Learning Algorithms for Intelligent Agents and Mechanisms

Abstract

The ability to learn from past experiences and adapt one’s behavior accordingly within an environment or context to achieve a certain goal is a characteristic of a truly intelligent entity. Developing efficient, robust, and reliable learning algorithms towards that end is an active area of research and a major step towards achieving artificial general intelligence. In this thesis, we research learning algorithms for optimal decision making in two different contexts, Reinforcement Learning in Part I and Auction Design in Part II.

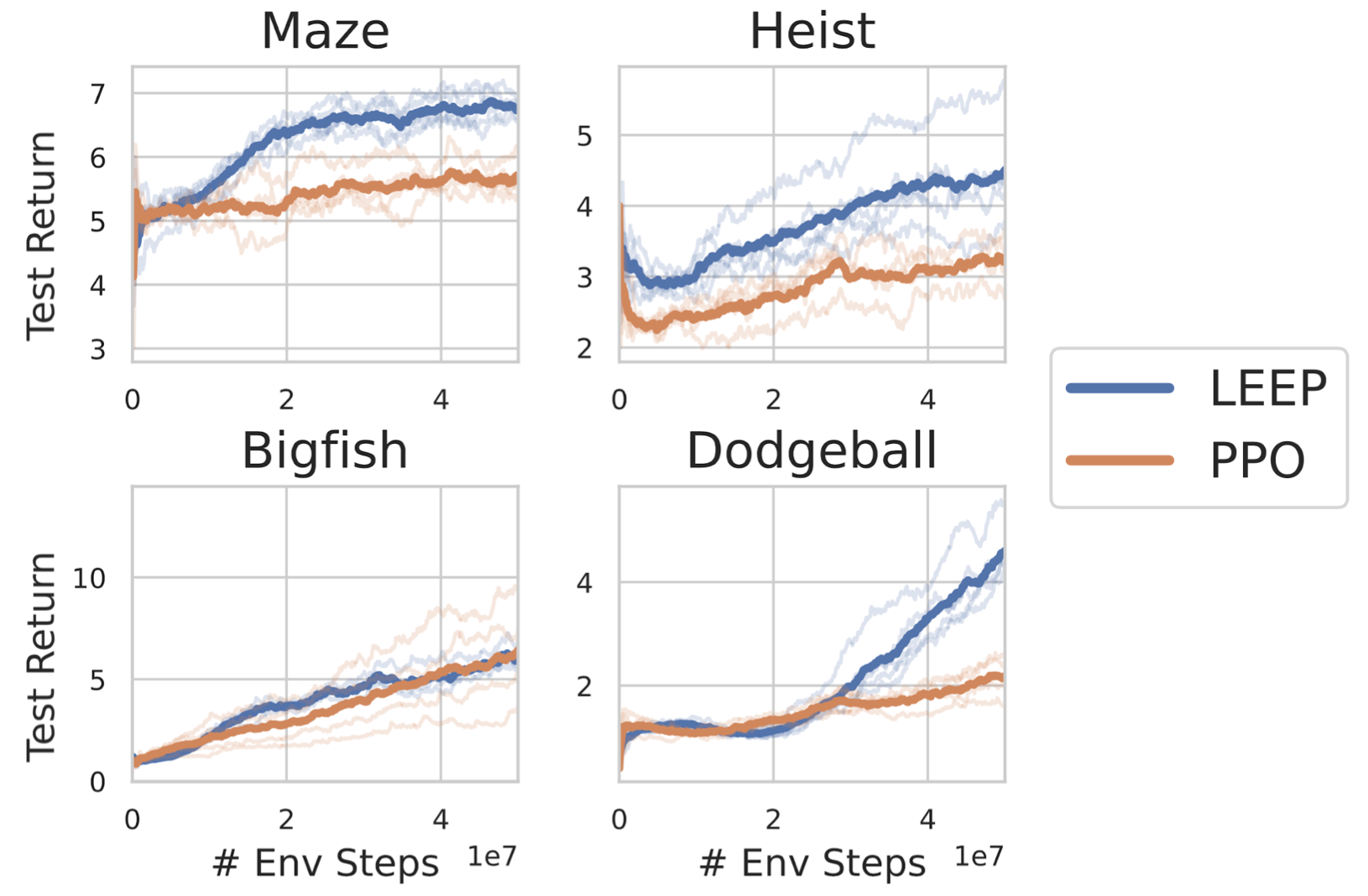

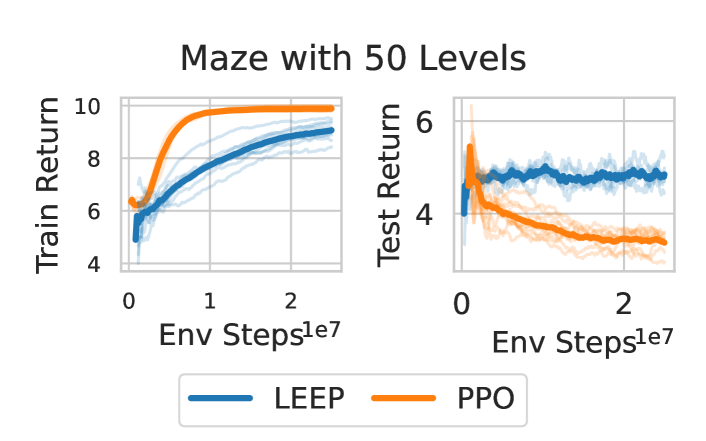

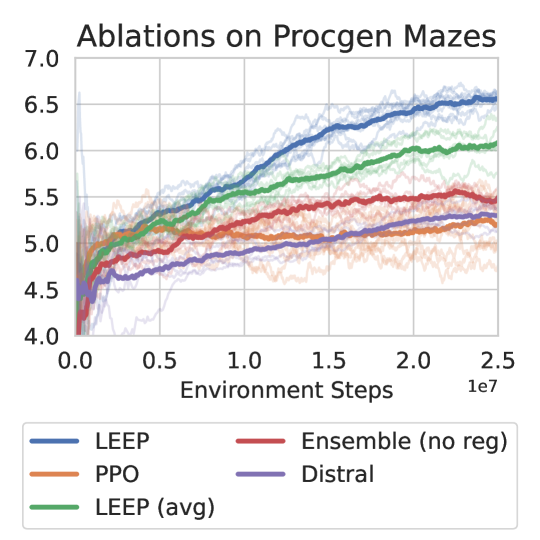

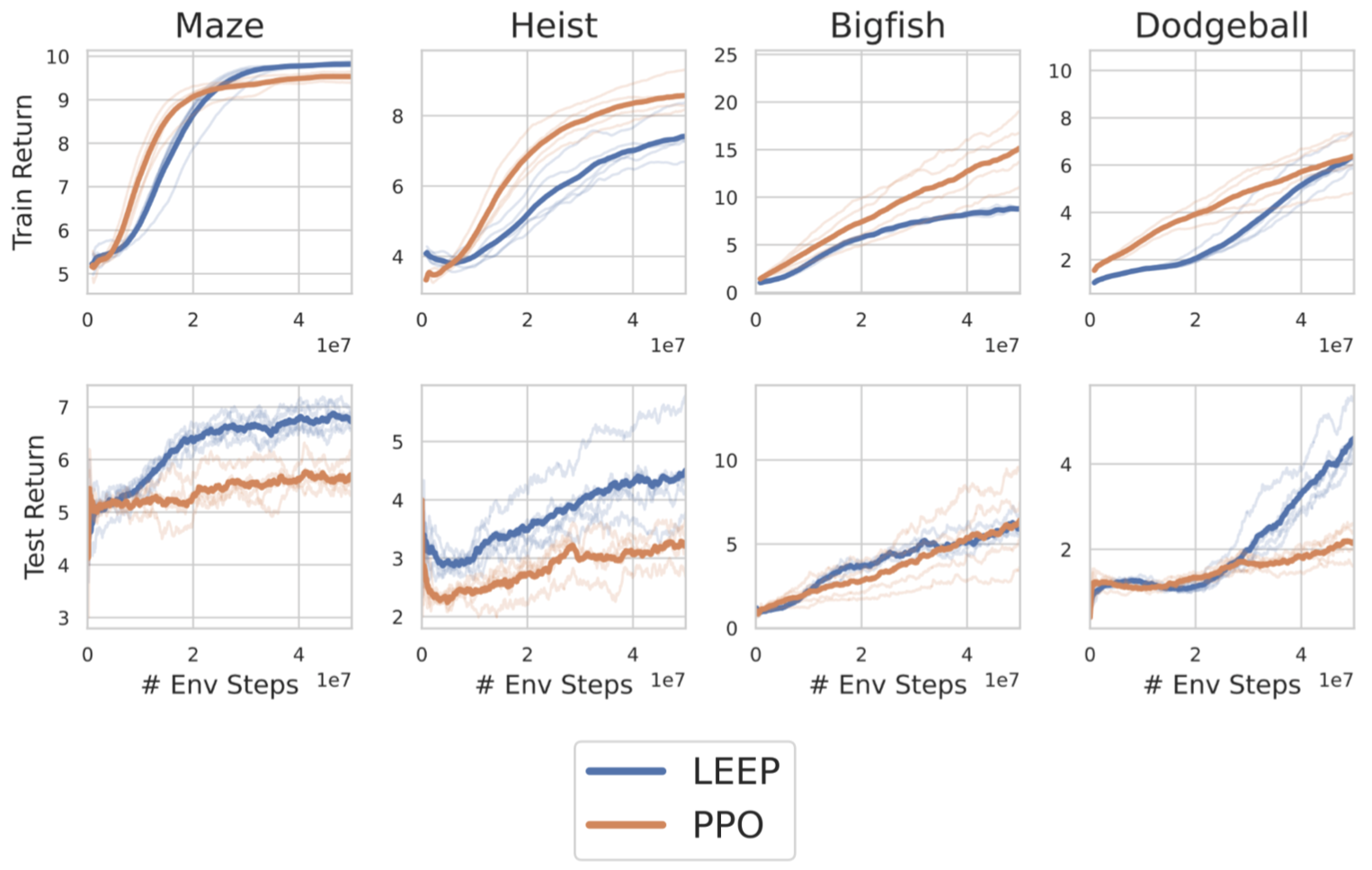

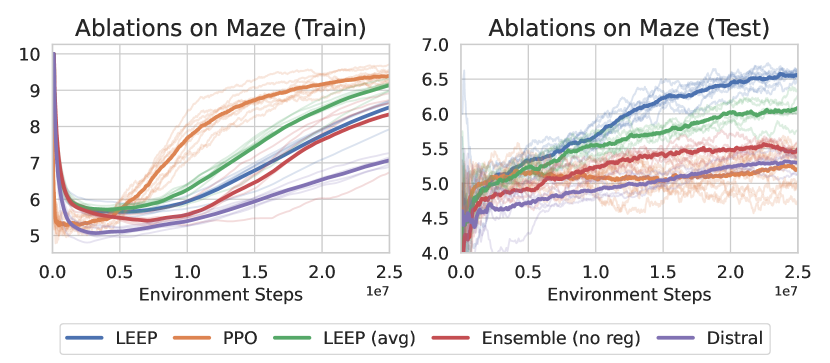

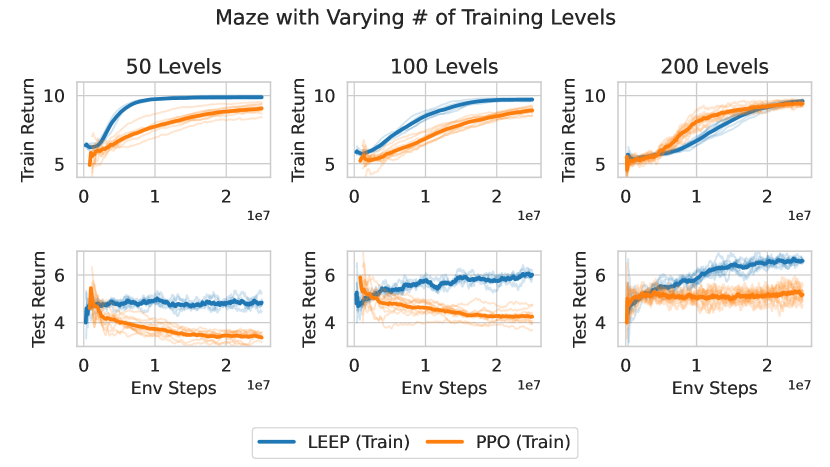

Reinforcement learning (RL) is an area of machine learning that is concerned with how an agent should act in an environment in order to maximize its cumulative reward over time. In Chapter 2, inspired by statistical physics, we develop a novel approach to RL that not only learns optimal policies with enhanced desirable properties but also sheds new light on maximum entropy RL. In Chapter 3, we tackle the generalization problem in RL using a Bayesian perspective. We show that imperfect knowledge of the environment’s dynamics effectively turn a fully-observed Markov Decision Process (MDP) into a Partially Observed MDP (POMDP) that we call the Epistemic POMDP. Informed by this observation, we develop a new policy learning algorithm LEEP which has improved generalization properties.

An auction is the process of organizing the buying and selling of products and services that is of great practical importance. Designing an incentive compatible, individually rational auction that maximizes revenue is a challenging and intractable problem. Recently, a deep learning based approach was proposed to learn optimal auctions from data. While successful, this approach suffers from a few limitations, including sample inefficiency, lack of generalization to new auctions, and training difficulties. In Chapter 4, we construct a symmetry preserving neural network architecture, EquivariantNet, suitable for anonymous auctions. EquivariantNet is not only more sample efficient but is also able to learn auction rules that generalize well to other settings. In Chapter 5, we propose a novel formulation of the auction learning problem as a two player game. The resulting learning algorithm, ALGNet, is easier to train, more reliable and better suited for non stationary settings.

sn edges/.style=for tree=edge=-¿ \submittedSeptember 2022 \adviserRyan P. Adams \departmentprefixProgram in

Acknowledgements.

First of all, I would like to thank my adviser, Ryan Adams, for his guidance and support throughout my doctoral studies at Princeton. I’m grateful for his availability, flexibility, and generosity, especially when it comes to sharing research ideas and insights on a wide range of topics. Throughout my PhD, I was fortunate to have the support of many Princeton faculty and administrative staff. I’m grateful to Matt Weinberg for his guidance and mentorship. His knowledge and expertise in mechanism design were critical when it came to bringing the second part of this thesis to fruition. I would also like to thank Peter Ramadge, Szymon Rusinkiewicz, Karthik Narasimhan for completing my thesis committee. I extend my gratitude to the supportive PACM department and Davis International Center. I was also fortunate to take part in many opportunities outside of Princeton. I would like to express my gratitude to Sergey Levine for inviting me to visit his lab at UC Berkeley during the 2020-2021 academic year. His extensive knowledge and perspective on reinforcement learning helped me gain novel insights in the field. I’m also grateful for the summer internship opportunities I had at Quantlab, Susquehanna, and D.E. Shaw & Co. Despite being mostly virtual due to the pandemic, these experiences were very enriching and helped me acquire valuable knowledge, both theoretical and practical. I would also like to thank my co-authors and collaborators including: Samy Jelassi, Aviral Kumar, Benjamin Eysenbach, Bianca Dumitrascu, Dibya Ghosh, Joan Bruna and Amy Zhang. I extend my gratitude to my colleagues in the Laboratory for Intelligent Probabilistic Systems (LIPS) at Princeton. Last but not least, I would like to thank my parents, brother, sister, grandparents, family members, and Iryna for their never-ending support. \dedicationTo my parents. \nobibliography* \makefrontmatterChapter 1 Introduction

1.1 Overview

Reinforcement learning (RL) is an area of machine learning that is concerned with how an agent should act in an environment in order to maximize its cumulative reward over time. Whenever the agent takes an action, the state of the environment changes and the agent is rewarded accordingly. Based on observations of the dynamics, the agent gains a better understanding of its environment, which enables it to refine its strategy, also called policy, by choosing actions that are increasingly closer to optimality. The difficulty in reinforcement learning is that the dynamics of the environment and their associated rewards (the rules of the game) are unknown to the agent in advance; they can only be inferred through trial and error. This translates in practice to a tension between two types of behavior: exploration and exploitation. Exploration consists of trying new strategies with the hope of finding better ones or gaining a better knowledge of the rules of the game. Exploitation on the other hand is a more conservative attitude that consists of accumulating rewards via strategies that are already known to be good. Optimally balancing these two behaviors is at the core of RL and remains a major open question to this day.

Recent advancements on this challenging problem resulted in successes on tasks that were thought to be out of reach for our current technology. One of the most notable examples is AlphaGo Zero (Silver et al., 2017), a computer program that achieved super-human performance in the traditional board game of Go through self-play. The scope of reinforcement learning is, however, not limited to games; RL offers a very general framework to reason about a broad range of problems such as robotic manipulation and dexterity (Andrychowicz et al., 2020), data center cooling (Lazic et al., 2018), and optimizing chemical reactions (Zhou et al., 2017). Recently RL has been successfully applied on various physics problems including optimal jet grooming (Carrazza and Dreyer, 2019), quantum state preparation (Bukov et al., 2018; Bukov, 2018; Albarrán-Arriagada et al., 2018), quantum gate design (Niu et al., 2019) and quantum error correction (Fösel et al., 2018), often outperforming previous optimization methods.

Many approaches could be taken to tackle a reinforcement learning problem. Most of the successful ones however end up learning a quantity called a value function in one way or another. A value function is a function that takes a state of the environment and returns the expected cumulative rewards an agent can achieve starting from that state. A more technical definition of the value function can be found in Section 1.3. In a game of chess or Go, a value function could for example look at the state of the board and compute the probability that Black wins.

Rewards and value functions have a very similar flavor to energies - they are extensive quantities and the agent is trying to find a path that maximizes them. Many natural phenomena can be understood via an extremization principle. For example, in classical mechanics or electrodynamics, the principle of least action dictates that a mass or light will follow the path that minimizes a physical quantity called the action. Similarly, in thermodynamics, a system with many degrees of freedom—such as a gas—will explore its configuration space in search of a configuration that minimizes its free energy. In RL, value functions are often treated as the central object of study. This stands in contrast to statistical physics formulations of such problems in which a quantity called the partition function is the primary abstraction, from which all the relevant thermodynamic quantities—average energy, entropy, heat capacity—can be derived. A natural question to ask is whether there exists a theoretical framework for reinforcement learning that is centered on a partition function, in which value functions can be interpreted via average energies?

This question is explored in Chapter 2. Inspired by the construction of partition functions in Statistical Physics, we construct a partition function for every state of the environment from the ensemble of possible trajectories spanning from that state. Although value functions can be derived from these partition functions and interpreted via average energies, we show that our purely partition function based approach can form the basis of alternative dynamic programming approaches.

Compared to classical reinforcement learning methods, our approach has three main benefits. First, in deterministic environments, partition functions obey linear Bellman equations allowing direct solutions that were unavailable for the nonlinear equations associated with the use of traditional value functions. Second, our approach is able to treat all rewards equally over time, which contrasts with traditional approaches that need to discount future rewards in order to get well defined Bellman equations. Third, our approach learns policies that are qualitatively different from the ones found by classical RL algorithms. These policies not only optimize for energy (the sum of future rewards) but also take entropy into account, favoring states from which many good outcomes are possible. To illustrate that point, let’s consider a simple setting in which an agent is trying to go from point A to point B. At point A, two actions are possible: going up or going down. If the agent chooses up then there is only one path that leads to B, but if he chooses down then there are 99 valid paths that lead to B. Let’s further assume that all these paths are equally good. Traditional RL approaches will not have a preference between going up or going down as both of them lead to B. Our approach however will prefer going down and even prescribes choosing the down action 99 times more frequently than the up action. Such policies are desirable for their exploratory and robustness properties.

From this example, we can see that our statistical physics based approach to reinforcement learning naturally leads our agent to select action in a stochastic way - this is referred to as a stochastic policy. In contrast, a policy is deterministic if the agent always selects the same action given a certain state. If an environment is known and Markovian, commonly referred to as a Markov Decision Process (MDP), one could prove that there always exists a deterministic policy that acts optimally in that environment. As a result, one could think that learning a deterministic policy is optimal (Sutton and Barto, 2018). However, when the environment is not fully known, this is not the case and deterministic policies can then fail in a miserable way.

To illustrate that, consider a simple task in which an agent is first presented with an image of an animal and then has identify it with as few guesses as possible. In this example, a policy is just a mapping from images to guesses or labels. During the training phase, the agent is presented with images of dogs, cats and other animals from the training set and learns how to identify them. During the testing phase the agent is presented with new images of the same animals. In the hypothetical case where the training set is exhaustive, containing every picture of every animal from every angle, background and lighting condition, a deterministic policy learned on the training set will perform equally as good on the testing set. In real life however, data is limited and it is very unlikely that the agent will be able to learn a perfect classifier that correctly generalizes to new images with perfect accuracy. As a result, during the testing phase, the agent will at some point encounter an image that he is unable to classify correctly, not only in his first guess but in all the subsequent infinite number of available guesses as well because the policy is deterministic. This is problematic, especially given that even a completely random guessing policy will eventually guess the correct label.

This simple toy experiment seems to indicate that there is a benefit in learning a stochastic policy to improve generalization. In fact, many successful RL algorithms encourage the agent to learn a stochastic policy by explicitly regularizing the entropy of the policy in the optimization objective. Adding uniform randomness everywhere is, however, sub optimal. The randomness in the agent’s policy should reflect his uncertainty and confidence about his decision making. In Chapter 3 we study the generalization problem in Reinforcement Learning from a Bayesian perspective by modeling the uncertainty the agent has about the environment. We show how incomplete and imperfect knowledge of the environment implicitly turns a fully observed and Markovian environment (MDP), into a Partially Observed MDP (POMDP) (Sondik, 1971) which we call the Epistemic POMDP. This novel point of view allows us to derive a new RL algorithm, LEEP, with improved generalization properties.

Having robust, data efficient, and reliable learning algorithms is a necessary ingredient to solve real world problems with RL. An equally important and crucial ingredient is having a good reward function. After all, this is the quantity that RL algorithms are trying to optimize. Many real world problems do not come with natural reward functions - these are usually crafted by humans. Even in situations where there is a natural reward function to optimize, there is still some benefit in engineering a new reward function that makes the optimization problem easier to solve. For instance in the game of chess, a natural reward function is to reward an agent with a +1 for win, 0 for a draw and -1 for a loss. This is an example of a sparse reward function because the agent only gets rewarded at the end of the game without intermediate feedback. Sparse reward functions are hard to optimize and it is sometimes helpful to introduce intermediate rewards that are positive when the agent captures an opponents’ piece and negative when they lose one. While it’s helpful to introduce intermediate rewards and more generally handcraft a reward function, reward shaping introduces human bias into the problem and in many cases, the policy that the agent learns will exploit the reward function in ways that the designer did not foresee. In some cases, the policy that maximizes the human engineered reward function does not solve the original task. One example of that is a game called Coast Runners where boats compete to finish a race as quickly as possible. To help them, intermediate targets were designed along the racetrack that not only help them get speed boosts but also reward them with extra bonus points when they are hit. It turned out that these intermediate targets disincentivized the agent from learning to win the race. The highest possible score is achieved by ignoring the race and focusing on hitting these intermediate targets (Clark and Amodei, 2016).

Unintended negative consequences of an incentive are not restricted to games or RL, they can be found in many real life societal policies as well. The Cobra effect (Siebert, 2001) is a historical anecdote used to illustrate perverse incentives that presumably occurred in India during the British rule. The British government, concerned about the increasing number of venomous cobras in Delhi, offered a bounty incentive for every dead cobra in hopes of reducing their numbers. This policy was very successful at reducing the number of cobras until the people realized that they could significantly increase their income by breeding cobras. The policy was subsequently canceled and the final situation was worse than the starting point.

Designing reward functions that are robust to these perverse incentives is not a very well studied subject within reinforcement learning. It is however a central theme in Mechanism Design, a sub field of Game Theory. Game Theory studies the emergent macroscopic behavior resulting from known microscopic interactions between agents. Mechanism Design goes the other way - it starts from a desirable macroscopic behavior and then tries to design mechanisms and incentives, or the rules of the game, that would result in this global behavior, assuming individuals act rationally. That’s why it’s sometimes referred to as reverse game theory. Mechanism design has been applied to many fields from economics and politics to many problems such as market design, auction theory, social choice theory, voting systems, networked-systems, and many others. In this thesis, we will focus on Auction Theory, and while some of the ideas and methods we introduce are specific to that domain, others are more generally applicable to other domains in mechanism design.

An auction is a process of organizing the buying and selling of products and services that is of great practical importance in many private and public sectors. Examples include the sales of treasury bills by the US government, radio wave frequencies by the FCC, art by Christie’s, or ads by Google. A simple auction model goes as follows: at the start of the auction, each one of the bidders place a bid on each one of the items. All of these bids are then collected by the Auctioneer who decides the item allocation as well as the amount each bidder has to pay for their participation in the auction. While any mapping from bids to allocations and from bids to payments could constitute a valid auction mechanism, in practice, we prefer auctions that verify some desirable properties.

The first desirable property is called incentive compatibility. An incentive compatible auction mechanism is one where the utility of each bidder is maximized by bidding truthfully on each one of the items. This means that the optimal bid on an item is exactly the amount of money that the bidder is willing to pay for the item. If an auction is not incentive compatible, bidders could strategically choose their bids and potentially bid untruthfully to maximize the value they get from participating in the auction. Enforcing incentive compatibility disincentivises any strategic behavior and as a result levels the playing field for all the bidders, irrespective of their experience, motivation, and means. Incentive compatible auctions are sometimes referred to as strategy-proof auctions.

The second desirable property is called individual rationality. An individually rational auction is one where a bidder is never worse off after participating in the auction as long as their bid is truthful. For instance, this means that a bidder will not be charged for participating in the auction if she didn’t end up getting any of the items. More generally, the value of the items that a truthful bidder gets is always greater than or equal to the amount she has to pay to the auctioneer. Individual rationality encourages participation in the auction.

How to design an incentive compatible, individually rational auction mechanism that maximizes revenue for the auctioneer? Despite its apparent simplicity, this problem turns out to be surprisingly hard. In the case where there is a single item for sale, the solution is known from Myerson’s seminal piece of work (Myerson, 1981). Beyond the single item setting, the problem is not completely resolved even for auctions as simple as two bidders and two items, despite forty years of mathematical research. Another line of work to confront this theoretical hurdle consists in building automated methods to find the optimal auction, typically by framing the problem as a linear program. However, this approach suffers from severe scalability issues as the number of constraints and variables grows exponentially with the number of bidders and items (Guo and Conitzer, 2010).

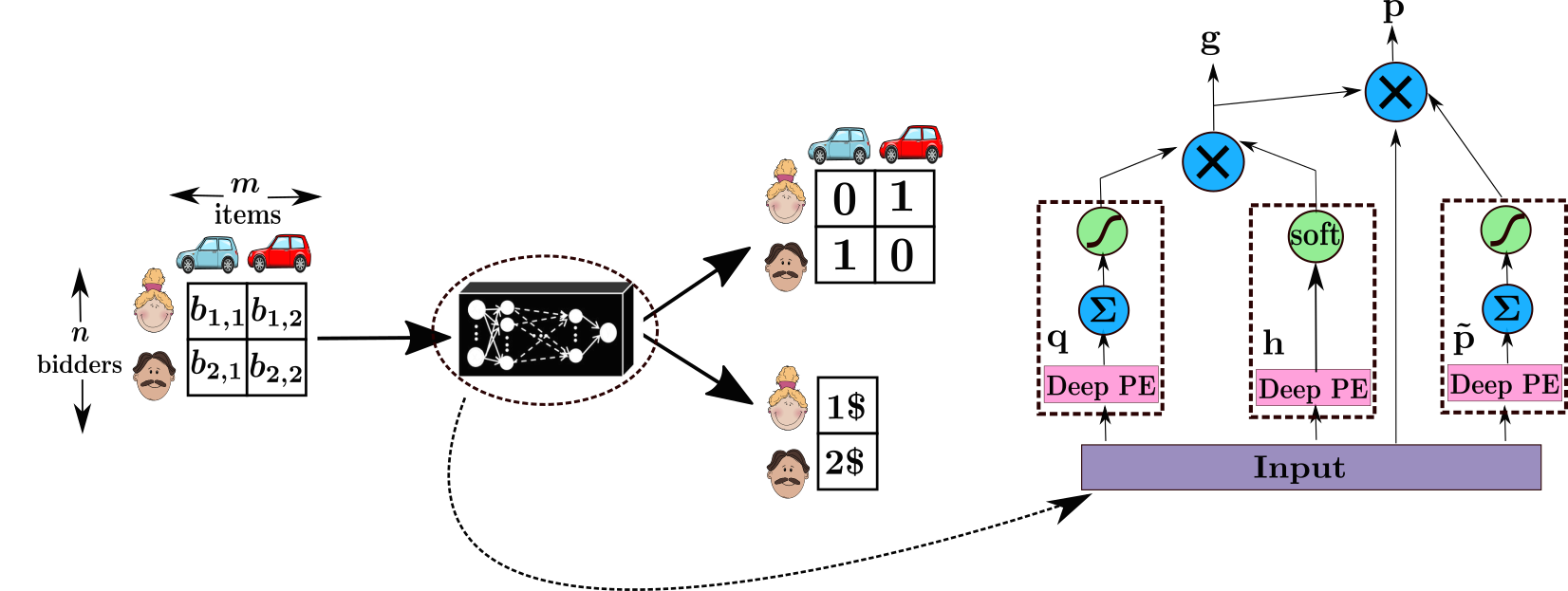

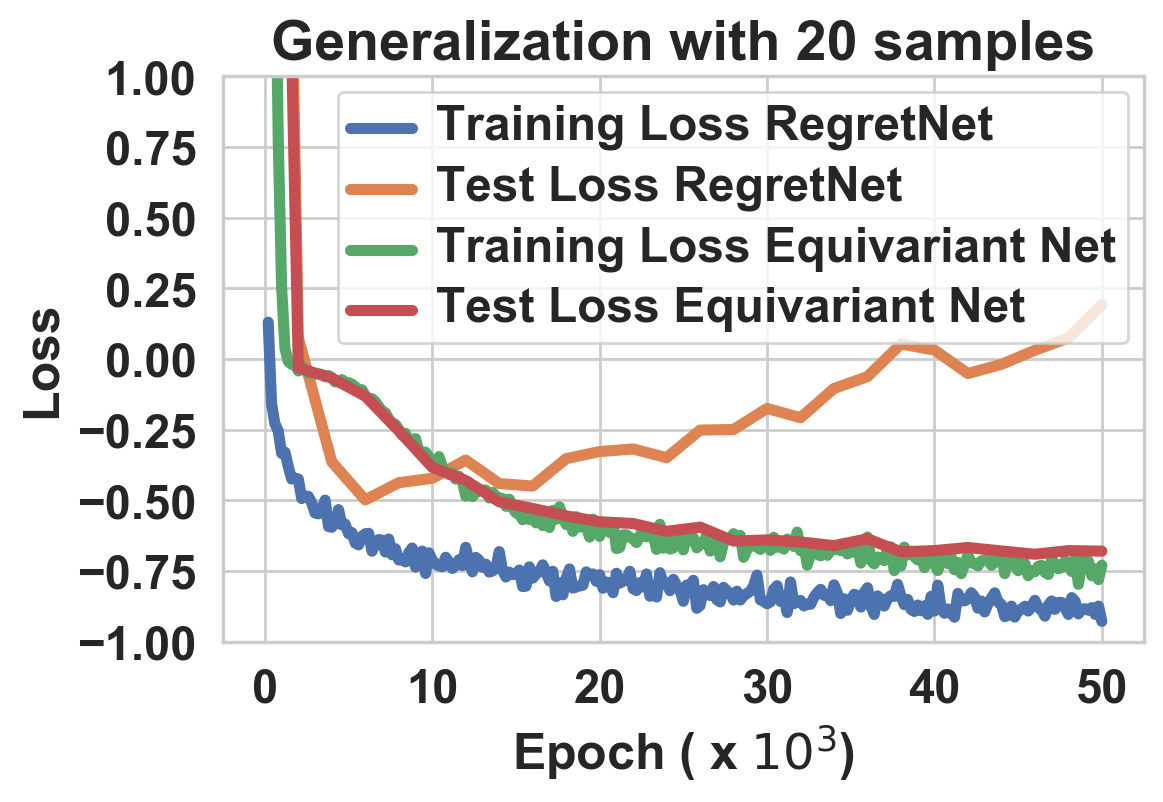

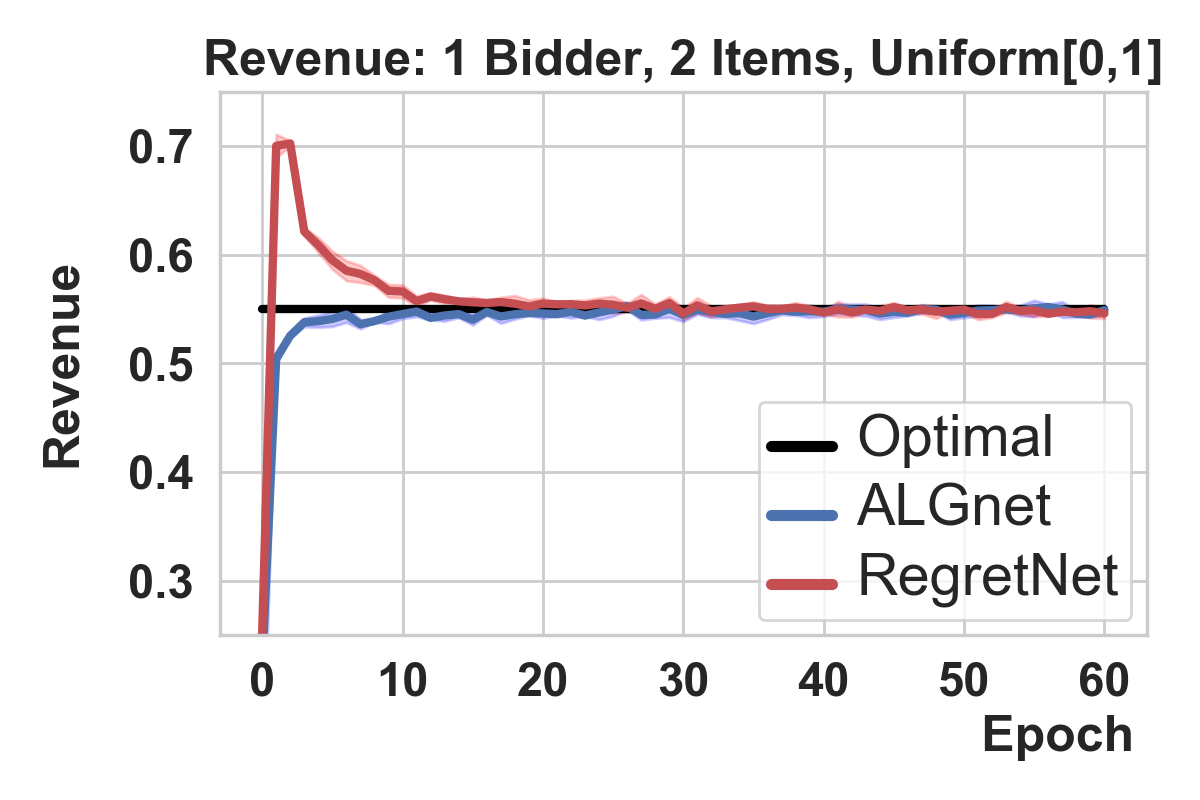

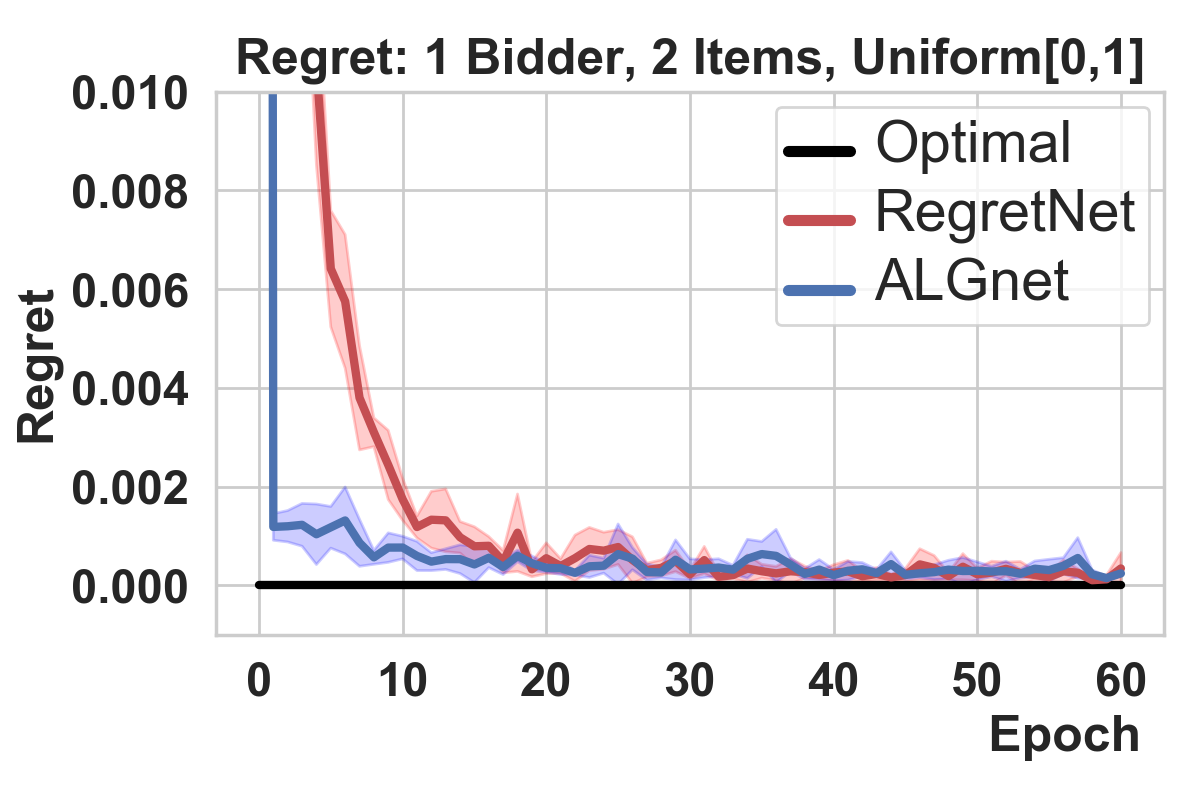

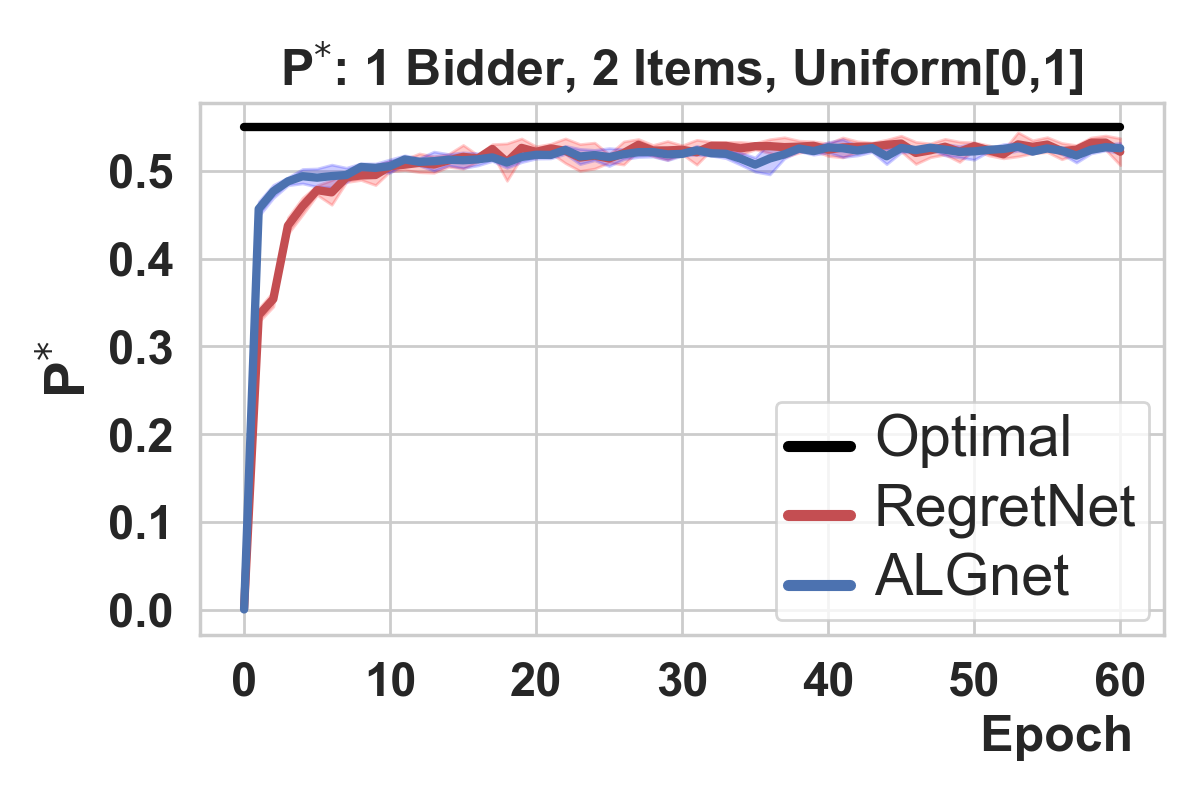

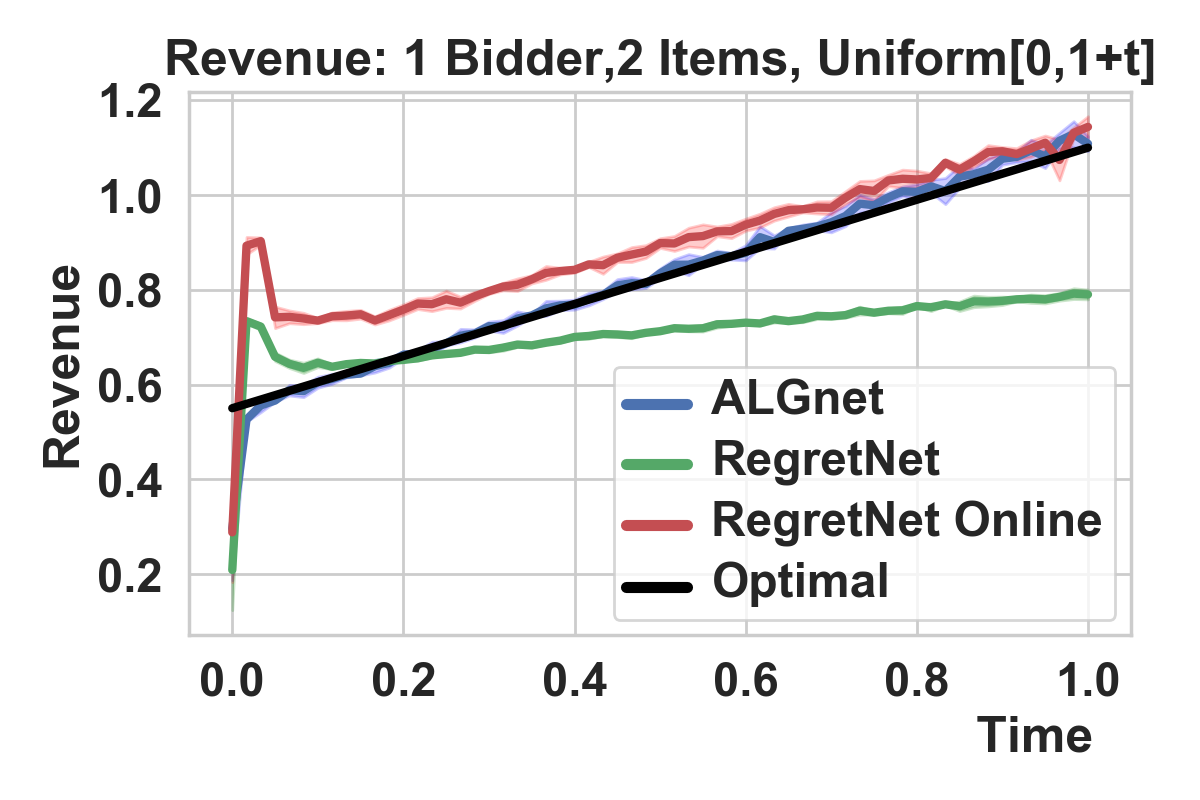

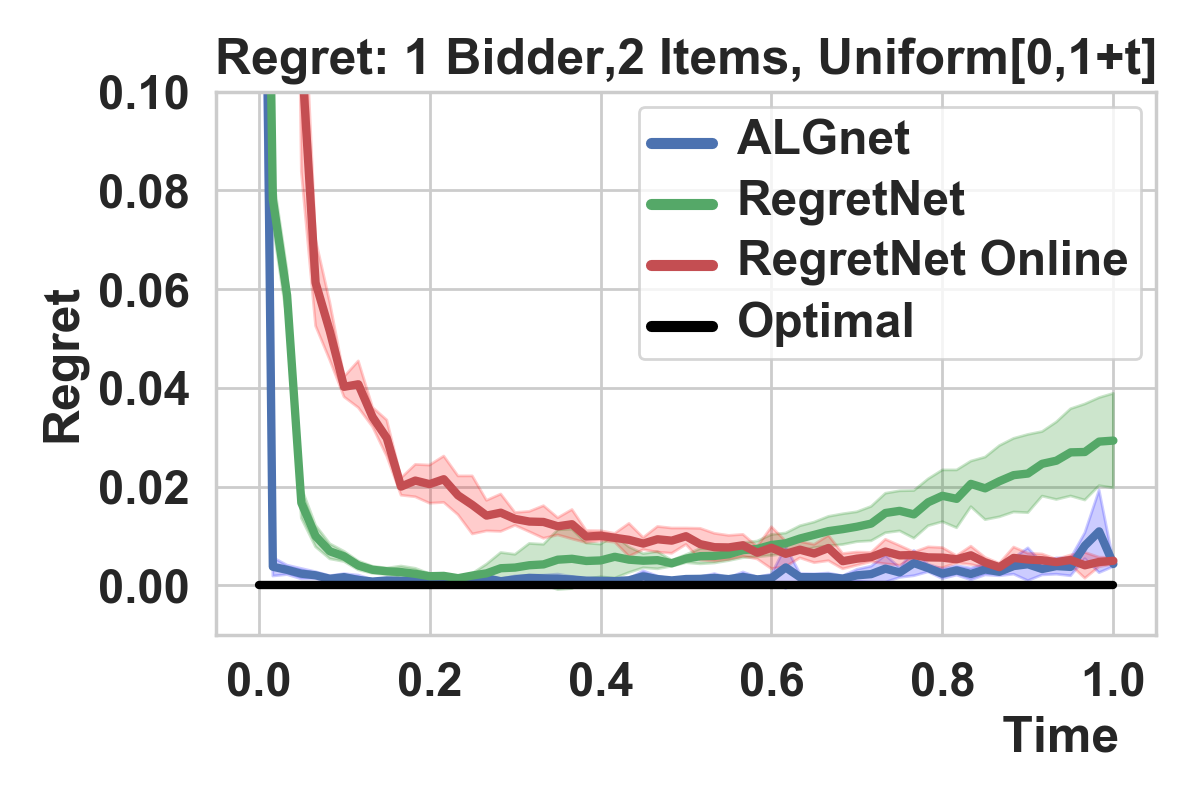

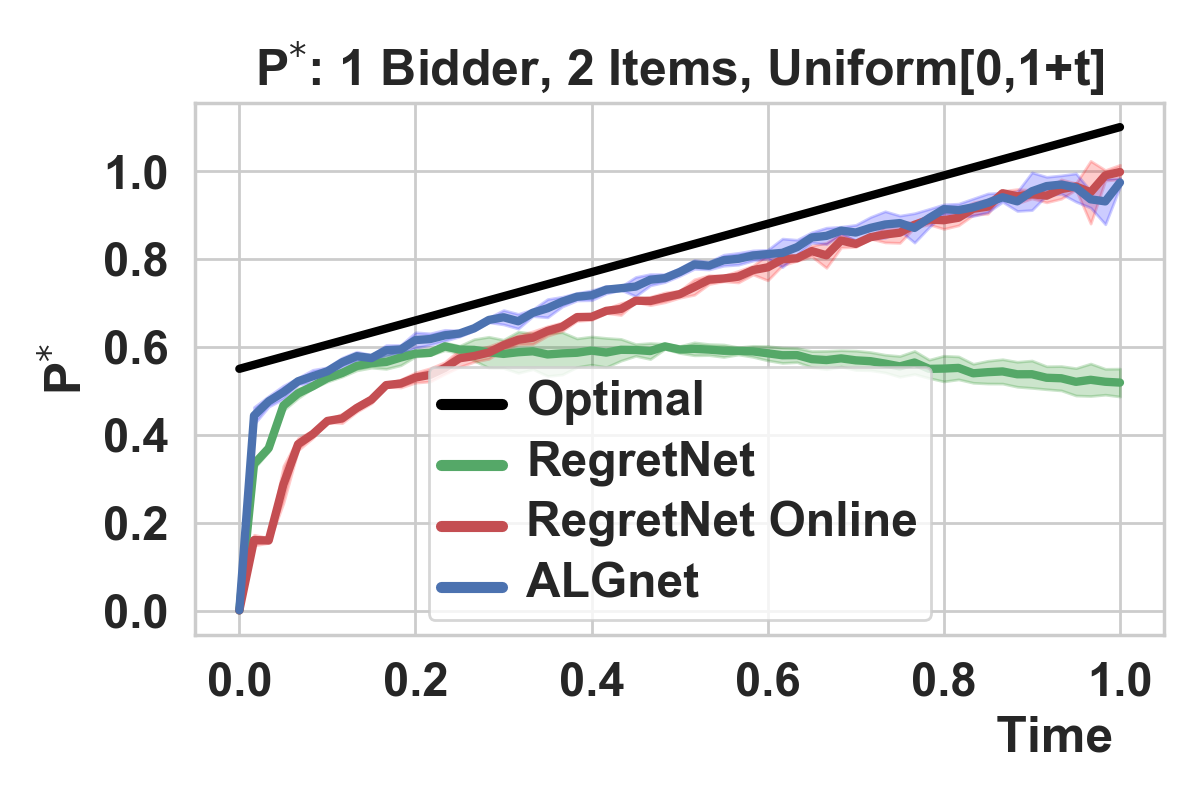

A recent line of work initiated by Duetting et al. (2019) leverages the expressivity and scalability of neural networks to go beyond the limitations of linear programs. Their idea is to parameterize the allocation and payment functions with deep neural networks and use gradient descent to learn an incentive compatible, individually rational auction mechanism that maximizes revenue. Their algorithm, RegretNet is capable of finding near-optimal results in several known settings and obtaining new mechanisms in unknown cases. While very successful, RegretNet suffers from two weakness. In practice, the algorithm is sample inefficient and hard to train.

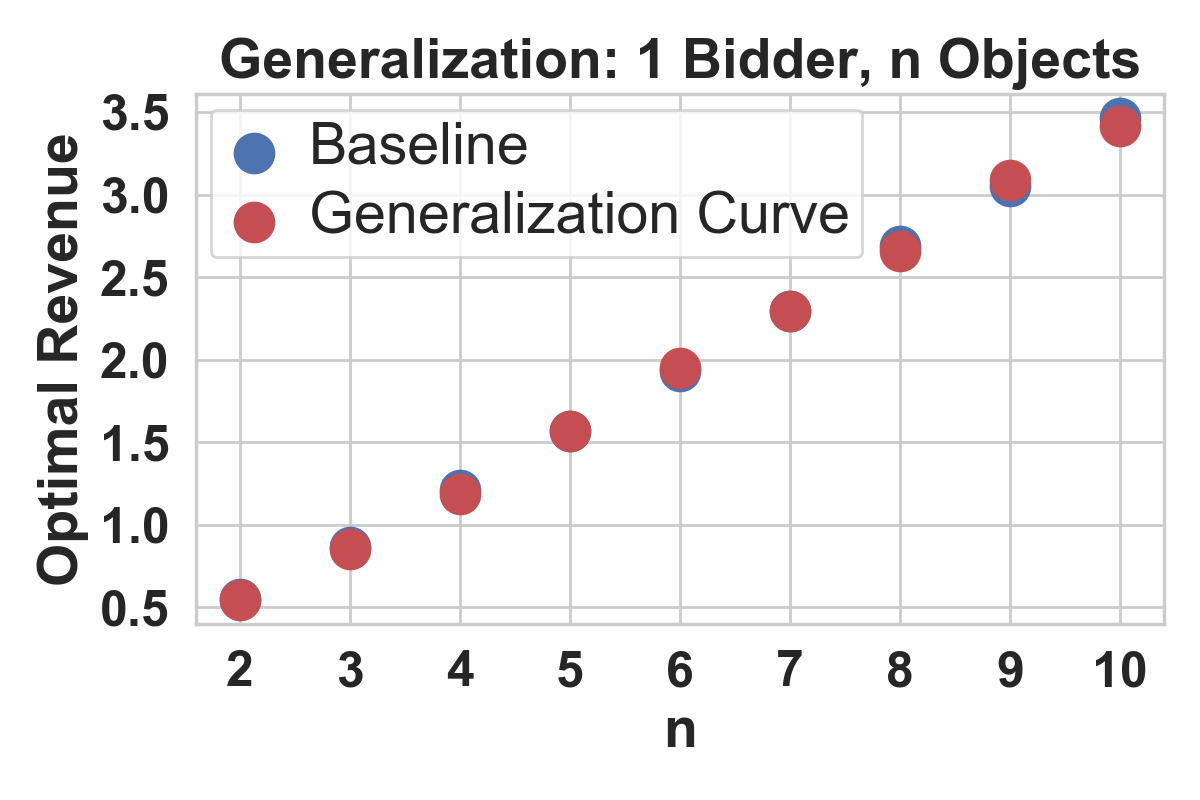

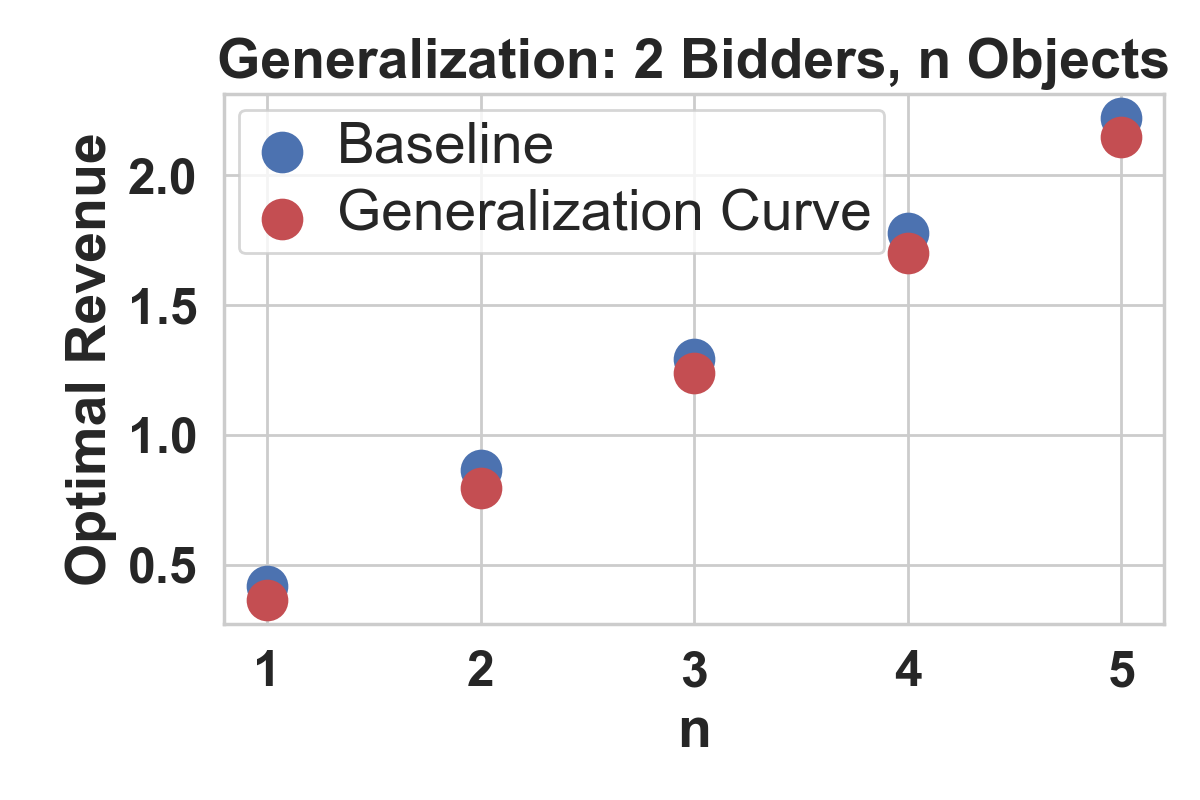

RegretNet can require a large number of samples to learn an optimal auction. Furthermore, it is incapable of generalizing to new auctions with a different number of bidders and items. An optimal mechanism learned by RegretNet for an auction consisting of bidders and items can only be used on auctions with bidders and items because the neural network expects inputs of a specific dimension. If an additional bidder were to join or leave the auction or a new item was added or removed, then we would have to build and train a new auction mechanism from scratch. In Chapter 4, we tackle these two issues in the case of symmetric auctions. These are auctions which are invariant to the relabeling of the items or bidders. More specifically, such auctions are anonymous (in that they can be executed without any information about the bidders, or labeling them) and item-symmetric (in that it only matters what bids are made for an item, and not its a priori label). We prove that these auctions always admit optimal allocation and payment functions that are equivariant and then proceed to build equivariant neural network architectures that respect this symmetry. Our algorithm, EquivariantNet, is more sample efficient than RegretNet and can also generalize to different auctions.

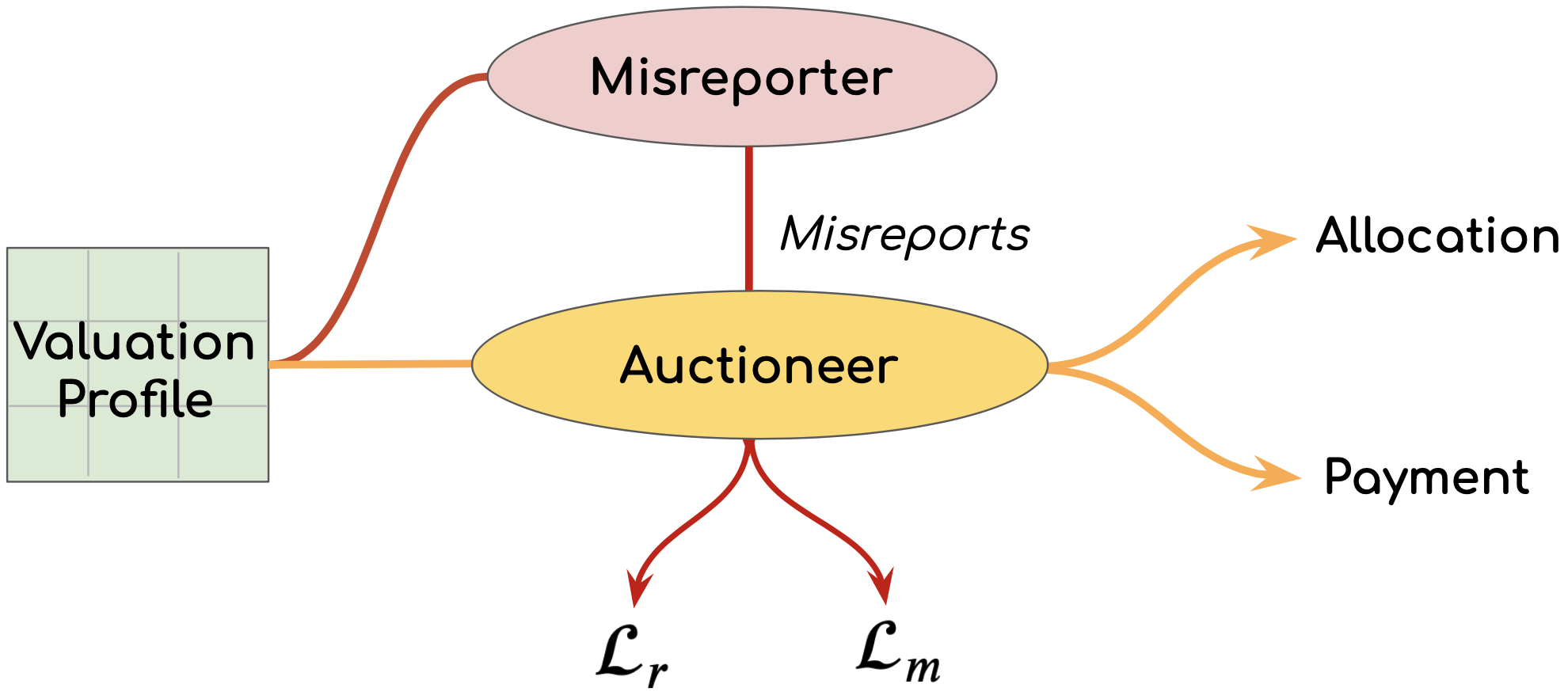

The loss function in RegretNet is non stationary. It depends on several hyperparameters whose values change over time according to a predefined schedule. This makes RegretNet hard to train in practice. We also observe experimentally that the algorithm is very sensitive to the choice of these hyperparameters, converging to a suboptimal mechanism when these are not picked appropriately. Furthermore, these hyperparameters are setting dependent, their values depend on the number of bidders and items in the auction, and are currently found through an expensive hyperpameter search. In Chapter 5, we construct a novel, stationary, and hyperparameter-free loss function inspired by recent theoretical results from Auction Theory and propose a novel formulation of the auction learning problem as a two player game. The first player, the Auctioneer, proposes new auction rules. The second player, the Misreporter, is trying to exploit these rules and find optimal ways to bid untruthfully. These two players interact and over time, the Misreporter becomes better at finding optimal bids and the Auctioneer becomes better at proposing auction mechanisms that increasingly get closer to being incentive compatible. We call this algorithm ALGNet and we show that it’s as good or better than RegretNet, while being nearly hyper-parameter free.

1.2 Summary of Contributions

The contributions of this dissertation are summarized below:

-

•

In Chapter 2, we propose a novel approach to the Reinforcement Learning problem. Inspired by Statistical Physics, we construct a partition function for each state of the environment and derive the corresponding Bellman equation. Our approach has three main benefits. First, it results in simpler equations, especially if the environment is deterministic. Second, it is able to treat all rewards equally over time (no need for a discount factor). Third, it learns policies that not only optimize for rewards but also take entropy into account, favoring states from which many good outcomes are possible.

Chapter 2 is based on the following work:

\bibentryrahme2019theoretical.

-

•

In Chapter 3, we study the generalization problem in Reinforcement Learning from a Bayesian perspective by modeling the uncertainty the agent has about the environment. We show how incomplete and imperfect knowledge of the environment implicitly turns a fully observed and Markovian environment (MDP) into a Partially Observed MDP (POMDP), which we call the Epistemic POMDP. This novel point of view allows us to derive a new RL algorithm, LEEP, with improved generalization properties.

Chapter 3 is based on the following work (* indicates equal contribution):

\bibentryrahme2021generalization.

-

•

In Chapter 4, we prove that symmetric auctions always admit optimal allocation and payment functions that are equivariant and then proceed to build an equivariant neural network architecture that respects this symmetry. We show that our algorithm, EquivariantNet, is not only more sample efficient than previous methods but can also generalize well to different auctions.

Chapter 4 is based on the following work:

\bibentryRahme_Jelassi_Bruna_Weinberg_2021.

-

•

In Chapter 5, we construct a novel, stationary, and hyperparameter-free loss function for the auction learning problem inspired by recent theoretical results from auction theory, and propose a novel formulation of the auction learning problem as a two player game (similar to GANs, (Goodfellow et al., 2014)). We show that the resulting algorithm ALGNet is as good or better than RegretNet, while being nearly hyper-parameter free.

Chapter 5 is based on the following work:

\bibentryalgnet.

The following two sections cover some background material on Reinforcement Learning and Auction Theory.

1.3 Background in Reinforcement Learning

In this section, we review the setup of the Reinforcement Learning problem as well as some of its basic concepts and approaches. A good reference on Reinforcement Learning can be found in Sutton and Barto (2018).

1.3.1 The RL Problem

RL as a Markov Decision Problem

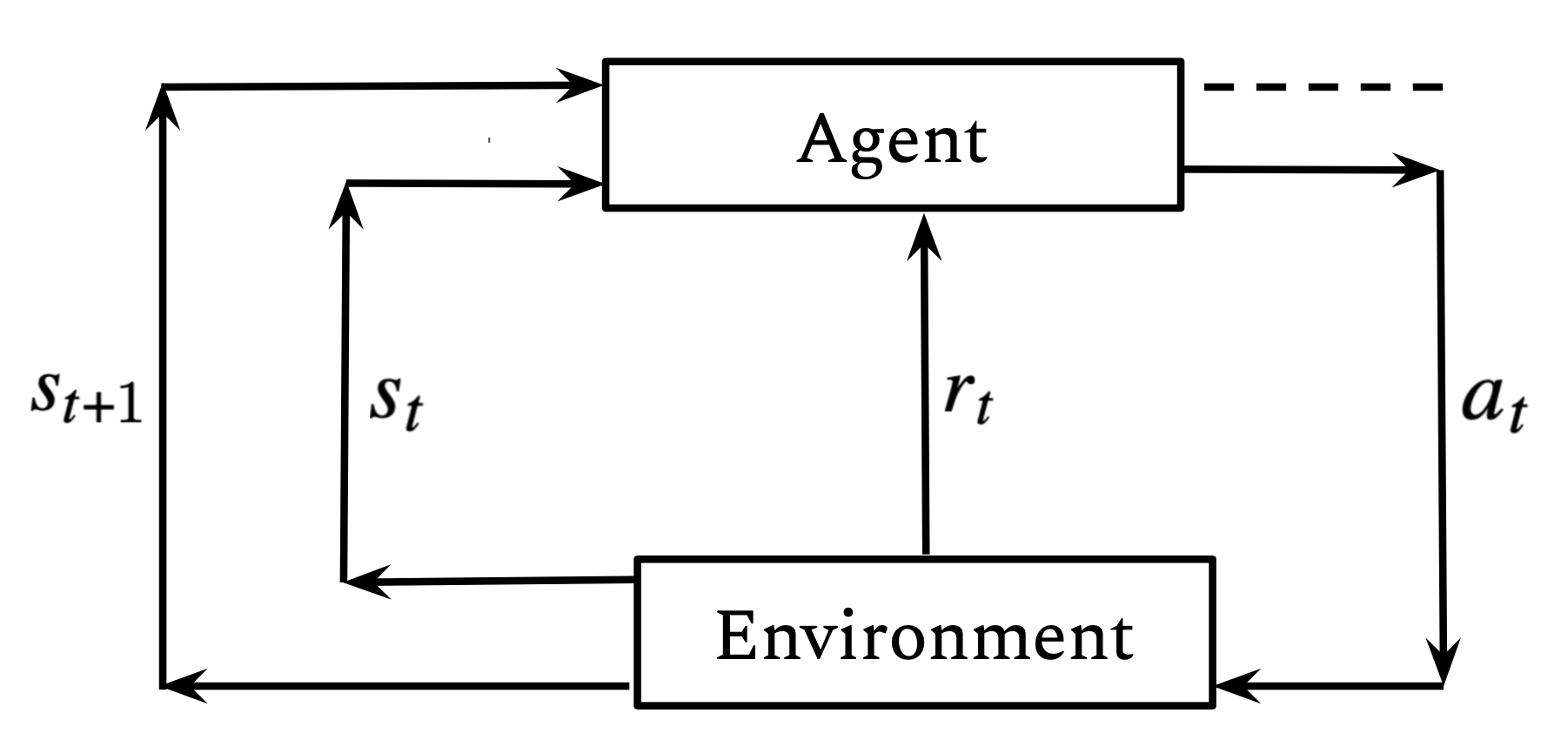

Reinforcement Learning (RL) is an area of Machine Learning (ML) that studies how agents should behave in an environment in order to maximize their cumulative reward. The agent’s sequential decision-making process is usually modeled as a Markov Decision Process (MDP).

At every time step , the agent observes the state of the environment, , and then decides what action to take, . This action has two effects - first, it changes the state of the environment from to and second, it rewards the agent with a reward . The state and the reward are random variables - the same causes don’t necessarily results in the same effects. In an MDP, the environment’s dynamics are allowed to be stochastic but they have to be Markovian. This means that the distribution of states that the agents lands in after taking action from state only depends on and , and not on past states or past actions . This also holds for the reward : its distribution is only a function of the initial state , the action taken , and the landing state .

More formally, an MDP is defined by the objects where:

-

•

is the set of states the environment can be in,

-

•

is the set of actions an agent can take,

-

•

is the probability of landing in state after taking action while still in state ,

-

•

is the reward resulting from the transition . is a random variable. We usually assume that all rewards are bounded from above by .

Deterministic MDPs: An MDP is deterministic if is for all states except one, which will be conveniently denoted by . In this case we have and we will concisely denote by . is also assumed to be deterministic.

Policies

In RL, the policy describes how the agent acts in the environment. denotes the probability that the agent picks action while in state . If we denote the reward resulting from the -th transition by , so that , we can express the cumulative reward of such a policy as:

| (1.1) |

where the expectations are taken with respect to the realized sequences of states and actions, according to the policy and environment dynamics. Here is called the discount factor that can be interpreted as a preference for immediate rewards over future ones. The discount factor is also necessary for mathematical reasons: without this discount factor, many quantities in RL are not well defined. For example, the infinite series determining could diverge.

The RL Objective

The goal of RL is to find an optimal policy that maximizes :

There are two main approaches to solving a RL problem: value function type approaches and policy gradient type approaches. In the following sections we will give a quick exposition of both of these approaches. These sections are not meant to be exhaustive or extensive by any measure, their goal is to give the reader some background that could help them contrast traditional approaches to RL with the novel approaches and methods that we propose in Chapters 2 and 3.

1.3.2 Value Function Approaches

Value functions associated with a policy

The value function associated with a policy is a function of the state that measures the expected cumulative reward an agent will get by following the policy starting from state :

The value functions at different states are connected by a recursion called the Bellman equation:

In the Bellman equation above, the expectation is taken with respect to a single action and a single state transition. Similar to , we can define another type of value function (the “Q-function”) which is a function of a state-action pair , now measuring expected cumulative reward from following the policy after taking action from state :

also follows a Bellman equation given by:

Optimal value functions

When the policy is optimal, , the Bellman equations for and are referred to as the optimal Bellman equations and are given by:

| (1.2) | ||||

These optimal Bellman equations are fixed point equations. The mapping underlying these fixed point equations is called the Bellman operator. One can show that when , these Bellman operators are contractions of norm . As a result, when the Bellman operator is known, one can converge to and by successive iterations of their Bellman operators starting from any initialization (via the Banach fixed-point theorem). The optimal policy can then be recovered from the optimal value function, as:

Finding the optimal value function through iteration of the Bellman operator is not always possible. In most settings, the dynamics of the MDP, , and the reward function, , are not fully known and as a result, it’s not possible to solve the RL problem through an exact fixed point iteration scheme. Furthermore, even when the dynamics of the environment are known, it is not always possible to proceed through fixed point iteration and this is especially true for MDPs with large state and actions spaces.

Exploration

When the dynamics of the environment ( and ) are unknown, the expectations in the Bellman equations cannot be computed exactly; they can only be estimated using samples collected through interactions with the environment.

The policy used by the agent to collect these samples and learn about the environment is called the exploration policy. Depending on the problem, some exploration policies can be better than others. Two of the most popular exploration policies are:

-

•

-greedy: Pick with probability , and any action uniformly at random with probability .

-

•

Boltzmann exploration of parameter : At state , pick action proportionally to .

Both of these exploration policies use current estimates of the -function. In the beginning, when the agent only had a few interactions with the environment, the estimate for the optimal -function is very uncertain, and typical values for and are chosen to be and respectively. This corresponds to taking actions uniformly at random. As the agent interacts more with the environment and collects more data, is decreased to and is increased to a large number. This reflects our confidence that the -function is becoming more accurate over time.

Some RL algorithms (e.g. -learning) only use the latest transition seen by the exploration policy to update the values and as a result don’t need to store past past transitions. Other algorithms (e.g. DQN) don’t limit themselves to the latest transition but also use previously seen transitions to update their current values. When that is the case, all the interactions with the environment are recorded and stored in a dataset called a Replay Buffer. A typical entry in the replay buffer takes the form a tuple , where is a Boolean entry that indicates whether the episode ended or is still ongoing.

-learning

The -learning algorithm is a popular value function based, RL learning algorithm first introduced in Watkins (1989). -learning does not assume that the dynamics of the environment are known - it’s a model-free algorithm.

The algorithm goes as follows: Initially, all values are initialized to arbitrary values (or randomly). Then, at each time step , the agent looks at the state of the environment, takes action , and observes the next state, , and the reward associated with the transition, . The algorithm then updates the value of the state-action pair according the following learning rule:

| (1.3) |

The parameter in this equation is called the learning rate and can be time-dependent. Intuitively, this update rule is trying to close the gap between the left hand side and the right hand side of the optimal Bellman equations for the -function (Equation 1.2). The -learning algorithm is summarized in Algorithm 1:

The -learning algorithm provably learns the optimal function under some reasonable assumptions:

-

•

The learning rate has to decrease to but not too fast ( should diverge and should converge).

-

•

Each state action pair must be visited an infinite number of times by the exploration policy.

A more technical statement of these assumptions and a proof of the convergence result can be found in Watkins and Dayan (1992).

-learning works well for MDPs with small state and action spaces but becomes intractable in larger ones. In the following section, we will see how to scale -learning to larger MDPs with the help of function approximations and deep learning.

Deep Networks (DQN)

In the previous section, the learning algorithm had to learn a table of values, one for each state-action pair . This is not possible for MDPs with a large state and action space, such as MDPs with continuous state spaces. This is where function approximations become useful.

The idea is to parameterize the function with a family of functions , typically a neural network, and then learn the optimal value of the parameter such that we have . Note that this problem is tractable because the dimensionality of the learning problem, , is independent of the size of the MDP. The optimal value of the parameter is learned by minimizing the Bellman error with (a variant of) gradient descent:

| (1.4) |

The expectation in is empirically estimated by sampling a batch of random transitions from the replay buffer. Optimizing is not as straightforward as it seems and many tricks are required to stabilize the learning algorithm. For instance, when computing the gradient of , the target is treated as a constant and does not contribute to the overall gradient. In fact, the target is computed using a “delayed” version of the parameter .

The details of the training procedure and the empirical tricks needed to stabilize the learning algorithm can be found in the original DQN paper (Mnih et al., 2013). Many additional improvements to the DQN algorithm were discovered since its initial publication and some of the major ones are reported in Hessel et al. (2018).

1.3.3 Policy Gradient Approaches

Instead of learning an optimal value function from which an optimal policy can be inferred, policy gradient approaches tackle the RL problem by learning the optimal policy directly. In the following we will parameterize the policy space by a family of functions .

REINFORCE

The RL objective (Equation 1.1) can be re-written more explicitly as an expectation over trajectories , as:

where is the total reward encountered by the trajectory , and:

is the probability of observing trajectory by following the policy . Using the log trick, , we can write as:

Since does not depend on , we have:

and finally we find a very simple estimate of :

| (1.5) |

This result was first derived by Williams (1992). Optimizing by following an empirical estimate of the gradient above (Equation 1.5) is known at the REINFORCE algorithm.

Beyond REINFORCE

The gradient estimates in REINFORCE are usually very noisy as they suffer from high variance which can destabilize the learning process. The algorithm can be made more reliable through the usage of variance reduction schemes. These usually involve introducing value function estimates inside the REINFORCE formula. For instance, further analysis of Equation 1.5 shows that it can be re-written as:

where is the function of policy and is the state marginal distribution resulting from following the policy . This expression could be further re-written as:

| (1.6) |

where is called the advantage function. The advantage function measures how good an action is at a given state. A positive (negative) advantage indicates that the action is better (worse) than average. Using Equation 1.6 to estimate gradients leads to less noisy estimates and results in a more stable and improved policy learning algorithm. Further details on how to estimate as well as a technical analysis of variance reduction schemes in policy gradient methods can be found in Schulman et al. (2015b) and Greensmith et al. (2004).

REINFORCE minimizes the RL objective by taking a step in the direction of the gradient . While this can provably improve the policy in the limit of small step sizes, it is not necessarily the best direction to follow. Indeed, the gradient points towards the direction of steepest ascent when distances are measured using the Euclidean distance in the parameter space, . Without any additional assumptions on the mapping , measuring distances in the parameter space might not be appropriate. Small differences in the parameter could lead to large differences in the policy space and as a result, in the agent’s performance. Conversely, large changes in could correspond to infinitesimal policy changes and imperceptible changes of the agent’s behavior.

Consequently, it seems more appropriate to measure distances at the policy level instead of the underlying parameter’s level. This results in a different gradient called the natural gradient and a different policy gradient algorithm called the Natural Policy Gradient (NPG) (Kakade, 2001). Many policy gradient methods were then developed following up and improving on that line of work, including Trust Region Policy Optimization (TRPO) by Schulman et al. (2015a), Proximal Policy Optimization (PPO) by Schulman et al. (2017), and Actor-Critic using Kronecker-factored Trust Region (ACKTR) by Wu et al. (2017).

1.4 Background in Auction Theory

In this section, we give a brief high level introduction to auction theory that gives more context for Chapters 4 and 5. A good reference on auction theory and mechanism design more generally can be found in Nisan et al. (2007) or Roughgarden (2016).

1.4.1 A Simple Model For Auctions

Setting

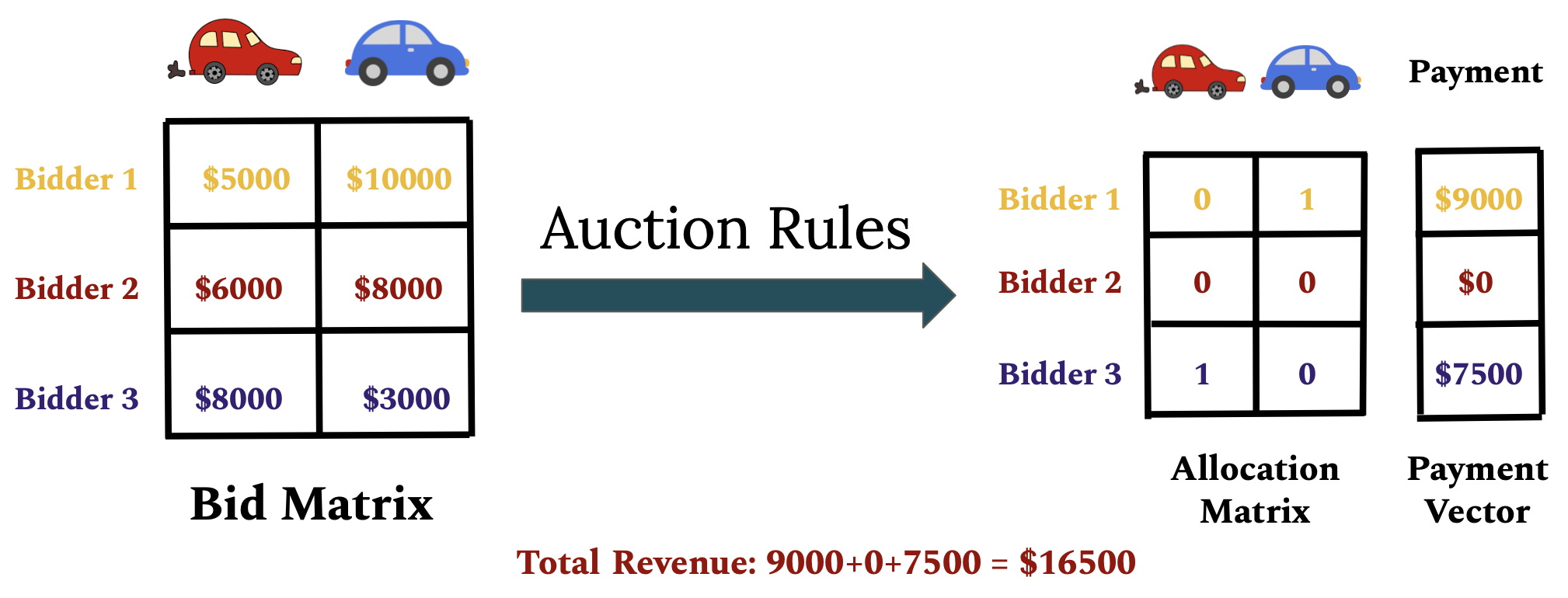

An auction consists of bidders and items. Let and denote the set of bidders and items respectively. At the start of the auction, each one of the bidders bids a sum of money on each one of the items. We will denote the bid of bidder on item by . These bids can be grouped into a matrix called the bid matrix.

The allocation and payment functions

An auction mechanism is characterized by two functions, the allocation function and the payment function , both of which have the bid matrix as an input.

The allocation function computes the allocation matrix where is the probability that bidder gets item . Since it’s possible for an item to not be allocated to any of the bidders, we have . It is sometimes convenient to denote the allocation function restricted to bidder , by by , i.e. .

The payment function computes the payment vector where is the amount of money bidder has to pay to the Auctioneer. The revenue of the Auctioneer is the sum of the payments made by all the bidders, .

Additive auctions

A subset of items does not have the same value for each one of the bidders. Each bidder has his own valuation function, , where denotes how much bidder values the subset of items . In principle can be arbitrary, assigning arbitrary values to each one of the possible subsets.

Depending on the context, it makes sense to consider simpler valuation functions that have more structure to them. For example, we could consider valuation functions in which the value of a basket of items is equal to the highest individual item value in that basket: . This is called a unit-demand valuation function. Other examples are value functions in which the value of a basket of items is equal to the sum of the values of its components: . Such valuations are called additive. Additive valuations are among the most studied valuation functions in auction theory and will be the main focus of this thesis.

An additive valuation function is fully specified by the individual values for each one of the items. In the following, we denote the value that bidder gives for item by . These values can be grouped into a matrix called the valuation matrix. Note that in general, the bid matrix can be different than the value matrix. In the following we will denote the -th row of the value matrix by .

The utility of a bidder

The utility of a bidder is the net amount of value obtained as a result of his participation in the auction. We can compute it as the difference between the total value of the items that the bidder got and the amount he had to pay to the auctioneer. The utility of bidder , , is given by :

Notice that the total value received by bidder in this expression is computed using the valuation function of bidder . For additive auction, this expression can be re-written as:

| (1.7) |

1.4.2 Problem Statement

While there exist infinite choices of allocation functions and payment functions that constitute a valid auction mechanism, in practice, we care about auctions that satisfy certain desirable properties. In the following we will focus on two desirable properties, incentive compatibility and individual rationality.

Notation: Given a matrix and we will denote the -th row of the matrix by and the matrix that one gets from by removing -th row by . Given a vector , we will denote the matrix that we get by replacing row with in by . The rows of are .

If is a bid matrix, then is the vector of bids of bidder , is the bid matrix of all the bidders except bidder , and is a bid matrix that we get if bidder modifies his bid from to .

Incentive Compatibility

Strategic bidders seek to maximize their utility and may report bids that are different from their true valuations (). In hindsight, once all the bids are known, the optimal bid of bidder , , is given by:

In general, we should expect that is different from . In some auctions however, the utility of a bidder is always maximized when his bid is truthful regardless of the other bids and we have . These auctions are called dominant strategy incentive compatible auctions (DSIC). The following provides a formal definition.

Definition 1.

An auction is dominant strategy incentive compatible (DSIC) if each bidder’s utility is maximized by reporting truthfully no matter what the other bidders report. For every bidder valuation , bid and bids , we have:

DSIC is a desirable property because it levels the playing field to all the bidders. It not only makes it easier for bidders to bid optimally (by bidding truthfully), but also makes it easier for the auctioneer to predict the outcome of an auction since the optimal bids are easily characterized. DSIC auctions are sometimes called strategy-proof auctions.

Individual Rationality

The payment function in an auction can, in principle, charge a positive amount of money to a bidder who has not been allocated any of the items. It can also charge a bidder more than the total value of the items he got from the auction. In both of these cases, the utility of the bidder is negative, which means that the bidder is worse off after participating in the auction. An individually rational auction guarantees that such cases cannot happen to a bidder as long as he’s bidding truthfully. A truthful bidder always has a non negative utility function regardless of what the other bidders decide to do. The following provides a formal definition.

Definition 2.

An auction is individually rational (IR) if for all , and we have:

| (1.8) |

Individually rational auctions are desirable because they encourage bidder participation in the auction.

The auction learning problem

Each bidder knows how much each item is worth to them. This information is not known to the other bidders nor to the auctioneer. This setting is referred to as a private value auction. However, a common assumption is that each bidder draws their value vector, , from some prior probability distribution, , which is common knowledge.

The goal of the auctioneer is to design an incentive compatible, individually rational auction that maximizes his expected revenue given a prior on the bidder’s value vectors .

Formally, we can rewrite the problem as:

1.4.3 Optimal Single Item Auction

This section is intended to give the curious reader a peek into one of the most celebrated results in auction theory. While reading this section is not strictly necessary to understand the work presented in this thesis, it could be interesting to contrast the analytical approach to finding the optimal auction presented in this section with the machine learning based approaches of Chapters 4 and 5.

Finding the optimal single item auction was fully resolved by Myerson in his seminal 1981 paper (Myerson, 1981). In this section, we include a high level derivation of Myerson’s result that makes some simplifying assumptions. A complete and technical derivation can be found in Myerson’s original paper (Myerson, 1981).

The allocation function is monotonic.

Our goal in this section is to prove that the optimal allocation function is monotonic non-decreasing with respect to the bids of each one of the bidders:

We remind the reader that since we’re in a single item setting, is a real number that we conveniently represent by . Intuitively this result makes sense. A bidder can expect to increase the probability of getting the item by increasing his bid, assuming that all the other bids remain constant. We will see that this result follows naturally from the DSIC property.

Notation: In the following, we will fix a bidder and the bids of all the other bidders . This allows us to adopt the following convenient notations: , and . With these simplifying notations, our goal is to prove that the function is monotonic non decreasing.

For a DSIC auction, we have for all and . Through simple manipulations we can re-write this inequality as:

By permuting the roles of and , we also get that . We conclude that:

| (1.9) |

This inequality implies that which proves that the function is monotonic non decreasing as claimed.

A relation between the allocation and payment functions

In this section, we derive a relation between the allocation function and payment function for a truthful mechanism. For the sake of simplicity, we will make the assumption that the function is differentiable. While this assumption simplifies the proof, it is not a necessary one. Only the monotonicity of is required in the more general proof (Myerson, 1981).

Taking , we can rewrite equation 1.9 as:

| (1.10) |

In the limit of , we find that:

| (1.11) |

For an individually rational auction, we have and we get:

| (1.12) |

Going back to our original (non simplified) notation, we can rewrite this equation as:

| (1.13) |

Equation 1.13 shows that given an allocation function there is at most one candidate payment function such that the mechanism defined by is incentive compatible and individually rational. Conversely, one can prove that given a monotonic non decreasing allocation function , the mechanism defined by where is given by equation 1.13 is DSIC and IR.

Deriving the optimal allocation function

Now that we have the characterization of the space of incentive compatible individually rational auctions, we move on to finding the revenue maximizing auction.

Let’s denote by the probability distributions from which the bidders’ value is sampled: . Since we’re in a single-item setting, the distribution is a probability distribution over the real numbers. To simplify the derivation, we will assume that all values are bounded by and that has a continuous probability density function which we’ll denote as . We will use to denote the corresponding cumulative distribution function.

Conditioned on , the expected payment of bidder , , is given by:

| (1.14) | ||||

where in the last equality we used the characterization of the payment function in terms of the allocation function as found in equation 1.13. This expression can be further simplified by first permuting the order of integration and then by integrating by parts:

The quantity that appears under the integral is called the virtual valuation of bidder . Note that this quantity only depends on bidder , it does not depend on any of the other bidders, and it can be negative.

The total expected revenue for the auctioneer is then given by:

| (1.15) |

From equation 1.15 we can see that the expected revenue is a linear combination of the virtual values.

If all these virtual values are negative, then the optimal allocation is for all bidders. Otherwise, optimality is reached by allocating the item to the bidder with the highest virtual value. The optimal payment function can then be inferred using equation 1.13.

An example

To illustrate how that works in practice, let’s consider the case where . The virtual valuation function is then given by .

If all the bids are smaller than , then all the virtual bids are negative and the item is not allocated, so none of the bidders have to pay any amount of money to the auctioneer. is called the reserve price, which is the value under which the auctioneer is not willing to sell his item.

If this is not the case, then there is at least one bidder that bid more than . Without loss of generality we can assume that bidder has the highest bid and bidder has the second highest bid. In this case, bidder gets the item. The allocation function of bidder is given by:

Its derivative is given by where is the Dirac function. By plugging this expression into equation 1.13, we find that bidder has to pay to the auctioneer. The optimal auction can be summed up by the following two cases:

This is called a second price auction with a reserve price.

Generalizing these results to larger auctions is not straightforward. In fact, despite decades of research, there is no known analytical derivation that would enable us to systematically derive optimal mechanism for a general auction. In Chapter 4 and 5 we will see a machine learning based approach to approximate optimal auctions.

Part I Reinforcement Learning

Chapter 2 A Theoretical Connection Between Statistical Physics and Reinforcement Learning

2.1 Abstract

Sequential decision making in the presence of uncertainty and stochastic dynamics gives rise to distributions over state/action trajectories in reinforcement learning (RL) and optimal control problems. This observation has led to a variety of connections between RL and inference in probabilistic graphical models (PGMs). Here we explore a different dimension to this relationship, examining reinforcement learning using the tools and abstractions of statistical physics. The central object in the statistical physics abstraction is the idea of a partition function , and here we construct a partition function from the ensemble of possible trajectories that an agent might take in a Markov decision process. Although value functions and -functions can be derived from this partition function and interpreted via average energies, the -function provides an object with its own Bellman equation that can form the basis of alternative dynamic programming approaches. Moreover, when the MDP dynamics are deterministic, the Bellman equation for is linear, allowing direct solutions that are unavailable for the nonlinear equations associated with traditional value functions. The policies learned via these -based Bellman updates are tightly linked to Boltzmann-like policy parameterizations. In addition to sampling actions proportionally to the exponential of the expected cumulative reward as Boltzmann policies would, these policies take entropy into account favoring states from which many outcomes are possible.

2.2 Introduction

One of the central challenges in the pursuit of machine intelligence is robust sequential decision making. In a stochastic and uncertain environment, an agent must capture information about the distribution over ways they may act and move through the state space. Indeed, the algorithmic process of planning and learning itself can lead to a well-defined distribution over state/action trajectories. This observation has led to a variety of connections between reinforcement learning (RL) and inference in probabilistic graphical models (PGMs) (Levine, 2018). In some ways this connection is unsurprising: belief propagation (and its relatives such as the sum-product algorithm) is understood to be an example of dynamic programming (Koller and Friedman, 2009) and dynamic programming was developed to solve control problems (Bellman, 1966; Bertsekas, 1995). Nevertheless, the exploration of the connection between control and inference has yielded fruitful insights into sequential decision making algorithms (Kalman, 1960; Attias, 2003; Ziebart, 2010; Kappen, 2011; Levine, 2018).

In this chapter, we present another point of view on reinforcement learning as a distribution over trajectories, one in which we draw upon useful abstractions from statistical physics. This view is in some ways a natural continuation of the agenda of connecting control to inference, as many insights in probabilistic graphical models have deep connections to, e.g., spin glass systems (Hopfield, 1982; Yedidia et al., 2001; Zdeborová and Krzakala, 2016). More generally, physics has often been a source of inspiration for ideas in machine learning (MacKay, 2003; Mezard and Montanari, 2009). Boltzmann machines (Ackley et al., 1985), Hamiltonian Monte Carlo (Duane et al., 1987; Neal et al., 2011; Betancourt, 2017) and, more recently, tensor networks (Stoudenmire and Schwab, 2016) are a few examples. In addition to direct inspiration, physics provides a compelling framework to reason about certain problems. The terms momentum, energy, entropy, and phase transition are ubiquitous in machine learning. However, abstractions from physics have generally not been so far helpful for understanding reinforcement learning models and algorithms. That is not to say there is a lack of interaction; RL is being used in some experimental physics domains, but physics has not yet as directly informed RL as it has, e.g., graphical models (Carleo et al., 2019).

Nevertheless, we should expect deep connections between reinforcement learning and physics: an RL agent is trying to find a policy that maximizes expected reward and many natural phenomena can be viewed through a minimization principle. For example, in classical mechanics or electrodynamics, a mass or light will follow a path that minimizes a physical quantity called the action, a property known as the principle of least action. Similarly, in thermodynamics, a system with many degrees a freedom—such as a gas—will explore its configuration space in the search for a configuration that minimizes its free energy. In reinforcement learning, rewards and value functions have a very similar flavor to energies, as they are extensive quantities and the agent is trying to find a path that maximizes them. In RL, however, value functions are often treated as the central object of study. This stands in contrast to statistical physics formulations of such problems in which the partition function is the primary abstraction, from which all the relevant thermodynamic quantities—average energy, entropy, heat capacity—can be derived. It is natural to ask, then, is there a theoretical framework for reinforcement learning that is centered on a partition function, in which value functions can be interpreted via average energies?

In this chapter, we show how to construct a partition function for a reinforcement learning problem. In a deterministic environment (Section 2.3), the construction is elementary and very natural. We explicitly identify the link between the underlying average energies associated with these partition functions and value functions of Boltzmann-like stochastic policies. As in the inference-based view on RL, moving from deterministic to stochastic environments introduces complications. In Section 2.4.2, we propose a construction for stochastic environments that results in realistic policies. Finally, in Section 2.5, we show how the partition function approach leads to an alternative model-free reinforcement learning algorithm that does not explicitly represent value functions.

We model the agent’s sequential decision-making task as a Markov decision process (MDP), as is typical. The agent selects actions in order to maximize its cumulative expected reward until a final state is reached. The MDP is defined by the objects . and are the sets of states and actions, respectively. is the probability of landing in state after taking action from state . is the reward resulting from this transition. We also make the following additional assumptions:

-

1.

is finite,

-

2.

all rewards are bounded from above by and are deterministic,

-

3.

the number of available actions is uniformly bounded over all states by .

We also allow for terminal states to have rewards even though there are no further actions and transitions. We denote these final-state rewards by . By shifting all rewards by we can assume without loss of generality that making all transition rewards non positive. The final state rewards are still allowed to be positive however.

2.3 Partition Functions for Deterministic MDPs

Our starting point is to consider deterministic Markov decision processes. Deterministic MDPs are those in which the transition probability distributions assign all their mass to one state. Deterministic MDPs are a widely studied special case (Madani, 2002; Wen and Van Roy, 2013; Dekel and Hazan, 2013) and they are realistic for many practical control problems, such as robotic manipulation and locomotion, drone maneuver or machine-controlled scientific experimentation. For the deterministic setting, we will use to denote the state that follows the taking of action in state . Similarly, we will denote the reward more concisely as .

2.3.1 Construction of State-Dependent Partition Functions

To construct a partition function, two ingredients are needed: a statistical ensemble, and an energy function on that ensemble. We will construct our ensembles from trajectories through the MDP; a trajectory is a sequence of tuples such that state is a terminal state. We use the notation , , and to indicate the state, action, and reward, respectively, of trajectory at step . Each state-dependent ensemble is then the set of all trajectories that start at , i.e., for which . We will use these ensembles to construct a partition function for each state . Taking to be the length of the trajectory, we write the energy function as

| (2.1) |

The form on the right takes a notational shortcut of defining for the reward of the terminal state. Since the agent is trying to maximize their cumulative reward, is a reasonable measure of the agent’s preference for a trajectory in the sense that lower energy solutions accumulate higher rewards. Note in particular that the ground state configurations are the most rewarding trajectories for the agent. With the ingredients and defined, we get the following partition function

| (2.2) | ||||

| (2.3) |

In this expression, is a hyper-parameter that can be interpreted as the inverse of a temperature. (This interpretation comes from statistical physics where , where is the Boltzmann constant.) This partition function does not distinguish between two trajectories having identical cumulative rewards but different lengths. However, among equivalently rewarding trajectories, it seems natural to prefer shorter trajectories. One way to encode this preference is to add an explicit penalty on the length of a trajectory, leading to a partition function

| (2.4) |

In statistical physics, is called a chemical potential and it measures the tendency of a system (such as a gas) to accept new particles. It is sometimes inconvenient to reason about systems with a fixed number of particles, adding a chemical potential offers a way to relax that constraint, allowing a system to have a varying number of particles while keeping the average fixed.

Note that since MDPs can allow for both infinitely long trajectories and infinite sets of finite trajectories, can be infinite even in relatively simple settings. In Appendix 2.A.1, we find that a sufficient condition for to be well defined is taking . As written, the partition function in Eq. 2.4 is ambiguous for final states. For clarity we define for a terminal state . We will refer to these as the boundary conditions.

Mathematically, the parameter has a similar role as the one played by , the discount rate commonly used in reinforcement learning problems. They both make infinite series convergent in an infinite horizon setting, and ensure that the Bellman operators are contractions in their respective frameworks (Appendices 2.A.3 and 2.B.3). However, when using , the order in which the rewards are observed can have an impact on the learned policy which does not happen when is used. This could be a desirable property for some problems as it uncouples rewards from preferences for shorter paths.

2.3.2 A Bellman Equation for

As we have defined an ensemble for each state , there is a partition function defined for each state. These partition functions are all related through a Bellman-like recursion:

| (2.5) |

where, as before, indicates the state deterministically following from taking action in state . This Bellman equation can be easily derived by decomposing each trajectory into two parts: the first transition resulting from taking initial action and the remainder of the trajectory which is a member of . The total energy and length can also be decomposed in the same way, so that:

Note in particular that this Bellman recursion is linear in .

2.3.3 The Underlying Value Function and Policy

The partition function can be used to compute an average energy to shed light on the behavior of the system. This average is computed under the Boltzmann (Gibbs) distribution induced by the energy on the ensemble of trajectories :

| (2.6) |

In probabilistic machine learning, this is usually how one sees the partition function: as the normalizer for an energy-based learning model or an undirected graphical model (see, e.g., Murray and Ghahramani (2004)). Under this probability distribution, high-reward trajectories are the most likely but sub-optimal ones could still be sampled. This approach is closely related to the soft-optimality approach to RL (Levine, 2018). This distribution over trajectories allows us to compute an average energy for state either as an explicit expectation or as the partial derivative of the log partition function with respect to the inverse temperature:

| (2.7) |

The negative of the average energy is the value function:

This is an intuitive result: recall that the energy is low when the trajectory accumulates greater rewards, so lower average energy indicates that the expected cumulative reward—the value—is greater. Since the partition functions are connected by a Bellman equation, we expect that the underlying value functions would be connected in a similar way, and there is indeed a non-linear Bellman recursion:

The derivative rule for natural log gives us:

and as a result we have:

| (2.8) |

Note that the quantities inside the summation of Equation 2.8 are positive and sum to due to the Bellman recursion for from Equation 2.5. Thus we can view this Bellman equation for as an expectation under a distribution on actions, i.e., a policy:

| (2.9) | |||

| (2.10) |

The policy resembles a Boltzmann policy but strictly speaking it is not. A Boltzmann policy selects actions proportionally to the exponential of their expected cumulative reward:

In particular, does not take entropy into account: if two actions have the same expected optimal value, they will be picked with equal probability regardless of the possibility that one of them could achieve this optimality in a larger number of ways. In the partition function view, does take entropy into account and to clarify this difference we will look at the two extreme cases .

When , where the temperature of the system is infinite, rewards become irrelevant and we find that: . This means that is picking action proportionally to the number of trajectories that begin with . Here the counting of trajectories happens in a weighted way: longer trajectories contribute less than shorter ones. This is different from a Boltzmann policy that would pick actions uniformly at random.

sn edges[ [[ ][ ]][[ ]][[ ]]]

When , the low-temperature limit, we find in Section 2.A.2 that:

where is a weighted count of the number of optimal trajectories that begin at the state . Boltzmann policies completely ignore the entropic factor.

To illustrate this difference more clearly, we consider the deterministic decision tree MDP shown in Figure 2.1 where is the initial state and the leafs , , , and are the final states. The arrows represent the actions available at each state. There are no rewards and the boundary conditions are: and . This gives us the boundary condition:

Computing the -functions at the intermediate states and we find:

Finally we have . The underlying policy for picking the first action is given by:

| (2.11) |

When , we get:

.

A Boltzmann policy would pick these three actions with equal probability. The policy is biased towards the heavier subtree.

When we get:

A Boltzmann policy would pick action and with a probability of . prefers states from which many possible optimal trajectories are possible.

2.3.4 A Planning Algorithm

When the dynamics of the environment are known, it is possible to to learn by exploiting the Bellman equation (2.5). We denote by the property that there exists an action that takes an agent from state to state . The reward associated with this transition will be denoted . Let be the vector of all partition functions and be the matrix:

| (2.12) |

is a matrix representation of the Bellman operator in Equation 2.5. With these notations, the Bellman equations in (2.5) can be compactly written as:

| (2.13) |

highlighting the fact that is a fixed point of the map:

| (2.14) |

In Appendix 2.A.3, we show that is a contraction which makes it possible to learn by starting with an initial vector having compatible boundary conditions and successively iterating the map : . We could also interpret as an eigenvector of . In this context, this algorithm is simply doing a power method.

Interestingly, we can learn by solving the underdetermined linear system with the right boundary conditions. We show in Appendix 2.A.2 that the policies learned are related to Boltzmann policies which produce non linear Bellman equations at the value function level:

| (2.15) |

where is the discount factor and is a normalization constant different from .

By working with partition functions we transformed a non linear problem into a linear one. This remarkable result is reminiscent of linearly solvable MDPs (Todorov, 2007).

Once is learned the agent’s policy is given by: .

2.4 Partition functions for Stochastic MDPs

We now move to the more general MDP setting. The dynamics of the environment can now be stochastic. However, as mentioned at the end of the introduction, we still assume that given an initial state , an action , and a landing state , the reward is deterministic.

2.4.1 A First Attempt: Averaging the Bellman Equation

A first approach to incorporating the stochasticity of the environment is to average the right-hand side of the Bellman Equation 2.5 and define as the solution of:

| (2.16) | ||||

Interestingly, the solution of this equation can be constructed in the same spirit of Section 2.3.1 by summing a functional over the set of trajectories. If we define to be the log likelihood of a trajectory: then is defined by

| (2.17) |

satisfies the Bellman Equation 2.16. The proof can be found in Appendix 2.B.1. In Appendix 2.B.2 we derive the Bellman equation satisfied by the underlying value function and we find:

| (2.18) |

This Bellman equation does not correspond to a realistic policy; the policy depends on the landing state which is a random variable. The agent’s policy and the environment’s transitions cannot be decoupled. This is not surprising, from Equation 2.17 we see that puts rewards and transition probabilities on an equal footing. As a result an agent believes they can choose any available transition as long as they are willing to pay the price in log probability. This encourages risky behavior: the agent is encouraged to bet on highly unlikely but beneficial transitions. These observations were also noted in Levine (2018).

2.4.2 A Variational Approach

Constructing a partition function for a stochastic MDP is not straightforward because there are two types of randomness: the first comes from the agent’s policy and the second from stochasticity of the environment. Mixing these two sources of randomness can lead to unrealistic policies as we saw in Section 2.4.1. A more principled approach is needed.

We construct a new deterministic MDP from . We take to be the space of probability distributions over , similar to belief state representations for partially-observable MDPs (Astrom, 1965; Sondik, 1978; Kaelbling et al., 1998). We make the assumption that the actions are the same for all states and take . For and we define where is the transition matrix corresponding to choosing action in the original MDP. We define .

being finite, it has a finite number of final states which we denote . The final states of are of the form where verify and is a Dirac delta function at state . The intrinsic value of such a final state is then given by . This leads to the boundary conditions:

| (2.19) | ||||

This new MDP is deterministic, and we can follow the same approach of Section 2.3 and construct a partition function on . can be recovered by evaluating . From this construction we also get that satisfies the following Bellman equation:

| (2.20) |

Just as it is the case for deterministic MDPs, the Bellman operator associated with this equation is a contraction. This is proved in Appendix 2.B.3. However is now infinite which makes solving Equation 2.20 intractable. We adopt a variational approach which consists in finding the best approximation of within a parametric family . We measure the fitness of a candidate through the following loss function:

.

For illustration purposes, and inspired by the form of the boundary conditions (Equation 2.19), we consider a simple parametric family given by the partition functions of the form , where . The optimal can be found using usual optimization techniques such as gradient descent. By evaluation of at we see that we must have and consequently we have . The optimal solution satisfies the following Bellman equation:

| (2.21) |

The underlying value function verifies:

where the policy is given by . This approach leads to a realistic policy as its only dependency is on the current state, not a future one, unlike the policies arising from Equation 2.18.

2.5 The Model-Free Case

2.5.1 Construction of State-Action-Dependent Partition Function

In a model free setting, where the transition dynamics are unknown, state-only value functions such as are less useful than state-action value functions such as . Consequently, we will extend our construction to state-action partition functions . For a deterministic environment, we extend the construction in Section 2.3 and define by

| (2.22) | ||||

| (2.23) |

where denotes the set of trajectories having . Since , we have . As a consequence of this construction, satisfies the following linear Bellman equation:

| (2.24) |

This Bellman equation can be easily derived by decomposing each trajectory into two parts: the first transition resulting from taking initial action and the remainder of the trajectory which is a member of for some action . The total energy and length can also be decomposed in the same way, so that:

In the same spirit of Section 2.3.3, one can show that the average underlying value function satisfies a Bellman equation:

| (2.25) | |||

| (2.26) |

can be then reinterpreted as the -function of the policy . Similarly to the results of Section 2.3.3 and Appendix 2.A.2, the policy can be thought of a Boltzmann policy of parameter that takes entropy into account.

This construction can be extend to a stochastic environments by following the same approach used in Section 2.4.2.

In the following we show how learning the state-action partition function leads to an alternative approach to model-free reinforcement learning that does not explicitly represent value functions.

2.5.2 A Learning Algorithm

In -Learning, the update rule typically consists of a linear interpolation between the current value estimate and the one arising a posteriori:

| (2.27) |

where is the learning rate and is the discount factor. For -functions we will replace the linear interpolation with a geometric one. We take the update rule for -functions to be the following:

| (2.28) |

To understand what this update rule is doing, it is insightful to look at how how the underlying -function, is updated. We find:

| (2.29) |

We see that we recover a weighted version of the SARSA update rule. This update rule is referred to as expected SARSA. Expected SARSA is known to reduce the variance in the updates by exploiting knowledge about stochasticity in the behavior policy and hence is considered an improvement over vanilla SARSA (Van Seijen et al., 2009).

Since the underlying update rule is equivalent to the expected SARSA update rule, we can use any exploration strategy that works for expected SARSA. One exploration strategy could be -greedy which consists in taking action with probability and picking an action uniformly at random with probability . Another possibility would be a Boltzmann-like exploration which consists in taking action with probability .

We would like to emphasize that even though the expected SARSA update is not novel, the learned policies through this updates rule are proper to the partition-function approach. In particular, the learned policies are Boltzmann-like policies with some entropic preference properties as described in Section 2.3.3 and Appendix 2.A.2.

2.6 Conclusion

In this chapter we discussed how planning and reinforcement learning problems can be approached through the tools and abstractions of statistical physics. We started by constructing partition functions for each state of a deterministic MDP and then showed how to extend that definition to the more general stochastic MDP setting through a variational approach. Interestingly, these partition functions have their own Bellman equation making it possible to solve planning and model-free RL problems without explicit reference to value functions. Nevertheless, conventional value functions can be derived from our partition function and interpreted via average energies. Computing the implied value functions can also shed some light on the policies arising from these algorithms. We found that the learned policies are closely related to Boltzmann policies with the additional interesting feature that they take entropy into consideration by favoring states from which many trajectories are possible. Finally, we observed that working with partition functions is more natural in some settings. In a deterministic environment for example, near-optimal Bellman equations become linear which is not the case in a value-function-centric approach.

Appendix

Appendix 2.A Deterministic MDPs

2.A.1 is well defined

Proposition 1.

is well defined for .

Proof.

The MDP being finite, has a finite number of final state we can then find a constant such that, for all final states we have .

Where used the fact that all rewards are non positive and that the number of available actions at each state is bounded by . When , the sum becomes convergent and is well defined. ∎

Remark 2.A.1.

is a sufficient condition, but not a necessary one. could be well defined for all values of . This happens for instance when is finite for all .

2.A.2 The underlying policy is Boltzmann-like

For high values of , the sum will become dominated by the contribution of few of its terms. As , the sum will be dominated by the contribution of the paths with the biggest reward. We have

We see that .

Since the MDP is finite and deterministic, it has a finite number of transitions and rewards. Consequently, the set takes discrete values, in particular, there is a finite gap between the maximum value and the second biggest value of this set. Let’s denote by the set of trajectories that achieve this maximum and by .