Statistical learning for -weakly dependent processes

Mamadou Lamine DIOP 111Supported by the MME-DII center of excellence (ANR-11-LABEX-0023-01) and William KENGNE 222Developed within the ANR BREAKRISK: ANR-17-CE26-0001-01 and the CY Initiative of Excellence (grant ”Investissements d’Avenir” ANR-16-IDEX-0008), Project ”EcoDep” PSI-AAP2020-0000000013

THEMA, CY Cergy Paris Université, 33 Boulevard du Port, 95011 Cergy-Pontoise Cedex, France

E-mail: mamadou-lamine.diop@cyu.fr ; william.kengne@cyu.fr

Abstract: We consider statistical learning question for -weakly dependent processes, that unifies a large class of weak dependence conditions such as mixing, association, The consistency of the empirical risk minimization algorithm is established. We derive the generalization bounds and provide the learning rate, which, on some Hölder class of hypothesis, is close to the usual obtained in the i.i.d. case. Application to time series prediction is carried out with an example of causal models with exogenous covariates.

Keywords: Statistical learning, -weak dependence, ERM principle, generalization bound, consistency.

1 Introduction

Statistical learning has received a considerable attention in the literature in the recent decades. This interest is still increasing nowadays, mainly due to the significant successes of the applications of machine learning algorithms and the theoretical properties of these algorithms, which are now well studied in many cases. For instance, see [31], [9], [7], [27] for some results when the training samples are independent and identically distributed (i.i.d.). But, the i.i.d. assumption fails in many real life applications: market prediction, GDP (gross domestic product) prediction, signal processing, meteorological observations, There is a vast literature on learning with dependent observations, we refer to [29], [36], [28], [32], [23] and the references therein for an overview of this issue.

We consider the supervised learning setting and let (the training sample) be a trajectory of a stationary and ergodic process , which takes values in , where is the input space and the output space. Denote by the set of hypothesis (a family of predictors) and consider a loss function . In this context of learning from dependent data, the generalization error (risk) can be defined in various ways, see for instance [23]. We deal with the widely-used averaged risk (see for instance, [36], [28], [1], [17], [6]), given for any hypothesis by

The goal is to construct a learner such that, for any , is average ”close” to ; that is, a learner which achieves the small averaged risk. The empirical risk (with respect to the training sample) of a hypothesis is given by

In the sequel, we set for all and . The setting considered here covers many commonly used situations: regression estimation, classification (pattern recognition when is finite), autoregressive models prediction (we can take and for some ), autoregressive models with exogenous covariates.

Consider a target (with respect to ) function (assumed to exist), given by,

and the empirical target

| (1.1) |

We focus on the empirical risk minimization (ERM) principle and aim to study the relevance of estimation of by . The capacity of to approximate is now as the generalization capability of the ERM algorithm. This generalization capability is accessed by studying how is close to . The deviation between and is the generalization error the algorithm. When , the ERM algorithm is said to be consistent within the hypothesis class .

The study of a learning algorithm includes the calibration of a bound of the generalization error for any fixed (non asymptotic property) and the investigation of consistency (asymptotic property). There exist several important contributions in the literature devoted to statistical learning for dependent observations, with various types of dependence structure. See among others papers, [25], [26], [36], [28], [35], [18], [23] for some developments under mixing conditions and [39], [37], [38], [33] for some results for Markov chains. [1] considered a prediction of time series under -weakly dependent condition. They established convergence rates using the PAC-Bayesian approach. See also [6], [22], [24] for some Bernstein-type inequality for -mixing process and some advances on time series forecasting using statistical learning paradigm. However, most of the above works are developed within a mixing condition or for time series prediction or do not consider a general setting that includes pattern recognition, regression estimation, time series prediction,

In this new contribution, we consider a general learning framework where the observations is a trajectory of a -weakly dependent process with values in a Banach space . The following issues are addressed.

-

(i)

Consistency of the ERM algorithm. We establish the consistency of the ERM algorithm within any space of Lipschitz predictors. In comparison with the existing works, let us stress that, the -weakly dependent structure considered here is a more general concept and it is well known that many weak dependent processes do not fulfill the mixing conditions, see for instance [10].

-

(ii)

Generalization bounds and convergence rates. When (with ), and is a subset of a Hölder space for some , generalization bounds are derived and the learning rate is provided. This rate is close to the usual when .

-

(iii)

Application to time series prediction. Application to the prediction of affine causal models with exogenous covariates is carried out. We show that, these models fulfill the conditions that ensure the consistency of the ERM algorithm and enjoy the generalization bounds established.

The rest of the paper is structured as follows. In Section 2, we set some notations and assumptions. Section 3 provides the main results on consistency, generalization bounds and convergence rates. Application to the prediction of affine causal models with exogenous covariates is carried out in Section 4, whereas Section 5 is devoted to the proofs of the main results.

2 Notations and assumptions

In the sequel, we assume that and are subsets of separable Banach spaces equipped with norms and respectively and consider the covering number as the complexity measure of . The complexity of the hypothesis set play a key role in such study. Recall that, for any , the -covering number of with the norm is the minimal number of balls of radius needed to cover ; that is,

where . For two Banach spaces and equipped with a norm , and any function set,

and for any , (simply when ) denotes the set of functions for some , such that and . When , we set . In the whole sequel, denotes and if are separable Banach spaces equipped with norms respectively, then we set for any . We set the following assumptions for the sequel.

-

(A1):

There exists such that is a subset of and .

-

(A2):

There exists such that, the loss function belongs to and .

Under (A1) and (A2), we have

| (2.1) |

Under the pre-compact condition in (A1), for any , the -covering number is finite. If is bounded, then examples of loss functions

| (2.2) |

fulfill the conditions in assumption (A2) with and respectively. In both cases, one can easily see that .

Definition 2.1

An -valued process is said to be -weakly dependent if there exists a function and a sequence decreasing to zero at infinity such that, for any with , () and for any -tuple and any -tuple with , the following inequality is fulfilled:

For example, we have the following choices of (see also [10]).

-

•

: the -weak dependence, then denote ;

-

•

: the -weak dependence, then denote ;

-

•

: the -weak dependence, then denote ;

-

•

: the -weak dependence, then denote .

One can easily see that for all . In the sequel, for each of the four choices of above, we set respectively, , , and .

Now, we set the weak-dependence assumption.

-

(A3):

Let be one of the four choices above. The process is stationary ergodic and -weakly dependent such that, there exist satisfying

(2.3)

3 Main results

3.1 Generalization bound and consistency

The following proposition provides an inequality of the deviation of the empirical risk around the risk, for any fixed predictor.

Proposition 3.1

Assume that the conditions (A1)-(A3) hold. Let . For all , , we have

for any real numbers and satisfying:

The next theorem provides a uniform concentration inequality between risk and its empirical version.

Theorem 3.2

Remark 3.3

Note that, as one can see in the proof of Theorem 3.2, (3.1) still holds with ; that is,

| (3.3) |

Therefore, by taking as in Remark 3.3, we have for all ,

| (3.4) |

Hence,

| (3.7) |

where the last inequality above holds since from (1.1). Thus, whenever the -covering number of the hypothesis set is finite for all , the EMR algorithm (1.1) with weakly dependent observations is consistent.

Let us stress that, the equation (3.1) in Theorem 3.2 is a non asymptotic result. The following theorem provides an asymptotic result with weaker condition than (A3).

Theorem 3.4

Assume that (A1)-(A2) hold and that is -weakly dependent with . For any and for large enough, we have for all ,

| (3.8) |

with , and some constant .

Under the assumption of Theorem 3.4 with for some and from [19], we can find a constant such that for any ,

| (3.9) |

Therefore, by taking as in Remark 3.3, we can see from Theorem 3.4 that . This shows the consistency of the EMR algorithm (1.1) under a weaker condition than (A3) when the -covering number of is finite for all .

3.2 Generalization error bounds and convergence rates

Let us derive the generalization error bounds of the ERM algorithm under the weak dependence conditions. We deal with the Hölder space with , and set the assumption,

-

(A4):

(with ) is pre-compact, , is a subset of a Hölder space for some , where denotes the closure of .

Let . Recall that, the Hölder space is a set of functions such that for any with , and for any multi-integers with , ; where denotes the integer part of . Equipped with the norm

is a Banach space (see [30]).

Proposition 3.5

In the proposition above, the bound (3.11) evaluates the estimation of the risk of from the empirical one, and the bound in (3.12) assesses how close this risk to the smallest possible risk on . The learning rate of the ERM algorithm in this general case is . The following proposition provides more faster learning rate.

Proposition 3.6

The learning rate in the bounds (3.14) and (3.15) is . In comparison with existing results based on a Hölder class, let us note that, this rate is the same to that obtained by [37] and [39] on uniformly and V-geometrically ergodic Markov chains, and is close to the one from exponentially strongly mixing and geometrically beta-mixing observations, see [36] and [35]. When , this learning rate is close to , which is the usual rate obtained in the i.i.d. case.

4 Applications to time series prediction

4.1 Affine causal models with exogenous covariates

Let be a process of covariates with values in , . Consider the class of affine causal models with exogenous covariates (see [12]) defined by

Class - A process belongs to - if it satisfies:

| (4.1) |

where are two measurable functions, and is a sequence of zero-mean i.i.d random variable satisfying for some and . Note that, if for some constant (absence of covariates) then, (4.1) reduces to the classical affine causal models studied among other by [5], [4], [3], [21]. Let us point out that, ARMAX, TARX, GARCH-X, APARCH-X (see [16]) models belong to the class -. Other examples of models such as APARCH-X, ARX()-ARCH() introduced by [12], belong to the class -. We refer also to [12], for the inference for -, in a semiparametric setting.

To study the stability properties of the model (4.1), we set following Lipschitz-type conditions on the function , or , see also [12]. In the sequel, denotes the null vector of any vector space. For or , consider the assumption,

Assumption A: and there exists two sequences of non-negative real numbers and satisfying , ; such that for any ,

where denotes a vector norm in , for any .

The next assumption is set on the function in the cases of ARCH-X type process.

Assumption A: Assume that , and there exists two sequences of non-negative real numbers and satisfying , ; such that for any ,

In the sequel, we make the convention that if A holds, then for all and if A holds, then for all . As in [12], we impose an autoregressive-type structure on the covariates:

| (4.2) |

where is a sequence of centered random variables with values in () such as is i.i.d and is a -valued function such that

| (4.3) |

for some , a non-negative sequence satisfying ; and for any random vector .

We consider model (4.1) with (4.2) and (4.3), and assume that A and (A or A) hold with

| (4.4) |

Under the conditions (4.4), there exists a -weakly dependent stationary, ergodic and non anticipative solution of (4.1) satisfying (see [12]).

Let us recall the -coefficient (see also [11]) for weak dependence. Let be a probability space, a -subalgebra of and a random variable with values in a separable Banach space , and satisfying . Define the -coefficient as

Now, consider an -valued strictly stationary process and set for all , . The dependence between the past and the -tuples future of the process may be assessed as follows. Define

The process is said to be -weakly dependent when tends to 0 as . This weak dependence structure implies other dependence notions such as , -weak dependence. Indeed, we have for all , , see Definition 2.1 and [10]. Hence, there exists a solution of (4.1) which is -weakly dependent. Moreover, according to [15], we have as ,

| (4.5) |

where and .

4.2 Prediction by learning theory

Let be a trajectory of a stationary and ergodic process that satisfies (4.1) and (4.2). The aim is to predict from the observations , for some fixed . We carry out the learning theory developed in Section 3 with: , , , and a loss function . The set of hypothesis is a family of predictors, denoted

| (4.6) |

where is a compact subset of , for some fixed . A target predictor (assumed to exist) with respect to is , with

| (4.7) |

and the predictor obtained from the ERM procedure is , with

| (4.8) |

For any and , denote,

Therefore, the prediction of according to the any predictor is .

Example of linear autoregressive predictors:

These predictors are defined for all by,

| (4.9) |

where (fixed), is a family of functions (for example, a wavelet basis, splines,), with , , and T denotes the transpose. For example, if , , , , , , then

| (4.10) |

Now, consider the learning framework above with a general family of predictor at (4.6), with the assumption that, for all , the function is continuous on . Let us check the assumptions (A1)-(A4) for the class -.

-

(i)

Assume that, for any , there exists a sequence of non-negative real numbers with for some , such that for any ,

(4.11) In addition, if is bounded or , then, (A1) holds. Note that, for a solution of (4.1) and (4.2), we have

where and for all . Under the condition (4.4) and for a suitable norm on , we have for all and can find a non-negative sequence satisfying such that

see the proof of Proposition 1 in [12]. Therefore, according to the proof of Theorem 3.1 in [15] and the proof of Proposition 4.1 in [2], there exists a function and a sequence of non-negative real numbers , satisfying such that,

and

Hence, if the innovations is bounded (i.e, there exists such that a.s.), then one can easily see that process is bounded by . Thus, can be chosen to be bounded and in addition to (4.11), (A1) holds.

- (ii)

- (iii)

-

(iv)

As above, under (4.4) and if the innovations is bounded, then is bounded and can be chosen to be a bounded subset of . Therefore, the example of the set of linear autoregressive predictors , defined in (4.10) with is pre-compact and is included in for all . Thus, (A4) holds for such linear predictors.

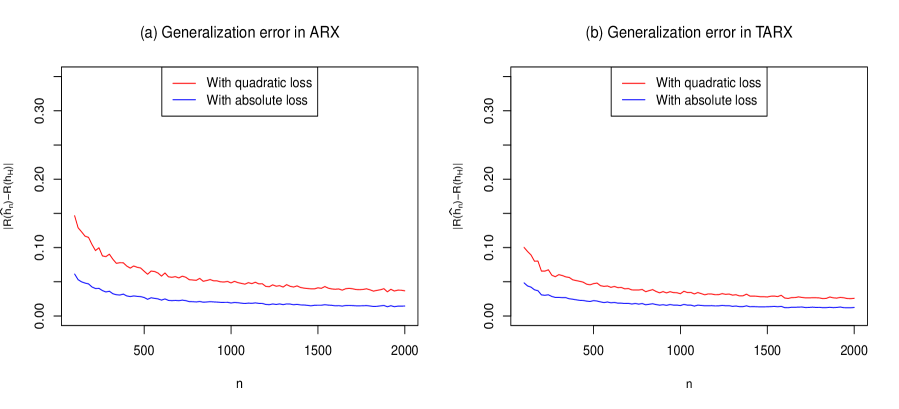

4.3 Some simulation results

We present some simulation experiments conducted to assess the generalization bound of the ERM algorithm. To this end, we consider the class of linear autoregressive predictors defined in (4.10) with (hence, ). We evaluate the difference in linear and nonlinear dynamic models.

Now, consider the ARX(2) and Threshold-ARX(1) (TARX) models given by:

| (4.12) | ||||

| (4.13) |

where represents innovations generated from a standardized uniform distribution and follows an 1-dimensional AR(1) process with nonzero mean and generated with a standardized innovations.

First, for each of the models (4.12) and (4.13), a sample with is generated and is estimated by where

Therefore, is estimated by . Secondly, for , a trajectory is generated to compute , which is equal to , where

Hence, is estimated by , with

where is generated from the model and is independent of the sample used for the estimation of . Each simulation for fixed is repeated 500 times and the Monte Carlo estimate of is computed. Figure 1 displays the curve of points obtained with the absolute and squared losses. One can see that, for both these losses, the value of approaching zero when the sample size increases. These findings are in accordance with the theoretical results of the consistency of the ERM algorithm within the class and the generalization bound (3.12) in Proposition 3.5 which decreases to zero with high probability.

5 Proofs of the main results

5.1 Proof of Proposition 3.1

Let .

Firstly, we derive an exponential inequality for .

For any , we have

Since , (from (A1) and (A2)), then the function is -Lipschitz. Thus, from the hereditary property of the weak dependence (see [10]), the process is stationary ergodic and weakly dependent. Moreover, under (A3), from Proposition 8 and as in Remark 9 in [14], one can see that the conditions of Theorem 1 in [14] are satisfied with , . Let a sequence such that . From Theorem 1 of [14], we have for all ,

| (5.1) |

with . Thus, the proposition follows.

5.2 Proof of Theorem 3.2

We proceed as in [36].

Let and .

Denote by (for ) the balls with center

and radius needed to cover ; i.e,

.

We have

| (5.2) |

Let us define

For any , we get

It comes that

which implies

| (5.3) |

From (5.3), we have

Then, taking , (5.2) implies

| (5.4) |

Hence, according to Proposition 3.1, we get

which establishes the Theorem 3.2.

5.3 Proof of Theorem 3.4

5.4 Proof of Proposition 3.5

(i) Let . Since is compact (from (A4)), there exists a constant such that (as in [34] and [36])

| (5.7) |

Note that, if , then . For , according to (3.2), we have

| (5.8) |

Let . Consider the following equation with respect to :

It is equivalent to

| (5.9) |

with

According to Lemma 7 in [8], the equation (5.9) has an unique positive solution satisfying

| (5.10) |

Note that, since , we get

with . Hence, according to (3.10) and (5.10) , one can easily see that . From (5.4), we deduce that with probability at least ,

which implies

| (5.11) |

Hence, the first part of the proposition holds.

(ii) Let us note that, going along similar lines as in Proposition 3.1, we can establish that the following inequality also follows for all :

Thus, taking (as in Remark 3.3), with the function , it comes that

| (5.12) |

where .

Now, consider the equation (with respect to )

A solution of this equation is

Thus, from (5.4), we have

with probability at least . Since (because ), we deduce

| (5.13) |

Combining the inequalities (5.11) and (5.13), with probability at least , we obtain

This completes the proof of the proposition.

5.5 Proof of Proposition 3.6

(i) According to (3.9), we can take ; which gives . Thus, for , by using (3.8) and (5.7) and going as in the proof of Proposition 3.5, we get for large enough,

| (5.14) |

Now, consider the following equation with respect to :

which is the equivalent to

with

This equation has an unique positive solution satisfying (see also [8])

Note that, since , for large enough, we have

Moreover,

Therefore, for and from the inequality for , we get,

Hence,

In the same way,

Then, for large enough and

it holds that .

Thus, using (5.14), we deduce that with probability at least ,

| (5.15) |

Hence, the part (i) holds.

References

- [1] Alquier, P., Li, X., and Wintenberger, O. Prediction of time series by statistical learning: general losses and fast rates. Dependence Modeling 1, 2013 (2013), 65–93.

- [2] Alquier, P., and Wintenberger, O. Model selection for weakly dependent time series forecasting. Bernoulli 18, 3 (2012), 883–913.

- [3] Bardet, J.-M., Kamila, K., and Kengne, W. Consistent model selection criteria and goodness-of-fit test for common time series models. Electronic Journal of Statistics 14, 1 (2020), 2009–2052.

- [4] Bardet, J.-M., Kengne, W., and Wintenberger, O. Multiple breaks detection in general causal time series using penalized quasi-likelihood. Electronic Journal of Statistics 6 (2012), 435–477.

- [5] Bardet, J.-M., and Wintenberger, O. Asymptotic normality of the quasi-maximum likelihood estimator for multidimensional causal processes. The Annals of Statistics 37, 5B (2009), 2730–2759.

- [6] Blanchard, G., and Zadorozhnyi, O. Concentration of weakly dependent banach-valued sums and applications to statistical learning methods. Bernoulli 25, 4B (2019), 3421–3458.

- [7] Bousquet, O., Boucheron, S., and Lugosi, G. Introduction to statistical learning theory. In Summer school on machine learning (2003), Springer, pp. 169–207.

- [8] Cucker, F., and Smale, S. Best choices for regularization parameters in learning theory: on the bias-variance problem. Foundations of computational Mathematics 2, 4 (2002), 413–428.

- [9] Cucker, F., and Smale, S. On the mathematical foundations of learning. Bulletin of the American mathematical society 39, 1 (2002), 1–49.

- [10] Dedecker, J., Doukhan, P., Lang, G., León, J. R., Louhichi, S., and Prieur, C. Weak dependence: With Examples and Applications. Lecture Notes in Statistics 190, Springer-Verlag, New York, 2007.

- [11] Dedecker, J., and Prieur, C. Coupling for -dependent sequences and applications. Journal of Theoretical Probability 17, 4 (2004), 861–885.

- [12] Diop, M. L., and Kengne, W. Inference and model selection in general causal time series with exogenous covariates. Electronic Journal of Statistics 16, 1 (2022), 116–157.

- [13] Doukhan, P., and Louhichi, S. A new weak dependence condition and applications to moment inequalities. Stochastic processes and their applications 84, 2 (1999), 313–342.

- [14] Doukhan, P., and Neumann, M. H. Probability and moment inequalities for sums of weakly dependent random variables, with applications. Stochastic Processes and their Applications 117, 7 (2007), 878–903.

- [15] Doukhan, P., and Wintenberger, O. Weakly dependent chains with infinite memory. Stochastic Processes and their Applications 118, 11 (2008), 1997–2013.

- [16] Francq, C., et al. Qml inference for volatility models with covariates. Econometric Theory 35, 1 (2019), 37–72.

- [17] Hang, H., and Steinwart, I. Fast learning from -mixing observations. Journal of Multivariate Analysis 127 (2014), 184–199.

- [18] Hang, H., and Steinwart, I. A bernstein-type inequality for some mixing processes and dynamical systems with an application to learning. The Annals of Statistics 45, 2 (2017), 708–743.

- [19] Hwang, E., and Shin, D. W. A study on moment inequalities under a weak dependence. Journal of the Korean Statistical Society 42, 1 (2013), 133–141.

- [20] Hwang, E., and Shin, D. W. A note on exponential inequalities of -weakly dependent sequences. Communications for Statistical Applications and Methods 21, 3 (2014), 245–251.

- [21] Kengne, W. Strongly consistent model selection for general causal time series. Statistics & Probability Letters 171 (2021), 109000.

- [22] Kuznetsov, V., and Mohri, M. Time series prediction and online learning. In Conference on Learning Theory (2016), PMLR, pp. 1190–1213.

- [23] Kuznetsov, V., and Mohri, M. Generalization bounds for non-stationary mixing processes. Machine Learning 106, 1 (2017), 93–117.

- [24] Kuznetsov, V., and Mohri, M. Theory and algorithms for forecasting time series. arXiv preprint arXiv:1803.05814 (2018).

- [25] Mohri, M., and Rostamizadeh, A. Stability bounds for non-iid processes. Advances in Neural Information Processing Systems 20 (2007).

- [26] Mohri, M., and Rostamizadeh, A. Rademacher complexity bounds for non-iid processes. Advances in Neural Information Processing Systems 21 (2008).

- [27] Mohri, M., Rostamizadeh, A., and Talwalkar, A. Foundations of machine learning. MIT press, 2018.

- [28] Steinwart, I., and Christmann, A. Fast learning from non-iid observations. Advances in neural information processing systems 22 (2009).

- [29] Steinwart, I., Hush, D., and Scovel, C. Learning from dependent observations. Journal of Multivariate Analysis 100, 1 (2009), 175–194.

- [30] Triebel, H. Theory of function spaces II, vol. 84 of Monogr. Math., Basel. Basel: Birkhäuser Verlag, 1992.

- [31] Vapnik, V. The nature of statistical learning theory. Springer science & business media, 1999.

- [32] Vidyasagar, M. Learning and generalisation: with applications to neural networks. Springer Science & Business Media, 2013.

- [33] Xu, J., Tang, Y. Y., Zou, B., Xu, Z., Li, L., and Lu, Y. Generalization performance of gaussian kernels svmc based on markov sampling. Neural networks 53 (2014), 40–51.

- [34] Zhou, D.-X. Capacity of reproducing kernel spaces in learning theory. IEEE Transactions on Information Theory 49, 7 (2003), 1743–1752.

- [35] Zou, B., Chen, R., and Xu, Z. Learning performance of tikhonov regularization algorithm with geometrically beta-mixing observations. Journal of Statistical Planning and Inference 141, 3 (2011), 1077–1087.

- [36] Zou, B., Li, L., and Xu, Z. The generalization performance of erm algorithm with strongly mixing observations. Machine learning 75, 3 (2009), 275–295.

- [37] Zou, B., Xu, Z., and Chang, X. Generalization bounds of erm algorithm with v-geometrically ergodic markov chains. Advances in Computational Mathematics 36, 1 (2012), 99–114.

- [38] Zou, B., Xu, Z.-b., and Xu, J. Generalization bounds of erm algorithm with markov chain samples. Acta Mathematicae Applicatae Sinica, English Series 30, 1 (2014), 223–238.

- [39] Zou, B., Zhang, H., and Xu, Z. Learning from uniformly ergodic markov chains. Journal of Complexity 25, 2 (2009), 188–200.