Stackelberg POMDP: A Reinforcement Learning Approach for Economic Design

Abstract

We introduce a reinforcement learning framework for economic design where the interaction between the environment designer and the participants is modeled as a Stackelberg game. In this game, the designer (leader) sets up the rules of the economic system, while the participants (followers) respond strategically. We integrate algorithms for determining followers’ response strategies into the leader’s learning environment, providing a formulation of the leader’s learning problem as a POMDP that we call the Stackelberg POMDP. We prove that the optimal leader’s strategy in the Stackelberg game is the optimal policy in our Stackelberg POMDP under a limited set of possible policies, establishing a connection between solving POMDPs and Stackelberg games. We solve our POMDP under a limited set of policy options via the centralized training with decentralized execution framework. For the specific case of followers that are modeled as no-regret learners, we solve an array of increasingly complex settings, including problems of indirect mechanism design where there is turn-taking and limited communication by agents. We demonstrate the effectiveness of our training framework through ablation studies. We also give convergence results for no-regret learners to a Bayesian version of a coarse-correlated equilibrium, extending known results to the case of correlated types.

1 Introduction

A digital transformation is seeing markets become algorithmic systems that make use of complex mechanisms to facilitate the matching of supply and demand. Examples include Amazon’s marketplace, Uber, GrubHub, and AirBnB. These market platforms allow for an unprecedented level of control over mechanisms for matching and pricing. However, mechanism design—the engineering field of economic theory—does not always provide enough guidance in regard to how to design these markets to achieve properties of interest, whether economic efficiency or some other target.

Mechanism design theory has mainly focused on direct revelation mechanisms, where participants directly report their preferences and in an incentive-aligned way. While in theory this is without loss of generality due to the revelation principle (Laffont and Tirole, 1993), in practice most mechanisms deployed on market platforms are indirect—participants respond to product choices and prices, and do not communicate directly about their preferences. This emphasis on indirect mechanisms gives rise to the need to consider the behaviors of agents that is induced by the rules of a mechanism: no longer can one simply look for direct mechanisms in which it is incentive compatible to make truthful reports of preferences. Rather, we need to ask, for example, how agents will make use of simpler messaging schemes and respond to an array of products and prices.

This problem of indirect mechanism design can be modeled as one of finding an optimal leader strategy in a Stackelberg game. In this game, the strategy of the leader corresponds to a commitment to the rules of the mechanism that is used for pricing and allocation, and the followers correspond to the market participants who respond to the induced economic environment. We introduce a new methodology for finding optimal leader strategies in complex Stackelberg games, demonstrating how it can be applied to economic scenarios capturing many aspects of indirect mechanisms, including communication, multi-round interaction, and uncertainty regarding participants’ types. Our methodology is designed for offline use, where the leader can simulate the behavior of the followers during the design process. This approach is commonly used in economic design problems.

Stackelberg games have been widely studied in computer science, with applications to security (Sinha et al., 2018), wildlife conservation (Fang et al., 2016), and taxation policies (Zhou et al., 2019; Wang, 1999), among others. Much of the research has focused on solving these games in simple settings, such as those with a single follower (Goktas and Greenwald, 2021, e.g.), complete information settings where followers move simultaneously (Basilico et al., 2017, e.g.), or settings where the leader’s strategies can be enumerated (Cheng et al., 2017; Bai et al., 2021, e.g.). A more recent research thread (Zhang et al., 2023a, b) focused on designing payment schemes that steer no-regret-learning agents to play desirable equilibria in extensive-form games. In our work, we consider multi-round games with incomplete information where the leader’s interventions are not solely based on payments, but also involve soliciting bids and allocating items.111In one of our scenarios, the leader’s task involves generating a game that allows for communication between a mechanism and agents, where the semantics of this communication arises from the strategic response of followers, and where the order with which agents participate in the market and the prices they see depends, through the rules of the mechanism, on this communication. Additionally, we do not limit followers to using no-regret algorithms to adapt their behavior in response to the leader’s strategy. Instead, we introduce a framework that can accommodate a variety of followers’ behavioral models.

Formally, we model our settings as Partially Observable Markov Games (POMGs),222The partial observability is due to followers’ private types. where one of the agents is the leader and makes a commitment to its strategy, and the behavior of the other agents, the followers, comes in response to this commitment. To our knowledge, this work is the first to provide a framework that supports a proof of convergence to a Stackelberg policy in POMGs.333Zhong et al. (2021) support convergence to an optimal leader strategy in POMGs, but they restrict their followers to be myopic. We achieve this result through the suitable construction of a single-agent leader learning problem integrating the behavior of the followers, in learning to adapt to the leader’s strategy, into the leader’s learning environment.

The learning method that we develop for solving for the Stackelberg leader’s policy in POMGs works for any model of followers in which they learn to respond to the leader’s policy by interacting with the leader’s policy across trajectories of states sampled from the POMG. We refer to these follower algorithms as policy-interactive learning algorithms. Our insight is that since the followers’ policy-interactive learning algorithms adapt to a leader’s strategy by taking actions in game states, we can incorporate these algorithms into a carefully constructed POMDP representing the leader’s learning problem. In this POMDP, the policy’s actions determine the followers’ response (indirectly through the interaction of the leader’s policy with the followers’ learning algorithms) and in turn the reward to the leader. This idea allows us to establish a connection between solving POMDPs and solving Stackelberg games: we prove that the optimal policy in our POMDP under a limited set of policy options is the optimal Stackelberg leader strategy for the given model of follower behavior. We handle learning under limited policy options via a novel use of actor-critic algorithms based on centralized training and decentralized execution (Lowe et al., 2017, see, e.g.,).

With this general result in place, we give algorithmic results for a model of followers as no-regret learners, and demonstrate the robustness and flexibility of the resulting Stackelberg POMDP by evaluating it across an array of increasingly complex settings.

Further related work.

The Stackelberg POMDP framework introduced in the present paper has been further explored in subsequent studies. In Brero et al. (2022), Stackelberg POMDP is utilized for discovering rules for economic platforms that mitigate collusive behavior among pricing agents employing Q-learning algorithms. Gerstgrasser and Parkes (2023) have further generalized Stackelberg POMDP to accommodate domain-specific queries for faster followers’ response via meta-learning. These techniques allowed them to derive optimal leader strategies in complex Atari 2600 settings involving one leader and one follower.

2 Preliminaries

In full generality, we consider a Bayesian Stackelberg game with agents, denoted by , and a finite number of rounds, indexed by (we allow ). The first agent, agent , is the leader, while the remaining agents, are the followers. The leader has the advantage of committing to a strategy, which is observed by the followers who select their strategies in response. In the Bayesian setting, each follower has a private type, which we denote as . The type profile, , is sampled from a possibly correlated distribution . As is standard in many economic design problems, we will assume that the leader has no private type.

We will formulate this Bayesian Stackelberg game through the formalism of a partially observable Markov game (Hansen et al., 2004) between the leader and the followers. Partially observable Markov games are a multiagent generalization of partially observable Markov decision processes (POMDPs):

Definition 2.1 (Partially observable Markov game).

A partially observable Markov game (POMG) with agents (indexed from to ) is defined by the following components:

-

•

A set of states, , with each state containing the necessary information on game history to predict the game’s progression based on agents’ actions.

-

•

A set of actions, for each agent . The action profile is denoted by , where .

-

•

A set of observations, for each agent . The agents’ observation profile is denoted , where .

-

•

A state transition function, , which defines the probability of transitioning from one state to another given the current state and action profile: .

-

•

A reward function, , which maps for each agent the current state and action profile to the immediate reward received by agent , .

-

•

A finite time horizon, .

Each agent aims to maximize its expected total reward over steps. Going forward, we use a subscript with every POMG variable to refer to its value at the -th step of the game. The history of agent ’s observations at step is denoted by , while represents a generic history with unspecified time step and is the set of these histories. Agent ’s behavior in the game is characterized by its policy, , where is its action when observing history . We let be the set of these policies.

For modeling the Bayesian Stackelberg setting, we adopt a POMG with agents, with one leader and followers. We define the leader’s initial observation, , to be empty. Conversely, every follower starts the game with an initial observation , which corresponds to their type .

We define a subgame in , which is induced by fixing the policies for some subset, , of agents.

Definition 2.2 (Subgame of a POMG (Informal Definition)).

Given a POMG , a subset of the agents, and a policy profile for agents in , we define the subgame POMG, , as the game induced among agents by policy profile . Actions, rewards, and observations remain the same as in , while states are augmented to include policies and observation histories . State transitions in are induced by the state transition function in , with the actions of the agents in in computed “internally” by the game by applying policies on histories .444See appendix for a formal definition.

With this, we can model a Bayesian Stackelberg game. We denote the game induced by leader policy in POMG as . This is the subgame in which the followers respond to the leader’s policy. Given this, the leader in a Stackelberg game makes its reward by anticipating how the followers will respond to its strategy. For this, we model followers with a behavior function , which takes the leader’s strategy , and returns response strategies, , where . We use this behavior function to model the result of various kinds of follower responses, such as the Bayesian Coarse Correlated equilibria that arise from no-regret dynamics (see Appendix). We let be a state-action trajectory in generated by and and be the distribution on trajectories. We formulate the leader’s problem:

Definition 2.3 (Optimal leader strategy).

Given a POMG, , and a behavior function , the leader’s problem is defined as finding a policy that maximizes its expected reward under the followers’ induced behavior:

There are various kinds of plausible response behaviors for followers in Bayesian multi-stage settings with general-sum interactions. This formal model allows for different choices of follower models, through the particular choice of behavior function . As a particular instantiation, in our experiments we adopt a behavior function that corresponds to a Bayesian Coarse Correlated Equilibrium (BCCE) as defined by Hartline et al. (2015). This is relevant because no-regret learning algorithms converge to the set of BCCEs (we prove this for the general setting of correlated types).

3 Learning an Optimal Leader Policy

In this section, we formulate the Stackelberg leader problem as a single-agent partially observable Markov decision process (POMDP), referred to as the Stackelberg POMDP. This formulation is the main conceptual contribution of the paper. In effect, we fold the response model of followers into the stochastic environment corresponding to a carefully constructed POMDP that represents the leader’s problem and expose the leader to the effect of its policy on the behavior of followers.

To formulate the Stackelberg POMDP, we assume that the followers are computing their response strategies via policy-interactive response algorithms, which we define as follows.

Definition 3.1 (Policy-interactive response algorithm).

Given a leader policy and a partially observable Markov game with followers, we define a Policy-Interactive (PI) Response Algorithm, denoted as . This algorithm determines a behavior function for the followers in the subgame by repeatedly playing game .

A PI response algorithm consists of the following elements:

-

•

A set of states, , where each state is comprised of two parts: a policy profile representing the followers’ strategies in , and an additional information state utilized for state transitions.

-

•

A state transition function, , that defines the probability of transitioning from one state to another. The transition is based on the current state and the outcome of game played using the follower policies in and the leader’s actions queried from .555For ease of exposition, we only allow PI response algorithms to update their states at the end of gameplays. However, this aspect can be easily generalized to accommodate intra-game updates.

-

•

A finite time horizon , corresponding to the total number of game plays run by the algorithm.

As previously done for POMGs, we use subscript with every variable of our PI algorithm to refer to its value at the -th game play. Consequently, the final state of our PI algorithm includes the joint policy returned by the behavior function .

A concrete example of a PI response algorithm is a no-regret learning algorithm, which determines an approximate coarse-correlated equilibrium for the followers Hartline et al. (2015).666Please refer to the appendix for a description of how no-regret algorithms can be formulated as PI response algorithms. However, PI response algorithms are quite general, and also include conventional MARL algorithms such as multi-agent Q learning, as well as centralized ones, such as the Multi-Agent Deep Deterministic Policy Gradient algorithm Lowe et al. (2017).

We are now ready to introduce the Stackelberg POMDP formulation, which constructs a single-agent POMDP for a given policy-interactive response algorithm of followers. We will show that this single-agent POMDP can be used to derive a solution to the Stackelberg leader problem for the behavior function corresponding to the final state of the policy-interactive response algorithm.

Definition 3.2 (Stackelberg POMDP).

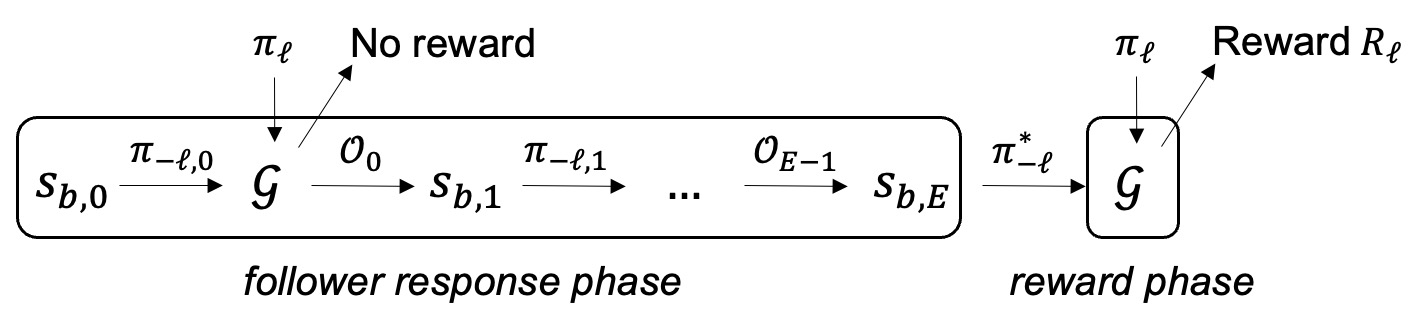

Given a partially observable Markov game , with leader and a PI response algorithm determining followers’ policies , the Stackelberg POMDP is constructed as a finite-horizon, episodic POMDP that models the leader’s problem, where an episode of the Stackelberg POMDP is divided into two phases:

-

1.

A follower response phase, consisting of steps, during which game is played times against the strategies contained in the states of the algorithm. For the Stackelberg POMDP,

The state at step , denoted , is defined as a tuple comprising the internal algorithm state of , where , and the game state at the current game step . The initial state corresponds to initializing the algorithm state of , and sampling the game state according to the distribution on initial game states.

The observation at step , denoted , corresponding to the leader’s observations in game at the current game step and during the iteration of gameplay.

For any step that is not a last step of the game , the state transition is induced by rules of game , and depends on the action of the leader and the followers in , where the actions of the followers are determined by . The state transition for a step that is the last step of the game corresponds to updating the algorithm state of and sampling the game state according to the distribution on initial game states.

The action at step , denoted , models the action of the leader at the game step of the iteration of gameplay, and is determined by the POMDP policy.

There is zero reward at every step of the follower response phase (this models zero reward to the leader; the PI response algorithm of the followers can make use of the game reward of the followers).

-

2.

A reward phase, consisting of steps, and corresponding to a single play of , where the followers adopt policies given by the final algorithm state, , of . The state, observation, and action are defined as in the follower response phase. For the state transition, the follower actions now depend on the final algorithm state of . The reward corresponds to the reward to the leader in game at the current game step .

Figure 1 provides a graphical representation of our Stackelberg POMDP. For concreteness, we describe in the Appendix the Stackelberg POMDP for one of the settings we consider in our experiments.

Before presenting our main result, it is important to highlight that the set of leader’s policies in is a subset of the set of history-dependent policies in our Stackelberg POMDP. We can now state our key theorem that establishes the connection between finding an optimal policy in our POMDP and solving the leader’s Stackelberg problem.

Theorem 3.1.

Let be the optimal policy in our Stackelberg POMDP among the set of leader’s policies . Then, also solves the leader’s Stackelberg problem of Definition 2.3.

It’s important to underscore that the limitation of our policy space to prevents us from adopting conventional techniques typically used for solving POMDPs, such us formulating policies over belief states or (sufficient statistics of) histories of observations. This is crucial, as otherwise, the solution cannot be applied to the original game . In light of this constraint, our approach to tackling POMDPs involves a novel utilization centralized training and decentralized execution training algorithms (Lowe et al., 2017, see, e.g.). These algorithms revolve around actor-critic algorithms for reinforcement learning. The critic network receives the entire state information of the POMDP as input, while the actor network, which corresponds to the policy, only interacts with a limited portion of the state information. As explained further in the appendix, this methodology ensures the suitability of our approach to compute the optimal policy in our POMDP. It achieves this by exposing the critic network to a Markovian environment while constraining the learned policy (i.e., the actor network) to use solely the information available during deployment.

In the remainder of the paper, we instantiate the policy-interactive response algorithm to the multiplicative-weights algorithm, a specific no-regret learning dynamic. We present an extensive description of no-regret learning dynamics in the appendix, including a proof that shows how these dynamics lead to a Bayesian version of a coarse-correlated equilibria that we call Bayesian Coarse-Correlated Equilibria (BCCE). This extends a result proven by Hartline et al. (2015) to the case of correlated types. We note that BCCEs are equivalent to Coarse-Correlated Equilibria (CCE) when the followers only have one type, i.e., the setting is effectively non-Bayesian.

4 Applications of Stackelberg POMDP

| Setting | Followers | Bayesian | Followers’ Behavior |

|---|---|---|---|

| Normal form games | Single | No | Best response |

| Matrix design games | Multiple | No | CCE |

| Simple allocation mechanism | Single | Yes | Best response |

| MSPM | Multiple | Yes | BCCE |

In this section, we demonstrate the robustness and flexibility of the Stackelberg POMDP learning framework through a series of experiments, each conducted in a setting of increasing complexity (Table 1). Two of these settings are Bayesian and two are not. In all cases, we use multiplicative-weights for the follower model, with this corresponding to different solution concepts depending on the context.

Throughout, we train the leader’s policy by implementing a centralized training decentralized execution algorithm based on the Proximal Policy Optimization (PPO) algorithm Schulman et al. (2017). Consistent with the literature, we call this variant Multi-Agent PPO (MAPPO) (Lowe et al., 2017). Specifically, we start from the PPO version implemented in Stable Baselines3 (Raffin et al., 2021, MIT License) and modify the network architecture so that the critic network has access the followers’ internal information. PPO’s default parameters are not modified, except that we do not discount rewards. In addition to testing performance on different settings with different variants, we will perform ablation studies on our training algorithm by comparing its performance with the (non-centralized) PPO algorithm, as implemented in Stable Baselines3.

To reduce the variance in followers’ responses (due to non-deterministic policy behavior of the leader), we only consider deterministic policies. In particular, we maintain an observation-action map throughout each episode. When a new observation is encountered during the episode, the policy chooses an action following the default training behavior and stores this new observation-action pair in the map. Otherwise, the policy simply uses the action stored in the map.777In general, optimal leader policies can be non-deterministic (e.g., Conitzer and Sandholm, 2006). In one of our experiments, we show that we can also successfully learn optimal non-deterministic policies by modifying the leader’s action space accordingly. We also restrict the followers to deterministic behavior in the reward phase by having them play according to the action with maximum weight.

While training the leader’s policy, we log the rewards arising from the reward phase of a separate Stackelberg POMDP episode, and run this every 10k training steps. These evaluation episodes use the current leader policy, and operate it executing the action with the highest weight given each observation. In the non-Bayesian settings, we run the Stackelberg POMDP for 100 follower response steps. In the Bayesian settings, we run the Stackelberg POMDP for 1000 follower response steps and sample new types for followers at the beginning of each new game. In the Bayesian settings, we further execute each game 30 times during the reward phase of the Stackelberg POMDP, each time sampling new types. Executing the game multiple times in the reward phase significantly reduces the computation time by avoiding the need to re-run the response phase for different types. With this optimization, we are able to complete each training run in less than 8 hours using 4 cores on an Intel(R) Xeon(R) Platinum 8268 CPU 2.90GHz machine.

4.1 Normal Form Games

First, we test our approach on complete information, normal form games involving one leader and one follower. In these scenarios, the no-regret learning dynamics lead to follower best responses, and these responses are unique in any Stackelberg equilibrium of the games that we consider.

In a normal-form game, the agent payoffs are specified via a matrix. The leader’s strategy is to choose a row, and as a response, the follower chooses a column. In the randomized variant, the leader’s strategy space is the set of distributions over the rows. In both cases, the follower’s optimal strategy is deterministic; i.e., to choose a single row.

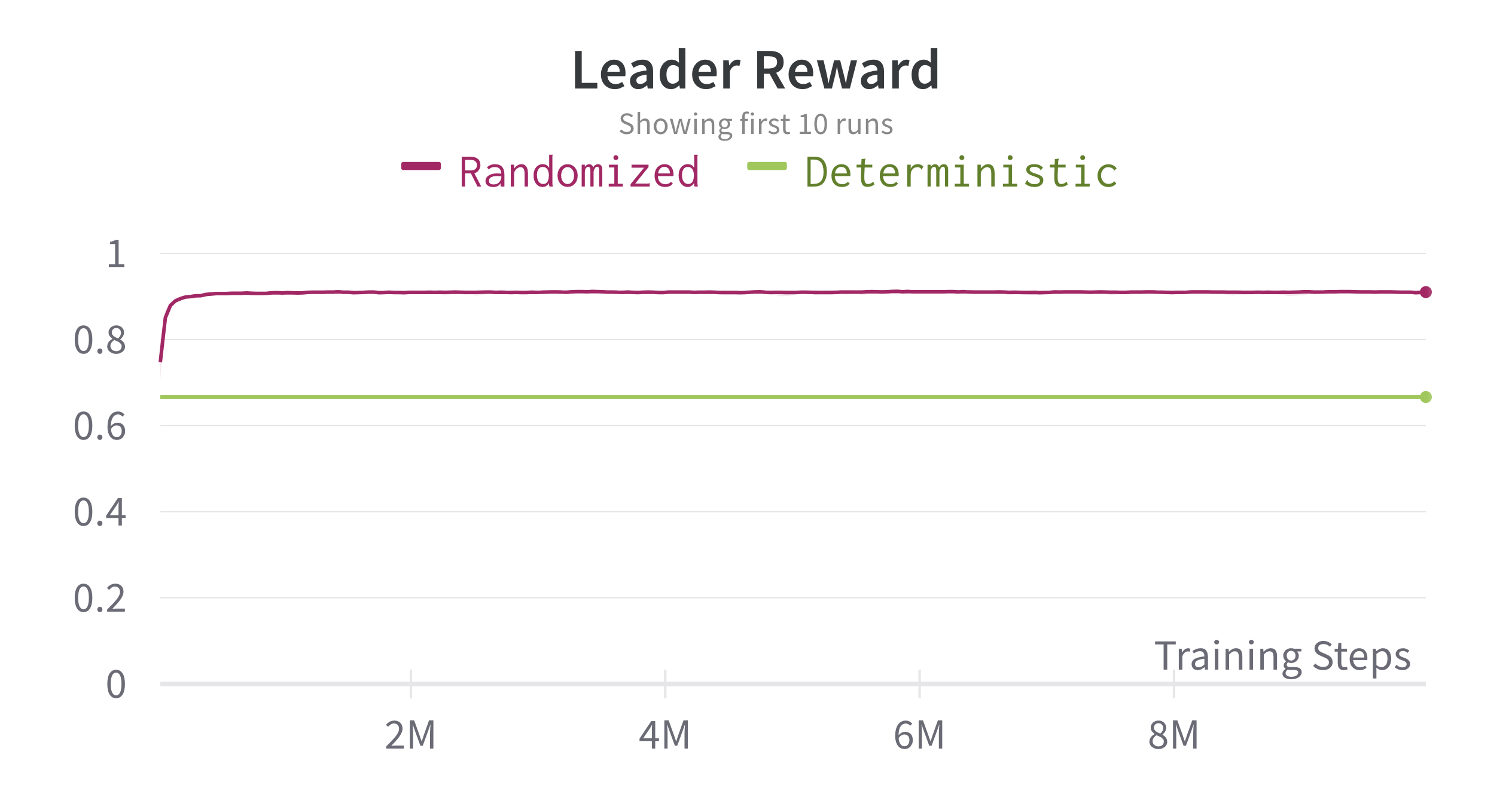

We consider the two normal form games from Zhang et al. (2019), namely Maintain and Escape. Table 2 describes Maintain and we defer a discussion of Escape to the Appendix. In Maintain, the optimal deterministic leader action is , with the follower responding with action and generating payoff to the leader. This contrasts with the Nash equilibria, which are and (pure), and one in which each player independently mixes on and .

The leader can further improve its payoff by picking a randomized action, and playing with probability and with probability , for some small . In this scenario, the follower still maximizes its payoff by playing , and the leader’s expected utility is . In order to accommodate randomized leader strategies, we modify the original POMG , letting the leader’s action be an assignment of weights, one to each row, with these weights selected from the space of non-negative real vectors. The row weights are normalized to obtain probabilities over the action of the leader in the matrix form game.

The results of using Stackelberg POMDP on Maintain are given in Figure 2. MAPPO immediately learns to play the optimal strategy when leader actions are deterministic. In contrast, this performance is not attained by any of the algorithms tested in Zhang et al. (2019). In addition, MAPPO is also able to learn the optimal leader strategy in the randomized scenario.

4.2 Matrix Design Games

In this section, we consider a different complete information setting, namely that of matrix design games Monderer and Tennenholtz (2003). In these games, the role of the leader is to modify the payoffs in a Normal form game that is played by multiple followers. Here, it is known that the multiplicative-weight learning dynamics approximate a coarse correlated equilibrium (CCE) in the game.

Specifically, the leader is allowed to adjust each of a particular subset of the payoffs in the payoff matrix by an amount, . The followers play an equilibrium in the modified matrix game, and the leader’s goal is to maximize the followers’ welfare in the original matrix game and to do so without having to make payment (i.e., the ideal solution is that the follower actions correspond to an unmodified matrix cell).

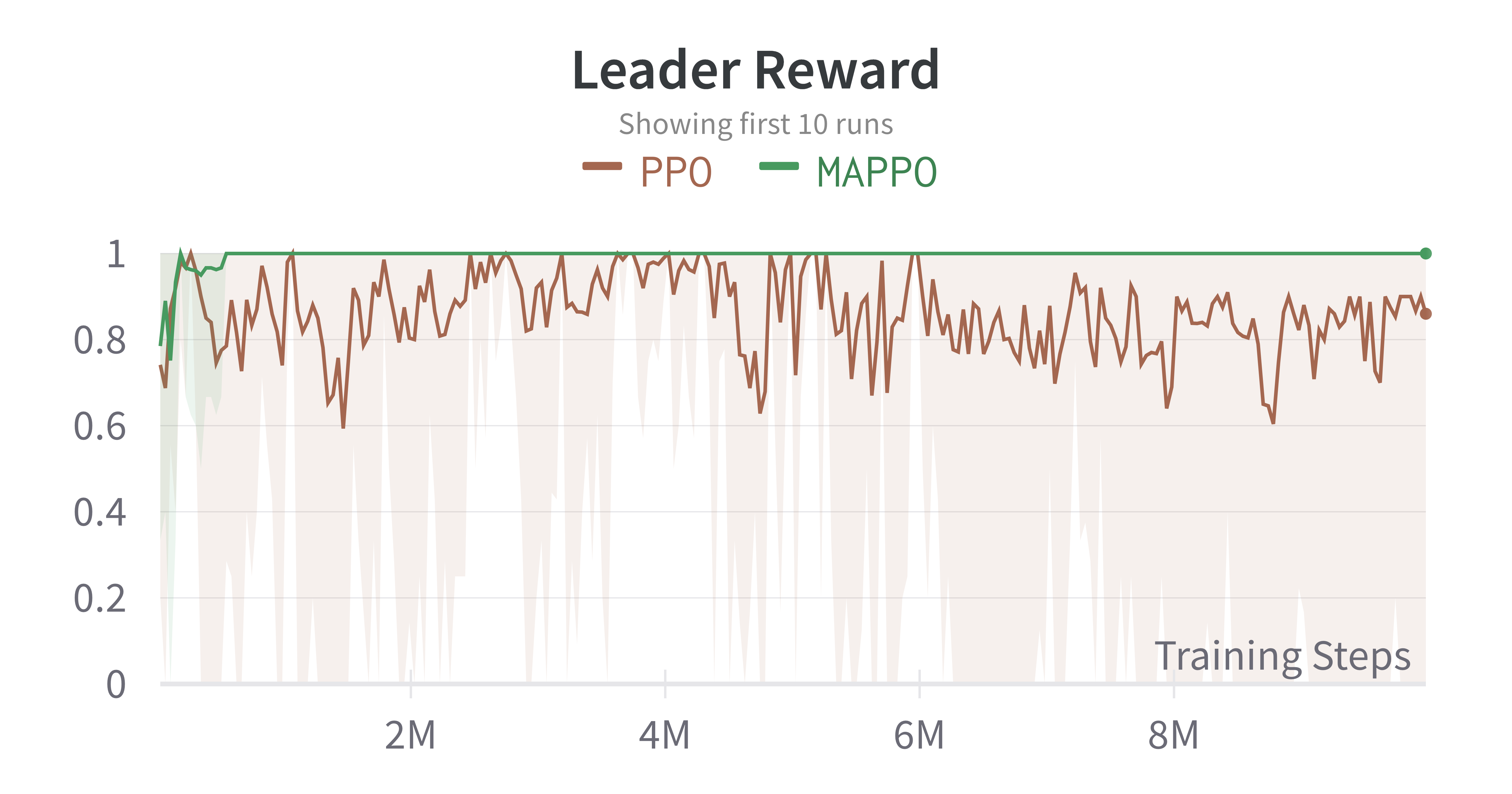

In this experiment, we consider the first example presented by Monderer and Tennenholtz (2003), which is the matrix design game in Figure 3. The unmodified game has two Nash equilibria, and . This makes it hard for the followers to coordinate their gameplays to maximize their welfare. However, when , becomes the unique dominant strategy equilibrium, simplifying the followers’ coordination process. Note, also, that this strategy profile does not make use of the -adjusted payoffs.

The results of using Stackelberg POMDP are given in Figure 3. When used together with the MAPPO algorithm to solve the leader learning problem (the Stackelberg POMDP), the Stackelberg leader achieves the welfare-optimal outcome after approximately 200k training steps. At the end of training, the leader consistently selects in each run, and the followers consistently respond by playing the dominant strategy equilibrium. In contrast, the critic in PPO lacks access to the complete state information, including agents’ strategies, and cannot accurately evaluate the current state of the POMDP and PPO applied to the Stackelberg POMDP exhibits suboptimal behavior.

4.3 Sequential Price Mechanisms with Messages

As a second Bayesian setting, we design sequential price mechanisms (Brero et al., 2021b; Sandholm and Gilpin, 2006), extended here to include an initial messaging round, similar to the one used for the simple allocation mechanism. We refer to this environment as message sequential price mechanisms (MSPM).

In this setting, there are one or more items to allocate to each of multiple followers, each with private valuations on different bundles of items. There are multiple followers, each interacting with the mechanism across multiple rounds. Here, multiplicative-weights learns an approximate, Bayesian coarse correlated equilibrium (BCCE) in the game induced by the leader.

In the first round of the mechanism, each agent observes its type and communicates a message, , to the mechanism. Subsequently, the mechanism visits each agent in turn, possibly in an adaptive order: the mechanism selects an unvisited agent , and announces a price for each item that has not yet been purchased. Agent then selects the bundle of items that maximizes its utility given these prices. The objective of the mechanism is to maximize the expected social welfare.

We test two single-item, two-agent settings, and give the full details in the Appendix. In each setting, the mechanism’s design goal is to maximize expected welfare. For these experiments, we reduce the default learning rate by a factor of 100, to avoid exploding gradients.

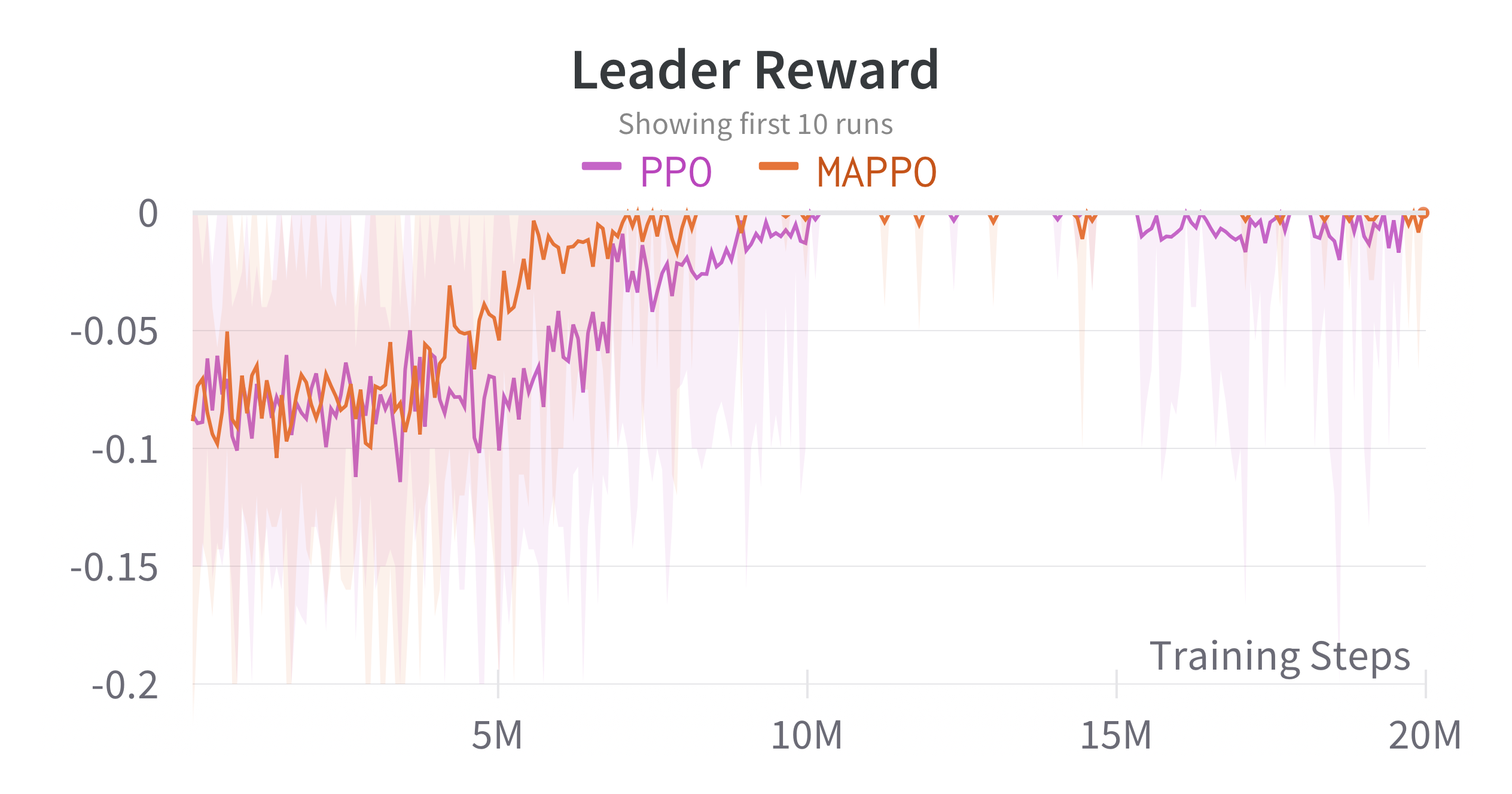

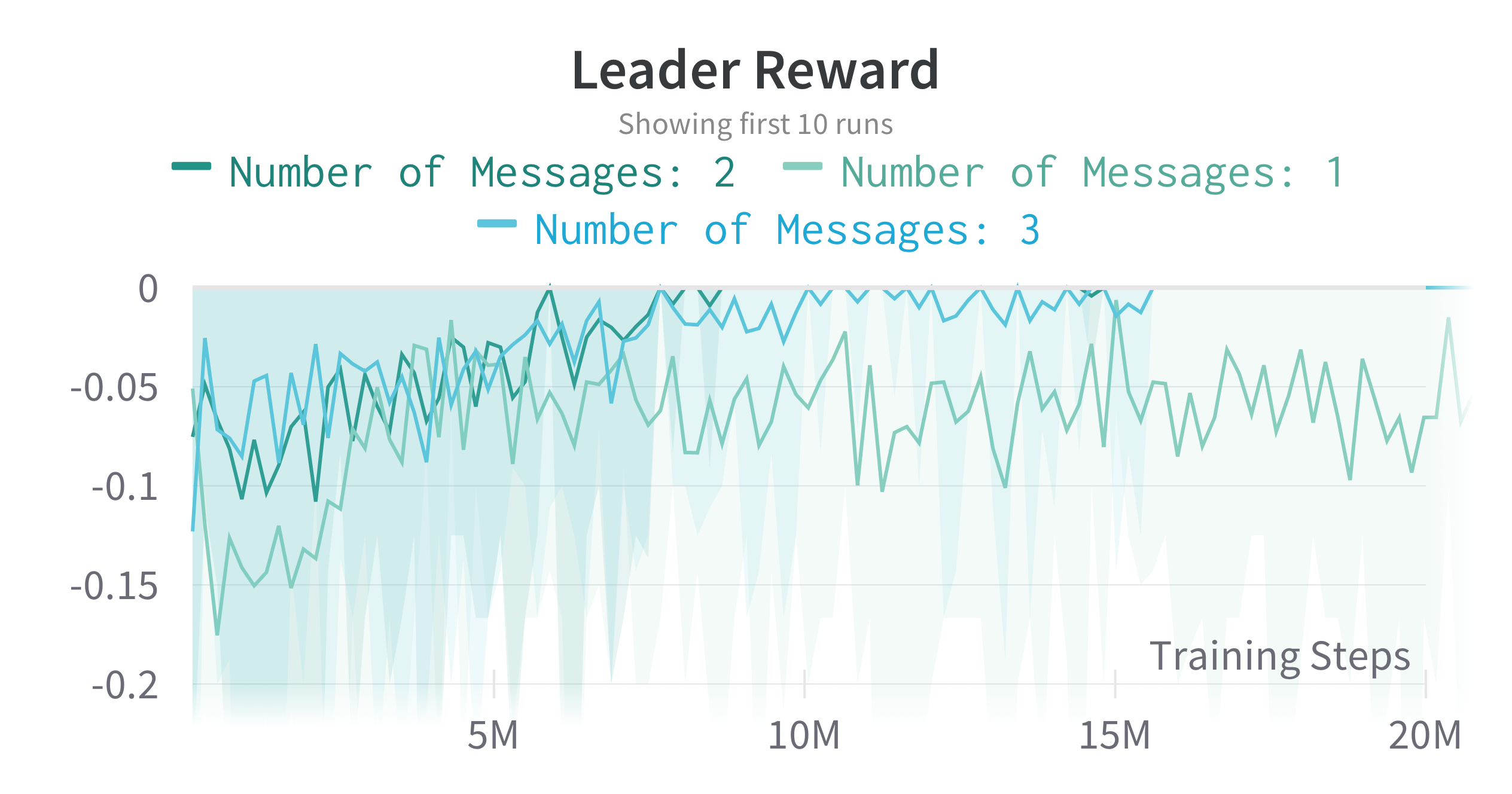

The first setting that we study was introduced by Agrawal et al. (2020) and has two possible types for each agent (see the Appendix). In this scenario, and as detailed in the Appendix, standard SPMs, which operate without message passing, cannot achieve optimal results. Figure 4 demonstrates that MAPPO applied to the Stackelberg POMDP achieves an optimal performance across each of our 10 runs. Specifically, MAPPO consistently learns a mechanism that prompts one of the agents to disclose its type by supporting this strategy in a dominant strategy equilibrium. Then, MAPPO uses this agent’s message to establish the order of visits (see the Appendix for details). Conversely, PPO remains unstable, when applied to the Stackelberg POMDP, even at the end training.

The second setting that we study is similar, but each agent’s type space has size three (again, see the Appendix for details). As in the first setting, standard SPMs, which operate without message passing, cannot achieve optimal results. However, and despite the larger type space, there exists optimal mechanisms with a message size of two in which the agents’ dominant strategy is to use the message to signal their highest type. See the Appendix for an extended discussion on the learned designs, which are interesting for their intricacy. Figure 4 confirms this, and we further see that the fastest training speed in achieving optimal performance is achieved when two messages are available (rather than three messages). Optimal performance is also achieved when agents are given three messages, but this requires a longer training period. This suggests that the Stackelberg POMDP learning framework is effective in identifying the most concise communication protocols.

5 Conclusion

This paper has introduced a reinforcement learning approach to compute optimal leader strategies in Bayesian Stackelberg games over multiple rounds. Specifically, we can solve for Stackelberg leader strategies when follower behavior types can be instantiated as policy-interactive response algorithms. By integrating these follower algorithms into the leader’s learning environment, we attain the single-agent Stackelberg POMDP, with the useful property that the optimal policy in this single-agent POMDP under a limited set of policy options yields the optimal leader strategy in the original Stackelberg game. We showed how the centralized training with decentralized execution framework can be used to solve POMDPs within this restricted policy space, confirming the necessity of this approach via ablation studies.

As an application of this new framework, we have demonstrated that we can learn optimal policies in the Stackelberg POMDP in environments of increasing complexity, including ones featuring limited communication and turn-taking play by agents. To the best of our knowledge, this is the first use of end-to-end, automated mechanism design for indirect mechanism with strategic agents.

A challenge in scaling the Stackelberg POMDP to larger settings is to handle a long response process, which leads to sparse rewards for the leader in the POMDP formulation. In general, one could accelerate this process by tailoring follower responses using domain-specific queries, which can significantly expedite adaptation. While these queries can be seamlessly integrated into the framework, they will require domain-specific designs, which we believe are out of scope for this first paper that focuses on the plain Stackelberg POMDP implementation. In the meantime, this research direction has already been explored by Gerstgrasser and Parkes (2023) via the use of follower policies trained with meta-learning that can produce response behavior through a limited number of domain-specific queries. Further domain adaptation can pave the way for even larger applications.

Looking forward, we believe that the Stackelberg POMDP can be used to develop insights and in turn new theoretical results in regard to the design of market platforms. Indeed, studying the properties of learning algorithms as models of agent behavior is of growing interest to economists, especially considering recent work investigating which learning algorithms can lead to collusive behaviors, such as the studies by Cartea et al. (2022) and Brown and MacKay (2023). For instance, the Stackelberg POMDP framework could assist in classifying followers’ response algorithms based on the type of intervention needed to achieve desired outcomes.

Broader Impact and Limitations.

When using simulators to develop AI-based policies, for example to mediate market transactions on platforms, it is important that the data used to build the simulator is representative of the target population. Moreover, the behaviors (and preferences) assumed in training might not reflect the behaviors when deployed, suggesting the importance of continual monitoring to check for assumptions. Additionally, when designing rules for multi-agent systems, it is important to adopt an appropriate design objective. In this paper, we mostly focus on economic welfare, but it should ultimately be up to the relevant stakeholders to determine the best objective.

Acknowledgements

This research is funded in part by Defense Advanced Research Projects Agency under Cooperative Agreement HR00111920029. The content of the information does not necessarily reflect the position or the policy of the Government, and no official endorsement should be inferred. This is approved for public release; distribution is unlimited. The work of G. Brero was also supported by the SNSF (Swiss National Science Foundation) under Fellowship P2ZHP1_191253.

References

- Agrawal et al. (2020) Shipra Agrawal, Jay Sethuraman, and Xingyu Zhang. On optimal ordering in the optimal stopping problem. In Proc. EC ’20: The 21st ACM Conference on Economics and Computation, pages 187–188, 2020.

- Bai et al. (2021) Yu Bai, Chi Jin, Huan Wang, and Caiming Xiong. Sample-efficient learning of Stackelberg equilibria in general-sum games. In Advances in Neural Information Processing Systems 34, pages 25799–25811, 2021.

- Basilico et al. (2017) Nicola Basilico, Stefano Coniglio, and Nicola Gatti. Methods for finding leader–follower equilibria with multiple followers. arXiv preprint arXiv:1707.02174, 2017.

- Brero et al. (2021a) Gianluca Brero, Darshan Chakrabarti, Alon Eden, Matthias Gerstgrasser, Vincent Li, and David C Parkes. Learning Stackelberg equilibria in sequential price mechanisms. In Proc. ICML Workshop for Reinforcement Learning Theory, 2021a.

- Brero et al. (2021b) Gianluca Brero, Alon Eden, Matthias Gerstgrasser, David C. Parkes, and Duncan Rheingans-Yoo. Reinforcement learning of sequential price mechanisms. In Thirty-Fifth AAAI Conference on Artificial Intelligence, AAAI, pages 5219–5227, 2021b.

- Brero et al. (2022) Gianluca Brero, Eric Mibuari, Nicolas Lepore, and David C. Parkes. Learning to mitigate AI collusion on economic platforms. Advances in Neural Information Processing Systems, 2022.

- Brown and MacKay (2023) Zach Y Brown and Alexander MacKay. Competition in pricing algorithms. American Economic Journal: Microeconomics, 15(2):109–156, 2023.

- Cartea et al. (2022) Álvaro Cartea, Patrick Chang, José Penalva, and Harrison Waldon. Learning to collude: A partial folk theorem for smooth fictitious play. Available at SSRN, 2022.

- Cheng et al. (2017) C. Cheng, Z. Zhu, B. Xin, and C Chen. A multi-agent reinforcement learning algorithm based on Stackelberg game. In 6th Data Driven Control and Learning Systems (DDCLS), pages 727–732, 2017.

- Conitzer and Sandholm (2006) Vincent Conitzer and Tuomas Sandholm. Computing the optimal strategy to commit to. In Proceedings 7th ACM Conference on Electronic Commerce (EC-2006), pages 82–90, 2006.

- Fang et al. (2016) Fei Fang, Thanh Hong Nguyen, Rob Pickles, Wai Y Lam, Gopalasamy R Clements, Bo An, Amandeep Singh, Milind Tambe, Andrew Lemieux, et al. Deploying PAWS: Field optimization of the protection assistant for wildlife security. In AAAI, volume 16, pages 3966–3973, 2016.

- Gerstgrasser and Parkes (2023) Matthias Gerstgrasser and David C Parkes. Oracles & followers: Stackelberg equilibria in deep multi-agent reinforcement learning. In International Conference on Machine Learning, pages 11213–11236. PMLR, 2023.

- Goktas and Greenwald (2021) Denizalp Goktas and Amy Greenwald. Convex-concave min-max Stackelberg games. Advances in Neural Information Processing Systems, 34:2991–3003, 2021.

- Hansen et al. (2004) Eric A. Hansen, Daniel S. Bernstein, and Shlomo Zilberstein. Dynamic programming for partially observable stochastic games. In Proceedings of the Nineteenth National Conference on Artificial Intelligence, pages 709–715. AAAI Press / The MIT Press, 2004.

- Hartline et al. (2015) Jason Hartline, Vasilis Syrgkanis, and Eva Tardos. No-regret learning in bayesian games. Advances in Neural Information Processing Systems, 28, 2015.

- Laffont and Tirole (1993) Jean-Jacques Laffont and Jean Tirole. A theory of incentives in procurement and regulation. MIT press, 1993.

- Lowe et al. (2017) Ryan Lowe, Yi Wu, Aviv Tamar, Jean Harb, Pieter Abbeel, and Igor Mordatch. Multi-agent actor-critic for mixed cooperative-competitive environments. In Advances in Neural Information Processing Systems 30, pages 6379–6390, 2017.

- Monderer and Tennenholtz (2003) Dov Monderer and Moshe Tennenholtz. k-implementation. In Proceedings of the 4th ACM conference on Electronic Commerce, pages 19–28, 2003.

- Raffin et al. (2021) Antonin Raffin, Ashley Hill, Adam Gleave, Anssi Kanervisto, Maximilian Ernestus, and Noah Dormann. Stable-baselines3: Reliable reinforcement learning implementations. Journal of Machine Learning Research, 22(268):1–8, 2021.

- Sandholm and Gilpin (2006) Tuomas Sandholm and Andrew Gilpin. Sequences of take-it-or-leave-it offers: Near-optimal auctions without full valuation revelation. In Proceedings of the fifth international joint conference on Autonomous agents and multiagent systems, pages 1127–1134, 2006.

- Schulman et al. (2017) John Schulman, Filip Wolski, Prafulla Dhariwal, Alec Radford, and Oleg Klimov. Proximal policy optimization algorithms. arXiv preprint arXiv:1707.06347, 2017.

- Sinha et al. (2018) Arunesh Sinha, Fei Fang, Bo An, Christopher Kiekintveld, and Milind Tambe. Stackelberg security games: Looking beyond a decade of success. IJCAI, 2018.

- Sutton and Barto (2018) Richard S. Sutton and Andrew G. Barto. Reinforcement Learning: An Introduction. The MIT Press, 2018. ISBN 978-0262039246.

- Wang (1999) You-Qiang Wang. Commodity taxes under fiscal competition: Stackelberg equilibrium and optimality. American Economic Review, 89(4):974–981, 1999.

- Zhang et al. (2023a) Brian Hu Zhang, Gabriele Farina, Ioannis Anagnostides, Federico Cacciamani, Stephen Marcus McAleer, Andreas Alexander Haupt, Andrea Celli, Nicola Gatti, Vincent Conitzer, and Tuomas Sandholm. Computing optimal equilibria and mechanisms via learning in zero-sum extensive-form games. arXiv preprint arXiv:2306.05216, 2023a.

- Zhang et al. (2023b) Brian Hu Zhang, Gabriele Farina, Ioannis Anagnostides, Federico Cacciamani, Stephen Marcus McAleer, Andreas Alexander Haupt, Andrea Celli, Nicola Gatti, Vincent Conitzer, and Tuomas Sandholm. Steering no-regret learners to optimal equilibria. arXiv preprint arXiv:2306.05221, 2023b.

- Zhang et al. (2019) Haifeng Zhang, Weizhe Chen, Zeren Huang, Minne Li, Yaodong Yang, Weinan Zhang, and Jun Wang. Bi-level actor-critic for multi-agent coordination, 2019.

- Zhong et al. (2021) Han Zhong, Zhuoran Yang, Zhaoran Wang, and Michael I Jordan. Can reinforcement learning find Stackelberg-Nash equilibria in general-sum markov games with myopic followers? arXiv preprint arXiv:2112.13521, 2021.

- Zhou et al. (2019) Dequn Zhou, Yunfei An, Donglan Zha, Fei Wu, and Qunwei Wang. Would an increasing block carbon tax be better? A comparative study within the Stackelberg game framework. Journal of environmental management, 235:328–341, 2019.

Appendix A Formal Definition of Subgame of a POMG

Definition A.1 (Subgame of a POMG).

Given a POMG , a subset of the agents in , and a policy profile for agents in , we define the subgame POMG, , as the POMG among agents in where:

-

•

Each state is formed by enhancing a state of with policies and observation histories : .

-

•

The action of each agent , , remains unchanged from the original game: for all .

-

•

The observation of each agent , , is also the same as in the original game: for all .

-

•

The state transition function corresponds to the state transition function in , with the actions of agents in computed using the observation histories and policies in the state. Formally, given , , and , we let , and is equal to if is augmented with new observations generated in , and zero otherwise.

-

•

The reward of each agent , , where , is the reward in , , where .

-

•

The time horizon is the same as the time horizon in the original game .

Appendix B Optimal Policy in Stackelberg POMDP

See 3.1

Proof.

Let denote the set of leader policies in our Stackelberg POMDP and be one of these policies. Let denote a state-action trajectory determined by executing policy in the Stackelberg POMDP. The optimal policy in Stackelberg POMDP solves

| (1) |

recognizing for . In the reward phase, the state transitions are dictated by the transitions of , which represent the state transitions in using the followers’ actions derived from (as defined in Definition 2.2). Thus, for steps , the reward function is equivalent to , where represents the actions of the followers according to the response strategy . We let and reformulate (1) as

| (2) |

We conclude by noticing that, if we restrict the set of leader’s policies considered in equation (2) to , we obtain the leader’s Stackelberg problem in Definition 2.3. ∎

Appendix C Learning an Optimal Policy in Stackelberg POMDP

In this section we show how we can use policy gradient methods [Sutton and Barto, 2018, chapter 13] to optimize Stackelberg POMDP policies within the set of the leader policies in a POMG . As we described in the main paper, these policies map histories of game observations to leader actions in our game. In line with our offline design principles, our policy gradient methods assume access to full POMDP states during training (including followers’ strategies and observations) but learn policies that only require leader observations to determine their actions. This technique is a variant of the centralized training decentralized execution approach [Lowe et al., 2017, see e.g.].

We first consider a parameterized policy and let be the objective in Equation (2) under this generic policy, i.e.,

where and is a trajectory of states, observations, and actions in our POMDP. We have that

where and is the history of game observations after steps of the game-play in our Stackelberg POMDP episode. The gradient of with respect to can be expressed as

where the last equality follows since future actions do not affect past rewards in a POMDP. is approximated by sampling different trajectories :

One problem with this approach is that its gradient approximation has high variance as its value depends on sampled trajectories. A common solution is to replace each term with , where

is the “critic”. Note that can be accessed at training time as we have access to the full state of the POMDP.

Appendix D No-Regret Followers

In this section, we take up a specific kind of policy-interactive response algorithm and show that it leads the followers to the set of Bayesian coarse correlated equilibria.

To simplify the exposition, throughout this section we assume that the POMG among the followers consists of a single step (), where each follower observes its type and picks an action , receiving reward . Note that even in this single step case, we still need to model the leader’s problem as (multi-step) POMDP because we need to capture followers’ learning dynamics across games.888One could reformulate a general POMG into a POMG in which the followers only operate in the first step, and where the action they take in this step determines their policy throughout the original game . In general, this formulation would lead to POMGs with very large action spaces, but remains tractable in the applications we consider in the present paper. Indeed, in normal form games, matrix design games, and simple allocation mechanisms, followers only operate in one step. In sequential price mechanisms with messages, each follower interacts with the mechanism twice, but the dominant-strategy in the second interaction is to be truthful [Brero et al., 2021b, e.g.,].

For the PI response algorithm, we adopt in this application no-regret dynamics for Bayesian games, as described by Hartline et al. [2015]. In these dynamics, each agent independently runs a no-regret algorithm for each possible type it might have. At each step, a type profile is sampled from , with each agent simultaneously choosing their actions using the strategy associated with its type . After observing all other agents’ actions in the game , each agent then uses a no-regret algorithm to update its strategy for its type (see Algorithm 1).

Specifically, we use multiplicative-weights, which we describe in the next section. This algorithm maintains an internal state consisting of agent-specific weights assigned to each action for each possible agent type. These weights represent probabilities over actions and are adjusted based on the rewards obtained by the agent during gameplay.

We next introduce the solution concept of Bayesian Coarse Correlated Equilibrium (BCCE) Hartline et al. [2015], which is an extension of the Coarse Correlated Equilibrium to Bayesian settings. Importantly, the BCCE arises naturally from no-regret dynamics.

Definition D.1 (Bayesian coarse correlated equilibrium).

Consider a Bayesian game with agents, each with type space (), action space (), and a payoff function . Let be the joint type distribution, and the type distribution of all agents but , conditioned on agent having type . Let be a joint randomized strategy profile that maps the type profile of all agents to an action profile. Strategy profile is a Bayesian Coarse-Correlated Equilibrium (BCCE) if for every , and for every , we have

| (3) |

where is a mapping from type profile to actions, excluding agent ’s action.

It is noteworthy that in the definition above, agents jointly map their realized types to actions.

This concept of BCCE generalizes many other known solution concepts such as Mixed Nash Equilibria and Bayes-Nash Equilibria, where and , respectfully; that is, each agent chooses an action using a separate strategy , without correlating the action with other agents.

Hartline et al. [2015] prove that the no regret dynamics described in Algorithm 1 converge to a BCCE for the case of independent types. We generalize this convergence result to the case of correlated types.

Theorem D.1.

For every type distribution , the empirical distribution over the history of actions in the iterative no regret dynamics algorithm for any type profile converges to the set of BCCEs. That is, for every , , , and , we have

| (4) |

where is the empirical distribution after steps.

Proof.

Fix agent , and a type . Let denote the set of time steps at which is sampled as the type of agent , denote the set of time steps at which is sampled as the type profile, and denote the set of time steps at which is sampled and were the agents’ actions. The expected value of agent with type when playing the agent’s action according to the empirical distribution of actions is:

| (5) | |||||

By the Glivenko-Cantelli Theorem, as , . Since it is multiplied by

a bounded term, the second summand of Eq. (5) goes to 0 as .

As for the first summand, we have

By replacing with an arbitrary fixed action in the above derivation, we get that

where as .

Since agent uses a no-regret algorithm for each type , we have that for (which implies ),

for every , where the expectation is over the randomization of the no regret algorithm. Therefore, we have that as ,

which implies that as , the iterative no-regret dynamics converge to a BCCE. ∎

Appendix E Multiplicative-Weights Algorithm

In this section, we describe the multiplicative-weights algorithm that we use to update followers’ strategies (Algorithm 2). The algorithm has three parameters. The payoff function of the agents (in our case, this is the payoff function of the game induced by a leader’s policy ), which determines the game played by our agents, a real number controlling the magnitude of the weight updates, and an integer determining the number of iterations. Each follower is assigned a weight matrix of size by , where all entries are initialized to 1. The following procedure is repeated times: First, a type profile is sampled from distribution . Then, for each follower an action is sampled according to weights . Finally, we compute each agent ’s payoffs when choosing any action , and when the other agents are playing ; we scale each weight accordingly.

Appendix F Illustrating the Stackelberg POMDP for the MSPM Problem

In this section, we describe the Stackelberg POMDP for the MSPM setting, and assuming that followers use the multiplicative-weights algorithm (see Algorithm 2).

F.1 Policy Interactive Response Algorithm

We start by describing how to instantiate our multiplicative-weights algorithm as a policy interactive (PI) response algorithm (see Definition 3.1).

-

•

States: A generic PI state, denoted as , includes:

- –

- –

- –

- –

- –

We note that states can be expressed as since the strategies of the followers, , played during the response phase can be derived by the messages , the agent index , and the message under exploration.

-

•

State transitions: State transitions are described as follows:

-

–

The initial response state, , is determined by:

- *

- *

- *

- *

- *

- –

-

–

Any state satisfying is derived from by:

-

*

Resampling the type profile and followers’ messages ,

-

*

Reinitializing the agent index to zero, and

-

*

Resetting the message under exploration, , to the first message in the list.

-

*

-

–

-

•

Time horizon: The time horizon is determined by .

F.2 Stackelberg POMDP

Using the PI response algorithm described above, we can describe our Stackelberg POMDP for MSPM as follows:

-

•

States: Each state in the Stackelberg POMDP for the MSPM problem comprises of the PI algorithm state and a game state that includes:

-

–

The types of the followers in the current gameplay, which are the same as those in the algorithmic state,

-

–

The followers’ messages in the current game play,

-

–

The partial allocation at the current game step, and

-

–

The residual setting at the current game step (specifying the unvisited agents and unsold items).

-

–

-

•

Observations: These consist of messages , partial allocation , and the residual setting at the current state.

-

•

Actions: The action of the leader consists of the agent to be visited, and the prices to be quoted to this agent, in the upcoming game step.

-

•

State transitions: While the PI algorithm states are updated following the description of our PI response algorithm, the game states are updated as described below:

-

–

Game initialization: We then initialize the partial allocation as and the residual setting as . Then,

-

*

Followers’ response phase: If we are in this phase, types and in-game messages are derived from the algorithmic state (with messages being obtained from messages by substituting the message under exploration ).

-

*

Reward phase: otherwise, we sample types from distribution and let be the equilibrium strategies derived in the response phase (in our implementation, these are derived from the weights in the final algorithmic state).

-

*

-

–

Game progression: The game advances for steps. During each step, the leader policy observes and takes action , where is the next selected agent and is the vector of posted prices. Agent chooses a set of items that maximize its profit at prices . The new game state is obtained by adding the bundle selected by agent to the previous partial allocation to form a new partial allocation , and the items and agent are removed from the residual setting . If there are no more agents to visit (i.e., game ends), game state is restarted as described above. If we are in the reward phase, a reward capturing the objective of the designer, for example the social welfare or revenue to the seller, is generated.

-

–

Appendix G The Escape Game

In this section we give results for the Escape game described in Zhang et al. [2019], and explained in Table 4. Here, the optimal leader action is to play row . Indeed, if the leader chooses , the follower responds with column and both follower and leader realize their maximum payoff. This is also a Nash equilibrium, as is and . As we can see from Figure 5, the leader learns to play row C immediately, with both MAPPO and PPO used to solve the Stackelberg POMDP.

Appendix H MSPM Settings: Description and Analyses

H.1 First Setting: One item, two agents, two possible types

In the setting introduced by Agrawal et al. [2020], we consider a situation with two agents and one item. Each agent’s type, which corresponds to their value for the item, has two possible values. The first agent has type , assigned probabilities . For our experiments, we use a value of . The second agent’s type with each possibility having equal probability .

The welfare-optimal allocation cannot always be realized when followers cannot signal their types. Indeed, the optimal sequential price mechanism (without the ability for agent messaging) visits agent 2 first and then agent 1, using price zero in both cases. However, this design is inefficient when and , as it would allocate the item to agent 2, which has the lowest value.

Stackelberg POMDP was able to identify two optimal MSPMs with 2 messages (each bidder either sends 0 or 1):

-

1.

When agent 1 sends message 0, the mechanism opts for a minimal price (for instance, 0.1) in every round and visits agent 2 first. On the other hand, if agent 1 sends message 1, the mechanism sets the price between and in the initial round and visits agent 1 first. This mechanism ensures welfare is maximized for all possible value combinations. Importantly, it is a dominant strategy for agent 1 to send message 0 when their value is low. Should they send message 1, they would be visited first, but the quoted price would exceed their value.

-

2.

A second type of MSPMs identified by our Stackelberg POMDP uses the bid from agent 2. In this scenario, agent 1 is always visited first. However, the price offered to agent 1 depends on agent 2’s bid: if agent 2 bids 1, the price lies between and ; if agent 2 bids 0, the price is less than . In this setup, it remains a dominant strategy for agent 2 to bid truthfully, as signaling a high value increases their chances of allocation since agent 1 is presented with a higher price.

H.2 Second Setting: One item, two agents, three possible types

In the second setting we have two identical agents and one item. Each agent’s value for the item is drawn uniformly from .

For an SPM that without messages, the optimal mechanism randomly selects one of the identical agents to visit first and offers a price of . If the first agent does not buy the item, the mechanism then visits the second agent, offering a price of 0. However, this mechanism is inefficient if the first agent visited has a value of and the second one has a value of .

Stackelberg POMDP is able to identify various optimal MSPMs with two messages, labelled as 0 and 1:

-

1.

In the first category of MSPMs discovered by Stackelberg POMDP, the first agent, e.g. agent 1, bids 0 if its value is 0, and 1 otherwise. The mechanism always visits agent 2 first, and sets the price at 0 if agent 1’s bid is 0. If agent 1’s bid is anything else, the price is set between 0.5 and 1. The second price quoted is always 0.

-

2.

The second category of MSPMs discovered by Stackelberg POMDP is slightly more complex and takes into account both bids. The first quoted price is always set at 1, while the second is always 0. Both agents signal 0 if their value is 0, and 1 otherwise. If an agent signals 1, they are visited second, giving them an opportunity to achieve a strictly positive payoff. If both agents signal 1, preference is given to one of the agents, which is visited second, to break the tie.

In both types of mechanisms, it is a dominant strategy for agents to signal their types. Notably, even though in this setting agents are a priori identical (i.e., their values are sampled from the same distribution), the mechanisms learned lead to an imbalance, with one player having higher expected utility than the other.

The first category of mechanisms benefit the agent who places the informative bid: if this agent signals a positive value, the other agent cannot achieve a payoff greater than 0.5. The second category of mechanisms favor the agent who is visited second in the case that both agents signal 1. An interesting question for future investigation is whether we can modify the leader’s reward to promote more equitable outcomes.

Appendix I Additional Experimental Setting: Simple Allocation Mechanisms

As a first Bayesian setting, we explore a scenario with a single follower, and where the leader’s problem is to design a simple allocation mechanism. As with the full information single-follower settings, multiplicative-weights converges to a follower best response, and this best response is unique when responding to an optimal leader’s strategy.

Here, we study a problem in which a mechanism must allocate one of three items to an agent, and where the agent is interested in only one item. When the game begins, the agent’s item of interest (i.e., its type) is sampled uniformly at random. The agent can send a message, , to the mechanism, and the mechanism allocates one of the items to the agent on the basis of this message. If the agent receives its item of interest, the utility of both the mechanism and the agent is 1, and the utility of each of the mechanism and agent is 0 otherwise. Thus, the mechanism’s design goal is to maximize expected welfare.

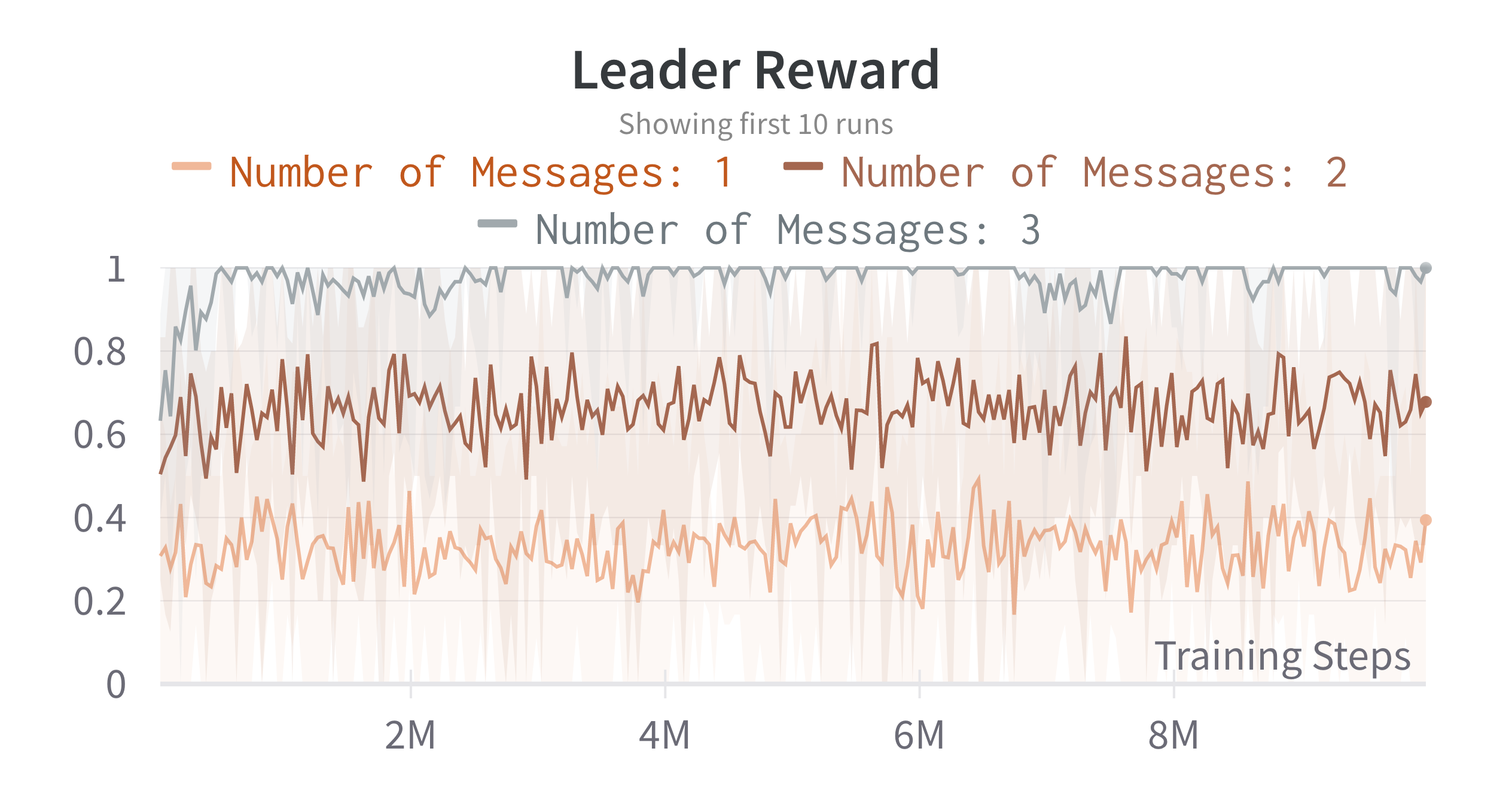

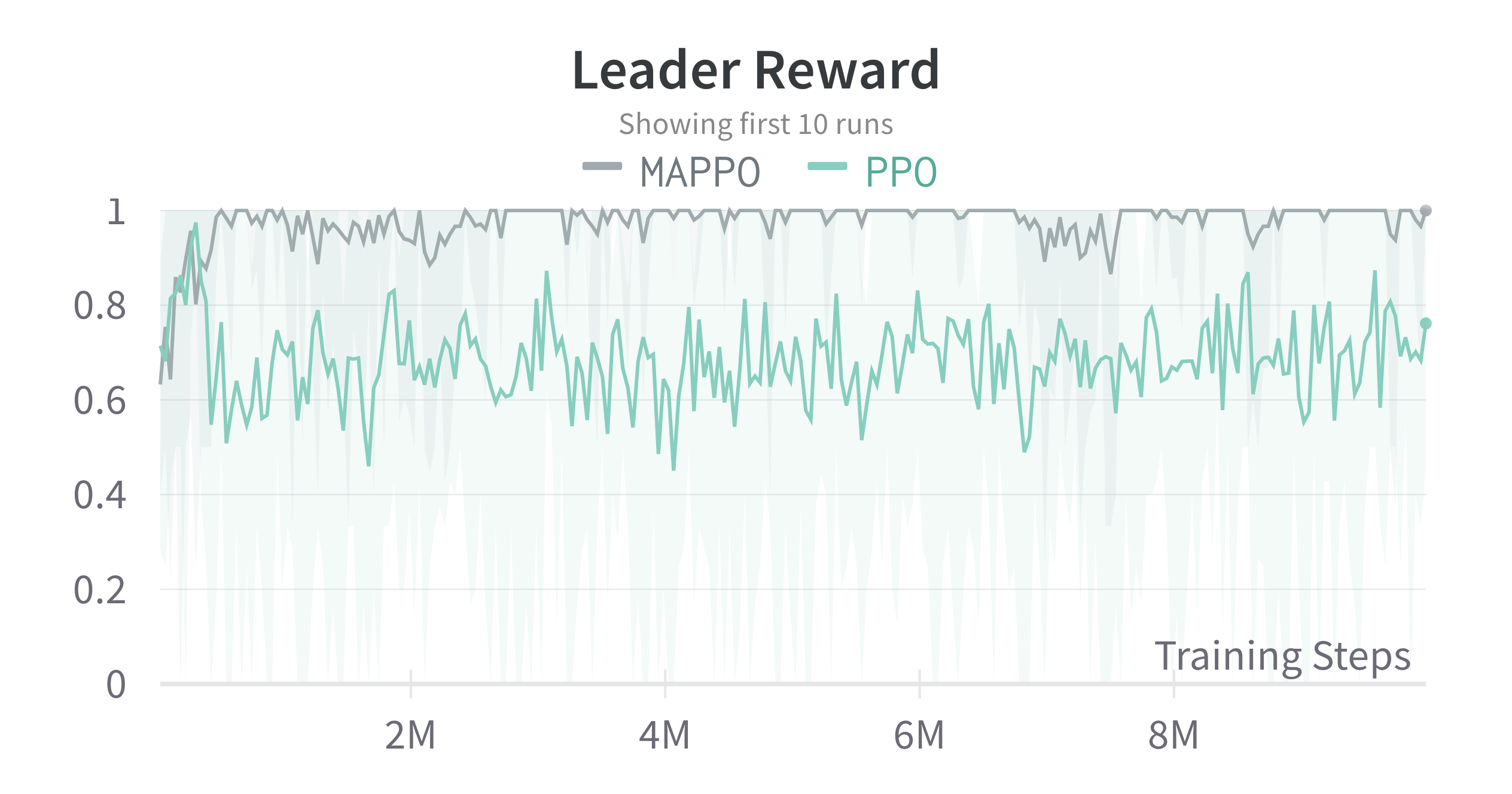

We test the performance of MAPPO and Stackelberg POMDP when varying the number of distinct messages that can be sent, in . For , the communication is uninformative because the agent must always send the same message and this provides a simple baseline. The results are displayed in Figure 6(a). When , the agent cannot inform the mechanism, and the mechanism chooses a random item and only succeeds one third of the time. When , the agent can signal its preferred item one third of the time by reserving a message for a specific type and utilizing the other message for the remaining types. This signaling capability enables the mechanism to increase the expected reward to . When , the agent can signal its type exactly, and the mechanism can always realize the maximum reward (i.e., 1). As we can see, MAPPO realizes this optimal payoff after a relatively short training phase.

We also compare MAPPO and PPO in this scenario, for the case of . As we can see from Figure 6(b), MAPPO again significantly outperforms PPO when used within the Stackelberg POMDP framework.