Boundary-safe PINNs extension: Application to non-linear parabolic PDEs in counterparty credit risk111The authors have no conflict of interest to disclose.

M2NICA research group, University of Coruña, Spain

CITIC research center, Spain

E-mails: joel.perez.villarino@udc.es / alvaro.leitao@udc.es / jose.garcia.rodriguez@udc.es

ABSTRACT.

The goal of this work is to develop deep learning numerical methods for solving option XVA pricing problems given by non-linear PDE models. A novel strategy for the treatment of the boundary conditions is proposed, which allows to get rid of the heuristic choice of the weights for the different addends that appear in the loss function related to the training process. It is based on defining the losses associated to the boundaries by means of the PDEs that arise from substituting the related conditions into the model equation itself. Further, automatic differentiation is employed to obtain accurate approximation of the partial derivatives.

Keywords : deep learning, PDEs, PINNs, boundary conditions, nonlinear, automatic differentiation, option pricing, XVA.

1 Introduction

Deep learning techniques are machine learning algorithms based on neural networks, also known as artificial neural networks (ANNs), and representation learning, see [36] and the references therein. From a mathematical point of view, ANNs can be interpreted as multiple chained compositions of multivariate functions, and deep neural networks is the term used for ANNs with several interconnected layers. Such networks are known for being universal approximators, property given by the Universal Approximation Theorem, which essentially states that any continuous function in any dimension can be represented to arbitrary accuracy by means of an ANN. For this reason, ANNs have a wide range of application, and their use has become ubiquitous in many fields: computer vision, natural language processing, autonomous vehicles, etc. Deep learning algorithms are usually classified according to the amount and type of supervision they get during training and, among all the categories that can be identified, we highlight the supervised and the unsupervised algorithms. They differ in whether they receive the desired solutions in the training set or not.

The aforementioned universal approximation property was exploited in the seminal papers [52], [29] and [48] to introduce a technique to solve partial differential equations (PDEs) by means of ANNs. In recent years there has been a growing interest in approximating the solution of PDEs by means of deep neural networks. They promise to be an alternative to classical methods such as Finite Differences (FD), Finite Volumes (FV) or Finite Elements (FE). For example, the FE technique consists in projecting the solution in some functional space, the Galerkin spaces. Then, by passing to the weak variational formulation and taking the discrete basis, we can find a linear system of equations whose unknowns are the approximated values of the solution as each point of the mesh. In a similar manner, the ANN can be trained to learn data from a physical law that is given by a PDE or a system of PDEs. The idea is quite similar to the classical Galerkin methods, but instead of representing the solution as a projection in some flavour of Galerkin space, the solution is written in terms of ANNs as the composition of nonlinear functions depending on some network weights. As a result, instead of a high dimensional linear system, a high dimensional nonlinear optimization problem is obtained for the ANN weights. This problem must be solved using nonlinear optimization algorithms such as stochastic gradient descent-based methods, e.g., [45], and/or quasi-Newton methods, e.g., L-BFGS, [7]. More recently, with the advances in automatic differentiation algorithms (AD) and hardware (GPUs), this kind of techniques have gained more momentum in the literature and, currently, the most promising approach is known as physics-informed neural networks (PINNs), see [53] [59], [51], [54], [23].

In the last few years, PINNs have shown a remarkable performance. However, there is still some room for improvements within the methodology. One of the disadvantages of PINNs is the lack of theoretical results for the control of the approximation error. Obtaining error estimates or results for the order of approximation in PINNs is a non-trivial task, much more challenging than in classical methods. Even so, the authors in [25], [4], [54], [28], [26], [24] and [27] (among others) have derived estimates and bounds for the so-called generalization error considering particular models. Another drawback is the difficulty when imposing the boundary conditions (a fact discussed further later in this section). Nevertheless the use of ANNs has several advantages for solving PDEs: they can be used for nonlinear PDEs without any extra effort; they can be extended to (moderate) high dimensions; and they yield accurate approximations of the partial derivatives of the solution thanks to the AD modules provided by modern deep learning frameworks.

PINNs is not the only approach relying on ANNs to address PDE-based problems. They can be used as a complement for classical numerical methods, for example training the neural network to obtain smoothness indicators, or WENO reconstructions in order for them to be used inside a classical FV method, see [46], [47]. Also ANNs are being used to solve PDE models by means of their backward stochastic differential equation (BSDE) representation as long as the Feynmann-Kàc theorem can be applied, which is the usual situation in computational finance, for example. In [37], the authors present the so called DeepBSDE numerical methods and their application to the solution of the nonlinear Black-Scholes equation, the Hamilton-Jacobi-Bellman equation, and the Allen-Cahn equation in very high (hundreds of) dimensions. The connection of such method with the recursive multilevel Picard approximations allows the authors to prove that DeepBSDEs are capable of overcoming the so called “curse of dimensionality” for a certain kind of PDEs, see [68], [42].

The main goal of the present work is to develop robust and stable deep learning numerical methods for solving nonlinear parabolic PDE models by means of PINNs. The motivation arises from the difficulty of finding and numerically imposing the boundary conditions, which are always delicate and critical tasks both in the classical FD/FV/FE setting and thus also in the ANN setting. The common approach consists in assigning weights to the different terms involved in the loss function, where the selection of this weights must be done heuristically. We introduce a new idea that consists in introducing the loss terms due to the boundary conditions by means of evaluating the PDE operator restricted to the boundaries. In this way the value of such addends is of the same magnitude of the interior losses. Although this is non feasible in the classical PDE solving algorithms, it is very intuitive within the PINNs framework since, by means of AD, we can evaluate this operator in the boundary even in the case it contains normal derivatives to such boundary. Thus, this novel treatment of the boundary conditions in PINNs is the main contribution of this work, allowing to get rid of the heuristic choice of the weights for the contributions of the boundary addends to the loss function that come from the boundary conditions. Further, AD can be naturally exploited to obtain accurate approximations of the partial derivatives of the solution with respect to the input parameters (quantities of much interest in several fields).

Although the proposed methodology could be presented for a wide range of applications, here we will focus on the solution of PDE models for challenging problems appearing the the computational finance field. In particular, we consider the derivative valuation problem in the presence of counterparty credit risk (CCR), which includes in its formulation the so-called x-value adjustments (XVA). This term refers to the different valuation adjustment that arise in the models when the CCR is considered, i.e., when the possibility of default of the parties involved in the transaction is taking into account. These adjustments can come from different sources within a derivative portfolio: credit (CVA), debit (DVA); funding costs (FVA); collateral requirements (ColVA); and capital requirements (KVA), among others. After the - financial crisis, CCR management became of key importance in the financial industry. Several models were developed in order to enrich the classical pricing models by the introduction of risk terms. In this sense, the value adjustments are terms to be added to, or subtracted from, an idealised reference portfolio value, computed in the absence of frictions, in order to obtain the final value of the transaction.

The first works in this topic appeared before the above-mentioned crisis, focusing on analyzing the CVA concept. Some seminal works from this period are [30], [11] and [18]. After the crisis, the XVA adjustments gained huge attention. The models in which the possibility of default of the parties involved in a transaction were revised by the introduction of the DVA factor, [13], [9]. Additionally, the increasingly important role of collateral agreements demands for a portfolio-wide view of valuation by introducing the ColVA factor. In a Black-Scholes economy, [57] gives valuation formulas both in the collateralized and uncollateralized case. In addition, generalizations to the case of a multi-currency economy can be found in [58], [31], [32], and [35]. Another important aspect for the industry, apart from default risk, is represented by funding costs. Currently, the trading activity is dependent on different sources of liquidity such as the interest rate multi-curve, [22], and the old assumption of a unique risk-free interest rate is no longer realistic. In [55], the FVA is included into a risk-neutral pricing framework for CCR considering realistic settings. Such work is extended in [12], where the effect of Central Clearing Counterparties (CCPs) on funding costs is studied. In this regard, there are many more contributions in obtaining a single risk management framework which includes funding and default risk. In [8] is developed a unified valuation theory that incorporates credit risk, collateralization and funding costs by means of the so-called discounting approach. The authors in [15], [14] generalize the classical Black-Scholes replication approach to include some of the aforementioned effects. A more general BSDE approach is provided by [20], [21], [5], and [6]. In addition, the equivalence between the discounting and BSDE-based approaches is demonstrated in [8].

Of course, the world of quantitative finance in general, and CCR management in particular, has not been exempt from the advances in deep learning and, nowadays, ANNs are employed for a wide variety of tasks in the industry. Unsupervised ANNs, in both flavours, PINNs and DeepBSDEs, have been recently used for solving challenging financial problems. For example, in [62] the authors apply PINNs for solving the linear one and two dimensional Black-Scholes equation, and [67] introduces the solution of high dimensional Black-Scholes problems using BSDEs. In [34] the authors present a novel computational framework for portfolio-wide risk management problems with a potentially large number of risk factors that makes traditional numerical techniques ineffective. They use a coupled system of BSDEs for XVA which is addressed by a recursive application of an ANN-based BSDE solver. Other relevant works that make use of ANNs for computational finance problems, although not formulated as PDEs, include [40], [41], or [50], for example.

The outline of this paper is as follows. In Section 2 we start by revisiting the PINNs framework for solving PDEs. Section 3 introduces the new methodology for the treatment of the boundary conditions in the PINNs setting. In Section 4, the XVA PDE models that we solve in this paper and the adaptation to our PINNs extension are described; more precisely, XVA problems in one and two dimensions, under on Black-Scholes and Heston models. Finally, in Section 5, the numerical experiments that assess the accuracy of the approximation for option prices and their partial derivatives (the so-called Greeks) are presented.

2 PINNs

In this section we introduce the so-called PINNs methodology for solving PDEs. The illustration is carried out according to the kind of PDEs that arise in the selected financial problems, i.e., semilinear parabolic PDEs with source terms. Thus, let be a bounded, closed and connected domain and . Consider the following boundary value problem. Given a function and setting , find such that

| (1) |

where is a strongly elliptic differential operator of second order in the space variables , and is a boundary operator defined, for example, by a Dirichlet and/or Neumann boundary conditions. The goal is to approximate this unknown function by means of a feed-forward neural network, where are the network parameters.

2.1 Feed-forward neural networks

A feed-forward network is a map that transforms an input into an output by means of the composition of a variable number, , of vector-valued functions called layers. These consist of units (neurons), which are the composition of affine-linear maps with scalar non-linear activation functions, [36]. Thus, assuming a -layer network with neurons per layer, it admits the representation

| (2) |

where, for any ,

| (3) |

with and .

Usually (and this is taken as a guideline in this paper) the activation functions are assumed to be the same in all layers except in the last one, where we consider the identity map, . In addition, taking into account the nature of the problem, it is required that the neural network fulfills the differentiability conditions imposed by (1), requiring sufficiently smooth activation functions such as the sigmoid or the hyperbolic tangent, [63].

Lastly, it should be noted that a network as the one described above has neurons, with parameters per layer, yielding a total of

| (4) |

parameters, which determine the network’s capacity.

2.2 Loss function and training algorithm

In order to obtain an approximation of the function by means of a neural network, , we need to find the network’s parameters, , that yields the best approximation of (1). This leads to a global optimization problem that can be written in terms of the minimization of a loss function, that measures how good the approximation is. The most popular choice for PINNs’ methods is to reduce the problem (1) to an unconstrained optimization problem, [29], leading to the family of loss functions involving the error minimization of the interior, initial and boundary residuals. Thus, the loss function, , is defined as

or, equivalently,

| (5) |

where

| (6) | ||||||

| (7) | ||||||

| (8) |

account for the residuals of the equation, the boundary condition and the initial condition, respectively. The are preset hyperparameters (or updateables during optimization) that allow to impose a weight to each addend of the loss, as can be seen in, e.g., [66], [44]. Note that, for the computation of the residuals (6), (7), it is necessary to obtain the derivatives of the neural network with respect to the input space and time variables, well defined under the premise of using sufficiently smooth activation functions. Numerically, they are calculated with the help of AD modules, such those included in Tensorflow, [1], and Pytorch, [56]. Finally, the strategy followed in PINNs consists of minimizing the loss function (5), i.e, finding such that

| (9) |

where is the set of admissible parameters.

Except for the simple cases, the integrals appearing in (5) must be computed numerically by means of quadrature rules, [54]. For this reason, we need to select a set of training points, , where

acting as nodes in the quadrature formulas.

Clearly, the choice of the quadrature technique has a direct influence on how these points are selected, and may correspond to, for example, a suitable mesh for a trapezoidal quadrature rule, SOBOL low-discrepancy sequences, a latin hypercube sampling, etc. Moreover, such choice is highly influenced by the problem’s time-space dimension, being necessary to use random sampling in high-dimensional domains.

In general terms, we can define the quadrature rule to calculate the integral of a function , as

| (10) |

with the weights and the nodes of the quadrature rule. This allows us to rewrite the loss function (5) taking into account the chosen discretization and quadrature as follows,

| (11) |

From now, we will call “training” the process of finding the minimum of the problem (9) with the loss function defined in (11). Even in the case of working with linear PDEs, where the defined functional would be convex, transferring the problem to the parameter space of the neural network yields a high dimensional and highly non-convex problem, [66]. As a consequence, the uniqueness of the solution is not guaranteed, and we can only expect to reach a sufficiently low local minima. For this reason, it is common to employ stochastic gradient descent-based methods, such as Adam, [45], or higher-order quasi-Newton optimizers, such as L-BFGS, [49]. In practice, it also implies that a proper choice of model hyperparameters, such as the network size or the learning rate, is essential to achieve a high degree of accuracy. Taking into account what has been explained throughout this section, we detail the steps to find a neural network that approximates the solution of the problem (1) in Algorithm 1.

Essentially, and except for some particularities, the training process in the case of PINNs is similar to that presented in any other supervised or unsupervised tasks in the field of deep learning. Thus, many of the techniques developed to improve training in such areas can be trivially applied to our case, such as regularization techniques, [36], Dropout, [64], transfer learning, [33], or other strategies designed to improve the performance of the global optimizer. Once trained, the network serves as an approximate solution to problem (1). It can be evaluated at any point in the domain, and its derivatives can be calculated by AD in few seconds.

Remark 1.

One of the most popular quadrature techniques is Monte Carlo integration. On the one hand, it is a mesh-free method since the points are sampled randomly, making it suitable for high dimensional problems as it does not suffer from the curse of dimensionality. On the other hand, applied to the error expression (11), it gives rise to the mean squared error function, widely used in the deep learning’s world.

If we consider a random set of collocation points and define the quadrature weights as

and taking

| (12) |

with , then we obtain

where

which resembles the loss function employed in most of the works in this topic.

2.3 Convergence and generalization error bounds

With the growth of these methodologies, it is of increasing interest to derive convergence results, as they exist in the finite differences and finite elements world. There are works, such as [63], in which classical notions of consistency and stability are exploited to prove the strongly convergence of the minimizer to the solution of the linear second-order elliptic or parabolic problem, as the number of collocation points grows. This assumes a random discretization of the domain, together with Monte Carlo integration.

However, most of the theoretical work on PINNs is dominated by the search for generalization error bounds, where the generalization error, , is understood as the total error of the approximated solution, which in our case is given by the square root of the loss function (5), i.e.,

and depends on the network parameters . As discussed in the previous section, evaluating this expression requires the use of numerical integration methods with their respective quadrature points, . In this sense, the square root of the discretized version of the loss function, given in (11), serves to approximate the generalization error and is also known as training error, .

Under this setting, we find several papers that attempt to bound the generalization error, for specific problems, in terms of the training error, the chosen quadrature rule, the number of collocation points and the stability of the underlying PDE. For example, such bounds are obtained for the linear Kolmogorov equation, [25], the equation related to the viscous scalar conservation laws and the semi-linear parabolic equation, [54], among others. Thus, under existence, uniqueness and regularity assumptions for the semi-linear parabolic case with Lipschitz nonlinearities, the Theorem from [54] states that the generalization error can be estimated as

where are the training errors which verify the relationship . In addition, are the bounds of the quadrature error related to the initial condition, interior domain and boundary, respectively; and , are constants that depend on the regularity of the true solution and neural network approximation on the boundary, together with the temporal domain. This result is of special interest because its hypotheses fit within our general problem (1) and, furthermore, since we will work with a non-linear contractive source term, the result can be easily applied to the particular problems presented in Section 4.

In a recently published paper, [27] present several error bounds in a more abstract framework. Under sufficiently smooth domains, and under the assumptions: there exist a neural network that can approximate the solution of the time-dependent PDE at time with a prescribed tolerance ; and the error of the PINNs algorithm can be bounded by means of the error related to its partial derivatives; the following theorem holds.

Theorem 1.

([27]) Let , , let be the solution of the abstract time-dependent PDE with initial condition and let the above assumptions be satisfied. There exists a constant such that for every and there exist a neural network , with the hyperbolic tangent as activation function, for which it holds that,

where is the number of spatial intervals chosen in the discretization.

Moreover, this theorem includes an additional result in which the -norm of the operator applied to the neural network is bounded, and both statements together imply that there exists a neural network for which the generalization error and the PINN’s loss function can be made as small as possible. Since our framework is embedded within this abstract formulation, such result ensures a solid theoretical foundation for our work.

3 Novel treatment of boundary conditions

Ideally, the loss function correctly captures how far away we are from the exact solution of the problem and how well the boundary restrictions are fulfilled, so that the optimization algorithm can get us close to a good local minima, at least. However, in practice, this situation is not always reproduced when applying numerical methods. In the case of PINNs we also have this problem and, although the reasons why this happens are poorly understood, previous works, such as [44], point to the fact that training is focused on getting a small PDE residual in the interior domain, while leading to large errors in the fitting of the boundary conditions. This suggest that the contribution of the some boundary errors vanishes.

In most of the works on this topic, this problem is usually solved by introducing the lambda weights seen before, which preponderate the contribution of each of the terms involved in the elaboration of the loss function (11). The optimal choice of this weights is of paramount importance for the algorithm. The main drawback of this methodology is that the choice of these values is problem-dependent and in most situations is carried out heuristically, [44].

We identify that the introduction of the overriding factors is mainly driven by two features. On the one hand, we encounter the problem that the integrals involved in the loss function present different domain dimensionality, i.e., introduce different magnitudes of volume. The integral referring to the residual in the interior of the domain involves a -volume, while the integrals associated with the initial and boundary residuals involve a (-)-volume.

An easy solution to solve this situation is to force these lambdas to be inversely proportional to the volume of the each integral’s domain considered (as we have shown for the Monte Carlo case). Then, taking into account (12), we rewrite the discrete loss function (11) as

| (13) |

On the other hand, the magnitude of the contributions to the loss function can differ in several orders, i.e., there are addends which are negligible with respect to others, leading to a worse local minima in the training, or the need to extend training time. In general, there are two possible situations that can occur simultaneously in a boundary value problem. One of them is that we can find residuals with large relative losses as the beginning of training. As a consequence, they can cause longer training times, as in the early stages of training the loss function only provides information regarding such losses. The other possibility is that we can find boundaries in which the residuals exhibit relatively much smaller values, so their contribution to the loss function is, in many cases, negligible. As a consequence, such constrains could not provide information to the training.

In order to avoid the arbitrary selection of the loss function weights, it is essential to reduce the differences in magnitude among residuals. For this reason, we propose, for the first time to the best of our knowledge, a novel approach which overcomes these weights’ issue. It is based on reformulating, whenever possible, the residuals related to Dirichlet or Neumann (Robin, higher order derivatives) conditions. This reformulation relies on taking as a residual not the boundary condition itself but the resulting PDE restricted to the corresponding boundary. This will produce losses of an order of magnitude similar to that produced by the interior residual, once these quantities are dimensionless.

Thus, most of the Neumann, Robin or higher order derivative boundary residuals we will work with can be written in this form. It suffices to substitute the condition into the PDE of the interior domain and impose the resulting equation on the related boundary residual. However, it will only be possible to impose Dirichlet conditions in this way when they naturally occur at the boundary, i.e., when the Dirichlet condition arises from solving the differential equation that results at the boundary.

As an illustrative example, let us consider a particular case of the parabolic problem defined in (1), where Dirichlet and Neumann boundary conditions are presented. Under the spatial domain , the upper boundaries

and the lower boundaries

we want to find the parameters of an ANN in order to make it verify

| (14) |

where , and , . For example, when defining the residuals associated with the Neumann conditions, the usual approach is to take the condition itself as the residual, i.e.

Alternatively, in our proposal, we plug the Neumann condition into the PDE and impose the resulting equation as a residual, obtaining

For Dirichlet conditions, the proposed strategy can only be applied when verifies the PDE and the initial condition of (14) at the boundary . In such cases we can define the residual in the same way as the residual of the PDE, i.e.,

Because of that, such kind of Dirichlet conditions does not even need to be included as boundary residuals. Depending on the quadrature scheme employed, it would be enough to force the existence of interior domain collocation points on such boundary.

Remark 2.

As a summary, we have first briefly described the main problems that lead to the introduction of additional weights in the loss function. Then we have proposed a new treatment of the boundary residuals that allows to avoid such weights. When we deal with derivative-based boundary conditions, the related residuals are defined by taking the equation resulting from substituting the boundary conditions in the PDE. For residuals associated with Dirichlet boundary conditions, we can impose the PDE itself as a boundary residual as long as it arises naturally on such boundary.

4 Application to problems in computational finance

In this section we present the PDE formulation of the particular problems we will address in this work. We focus on some relevant (and challenging) state-of-the-art problems appearing in computational finance, specifically, in the area of the CCR assessment. Thus, we consider the valuation of some financial derivatives when accounting for such a risk, namely the pricing of different risky European option under the Black-Scholes and Heston model. All of them are extensions of the risk-free derivative pricing models to a formulation that takes into account the effects of bilateral default risk and the funding costs, i.e., which includes CVA, DVA and FVA adjustments, following the approach of [15]. We chose this methodology for its simplicity, but any more complex extension, such as [10], can fit into our framework.

4.1 General pricing problem formulation

Let us consider a derivative contract on spot assets, , between two parties, the seller B and its counterparty C, where both may default. We assume that the default of either B or C does not affect . Such derivative pays the seller B the amount at maturity . In addition, let the same derivative between two parties that cannot default, i.e., the non-risky derivative value.

Under the described setting, if either the seller or the counterparty defaults, the International Swaps and Derivative Association (ISDA) Master Agreement determines that the value of the derivative is fixed by a Mark-to-Market rule , which is chosen to be either or , adjusted by means of , the recovery rates on if seller or counterparty defaults, respectively. Considering as the risk-free interest rate, the seller’s bond yield and the counterparty’s bond yield. Following [15] and [61] we can define the B and C’s default intensities, and , by means of the spread between their bond yields and the risk-free interest rate, i.e.,

In addition, the seller’s funding rate for borrowed cash is considered. If the derivative can be used as collateral, is taken, while if collateral cannot be used as collateral, is taken. In this regard, we define the funding spread as

From now on, we establish the Mark-to-Market rule and that the derivative cannot be used as collateral, so a non-linear PDE model for is obtained. It follows the general definition

| (15) |

where is the time to maturity variable, the differential elliptic operator defined by the chosen problem, and the non-linear source term given by

| (16) |

In addition, the derivative value without considering counterparty risk, , obeys the PDE

| (17) |

4.2 Specific pricing problem formulation

Having defined the general context of the financial problems to be addressed, we are in a position to present the boundary value problems obtained in each specific case, as well as their adaptation to the methodology presented in Section 2.

4.2.1 European option under the Black-Scholes model

We consider an European option with strike and maturity . Let the underlying stock value, the volatility in and the stock repo rate minus the dividend yield under the Black-Scholes model. The option price, , is given by equation (15) taking the elliptic operator as

| (18) |

and the initial condition the vanilla payoff,

| (19) |

with and for put and call options, respectively. In this case, an analytic solution for (18)-(19) is known, [15],

| (20) |

where is the solution of the classical Black-Scholes equation:

| (21) |

with the cumulative distribution function of a standard normal variable, and

In order to apply the methodology introduced in Section 2 for its resolution, it is necessary to carry out a truncation of the semi-infinite domain into . This step enforces us to include boundary conditions when . For the left boundary, , it is sufficient to substitute in the equation (15) with (18)-(19), obtaining

| (22) |

which can be imposed as the following Dirichlet boundary condition,

| (23) |

Taking into account that

| (24) |

we can consider such linear boundary condition for the right boundary, , when is large enough. Examples of application can be viewed in, e.g. [17].

Thus, for , the European option considering CCR from above verifies the following boundary value problem. Find such that

| (25) |

Moreover, it is straightforward to prove that the European option without considering counterparty risk verifies the equation (25) by taking or, equivalently, taking .

Such formulations fits into problem (1) so we can apply everything explained in Section 2 to solve it. In order to do this, we consider a discretization of the domain

by a uniform discretization of each of the presented subsets. For the sake of clarity, we present here a uniform mesh throughout the domain. Thus, calling the number of steps in the -direction and the number of time steps, we take the grids,

with and the steps size. Therefore, the set of collocation points of the problem is given by

| (26) |

with size

| (27) |

To approximate the desired solution we consider a neural network, , with hidden layers. Without loss of generality, we assume that the number of neurons per hidden layer is the same, . Based on the boundary value problem given in (25), we choose the network residuals taking into account our proposal to solve the aforementioned training issues. Thus, since on the boundary the Dirichlet condition arises naturally, we can use the expression (22) as boundary residual. Moreover, on the boundary we have a higher-order derivative condition, so we can substitute this condition, (24), into the equation (15) in order to impose such residual in the same way as we explain in Section 3. Applying these considerations, we obtain the following residuals,

| in | (28) | |||||

| in | (29) | |||||

| in | (30) | |||||

| in | (31) |

Using these residuals, the loss function is defined in the same way as in (13) by taking the lambda weights equal to one and the quadrature weights corresponding to the trapezoidal rule,

| (32) |

4.2.2 European basket option under the Black-Scholes model

Next, we present a European basket option driven by two assets, and , with strike and maturity . As we did before, for each asset we consider its volatility , and its repo rate minus dividend yield , with for the first asset and for the second. Further, we define the correlation between assets, , verifying that The basket options’ price, , is given by the equation (15) taking the elliptic operator

| (33) |

with the initial condition the derivative’s payoff . In our case, we work with two challenging and practically appearing payoffs, namely, the arithmetic average payoff,

| (34) |

and the worst-of payoff:

| (35) |

It is worth noting that in the case of the worst-of risk-free option, an analytical solution is known, see for example [65], [38].

The spatial domain is a Cartesian product of semi-infinite intervals, , and, for its numerical resolution, each interval is truncated, obtaining . Moreover, additional conditions must be imposed on the boundaries , , and . For the lower boundaries it is possible to impose Dirichlet conditions which again arise naturally. At each boundary, , we substitute obtaining

| (36) |

which, with the initial condition (34), gives rise to the one-dimensional risky Black-Scholes equation (20) depending on the other underlying. If we consider the initial condition (35) we can impose the expression (23), since the initial condition does not depend on the remaining underlying.

For the upper boundaries , we work with the linear boundary condition (24), used for the non-risky cases in, e.g., [60], since the qualitative behaviour of the solution does not change in the limit.

Thus, the European arithmetic average basket option considering CCR verifies the boundary value problem of finding such that

| (37) |

where refers to the Black-Scholes formula (20) applied to .

The European worst-of basket option with counterparty risk verifies the value problem of finding the function such that

| (38) |

Similarly to the one-dimensional problem seen before, the same boundary problems are valid for the associated risk-free options by taking .

Both formulations fit into the problem (1), and can be applied as discussed in the Section 2. Thus, we consider a discretization of the domain

by a uniform discretization of each of the resulting subsets of the decomposition, although for illustrative purposes we present the simplest case. We denote as and the number of steps in the , and time-direction. Given these values, the grids are given by

with and the step size related to each cartesian direction. Thus, the set of collocation points is given by

with size

In order to obtain an approximate solution to the problems, a neural network under the same structural assumptions as for the one-dimensional case is considered. For both problems we can take the same residuals, except to that related to the initial condition, following the strategy presented in Section 3, so that,

| in | (39) | |||||

| in | (40) | |||||

| in | (41) | |||||

| in | (42) | |||||

where is given by (34) or (35) for the arithmetic average or the worst-of option, respectively . Taking such residuals into account, it is straightforward to obtain an expression for the loss function similar to (32).

4.2.3 European option under the Heston model

The last problem we address is the pricing of a European option accounting for CCR, with strike and maturity , under the assumption that the variance of the underlying follows a stochastic process. Thus, let be the underlying stock value and the stock repo rate minus the dividend yield. We define the volatility of from its variance, , which follows a CIR process, [19], with the mean variance, the mean reversion rate, the volatility of the variance and the correlation between the asset and variance processes. Under this setting, the Heston model is obtained, [39].

The PDE problem for pricing the risky European option under the Heston model is derived in [61]. The option price is the solution of the equation (15) taking the elliptic operator

| (43) |

and as an initial condition the vanilla payoff (19).

As in the previous case, it is necessary to establish an effective domain in order to apply numerical methods. Thus, we define our computational domain as and , again, additional conditions must be imposed over the boundaries , , and .

Following the boundary condition analysis carried out in [61] and [16], it is not necessary to impose an additional condition on the boundary . In addition, it will be only necessary to impose a condition on the boundary if the Feller condition, , is violated. In such case, a common choice is to impose a Dirichlet condition obtained from the numerical resolution of the equation

| (44) |

On the boundary we keep the linearity condition (24), while on the boundary we choose to employ the Neumann condition derived from the fact that

| (45) |

We are in position to present the boundary value problem for pricing the risky European option under the Heston model. Therefore, we find such that

| (46) |

when the Feller condition is satisfied. Again, the risk-free Heston boundary problem is recovered by taking the risk parameters ; and such formulations fits into the problem (1), so the techniques in Section 2 can be readily applied.

At the methodological level, the development of this two-dimensional problem is similar to the one already seen. Starting from a discretization of the domain (we can think of the one given before), we define the residuals used in the training of a neural network in the task of approximating the solution of (46) as

| in | (47) | |||||

| in | (48) | |||||

| in | (49) | |||||

| in | (50) | |||||

| in | (51) | |||||

In this case, we decide to include the boundary-related residuals (49) and (50) as if they were boundary conditions, but they could be also considered as part of the interior of the domain straightforwardly. Then, is trained by means of a loss function like the one presented in (32), adapted to the residuals and higher dimension present here.

5 Numerical experiments

After presenting the mathematical models and discussing how they fit under our reformulation via PINNs, in this section we show the results of the tests performed to assess their effectiveness. One of the main advantages of this methodology over traditional numerical methods is that the container of the approximate solution is an ANN, i.e., a function. Thus, it is possible to compute its derivatives via AD. In this regard, we will focus not only on how well it approximates the desired solution, but also on how accurately it approximates its derivatives.

| Black Scholes parameters | |

|---|---|

| Strike, K | |

| Time to maturity, T | |

| Volatility, | |

| Repo rate minus dividend, | |

| Interest rate, | |

| xVA parameters | |

| Seller hazard rate, | |

| Counterparty hazard rate, | |

| Seller recovery rate, | |

| Counterparty recovery rate, | |

| Funding spread, | |

The section is divided into two parts. In the first, we focus on the one-dimensional parabolic problem, i.e., the pricing of options via Black-Scholes model; while the second covers two-dimensional parabolic problems, i.e., basket options and Heston option pricing. The same pattern is followed in both parts. First, an optimal network configuration, namely, the optimal number of layers and units per layer, is determined. For this purpose, the training metrics and the time required are taken into account. Subsequently, the error of the approximations is analyzed and, finally, tests relative to the computation of derivatives are presented. The reference values are computed by using the available analytic solutions or extremely reliable approximations based on classical resolution techniques such as FD or FE.

For the training, we use expression (13) as the loss function, adapted by following the analysis carried out in Section 4 and taking all lambda weights equals to one. In addition, we choose the trapezoidal rule as the quadrature method. Consequently, we take an uniform grid of collocation points with variable size depending on the problem. Each training is split into two stages, depending on the employed optimizer. In the first stage, Adam is used as a global optimizer with the reference parameters given in [45], and, in the second one, L-BFGS is used as a local optimizer.

5.1 Parabolic one-dimensional case

We study the one-dimensional parabolic case by means of the Black-Scholes equation presented in Section 4.2.1. For this purpose, we consider the model data presented in Table 1 and choose as the truncation value of the domain. In addition, we work with a spatial discretization of points and a temporal discretization of points, yielding a total of collocation points, which falls within the reference values that can be found in other works, such as [59].

First, a test is conducted to check how the network’s training behaves when varying its number of layers and neurons per layer. For this purpose, all possible combinations between layers and units per layer are considered. For each combination, a sample of training is made. The pricing of an European put option, , is the target, so we use the loss function (32) taking . The optimization process has steps with Adam and with L-BFGS. The accuracy of the PINNs solution is measured by comparing its relative error with the analytic solution (21).

| 2 | 4 | 8 | 16 | |

|---|---|---|---|---|

| 10 | -3.664 | -3.531 | -3.669 | -0.149 |

| 20 | -3.182 | -3.344 | -3.465 | -2.99 |

| 40 | -3.357 | -3.557 | -3.301 | -0.159 |

| 80 | -3.457 | -3.519 | -3.398 | -0.148 |

| 2 | 4 | 8 | 16 | |

|---|---|---|---|---|

| 10 | -3.113 | -3.098 | -0.937 | -0.202 |

| 20 | -3.160 | -3.308 | -3.396 | -2.969 |

| 40 | -3.351 | -3.447 | -3.356 | -0.188 |

| 80 | -3.382 | -3.441 | -3.419 | -0.209 |

| 2 | 4 | 8 | 16 | |

|---|---|---|---|---|

| 10 | -2.893 | -2.986 | -0.855 | -0.214 |

| 20 | -3.001 | -3.134 | -3.216 | -2.852 |

| 40 | -3.177 | -3.206 | -3.160 | -0.152 |

| 80 | -3.190 | -3.207 | -3.226 | -0.189 |

| 2 | 4 | 8 | 16 | |

|---|---|---|---|---|

| 10 | 0.465 | 0.536 | 0.677 | 0.721 |

| 20 | 0.468 | 0.547 | 0.693 | 0.928 |

| 40 | 0.481 | 0.590 | 0.758 | 1.000 |

| 80 | 0.530 | 0.680 | 0.946 | 0.926 |

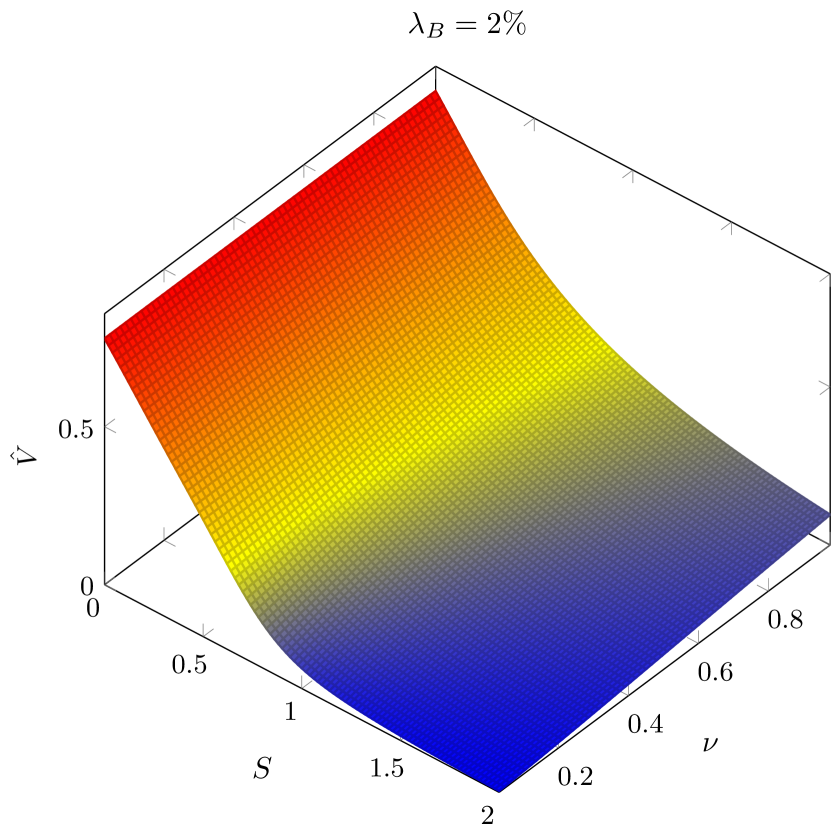

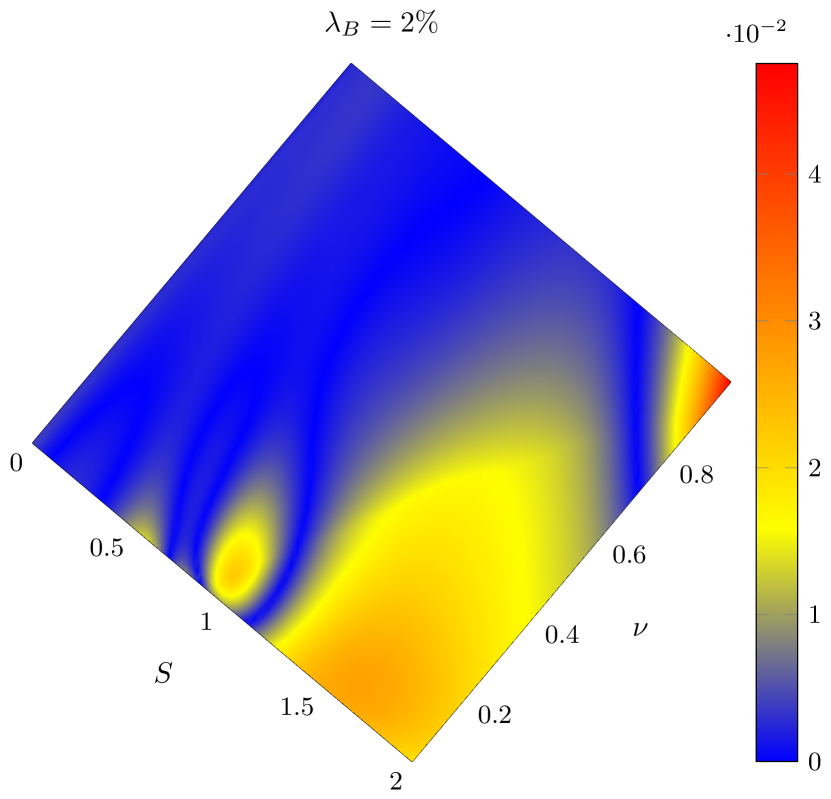

Tables 2(a), 2(b) and 2(c) show the relative error achieved in the worst training for each considered combination of layers and units per layer. As we can see, most of the combinations give good results, with the relative error similar to those obtained for the same task in [62], where the tuning of the lambda weights is performed and the Monte Carlo integration is employed as a quadrature rule. From these tables we can also see that the use of a large number of layers is unstable, since the convergence of the method fails for some trials. This situation is possibly related to problems in updating the network’s weights, such as vanishing gradient problems, due to the combination of very deep networks and bounded activation functions, [33].

Trying to find a balance between accuracy, robustness and performance, we have measured the training time for each studied combination and, in Table 2(d), we present the relative times obtained with respect to the largest one. Based on them, in what follows, we work with layers and units per layer, where we have achieved, in the best case, a relative error of , and for the , and -norm, respectively.

Once the size of our network has been selected, we present some results on its performance for the non-linear case. To do this, we consider six possible default scenarios depending on the seller hazard rate, namely , and train our network to price a risky put option with the rest of the parameters given in Table 1. As we did before, we perform samples per and we select network weights that give the best result. The optimization process setting is kept invariant. The obtained solution is compared with the analytical solution (20).

Figure 1 shows the comparison between the analytical and PINNs approximated solution for each considered. The risk-free option is added for completeness. Regardless of the default scenario chosen, the quantitative behaviour of our approximation is identical to that given by the analytical solution. The accuracy of the approximation is particularly good in the neighbourhood of the strike, an area of interest in our pricing task. This is supported by Table 3, where we can see that, for all cases, the error is of the order of . Moreover, we observe that there does not exist any loss of accuracy in the non-linear cases, thus requiring no further treatment.

| Case | ||||

|---|---|---|---|---|

| Risk-free | ||||

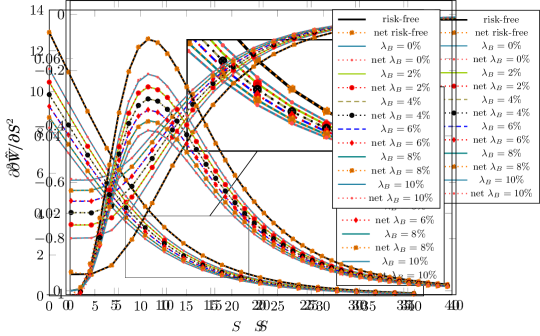

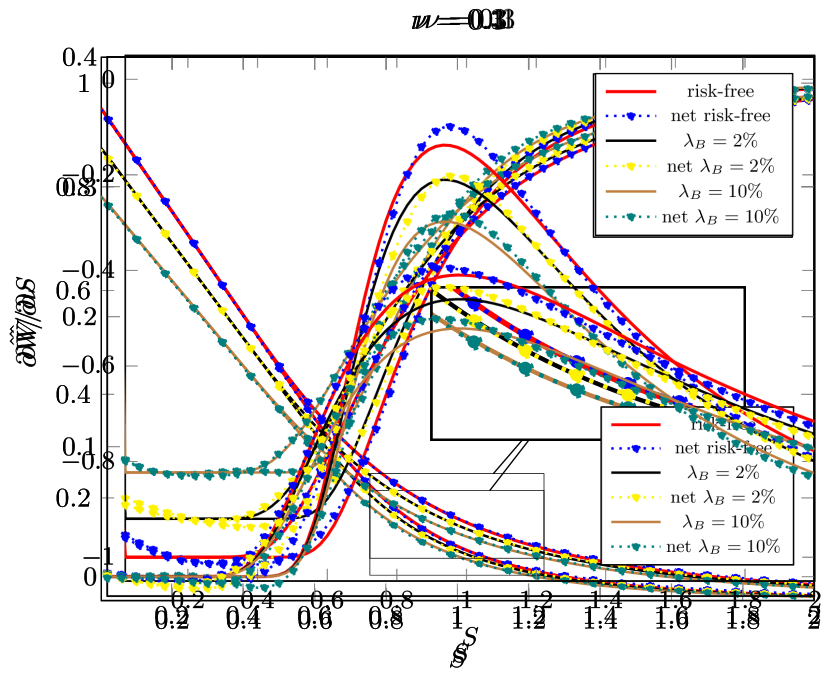

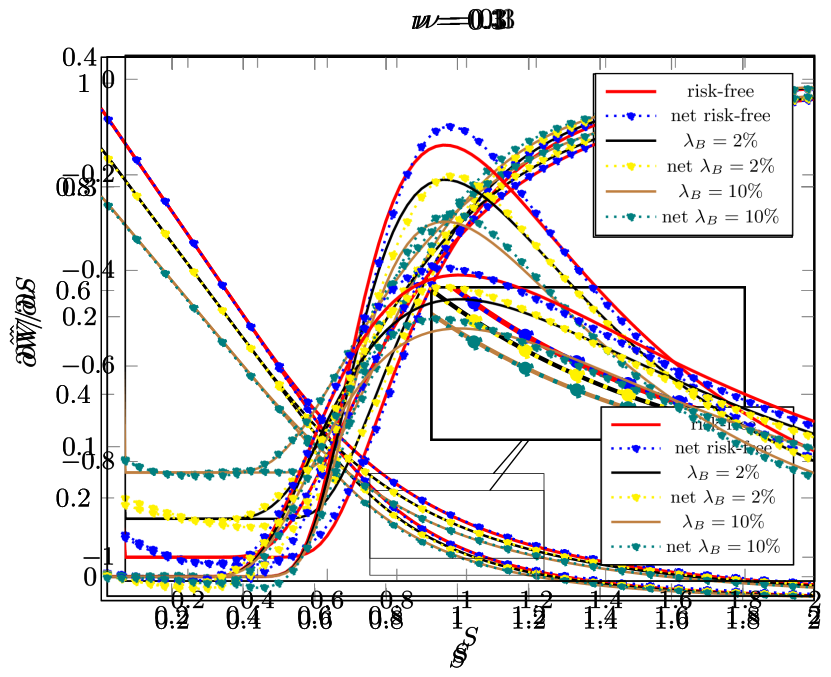

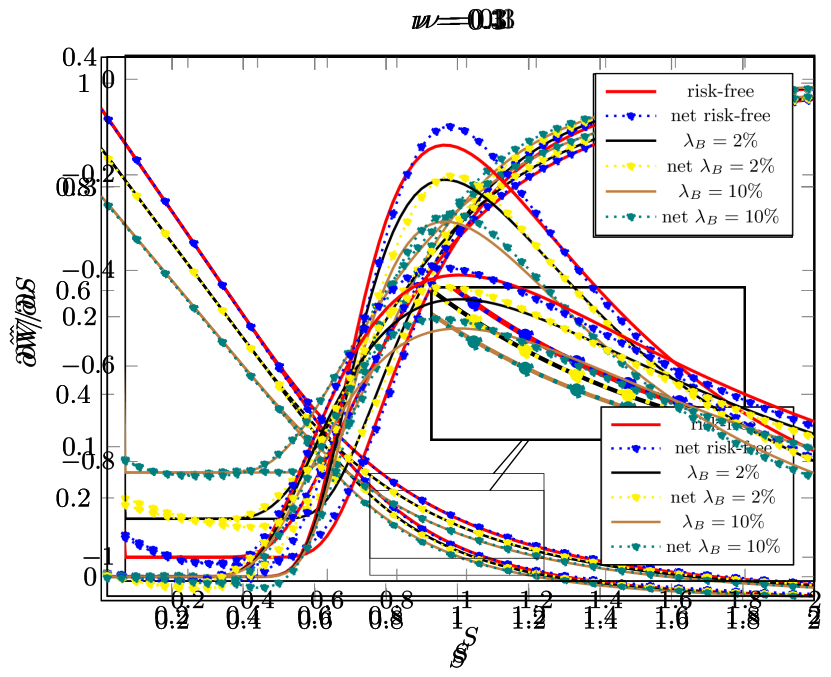

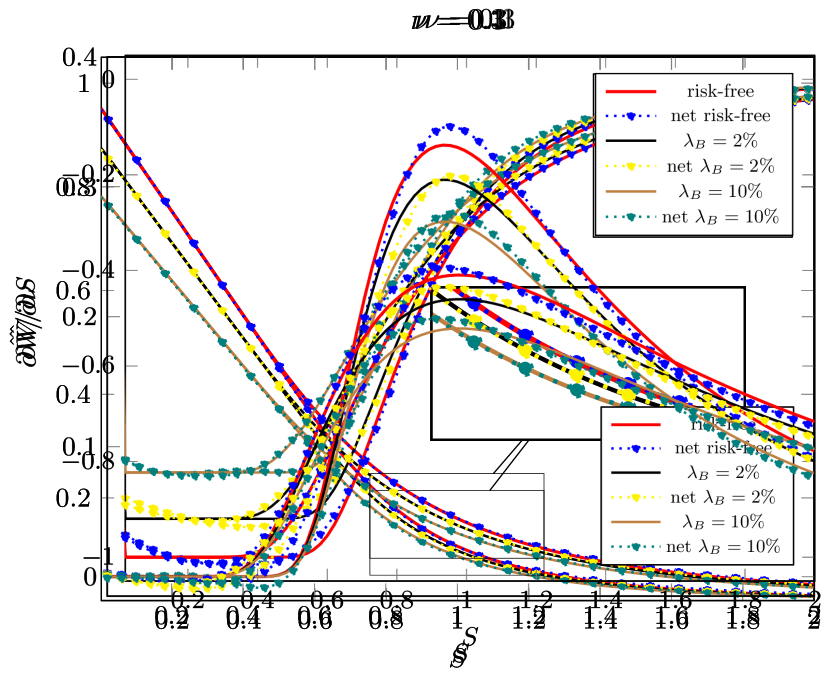

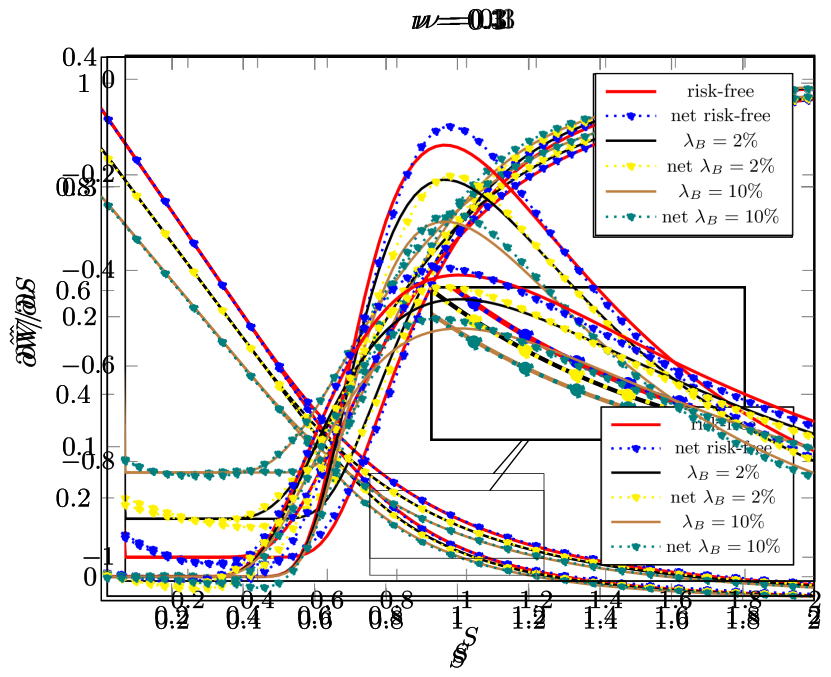

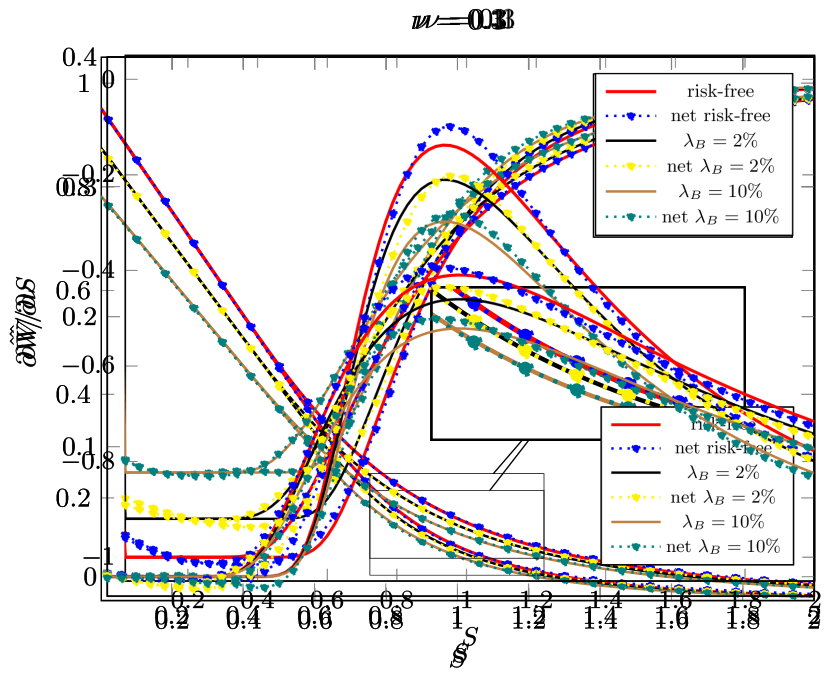

By means of the AD, we can compute the derivative of the option price with respect to its related quantities. Such expressions are known as Greeks in quantitative finance. Thus, in Figure 2(a) and Figure 2(b), we can observe the same comparison made for the price, now for delta and gamma Greeks222Delta and gamma Greeks are, respectively, the first and second-order derivative of the option price with respect to its underlying., respectively. In the delta case, a slight decrease in accuracy is observed near the boundary , which also transfers to the gamma case, as expected. In the rest of the domain there is not a loss of accuracy with respect to the pricing case. Specially in the neighbourhood of the strike, where we obtain relative errors of a similar order of magnitude, see Table 3. In the case of the second derivative we observe, in general, an increase in the relative error, now of the order of . This is also expected since it presents numerical instabilities that makes it more difficult to compute.

5.2 Parabolic two-dimensional case

Having seen the results obtained for the one-dimensional Black-Scholes equation, with and without considering counterparty risk, we now present the results obtained for the rest of the presented models.

5.2.1 Basket options under the Black-Scholes model

We first deal with the basket options, whose formulation has been presented in Section 4.2.2. For this purpose, we consider the model data given in Table 4, and choose as the truncation values of the domain .

| Black-Scholes parameters | ||

|---|---|---|

| Strike, | ||

| Time to maturity, | ||

| Interest rate, | ||

| Volatility, | ||

| Repo rate minus dividend, | ||

| Correlation, | ||

| xVA parameters | ||

| Seller hazard rate, | ||

| Counterparty hazard rate, | ||

| Seller recovery rate, | ||

| Counterparty recovery rate, | ||

| Funding spread, | ||

As in the previous case, we are interested in finding an optimal combination of layers and neurons per layer in terms of accuracy and training time required. Thus, we consider all possible combinations between layers and units per layer. Again, a sample of training trials is considered per combination. We use the pricing of a non-risky arithmetic average put option as a target, so we use the loss function given by the residuals (39)-(42) with .

In the training stage we use a total of collocation points (), and the optimization process has steps with Adam and with L-BFGS. Since the analytical solution for such options is not known, we measure the accuracy of the PINNs solution by comparing its relative error with an approximated solution of the non-risky boundary value problem (37) obtained via FD (Crank-Nicolson timestepping and centered differences).

| 2 | 4 | 8 | 12 | |

|---|---|---|---|---|

| 10 | -2.285 | -2.143 | -2.360 | -2.190 |

| 20 | -2.599 | -2.503 | -2.776 | -2.565 |

| 40 | -2.832 | -3.013 | -3.403 | -2.190 |

| 60 | -2.910 | -3.430 | -3.470 | -3.657 |

| 2 | 4 | 8 | 12 | |

|---|---|---|---|---|

| 10 | -2.127 | -2.067 | -2.233 | -2.088 |

| 20 | -2.466 | -2.380 | -2.705 | -2.473 |

| 40 | -2.688 | -2.908 | -3.339 | -2.127 |

| 60 | -2.728 | -3.326 | -3.418 | -3.553 |

| 2 | 4 | 8 | 12 | |

|---|---|---|---|---|

| 10 | -1.785 | -1.702 | -1.971 | -1.626 |

| 20 | -2.194 | -2.117 | -2.399 | -2.059 |

| 40 | -2.308 | -2.530 | -2.886 | -1.928 |

| 60 | -2.328 | -2.949 | -2.907 | -2.976 |

| 2 | 4 | 8 | 12 | |

|---|---|---|---|---|

| 10 | 0.233 | 0.291 | 0.401 | 0.994 |

| 20 | 0.233 | 0.291 | 0.3400 | 0.996 |

| 40 | 0.232 | 0.291 | 0.400 | 0.993 |

| 60 | 0.233 | 0.288 | 0.392 | 1.000 |

Tables 5(a), 5(b) and 5(c) show the relative error achieved in the worst training for each combination of layers and units per layer considered. We can observe a general increase in relative errors compared to the one-dimensional case, especially for combinations of layers and neurons that provide less capacity to the network. This is an expected situation since, on the one hand, the number of collocation points per spatial direction is much lower than in the previous case, and, on the other hand, the complexity of the function to be approximated increases. This situation is evident at-the-money333The at-the-money region is the subset of the underlyings’ domain where the option’s strike price is identical to the price given by the combination of the underlyings which defines the derivative contract. For example, the at-the-money region for the arithmetic average basket option is . In this way, the out-the-money region is the domain’s subset where the call (put) option’s strike price is larger (smaller) than the price which defines the derivative contract, and the in-the-money region is its opposite. (ATM), where there is a deterioration of the approximation in the presence of more complex payoff structures. We increase the number of collocation points in subsequent test to deal with this phenomenon.

In addition, we have also observed that the Adam’s performance is suboptimal, in the sense that it comes to a point during training where it gets stuck. To avoid such situation, an adaptive learning rate is introduced in the following tests. We will use the so-called inverse time decay strategy, [33], which follows the construction,

where is the initial learning rate, the learning rate at step , the decay rate and the decay step.

The increase in the problem dimension and in the number of input data also lead to a general increase in the time needed to perform the training, specially for the L-BFGS optimization step. Therefore, for the rest of the experiments in this work, we choose the combination of layers and units per layer, since it achieves relative errors very close to the best obtained, being about faster than the choices with less error, see Table 5(d). This setting has, in the best cases, a relative error of , and for the , and norms, respectively.

In order to evaluate the performance of our training algorithm for the risky non-linear case, a test similar to the one performed in the one-dimensional case is run, now with the residuals given by (39)-(42). For this purpose, we again consider six possible hazard rates, , being the remaining model parameters those given in Table 4. For each case, we do training trials with collocation points () and choose the best of them. We keep the number of Adam steps given before and take , . The number of L-BFGS steps is also maintained. We take, as a reference, the solutions of the boundary value problem (37) obtained via FD with a fixed point scheme to deal with the non-linearity. Examples of this treatment can be found in, e.g., [2], [3] or [17].

| Case | ||||

|---|---|---|---|---|

| Risk-free | ||||

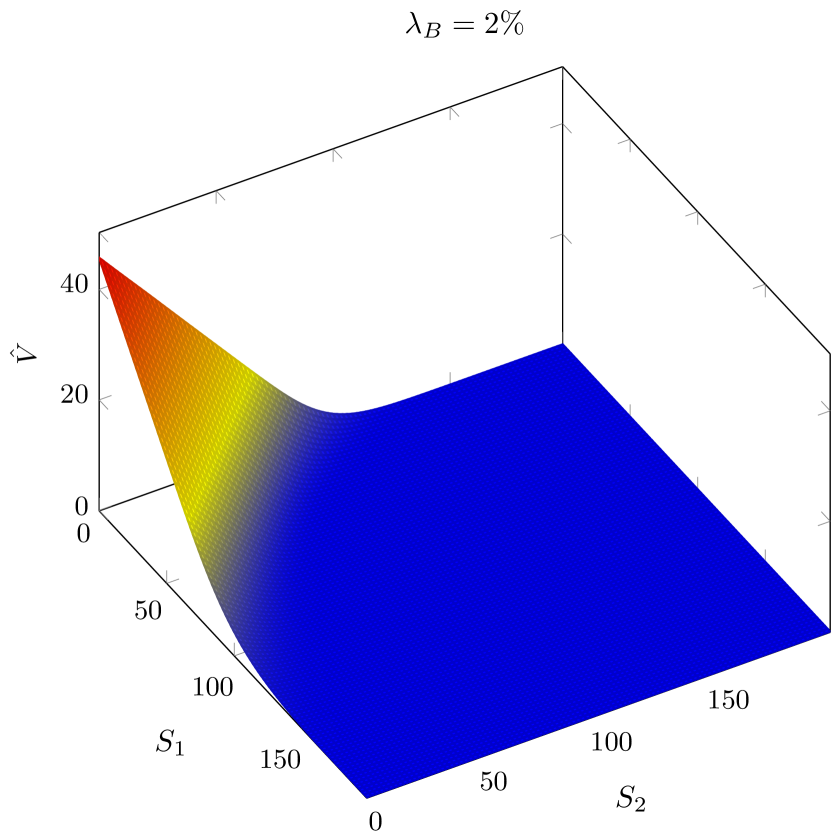

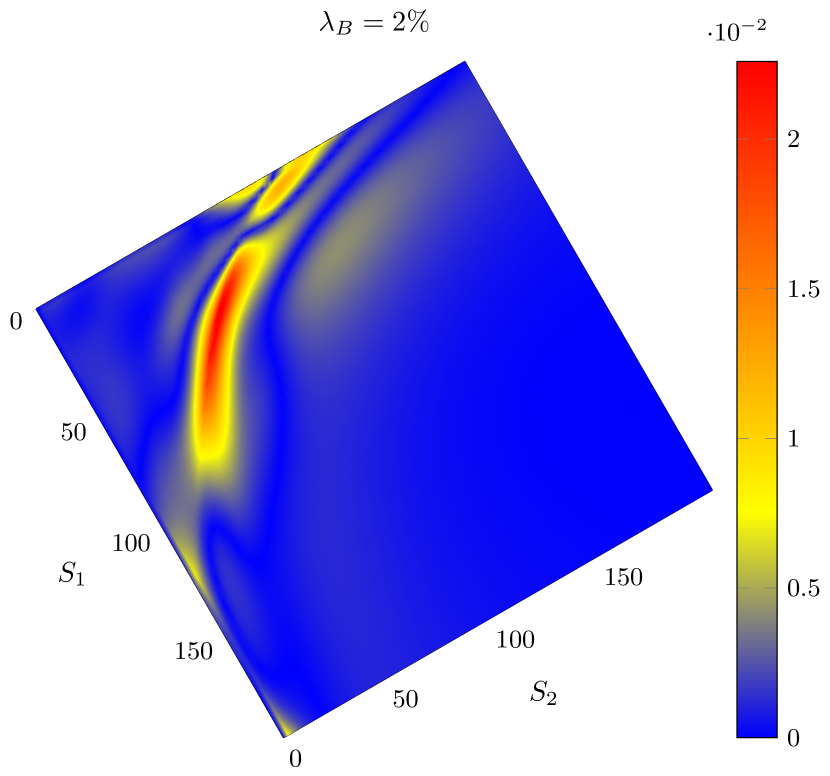

In Figure 3(a) the PINNs solution for the risky arithmetic average put option, with , is plotted; while Figure 3(b) shows the error compared to the reference solution. In order to avoid relative error instabilities due to values close to zero and thus obtain an adequate visualization of such error in the area of interest, its action is limited for option values greater than or equal to . Regions with smaller option values are treated in terms of the absolute error, scaled by the imposed limit. This is sufficient for quantitative finance purposes and it is also followed in the error plots given below.

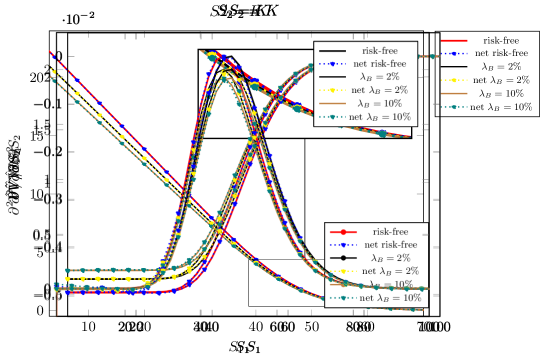

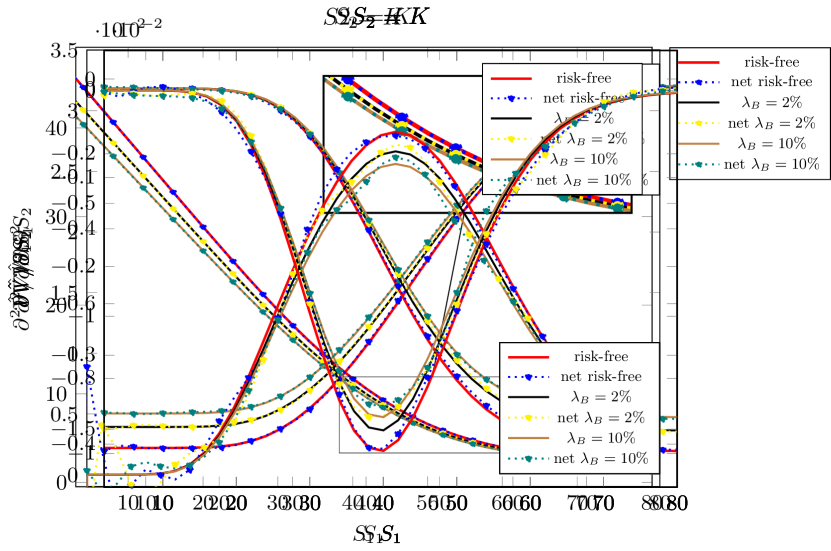

As expected, the largest errors are observed ATM levels and its neighbourhood, as is the case in classical schemes. Even so, the errors in this region are reasonable, being at most of the order of . Figure 4 shows a comparison between reference and network approximated prices in the same spirit as the one given for the previous case. We choose to show only two risky and the risk-free cases because the shorter maturity of the derivative leads to smaller adjustment between each scenario. In addition, slices of the first-order Greeks are added in Figure 5.

It is observed that the solution approximated by the trained ANN has an identical qualitative behaviour in the plotted cases. In the remaining cases, not shown, there are no significant differences to comment on. For the first-order partial derivatives a similar behaviour to that given in the one-dimensional case is observed. They suffer from some slight oscillations near the lower boundaries, but show excellent results in the rest of the domain. In particular, we do not observe a decrease in the relative error compared to that obtained in prices. These facts are also supported by Table 6, which shows the prices and Greeks’ relative error for concrete combinations of and .

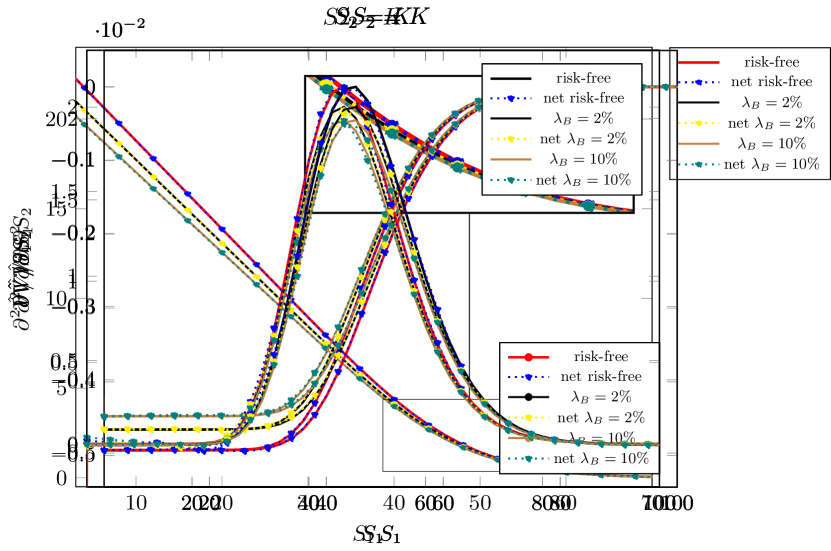

The same test is performed in the case of the worst-of put option, which is of interest in the industry because is a commonly offered product. We keep the test and parameters setup and we use the same methodology used in the arithmetic average case to compute the reference solutions.

In Figure 6(a) the network solution for the risky worst-of put option is plotted, while in Figure 6(b) is shown its error compared with the reference solution, both for the case . The maximum relative error remains in the same order of magnitude seen before and present the same pattern as seen before. Figures 7, 8(a) and 8(b) show the comparison between the reference and network approximated prices and first-order derivatives with respect to the and , respectively. The results are in line with what we would expect from the arithmetic average option case. In general, it is observed that the behaviour of the derivative is influenced by the direction it follows in relation to the ATM region. Thus, better approximations are obtained when they follow the downward direction, while their quality deteriorates in transverse direction. This situation can be seen in the derivative data given in Table 7, where it can be seen that, if , then the error in the derivative with respect to the is greater than the error in the derivative with respect to , obviously both evaluated at .

| Case | ||||

|---|---|---|---|---|

| Risk-free | ||||

5.2.2 Options under the Heston model

Finally, we present the results related to the valuation of options using the Heston model, which is based on the description given in Section 4.2.3. For this purpose, we work with the model data given in Table 8, and we select , , as the truncation values of the domain.

| Heston parameters | |

|---|---|

| Strike, K | |

| Time to maturity, T | |

| Repo rate minus dividend, | |

| Interest rate, | |

| Mean reversion rate, | |

| Mean variance, | |

| Volatility of variance, | |

| Correlation, | |

| xVA parameters | |

| Seller hazard rate, | |

| Counterparty hazard rate, | |

| Seller recovery rate, | |

| Counterparty recovery rate, | |

| Funding spread, | |

We keep the same goal as in the previous cases, namely, the evaluation of the performance of the PINNs algorithm for the Heston’s linear and non-linear case. Therefore, we repeat the previously performed experiments considering a put option, so that the loss function is defined by the residuals (47)-(51). We took a total of collocation points () and set the number of Adam’s steps to , applying the inverse time-decay strategy with and . The number of L-BFGS steps is remains the same. As in the previous cases, the reference solution is computed with FD, adding a fixed point scheme in the risky cases.

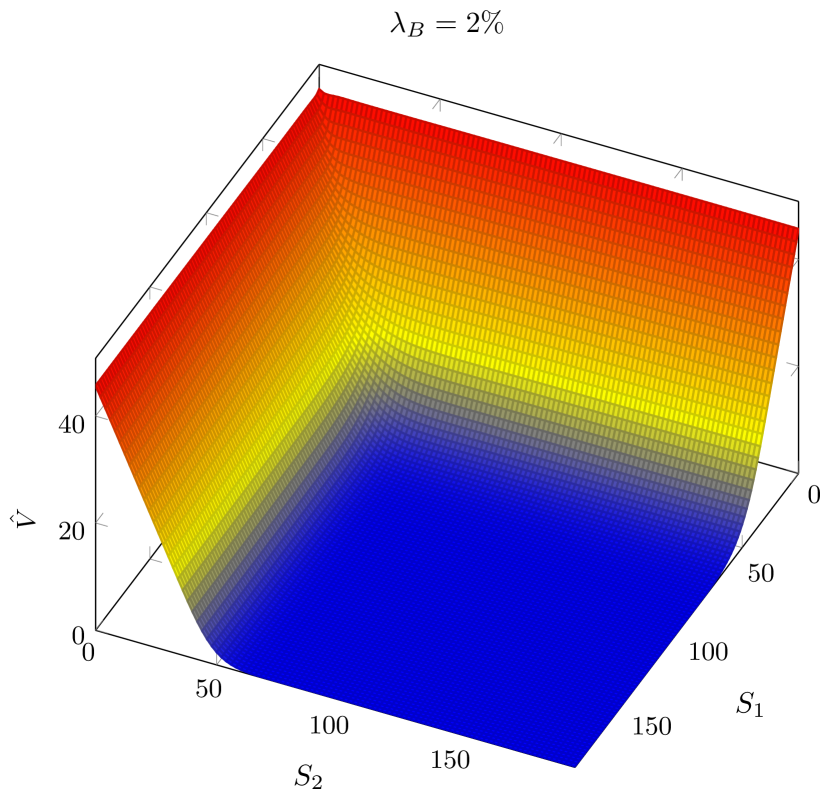

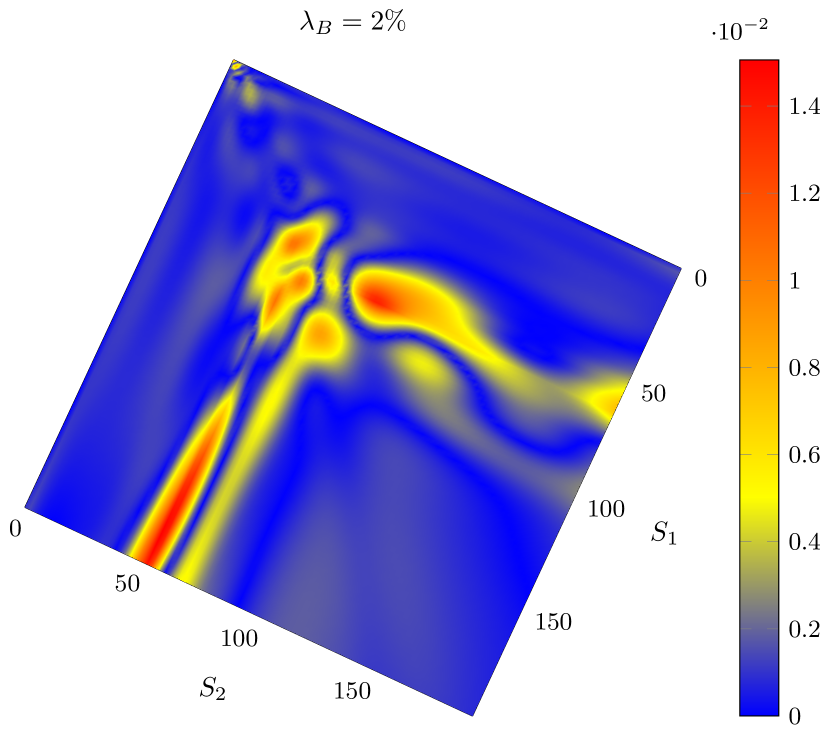

Figure 9 shows the price surface computed by the trained ANN (Figure 9(a)), as well as the errors obtained in relation with respect to the reference solution (Figure 9(b)), for the case . Both the qualitative and quantitative behaviour of the solution achieve the precision standards of the other two-dimensional cases studied above. However, a different distribution of the committed error is observed. In previous cases, the error was concentrated in the ATM region, mostly due to the non-differentiability of the payoff. Now, although we see the expected larger error in the ATM region when the values of are close to zero, it becomes dominant in the OTM region. Such error pattern has also been found in FD algorithms. This fact suggests that the chosen boundary conditions due to the truncation domain could be hampering the accuracy of the approximation.

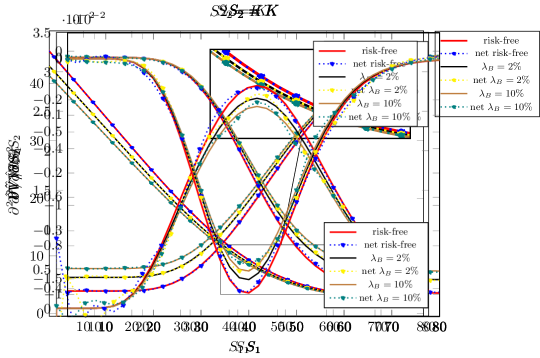

In the Figures 10, 11 and 12, -slices of the solution and its first order derivatives are shown. Such slices correspond to sections with and (values of interest in the industry). As in the examples seen above, the risk-free case and the cases with are considered. In the price plots (Figure 10), a similar performance to that seen in the previous cases can be observed. This results are supported by the Table 9, where the relative errors obtained for the points of interest are shown, achieving, at least, an order of .

For the first-order derivatives, the obtained accuracy is sufficient for financial purposes, although a slight decrease in the performance is found due to the more complex physics described by the PDE. In the case of deltas, Figure 11, the oscillatory behaviour near the boundary seen before is slightly magnified, specially for the risk-free and lower scenarios. However, it is able to perfectly capture its asymptotic behaviour as grows. The approximations around the strike are remarkably good, with relative errors an the order of , see Table 9. Figure 12 shows the vega slices, understanding vega as the derivative of the price with respect to the underlying’s variance444We assume an abuse of language. In reality, vega is understood as the partial derivative with respect to the square root of the variance but, considering fixed- slices, both expressions only differ in being multiplied by a constant.. Regardless of the chosen default scenario, the approximations close to are worse. Moreover, the estimations are affected by the closeness to the boundary , so that the closer you are to such boundary, the lower the accuracy is. However, this effect looses intensity or directly disappears for larger values of . Thus, the same order as that obtained for the deltas is observed in the neighbourhood of the strike, see Table 9, and the asymptotic behaviour is consistent with the Neumann condition imposed on the boundary.

| Case | ||||

|---|---|---|---|---|

| Risk-free | ||||

6 Conclusions

Thanks to the universal approximation property of ANNs and the dramatic increase of computing power of deep learning hardware, PINNs methods have become a serious alternative for solving hard PDE problems. Maybe the biggest weakness of PINNs is the imposition of the boundary conditions, as they enter as addends into the loss function for the network calibration, and the user must choose heuristically the magnitude of the addends that depend, of course, on the type of problem and the type of boundary conditions. These weights are not known a priori, as they depend of the solution itself, and must be estimated in some way, which is also problem dependent.

In this work a novel technique for the treatment of the boundary conditions in the PINNs framework has been introduced. It allows to get ride the heuristic selection of the weights of the boundary addends that appear in the loss function of the ANN that approximates the solution. The strategy is based on the direct evaluation of the differential operator at the boundaries taking into account the imposed boundary conditions. This yields an addend for the boundary that is in the same magnitude of the loss in the interior of the domain, avoiding to deal with the heuristic choice of the weights. To the best of our knowledge this procedure is introduced in this paper for the first time, and we feel that is a very interesting contribution that makes PINNs much more powerful and easier to use.

The new approach has been applied to several non-linear PDE problems that arise in computational finance when CCR is taking into account, although it is general enough and non problem-dependent to be applied in other fields, like for example fluid dynamics or solid mechanics. In particular, it has been employed to solve the boundary value problems related to the pricing of risky European options under the one and two-dimensional Black-Scholes model, as well as under the Heston model. The obtained solutions yield a good accuracy when compared with the analytical or reference solutions. Furthermore, embedding the obtained solution into an ANN has allowed us to compute their relevant partial derivatives by means of AD.

All in all, the partial derivatives’ computation in the PINNs framework is so far a generally unexplored avenue and we believe it may have a lot of potential, being one of the main advantages of PINNs over other deep-learning based methodologies. The optimization procedure takes these quantities into account since they are implicitly part of the loss function, so that under the assumption of having an ideal optimizer, there would be a perfect fit of both the solution and the derivatives that conform the PDE. Another of the most notables advantages is in terms of interpretability. Compared to other techniques, this methodology is closer to the classical PDE schemes, in the sense that the PDE solution is projected onto a space formed by the ANN weights.

Acknowledgements

All the authors thank to the support received from the CITIC research center, funded by Xunta de Galicia and the European Union (European Regional Development Fund - Galicia Program), by grant ED431G 2019/01.

A.L and J.A.G.R. acknowledge the support received by the Spanish MINECO under research project number PDI2019-108584RB-I00, and by the Xunta de Galicia under grant ED431C 2018/33.

References

- [1] M. Abadi, P. Barham, J. Chen, Z. Chen, A. Davis, J. Dean, M. Devin, S. Ghemawat, G. Irving, M. Isard, et al. TensorFlow: A system for large-scale Machine Learning. In 12th USENIX symposium on operating systems design and implementation (OSDI 16), pages 265–283, 2016.

- [2] I. Arregui, B. Salvador, and C. Vázquez. CVA computing by PDE models. In Numerical Analysis and Its Applications, pages 15–24, Cham, 2017. Springer International Publishing.

- [3] I. Arregui, B. Salvador, and C. Vázquez. PDE models and numerical methods for total value adjustment in European and American options with counterparty risk. Applied Mathematics and Computation, 308:31–53, 2017.

- [4] G. Bai, U. Koley, S. Mishra, and R. Molinaro. Physics informed neural networks (PINNs) for approximating nonlinear dispersive PDEs. Journal of Computational Mathematics, 39(6):816–847, 2021.

- [5] M. Bichuch, A. Capponi, and S. Sturm. Arbitrage-free pricing of XVA - Part II: PDE representation and numerical analysis. SSRN Electronic Journal, 02 2015.

- [6] M. Bichuch, A. Capponi, and S. Sturm. Arbitrage-free XVA. Mathematical Finance, 28(2):582–620, 2018.

- [7] L. Bottou, F. E. Curtis, and J. Nocedal. Optimization methods for large-scale machine learning. SIAM Review, 60(2):223–311, 2018.

- [8] D. Brigo, C. Buescu, M. Francischello, A. Pallavicini, and M. Rutkowski. Risk-neutral valuation under differential funding costs, defaults and collateralization. Risk Management and Analysis in Financial Institutions eJournal, 2018.

- [9] D. Brigo, A. Capponi, and A. Pallavicini. Arbitrage-free bilateral counterparty risk valuation under collateralization and application to credit default swaps. Mathematical Finance, 24(1):125–146, 2014.

- [10] D. Brigo, M. Francischello, and A. Pallavicini. Nonlinear valuation under credit, funding, and margins: Existence, uniqueness, invariance, and disentanglement. European Journal of Operational Research, 274(2):788–805, 2019.

- [11] D. Brigo and M. Masetti. Risk-neutral pricing of counterparty risk. Pykhtin (Ed.). London: Risk Books, 2005.

- [12] D. Brigo and A. Pallavicini. Nonlinear consistent valuation of CCP cleared or CSA bilateral trades with initial margins under credit, funding and wrong-way risks. Journal of Financial Engineering, 01(01):1450001, 2014.

- [13] D. Brigo, A. Pallavicini, and V. Papatheodorou. Arbitrage-free valuation of bilateral counterparty risk for interest-rate products: impact of volatilities and correlations. International Journal of Theoretical and Applied Finance, 14(06):773–802, 2011.

- [14] C. Burgard and M. Kjaer. In the balance. Risk journal, pages 72–75, 2011.

- [15] C. Burgard and M. Kjaer. Partial differential equation representations of derivatives with bilateral counterparty risk and funding costs. The Journal of Credit Risk, 7(3):1–19, 2011.

- [16] D. Castillo, A. M. Ferreiro, J. A. García-Rodríguez, and C. Vázquez. Numerical methods to solve PDE models for pricing business companies in different regimes and implementation in GPUs. Applied Mathematics and Computation, 219(24):11233–11257, 2013.

- [17] Y. Chen and C. Christara. Penalty methods for bilateral XVA pricing in European and American contingent claims by a PDE model. Journal of Computational Finance, Forthcoming, 2019.

- [18] U. Cherubini. Counterparty risk in derivatives and collateral policies: The replicating portfolio approach. In L. Tilman, editor, ALM of Financial Institutions. institutional Investor Books, 2005.

- [19] J. C. Cox, J. E. Ingersoll, and S. A. Ross. A theory of the term structure of interest rates. Econometrica, 53(2):385–407, 1985.

- [20] S. Crépey. Bilateral counterparty risk under funding constraints-part II: CVA. Mathematical Finance, 25(1):23–50, 2015.

- [21] S. Crépey. Gaussian process regression for derivative portfolio modelling and application to credit valuation adjustment computations. Risk journal, 24(1):47–81, 2020.

- [22] C. Cuchiero, C. Fontana, and A. Gnoatto. Affine multiple yield curve models. Mathematical Finance, 29(2):568–611, 2019.

- [23] M. De Florio, E. Schiassi, and R. Furfaro. Physics-informed neural networks and functional interpolation for stiff chemical kinetics. Chaos: An Interdisciplinary Journal of Nonlinear Science, 32(6):063107, 2022.

- [24] T. De Ryck, A. D. Jagtap, and S. Mishra. Error estimates for physics informed neural networks approximating the Navier-Stokes equations. arXiv 2203.09346, 2022.

- [25] T. De Ryck and S. Mishra. Error analysis for physics informed neural networks (PINNs) approximating Kolmogorov PDEs. arXiv 2106.14473, 2021.

- [26] T. De Ryck and S. Mishra. Error analysis for deep neural network approximations of parametric hyperbolic conservation laws. arXiv 2207.07362, 2022.

- [27] T. De Ryck and S. Mishra. Generic bounds on the approximation error for physics-informed (and) operator learning. arXiv 2205.11393, 2022.

- [28] T. De Ryck, S. Mishra, and R. Molinaro. wPINNs: Weak physics informed neural networks for approximating entropy solutions of hyperbolic conservation laws. arXiv 2207.08483, 2022.

- [29] M. Dissanayake and N. Phan-Thien. Neural network-based approximations for solving partial differential equations. Communications in Numerical Methods in Engineering, 10(3):195–201, 1994.

- [30] D. Duffie and M. Huang. Swap rates and credit quality. The Journal of Finance, 51(3):921–949, 1996.

- [31] M. Fujii, Y. Shimada, and A. Takahashi. Note on construction of multiple swap curves with and without collateral. SSRN Electronic Journal, 23(02), 2010.

- [32] M. Fujii, Y. Shimada, and A. Takahashi. A market model of interest rates with dynamic basis spreads in the presence of collateral and multiple currencies. Wilmott Journal, 54:61–73, 2011.

- [33] A. Geron. Hands-on machine learning with Scikit-Learn and TensorFlow : Concepts, tools, and techniques to build intelligent systems. O’Reilly Media, Sebastopol, CA, 2017.

- [34] A. Gnoatto, A. Picarelli, and C. Reisinger. Deep xVA solver – A neural network based counterparty credit risk management framework. SSRN Electronic Journal, 2020.

- [35] A. Gnoatto and N. Seiffert. Cross currency valuation and hedging in the multiple curve framework. SIAM Journal on Financial Mathematics, 12(3):967–1012, 2021.

- [36] I. Goodfellow, Y Bengio, and A. Courville. Deep learning. MIT Press, 2016.

- [37] J. Han, A. Jentzen, and E. Weinan. Solving high-dimensional partial differential equations using deep learning. Proceedings of the National Academy of Sciences, 115(34):8505–8510, 2018.

- [38] J. Herb. Options on the maximum or the minimum of several assets. Journal of Financial and Quantitative Analysis, 22(3):277–283, 1987.

- [39] S. L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The review of financial studies, 6(2):327–343, 1993.

- [40] B. Horvath, A. Muguruza, and M. Tomas. Deep learning volatility: a deep neural network perspective on pricing and calibration in (rough) volatility models. Quantitative Finance, 21(1):11–27, 2021.

- [41] B. Huge and A. Savine. Differential machine learning. arXiv 2005.02347, 2020.

- [42] M. Hutzenthaler, A. Jentzen, T. Kruse, T. Anh Nguyen, and P. von Wurstemberger. Overcoming the curse of dimensionality in the numerical approximation of semilinear parabolic partial differential equations. Proceedings Of The Royal Society A, 476, 2020.

- [43] K. J. In ’t Hout and S. Foulon. ADI finite difference schemes for option pricing in the Heston model with correlation. International Journal of Numerical Analysis and Modeling, 7(2):303–320, 2010.

- [44] A. Karpatne, R. Kannan, and V. Kumar. Knowledge-guided machine learning: Accelerating discovery using scientific knowledge and data. Chapman and Hall/CRC, 1st edition, 2022.

- [45] D. P. Kingma and J. Ba. Adam: A method for stochastic optimization. arXiv 1412.6980, 2014.

- [46] T. Kossaczká, M. Ehrhardt, and M. Günther. Enhanced fifth order WENO shock-capturing schemes with deep learning. Results in Applied Mathematics, 12:100201, 2021.

- [47] T. Kossaczká, M. Ehrhardt, and M. Günther. A neural network enhanced WENO method for nonlinear degenerate parabolic equations. Physics of Fluids, 34, 2022.

- [48] I.E. Lagaris, A. Likas, and D. I. Fotiadis. Artificial neural networks for solving ordinary and partial differential equations. IEEE Transactions on Neural Networks, 9(5):987–1000, 1998.

- [49] D. C. Liu and J. Nocedal. On the limited memory BFGS method for large scale optimization. Mathematical programming, 45(1):503–528, 1989.

- [50] S. Liu, A. Leitao, A. Borovykh, and C. W. Oosterlee. On a neural network to extract implied information from american options. Applied Mathematical Finance, 28(5):449–475, 2021.

- [51] Lu Lu, X. Meng, Z. Mao, and G. E. Karniadakis. DeepXDE: A deep learning library for solving differential equations. SIAM Review, 63(1):208–228, 2021.

- [52] A.J. Meade and A.A. Fernandez. The numerical solution of linear ordinary differential equations by feedforward neural networks. Mathematical and Computer Modelling, 19(12):1–25, 1994.

- [53] X Meng, Z Li, D. Zhang, and G. E. Karniadakis. PPINN: Parallel physics-informed neural network for time-dependent PDEs. Computer Methods in Applied Mechanics and Engineering, 370:113250, 2020.

- [54] S. Mishra and R. Molinaro. Estimates on the generalization error of physics-informed neural networks for approximating PDEs. IMA Journal of Numerical Analysis, 2022.

- [55] A. Pallavicini, D. Perini, and D. Brigo. Funding valuation adjustment: a consistent framework including CVA, DVA, collateral, netting rules and re-hypothecation. SSRN Electronic Journal, 2011.

- [56] A. Paszke, S. Gross, S. Chintala, G. Chanan, and E. Yang. Automatic differentiation in PyTorch. Neural Information Processing Systems, Tech. Rep, 2017.

- [57] V. Piterbarg. Funding beyond discounting: collateral agreements and derivatives pricing. Risk Magazine, 23(02):97–102, 2010.

- [58] V. Piterbarg. Cooking with collateral. Risk Magazine, 23(02):58–63, 2012.

- [59] M. Raissi, P. Perdikaris, and G. E. Karniadakis. Physics-informed neural networks: A deep learning framework for solving forward and inverse problems involving nonlinear partial differential equations. Journal of Computational Physics, 378:686–707, 2019.

- [60] C. Randall and D. A. Tavella. Pricing financial instruments: The finite difference method. Wiley, 2000.

- [61] B. Salvador and C. W. Oosterlee. Total value adjustment for a stochastic volatility model. A comparison with the Black-Scholes model. Applied Mathematics and Computation, 391:125489, 2021.

- [62] B. Salvador, C. W. Oosterlee, and R. van der Meer. Financial option valuation by unsupervised learning with artificial neural networks. Mathematics, 9(1), 2021.

- [63] Y. Shin, J. Darbon, and G. E. Karniadakis. On the convergence of physics informed neural networks for linear second-order elliptic and parabolic type PDEs. Communications in Computational Physics, 28(5):2042–2074, 2020.

- [64] N. Srivastava, G. Hinton, A. Krizhevsky, I. Sutskever, and R. Salakhutdinov. Dropout: A simple way to prevent neural networks from overfitting. Journal of Machine Learning Research, 15(1):1929–1958, 2014.

- [65] R. M. Stulz. Options on the minimum or the maximum of two risky assets: Analysis and applications. Journal of Financial Economics, 10(2):161–185, 1982.

- [66] R. van der Meer, C. W. Oosterlee, and A. Borovykh. Optimally weighted loss functions for solving PDEs with neural networks. Journal of Computational and Applied Mathematics, 405, 2022.

- [67] E. Weinan, J. Han, and A. Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics and Statistics, 5:349–380, 2017.

- [68] E. Weinan, M. Hutzenthaler, A. Jentzen, and T. Kruse. Multilevel Picard iterations for solving smooth semilinear parabolic heat equations. Partial Differential Equations and Applications, 2(6), nov 2021.