Tyranny-of-the-minority regression adjustment in randomized experiments

Abstract

Regression adjustment is widely used for the analysis of randomized experiments to improve the estimation efficiency of the treatment effect. This paper reexamines a weighted regression adjustment method termed as tyranny-of-the-minority (ToM), wherein units in the minority group are given greater weights. We demonstrate that the ToM regression adjustment is more robust than Lin, (2013)’s regression adjustment with treatment-covariate interactions, even though these two regression adjustment methods are asymptotically equivalent in completely randomized experiments. Moreover, we extend ToM regression adjustment to stratified randomized experiments, completely randomized survey experiments, and cluster randomized experiments. We obtain design-based properties of the ToM regression-adjusted average treatment effect estimator under such designs. In particular, we show that ToM regression-adjusted estimator improves the asymptotic estimation efficiency compared to the unadjusted estimator even when the regression model is misspecified, and is optimal in the class of linearly adjusted estimators. We also study the asymptotic properties of various heteroscedasticity-robust standard error estimators and provide recommendations for practitioners. Simulation studies and real data analysis demonstrate ToM regression adjustment’s superiority over existing methods.

Key words: cluster randomized experiments, covariate adjustment, design-based theory, randomization-based inference, randomized block experiments, survey experiments

1 Introduction

Since the seminal work of Fisher, (1935), randomized experiments have been the gold standard for drawing causal inference. Complete randomization balances confounding factors on average such that the treatment effects can be identified without untestable assumptions as in observational studies. Different experimental designs have been proposed to improve the efficiency or address practical concerns regarding completely randomized experiments. For example, stratified randomized experiments further balance important discrete covariates and improve the efficiency of treatment effect estimation (Fisher,, 1926; Imai et al.,, 2008; Imbens and Rubin,, 2015). Cluster randomized experiments are conducted when the individual-level treatment assignment is logistically unrealistic or when there are concerns regarding interference within clusters (Hayes and Moulton,, 2017). Completely randomized survey experiments address the lack of generalizability of completely randomized experiments (Imai et al.,, 2008; Yang et al.,, 2021).

Regression adjustment is widely used during the analysis stage to utilize covariate information to improve efficiency. Fisher, (1935) used covariates by adding them directly in the linear regression of outcome on treatment indicator and estimated the average treatment effect using the ordinary least squares (OLS). However, Freedman, (2008) criticized this practice by demonstrating that this may degrade efficiency compared to the simple difference-in-means estimator under an unbalanced design or in the presence of heterogeneity between treatment and control groups. Echoing the critique of Freedman, (2008) and to fix the efficiency loss issue, Lin, (2013) recommended the addition of both covariates and treatment-covariate interactions in the regression adjustment. Since then, Lin’s with-interaction regression adjustment has witnessed significant advances in the field of causal inference (Bloniarz et al.,, 2016; Liu and Yang,, 2020; Li and Ding,, 2020; Ma et al.,, 2022; Zhao and Ding, 2021a, ; Su and Ding,, 2021; Liu et al.,, 2021; Lei and Ding,, 2021; Zhao and Ding, 2021b, ; Liu et al.,, 2022; Lu et al.,, 2022; Zhao and Ding, 2022a, ; Zhao and Ding, 2022b, ).

However, practitioners may be wary of using the with-interaction regression adjustment because it doubles the degrees of freedom used for the coefficients of covariates (Schochet et al.,, 2021; Negi and Wooldridge,, 2021). Although this regression adjustment method can be extended to other experimental designs, it may degrade the efficiency compared to the unadjusted estimator (Ma et al.,, 2022; Liu and Yang,, 2020; Liu et al.,, 2021, 2022). One strategy to remedy this issue is to approach covariate adjustment from the perspective of projection or conditional inference and plug-in unknown projection coefficients using several regressions (Yang et al.,, 2021; Liu et al.,, 2021; Wang et al.,, 2021); however, this is more complicated and less robust than the weighted regression adjustment introduced later (see our simulation results). Additionally, heteroskedasticity-robust variance estimators from Lin’s with-interaction regression adjustment can be anti-conservative, under the superpopulation framework (Negi and Wooldridge,, 2021; Zhao and Ding, 2021a, ), completely randomized survey experiments (Yang et al.,, 2021), or when the dimension of covariates is relatively large compared to the sample size (Lei and Ding,, 2021).

Lin, (2013) discussed a weighted regression adjustment method named tyranny-of-the-minority (ToM), which embodies the principle of giving more weights to the units in the minority group. This method saves half of the degrees of freedom and is asymptotically equivalent to the with-interaction regression adjustment in completely randomized experiments (Lin,, 2013). However, Lin, (2013) and other follow-up research have not assessed the robustness of the method in completely randomized experiments and potential application in other experimental designs.

To address the gap and drawbacks of the with-interaction regression adjustment, we re-examine the ToM regression adjustment method in completely randomized experiments. We demonstrate the robustness of the ToM regression-adjusted average treatment effect estimator using theoretical justifications and simulation studies. Simulation results reveal that ToM regression adjustment dramatically enhances the estimation efficiency and inference reliability when the design is away from balance or the number of covariates is relatively large compared to the sample size.

ToM regression adjustment can be applied under other experimental designs to enhance the efficiency. We illustrate its use and design-based properties in stratified randomized experiments, completely randomized survey experiments, and cluster randomized experiments. Under mild moment conditions, we show that the ToM regression-adjusted average treatment effect estimator is asymptotically normal and optimal in the class of linearly adjusted estimators for each of the aforementioned experimental designs. Moreover, we study the asymptotic properties of various heteroscedasticity-robust standard error estimators. Our analysis is design-based, that is, the analysis is conducted by conditioning on the potential outcomes and covariates, along with treatment assignment as the only source of randomness. Our theoretical results allow the linear regression model to be arbitrarily misspecified. Finally, we conduct simulation to evaluate the finite-sample performance of the ToM regression-adjusted estimator. Simulation results demonstrate the superiority of the ToM regression-adjusted estimator compared to existing estimators. Based on the theoretical and finite-sample results, we provide practical suggestions for choosing point and variance estimators to analyze the experimental results. These suggested estimators can be conveniently obtained using off-the-shelf statistical software packages.

The remaining paper is structured as follows. In Section 2, we introduce ToM regression adjustment in the context of completely randomized experiments and compare it with Lin’s with-interaction regression adjustment to assess its robustness. In Section 3, we extend the application of ToM regression adjustment under stratified randomized experiments, demonstrating its optimality for this design. In Section 4, we extend ToM regression adjustment and demonstrate its optimality for completely randomized survey experiments. In Section 5, we conduct simulation to compare the finite-sample performance of ToM regression adjustment with that of the existing methods. In Section 6, we use ToM regression adjustment to analyze two real datasets. We discuss the combination of ToM regression adjustment and rerandomization in Section 7 and conclude the paper in Section 8. The application of ToM regression adjustment under cluster randomized experiments and proofs are provided in the Supplementary Material.

2 ToM regression adjustment in completely randomized experiments

2.1 Notation and framework

Consider a completely randomized experiment with units. We randomly assign units to the treatment group and to the control group, with . Let be the treatment indicator of the th unit with when it is assigned to the control group and when it is assigned to the treatment group. By design, . Let and be the set of units in the treatment and control groups, respectively. We use to denote the potential outcome of unit under treatment , for , with as the observed outcome. Let be the covariates of unit of length . In a realized experiment, we observe . We consider a design-based or randomization-based inference framework, under which are all fixed finite-population quantities and treatment assignment, , is the only source of randomness. Throughout the study, we assume the validity of the stable unit treatment value assumption (SUTVA) (Rubin,, 1980).

Let be the unit-level treatment effect. We are interested in the population average treatment effect . An unbiased estimator of is the difference in the observed means of the potential outcomes in the treatment and control groups (Imbens and Rubin,, 2015), which is referred to as the “difference-in-means” estimator:

We use the following notation. Let and be the population means of potential outcomes and covariates, respectively. The population variances and covariances are defined as

Let be the infinity norm of a vector. Let denote the ordinary least squares (OLS) regression of on with an intercept. Let denote the weighted least squares (WLS) regression of on with an intercept and weight .

2.2 Regression without and with treatment-covariate interactions

The covariates may be predictive of the potential outcomes. The difference-in-means estimator does not use the covariate information, which negatively affects the efficiency. Regression adjustment is widely used at the analysis stage to improve the efficiency by adjusting for the covariate imbalance between the treatment and control groups.

The difference-in-means estimator can be derived as the OLS estimator of the coefficient of in the regression . Thus, the easiest way of using covariates, which dates back to Fisher, (1935), is to directly add in the regression formula, The resulting regression-adjusted average treatment effect estimator is the OLS estimator of the coefficient of . We refer to this regression method as “Fisher’s regression.” Fisher’s regression has been constantly used in observational studies (Sloczynski,, 2018), completely randomized experiments (Negi and Wooldridge,, 2021), cluster randomized experiments (Schochet et al.,, 2021), and so on.

Freedman, (2008) criticized Fisher’s regression for its lack of guarantee regarding the improvement in efficiency compared to the difference-in-means estimator under unbalanced design or in the presence of heterogeneity between treatment and control groups. Echoing the critique of Freedman, (2008), Lin, (2013) discussed the possibility of remedying this problem by adding the treatment-covariate interactions in the regression,

| (1) |

The OLS estimator of the coefficient of , denoted by , is used as the average treatment effect estimator. Note that the covariates must be centered in the interaction term.

Schochet et al., (2021) pointed out that, to include the interaction term, we risk the loss of the degrees of freedom that could seriously reduce power. Researchers may feel uncomfortable in the absence of sufficient degrees of freedom in a with-interaction model that analyzes experiments with 20–100 units, such as clinics and schools, which is very common in development economics (Negi and Wooldridge,, 2021). In the same paper, Lin, (2013) commented on the ToM regression and demonstrated its asymptotic equivalence to the with-interaction regression for point estimation. However, most of the follow-up work focused on Fisher’s regression and Lin’s with-interaction regression. ToM regression was barely studied. Consequently, it is essential to re-examine ToM regression because it saves half of the degrees of freedom with respective to covariates.

2.3 ToM regression

ToM regression accounts for the drawback in Fisher’s regression by giving larger weights to the units in the minority group. This regression-adjusted estimator is derived as the WLS estimator of the coefficient of in the regression of on with weights , where and are the proportions of units assigned to the treatment and control groups, respectively. We denote the WLS regression as

| (2) |

Remark 1.

Lin, (2013) used the following weights: . These are equivalent to the weights ’s. We use ’s because they can be conveniently extended to other experimental designs.

Lin, (2013) observed that and have the same asymptotic distribution. In the remaining of this section, we demonstrate the optimality of , derive the asymptotic property of its heteroskedasticity-robust standard error, and show that is more robust than through the perspectives of calibrated estimator and leverage score.

In fact, all regression-adjusted estimators are linearly adjusted estimators, with the following form in completely randomized experiments: where and is some adjusted vector. Let correspond to linearly adjusted estimator with minimum sampling variance, that is, . As shown by Li and Ding, (2017), the covariance of is

Simple calculation gives and . It has been shown that has the same asymptotic distribution as the optimal linearly adjusted estimator (Lin,, 2013; Li et al.,, 2018; Li and Ding,, 2020). Under mild conditions, Lin, (2013) showed that and have the same asymptotic distribution, and therefore are both optimal. Proposition 1 presented below indicates this property.

Assumption 1.

As , for , (i) has a positive limit; (ii) , , , have finite limits, the limit of is positive and the limit of is nonsingular; and (iii) , .

Proposition 1.

Under Assumption 1, both and are asymptotically normal with zero mean and variance .

The heteroskedasticity-robust standard errors (Huber,, 1967; White,, 1980) are frequently used to approximate the true asymptotic standard errors and can be conveniently obtained by standard statistical software packages. The classical linear regression literature suggests different ways of correcting the degrees of freedom loss, which leads to . corresponds to the heteroskedasticity-robust standard error without correction. We have included the explicit formulas of in the Supplementary Material.

Let be the heteroscedasticity-robust standard error of of regression (2) corresponding to . Theorem 1 below depicts the conservativeness of the heteroscedasticity-robust standard error.

Theorem 1.

Let be the th quantile of a standard normal distribution. We can construct Wald-type () confidence intervals of :

whose asymptotic coverage rates are greater than or equal to .

Remark 2.

Let be the heteroscedasticity-robust standard error of in the with-interaction regression . Li and Ding, (2020) and Lei and Ding, (2021) showed that, under Assumption 1,

Since

produces a more conservative inference than . However, may produce a finite-sample confidence interval with coverage probability lower than the nominal level when the design is not balanced or the number of covariates is relatively large compared to the sample size; see Lei and Ding, (2021) and Section 5. Meanwhile, the classic Neyman-type variance estimator for the difference-in-means estimator is asymptotically equal to . Since

still improves the inference efficiency compared to the classic Neyman-type variance estimator.

ToM regression is more robust than the with-interaction regression because of the following two reasons. First, both and are special cases of calibrated estimators of the form , where ’s are the calibrated weights (Deville and Särndal,, 1992; Deville et al.,, 1993). Let be the sample mean of under treatment . As presented in the proof of Theorem 2, the calibrated weights for are

In contrast, the calibrated weights for are

We use and to denote the vector of ’s and ’s, respectively.

The non-calibrated weights used for the difference-in-means estimator are for units in the treatment arm . Although both and are asymptotically optimal, the calibrated weights of are not satisfactory. For example, negative or large weights may occur, which affect the robustness of the regression-adjusted treatment effect estimator. Deville and Särndal, (1992) proposed a distance between the calibrated and non-calibrated weights to measure the calibrated weights’ robustness. For complete randomization, the distance measure is derived as

Here is the distance between the ratio of the calibrated and non-calibrated weights and . Large value of suggests the existence of extreme calibrated weights. Theorem 2 below indicates that is better than in the sense of embodying non-extreme calibrated weights. In other words, makes fewer changes to the calibrated weights than to achieve the same level of efficiency improvement.

Theorem 2.

Second, for model-based inference, Huber, (2004) observed that the inverse of leverage score measures the number of units required to determine the fitted value of . The gross error is not reflected in the residuals of high leverage score points. Leverage score also plays an important role for design-based inference. High leverage score negatively affects the asymptotic theory and corresponding inferences (Dorfman,, 1991; Lei and Ding,, 2021). Theorem 3 below indicates that is better than in terms of having smaller leverage score.

Theorem 3.

Leverage scores in the with-interaction regression are

In contrast, leverage scores in ToM regression are

Moreover, for ,

Because cluster randomized experiments can be viewed as complete randomized experiments at the cluster level, we obtained results that correspond to cluster randomized experiments; see the Supplementary Material for more details. In the following two sections, we extend ToM regression to stratified randomized experiments and completely randomized survey experiments, respectively.

3 ToM regression adjustment in stratified randomized experiments

Stratified randomized experiments are a combination of several completely randomized experiments conducted independently in each stratum. It is natural to extend ToM regression adjustment to this experimental design. For simplicity, we use the same to denote covariate dimension. Consider a stratified randomized experiment with strata. We use index to denote quantities with respect to population in stratum , which leads to the stratum-specific analogs of , , , , , , , , , denoted by , , , , , , , , . Throughout this section, we assume that for all . We use double index to denote unit in stratum . Let , , , and be the potential outcomes, observed outcome, unit-level treatment effect, covariates, and treatment indicator of unit , respectively. Denote the total population size by and the proportion of population size of stratum by . The average treatment effect is

| (3) |

where is the average treatment effect in stratum .

Replacing in equation (3) by its unbiased estimator

we obtain an unbiased estimator of , . As demonstrated by Liu and Yang, (2020), is the OLS estimator of the coefficient of in the following regression:

where is the stratum indicator, if and otherwise.

The straightforward extension of Lin’s with-interaction regression to stratified randomized experiments is as follows:

However, it can be showed that this regression-adjusted estimator, that is, the OLS estimator of the coefficient of , guarantees the improvement of efficiency if the following Assumption 2 is true. Otherwise, it may degrade the efficiency.

Assumption 2.

(i) Propensity scores are the same across strata, that is, for all , (ii) or for all .

Equal propensity scores can be ensured across strata through the design; however, Assumption 2(ii) may be unrealistic in many stratified randomized experiments. To remedy this condition, Liu and Yang, (2020) proposed the following weighted regression:

where . They demonstrated that the resulting regression-adjusted estimator can guarantee the improvement of efficiency without Assumption 2(ii); however, Assumption 2(i) must still hold true. In this section, we apply ToM regression adjustment to stratified randomized experiments and demonstrate that this regression-adjusted estimator, denoted by , improves the efficiency without Assumption 2.

We define as the WLS estimator of the coefficient of in the following weighted regression:

| (4) |

with weights

Remark 3.

Although the weights seem like a straightforward extension of to stratified randomized experiments, only can guarantee the improvement of efficiency and optimality of . Moreover, when for , ’s are asymptotically equivalent to ’s.

Let with . We define linearly adjusted estimator as for some adjusted vector . By Wang et al., (2021, Proposition 2), has mean zero and covariance matrix

Let be the optimal linear projection coefficient defined as . Through simple calculation, we obtain , with .

To investigate the asymptotic normality and optimality of , we require Assumption 3 below.

Assumption 3.

As , for ,

-

(i)

for some constant independent of ;

-

(ii)

, , , have limiting values, the limit of is positive and the limit of is nonsingular;

-

(iii)

, .

Assumption 3 is quite general, with few requirements related to the number of strata, stratum sizes, and propensity scores across strata.

Theorem 4.

Under Assumption 3, is asymptotically normal with zero mean and variance . Moreover, is optimal with minimum asymptotic variance in the class of linearly adjusted estimators .

Let denote the variance estimator of from the regression formula (4) corresponding to . Theorem 5 below presents the asymptotic property of .

Theorem 5.

The variance of can be derived by replacing by in the formula of . The optimality of implies that

| (6) |

Equations (5) and (6) indicate that is an asymptotic conservative estimator of . Since , is also a conservative estimator. Therefore, the Wald-type confidence intervals

have asymptotic coverage rates greater than or equal to .

Remark 4.

can be anti-conservative and produce invalid confidence intervals. See the Supplementary Material for more details.

4 ToM regression adjustment in completely randomized survey experiments

Survey experiments usually comprise two stages: random sampling of units from a target population and random assignment of treatments to the sampled units. These experiments are widely used for estimating treatment effect of a target population (Imai et al.,, 2008). The standard survey experiments, completely randomized survey experiments, conduct simple random sampling without replacement to obtain a subset of units before assignment of sampled units through complete randomization into different treatment arms; see, for example Imbens and Rubin, (2015, chap. 6) and Yang et al., (2021).

In a completely randomized survey experiment, suppose units in the experiment are a simple random sample without replacement from a target population of size , with sampling fraction . When , it reduces to the completely randomized experiment. Let and be the sampling indicator and treatment assignment indicator with if unit is sampled, and otherwise, and if unit is assigned to the treatment group, and otherwise. Denote the set of the sampled units by . By design, is not defined if . Let be the observed potential outcome for the sampled unit . The average treatment effect of interest in completely randomized survey experiments is . The difference-in-means estimator is an unbiased estimator of (Imbens and Rubin,, 2015; Yang et al.,, 2021). Here and are the (fixed) numbers of treated and control units, respectively. Let ().

We can observe two kinds of covariates: () which is available at the sampling stage and usually collected from baseline survey conducted by some investigators or previous studies on the same target population, and which is available at the treatment assignment stage and usually collected after the experiment units are sampled. Here, can be a subset of .

By a slight abuse of the notation, we define the following finite-population quantities of the units. We use , , , to denote corresponding finite-population variances and , , , , to denote the corresponding finite-population covariances. Let , , be the finite-population means.

To motivate the form of weighted regression adjustment, we consider a general form of linearly adjusted estimator proposed by Yang et al., (2021):

where

The linearly adjusted estimator adjusts two kinds of covariate imbalances: the difference between the sample mean and population mean of the covariates measured by , and the difference between the covariate means in the treatment and control groups measured by . Note that is equal to the difference-in-means estimator applied to the observed adjusted potential outcomes,

| (7) |

Equation (7) catalyzes the use of covariates and in the regression adjustment. Therefore, we propose a WLS regression adjustment of the following form

| (8) |

with weights . Define as the estimated coefficient of through the WLS.

Remark 5.

Note that the regression formula only needs to center at its finite-population mean . In practice, it is very difficult to collect and for the units that are not in the sample, that is, . Fortunately, is still available from some baseline surveys. Thus, ToM regression adjustment is still applicable.

By Yang et al., (2021, Lemma B1), has mean zero and covariance

The optimal projection coefficients and produce the minimum variance,

Under Assumption 4 below, we demonstrate the asymptotic normality and optimality of in Theorem 6.

Assumption 4.

As , for ,

-

(i)

has a limit in and has a limit in ;

-

(ii)

, , , , , have finite limits, and the limit of is positive while the limits of and are nonsingular;

-

(iii)

, , .

Theorem 6.

Under Assumption 4, is asymptotic normal with zero mean and variance . Moreover, is optimal with minimum asymptotic variance in the class of linearly adjusted estimators .

We can estimate the variance of by the heteroscedasticity-robust standard error. Let denote the variance estimator of from the regression formula (8) corresponding to .

Theorem 7.

It is easy to show that can be derived by replacing by the adjusted potential outcome in the formula of . The optimality of implies that

| (10) |

where

Equations (9) and (10) indicate that is an asymptotic conservative estimator of , and thus an asymptotic conservative estimator of . Therefore, the Wald-type confidence intervals

have asymptotic coverage rates greater than or equal to .

With the assumption that the units are a random sample from an infinite superpopulation, Negi and Wooldridge, (2021) demonstrated that the variance estimator constructed by the with-interaction regression is anti-conservative if the covariates are not centered at their finite-population mean but at their sample mean which introduces an extra variability. This conclusion holds for completely randomized survey experiments with . In practice, is often not available; consequently, the with-interaction regression adjustment is not applicable for . In contrast, ToM regression adjustment does not require the centering of covariates at . The resulting point estimator is consistent and asymptotically normal and the variance estimator is asymptotically conservative regardless of .

5 Numerical studies

In this section, we compare the finite-sample performance of the point estimator and variance estimator derived by ToM regression adjustment with existing competitors in the literature in completely randomized experiments, stratified randomized experiments, and completely randomized survey experiments.

5.1 Complete randomized experiments

In his seminal paper, Lin, (2013) demonstrated the equivalence of with-interaction regression adjustment and ToM regression adjustment in a low-dimensional and large-sample setting that the asymptotic theory works perfectly. In this section, we consider a relatively large dimension of covariates compared to the sample size. We further investigate how “imbalance in information” between treatment and control groups can influence the performance of the estimators, which is reflected by and the signal-to-noise ratio defined later.

We set and generate data using the following model:

| (11) |

where has independent and identically distributed (i.i.d.) entries generated from , -distribution with three degrees of freedom, for . Thus, there is heterogeneity between treatment and control groups. The covariates ’s are realizations of independent random vectors drawn from with (), where if , and otherwise. The errors ’s are realizations of i.i.d. normal random variables with zero mean and variance fulfilling a given signal-to-noise ratio , that is, ratio of the finite-population variance of to that of . After generation, are fixed. The treatment assignment stage assigns units to the treatment group and a completely randomized experiment is simulated times.

We focus on the root mean squared errors (RMSE) of point estimators and empirical coverage probabilities of confidence intervals. We vary the , , and in each scenario. Table 1 presents the values of the factors considered in the simulation. Each scenario is repeated under different random seeds.

| completely randomized experiments | ||

|---|---|---|

| random seed | ||

| stratified randomized experiments | strata | |

| random seed | ||

| completely randomized survey experiments | random seed | |

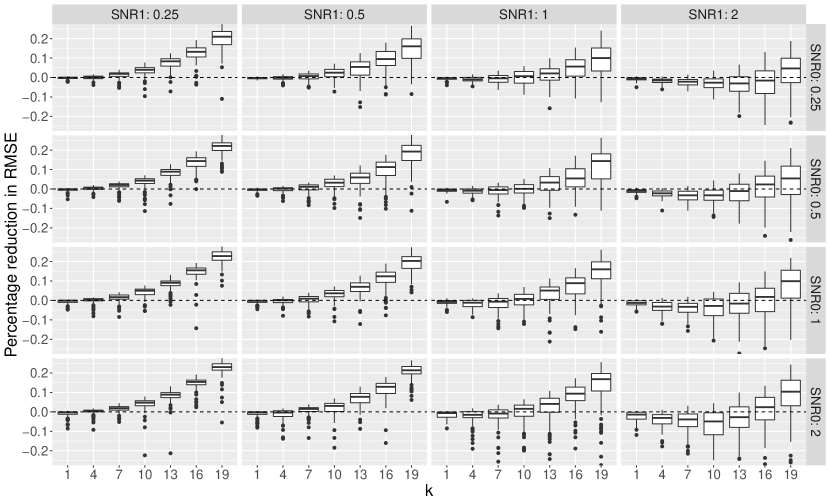

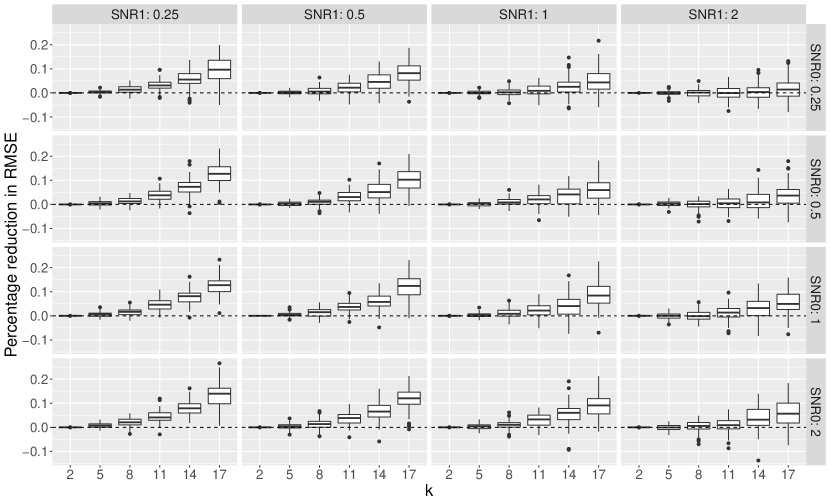

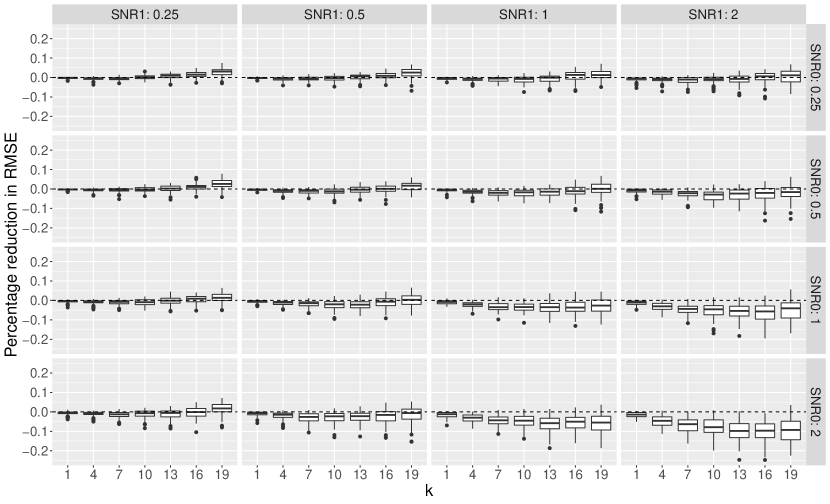

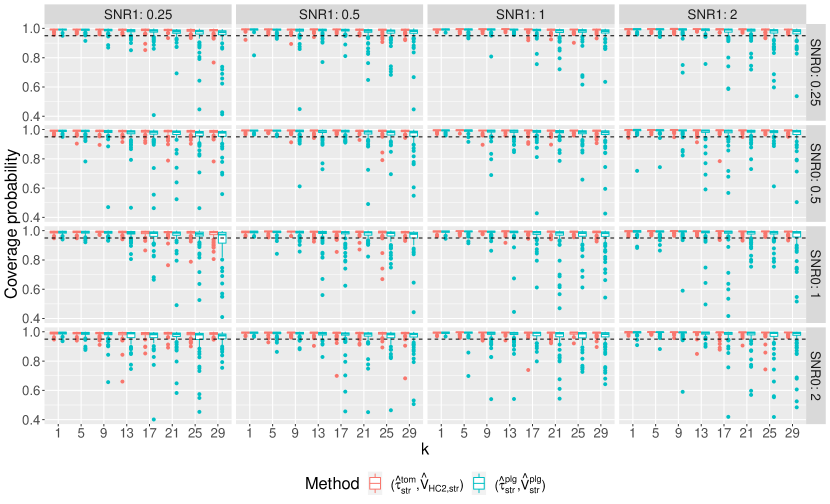

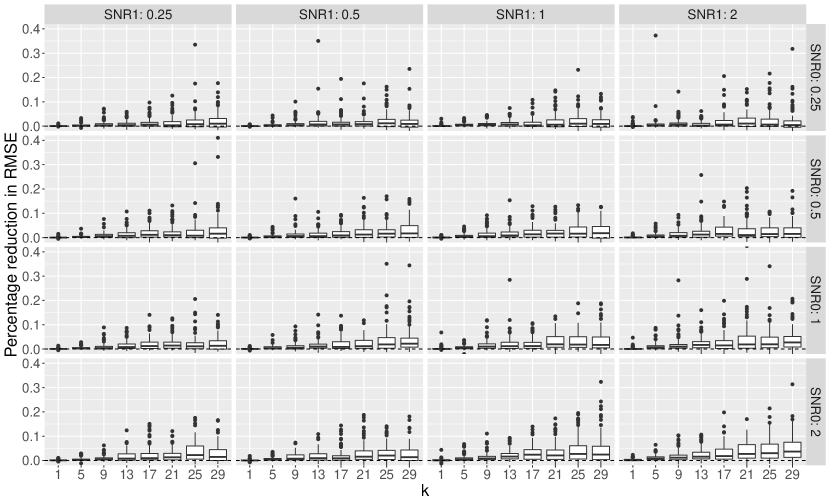

Figure 1 depicts the percentage reduction in RMSE of versus , that is, when . The results for are provided in the Supplementary Material. It can be observed that the RMSE of is overall smaller than that of and the percentage reduction in RMSE increases as becomes larger. ToM regression-adjusted estimator is clearly advantageous when the majority group (control group) has a larger SNR and the minority group (treatment group) has a smaller SNR. This is because uses the data from both groups in a pooled fashion, with larger weights bestowed to the minority group and in a separate fashion with equal weights. Therefore, the performance of heavily depends on how well it estimates the adjusted coefficient in the minority group. When the minority group has a small SNR, the adjusted coefficient may be poorly estimated by .

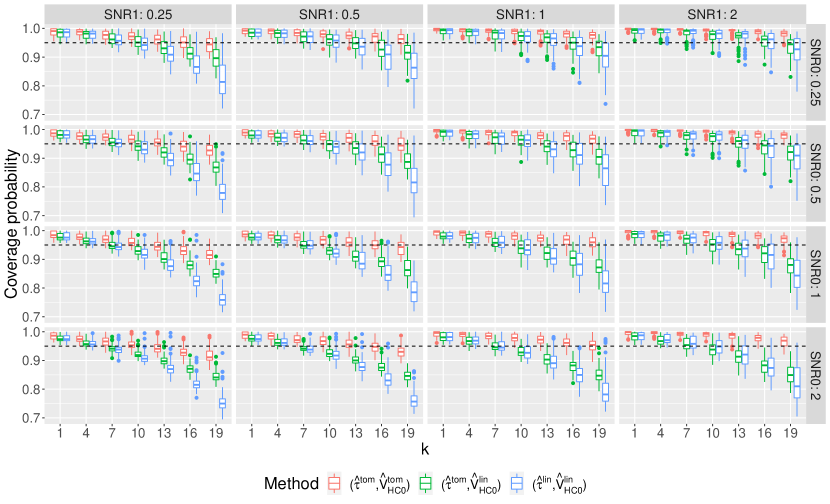

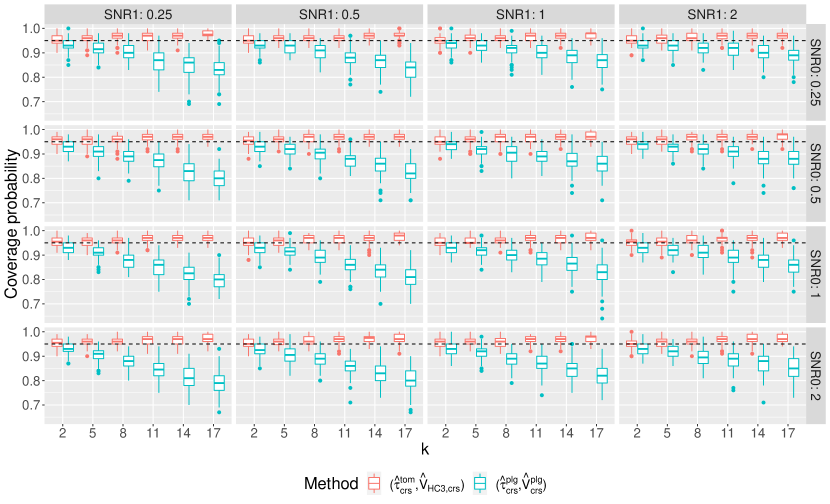

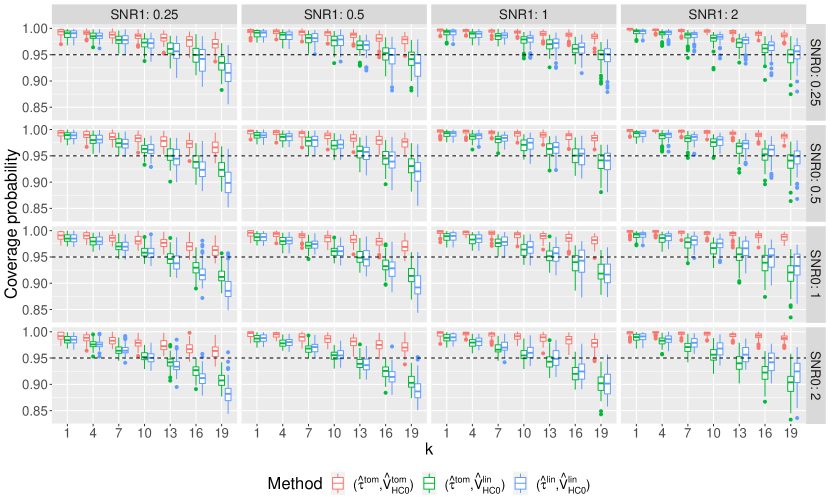

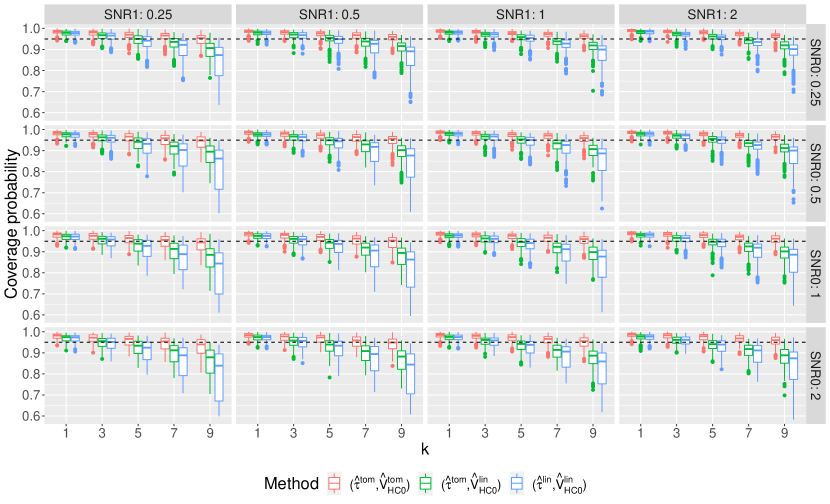

Figure 2 depicts the coverage probabilities of confidence intervals constructed by , , and when . It can be observed that these three methods tend to have worse coverage probabilities when becomes larger. Combination of is the most robust under all scenarios. Similar results were observed by Lei and Ding, (2021): tends to underestimate the variance for large . In contrast, provides a better variance estimation for large . Combination of has larger coverage probabilities on average than when is large. Therefore, its use is recommended. If one prefers a less conservative inference when is small, combination of is recommended. Moreover, all combinations have better coverage probabilities if the minority group has a larger SNR and majority group has a smaller SNR. In contrast, all combinations have worse coverage probabilities if the minority group has a smaller SNR and majority group has a larger SNR.

5.2 Stratified randomized experiments

We consider three kinds of strata size distributions: (1) many small strata (MS); (2) a few large strata (FL); and (3) many small strata compounded with a few large strata (MS+FL). For each scenario, strata sizes are generated as independent samples with (1) from uniform distribution on ; (2) from uniform distribution on ; and (3) with strata sizes from uniform distribution on and strata sizes from uniform distribution on .

The potential outcomes are generated from the following random effect model:

where the intercepts and slopes are generated by and with and embodying i.i.d. entries generated from and standard normal distribution, respectively. The covariates ’s are realizations of independent random vectors of length from with . ’s are realizations of i.i.d. normal random variables with zero mean and variance fulfilling a given signal-to-noise ratio , that is, the ratio of the finite-population variance of to that of .

We ensure at least two units in each treatment arm for each stratum. The number of units assigned to treatment ’s are generated by truncated at and , where ’s are i.i.d. samples from Beta distribution . We vary the strata size distribution, , and in each scenario. Values of these factors are presented in Table 1. Each scenario is repeated under random seeds. For each seed and each scenario, we simulate the stratified randomized experiments times and compute the empirical RMSE of point estimators and empirical coverage probabilities of confidence intervals.

So far, Lin’s with-interaction regression adjustment has not been extended to stratified randomized experiments. Therefore, we consider constructing point and variance estimators from the conditional inference or projection perspective and using a plug-in principle (Yang et al.,, 2021; Wang et al.,, 2021; Liu et al.,, 2021). Recall that the optimal linearly adjusted coefficient is . Let , , , and be the sample analogs of , , , and . We estimate by with

Therefore, can be estimated by . The plug-in principle is also used to estimate the normal component’s variance in the asymptotic distribution of under stratified rerandomization (Wang et al.,, 2021). This is equal to the variance of the optimal linearly adjusted estimator . We follow their procedure to derive a conservative variance estimator of ,

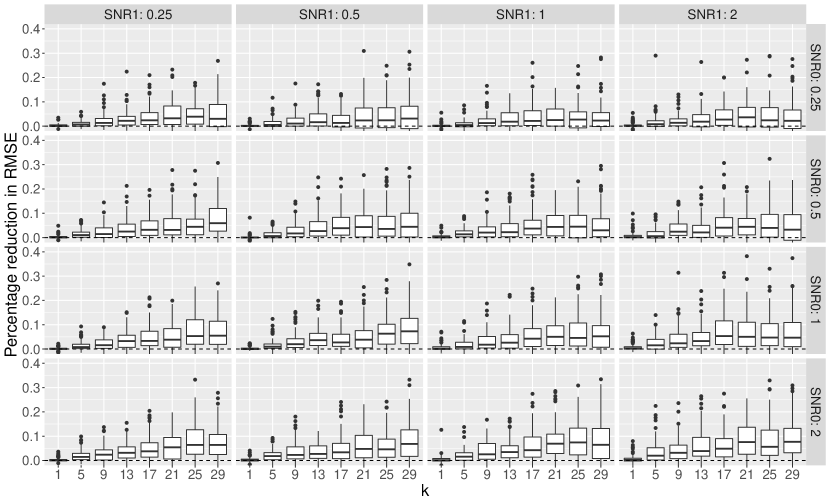

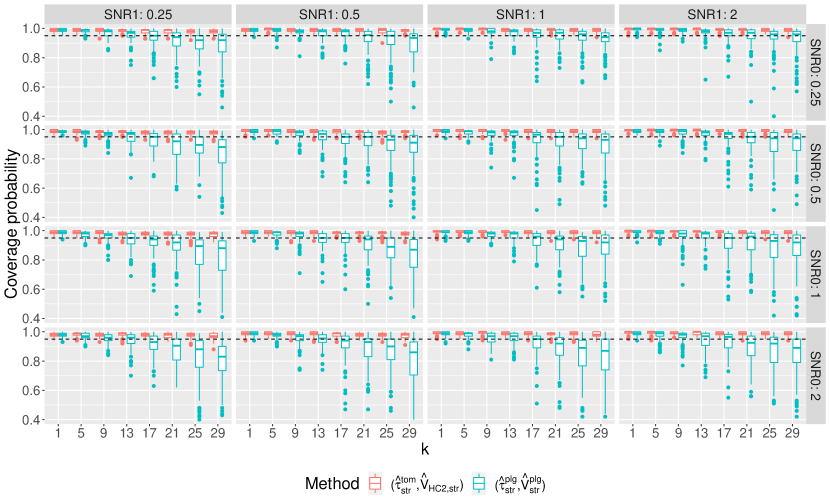

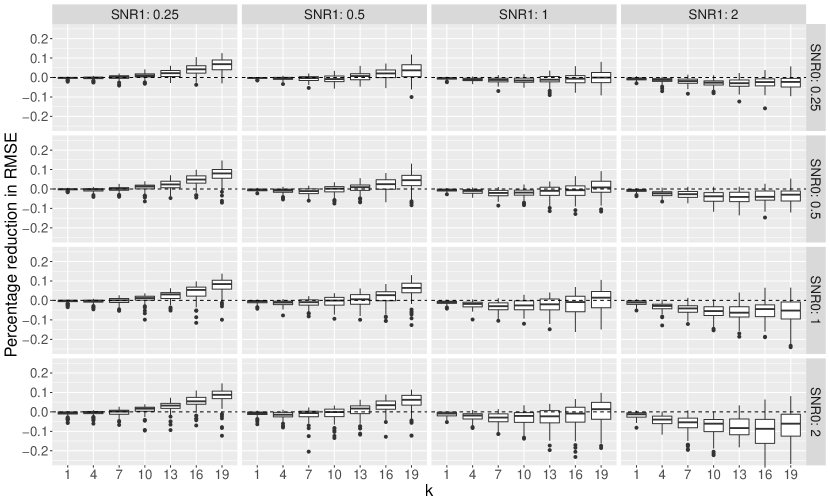

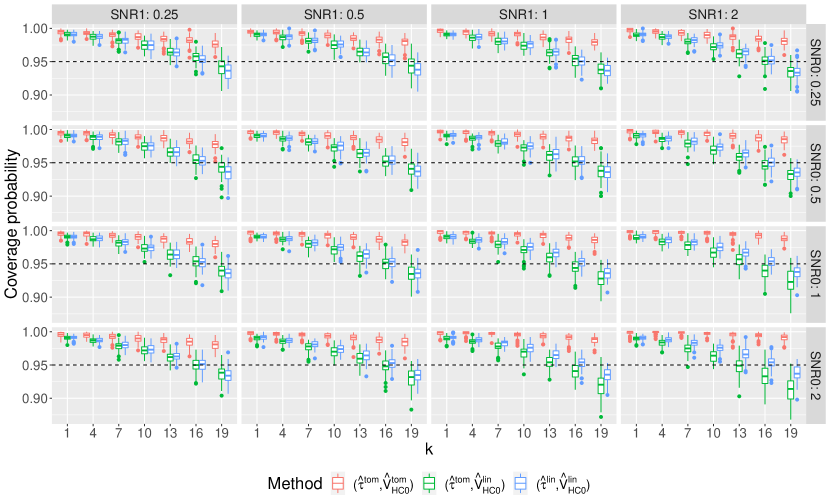

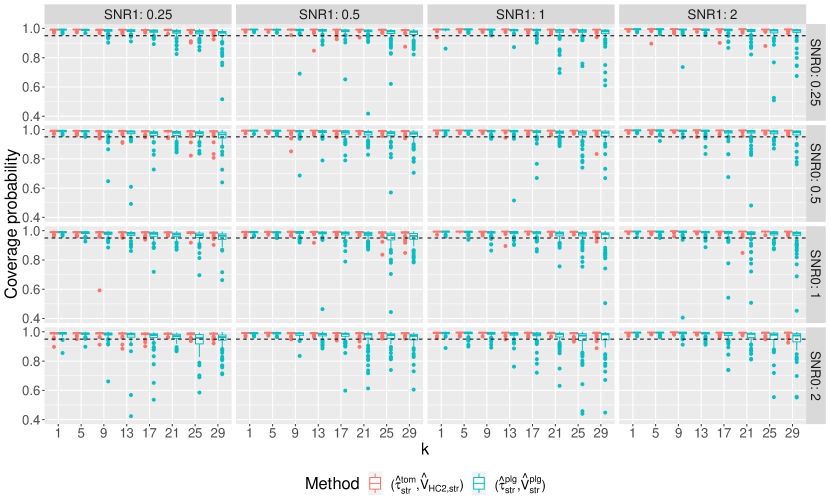

Figure 3 depicts the percentage reduction in RMSE of versus . Figure 4 presents the empirical coverage probabilities of confidence intervals constructed by and . Both figures are results of many small strata scenario. The results of other scenarios are similar so we degrade them to the Supplementary Material. It can be observed that, dominates the plug-in estimator under all scenarios, especially when the dimension of covariates grows. The increasing outliers in the boxplot as and dimension of covariates grow imply that is more robust than the plug-in estimator under these scenarios. Moreover, Figure 4 shows that the plug-in variance estimator tends to underestimate the true sampling variance and produce confidence intervals with coverage probabilities lower than the nominal level when the dimension of covariates is large. Therefore, we recommend for stratified randomized experiments.

5.3 Completely randomized survey experiments

We set the population size and sampling fraction to generate data using the same model as (11). Let be the covariates available at the sampling stage. We use in ToM regression adjustment, with dimensions. We set for the sampling stage and for the treatment assignment stage. We simulate the completely randomized survey experiments times to compute the empirical RMSE of point estimators and empirical coverage probabilities of confidence intervals. We vary the and in each scenario. Table 1 presents the values of these factors considered in the simulation. Each scenario is repeated under different random seeds.

Let and be the sample covariances of covariates under treatment arm . Let be the sample variance of and , be the sample covariances between covariates and outcomes. Yang et al., (2021) used the plug-in principle to derive linearly adjusted point and variance estimators. The point estimator is derived by replacing the optimal projection coefficients in the optimal linearly adjusted estimator with their consistent estimators , where

The variance estimator is derived using the estimated adjusted potential outcomes to replace in . Both and Yang et al.’s variance estimator tend to underestimate the true sampling variance for large in finite samples. To remedy this issue, we use the type estimator suggested by Lei and Ding, (2021).

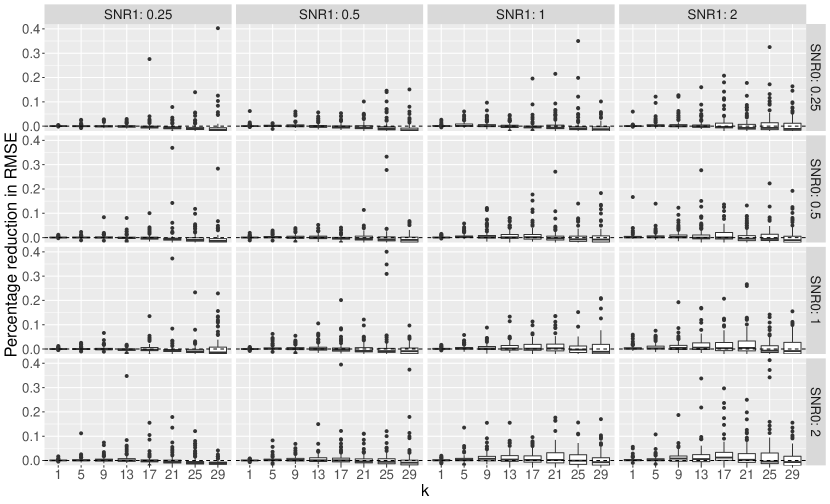

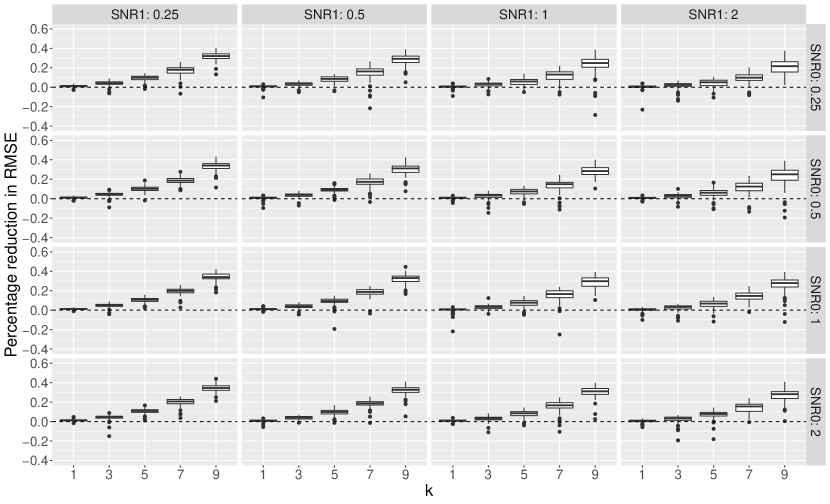

Figure 5 depicts the percentage reduction in RMSE of versus . Similar to the completely randomized experiments, outperforms when the dimension of covariates grows. The trend becomes more evident when the majority group has a larger SNR and the minority group has a smaller SNR. Figure 6 depicts the coverage probabilities of confidence intervals constructed by and . It can be observed that the combination of maintains an average of coverage probabilities, while the combination of tends to have low coverage probabilities for large and performs worse when the majority group has a larger SNR and the minority group has a smaller SNR. Therefore, we recommend for analyzing completely randomized survey experiments.

6 Applications

6.1 The “opportunity knocks” experiment

The “opportunity knocks” (OK) experiment (Angrist et al.,, 2014) was a stratified randomized experiment launched to evaluate the effect of financial incentive on college students’ academic performance. The experiment included first- and second-year students who applied for financial aid at a large Canadian commuter university. Based on sex and discretized high school grades, the students were grouped into strata with strata sizes ranging from to . In each stratum, approximately students received the treatment. Therefore, the ’s varied across strata. The grade point average (GPA) at the end of the fall semester was the outcome of interest. We consider covariates in ToM regression adjustment: high school grade, previous year GPA, age, whether the student’s mother tongue is English, whether the student lives at home, and whether the student has high concern about the funds.

Table 2 presents , the adjusted coefficient , and their hadamard product. We can see that adjusts because the treatment group’s previous year GPA is lower on average, and more students live at home and have high concerns about the funds.

| High school | Previous year | Age | Whether the student’s mother | Whether the student | Whether the student has | |

|---|---|---|---|---|---|---|

| grade | GPA | tongue is English | lives at home | high concern about the funds | ||

| 0.003 | -0.010 | 0.028 | 0.000 | 0.011 | 0.023 | |

| 0.186 | 7.543 | -0.089 | -0.201 | -2.447 | -1.914 | |

| 0.001 | -0.075 | -0.002 | -0.000 | -0.027 | -0.044 |

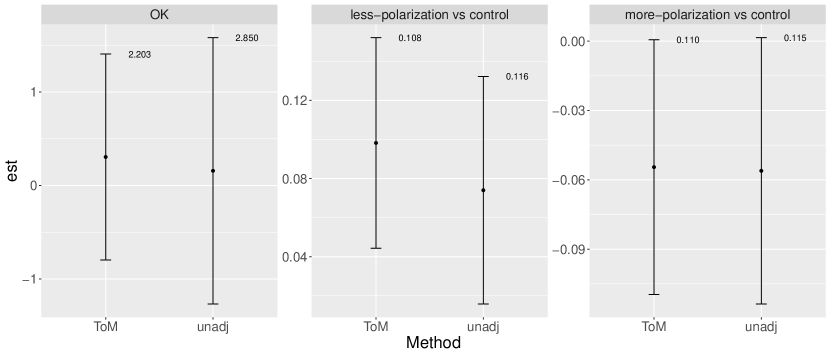

Figure 7 depicts the average treatment effect estimators, standard errors, and confidence intervals. Both ToM regression-adjusted and unadjusted estimators show that the average treatment effect is insignificant. That is, we do not have sufficient evidence to support the following: financial incentive affects students’ academic performance. However, it is interesting to see that ToM regression adjustment provides a larger average treatment effect estimator and decreases the estimated standard error by .

6.2 Social Trust in Polarized Times

We re-analyze the experimental dataset from Lee, (2022) to evaluate the impact of perceived polarization on social trust levels. In this experiment, 1006 Americans over 18 years old were recruited from an online survey panel. We treat the experimental units as a simple random sample from the target population, that is, the entire American population over 18 years old. The experimental units are randomly assigned to read one of the three news articles designed to either promote perceived polarization (more-polarization), reduce perceived polarization (less-polarization), or serve as a control article. We evaluate the treatment effects of more-polarization and less-polarization versus the control. The outcome is an index ranging from 0 to 1, with higher values indicating higher generalized social trust. The following types of covariates are used:

-

•

: whether the individual is white and non-Hispanic (race1), whether the individual is black or African American (race2), whether the individual is Hispanic (race3), whether the individual is female (sex), education type (education), household income type (income), marital status (marital), whether the individual does not go to college (nocollege), and age.

-

•

: race1, race2, race3, age, and sex. We obtain of the target population from the website of United States Census Bureau.

First, we add the main effect of and , quadratic terms of the continuous covariates of , and two-way interactions of in the full regression model, which produced a design matrix with columns. Then we use forward-backward stepwise regression to obtain a reduced model with and covariates entering ToM regression adjustment for the treatment effects of more-polarization and less-polarization versus the control, respectively. For both regression adjustments, none of the enters the model.

| age | age:education | age:marital | age:race3 | income:race1 | |

|---|---|---|---|---|---|

| income:race3 | sex:race2 | education:marital | nocollege:race1 | ||

| age:education | age:nocollege | income:race1 | education:nocollege | ||

|---|---|---|---|---|---|

For the treatment effect of less-polarization versus control, Table 3 and Figure 7 show that ToM regression adjusts upwards mainly because the treatment group is years younger than the control group. Both ToM regression-adjusted and unadjusted estimators indicate that the average treatment effect is significant, that is, less-polarization articles significantly affect people’s social trust. In contrast, the treatment effect of more-polarization versus control is insignificant as presented by Figure 7. ToM regression slightly adjusts ; see Table 4. Compared to the unadjusted estimator, ToM regression adjustment decreases the estimated standard error by and , respectively, for the less-polarization versus control and more-polarization versus control.

7 Extension to rerandomization

Regression adjustment is used at the analysis stage to adjust for covariate imbalance. Rerandomization is an alternative approach achieving covariate balance in the design stage (see, e.g., Morgan and Rubin,, 2012, 2015; Li et al.,, 2018; Li and Ding,, 2020; Li et al.,, 2020; Wang et al.,, 2021; Zhao and Ding, 2021b, ; Lu et al.,, 2022). Recent work by Li and Ding, (2020), Wang et al., (2021), and Zhao and Ding, 2021b showd that the combination of rerandomization and Lin’s with-interaction regression adjustment can further improve the efficiency if the analysis stage utilizes more covariate information than the design stage. The same conclusion holds true for the combination of rerandomization and ToM regression adjustment.

In randomized experiments, it is common that the covariates avaliable at the design stage are a subset or linear combinations of the covariates available at the analysis stage. In this case, the asymptotic normality and optimality of the ToM regression-adjusted estimator and the asymptotic properties of the heteroscedasticity-robust variance estimators still hold if (1) rerandomization (Morgan and Rubin,, 2012) is used in completely randomized experiments, or (2) stratified rerandomization (Wang et al.,, 2021) is used in stratified randomized experiments, or (3) rejective sampling and reradnomization (Yang et al.,, 2021) are used in completely randomized survey experiments, or (4) rerandomization based on cluster-level covariates (Lu et al.,, 2022) is used in cluster randomized experiments.

8 Discussion

We re-examine ToM regression adjustment and justify its robustness compared to the with-interaction regression adjustment from three perspectives: first, ToM regression adjustment produces less extreme calibrated-weights; second, ToM regression adjustment produces smaller leverage scores; third, when the dimension of covariates is large or there is an imbalance in information between treatment and control groups, ToM regression adjustment produces estimator with smaller mean squared errors and better coverage probabilities. We proved the applicability of ToM regression adjustment to stratified randomized experiments, completely randomized survey experiments and cluster randomized experiments. Under each design, we showed that the ToM regression-adjusted average treatment effect estimator is asymptotically normal and optimal in the class of linearly adjusted estimators. We also studied the asymptotic properties of several heteroscedasticity-robust variance estimators derived from the ToM regression adjustment and found that some of these variance estimators may be anti-conservative. Our results are design-based and allow model misspecification. Lastly, the inferential procedure can be easily implemented by standard statistical software packages.

The asymptotic theory may not be applicable when the number of experimental units is small. In such cases, we suggest using Fisher-randomization tests with studentized test statistics obtained from ToM regression adjustment (Zhao and Ding, 2021a, ). The Fisher-randomization tests yield finite-sample exact -values under the sharp null hypothesis and are asymptotically valid under the weak null hypothesis, with the average treatment effect as zero.

Our asymptotic analysis assumes that the number of covariates is fixed. However, in many randomized experiments, such as A/B tests, the number of covariates can be very large, even larger than the sample size (Bloniarz et al.,, 2016; Lei and Ding,, 2021). ToM regression adjustment can be easily extended to high-dimensional settings by adding an appropriate penalty on the adjusted coefficient. It would be interesting to study the design-based properties of this extension.

Finally, our theory focuses on experimental designs with binary treatment and perfect compliance. In practice, researchers may be interested in the effects of multiple-valued treatments in the presence of noncompliance. It is interesting to extend the applicability of ToM regression adjustment to analyze randomized experiments with multiple-valued treatments (Fisher,, 1935; Liu et al.,, 2021; Ye et al.,, 2022) and/or noncompliance (Imbens and Angrist,, 1994; Angrist and Imbens,, 1995; Angrist et al.,, 1996; Ding and Lu,, 2017).

Acknowledgement

This research is supported by the National Natural Science Foundation of China (12071242) and the Guo Qiang Institute of Tsinghua University.

References

- Angrist et al., (2014) Angrist, J., Oreopoulos, P., and Williams, T. (2014). When opportunity knocks, who answers? New evidence on college achievement awards. Journal of Human Resources, 49:572–610.

- Angrist and Imbens, (1995) Angrist, J. D. and Imbens, G. W. (1995). Two-stage least squares estimation of average causal effects in models with variable treatment intensity. Journal of the American Statistical Association, 90(430):431–442.

- Angrist et al., (1996) Angrist, J. D., Imbens, G. W., and Rubin, D. B. (1996). Identification of causal effects using instrumental variables. Journal of the American statistical Association, 91:444–455.

- Bloniarz et al., (2016) Bloniarz, A., Liu, H., Zhang, C.-H., Sekhon, J. S., and Yu, B. (2016). Lasso adjustments of treatment effect estimates in randomized experiments. Proceedings of the National Academy of Sciences, 113:7383–7390.

- Deville and Särndal, (1992) Deville, J.-C. and Särndal, C.-E. (1992). Calibration estimators in survey sampling. Journal of the American Statistical Association, 87:376–382.

- Deville et al., (1993) Deville, J.-C., Särndal, C.-E., and Sautory, O. (1993). Generalized raking procedures in survey sampling. Journal of the American statistical Association, 88:1013–1020.

- Ding, (2021) Ding, P. (2021). The frisch–waugh–lovell theorem for standard errors. Statistics & Probability Letters, 168:108945.

- Ding and Lu, (2017) Ding, P. and Lu, J. (2017). Principal stratification analysis using principal scores. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79:757–777.

- Dorfman, (1991) Dorfman, A. H. (1991). Sound confidence intervals in the heteroscedastic linear model through releveraging. Journal of the Royal Statistical Society: Series B (Methodological), 53:441–452.

- Fisher, (1926) Fisher, R. A. (1926). The arrangement of field experiments. Journal of the Ministry of Agriculture, 33:503–513.

- Fisher, (1935) Fisher, R. A. (1935). The Design of Experiments. Oliver and Boyd, Edinburgh, 1st edition.

- Freedman, (2008) Freedman, D. A. (2008). On regression adjustments to experimental data. Advances in Applied Mathematics, 40(2):180–193.

- Hayes and Moulton, (2017) Hayes, R. J. and Moulton, L. H. (2017). Cluster Randomised Trials. CRC Press, Florida.

- Huber, (1967) Huber, P. J. (1967). The behavior of maximum likelihood estimates under nonstandard conditions. In Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability, volume 1, pages 221–233.

- Huber, (2004) Huber, P. J. (2004). Robust Statistics. John Wiley & Sons.

- Imai et al., (2008) Imai, K., King, G., and Stuart, E. A. (2008). Misunderstandings between experimentalists and observationalists about causal inference. Journal of the Royal Statistical Society: Series A (Statistics in Society), 171(2):481–502.

- Imbens and Angrist, (1994) Imbens, G. W. and Angrist, J. D. (1994). Identification and estimation of local average treatment effects. Econometrica, 62(2):467–475.

- Imbens and Rubin, (2015) Imbens, G. W. and Rubin, D. B. (2015). Causal Inference in Statistics, Social, and Biomedical Sciences. Cambridge University Press.

- Lee, (2022) Lee, A. H.-Y. (2022). Social trust in polarized times: How perceptions of political polarization affect americans’ trust in each other. Political Behavior, in press.

- Lei and Ding, (2021) Lei, L. and Ding, P. (2021). Regression adjustment in completely randomized experiments with a diverging number of covariates. Biometrika, 108(4):815–828.

- Li and Ding, (2017) Li, X. and Ding, P. (2017). General forms of finite population central limit theorems with applications to causal inference. Journal of the American Statistical Association, 112:1759–1769.

- Li and Ding, (2020) Li, X. and Ding, P. (2020). Rerandomization and regression adjustment. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 82:241–268.

- Li et al., (2018) Li, X., Ding, P., and Rubin, D. B. (2018). Asymptotic theory of rerandomization in treatment–control experiments. Proceedings of the National Academy of Sciences, 115:9157–9162.

- Li et al., (2020) Li, X., Ding, P., and Rubin, D. B. (2020). Rerandomization in factorial experiments. The Annals of Statistics, 48:43–63.

- Lin, (2013) Lin, W. (2013). Agnostic notes on regression adjustments to experimental data: Reexamining freedman’s critique. The Annals of Applied Statistics, 7:295–318.

- Liu et al., (2021) Liu, H., Ren, J., and Yang, Y. (2021). Randomization-based joint central limit theorem and efficient covariate adjustment in randomized block factorial experiments. Journal of the American Statistical Association, in press.

- Liu et al., (2022) Liu, H., Tu, F., and Ma, W. (2022). Lasso-adjusted treatment effect estimation under covariate-adaptive randomization. Biometrika, in press.

- Liu and Yang, (2020) Liu, H. and Yang, Y. (2020). Regression-adjusted average treatment effect estimates in stratified randomized experiments. Biometrika, 107(4):935–948.

- Lu et al., (2022) Lu, X., Liu, T., Liu, H., and Ding, P. (2022). Design-based theory for cluster rerandomization. Biometrika, in press.

- Ma et al., (2022) Ma, W., Tu, F., and Liu, H. (2022). Regression analysis for covariate-adaptive randomization: A robust and efficient inference perspective. Statistics in Medicine, in press.

- Middleton and Aronow, (2015) Middleton, J. A. and Aronow, P. M. (2015). Unbiased estimation of the average treatment effect in cluster-randomized experiments. Statistics, Politics and Policy, 6:39–75.

- Morgan and Rubin, (2012) Morgan, K. L. and Rubin, D. B. (2012). Rerandomization to improve covariate balance in experiments. Annals of Statistics, 40:1263–1282.

- Morgan and Rubin, (2015) Morgan, K. L. and Rubin, D. B. (2015). Rerandomization to balance tiers of covariates. Journal of the American Statistical Association, 110:1412–1421.

- Negi and Wooldridge, (2021) Negi, A. and Wooldridge, J. M. (2021). Revisiting regression adjustment in experiments with heterogeneous treatment effects. Econometric Reviews, 40(5):504–534.

- Rubin, (1980) Rubin, D. B. (1980). Randomization analysis of experimental data: the fisher randomization test comment. Journal of the American Statistical Association, 75:591–593.

- Schochet et al., (2021) Schochet, P. Z., Pashley, N. E., Miratrix, L. W., and Kautz, T. (2021). Design-based ratio estimators and central limit theorems for clustered, blocked rcts. Journal of the American Statistical Association, in press.

- Sloczynski, (2018) Sloczynski, T. (2018). A general weighted average representation of the ordinary and two-stage least squares estimands. Technical report, IZA Discussion Paper.

- Su and Ding, (2021) Su, F. and Ding, P. (2021). Model-assisted analyses of cluster-randomized experiments. Journal of the Royal Statistical Society: Series B (Statistical Methodology), in press.

- Wang et al., (2021) Wang, X., Wang, T., and Liu, H. (2021). Rerandomization in stratified randomized experiments. Journal of the American Statistical Association, in press.

- White, (1980) White, H. (1980). A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica, 48:817–838.

- Yang et al., (2021) Yang, Z., Qu, T., and Li, X. (2021). Rejective sampling, rerandomization, and regression adjustment in survey experiments. Journal of the American Statistical Association, in press.

- Ye et al., (2022) Ye, T., Yi, Y., and Shao, J. (2022). Inference on the average treatment effect under minimization and other covariate-adaptive randomization methods. Biometrika, 109:33–47.

- (43) Zhao, A. and Ding, P. (2021a). Covariate-adjusted fisher randomization tests for the average treatment effect. Journal of Econometrics, in press.

- (44) Zhao, A. and Ding, P. (2021b). No star is good news: A unified look at rerandomization based on -values from covariate balance tests. arXiv preprint arXiv:2112.10545.

- (45) Zhao, A. and Ding, P. (2022a). Reconciling design-based and model-based causal inferences for split-plot experiments. The Annals of Statistics, 50:1170–1192.

- (46) Zhao, A. and Ding, P. (2022b). Regression-based causal inference with factorial experiments: estimands, model specifications, and design-based properties. Biometrika, 109:799–815.

Supplementary Material

Section A provides parallel results for cluster randomized experiments.

Section B provides additional simulation results.

Section C provides formulas of the heteroskedasticity-robust standard errors .

Section D provides proofs for the results under completely randomized experiments.

Section E provides proofs for the results under stratified randomized experiments.

Section F provides proofs for the results under completely randomized survey experiments.

Appendix A ToM regression adjustment in cluster randomized experiments

Cluster randomized experiments randomly assign the treatment at the cluster level with units in the same cluster receiving the same treatment status (Hayes and Moulton,, 2017). Cluster randomized experiments have been widely used in empirical research when individual-level treatment assignment is infeasible or inconvenient.

Consider units nested in clusters of sizes (, ). By design, clusters are randomly assigned to the treatment group and clusters are assigned to the control group. Let be the treatment assignment indicator for cluster . With a slight abuse of notation, let . We use to index unit in cluster (, ). Let and () be the covariates and potential outcomes for units . Let be the cluster-level covariates. The average treatment effect is

Let be the average cluster size. Let () be the potential outcome total of cluster scaled by and be the observed scaled potential outcome total. Then, the average treatment effect can be rewritten as

Similarly, we define scaled covariate total . We can view cluster randomized experiments as complete randomized experiments on the cluster level with cluster-level data (Li and Ding,, 2017; Middleton and Aronow,, 2015). Su and Ding, (2021) showed that regression adjustment using scaled covariate total together with cluster size leads to larger variance reduction compared with individual-level regression adjustment. Given assumption similar to Assumption 1 on , we have results in parallel with those in Section 2 in the main text.

Let be the estimated coefficient and heteroscedasticity-robust variance estimator of in the following weighted regression:

where . Corollary 1 below is a direct result of Proposition 1 and Theorem 1.

Corollary 1.

Under Assumption 1 with , , , (i) is consistent for , asymptotically normal, and optimal in the class of linearly adjusted estimators, (ii) the probability limit of () is larger than or equal to the true asymptotic variance of , and (iii) the Wald-type confidence intervals

have asymptotic coverage rates greater than or equal to .

Appendix B Additional simulation results

Figures 8–11 show the simulation results for completely randomized experiments when and . Under these two more balanced scenarios, the advantages of over are not as significant as that when . In particular, when both SNR1 and SNR0 are large, performs worse than . This may be because the adjusted coefficients in both the treatment and control groups are well estimated by . Therefore, for a nearly balanced design, we still recommend the use of .

Figures 12–15 show the simulation results for stratified randomized experiments with a few large strata and many small strata compounded with a few large strata. The conclusions are similar to those in the main text.

We also conduct simulation for cluster randomized experiments. The potential outcomes are generated by the following random effect model:

We set the number of clusters . The cluster sizes are generated uniformly from the set . The intercepts and slopes are generated by and , where and have i.i.d. entries generated from and standard normal distribution, respectively. The covariates ’s are realizations of independent random vectors of length from with , and ’s are realizations of i.i.d. normal random variables with zero mean and variance fulfilling a given signal-to-noise ratio , i.e., the ratio of the finite-population variance of to that of .

We set the proportion of clusters assigned to the treatment group . After we have generated the data, we use the scaled cluster totals in the analysis stage. We use covariates in the regression adjustment as suggested by Su and Ding, (2021). Again cluster randomized experiments are simulated and empirical RMSE and coverage probabilities are computed. We consider scenarios with all parameter values presented in Table 5.

| random seed | |

|---|---|

Appendix C Heteroskedasticity-robust standard error and notation

Let be the outcome vector, be the covariate matrix and be a diagonal matrix. Consider a weighted regression with working model

The leverage score of the th unit, denoted by , is the th diagonal entry of the following matrix:

Denote the estimated regression coefficient as , with

Let be the regression residual of unit . Suppose that the target estimand is , where is a known vector. Then the point estimator is and the heteroskedasticity-robust variance estimator is

where is a diagonal matrix consisting of squared scaled residuals , with varying for different estimating methods. In particular, for , for , for , and for .

We use lower case letter “” to denote sample variance and covariance. For example, is the sample covariance of and , and is the sample variance of . We use to denote sample mean, variance or covariance computed using samples from treatment arm . For example, is the sample covariance of in the treatment group and is the sample mean of in the treatment group. We use a hat to denote estimated quantity, such as . Let denote a vector with at the th dimension and at other dimensions. For square matrices and , write if is positive definite and if is non-negative definite. Let denote the th element of matrix . Let be the set of units under treatment arm (or for stratified experiment). Let and denote the operator norm and infinity norm of a matrix, respectively. For two random variables and , write if they have the same limiting distribution. Let be the identity matrix of dimension ; be the vector of all ’s of length ; and be the vector of all ’s of length . We use to denote for short. We use to denote for short.

Appendix D Proofs for the results under completely randomized experiments

D.1 Preliminary results

Proposition 2.

where

Proof.

Note that regression with weights is equivalent to OLS regression with data multiplied by . By Frisch–Waugh–Lovell (FWL) theorem (Ding,, 2021), the estimated coefficient of in the weighted regression can be derived by the OLS regression , where

Then

Simple algebra yeilds that

It follows that

By the property of OLS regression, is the estimated coefficient of in the WLS regression of

Therefore, ∎

Lemma 1.

Under Assumption 1,

Lemma 2.

Under Assumption 1,

Proof.

Lemma 3.

Under Assumption 1,

Proof.

Note that

where the last equality is due to the definition of , , and .

Taking derivative with respect to , we have

∎

Let denote the residual of unit derived from the ToM regression adjustment. Let denote the sample variance of the residuals corresponding to treatment arm , i.e.,

Lemma 4.

Under Assumption 1,

Proof.

D.2 Proof of Proposition 1

D.3 Proof of Theorem 1

D.4 Proof of Theorem 2

Proof.

Next, we prove that minimizes the total distance

under the constraints (12) and (13) below.

| (12) |

| (13) |

In contrast, minimizes the total distance under the constraints (12) and (14) below.

| (14) |

Denote the vector of ’s. Consider the following Lagrangian function:

Setting the gradient of to , we have

| (15) | |||

| (16) |

Summarizing equation (15) for and by the constraint (12), we have

| (17) |

Summarizing equation (16) for and by the constraint (12), we have

| (18) |

Plugging (17) into (15) and (18) into (16),

| (19) | |||

| (20) |

Therefore,

| (21) | |||

| (22) |

Plugging (21) and (22) into (13),

Therefore,

| (23) |

Plugging (23) into (21) and (22), the minimizer of under constraints (12) and (13) is

Similarly, consider the following lagrangian function:

Setting the gradient of to , we have

| (24) | |||

| (25) |

Summarizing equation (24) for and by the constraint (12), we have

| (26) |

Summarizing equation (25) for and by the constraint (12), we have

| (27) |

Plugging (26) into (24) and (27) into (25),

| (28) | |||

| (29) |

Therefore,

| (30) | |||

| (31) |

Plugging (30) and (31) into (14),

Therefore,

| (32) | |||

| (33) |

Plugging (32) into (30) and (33) into (31), the minimizer of under constraints (12) and (14) is

∎

D.5 Proof of Theorem 3

Proof.

By definition, the leverage score is the th diagonal element of

where is an matrix with the th row of being .

The leverage score is the th diagonal element of

where with the th row of being .

Let with the th row being . Let with the th row being . Since

then

Note that

Therefore,

Since and , then

Therefore,

∎

Appendix E Proofs for the results under stratified randomized experiments

E.1 Preliminary results

Let and . Let for , .

Proposition 4.

, where

Proof.

By FWL theorem, the estimated coefficient of in the weighted regression can be dervied as the OLS regression of . Therefore,

Simple algebra gives that

Therefore,

By the property of OLS, is the estimated coefficient of in the WLS regression:

It follows that . ∎

Lemma 5.

Under Assumption 3, for , we have

Lemma 6.

Under Assumption 3,

Proof.

By Lemma 5,

Therefore,

The first term is and the second term is . Therefore, the conclusion follows. ∎

Let be the residuals from the weighted regression (4). One of the variance estimator can be derived as

| (34) |

where

Lemma 7 below shows that (34) is a conservative estimator of the variance of .

Lemma 7.

Proof.

E.2 An equivalent form of regression formula

In this section, we prove that two regression formulas (37) and (38) below are equivalent in terms of point and variance estimators for the average treatment effect under stratified randomized experiments. It is useful for proving Theorem 5.

Recall the regression formula we use in the main text

| (37) |

where if and otherwise, and

It is equivalent to the following weighed regression

| (38) |

Let be the design matrix of regression (37) with the th row of being

Let be the design matrix of regression (38) with the th row of being

Let be the digonal matrix of ’s and be the vector of ’s . Let and be the estimated coefficients of regression (37) and (38), respectively. Then

Next, we prove some lemmas to build the equivalence between these two regressions. Let . Let be a vector of length . Lemma 8 below shows that they have the same estimated coefficient for the covariates.

Lemma 8.

Proof.

Lemma 9 below shows that we can derive the same average treatment effect estimator. Recall that is a vector with at the second dimension and at other dimensions.

Lemma 9.

Proof.

In the proof of Proposition 4, we have shown that

It suffices to show that

By the property of OLS and Lemma 8, the estimated coefficient of and can be derived in the WLS regression of

It follows that the estimated coefficients of and are, respectively,

for . Therefore,

∎

Proof.

By the property of OLS, the residuals of regression (38) are equal to those of the following regression:

The residuals of regression (37) are equal to those of the following regression:

Note that the fitted values of the above two regressions are the same for units in the same stratum under the same treatment arm. Therefore, the fitted value of unit is the mean value over the units in the same stratum under the same treatment arm with . Thus, the residuals of unit of regressions (37) and (38) are both equal to . ∎

The leverage scores of these two regressions are the diagonal elements of the following matrices

As shown in the proof of Lemma 11, (The explicit formula of can be found in the proof of Lemma 11). The fact that is an invertible matrix indicates that

Therefore, the leverage scores of these two regression formulas are the same. We denote by the leverage score corresponding to unit . We will derive the formula of in Section E.3.

Let be the regression residual of unit . Let be the scaled residual where for , for , for , for . Let be the diagonal matrix of .

Lemma 11 below shows the equivalence of these two variance estimators.

Lemma 11.

Proof.

First, we give the explicit formula of subject to . Let denote the matrix with the th element being and the other elements being . Let denote identify matrix of size . We can verify that

where

Here corresponds to the operation of changing to ; corresponds to the operation of changing to ; corresponds to the operation of changing to ; corresponds the operation of changing to ; corresponds to the operation of changing to ; corresponds to the operation of reordering the positions of the regressors; and corresponds to the operation of centering at .

After some calculation, we can verify that

Therefore,

∎

E.3 Leverage scores of ToM regression in stratified randomized experiments

Define Define the regression weights for units in stratum under treatment arm with

Proposition 6 below provides the formula of leverage scores of ToM regression in stratified randomized experiments.

Proposition 6.

Proof.

Let with the th row of being

There exists a squared and invertible matrix such that . Therefore,

Note that

Moreover,

Therefore,

∎

Lemma 12.

Under Assumption 3,

Proof.

Let

By Lemma 5, for ,

Therefore,

Thus,

Similarly,

Thus,

By Assumption 3, the limit of is an invertible matrix. Let be the smallest eigenvalue of and there exists a constant such that for sufficiently large . By Weyl’s inequality, with probability tending to one,

Therefore, with probability tending to one,

Thus, Since , then ∎

Define

Lemma 13.

Under Assumption 3,

Proof.

E.4 Proof of Theorem 4

E.5 Proof of Theorem 5

Proof.

We use the following formula of the variance estimator

Let . Define by

where

Define by

where

Define by

By the formula of inverse of block matrix, we have

Let it is easy to see that

| (42) |

To derive the formula of , we calculate the following two quantities:

For (i), we have

Denote by .

For (ii), we have

Expanding (42), we have

Let

Next, we derive the formula related to .

Next, we prove that and . Note that for , and by Lemma 13,

Therefore,

Note that , , , , , . Therefore, we derive the following stochastic order for terms related to ,

Note that . Therefore,

Thus,

Combining with Lemma 7, we complete the proof.

∎

E.6 Proof for Remark 4

We give an example to show that for are anti-conservative. Similar to the proof of Theorem 5, we have, for ,

Therefore

Let and for . By Lemmas 5 and 6, we have

Therefore, is anti-conservative when

is anti-conservative when

Appendix F Proofs for the results under completely randomized survey experiments

F.1 Preliminary results

Proposition 7.

where

Proof.

Recall the regression

Let . Recall that is the set of sampled units. By FWL theorem,

Simple algebra gives that

Therefore,

∎

The following lemma is from Lemma B16 in Yang et al., (2021).

Lemma 14.

Under Assumption 4, for ,

Lemma 15.

Under Assumption 4,

Proposition 8.

Under Assumption 4, is asymptotically normal with zero mean and covariance

F.2 Proof of Theorem 6

F.3 A plug-in variance estimator

With a slight abuse of notation, let be the residual of unit from the WLS regression (8). One of the variance estimators of can be derived by

| (43) |

where

Proposition 9 below demonstrates the asymptotic conservativeness of .

Proposition 9.

Proof.

F.4 Leverage scores of ToM regression in completely randomized survey experiments

Recall that and we similarly define . Define by

We define the weights for treatment arm as .

Proposition 10.

The leverage score of ToM regression for unit under completely randomized survey experiments is

Proof.

Let with the th row of being

There exists an invertible matrix such that . Therefore,

Note that

Therefore,

∎

Lemma 16.

Under Assumption 4,

Lemma 17.

Under Assumption 4,

F.5 Proof of Theorem 7

Let be the residual of unit . Let be the scaled residual with , where for , for , for , and for . The variance estimator derives as

where with the th row being , is the diagonal matrix of , and is the diagonal matrix of scaled residual squares .

Motivated by the following equivalent regression

An equivalent variance estimator derives as

where , with the th row being . Note that is unknown, and therefore the regression is infeasible, but it is useful for proving Theorem 7.

The proof of equivalence is similar to that in Section E.2, so we omit it. We will base our proof of Theorem 7 on this equivalent variance estimator.

Proof.

Let and . Define by

where

Define by

where

Define by

By the formula of inverse of block matrix, we have

Let it is easy to see that

| (51) |

Recall that

After some calculation, we have

where

We expand equation (51) as follows:

Let

Then,

Note that , by Lemma 17,

Therefore, for . Moreover, and by Proposition 9, . Therefore,

Note that , , , . Therefore,

∎