis complexity. The generalizatbility to unseen data is usually measured by the generalization bound, which depends on the hypothesis set’s complexity. To characterize the complexity of the hypothesis set, we introduce the following definitions of covering number and its corresponding distance . Based on the covering number, we can obtain a generalization bound in Theorem 3.6.

Definition 2.4 (-distance).

Let be a feature space and a space of functions from to . The -distance on the space is defined as .

Definition 2.5 (Covering number).

Covering number is the minimum number of balls with radius that can cover under -distance.

3 Theoretical Results

This section presents the theoretical results. For simplicity, we view as a matrix to present the prices the bidders should pay. We first prove that the permutation-equivariance induces the same expected revenue and a smaller expected ex-post regret in Section 3.1. Next in Section 3.2, we prove that the permutation-equivariant mechanism space has a smaller covering number, which promises a smaller required sample complexity and a better generalization. Detailed proofs are omitted from the main text and given in supplementary materials due to space limitation.

3.1 Benefits for Revenue and Ex-Post Regret

In this section, we discuss the benefits for the revenue and the ex-post regret in the conditions of bidder-symmetry and item-symmetry separately, and then discuss the benefits when both of them hold. Based on these results, we also study the learning process of non-permutation-equivariant neural networks for auction design.

3.1.1 Benefits in the Bidder/Item-Symmetry Condition

When the bidders come from the same distribution, the joint valuation distribution is invariant under bidder-permutation, i.e. for any . Meanwhile, when the items are indistinguishable, the joint distribution is invariant under item-permutation, i.e., for any . Both conditions do not always hold simultaneously. In this section, we study them separately.

To measure the “non-permutation-equivariance” of the mechanism, we introduce the conception of regret gap between the projected mechanism and the original mechanism as below,

where is the valuation profiles, is the valuation profile of bidder , is the bidder-context, is the item-context, and the orbit averaging can be the bidder averaging or the item averaging .

The bidder averaging and the item averaging acting on the allocation rule and the payment rule , respectively, are as below,

We thus can prove the following theorem that characterizes the benefits of permutation-equivariance for revenue and ex-post regret in the condition of bidder/item-symmetry.

Theorem 3.1 (Benefits for revenue and ex-post regret in the condition of bidder/item-symmetry).

When the valuation distribution is invariant under permutations of bidders/items, the projected mechanism has the same expected revenue and a smaller expected ex-post regret, that is,

| (1) | |||

| (2) |

where is the payment rule, is the ex-post regret, and is the bidder/item averaging.

A smaller expected ex-post regret implies this mechanism is closer to the dominant strategy incentive compatible condition. Conversely, and equivalently, when the expected ex-post regrets are fixed, the projected auction mechanism has a larger expected revenue. For any auction mechanism, in the bidder/item-symmetry condition, we can project it through the bidder/item averaging.

Remark 3.2.

The mechanism space can be decomposed into the direct sum of the permutation-equivariant mechanism space and the complementary space [13]. Thus, a mechanism has a unique decomposition: . The pure permutation-equivariant part contains all and only the “permutation-equivariance” of the mechanism . The pure non-permutation-equivariant part is independent from the permutation-equivairance. In this way, we may study the influence of permutation-equivariance by comparing the mechanism and its permutation equivariant part .

3.1.2 Interplay between Bidder-Symmetry and Item-Symmetry.

If the valuation distribution is invariant under both bidder-permutation and item-permutation, we can project the mechanism to be permutation-equivariant with respect to both bidder and item in two steps (by mapping or mapping ). Consequently, the projected mechanism has the same expected revenue and a smaller expected ex-post regret. Equivalently, we can also project an auction mechanism to be bidder-symmetric and item-symmetric immediately by the bidder-item aggregated averaging as below,

We can prove that the bidder-item aggregated averaging is the composition of the orbit averaging operators and , as shown in the following lemma. This lemma shows that the order of and would not influence their composition.

Lemma 3.3.

The bidder-item aggregated averaging is the composition of bidder averaging and item averaging:

Based on this lemma, we can prove the following theorem on the benefits of permutation-equivariance for revenue and ex-post regret in the condition of both bidder-symmetry and item-symmetry.

Theorem 3.4 (Benefits for revenue and ex-post regret in the condition of both bidder-symmetry and item-symmetry).

When the valuation distribution is invariant under both item-permutation and item-permutation, then the projected mechanism has a same expected revenue and a smaller expected ex-post regret, that is,

where is the payment rule, is the ex-post regret, and is the bidder-item aggregated averaging.

The difference between bidder-symmetry and item-symmetry is significant in practice. For example, for a symmetric valuation distribution, when the mechanism is already bidder-symmetric but not item-symmetric, we can project it to be item-symmetric to gain an extra benefit from item-symmetry. That means, the two regret gaps induced by and are “additive” as below,

In general, and thus Thus, the benefits from bidder-symmetry and item-symmetry are “additive” but not strictly “independent”.

3.1.3 Insights on Training Non-Permutation-Equivariant Mechanism

Because the expected revenue is always the same for the original mechanism and the projected permutation-equivariant mechanism, we only consider the gradient caused by the expected ex-post regret. We can decompose the original expected ex-post regret into the sum of the expected ex-post regret of the projected mechanism and the expectation of the regret gap as below,

The regret gap follows from the “non-permutation-equivariance” of the mechanism . When the distance tends to , the regret gap converges to . When the auction mechanism has a negligible ex-post regret, the expectation of the regret gap is also close to . That means, the mechanism is close to being permutation-equivariant. However, even using a symmetric dataset or adopting data augmentation in training, the learned mechanism will not be permutation-equivariant in general [19]. As a result, to achieve negligible ex-post regret, the non-permutation-equivariant models need to learn more samples to approach permutation-equivariance. That is because the non-permutation-equivariant part (expected regret gap) would mislead the gradient of the expected regret but have no benefit to the expected revenue and the expected ex-post regret.

On the other hand, the regret gap can be viewed as a regularizer in the ex-post regret to penalize the “non-permutation-equivariance” of the mechanism. When the optimizer tries to minimize the ex-post regret, the auction mechanism approaches to be permutation-equivariant. Therefore, if the mechanism achieves a negligible ex-post regret, it is almost to be permutation-equivariant. This result can explain why RegretNet struggles to find permutation-equivariant auction mechanisms [29]. However, in complex settings, it will be harder for non-permutation-equivariant models to approach the negligible ex-post regret. It can explain why the permutation-equivariant models show a significant improvement in complex settings, compared with that they have similar performances in simple settings [10, 17], which shows the great importance of adopting permutation-equivariant models in complex settings.

3.2 Benefits for Generalization

In this section, we study permutation-equivariance from the aspect of generalizability [22, 15], which characterizes the performance gap of a learned mechanism on collected training data and unseen data.

We first study the covering number of the permutation-equivariant mechanism space. Let and be the spaces of all possible utilities and payment rules, and and the spaces of all projected utilities and payment rules. In addition, let and be the minimum numbers of balls with radius that can cover and under -distance, respectively. We obtain the following result, which indicates the projected permutation-equivariant mechanism space has smaller covering numbers.

Theorem 3.5 (Covering number of the permutation-equivariant mechanism space).

The space of all projected bidder-symmetric mechanisms has smaller covering numbers, that is,

The space of all projected item-symmetric mechanisms has smaller covering numbers, that is,

Intuitively, the orbit averaging narrows the distance between two mechanisms: , for any two mechanisms. Then, any -cover for space or space induces an -cover for space or space .

Combining with Lemma 3.3, we have the following results,

We then prove that two generalization bounds of permutation-equivariant mechanisms, which characterize the gap between the expected revenue/ex-post regret and their empirical counterparts. Similar generalization results are existing in previous works [10, 12].

Theorem 3.6 (Generalization bounds of permutation-equivariant mechanisms).

If for any bidder, her valuation satisfies that for any , then with probability at least , we have the following inequalities with ,

| (3) | |||

| (4) |

where is the number of samples, and are the spaces of all possible utilities and payment rules.

Equivalently, we can rewrite this result in the form of the sample complexity,

Corollary 3.7.

Remark 3.8.

Combining Theorem 3.5, we have proved that the permutation-equivariance can improve the generalizability.

4 Experiments

This section presents our experimental results. More details and results are presented in the supplementary materials.

Model architecture. We project RegretNet [12] to the permutation-equivariant mechanism space via employing bidder-item aggregated averaging for the bidder-symmetry and item-symmetry condition. The projected model is called RegretNet-PE. We also project the well-trained RegretNet, called RegretNet-Test. Specifically, RegretNet is an auction mechanism defined as , in which both the allocation rule and the payment rule are neural networks that consist of three fully-connected layers, and is the overall model parameter of the auction mechanism. The detailed architecture is given in the supplementary materials.

Comparison with EquivariantNet. RegretNet uses two feed-forward fully-connected networks to learn the allocation rule and payment rule, respectively. We denote the weight matrix in the layer as . Both EquivariantNet and RegretNet-PE inherit the architecture of RegretNet (with some modifications), but utilize different approaches to realize the permutation-equivariance. EquivariantNet applies parameter-sharing in every layer during training, to constrain to be equivariant. In contrast, RegretNet-PE employs orbit averaging to be permutation-equivariant. Specifically, RegretNet-PE adopts a weight matrix in the first layer, weight matrices in the following layers, and multiples a matrix to the output layer, where is the scale of the group , represents the permutation operator on bidders and items, is an identity matrix, and is the Kronecker product. It is worth noting that RegretNet-PE is only designed for verifying our theory.

| Method | Uniform | Uniform | Uniform | ||||||

| Revenue | Regret | GE | Revenue | Regret | GE | Revenue | Regret | GE | |

| Optimal | 0 | - | 0 | - | 0 | - | |||

| RegretNet | |||||||||

| RegretNet-Test | - | - | - | ||||||

| RegretNet-PE | |||||||||

| Method | Uniform | Uniform | ||

| Revenue | Regret | Revenue | Regret | |

| RegretNet | ||||

| EquivariantNet | ||||

| RegretNet-Test | ||||

| RegretNet-PE | ||||

Auction settings. We first adopt the two-bidder single-item, two-bidder single-item, three-bidder single-item, and five-bidder single-item settings in the experiments that compare the learned mechanisms with theoretical optimal mechanisms. The optimal auction mechanism for any single-item auction is known [23]. We thus compare the mechanisms leaned by our method with the optimal auction mechanisms in the single-item settings. Also, we compare RegretNet-PE and EquivariantNet in the one-bidder, two-item setting, and the two-bidder, two-item setting. Besides, we employ a multivariate uniform distribution to model the bidder valuation profiles. In all settings, we sample 640,000 data points for training and 5,000 points for test. Due to the space limitation, we place the results of two-bidder five-item and five-bidder three-item settings in Appendix B.2.

Model training. We optimize the auction mechanism model via solving the following optimization problem, following the standard settings [12, 29, 10, 17],

where is the Lagrange multiplier and is the factor of the quadratic regularization term. During the training process, the objective function is minimized via Adam with a learning rate of with respect to the model parameter and the Lagrange multiplier is updated once in every 100 iterations, until the ex-post regret is smaller than . The regularization factor is set to initially and gradually increased along the training process. In calculating the best bid profile of every bidder , we first randomly initialize the bid profiles once in training and 1,000 times in test, optimize each of them individually via Adam with the same settings, and take the best one as the approximated best bidding.

Evaluation. We leverage three metrics to evaluate the performance of the auction mechanism, which are: (1) the empirical revenue , (2) the empirical ex-post regret averaging across all bidders, i.e., , and (3) the generalization error defined on top of regrets, i.e., , where and are the empirical ex-post regrets during test and training, respectively.

Computing resource. The experiments are conducted on 1 GPU (NVIDIA® Tesla® V100 16GB) and 10 CPU cores (Intel® Xeon® Processor E5-2650 v4 @ 2.20GHz).

Experimental results. We train a RegretNet and a RegretNet-PE on the training data. The well-trained RegretNet is then projected to be permutation-equivariant, denoted as “RegretNet-Test”. The results are collected in Tables 1 and 2.

From Tables 1 and 2, we observe that (1) compared to RegretNet, RegretNet-PE has a significantly higher revenue with a lower ex-post regret, and narrows the generalization gap between the training ex-post regret and its test counterpart; (2) compared to RegretNet, RegretNet-Test receives the same revenue with a significantly lower ex-post regret; and (3) under comparable ex-post regrets, RegretNet-PE has considerably higher revenue than EquivariantNet, while all permutation-equivariant models (RegretNet-Test and RegretNet-PE) can outperform RegretNet. These results show significant benefits of permutation-equivariance on revenue, ex-post regret, and generalizability, which fully supports our theoretical findings in Theorems 3.1, 3.4, and 3.5.

5 Conclusion and future works

In this paper, under additive valuation and symmetric valuation setting, we study the benefits of permutation-equivariance in auction mechanisms in two aspects: a better performance and a better generalization. First, we prove a smaller expected ex-post regret and the same expected revenue when projecting a mechanism to be permutation-equivariant. Next, we propose the permutation-equivariant mechanism space has a smaller covering number, which promises the permutation-equivariant models a better generalization. Extensive experiments are conducted to verify our theoretical results. Our results help understand the optimal auction mechanisms’ characterization and the learning processes difference between non-equivariant models and equivariant models.

Beyond the additive valuation setting, an interesting direction is to extend our results to other conditions, including the combinatorial and the unit-demand auctions. Meanwhile, the understanding of the difference in the aspect of the training process between non-equivariant models and equivariant models is still elusive.

Social impact. Our results can help understand and design optimal auction mechanisms for symmetric valuation distribution. As a result, our work could inspire more near-optimal auction mechanisms and promote economic growth. No potential negative social impact is identified.

Acknowledgments and Disclosure of Funding

This work was supported in part by the Major Science and Technology Innovation 2030 “New Generation Artificial Intelligence” Key Project (No. 2021ZD0111700), the National Natural Science Foundation of China (No. 62006137), and the Beijing Outstanding Young Scientist Program (No. BJJWZYJH012019100020098).

We sincerely appreciate Hang Yu, Xiaowen Wei, Kaifan Yang, Shaopeng Fu, and Qingsong Zhang for the valuable comments and the anonymous NeurIPS reviewers for the helpful feedback.

References

- [1] S. Alaei. Bayesian combinatorial auctions: Expanding single buyer mechanisms to many buyers. The 16th Annual Symposium on Foundations of Computer Science, 2011.

- [2] S. Alaei, H. Fu, N. Haghpanah, and J. Hartline. The simple economics of approximately optimal auctions. The 16th Annual Symposium on Foundations of Computer Science,, 2013.

- [3] M.-F. F. Balcan, T. Sandholm, and E. Vitercik. Sample complexity of automated mechanism design. Neural Information Processing Systems (NeurIPS), 2016.

- [4] L. Chen, L. Wang, and Y. Lan. Auction models with resource pooling in modern supply chain management. Modern Supply Chain Research and Applications, 2019.

- [5] R. Cole and T. Roughgarden. The sample complexity of revenue maximization. In ACM symposium on Theory of computing, 2014.

- [6] V. Conitzer and T. Sandholm. Complexity of mechanism design. Proceedings of the Eighteenth Conference on Uncertainty in Artificial Intelligence (UAI), 2002.

- [7] V. Conitzer and T. Sandholm. Self-interested automated mechanism design and implications for optimal combinatorial auctions. In ACM Conference on Electronic Commerce, 2004.

- [8] M. Curry, P.-Y. Chiang, T. Goldstein, and J. Dickerson. Certifying strategyproof auction networks. Neural Information Processing Systems (NeurIPS), 2020.

- [9] C. Daskalakis, A. Deckelbaum, and C. Tzamos. Strong duality for a multiple-good monopolist. Econometrica, 2017.

- [10] Z. Duan, J. Tang, Y. Yin, Z. Feng, X. Yan, M. Zaheer, and X. Deng. A context-integrated transformer-based neural network for auction design. arXiv preprint arXiv:2201.12489, 2022.

- [11] S. Dughmi, L. Han, and N. Nisan. Sampling and representation complexity of revenue maximization. Web and Internet Economic, 2014.

- [12] P. Dütting, Z. Feng, H. Narasimhan, D. Parkes, and S. S. Ravindranath. Optimal auctions through deep learning. In International Conference on Machine Learning (ICML), 2019.

- [13] B. Elesedy and S. Zaidi. Provably strict generalisation benefit for equivariant models. In International Conference on Machine Learning (ICML), 2021.

- [14] Z. Feng, H. Narasimhan, and D. C. Parkes. Deep learning for revenue-optimal auctions with budgets. In the 17th International Conference on Autonomous Agents and Multiagent Systems, 2018.

- [15] F. He and D. Tao. Recent advances in deep learning theory. arXiv preprint arXiv:2012.10931, 2020.

- [16] J. Huang, Z. Han, M. Chiang, and H. V. Poor. Auction-based resource allocation for cooperative communications. IEEE Journal on Selected Areas in Communications, 2008.

- [17] D. Ivanov, I. Safiulin, K. Balabaeva, and I. Filippov. Optimal-er auctions through attention. arXiv preprint arXiv:2202.13110, 2022.

- [18] B. J. Jansen and T. Mullen. Sponsored search: an overview of the concept, history, and technology. International Journal of Electronic Business, 2008.

- [19] C. Lyle, M. van der Wilk, M. Kwiatkowska, Y. Gal, and B. Bloem-Reddy. On the benefits of invariance in neural networks. arXiv preprint arXiv:2005.00178, 2020.

- [20] A. M. Manelli and D. R. Vincent. Bundling as an optimal selling mechanism for a multiple-good monopolist. Journal of Economic Theory, 2006.

- [21] M. Mohri and A. M. Medina. Learning theory and algorithms for revenue optimization in second-price auctions with reserve. International Conference on Machine Learning (ICML), 2013.

- [22] M. Mohri, A. Rostamizadeh, and A. Talwalkar. Foundations of machine learning. MIT press, 2018.

- [23] R. B. Myerson. Optimal auction design. Mathematics of operations research, 1981.

- [24] H. Narasimhan and D. C. Parkes. A general statistical framework for designing strategy-proof assignment mechanisms. Uncertainty in Artificial Intelligence (UAI), 2016.

- [25] N. Nisan, T. Roughgarden, E. Tardos, and V. V. Vazirani. Algorithmic game theory. Cambridge University Press, 2007.

- [26] G. Pavlov. Optimal mechanism for selling two goods. The BE Journal of Theoretical Economics, 2011.

- [27] G. Popescu. An algorithmic characterization of multi-dimensional mechanisms. Computing Reviews, 2012.

- [28] O. Puny, M. Atzmon, H. Ben-Hamu, E. J. Smith, I. Misra, A. Grover, and Y. Lipman. Frame averaging for invariant and equivariant network design. International Conference on Learning Representations (ICLR), 2022.

- [29] J. Rahme, S. Jelassi, J. Bruna, and S. M. Weinberg. A permutation-equivariant neural network architecture for auction design. In Proceedings of the AAAI Conference on Artificial Intelligence, 2021.

- [30] T. Roughgarden. Twenty lectures on algorithmic game theory. Cambridge Books, 2016.

- [31] T. Sandholm and A. Likhodedov. Automated design of revenue-maximizing combinatorial auctions. Operations Research, 2015.

- [32] V. Syrgkanis. A sample complexity measure with applications to learning optimal auctions. Neural Information Processing Systems (NeurIPS), 2017.

Checklist

-

1.

For all authors…

-

(a)

Do the main claims made in the abstract and introduction accurately reflect the paper’s contributions and scope? [Yes] Our contributions are stated in the 4th-8th sentences of the abstract, and the 4th-6th paragraphs of the introduction. The scope is described in the related work section.

-

(b)

Did you describe the limitations of your work? [Yes] We describes the problem setting we considered in the 3rd paragraph of the introduction. Our contributions are for this problem setting.

-

(c)

Did you discuss any potential negative societal impacts of your work? [Yes] Our work is committed to learn the optimal auction mechanism. No negative societal impact is identified.

-

(d)

Have you read the ethics review guidelines and ensured that your paper conforms to them? [Yes] We have read the ethics review guidelines. We ensure that our paper conforms all of them.

-

(a)

-

2.

If you are including theoretical results…

- (a)

-

(b)

Did you include complete proofs of all theoretical results? [Yes] Full proofs are given in the supplemental material.

-

3.

If you ran experiments…

-

(a)

Did you include the code, data, and instructions needed to reproduce the main experimental results (either in the supplemental material or as a URL)? [No] We are associated in a industrial organization. The code is currently under review of our organization.

- (b)

-

(c)

Did you report error bars (e.g., with respect to the random seed after running experiments multiple times)? [No]

-

(d)

Did you include the total amount of compute and the type of resources used (e.g., type of GPUs, internal cluster, or cloud provider)? [Yes] They are given in Section 4.

-

(a)

-

4.

If you are using existing assets (e.g., code, data, models) or curating/releasing new assets…

-

(a)

If your work uses existing assets, did you cite the creators? [Yes] They are given in Section 4.

-

(b)

Did you mention the license of the assets? [Yes] They are given in Section 4.

-

(c)

Did you include any new assets either in the supplemental material or as a URL? [No] We are associated in a industrial organization. The code is currently under review of our organization.

-

(d)

Did you discuss whether and how consent was obtained from people whose data you’re using/curating? [Yes] The data is synthetic in our data.

-

(e)

Did you discuss whether the data you are using/curating contains personally identifiable information or offensive content? [Yes] The data is synthetic in our data. No personally identifiable information or offensive content is contained.

-

(a)

-

5.

If you used crowdsourcing or conducted research with human subjects…

-

(a)

Did you include the full text of instructions given to participants and screenshots, if applicable? [N/A]

-

(b)

Did you describe any potential participant risks, with links to Institutional Review Board (IRB) approvals, if applicable? [N/A]

-

(c)

Did you include the estimated hourly wage paid to participants and the total amount spent on participant compensation? [N/A]

-

(a)

Appendix A Proofs

This appendix collects all proofs omitted from the main text due to space limitation.

A.1 Proofs about Orbit Averaging

In this section, we prove Proposition 2.3 and the feasibility of the projected mechanisms. For simplicity, we use the notations and to present the ranks of the bidder and the item after bidder-permutation and item-permutation , respectively.

Proof of Proposition 2.3.

By the definition of orbit averaging , we have

In addition, if is equivariant, then we have

Thus, orbit averaging is a projection to equivariant function space and fixes all equivariant functions. In addition, orbit averaging fixes all equivariant functions. That means, every equivariant function can be obtained by orbit averaging. In this sense, every equivariant models are contained in the orbit averaging framework.

Proof of the feasibility of projected mechanisms.

We verify all feasibility conditions for the projected mechanisms as follows.

Firstly, for the allocation rule, we have

and

thus we know the projected allocation rule is also feasible, which will never allocate one item more than once.

In addition, for the payment rule, we have

and

thus, we have completed this proof.

A.2 Proof of Theorem 3.1

In this section, we proves Theorem 3.1.

Proof of Theorem 3.1..

We first study the part in the condition of bidder-symmetry; i.e., the orbit averaging is the bidder averaging , acting on the allocation rule and the payment rule as below,

and

Step 1:

We first prove that the auction mechanism has the same expected revenue after projection, i.e.,

Given that for all permutation ,

we have the following equation,

Thus, we complete the first step.

Step 2:

We then prove that the sum of all bidders’ utilities remains the same after projection, i.e.,

Given that

we have the following equation,

Thus, we have completed the second step.

Step 3:

We lastly prove that the auction mechanism has a smaller ex-post regret after projection, i.e.,

For the simplicity, we denote by . Then, we have,

Combining the following inequality,

we have that

We thus have completed the proof of eqs. (1) and (2) when the orbit averaging is the condition of bidder-symmetry.

Then, we prove this theorem in the condition of item-symmetry; i.e., the orbit averaging is the item averaging , acting on the allocation rule and the payment rule as shown below,

and,

Step 1:

We first prove that the auction mechanism has the same expected revenue after projection, i.e.,

Since the valuation joint distribution is invariant under bidder permutation, we have Then, we have

We have thus completed the first step.

Step 2:

We then prove that the sum of all bidders’ utilities remains same after projection, i.e.,

Given that for all permutation ,

we have the following equation,

Thus, we have completed the second step.

Step 3:

We lastly prove that the auction mechanism have a smaller ex-post regret after projection, i.e.,

By the definition of the utility and the item averaging , we have

Combining the following inequality

we have

We thus have proved this theorem in the condition of item-symmetry.

The proofs are completed. ∎

A.3 Proof of Lemma 3.3

In this section, we present the proof of Lemma 3.3.

Proof of Lemma 3.3..

Both the bidder averaging and the item averaging are linear. Thus, we have the following results,

and

The above two equations hold for any . Then, we may prove that

which is exactly the claim of this theorem.

The proof is completed. ∎

A.4 Proof of Theorem 3.4

Proof of Theorem 3.4.

For the simplicity, we rewrite and as and , respectively. Then, for a payment rule , we have that,

Also, we have the following result,

Moreover, we have the following result on the regret gap ,

This proof is completed. ∎

A.5 Proof of Theorem 3.5

In this section, we present the proof of Theorem 3.5.

We start with the definitions or notations necessary for our proof. We define the allocation rule space and the payment rule space as follows,

where is the auction mechanism parameter and is the set of all feasible parameters. We then define the induced utility and ex-post regret spaces as follows,

and

Then, the -distance on and is defined as below,

and

We now present the proof of Theorem 3.5.

Proof of Theorem 3.5..

We prove Theorem 3.5 in two steps: (1) we first prove that the distance between any two mechanisms is smaller when we project them to be permutation-equivariant; (2) then, we prove that the smaller distance implies a smaller covering number.

Step 1:

We prove that the distance between two mechanisms becomes smaller after projection, i.e.,

and

where , , and or .

When is , we have that

and

Then, when is , we prove the result as below,

and

Thus, we have completed Step 1.

Step 2:

We prove that a smaller distance implies a smaller covering number.

Let and be two metric spaces with two different distances and , respectively. There exists a surjective mapping from to , such that for all . The covering numbers and are defined as the minimum numbers of balls with radius r that can cover and under and , respectively.

By the definition of the covering number , there exists a set of scale , such that

Then, is also a -cover for under distance , i.e., for any , we have

Because is surjective, for any , there exists an , such that . Then, for any , we have that

By the definition of , we have

Eventually, combining the results in Step 1 and in Step 2, we have that

and

for both the bidder averaging and the item averaging . ∎

A.6 Proof of Theorem 3.6 and Corollary 3.7

We first introduce two lemmas. The first lemma gives a concentration inequality via the covering number. This result can be used to bound the gap between expected revenue/ex-post regret and empirical revenue/ex-post regret. The second lemma bounds the covering number by the covering number . Both lemmas has been proved by [10]. We recall them here to make our paper completed.

Lemma A.1 (cf. Lemma E.1, [10]).

Let be a set of i.i.d. sample points drawn from a distribution over . Suppose is a set of functions from to such that for all and . We define on as

and as the minimum number of balls with radius that can cover under -distance. Then, we have the following concentration inequality,

Proof.

By the definition of , for any , there exists an such that is an -cover for and . Denote by . Then, we have

The third inequality follows from the fact that when , we have

for all and . Then, from the Hoeffding’s inequality, we have

The proof is completed. ∎

The following lemma bounds the covering number by the covering number . Then the gap between expected ex-post regret and empirical ex-post regret can be bounded by the covering number .

Lemma A.2 (cf. Lemma E.3, [10]).

We define and as the minimum numbers of balls with radius that can cover spaces and under distance , respectively. Then, we have that

Proof.

By the definition of , there exists an -cover for , such that and for any ,

We define as

Then, we can prove that is a -cover for the space , i.e.,

Eventually, we have

The proof is completed. ∎

Proof of Theorem 3.6 and Corollary 3.7.

Applying Lemma A.1 to the spaces and , we have that

and

where the last inequality follows from Lemma A.2.

Further, we assume that

Then, we have the following inequalities,

and

Thus, with probability at least , for any , we have that

| (5) |

and

| (6) |

Equivalently, when the number of samples is large enough, i.e.,

then, the eqs. (5) and (6) both hold with probability at least .

The proof is completed. ∎

A.7 Proof of the Generalization Bound for Myerson Auctions

Denote as , then we have the following theorem,

Theorem A.3.

Assume the item valuation for each bidder is not larger than . When the sample complexity satisfies , with probability at least , we have

Proof.

Since , we have

According to the Hoeffding’s inequality, we have

Let , then we obtain what we need. The proof is completed. ∎

A.8 Orbit Averaging over Subsets of Bidders/Items

In addition, we can extended our theory to orbit averaging over the subset of the bidders/items.

Theorem A.4.

Let be the orbit averaging over any subset of bidders and items, and be any mechanism. Then we have

and

where is the ex-post regret of bidder .

Proof.

Without loss of generality, we assume that takes average over the first bidders, takes average over the first items and takes average over the first bidders and items. Denote as and as . Following Theorem 3.1, we have

and

Then, combining the fact that , we have

and

Similarly, replace by , we can obtain the equations all hold for .

Finally, we prove that . The proof is same with the proof of Lemma 3.3. Only replace and by and respectively, and we obtain the result.

The proof is completed. ∎

Theorem A.5.

Let be the orbit averaging over any subset of bidders and items, and and the sets of all possible utilities and payment rules. Then we have

where and are the minimum numbers of balls with radius that can cover and under -distance, respectively.

Proof.

Without loss of generality, we assume that takes average over the first bidders, takes average over the first items and takes average over the first bidders and items.

We can prove the distance between two mechanisms becomes smaller after orbit averaging, i.e.,

Only replace and by and in the proof of Theorem 3.5, and we obtain the results.

The proof is completed. ∎

A.9 Average over Subgroups

It is worth noting that our proof only replies one assumption that the valuation joint distribution is invariant under the bidder/item permutation. Consequently, we may adopt orbit averaging over any subgroup of , while the benefits on revenue and ex-post regret still hold. Hence, there is a trade-off between the auction mechanism performance (revenue and ex-post regret) and the computational complexity: better performance requires more computation. In addition, the choice of the subgroup can also depend on the input feature [28], which could be more flexible.

Appendix B Additional Experimental Details

This section presents additional experimental details and results omitted from the main text due to space limitation.

B.1 Additional Experimental Settings

In this section, we present detailed experimental settings.

B.1.1 Network Architectures

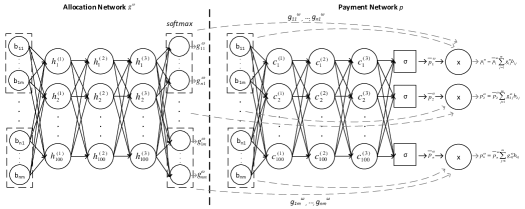

We first describe the RegretNet’s architecture [12]. A RegretNet consists of two parts: the allocation network and the payment network , both of which are modeled as three-layer fully-connected networks with tanh activations. Every layer in the two networks includes nodes.

For each item , the payment network outputs a probability vector , where is the probability of allocating the item to the bidder . To avoid allocating one item over once, a feasible allocation network needs to satisfy for all , , and . Therefore, we compute the allocation via a softmax activation function. In addition, to present the probability that the item is reserved, an extra dummy node is included in the softmax computation.

To ensure the individual rational condition, the payment network is required to output a payment vector , such that for all . Therefore, the payment network first computes a fractional payment for each bidder using a sigmoidal unit. Then, the final payment of the bidder is

An overview of the RegretNet’s architecture is illustrated in the following Figure 1.

RegretNet-PE is designed by modifying RegretNet. We adopt the allocation rule as and the payment rule as , respectively. In this way, we may guarantee that in RegretNet-PE, the allocation is feasible and the mechanism is individual rational, i.e., , and . We may also show that the RegretNet-PE is always permutation-equivariant and has the same number of coefficients as the RegretNet. The proof can be found in Appendix A.1.

B.1.2 Training Procedures

We adopt the augmented Lagrangian method to minimize the following object function with a quadratic penalty term for violating the constraints,

where is the number of samples, is a vector of Lagrange multipliers, and is a parameter to control the weight of the quadratic penalty. We alternately update the overall mechanism parameter and the Lagrange multiplier as follows:

(a) (every iteration);

(b) , (every iterations).

The training procedure is described in the following Algorithm 1.

We divide all training samples into batches of size . At iteration , we use the batch .

The update (a) is computed via Adam. The gradient of w.r.t. for a fixed is as below,

where

and

Because and both contain a “max” over misreports111The misreport refers to an arbitrary bid, rather than restricted to be a truthful bid [12]., we use another Adam to compute the approximated best biddings . In each update on , we perform updates to compute a best bidding for each . In particular, we maintain the misreports for each sample as the initial value in the next iteration. Then, we use these biddings to compute the gradient and then, update as . After every iterations, we update as . In addition, we increase the value of every a certain number of iterations, where we set the value of in each iteration prior to training.

| Method | Normal | Normal . | ||||

| Revenue | Regret | GE | Revenue | Regret | GE | |

| Optimal | - | 0 | - | |||

| RegretNet | ||||||

| RegretNet-Test | - | - | ||||

| RegretNet-PE | ||||||

| Method | Normal | Normal | ||||

| Revenue | Regret | GE | Revenue | Regret | GE | |

| RegretNet | ||||||

| RegretNet-Test | - | - | ||||

| RegretNet-PE | ||||||

| Method | Compound | Compound | ||

| Revenue | Regret | Revenue | Regret | |

| RegretNet | ||||

| EquivariantNet | ||||

| RegretNet-PE | ||||

| Method | Uniform | Uniform | ||||

| Revenue | Regret | GE | Revenue | Regret | GE | |

| RegretNet | ||||||

| RegretNet-Test | - | - | ||||

| RegretNet-PE | ||||||

B.1.3 Test Settings

To verify our Theorem 3.1 and Theorem 3.4, we first train a RegretNet and then project the will-trained RegretNet to be permutation-equivariant through bidder-item aggregated averaging , denoted as “RegretNet-Test”. To meet the symmetric valuation condition in Theorem 3.1 and Theorem 3.4, we sample a set of valuations from the distribution, which is denoted by , and then, induce a set of symmetric samples for test.

For a RegretNet-PE, there is no difference between test on and on , because

for any permutation-equivariant function and a RegretNet-PE is always permutation-equivariant.

To compute the best bidding for each bidder , we first randomly initialize misreports in all settings, and then, perform updates on each misreport via Adam with the same settings. Finally, we choose the best one (which induces a maximal utility of the bidder ) as the approximated best bidding .

B.1.4 Implementation Details

We train the models (RegretNet and RegretNet-PE) for up to 150 epochs with a batch size of 128 () and report the early-stop results for RegretNet-PE to obtain a comparable ex-post regret. The terminal iteration numbers for RegretNet-PE are in the setting, in the setting, in the setting, in the setting, and in the setting. Our insight is that the larger terminal iteration number required in the setting is because of the small model size, i.e., where the networks have three layers (each of nodes). The value of is initialized as and increased by every batches. For each update on , we initialize one misreport and update the misreport by Adam for each bidder with steps () and learning rate (). The final optimal misreports will be used to initialize the misreports for the same batch in the next epoch. We update via Adam for every batch with a learning rate of 0.001. Besides, we update every 200 batches.

B.2 Additional Experiment Results

We present additional experimental results. Each valuation is sampled independently from (1) a truncated normal distribution in ; (2) a compound distribution truncated in , where is sampled independently and uniformly from (cf. Setting A, [10]); and (3) a compound distribution , where and are sampled independently and uniformly from (Setting C, [10]). All results are shown in Table 3 and Table 4. The revenue and ex-post regret of RegretNet and EquivariantNet in Table 4 come from the previous work [10]. In Table 4, we report the ex-post regret as “” following the previous works.

Moreover, we extend our experiments to more complex settings, including two-bidder five-item and five-bidder three-item settings. Due to the computation limitations, we sample data points and initialize misreports for test. Each valuation is sampled from the uniform distribution and the truncated normal distribution in . The results are shown in Tables 3 and 5.

B.3 Allocation Rules Learned by RegretNet and RegretNet-PE

In this section, we show the allocation rules learned by RegretNet and RegretNet-PE in two-bidder, one-item setting and one-bidder, two-item setting, where the valuation is drawn from the uniform distribution . The optimal auction mechanisms are both known.

B.3.1 Two-bidder and One-item Setting

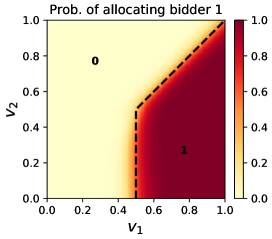

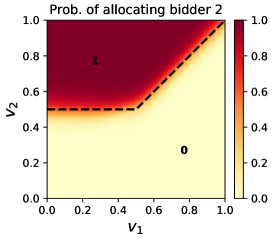

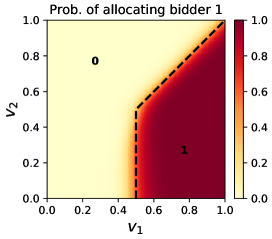

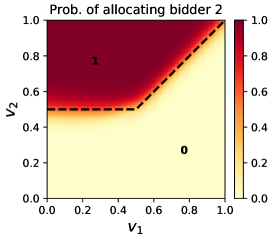

For the two-bidder, one-item setting, the optimal mechanism is well-known as Myerson auction [23], which allocates the item to the highest bidder with receiving a payment of the maximum of the second price and the reserve price, if the highest bid is higher than the reserve price. The allocation rules learned by RegretNet and RegretNet-PE are shown in Figure 2. From Figure 2. We can find that the two learned allocation rules are both almost the same as the optimal mechanism.

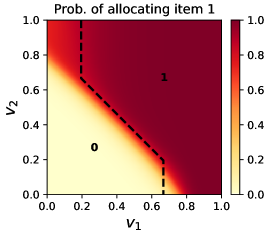

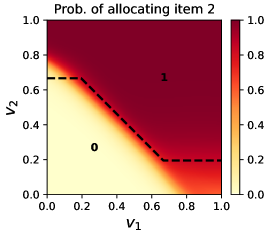

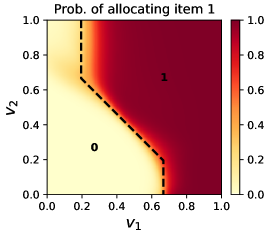

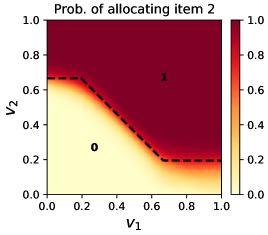

B.3.2 One-bidder and Two-item Setting

The optimal mechanism is given by [20]. Same with the above, we show the allocation rules learned by RegretNet and that learned by RegretNet-PE in Figure 3. The improvement is significant. when one item’s valuation is close to and another item’s is close to , the mechanism learned by RegretNet has a positive probability to allocate the item with the lower valuation to the bidder, while RegretNet-PE and the optimal mechanisms would not.