Causal Estimation for Text Data with (Apparent) Overlap Violations

Abstract

Consider the problem of estimating the causal effect of some attribute of a text document; for example: what effect does writing a polite vs. rude email have on response time? To estimate a causal effect from observational data, we need to adjust for confounding aspects of the text that affect both the treatment and outcome—e.g., the topic or writing level of the text. These confounding aspects are unknown a priori, so it seems natural to adjust for the entirety of the text (e.g., using a transformer). However, causal identification and estimation procedures rely on the assumption of overlap: for all levels of the adjustment variables, there is randomness leftover so that every unit could have (not) received treatment. Since the treatment here is itself an attribute of the text, it is perfectly determined, and overlap is apparently violated. The purpose of this paper is to show how to handle causal identification and obtain robust causal estimation in the presence of apparent overlap violations. In brief, the idea is to use supervised representation learning to produce a data representation that preserves confounding information while eliminating information that is only predictive of the treatment. This representation then suffices for adjustment and satisfies overlap. Adapting results on non-parametric estimation, we find that this procedure is robust to conditional outcome misestimation, yielding a low-absolute-bias estimator with valid uncertainty quantification under weak conditions. Empirical results show strong improvements in bias and uncertainty quantification relative to the natural baseline. Code, demo data and a tutorial are available at https://github.com/gl-ybnbxb/TI-estimator.

1 Introduction

We consider the problem of estimating the causal effect of an attribute of a passage of text on some downstream outcome. For example, what is the effect of writing a polite or rude email on the amount of time it takes to get a response? In principle, we might hope to answer such questions with a randomized experiment. However, this can be difficult in practice—e.g., if poor outcomes are costly or take long to gather. Accordingly, in this paper, we will be interested in estimating such effects using observational data.

There are three steps to estimating causal effects using observational data (See Chapter 36 Murphy (2023)). First, we need to specify a concrete causal quantity as our estimand. That is, give a formal quantity target of estimation corresponding to the high-level question of interest. The next step is causal identification: we need to prove that this causal estimator can, in principle, be estimated using only observational data. The standard approach for identification relies on adjusting for confounding variables that affect both the treatment and the outcome. For identification to hold, our adjustment variables must satisfy two conditions: unconfoundedness and overlap. The former requires the adjustment variables contain sufficient information on all common causes. The latter requires that the adjustment variable does not contain enough information about treatment assignment to let us perfectly predict it. Intuitively, to disentangle the effect of treatment from the effect of confounding, we must observe each treatment state at all levels of confounding. The final step is estimation using a finite data sample. Here, overlap also turns out to be critically important as a major determinant of the best possible accuracy (asymptotic variance) of the estimator Chernozhukov et al. (2016).

Since the treatment is a linguistic property, it is often reasonable to assume that text data has information about all common causes of the treatment and the outcome. Thus, we may aim to satisfy unconfoundedness in the text setting by adjusting for all the text as the confounding part. However, doing so brings about overlap violation. Since the treatment is a linguistic property determined by the text, the probability of treatment given any text is either 0 or 1. The polite/rude tone is determined by the text itself. Therefore, overlap does not hold if we naively adjust for all the text as the confounding part. This problem is the main subject of this paper. Or, more precisely, our goal is to find a causal estimand, causal identification conditions, and a robust estimation procedure that will allow us to effectively estimate causal effects even in the presence of such (apparent) overlap violations.

In fact, there is an obvious first approach: simply use a standard plug-in estimation procedure that relies only on modeling the outcome from the text and treatment variables. In particular, do not make any explicit use of the propensity score, the probability each unit is treated. Pryzant et al. (2020) use an approach of this kind and show it is reasonable in some situations. Indeed, we will see in Sections 3 and 4 that this procedure can be interpreted as a point estimator of a controlled causal effect. Even once we understand what the implied causal estimand is, this approach has a major drawback: the estimator is only accurate when the text-outcome model converges at a very fast rate. This is particularly an issue in the text setting, where we would like to use large, flexible, deep learning models for this relationship. In practice, we find that this procedure works poorly: the estimator has significant absolute bias and (the natural approach to) uncertainty quantification almost never includes the estimand true value; see Section 5.

The contribution of this paper is a method for robustly estimating causal effects in text. The main idea is to break estimation into a two-stage procedure, where in the first stage we learn a representation of the text that preserves enough information to account for confounding, but throws away enough information to avoid overlap issues. Then, we use this representation as the adjustment variables in a standard double machine-learning estimation procedure Chernozhukov et al. (2016; 2017a). To establish this method, the contributions of this paper are:

-

1.

We give a formal causal estimand corresponding to the text-attribute question. We show this estimand is causally identified under weak conditions, even in the presence of apparent overlap issues.

-

2.

We show how to efficiently estimate this quantity using the adapted double-ML technique just described. We show that this estimator admits a central limit theorem at a fast () rate under weak conditions on the rate at which the ML model learns the text-outcome relationship (namely, convergence at rate). This implies absolute bias decreases rapidly, and an (asymptotically) valid procedure for uncertainty quantification.

-

3.

We test the performance of this procedure empirically, finding significant improvements in bias and uncertainty quantification relative to the outcome-model-only baseline.

Related work

The most related literature is on causal inference with text variables. Papers include treating text as treatment Pryzant et al. (2020); Wood-Doughty et al. (2018); Egami et al. (2018); Fong & Grimmer (2016); Wang & Culotta (2019); Tan et al. (2014)), as outcome Egami et al. (2018); Sridhar & Getoor (2019), as confounder Veitch et al. (2019); Roberts et al. (2020); Mozer et al. (2020); Keith et al. (2020), and discovering or predicting causality from text del Prado Martin & Brendel (2016); Tabari et al. (2018); Balashankar et al. (2019); Mani & Cooper (2000). There are also numerous applications using text to adjust for confounding (e.g., Olteanu et al., 2017; Hall, 2017; Kiciman et al., 2018; Sridhar et al., 2018; Sridhar & Getoor, 2019; Saha et al., 2019; Karell & Freedman, 2019; Zhang et al., 2020). Of these, Pryzant et al. (2020) also address non-parametric estimation of the causal effect of text attributes. Their focus is primarily on mismeasurement of the treatments, while our motivation is robust estimation.

This paper also relates to work on causal estimation with (near) overlap violations. D’Amour et al. (2021) points out high-dimensional adjustment (e.g., Rassen et al., 2011; Louizos et al., 2017; Li et al., 2016; Athey et al., 2017) suffers from overlap issues. Extra assumptions such as sparsity are often needed to meet the overlap condition. These results do not directly apply here because we assume there exists a low-dimensional summary that suffices to handle confounding.

D’Amour & Franks (2021) studies summary statistics that suffice for identification, which they call deconfounding scores. The supervised representation learning approach in this paper can be viewed as an extremal case of the deconfounding score. However, they consider the case where ordinary overlap holds with all observed features, with the aim of using both the outcome model and propensity score to find efficient statistical estimation procedures (in a linear-gaussian setting). This does not make sense in the setting we consider. Additionally, our main statistical result (robustness to outcome model estimation) is new.

2 Notation and Problem Setup

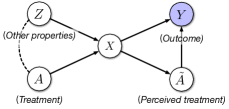

We follow the causal setup of Pryzant et al. (2020). We are interested in estimating the causal effect of treatment on outcome . For example, how does writing a negative sentiment () review () affect product sales ()? There are two immediate challenges to estimating such effects with observed text data. First, we do not actually observe , which is the intent of the writer. Instead, we only observe , a version of that is inferred from the text itself. In this paper, we will assume that almost surely—e.g., a reader can always tell if a review was meant to be negative or positive. This assumption is often reasonable, and follows Pryzant et al. (2020). The next challenge is that the treatment may be correlated with other aspects of the text () that are also relevant to the outcome—e.g., the product category of the item being reviewed. Such can act as confounding variables, and must somehow be adjusted for in a causal estimation problem.

Each unit is drawn independently and identically from an unknown distribution . Figure 1 shows the causal relationships among variables, where solid arrows represent causal relations, and the dotted line represents possible correlations between two variables. We assume that text contains all common causes of and the outcome .

3 Identification and Causal estimand

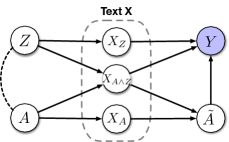

The first task is to translate the qualitative causal question of interest—what is the effect of on —into a causal estimand. This estimand must both be faithful to the qualitative question and be identifiable from observational data under reasonable assumptions. The key challenges here are that we only observe (not itself), there are unknown confounding variables influencing the text, and is a deterministic function of the text, leading to overlap violations if we naively adjust for all the text. Our high-level idea is to split the text into abstract (unknown) parts depending on whether they are confounding—affect both and —or whether they affect alone. The part of the text that affects only is not necessary for causal adjustment, and can be thrown away. If this part contains “enough” information about , then throwing it away can eliminate our ability to perfectly predict , thus fixing the overlap issue. We now turn to formalizing this idea, showing how it can be used to define an estimand and to identify this estimand from observational data.

Causal model

The first idea is to decompose the text into three parts: one part affected by only , one part affected interactively by and , and another part affected only by . We use , and to denote them, respectively; see Figure 2 for the corresponding causal model. Note that there could be additional information in the text in addition to these three parts. However, since they are irrelevant to both and , we do not need to consider them in the model.

Controlled direct effect (CDE)

The treatment affects the outcome through two paths. Both “directly” through —the part of the text determined just by the treatment—and also through a path going through —the part of the text that relies on interaction effects with other factors. Our formal causal effect aims at capturing the effect of through only the first, direct, path.

| (3.1) |

Here, is Pearl’s do notation, and the estimand is a variant of the controlled direct effect (Pearl, 2009). Intuitively, it can be interpreted as the expected change in the outcome induced by changing the treatment from 1 to 0 while keeping part of the text affected by the same as it would have been had we set . This is a reasonable formalization of the qualitative “effect of on ”. Of course, it is not the only possible formalization. Its advantage is that, as we will see, it can be identified and estimated under reasonable conditions.

Identification

To identify we must rewrite the expression in terms of observable quantities. There are three challenges: we need to get rid of the operator, we don’t observe (only ), and the variables are unknown (they are latent parts of ).

Informally, the identification argument is as follows. First, block all backdoor paths (common causes) in Figure 2. Moreover, because we have thrown away , we now satisfy overlap. Accordingly, the operator can be replaced by conditioning following the usual causal-adjustment argument. Next, almost surely, so we can just replace with . Now, our estimand has been reduced to:

| (3.2) |

The final step is to deal with the unknown . To fix this issue, we first define the conditional outcome according to:

| (3.3) |

A key insight here is that, subject to the causal model in Figure 2, we have . But this is exactly the quantity in Equation 3.2. Moreover, is an observable data quantity (it depends only on the distribution of the observed quantities). In summary:

Theorem 1.

Assume the following:

1. (Causal structure) The causal relationships among , , , , and satisfy the causal DAG in Figure 2;

2. (Overlap) ;

3. (Intention equals perception) almost surely with respect to all interventional distributions.

Then, the CDE is identified from observational data as

| (3.4) |

where .

The proof is in Appendix B.

We give the result in terms of an abstract sufficient statistic to emphasize that the actual conditional expectation model is not required, only some statistic that is informationally equivalent. We emphasize that, regardless of whether the overlap condition holds or not, the propensity score of is accessible and meaningful. Therefore, we can easily identify when identification fails as long as is well-estimated.

4 Method

Our ultimate goal is to draw a conclusion about whether the treatment has a causal effect on the outcome. Following the previous section, we have reduced this problem to estimating , defined in Theorem 1. The task now is to develop an estimation procedure, including uncertainty quantification.

4.1 Outcome only estimator

We start by introducing the naive outcome only estimator as a first approach to CDE estimation. The estimator is adapted from Pryzant et al. (2020). The observation here is that, taking in Equation 3.4, we have

| (4.1) |

Since is a function of the whole text data , it is estimable from observational data. Namely, it is the solution to the square error risk:

| (4.2) |

With a finite sample, we can estimate as by fitting a machine-learning model to minimize the (possibly regularized) square error empirical risk. That is, fit a model using mean square error as the objective function. Then, a straightforward estimator is:

| (4.3) |

where is the number of treated units.

It should be noted that the model for is not arbitrary. One significant issue for those models which directly regress on and is when overlap does not hold, the model could ignore and only use as the covariate. As a result, we need to choose a class of models that force the use of the treatment . To address this, we use a two-headed model that regress on for separately in the conditional outcome learning model (See Section 4.2 and Figure 3).

As discussed in the introduction Section 1, this estimator yields a consistent point estimate, but does not offer a simple approach for uncertainty quantification. A natural guess for an estimate of its variance is:

| (4.4) |

That is, just compute the variance of the mean conditional on the fitted model. However, this procedure yields asymptotically valid confidence intervals only if the outcome model converges extremely quickly; i.e., if . We could instead bootstrap, refitting on each bootstrap sample. However, with modern language models, this can be prohibitively computationally expensive.

4.2 Treatment Ignorant Effect Estimation (TI-estimator)

Following Theorem 1, it suffices to adjust for . Accordingly, we use the following pipeline. We first estimate and (using a neural language model), as with the outcome-only estimator. Then, we take and estimate . That is, we estimate the propensity score corresponding to the estimated representation. Finally, we plug the estimated and into a standard double machine learning estimator (Chernozhukov et al., 2016).

We describe the three steps in detail.

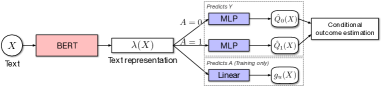

Q-Net

In the first stage, we estimate the conditional outcomes and hence obtain the estimated two-dimensional confounding vector . For concreteness, we will use the dragonnet architecture of Shi et al. (2019). Specifically, we train DistilBERT (Sanh et al., 2019) modified to include three heads, as shown in Figure 3. Two of the heads correspond to and respectively. As discussed in the Section 4.1, applying two heads can force the model to use the treatment . The final head is a single linear layer predicting the treatment. This propensity score prediction head can help prevent (implicit) regularization of the model from throwing away information that is necessary for identification. The output of this head is not used for the estimation since its purpose is to force the DistilBERT representation to preserve all confounding information. This has been shown to improve causal estimation (Shi et al., 2019; Veitch et al., 2019).

We train the model by minimizing the objective function

| (4.5) |

where are the model parameters, , are hyperparameters and is the masked language modeling objective of DistilBERT.

There is a final nuance. In practice, we split the data into -folds. For each fold , we train a model on the other folds. Then, we make predictions for the data points in fold using . Slightly abusing notation, we use to denote the predictions obtained in this manner.

Propensity score estimation

Next, we define and estimate the propensity score . To do this, we fit a non-parametric estimator to the binary classification task of predicting from in a cross fitting or K-fold fashion. The important insight here is that since is 2-dimensional, non-parametric estimation is possible at a fast rate. In Section 5, we try several methods and find that kernel regression usually works well.

We also define as the idealized propensity score. The idea is that as , we will also have so long as we have a valid non-parametric estimate.

CDE estimation

The final stage is to combine the estimated outcome model and propensity score into a estimator. To that end, we define the influence curve of as follows:

| (4.6) |

where . Then, the standard double machine learning estimator of Chernozhukov et al. (2016), and the -level confidence interval of this estimator, is given by

| (4.7) |

where

| (4.8) |

, is the -upper quantile of the standard normal, and is the sample standard deviation.

Validity

We now have an estimation procedure. It remains to give conditions under which this procedure is valid. In particular, we require that it should yield a consistent estimate and asymptotically correct confidence intervals.

Theorem 2.

Assume the following.

-

1.

The mis-estimation of conditional outcomes can be bounded as follows

(4.9) -

2.

The propensity score function is Lipschitz continuous on , and ,

-

3.

The propensity score estimate converges at least as quickly as k nearest neighbor;

i.e., Györfi et al. (2002); -

4.

There exist positive constants , , , and such that

Then, the estimator is consistent and

| (4.10) |

where .

The proof is provided in Appendix A.

The key point from this theorem is that we get asymptotic normality at the (fast) -rate while requiring only a slow () convergence rate of . Intuitively, the reason is simply that, because is only 2-dimensional, it is always possible to nonparametrically estimate the propensity score from at a fast rate—even naive KNN works! Effectively, this means the rate at which we estimate the true propensity score is dominated by the rate at which we estimate , which is in turn determined by the rate for . Now, the key property of the double ML estimator is that convergence only depends on the product of the convergence rates of and . Accordingly, this procedure is robust in the sense that we only need to estimate at the square root of the rate we needed for the naive -only procedure. This is much more plausible in practice. As we will see in Section 5, the TI-estimator dramatically improves the quality of the estimated confidence intervals and reduces the absolute bias of estimation.

Remark 3.

In addition to robustness to noisy estimation of , there are some other advantages this estimation procedure inherits from the double ML estimator. If is consistent, then the estimator is nonparametrically efficient in the sense that no other non-parametric estimator has a smaller asymptotic variance. That is, the procedure using the data as efficiently as possible.

5 Experiments

We empirically study the method’s capability to provide accurate causal estimates with good uncertainty quantification Testing using semi-synthetic data (where ground truth causal effects are known), we find that the estimation procedure yields accurate causal estimates and confidence intervals. In particular, the TI-estimator has significantly lower absolute bias and vastly better uncertainty quantification than the -only method.

Additionally, we study the effect of the choice of nonparametric propensity score estimator and the choice of double machine-learning estimator, and the method’s robustness in regard to ’s miscalibration. These results are reported in Appendices C and D. Although these choices do not matter asymptotically, we find they have a significant impact in actual finite sample estimation. We find that, in general, kernel regression works well for propensity score estimation and the vanilla the Augmented Inverse Probability of Treatment weighted Estimator (AIPTW) corresponding to the CDE works well.

Finally, we reproduce the real-data analysis from Pryzant et al. (2020). We find that politeness has a positive effect on reducing email response time.

5.1 Amazon Reviews

| Noise: | Low | High | |||||||

|---|---|---|---|---|---|---|---|---|---|

| True CDE: | 1.0 | 0.0 | 1.0 | 0.0 | |||||

| Confounding: | Low | High | Low | High | Low | High | Low | High | |

| 0.100 | 0.376 | 0.076 | 0.326 | 0.563 | 0.548 | 0.502 | 0.498 | ||

| 0.069 | 0.059 | 0.114 | 0.074 | 0.088 | 0.049 | 0.002 | 0.089 | ||

| Noise: | Low | High | |||||||

|---|---|---|---|---|---|---|---|---|---|

| True CDE: | 1.0 | 0.0 | 1.0 | 0.0 | |||||

| Confounding: | Low | High | Low | High | Low | High | Low | High | |

| 0% | 0% | 2% | 0% | 0% | 0% | 0% | 0% | ||

| 57% | 84% | 57% | 79% | 87% | 80% | 77% | 81% | ||

Dataset

We closely follow the setup of Pryzant et al. (2020). We use publicly available Amazon reviews for music products as the basis for our semi-synthetic data. We include reviews for mp3, CD and vinyl, and among these exclude reviews for products costing more than $100 or shorter than 5 words. The treatment is whether the review is five stars () or one/two stars ().

To have a ground truth causal effect, we must now simulate the outcome. To produce a realistic dataset, we choose a real variable as the confounder. Namely, the confounder is whether the product is a CD () or not (). Then, outcome is generated according to . The true causal effect is controlled by . We choose to generate data with and without causal effects. In this setting, is the oracle value of our causal estimand. The strength of confounding is controlled by . We choose . The ground-truth propensity score is . We set it to have the value and (by subsampling the data). is an offset , where , are estimated from data. Finally, the noise level is controlled by ; we choose and to simulate data with small and large noise. The final dataset has data entries.

Protocol

For the language model, we use the pretrained distilbert-base-uncased model provided by the transformers package. The model is trained in the k-folding fashion with 5 folds. We apply the Adam optimizer (Kingma & Ba, 2014) with a learning rate of and a batch size of 64. The maximum number of epochs is set as 20, with early stopping based on validation loss with a patience of 6. Each experiment is replicated with five different seeds and the final predictions are obtained by averaging the predictions from the 5 resulting models. The propensity model is implemented by running the Gaussian process regression using GaussianProcessClassifier in the sklearn package with DotProduct + WhiteKernel kernel. (We choose different random state for the GPR to guarantee the convergence of the GPR.) The coverage experiment uses 100 replicates.

Results

The main question here is the efficacy of the estimation procedure. Table 1(b) compares the outcome-only estimator and the estimator . First, the absolute bias of the new method is significantly lower than the absolute bias of the outcome-only estimator. This is particularly true where there is moderate to high levels of confounding. Next, we check actual coverage rates over 100 replicates of the experiment. First, we find that the naive approach for the outcome-only estimator fails completely. The nominal confidence interval almost never actually includes the true effect. It is wildly optimistic. By contrast, the confidence intervals from the new method often cover the true value. This is an enormous improvement over the baseline. Nevertheless, they still do not actually achieve their nominal (95%) coverage. This may be because the estimate is still not good enough for the asymptotics to kick in, and we are not yet justified in ignoring the uncertainty from model fitting.

5.2 Application: Consumer Complaints to the Financial Protection Bureau

We follow the same pipeline of the real data experiment in (Pryzant et al., 2020, §6.2). The dataset is consumers complaints made to the financial protection. Treatment is politeness (measured using Yeomans et al. (2018)) and the outcome is a binary indicator of whether complaints receive a response within 15 days.

We use the same training procedure as for the simulation data. Table 2 shows point estimates and their 95% confidence intervals. Notice that the naive estimator show a significant negative effect of politeness on reducing response time. On the other hand, the more accurate AIPTW method as well as the outcome-only estimator have confidence intervals that cover only positive values, so we conclude that consumers’ politeness has a positive effect on response time. This matches our intuitions that being more polite should increase the probability of receiving a timely reply.

| Estimator | CDE | Confidence Interval |

|---|---|---|

| unadjusted | -0.038 | [ -0.0679, -0.0073 ] |

| 0.195 | [ 0.1910, 0.1993 ] | |

| 0.200 | [ 0.1708, 0.2288 ] |

6 Discussion

In this paper, we address the estimation of the causal effect of a text document attribute using observational data. The key challenge is that we must adjust for the text—to handle confounding—but adjusting for all of the text violates overlap. We saw that this issue could be effectively circumvented with a suitable choice of estimand and estimation procedure. In particular, we have seen an estimand that corresponds to the qualitative causal question, and an estimator that is valid even when the outcome model is learned slowly. The procedure also circumvents the need for bootstrapping, which is prohibitively expensive in our setting.

There are some limitations. The actual coverage proportion of our estimator is below the nominal level. This is presumably due to the imperfect fit of the conditional outcome model. Diagnostics (see Appendix D) show that as conditional outcome estimations become more accurate, the TI estimator becomes less biased, and its coverage increases. It seems plausible that the issue could be resolved by using more powerful language models.

Although we have focused on text in this paper, the problem of causal estimation with apparent overlap violation exists in any problem where we must adjust for unstructured and high-dimensional covariates. Another interesting direction for future work is to understand how analogous procedures work outside the text setting.

Acknowledgement

Thanks to Alexander D’Amour for feedback on an earlier draft. We acknowledge the University of Chicago’s Research Computing Center for providing computing resources. This work was partially supported by Open Philanthropy.

References

- Athey et al. (2017) Susan Athey, Guido Imbens, Thai Pham, and Stefan Wager. Estimating average treatment effects: Supplementary analyses and remaining challenges. American Economic Review, 107(5):278–81, 2017.

- Balashankar et al. (2019) Ananth Balashankar, Sunandan Chakraborty, Samuel Fraiberger, and Lakshminarayanan Subramanian. Identifying predictive causal factors from news streams. In Proceedings of the 2019 Conference on Empirical Methods in Natural Language Processing and the 9th International Joint Conference on Natural Language Processing (EMNLP-IJCNLP), pp. 2338–2348, 2019.

- Chernozhukov et al. (2016) Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and causal parameters. arXiv preprint arXiv:1608.00060, 2016.

- Chernozhukov et al. (2017a) Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, and Whitney Newey. Double/debiased/neyman machine learning of treatment effects. American Economic Review, 107(5):261–65, May 2017a. doi: 10.1257/aer.p20171038. URL http://www.aeaweb.org/articles?id=10.1257/aer.p20171038.

- Chernozhukov et al. (2017b) Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 2017b.

- D’Amour & Franks (2021) Alexander D’Amour and Alexander Franks. Deconfounding scores: Feature representations for causal effect estimation with weak overlap. arXiv preprint arXiv:2104.05762, 2021.

- D’Amour et al. (2021) Alexander D’Amour, Peng Ding, Avi Feller, Lihua Lei, and Jasjeet Sekhon. Overlap in observational studies with high-dimensional covariates. Journal of Econometrics, 221(2):644–654, 2021.

- del Prado Martin & Brendel (2016) Fermin Moscoso del Prado Martin and Christian Brendel. Case and cause in icelandic: Reconstructing causal networks of cascaded language changes. In Proceedings of the 54th Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers), pp. 2421–2430, 2016.

- Egami et al. (2018) Naoki Egami, Christian J Fong, Justin Grimmer, Margaret E Roberts, and Brandon M Stewart. How to make causal inferences using texts. arXiv preprint arXiv:1802.02163, 2018.

- Fong & Grimmer (2016) Christian Fong and Justin Grimmer. Discovery of treatments from text corpora. In Proceedings of the 54th Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers), pp. 1600–1609, 2016.

- Györfi et al. (2002) László Györfi, Michael Kohler, Adam Krzyzak, Harro Walk, et al. A distribution-free theory of nonparametric regression, volume 1. Springer, 2002.

- Hall (2017) Allie Hall. How hiring language reinforces pink collar jobs. Textio Word Nerd, 2017.

- Karell & Freedman (2019) Daniel Karell and Michael Freedman. Rhetorics of radicalism. American Sociological Review, 84(4):726–753, 2019.

- Keith et al. (2020) Katherine A Keith, David Jensen, and Brendan O’Connor. Text and causal inference: A review of using text to remove confounding from causal estimates. arXiv preprint arXiv:2005.00649, 2020.

- Kiciman et al. (2018) Emre Kiciman, Scott Counts, and Melissa Gasser. Using longitudinal social media analysis to understand the effects of early college alcohol use. In Twelfth International AAAI Conference on Web and Social Media, 2018.

- Kingma & Ba (2014) Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980, 2014.

- Li et al. (2016) Sheng Li, Nikos Vlassis, Jaya Kawale, and Yun Fu. Matching via dimensionality reduction for estimation of treatment effects in digital marketing campaigns. In IJCAI, pp. 3768–3774, 2016.

- Louizos et al. (2017) Christos Louizos, Uri Shalit, Joris M Mooij, David Sontag, Richard Zemel, and Max Welling. Causal effect inference with deep latent-variable models. Advances in neural information processing systems, 30, 2017.

- Mani & Cooper (2000) Subramani Mani and Gregory F Cooper. Causal discovery from medical textual data. In Proceedings of the AMIA Symposium, pp. 542. American Medical Informatics Association, 2000.

- Mozer et al. (2020) Reagan Mozer, Luke Miratrix, Aaron Russell Kaufman, and L Jason Anastasopoulos. Matching with text data: An experimental evaluation of methods for matching documents and of measuring match quality. Political Analysis, 28(4):445–468, 2020.

- Murphy (2023) Kevin P. Murphy. Probabilistic Machine Learning: Advanced Topics. MIT Press, 2023. URL http://probml.github.io/book2.

- Olteanu et al. (2017) Alexandra Olteanu, Onur Varol, and Emre Kiciman. Distilling the outcomes of personal experiences: A propensity-scored analysis of social media. In Proceedings of the 2017 ACM Conference on Computer Supported Cooperative Work and Social Computing, pp. 370–386, 2017.

- Pearl (2009) J. Pearl. Causality. Cambridge University Press, 2nd edition, 2009.

- Pryzant et al. (2020) Reid Pryzant, Dallas Card, Dan Jurafsky, Victor Veitch, and Dhanya Sridhar. Causal effects of linguistic properties. arXiv preprint arXiv:2010.12919, 2020.

- Rassen et al. (2011) Jeremy A Rassen, Robert J Glynn, M Alan Brookhart, and Sebastian Schneeweiss. Covariate selection in high-dimensional propensity score analyses of treatment effects in small samples. American journal of epidemiology, 173(12):1404–1413, 2011.

- Roberts et al. (2020) Margaret E Roberts, Brandon M Stewart, and Richard A Nielsen. Adjusting for confounding with text matching. American Journal of Political Science, 64(4):887–903, 2020.

- Saha et al. (2019) Koustuv Saha, Benjamin Sugar, John Torous, Bruno Abrahao, Emre Kıcıman, and Munmun De Choudhury. A social media study on the effects of psychiatric medication use. In Proceedings of the International AAAI Conference on Web and Social Media, volume 13, pp. 440–451, 2019.

- Sanh et al. (2019) Victor Sanh, Lysandre Debut, Julien Chaumond, and Thomas Wolf. Distilbert, a distilled version of bert: smaller, faster, cheaper and lighter. arXiv preprint arXiv:1910.01108, 2019.

- Shi et al. (2019) Claudia Shi, David M. Blei, and Victor Veitch. Adapting neural networks for the estimation of treatment effects. In Advances in Neural Information Processing Systems, 2019.

- Sridhar & Getoor (2019) Dhanya Sridhar and Lise Getoor. Estimating causal effects of tone in online debates. arXiv preprint arXiv:1906.04177, 2019.

- Sridhar et al. (2018) Dhanya Sridhar, Aaron Springer, Victoria Hollis, Steve Whittaker, and Lise Getoor. Estimating causal effects of exercise from mood logging data. In IJCAI/ICML Workshop on CausalML, 2018.

- Tabari et al. (2018) Narges Tabari, Piyusha Biswas, Bhanu Praneeth, Armin Seyeditabari, Mirsad Hadzikadic, and Wlodek Zadrozny. Causality analysis of twitter sentiments and stock market returns. In Proceedings of the first workshop on economics and natural language processing, pp. 11–19, 2018.

- Tan et al. (2014) Chenhao Tan, Lillian Lee, and Bo Pang. The effect of wording on message propagation: Topic-and author-controlled natural experiments on twitter. arXiv preprint arXiv:1405.1438, 2014.

- Veitch et al. (2019) Victor Veitch, Dhanya Sridhar, and David M. Blei. Using text embeddings for causal inference. arXiv e-prints, art. arXiv:1905.12741, May 2019.

- Wang & Culotta (2019) Zhao Wang and Aron Culotta. When do words matter? understanding the impact of lexical choice on audience perception using individual treatment effect estimation. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pp. 7233–7240, 2019.

- Wood-Doughty et al. (2018) Zach Wood-Doughty, Ilya Shpitser, and Mark Dredze. Challenges of using text classifiers for causal inference. In Proceedings of the Conference on Empirical Methods in Natural Language Processing. Conference on Empirical Methods in Natural Language Processing, volume 2018, pp. 4586. NIH Public Access, 2018.

- Yeomans et al. (2018) Michael Yeomans, Alejandro Kantor, and Dustin Tingley. The politeness package: Detecting politeness in natural language. R Journal, 10(2), 2018.

- Zhang et al. (2020) Justine Zhang, Sendhil Mullainathan, and Cristian Danescu-Niculescu-Mizil. Quantifying the causal effects of conversational tendencies. Proceedings of the ACM on Human-Computer Interaction, 4(CSCW2):1–24, 2020.

Appendix A Proof of Asymptotic Normality

See 2

Proof.

We first prove that misestimation of propensity score has the rate . For simplicity, we use , : to denote conditional probability and the estimated propensity function by running the nonparametric regression . Specifically, we have and . Since , and is Lipschitz continuous, we have

| (A.1) |

Since the true propensity function is Lipschitz continuous on , the mean squared error rate of the k nearest neighbor is Györfi et al. (2002). In addition, since the propensity score function and its estimation are bounded under 1, we have the following equation

| (A.2) |

due to the dominated convergence theorem. By Equation A.1 and Equation A.2, we can bound the mean squared error of estimated propensity score in the following form:

| (A.3) |

that is .

Before we apply the conclusion of Theorem 5.1 in (Chernozhukov et al., 2017b), we need to check all assumptions in Assumption 5.1 hold in Chernozhukov et al. (2017b). Let .

-

(a)

, are easily checked by invoking definitions of and .

-

(b)

, , and

are guaranteed by the fourth condition in the theorem. -

(c)

is the second condition in the theorem.

-

(d)

Since propensity score function and its estimation are bounded under 1, we have

-

(e)

Based on Equation A.3 and condition 1 in the theorem, we have

-

(f)

Based on condition 3 in the theorem, we have

We consider a smaller positive constant instead of . Note that for , we still have . Then,

Hence, .

With (a)-(f), we can invoke the conclusion in Theorem 5.1 in (Chernozhukov et al., 2017b), and get the asymptotic normality of the TI estimator. ∎

Appendix B Proof of Causal Identification

See 1

Proof.

We first prove that this two-dimensional confounding part satisfies positivity. Since is a function of , the following equations hold:

| (B.1) |

As , we have . Furthermore, we have due to almost everywhere equivalence of and .

Since , we can rewrite Equation 3.1 by replacing with in the following form:

| (B.2) |

The equivalence of the first and the second line is because , block all backdoor paths between and (See Figure 2) and . Thus, the “do-operation” in the first line can be safely removed. Equivalence of the second line and the third line is due to , which is subject to the causal model in Figure 2. The last equation is based on the fact that is a function of only and . (It can be easily checked by using the definition of the expectation.)

Equation B.2 shows that is a two-dimensional confounding variable such that CDE is identifiable when we adjust for it as the confounding part.

∎

Note that if and are two invertible functions on , also suffices the identification for CDE. Since the sigma algebra should be the same for and , i.e.,

Hence, we have

| (B.3) |

Appendix C Additional Experiments

We conduct additional experiments to show how the estimation of causal effect changes 1) over different nonparametric models for the propensity score estimation, and 2) when using different double machine learning estimators on causal estimation. Specifically, for the first study, we apply different nonparametric models and the logistic regression to the estimated confounding part to obtain propensity scores. We use ATT AIPTW in all above cases for causal effect estimation. For the second study, we fix the first two stages of the TI estimator, i.e. we apply Q-Net for the conditional outcomes and compute propensity scores with the Gaussian process regression where the kernel function is the summation of dot product and white noise. Estimated conditional outcomes and propensity scores are plugged into different double machine learning estimators. We make the following conclusions with results of above experiments.

The choice of nonparametric models is significant.

Table 3(b) summarizes results with applying different regression models for the propensity estimation. We can see that suitable nonparametric models will strongly increase the coverage proportion over true causal estimand. Therefore, we conclude that the accuracy in causal estimation is highly dependent on the choice of nonparametric models. In practice, when there is some prior information about the propensity score function, we should apply the most suitable nonparametric model to increase the reliability of our causal estimation.

The ATT AIPTW is consistently the best double machine learning estimator.

Table 4(b) shows results by applying different double machine learning estimators. We apply both estimators for the average treatment effect (ATE) and the controlled direct effect (CDE). The bias of “unadjusted” estimator is also included in Table 4(b) (a). For absolute bias, ATT AIPTW has comparable results with other double machine learning estimators in most cases. For coverage proportion of confidence intervals, though it has lower rates in some cases, has consistently the best performance. Especially in high confounding situations, the advantage of is obvious.

Estimator

For each dataset, we compute estimators as follows. and stands for the number of individuals in the treated and controlled group. is the total number of individuals.

-

•

“Unadjusted” baseline estimator:

-

•

“Outcome-only” estimator:

-

•

ATT AIPTW:

| Noise: | Low | High | ||||||

|---|---|---|---|---|---|---|---|---|

| Treatment (oracle causal effect): | 1.0 | 0.0 | 1.0 | 0.0 | ||||

| Confounding: | Low | High | Low | High | Low | High | Low | High |

| GPR (Dot Product+White Noise) | 0.069 | 0.059 | 0.113 | 0.074 | 0.088 | 0.049 | 0.002 | 0.089 |

| GPR (RBF) | 0.150 | 0.348 | 0.156 | 0.329 | 0.363 | 0.452 | 0.344 | 0.424 |

| KNN | 0.147 | 0.334 | 0.144 | 0.313 | 0.316 | 0.372 | 0.304 | 0.356 |

| AdaBoost | 0.074 | 0.349 | 0.061 | 0.323 | 0.526 | 0.497 | 0.479 | 0.464 |

| Logistic | 0.070 | 0.057 | 0.114 | 0.073 | 0.086 | 0.047 | -0.001 | 0.087 |

| Noise: | Low | High | ||||||

|---|---|---|---|---|---|---|---|---|

| Treatment (oracle causal effect): | 1.0 | 0.0 | 1.0 | 0.0 | ||||

| Confounding: | Low | High | Low | High | Low | High | Low | High |

| GPR (Dot Product+White Noise) | 57% | 84% | 57% | 79% | 87% | 80% | 77% | 81% |

| GPR (RBF) | 31% | 0% | 41% | 0% | 7% | 7% | 17% | 19% |

| KNN | 18% | 0% | 39% | 0% | 11% | 8% | 11% | 8% |

| AdaBoost | 25% | 0% | 35% | 0% | 0% | 0% | 0% | 0% |

| Logistic | 58% | 84% | 57% | 79% | 87% | 80% | 78% | 81% |

| Noise: | Low | High | ||||||

|---|---|---|---|---|---|---|---|---|

| Treatment (oracle CDE): | 1.0 | 0.0 | 1.0 | 0.0 | ||||

| Confounding: | Low | High | Low | High | Low | High | Low | High |

| unadjusted | 1.071 | 2.143 | 1.071 | 2.1453 | 1.068 | 2.140 | 1.069 | 2.140 |

| ATE AIPTW | 0.094 | 0.178 | 0.128 | 0.195 | 0.122 | 0.106 | 0.061 | 0.140 |

| ATE BMM | 0.094 | 0.176 | 0.128 | 0.193 | 0.122 | 0.106 | 0.061 | 0.140 |

| ATE IPTW | -0.574 | -1.492 | -1.839 | -1.807 | -0.082 | -0.592 | -0.393 | -0.649 |

| ATT AIPTW: | 0.069 | 0.059 | 0.114 | 0.074 | 0.088 | 0.049 | 0.002 | 0.089 |

| ATT BMM | 0.075 | 0.147 | -0.031 | 0.062 | 0.621 | 0.454 | 0.464 | 0.337 |

| ATT TMLE: | 0.084 | 0.194 | 0.085 | 0.196 | 0.186 | 0.136 | 0.174 | 0.163 |

| Noise: | Low | High | ||||||

|---|---|---|---|---|---|---|---|---|

| Treatment (oracle CDE): | 1.0 | 0.0 | 1.0 | 0.0 | ||||

| Confounding: | Low | High | Low | High | Low | High | Low | High |

| ATE AIPTW | 37% | 36% | 69% | 33% | 75% | 79% | 79% | 71% |

| ATE BMM | 39% | 35% | 70% | 36% | 75% | 79% | 79% | 71% |

| ATE IPTW | 11% | 1% | 0% | 1% | 90% | 39% | 44% | 37% |

| ATT AIPTW: | 57% | 84% | 57% | 79% | 87% | 80% | 77% | 81% |

| ATT BMM | 26% | 4% | 49% | 41% | 1% | 3% | 1% | 14% |

| ATT TMLE | 48% | 22% | 75% | 24% | 51% | 77% | 72% | 67% |

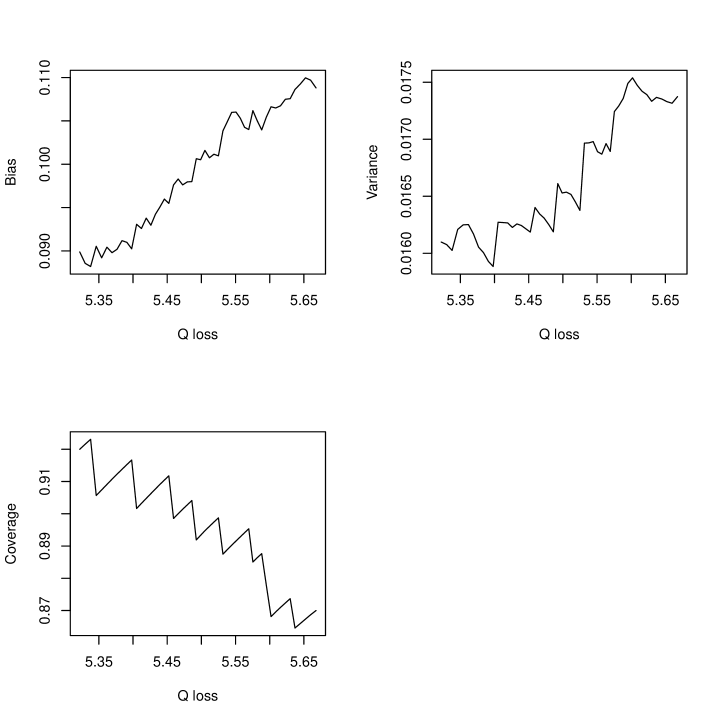

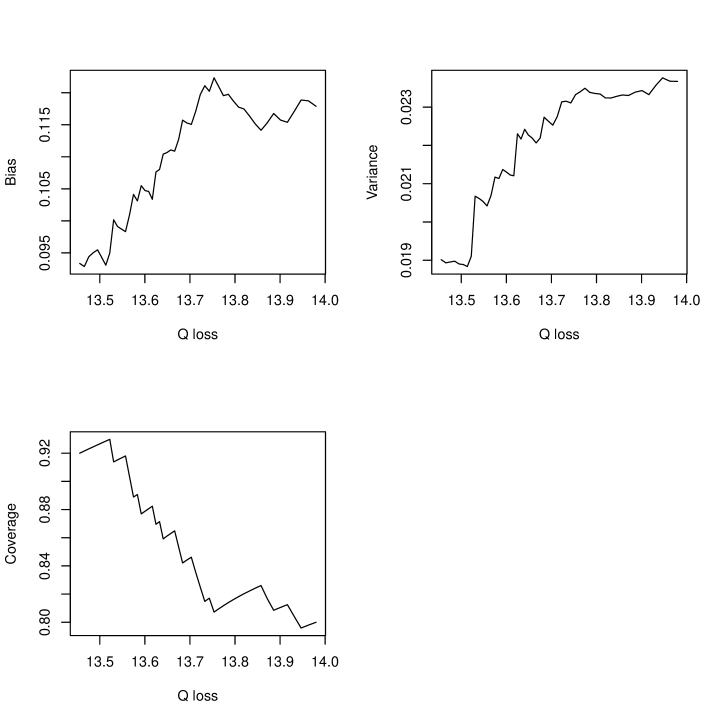

Appendix D Discussion of Low Coverage

In this section, we discuss why the confidence intervals we get (See Table 1(b)) have lower coverage than the nominated level 95%. We conduct diagnostics and find that the inaccuracy of ’s estimations is responsible for the low coverage. We compute absolute biases, variances, and coverages of ’s with different mean squared errors by using different numbers of datasets. According to Figure 4–Figure 5, as the mean squared error of increases, the bias of grows and the coverage of drops. Specifically, the highest coverage of each setting is almost 95% (use 50 datasets with most accurate conditional outcome estimations). In practice, one direct way to improve the TI estimator’s accuracy is to apply better NLP models so that more accurate conditional outcome estimations can be obtained.